Embed Size (px)

Citation preview

Höegh LNG - the FSRU provider

1

4Q 2017Presentation of financial results

28 February 2018

Forward looking statements

2

This presentation contains forward-looking statements which reflects management’s current expectations, estimates and projections about Höegh LNG’s

operations. All statements, other than statements of historical facts, that address activities and events that will, should, could or may occur in the future are

forward-looking statements. Words such as “may,” “could,” “should,” “would,” “expect,” “plan,” “anticipate,” “intend,” “forecast,” “believe,” “estimate,” “predict,”

“propose,” “potential,” “continue” or the negative of these terms and similar expressions are intended to identify such forward-looking statements. These

statements are not guarantees of future performance and are subject to certain risks, uncertainties and other factors, some of which are beyond our control and

are difficult to predict. Therefore, actual outcomes and results may differ materially from what is expressed or forecasted in such forward-looking statements.

You should not place undue reliance on these forward-looking statements, which speak only as of the date of this presentation. Unless legally required, Höegh

LNG undertakes no obligation to update publicly any forward-looking statements whether as a result of new information, future events or otherwise.

Among the important factors that could cause actual results to differ materially from those in the forward-looking statements are: changes in LNG transportation

and regasification market trends; changes in the supply and demand for LNG; changes in trading patterns; changes in applicable maintenance and regulatory

standards; political events affecting production and consumption of LNG and Höegh LNG’s ability to operate and control its vessels; change in the financial

stability of clients of the Company; Höegh LNG’s ability to win upcoming tenders and securing employment for the FSRUs on order; changes in Höegh LNG’s

ability to convert LNG carriers to FSRUs including the cost and time of completing such conversions; changes in Höegh LNG’s ability to complete and deliver

projects awarded; changes to the Company’s cost base; changes in the availability of vessels to purchase; failure by yards to comply with delivery schedules;

changes to vessels’ useful lives; changes in the ability of Höegh LNG to obtain additional financing, including the impact from changes in financial markets;

changes in the ability to achieve commercial success for the projects being developed by the Company; changes in applicable regulations and laws; and

unpredictable or unknown factors herein also could have material adverse effects on forward-looking statements.

