Embed Size (px)

Citation preview

HELLENIC CABLES GROUP

May 2015 CORPORATE PRESENTATION

Contents

CABLEL Group at a

Glance

2014 Results Highlights

Strong Market Position

Positive Market Outlook

CapEx Fueling Growth

2

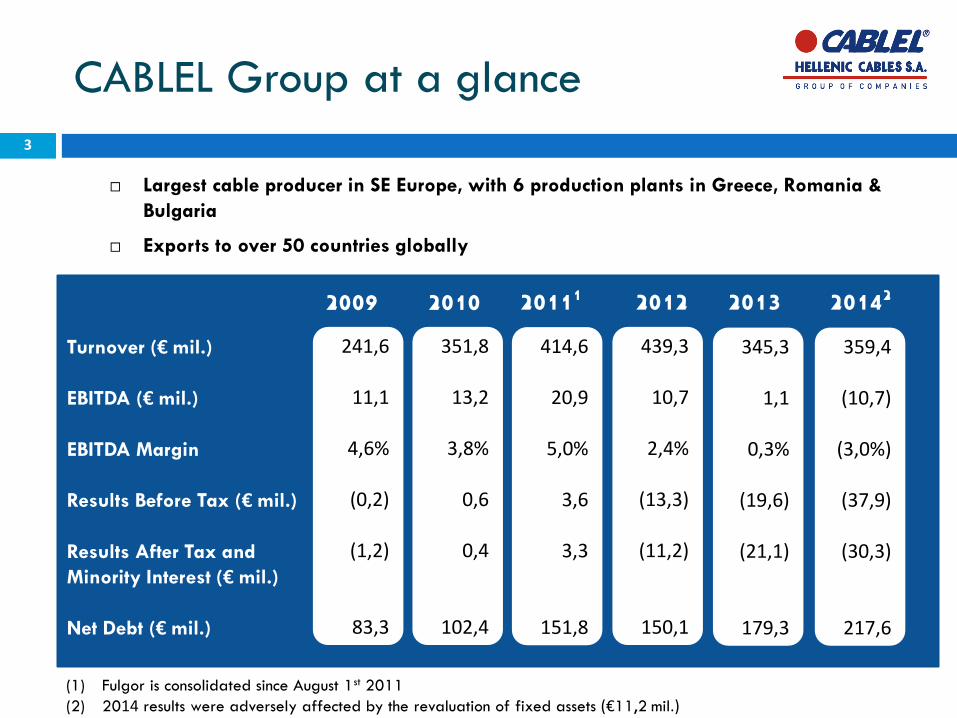

CABLEL Group at a glance

Largest cable producer in SE Europe, with 6 production plants in Greece, Romania &

Bulgaria

Exports to over 50 countries globally

351,8

13,2

3,8%

0,6

0,4

102,4

414,6

20,9

5,0%

3,6

3,3

151,8

2010 20111 2012

Turnover (€ mil.)

EBITDA (€ mil.)

EBITDA Margin

Results Before Tax (€ mil.) Results After Tax and

Minority Interest (€ mil.) Net Debt (€ mil.)

2009

439,3

10,7

2,4%

(13,3)

(11,2)

150,1

241,6

11,1

4,6%

(0,2)

(1,2)

83,3

2013

345,3

1,1

0,3%

(19,6)

(21,1)

179,3

20142

359,4

(10,7)

(3,0%)

(37,9)

(30,3)

217,6

(1) Fulgor is consolidated since August 1st 2011 (2) 2014 results were adversely affected by the revaluation of fixed assets (€11,2 mil.)

3

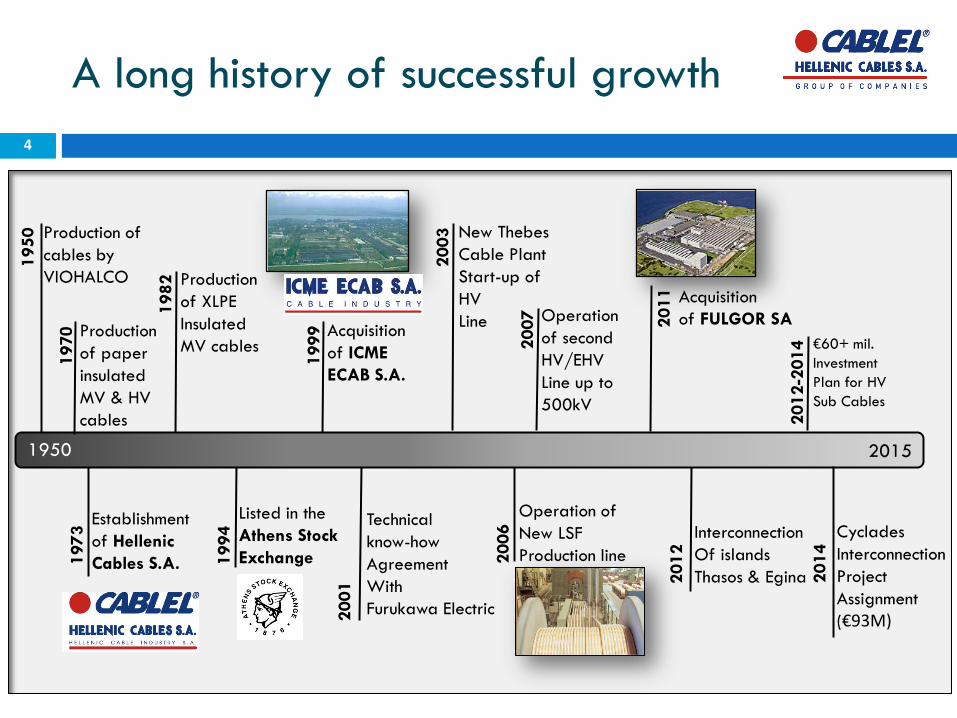

Production of

cables by

VIOHALCO

1950

Operation of

New LSF

Production line 2006

New Thebes

Cable Plant

Start-up of

HV

Line

2003

1999

Acquisition

of ICME

ECAB S.A.

Listed in the

Athens Stock

Exchange 1994

1982

Production

of XLPE

Insulated

MV cables

Establishment

of Hellenic

Cables S.A. 1973

2001

Technical

know-how

Agreement

With

Furukawa Electric

Interconnection

Of islands

Thasos & Egina 2012

Operation

of second

HV/EHV

Line up to

500kV

2007

1950 2015

Acquisition

of FULGOR SA 2011

A long history of successful growth

€60+ mil.

