Embed Size (px)

Citation preview

CompliancePlus Consulting Limited801, Two Exchange Square, 8 Connaught Place, Central, Hong KongTel: (852) 3487 6903 www.complianceplus.hk

HEDGE FUND FEE STRUCTURE & MARKETING

July 2013

Josephine Chung, Director Hayden Cheung, Research Assistant

CompliancePlus Consulting

Disclaimer

2

The information in this presentation is CONFIDENTIAL. It is intended solely for use bythe person to whom it is given and may not be reproduced or redistributed. Thispresentation is not for distribution to the general public but for intended recipients onlyand may not be published, circulated, reproduced or distributed in whole or part to anyother person without the written consent of CompliancePlus Consulting Limited.

In addition, this presentation is for informational and illustrative purposes only and shouldnot be construed as legal, tax, investment or other advice. This presentation does notconstitute an offer to provide legal and accounting services and opinion byCompliancePlus Consulting Limited.

All Copyrights reserved.

Confidential

CompliancePlus Consulting

TA

BLE

OF

CO

NT

EN

TS

Table of Contents

1. Hedge fund fee structure

2. Criticisms on fee structure

3. Change in US hedge fund marketing rules

4. Other trends and developments

3

CompliancePlus Consulting

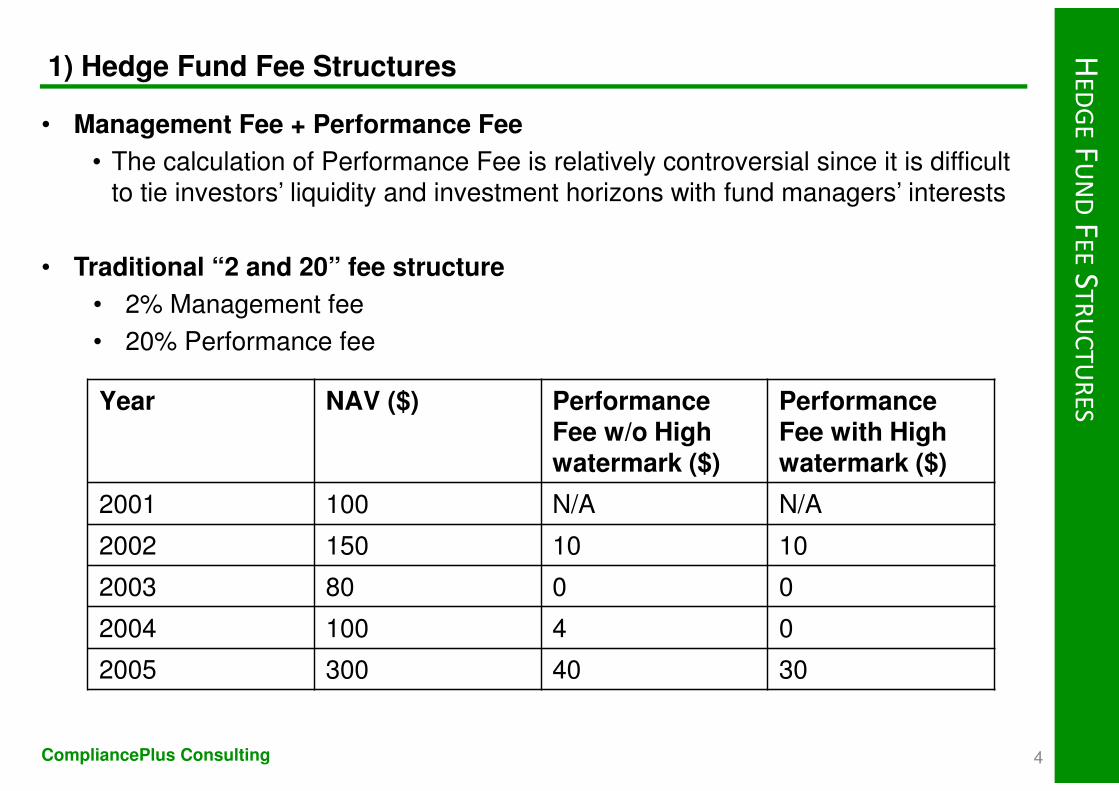

• Management Fee + Performance Fee

• The calculation of Performance Fee is relatively controversial since it is difficult to tie investors’ liquidity and investment horizons with fund managers’ interests

