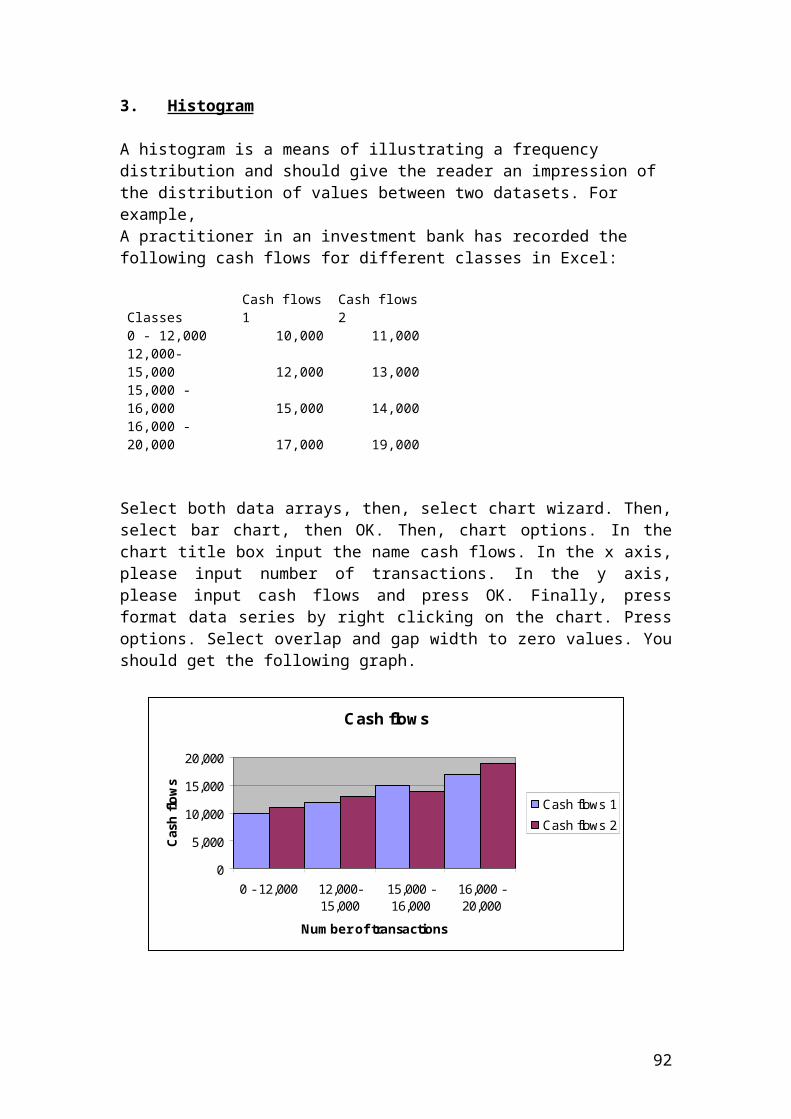

Embed Size (px)

Citation preview

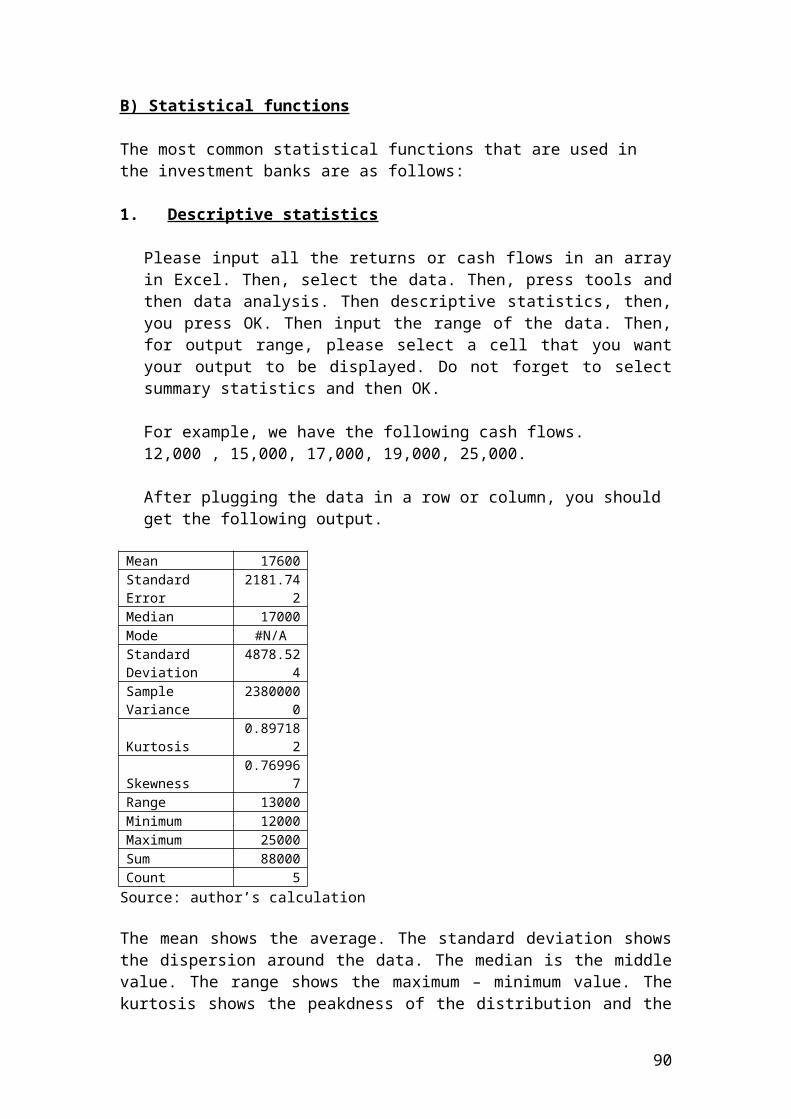

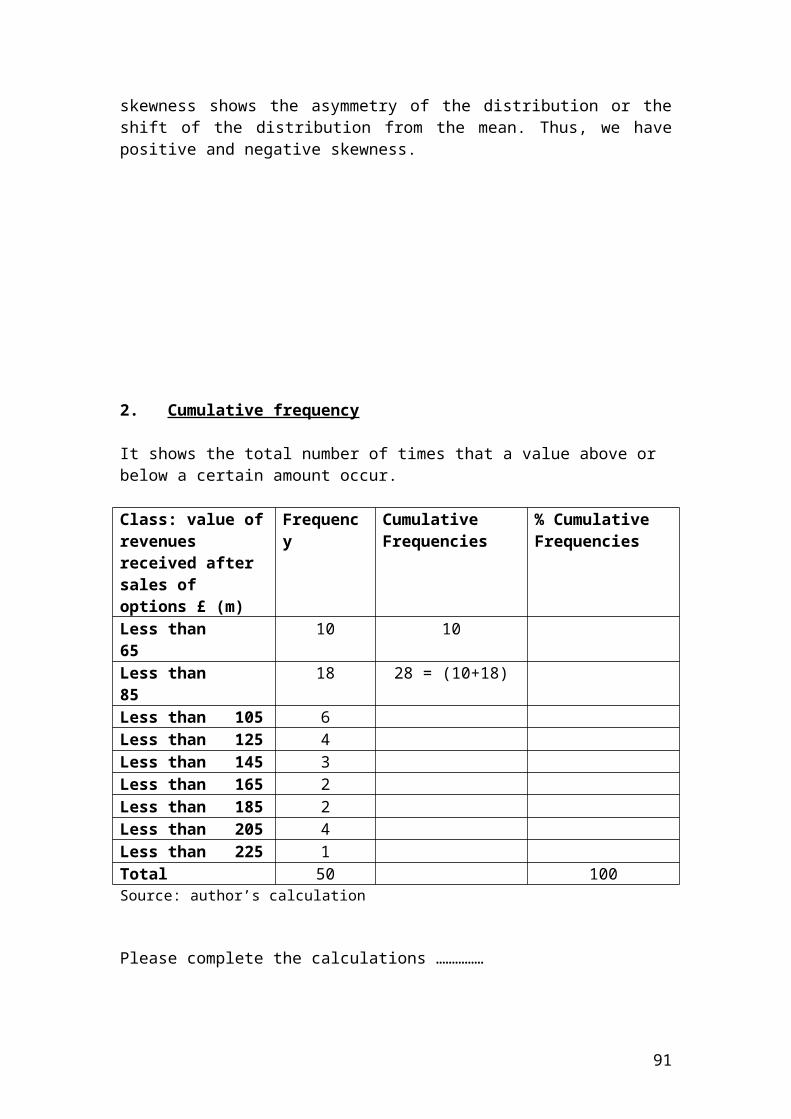

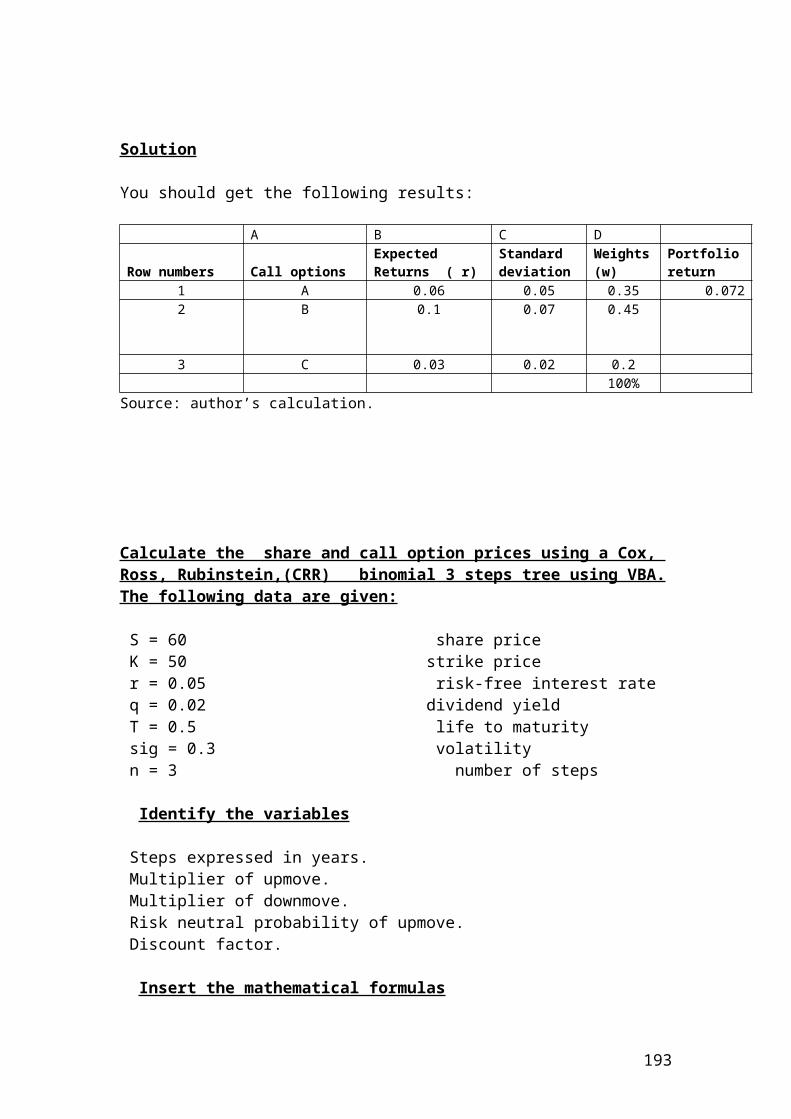

Investments in hedge funds and other private investment funds involve a high degree of risk. You could lose all or a substantial amount of your investment. Check carefully the trading strategy that you are going to invest. Each fund is associated with different types of risks. When investing in a particular hedge fund, you should carefully read a fund’s offering materials and related information for specific risk and other important information regarding your investment. I have attached a monthly performance of a hedge fund and the related statistics.

Check the skill of the hedge fund manager or alpha defined as the intercept from the regression. Alpha, is used to measure the ability of managers to outperform the base index. A positive and statistically significant indicates a skilled fund manager whose decisions add value to the fund. Rhodes (2000) argued, that “persistent performance shows that some fund managers are able to outperform their peers. This implies that the fund managers must either have access to information that is insider or not widespread or make use of information in a speedier way than other managers. As markets become more efficient it will be more difficult for any fund manager to outperform the market continuously”(Rhodes,2000,p.7). On the other hand, negative values or statistically insignificant values represent inferior or neutral performance of the manager. In other words, a negative indicates a poorly performing manager whose decisions affect negatively the value of the fund. Check the risk premium which equal to the slope of the security market line. It is the difference between the expected return of the portfolio and the risk – free rate. Calculate monthly mean returns and standard deviations of different hedge funds categories and check the volatility of returns. The best fund is the one with high mean return and low standard deviation. Seventy percent of alphas come from the dynamic rebalancing of strategies. The other 30% comes from superior manager selection. The average manager that is employed in the fund has about $1 billion in assets under management. He/she has been in business five to seven years and has a five to seven year track record that has outperformed its own benchmark. In other words, if it were a distressed debt manager, it would be someone who would have outperformed the distressed debt sub-index of the Tremont index when the trading strategy is distressed securities. Usually, when balance sheets were stressed, we have an economic recovery which is forcing yield spreads to compress. Please analyze economic cycles along two dimensions, growth and interest rates, and break it into quadrants. All economic cycles begin with a low growth, low interest rate environment. Then proceed clockwise through a quadrant scenario, where we are moving to a higher growth, low interest rate area where the Fed is being supportive of growing the economy. Then we move into a high growth, high interest rate quadrant, and that is typically where the Fed is now beginning to be concerned or the central banks become concerned about inflation and overheating the economy. That forces the economy into the final stage, which is high interest rate and low growth type of environment where you have an inverted yield curve. Check the meaning of the invested yield curve in the fixed – income investments document.

1

Check the relationship between incentive and management fees. Select the fund with the lowest fees.