Agenda

3

▪ Highlights

▪ Operational update

▪ Market update

▪ Financials

▪ Summary

Highlights for the fourth quarter of 2017 and subsequent events

Key financials

▪ Total income: USD 76.1 million

▪ EBITDA USD 43 million

▪ Net profit USD 20 million

4

Highlights

▪ Closing of the sale of the remaining 49% interest in Höegh

Grace to Höegh LNG Partners for USD 86.7 million, net of

debt

▪ Dividend of USD 0.125 per share paid for the fourth quarter

of 2017

Subsequent events

▪ Höegh Giant commences 3-year LNGC/FSRU contract

with Gas Natural Fenosa

▪ Höegh LNG Partners initiates ATM equity raising

programme

▪ Dividend of USD 0.025 per share declared in the first

quarter of 2018

Agenda

5

▪ Highlights

▪ Operational update

▪ Market update

▪ Financials

▪ Summary

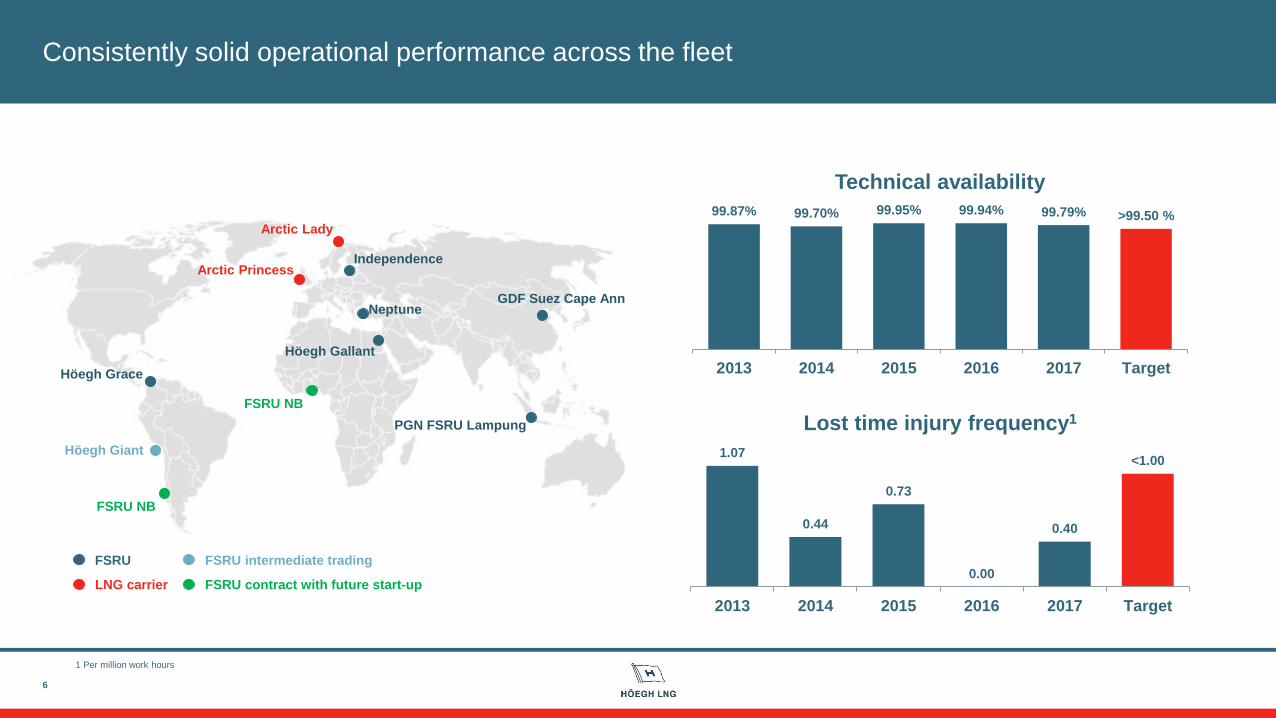

Consistently solid operational performance across the fleet

6

GDF Suez Cape Ann

PGN FSRU Lampung

Neptune

Independence

Höegh Grace

Höegh Giant

Arctic Princess

Arctic Lady

Höegh Gallant

FSRU NB

FSRU intermediate trading

LNG carrier

FSRU

FSRU contract with future start-up

99.87% 99.70% 99.95% 99.94% 99.79% >99.50 %

2013 2014 2015 2016 2017 Target

Technical availability

1.07

0.44

0.73

0.00

0.40

<1.00

2013 2014 2015 2016 2017 Target

Lost time injury frequency1FSRU NB

1 Per million work hours

Project execution update

GNL Penco, Chile

▪ The GNL Penco FSRU project continues its revised

environmental approval process, in accordance with GNL

Penco’s plans

▪ Solid commercial platform given GNL Penco’s long-term

contract to deliver electricity to the Chilean market

Quantum Power, Ghana

▪ Quantum power/Höegh LNG FSRU solution represents the

fastest way for Ghana to access LNG markets

▪ Remains subject to government approval

7

▪ First cargo under the Gas Natural Fenosa contract received

in Sabine Pass, US

▪ Hybrid LNGC/FSRU contract, 3 years plus options

Index-linked LNGC rate when trading as a carrier

Pre-determined FSRU rate when entering an FSRU contract

Höegh Giant delivered to the GNF charter

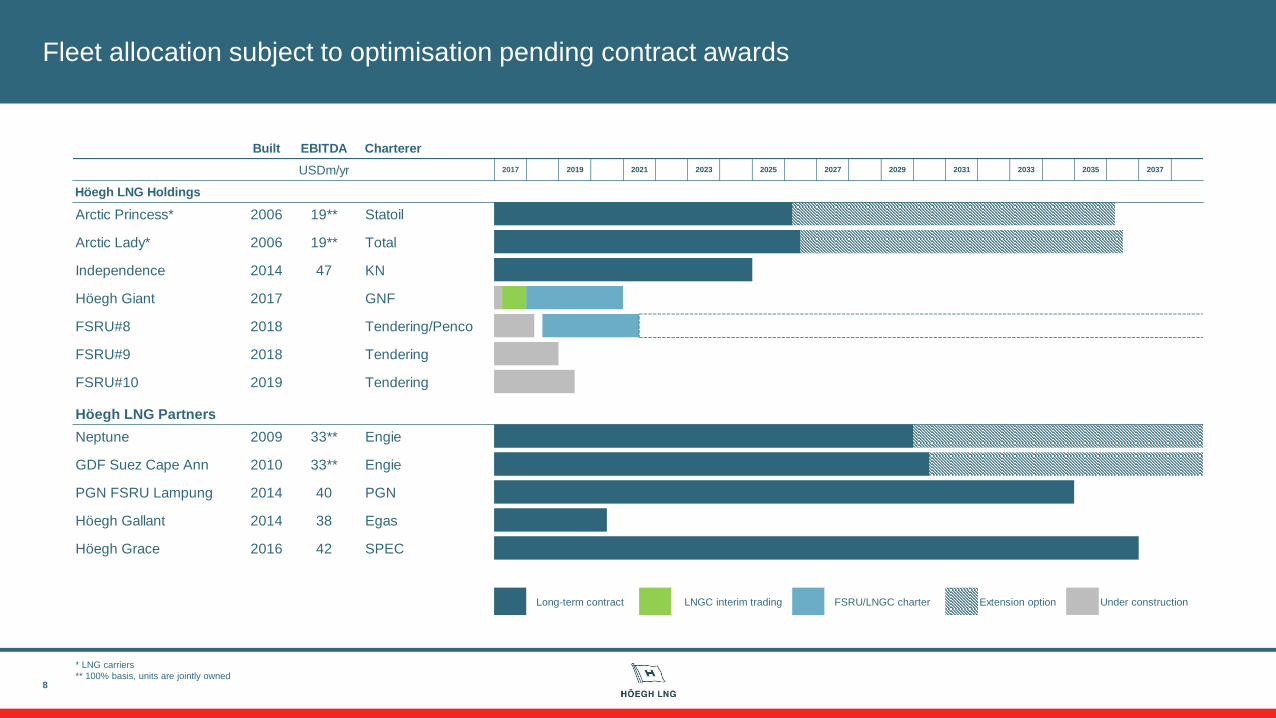

Fleet allocation subject to optimisation pending contract awards

8

* LNG carriers

** 100% basis, units are jointly owned

Built EBITDA Charterer

USDm/yr 2020 2022 2024 2026 2028 2030 2032 2034 2036 2038

Höegh LNG Holdings

Arctic Princess* 2006 19** Statoil

Arctic Lady* 2006 19** Total

Independence 2014 47 KN

Höegh Giant 2017 GNF

FSRU#8 2018 Tendering/Penco

FSRU#9 2018 Tendering

FSRU#10 2019 Tendering

Höegh LNG Partners

Neptune 2009 33** Engie

GDF Suez Cape Ann 2010 33** Engie

PGN FSRU Lampung 2014 40 PGN

Höegh Gallant 2014 38 Egas

Höegh Grace 2016 42 SPEC

Long-term contract LNGC interim trading FSRU/LNGC charter Extension option Under construction