Investment

Plan for HV

Sub Cables

2012-2

014

4

19

70

Production

of paper

insulated

MV & HV

cables

Cyclades

Interconnection

Project

Assignment

(€93Μ)

2014

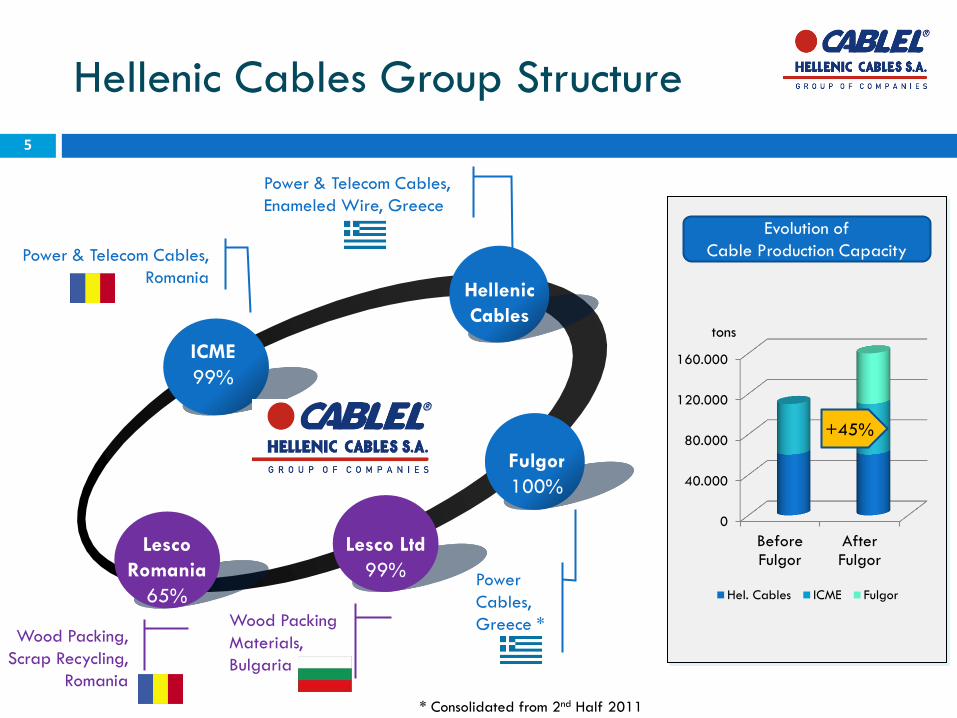

Hellenic Cables Group Structure

Power

Cables,

Greece *

Lesco

Romania

65%

ICME

99%

Fulgor

100%

Lesco Ltd

99%

Hellenic

Cables

Wood Packing,

Scrap Recycling,

Romania

Power & Telecom Cables,

Romania

* Consolidated from 2nd Half 2011

0

40.000

80.000

120.000

160.000

BeforeFulgor

AfterFulgor

Hel. Cables ICME Fulgor

Power & Telecom Cables,

Enameled Wire, Greece

Wood Packing

Materials,

Bulgaria

+45%

Evolution of

Cable Production Capacity

tons

5

Contents

CABLEL Group at a

Glance

2014 Results Highlights

Strong Market Position

Positive Market Outlook

CapEx Fueling Growth

6

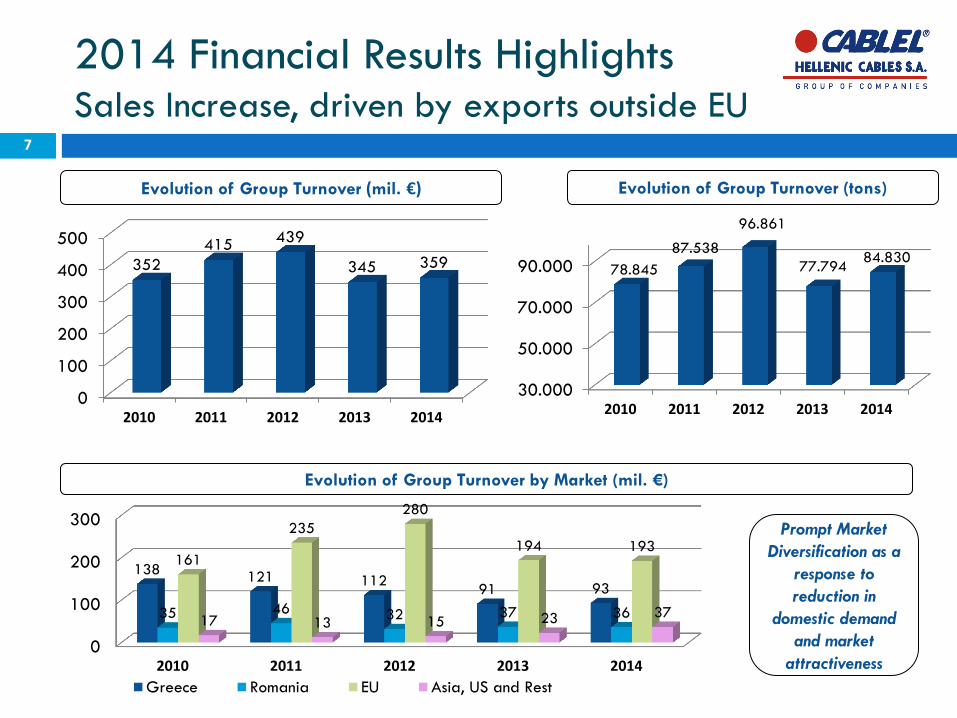

2014 Financial Results Highlights Sales Increase, driven by exports outside EU

7

30.000

50.000

70.000

90.000

2010 2011 2012 2013 2014

78.845

87.538

96.861

77.794 84.830

0

100

200

300

400

500

2010 2011 2012 2013 2014

352

415 439

345 359

Evolution of Group Turnover (tons) Evolution of Group Turnover (mil. €)

0

100

200

300

2010 2011 2012 2013 2014

138 121 112

91 93

35 46 32 37 36

161

235

280

194 193

17 13 15 23 37

Greece Romania EU Asia, US and Rest

Prompt Market

Diversification as a

response to

reduction in

domestic demand

and market

attractiveness

Evolution of Group Turnover by Market (mil. €)

