Embed Size (px)

Citation preview

HEALTHCARE

KPJ HEALTHCARE BHD(KPJ MK, KPJH.KL) 9 April 2012

Back on an aggressive expansion mode

Company report BUY

Low Soo Fang

+603 2036 2292

(Initiation)

Rationale for report: Initiation coverage

Price RM5.14

Fair Value RM6.15

52-week High/Low RM5.17/RM3.84

Key Changes

Fair value Initiation

EPS Initiation

YE to Dec FY11 FY12F FY13F FY14F

Revenue (RMmil) 1,891.3 2,134.3 2,432.2 2,773.6

Core net profit (RMmil) 142.3 158.7 189.6 228.2

EPS (Sen) 26.1 29.1 34.7 41.8

EPS growth (%) 15.4 11.5 19.5 20.4

Consensus EPS (Sen) 25.9 29.0 35.8

DPS (Sen) 7.4 14.5 17.0 21.0

PE (x) 19.7 17.7 14.8 12.3

EV/EBITDA (x) 11.1 9.2 7.8 6.5

Div yield (%) 1.4 2.8 3.3 4.1

ROE (%) 17.2 17.4 18.8 20.1

Net Gearing (%) 17.9 11.9 8.5 net cash

Stock and Financial Data

Shares Outstanding (million) 546.1

Market Cap (RMmil) 2,807.1

Book value (RM/share) 1.62

P/BV (x) 3.2

ROE (%) 17.2

Net Gearing (%) 17.9

Major Shareholders Johor Corp (40.7%)

EPF (11.0%)

Free Float (%) 24.3

Avg Daily Value (RMmil) n/a

Price performance 3mth 6mth 12mth

Absolute (%) 19.4 9.2 31.0

Relative (%) 10.3 3.8 28.5

1,150

1,284

1,417

1,551

0.00

1.50

3.00

4.50

6.00

Apr-07

Oct-07

Apr-08

Oct-08

Apr-09

Oct-09

Apr-10

Oct-10

Apr-11

Oct-11

Index Points

(RM)

KPJ FBM KLCI

PP 12247/06/2012 (030106)

Investment Highlights

• We initiate coverage on KPJ Healthcare (KPJ) with a BUY

recommendation and a DCF-fair value of RM6.15/share, offering

potential returns of ~ 20%. We see further upside to the share price

in a likely sector-wide re-rating from the impending listing of regional

healthcare provider Integrated Healthcare Holdings (IHH) which have

acquired assets at 16x-26x PERs.

• As it is, KPJ’s current valuations are attractive. Fully-diluted PERs of

17x and 20x are at a 10%-13% discount to closest peer, Thailand-

based Bumrungrad Hospital, and a wider 23%-33% discount to

regional peers’ average.

• We like KPJ’s defensive earnings profile. Also, a step-up increase in

bed capacity via a pipeline of 7 new hospitals would accelerate

earnings momentum to achieve our conservative 3-year CAGR of

17%. Faster-than-expected patient admission growth, coupled with a

one-year hiatus from hospital expansion, has led to shrinking ready

capacity. Current occupancy rate of 70%-75% is a tad below

overcrowded thresholds of 85%-90%.

• With a sizeable 22% market share, KPJ is Malaysia’s largest private

healthcare provider with a national footprint and growing scale. It is

well placed to capitalise on the booming and lucrative health

tourism, with the doubling of the strategic existing hospital chain in

Johor – a focal area slated to become the primary destination for

medical tourists.

• Increased demand as spurred by recent regulatory changes on cross

border medical reimbursement between Malaysia and Singapore is

expected to power the segment’s contribution from 10% currently to

25% of group revenue by 2020F.

• KPJ also operates KPJ International University College of Nursing

and Health Sciences (KPJUIC) with annual revenues of RM40-

RM50mil. Despite minimal contribution to group earnings, the

education arm complements its hospital operations in that it serves

to mitigate staffing risks of qualified nurses and medical staff.

Management has earmarked a RM120mil capex for the Nilai branch

expansion and commissioning of a new campus at Bukit Mertajam. It

aims to quadruple student in-takes to 10,000 in 5 years’ time.

• The non-core operation in the retirement/aged care industry will

remain insignificant in the medium term. Nevertheless, we reckon

the ‘know-how’ attained via KPJ’s 51% stake in Australia-based Jeta

Gardens Waterford Trust would be beneficial for future potential

opportunities within the niche market.

• Net gearing is at a manageable level of 12%, aided by the group’s

asset-light model. Asset injections of hospitals into 49%-owned Al-

Aqar Healthcare REIT (AQAR Mk Equity, BUY) has enabled for better

deployment of free cash flows to fund future expansion, whilst

lending support to its dividend policy. We have assumed a dividend

payout of 50% p.a., in line with management guidance (yields: 3%-

4%).