2017 2019 2021 2023 2025 2027 2029 2031 2033 2035 2037

Increasing business development activity

9

▪ In discussions for interim employment for FSRU #8 from

mid-2018 until start-up under the contract with GNL Penco

in Chile

▪ Main commercial focus on securing long-term employment

for FSRU #9 and #10, which deliver in December 2018 and

May 2019 respectively

▪ Currently involved in several advanced tendering

processes with decisions expected in 2018

▪ Business development activity continues to increase

Coinciding with LNG trade exceeding expectations

New tenders being launched

Ongoing tender processes picking up momentum

LNG net exports, 2017 y/y growth vs expectations

Source: Shell LNG outlook 2018

Agenda

10

▪ Highlights

▪ Operational update

▪ Market update

▪ Financials

▪ Summary

LNG trade up 11% in 2017

11

0

50

100

150

200

250

300

350

2010 2011 2012 2013 2014 2015 2016 2017

mtp

a

LNG trade by exporter

Qatar MEG ex Qatar Africa Asia Australia USA South America Europe

0

50

100

150

200

250

300

350

2010 2011 2012 2013 2014 2015 2016 2017

mtp

a

LNG trade by importer

Japan+Korea China RoA MEG Africa Europe North America South America

Australia

and US

volumes

Chinese

imports

exceeding

South

korea

Source: Waterborne LNG, IHS Markit

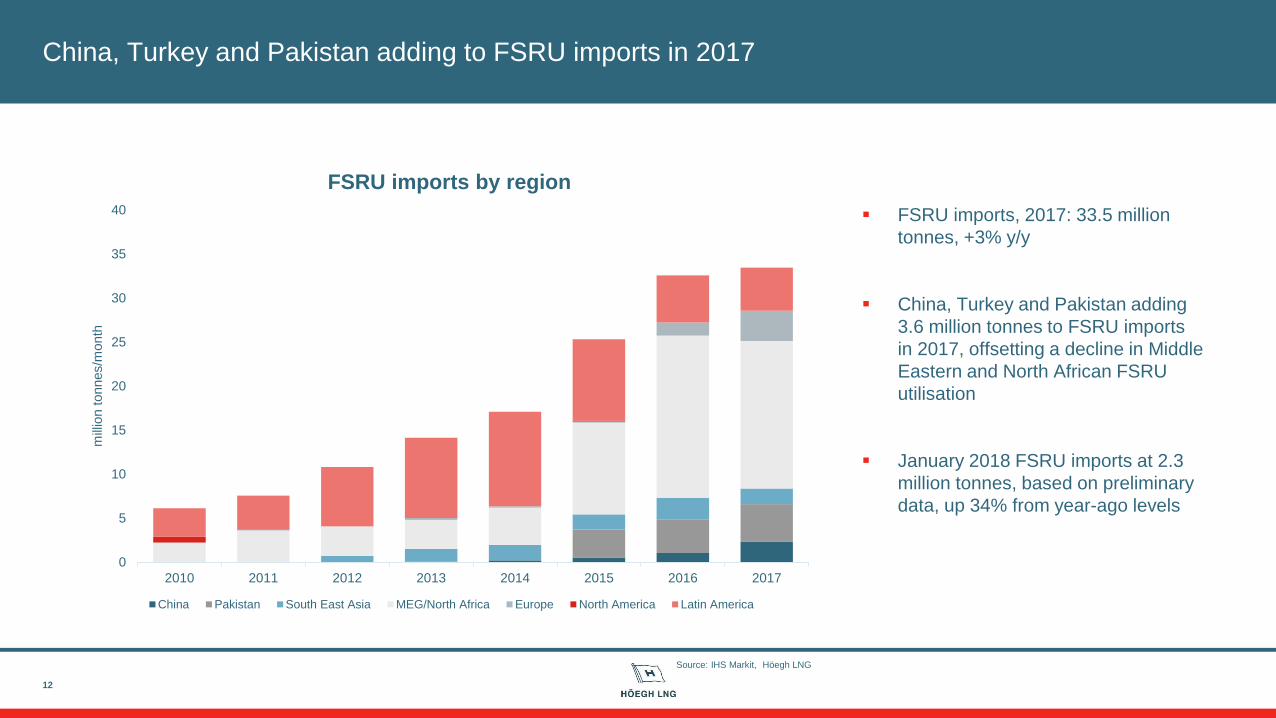

China, Turkey and Pakistan adding to FSRU imports in 2017

▪ FSRU imports, 2017: 33.5 million

tonnes, +3% y/y

▪ China, Turkey and Pakistan adding

3.6 million tonnes to FSRU imports

in 2017, offsetting a decline in Middle

Eastern and North African FSRU

utilisation

▪ January 2018 FSRU imports at 2.3

million tonnes, based on preliminary

data, up 34% from year-ago levels

12

0

5

10

15

20

25

30

35

40

2010 2011 2012 2013 2014 2015 2016 2017

mill

ion t

onnes/m

onth

FSRU imports by region

China Pakistan South East Asia MEG/North Africa Europe North America Latin America

