Embed Size (px)

Citation preview

Healthcare Enrollment Seminar

Presented by Debbie Fleck

Do you have Health Care Insurance?

IT’S THE LAW

2015 OPEN ENROLLMENT

November 15, 2014 to February 15, 2015

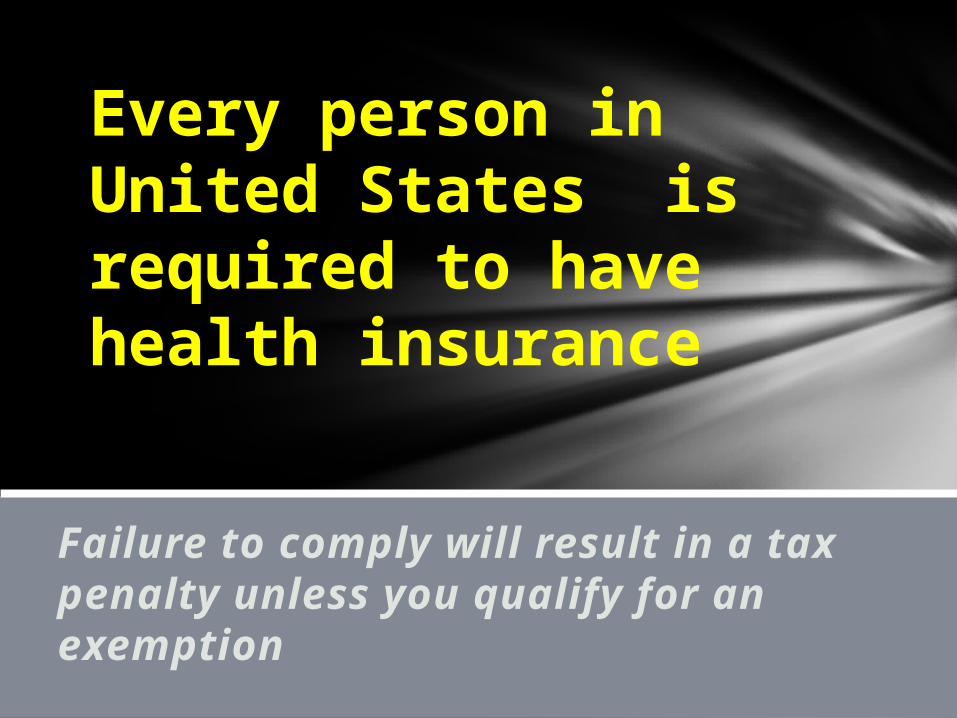

Failure to comply will result in a tax penalty unless you qualify for an exemption

Every person in United States is required to have health insurance beginning in 2014

You are uninsured for less than 3 mos of year

You have no tax filing requirement

You are incarcerated

You are not lawfully present in the US

You suffered a hardship

You do not have access to affordable coverage

You may qualify for an Exemption

You may be eligible for government subsidies to help you pay for your health insurance

1. Tax Credit

2. Cost Sharing

Two Types of Healthcare Subsidies

Tax Credit Subsidy

Government pays a part of your insurance premium based on your household income

Individuals with incomes under 400% of FPL may qualify for monthly tax credits

TAX CREDIT SUBSIDY

You can request your Tax Credit as an Advance Tax Credit so it can be used right away to lower your monthly premiums

Cost Sharing SubsidyDepending on Income the Government may subsidize a part of your deductible and out of pocket

Individuals with incomes under 250% of FPL may qualify for subsidized deductible and maximum out of pocket

Cost Sharing Subsidy

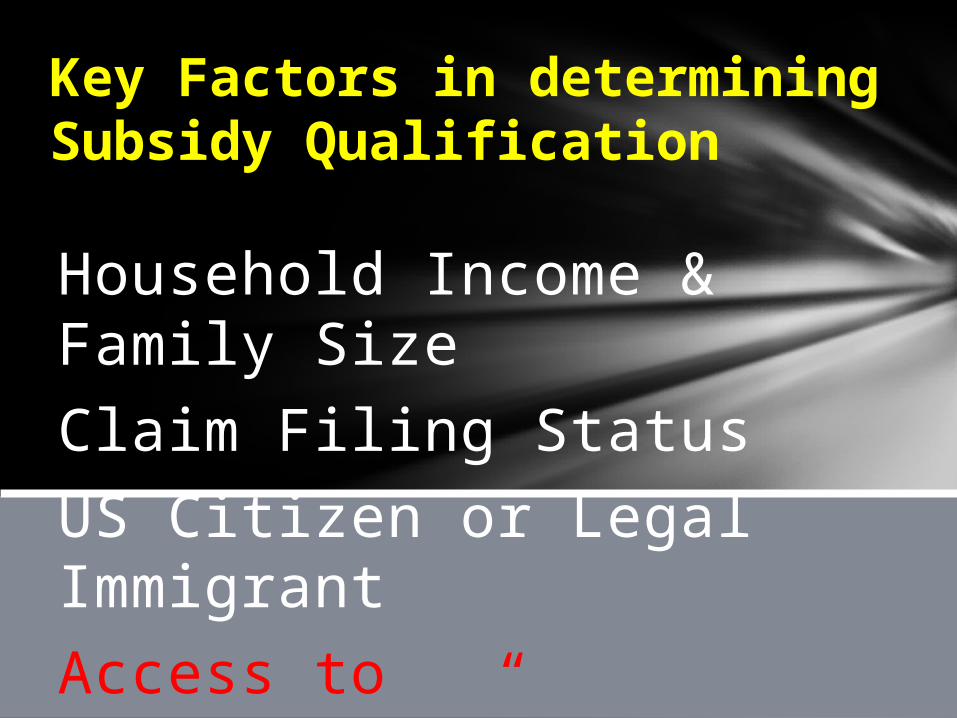

Household Income & Family Size

Claim Filing Status

US Citizen or Legal Immigrant

Access to “affordable” Employer-based Coverage or other coverage

Key Factors in determining Subsidy Qualification

If married at the end of 2015, you must file a joint income tax return with your Spouse

To Qualify for Subsidies

No one else will be able to claim you as a dependent on their 2015 tax return

You must file a federal income tax return in 2016 for the tax year 2015

If you have access to “affordable” employer-based coverage , you will not qualify for healthcare subsidies