KPJ Healthcare Bhd 9 April 2012

AmResearch Sdn Bhd 2

BACK ON AN AGGRESSIVE EXPANSION MODE

We initiate coverage on KPJ Healthcare (KPJ) with a

BUY recommendation and a fair value of RM6.15/share,

offering potential returns of ~20%.

We see further upside to the share price in a likely sector-

wide re-rating from the impending listing of regional

healthcare provider Integrated Healthcare Holdings (IHH)

which have acquired assets at 16x-26x PERs.

As it is, KPJ’s current valuations are attractive. Fully

diluted PERs of 17x and 20x are at a 10%-13% discount

to closest peer Thailand-based Bumrungrad Hospital,

and a wider 23%-33% discount to regional peers’

average.

STEP-UP INCREASE IN BED CAPACITY

� 7 new hospitals in the pipeline by end-FY15F

KPJ is an excellent play into Malaysia’s fast-growing

healthcare industry (YoY: 10%-13%), which is worth an

estimated RM25bil.

We like KPJ’s defensive earnings profile. Also, a step-up

increase in bed capacity from a pipeline of 7 new

hospitals would accelerate earnings momentum, to

achieve our conservative 3-year CAGR of 17%.

� Current occupancy rate a tad below overcrowded thresholds

Faster-than-expected patient admission growth, coupled

with a one-year hiatus from hospital expansion, has led to

shrinking ready capacity.

The current occupancy rate of 70%-75% is a tad below

overcrowded thresholds of 85%-90%. A small balance is

typically allocated for emergency cases.

The group recorded net profit of RM142mil for FY11,

representing a 20% YoY growth. Earnings track record

has been consistent, with an average of 15% growth per

annum (p.a.) over FY08-11 (See Chart 1).

� FY13F-14F to see strong earnings growth on step-up increase in capacity

We forecast an annual capex of RM200mil for the group’s

hospital expansion, with the construction of all 7 hospitals

to be completed by end-FY15F (See Table 1). Most

hospital expansion would be implemented in phases,

each typically comprising 90-100 beds.

Bandar Baru Klang Specialist, which was initially targeted

for opening late last year, is on schedule for operations

by 1HFY12F, with Phase I consisting of 94 beds. We

understand hospital inspection by the Ministry of Health

(MoH) would be finalised soon.

The group is also planning to open Sabah Medical Centre

to replace the old building in FY12F, with a total capacity

of 250 beds.

Part of the capex would be allocated for the

commissioning of KPJ Perlis Specialist Hospital. The

60:40 joint venture with Yayasan Islam Perlis will be

KPJ’s maiden hospital in Perlis. Expected completion

date is by early-FY14F.

That same year, KPJ will be adding a hospital in Tanjung

Lumpur, Pahang based on a 70:30 joint venture with

Pasdec Corporation. It has a target of 122 beds under

Phase I.

CHART 1 : QUARTERLY EARNINGS PERFORMANCE

Source: Company, AmResearch

KPJ Healthcare Bhd 9 April 2012

AmResearch Sdn Bhd 3

TABLE 1 : LIST OF KPJ HOSPITALS (MALAYSIA)

Hospitals State Number of licensed beds Remarks

1 KPJ Johor Specialist Johor 215

2 Kluang Utama Specialist Hospital Johor 40

3 Puteri Specialist Hospital Johor 150

4 Kedah Medical Centre Kedah 106

5 KPJ Perdana Specialist Kelantan 83

6 KPJ Seremben Specialist Negeri Sembilan 109

7 Kuantan Specialist Hospital Pahang 81

8 KPJ Penang Specialist Penang 136

9 Taiping Medical Centre Perak 48

10 KPJ Ipoh Perak 260

11 Damai Specialist Hospital Sabah 48

12 Sabah Medical Sabah 178

13 Kuching Specialist Sarawak 75

14 Sibu Specialist Sarawak 35

15 KPJ Ampang Puteri Selangor 230

16 KPJ Damansara Specialist Selangor 155

17 KPJ Selangor Specialist Selangor 180

18 KPJ Kajang Specialist Selangor 68

19 KPJ Tawakal Specialist Hospital W. Persekutuan 191

20 Sentosa Medical Centre W. Persekutuan 212

21 Bandar Baru Klang Specialist Selangor 200 Phase 1: 94 beds, MoH inspection expected to be completed in few weeks’ time.