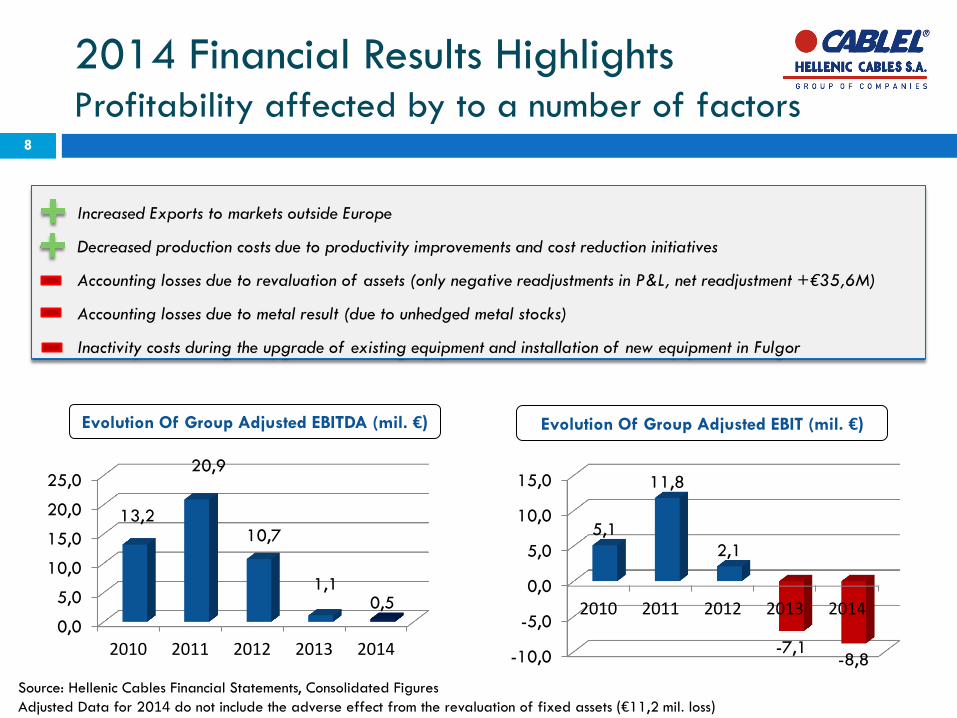

2014 Financial Results Highlights Profitability affected by to a number of factors

Evolution Of Group Adjusted EBITDA (mil. €) Evolution Of Group Adjusted EBIT (mil. €)

0,0

5,0

10,0

15,0

20,0

25,0

2010 2011 2012 2013 2014

13,2

20,9

10,7

1,1 0,5

-10,0

-5,0

0,0

5,0

10,0

15,0

2010 2011 2012 2013 2014

5,1

11,8

2,1

-7,1 -8,8

Source: Hellenic Cables Financial Statements, Consolidated Figures

Adjusted Data for 2014 do not include the adverse effect from the revaluation of fixed assets (€11,2 mil. loss)

• Increased Exports to markets outside Europe

• Decreased production costs due to productivity improvements and cost reduction initiatives

• Accounting losses due to revaluation of assets (only negative readjustments in P&L, net readjustment +€35,6M)

• Accounting losses due to metal result (due to unhedged metal stocks)

• Inactivity costs during the upgrade of existing equipment and installation of new equipment in Fulgor

