Embed Size (px)

Citation preview

IV

Copyright ©2016

NASSCOM 4E-Vandana Building (4th Floor) 11, Tolstoy Marg, Connaught Place New Delhi 110 001, India T +91 11 4151 9230; F +91 11 4151 9240 E [email protected] W www.nasscom.in

Published by NASSCOM, New Delhi

Disclaimer

The Report includes projections, forecasts and other predictive statements which are based on assumptions and expectations in the light of currently available information. These projections and forecasts are based on industry trends, circumstances and factors which involve risks, variables and uncertainties. NASSCOM disclaims all warranties as to the accuracy, completeness or adequacy of such information. NASSCOM and/or its Affiliates and its officers, directors and employees including the analysts/authors/advisors shall not be in any way responsible for any direct, indirect, special or consequential damages that may arise to any person from any inadvertent error in the information or judgement or opinion contained in the report nor do they take guarantee or assume liability for any omissions of the information contained therein. The projections and forecasts described in this report should be evaluated keeping in mind the fact that these are not scientifically proven to guarantee certain intended results and are not published as a warranty and do not carry any evidentiary value. Opinions expressed therein are current opinion as of the date appearing on the report only. Data may be subject to update and correction without notice.

Every effort has been made to trace the owners of the copyright material included in this Report. The material in this publication is copyrighted. Reproduction or dissemination, directly or indirectly, either on paper or on electronic media, of the research data and report in any form is prohibited except with the written permission of NASSCOM. The user should consult their own advisors before making use of any information or data contained in the report.

The publishers would be grateful for any omissions brought to their notice for acknowledgement in future editions of the book.

Analysis of Talent Demand and Supply V

ForewordThe Indian IT-BPM story has demonstrated disruptive potential across the globe over the last three decades. It is India’s largest and most diverse private sector employer, estimated to account for revenues of approximately USD 160 billion in FY2016, with a direct workforce nearing 3.7 million and effecting over 10 million indirect jobs.

Today, yet again, it is set to play an integral role in ushering in a new paradigm. NASSCOM’s ‘Perspective 2025’ Report focuses on to a new force: the changing role of digital technology. The needle has shifted towards automation, e-commerce, start-up ecosystem building, which combined with the impact of policy mandates such as Digital India, Smart Cities and Skill India sets the national agenda on a trajectory to realize the vast potential of digital technologies.

At this juncture, it is crucial that the national program incorporates a commitment to sustainably developing a skilled and job-ready workforce at par with global standards. IT-ITeS Sector Skills Council NASSCOM (SSC NASSCOM) has been entrusted with the responsibility to identify and facilitate the building of required capacity. A key function of the SSC NASSCOM is therefore to focus on bridging the employability gaps within the industry.

This report is an analysis of the talent demand and supply in IT-BPM industry, and an exploration of the forces that currently shape the ecosystem. The research effort comprises quantitative and qualitative analyses of aggregate economic data and trends, and also lays down expectations for the next three to five year period. Effectively, the report is designed to engage all stakeholders in the endeavour to establish and nurture a standards-based employment ecosystem.

We remain deeply committed to the mission of growth in the industry, and hope this report will prove to be a meaningful addition to your own efforts.

R ChandrashekarPresident, NASSCOM

VI

Analysis of Talent Demand and Supply VII

AcknowledgementsWe are grateful to Dr. BVR Mohan Reddy, Chairman, IT-ITeS Sector Skills Council NASSCOM, and Founder & Executive Chairman, Cyient Ltd., and Mr. R Chandrashekhar, President, NASSCOM for their strategic leadership and support towards this key report.

Special gratitude to the concerned officials and leadership at the Ministry of Skill Development and Entrepreneurship (MSDE), the Ministry of Communications and Information Technology (MCIT), the Ministry of Labour and Employment (MoLE), the Prime Minister's Office (PMO), and the National Skills Development Corporation (NSDC), each having supported this endeavour by providing relevant information and insights that have enhanced the report.

Our heartfelt thanks to NASSCOM members and the educational institutes for their contribution towards quantitative and qualitative perspectives, both of which have been critical to this effort.

We extend our thanks to the members of the Project Board, Mr. Anil Menon at CMS, Mr. Arjun Raghunathan at HCL Technologies, Mr. Sameer Kohli at CSC, Mr. Srikantan Moorthy at Infosys, and Mr. Vidyut Navelkar at TCS.

We are also grateful for the complementary support and insights provided by the NASSCOM Research team, including Sangeeta Gupta, Achyuta Ghosh, Diksha Nerurkar and Nirmala Balakrishnan.

We thank the Deloitte Project team consisting of Mr. Anindya Mallick, Mr. Mohammed Shariff, Mr. Arvind B., Mr. S Badrinarayanan and Ms. Neha Yadav for conducting the research and putting this report together.

VIII

Analysis of Talent Demand and Supply IX

ContentsForeword III

Acknowledgements V

Executive Summary 1

Approach and Methodology 5

Analysis of the IT-BPM industry 8 Trends in Global IT sector spends 8 India’s rising share of global IT-BPM spend 9 Overview of Indian IT industry 10 Performance within the IT-BPM industry 11 Key forces of disruption 12 Investment Scenario in the IT Industry 18 Shifting focus of delivery locations 19 Key Takeaways 20

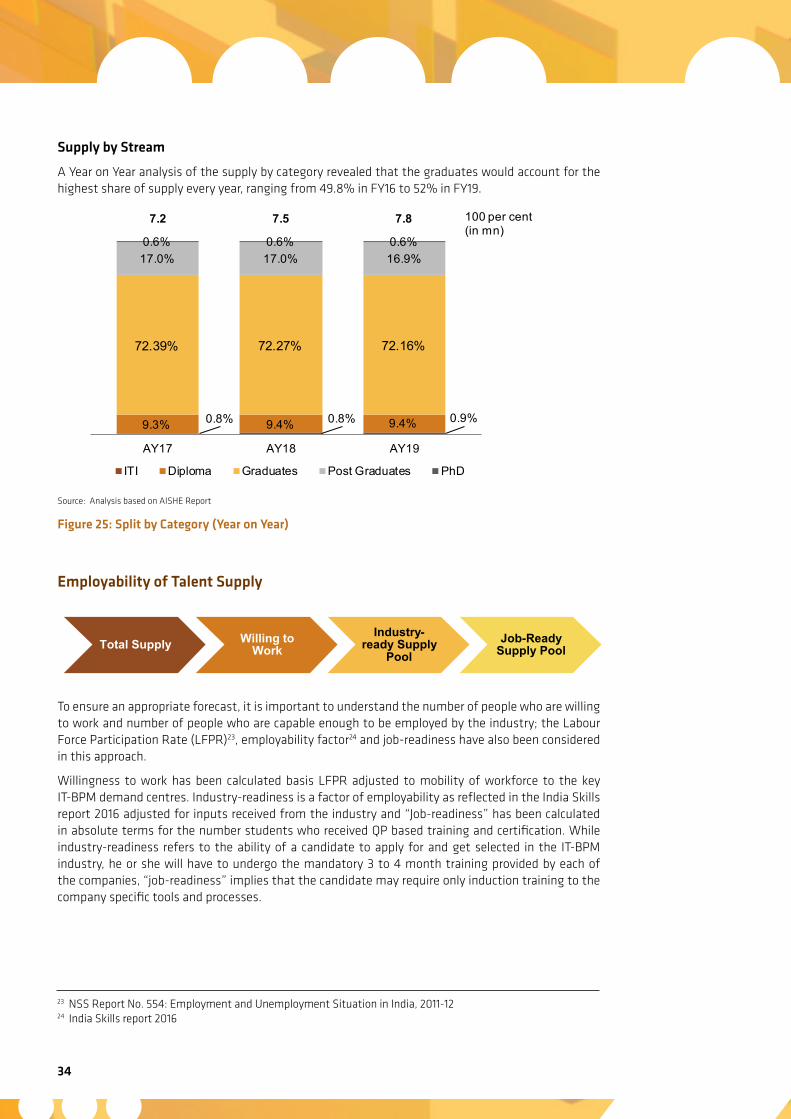

Analysis of Demand for Talent 21 Overview of Indian IT Industry 21 Indian IT Industry Revenue projections - 2015 to 2019 21 Industry employment projections - 2015 to 2019 22 Employment and Hiring by IT Sub-sector 23 Employment and Hiring in IT-BPM by region 23 The skilling imperative to the disruptions expected 24 High Demand Occupations and New age Skills 25 Key Takeaways 27

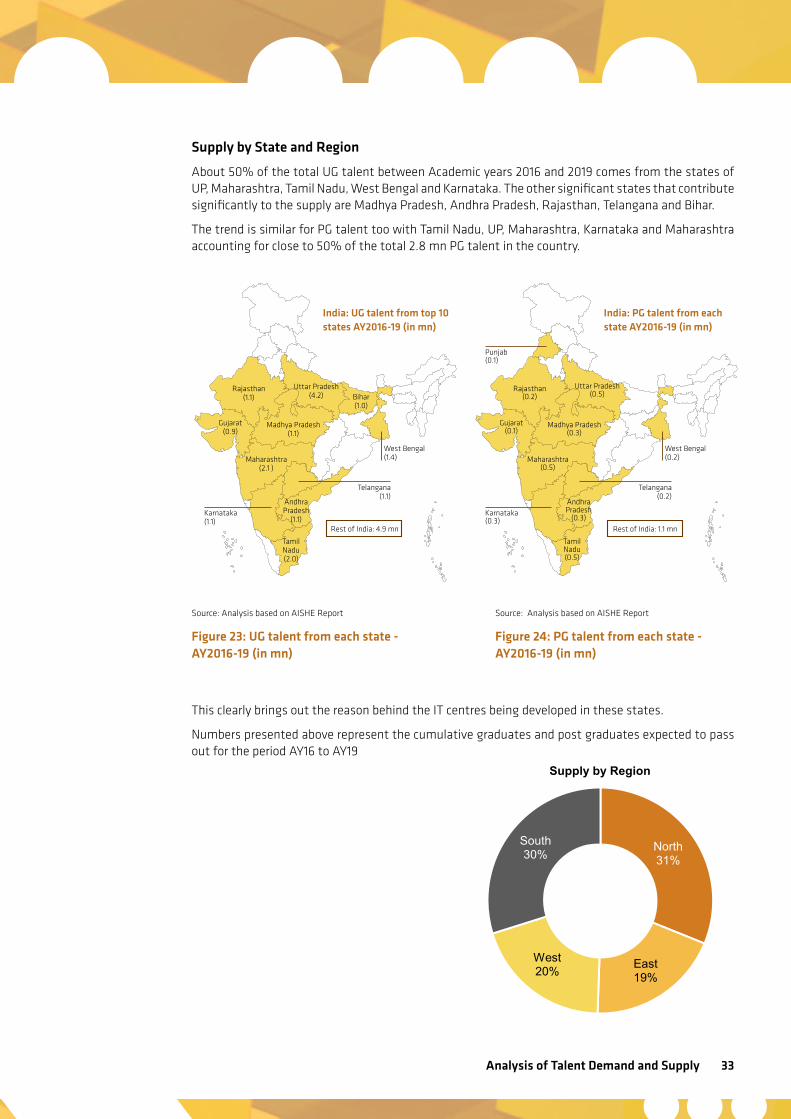

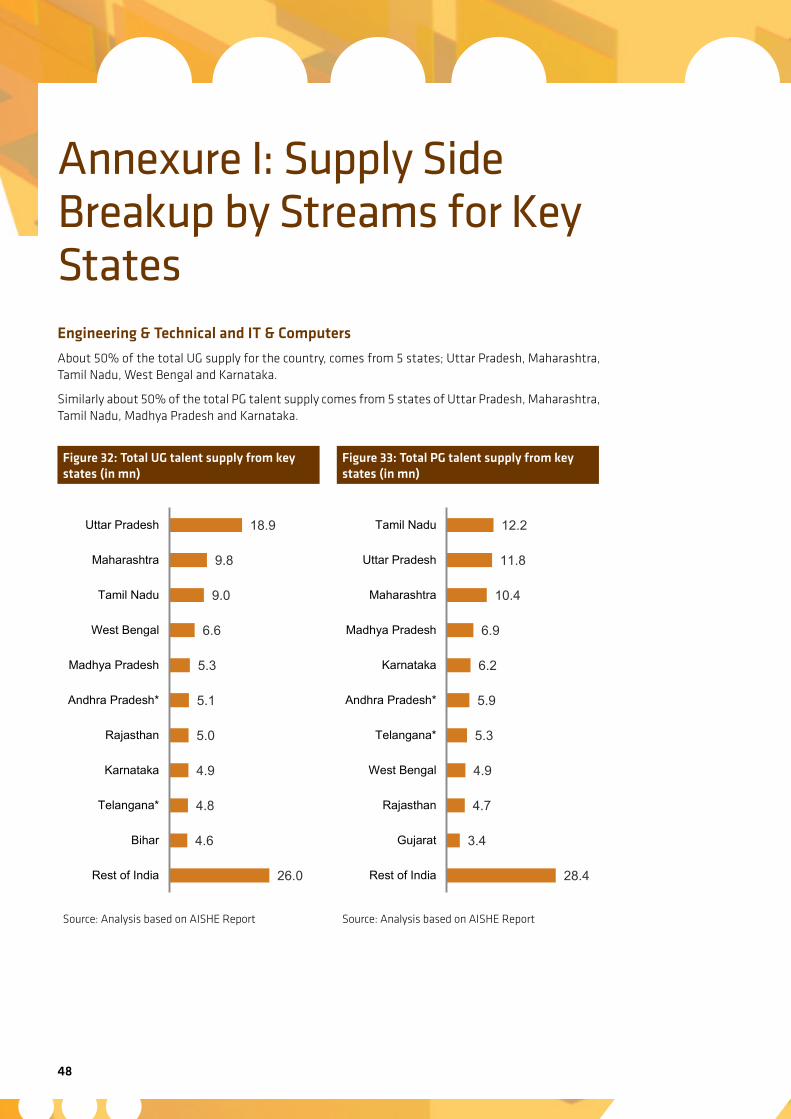

Analysis of Supply of Talent 28 Overview of the National Talent Supply 28 Overview of Total Supply to the IT-BPM Industry 32 Supply by State and Region 33 Supply by Stream 34 Employability of Talent Supply 34 Overview of skilling ecosystem 35 Role of SSC NASSCOM in the Skilling Ecosystem 36 Certification Landscape 36 Academic Perspective of Skilling Ecosystem 37 Role of Industry in Skill Development through CSR funds 37 Key Takeaways 38

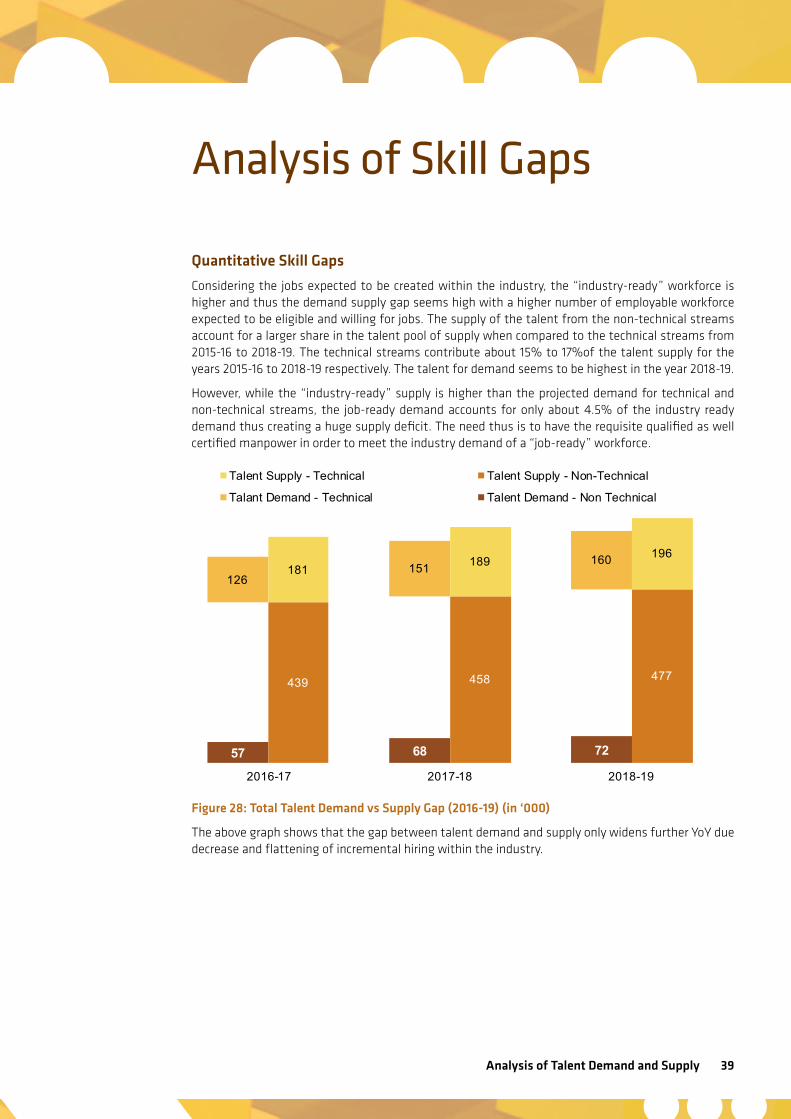

Analysis of Skill Gaps 39 Quantitative Skill Gaps 39 Incremental Employment Demand- Supply Analysis by State and Region 40

The Way Forward 43

ANNEXURES 47 Annexure I: Supply Side Breakup by Streams for Key States 48 Annexure II: List of Figures 56 Annexure III: List of Tables 58 Annexure IV: Bibliography 59

Analysis of Talent Demand and Supply 1

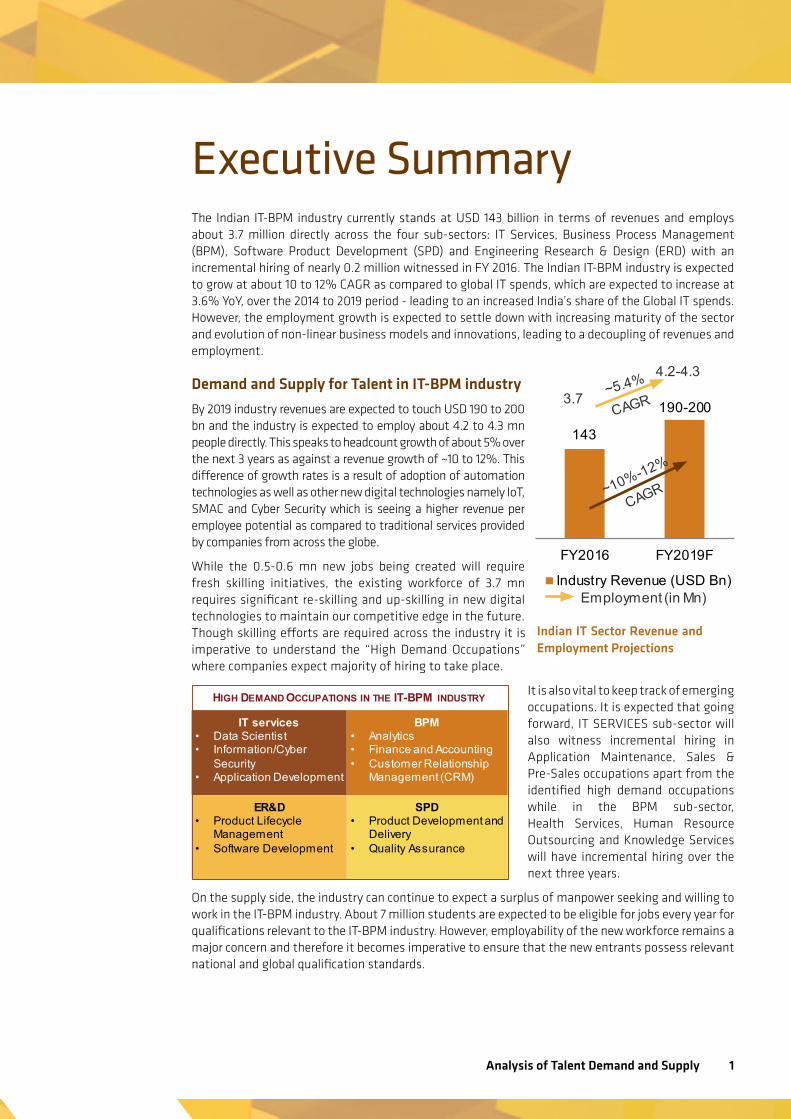

143

190-200

FY2016 FY2019F

Industry Revenue (USD Bn)

3.7

4.2-4.3

Employment (in Mn)

Executive SummaryThe Indian IT-BPM industry currently stands at USD 143 billion in terms of revenues and employs about 3.7 million directly across the four sub-sectors: IT Services, Business Process Management (BPM), Software Product Development (SPD) and Engineering Research & Design (ERD) with an incremental hiring of nearly 0.2 million witnessed in FY 2016. The Indian IT-BPM industry is expected to grow at about 10 to 12% CAGR as compared to global IT spends, which are expected to increase at 3.6% YoY, over the 2014 to 2019 period - leading to an increased India’s share of the Global IT spends. However, the employment growth is expected to settle down with increasing maturity of the sector and evolution of non-linear business models and innovations, leading to a decoupling of revenues and employment.