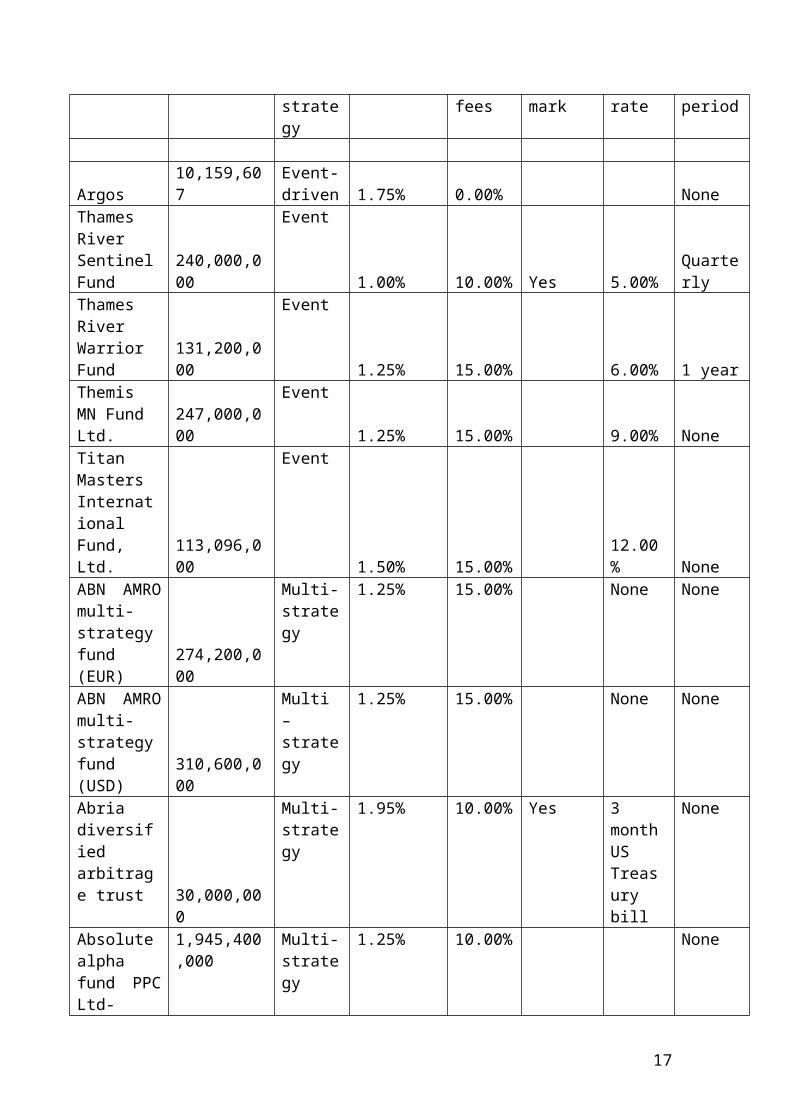

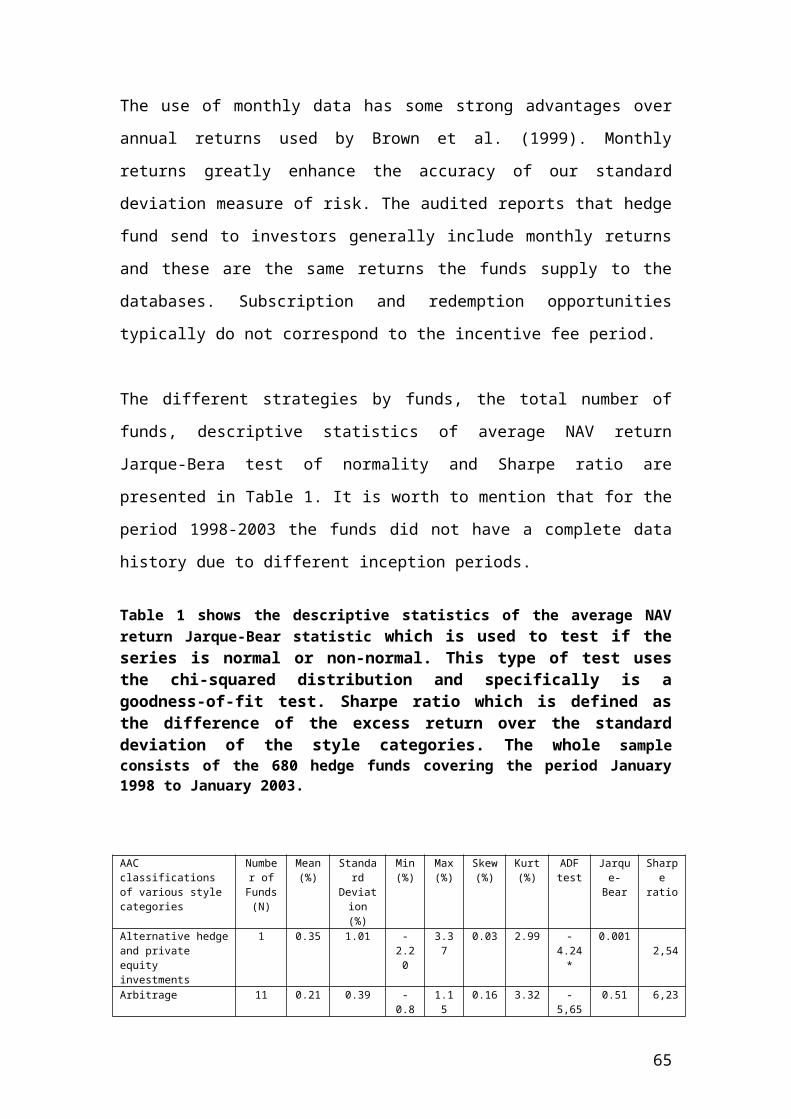

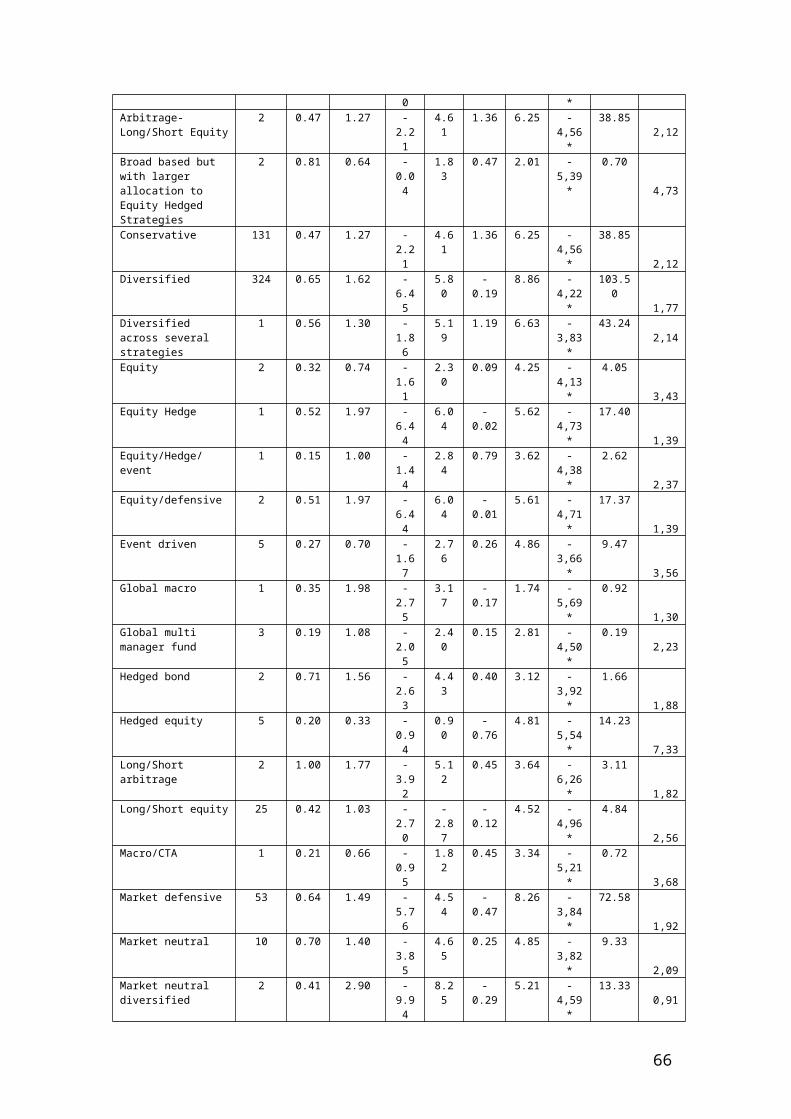

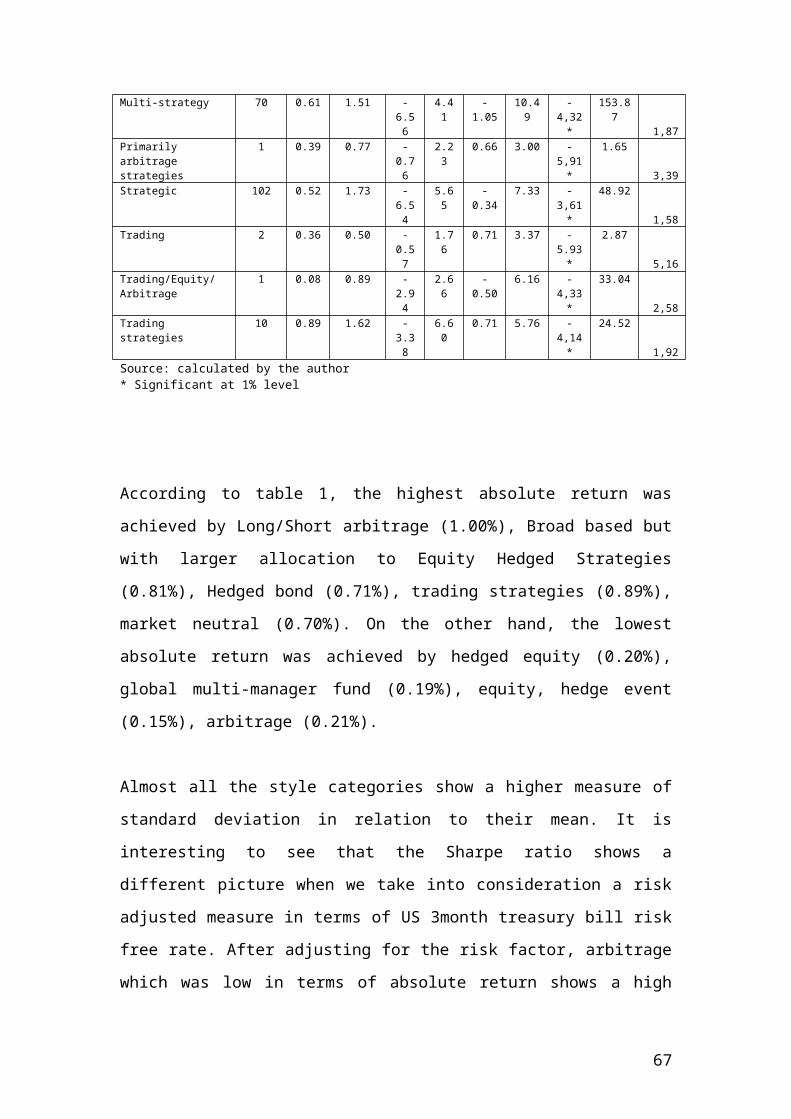

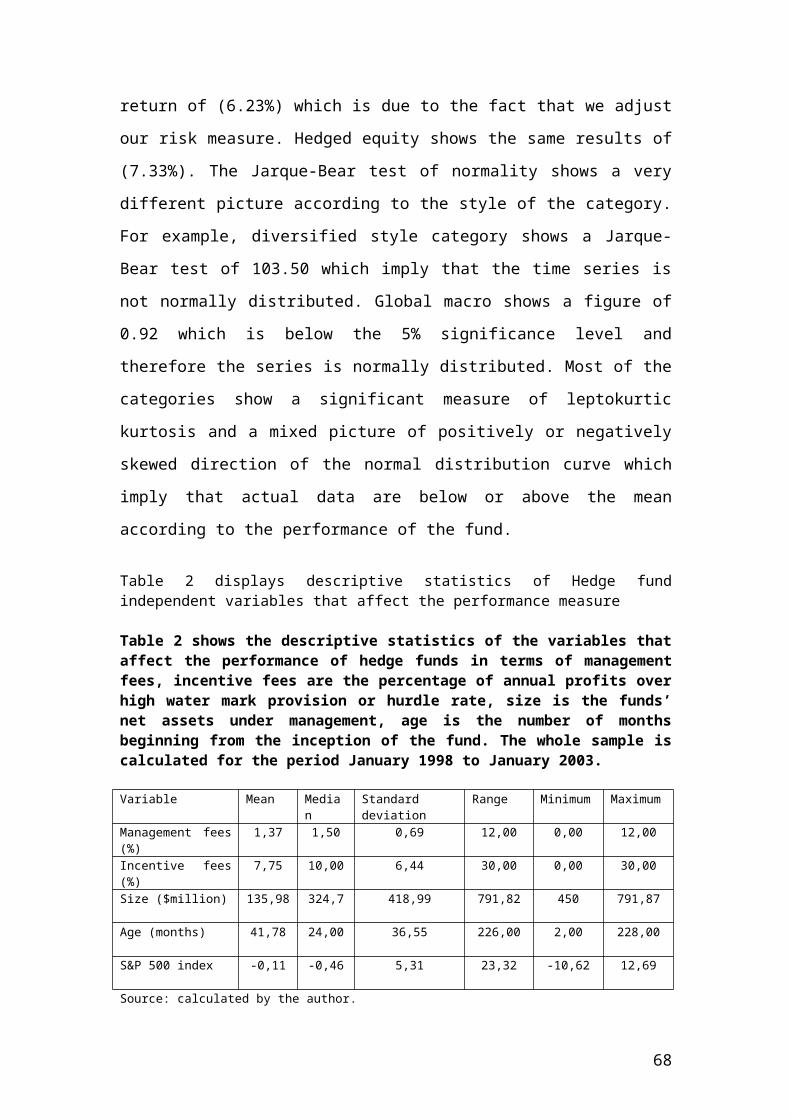

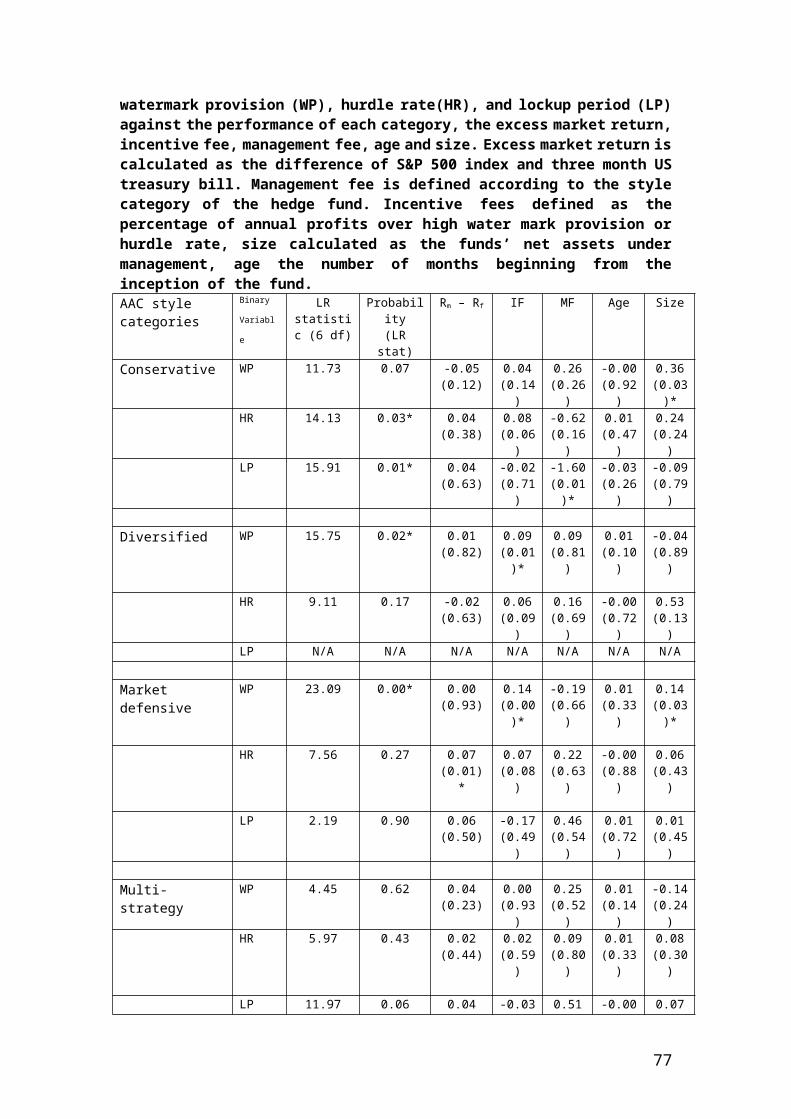

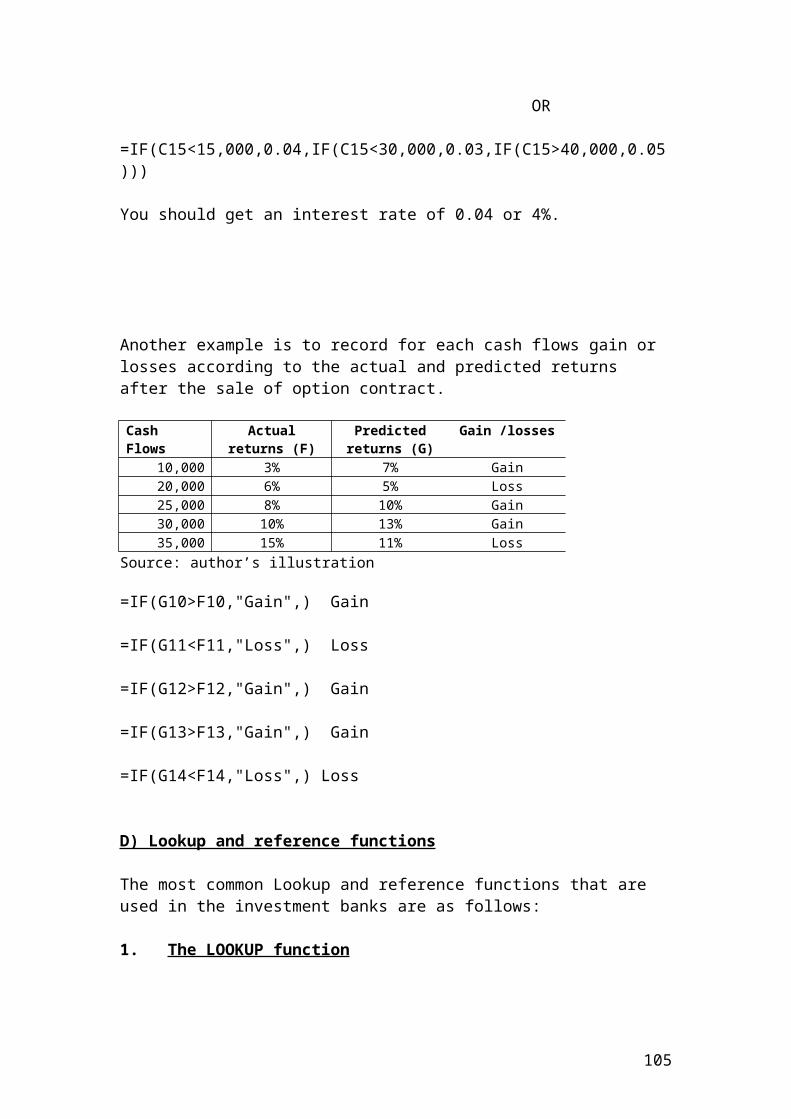

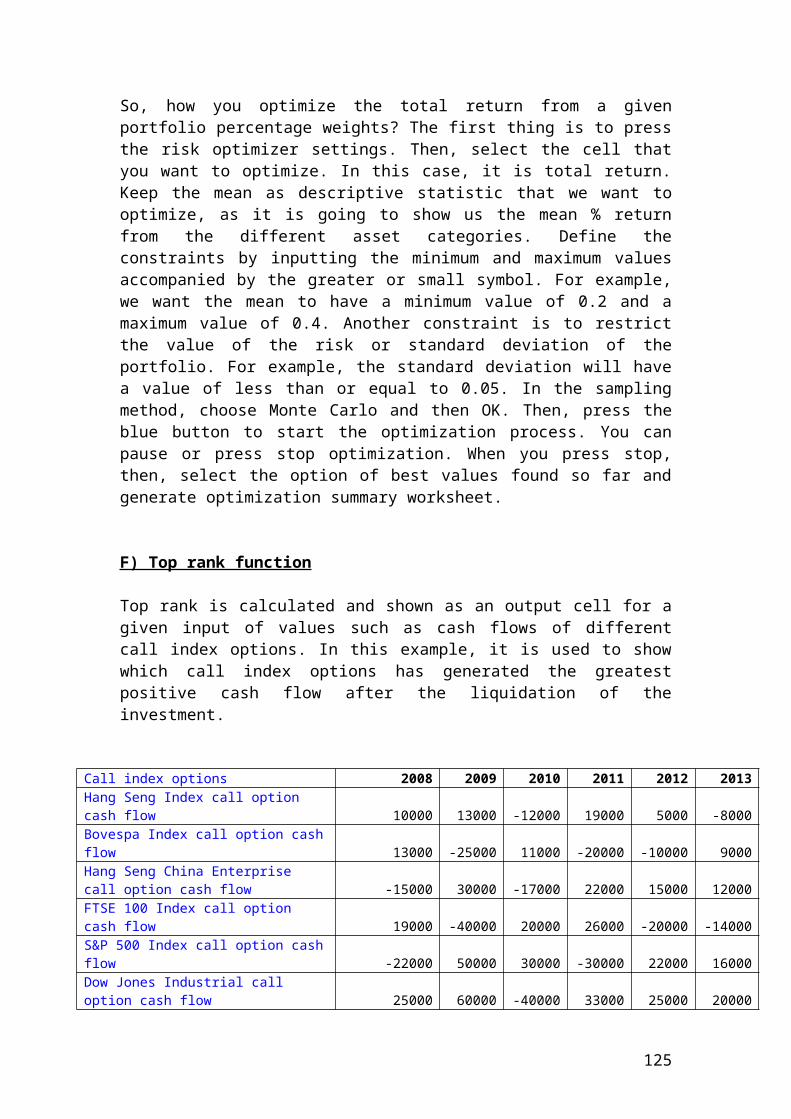

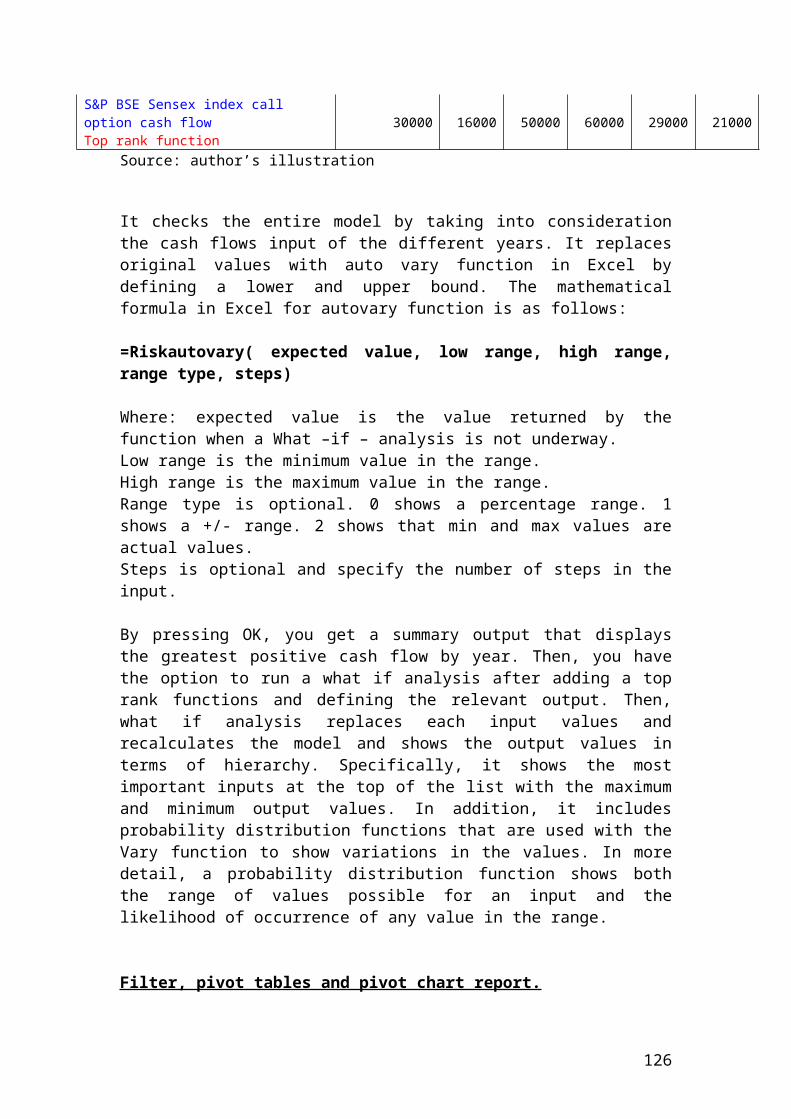

I have attached a table with a sample of hedge funds to show the structure and their performance in terms of trading strategy, assets under management, management fees, incentive, fees, high – water mark, hurdle rate, and lock-up period.

Please check the different ratios that are used in the hedge fund industry. I have added a sample of the funds that constitute each investment strategy and index.

Due to confidentiality reasons, I will not be able to disclose information and data related to the funds that constitute the various trading strategies. For example, I cannot disclose from the Credit Suisse site information related to the performance of the different indices. Please refer to the web site of Credit Suisse. www.hedgeindex.com

You will find information concerning monthly performance, indices and sub categories of the various trading strategies. In addition, it is listed the monthly standard deviation annualized and Sharpe ratio data. The Sharpe ratio is calculated through the use of the 90 day Treasury bill rate that represents the risk – free rate. You will also find Dow Jones indices and other information such as alternative beta indexes. After taking into consideration copyright agreement, you can e-mail them for a login account to download cumulative statistics, NAV prices in different currencies and for different indexes such as the Credit Suisse broad hedge fund index, the credit Suisse all hedge index, and the Credit Suisse blue chip hedge fund index. Finally, you will find information concerning the correlations matrix between an investment strategy and the relevant index, quarterly and monthly performance data. Good luck!

To solve my problem, I am going to use a past database that includes information concerning the individual funds that constitute the strategy, the lockup period, the hurdle rate, incentive and management fees and watermark provision. I would like to thanks Karen Henseleit sales manager for passing to me the data from Datafeeder. The Alternative Asset Center (AAC), the Fund of Hedge Funds Specialist and the Hedge Funds DataFeeder. I am trying to facilitate you to understand how the hedge funds industry is working. Thanks for the participation. The old database provide information concerning the fund name under different strategies, the management fees, the incentive fees, the high water mark provision, the hurdle rate, the lock-up period, the fund assets, monthly returns and monthly standard deviations.

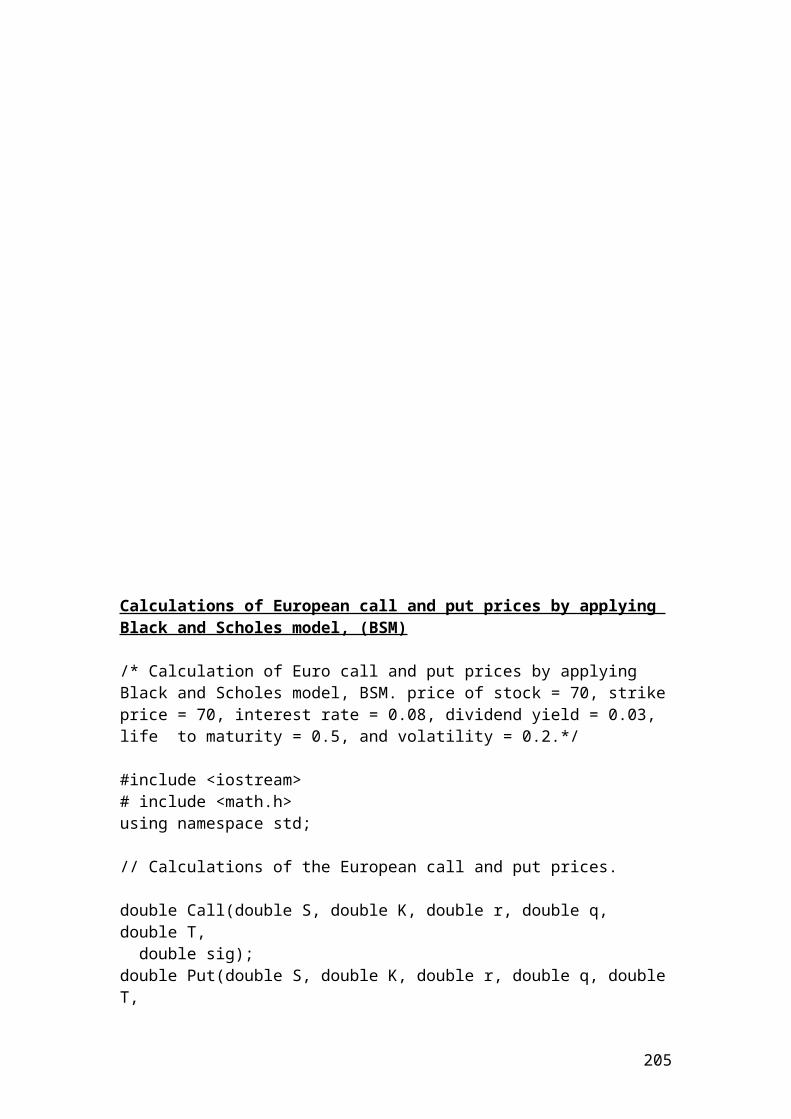

I have added the introduction, a detailed section of the trading strategies, Excel and the computer programming in terms of C++, Java, VBA, Python, etc…

The book is under construction and it is lacking many sections. Hedge funds are very important in the investment industry. They are used to hedge different types of risk by using derivatives products. Hedge fund managers use call and put options, commodity futures, forward contracts, index, currency and fixed

2

income options and futures to hedge credit risk, market risk, country risk, sector risk, company risk, interest rate risk and currency risk. Thus, in addition to stocks and bonds they use their derivatives product to hedge or speculate according to the investment strategy, the market and political trend. They are used from wealthy investors that have a capital higher than 250,000 USD. In some cases the invested capital could be 1,000,000 USD or more than 10,000,000 USD.

Step – by - step introduction to Hedge funds. A practical guide for postgraduate, research students and investors.

Dr Michel Zaki Guirguis 19/01/2017

Bournemouth UniversityInstitute of Business and LawFern BarrowPoole, BH12 5BB, UKTel:0030-210-9841550Mobile:0030-6982044429Email: [email protected]

1 Τhe permanent address of the author’s is 94, Terpsichoris road, Palaio-Faliro, Post Code:17562, Athens, Greece.

3

Table of Contents

Preface

Acknowledgments

Chapter 1

Hedge funds categories and strategies

Introduction

Definition and purpose of the hedge funds industry Convertible arbitrage Emerging markets Equity market neutral Event driven Distressed securities Fixed income arbitrage Global macro Long/short equity Options Fund of funds Managed futures / CTAs Multi - strategy

Chapter 2

Hedge funds indices

Credit Suisse convertible arbitrage index Dow Jones world emerging markets index Equity market neutral S&P 500 index Credit Suisse event driven index Suisse high yield II and credit index distressed securities Citigroup world government bond index,WGBI, for fixed income arbitrage Credit Suisse global macro index Credit Suisse long/short equity index S&P Goldman Sachs commodities index options Credit Suisse all hedge fund index fund of funds Credit Suisse managed futures/CTAs index Dow Jones world index multi - strategy

4

Chapter 3

Performance measurement and attribution of hedge funds

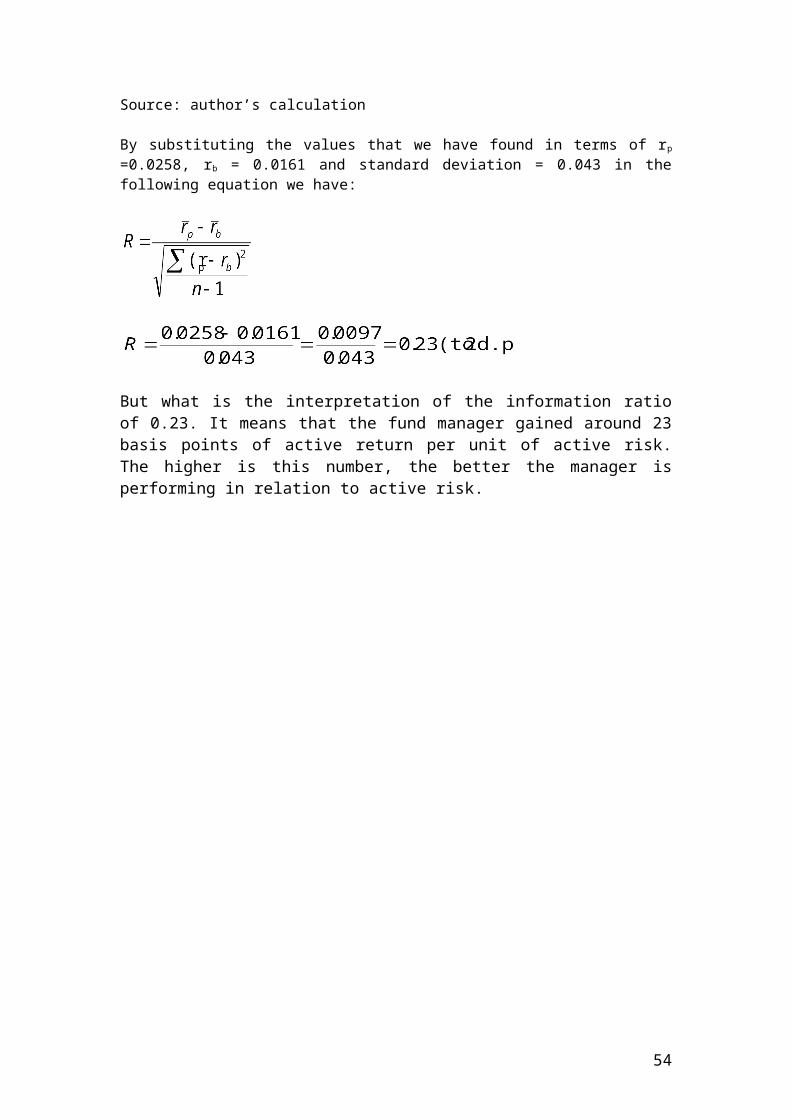

Introduction to style analysis Rolling methodology of performance measurement Introduction to different types of ratios Passive management, tracking error, and the information ratio

Chapter 4

Fees structure interrelation to hedge funds

Management fees Incentive fees Water marks Hurdle rate Lock –up period

Chapter 5

Related articles of hedge funds. Application with industrial examples. An empirical analysis of the performance of Hedge Funds over the period

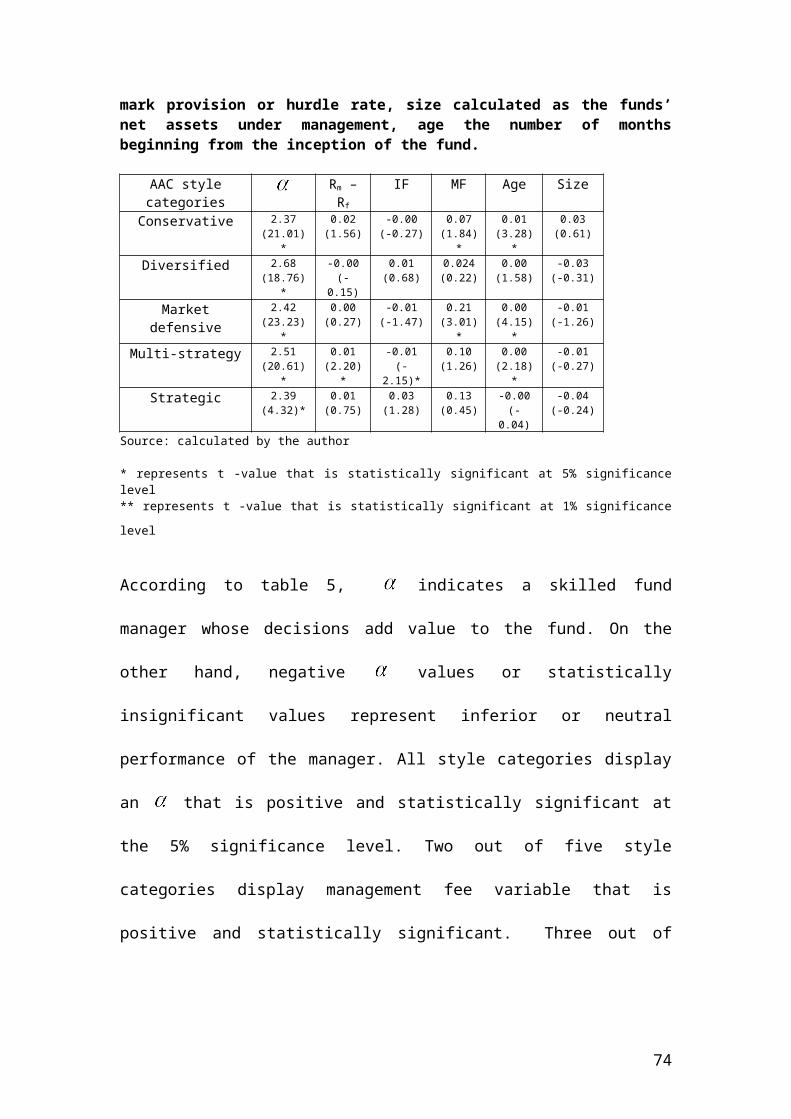

1998 to 2003 in terms of incentive fees, management fees, size, age, hurdle rate, high watermark provision and lockup period.

