Embed Size (px)

DESCRIPTION

A concise review on health insurance policy in India. India as of now do not have any centralized health coverage. In this slides, you will get to know what are the prevailing situations in terms of health insurance, the recommendations and suggestions.

Citation preview

HEALTH INSURANCE POLICYGROUP 6, BC2 PRESENTATION

TISS, MUMBAI

INTRODUCTION India currently spends about 6% of its GDP on health care.

Out of this more than 70% is “Out of pocket expense.”

Despite such high share of individual expenditure, provision of health care

not satisfactory.

More than 40% of hospitalized Indians have to borrow or sell assets to meet

hospitalization costs.

Around 25% of hospitalized Indians fall below poverty line in a single year as

a result of hospitalization expenses, causing a rise of 2% in proportion of

poor population.

Therefore, urgent need for alternative mechanism for meeting health care

needs of poor in India.

Table 1: Estimate of total health expenditure in India (1990-91)

PUBLIC SECTOR

Sub Total 5,779 68.8 21.5 1.3

PRIVATE SECTOR

Sub Total 21,042 250.5 78.5 4.7

TOTAL 26, 821 319.3 100.0 6.0

Centre

Municipalities

External aid

State

Out-of-pocket

Private employers

ESIS contributions

Other sources

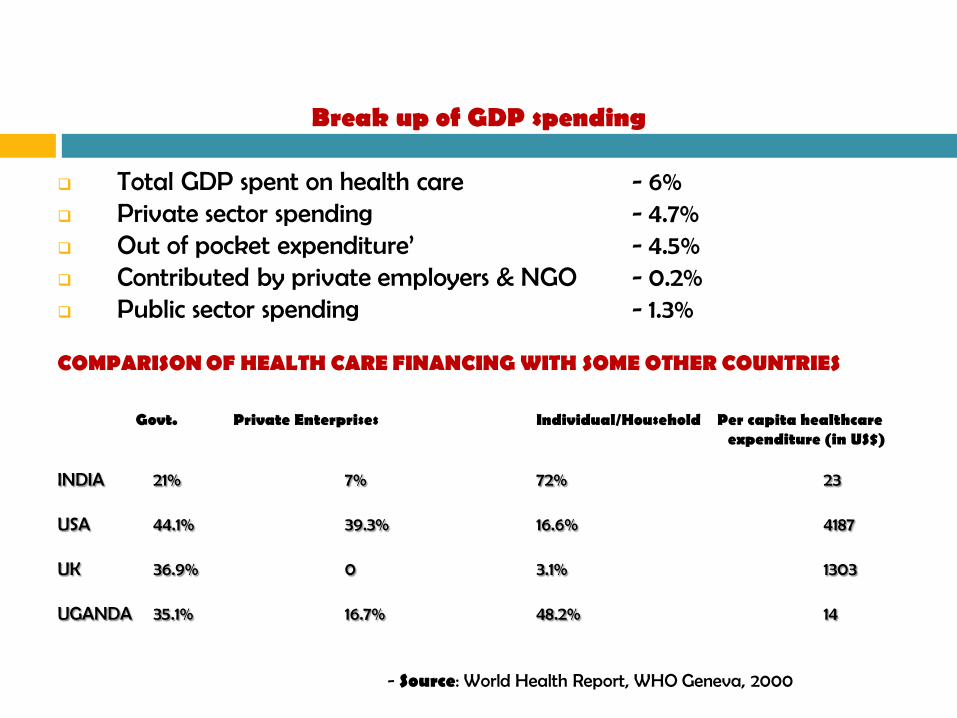

Break up of GDP spending

Total GDP spent on health care - 6% Private sector spending - 4.7% Out of pocket expenditure’ - 4.5% Contributed by private employers & NGO - 0.2% Public sector spending - 1.3%

COMPARISON OF HEALTH CARE FINANCING WITH SOME OTHER COUNTRIES

Govt. Private Enterprises Individual/Household Per capita healthcare expenditure (in US$)

INDIA 21% 7% 72% 23

USA 44.1% 39.3% 16.6% 4187

UK 36.9% 0 3.1% 1303

UGANDA 35.1% 16.7% 48.2% 14

- Source: World Health Report, WHO Geneva, 2000

Health Insurance

Definition

Individuals or families pay when they are healthy and able to pay and when affected by illness, health insurance fund used to finance their health care needs.

