Embed Size (px)

Citation preview

Helicopter Money – Let It Rain?

STRICTLY CONFIDENTIAL \\ NOT FOR DISTRIBUTION

A S T E L L O NN O T E S N o . 2 2

2016

2

A reality check survey of 2,500

individuals across Europe

KEY THOUGHTS

1

Hyperactive and easy monetary policy has failed to deliver both a revival of global growth and the return of inflation expectations to

target levels

It has in practise led to asymmetric wealth distribution through inflation of asset prices

This comes at the expense of true price discovery in asset markets and increasingly deflationary behaviour by market participants and

corporate decision makers

The market continues to believe that central banks will fail to achieve their mandated objectives (e.g., inflation)

Helicopter money is increasingly being contemplated in major economies; e.g., Switzerland will hold a referendum in June 2016

regarding an unconditional minimum pay of CHF 2,500 p/m p/citizen

Little has been written about the impact of negative rates and helicopter money on the behaviour of the average household

Astellon Capital has conducted a proprietary survey, polling over 2,500 individuals in Germany, Italy, France, and Spain

Main conclusions:

Only one in three consumers/households knows that QE exists

Passing on negative interest rates by banks to retail depositors would likely lead to bank runs

Negative rates (and bank runs) would lead to hoarding of physical cash or alternative forms of savings, not increased consumption

Helicopter money would on the other hand increase consumption in all countries irrespective of income levels

Disclaimer: For the avoidance of a doubt, Astellon Capital is not a proponent of excessively easy monetary policies such as QE, negative interest rates or helicopter money

Quantitative Easing (QE) to Quantitative Failure (QF)

2

HOW MUCH “MORE-OF-THE-SAME” POLICY, DESPITE ITS FAILURES?

3

650+ rate cuts globally since Sep-08

(every 3 trading days)

US$8 trnof negative-yielding government debt

outstanding globally

63% / 67%of the time inflation was below the

ECB/Fed target of 2% since 2008

Lowest interest rates in

5,000 years

US$21 trnincrease in world market cap (MSCI) since 2009

€80 bn ≈ €300 per capitaECB purchases per month equivalent per head in the EU

US$5.5 trnof G5 central bank balance sheet expansion

5x NIRP negative interest rates in Japan, Switzerland,

Eurozone, Denmark and Sweden

THE FED OVERESTIMATED THE RECOVERY EVERY YEAR FOR THE LAST DECADE

4

14.0

14.5

15.0

15.5

16.0

16.5

17.0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

US Actual Avg forecast in 2007 Avg forecast in 2008

Avg forecast in 2009 Avg forecast in 2010 Avg forecast in 2011

Avg forecast in 2012 Avg forecast in 2013 Avg forecast in 2014

Note: (1) Average of two forecasts during the year (February, July)Source: Federal Reserve, BEA

Real US GDP (2005-2015): actual vs Fed forecast (1) (US$ trn, 2009 constant prices)

Actual

ECB ESTIMATES ARE TOO OPTIMISTIC EACH YEAR AS WELL

5

Real GDP Euro area (1) (2005-2015): actual vs ECB forecast (2) (€ trn, 2010 constant prices)

8.8

9.0

9.2

9.4

9.6

9.8

10.0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Euro area actual Avg forecast in 2007

Avg forecast in 2008 Avg forecast in 2011

Avg forecast in 2012

Note: (1) Actual Euro area composition changed: Euro 12 in 2006, Euro 13 in 2007, Euro 15 in 2008, Euro 16 in 2010, Euro 17 in 2013, Euro 18 in 2014, Euro 19 in 2015

(2) Average of four forecasts during the year (March, June, September, December)

Source: Eurostat, ECB

Actual

MARKETS IMPLY THAT INFLATION WILL CONTINUE TO BE WELL BELOW 2% TARGET

6

ECB balance sheet total assets in €m (left axis) vs EUR 5yr inflation swap and core inflation (right axis)

ECB inflation target: 2%

Source: Bloomberg, Astellon Capital

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

2.0%

2.2%

2.4%

2.6%

2.8%

3.0%

500

1,000

1,500

2,000

2,500

3,000

01/2005 01/2006 01/2007 01/2008 01/2009 01/2010 01/2011 01/2012 01/2013 01/2014 01/2015 01/2016

ECB total assets EUR 5yr inflation swap Eurozone core inflation

03/2015

Launch of ECB QE 1

Inflation target of 2%

INFLATING ASSET PRICES THROUGH MONETARY POLICY: OBJECTIVE ACHIEVED

7

QE impact (1) on Eurostoxx 600 since November 2008 Citi Credit Spread Pure Europe Total Return Index