Source: IHS Markit, Höegh LNG

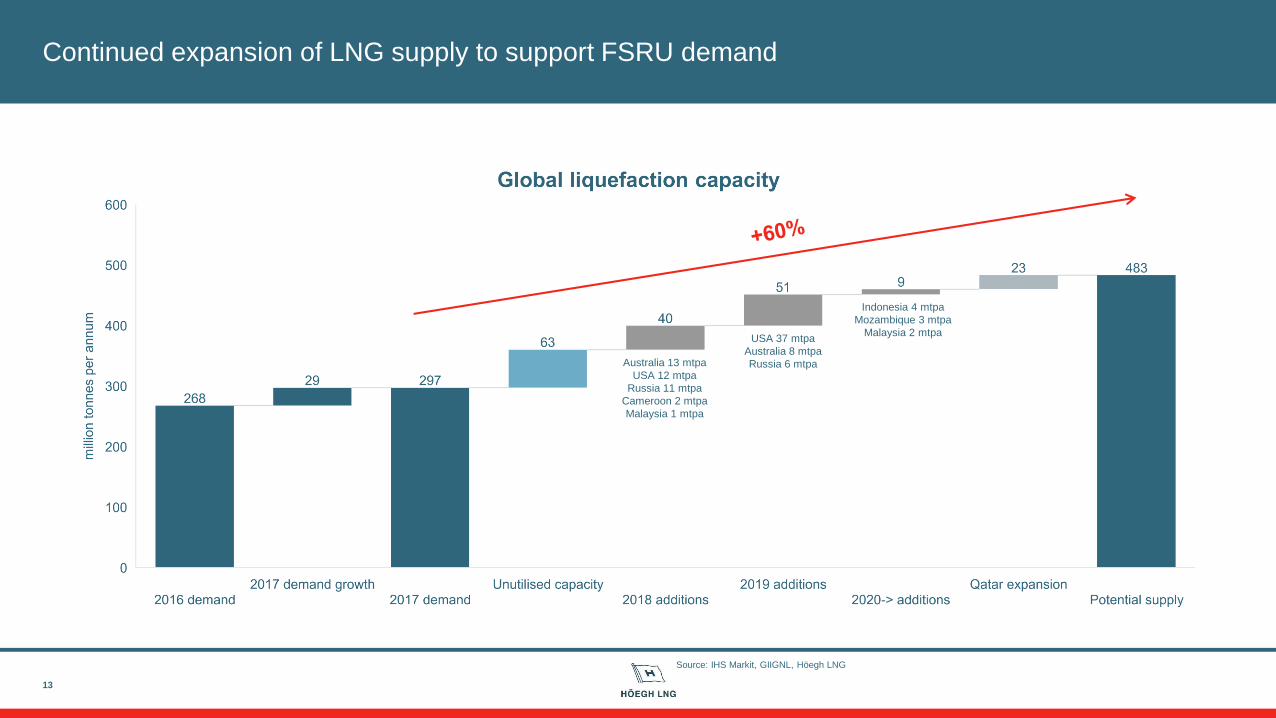

Continued expansion of LNG supply to support FSRU demand

13

Australia 13 mtpa

USA 12 mtpa

Russia 11 mtpa

Cameroon 2 mtpa

Malaysia 1 mtpa

USA 37 mtpa

Australia 8 mtpa

Russia 6 mtpa

Indonesia 4 mtpa

Mozambique 3 mtpa

Malaysia 2 mtpa

Source: IHS Markit, GIIGNL, Höegh LNG

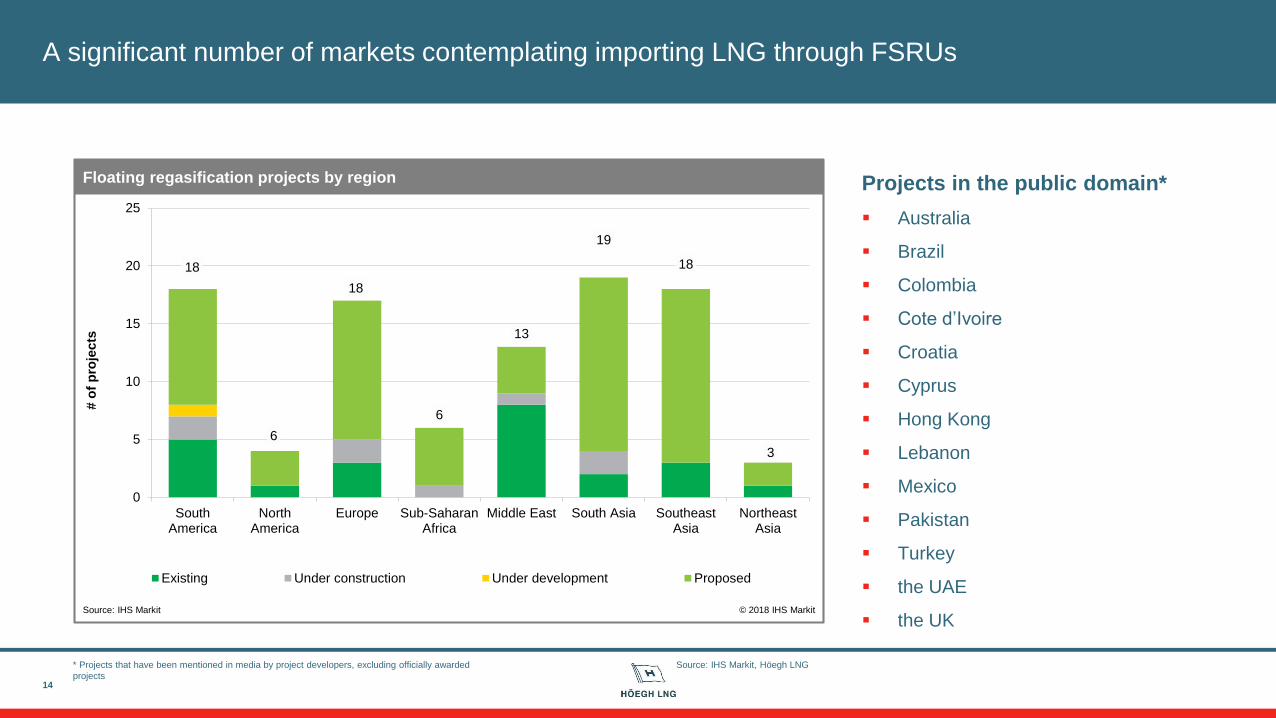

A significant number of markets contemplating importing LNG through FSRUs

Projects in the public domain*

▪ Australia

▪ Brazil

▪ Colombia

▪ Cote d’Ivoire

▪ Croatia

▪ Cyprus

▪ Hong Kong

▪ Lebanon

▪ Mexico

▪ Pakistan

▪ Turkey

▪ the UAE

▪ the UK

14

18

6

18

6

13

19

18

3

0

5

10

15

20

25

SouthAmerica

NorthAmerica

Europe Sub-SaharanAfrica

Middle East South Asia SoutheastAsia

NortheastAsia

Existing Under construction Under development Proposed

Floating regasification projects by region

Source: IHS Markit © 2018 IHS Markit

# o

f p

roje

cts