Demand and Supply for Talent in IT-BPM industry

By 2019 industry revenues are expected to touch USD 190 to 200 bn and the industry is expected to employ about 4.2 to 4.3 mn people directly. This speaks to headcount growth of about 5% over the next 3 years as against a revenue growth of ~10 to 12%. This difference of growth rates is a result of adoption of automation technologies as well as other new digital technologies namely IoT, SMAC and Cyber Security which is seeing a higher revenue per employee potential as compared to traditional services provided by companies from across the globe.

While the 0.5-0.6 mn new jobs being created will require fresh skilling initiatives, the existing workforce of 3.7 mn requires significant re-skilling and up-skilling in new digital technologies to maintain our competitive edge in the future. Though skilling efforts are required across the industry it is imperative to understand the “High Demand Occupations” where companies expect majority of hiring to take place.

It is also vital to keep track of emerging occupations. It is expected that going forward, IT SERVICES sub-sector will also witness incremental hiring in Application Maintenance, Sales & Pre-Sales occupations apart from the identified high demand occupations while in the BPM sub-sector, Health Services, Human Resource Outsourcing and Knowledge Services will have incremental hiring over the next three years.

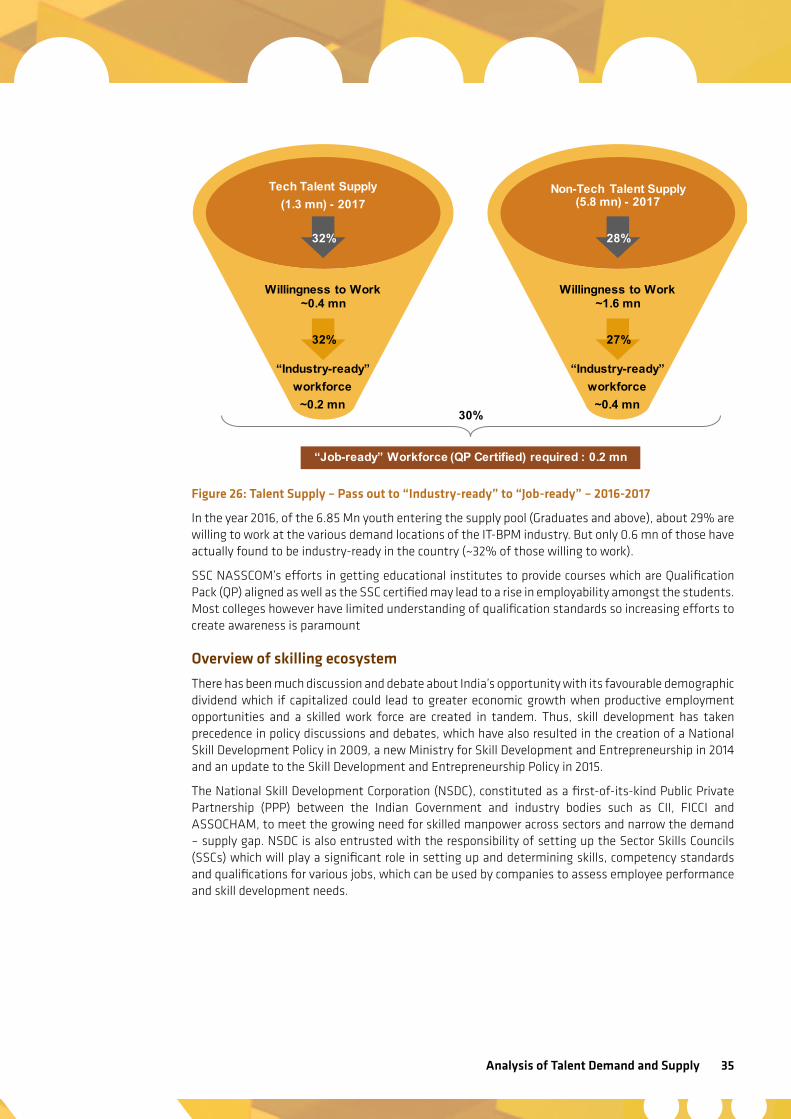

On the supply side, the industry can continue to expect a surplus of manpower seeking and willing to work in the IT-BPM industry. About 7 million students are expected to be eligible for jobs every year for qualifications relevant to the IT-BPM industry. However, employability of the new workforce remains a major concern and therefore it becomes imperative to ensure that the new entrants possess relevant national and global qualification standards.

Indian IT Sector Revenue and Employment Projections

IT services• Data Scientist• Information/Cyber

Security• Application Development

SPD• Product Development and

Delivery • Quality Assurance

ER&D• Product Lifecycle

Management• Software Development

BPM• Analytics• Finance and Accounting• Customer Relationship

Management (CRM)

HIGH DEMAND OCCUPATIONS IN THE IT-BPM INDUSTRY

2

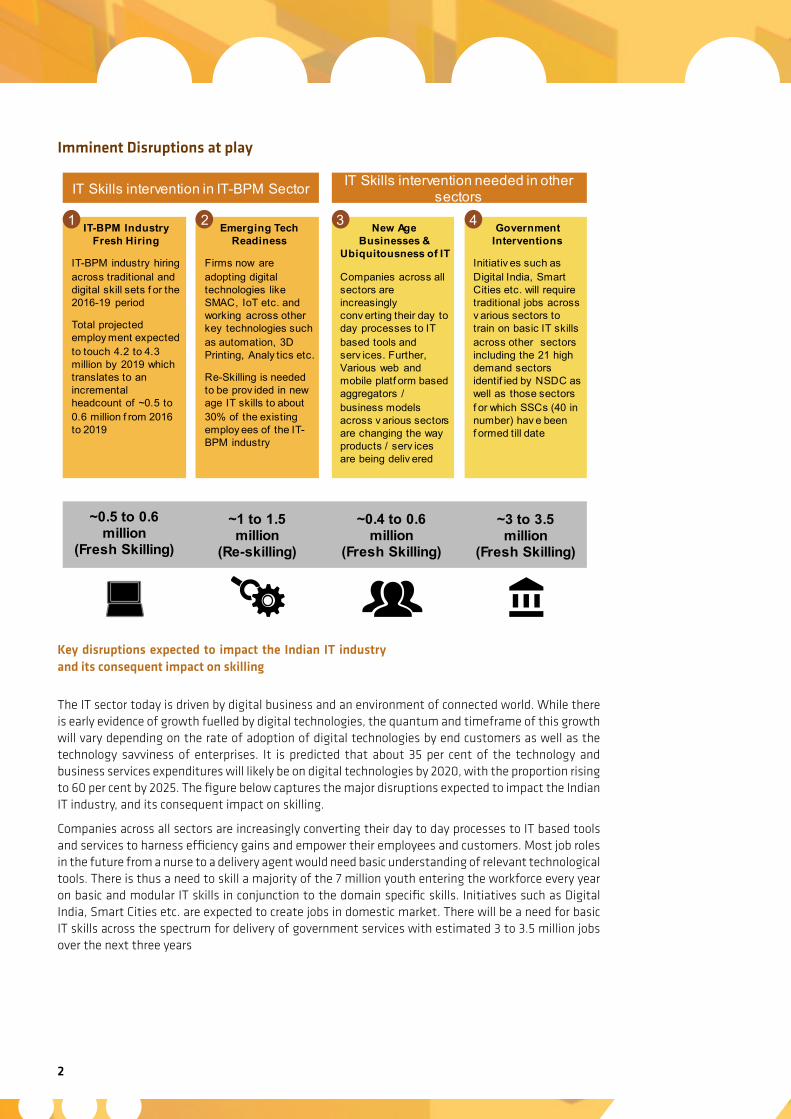

Imminent Disruptions at play

The IT sector today is driven by digital business and an environment of connected world. While there is early evidence of growth fuelled by digital technologies, the quantum and timeframe of this growth will vary depending on the rate of adoption of digital technologies by end customers as well as the technology savviness of enterprises. It is predicted that about 35 per cent of the technology and business services expenditures will likely be on digital technologies by 2020, with the proportion rising to 60 per cent by 2025. The figure below captures the major disruptions expected to impact the Indian IT industry, and its consequent impact on skilling.

Companies across all sectors are increasingly converting their day to day processes to IT based tools and services to harness efficiency gains and empower their employees and customers. Most job roles in the future from a nurse to a delivery agent would need basic understanding of relevant technological tools. There is thus a need to skill a majority of the 7 million youth entering the workforce every year on basic and modular IT skills in conjunction to the domain specific skills. Initiatives such as Digital India, Smart Cities etc. are expected to create jobs in domestic market. There will be a need for basic IT skills across the spectrum for delivery of government services with estimated 3 to 3.5 million jobs over the next three years

Key disruptions expected to impact the Indian IT industry and its consequent impact on skilling

IT Skills intervention in IT-BPM Sector IT Skills intervention needed in other sectors

IT-BPM Industry Fresh Hiring

IT-BPM industry hiring across traditional and digital skill sets f or the 2016-19 period

Total projected employ ment expected to touch 4.2 to 4.3 million by 2019 which translates to an incremental headcount of ~0.5 to 0.6 million f rom 2016 to 2019

Emerging Tech Readiness

Firms now are adopting digital technologies like SMAC, IoT etc. and working across other key technologies such as automation, 3D Printing, Analy tics etc.

Re-Skilling is needed to be prov ided in new age IT skills to about 30% of the existing employ ees of the IT-BPM industry

New Age Businesses &

Ubiquitousness of IT

Companies across all sectors are increasingly conv erting their day to day processes to IT based tools and serv ices. Further, Various web and mobile platf orm based aggregators / business models across v arious sectors are changing the way products / serv ices are being deliv ered

GovernmentInterventions

Initiativ es such as Digital India, Smart Cities etc. will require traditional jobs across v arious sectors to train on basic IT skills across other sectors including the 21 high demand sectors identif ied by NSDC as well as those sectors f or which SSCs (40 in number) hav e been f ormed till date

~0.5 to 0.6 million

(Fresh Skilling)

~0.4 to 0.6 million

(Fresh Skilling)

~1 to 1.5 million

(Re-skilling)

~3 to 3.5 million

(Fresh Skilling)

21 43

Analysis of Talent Demand and Supply 3

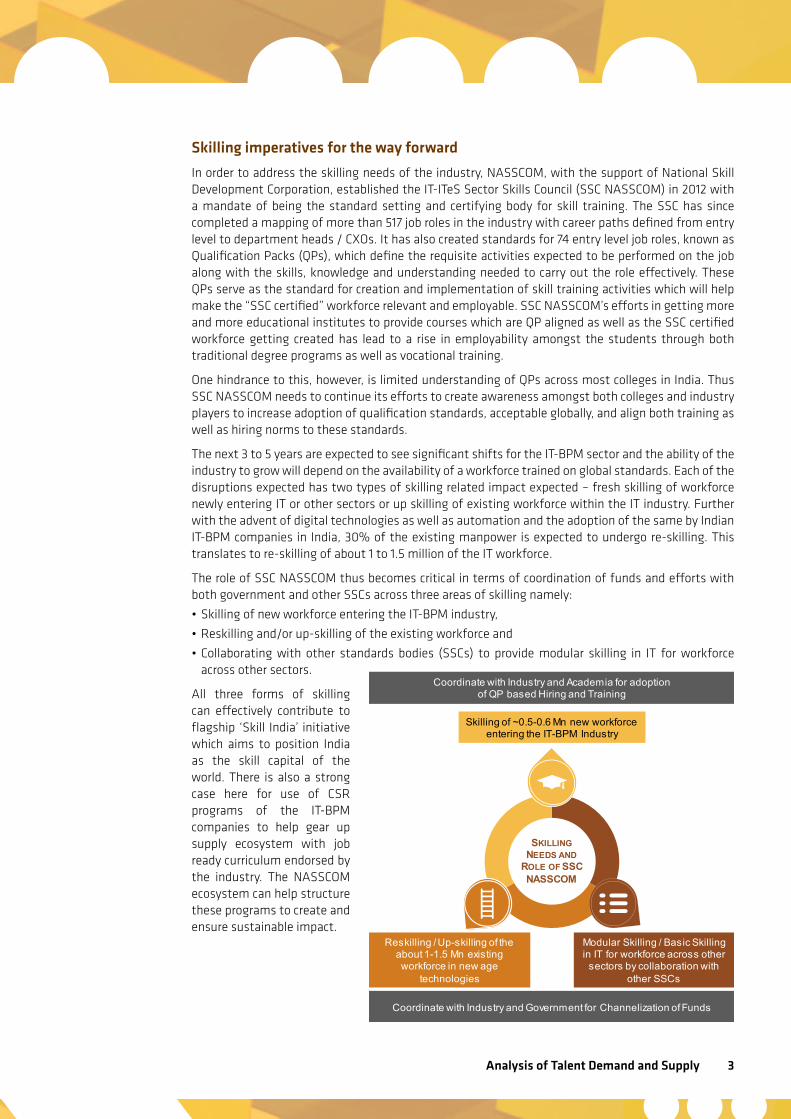

Skilling imperatives for the way forward

In order to address the skilling needs of the industry, NASSCOM, with the support of National Skill Development Corporation, established the IT-ITeS Sector Skills Council (SSC NASSCOM) in 2012 with a mandate of being the standard setting and certifying body for skill training. The SSC has since completed a mapping of more than 517 job roles in the industry with career paths defined from entry level to department heads / CXOs. It has also created standards for 74 entry level job roles, known as Qualification Packs (QPs), which define the requisite activities expected to be performed on the job along with the skills, knowledge and understanding needed to carry out the role effectively. These QPs serve as the standard for creation and implementation of skill training activities which will help make the “SSC certified” workforce relevant and employable. SSC NASSCOM’s efforts in getting more and more educational institutes to provide courses which are QP aligned as well as the SSC certified workforce getting created has lead to a rise in employability amongst the students through both traditional degree programs as well as vocational training.

One hindrance to this, however, is limited understanding of QPs across most colleges in India. Thus SSC NASSCOM needs to continue its efforts to create awareness amongst both colleges and industry players to increase adoption of qualification standards, acceptable globally, and align both training as well as hiring norms to these standards.

The next 3 to 5 years are expected to see significant shifts for the IT-BPM sector and the ability of the industry to grow will depend on the availability of a workforce trained on global standards. Each of the disruptions expected has two types of skilling related impact expected – fresh skilling of workforce newly entering IT or other sectors or up skilling of existing workforce within the IT industry. Further with the advent of digital technologies as well as automation and the adoption of the same by Indian IT-BPM companies in India, 30% of the existing manpower is expected to undergo re-skilling. This translates to re-skilling of about 1 to 1.5 million of the IT workforce.

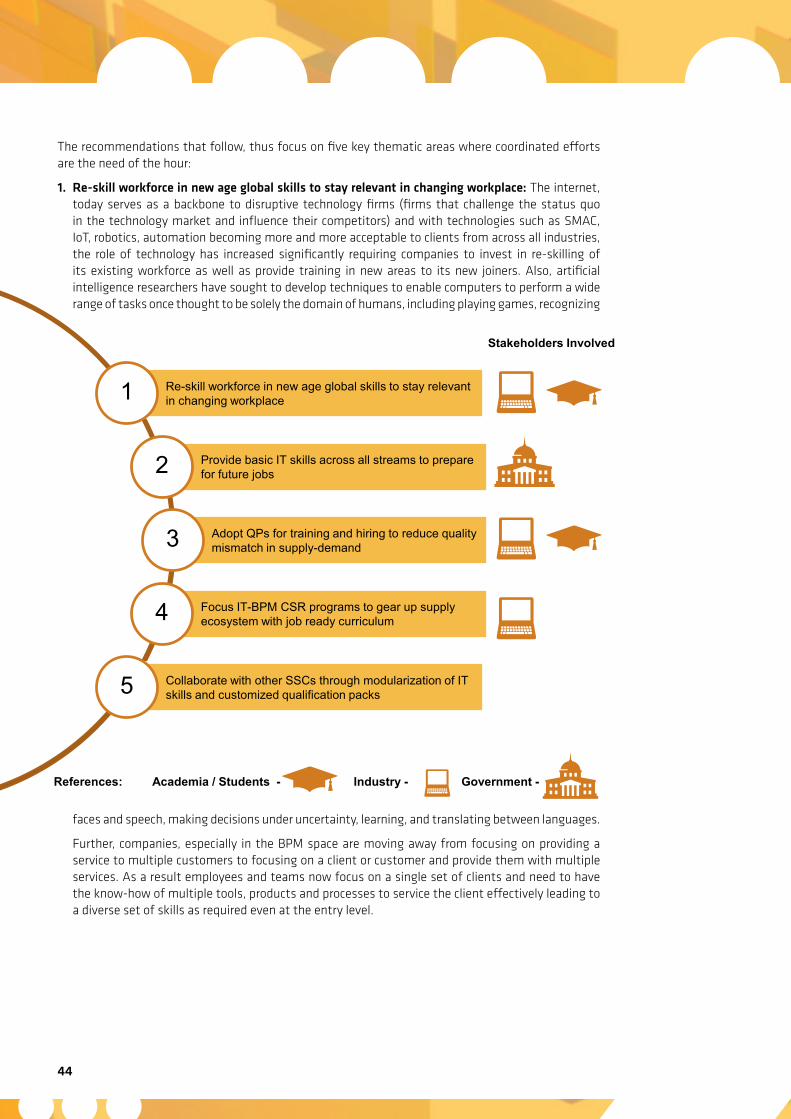

The role of SSC NASSCOM thus becomes critical in terms of coordination of funds and efforts with both government and other SSCs across three areas of skilling namely:

• Skilling of new workforce entering the IT-BPM industry,

• Reskilling and/or up-skilling of the existing workforce and

• Collaborating with other standards bodies (SSCs) to provide modular skilling in IT for workforce across other sectors.

All three forms of skilling can effectively contribute to flagship ‘Skill India’ initiative which aims to position India as the skill capital of the world. There is also a strong case here for use of CSR programs of the IT-BPM companies to help gear up supply ecosystem with job ready curriculum endorsed by the industry. The NASSCOM ecosystem can help structure these programs to create and ensure sustainable impact.