Some important values of Health Insurance are:

Some risks that are peculiar to health insurance:

1. Social Health Insurance:

2. Community Health Insurance:

3. Private Health Insurance:

TYPES OF HEALTH INSURANCE

HISTORY OF HEALTH INSURANCE IN INDIA

Present state of health insurance in India

Residence % covered ESIS CGHS Community Other Medical Privatelyby scheme Health employee Reimbursement Purchased

based

OBJECTIVES

To improve the equity, efficiency and quality of health

care distribution and services.

To develop an alternative mechanism for healthcare

funding to cater the need.

To bring more people under the purview of health

insurance under different schemes so that health care is

accessible to all irrespective of their paying capacity.

CGHS ESIS

CENTRAL GOVERNMENT HEALTH INSURANCE SCHEME

Central Government Health Insurance Scheme

The Central Govt. Health Scheme was initially started in New Delhi in 1954.

Provides comprehensive health care to the CGHS beneficiaries in India.

FEATURES

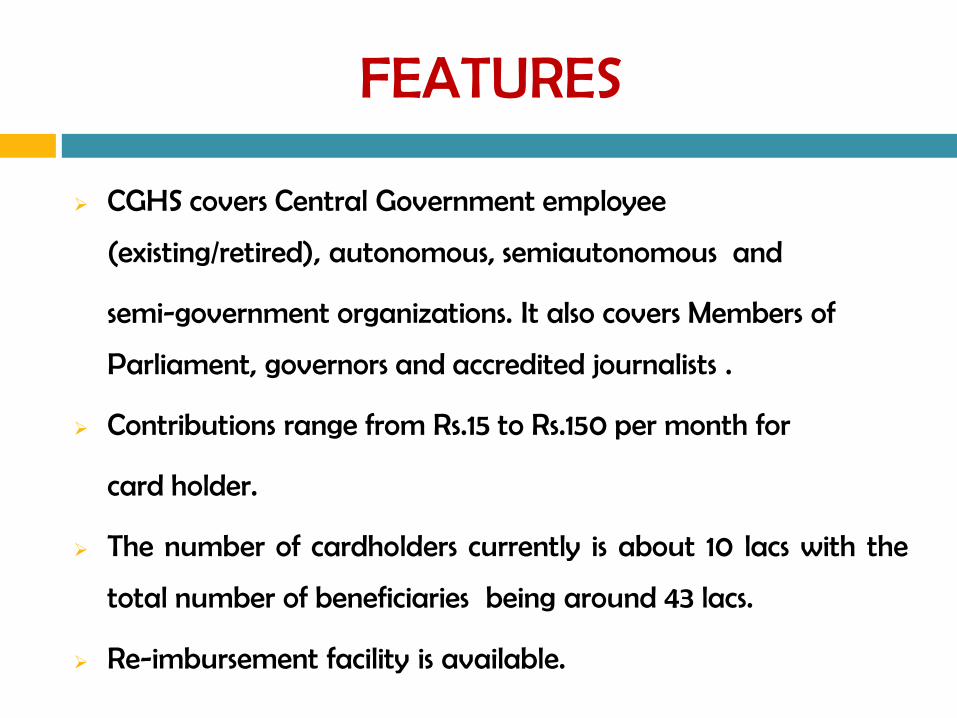

CGHS covers Central Government employee

(existing/retired), autonomous, semiautonomous and

semi-government organizations. It also covers Members of

Parliament, governors and accredited journalists .

Contributions range from Rs.15 to Rs.150 per month for

card holder.

The number of cardholders currently is about 10 lacs with the

total number of beneficiaries being around 43 lacs.

Re-imbursement facility is available.

CMO/In-charges can directly refer the beneficiaries forservices which are not available under government settings.

Cities of Operation:

Allahabad, Ahmedabad, Bangalore, Bhubhaneshwar,

Bhopal, Chandigarh, Chennai, Delhi, Dehradun, Guwahati,

Hyderabad, Jaipur, Jabalpur, Kanpur, Kolkata, Lucknow, Meerut,

Mumbai, Nagpur, Patna, Pune, Ranchi, Shillong,

Trivandrum and Jammu.