• Traditional “2 and 20” fee structure

• 2% Management fee

• 20% Performance fee

HE

DG

EF

UN

DF

EE

ST

RU

CT

UR

ES

1) Hedge Fund Fee Structures

4

Year NAV ($) Performance Fee w/o High watermark ($)

Performance Fee with High watermark ($)

2001 100 N/A N/A

2002 150 10 10

2003 80 0 0

2004 100 4 0

2005 300 40 30

CompliancePlus Consulting

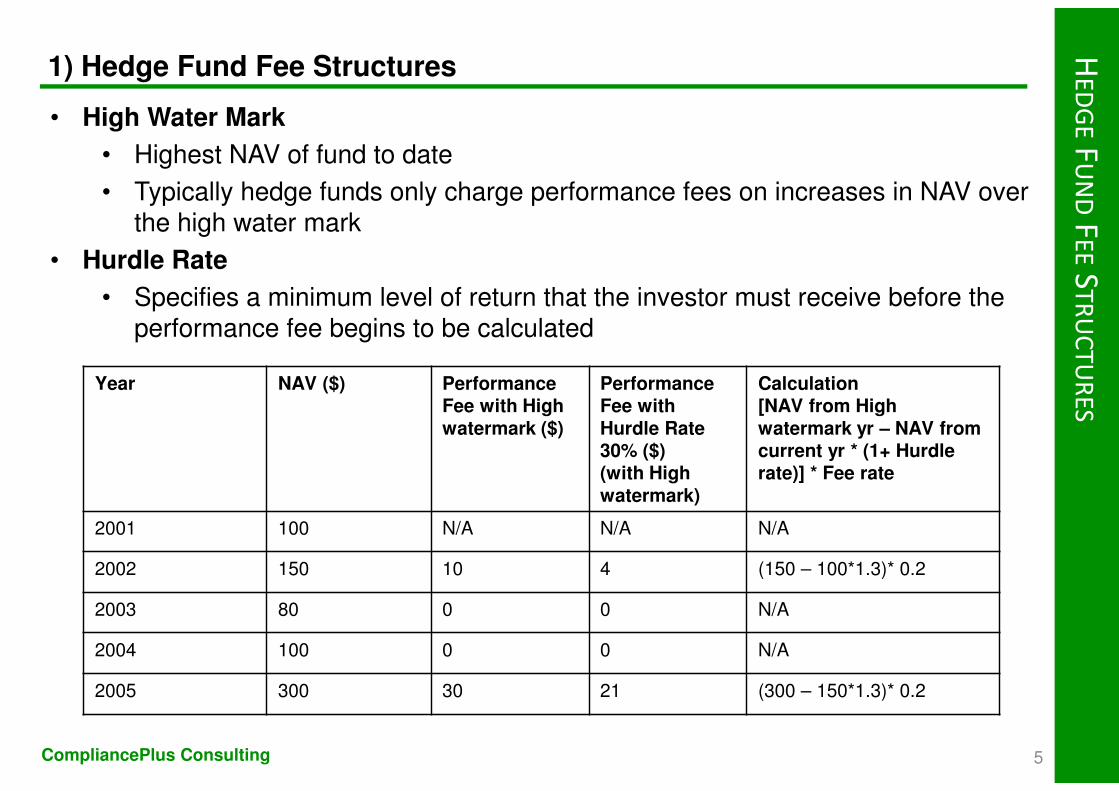

• High Water Mark

• Highest NAV of fund to date

• Typically hedge funds only charge performance fees on increases in NAV over the high water mark

• Hurdle Rate

• Specifies a minimum level of return that the investor must receive before the performance fee begins to be calculated

HE

DG

EF

UN

DF

EE

ST

RU

CT

UR

ES

1) Hedge Fund Fee Structures

5

Year NAV ($) Performance Fee with High watermark ($)

Performance Fee with Hurdle Rate 30% ($)(with High watermark)

Calculation[NAV from High watermark yr – NAV from current yr * (1+ Hurdle rate)] * Fee rate

2001 100 N/A N/A N/A

2002 150 10 4 (150 – 100*1.3)* 0.2

2003 80 0 0 N/A

2004 100 0 0 N/A

2005 300 30 21 (300 – 150*1.3)* 0.2

CompliancePlus Consulting

• Clawback

• The ability for fund clients to reclaim fees awarded the previous year should gains evaporate.