Affordability Test in 2015

If the premium for the lowest cost plan for employee only coverage is less then 9.56% of household income, the coverage is considered affordable

“Mixed status” families can apply for a tax credit or cost sharing subsidies costs for dependent family members who have legal immigration status

If you do not have legal immigration status, you will not qualify for subsidies

1. Am I eligible to purchase group coverage through my employer? Is my family eligible?

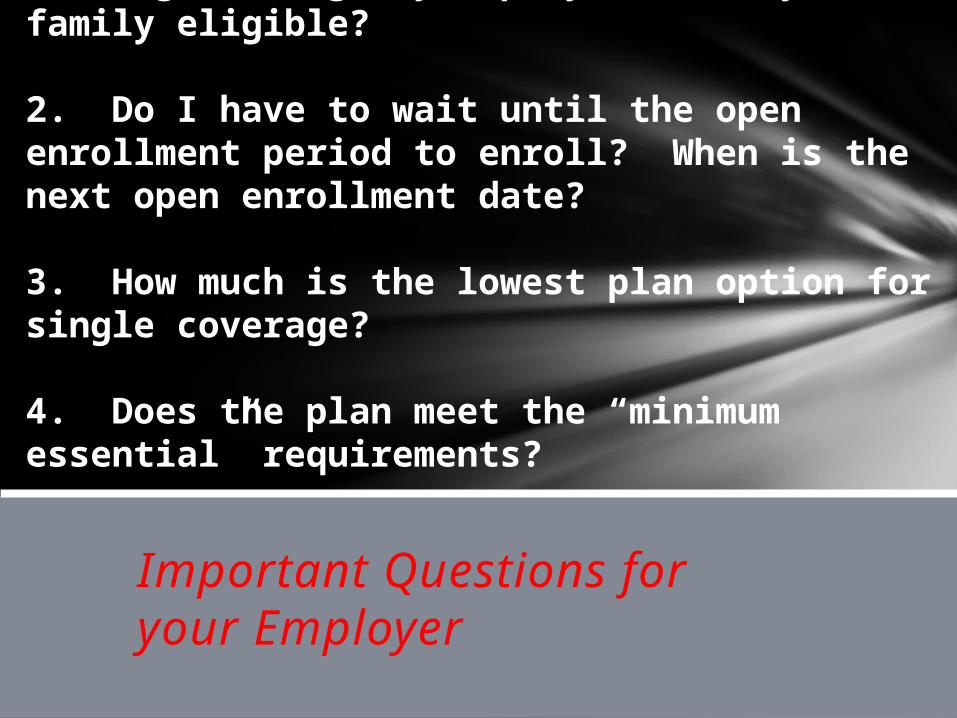

2. Do I have to wait until the open enrollment period to enroll? When is the next open enrollment date?

3. How much is the lowest plan option for single coverage?

4. Does the plan meet the “minimum essential” requirements?

Important Questions for your Employer

What are the Income Thresholds to Qualify for Healthcare Tax Credit Subsidy?

TAX CREDIT SUBSIDIES

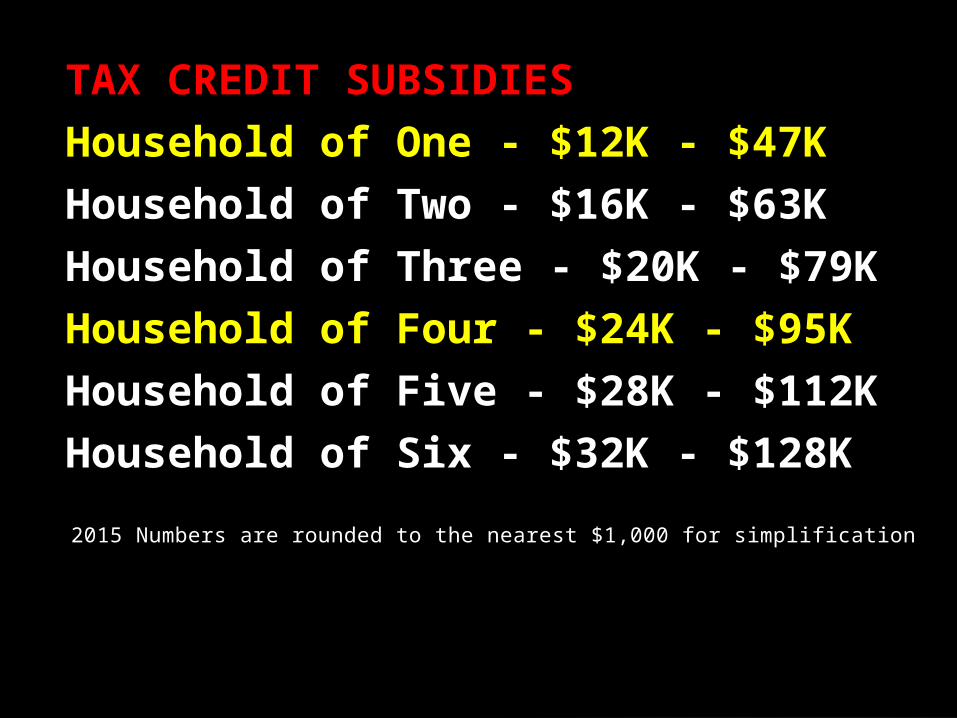

Household of One - $12K - $47K

Household of Two - $16K - $63K

Household of Three - $20K - $79K

Household of Four - $24K - $95K

Household of Five - $28K - $112K

Household of Six - $32K - $128K

2015 Numbers are rounded to the nearest $1,000 for simplification

What are the Income Thresholds to Qualify for the Cost Sharing Subsidy?