8

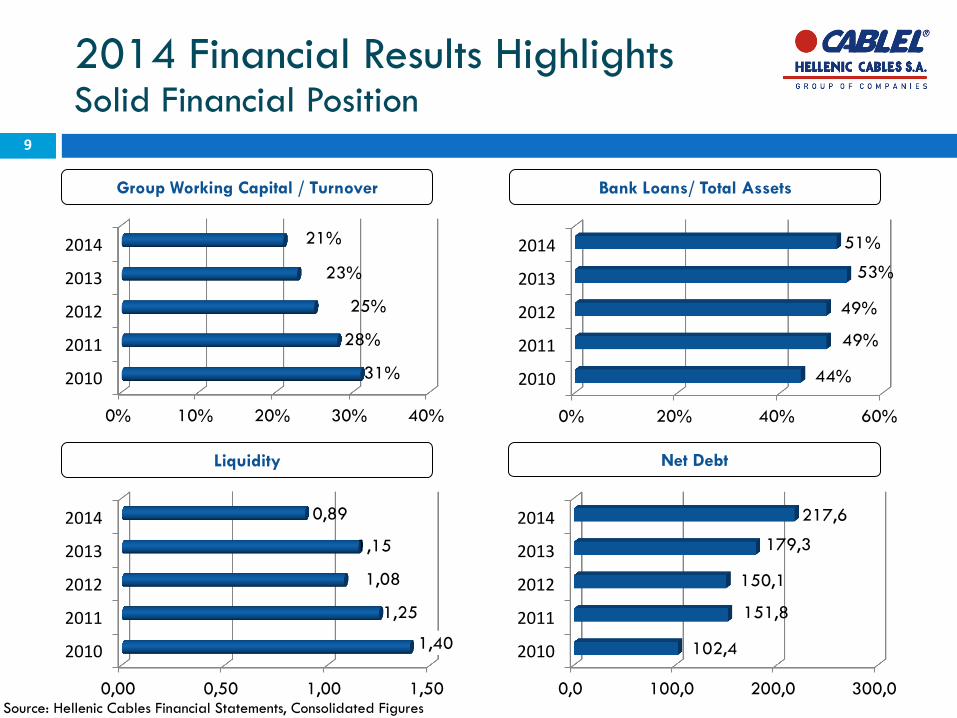

0% 10% 20% 30% 40%

2010

2011

2012

2013

2014

31%

28%

25%

23%

21%

Group Working Capital / Turnover

Net Debt Liquidity

0,0 100,0 200,0 300,0

2010

2011

2012

2013

2014

102,4

151,8

150,1

179,3

217,6

0,00 0,50 1,00 1,50

2010

2011

2012

2013

2014

1,40

1,25

1,08

1,15

0,89

Bank Loans/ Total Assets

0% 20% 40% 60%

2010

2011

2012

2013

2014

44%

49%

49%

53%

51%

9

Source: Hellenic Cables Financial Statements, Consolidated Figures

2014 Financial Results Highlights Solid Financial Position

10

Strategic Targets for 2015

Contents

CABLEL Group at a

Glance

2014 Results Highlights

Strong Market Position

Positive Market Outlook

CapEx Fueling Growth

11

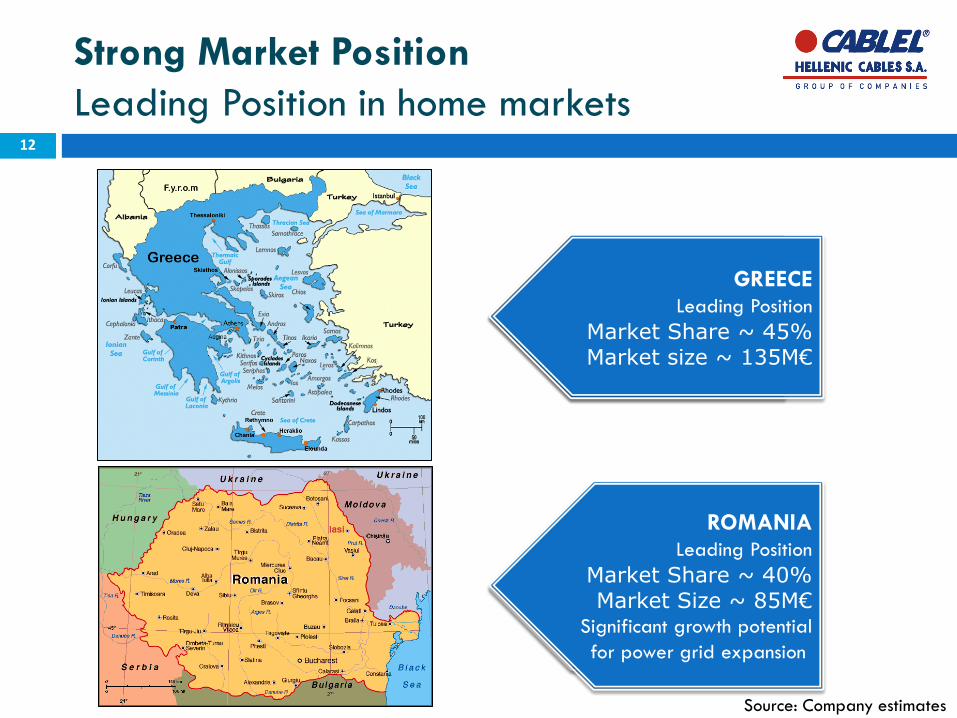

Strong Market Position

Leading Position in home markets

GREECE Leading Position