DISADVANTAGES

Criticised for quality and accessibility.

Access to specialist consultants done usually without any

referrals.

Long waiting periods.

Significant out of pocket costs of treatment.

Inadequate supplies of medicines and equipment.

Inadequate staff and conditions that are often unhygienic.

NEW MODIFICATIONS

The long standing demand from Central Govt. pensioners residing in non CGHS areas for medical services at par with those available to Central Govt Employee; The Govt. of India proposes a new scheme called Central Government Employees & Pensioners Health Insurance Scheme (CGEPHIS).

This scheme offers choice to select the best available health facilities of theCentral Government employee (existing/ retired) in their close proximity.

In addition to the coverage offered under a standard medical insurancepolicy, the following is also be covered under CGEPHIS:

Pre-existing diseases Maternity benefit Day-care coverage for all diseases New-born babies Pre and Post hospitalization cover of 30 days and 60

days respectively Domiciliary Hospitalization

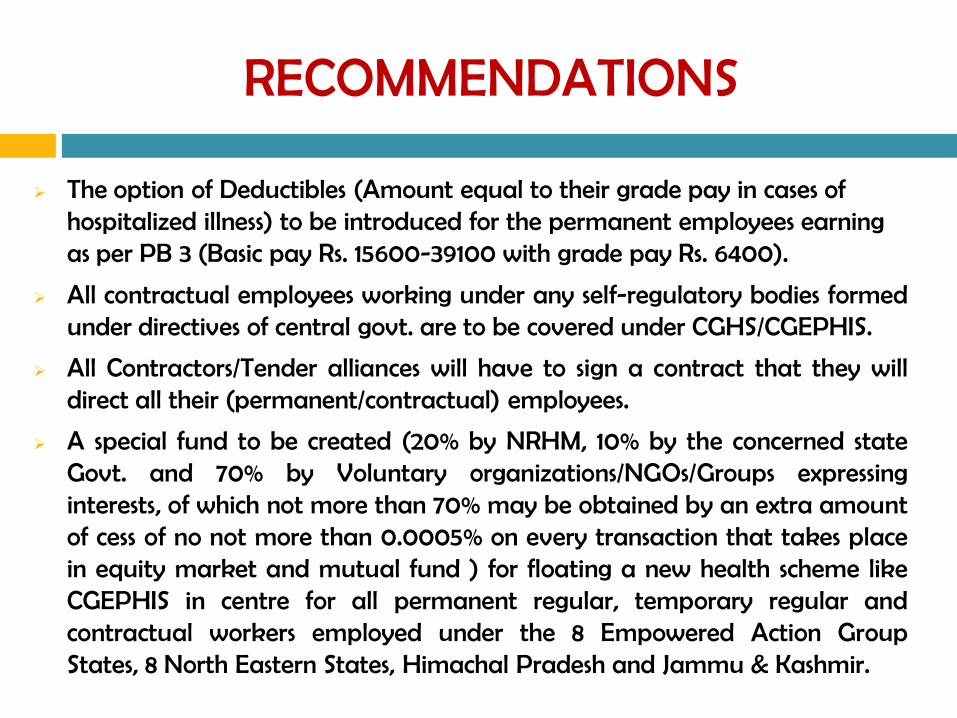

RECOMMENDATIONS

The option of Deductibles (Amount equal to their grade pay in cases of hospitalized illness) to be introduced for the permanent employees earning as per PB 3 (Basic pay Rs. 15600-39100 with grade pay Rs. 6400).

All contractual employees working under any self-regulatory bodies formedunder directives of central govt. are to be covered under CGHS/CGEPHIS.

All Contractors/Tender alliances will have to sign a contract that they willdirect all their (permanent/contractual) employees.

A special fund to be created (20% by NRHM, 10% by the concerned stateGovt. and 70% by Voluntary organizations/NGOs/Groups expressinginterests, of which not more than 70% may be obtained by an extra amountof cess of no not more than 0.0005% on every transaction that takes placein equity market and mutual fund ) for floating a new health scheme likeCGEPHIS in centre for all permanent regular, temporary regular andcontractual workers employed under the 8 Empowered Action GroupStates, 8 North Eastern States, Himachal Pradesh and Jammu & Kashmir.