22 Sabah Medical Centre Sabah 250 Phase 1: 80-100 beds, end-FY12F.

23 Pasir Gudang Johor 120 Phase 1: 60-90 beds, end-FY12F / early FY13F.

24 Muar Johor 120 FY13F

25 Tanjung Lumpur, Kuantan Pahang 200 Phase 1: 122 beds, FY14F.

26 KPJ Perlis Specialist Hospital Perlis 90 Phase 1: 60 beds, FY14F.

27 Bandar Dato' Onn, Iskandar Johor 400 End-FY14F / early FY15F.

Source: Company, AmResearch

KPJ Healthcare Bhd 9 April 2012

AmResearch Sdn Bhd 4

HEALTH TOURISM TO POWER KPJ’S NEXT LEG

OF GROWTH

� Largest private healthcare provider with 22% market share

With a sizeable 22% market share, KPJ is Malaysia’s

largest private healthcare provider with a national

footprint and growing scale (See Chart 2).

With its network of 20 hospitals in Malaysia, laboratory

services and a private nursing college under the KPJ

umbrella, the group is well ahead of competitors in scale,

service offerings and brand recognition – effectively

enhancing its pricing power. This is evident given the

gradual expansion in EBITDA margins over the last five

years.

CHART 2 : KPJ HAS DOMINANT MARKET SHARE(2009)

Source: APHM, AmResearch

� Investments in health tourism in line with government’s ETP policies

More importantly, KPJ is well placed to capitalise on the

booming and lucrative health tourism with the doubling of

the existing hospital chain in Johor.

� Rising demand from foreign patients to underpin health tourism’s robust growth

We see strong prospects for this fast-growing sub-

segment, which makes up 10% of the total healthcare

market. As an indication, health tourism recorded a

CAGR of 20% over the last five years.

We expect this segment to sustain its growth trajectory,

buoyed by increasing demand from foreign patients,

namely those from Indonesia and Singapore (See Table

2).

TABLE 2 : MEDICAL TOURISM REVENUE (2007)

Country 2007

Indonesia 72

Singapore 10

Japan 5

India 4

Europe 3

Others 6

100

Source: APHM, AmResearch

� Cross border medical reimbursement agreements bode well for operators in Johor

In particular, recently-sealed agreements between

Malaysia and Singapore on cross-border medical

reimbursement bode well for healthcare providers with

exposure to Johor.

Patients from Singapore represent the second largest

health tourist group after Indonesia. In addition, the

mainly non-elective nature of surgeries by most medical

tourists typically translate to higher average revenues per

patient, helping to mitigate some of the earnings risks.

� Cementing Johor presence by adding 3 more hospitals in the state

Part of KPJ’s hospital expansion plan will see three

additional hospitals strategically located within the state

neighbouring Singapore.

First on the list is a hospital in Pasir Gudang by end of

this year, followed by another one in Muar next year and

a larger-scale 400-bed hospital in Bandar Dato’ Onn,

Iskandar the following year.

All in, they are expected to more than doubled KPJ’s total

capacities to a total of 935 beds upon completion. This

would help boost group revenue contribution from health

tourism from circa 10% currently to 25% by 2020.

KPJ Healthcare Bhd 9 April 2012

AmResearch Sdn Bhd 5

INDUSTRY PROSPECTS

The operating environment is supportive of growth, with

private hospital services in Malaysia expected to hit

RM14bil by 2015. We underline two key factors

underpinning the industry’s robust growth outlook:-

1) Rising healthcare spending in tandem with

growing middle class and aging populace;

2) Healthcare being targeted for accelerated

development as part of the government’s long-term

economic transformation programme (ETP).

� Malaysia a dual healthcare system

Malaysia practises a dual healthcare system where public

healthcare is heavily subsidised, while the private

healthcare system is thriving but predominantly urban

focussed.

Individuals and households contribute 40% towards

healthcare expenditure, with the government contributing

the balance of 60%. All in, total healthcare expenditure

amounts to 5% of the nation’s GDP. In comparison,

healthcare expenditure by OECD countries average 9.6%

- indicating room for meaningful growth for Malaysia.

� Need to streamline industry to tackle nation’s rising healthcare demand

This has largely led to the inclusion of healthcare as part

of the government’s long term economic transformation

programme (ETP) as it seeks to streamline the industry

to tackle the nation’s rising healthcare needs.

� Aspires to achieve healthcare standards of a developed country by 2020

To match standards equivalent to other developed

countries, the doctor to population ratio of 1:859 (2010)

would need to rise to 1:600 by 2015, and to 1:400 by

2020, according to the Ministry of Health (MoH) (See

Table 3). This translates to total public and private health

expenditure of approximately 7% of GDP by 2020.

� Broader role of healthcare industry as engines of economic growth under ETP

More importantly, government policies under the ETP are

primarily aimed at transforming designated industries as

future engines of economic growth via public-private

partnerships. Already, it has identified 3 key areas for

growth within healthcare – pharmaceuticals, health travel

and medical technology products.