Market Share ~ 55%

ROMANIA Leading Position

Market Share ~ 40%

Source: Company estimates

12

GREECE Leading Position

Market Share ~ 45% Market size ~ 135M€

ROMANIA Leading Position

Market Share ~ 40% Market Size ~ 85Μ€

Significant growth potential

for power grid expansion

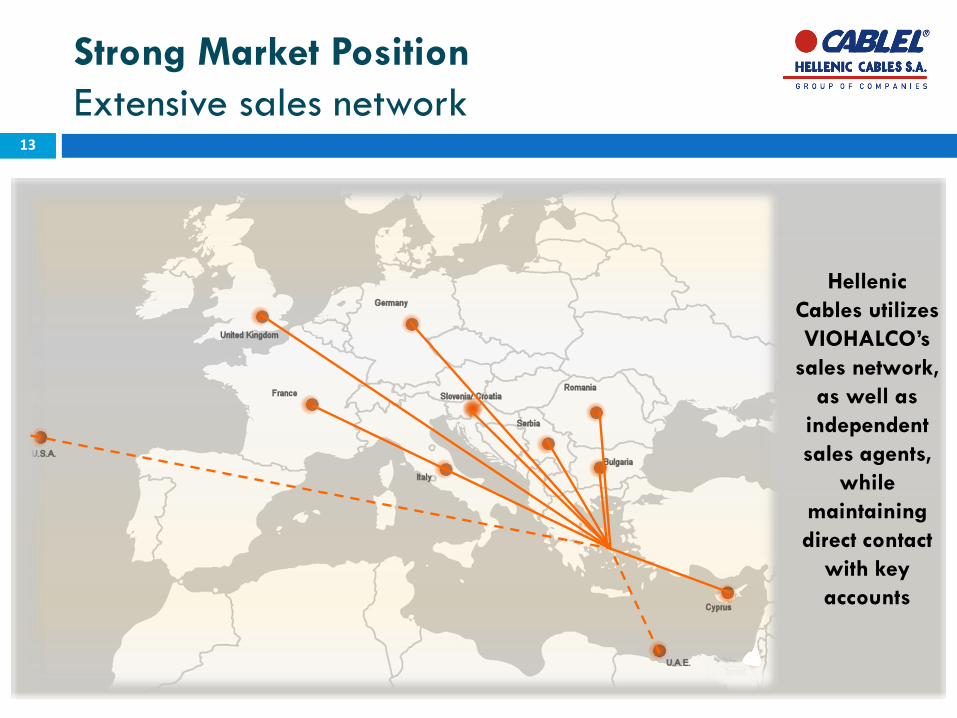

Strong Market Position

Extensive sales network

Hellenic

Cables utilizes

VIOHALCO’s

sales network,

as well as

independent

sales agents,

while

maintaining

direct contact

with key

accounts

13

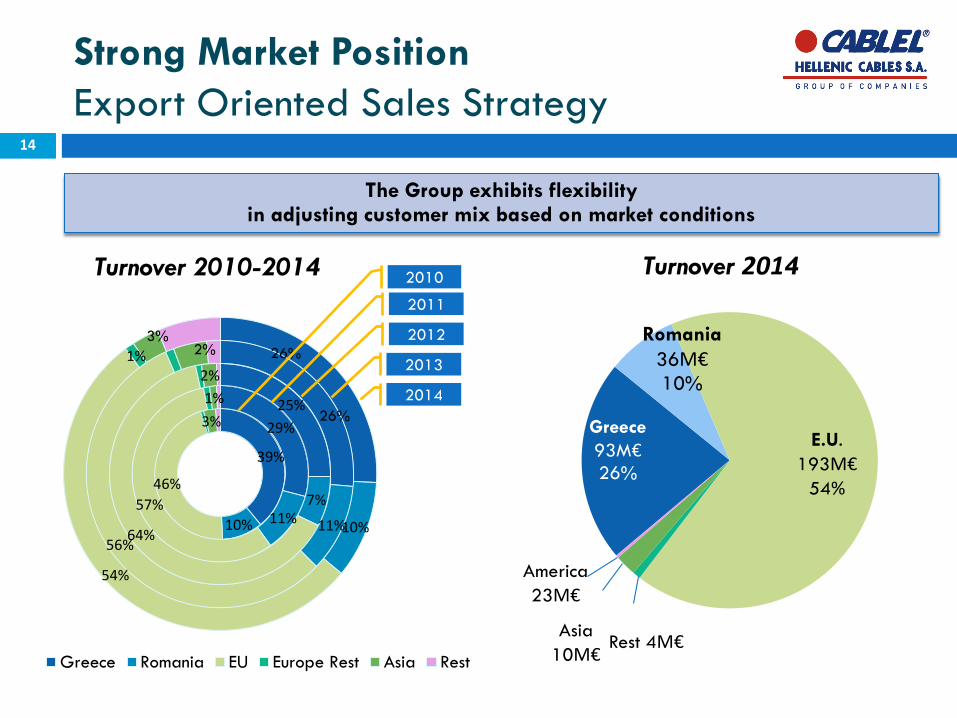

39%

10%

46%

3% 29%

11% 57%

1% 25%

7%

64%

2%

26%

11% 56%

2% 26%

10%

54%

1%

3%

Greece Romania EU Europe Rest Asia Rest

2012

2011

2010

2013

2014

Strong Market Position

Export Oriented Sales Strategy

The Group exhibits flexibility in adjusting customer mix based on market conditions