Skilling of ~0.5-0.6 Mn new workforce entering the IT-BPM Industry

Reskilling / Up-skilling of the about 1-1.5 Mn existing workforce in new age

technologies

Modular Skilling / Basic Skilling in IT for workforce across other

sectors by collaboration with other SSCs

SKILLINGNEEDS AND

ROLE OF SSC NASSCOM

Coordinate with Industry and Government for Channelization of Funds

Coordinate with Industry and Academia for adoption of QP based Hiring and Training

4

Analysis of Talent Demand and Supply 5

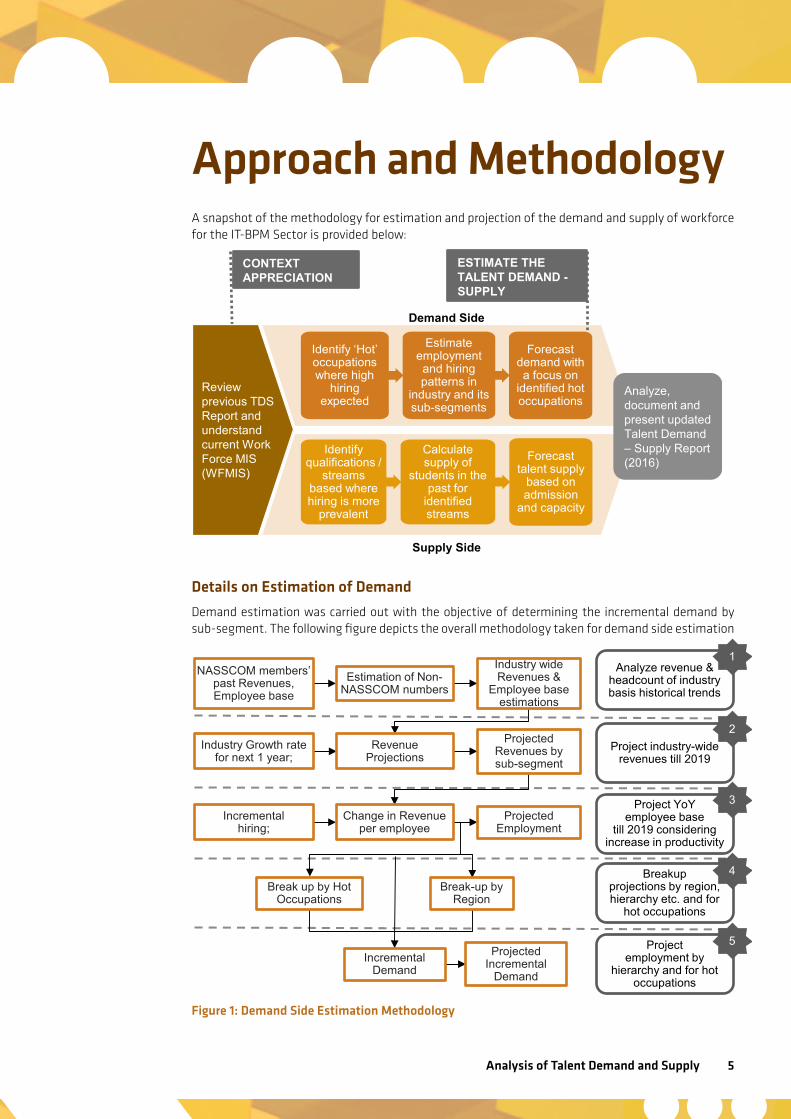

Approach and MethodologyA snapshot of the methodology for estimation and projection of the demand and supply of workforce for the IT-BPM Sector is provided below:

Details on Estimation of Demand

Demand estimation was carried out with the objective of determining the incremental demand by sub-segment. The following figure depicts the overall methodology taken for demand side estimation

Figure 1: Demand Side Estimation Methodology

CONTEXT APPRECIATION

ESTIMATE THE TALENT DEMAND - SUPPLY

Review previous TDS Report and understand current Work Force MIS (WFMIS)

Identify ‘Hot’ occupations where high

hiring expected

Estimate employment and hiring patterns in

industry and its sub-segments

Forecast demand with a focus on

identified hot occupations

Identify qualifications /

streams based where hiring is more

prevalent

Calculate supply of

students in the past for

identified streams

Forecast talent supply

based on admission

and capacity

Analyze, document and present updated Talent Demand – Supply Report (2016)

Demand Side

Supply Side

Analyze revenue & headcount of industry basis historical trends

Project industry-wide revenues till 2019

Project YoY employee base

till 2019 considering increase in productivity

Breakup projections by region, hierarchy etc. and for

hot occupations

Project employment by

hierarchy and for hot occupations

5

4

3

2

1

Estimation of Non-NASSCOM numbers

NASSCOM members’ past Revenues, Employee base

Industry wide Revenues &

Employee base estimations

Revenue Projections

Industry Growth rate for next 1 year;

Projected Revenues by sub-segment

Change in Revenue per employee

Incremental hiring;

Projected Employment

Incremental Demand

Projected Incremental

Demand

Break up by Hot Occupations

Break-up by Region

6

The estimation of demand has taken into consideration …

1. Estimated industry revenues, employee base and hiring pattern

• Estimated the aggregate industry revenue, employee base and hiring numbers.

2. Forecasted sub-segment wise demand

• Compiled the growth rate in terms of revenue and hiring numbers over the last three years.

• Projected demand, for the next 3 years on annual basis, based on the past growth as well as based on rise of global IT spends.

• Adjusted the expected rise in employment based on the change in revenue per employee.

3. Projected employment opportunities for identified 10 hot occupations

• Through secondary research, collected the information on job postings at the occupational level for IT services and BPM sub-sectors.

• Applied the percentage of each occupation to the respective sub-segment’s workforce to the demand estimation to arrive at demand for identified hot occupations.

4. Estimated incremental manpower demand for sub-segments as well as for 10 hot occupations for three years

Secondary research included

• Annual reports of the last three years of the top IT companies in each of the four sub segment

• Relevant reports like Skill Gap Study for IT/ITeS industry, employability report and State Skill Gap Study conducted for the key states (A.P., T.N., Karnataka, Kerala, Delhi and Maharashtra)

• Policy documents related to Make in India and Digital India

• NASSCOM/ SSC NASSCOM reports like Quarterly Industry Review, Innovation Report, India’s Domestic IT-BPO Market, BPO Career Guide, Indian Knowledge Services Outsourcing Report, The IT-BPO Sector in India: Strategic Review, etc.

• Report from reputed IT sector analysts like Gartner, IDC and Forrester.

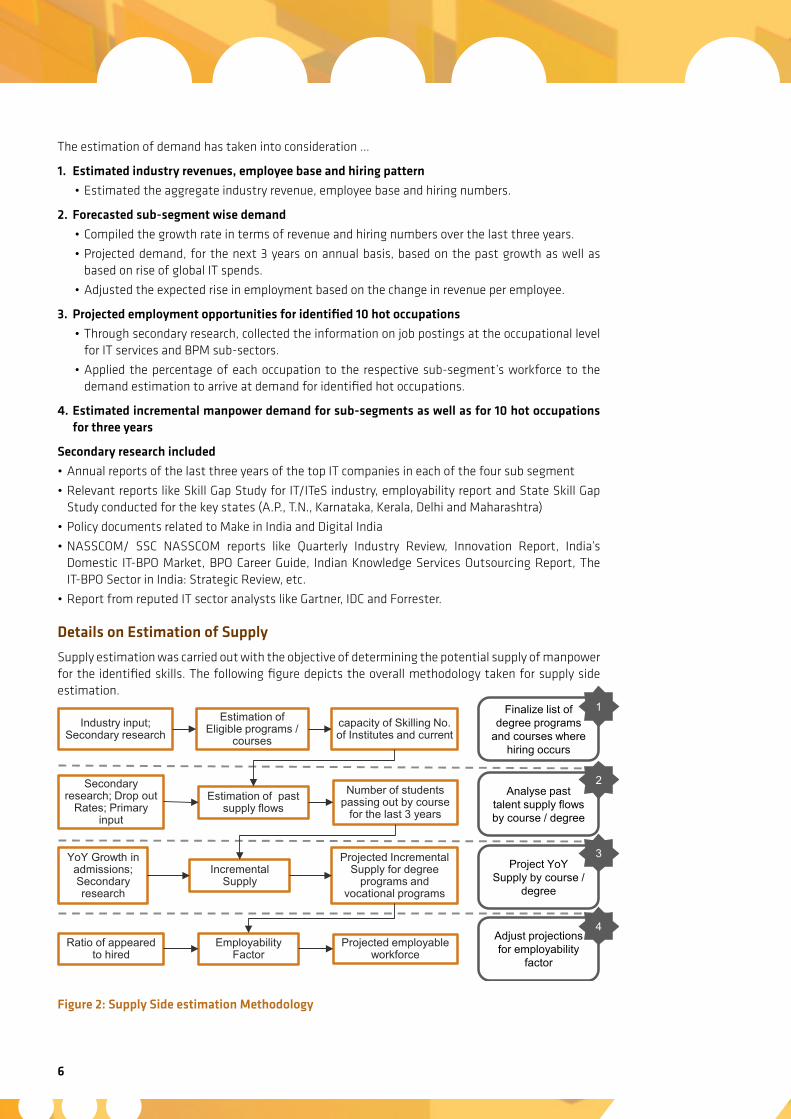

Details on Estimation of Supply

Supply estimation was carried out with the objective of determining the potential supply of manpower for the identified skills. The following figure depicts the overall methodology taken for supply side estimation.

Figure 2: Supply Side estimation Methodology

Estimation of Eligible programs /

courses Industry input;

Secondary research capacity of Skilling No. of Institutes and current

Finalize list of degree programs

and courses where hiring occurs

Estimation of past supply flows

Secondary research; Drop out

Rates; Primary input

Number of students passing out by course

for the last 3 years

Analyse past talent supply flows by course / degree

Incremental Supply

YoY Growth in admissions; Secondary research

Projected Incremental Supply for degree

programs and vocational programs

Project YoY Supply by course /

degree

Adjust projections for employability

factor

4

3

2

1

Employability Factor

Ratio of appeared to hired

Projected employable workforce

Analysis of Talent Demand and Supply 7

The following steps were used for supply estimation

1. Identified qualifications and estimation of potential number of institutes

• Mapped the current qualifications being hired across the industry through industry interaction and qualifications required for each job role as mentioned in QPs created.

• Identified various streams, number of institutes within each stream in the country and calculation of current capacity, admissions and number of students passing out by state.

2. Calculated enrolment, number of students passing by streams

• For each of the streams identified (Computer Science, BCA/MCA etc.), calculated enrolment and students pass outs to estimate growth rates.

• Applied the drop-out rates available through secondary research to the aggregate data to arrive at the number of students passing out of every stream.

3. Estimated Supply

• Based on the growth rates YoY, drop-out rates and growth of vocational skills training, estimated the following:

– Number of students enrolled by course and level for period constituting supply for the period 2016-2019 for each state – Number of students passing out by course and level for period 2016-2019 for each state

4. Incorporated willingness to work employability factor at entry levels

• Based on Workforce Participation Rate (Wfpr) rates available and secondary research the ratio of people passing out to willing to work to employable workforce.

• This ratio is applied on the total number of incremental workforce to get the actual number of people found to be employable

Demand - Supply gap estimation

Calculated the demand-supply gap considering the incremental demand and supply from the calculations as explained above. The demand supply gap analysis also included impact of disruption lead factors and the qualitative skilling aspects of the same. Further, the slicing of demand vs supply was also done at a state and regional level to provide the policy makers with requisite perspective.

8

Analysis of the IT-BPM industryTrends in Global IT-BPM spends

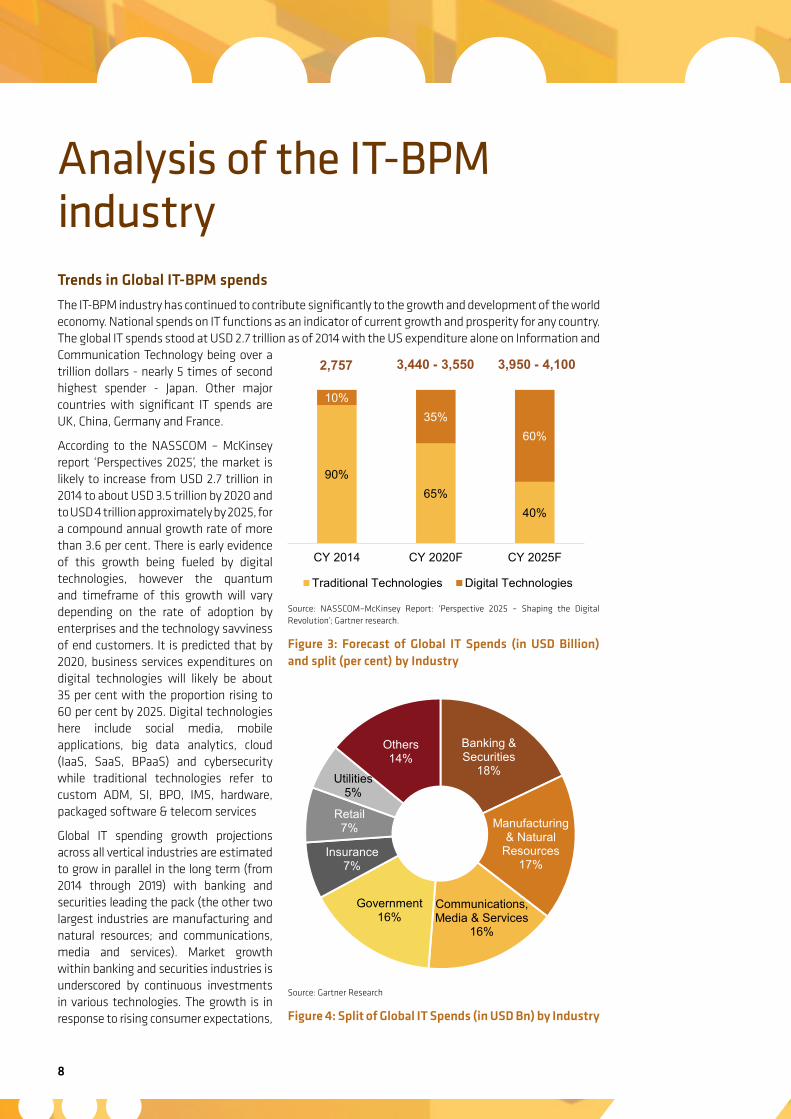

The IT-BPM industry has continued to contribute significantly to the growth and development of the world economy. National spends on IT functions as an indicator of current growth and prosperity for any country. The global IT spends stood at USD 2.7 trillion as of 2014 with the US expenditure alone on Information and Communication Technology being over a trillion dollars - nearly 5 times of second highest spender - Japan. Other major countries with significant IT spends are UK, China, Germany and France.

According to the NASSCOM – McKinsey report ‘Perspectives 2025’, the market is likely to increase from USD 2.7 trillion in 2014 to about USD 3.5 trillion by 2020 and to USD 4 trillion approximately by 2025, for a compound annual growth rate of more than 3.6 per cent. There is early evidence of this growth being fueled by digital technologies, however the quantum and timeframe of this growth will vary depending on the rate of adoption by enterprises and the technology savviness of end customers. It is predicted that by 2020, business services expenditures on digital technologies will likely be about 35 per cent with the proportion rising to 60 per cent by 2025. Digital technologies here include social media, mobile applications, big data analytics, cloud (IaaS, SaaS, BPaaS) and cybersecurity while traditional technologies refer to custom ADM, SI, BPO, IMS, hardware, packaged software & telecom services

Global IT spending growth projections across all vertical industries are estimated to grow in parallel in the long term (from 2014 through 2019) with banking and securities leading the pack (the other two largest industries are manufacturing and natural resources; and communications, media and services). Market growth within banking and securities industries is underscored by continuous investments in various technologies. The growth is in response to rising consumer expectations,

90% 65%

40%

10% 35%

60%

CY 2014 CY 2020F CY 2025F

Traditional Technologies Digital Technologies

2,757 3,440 - 3,550 3,950 - 4,100

Source: NASSCOM–McKinsey Report: ‘Perspective 2025 – Shaping the Digital Revolution’; Gartner research.

Figure 3: Forecast of Global IT Spends (in USD Billion) and split (per cent) by Industry

Source: Gartner Research

Figure 4: Split of Global IT Spends (in USD Bn) by Industry

Banking & Securities

18%

Manufacturing & Natural

Resources 17%

Communications, Media & Services

16%

Government 16%

Insurance 7%

Retail 7%

Utilities 5%

Others 14%

Analysis of Talent Demand and Supply 9

increased regulatory expectations, cybersecurity and competition from new "fintech" companies that, after growing their presence in niche banking areas, are challenging the traditional banking industry. Healthcare providers and insurance are the other two fastest-growth industries.

The communications, media and services industry is now in the midst of a massive digital transformation, with the traditional industry heavyweights (across telecommunications, cable, television, newspapers and online) challenged by the existing and new emerging market competitors (for example, over-the-top players or Uber-like organizations). To be competitive, companies are now focusing on discovering new business models (digital business) and on improving existing business processes (creating bimodal business delivery platforms) that favor innovation and decrease time to market. Thus, IT spending priorities in the industry are dominated by BI/analytics (opportunity to harvest real business value from insight), infrastructure and cloud projects. By 2018, 20% of the top 1,000 global enterprises will implement MVNO capabilities to support their IoT needs. To meet this demand, many communications service providers and IT services firms are investing in creating their IoT platforms.1

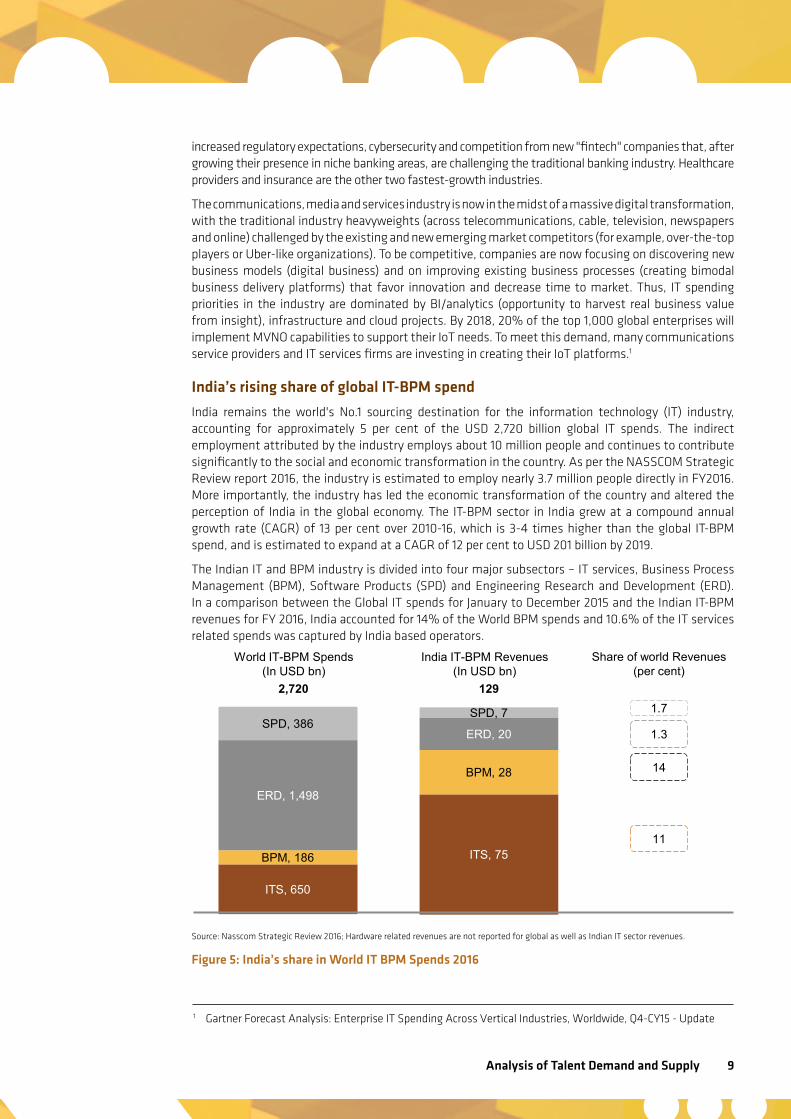

India’s rising share of global IT-BPM spend

India remains the world's No.1 sourcing destination for the information technology (IT) industry, accounting for approximately 5 per cent of the USD 2,720 billion global IT spends. The indirect employment attributed by the industry employs about 10 million people and continues to contribute significantly to the social and economic transformation in the country. As per the NASSCOM Strategic Review report 2016, the industry is estimated to employ nearly 3.7 million people directly in FY2016. More importantly, the industry has led the economic transformation of the country and altered the perception of India in the global economy. The IT-BPM sector in India grew at a compound annual growth rate (CAGR) of 13 per cent over 2010-16, which is 3-4 times higher than the global IT-BPM spend, and is estimated to expand at a CAGR of 12 per cent to USD 201 billion by 2019.