121% (50%)

72%

--

20%

40%

60%

80%

100%

120%

QE impact No QE impact Overall gains

Source: Astellon Capital, Bianco Research, Bloomberg

(1) Updated as of 22 Mar 2016: period has been divided into times when QE was

operational at either the Fed or ECB and periods when it was discontinued

80

90

100

110

120

130

140

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

November

2008

QE 1 starts

Aug

2010

QE 2

starts

Aug

2012

QE 3

hinted

Oct

2014

QE 4

rumours

Jan 2015

European

QE

Source: Astellon Capital calculations, Bloomberg

HELICOPTER MONEY ALREADY BEING TESTED OR CONTEMPLATED

8

Summary of Helicopter Money initiatives

Country Description Status5-yr GDP

CAGR %

Unemployment

rate

Switzerland

CHF2,500 a month to adults and CHF625 to children

Estimated costs of CHF208bn p.a. (gross) and CHF25bn p.a. (net) as it substitutes existing

subsidies/welfare contributions

Referendum in

June 20161.6% 3.6%

Finland

Government provides €20m for trial of 2 years. Three options considered:

• Full basic income: €800 per month

• Partial basic income: €550 per month, with existing insurance-based benefits

• Negative income tax

Final report in Nov

2016

Launch in 2017

0.0% 9.4%

Canada

(Ontario)

Previously trialled in Dauphine Canada 1974-1979 and was proved to reduce poverty

Pilot programme currently being developed for 2016 Launch in 2016 2.1% 7.1%

Netherlands

(Ultrecht, Tilburg,

Groningen,

Wageningen)

4 options being considered:

• A pure version with no strings attached

• Require recipients to volunteer a certain number of hours

• A mix of the first two with a higher payout for volunteers

• Only pay people who are not working

TBD 0.6% 6.9%

United Kingdom

Supported mainly by Labour Party

Think tank RSA suggested between £244 to £618 a week (to replace welfare state) depending on

age group

TBD 2.1% 5.3%

FranceAn economics feasibility study for universal basic income is being developed under a

parliamentary working commissionTBD 0.8% 10.4%

Source: Eurostat, IMF

Astellon survey on negative rates and helicopter money

A reality check across Germany, France, Italy and Spain

9

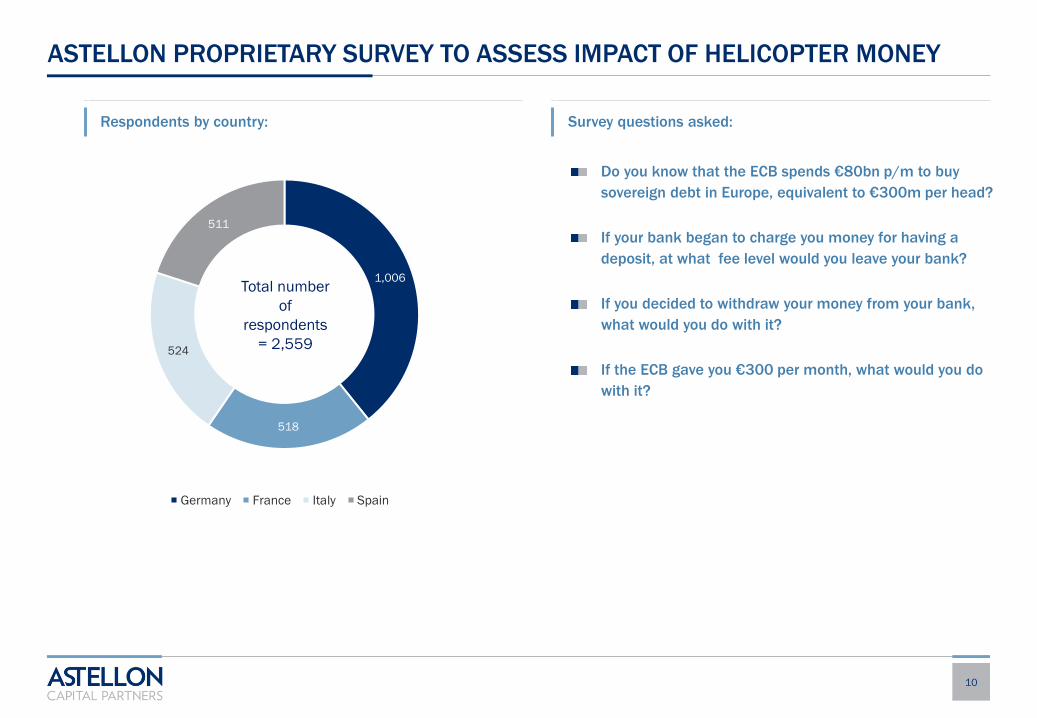

ASTELLON PROPRIETARY SURVEY TO ASSESS IMPACT OF HELICOPTER MONEY

10

Respondents by country: Survey questions asked:

1,006

518

524

511

Germany France Italy Spain

Total number

of

respondents

= 2,559

Do you know that the ECB spends €80bn p/m to buy

sovereign debt in Europe, equivalent to €300m per head?