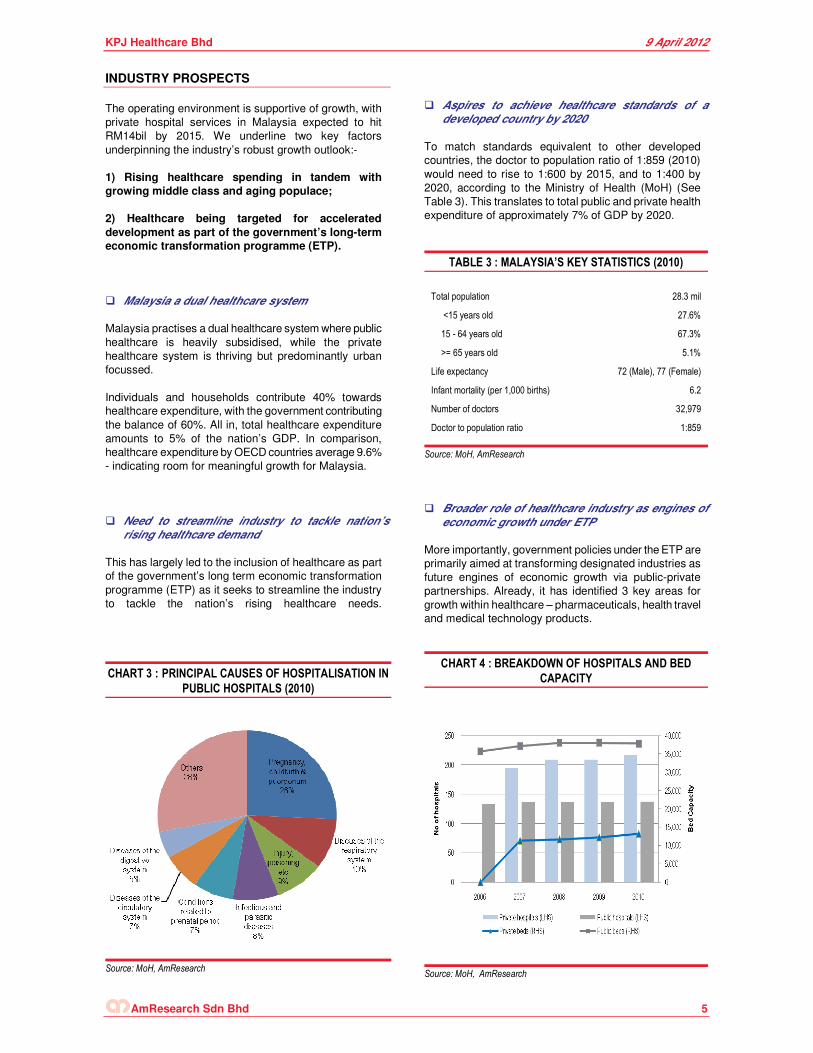

CHART 3 : PRINCIPAL CAUSES OF HOSPITALISATION IN

PUBLIC HOSPITALS (2010)

Source: MoH, AmResearch

TABLE 3 : MALAYSIA’S KEY STATISTICS (2010)

Total population 28.3 mil

<15 years old 27.6%

15 - 64 years old 67.3%

>= 65 years old 5.1%

Life expectancy 72 (Male), 77 (Female)

Infant mortality (per 1,000 births) 6.2

Number of doctors 32,979

Doctor to population ratio 1:859

Source: MoH, AmResearch

CHART 4 : BREAKDOWN OF HOSPITALS AND BED

CAPACITY

Source: MoH, AmResearch

KPJ Healthcare Bhd 9 April 2012

AmResearch Sdn Bhd 6

� Increased competition among healthcare providers will raise standards

Admittedly, we do anticipate increased competition among

healthcare providers, along with the rapid structural

developments taking place within the healthcare industry.

� Parkway-Pantai seen expanding aggressively

Coming close to industry leader KPJ is the Parkway-Pantai

group which operates the Pantai and Gleneagles hospitals.

Parkway-Pantai was privatised by Khazanah Nasional

(Khazanah) back in June 2010, and is now part of

Khazanah’s Integrated Healthcare Holdings (IHH).

Plans are underway for Parkway-Pantai to add five new

hospitals by end-2015, with the combined additional bed

capacities of 1,150 beds – some 15%-20% short of KPJ’s

(See Table 4).

Besides Parkway-Pantai, IHH controls Turkey-based

hospital chain Acibadem, Malaysian-based IMU Education

Group and an 11.2% equity stake in India-based Apollo

Hospitals Enterprises Ltd (APLH Bo Equity, Non-rated).

NON-CORE OPS: EDUCATION & RETIREMENT

VILLAGE

� In-house education arm mitigates staffing risks of nurses and qualified medical staff

KPJ also operates KPJ International University College of

Nursing and Health Sciences (KPJIUC) with annual

revenue of RM40-RM50mil.

