Embed Size (px)

Citation preview

Health Insurance Marketplaces: Preparing to assist people with

disabilities

What do you know? What do you need to know?

August 7, 2013

Webinar Recording & Slides - www.friendsofncbddd.org Q & A - Please submit your questions throughout the webinar via the “question box” on your webinar dashboard. Questions will be answered following the presentation. Survey - Please complete the short survey at the end of the webinar!

Webinar Overview

Barbara Kornblau, JD, OTR, FAOTA, Coalition for Disability Health Equity Rachel Patterson, MPA, Association of University Centers on Disabilities Niketa Sheth, MPA, Christopher & Dana Reeve Foundation

Introductions

Health Insurance Marketplaces: Preparing to assist people with

disabilities What do you know?

What do you need to know?

Barbara L. Kornblau, JD, OTR Coalition for Disability Health Equity

Florida A&M University

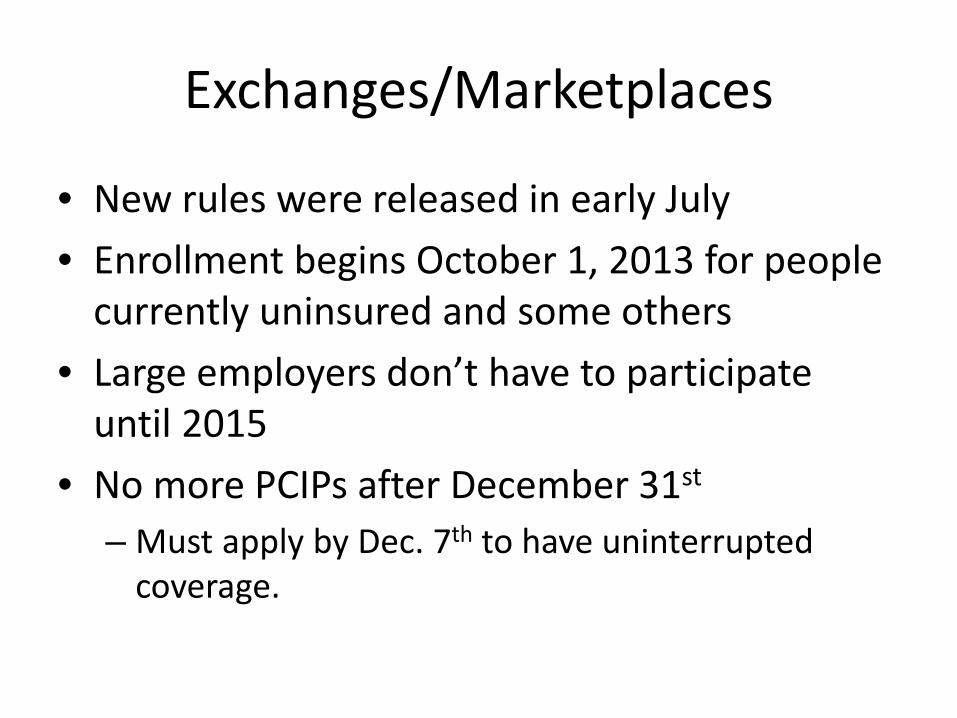

Exchanges/Marketplaces

• New rules were released in early July • Enrollment begins October 1, 2013 for people

currently uninsured and some others • Large employers don’t have to participate

until 2015 • No more PCIPs after December 31st

– Must apply by Dec. 7th to have uninterrupted coverage.