If your bank began to charge you money for having a

deposit, at what fee level would you leave your bank?

If you decided to withdraw your money from your bank,

what would you do with it?

If the ECB gave you €300 per month, what would you do

with it?

SUMMARY OF SOCIO-DEMOGRAPHIC PROFILES OF RESPONDENTS

11

Age Gender

Annual income Household size

39%

44%

17%

18-34 35-54 55+

48%52%

Male Female

60%26%

2%

12%

<40K 40K-100K >100K Not sure

68%

31%

1%

1 to 3 4 to 6 >6

ONLY ONE IN THREE CONSUMERS KNOWS THAT QE EXISTS

12

33.0%34.4%

45.0%

37.0%

67.0% 65.6% 55.0% 63.0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Germany France Italy Spain

1. Did you know ECB spends €80 billion every month to buy sovereign debt of different countries in Europe?

Yes

No

PASSING ON NEGATIVE RATES TO CONSUMERS WOULD RESULT IN BANK RUNS

13

24.8% 25.1%

33.2%

14.9%

75.2% 74.9% 66.8% 85.1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Germany France Italy Spain

2. If you need to pay to save with a bank, would you leave?

Unwilling

to pay

Willing

to pay

BANK RUNS WOULD LEAD TO ALTERNATIVE SAVINGS, NOT CONSUMPTION

14

66.8%

54.6%57.6%

63.7%

27.5%38.2%

38.0% 33.1%

5.7% 7.2%4.4% 3.2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Germany France Italy Spain

Savings Investment Consumption

3. If you decided to withdraw from your bank, where would you keep your money?

Note: Respondents could select multiple answers so results were scaled down to add up to 100%, on average respondents selected ~1.6 different answers to this question

HELICOPTER MONEY WOULD (AT LEAST) INCREASE CONSUMPTION

15

52.5% 51.1%48.6%

44.7%

19.1%23.2%

21.9%24.0%

13.1% 8.9%12.8% 16.8%

8.8% 10.7% 10.0%9.2%

6.5% 6.1% 6.7% 5.3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Germany France Italy Spain

Consumption Savings De-leveraging Investment Labour reduction

4. If you received a cheque of €300 per month, what would you do with it?

Note: Respondents could select multiple answers so results were scaled down to add up to 100%, on average respondents selected ~2.0 different answers to this question

GERMANS WERE SPLIT BY INCOME BUT IT SHOWS NO STATISTICAL DIFFERENCE

16

1. Did you know ECB spends €80bn every month to buy debt? 2. If you need to pay to save, would you leave your bank?

3. % of respondents that would put some cash in other forms

of savings if they left their banks

4. % of respondents that would increase consumption if €300

per month was given by ECB

100.0% 100.0%

0%

20%

40%

60%

80%

100%

Under EUR 40K Above EUR 40K

Consumption

100.0% 100.0%

0%

20%

40%

60%

80%

100%

Under EUR 40K Above EUR 40K

Saving

25.3% 24.3%

74.7% 75.7%

0%

20%

40%

60%

80%

100%

Under EUR 40K Above EUR 40K

Will never pay Willing to pay

32.8% 33.2%

67.2% 66.8%

0%

20%

40%

60%

80%

100%

Under EUR 40K Above EUR 40K

No Yes

Disclaimer This document has been prepared by Astellon Capital Partners LLP (“ACP”) for persons reasonably believed by ACP to be of the kind to whom ACP is permitted to communicate financial promotions pursuant to the Financial

Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended, to give preliminary information about the investment proposition described herein (the “Fund”). It is a confidential communication to, and solely for the use of,

the recipient. Astellon Capital Partners LLP is authorised and regulated by the Financial Conduct Authority.

Astellon Capital Partners LLP | 100 Brompton Road, 5th Floor | London | SW3 1ER

T: +44 (0)203 140 8180

www.astelloncapital.com

For more information: Astellon Capital Partners, LLP

Investor Relations

T: +44 (0) 203 140 8187