COST SHARING SUBSIDIES

Household of One - $12K - $29K

Household of Two - $16K - $39K

Household of Three - $20K - $49K

Household of Four - $24K - $60K

Household of Five - $28K - $70K

Household of Six - $32K - $80K

2015 Numbers are rounded to the nearest $1,000 for simplification

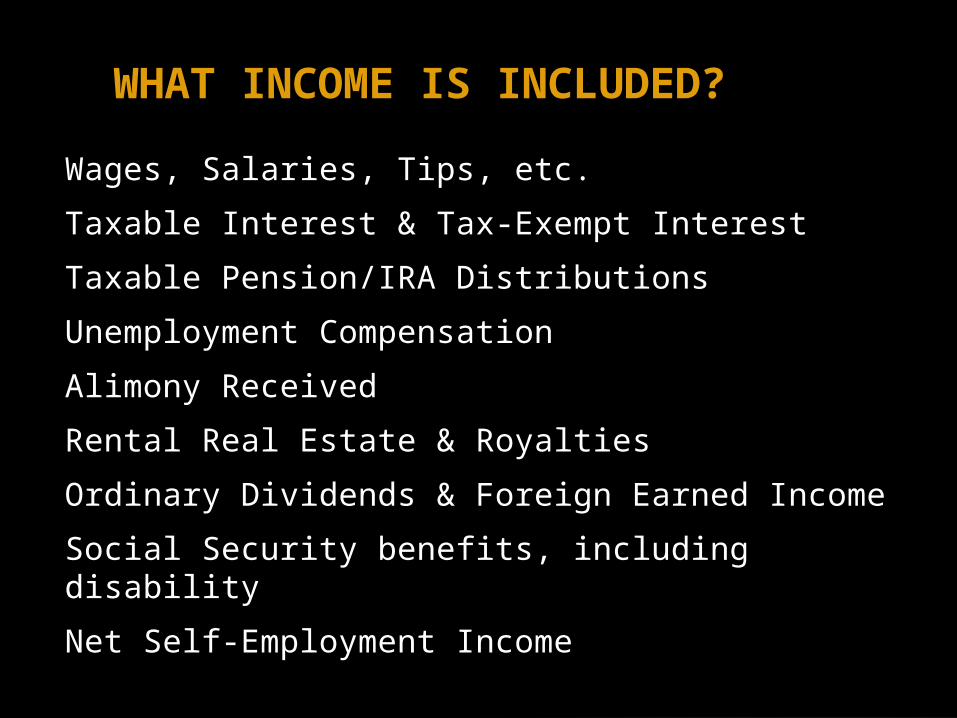

Wages, Salaries, Tips, etc.

Taxable Interest & Tax-Exempt Interest

Taxable Pension/IRA Distributions

Unemployment Compensation

Alimony Received

Rental Real Estate & Royalties

Ordinary Dividends & Foreign Earned Income

Social Security benefits, including disability

Net Self-Employment Income

WHAT INCOME IS INCLUDED?

Self-employed Business Expenses

IRA Deduction & H S A Contributions

Alimony Paid

Supplemental Security Income (SSI)

Veterans’ Disability & Worker’s Compensation

Tuition/Fees

Moving Expenses

Gifts

Child Support

DO NOT INCLUDE …

Worker Visa

Student Visa

Temporary Protected Status (TPS)

Lawful Temporary Resident

Asylum & Refugee

Registry Applicants

Order of Supervision

Lawful Permanent ResidentGREEN CARD

Eligible Immigration Examples

Green Card (1-551)

Reentry Permit (I-327)

Alien Number (I-94)

Notice of Action (I-797)

Temporary I-551 Stamp (I-94/I-94A)

Employment Authorization Cfard (I-766)

Refugee Travel Document (I-571)

Common Immigration Documentation

Tax Credit Subsidy is subject to Reconciliation up to Cap

Cost Sharing Subsidy is not subject to Reconciliation

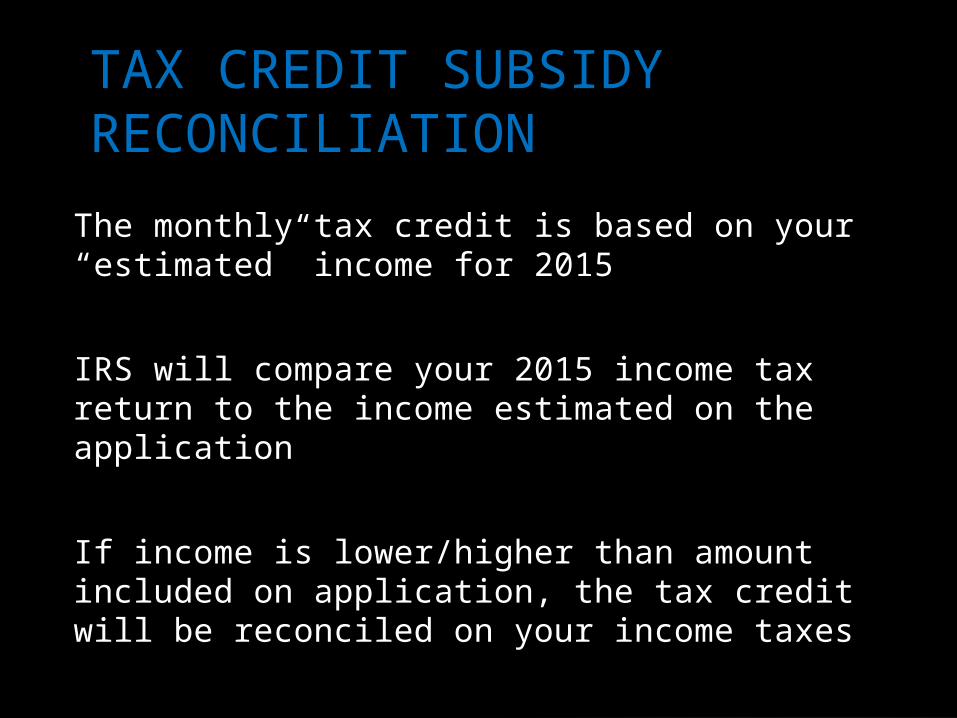

The monthly tax credit is based on your “estimated” income for 2015

IRS will compare your 2015 income tax return to the income estimated on the application

If income is lower/higher than amount included on application, the tax credit will be reconciled on your income taxes

TAX CREDIT SUBSIDY RECONCILIATION

Failure to comply will result in a tax penalty unless you qualify for an exemption

Every person in United States is required to have health insurance

Tax Penalty for Non-Compliance

Higher of:

Two (2) % of your yearly household income

$325 per person up to $975 per family $162.50 per child under 18

Name & Date of Birth

Social Security Number

Employer Name & Phone Number

Household Income

Immigration Documents (if not US citizen)

General Information (address, tax filing, etc.)

What information do I need for each member of my family?