Source: IHS Markit, Höegh LNG* Projects that have been mentioned in media by project developers, excluding officially awarded

projects

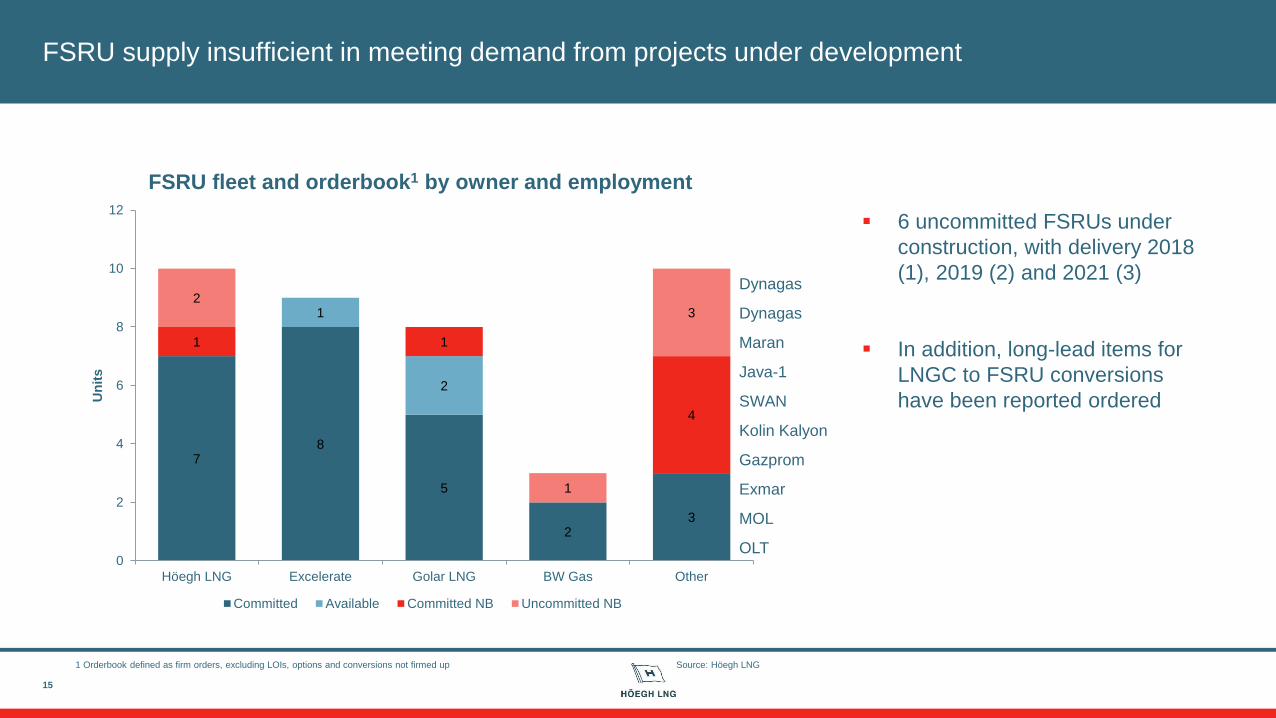

FSRU supply insufficient in meeting demand from projects under development

▪ 6 uncommitted FSRUs under

construction, with delivery 2018

(1), 2019 (2) and 2021 (3)

▪ In addition, long-lead items for

LNGC to FSRU conversions

have been reported ordered

15

78

5

23

1

2

1 1

4

2

1

3

0

2

4

6

8

10

12

Höegh LNG Excelerate Golar LNG BW Gas Other

Un

its

FSRU fleet and orderbook1 by owner and employment

Committed Available Committed NB Uncommitted NB

OLT

MOL

Gazprom

Maran

Kolin Kalyon

SWAN

Dynagas

Dynagas

Java-1

Exmar

Source: Höegh LNG1 Orderbook defined as firm orders, excluding LOIs, options and conversions not firmed up

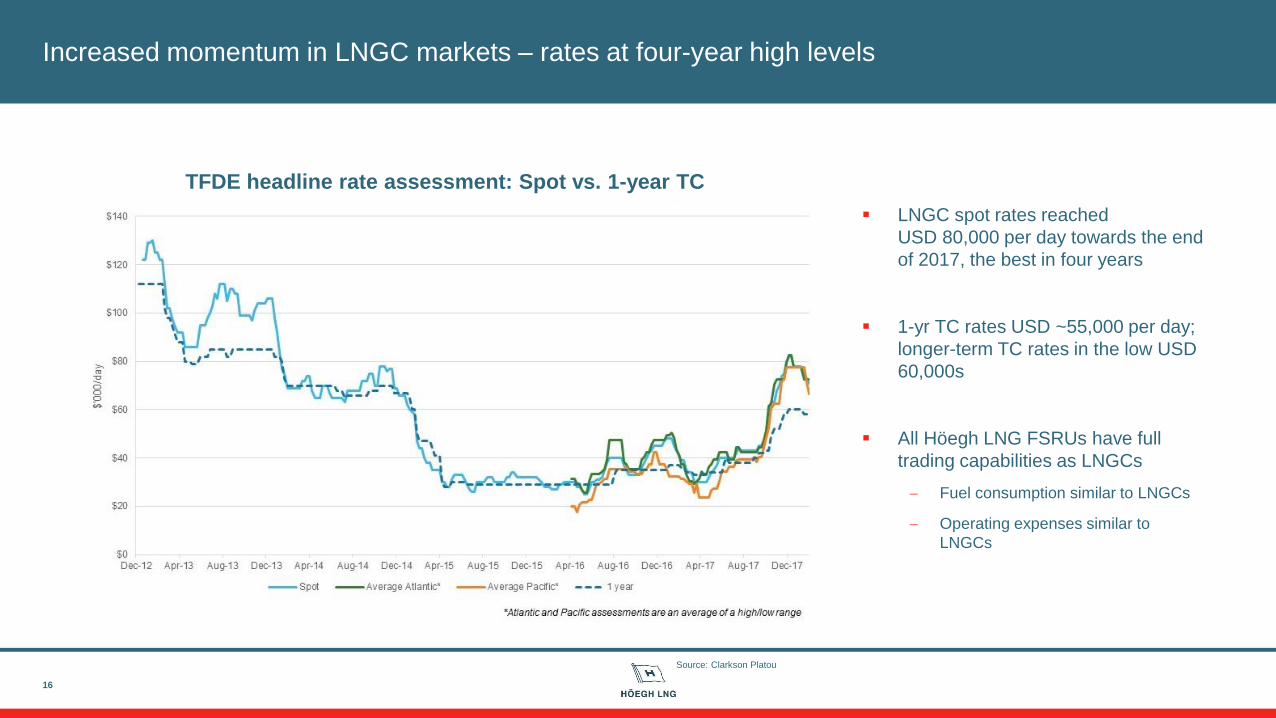

Increased momentum in LNGC markets – rates at four-year high levels

▪ LNGC spot rates reached

USD 80,000 per day towards the end

of 2017, the best in four years

▪ 1-yr TC rates USD ~55,000 per day;