The Indian IT and BPM industry is divided into four major subsectors – IT services, Business Process Management (BPM), Software Products (SPD) and Engineering Research and Development (ERD). In a comparison between the Global IT spends for January to December 2015 and the Indian IT-BPM revenues for FY 2016, India accounted for 14% of the World BPM spends and 10.6% of the IT services related spends was captured by India based operators.

Source: Nasscom Strategic Review 2016; Hardware related revenues are not reported for global as well as Indian IT sector revenues.

Figure 5: India’s share in World IT BPM Spends 2016

1 Gartner Forecast Analysis: Enterprise IT Spending Across Vertical Industries, Worldwide, Q4-CY15 - Update

ITS, 650

BPM, 186

ERD, 1,498

SPD, 386

ITS, 75

BPM, 28

ERD, 20

SPD, 7

Share of world Revenues (per cent)

14

11

World IT-BPM Spends (In USD bn)

2,720

India IT-BPM Revenues (In USD bn)

129 1.7

1.3

10

This share is expected to grow in light of overall growth of IT spends across the world. India’s Share of Global IT spends in the IT services segment is expected to rise from about 11% currently to about 14% by FY19. This is followed by BPM sub-sector which rises to 16% of global IT spends. ERD and SPD are expected to rise marginally to 1.7% and 2.3% of respective Global IT spends. For this to hold true Indian IT companies need to up their services through digital technologies as well as build skillsets required for such technologies.

IT services in India are approximately 3-4 times cheaper than in the US and this cost competitiveness continues to be the mainstay of its unique selling proposition (USP) in the global sourcing market. In recent times India has also gained prominence in terms of housing intellectual capital as evidenced by several global IT firms setting up their innovation centres in India. India remains the world's No.1 sourcing destination for the information technology (IT) industry, accounting for approximately 56 per cent of the USD 162-166 billion market (not including hardware)

Overview of Indian IT industry

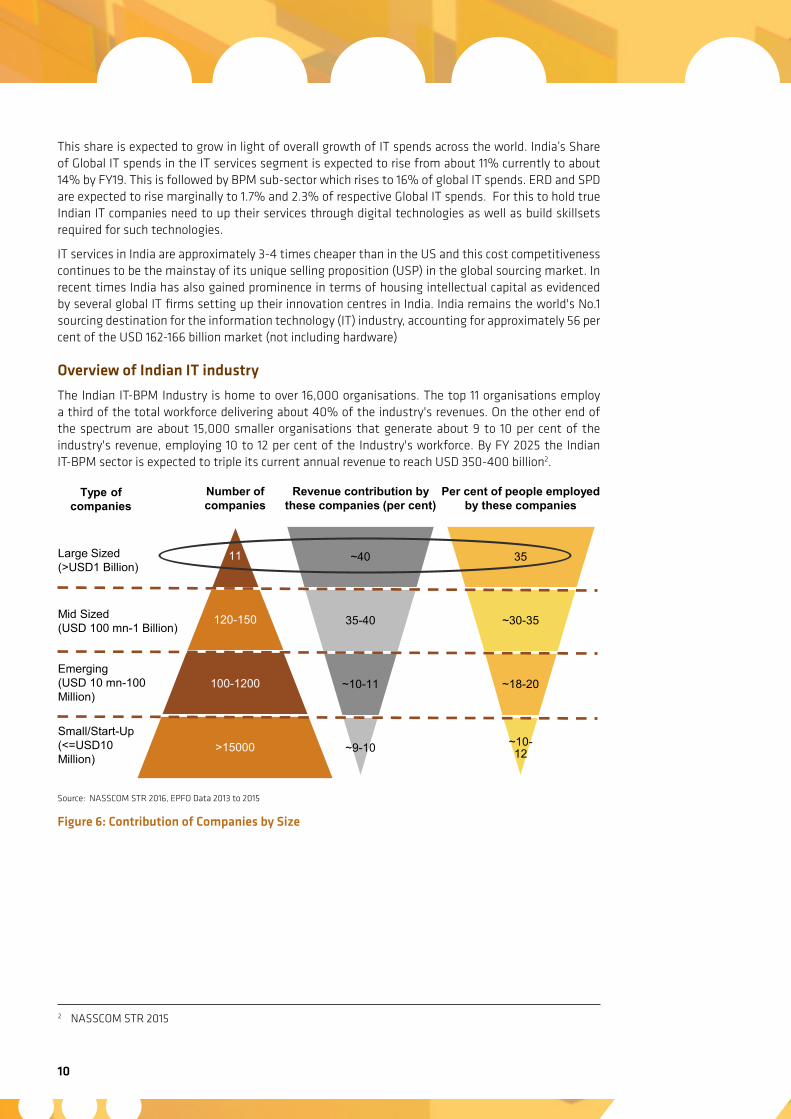

The Indian IT-BPM Industry is home to over 16,000 organisations. The top 11 organisations employ a third of the total workforce delivering about 40% of the industry's revenues. On the other end of the spectrum are about 15,000 smaller organisations that generate about 9 to 10 per cent of the industry's revenue, employing 10 to 12 per cent of the Industry's workforce. By FY 2025 the Indian IT-BPM sector is expected to triple its current annual revenue to reach USD 350-400 billion2.

Source: NASSCOM STR 2016, EPFO Data 2013 to 2015

Figure 6: Contribution of Companies by Size

11

120-150

100-1200

>15000

Number of companies

Per cent of people employed by these companies

Revenue contribution by these companies (per cent)

~40

35-40

~10-11

~9-10

35

~30-35

~18-20

~10-12

Large Sized (>USD1 Billion)

Mid Sized (USD 100 mn-1 Billion)

Emerging (USD 10 mn-100 Million)

Type of companies

Small/Start-Up (<=USD10 Million)

2 NASSCOM STR 2015

Analysis of Talent Demand and Supply 11

Performance within the IT-BPM industry

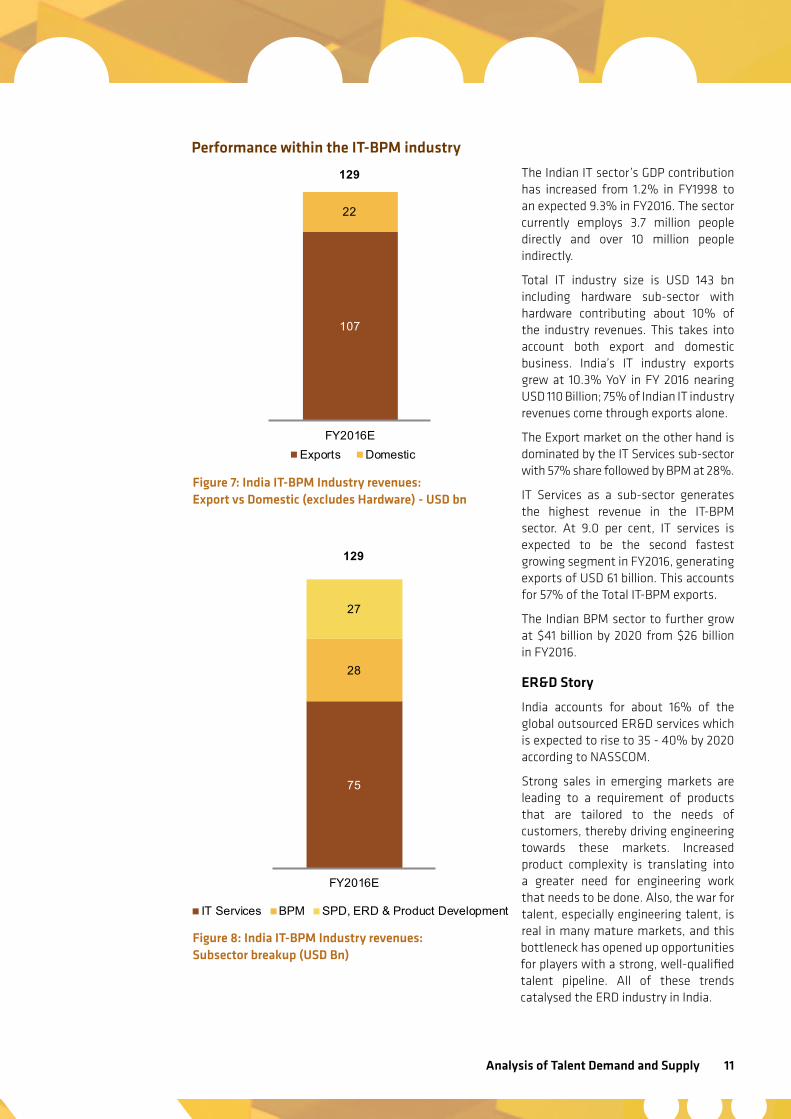

The Indian IT sector’s GDP contribution has increased from 1.2% in FY1998 to an expected 9.3% in FY2016. The sector currently employs 3.7 million people directly and over 10 million people indirectly.

Total IT industry size is USD 143 bn including hardware sub-sector with hardware contributing about 10% of the industry revenues. This takes into account both export and domestic business. India’s IT industry exports grew at 10.3% YoY in FY 2016 nearing USD 110 Billion; 75% of Indian IT industry revenues come through exports alone.

The Export market on the other hand is dominated by the IT Services sub-sector with 57% share followed by BPM at 28%.

IT Services as a sub-sector generates the highest revenue in the IT-BPM sector. At 9.0 per cent, IT services is expected to be the second fastest growing segment in FY2016, generating exports of USD 61 billion. This accounts for 57% of the Total IT-BPM exports.

The Indian BPM sector to further grow at $41 billion by 2020 from $26 billion in FY2016.

ER&D Story

India accounts for about 16% of the global outsourced ER&D services which is expected to rise to 35 - 40% by 2020 according to NASSCOM.

Strong sales in emerging markets are leading to a requirement of products that are tailored to the needs of customers, thereby driving engineering towards these markets. Increased product complexity is translating into a greater need for engineering work that needs to be done. Also, the war for talent, especially engineering talent, is real in many mature markets, and this bottleneck has opened up opportunities for players with a strong, well-qualified talent pipeline. All of these trends catalysed the ERD industry in India.

Figure 7: India IT-BPM Industry revenues: Export vs Domestic (excludes Hardware) - USD bn

Figure 8: India IT-BPM Industry revenues: Subsector breakup (USD Bn)

107

22

FY2016EExports Domestic

129

75

28

27

FY2016E

IT Services BPM SPD, ERD & Product Development

129

12

According to a study3, growth in global ERD spend is being driven by four emerging trends:

• Continued R&D investment considered imperative by multinational conglomerates when it comes to pursuing innovation and penetrating new, emerging markets

• Increasing use of electronics, the search for alternate fuel sources and greater fuel efficiency, and the convergence of technologies that enable a single device to perform multiple functions

• Growing sophistication and maturity of the ERD services industry

• Changing view of India as a strategic partner focused on innovation rather than simply sustenance and maintenance of existing products

Key forces of disruption

India is currently the third largest IT market in the APAC region, following China and Australia, and is expected to take the second position by 2019. The confluence of digital technologies (cloud, mobility, IoT, social, big data), changing business models, rapidly growing innovative start-up ecosystem, government’s vision of driving digitization, and India’s consumer economy have been identified as major trends projected to spearhead this growth. The Industry is expected to reach US$350 billion by 20254.

To realise this growth potential, it is imperative that India capitalise on the opportunities presented by the paradigm shifts taking place within the industry over the next five years. The shifts in play are both global and India-centric in nature, affecting the way businesses will be run and the workforce required to do so.

Global Factors

There have been marked phases in the story in the IT industry, with firms of newer generations often supplanting incumbent market leaders, as evidenced by the shift from leadership in mainframes, to minicomputers, to personal computers, to the present era of the internet and mobile. Once-great firms unable to keep up or embrace the new paradigm saw themselves be ousted form relevance. The key therefore is to identify the next set of disruptions expected within the industry globally and to prepare for the same.

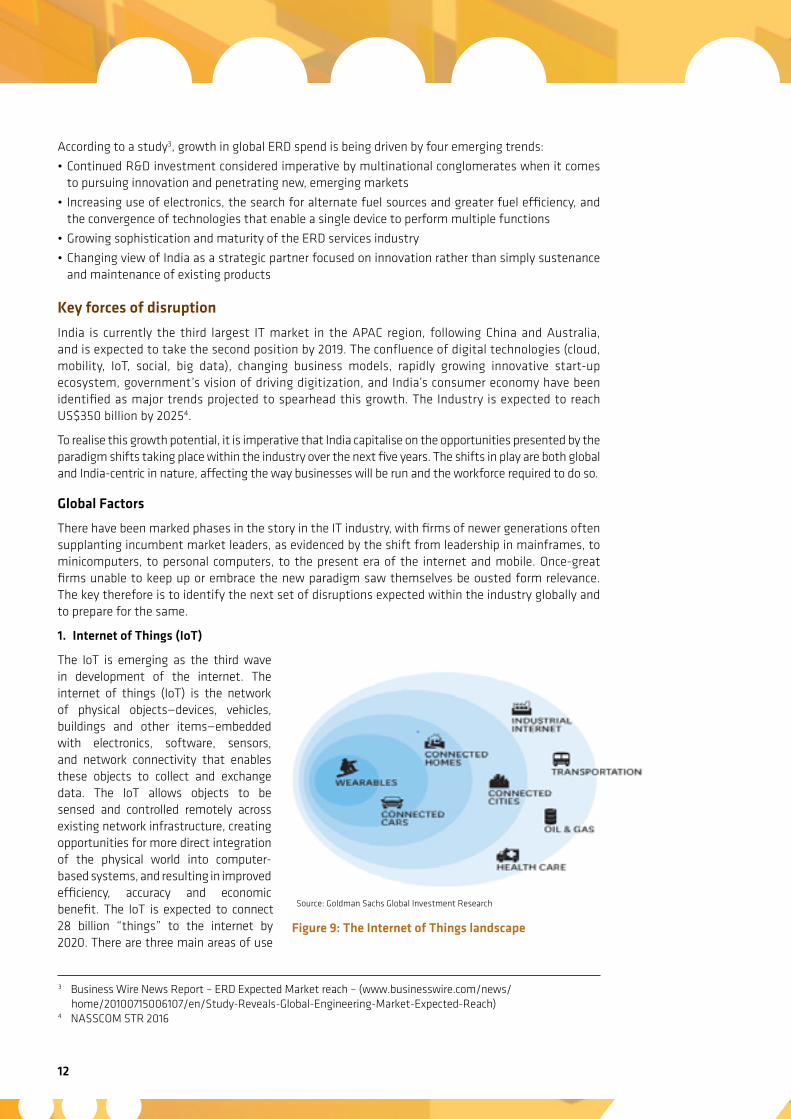

1. Internet of Things (IoT)

The IoT is emerging as the third wave in development of the internet. The internet of things (IoT) is the network of physical objects—devices, vehicles, buildings and other items—embedded with electronics, software, sensors, and network connectivity that enables these objects to collect and exchange data. The IoT allows objects to be sensed and controlled remotely across existing network infrastructure, creating opportunities for more direct integration of the physical world into computer-based systems, and resulting in improved efficiency, accuracy and economic benefit. The IoT is expected to connect 28 billion “things” to the internet by 2020. There are three main areas of use

3 Business Wire News Report – ERD Expected Market reach – (www.businesswire.com/news/home/20100715006107/en/Study-Reveals-Global-Engineering-Market-Expected-Reach)

4 NASSCOM STR 2016

Figure 9: The Internet of Things landscape

Source: Goldman Sachs Global Investment Research

Analysis of Talent Demand and Supply 13

for IoT devices - government, enterprise, and the home. The aggregate number of IoT devices estimated in use is expected to grow from 0.6 billion in 2014 to 6.7 billion by 2019, reflecting a CAGR of 61%.

The IoT companies' revenue opportunity lies primarily with those who can create the infrastructure and networks that IoT devices run on. It is estimated that hardware will account for only $50 billion by 2019, whereas software and service providers will generate up to $550 billion. Gartner predicts that spending on IOT hardware will exceed 2.5USD million every minute in 2016.5

IoT in India is given a major push by government of India through its smart city project. Governments’ objective is to create an IoT industry in India of USD 15 billion by 2020.Another key initiative taken by Government is the formation of Centre of Excellence on Internet of Things as a joint initiative with NASSCOM.

Some of the companies who are active in the IoT space in India are Intel, Volkswagen, MediaTek, Hero Motocorp, Hindustan Petroleum, Apollo Hospitals, Cisco, Bharti Infratel, TVS Motor, and IBM.6

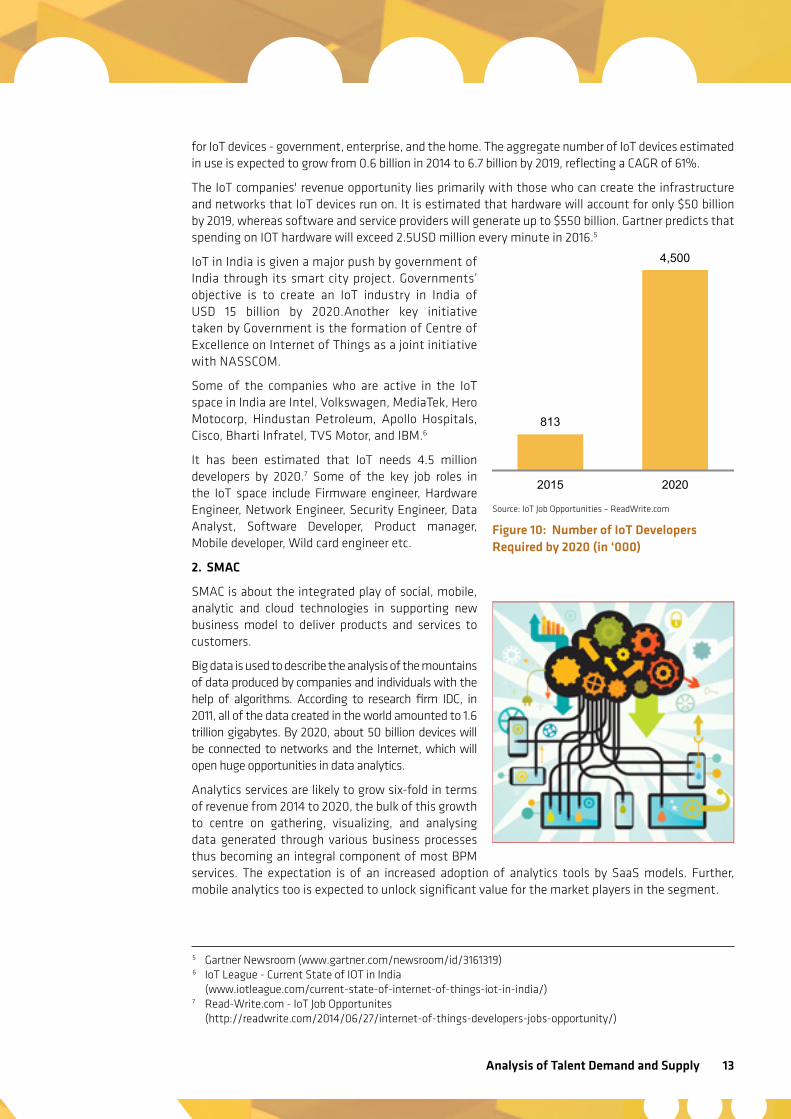

It has been estimated that IoT needs 4.5 million developers by 2020.7 Some of the key job roles in the IoT space include Firmware engineer, Hardware Engineer, Network Engineer, Security Engineer, Data Analyst, Software Developer, Product manager, Mobile developer, Wild card engineer etc.