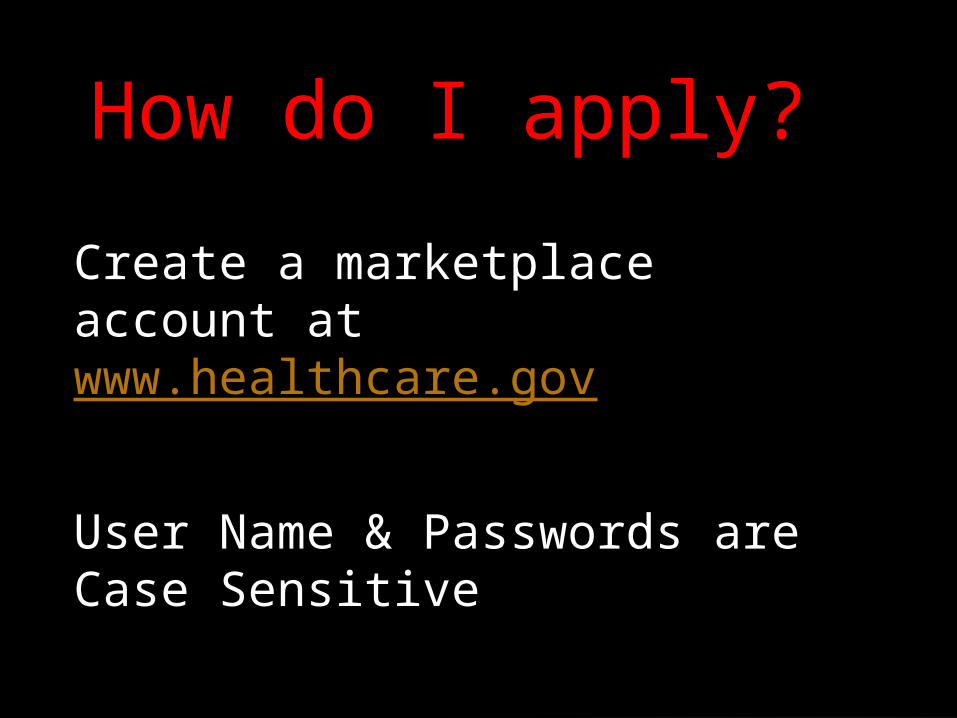

Create a marketplace account at www.healthcare.gov

User Name & Passwords are Case Sensitive

How do I apply?

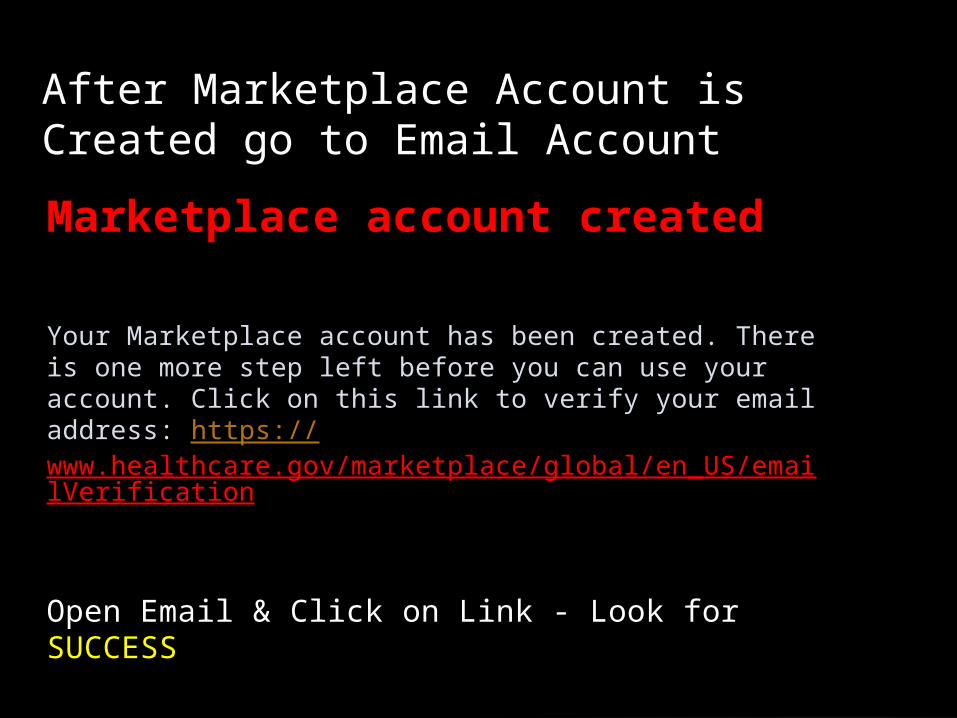

Marketplac e account created

Your Marketplace account has been created. There is one more step left before you can use your account. Click on this link to verify your email address: https://www.healthcare.gov/marketplace/global/en_US/emailVerification

Open Email & Click on Link - Look for SUCCESS

After Marketplace Account is Created go to Email Account

Verify your Identify

Complete your Marketplace Application

What are the Next Steps?