Despite minimal contribution to group earnings, the

education arm complements its hospital operations in that

it serves to mitigate staffing risks of qualified nurses and

medical staff.

KPJUIC was awarded university college status in July

last year, and now offers its own degree programmes. It

hopes to attain a full university status, complete with its

own medical school, by 2016F.

Management has earmarked a RM120mil capex for the

Nilai main campus expansion and the commissioning of a

new campus at Bukit Mertajam, Penang.

The Penang campus is expected to commence

operations by end-FY12F. It aims to quadruple student

in-takes to 10,000 in five years’ time.

� Tapping into lucrative retirement/aged care industry in Australia

The non-core operation in the retirement/aged care

industry will remain insignificant in the medium term.

Nevertheless, we reckon the ‘know-how’ attained via

KPJ’s 51% stake in Australia-based Jeta Gardens

Waterford Trust (JGWT) would be beneficial for future

potential opportunities within the niche market.

JGWT has full ownership and operational control of a 64-

acre retirement village known as Jeta Gardens in

Waterford, Queensland – located approximately 45km

from Surfers Paradise, Gold Coast, Australia (See Chart

8).

Modelled as a full-fledged retirement village, Jeta

Gardens comprises a 108-bedded aged care facility, 23

retirement villas and 32 apartment units.

TABLE 4 : UPCOMING PRIVATE HOSPITALS

Location Capacity (beds) Opening target

Parkway-Pantai Gleneagles Kota Kinabalu Sabah 200 2014

Gleneagles Iskandar Johor 300 2015

Gleneagles KL (extension) KL 100 2014

Pantai Manjung Perak 100 2012

Pantai Bangsar (extension) Selangor 450 2014

Sime Darby Healthcare Sime Darby Medical Centre Parkcity Selangor 300 2013

Others Hang Tuah Jaya Resort Specialist Centre Melaka 390 2013

Melaka Straits Medical Centre Melaka 350 2014

Mahkota Medical Centre, Melaka (extension) Melaka 220 2014

Columbia Asia Hospital Petaling Jaya Selangor <90 2014

Thomson Medical Centre Pte Ltd n.a. 200 2015

Source: Various, AmResearch

KPJ Healthcare Bhd 9 April 2012

AmResearch Sdn Bhd 7

We understand plans are underway for development of

additional facilities on the remaining balance of vacant

land measuring 30-32 acres.

� Jeta Gardens a strategic target for KPJ’s medical tourism business

More importantly, we view the group’s venture in Jeta

Gardens positively given cross-selling potential of

medical tourism services.

We see scope for Jeta Gardens acting as first point of

contact in attracting local Australians to medical

treatments offered by KPJ-owned hospitals in Malaysia.

EARNINGS FORECASTS & FINANCIALS

� Decent patient volume growth of 10% p.a.

Our earnings model indicates a 3-year CAGR of 17%,

underpinned by new bed capacities from new hospital

openings.

We have assumed patient volume growth of 10% per

annum (p.a.). This is slightly higher than the group’s

historical average of 9%, but within the 7%-13% range

over the past years.

In addition, we have factored in a conservative 2%

increase in average revenues per patient.

We forecast a small 5% annual rise in average consultant

fees, largely in line with its historical increase of 6% p.a.

Management has been able to maintain its optimum

consultants to staff ratio of 1:10, ensuring an efficient cost

structure (See Chart 5).

Consultant fees and staff labour costs make up

approximately 49% of group operating expenses (See

Chart 6).

The other half is made up of material costs and hospital

administrative expenses. Overall, our earnings model

suggests a marginal improvement to EBITDA margin of

14%.

� Net gearing at manageable level of 12%, dividend payout of 50% p.a.

Net gearing is at a manageable level of 12%, aided by the

group’s asset-light model. Asset injections of hospitals into

49%-owned Al-Aqar Healthcare REIT (AQAR Mk Equity,

Buy) has enabled a better deployment of free cash flows

to fund future expansion, whilst lending support to its

dividend policy.

The group is in the midst of concluding REIT injection of

Bandar Baru Klang hospital worth RM85mil, to be satisfied

partly in cash and shares. Timeline for completion is at

end 1H2012.

The group may opt to distribute a special dividend in-

specie of Al-Aqar Healthcare REIT shares in order to

maintain its equity stake below the 50% level.

We have assumed a dividend payout of 50% p.a., in line

with management guidance. This translates to dividend

yields of 3%-4% p.a. based on the current share price.

Any special dividends would be an added bonus to

shareholders.