longer-term TC rates in the low USD

60,000s

▪ All Höegh LNG FSRUs have full

trading capabilities as LNGCs

Fuel consumption similar to LNGCs

Operating expenses similar to

LNGCs

16

TFDE headline rate assessment: Spot vs. 1-year TC

Source: Clarkson Platou

Agenda

17

▪ Highlights

▪ Operational update

▪ Market update

▪ Financials

▪ Summary

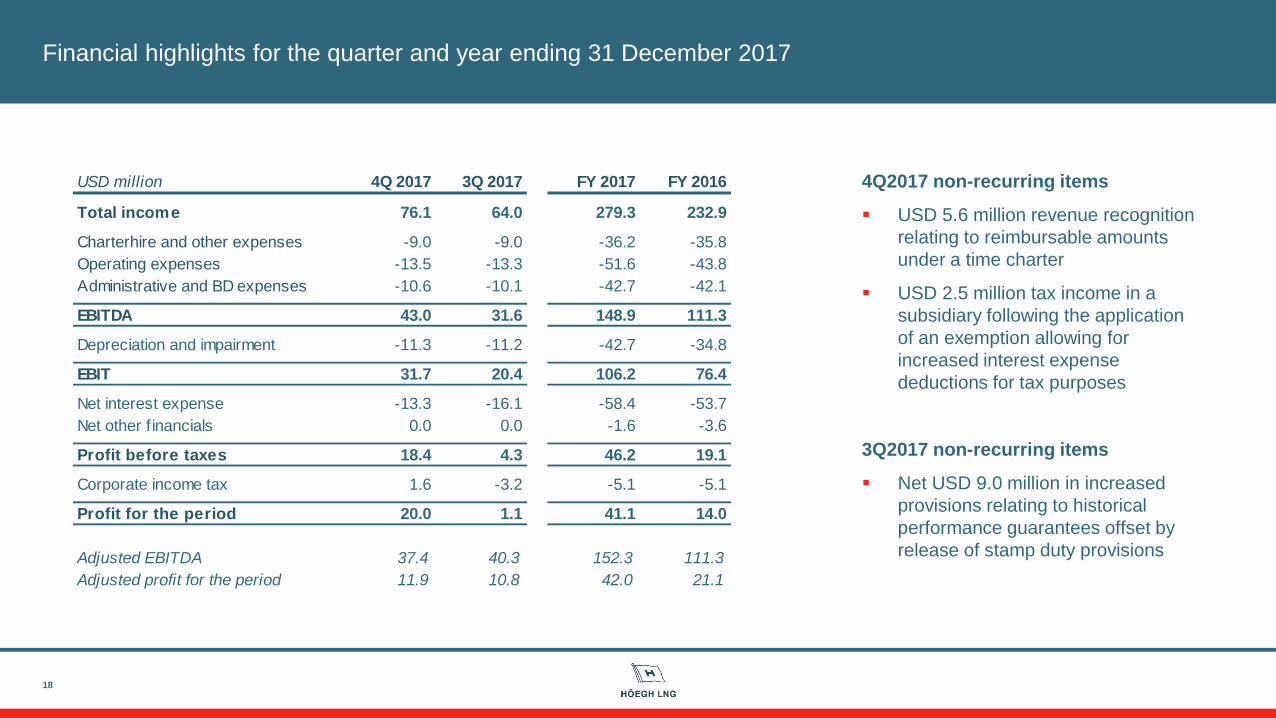

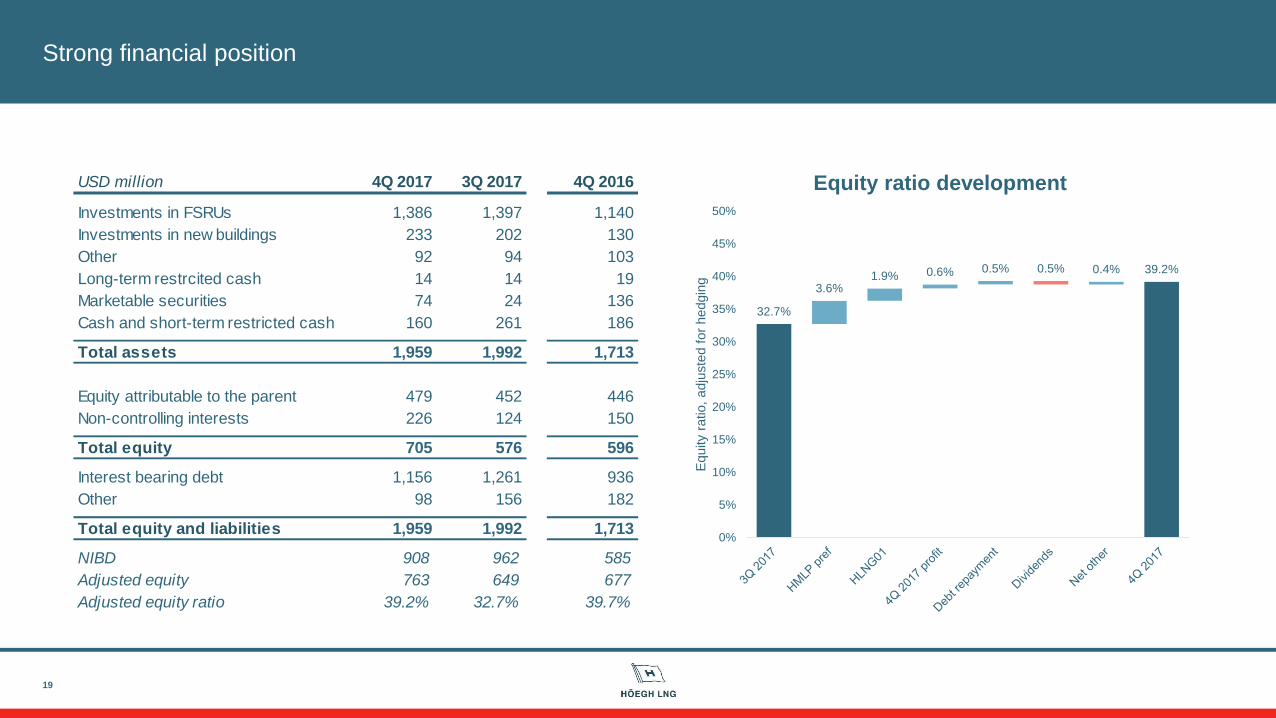

USD million 4Q 2017 3Q 2017 FY 2017 FY 2016

Total income 76.1 64.0 279.3 232.9

Charterhire and other expenses -9.0 -9.0 -36.2 -35.8

Operating expenses -13.5 -13.3 -51.6 -43.8

Administrative and BD expenses -10.6 -10.1 -42.7 -42.1

EBITDA 43.0 31.6 148.9 111.3

Depreciation and impairment -11.3 -11.2 -42.7 -34.8

EBIT 31.7 20.4 106.2 76.4

Net interest expense -13.3 -16.1 -58.4 -53.7

Net other f inancials 0.0 0.0 -1.6 -3.6

Profit before taxes 18.4 4.3 46.2 19.1

Corporate income tax 1.6 -3.2 -5.1 -5.1

Profit for the period 20.0 1.1 41.1 14.0

Adjusted EBITDA 37.4 40.3 152.3 111.3

Adjusted profit for the period 11.9 10.8 42.0 21.1

Financial highlights for the quarter and year ending 31 December 2017

18

4Q2017 non-recurring items

▪ USD 5.6 million revenue recognition

relating to reimbursable amounts

under a time charter

▪ USD 2.5 million tax income in a

subsidiary following the application

of an exemption allowing for

increased interest expense

deductions for tax purposes

3Q2017 non-recurring items

▪ Net USD 9.0 million in increased

provisions relating to historical

performance guarantees offset by

release of stamp duty provisions

USD million 4Q 2017 3Q 2017 4Q 2016

Investments in FSRUs 1,386 1,397 1,140

Investments in new buildings 233 202 130

Other 92 94 103

Long-term restrcited cash 14 14 19

Marketable securities 74 24 136

Cash and short-term restricted cash 160 261 186

Total assets 1,959 1,992 1,713

Equity attributable to the parent 479 452 446

Non-controlling interests 226 124 150

Total equity 705 576 596

Interest bearing debt 1,156 1,261 936

Other 98 156 182

Total equity and liabilities 1,959 1,992 1,713

NIBD 908 962 585

Adjusted equity 763 649 677

Adjusted equity ratio 39.2% 32.7% 39.7%

Strong financial position

19

32.7%

3.6%1.9% 0.6% 0.5% 0.5% 0.4% 39.2%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Equity