Select a Plan

You will need to pay your 1st Month’s Premium to Activate your Policy

FINAL STEP

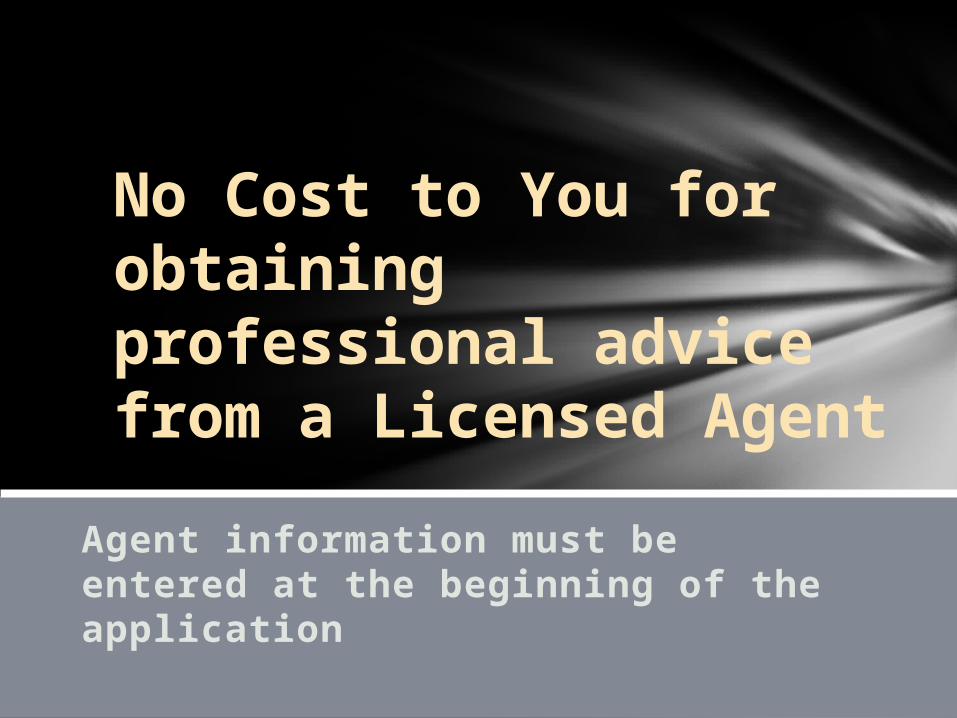

No Cost to You for obtaining professional advice from a Licensed Agent

Agent information must be entered at the beginning of the application

Navigators, Application Assisters, & Customer Service Representatives are not licensed agents and cannot provide professional advice on selecting a plan

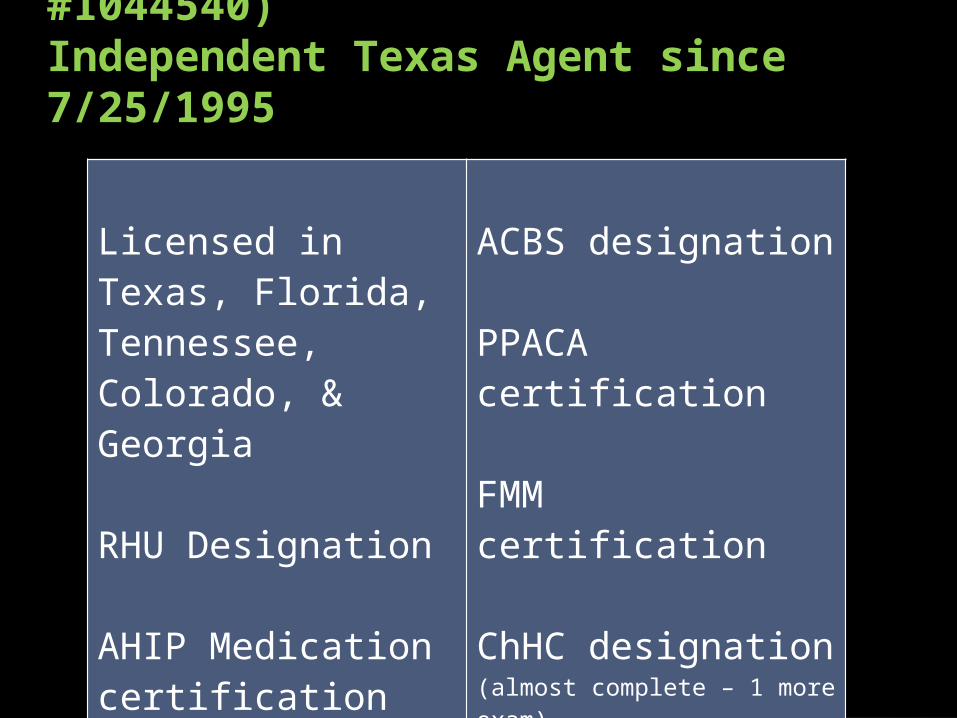

Debbie Fleck (License #1044540)Independent Texas Agent since 7/25/1995

Licensed in Texas, Florida, Tennessee, Colorado, & Georgia

RHU Designation

AHIP Medication certification

SgS designation

ACBS designation

PPACA certification

FMM certification

ChHC designation (almost complete – 1 more exam)

REBC designation (almost complete – 2 more courses)

Deborah Fleck

The Diamond Benefit

FFM User ID: FADKAL1044540

NPN #: 1019320

Debbie Fleck can assist with healthcare enrollment - Information must be included at beginning of application

No changes to your plan

until the next open

enrollment period

Pick your Plan Carefully

What is Your Budget?