Application of a GARCH, TGARCH and EGARCH models to test the volatility of monthly returns of Credit Suisse All Hedge Market Neutral Funds.

Application of a linear Gaussian space model and the Kalman filter in estimating expectations of the natural logarithmic monthly returns of offshore strategic hedge funds.

Comparison of the census X12 and Tramo / Seats additive ARIMA (p,d,q) seasonal adjustment models applied to diversification of long/short equity hedge funds categories.

Measuring technical, allocative and overall cost efficiency of commodity hedge funds futures contracts by applying data envelopment analysis, (DEA).

Applying and comparing Sharpe style analysis versus a rolling methodology of loagarithmic monthly returns of long/short funds, market – neutral funds, global macro funds, event – driven funds and their related indices.

Chapter 6

5

Workshops of hedge funds in terms of Excel and other computer language programming

Workshop of functions application in Excel Workshop of functions application in Excel in terms of the

Decision tools and Stat tools Suite from Palisade organisation. http://www.palisade.com Workshop of language programming in terms of VBA in Excel Workshop of language programming in terms of C++ Workshop of language programming in terms of SQL Workshop of language programming in terms of Oracle Workshop of language programming in terms of Python Workshop of detailed explanation of Matlab Workshop of analysis of financial data, scientific programming

and simulation using R language programming Workshop of statistical analysis and applications by using Java

statistical program

References & Bibliography

Preface

6

This book is designed to provide an overview and introduction to the hedge funds industry. Hedge funds are not a complicated subject. To better understand them, please refer to my previous book introduction to financial derivatives. The reason is that hedge funds strategies are based on leveraged, long and short positions of derivatives products.

A lot of students and especially the one that do not have strong quantitative skills will feel vulnerable when taking this subject. If the level of mathematical sophistication is too high, the material is likely to be inaccessible to many students. If it is too low, some important issues will inevitable be treated in a rather superficial way. The book covers BA and BS, MA and MS in Risk Management, Business Administration, Financial Services, Computational Finance and International Business and Financial Derivatives.

Specifically, the book will have a lot of features that will distinguish it from the already published books. It provides a new approach of gaining some basic familiarity with the essential concepts of the hedge funds industry and the Orthodox Christianity. The aim of trading is to help the poors and the beggars. In addition, it is written in a very accessible style that will not frighten the students.

Most importantly, the book includes a range of materials to help the student, the practitioners and the investors to reinforce their learning skills. Each section offers a solid explanation of basic concepts, followed by examples for the reader to work through. Moreover, each chapter will include practical examples from Financial Times and visual representation of graphs in order to help the reader to combine the basic theoretical concepts with real situations examples from various companies. This book is aimed to cover the learning needs of a variety of readers. The basic needs of the above mentioned target group are similar in terms that both lack confidence about their numerical skills and both are motivated to learn basic knowledge. The average investor wants to learn how these products work but he/she cannot understand very easily the academic terminology. On the other hand, postgraduate students need to learn quickly the basic concepts in order to proceed to more advanced textbooks that deals with advanced stochastic calculus.

The market will be very responsive for our book especially that a lot of international students experience problem with their English and their numerical skills. It will cover the basic needs of postgraduate students and those who are interesting in alternative investments. The market in the next five years will become very complicated and would require the use of sophisticated risk management techniques in order to hedge market, operational, and credit risk. The use of derivatives and Hedge funds will be essential even for the average investor in terms of profit and protection from the highly competitive and hostile environment. This book will have a broader international appeal as it covers the UK, the European, and the US market.

In addition, we will include a variety of workshops related to language programming in terms of VBA for Excel, C++, SQL, Oracle, Python, R language programming, and Java. I will also include a mathematical and statistical software such as Matlab and the decision tools and stat tools suite from Palisade organisation. The aim is to facilitate the undergraduate, postgraduate and research students to proceed smoothly in their career in the investment banks without stress and confusion.

7

The investment industry will hire persons that possess practical expertise that sustain quality, spiritual integrity and efficiency in the financial market. Investment banks will hire applicants that are able to hedge different types of risk and achieve successful spiritual and therefore investment decisions. After reading this book, students of Bournemouth University could easily and in a relaxed way join the back and front office of alternative investments department of JP Morgan Chase or other investment bank.

Acknowledgments

First of all, I would like to thank my parents and especially my mother and father for giving me the opportunity to write this book and for their continued support, encouragement, and sacrifices during this period. I would also like to thank my supervisors Professor Philip Hardwick and Dr Geoff Willcocks for their continued

8

support and help. I would like to thank the Schweser Kaplan organisation for the professional education that covers the syllabus of the Chartered Financial Institute, (CFA). I would like to thank Mr Chandan Sengupta for helping me through his book to understand in detail how to apply financial analysis and modelling using Excel and VBA. I would like to thank Palisade organisation for issuing me demo academic software that shows the application of the decision tools and Stat tools Suite in Excel. I strongly recommend that you buy this software. Their website is http://www.palisade.com . I would like to thank Bloomberg Financial data and analysis. Their website is http://www.bloomberg.com

I would like to thank Matlab organization from providing free trial software in the past. I strongly recommend that you also subscribe to Matlab. Their website is http://www.mathworks.com.

Chapter 1

Definition and purpose of the hedge funds industry

9

Hedge funds are also known as alternative investments that are suited to institutional investors or wealthy investors with significant experience and knowledge in investment. They are used to hedge different types of risk by using derivatives products. Hedge fund managers use call and put options, commodity futures, forward contracts, index, currency and fixed income options and futures to hedge credit risk, market risk, country risk, sector risk, company risk, interest rate risk and currency risk. Thus, in addition to stocks and bonds they use their derivatives product to hedge or speculate according to the investment strategy, the market and political trend. Hedge funds are divided in several categories according to the investment strategy that is adopted by the fund manager. They use leverage through derivatives products, long and short position on securities, currencies, bonds and other investment products. They try to reduce risk, offset loses and positively increase the performance of the fund. They are not liquid as they use a lockup period for a certain period of time. They are used from wealthy investors that have a capital higher than 250,000 USD. In some cases the invested capital could be 1,000,000 USD or more than 10,000,000 USD.

The most interesting feature of hedge funds is the interrelation of their structure and their performance. As a result, the payroll structure which is based on three components namely performance fees, incentive fees and management fees are closely related to performance. Payroll structure is based on a minimum investment of $250.000, an annual fee of 1% - 2%, and an incentive fee of 5% to 25% of annual profits. This payroll structure usually includes another component known as high water mark that adds past performance to current ones. On the other hand, investors in hedge funds are often restricted with lockup periods which are the time period that initial investment cannot be redeemed from the fund. Limitations on cash withdrawals are a result of cash fluctuations and give fund managers more freedom in setting up long-term positions. This lockup period could have an adverse effect for active investors’.

Another factor that affects directly the performance of the fund is manager incentive fees which are related to the hurdle rate. The former are additional fees based on new profits from the funds according to the performance. The manager is rewarded only when the fund does well. The later is the return above which the manager begins to take incentive fees. For example, if the fund has a hurdle rate of 10% and the fund returns 25% for the year, the fund will take incentive fees on the 15% return above the hurdle rate. Thus, if the fund performance is below the high water mark limit, then the manager will be restricted to charge incentive fees which could lead to a consequent bad performance of the fund and finally liquidation of the fund. This incentive fee is generally subject to a high water mark provision. It is a benchmark used by funds to take fees only when profits are recorded from the positive performance of the fund. For example a $1 million investment is made in year 1 and the fund declines by 50%, leaving $500 thousand. In year 2, the fund returns 100% which equal to the initial investment. It will not take incentive fees on the return in year 2 as the initial investment was not increased. If the fund shows a negative performance, then the manager must cover the loss in the next year before the incentive fee becomes applicable. We relax the assumptions that if new investors have different high-water marks, then returns are not the same for all investors in the fund. Usually, databases report the returns for the initial or the average investor. Finally, management fees are taken by the manager on the entire asset level of the investment.

10

Hedge funds have been first created by Alfred Winslow Jones in (1949). It was a market neutral fund. Winslow strategy was to buy securities that were undervalued and to sell overvalued securities. The securities sold short provided a natural hedge against market risk and provided with positive return for his portfolio. As a matter of fact, there is no universally accepted definition of hedge funds. They are owned by private managers and wealthy individuals. Since the early 1990s, there has been a growing interest in the use of hedge funds. They are a growing business with more than $200 billion. The Assets under management in the hedge fund industry have grown from $25 billion in 1990 to more than $20 trillion in 2016. This growth has been due to new financial products as well as changes in technology that permit sophisticated investment strategies to be designed, implemented and offered to investors. Hedge funds offer a lot of advantages such as reduction of stock and bond portfolio volatility risk. They enhance portfolio returns in economic environments in which traditional stock and bond investments offer limited opportunities. They use a variety of long, short, spread, straddle options and commodity futures. Hedge funds returns are driven by market factors such as changes in credit spreads for convertible and fixed income arbitrage or market volatility for long and short strategies. In addition, the hedge funds returns are driven by the manager’s alpha. Therefore, manager’s skill is combined with the investment strategy to produce superior returns for the funds. Track record of investment experience and asset under management, AUM, are very important factors for the fund to be included in the relevant index.They are suitable for sophisticated investors as they offer greater flexibility in their asset allocation and have a relatively low covariance with other asset classes. The fact that they have low correlation in relation to traditional asset classes like equities and bonds makes them to offer a better diversification. Their structure in terms of fees is the most challenging issue among academics and practitioners as it affects performance return.

There has also been a lot of interest shown by both academics and practitioners in estimating the raw returns and risk-adjusted multi-factor performance of hedge funds and other investment vehicles (Fama and French (1993, 1996); Carhart (1997), Agarwal and Naik (2004); Capocci and Hubner (2004). Various studies have documented the comparison of hedge fund performance with that of S&P 500 used as a universe index.

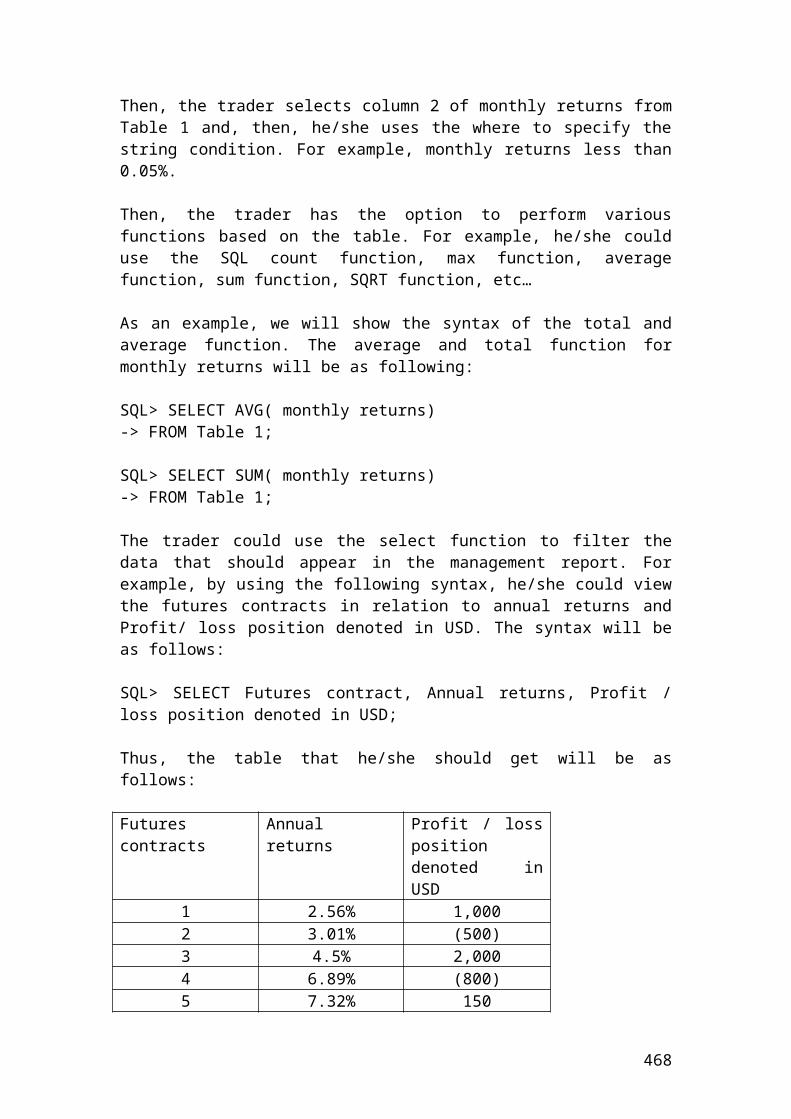

I have attached a table with a sample of hedge funds to show the structure and their performance.

Fund name Fund assets Trading strategy

Management fees

Incentive fees

Highwatermark

Hurdle rate

Lock-upperiod

Argos 10,159,607 Event- 1.75% 0.00% None

11

drivenThames River Sentinel Fund 240,000,000

Event

1.00% 10.00% Yes 5.00% QuarterlyThames River Warrior Fund 131,200,000

Event

1.25% 15.00% 6.00% 1 yearThemis MN Fund Ltd. 247,000,000

Event1.25% 15.00% 9.00% None

Titan Masters International Fund, Ltd. 113,096,000

Event

1.50% 15.00% 12.00% NoneABN AMRO multi-strategy fund (EUR) 274,200,000

Multi-strategy

1.25% 15.00% None None

ABN AMRO multi-strategy fund (USD) 310,600,000

Multi – strategy

1.25% 15.00% None None

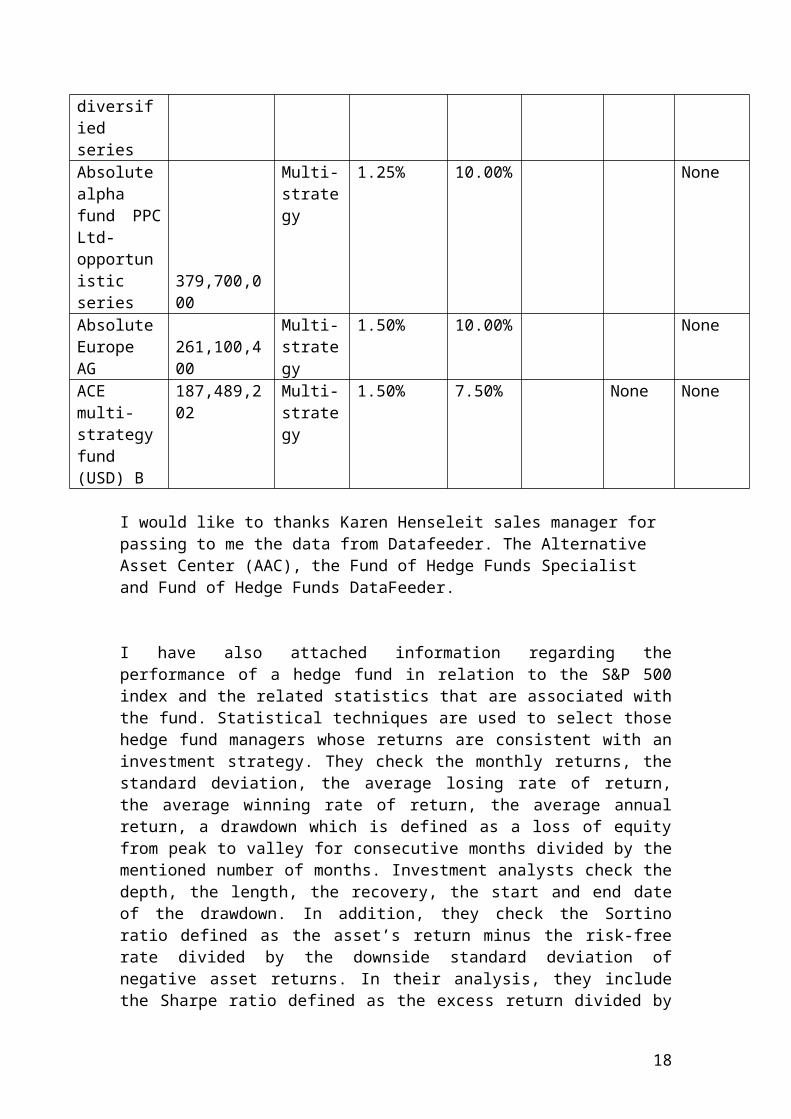

Abria diversified arbitrage trust 30,000,000

Multi- strategy

1.95% 10.00% Yes 3 month US Treasury bill

None

Absolute alpha fund PPC Ltd- diversified series 1,945,400,000

Multi- strategy

1.25% 10.00% None

Absolute alpha fund PPC Ltd- opportunistic series 379,700,000

Multi-strategy

1.25% 10.00% None

Absolute Europe AG 261,100,400

Multi-strategy

1.50% 10.00% None

ACE multi-strategy fund (USD) B

187,489,202 Multi-strategy

1.50% 7.50% None None

I would like to thanks Karen Henseleit sales manager for passing to me the data from Datafeeder. The Alternative Asset Center (AAC), the Fund of Hedge Funds Specialist and Fund of Hedge Funds DataFeeder.