CHART 5 : EFFECTIVE MANAGEMENT OF LABOUR

COSTS

Source: Company, AmResearch

CHART 6 : BREAKDOWN OF GROUP OPERATING

EXPENSES

Source: Company, AmResearch

KPJ Healthcare Bhd 9 April 2012

AmResearch Sdn Bhd 8

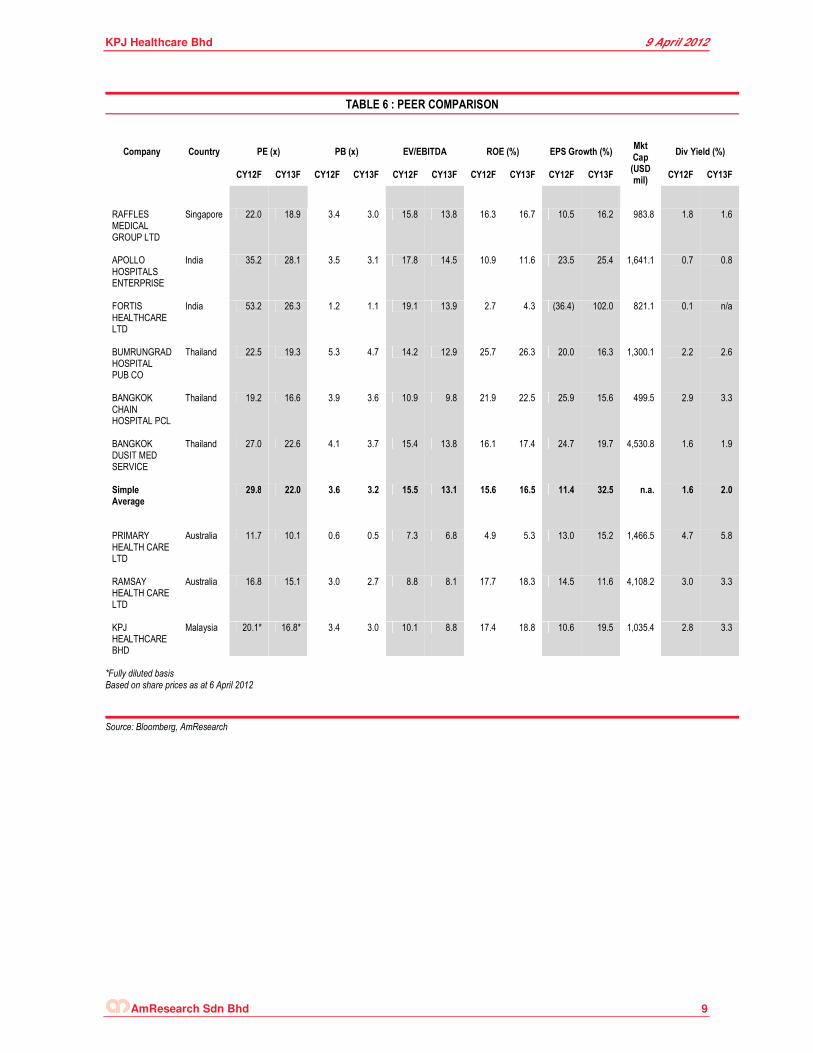

VALUATION & RECOMMENDATION

� Initiate with BUY, fair value of RM6.15/share

Despite the stock’s relative outperformance year-to-date,

we believe the current share price has not fully reflected

the stock’s potential value.

We initiate coverage on KPJ with a BUY recommendation

and a DCF-fair value of RM6.15/share, offering potential

returns of ~20%. We see further upside to the share price

in a likely sector wide re-rating from impending listing of

Khazanah’s IHH by year-end.

� IHH acquired healthcare assets at PERs of 16x-26x

Though no details are available at this juncture, various

news reports cited the fund-raising to be in excess of

USD3bil. Notwithstanding IHH’s larger scale and

earnings base, healthcare assets under IHH were

acquired at PERs of 16x-26x.

Further, KPJ’s valuation is undemanding in lieu of the

scarcity premium factor attached to quality healthcare

stocks. The stock’s fully diluted PERs of 17x and 20x are

at a 10%-13% discount to closest peer Thailand-based

Bumrungrad Hospital, and a wider 23%-33% discount to

regional peers’ average (See Table 6).

.

CHART 7 : GROUP EARNINGS PERFORMANCE

Source: Company, AmResearch

TABLE 5 : TOP 6 SHAREHOLDERS OF KPJ

Shareholder %

Johor Corp 38.6

EPF 11.9

Nomura Asset Management 8.2

Skim Amanah Saham Bumiputera 8.2

Kumpulan Waqaf An-nur Bhd 7.5

Lembaga Tabung Haji 4.6

Total 79.1

Source: Bloomberg, AmResearch

KPJ Healthcare Bhd 9 April 2012

AmResearch Sdn Bhd 9

TABLE 6 : PEER COMPARISON

Company Country PE (x) PB (x) EV/EBITDA ROE (%) EPS Growth (%) Mkt Cap

Div Yield (%)