Turnover 2014 Turnover 2010-2014

14

Greece

93M€

26%

Romania

36Μ€

10%

E.U. 193Μ€

54%

Rest 4Μ€ Asia

10Μ€

America 23Μ€

Strong Market Position

Indicative Customer References 15

E-ON * ENEL * ERDF * AREVA * PPC * IBERDROLA * INEO * CE

ELECTRIC UK * OTE * ELECTRICITY NORTHWEST * VATTENFALL

* MINISTRY OF ELECTRICITY AND WATER OF KUWAIT *

DEWA OF DUBAI * PUBLIC ELECTRICITY CORPORATION OF

LIBYA * MINISTRY OF WORKS, POWER AND WATER OF

BAHRAIN * ELECTRICITE DU LIBAN * ENERGIE AG *

SONELGAZ * EnBW * WTEC

Utilities Trade and Installers

HYUNDAI * SIEMENS * VE ELECTRIC UK * DOOSAN *

SAGEM * ABB * CARILLION * VATTENFALL * BRITISH

RAIL * ENERGIE AG * METRO DE MADRID * TERNA *

CYTA * STEWAG * SONELGAZ WTEC * GES

Industrial

BATT CABLES * FABER KABEL * CLEVELAND CABLE

COMPANY * ANIXTER * SONEPAR * MEINHART KABEL *

HELUKABEL

*Receivers of our products through our distribution lines

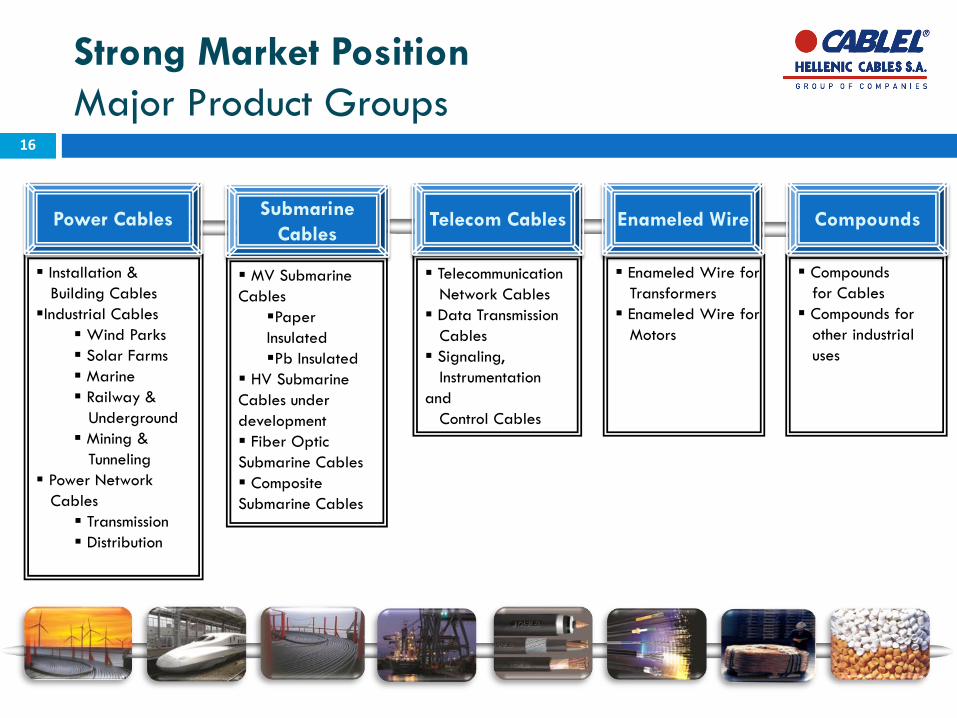

Enameled Wire for

Transformers

Enameled Wire for

Motors

Telecommunication

Network Cables

Data Transmission

Cables

Signaling,

Instrumentation

and

Control Cables

Installation &

Building Cables

Industrial Cables

Wind Parks

Solar Farms

Marine

Railway &

Underground

Mining &

Tunneling

Power Network

Cables

Transmission

Distribution

Compounds

for Cables

Compounds for

other industrial

uses

Strong Market Position

Major Product Groups

Power Cables Telecom Cables Enameled Wire Compounds

16

MV Submarine

Cables

Paper

Insulated

Pb Insulated

HV Submarine

Cables under

development

Fiber Optic

Submarine Cables

Composite

Submarine Cables

Submarine

Cables

Strong Market Position

Product Certifications 17

Contents

CABLEL Group at a

Glance

2014 Results Highlights

Strong Market Position

Positive Market Outlook

CapEx Fueling Growth

18

Significant growth prospects due to

increasing needs for infrastructure cables…

Network Expansion Projects are scheduled due to

increased needs for cross-border connectivity, connection

of renewable energy sources, implementation of smart

grid practices and replacement of aging power networks

Increased demand for underground HV/ EHV cables

within populated areas & submarine cables for island

connectivity

European SuperGrid 2050

Source: Friends of the SuperGrid

19

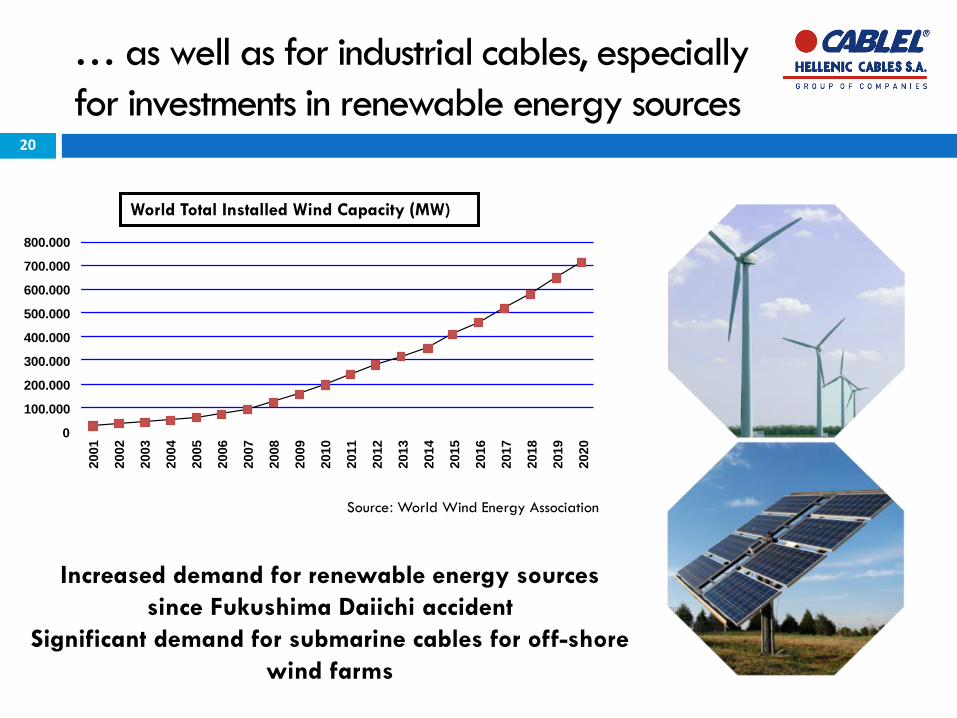

… as well as for industrial cables, especially

for investments in renewable energy sources

World Total Installed Wind Capacity (MW)

0

100.000

200.000

300.000

400.000

500.000

600.000

700.000

800.000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Source: World Wind Energy Association

Increased demand for renewable energy sources

since Fukushima Daiichi accident

Significant demand for submarine cables for off-shore

wind farms

20

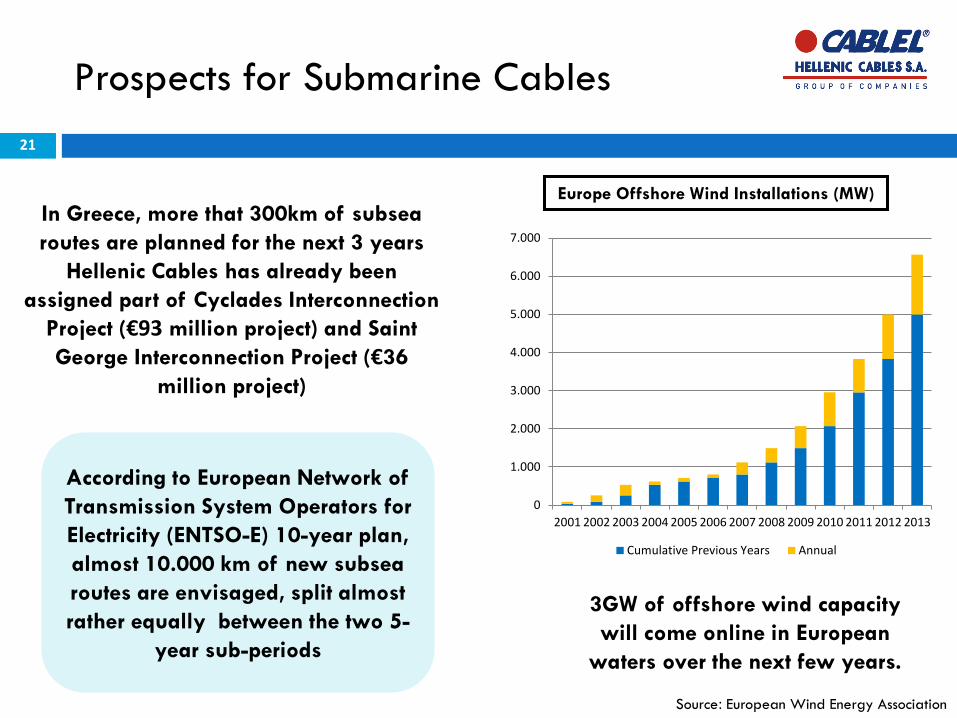

Prospects for Submarine Cables

21

Europe Offshore Wind Installations (MW)

3GW of offshore wind capacity

will come online in European

waters over the next few years.

Source: European Wind Energy Association

According to European Network of

Transmission System Operators for

Electricity (ENTSO-E) 10-year plan,

almost 10.000 km of new subsea

routes are envisaged, split almost

rather equally between the two 5-

year sub-periods

In Greece, more that 300km of subsea

routes are planned for the next 3 years

Hellenic Cables has already been

assigned part of Cyclades Interconnection

Project (€93 million project) and Saint

George Interconnection Project (€36

million project)

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Cumulative Previous Years Annual