Features

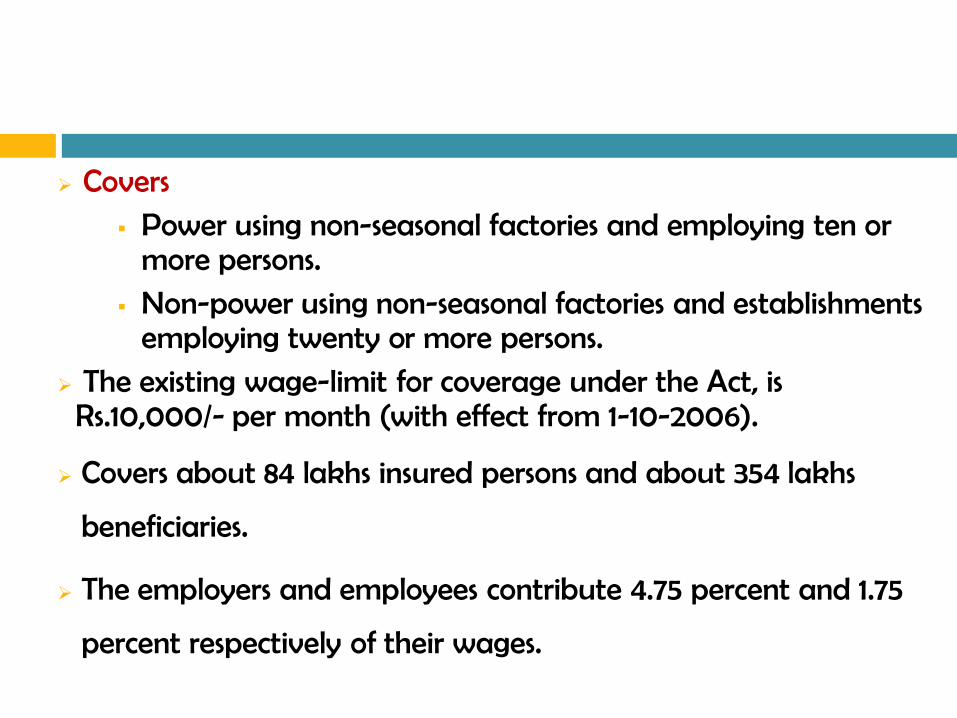

Covers Power using non-seasonal factories and employing ten or

more persons. Non-power using non-seasonal factories and establishments

employing twenty or more persons. The existing wage-limit for coverage under the Act, is

Rs.10,000/- per month (with effect from 1-10-2006).

Covers about 84 lakhs insured persons and about 354 lakhs

beneficiaries.

The employers and employees contribute 4.75 percent and 1.75

percent respectively of their wages.

Country’s largest medical infrastructural facility under one umbrella.

The most affordable system with the lowest contribution rate for

multiple health insurance benefits.

Only health insurance scheme that offers full medical care to workers

and their dependants without any ceiling on individual expenditure.

Offers a special package of full medical care to retired/disabled insured

persons for self and spouse for a nominal contribution of Rs. 120/- per

annum.

Area of operation:

All the states except Nagaland, Manipur, Tripura, Sikkim, Arunachal Pradesh and Mizoram.