CY12F CY13F CY12F CY13F CY12F CY13F CY12F CY13F CY12F CY13F

(USD mil)

CY12F CY13F

RAFFLES MEDICAL GROUP LTD

Singapore 22.0 18.9 3.4 3.0 15.8 13.8 16.3 16.7 10.5 16.2 983.8 1.8 1.6

APOLLO HOSPITALS ENTERPRISE

India 35.2 28.1 3.5 3.1 17.8 14.5 10.9 11.6 23.5 25.4 1,641.1 0.7 0.8

FORTIS HEALTHCARE LTD

India 53.2 26.3 1.2 1.1 19.1 13.9 2.7 4.3 (36.4) 102.0 821.1 0.1 n/a

BUMRUNGRAD HOSPITAL PUB CO

Thailand 22.5 19.3 5.3 4.7 14.2 12.9 25.7 26.3 20.0 16.3 1,300.1 2.2 2.6

BANGKOK CHAIN HOSPITAL PCL

Thailand 19.2 16.6 3.9 3.6 10.9 9.8 21.9 22.5 25.9 15.6 499.5 2.9 3.3

BANGKOK DUSIT MED SERVICE

Thailand 27.0 22.6 4.1 3.7 15.4 13.8 16.1 17.4 24.7 19.7 4,530.8 1.6 1.9

Simple Average

29.8 22.0 3.6 3.2 15.5 13.1 15.6 16.5 11.4 32.5 n.a. 1.6 2.0

PRIMARY HEALTH CARE LTD

Australia 11.7 10.1 0.6 0.5 7.3 6.8 4.9 5.3 13.0 15.2 1,466.5 4.7 5.8

RAMSAY HEALTH CARE LTD

Australia 16.8 15.1 3.0 2.7 8.8 8.1 17.7 18.3 14.5 11.6 4,108.2 3.0 3.3

KPJ HEALTHCARE BHD

Malaysia 20.1* 16.8* 3.4 3.0 10.1 8.8 17.4 18.8 10.6 19.5 1,035.4 2.8 3.3

*Fully diluted basis Based on share prices as at 6 April 2012

Source: Bloomberg, AmResearch

KPJ Healthcare Bhd 9 April 2012

AmResearch Sdn Bhd 10

CHART 8 : JETA GARDENS – 45KM FROM SURFERS PARADISE, GOLD COAST, AUSTRALIA

Source: Google map, AmResearch

KPJ Healthcare Bhd 9 April 2012

AmResearch Sdn Bhd 11

CHART 9 : PB BAND CHART

0.0

0.8

1.6

2.4

3.2

4.0

Nov-09

Feb-10

May-10

Aug-10

Nov-10

Feb-11

May-11

Aug-11

Nov-11

Feb-12

(x)

CHART 10 : PE BAND CHART

4.0

7.6

11.2

14.8

18.4

22.0

Nov-09

Feb-10

May-10

Aug-10

Nov-10

Feb-11

May-11

Aug-11

Nov-11

Feb-12

(x)

KPJ Healthcare Bhd 9 April 2012

AmResearch Sdn Bhd 12

TABLE 7 : FINANCIAL DATA

Income Statement (RMmil, YE 31 Dec) 2010 2011 2012F 2013F 2014F

Revenue 1,654.6 1,891.3 2,134.3 2,432.2 2,773.6

EBITDA 203.4 255.1 300.1 348.7 410.6

Depreciation (59.4) (71.2) (92.0) (103.9) (114.5)

Operating income (EBIT) 144.0 183.9 208.1 245 296.2

Other income & associates 30.4 25.1 25.6 28.4 31.8

Net interest (6.4) (6.4) (11.6) (11.0) (10.7)

Exceptional items 0.0 0.0 0.0 0.0 0.0

Pretax profit 168.0 202.6 222.1 262.1 317.3

Taxation (41.7) (47.4) (50.5) (59.6) (76.1)

Minorities/pref dividends (7.3) (12.9) (12.9) (12.9) (12.9)