ratio,

adju

ste

d f

or

hedgin

g

Equity ratio development

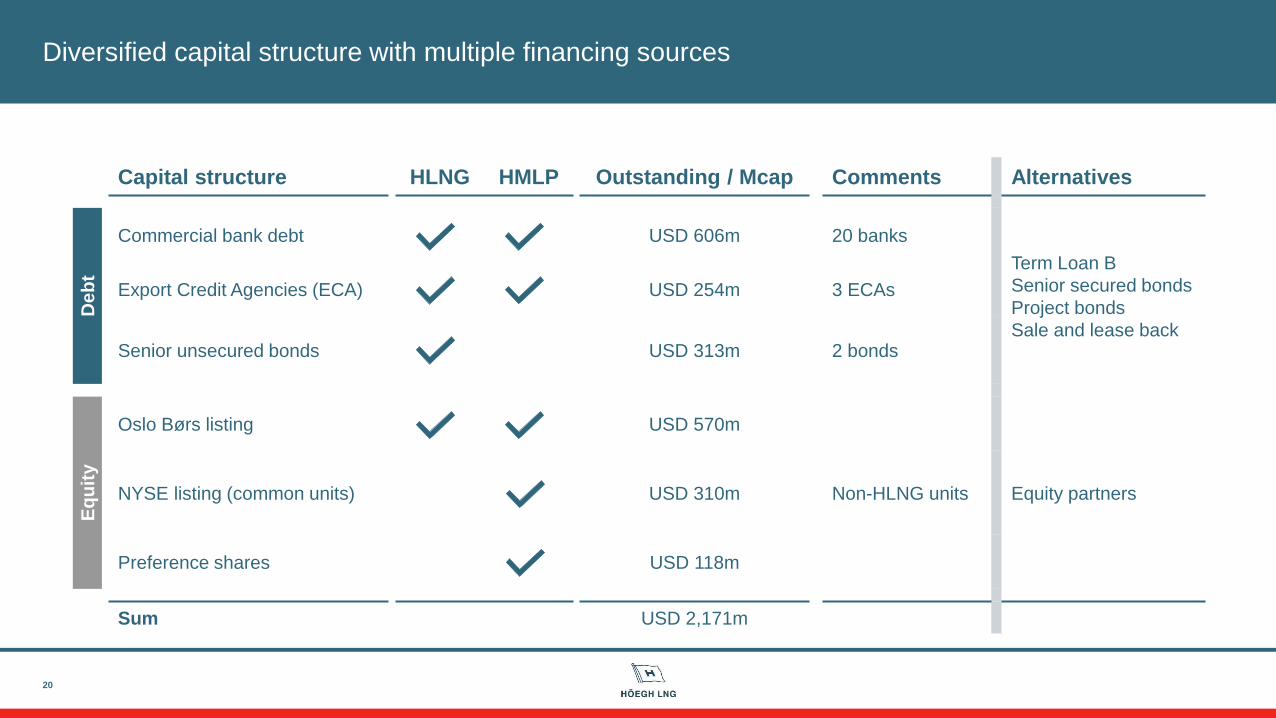

Capital structure HLNG HMLP Outstanding / Mcap Comments Alternatives

De

bt

Commercial bank debt USD 606m 20 banks

Term Loan B

Senior secured bonds

Project bonds

Sale and lease back

Export Credit Agencies (ECA) USD 254m 3 ECAs

Senior unsecured bonds USD 313m 2 bonds

Eq

uit

y

Oslo Børs listing USD 570m

Equity partnersNYSE listing (common units) USD 310m Non-HLNG units

Preference shares USD 118m

Sum USD 2,171m

Diversified capital structure with multiple financing sources

20

0

50

100

150

200

250

300

350

400

450

500

2018 2019 2020 2021 2022

US

D m

illio

n

Debt repayment schedule

Amortisation Amortisation refinanced debt Balloons Bonds

Debt repayments spread out in time

▪ Amortisation includes debt on

FSRUs #8-10, assuming that

financing for FSRUs #9-10 are

structured similarly to FSRU #8

▪ Amortisation of refinanced debt

assumes similar amortisation profile

as the current facilities, and that

balloons are refinanced in full

▪ Commercial debt tranches on

Independence, Gallant, Grace and

Lampung mature ahead of ECA

tranches with 12 year tenors

21

Independence

Höegh Gallant

HLNG02

Höegh Grace

Lampung

HLNG03

Höegh Giant

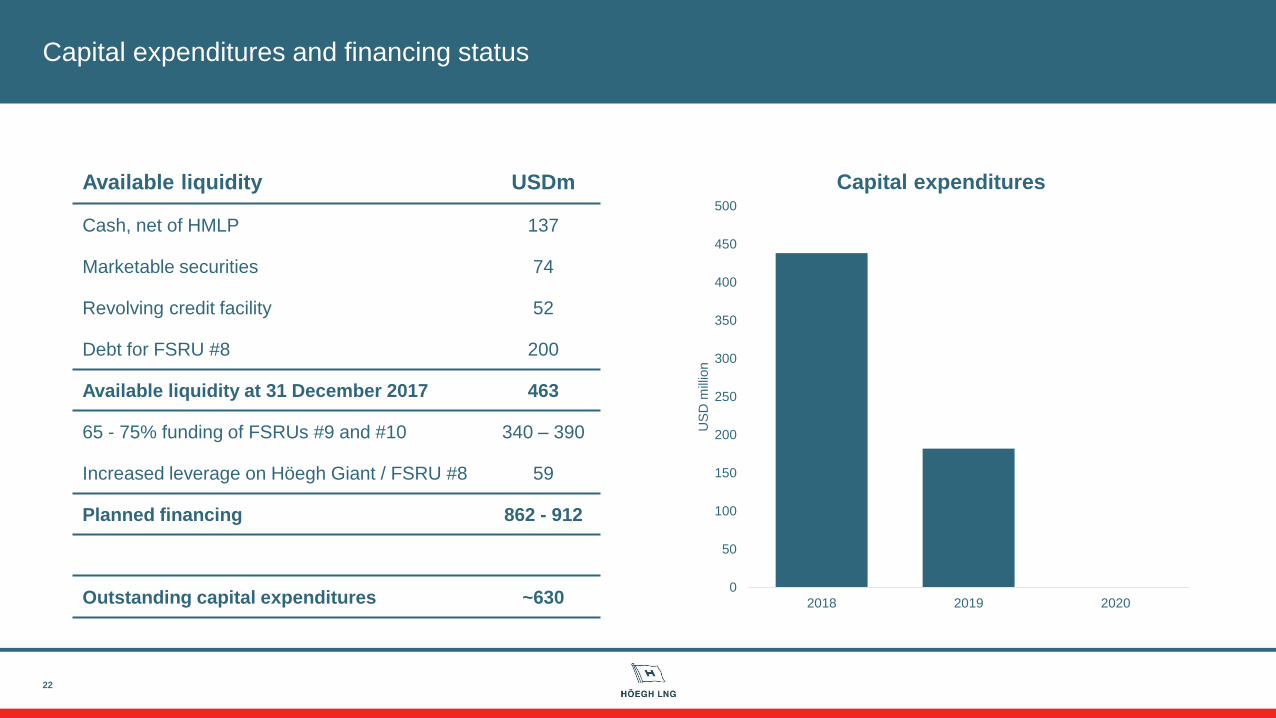

Capital expenditures and financing status

22

Available liquidity USDm

Cash, net of HMLP 137

Marketable securities 74

Revolving credit facility 52

Debt for FSRU #8 200

Available liquidity at 31 December 2017 463

65 - 75% funding of FSRUs #9 and #10 340 – 390

Increased leverage on Höegh Giant / FSRU #8 59

Planned financing 862 - 912

Outstanding capital expenditures ~6300

50

100

150

200

250

300

350

400

450

500

2018 2019 2020

US

D m

illio

n

Capital expenditures

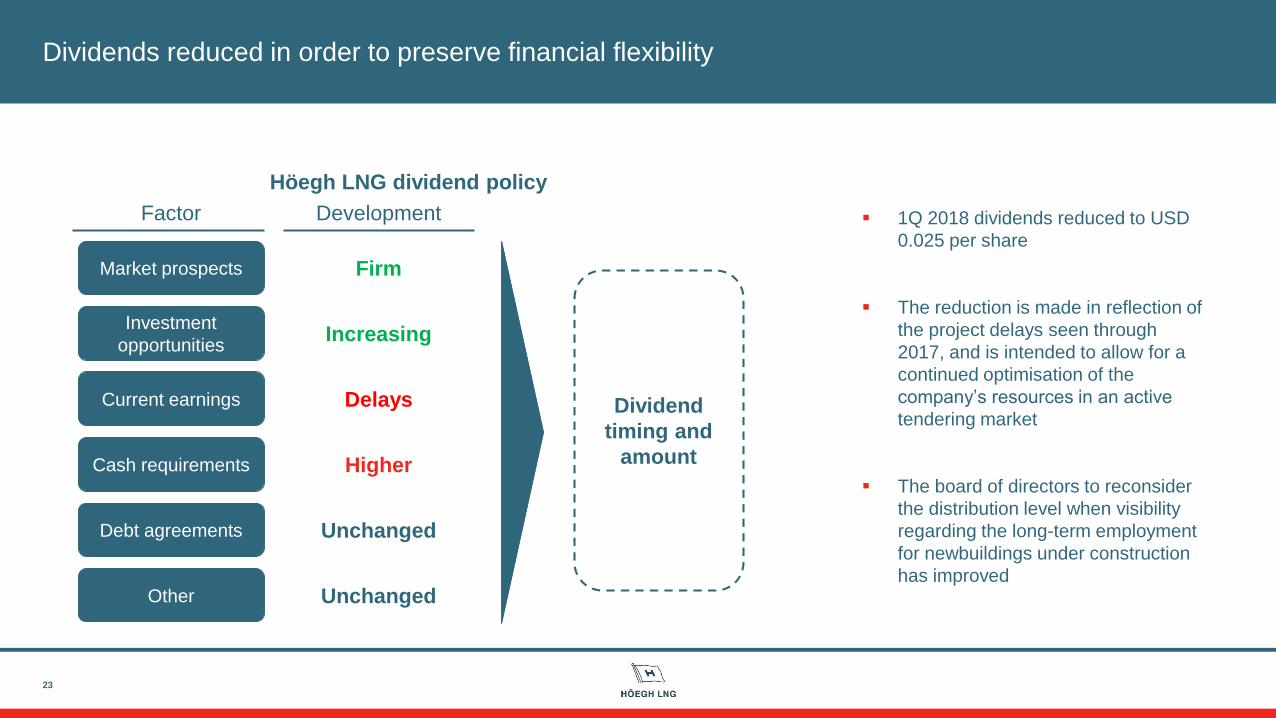

Dividends reduced in order to preserve financial flexibility

23

▪ 1Q 2018 dividends reduced to USD

0.025 per share

▪ The reduction is made in reflection of

the project delays seen through

2017, and is intended to allow for a

continued optimisation of the

company’s resources in an active

tendering market

▪ The board of directors to reconsider

the distribution level when visibility

regarding the long-term employment

for newbuildings under construction

has improved

Höegh LNG dividend policy