2. SMAC

SMAC is about the integrated play of social, mobile, analytic and cloud technologies in supporting new business model to deliver products and services to customers.

Big data is used to describe the analysis of the mountains of data produced by companies and individuals with the help of algorithms. According to research firm IDC, in 2011, all of the data created in the world amounted to 1.6 trillion gigabytes. By 2020, about 50 billion devices will be connected to networks and the Internet, which will open huge opportunities in data analytics.

Analytics services are likely to grow six-fold in terms of revenue from 2014 to 2020, the bulk of this growth to centre on gathering, visualizing, and analysing data generated through various business processes thus becoming an integral component of most BPM services. The expectation is of an increased adoption of analytics tools by SaaS models. Further, mobile analytics too is expected to unlock significant value for the market players in the segment.

5 Gartner Newsroom (www.gartner.com/newsroom/id/3161319)6 IoT League - Current State of IOT in India

(www.iotleague.com/current-state-of-internet-of-things-iot-in-india/)7 Read-Write.com - IoT Job Opportunites

(http://readwrite.com/2014/06/27/internet-of-things-developers-jobs-opportunity/)

Source: IoT Job Opportunities – ReadWrite.com

813

4,500

2015 2020

Figure 10: Number of IoT Developers Required by 2020 (in ‘000)

14

International Data Corp. (IDC) estimates that Indian IT vendors will generate at least USD 225 billion in overall revenue in 2020 on back of growth of SMAC. The break-up of spending expected across each of the components are 10% of the total IT budget on big data and analytics, 9.5% on cloud services, 5.3% on mobile apps and devices and 3.4% on social media. A survey of 410 global IT decision makers in 2014 predicted India will export $15 billion worth of SMAC software and services in FY17.

A McKinsey report also quotes a shortfall of up to 190,000 data scientists and 1.5 Mn data managers in the U.S. alone thus providing Currently, the skill base for analytics in India is estimated to be about 90,000. Some of the key job roles in analytics include Specialized Analytics Analyst, Big Data Engineer, and Software Engineer-Analytics etc.

3. Software Automation

Software automation, artificial technology and greater efficiency through digital technology will require significant re-skilling of existing workforce. Clients of IT firms are looking more and more to move to newer technologies and cut costs on the older systems through automation.8 Some place cognitive technologies or automations on the same historical path as other breakthroughs – generating employment. Cognitive technologies may eliminate some kinds of work, it's much more likely that they will take over discrete tasks, making human workers more effective. Certain kinds of tasks—those that involve dealing with ambiguity, common sense, creativity, and human interaction—are likely to remain out of reach of computers for some time. Combining the skills of a smart human with a smart machine is more likely to make businesses competitive.9

4. Robotics

Robotics is a field of hardware based automation which concerns with the adoption of such automation to ensure quality production and meet market demand, and the growing demand from small- and medium-scale enterprises in developing countries. Key players in the market are increasingly developing low-cost, affordable, compact and energy-efficient solutions to cater the growing demands of the customers.

By 2018, around 1.3 million industrial robots will be entering service in factories around the world Industrial robotics market is expected to grow at CAGR of 11.9% between 2016 and 2022, and reach USD 79.56 Billion by 202210. In the high-revenue automotive sector, global investments in industrial robots increased by a record-breaking 43 percent (2013-2014) within one year. The current global leader in industrial robotic automation is South Korea.

8 Economic Times News Report - Surviving the Digital Age (http://economictimes.indiatimes.com/jobs/surviving-the-digital-wave-it-employees-need-to-upgrade-their-skills-to-stay-relevant/articleshow/50004219.cms)

9 Deloitte Research Report - Redesigning Work for Cognitive Technologies (www2.deloitte.com/content/dam/Deloitte/tr/Documents/technology-media-telecommunications/ redesigningworkcognitivetechnologies.pdf)

10 Industrial Robotics Market by Type, Application, Component, and Geography - Analysis & Forecast to 2022"

Analysis of Talent Demand and Supply 15

Never before have so many robot units been sold in one year as were sold in China in 2014 (57,100 units). The boom is continuing unabated in line with the forecasts: In 2018, China will account for more than one-third of the industrial robots installed worldwide. By 2018 global sales of industrial robots will on average grow year on year by 15 percent; the numbers of units sold will double to around 400,000 units. Five major markets representing 70 percent of the total sales volume: China, Japan, USA, South Korea and Germany.11

The APAC market is expected to grow at the highest CAGR between 2016 and 2022. The main drivers for this growth are the demand for collaborative industrial robots from small- and medium-scale enterprises in China, Japan, South Korea, and India as well as the growing investments in countries such as India to boost manufacturing under projects such as Make in India.12

The market in India for industrial robots is gathering momentum as automobile companies and electronics assembly manufacturers expand their operations in the country. In 2011, the sale of robotic devices in India doubled to 1,547units were expected to rise to about 4,000 units a year until 2015. The main applications of robots in India are welding, handling and dispensing. Hence, it is likely that more than 70 per cent of the robot sales ended up in the automotive industry.13 This growth is an indication of an environment that is increasingly conducive for new entrants and start-ups to establish themselves.

Some of the job roles within robotics requiring key IT skills are Robotics Developer, Automation and Robotics engineer etc.

5. 3D Printing

Canalys, a market research firm, anticipates changes ahead and predicts the global market for 3-D printers and services will grow from $2.5 billion in 2013 to $16.2 billion in 2018, a CAGR of 45.7 percent.14

The India 3D printer market is expected to cross $79 million by 2021, with automotive applications accounting for the biggest chunk of business. India primarily imports 3D printers in the country from countries such as China, U.S. and Germany. However, with government initiatives to boost domestic manufacturing like the “Make in Campaign”, many local players are expected to emerge in the forecast period.

Most of job roles related to 3D printing currently are manufacturing related. However, as the technology becomes more common place the jobs for Application Engineer CAD & 3D Printing as well as 3D Designer are expected to pick up.

11 World Robotics - Industrial Robots Market share (www.worldrobotics.org/index.php?id=home&news_id=287)

12 Markets and Markets - Press Release - APAC Growth (www.marketsandmarkets.com/PressReleases/industrial-robotics.asp)

13 OEM Update - Robot Sales in Auto Industry (www.oemupdate.com/Article.php?ItemId=1761)

14 PWC Report - Future of 3D Printing (www.pwc.com/us/en/technology-forecast/2014/3d-printing/features/future-3d-printing.html)

16

India Centric Factors

Whereas global would affect all markets, there are some changes specific to the Indian context. These factors

1. Government Initiatives - Digital India Program

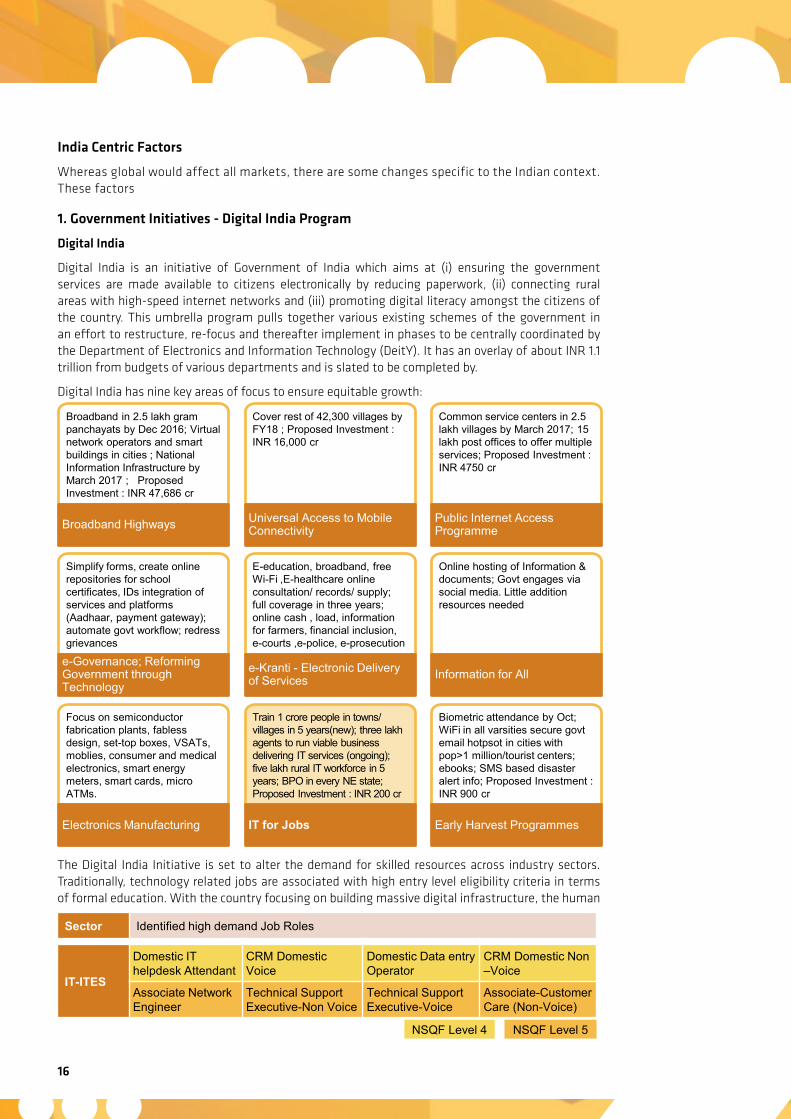

Digital India

Digital India is an initiative of Government of India which aims at (i) ensuring the government services are made available to citizens electronically by reducing paperwork, (ii) connecting rural areas with high-speed internet networks and (iii) promoting digital literacy amongst the citizens of the country. This umbrella program pulls together various existing schemes of the government in an effort to restructure, re-focus and thereafter implement in phases to be centrally coordinated by the Department of Electronics and Information Technology (DeitY). It has an overlay of about INR 1.1 trillion from budgets of various departments and is slated to be completed by.

Digital India has nine key areas of focus to ensure equitable growth:

The Digital India Initiative is set to alter the demand for skilled resources across industry sectors. Traditionally, technology related jobs are associated with high entry level eligibility criteria in terms of formal education. With the country focusing on building massive digital infrastructure, the human

Broadband in 2.5 lakh gram panchayats by Dec 2016; Virtual network operators and smart buildings in cities ; National Information Infrastructure by March 2017 ; Proposed Investment : INR 47,686 cr

Broadband Highways

Cover rest of 42,300 villages by FY18 ; Proposed Investment : INR 16,000 cr

Universal Access to Mobile Connectivity

Common service centers in 2.5 lakh villages by March 2017; 15 lakh post offices to offer multiple services; Proposed Investment : INR 4750 cr

Public Internet Access Programme

Simplify forms, create online repositories for school certificates, IDs integration of services and platforms (Aadhaar, payment gateway); automate govt workflow; redress grievances

e-Governance; Reforming Government through Technology

E-education, broadband, free Wi-Fi ,E-healthcare online consultation/ records/ supply; full coverage in three years; online cash , load, information for farmers, financial inclusion, e-courts ,e-police, e-prosecution

e-Kranti - Electronic Delivery of Services

Online hosting of Information & documents; Govt engages via social media. Little addition resources needed

Information for All

Focus on semiconductor fabrication plants, fabless design, set-top boxes, VSATs, moblies, consumer and medical electronics, smart energy meters, smart cards, micro ATMs.

Electronics Manufacturing

Train 1 crore people in towns/ villages in 5 years(new); three lakh agents to run viable business delivering IT services (ongoing); five lakh rural IT workforce in 5 years; BPO in every NE state; Proposed Investment : INR 200 cr

IT for Jobs

Biometric attendance by Oct; WiFi in all varsities secure govt email hotpsot in cities with pop>1 million/tourist centers; ebooks; SMS based disaster alert info; Proposed Investment : INR 900 cr

Early Harvest Programmes

Sector Identified high demand Job Roles

IT-ITES

Domestic IT helpdesk Attendant

CRM Domestic Voice

Domestic Data entry Operator

CRM Domestic Non –Voice

Associate Network Engineer

Technical Support Executive-Non Voice

Technical Support Executive-Voice

Associate-Customer Care (Non-Voice)

NSQF Level 4 NSQF Level 5

Analysis of Talent Demand and Supply 17

resources requirement in these industries may shift, giving rise to jobs which do not have formal education as an eligibility constraint. The identified job roles have low-eligibility barriers, and can be instrumental in implementing the Digital India vision:-

2. E-Commerce and the rise of the Indian startups

E-commerce

E-commerce has become commonplace because of its ability to attract a wide customer base with the best deals for products and services. The tech-savvy population has increased rapidly worldwide, driving the market growth. This has also increased the need for enhanced software, services, and analytics that can track buying patterns and online behaviour.

The global e-commerce industry generated revenues of USD 1.5 Trillion, growing at 20 per cent; the US being the world’s largest market, followed by China15. The Indian ecommerce industry today is clocking revenues of about USD 17 Billion, growing at a CAGR of over 30%16. Growing internet penetration, entry of global majors, rise in smartphones adoption, innovations in mobile technology, security, and payments, and access to funding helping accelerate the growth of e-commerce. Diverse demographics and inadequate infrastructure will catalyse the transformation of the e-commerce sector into a hyper local, on demand market. Augmented transaction values, increased data usage and higher online shopping penetration has the capacity to take the Indian e-Commerce revenues to USD 200 billion in gross merchandize value by 2030. The growth of ecommerce has attracted tremendous investments and it has resulted in the creation of jobs across different areas including IT-BPM.

The booming Internet commerce sector (e-commerce) was one of the major growth drivers of the economy in 2014. The nascent, yet growing, industry not only played a crucial role in generating new jobs but also in perking up salaries.

IT in E-Commerce companies includes design, development, implementation, and maintenance of the whole technical architecture. E-commerce enterprises' IT spending is directly linked to the company's strategy and goals. IT investments are critical and dependent on business needs and expansion strategies. However, the dynamism observed in sales patterns and consumer behaviour largely determines the utility value of IT investments.17 Some of the IT based job roles within E-Commerce companies include Software Engineer-Python Developer, Front Developer, Software Developer etc.

The Startup Story

India is the third largest base for new businesses in the world and home to over 4,200 tech start-ups, a number that is set to increase to 11,500 by 2020. The growth of tech startups has been fuelled by internet / app based business as well as new digital technologies. Some of factors leveraging the developments are:

• India’s internet economy is expected to touch USD 151.6 billion by 2018, accounting for 5 per cent of the country’s gross domestic product (GDP)18. India’s internet user base is expected to reach over 462 million by June 2016, the third largest in the world, while the number of social media users grow to 160 million

• Public cloud services revenue in India is expected to reach USD 0.9 billion in 2015, growing by 33 per cent YoY, as per a report by Gartner Inc. In yet another Gartner report, the public cloud market alone in the country was estimated to treble to USD 1.9 billion by 2018 from USD 0.6 billion in 2014. Increased penetration of internet (including in rural areas) and rapid emergence of e-commerce are the main drivers for continued growth of data centre co-location and hosting market in India.19 It is likely that these will be the key drivers for demand in the current economic scenario of uncertainty.

15 NASSCOM Report – e-commerce in India – Fueling a billion dreams16 NASSCOM STR 201617 Global E-commerce Software and Services Spending Market - 2015 to 2019, Technovio Report18 India @ D-gital. Bharat - BCG and IAMAI report - 201519 Indian in Business News Report

(http://indiainbusiness.nic.in/newdesign/index.php?param=industryservices_landing/395/3)

18

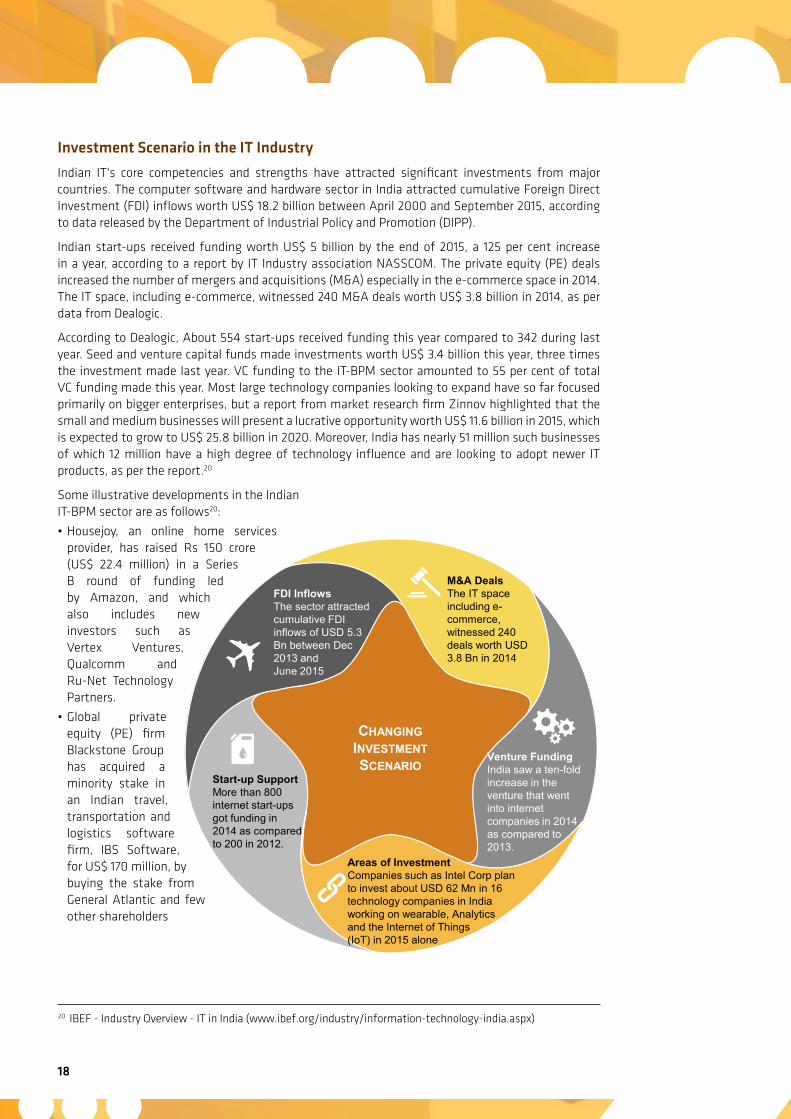

Investment Scenario in the IT Industry

Indian IT's core competencies and strengths have attracted significant investments from major countries. The computer software and hardware sector in India attracted cumulative Foreign Direct Investment (FDI) inflows worth US$ 18.2 billion between April 2000 and September 2015, according to data released by the Department of Industrial Policy and Promotion (DIPP).

Indian start-ups received funding worth US$ 5 billion by the end of 2015, a 125 per cent increase in a year, according to a report by IT Industry association NASSCOM. The private equity (PE) deals increased the number of mergers and acquisitions (M&A) especially in the e-commerce space in 2014. The IT space, including e-commerce, witnessed 240 M&A deals worth US$ 3.8 billion in 2014, as per data from Dealogic.

According to Dealogic, About 554 start-ups received funding this year compared to 342 during last year. Seed and venture capital funds made investments worth US$ 3.4 billion this year, three times the investment made last year. VC funding to the IT-BPM sector amounted to 55 per cent of total VC funding made this year. Most large technology companies looking to expand have so far focused primarily on bigger enterprises, but a report from market research firm Zinnov highlighted that the small and medium businesses will present a lucrative opportunity worth US$ 11.6 billion in 2015, which is expected to grow to US$ 25.8 billion in 2020. Moreover, India has nearly 51 million such businesses of which 12 million have a high degree of technology influence and are looking to adopt newer IT products, as per the report.20

Some illustrative developments in the Indian IT-BPM sector are as follows20:

• Housejoy, an online home services provider, has raised Rs 150 crore (US$ 22.4 million) in a Series B round of funding led by Amazon, and which also includes new investors such as Vertex Ventures, Qualcomm and Ru-Net Technology Partners.