• E.g. Abax Dymon Asia Macro Fund

• Half of its 20 percent performance fees will be paid back if the fund loses money the next year.

HE

DG

EF

UN

DF

EE

ST

RU

CT

UR

ES

1) Hedge Fund Fee Structures

6

CompliancePlus Consulting

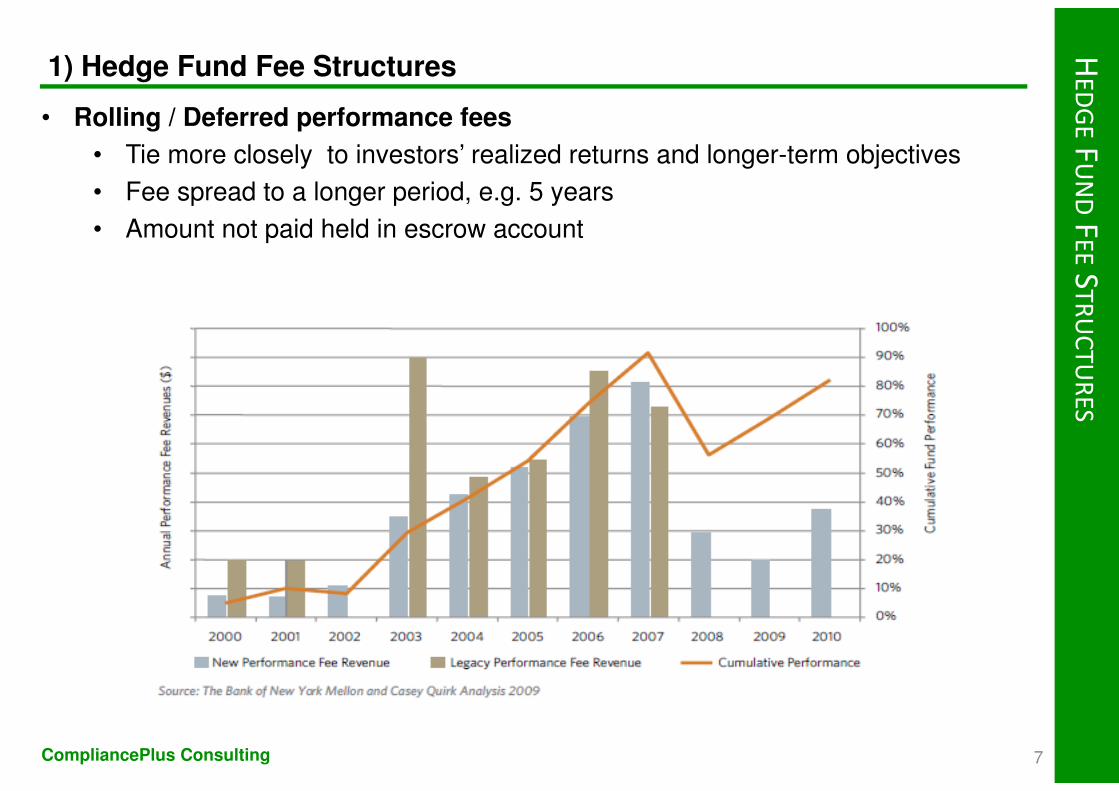

• Rolling / Deferred performance fees

• Tie more closely to investors’ realized returns and longer-term objectives

• Fee spread to a longer period, e.g. 5 years

• Amount not paid held in escrow account

HE

DG

EF

UN

DF

EE

ST

RU

CT

UR

ES

1) Hedge Fund Fee Structures

7

CompliancePlus Consulting

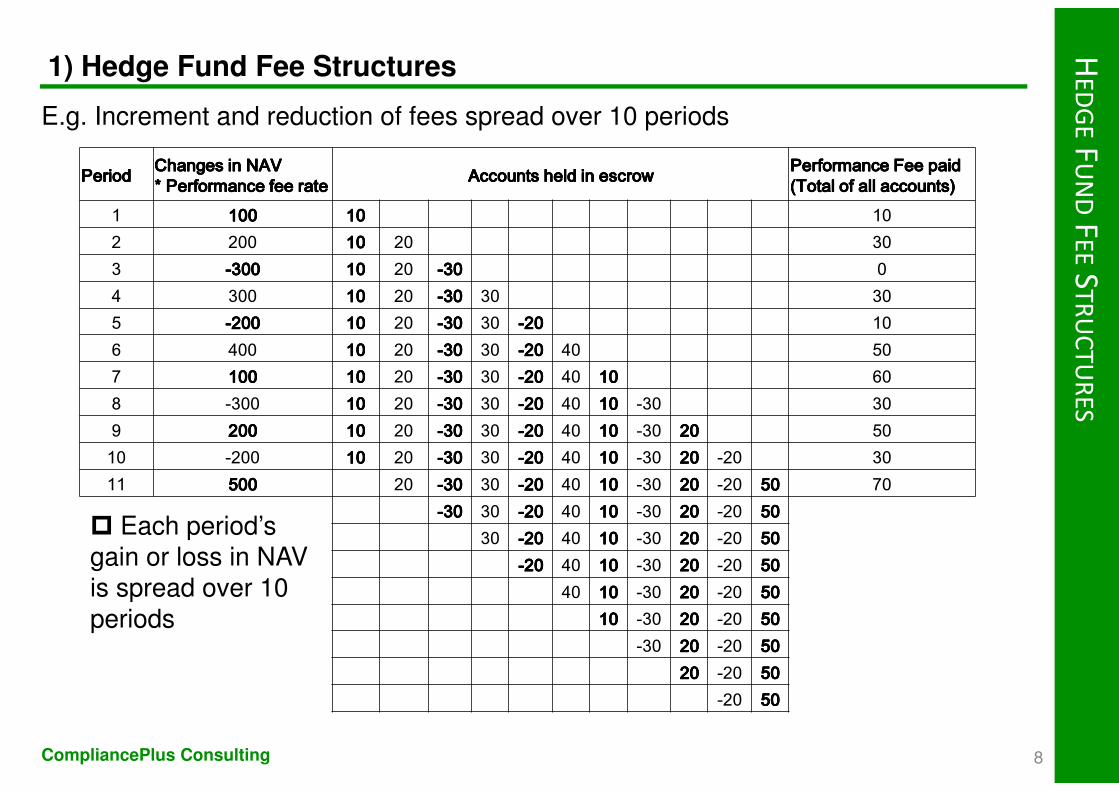

PeriodPeriodPeriodPeriod Changes in NAV Changes in NAV Changes in NAV Changes in NAV * Performance fee rate* Performance fee rate* Performance fee rate* Performance fee rate Accounts held in escrowAccounts held in escrowAccounts held in escrowAccounts held in escrow Performance Fee paid Performance Fee paid Performance Fee paid Performance Fee paid

(Total of all accounts)(Total of all accounts)(Total of all accounts)(Total of all accounts)1 100100100100 10101010 102 200 10101010 20 303 ----300300300300 10101010 20 ----30303030 04 300 10101010 20 ----30303030 30 305 ----200200200200 10101010 20 ----30303030 30 ----20202020 106 400 10101010 20 ----30303030 30 ----20202020 40 507 100100100100 10101010 20 ----30303030 30 ----20202020 40 10101010 608 -300 10101010 20 ----30303030 30 ----20202020 40 10101010 -30 309 200200200200 10101010 20 ----30303030 30 ----20202020 40 10101010 -30 20202020 5010 -200 10101010 20 ----30303030 30 ----20202020 40 10101010 -30 20202020 -20 3011 500500500500 20 ----30303030 30 ----20202020 40 10101010 -30 20202020 -20 50505050 70