12

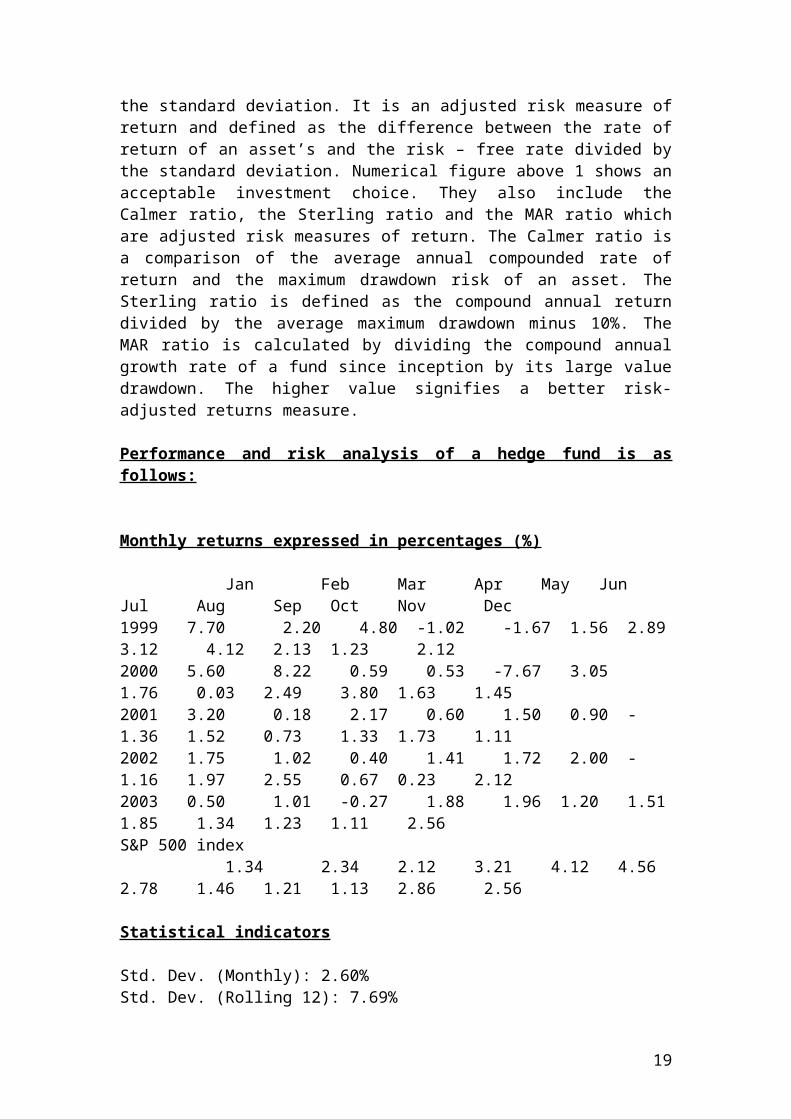

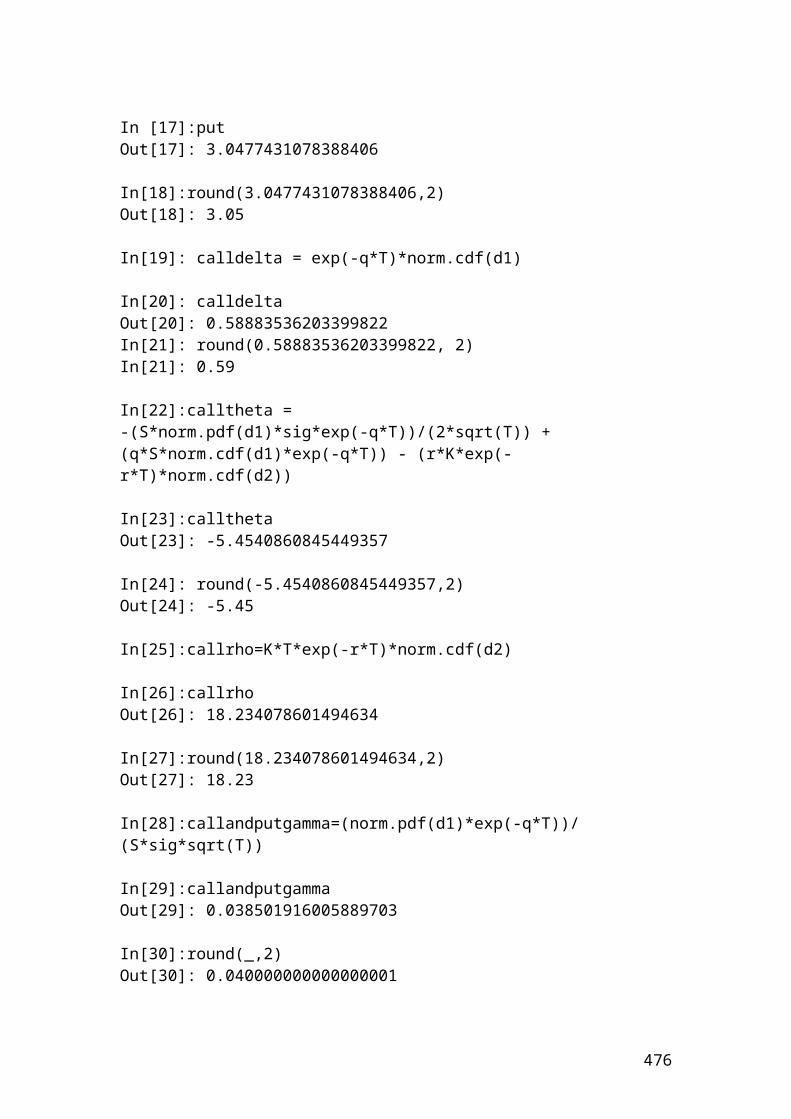

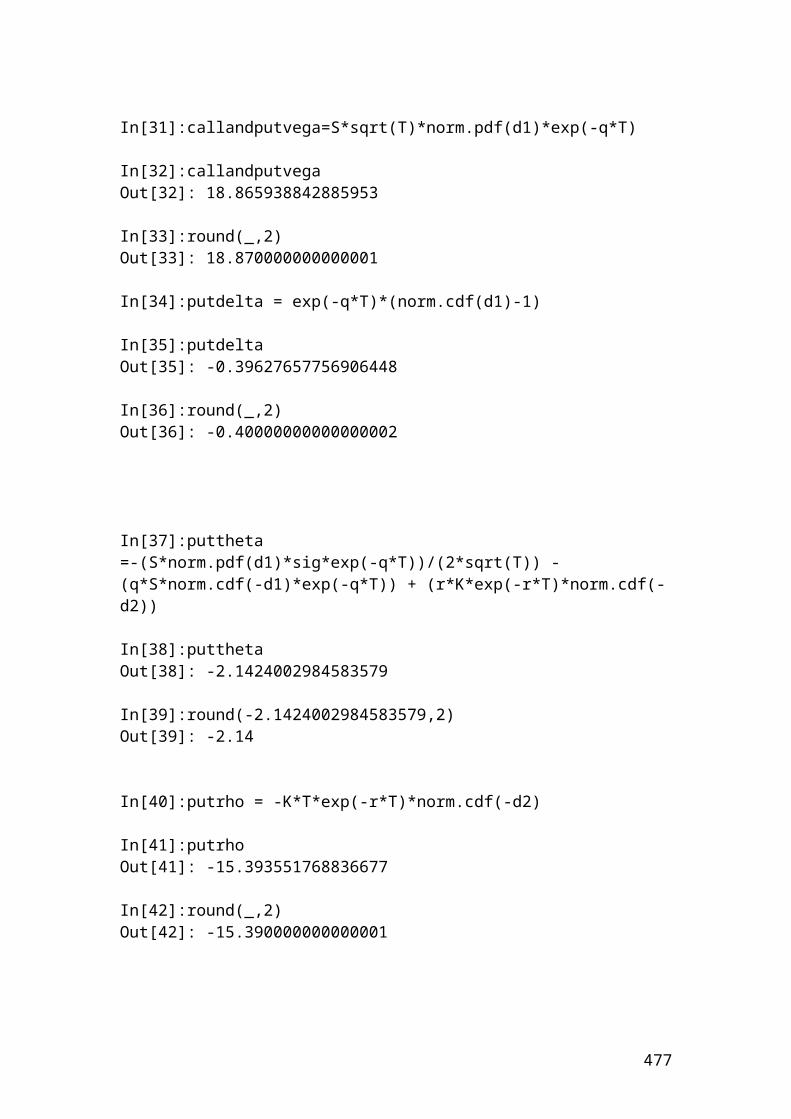

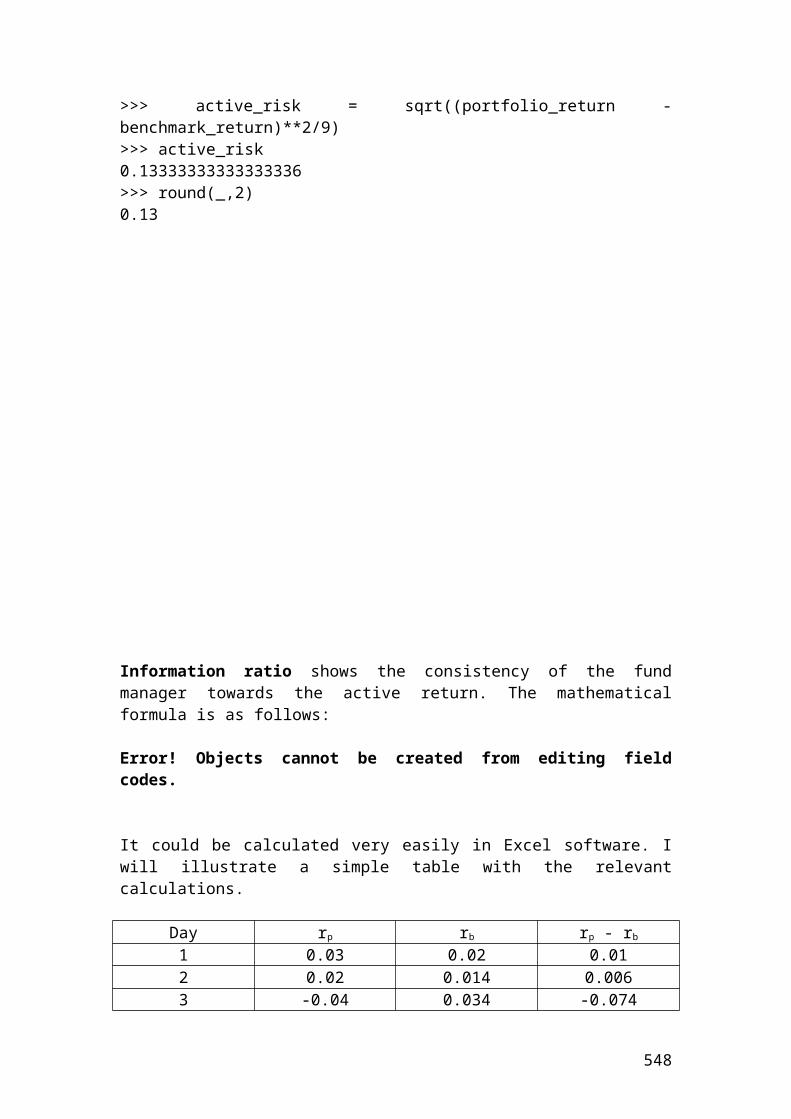

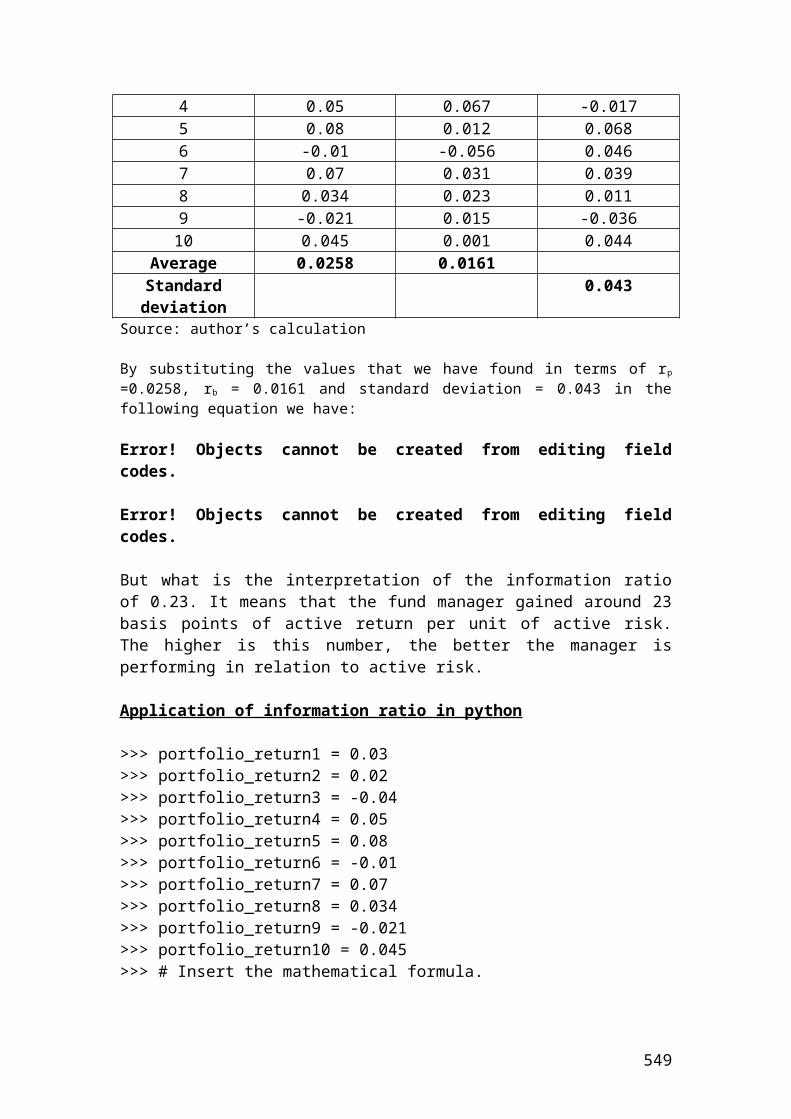

I have also attached information regarding the performance of a hedge fund in relation to the S&P 500 index and the related statistics that are associated with the fund. Statistical techniques are used to select those hedge fund managers whose returns are consistent with an investment strategy. They check the monthly returns, the standard deviation, the average losing rate of return, the average winning rate of return, the average annual return, a drawdown which is defined as a loss of equity from peak to valley for consecutive months divided by the mentioned number of months. Investment analysts check the depth, the length, the recovery, the start and end date of the drawdown. In addition, they check the Sortino ratio defined as the asset’s return minus the risk-free rate divided by the downside standard deviation of negative asset returns. In their analysis, they include the Sharpe ratio defined as the excess return divided by the standard deviation. It is an adjusted risk measure of return and defined as the difference between the rate of return of an asset’s and the risk – free rate divided by the standard deviation. Numerical figure above 1 shows an acceptable investment choice. They also include the Calmer ratio, the Sterling ratio and the MAR ratio which are adjusted risk measures of return. The Calmer ratio is a comparison of the average annual compounded rate of return and the maximum drawdown risk of an asset. The Sterling ratio is defined as the compound annual return divided by the average maximum drawdown minus 10%. The MAR ratio is calculated by dividing the compound annual growth rate of a fund since inception by its large value drawdown. The higher value signifies a better risk-adjusted returns measure.

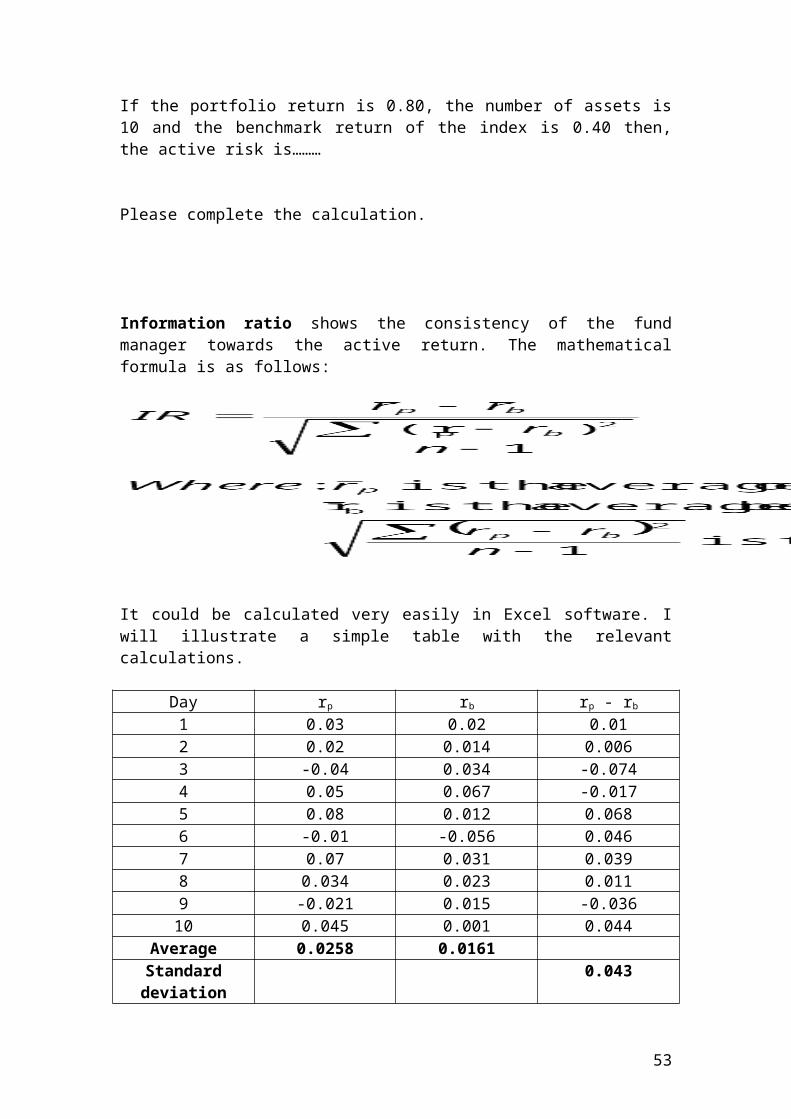

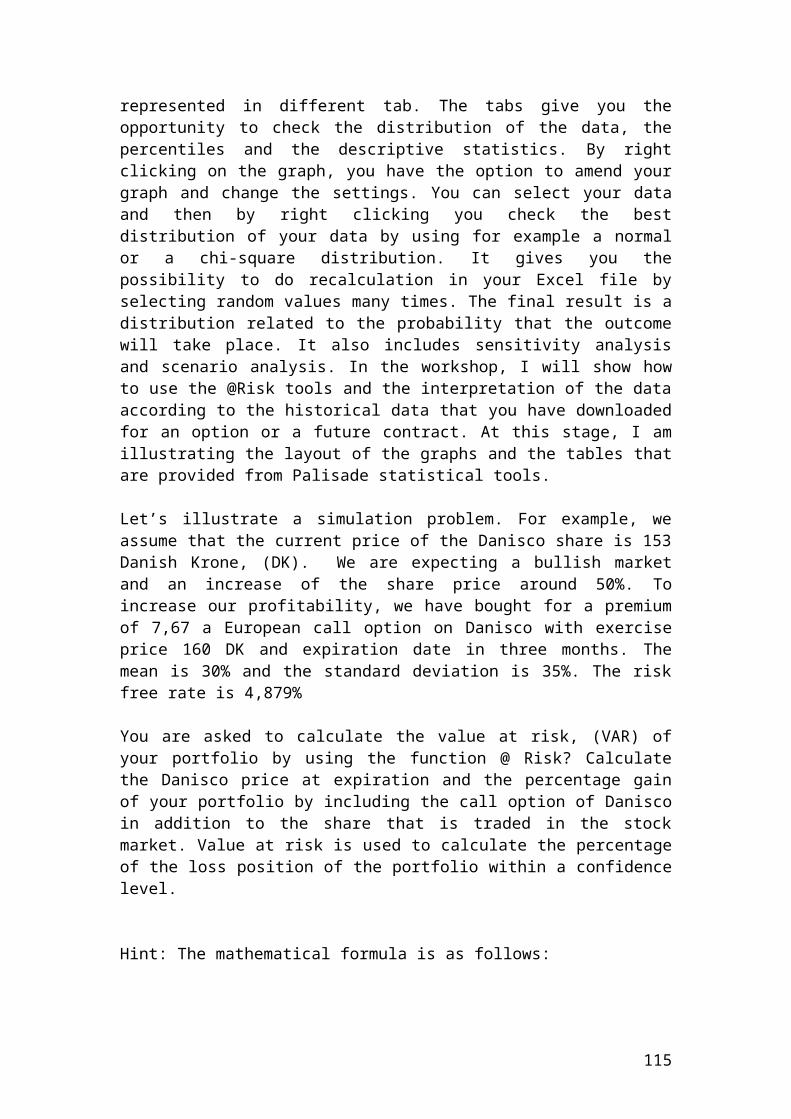

Performance and risk analysis of a hedge fund is as follows:

Monthly returns expressed in percentages (%)

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec1999 7.70 2.20 4.80 -1.02 -1.67 1.56 2.89 3.12 4.12 2.13 1.23 2.12 2000 5.60 8.22 0.59 0.53 -7.67 3.05 1.76 0.03 2.49 3.80 1.63 1.452001 3.20 0.18 2.17 0.60 1.50 0.90 -1.36 1.52 0.73 1.33 1.73 1.11 2002 1.75 1.02 0.40 1.41 1.72 2.00 -1.16 1.97 2.55 0.67 0.23 2.122003 0.50 1.01 -0.27 1.88 1.96 1.20 1.51 1.85 1.34 1.23 1.11 2.56S&P 500 index 1.34 2.34 2.12 3.21 4.12 4.56 2.78 1.46 1.21 1.13 2.86 2.56

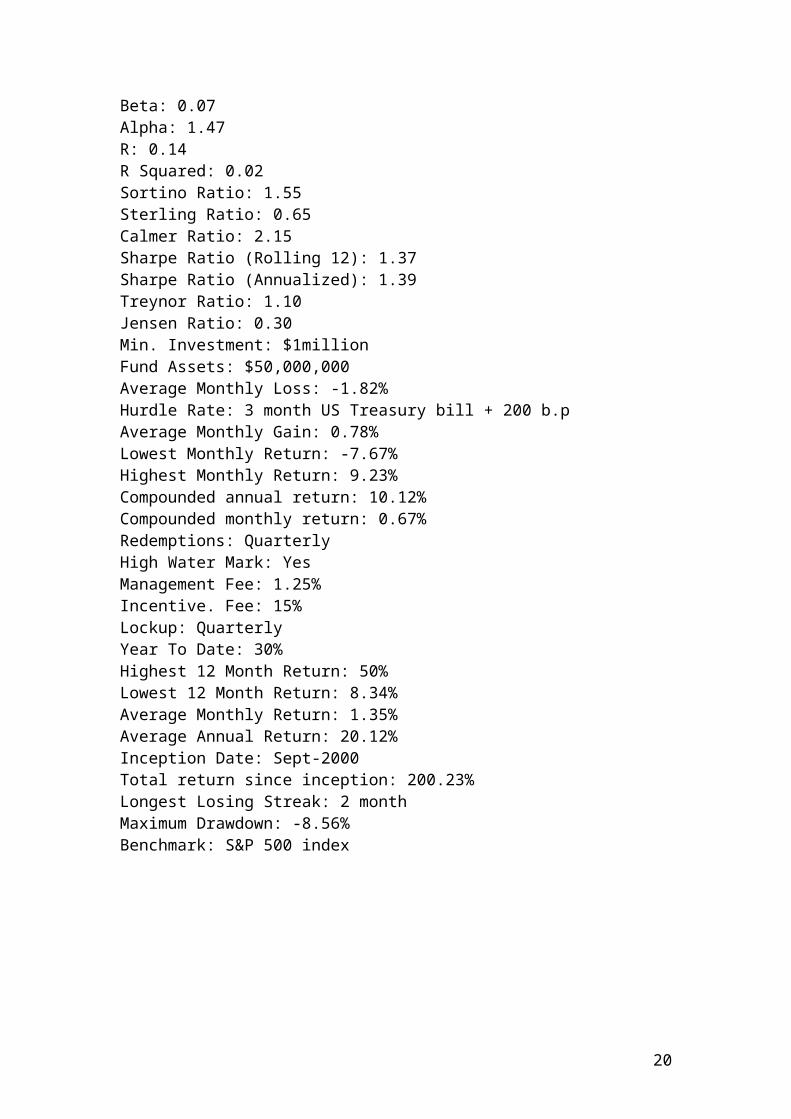

Statistical indicators

Std. Dev. (Monthly): 2.60%Std. Dev. (Rolling 12): 7.69%Beta: 0.07Alpha: 1.47R: 0.14R Squared: 0.02Sortino Ratio: 1.55Sterling Ratio: 0.65Calmer Ratio: 2.15Sharpe Ratio (Rolling 12): 1.37Sharpe Ratio (Annualized): 1.39Treynor Ratio: 1.10

13

Jensen Ratio: 0.30Min. Investment: $1millionFund Assets: $50,000,000 Average Monthly Loss: -1.82%Hurdle Rate: 3 month US Treasury bill + 200 b.pAverage Monthly Gain: 0.78%Lowest Monthly Return: -7.67%Highest Monthly Return: 9.23%Compounded annual return: 10.12%Compounded monthly return: 0.67%Redemptions: QuarterlyHigh Water Mark: YesManagement Fee: 1.25%Incentive. Fee: 15%Lockup: QuarterlyYear To Date: 30%Highest 12 Month Return: 50%Lowest 12 Month Return: 8.34%Average Monthly Return: 1.35%Average Annual Return: 20.12%Inception Date: Sept-2000Total return since inception: 200.23%Longest Losing Streak: 2 monthMaximum Drawdown: -8.56%Benchmark: S&P 500 index

14

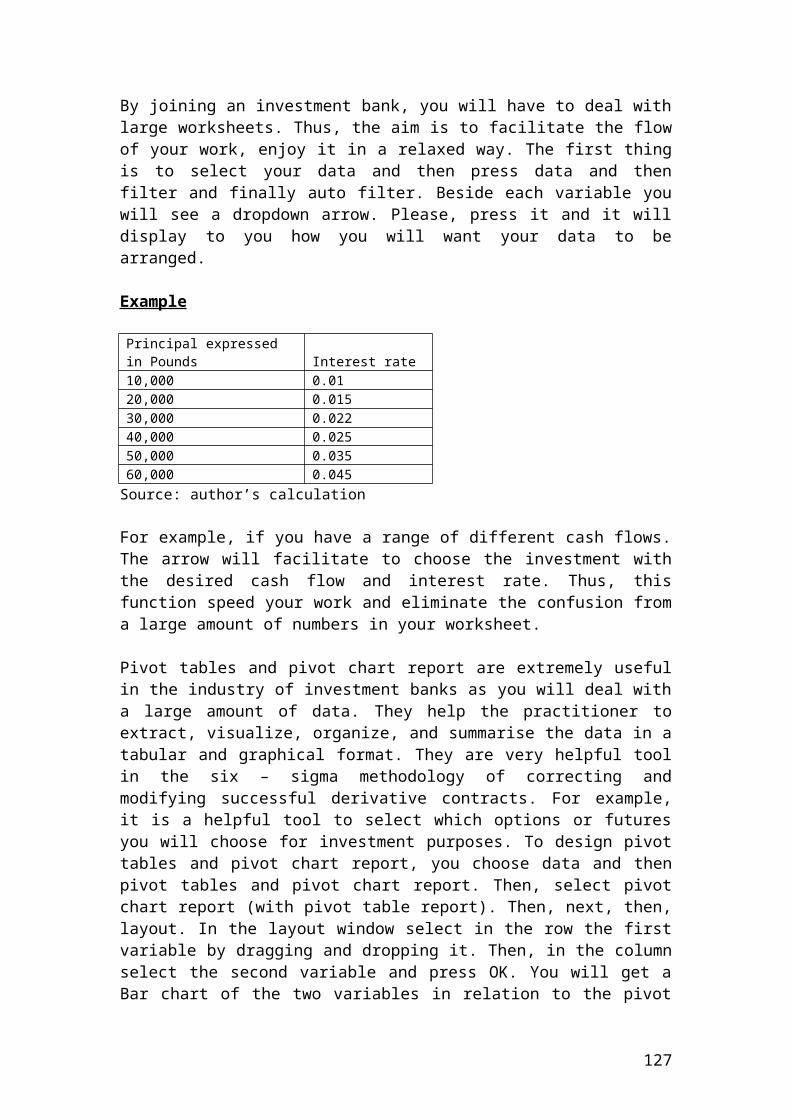

Hedge funds categories and trading strategies

1. Convertible Arbitrage

The overall objective and aim of this category is the use of convertible securities. It is expected that the performance of the fund will be greater than the benchmark by using a long /short position than a traditional long only position. The hedge fund manager invests in convertible bonds, warrants and convertible preferred stock that could be exchanged by buying a stock. It is converted in a particular amount of shares to take advantage about stock price rises.

Usually, we purchase the bond and we sell the stock to anticipate market movements in terms of increase of the bond price or further decrease of the stock. The delta of a long position in the convertible security is typically hedged by selling the stock short. Ideally, the trader wants a delta neutral position. The risks that the trader tries to hedge are changes in the price of the stock, changes in expected volatility of the stock, and changes in the level of interest rates. The basic idea is to gain from pricing differences between the bond and the stock. This strategy is based on anticipating the changes of short – term interest rates. The trader will achieve positive returns if expected volatility rises, if stock prices increases and if the credit issuer rating is improved.Thus, when interest rates rise, the bond prices will fall and the stock prices increase. Specifically, the fund manager takes a long position in the stock that is expected to rise and a short position in the stock or option that is going to decrease in value by shortens his position in the bond. The fund targets overvalued or undervalued securities. In other words, he/she buys and sells securities according to their CAPM security market line. He/she could also use a strategy of buying and selling shares of companies in different markets that are going to acquire each other. The purpose of arbitrage is to profit from price discrepancy in two different markets.

2. Emerging markets

Emerging markets hedge funds invests primarily in countries that have a closed market economy and are in the process of developing and expanding its infrastructure such as Brazil, India, Latin America, Africa, Eastern Europe, Korea and China. Hedge funds use in addition to stocks and bond a mixture of derivatives products such as commodity futures, forward contracts, fixed-income instruments, currency and index options to take advantage from the leverage effect due to substantial increase or decrease of prices. Therefore, the risk in emerging economies is higher for potential losses and gains. Another difficulty that hedge funds face in emerging economies is transparency and lack of liquidity which increase the volatility of the prices. Therefore, the risk and return are significant high and requires significant capital and investment knowledge to trade in such markets.

3. Equity market neutral

A market neutral strategy combines both long and short positions. The net exposure is equal to zero. The purpose of using such strategy is to eliminate the market risk. The

15

hedge fund manager is trying to increase the positive return by opening a long position in a bull market and short positions in a bear market. The purpose is to hedge and decrease market volatility. The hedge fund manager is checking the correlation structure of different segment or industries and accordingly aligns his/her investment strategy to buy or sell the different shares according to the sector, industry and market capitalization. It aims to provide a stable and consistent return profile that has no correlation to either equity or bond market movements, and to produce a consistent return. The fund manager has equally the same long and short positions, so the net exposure is zero.