COVERAGE (As on 31st March 2006)No. of Insured Person family units 91,48,605

No. of Employees 84,00,526

Total No. of Beneficiaries 3,54,96,589

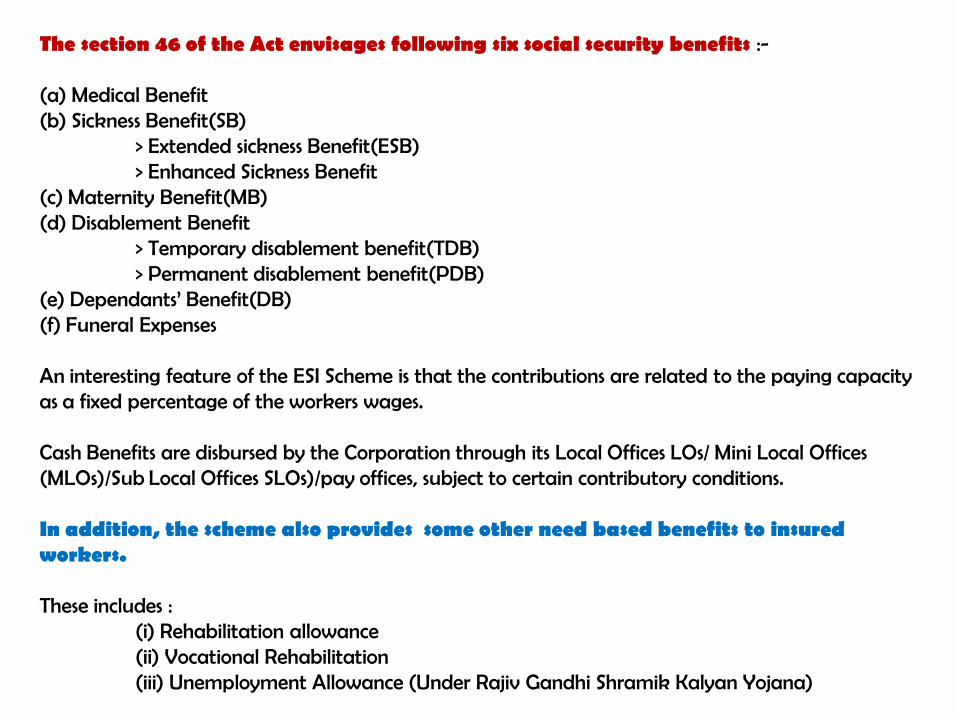

The section 46 of the Act envisages following six social security benefits :-

(a) Medical Benefit(b) Sickness Benefit(SB)

> Extended sickness Benefit(ESB)> Enhanced Sickness Benefit

(c) Maternity Benefit(MB)(d) Disablement Benefit

> Temporary disablement benefit(TDB)> Permanent disablement benefit(PDB)

(e) Dependants’ Benefit(DB)(f) Funeral Expenses

An interesting feature of the ESI Scheme is that the contributions are related to the paying capacity as a fixed percentage of the workers wages.

Cash Benefits are disbursed by the Corporation through its Local Offices LOs/ Mini Local Offices (MLOs)/Sub Local Offices SLOs)/pay offices, subject to certain contributory conditions.

In addition, the scheme also provides some other need based benefits to insured workers.

These includes :(i) Rehabilitation allowance (ii) Vocational Rehabilitation(iii) Unemployment Allowance (Under Rajiv Gandhi Shramik Kalyan Yojana)

Recommendations

Improve services provided by hospitals.

Ensure the drugs availability.

Reduce the waiting time period in hospitals.

Training to improve motivation of ESIS personnel.

Workshop to improve awareness of ESIS procedures

among employers.

PRIVATE HEALTH INSURANCE

Started in 1999 as Mediclaim

Ensure the user for access to health care whenthey need it.

Scenario

In 2001, there were 7.8 million persons covered under Mediclaim. The

subscribers are usually the middle and upper class, especially as there is a tax

benefit in subscribing to Mediclaim.

The standard Mediclaim policy covers only hospital care and domiciliary

hospitalisation benefits. Most medical conditions are reimbursed though

there are important exclusions. These include – pre-existing

diseases, pregnancy and child birth, HIV-AIDS, etc. Traditionally only

reimbursement insurance is provided, though the companies have tried a

third payment system with TPAs. Hospitals with more than 15 beds and

registered with a local authority can be identified as providers.