----30303030 30 ----20202020 40 10101010 -30 20202020 -20 5050505030 ----20202020 40 10101010 -30 20202020 -20 50505050

----20202020 40 10101010 -30 20202020 -20 5050505040 10101010 -30 20202020 -20 50505050

10101010 -30 20202020 -20 50505050-30 20202020 -20 50505050

20202020 -20 50505050-20 50505050

E.g. Increment and reduction of fees spread over 10 periods

HE

DG

EF

UN

DF

EE

ST

RU

CT

UR

ES

1) Hedge Fund Fee Structures

8

� Each period’s gain or loss in NAV is spread over 10 periods

CompliancePlus Consulting

HE

DG

EF

UN

DF

EE

ST

RU

CT

UR

ES

1) Hedge Fund Fee Structures

9

• Minimum Investment Requirement

• Single strategy hedge fund: US$50,000

• Lock-up Period

• ‘Hard lock-up’: Cannot redeem from the fund until after a certain time period

• ‘Soft lock-up’: A redemption penalty will be charged if investors redeem prior to a certain investment period

• Incorporated into the formal Private Placement Memorandum (PPM) or offering documents

CompliancePlus Consulting

CR

ITIC

ISM

SO

NF

EE

ST

RU

CT

UR

E

2) Criticisms on fee structure

• High fees

• Hedge fund manager generally retain a larger fraction of “alpha” (return in excess of a passive benchmark unique to each fund) than long-only managers

• As main stream investors have entered the market, the legacy structure of fixed management fee and annual performance fee is outdated when the strategies and investors of hedge fund have changed

• The fundamental differences in investment strategies between hedge funds and mutual funds are shrinking, hedge funds should not maintain a much higher level of fees than mutual funds

10

CompliancePlus Consulting

CR

ITIC

ISM

SO

NF

EE

ST

RU

CT

UR

E

2) Criticisms on fee structure

11

• Lack of transparency

• Incomplete visibility into managers’ portfolio risks and operations

• The industry generally ignored new investors’ need for relevant information on their hedge fund investments

• Lack of transparency in the fund’s portfolio may assist fraud/exaggeration in performance of the fund

• Conflict of interest as often the prime broker acts as both custodian of assets and administrator (who calculates the NAV)

CompliancePlus Consulting

CR

ITIC

ISM

SO

NF

EE

ST

RU

CT

UR

E

2)Criticisms on fee structure

12

• Effect of the current fee structure on fund manager

• High water mark

• Excessive risk-taking in an attempt to make up losses• “By allowing managers to take a share of profit but providing

no mechanism for them to share losses, performance fees give managers an incentive to take excessive risk rather than targeting high long-term returns”—Warren Buffett

• Manager gives up fund easily

• A manager who has lost a significant percentage of the fund's value may close the fund and start again with a clean slate, rather than continue working for no performance fee until the loss has been made good

CompliancePlus Consulting

• Lifted 80 year old ban on marketing via the Jumpstart Our Business Startups (JOBS) Act

• Hedge Funds and other companies seeking private investments can now advertise publicly for funding

• JOBS act focused on encouraging funding of US small businesses via easing securities regulations

• Further regulations might occur

• SEC will vote separately to introduce a new proposal that seeks to monitor how advertising is used and whether it is contributing to more fraud

CH

AN

GE

INU

S H

ED

GE

FU

ND

MA

RK

ET

ING

RU

LES

3) Change in US hedge fund marketing rules

13

CompliancePlus Consulting

• Restrictions to Hedge Fund customers still apply

• Hedge Funds serve only accredited investors (wealthy investors)

• Free up hedge-fund managers to communicate more freely at conferences; unlikely for hedge funds to advertise on TV & mass media