• Global private equity (PE) firm Blackstone Group has acquired a minority stake in an Indian travel, transportation and logistics software firm, IBS Software, for US$ 170 million, by buying the stake from General Atlantic and few other shareholders

20 IBEF - Industry Overview - IT in India (www.ibef.org/industry/information-technology-india.aspx)

CHANGING INVESTMENT SCENARIO

M&A Deals The IT space including e-commerce, witnessed 240 deals worth USD 3.8 Bn in 2014

Venture Funding India saw a ten-fold increase in the venture that went into internet companies in 2014 as compared to 2013.

Areas of Investment Companies such as Intel Corp plan to invest about USD 62 Mn in 16 technology companies in India working on wearable, Analytics and the Internet of Things (IoT) in 2015 alone

Start-up Support More than 800 internet start-ups got funding in 2014 as compared to 200 in 2012.

FDI Inflows The sector attracted cumulative FDI inflows of USD 5.3 Bn between Dec 2013 and June 2015

Analysis of Talent Demand and Supply 19

• India’s top-tier information technology (IT) company, Infosys Ltd, has bought a minority stake worth US$ 3 million in Whoop, which is a US-based start-up that makes activity trackers worn by athletes.

• Microsoft Ventures is planning to incubate 500 start-ups in India in the next five years with a vision to create a viable and profitable business out of the booming start-up sector in India.

• National Association of Software and Services Companies (NASSCOM) plans to open four more tech start-up incubation centres in different parts of India, in addition to existing three, in support of Government of India’s ‘Start-up India’ initiative.

• Infosys, India’s second largest Information Technology services company has acquired US-based Noah Consulting, a provider of advanced information management consulting services for the oil and gas industry.

• US-based Callidus Software Inc, a cloud-based sales, marketing, learning and customer experience solutions provider, has opened its centre in Hyderabad and also launched its ‘The Lead to Money’ suite in Indian markets.

Shifting focus of delivery locations

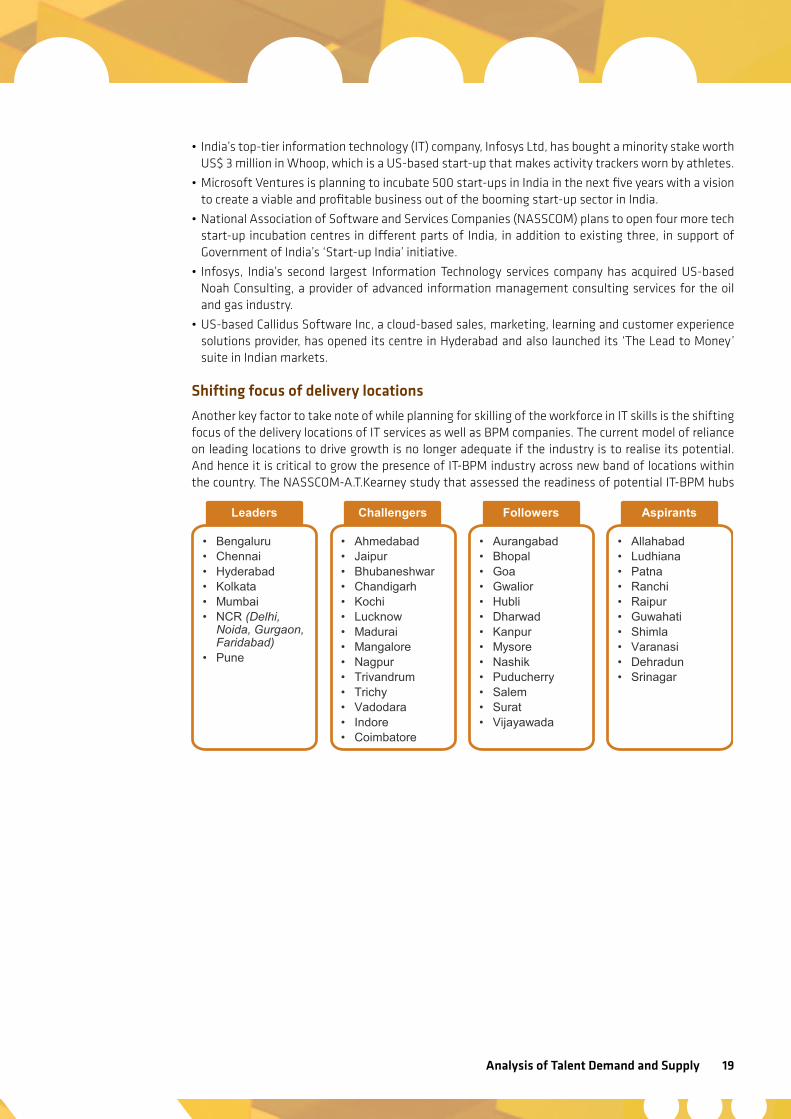

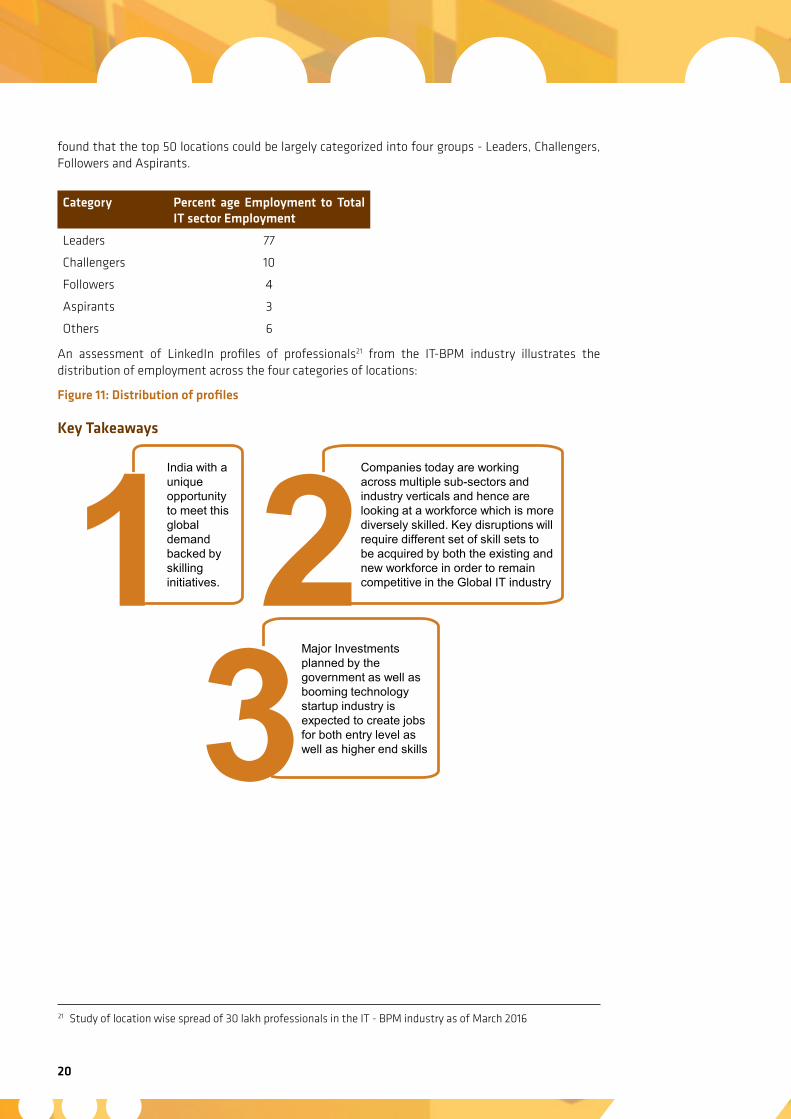

Another key factor to take note of while planning for skilling of the workforce in IT skills is the shifting focus of the delivery locations of IT services as well as BPM companies. The current model of reliance on leading locations to drive growth is no longer adequate if the industry is to realise its potential. And hence it is critical to grow the presence of IT-BPM industry across new band of locations within the country. The NASSCOM-A.T.Kearney study that assessed the readiness of potential IT-BPM hubs

Leaders

• Bengaluru • Chennai • Hyderabad • Kolkata • Mumbai • NCR (Delhi,

Noida, Gurgaon, Faridabad)

• Pune

Challengers

• Ahmedabad • Jaipur • Bhubaneshwar • Chandigarh • Kochi • Lucknow • Madurai • Mangalore • Nagpur • Trivandrum • Trichy • Vadodara • Indore • Coimbatore

Followers

• Aurangabad • Bhopal • Goa • Gwalior • Hubli • Dharwad • Kanpur • Mysore • Nashik • Puducherry • Salem • Surat • Vijayawada

Aspirants

• Allahabad • Ludhiana • Patna • Ranchi • Raipur • Guwahati • Shimla • Varanasi • Dehradun • Srinagar

20

found that the top 50 locations could be largely categorized into four groups - Leaders, Challengers, Followers and Aspirants.

An assessment of LinkedIn profiles of professionals21 from the IT-BPM industry illustrates the distribution of employment across the four categories of locations:

Figure 11: Distribution of profiles

Key Takeaways

Category Percent age Employment to Total IT sector Employment

Leaders 77

Challengers 10

Followers 4

Aspirants 3

Others 6

21 Study of location wise spread of 30 lakh professionals in the IT - BPM industry as of March 2016

India with a unique opportunity to meet this global demand backed by skilling initiatives. 1

Companies today are working across multiple sub-sectors and industry verticals and hence are looking at a workforce which is more diversely skilled. Key disruptions will require different set of skill sets to be acquired by both the existing and new workforce in order to remain competitive in the Global IT industry 2

Major Investments planned by the government as well as booming technology startup industry is expected to create jobs for both entry level as well as higher end skills 3

Analysis of Talent Demand and Supply 21

Analysis of Demand for TalentOverview of Indian IT Industry

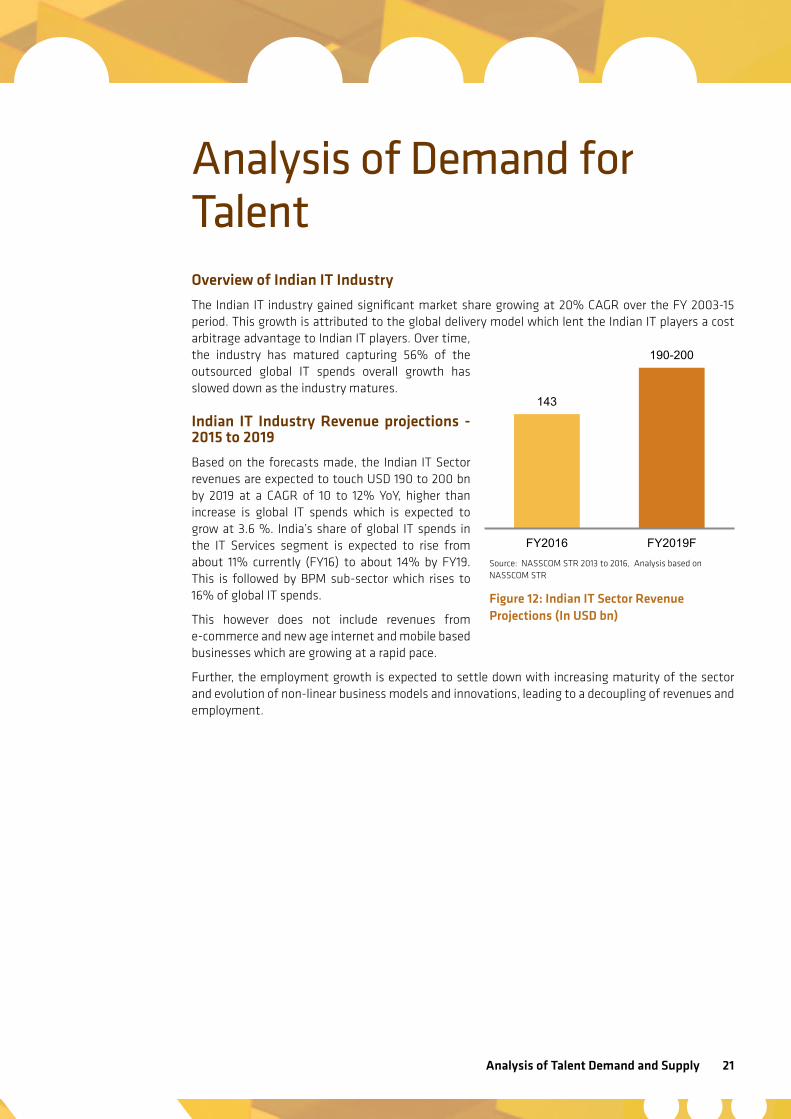

The Indian IT industry gained significant market share growing at 20% CAGR over the FY 2003-15 period. This growth is attributed to the global delivery model which lent the Indian IT players a cost arbitrage advantage to Indian IT players. Over time, the industry has matured capturing 56% of the outsourced global IT spends overall growth has slowed down as the industry matures.

Indian IT Industry Revenue projections - 2015 to 2019

Based on the forecasts made, the Indian IT Sector revenues are expected to touch USD 190 to 200 bn by 2019 at a CAGR of 10 to 12% YoY, higher than increase is global IT spends which is expected to grow at 3.6 %. India’s share of global IT spends in the IT Services segment is expected to rise from about 11% currently (FY16) to about 14% by FY19. This is followed by BPM sub-sector which rises to 16% of global IT spends.

This however does not include revenues from e-commerce and new age internet and mobile based businesses which are growing at a rapid pace.

Further, the employment growth is expected to settle down with increasing maturity of the sector and evolution of non-linear business models and innovations, leading to a decoupling of revenues and employment.

Source: NASSCOM STR 2013 to 2016, Analysis based on NASSCOM STR

Figure 12: Indian IT Sector Revenue Projections (In USD bn)

143

190-200

FY2016 FY2019F

22

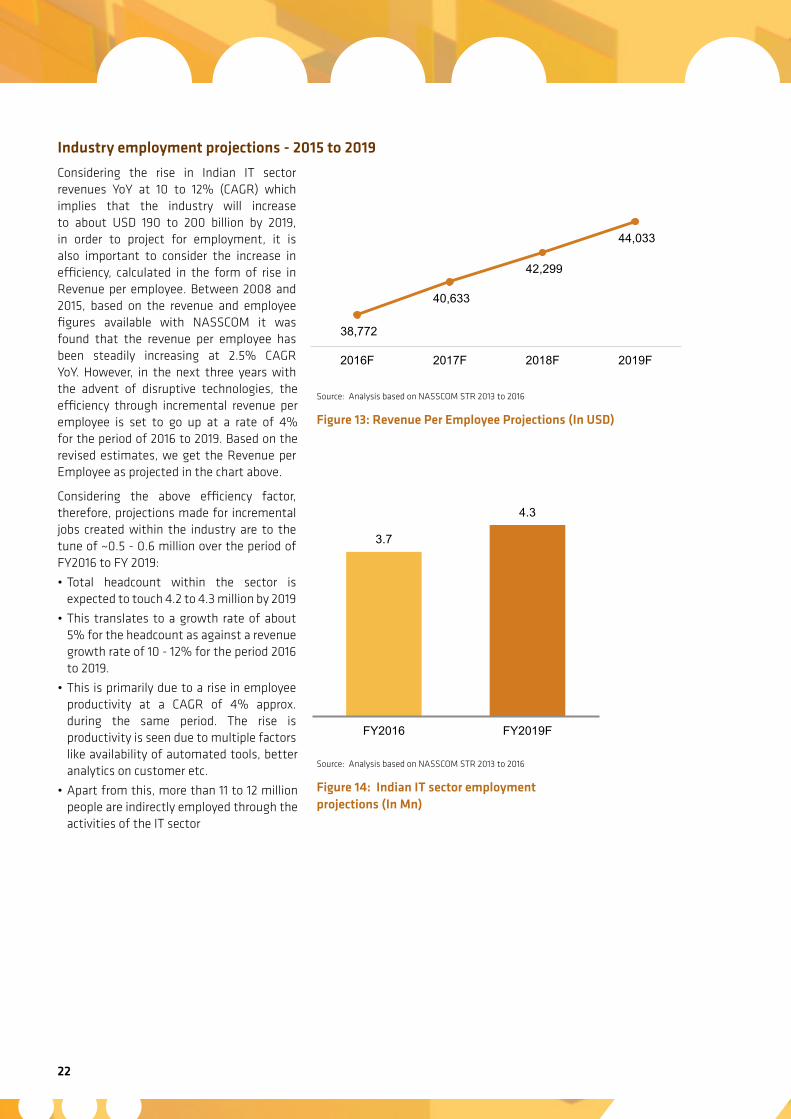

Industry employment projections - 2015 to 2019

Considering the rise in Indian IT sector revenues YoY at 10 to 12% (CAGR) which implies that the industry will increase to about USD 190 to 200 billion by 2019, in order to project for employment, it is also important to consider the increase in efficiency, calculated in the form of rise in Revenue per employee. Between 2008 and 2015, based on the revenue and employee figures available with NASSCOM it was found that the revenue per employee has been steadily increasing at 2.5% CAGR YoY. However, in the next three years with the advent of disruptive technologies, the efficiency through incremental revenue per employee is set to go up at a rate of 4% for the period of 2016 to 2019. Based on the revised estimates, we get the Revenue per Employee as projected in the chart above.

Considering the above efficiency factor, therefore, projections made for incremental jobs created within the industry are to the tune of ~0.5 - 0.6 million over the period of FY2016 to FY 2019:

• Total headcount within the sector is expected to touch 4.2 to 4.3 million by 2019

• This translates to a growth rate of about 5% for the headcount as against a revenue growth rate of 10 - 12% for the period 2016 to 2019.

• This is primarily due to a rise in employee productivity at a CAGR of 4% approx. during the same period. The rise is productivity is seen due to multiple factors like availability of automated tools, better analytics on customer etc.