4. Event Driven

The fund manager primarily is targeting financial, micro and macro economic or political events that will affect positively the net asset value, NAV, performance of the fund. The portfolio is exposed in long and short positions in bonds and shares according to business events, merger, acquisition, restructuring, legislative changes, and political turmoil. He /she is trying to increase the value of the portfolio by taking into consideration event driven scenario. This strategy is based in public information of forthcoming events that will affect positively or negatively the performance of the hedge fund. The fund manager seeks to take advantage of the price spread between current market prices of corporate securities and their value when the takeover is completed. Merger arbitrage involves buying the stock of the target companies after a merger announcement and shorting the acquiring company’s stock. Hedge funds hedge this risk by holding a large portfolio of different probabilistic scenarios of merger prices to eliminate the discrepancy between the present value of the merger offer and the current stock price. The present value valuation model takes into consideration the possibility that the merger will fail. Hedge funds perform better when the economy is booming and there are positive news regarding the corporate business plan of the different companies. They could also take advantage of the political turmoil and instability and sell stocks or bonds by opening short positions. The investment vehicles that they use are equities, debt securities, options, futures and convertible bonds.

5. Distressed securities

Distressed securities are related to the corporate bonds of bankrupted companies that start to get out from the crisis and are trying to reduce their loan exposures in the market. It could be also trading in distressed companies that are going to bankrupt and their debt value are reduced. The corporate bonds and shares are traded in discounted values. Their price is low and the investors’ anticipate a change in the management in terms of paying the debtors obligations. The risk that the hedge manager is exposed is that the company could increase its liabilities instead its assets and finally bankrupt. The stocks and bonds have no monetary value and the fund will display a negative NAV return. Therefore, the investors will face losses. Hedge funds or institutional investors buy distressed securities to better access the liquidity and the effort of the companies trying to get out from bankruptcy. Hedge funds perform better when the economy is in recession and the companies are distressed. They examine the equity to debt ratio and accordingly they decide whether it is favourable to buy them at a discounted debt value and sell them at a higher price.

16

6. Multi-strategy

The objective of the multi-strategy fund is to achieve positive NAV return by investing in diversified and professionally managed investment funds of equities and bonds. He/she is trying to monitor and hedge market and credit risk. The hedge funds invests in alternative investment strategies such as merger arbitrage, equity short bias, mortgage arbitrage, statistical arbitrage, structural arbitrage, market neutral strategies, convertible arbitrage, global macro, and CTA Managers.

7. Fixed income arbitrage

These funds engage principally in arbitrage strategies in the global corporate debt securities markets taking advantage of mispricings. Fixed income arbitrage funds take advantage of mispricing between fixed – income securities. Hedge fund managers open two positions at the same time to eliminate losses. A short and a long position aim to take advantage for price differences in the traded fixed – income securities. Government or municipal, corporate bonds and credit default swap are used to leverage the fund’s return. They use derivatives product to hedge against credit risk. Another strategy is yield curve arbitrage and credit yield curve. The profit or loss is resulted from studying the difference between a short 3 month US bond and long term 10 year US bond yield curve. Sometimes, they use mortgage backed securities arbitrage.

8. Global m acro

Investment risks are spread over different asset classes and investment strategies. Global macro hedge fund managers’ focus to generate positive returns based on currency futures and options, fixed – income securities derivatives products or stock indices futures and options. They are trying to eliminate the market risk by examining carefully the macroeconomic indicators and the political trends. They are checking the appreciation or depreciation of currencies by using options and futures. They use spot and forward rates futures and options by checking the interest rates. They check the monetary policy of each country in relation to the macroeconomic indicators, related to employment, gross domestic product, inflation and production. In addition, they check changes in interest rates resulted from short and long – term US treasury fixed income products. Please check the document financial derivatives for more information related to currency and Eurodollar futures. Another strategy is to use index option and futures or commodity futures such as gold, silver, sugar, cocoa, oil to take advantage of inflation or deflation. For example, in an inflationary environment, commodity prices will rise and a long strategy will be profitable. In contrast, in a deflationary environment commodity prices will fall and therefore a short strategy will be profitable. The hedge fund portfolio is leveraged and the degree of risk is very high.

17

9. Long/Short Equity

The hedge fund primarily goal is to invest in long and short position of the security to take advantage from increase or decrease of the prices. Thus, he/she buys a security that is expected to rise and sell a security that is expected to fall. In other words, the hedge fund manager buys an undervalued share and sells an overvalued share. The main purpose is to minimize the market exposure and profit from the spread of a long/ short strategy between the shares. The net exposure should outweigh the long versus the short position or vice versa. The risk is still high because the market could move sharply in one direction and affect negatively the investment in the opposite direction. For example, if you invest 250,000 USD in a long position and 500,000 USD in a short position, the difference due to beta of the market direction could affect positively or negatively the entire investment. The fund manager could also use equity futures and options for small and large capitalization companies or blue chips companies.

10.Option strategies

Hedge funds are using different option strategies to hedge their portfolio from market risk. Options are a special type of financial asset that gives the holder the right but not the obligation to buy or sell an underlying security at a predetermined price. Options are of two types: put options and call options. A call option gives the right but not the obligation to buy, and a put option the right to sell at a specific price within a certain time period. American options give the right to the investors to exercise it before as well as on the expiry date. In contrast, European options give the right to exercise it only on the expiry date. The advantage of buying an option is that the initial outlay is smaller in comparison with buying a large number of shares. Furthermore, the downside risk is limited to a certain amount. In contrast, if the share price falls by a significant amount, then the investor’s could loose a large amount of his/her capital. Finally, the percentage positive return is greater due to the leverage effect. The investor can also take the position to as referred long or short straddle. Let’s take as an example the first case of buying a straddle. It involves taking a long position in a call and a long position in a put with the same strike, share price and expiration date. This strategy is appropriate when an investor is expecting a large move in a price on an underlying share, but does not know in which direction the move will be in the index (Traded options, investor chronicle, 1997, p.38). Selling straddle or taking a short position involves more risk for limited reward. To reduce the risk of large losses, a straddle seller may buy a put with a lower strike and a call with a higher strike. The resulting position looks similar to a butterfly spread (Ritchken, 1987,p.54)It involves taking a short position in a call and a short position in a put with the same strike price, share price and expiration or maturity date. This strategy is appropriate when an investor is expecting a minor move in a price on an underlying share, but does not know in which direction the move will be in the index. Another type of strategy which involves a combination in both call and puts is referred to as a strangle. There are two strategies which are buying and selling a strangle. The first strategy consists of a long position in a call and a put with different strike prices, the same maturity or expiration date and the same underlying share. The second strategy consists of a short position in a call and a put with different strike prices the same

18

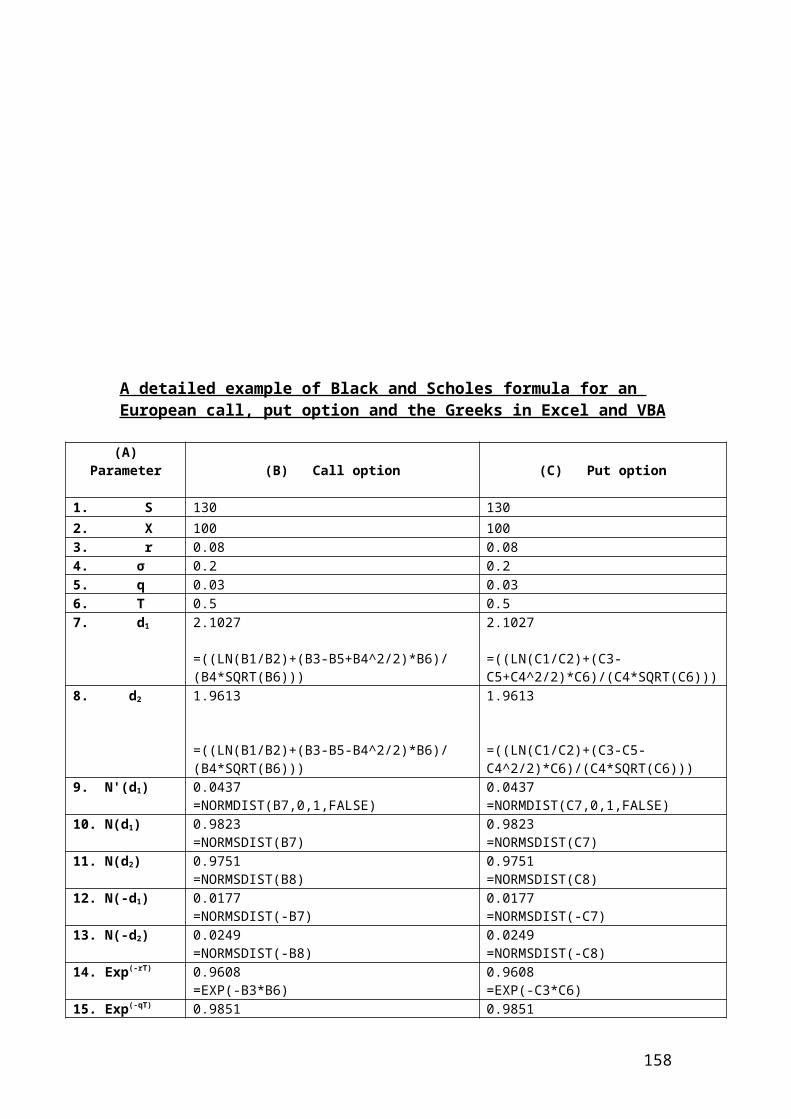

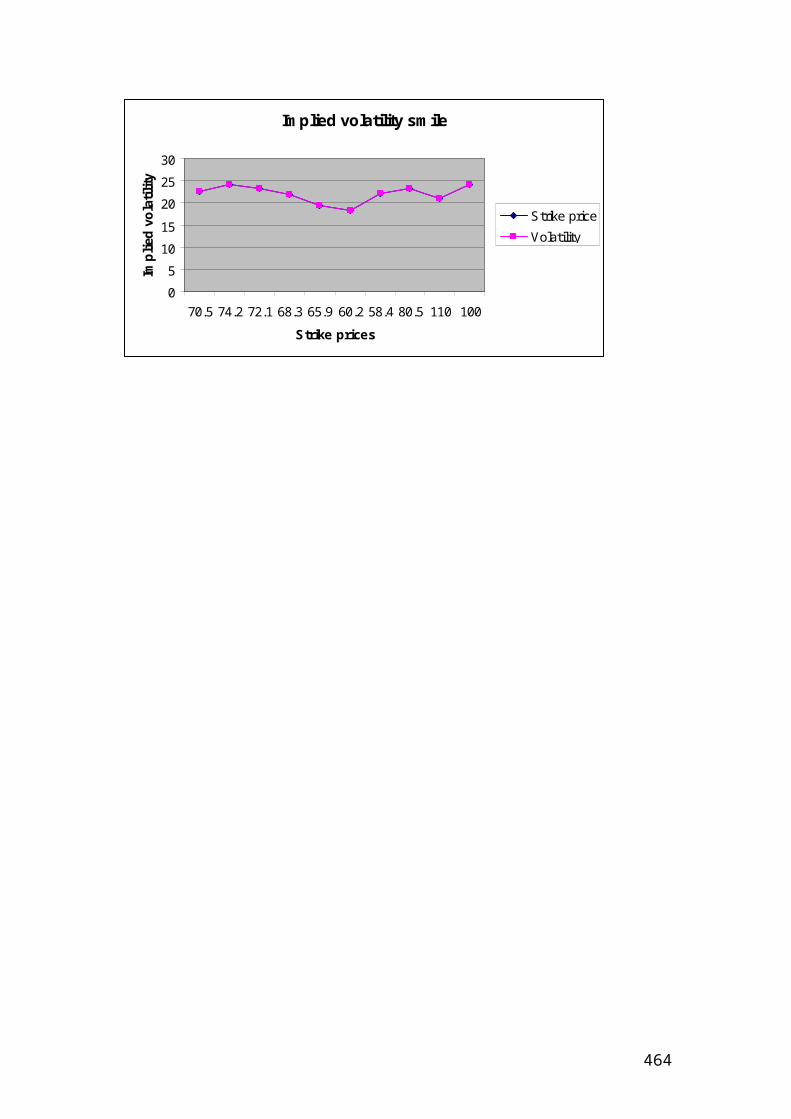

maturity or expiration date and the same underlying share. Implied volatility is estimated when the current market price of the option is different from the theoretical pricing price that is calculated from the Black - Scholes formula. The deviation or difference in price is related to the volatility that is incorporated in the option pricing formula. The implied volatility is calculated in Excel by using the functions of Goal Seek. It applies trial and error test to find the accurate value of the volatility implied.

Check the implied volatility of the S&P 500 index which shows the estimated future movement of an asset. Therefore, high implied volatility signifies to sell the option of the specific share. Low implied volatility signifies to buy the option of the specific share. Check the Bollinger bands with a 2 standard deviations and a 30 day moving average.

11. Funds of funds

Funds of hedge funds invest solely in other hedge funds. The hedge fund manager selects funds based on a specific investment strategy or a combination of different investment strategies to achieve a better return. The benefit of combining different investment strategies is to achieve diversification and skilful management to reduce market risk. The disadvantages are the fees of asset management and the incentive fees that are charged to manage these funds. They charge a 2% fee and an incentive fee of 15% to 25 % from the profit that is generated. The double fee structure is a disadvantage of investing in funds of funds. The risk is that you could loose from your initial capital due to low return and high transaction fees. Fund of funds cannot as easily be liquidated. They have a withdrawal period of either monthly or quarterly. As an example, we can mention large cap equity stocks that are traded in the S&P500 index in the USA and government bonds. The equity benchmark rate waseither the S&P 500 or MSCI World while the government bonds benchmark rate is the Citigroup world government bond index,WGBI. Different funds of funds have different objectives and as a result different level of volatilities. Therefore, a diversified portfolio with negative correlations between various investment products reduces the level of market - beta risk and manager risk. Beta and alpha measures are compared to show the skilful capability of the hedge fund manager. Funds with monthly returns of five years showed an annual standard deviation of volatility equal to 50% whereas the lowest rate was 15%.

12. Managed futures / CTAs

CTA, commodity trading advisers, or managed futures managers’ trade in the commodity market. The hedge funds invest in commodity futures, currencies, bonds and shares. The portfolio is leveraged and the risk is quite high. Forward and futures contracts have similarities in terms that they involve two parties to exchange a commodity, a currency or a bond at a specified price in the future. The costs of carry that characterize these contracts are insurance, storage and interest costs. A standardized future contract is traded based on a specified amount at a fixed future date and at a fixed price. In contrast, in the forward contract the two parties negotiate the amount that will be traded. Futures contracts are exchanged on a stock exchange.

19

Forward contracts are done between the parties and they are over - the -counter contracts. The fact that there is a clearing house that regulate the settlements through a margin call make the standardized futures contract more safe by eliminating the credit risk of default. In contrast, forward contracts, as they are over - the - counter are not regulated by a clearing house of the futures exchange and the parties could experience large losses. The only advantage of over-the- counter contracts are that the involved parties could negotiate the quantity, the price and the expiration date. The biggest problem is the risk of default, the lack of liquidity and buying or selling in the wrong price. Standardized futures contract provide liquidity to the parties involved, as they can be sold to another party at any time of the contract until maturity. In contrast, forward contracts could not be sold to a third party, which makes them to lack liquidity. To sum up, the standardized futures contract are regulated, offer high liquidity, correct pricing and low credit risk. The forward contracts offer less pricing transparency, low liquidity, higher credit risk and they are traded over- the- counter. The characteristic of a future contract is the underlying, the standardized unit multiplied by the index points, the initial margin, the settlement method, the minimum price move, the minimum tick value and the time period expressed in months. For example, if you buy the Financial Times, (FT), newspaper and check a future contract for the FTSE - 100 Index, you will see a standardized value of 25 Pounds multiplied by the index point. Other characteristics of the index future contract is the time period expressed in months, open interest, the closing price for each trading day, the high, the low, the previous value and the settlement price. Settlement price refers to the closing price of the contract. Open interest refers to the total number of contracts in terms of buying or selling positions. Hedge funds use managed futures in terms of indices, treasuries, fixed –income securities and commodities such as gold, silver, oil , corn, cocoa, sugar etc.

20

Chapter 2

Hedge funds indices

Credit Suisse convertible arbitrage index Dow Jones world emerging markets index Equity market neutral S&P 500 index Credit Suisse event driven index Suisse high yield II and credit index distressed securities Citigroup world government bond index,WGBI, for fixed income arbitrage Credit Suisse global macro index Credit Suisse long/short equity index S&P Goldman Sachs commodities index options Credit Suisse all hedge fund index fund of funds Credit Suisse managed futures/CTAs index Dow Jones world index multi - strategy

Due to confidentiality reasons, I will not be able to disclose information and data related to the performance of the indices that constitute the various trading strategies. For example, I cannot disclose from the credit Suisse site information related to the performance of the different indices. Please refer to the web site of credit Suisse, www.hedgeindex.com

You will also find Dow Jones indices and other information such as alternative beta indexes. After taking into consideration copyright agreement, you can e-mail them for a login account to download cumulative statistics, NAV prices in different currencies and for different indexes such as the credit Suisse broad hedge fund index, the credit Suisse all hedge index, and the credit Suisse blue chip hedge fund index. Finally, you will find information concerning the correlations matrix between an investment strategy and the relevant index, quarterly and monthly performance data. Check the correlation matrix as we did in the seminar group between individual investment strategies and the relevant hedge fund index. Good luck!

Fund managers who satisfy institutional criteria for number of years, track record, assets under management, AUM, of 50 million USD and an audited financial statement are considered for inclusion in the hedge fund indices. Additional checks are made to ensure that performance is consistent with the manager’s investment style. An index committee is comprised from investment analysts who are responsible to review the methodology of index creation. This committee may propose additional criteria to or eliminate hedge fund managers to join the index. Statistical techniques are used to select those hedge fund managers whose returns are consistent with an investment strategy. They check the monthly returns, the standard deviation, the average losing rate of return, the average winning rate of return, the average annual return, a drawdown which is defined as a loss of equity from peak to valley for consecutive months divided by the mentioned number of months. Investment analysts check the depth, the length, the recovery, the start and end date of the drawdown. In addition, they check the Sortino ratio defined as the asset’s return minus the risk-free rate divided by the downside standard deviation of negative asset returns. In their

21

analysis, they include the Sharpe ratio defined as the excess return divided by the standard deviation. It is an adjusted risk measure of return and defined as the difference between the rate of return of an asset’s and the risk – free rate divided by the standard deviation. Numerical figure above 1 shows an acceptable investment choice. They also include the Calmer ratio, the Sterling ratio and the MAR ratio which are adjusted risk measures of return. The Calmer ratio is a comparison of the average annual compounded rate of return and the maximum drawdown risk of an asset. The Sterling ratio is defined as the compound annual return divided by the average maximum drawdown minus 10%. The MAR ratio is calculated by dividing the compound annual growth rate of a fund since inception by its large value drawdown. The higher value signifies a better risk-adjusted returns measure.They also check the correlation matrix of the investment strategy, for example, event driven funds and compare them with a Credit Suisse event driven index. Therefore, the indices methodology begins by identifying a set of candidate hedge fund managers who are selected by the index committee.

The returns for each style funds are entered into a database and each fund is then controlled by a number of screens in order to identify a subset of funds that satisfies the investment criteria’s. For example, the first criterion for inclusion in the hedge fund index is a two year performance track record. It is difficult to use statistically based style analysis with relatively few monthly returns. The second criterion is assets under management. The committee requires minimum 50 million USD as assets under management. The purpose of the minimum asset requirement is to ensure that hedge fund managers have a demonstrated organizational and managerial infrastructure and have a demonstrated ability to raise funds from wealthy investors.

The index methodology that is used is cluster analysis. The indices initially use a measure of correlation of the fund returns versus a benchmark. The first component that is checked is correlation matrix of returns by using Pearson correlation measure. The purpose is to check and compare the volatility of those returns versus a benchmark or an index. This technique shows also the degree of leverage of the portfolio. Low correlation levels monthly returns were determined to hedge against market risk and ensure high degree of diversification. Managers who did not satisfy the minimum correlation criteria were eliminated. For funds that do not meet these criteria, fund managers use non-parametric measures of correlation, such as Spearman rank correlation to check the ranking of each fund. Cluster-based classification is a statistical technique for choosing and collecting data into sets of similar members. Collection may be done either hierarchically or non-hierarchically, where each element is associated with a set, where the sets do not overlap. Clustering techniques were used to group managers and to check for consistency of returns and risk levels. Investment analysts use also x –y scatter plot to find in which quadrant the hedge funds returns show similarity or dissimilarity. Cluster analysis aims to minimize intra – group data variation. We group funds with the same investment strategy and level of leverage. Volatility is measured by the standard deviation or the mean absolute deviation in some cases and simulation and bootstrapping methods are employed. Variation in index returns can be explained by debt and swap spreads, bonds and equity volatility or implied volatility. For example, market neutral strategy groups funds with the same objectives. As an example, we can mention the Amazon market

22

neutral fund. Fund managers who satisfy the criteria were contacted and asked to provide historical monthly returns data

Each manager in the index is given equal weight. Indices are checked every three months with a 1-month lag. Inclusions or exclusions from an index will be determined by the index committee and are incorporated into the index at the start of each quarter.Hedge fund managers who have stopped trading are removed from the index after audited results. This helps us to eliminate survivor bias in the index or reporting dead fund performance that does not exist.