• Able to offer more information about fund performance on their websites

CH

AN

GE

INU

S H

ED

GE

FU

ND

MA

RK

ET

ING

RU

LES

3) Change in US hedge fund marketing rules

14

CompliancePlus Consulting

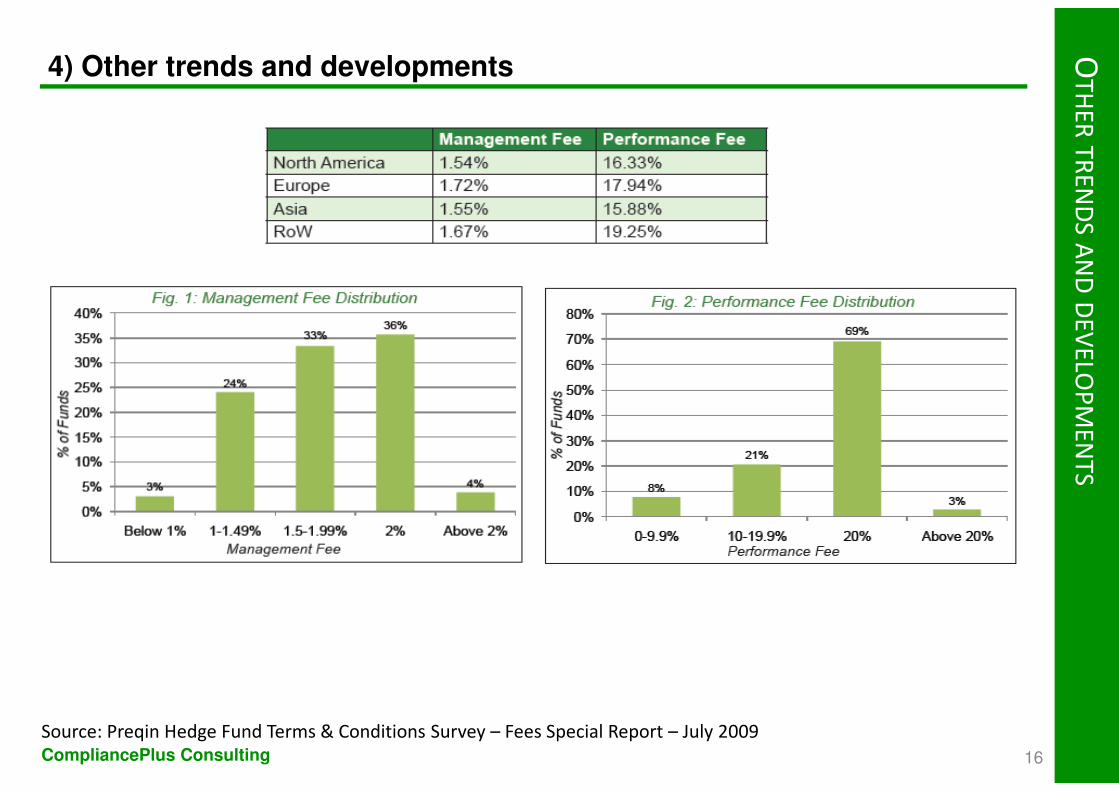

• Lower Fees

• Mean management fee = 1.63%

• Mean performance fee = 17.21%

(Results of Preqin’s Hedge Fund Terms & Conditions Survey – Fees Special Report – July 2009)

• Investors are becoming more powerful in the manager/client relationship

• E.g. Core Macro Fund by Cantab Capital

• 0.5% Mgmt fee & 10% performance fee

OT

HE

RT

RE

ND

SA

ND

DE

VE

LOP

ME

NT

S

4) Other trends and developments

15

CompliancePlus Consulting

OT

HE

RT

RE

ND

SA

ND

DE

VE

LOP

ME

NT

S

4) Other trends and developments

16

Source: Preqin Hedge Fund Terms & Conditions Survey – Fees Special Report – July 2009