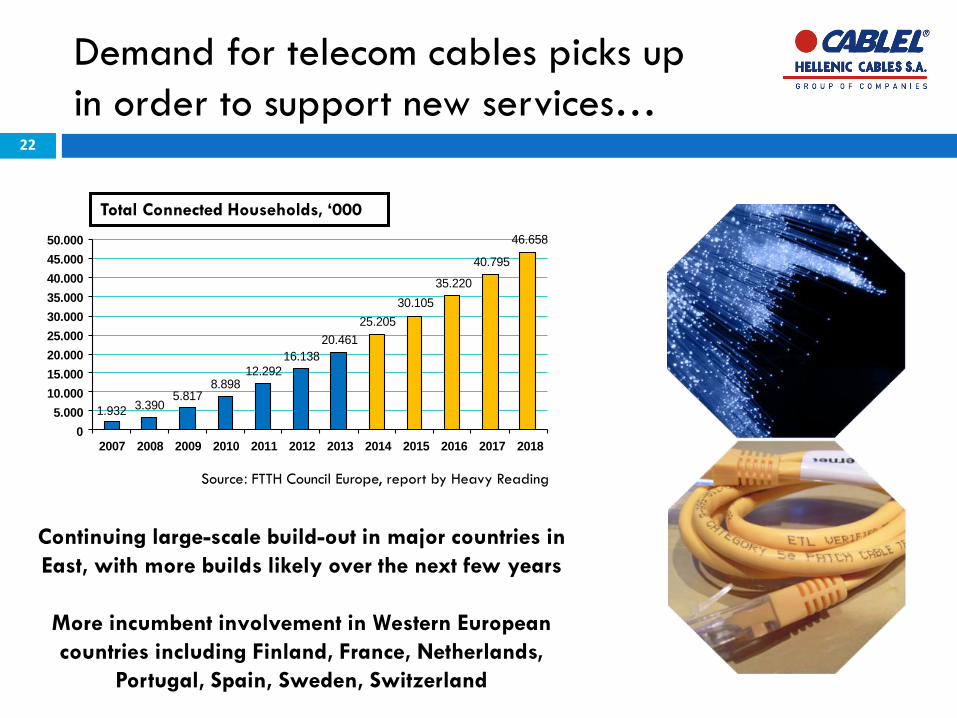

Demand for telecom cables picks up

in order to support new services…

Continuing large-scale build-out in major countries in

East, with more builds likely over the next few years

More incumbent involvement in Western European

countries including Finland, France, Netherlands,

Portugal, Spain, Sweden, Switzerland

1.932 3.3905.817

8.89812.292

16.138

20.461

25.205

30.105

35.220

40.795

46.658

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

45.000

50.000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Source: FTTH Council Europe, report by Heavy Reading

Total Connected Households, ‘000

22

…while demand for building cables &

enameled wires can only improve

Demand stabilized after building sector downturn Gradual increase in demand expected due to new buildings, replacement of existing wiring and implementation of smart grid technologies in households Focus on value added products, such as flame retardant cables

Building Cables

Demand increase expected in 2015, affected

significantly by developments in the energy sector Opportunities such as investments in the energy sector, hybrid & electric autos, EU programs for energy efficiency

Enameled Wires

Both copper and aluminium is used in power cables

thus no substitution risks due to metal prices

23

Contents

CABLEL Group at a

Glance

2014 Results Highlights

Strong Market Position

Positive Market Outlook

CapEx Fueling Growth

24

CapEx Fueling Growth

Modern production facilities

Cable Plant, Thebes, Greece

Capacity: 60.000 Tons

Enameled Wire Plant,

Livadia, Greece

Capacity: 14.000 Tons

Compound Plant,

Inofita, Greece

Capacity: 24.000 Tons

ICME, Bucharest, Romania

Capacity: 50.000 Tons

1

2

3

4

25

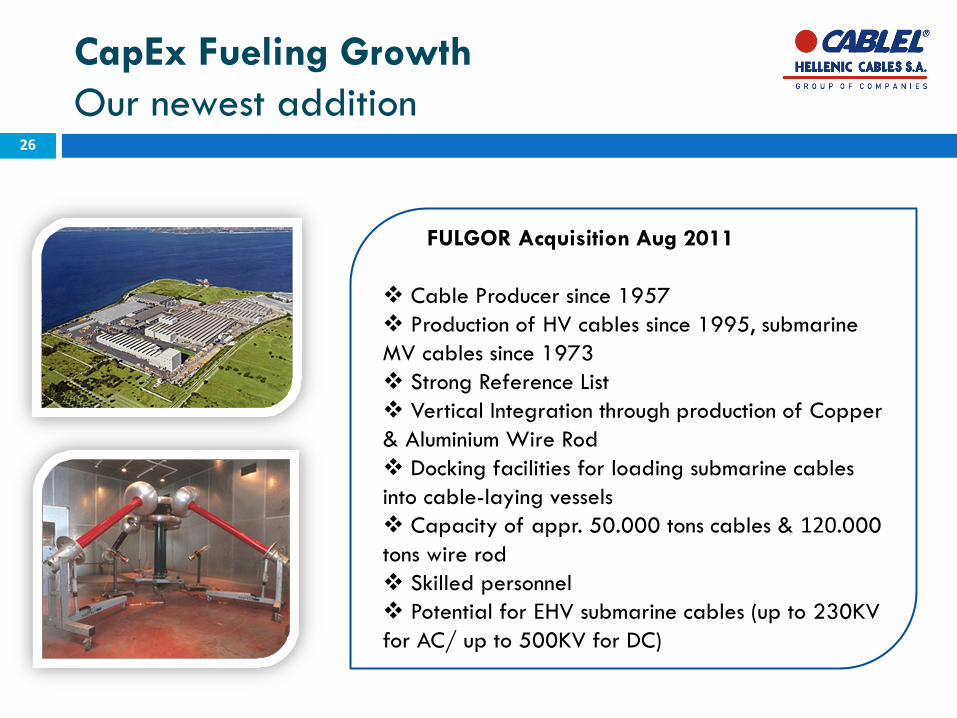

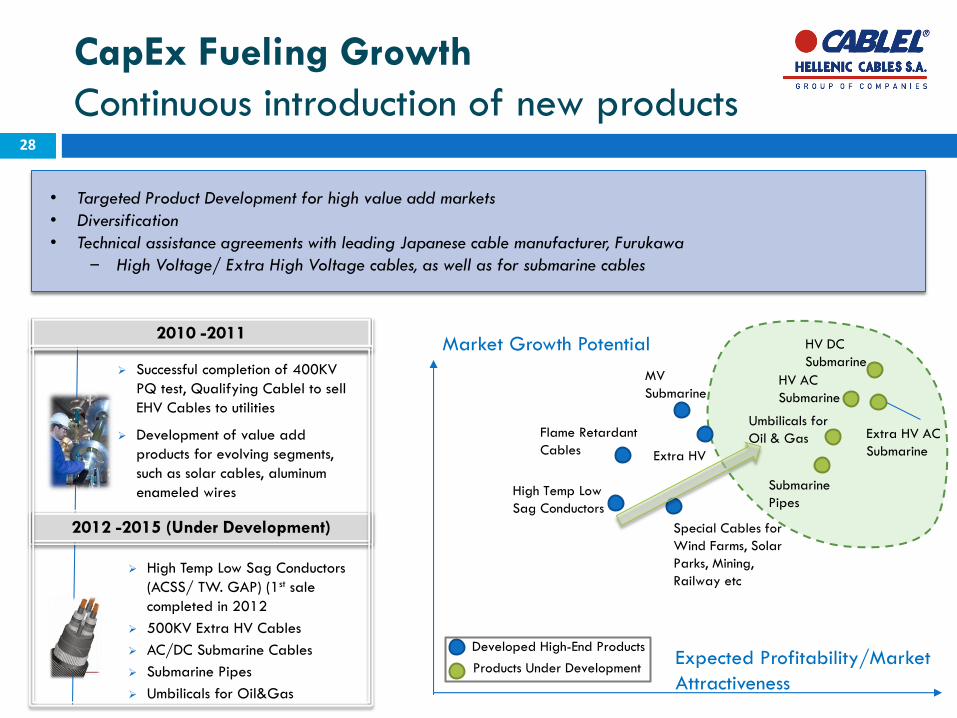

CapEx Fueling Growth

Our newest addition

FULGOR Acquisition Aug 2011

Cable Producer since 1957

Production of HV cables since 1995, submarine

MV cables since 1973

Strong Reference List

Vertical Integration through production of Copper

& Aluminium Wire Rod

Docking facilities for loading submarine cables

into cable-laying vessels

Capacity of appr. 50.000 tons cables & 120.000

tons wire rod

Skilled personnel

Potential for ΕHV submarine cables (up to 230KV

for AC/ up to 500KV for DC)