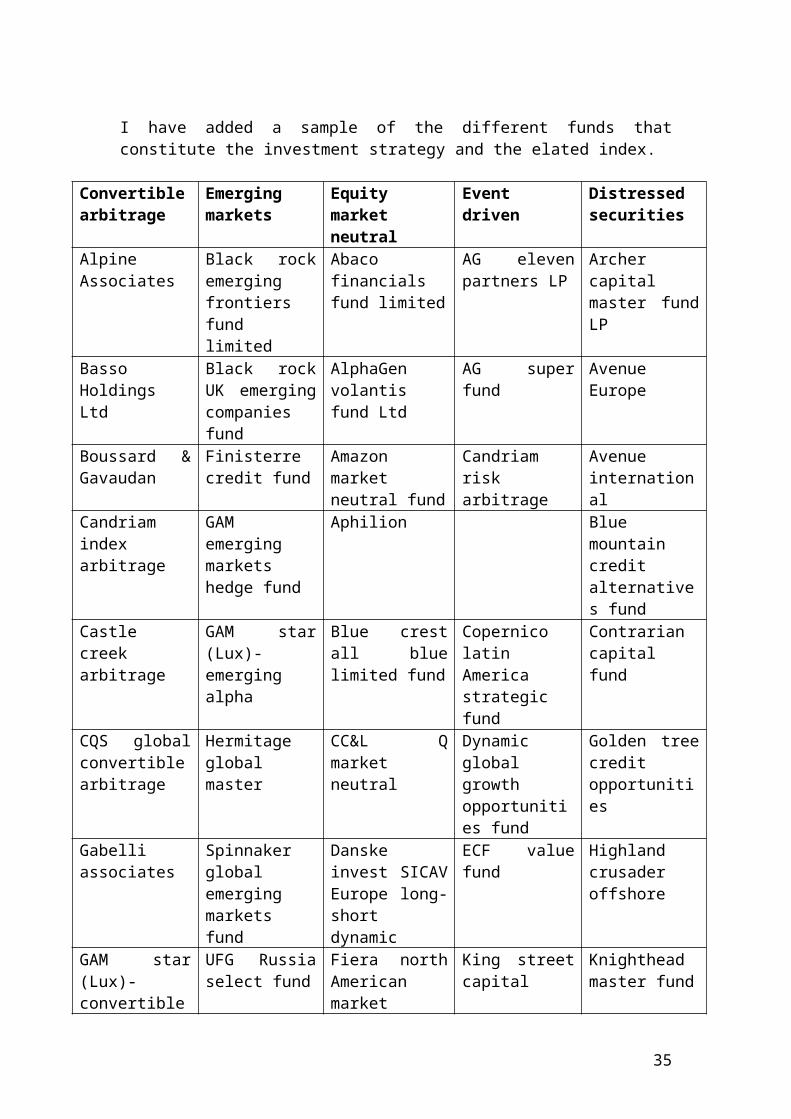

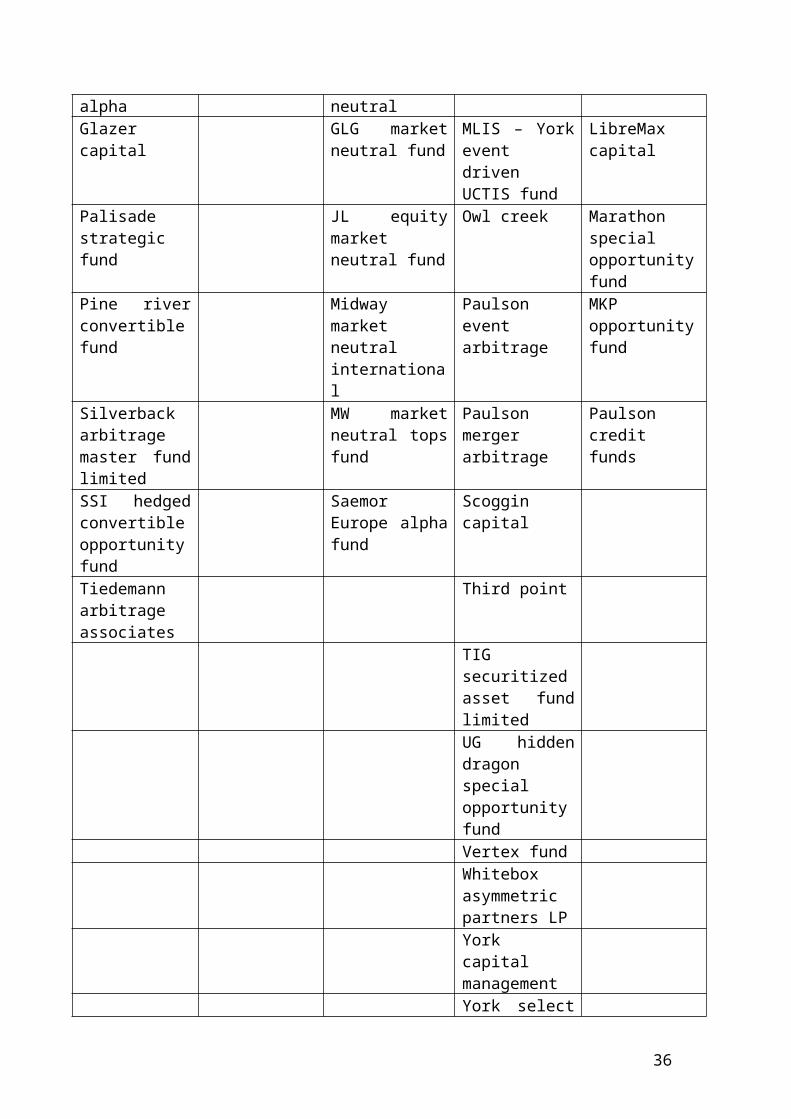

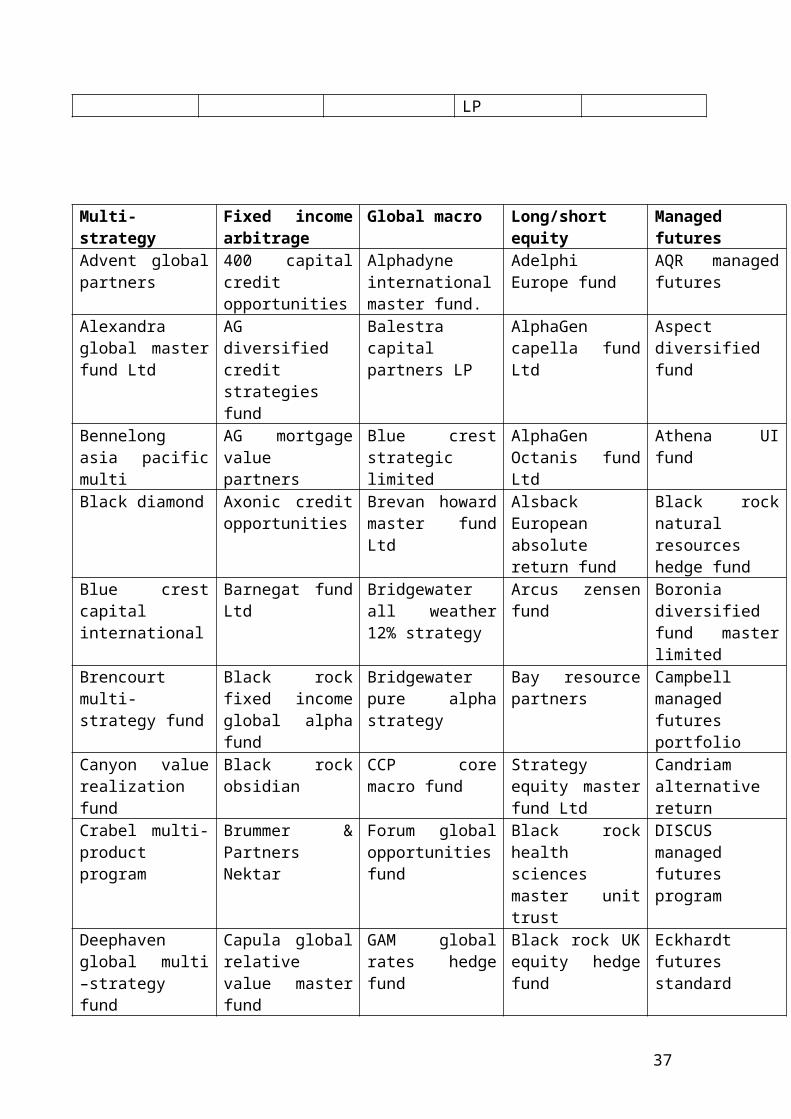

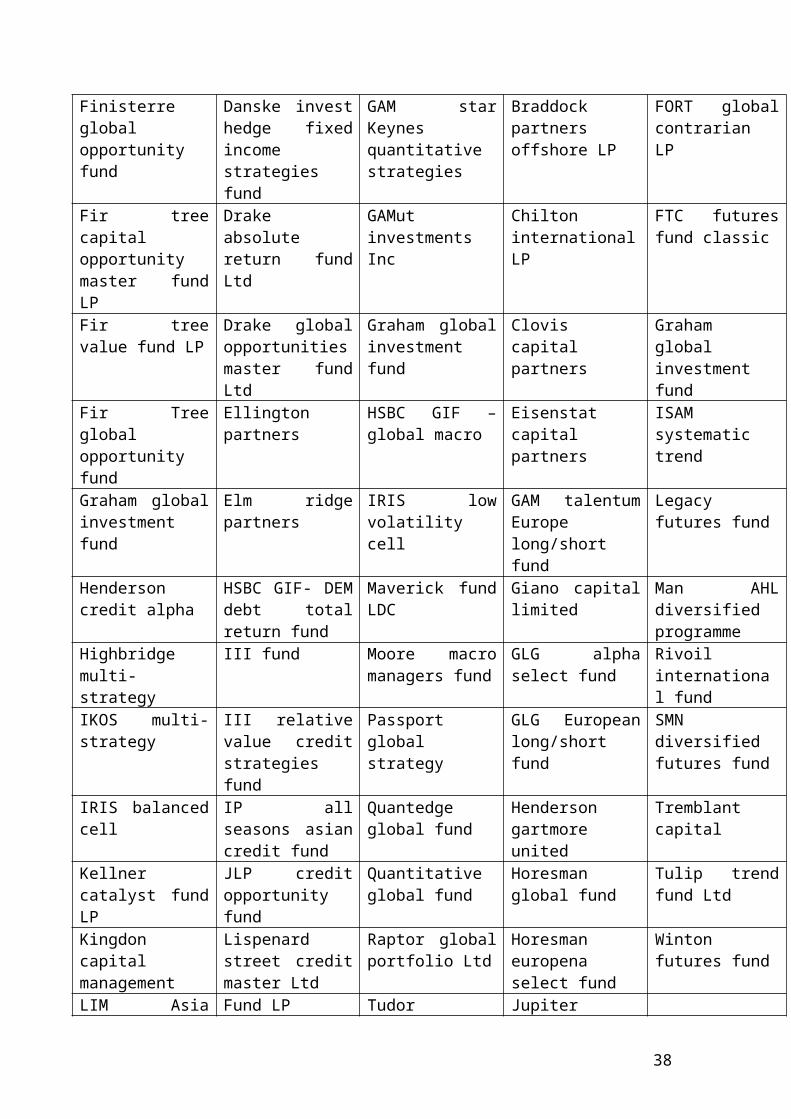

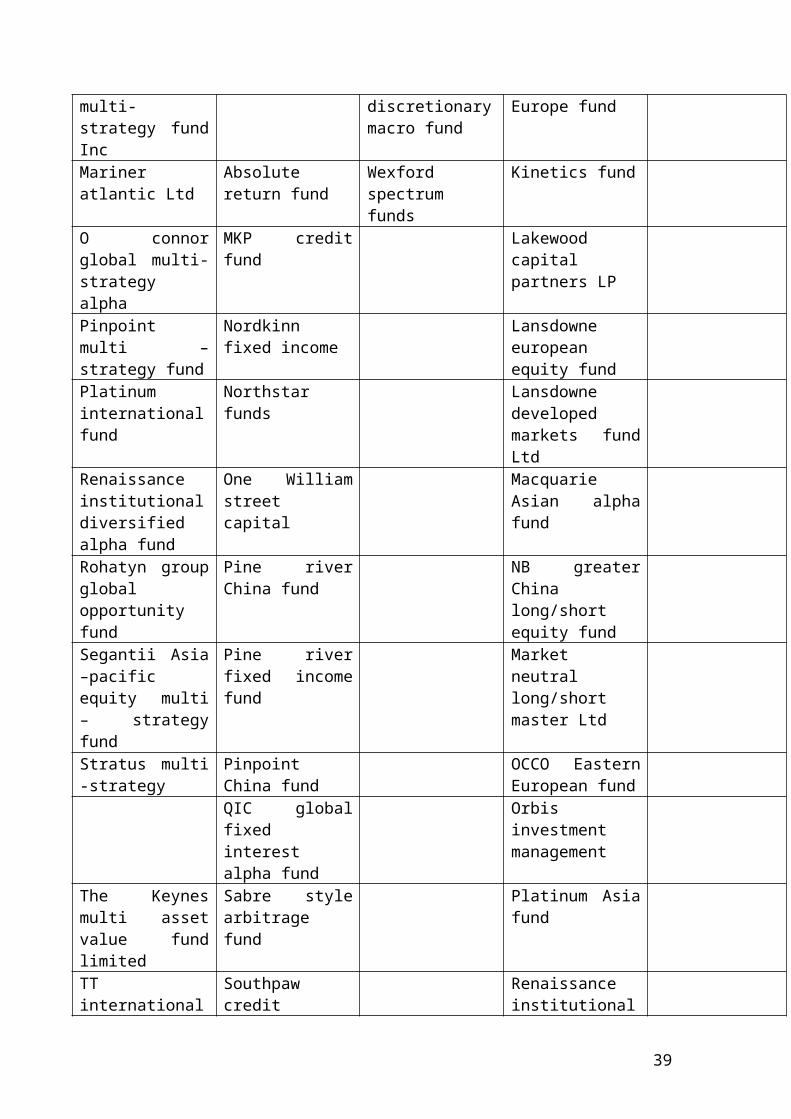

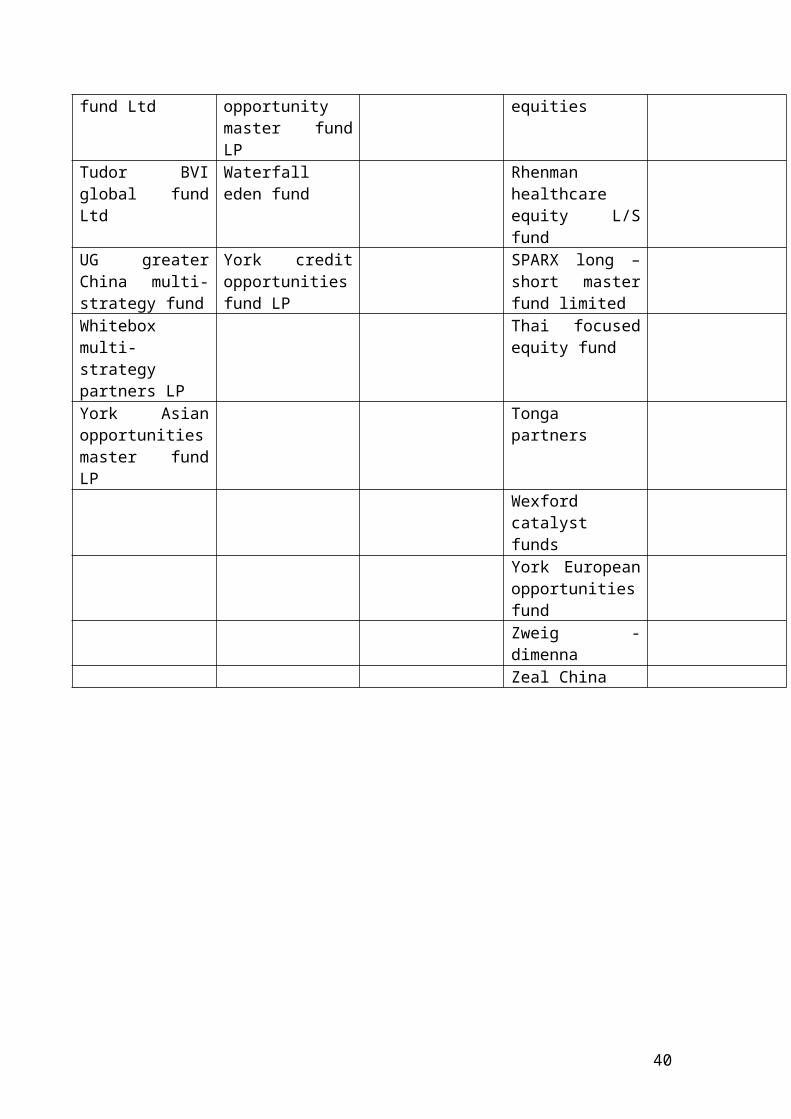

I have added a sample of the different funds that constitute the investment strategy and the elated index.

Convertible arbitrage

Emerging markets

Equity market neutral

Event driven Distressed securities

Alpine Associates

Black rock emerging frontiers fund limited

Abaco financials fund limited

AG eleven partners LP

Archer capital master fund LP

Basso Holdings Ltd

Black rock UK emerging companies fund

AlphaGen volantis fund Ltd

AG super fund Avenue Europe

Boussard & Gavaudan

Finisterre credit fund

Amazon market neutral fund

Candriam risk arbitrage

Avenue international

Candriam index arbitrage

GAM emerging markets hedge fund

Aphilion Blue mountain credit alternatives fund

Castle creek arbitrage

GAM star (Lux)- emerging alpha

Blue crest all blue limited fund

Copernico latin America strategic fund

Contrarian capital fund

CQS global convertible arbitrage

Hermitage global master

CC&L Q market neutral

Dynamic global growth opportunities fund

Golden tree credit opportunities

Gabelli associates

Spinnaker global emerging markets fund

Danske invest SICAV Europe long-short dynamic

ECF value fund Highland crusader offshore

GAM star (Lux)- convertible alpha

UFG Russia select fund

Fiera north American market neutral

King street capital

Knighthead master fund

Glazer capital GLG market neutral fund

MLIS – York event driven UCTIS fund

LibreMax capital

Palisade strategic fund

JL equity market neutral fund

Owl creek Marathon special opportunity fund

Pine river convertible fund

Midway market neutral international

Paulson event arbitrage

MKP opportunity fund

23

Silverback arbitrage master fund limited

MW market neutral tops fund

Paulson merger arbitrage

Paulson credit funds

SSI hedged convertible opportunity fund

Saemor Europe alpha fund

Scoggin capital

Tiedemann arbitrage associates

Third point

TIG securitized asset fund limitedUG hidden dragon special opportunity fundVertex fundWhitebox asymmetric partners LPYork capital managementYork select LP

Multi-strategy Fixed income arbitrage

Global macro Long/short equity Managed futures

Advent global partners

400 capital credit opportunities

Alphadyne international master fund.

Adelphi Europe fund

AQR managed futures

Alexandra global master fund Ltd

AG diversified credit strategies fund

Balestra capital partners LP

AlphaGen capella fund Ltd

Aspect diversified fund

Bennelong asia pacific multi

AG mortgage value partners

Blue crest strategic limited

AlphaGen Octanis fund Ltd

Athena UI fund

Black diamond Axonic credit opportunities

Brevan howard master fund Ltd

Alsback European absolute return fund

Black rock natural resources hedge fund

Blue crest capital international

Barnegat fund Ltd Bridgewater all weather 12% strategy

Arcus zensen fund Boronia diversified fund master limited

Brencourt multi-strategy fund

Black rock fixed income global alpha fund

Bridgewater pure alpha strategy

Bay resource partners

Campbell managed futures portfolio

Canyon value realization fund

Black rock obsidian CCP core macro fund

Strategy equity master fund Ltd

Candriam alternative return

Crabel multi-product program

Brummer & Partners Nektar

Forum global opportunities fund

Black rock health sciences master unit

DISCUS managed futures program

24

trustDeephaven global multi –strategy fund

Capula global relative value master fund

GAM global rates hedge fund

Black rock UK equity hedge fund

Eckhardt futures standard

Finisterre global opportunity fund

Danske invest hedge fixed income strategies fund

GAM star Keynes quantitative strategies

Braddock partners offshore LP

FORT global contrarian LP

Fir tree capital opportunity master fund LP

Drake absolute return fund Ltd

GAMut investments Inc

Chilton international LP

FTC futures fund classic

Fir tree value fund LP

Drake global opportunities master fund Ltd

Graham global investment fund

Clovis capital partners

Graham global investment fund

Fir Tree global opportunity fund

Ellington partners HSBC GIF – global macro

Eisenstat capital partners

ISAM systematic trend

Graham global investment fund

Elm ridge partners IRIS low volatility cell

GAM talentum Europe long/short fund

Legacy futures fund

Henderson credit alpha

HSBC GIF- DEM debt total return fund

Maverick fund LDC

Giano capital limited

Man AHL diversified programme

Highbridge multi-strategy

III fund Moore macro managers fund

GLG alpha select fund

Rivoil international fund

IKOS multi-strategy

III relative value credit strategies fund

Passport global strategy

GLG European long/short fund

SMN diversified futures fund

IRIS balanced cell IP all seasons asian credit fund

Quantedge global fund

Henderson gartmore united

Tremblant capital

Kellner catalyst fund LP

JLP credit opportunity fund

Quantitative global fund

Horesman global fund

Tulip trend fund Ltd

Kingdon capital management

Lispenard street credit master Ltd

Raptor global portfolio Ltd

Horesman europena select fund

Winton futures fund

LIM Asia multi-strategy fund Inc

Fund LP Tudor discretionary macro fund

Jupiter Europe fund

Mariner atlantic Ltd Absolute return fund

Wexford spectrum funds

Kinetics fund

O connor global multi-strategy alpha

MKP credit fund Lakewood capital partners LP

Pinpoint multi –strategy fund

Nordkinn fixed income

Lansdowne european equity fund

Platinum international fund

Northstar funds Lansdowne developed markets fund Ltd

Renaissance institutional diversified alpha fund

One William street capital

Macquarie Asian alpha fund

Rohatyn group Pine river China NB greater China

25

global opportunity fund

fund long/short equity fund

Segantii Asia –pacific equity multi – strategy fund

Pine river fixed income fund

Market neutral long/short master Ltd

Stratus multi -strategy

Pinpoint China fund OCCO Eastern European fund

QIC global fixed interest alpha fund

Orbis investment management

The Keynes multi asset value fund limited

Sabre style arbitrage fund

Platinum Asia fund

TT international fund Ltd

Southpaw credit opportunity master fund LP

Renaissance institutional equities

Tudor BVI global fund Ltd

Waterfall eden fund Rhenman healthcare equity L/S fund

UG greater China multi-strategy fund

York credit opportunities fund LP

SPARX long – short master fund limited

Whitebox multi-strategy partners LP

Thai focused equity fund

York Asian opportunities master fund LP

Tonga partners

Wexford catalyst fundsYork European opportunities fundZweig - dimennaZeal China

26

Chapter 3

Performance measurement and attribution of hedge funds

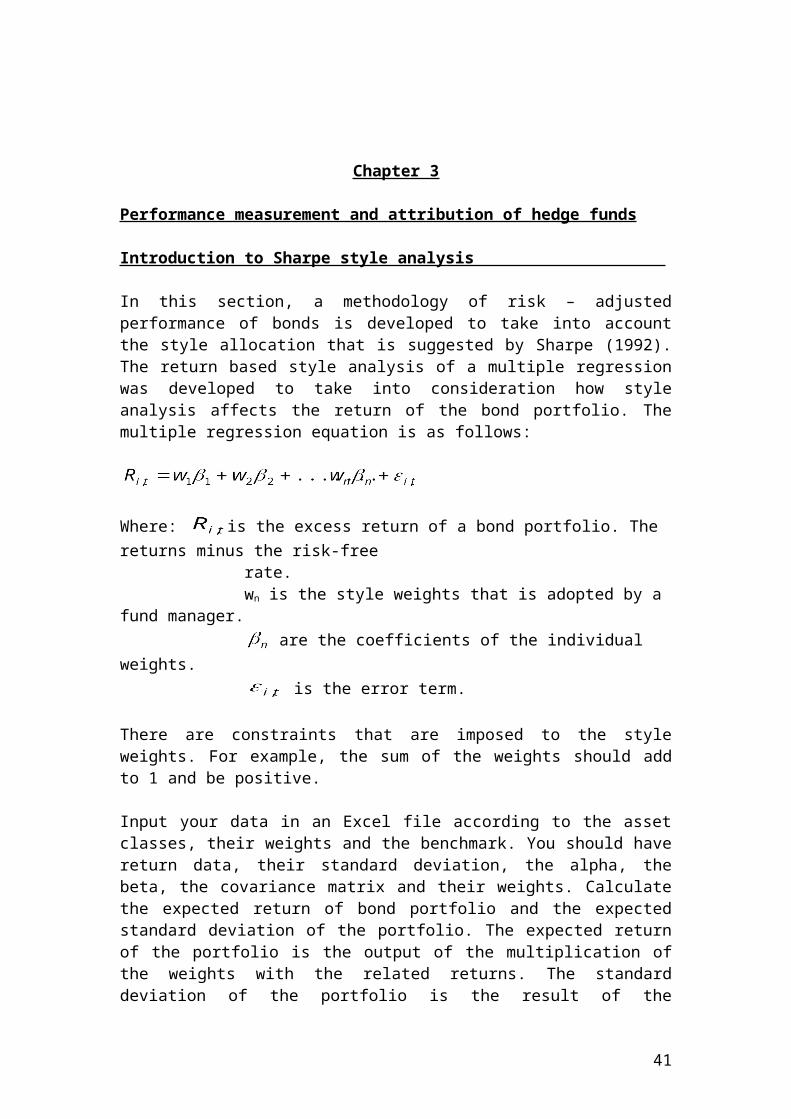

Introduction to Sharpe style analysis

In this section, a methodology of risk – adjusted performance of bonds is developed to take into account the style allocation that is suggested by Sharpe (1992). The return based style analysis of a multiple regression was developed to take into consideration how style analysis affects the return of the bond portfolio. The multiple regression equation is as follows:

Where: is the excess return of a bond portfolio. The returns minus the risk-free rate. wn is the style weights that is adopted by a fund manager. are the coefficients of the individual weights. is the error term. There are constraints that are imposed to the style weights. For example, the sum of the weights should add to 1 and be positive.

Input your data in an Excel file according to the asset classes, their weights and the benchmark. You should have return data, their standard deviation, the alpha, the beta, the covariance matrix and their weights. Calculate the expected return of bond portfolio and the expected standard deviation of the portfolio. The expected return of the portfolio is the output of the multiplication of the weights with the related returns. The standard deviation of the portfolio is the result of the multiplication of the variances with the weights, the individual standard deviations the weights and the correlation coefficients. Specifically, use the Solver add-in function in Excel. It is very important for a mutual bond fund investor to be sure that the manager’s selects the investment weights that will maximise the return on the portfolio. If the investor wants to consider all possible efficient portfolios that can be formed from n securities, it must be possible to determine the composition of each one of these portfolios.

The above can be achieved through Solver add – in Excel function, which is basically linear programming. But what is linear programming? It is a mathematical solution technique, which can make it possible to find the investment weights that will maximise the return of a portfolio. The investor must select a solution procedure that maximise the returns of the portfolio. Solver add - in model in Excel consists of three components. Set target cell. You select a formula cell in Excel. For example, expected return calculation, portfolio standard deviation, the alpha return or the Sharpe ratio measured as the excess return divided by the portfolio standard deviation. Excess return is the expected portfolio return minus the risk- free rate.

By changing cells select the cells of the weights that you want to maximize. Finally, subject to constraints, you press add and you select the cell that the constraints will be applied. Select the relationship you want to add or change ( <=, =, >=, int, or bin )

27

between the referenced cell and the constraint. Then enter for the constraint a number the box to the right. For example, there are constraints that are imposed to the style weights. For example, the sum of the weights should add to 1 or equal to 1 and should be >= than 0. These two constraints are added for example when setting as a target cell the Sharpe ratio.

We assume that investors are risk averse. They prefer a low level of risk. The level of risk is measured by the beta of the bond portfolio. The weighted average of the expected returns on the individual bonds in the portfolio is the weights of the bonds expressed as a fraction of the total portfolio invested in each bond. The first constraint is beta or portfolio standard deviation. Beta is a risk measure of the tendency of a bond to move up or down with the market. In the case that =1, the portfolio moves according to the market index. A beta value greater than 2 indicated a high degree of market risk. The second constraint is the alpha value. The difference between the actual expected return and the expected return is known as the alpha value of a security. Alpha is the intercept of the regression equation and beta is the slope of the regression equation. The alpha value of a bond portfolio is the weighted average of the alpha value of the individual bonds that constitute the portfolio. Check the weight changes after optimisation to find if bond weighting was allocated appropriately and the resources were used efficiently.