PLATINUMGoldSilverBronze

Your options Depends on Your Budget

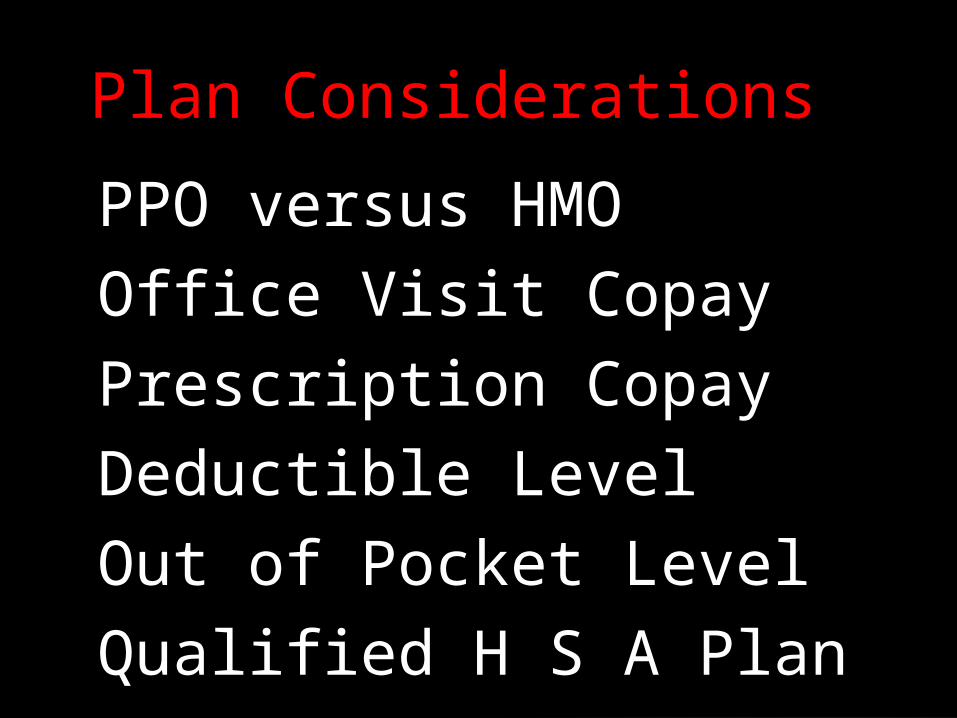

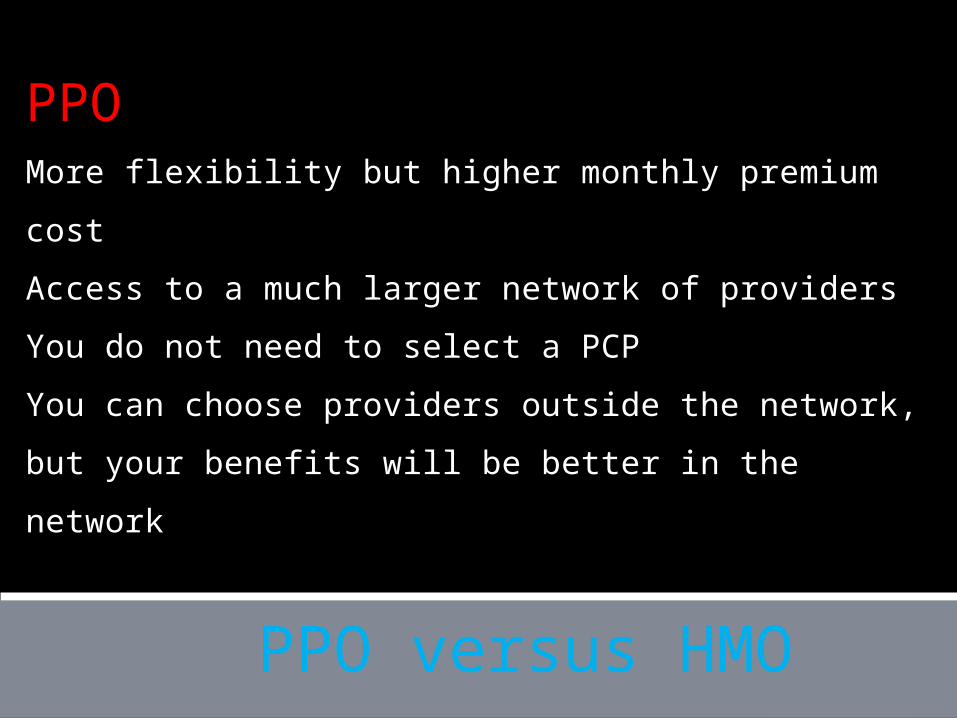

PPO versus HMOOffice Visit CopayPrescription CopayDeductible LevelOut of Pocket LevelQualified H S A Plan

Plan Considerations

PPO More flexibility but higher monthly premium

cost

Access to a much larger network of providers

You do not need to select a PCP

You can choose providers outside the network,

but your benefits will be better in the network

PPO versus HMO

HMO Less flexibility but lower monthly premium cost

Access to a smaller network of providers

You must select a primary care physician (PCP)

who will coordinate your care

You will need a PCP referral to see a specialist

You must obtain services from only HMO

providers

PPO versus HMO

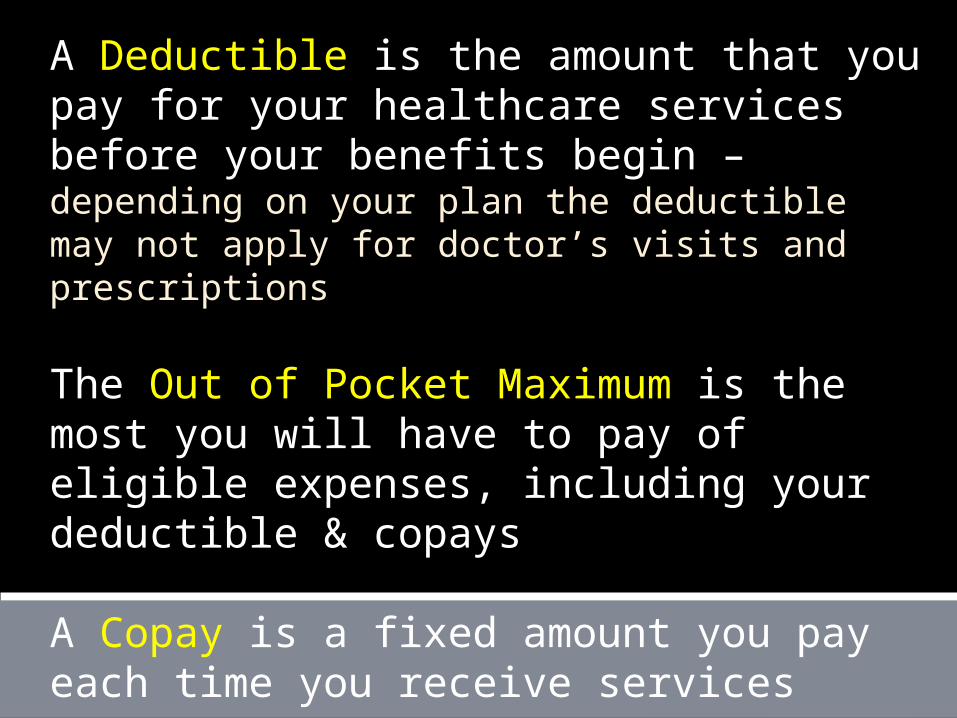

A Deductible is the amount that you pay for your healthcare services before your benefits begin – depending on your plan the deductible may not apply for doctor’s visits and prescriptions The Out of Pocket Maximum is the most you will have to pay of eligible expenses, including your deductible & copays

A Copay is a fixed amount you pay each time you receive services

All Plans Provide Preventative with No Cost Sharing (100%, No Deductible)

All Plans are Unlimited (No $ Limit) which provides protection for large medical bills

Some plans include Office Visit and Prescription Copays without having to meet the Deductible