CompliancePlus Consulting

OT

HE

RT

RE

ND

SA

ND

DE

VE

LOP

ME

NT

S

4) Other trends and developments

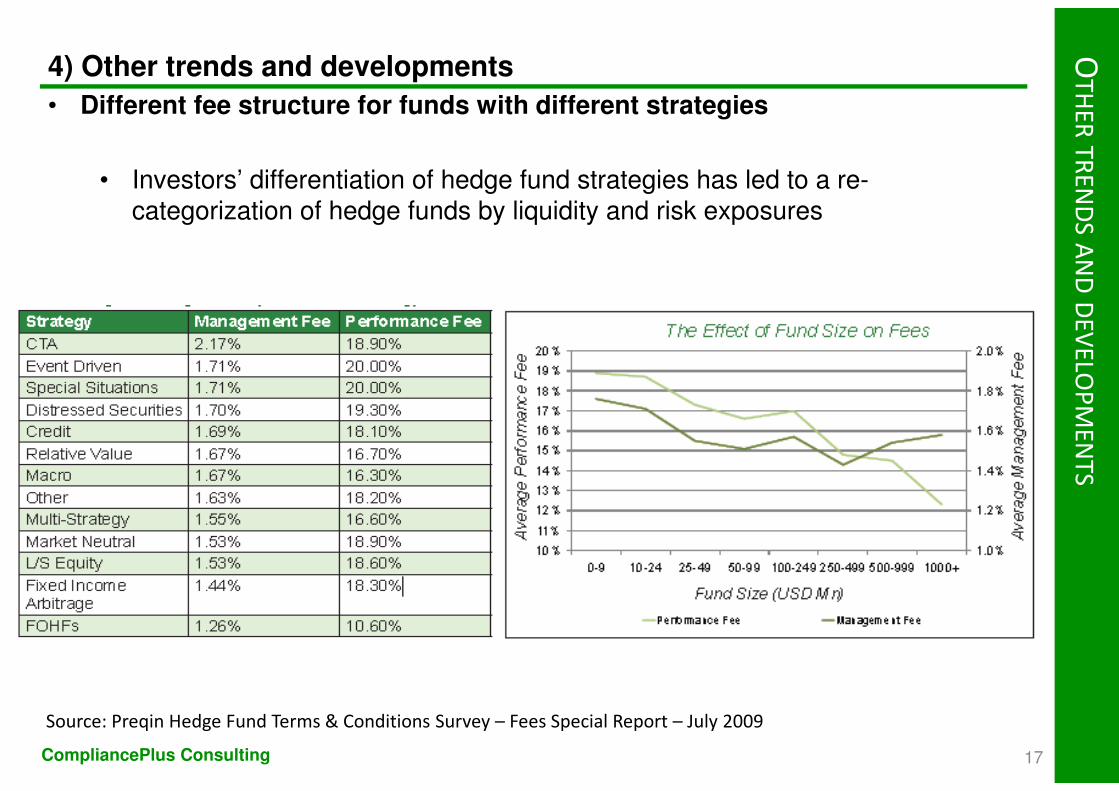

• Different fee structure for funds with different strategies

• Investors’ differentiation of hedge fund strategies has led to a re-categorization of hedge funds by liquidity and risk exposures

17

Source: Preqin Hedge Fund Terms & Conditions Survey – Fees Special Report – July 2009