26

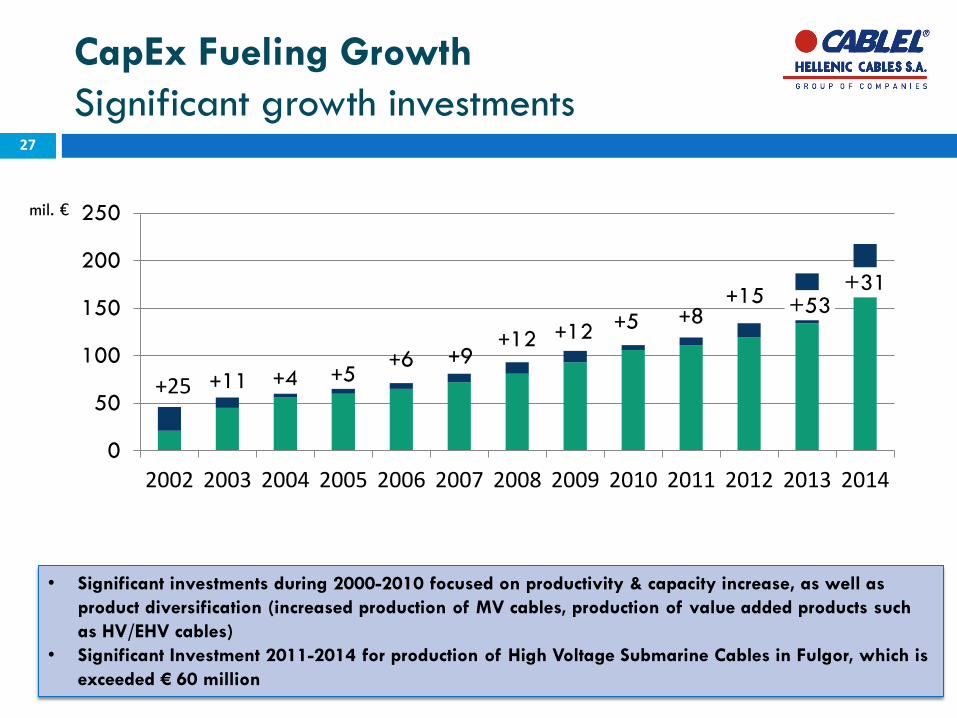

CapEx Fueling Growth

Significant growth investments

• Significant investments during 2000-2010 focused on productivity & capacity increase, as well as

product diversification (increased production of MV cables, production of value added products such

as HV/EHV cables)

• Significant Investment 2011-2014 for production of High Voltage Submarine Cables in Fulgor, which is

exceeded € 60 million

mil. €

27

+25 +11 +4 +5 +6 +9

+12 +12 +5 +8 +15 +53

+31

0

50

100

150

200

250

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

28

Market Growth Potential

Expected Profitability/Market

Attractiveness

Extra HV

MV

Submarine HV AC

Submarine

HV DC

Submarine

Developed High-End Products

Products Under Development

Extra HV AC

Submarine

Submarine

Pipes

Umbilicals for

Oil & Gas

High Temp Low

Sag Conductors

Flame Retardant

Cables

Special Cables for

Wind Farms, Solar

Parks, Mining,

Railway etc

CapEx Fueling Growth

Continuous introduction of new products

Successful completion of 400KV

PQ test, Qualifying Cablel to sell

EHV Cables to utilities

Development of value add

products for evolving segments,

such as solar cables, aluminum

enameled wires

2010 -2011

2012 -2015 (Under Development)

High Temp Low Sag Conductors

(ACSS/ TW. GAP) (1st sale

completed in 2012

500KV Extra HV Cables

AC/DC Submarine Cables

Submarine Pipes

Umbilicals for Oil&Gas

• Targeted Product Development for high value add markets

• Diversification

• Technical assistance agreements with leading Japanese cable manufacturer, Furukawa

‒ High Voltage/ Extra High Voltage cables, as well as for submarine cables

Disclaimer

The information contained in this presentation has not been independently verified and no representation or warranty, express

or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the

information or opinions contained herein. None of the Company, shareholders or any of their respective affiliates, advisers or

representatives shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of

this document or its contents or otherwise arising in connection with this document.

Unless otherwise stated, all financials contained herein are stated in accordance with International Financial Reporting Standards

(‘IFRS’ ) or Greek GAAP.

This presentation does not constitute an offer or invitation to purchase or subscribe for any shares and neither it or any part of it

shall form the basis of, or be relied upon in connection with, any contract or commitment whatsoever.

The information included in this presentation may be subject to updating, completion, revision and amendment and such

information may change materially. No person is under any obligation to update or keep current the information contained in

the presentation and any opinions expressed in relation thereof are subject to change without notice.

This presentation is only for persons having professional experience in matters relating to investments and must not be acted or

relied on by persons who do not have relevant experience.

FORWARD LOOKING STATEMENTS

This document contains forward-looking statements.

Except for historical information, the matters discussed in this presentation are forward-looking statements that are subject to

certain risks and uncertainties that could cause the actual results of operations, financial condition, liquidity, performance,

prospects and opportunities to differ materially, including but not limited to the following: the uncertainty of the national and

global economy; economic conditions generally and the Company’s sector specifically; competition from other Companies.

Although the Company believes the expectations reflected in such forward-looking statements are based on reasonable

assumptions, it can give no assurance that its expectations will be attained. The forward-looking statements are made as of the

date of this presentation, and we undertake no obligation to publicly update or revise any forward-looking statement, whether

as a result of new information, future events or otherwise.

29