Components

Government

Health providers

Distributor/agents to distribute the products

Insurance products

TPA’s

Insurance Company

Regulators and regulations

Employers

Community

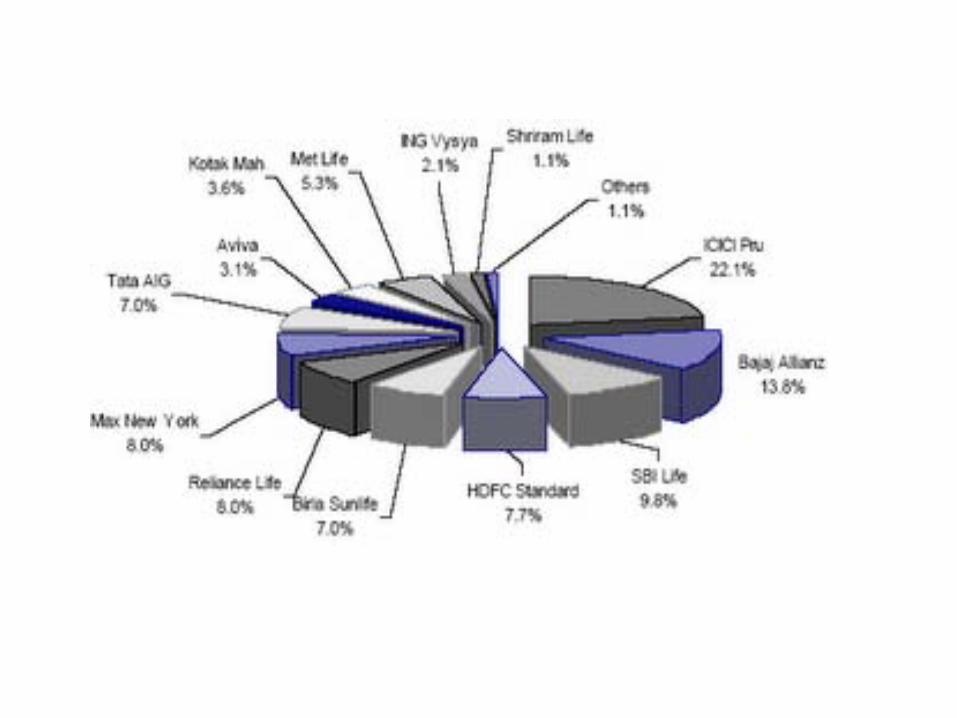

Major Providers

ICICI Prudential Life- 22.1% Bajaj Allianz- 13.8% SBI Life- 9.8% Reliance Life- 8% Max New York- 8%

Strengths of the Mediclaim policy

The only voluntary health insurance policy in the

country currently, with about 8 million subscribers.

Provides protection against catastrophic health

expenditure.

Easily available in most insurance companies.

Is being modified to make it customer friendly.

Drawbacks of Mediclaim

Most of the insurance companies are wary about selling health insurance as they do not have the data, the expertise and the power to regulate the providers.

Problems of reimbursement ranging from long delays to partial reimbursements.

There are also reported fraud and manipulation by clients and providers. The monitoring systems are weak.

The benefit package needs to be modified to suit the needs of the customers.

Exclusions go against the health system logic of covering risks.

Lastly, the reimbursement method of payment is highly unpopular among the customers. The experiment with TPAs appears to have been unsuccessful and the reasons for this needs to be studied

IRDA

Insurance Regulatory and Development Authority

Set up by the Parliament through IRDA act 1999

Mission:To protect the interests of the policy holders, to regulate, to promote and ensure orderly growth of the insurance industry and for matters connected therewith or incidental thereto.

Suggested Recommendations

Flexible premiums schemes.

Diseases like Tuberculosis should be considered as exception so as to cover OPD basis reimbursement of the treatment cost for special cases.

Limit exclusions for pre-existing conditions. For eg. STDs, AIDS. Exclusions for pre existing conditions can be made valid for not more than 1 year.

Formulating innovative schemes for inclusion of maternity hospitalization. It will help to facilitate institutional deliveries and hence reducing IMR and MMR.

Contd…Suggested Recommendations

Inclusion of reimbursement plans for Homoeopathic IPD level treatment in exceptional cases.

Create public awareness about benefits of insurance.

Discourage insurance for selective diseases to broaden the coverage.

Encourage health insurance for specially vulnerable population.

COMMUNITY HEALTH INSURANCE SCHEME

A not-for-profit insurance scheme that is primarily aimed at the informal sector (BPL and unorganized) and formed on the basis of collective pooling of health risk, and in which the members participate in its management.