• Apart from this, more than 11 to 12 million people are indirectly employed through the activities of the IT sector

Source: Analysis based on NASSCOM STR 2013 to 2016

Figure 13: Revenue Per Employee Projections (In USD)

Source: Analysis based on NASSCOM STR 2013 to 2016

Figure 14: Indian IT sector employment projections (In Mn)

38,772

40,633

42,299

44,033

2016F 2017F 2018F 2019F

3.7

4.3

FY2016 FY2019F

Analysis of Talent Demand and Supply 23

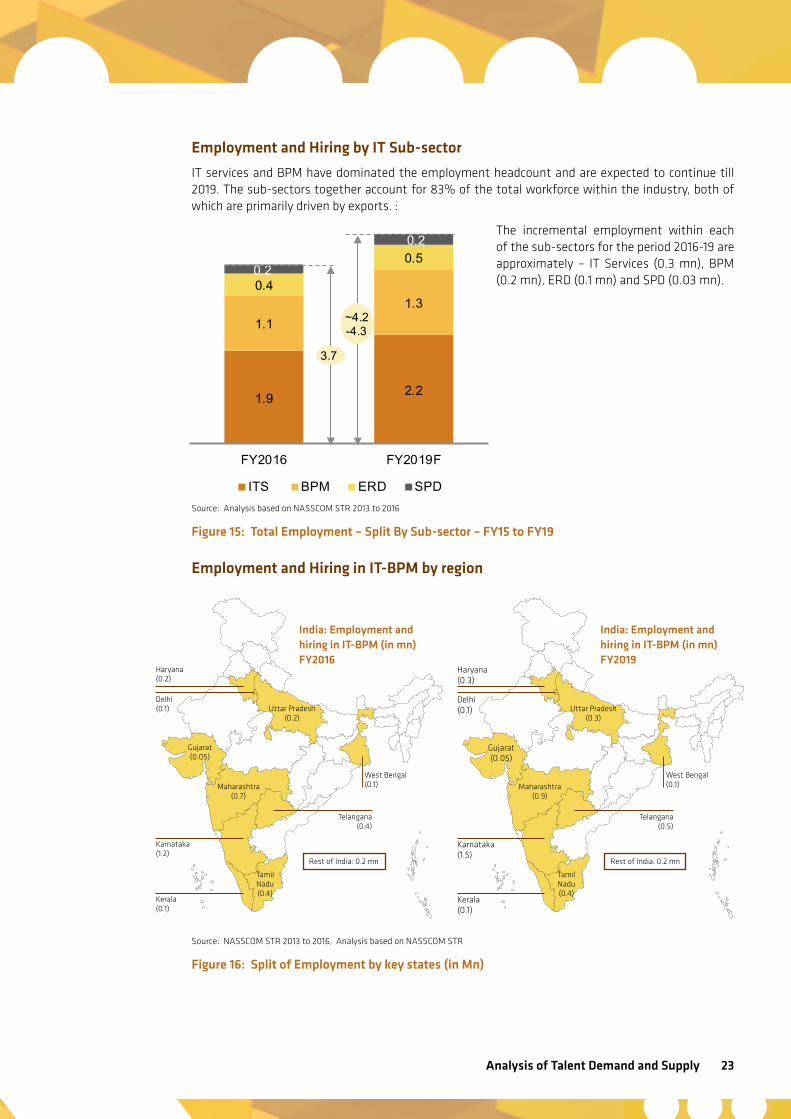

Employment and Hiring by IT Sub-sector

IT services and BPM have dominated the employment headcount and are expected to continue till 2019. The sub-sectors together account for 83% of the total workforce within the industry, both of which are primarily driven by exports. :

The incremental employment within each of the sub-sectors for the period 2016-19 are approximately – IT Services (0.3 mn), BPM (0.2 mn), ERD (0.1 mn) and SPD (0.03 mn).

Employment and Hiring in IT-BPM by region

Source: NASSCOM STR 2013 to 2016, Analysis based on NASSCOM STR

Figure 16: Split of Employment by key states (in Mn)

Source: Analysis based on NASSCOM STR 2013 to 2016

Figure 15: Total Employment – Split By Sub-sector – FY15 to FY19

Haryana (0.3)

Delhi (0.1)

Kerala (0.1)

Telangana (0.5)

Tamil Nadu (0.4)

Maharashtra (0.9)

Gujarat (0.05)

Karnataka(1.5)

Rest of India: 0.2 mn

India: Employment and hiring in IT-BPM (in mn) FY2019

Uttar Pradesh (0.3)

West Bengal (0.1)

Haryana (0.2)

Delhi (0.1)

Kerala (0.1)

Telangana (0.4)

Tamil Nadu (0.4)

Maharashtra (0.7)

Gujarat (0.05)

Karnataka(1.2)

Rest of India: 0.2 mn

India: Employment and hiring in IT-BPM (in mn) FY2016

Uttar Pradesh (0.2)

West Bengal (0.1)

1.9 2.2

1.11.3

0.4

0.50.2

0.2

FY2016 FY2019F

ITS BPM ERD SPD

3.7

~4.2-4.3

24

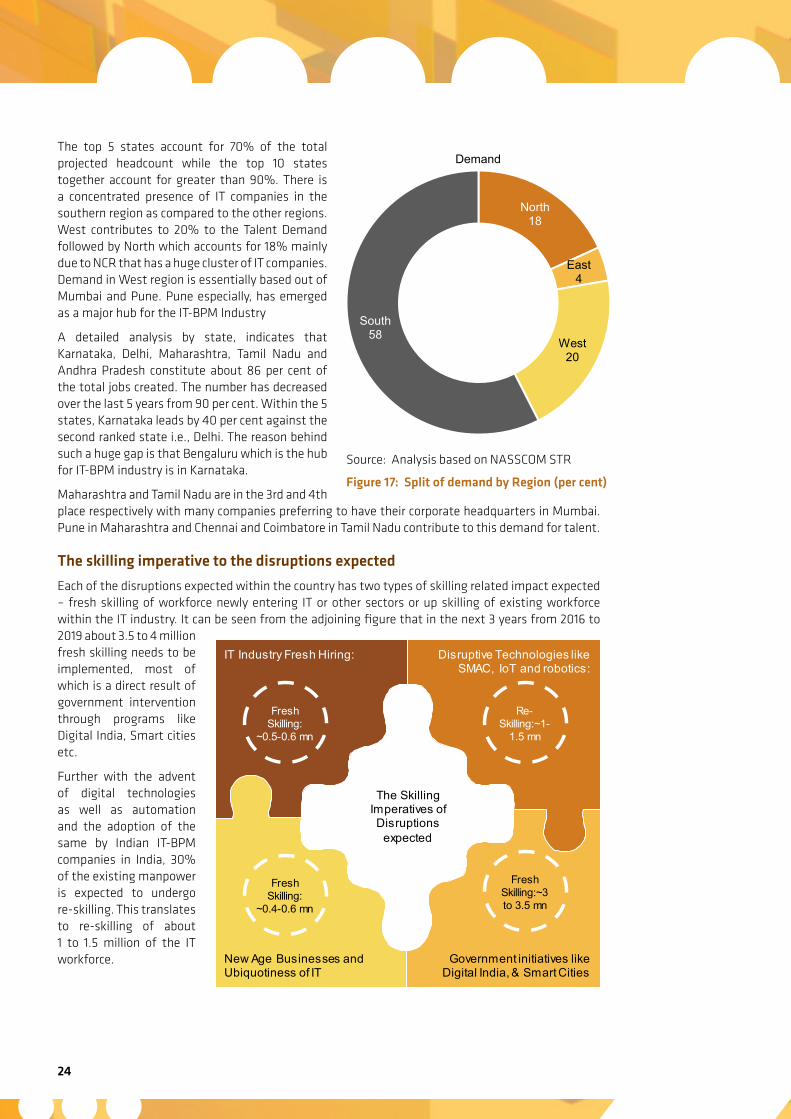

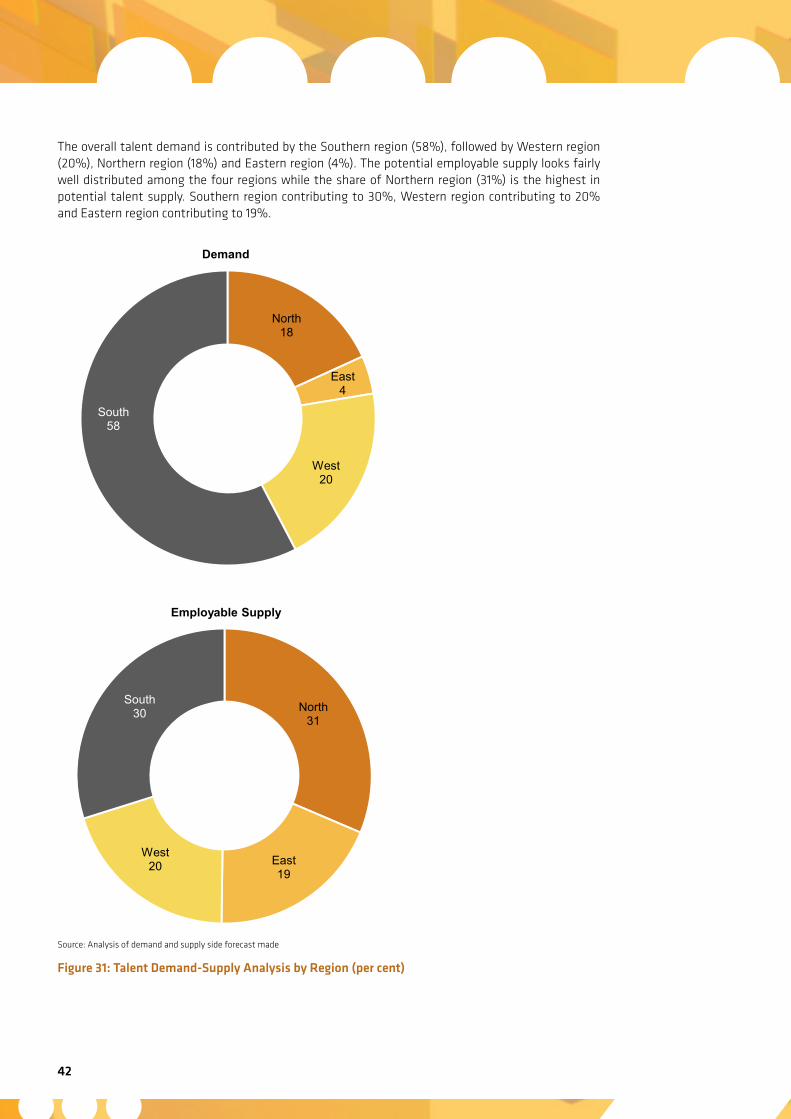

The top 5 states account for 70% of the total projected headcount while the top 10 states together account for greater than 90%. There is a concentrated presence of IT companies in the southern region as compared to the other regions. West contributes to 20% to the Talent Demand followed by North which accounts for 18% mainly due to NCR that has a huge cluster of IT companies. Demand in West region is essentially based out of Mumbai and Pune. Pune especially, has emerged as a major hub for the IT-BPM Industry

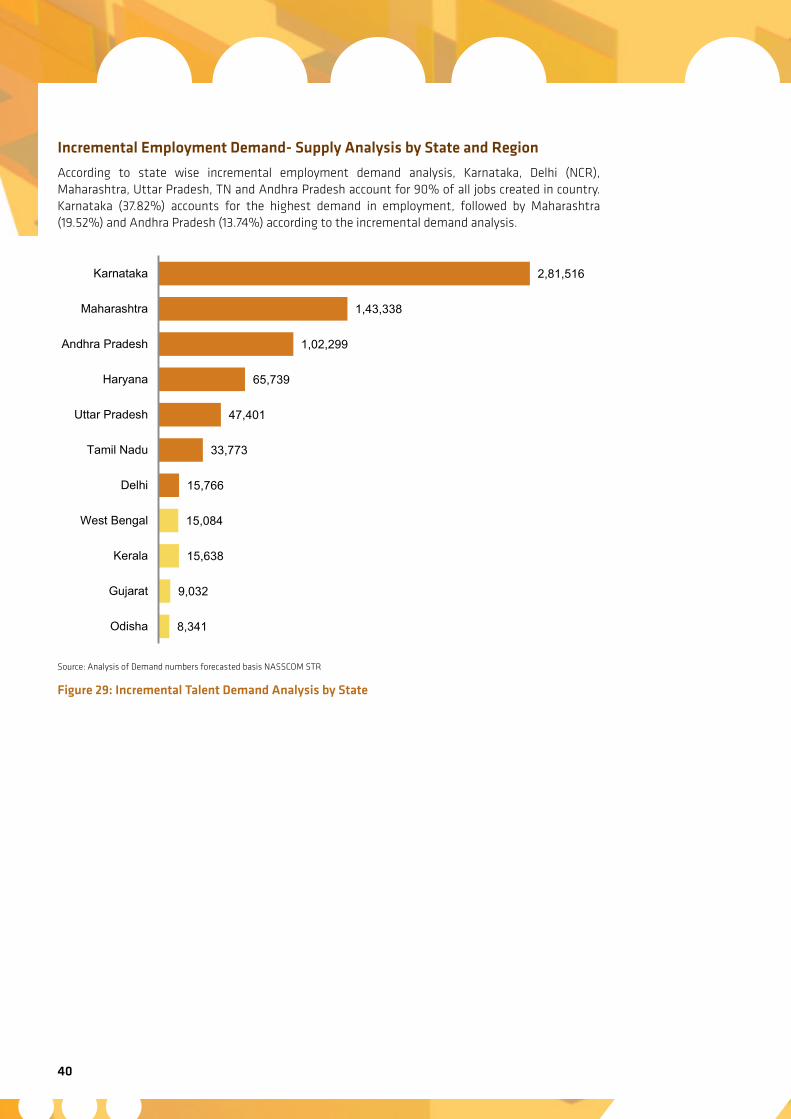

A detailed analysis by state, indicates that Karnataka, Delhi, Maharashtra, Tamil Nadu and Andhra Pradesh constitute about 86 per cent of the total jobs created. The number has decreased over the last 5 years from 90 per cent. Within the 5 states, Karnataka leads by 40 per cent against the second ranked state i.e., Delhi. The reason behind such a huge gap is that Bengaluru which is the hub for IT-BPM industry is in Karnataka.

Maharashtra and Tamil Nadu are in the 3rd and 4th place respectively with many companies preferring to have their corporate headquarters in Mumbai. Pune in Maharashtra and Chennai and Coimbatore in Tamil Nadu contribute to this demand for talent.

The skilling imperative to the disruptions expected

Each of the disruptions expected within the country has two types of skilling related impact expected – fresh skilling of workforce newly entering IT or other sectors or up skilling of existing workforce within the IT industry. It can be seen from the adjoining figure that in the next 3 years from 2016 to 2019 about 3.5 to 4 million fresh skilling needs to be implemented, most of which is a direct result of government intervention through programs like Digital India, Smart cities etc.

Further with the advent of digital technologies as well as automation and the adoption of the same by Indian IT-BPM companies in India, 30% of the existing manpower is expected to undergo re-skilling. This translates to re-skilling of about 1 to 1.5 million of the IT workforce.

Disruptive Technologies like SMAC, IoT and robotics:

Government initiatives like Digital India, & Smart Cities

New Age Businesses and Ubiquotiness of IT

IT Industry Fresh Hiring:

The Skilling Imperatives of Disruptions

expected

Fresh Skilling:

~0.5-0.6 mn

Re-Skilling:~1-

1.5 mn

Fresh Skilling:~3 to 3.5 mn

Fresh Skilling:

~0.4-0.6 mn

Source: Analysis based on NASSCOM STR

Figure 17: Split of demand by Region (per cent)

North 18

East 4

West 20

South 58

Demand

Analysis of Talent Demand and Supply 25

High Demand Occupations and New age Skills

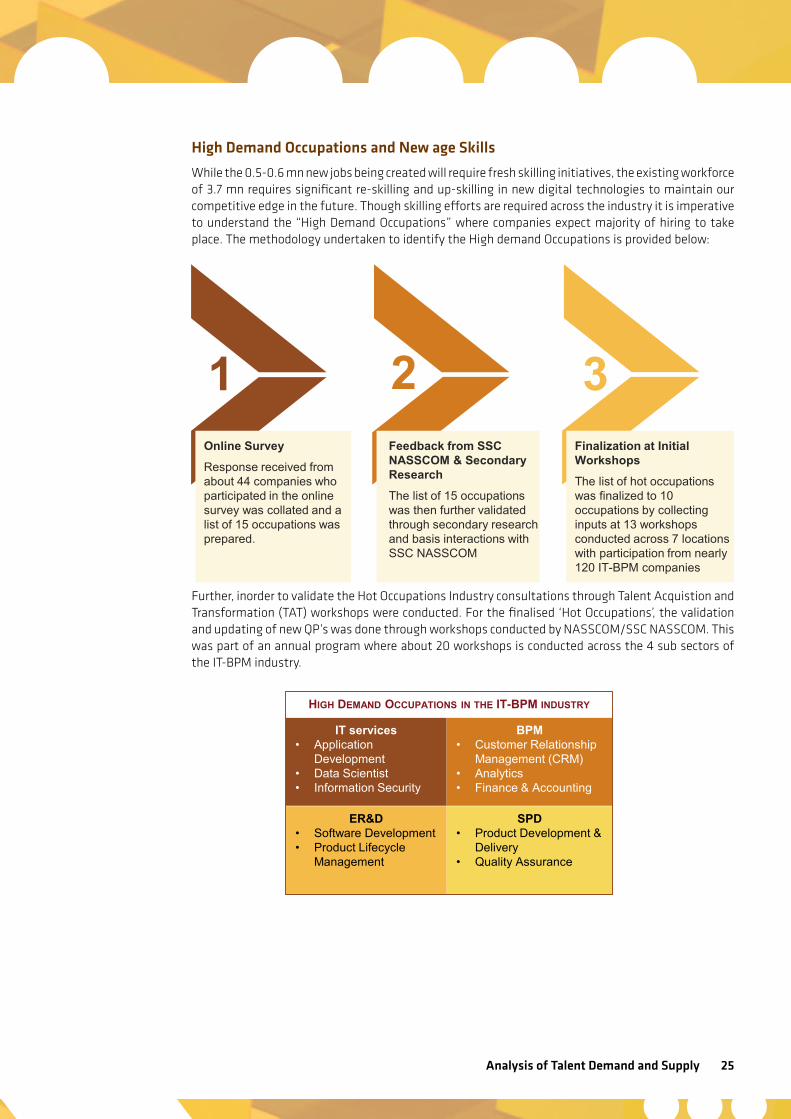

While the 0.5-0.6 mn new jobs being created will require fresh skilling initiatives, the existing workforce of 3.7 mn requires significant re-skilling and up-skilling in new digital technologies to maintain our competitive edge in the future. Though skilling efforts are required across the industry it is imperative to understand the “High Demand Occupations” where companies expect majority of hiring to take place. The methodology undertaken to identify the High demand Occupations is provided below:

Further, inorder to validate the Hot Occupations Industry consultations through Talent Acquistion and Transformation (TAT) workshops were conducted. For the finalised ‘Hot Occupations’, the validation and updating of new QP’s was done through workshops conducted by NASSCOM/SSC NASSCOM. This was part of an annual program where about 20 workshops is conducted across the 4 sub sectors of the IT-BPM industry.

IT services • Application

Development • Data Scientist • Information Security

SPD

• Product Development & Delivery

• Quality Assurance

ER&D • Software Development • Product Lifecycle

Management

BPM • Customer Relationship

Management (CRM) • Analytics • Finance & Accounting

HIGH DEMAND OCCUPATIONS IN THE IT-BPM INDUSTRY

Online Survey Response received from about 44 companies who participated in the online survey was collated and a list of 15 occupations was prepared.