I have selected the following asset classes and benchmark indexes

Asset Classes

Treasury bills less than 90 days to maturity.Medium - term government bonds with maturity less than 10 years. Long-term government bonds with a maturity greater than 10 years.High yield corporate bonds involves high credit riskHigh grade corporate bonds

Benchmark Indexes

JPM GBI SwedenNDEA Denmark government bond constant maturity 5YJPM GBI United KingdomJPM GBI United StatesBMAL European Union governmentJPM EMBI global diversifiesBAML blended high yield bondsBAML Euro corporate

28

Rolling methodology of performance measurement

The quality of mutual fund management has been investigated in the literature largely in relation to the ability to select stocks and market-timing ability. Their focus was to test the null hypothesis that fund managers cannot outperform the market and do not have market timing skills. The alternative hypothesis is that fund managers can outperform the market and have market timing skills which enable them to predict the movement of the market.

To test these hypotheses, we use a rolling methodology for the first, third, fifth and ninth years. The term ‘rolling’ means that the third year includes the first, second and third years and the fifth year includes all the previous years. We test the hypothesis of Hendricks, Patel, and Zeckhauser (1993), Goetzmann and Ibboston (1994), Brown and Goetzmann (1995), and Wermers (1996) who found evidence of persistence in mutual fund performance over relatively short-term horizons of one to three years and attribute the persistence to skilled and market timing fund managers. The ninth year includes observations that start from the fifth year. We test the hypothesis of Grinblatt and Titman (1992), Elton, Gruber, Das and Hlavha (1993), and Elton, Gruber, Das, and Blake (1996a) who documented mutual fund return persistence over longer horizons periods of five to ten years and attribute the persistence to skilled managerial performance. The rolling methodology approach is consistent with Gruber (1996), Fama and French (1993), and Carhart (1997).

Our first approach follows Fama and French’s (1993) three-factor model and aims to measure performance as the intercept from the regression that includes size, a book-to-market factor and the excess market return as independent variables. Our second approach is the Fama and French (1993) three-factor model extended to include a variable from the Treynor and Mazuy (1966) model related to market timing ability. This additional independent variable is the square of the market rate of return. The third approach is Carhart’s (1997) performance persistence theory which takes into consideration an additional anomaly referred to as momentum.

In terms of signs of the independent variables, we expect to find positive values for the coefficients of size, market and negative values are expected for the book-to-market effect. Positive or negative values are expected for momentum. In more detail, size effect was documented in Fama and French’s model in terms that small firms outperform big companies and therefore we expect a positive effect. Market effect has always played an important role in return explanation based on the CAPM. Book-to-market effect is expected to have a negative value based on the hypothesis of Pontiff (1997) who found that the book-to market effect is negative and insignificant and affects funds with low premiums and discounts. Momentum is expected to have a positive sign during the short-term according to the hypothesis of Jegadeesh and Titman (1993). In more detail, Jegadeesh and Titman (1993) show that buying past winners and selling past losers generates significant profits when returns are measured over three to twelve-month periods. This hypothesis is tested later by using deciles and trying to test the significance between rankings. In contrast, momentum is

29

expected to have a negative sign over the long term as we assume that information both private and public were incorporated in the prices of funds.

The model of Fama and French (1993) was constructed and implemented on various portfolios of shares to explain various anomalies in financial markets in terms of size and the book-to-market ratio. This led to the three-factor model. Gruber (1996) tested performance persistence by identifying four factors: the local equity market index, a size index, a bond index and an index which measures the performance of the difference between growth and value stocks. The last factor is used because of the importance of the book to market ratio in explaining returns (Fama and French, 1993). The bond index factor focuses on income funds that invest in bonds.

Following Gruber (1996) and Fama and French (1993), we define one, three, five and nine year managerial performance based on monthly returns which are defined as excess NAV returns for the period January 1990 to January 2003. The intercepts

from the regression equations for one, three, five and nine years respectively are used to measure the contribution of the manager to the performance of the fund. Thus, a positive and statistically significant alpha indicates superior performance of the fund, whereas negative values or statistically insignificant values represent inferior or neutral managerial performance.

The hypotheses to be tested are as follows:

H0 : ≤ 0, Fund managers have an inferior or neutral performanceH1: 0 Fund managers have a superior performance

We extend Fama and French’s model to include an additional independent variable following the Treynor and Mazuy (1966) model. The extra variable is the square of the market return which is included in an attempt to capture market timing ability. The intercepts from the regression equations for one, three, five and nine years respectively are used to measure the contribution of the manager to the performance of the fund. Thus, as before, a positive and statistically significant alpha indicates superior managerial performance of the fund, whereas negative values or statistically insignificant values represent inferior or neutral managerial performance. In their paper, Treynor and Mazuy (1966) assume that if a mutual fund is not engaged in market timing and maintains a constant fund beta, the relationship between the fund return and the return on the benchmark will be linear. However, if the fund is successful at market timing, the fund return will be higher than the benchmark return, and the relationship between the fund return and the return on the benchmark will be non-linear. Thus we can test for timing ability by testing for this nonlinearity. To do this, we include the square of the market return as an additional independent variable (with coefficient ). A negative or zero means that fund managers do not have market timing ability, whereas a positive would imply that fund managers have market timing ability.

The hypotheses to be tested are as follows:

H0 : ≤ 0, ≤ 0 Fund managers have an inferior or neutral performance

30

H1: 0, 0 Fund managers have a superior performance

Mutual fund persistence is well documented in the finance literature. Wermers (1996) suggests that it is momentum that generates short-term persistence. Carhart (1997) argues that persistence of returns can be attributed mainly to the difference in expenses charged. Much of the remaining persistence is driven by the one-year momentum effect of Jegadeesh and Titman (1993). In more detail, Jegadeesh and Titman (1993) show that buying past winners and selling past losers generates significant profits when returns are measured over three to twelve-month periods. They show, with NYSE and AMEX securities over the period 1965-1989, that a successful momentum strategy was buying the winners from the previous six months, (for example, the assets at the top of the rankings) and selling the losers from the previous six months. This shows that asset returns exhibit momentum, which means that the winners of the past continue to perform well and the losers of the past continue to perform badly. Fama and French (1993) stress that their model does not explain the short-term persistence of returns highlighted by Jegadeesh and Titman (1993). Carhart (1997), on the other hand, suggests that performance persistence is due to the use of momentum strategies by the fund managers, rather than the managers being particularly skilful at picking winning stocks.

Using our sample of 120 investment trusts funds, both alive and dead, and 30 US closed end funds, we test the hypothesis of managerial performance persistence and secondly, we test the hypothesis of discount persistence. Performance is defined as gross managerial performance less expenses charged by managers. Funds are grouped into portfolios ranked on the level of past performance and allocated to deciles. As before, past performance is measured over one, three five and nine year periods by using monthly data from 01/01/1990 to 01/01/2003. In the finance literature, the most frequent test that is used to test performance persistence is the Spearman rank correlation coefficient. The purpose for using the Spearman rank correlation coefficient is to break down the distribution into tenths in order to be able to detect persistence among the deciles through the various years. The weakness of this methodology is that author’s arbitrarily choose as a benchmark the past performance that will be compared with subsequent years. Dimson and Minio-Kozerski (2001) found that there is managerial performance persistence during the first two years of the life of the funds. Similarly, Allen and Tan (1999) used as a benchmark the first two-year period compared with the subsequent two-year period. Our approach is different in terms of the subsequent years. We test for short and long-term persistence by using as a benchmark the first two years measured as the average NAV return and test for persistence over the first, third, fifth, and ninth years thereafter.

Try to apply this methodology in bond portfolio management for bonds that are traded at a premium and others that are traded at a discount. The hypothesis test should focus on managerial performance persistence measured in terms of market timing and skill selection.

31

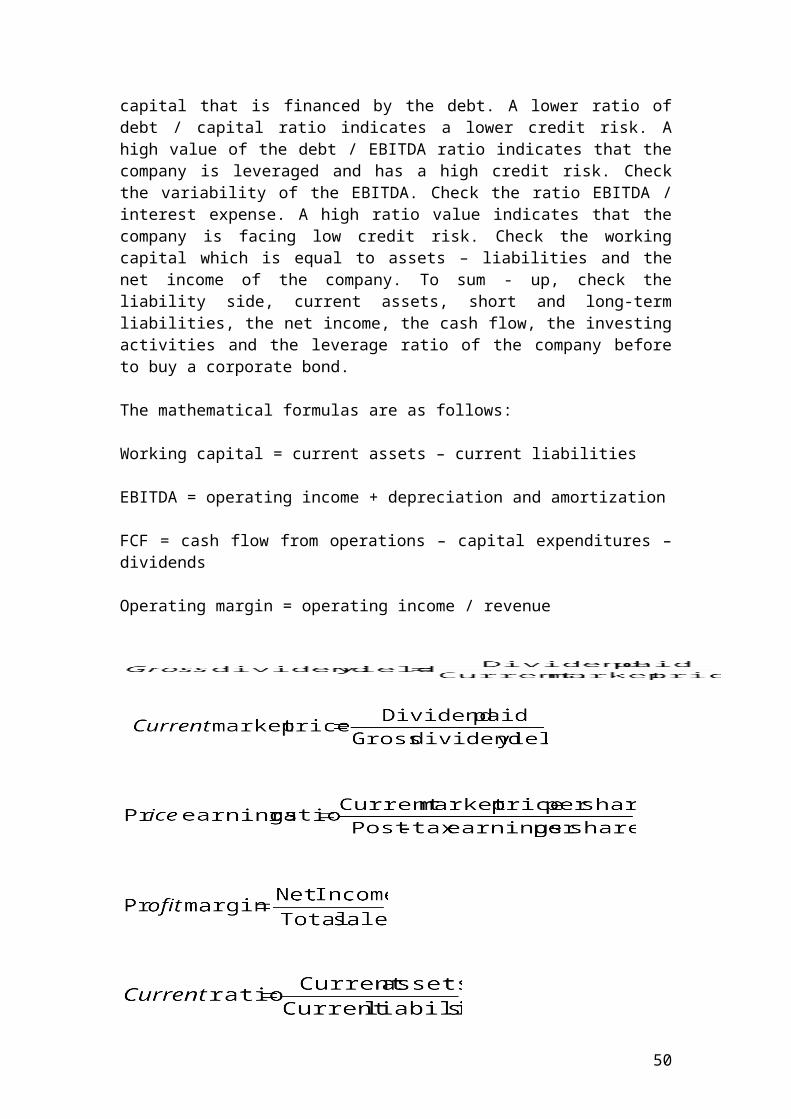

Introduction to different types of bond financial ratios It is also important to measure the value of the business before to make any investment. The most common measures that are used are gross dividend yield, current market price, and price/earnings ratio. In addition, check carefully the cash flows from investing and financing activities. Is there an increase in cash in the statement of cash flows that will be used in the subsequent years? On the other hand, please have a look to the profit and loss account. Check carefully that the revenues are exceeding the expenses and that you get a positive net income. In other words, the company is recording a gain and not a loss. Check the fixed and variables costs and make sure that they are covered from the sales that the company is doing. Don’t take blind risk that could destroy the capital of the client. Please pay particular attention to this point. Check the number of times interest earned to cover interest expenses from potential loans. Check the profit margin, the current ratio, the acid test ratio and the account receivable turnover, the earning per share and the dividends that are paid annually. In addition, check the earnings before interest, taxes, depreciation and amortization, EBITDA. Check the free cash flow after dividends, FCF, the operating margin, the debt / EBITDA, the EBITDA/interest, FCF/debt, EBITDA/interest expense and the debt/capital ratio. It is very important to find the percentage of capital that is financed by the debt. A lower ratio of debt / capital ratio indicates a lower credit risk. A high value of the debt / EBITDA ratio indicates that the company is leveraged and has a high credit risk. Check the variability of the EBITDA. Check the ratio EBITDA / interest expense. A high ratio value indicates that the company is facing low credit risk. Check the working capital which is equal to assets – liabilities and the net income of the company. To sum - up, check the liability side, current assets, short and long-term liabilities, the net income, the cash flow, the investing activities and the leverage ratio of the company before to buy a corporate bond.

The mathematical formulas are as follows:

Working capital = current assets – current liabilities

EBITDA = operating income + depreciation and amortization

FCF = cash flow from operations – capital expenditures – dividends

Operating margin = operating income / revenue

32

In the workshop, I will include practical examples from the account of companies listed in the stock exchange.

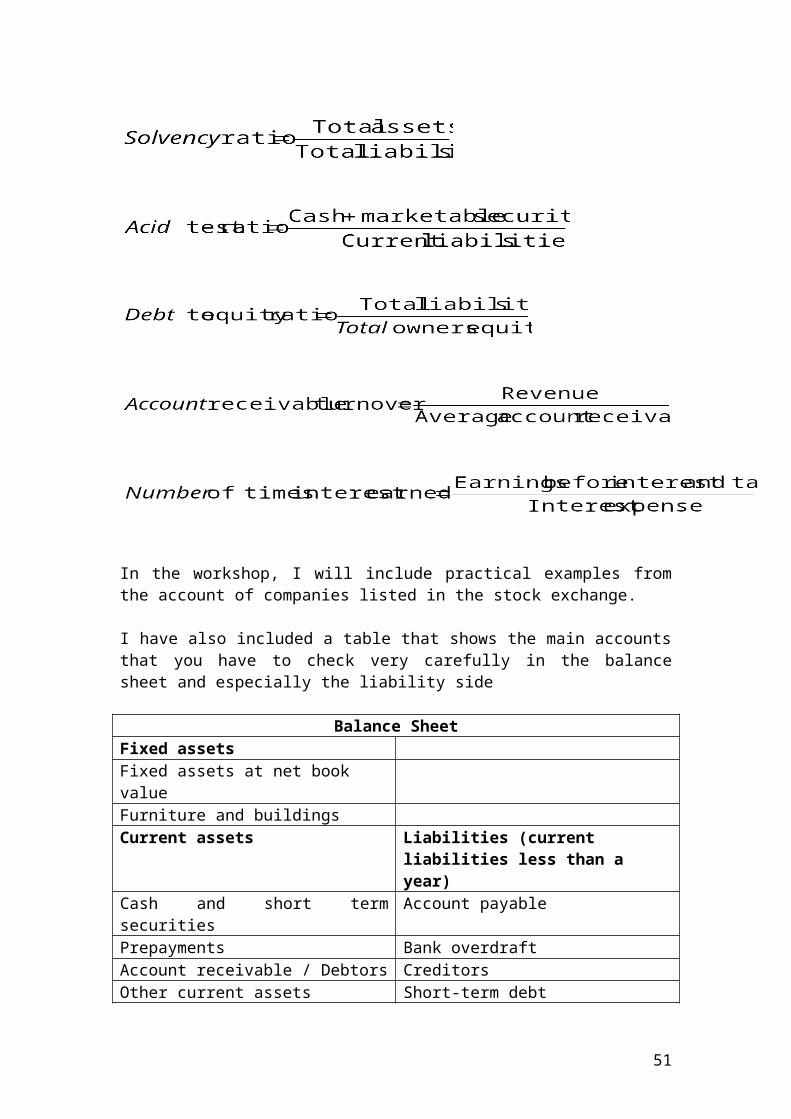

I have also included a table that shows the main accounts that you have to check very carefully in the balance sheet and especially the liability side

Balance SheetFixed assetsFixed assets at net book valueFurniture and buildingsCurrent assets Liabilities (current liabilities less than

a year)Cash and short term securities Account payablePrepayments Bank overdraftAccount receivable / Debtors CreditorsOther current assets Short-term debtShareholder’s equityShare capital Long-term liabilities (more than a

year)Retained earnings Long-term debt

Source: author’s illustration.