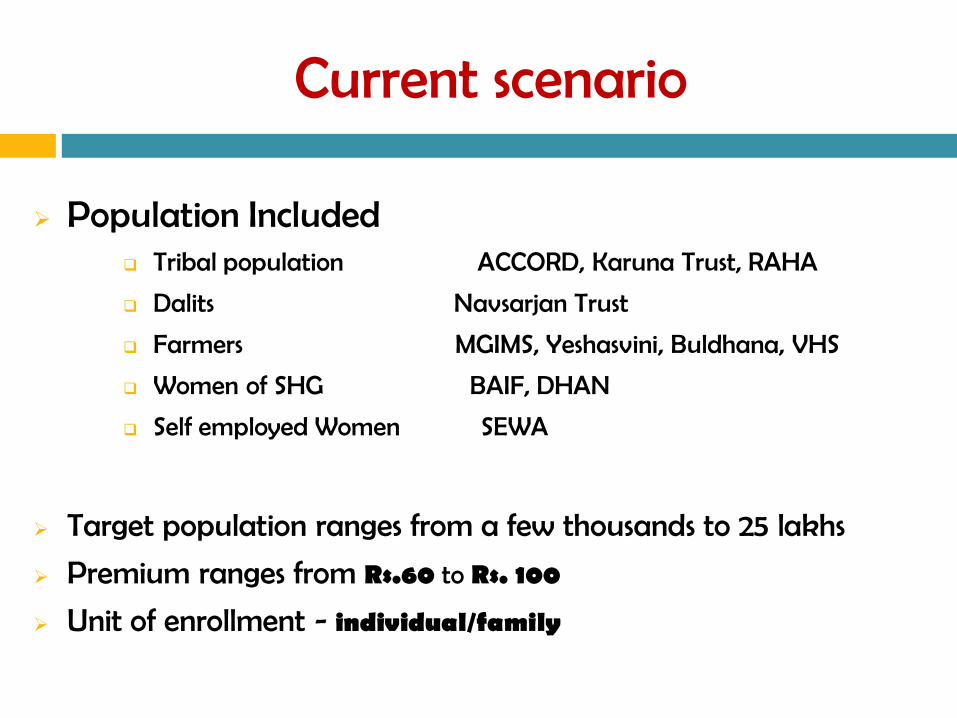

Current scenario

Population Included Tribal population ACCORD, Karuna Trust, RAHA

Dalits Navsarjan Trust

Farmers MGIMS, Yeshasvini, Buldhana, VHS

Women of SHG BAIF, DHAN

Self employed Women SEWA

Target population ranges from a few thousands to 25 lakhs

Premium ranges from Rs.60 to Rs. 100

Unit of enrollment - individual/family

To provide accessible and affordable health care to

community.

To provide Quality Health care services to

community.

To legalize the current CBHI scheme.

To create awareness in community about CBHI.

AIMS

Guidelines

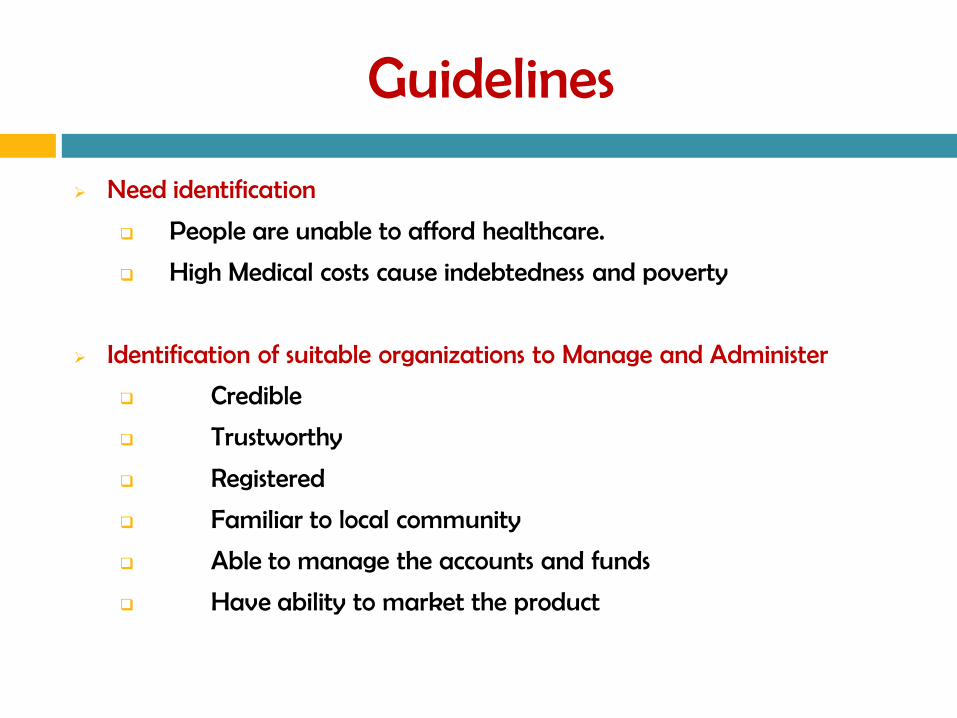

Need identification

People are unable to afford healthcare.