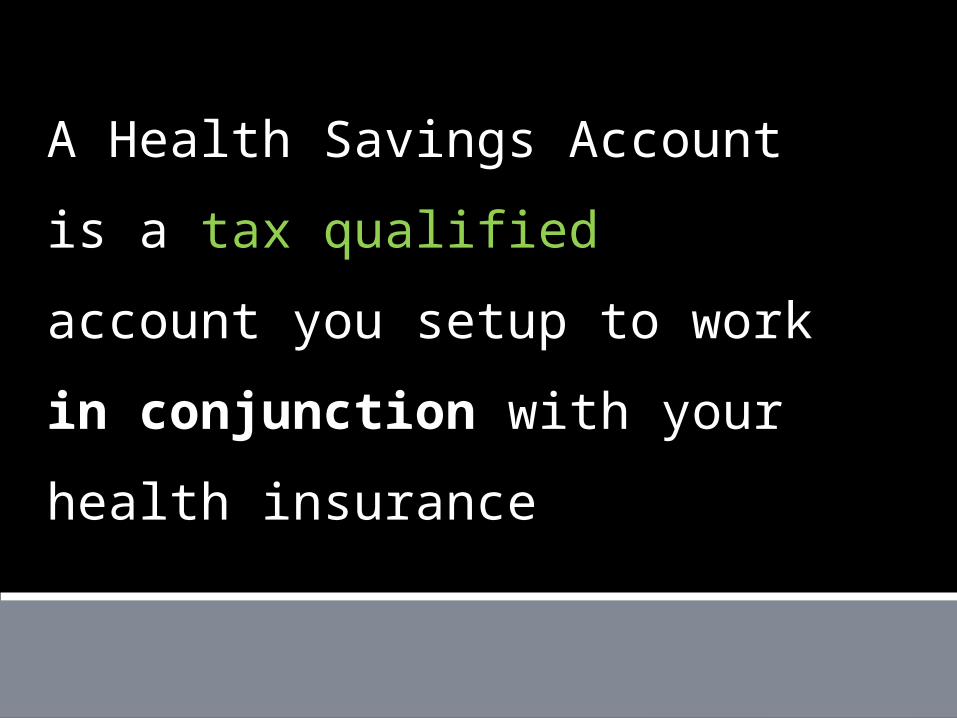

A Health Savings Account is

a tax qualified account you

setup to work in

conjunction with your

health insurance

Your HSA contributions can be used to pay the health insurance deductible and qualified medical expenses not covered by the health insurance, including dental and vision

You must be covered by a High Deductible Health Plan (HDHP) to qualify for an HSA

Health Savings Account (HSA)

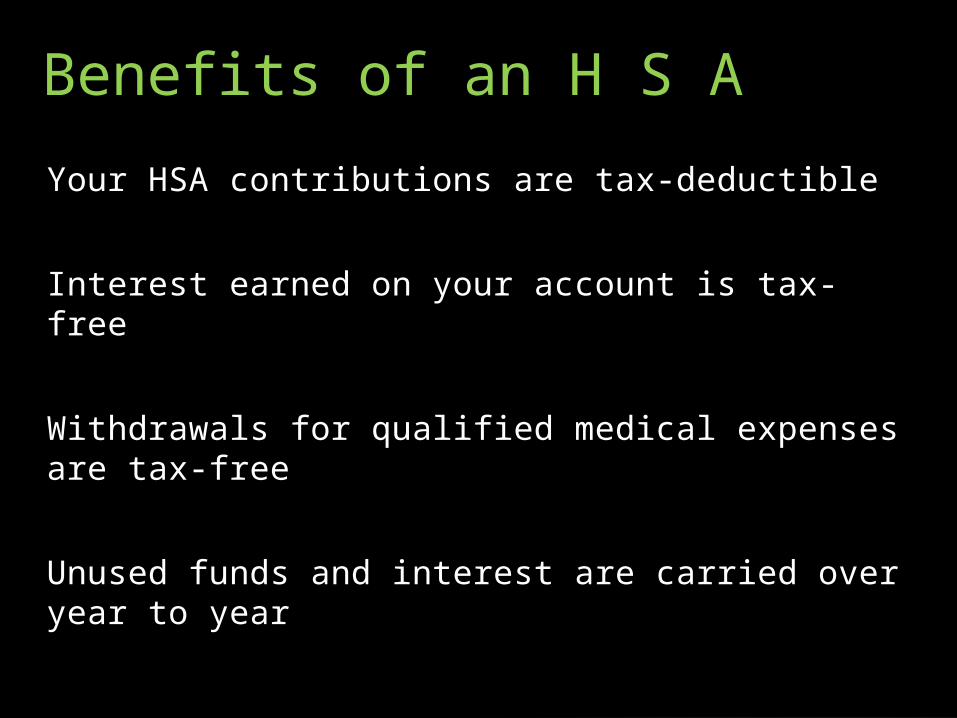

Your HSA contributions are tax-deductible

Interest earned on your account is tax-free

Withdrawals for qualified medical expenses are tax-free

Unused funds and interest are carried over year to year

Benefits of an H S A

Enrollment must be completed by the 15th of the preceeding month during open enrollment to go effective the next 1st of the month

Open EnrollmentNovember 15, 2014 to February 15, 2015

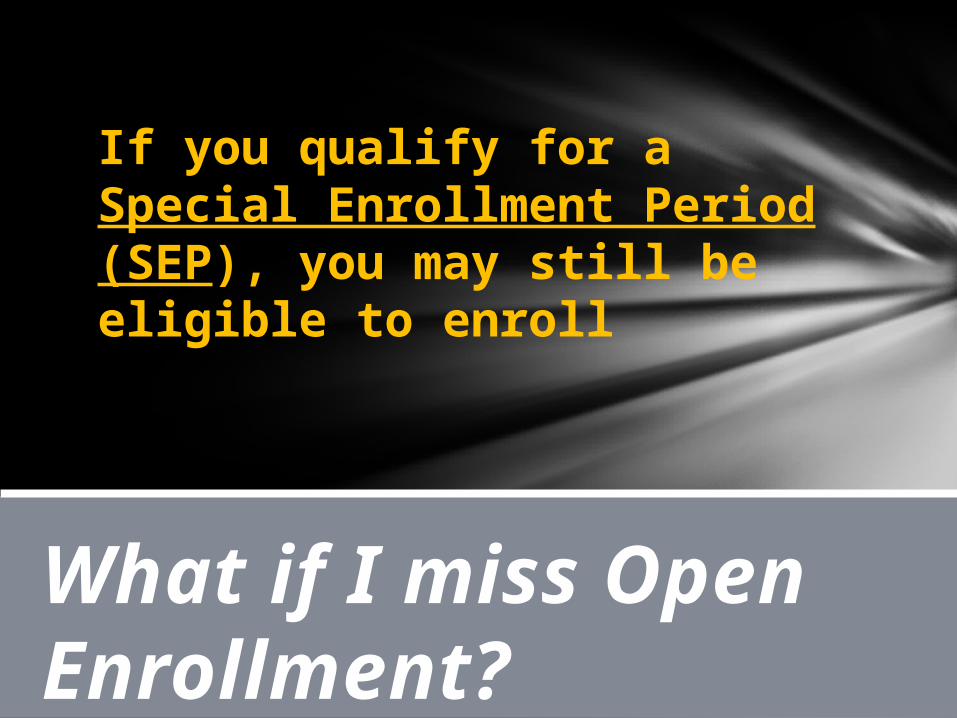

What if I miss Open Enrollment?