1 Feedback from SSC NASSCOM & Secondary Research The list of 15 occupations was then further validated through secondary research and basis interactions with SSC NASSCOM

Finalization at Initial Workshops The list of hot occupations was finalized to 10 occupations by collecting inputs at 13 workshops conducted across 7 locations with participation from nearly 120 IT-BPM companies

2 3

26

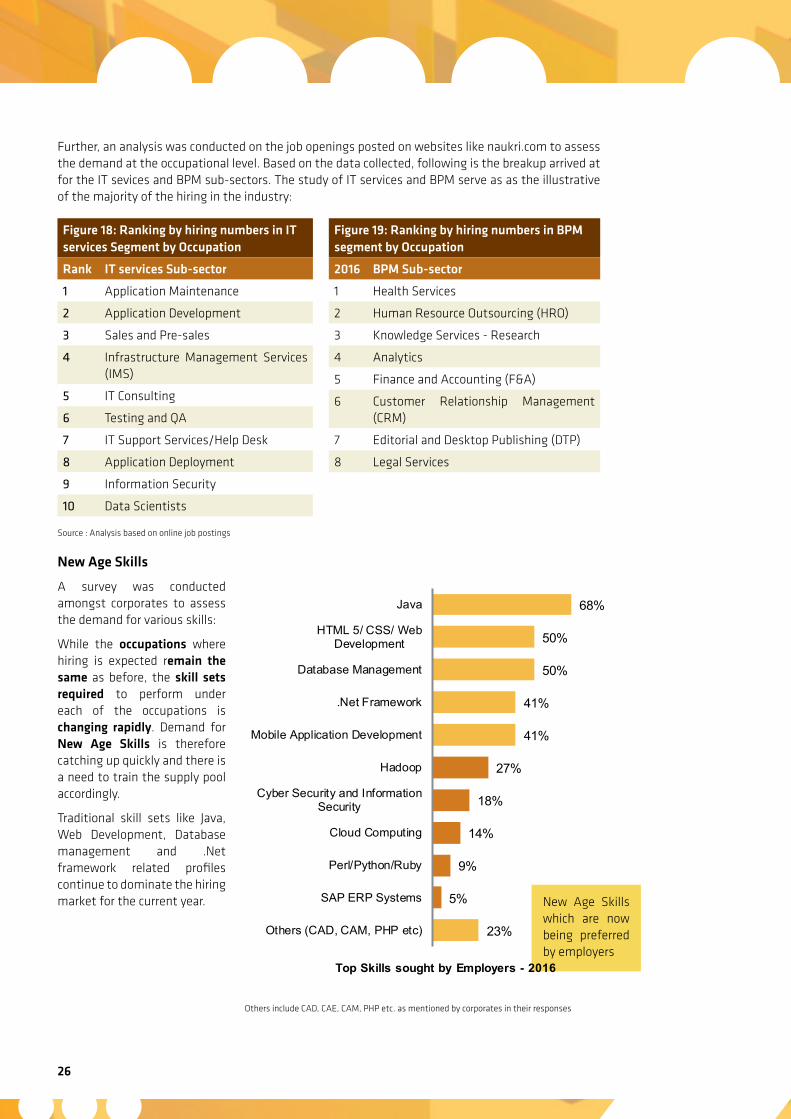

Further, an analysis was conducted on the job openings posted on websites like naukri.com to assess the demand at the occupational level. Based on the data collected, following is the breakup arrived at for the IT sevices and BPM sub-sectors. The study of IT services and BPM serve as as the illustrative of the majority of the hiring in the industry:

Source : Analysis based on online job postings

New Age Skills

A survey was conducted amongst corporates to assess the demand for various skills:

While the occupations where hiring is expected remain the same as before, the skill sets required to perform under each of the occupations is changing rapidly. Demand for New Age Skills is therefore catching up quickly and there is a need to train the supply pool accordingly.

Traditional skill sets like Java, Web Development, Database management and .Net framework related profiles continue to dominate the hiring market for the current year.

Figure 18: Ranking by hiring numbers in IT services Segment by Occupation

Rank IT services Sub-sector

1 Application Maintenance

2 Application Development

3 Sales and Pre-sales

4 Infrastructure Management Services (IMS)

5 IT Consulting

6 Testing and QA

7 IT Support Services/Help Desk

8 Application Deployment

9 Information Security

10 Data Scientists

Figure 19: Ranking by hiring numbers in BPM segment by Occupation

2016 BPM Sub-sector

1 Health Services

2 Human Resource Outsourcing (HRO)

3 Knowledge Services - Research

4 Analytics

5 Finance and Accounting (F&A)

6 Customer Relationship Management (CRM)

7 Editorial and Desktop Publishing (DTP)

8 Legal Services

Others include CAD, CAE, CAM, PHP etc. as mentioned by corporates in their responses

New Age Skills which are now being preferred by employers

23%

5%

9%

14%

18%

27%

41%

41%

50%

50%

68%

Others (CAD, CAM, PHP etc)

SAP ERP Systems

Perl/Python/Ruby

Cloud Computing

Cyber Security and InformationSecurity

Hadoop

Mobile Application Development

.Net Framework

Database Management

HTML 5/ CSS/ WebDevelopment

Java

Top Skills sought by Employers - 2016

Analysis of Talent Demand and Supply 27

Key Takeaways

About 0.5-0.6 mn direct jobs are expected to be created within the industry for which fresh skilling initiatives need to be prepared for. This will further also enhance indirect jobs which get created as a result of growing IT-BPM industry1

While the occupations where hiring is expected remain the same as before, the skill sets required to perform under each of the occupations is changing rapidly. Demand for New Age Skills is therefore catching up quickly and there is a need to train the supply pool accordingly.2

28

Analysis of Supply of TalentOverview of the National Talent Supply

India has one of the world's largest education systems, which includes 1.3 million schools, over 35,000 higher educational institutions including colleges and universities. Over the last decade, the education market, especially the higher education sector, has witnessed massive expansion in terms of growth and enrolment.National focus on education, especially higher education, is not new. Many governments of the past have understood the pivotal role it plays in shaping a nation’s socio-economic makeup. In recent times, several big-ticket reforms and progressive initiatives have been ideated on and discussed to strengthen the sector and its preparedness for future opportunities.

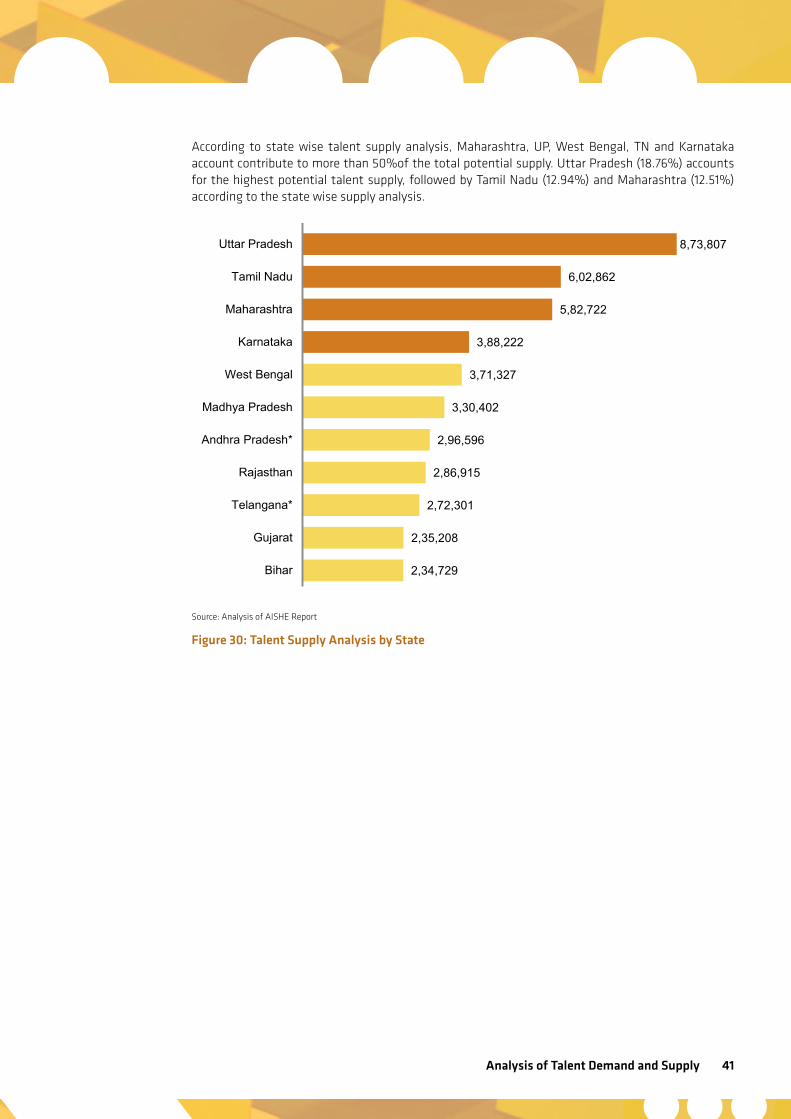

The announcement by the Centre in the Union budget 2015 to establish new institutes of excellence including IIMs and IITs in the country, setting up of financing authority, extending additional funds for infrastructural development of institutions of national importance, amongst others, are expected to essay a new storyline for the higher education sector in the country. At the statelevel, the states of UP, Tamil Nadu, Maharashtra, amongst others are some of the leading states in terms of students enrolment in higher educational institutions. Five southern states led by Tamil Nadu and Karnataka accounts for almost 30 percent of total enrolments in the country.

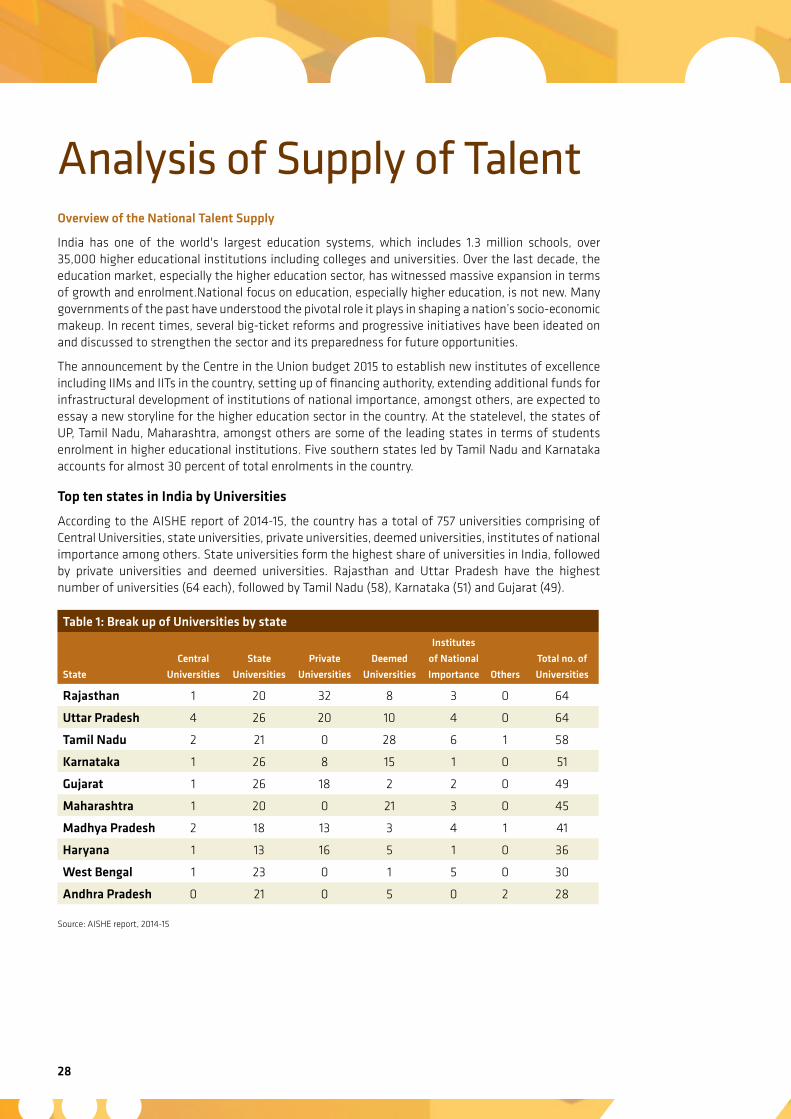

Top ten states in India by Universities

According to the AISHE report of 2014-15, the country has a total of 757 universities comprising of Central Universities, state universities, private universities, deemed universities, institutes of national importance among others. State universities form the highest share of universities in India, followed by private universities and deemed universities. Rajasthan and Uttar Pradesh have the highest number of universities (64 each), followed by Tamil Nadu (58), Karnataka (51) and Gujarat (49).

Source: AISHE report, 2014-15

Table 1: Break up of Universities by state

State

Central

Universities

State

Universities

Private

Universities

Deemed

Universities

Institutes

of National

Importance Others

Total no. of

Universities

Rajasthan 1 20 32 8 3 0 64

Uttar Pradesh 4 26 20 10 4 0 64

Tamil Nadu 2 21 0 28 6 1 58

Karnataka 1 26 8 15 1 0 51

Gujarat 1 26 18 2 2 0 49

Maharashtra 1 20 0 21 3 0 45

Madhya Pradesh 2 18 13 3 4 1 41

Haryana 1 13 16 5 1 0 36

West Bengal 1 23 0 1 5 0 30

Andhra Pradesh 0 21 0 5 0 2 28

Analysis of Talent Demand and Supply 29

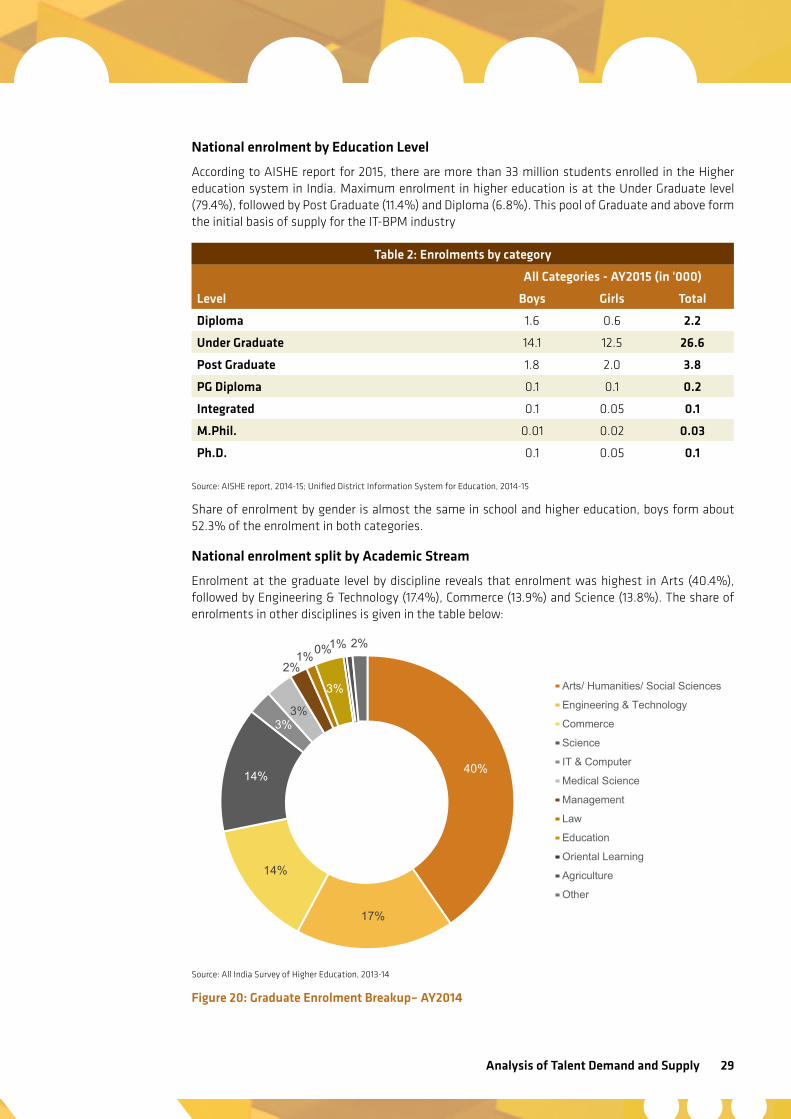

National enrolment by Education Level

According to AISHE report for 2015, there are more than 33 million students enrolled in the Higher education system in India. Maximum enrolment in higher education is at the Under Graduate level (79.4%), followed by Post Graduate (11.4%) and Diploma (6.8%). This pool of Graduate and above form the initial basis of supply for the IT-BPM industry

Source: AISHE report, 2014-15; Unified District Information System for Education, 2014-15

Share of enrolment by gender is almost the same in school and higher education, boys form about 52.3% of the enrolment in both categories.

National enrolment split by Academic Stream

Enrolment at the graduate level by discipline reveals that enrolment was highest in Arts (40.4%), followed by Engineering & Technology (17.4%), Commerce (13.9%) and Science (13.8%). The share of enrolments in other disciplines is given in the table below:

Source: All India Survey of Higher Education, 2013-14

Figure 20: Graduate Enrolment Breakup– AY2014

Table 2: Enrolments by category

All Categories - AY2015 (in '000)

Level Boys Girls Total

Diploma 1.6 0.6 2.2

Under Graduate 14.1 12.5 26.6

Post Graduate 1.8 2.0 3.8

PG Diploma 0.1 0.1 0.2

Integrated 0.1 0.05 0.1

M.Phil. 0.01 0.02 0.03

Ph.D. 0.1 0.05 0.1

40%

17%

14%

14%

3% 3%

2% 1%

3%

0% 1% 2%

Arts/ Humanities/ Social Sciences

Engineering & Technology

Commerce

Science

IT & Computer

Medical Science

Management

Law

Education

Oriental Learning

Agriculture

Other

30

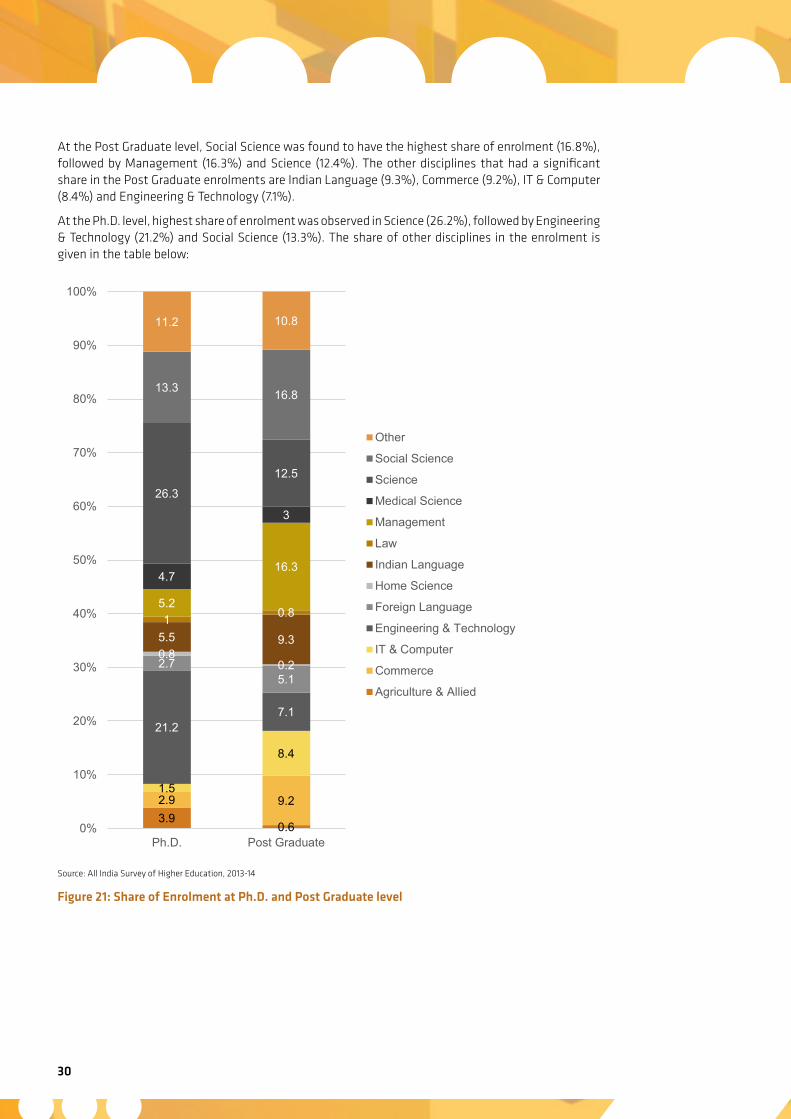

At the Post Graduate level, Social Science was found to have the highest share of enrolment (16.8%), followed by Management (16.3%) and Science (12.4%). The other disciplines that had a significant share in the Post Graduate enrolments are Indian Language (9.3%), Commerce (9.2%), IT & Computer (8.4%) and Engineering & Technology (7.1%).

At the Ph.D. level, highest share of enrolment was observed in Science (26.2%), followed by Engineering & Technology (21.2%) and Social Science (13.3%). The share of other disciplines in the enrolment is given in the table below:

Source: All India Survey of Higher Education, 2013-14

Figure 21: Share of Enrolment at Ph.D. and Post Graduate level

3.9 0.6

2.9 9.2 1.5

8.4

21.2 7.1

2.7 5.1

0.8 0.2

5.5 9.3 1 0.8

5.2

16.3 4.7

3

26.3 12.5

13.3 16.8

11.2 10.8

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Ph.D. Post Graduate

Other

Social Science

Science

Medical Science

Management

Law