33

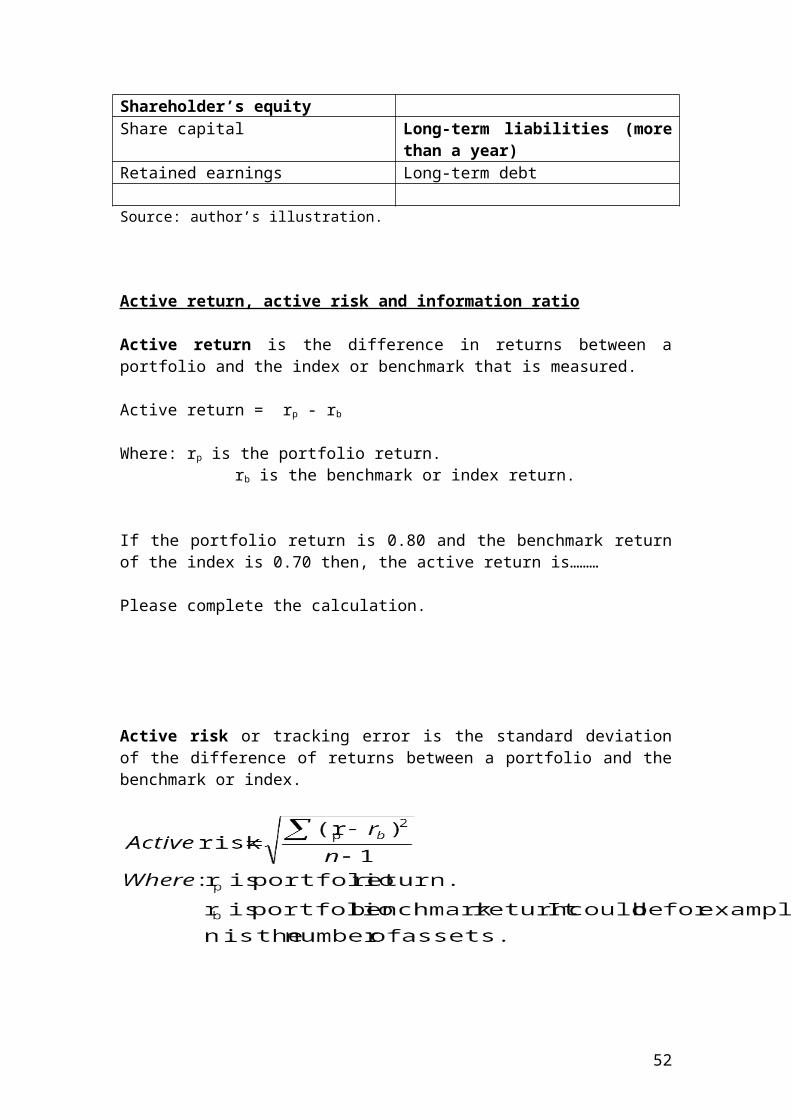

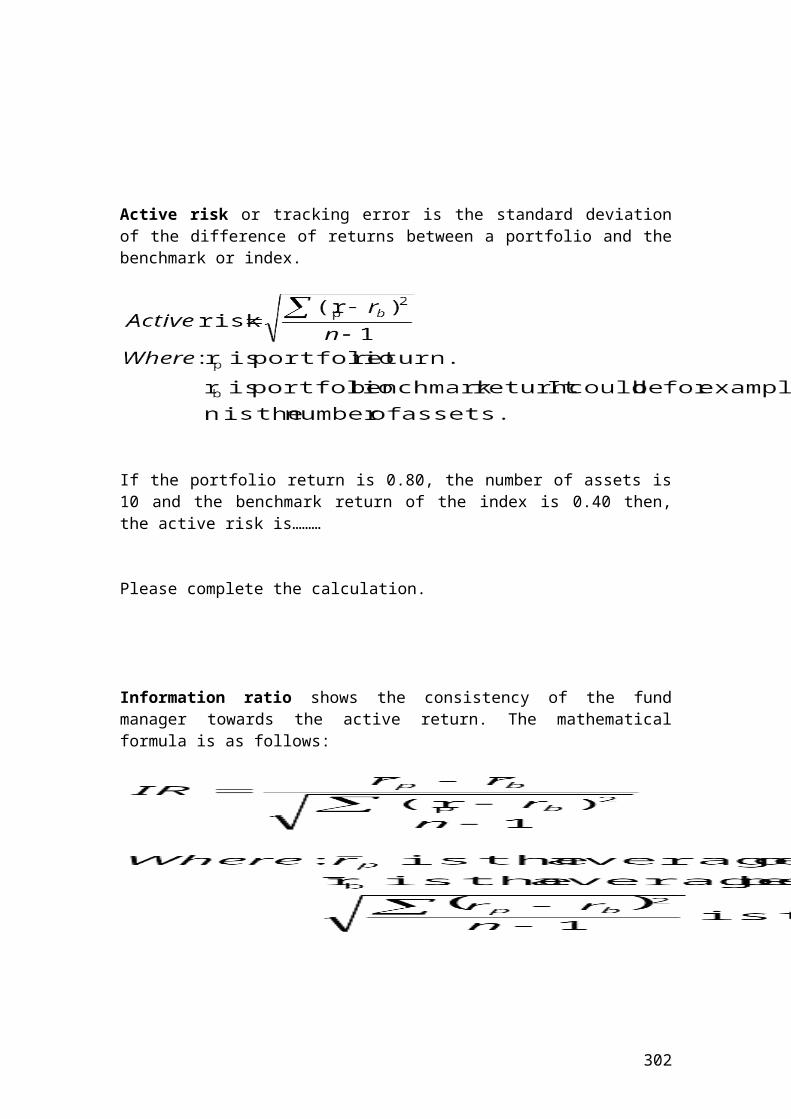

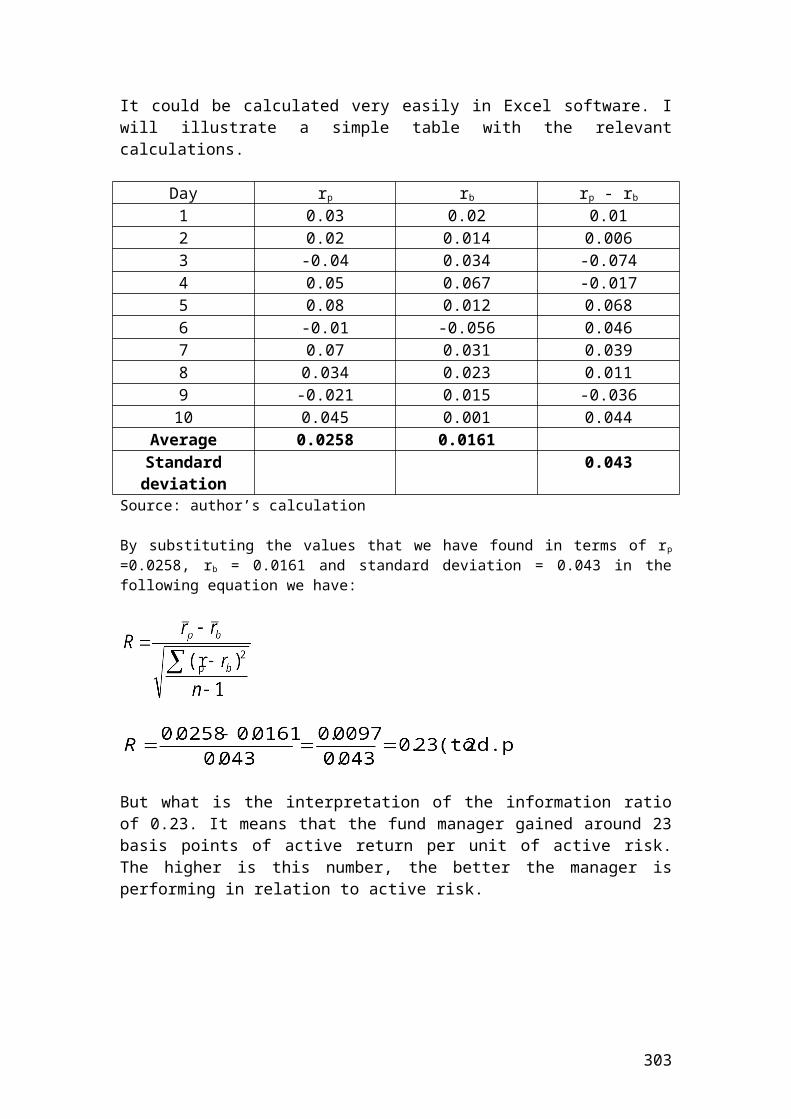

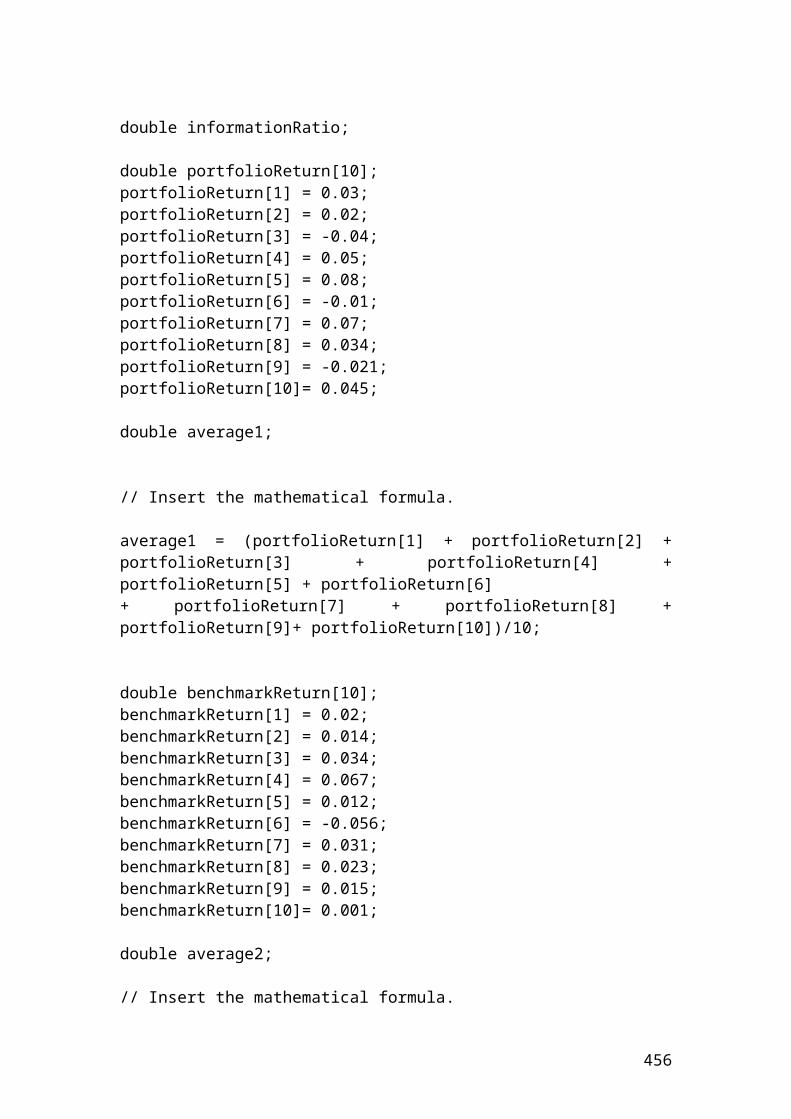

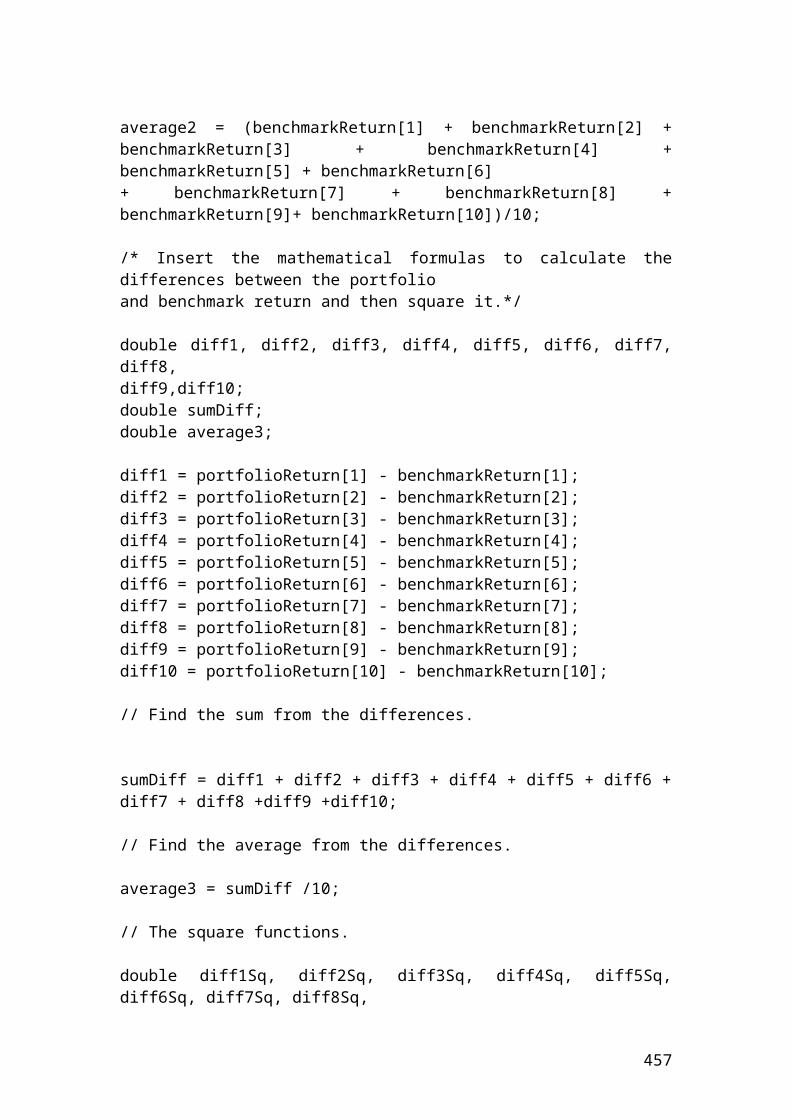

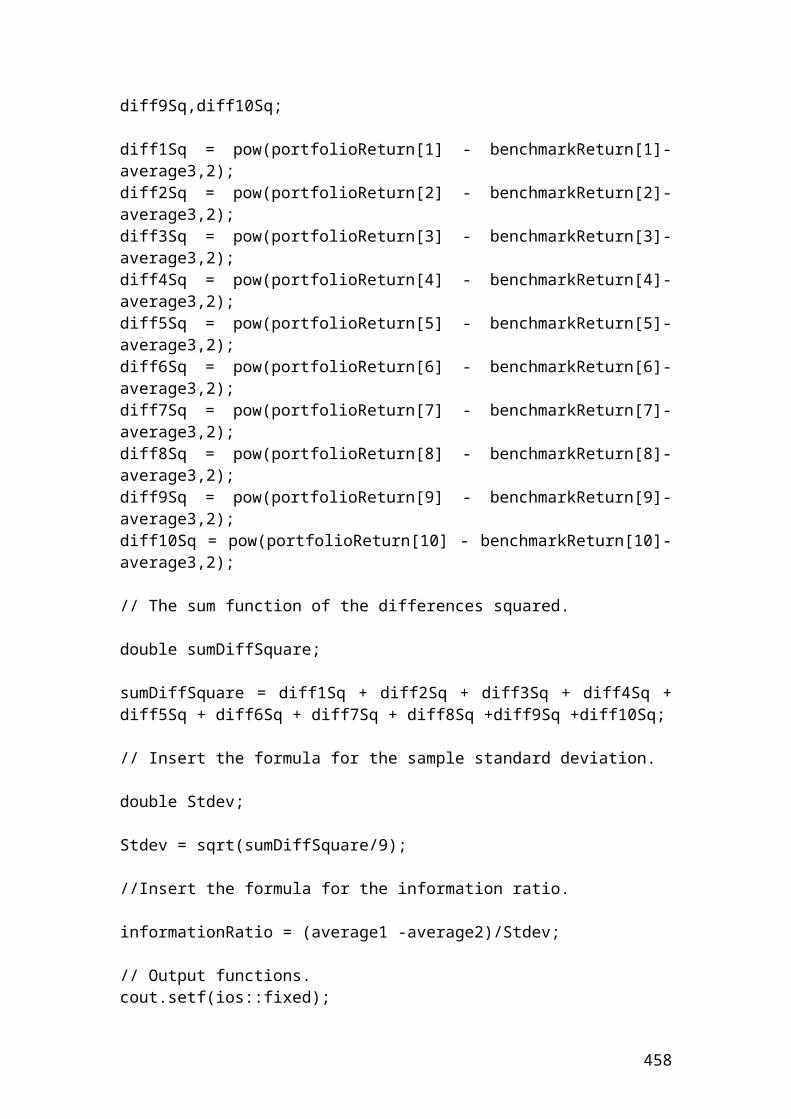

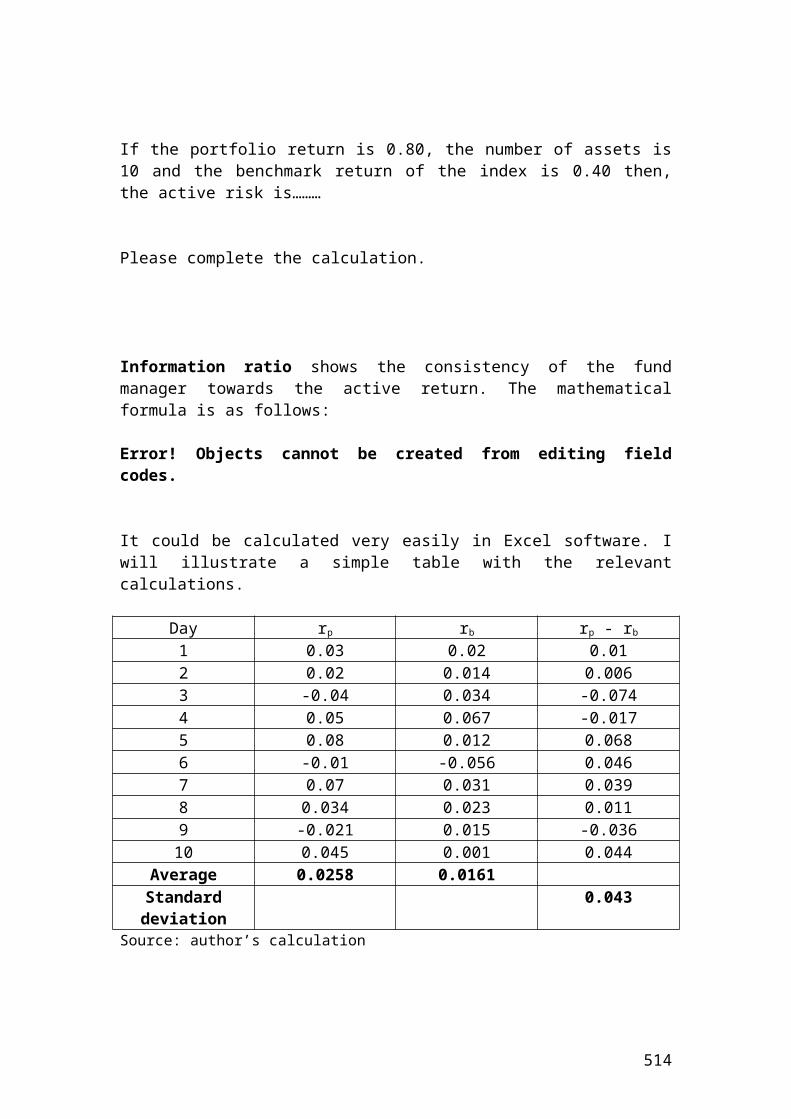

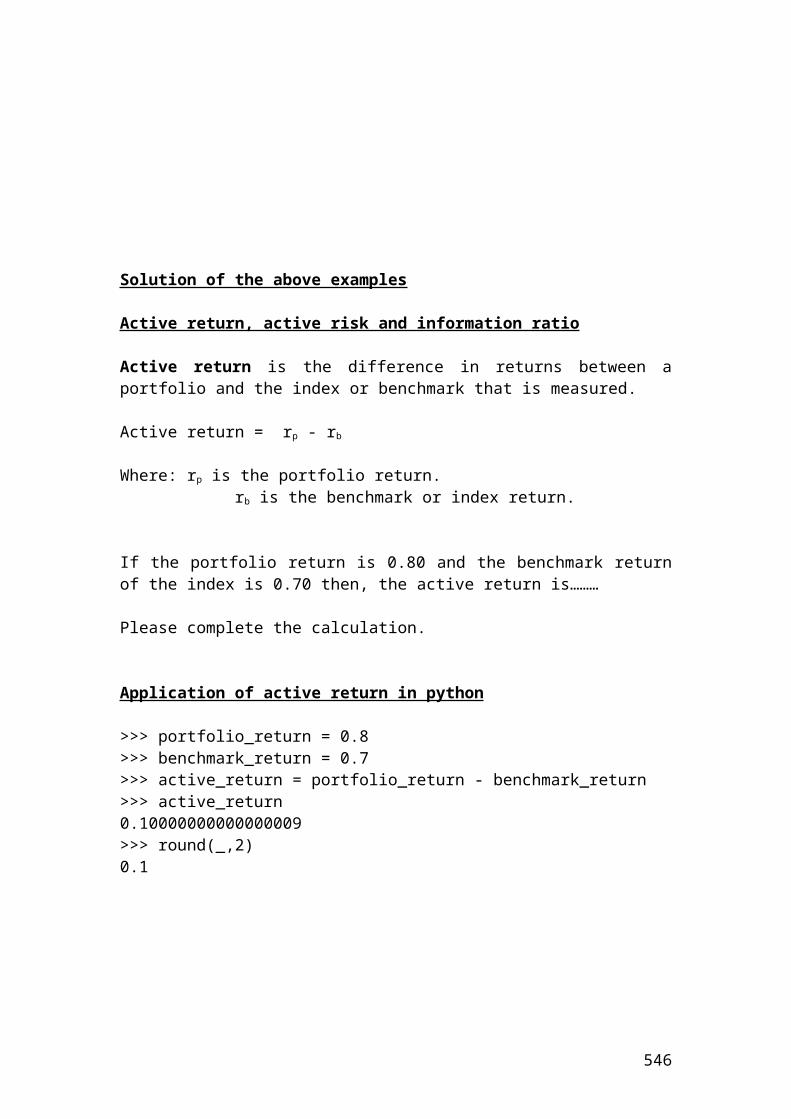

Active return, active risk and information ratio

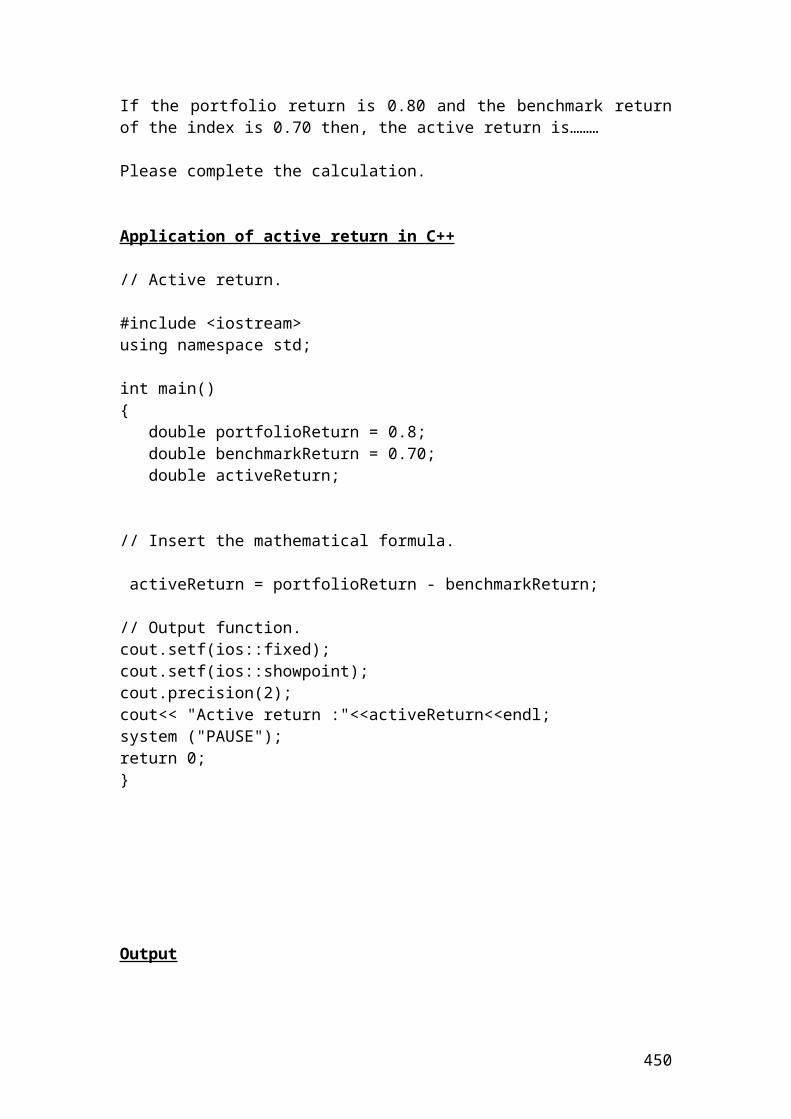

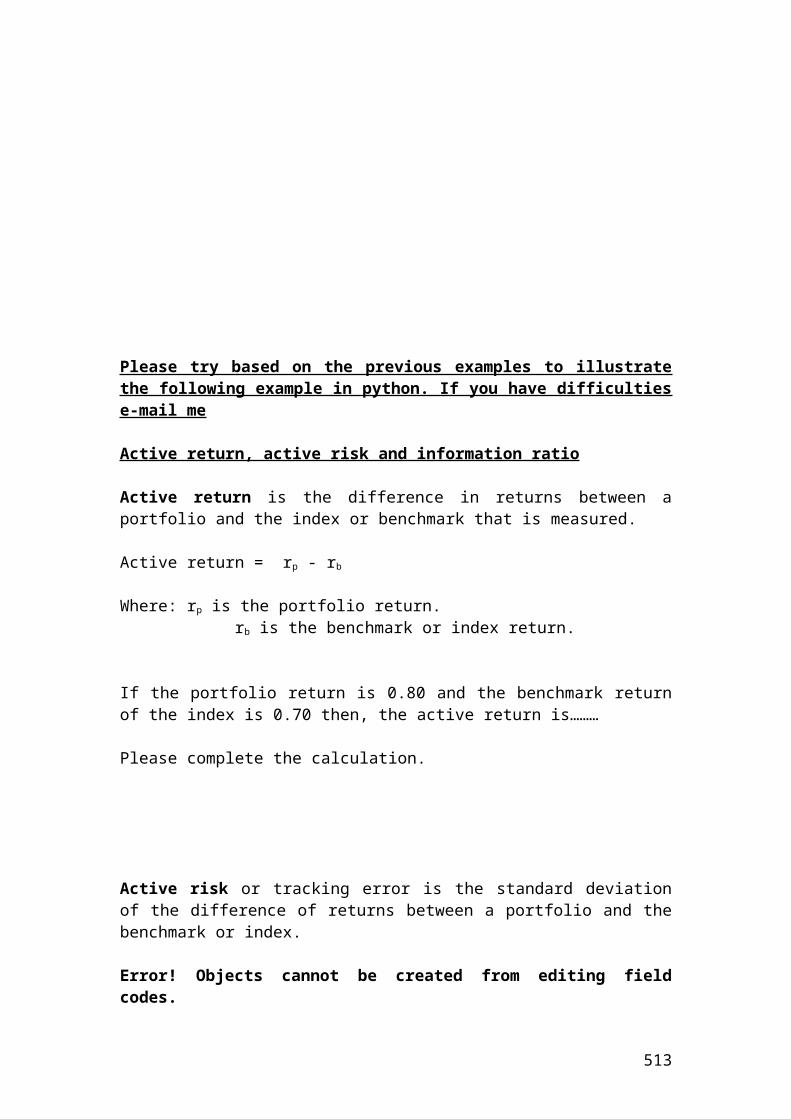

Active return is the difference in returns between a portfolio and the index or benchmark that is measured.

Active return = rp - rb

Where: rp is the portfolio return. rb is the benchmark or index return.

If the portfolio return is 0.80 and the benchmark return of the index is 0.70 then, the active return is………

Please complete the calculation.

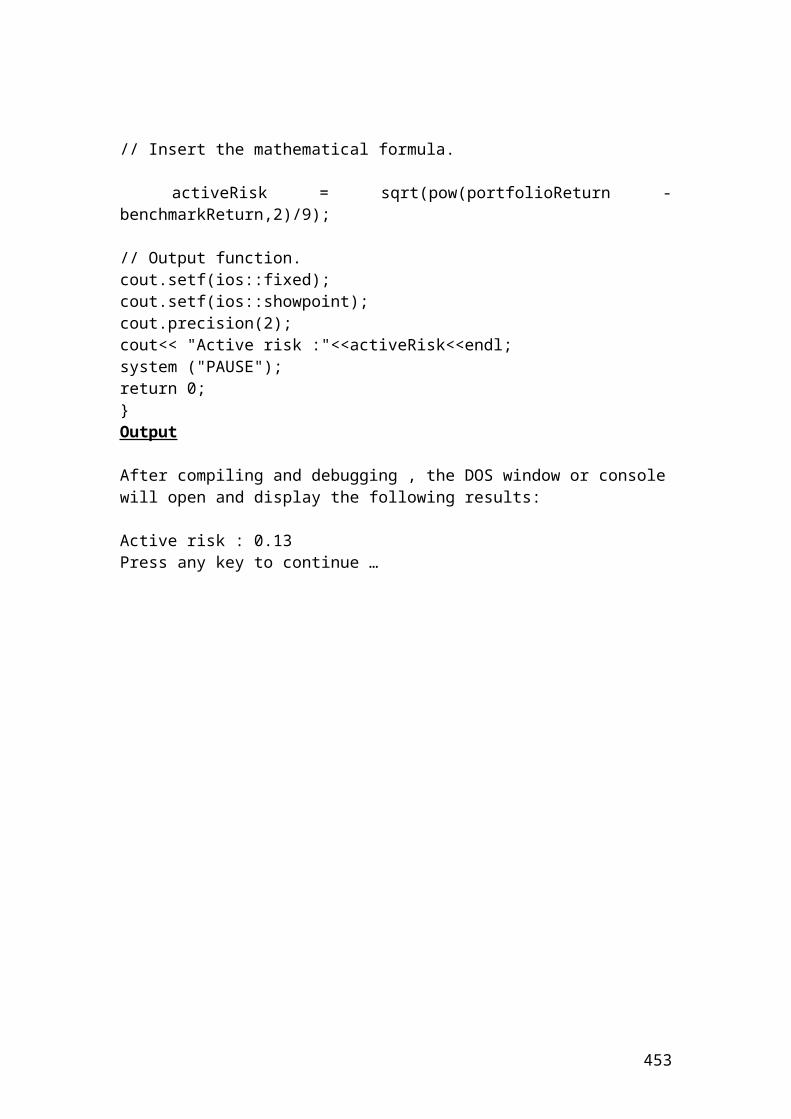

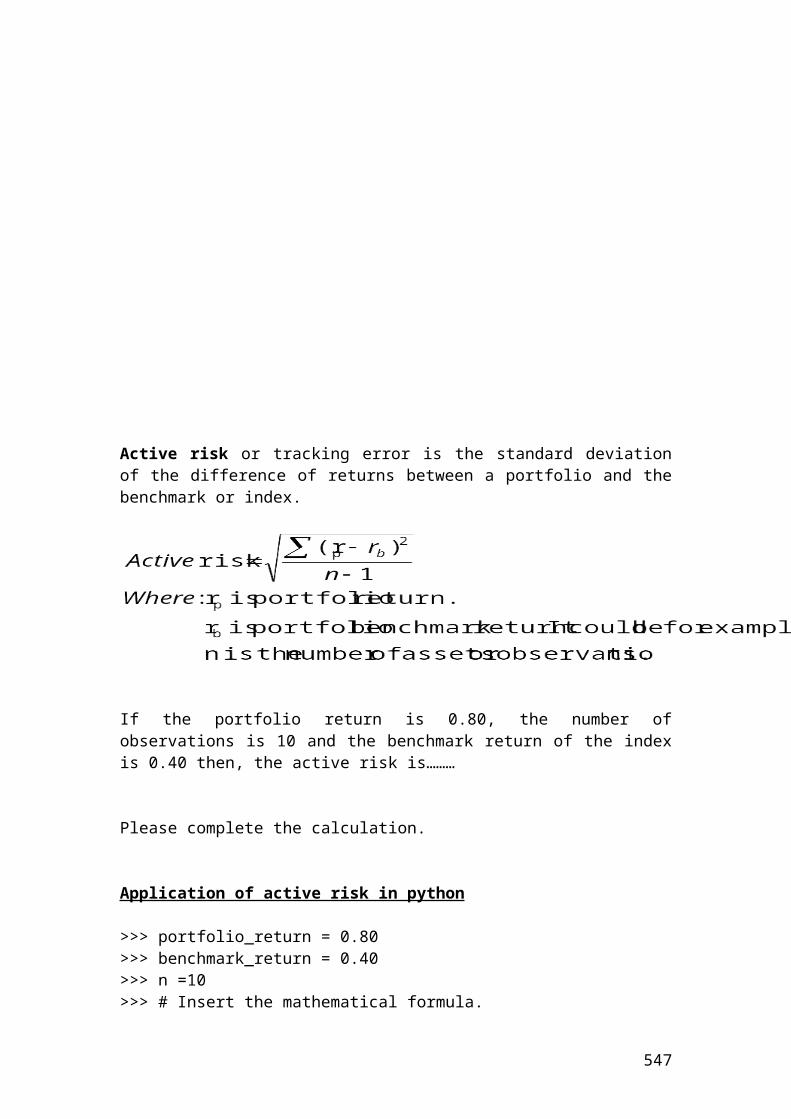

Active risk or tracking error is the standard deviation of the difference of returns between a portfolio and the benchmark or index.