High Medical costs cause indebtedness and poverty

Identification of suitable organizations to Manage and Administer

Credible

Trustworthy

Registered

Familiar to local community

Able to manage the accounts and funds

Have ability to market the product

Contd…Guidelines

Target Community identification

Self Help Group

Cooperative society members

Shop keepers associations

Drivers Association

Identifying the Providers

Be according to the community needs

Should be acceptable and reliable

Registered hospitals

Should ready provide Cashless or credit based service

Contd…Guidelines

Identifying the insurer

Registered.

Ready to provide cashless service.

Ready to serve community needs – minimal

exclusion of disease.

Less documentation.

Benefit package Definition

Designed as per the requirement of community.

Coverage of OPD and IPD service considered.

Minimal exclusion of disease.

Contd…Guidelines

Fixing and collecting the PremiumConstructed according to socio-economic status of

purchaser.

Premium can be collected either in cash or in kind

e.g. grains.

Collection of premium within specified time period

in a year.

RISK MANAGEMENT

Adverse Selection

Enroll large number of participant.

Mandatory enrollment for group and family.

Waiting period.

Moral Hazards

Preauthorization by panel doctor.

Comprehensive referral system.

Preventing Fraud

Set committee to monitor functioning.

Committee member must include NGO member, provider member, insurer member and community member.

Design Model for CHI

Provider Model Mutual Model Linked ModelEg: ACCORD, RAHA Eg: DHAN, Yeshasvini Eg: BAIF, Buldhana, Karuna Trust, SEWA

Any one of above three models can be implemented in efficient manner as per community need and strength and weakness of implementing organizations.

Insurer (NGO)R

eimbursem

entR

eimbursem

ent

Pre

miu

m

Prem

ium

Pre

miu

m

InsuranceCompany

Community

Care

Provider

Provider

Community

RECOMMENDATIONS

Provide subsidy or start up cost of fixed nature.

To provide subsidy for recurring Administrative expenses.

Subsidize premium for poor member.

Financing cost of generating health awareness among public.

Strengthening supply of health care service.

Providing legal status to CBHI.

Link CBHI to promote certain desirable behavior e.g. In AP Arogya

Raksha scheme links family planning with health insurance.

To reduce public subsidization of services for those who have ample

ability to pay. E.g. Apollo Hospital gets public loan, expensive tertiary

level public hospitals get subsidized.

Relaxation in IRDA norms for CBHI.

OTHER ASPECTS

Empowerment: Community should be involved in designing, managing and monitoring the scheme.

Employment opportunity for local community members.

Scaling up of the scheme.

Lessons from Public Health Insurance systems world over

Universal coverage is possible only through a mandate that every individual purchase a basic insurance plan.

Harbouring a private sector as a necessary parallel financing and provision system thus complimenting the services provided by public health insurance.

Centralised risk pooling between various providers for equalising risk.

Single Comprehensive health benefit package covering most necessary services including alternative health care services.

Regulations to fix the rates for all possible medical expenses .

Contd…Lessons from Public Health Insurance systems world over

Personal insurance than employment based insurance.

Right to emergency treatment for all citizens and prompt reimbursement of expenses.

Reliance on Information technology- reduces processing time, eases periodic monitoring and saves administrative costs.

Ensure quality of care and respect patient freedom.

Strengthening the gatekeepers and their role- Fortifying primary care and paramedical personnel and initiatives through them.

THANK YOU FOR YOUR KIND ATTENTION!

Presented by:

Dr. Irvind Jote KaurDr. Nikhil N. YadavDr. Srinivas P. KodiyathMr. Anuj Anthony EkkaDr. Parag Balu ChaudhariDr. Sujay BishnuMr. Lalhmangaih HauzelDr. Rajesh KamathDr. Vinay Preet KaurDr. Lord Wasim RezaDr. Sandeep A. Chavan