Net profit 118.9 142.3 158.7 189.6 228.2

Core net profit 118.9 142.3 158.7 189.6 228.2

Balance Sheet (RMmil, YE 31 Dec) 2010 2011 2012F 2013F 2014F

Fixed assets 536.8 616.6 744.5 840.6 926.1

Intangible assets 136.3 165.6 165.6 165.6 165.6

Other long-term assets 457.4 449.0 422.0 422.8 423.6

Total non-current assets 1,130.5 1,231.2 1,332.1 1,429.0 1,515.3

Cash & equivalent 197.1 177.3 237.1 259.2 322.8

Stock 41.6 45.2 42.2 47.9 54.4

Trade debtors 298.4 300.8 311.6 353.9 401.4

Other current assets 12.3 10.5 0.0 0.0 0.0

Total current assets 549.5 533.9 590.9 661.1 778.6

Trade creditors 308.1 248.9 333.3 379.8 433.1

Short-term borrowings 362.7 118.8 110.6 105.6 103.0

Other current liabilities 54.1 72.9 112.2 135.0 155.0

Total current liabilities 724.9 440.5 556.1 620.5 691.2

Long-term borrowings 36.7 274.1 268.3 262.1 261.1

Other long-term liabilities 55.0 59.9 44.5 33.4 25.0

Total long-term liabilities 91.7 334.0 312.8 295.5 286.2

Shareholders’ funds 768.6 882.9 946.2 1,066.2 1,208.4

Minority interests 94.7 107.6 107.8 107.9 108.1

BV/share (RM) 1.46 1.62 1.73 1.95 2.21

Cash Flow (RMmil, YE 31 Dec) 2010 2011 2012F 2013F 2014F

Pretax profit 168.0 202.6 222.1 262.1 317.3

Depreciation 59.4 71.2 92.0 103.9 114.5

Net change in working capital 31.0 (48.7) 76.7 (1.6) (0.6)

Others (70.1) (72.6) (50.5) (59.6) (76.1)

Cash flow from operations 188.3 152.5 340.3 304.8 355.0

Capital expenditure (227.5) (171.0) (200.0) (200.0) (200.0)

Net investments & sale of fixed assets 0.0 0.0 0.0 0.0 0.0

Others 28.1 (1.9) (1.9) (1.9) (1.9)

Cash flow from investing (199.5) (172.8) (201.9) (201.9) (201.9)

Debt raised/(repaid) 30.6 (4.1) (14.0) (11.2) (3.5)

Equity raised/(repaid) 54.9 42.6 0.0 0.0 0.0

Dividends paid (26.5) (48.3) (59.4) (69.6) (86.0)

Others 0.0 10.6 0.0 0.0 0.0

Cash flow from financing 59.0 0.8 (73.4) (80.8) (89.6)

Net cash flow 47.8 (19.6) 65.1 22.1 63.6

Net cash/(debt) b/f 17.2 (15.5) 79.1 33.3 67.1

Net cash/(debt) c/f (202.3) (215.6) (141.8) (108.5) (41.4)

Key Ratios (YE 31 Dec) 2010 2011 2012F 2013F 2014F

Revenue growth (%) 13.6 14.3 12.8 14.0 14.0

EBITDA growth (%) 8.8 25.4 17.7 16.2 17.8

Pretax margins (%) 10.2 10.7 10.4 10.8 11.4

Net profit margins (%) 7.2 7.5 7.4 7.8 8.2

Interest cover (x) 10.6 10.8 17.9 22.3 27.8

Effective tax rate (%) 24.8 23.4 22.7 22.7 24.0

Net dividend payout (%) 49.8 28.0 37.4 36.7 37.7

Debtors turnover (days) 60 58 52 50 50

Stock turnover (days) 8 8 7 7 7

Creditors turnover (days) 63 54 50 54 53

Source: Company, AmResearch estimates

KPJ Healthcare Bhd 9 April 2012

AmResearch Sdn Bhd 13

Anchor point for disclaimer text box

Published by

AmResearch Sdn Bhd (335015-P) (A member of the AmInvestment Bank Group) 15 t h F l oo r B a ng un an A mB a n k Gr o u p 55 Jalan Raja Chulan 50200 Kuala Lumpur Tel: ( 03 ) 2 07 0- 2 4 4 4 ( r e sea rc h ) F a x: ( 03 ) 2 07 8- 3 1 6 2

Printed by

AmResearch Sdn Bhd (335015-P) (A member of the AmInvestment Bank Group) 15 t h F l oo r B a ng un an A mB a n k Gr o u p 55 Jalan Raja Chulan 50200 Kuala Lumpur Tel: ( 03 ) 2 07 0- 2 4 4 4 ( r e sea rc h ) F a x: ( 03 ) 2 07 8- 3 1 6 2

The information and opinions in this report were prepared by AmResearch Sdn Bhd. The investments discussed or recommended in this report may not be suitable for all investors. This report has been prepared for information purposes only and is not an offer to sell or a solicitation to buy any securities. The directors and employees of AmResearch Sdn Bhd may from time to time have a position in or with the securities mentioned herein. Members of the AmInvestment Group and their affiliates may provide services to any company and affiliates of such companies whose securities are mentioned herein. The information herein was obtained or derived from sources that we believe are reliable, but while all reasonable care has been taken to ensure that stated facts are accurate and opinions fair and reasonable, we do not represent that it is accurate or complete and it should not be relied upon as such. No liability can be accepted for any loss that may arise from the use of this report. All opinions and estimates included in this report constitute our judgement as of this date and are subject to change without notice.

For AmResearch Sdn Bhd

Benny Chew Managing Director