Market prospects

Current earnings

Investment

opportunities

Cash requirements

Debt agreements

Other

Factor Development

Dividend

timing and

amount

Firm

Increasing

Delays

Higher

Unchanged

Unchanged

Agenda

24

▪ Highlights

▪ Operational update

▪ Market update

▪ Financials

▪ Summary

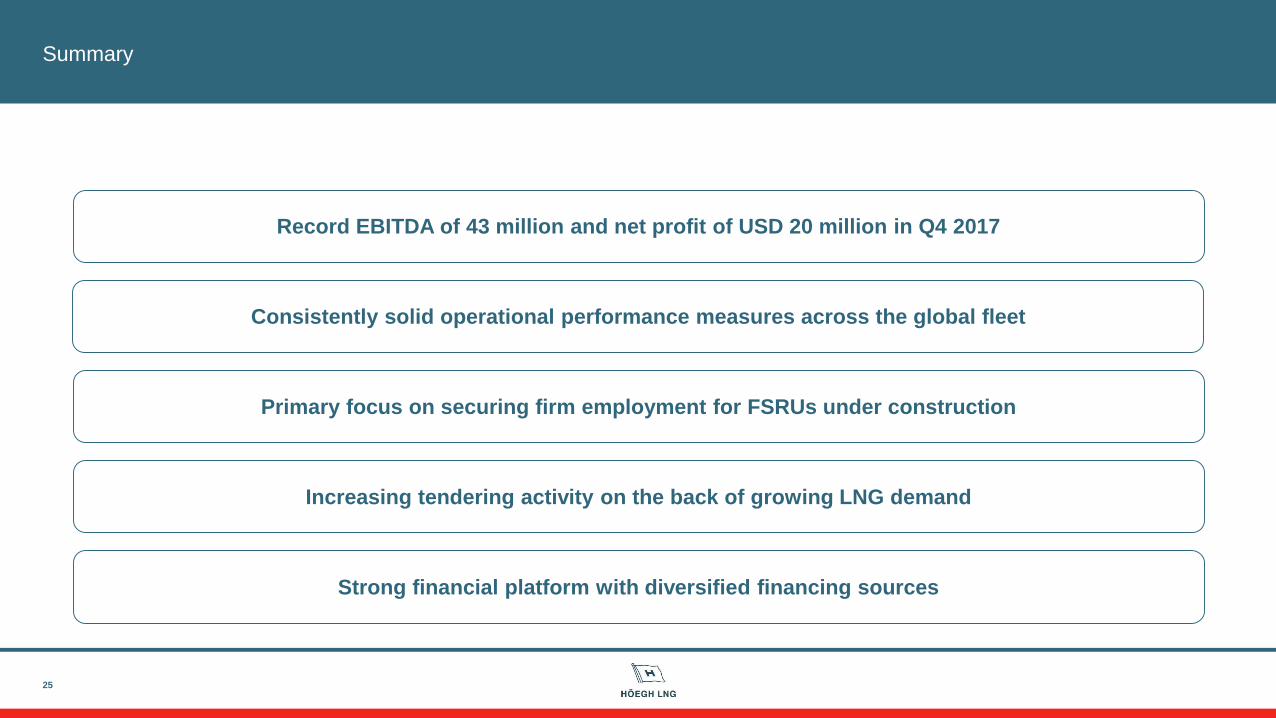

Summary

25

Consistently solid operational performance measures across the global fleet

Record EBITDA of 43 million and net profit of USD 20 million in Q4 2017

Strong financial platform with diversified financing sources

Increasing tendering activity on the back of growing LNG demand

Primary focus on securing firm employment for FSRUs under construction

26

Q&A session

Call-in details:

Norway +47 21 00 26 10

United Kingdom +44 (0)330 336 9105

United States +1 323 794 2093

Participant passcode: 2575256

Webcast:

http://webtv.hegnar.no/presentation.php?webcastId=77876347

Agenda

27

▪ Appendices

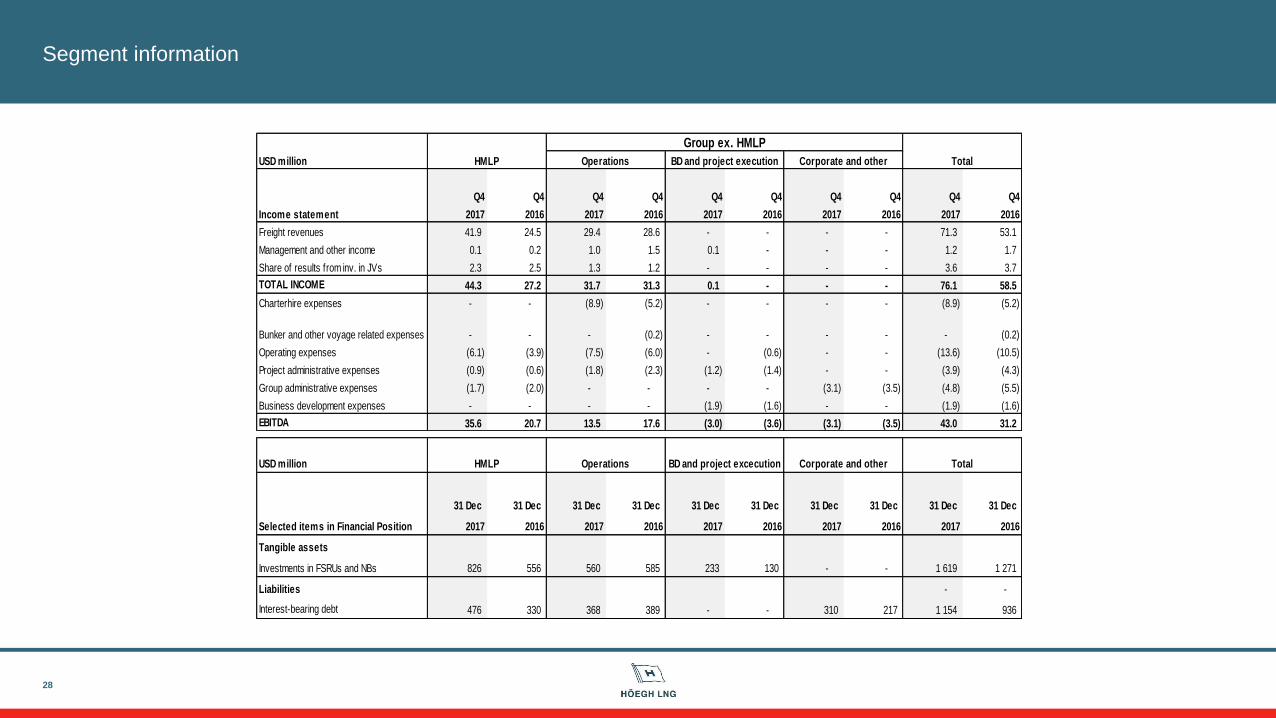

Segment information

28

Group ex. HMLP

USD million HMLP Operations BD and project execution Corporate and other Total

Q4 Q4 Q4 Q4 Q4 Q4 Q4 Q4 Q4 Q4

Income statement 2017 2016 2017 2016 2017 2016 2017 2016 2017 2016

Freight revenues 41.9 24.5 29.4 28.6 - - - - 71.3 53.1

Management and other income 0.1 0.2 1.0 1.5 0.1 - - - 1.2 1.7

Share of results from inv. in JVs 2.3 2.5 1.3 1.2 - - - - 3.6 3.7

TOTAL INCOME 44.3 27.2 31.7 31.3 0.1 - - - 76.1 58.5

Charterhire expenses - - (8.9) (5.2) - - - - (8.9) (5.2)

Bunker and other voyage related expenses - - - (0.2) - - - - - (0.2)

Operating expenses (6.1) (3.9) (7.5) (6.0) - (0.6) - - (13.6) (10.5)

Project administrative expenses (0.9) (0.6) (1.8) (2.3) (1.2) (1.4) - - (3.9) (4.3)

Group administrative expenses (1.7) (2.0) - - - - (3.1) (3.5) (4.8) (5.5)

Business development expenses - - - - (1.9) (1.6) - - (1.9) (1.6)

EBITDA 35.6 20.7 13.5 17.6 (3.0) (3.6) (3.1) (3.5) 43.0 31.2

USD million

31 Dec 31 Dec 31 Dec 31 Dec 31 Dec 31 Dec 31 Dec 31 Dec 31 Dec 31 Dec

Selected items in Financial Position 2017 2016 2017 2016 2017 2016 2017 2016 2017 2016

Tangible assets

Investments in FSRUs and NBs 826 556 560 585 233 130 - - 1 619 1 271

Liabilities - -

Interest-bearing debt 476 330 368 389 - - 310 217 1 154 936

TotalHMLP Operations BD and project excecution Corporate and other