CompliancePlus Consulting

OT

HE

RT

RE

ND

SA

ND

DE

VE

LOP

ME

NT

S

4) Other trends and developments

18

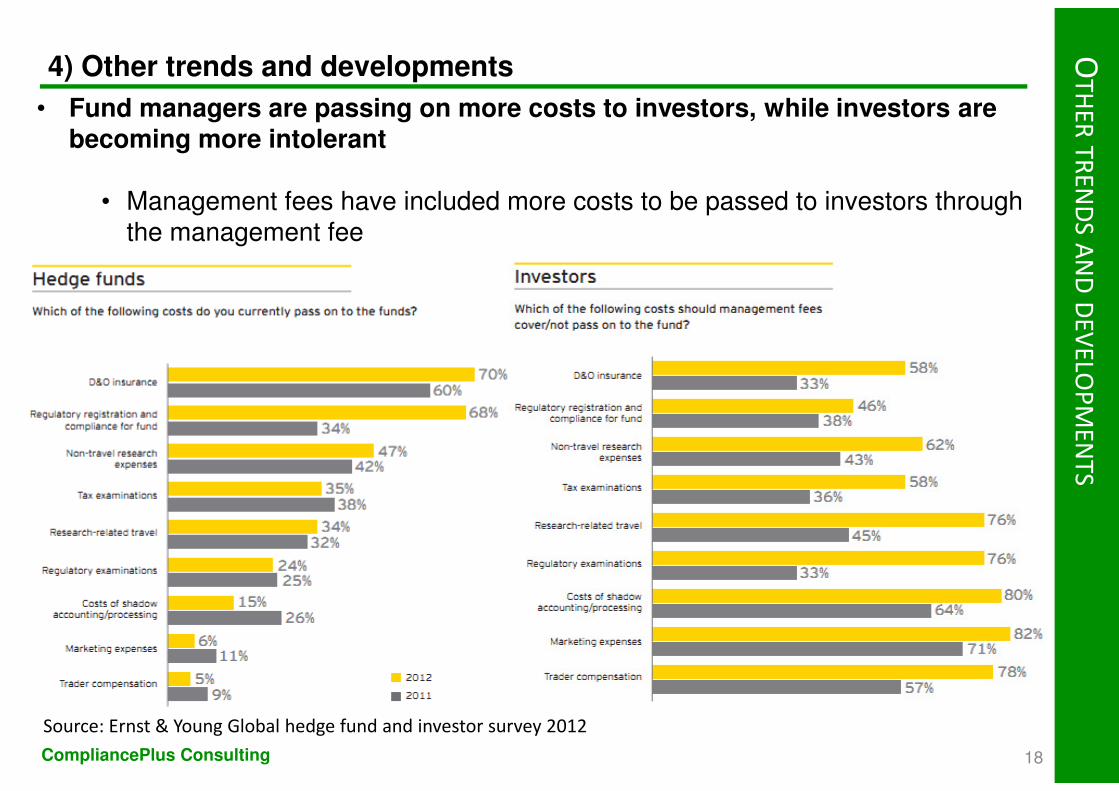

Source: Ernst & Young Global hedge fund and investor survey 2012

• Fund managers are passing on more costs to investors, while investors are becoming more intolerant

• Management fees have included more costs to be passed to investors through the management fee

CompliancePlus Consulting

OT

HE

RT

RE

ND

SA

ND

DE

VE

LOP

ME

NT

S

4) Other trends and developments

• Different fee structure for funds with different size

• Small funds tend to invest in niche strategies that are often more volatile, but with the potential for higher returns, so a higher fees is charged

• For fund with ultra-high size, there is a high demand due to the security they can offer through sheer scale and the returns they can delivered

• A separate third party

• Separation of custodian and administrator (who calculates the NAV) to avoid conflict of interest

• Multiple prime brokers to avoid risk of default

• A third party that can provide critical middle and back-office activities such as independent pricing and valuation, portfolio accounting, custody of non-collateral assets to avoid fraud

19

CompliancePlus Consulting

• Increase in the use of other fee structures/provisions e.g. clawback / rolling

• Investors are demanding better terms from managers after hedge funds worldwide lost an average of 19 percent last year

• With fund managers eager to retain clients in an environment where capital is scarce, investors have gained the upper hand

• Alternative fee structures tend to align investor’s investment goal with fund managers’ interests more

OT

HE

RT

RE

ND

SA

ND

DE

VE

LOP

ME

NT

S

4) Other trends and developments

20

CompliancePlus Consulting

About CompliancePlus

21Confidential

CompliancePlus Consulting specializes in compliance and regulatory requirements for licensed firms, licensed persons, fund management companies, hedge fund managers and all types of financial institutions in Asia.

Our team members have a proven track record of delivering practical and tested compliance solutions to our clients, with extensive industry experience in different areas and business divisions of the finance industry. Some of them have served as Senior Compliance personnel in major financial institutions with offices and operations across the Asia Pacific Region.

CompliancePlus brings the most comprehensive and value-added compliance services to our clients, enhancing their competitiveness in the finance industry.

This presentation is for information only and in no way constitute legal or other professional advice

Contact : Josephine Chung, Director, CompliancePlus ConsultingEmail : [email protected]: 852-3487 6903

Copyrights 2013 CompliancePlus Consulting Limited