If you qualify for a Special Enrollment Period (SEP), you may still be eligible to enroll

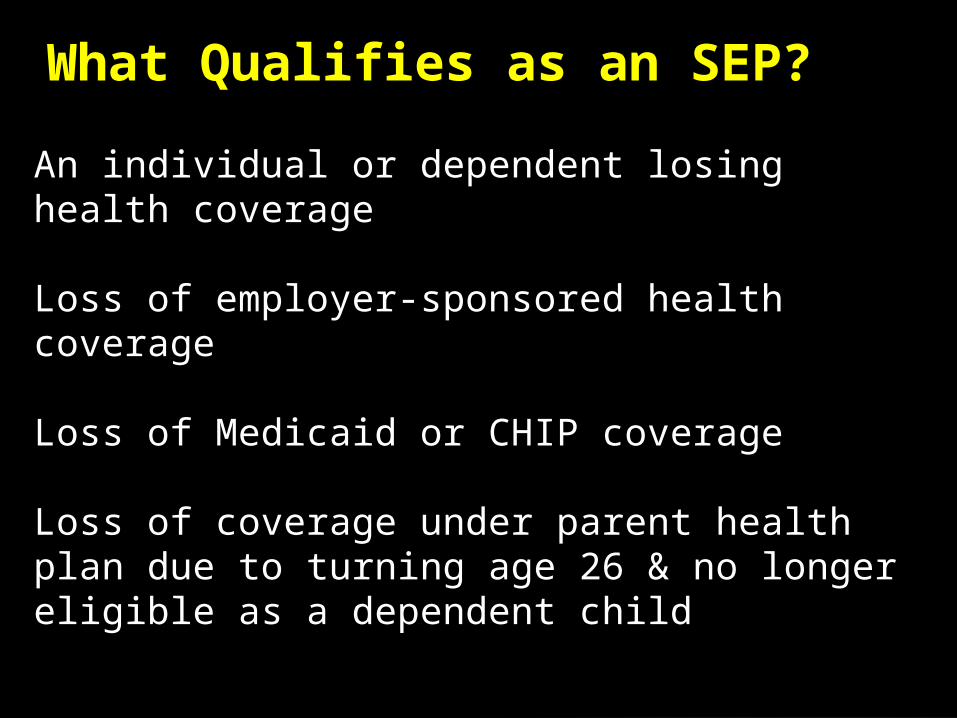

An individual or dependent losing health coverage

Loss of employer-sponsored health coverage

Loss of Medicaid or CHIP coverage

Loss of coverage under parent health plan due to turning age 26 & no longer eligible as a dependent child

What Qualifies as an SEP?

Loss of coverage resulting from Death or Divorce

Birth or Adoption of Child

Expiration of COBRA or short term medical plan

Release from incarceration

Other exceptional circumstances

What Qualifies as an SEP?

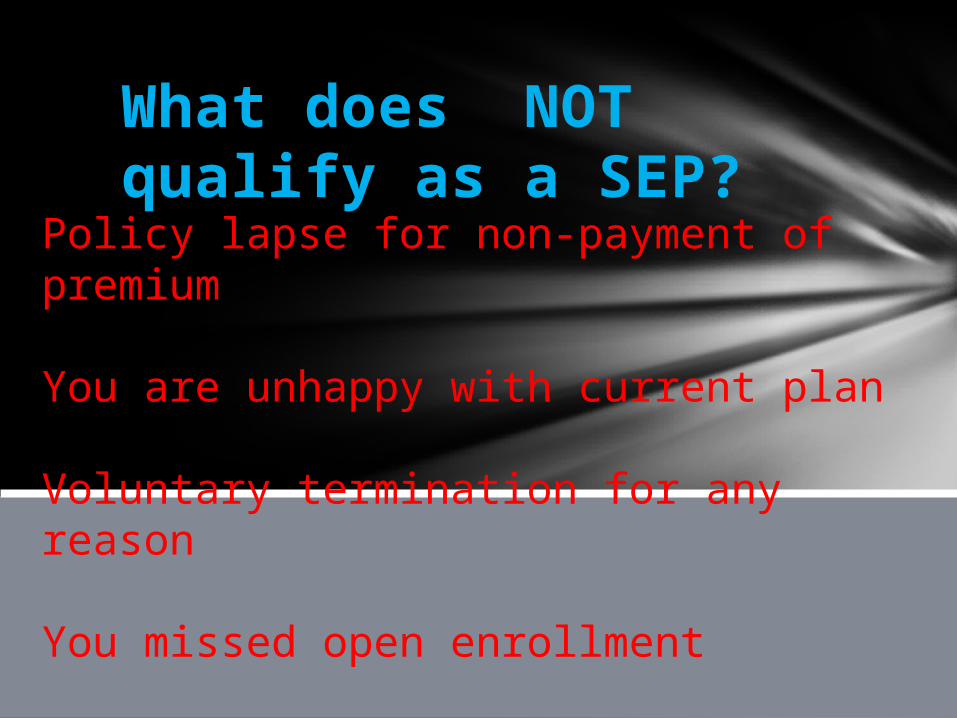

What does NOT qualify as a SEP?

Policy lapse for non-payment of premium

You are unhappy with current plan

Voluntary termination for any reason

You missed open enrollment

An individual or dependent losing health coverage

Loss of employer-sponsored health coverage

Loss of Medicaid or CHIP coverage

Loss of coverage under parent health plan due to turning age 26 & no longer eligible as a dependent child

What Qualifies as an SEP?

Loss of coverage resulting from Death or Divorce

Birth or Adoption of Child

Expiration of COBRA or short term medical plan

Release from incarceration

Other exceptional circumstances

What Qualifies as an SEP?

What does NOT qualify as a SEP?

Policy lapse for non-payment of premium

You are unhappy with current plan

Voluntary termination for any reason

You missed open enrollment

Resources

www.thediamondbenefitgroup.comwww.join.mewww.healthcare.gov