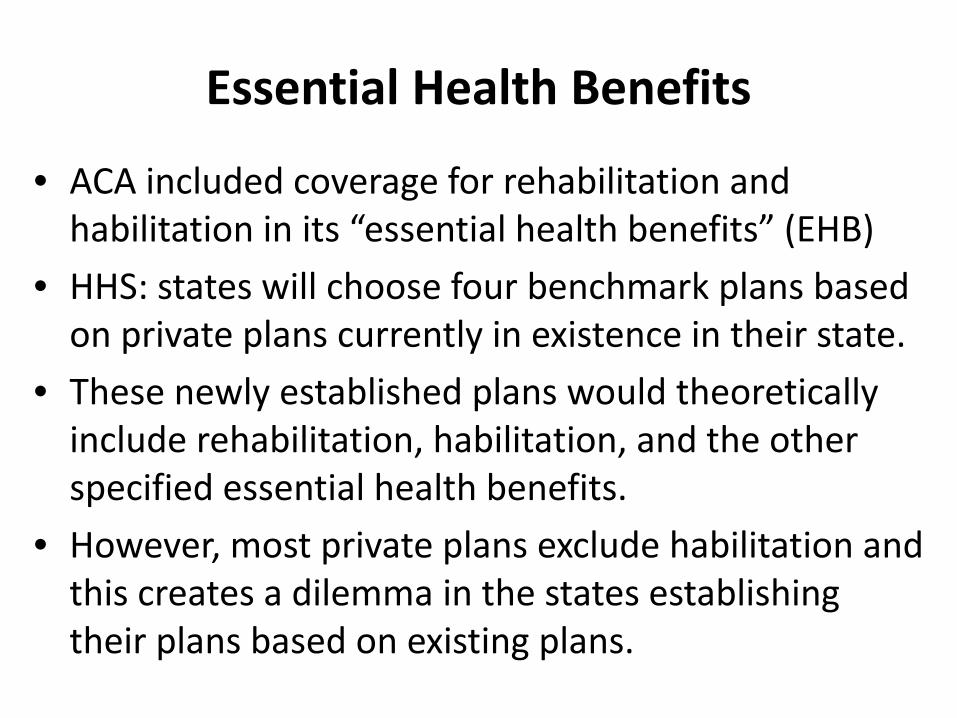

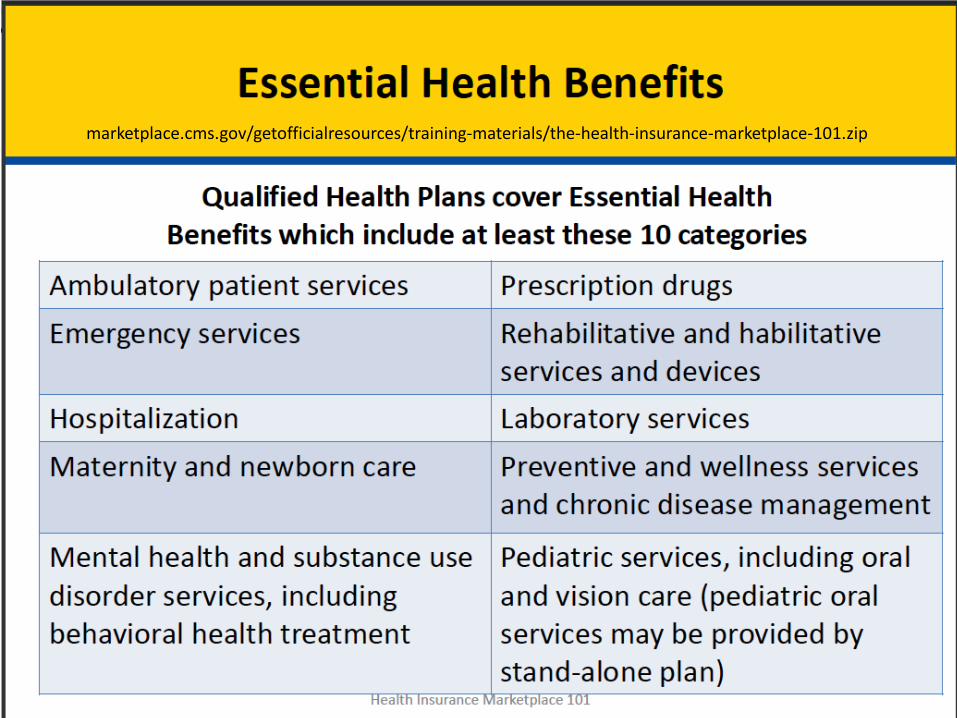

Essential Health Benefits

• ACA included coverage for rehabilitation and habilitation in its “essential health benefits” (EHB)

• HHS: states will choose four benchmark plans based on private plans currently in existence in their state.

• These newly established plans would theoretically include rehabilitation, habilitation, and the other specified essential health benefits.

• However, most private plans exclude habilitation and this creates a dilemma in the states establishing their plans based on existing plans.

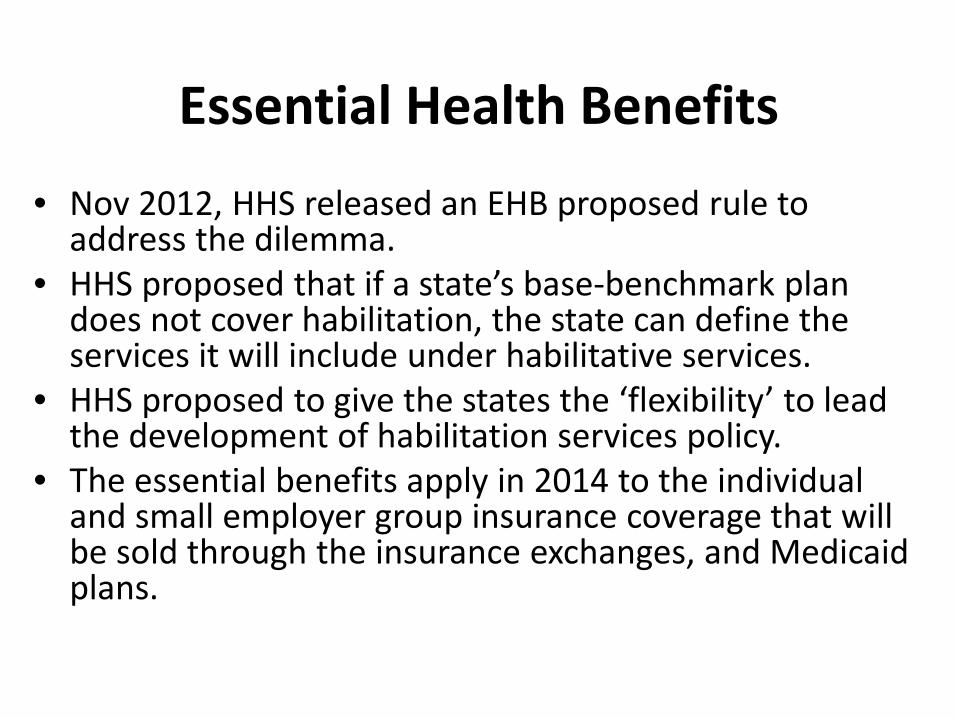

Essential Health Benefits • Nov 2012, HHS released an EHB proposed rule to

address the dilemma. • HHS proposed that if a state’s base-benchmark plan

does not cover habilitation, the state can define the services it will include under habilitative services.

• HHS proposed to give the states the ‘flexibility’ to lead the development of habilitation services policy.

• The essential benefits apply in 2014 to the individual and small employer group insurance coverage that will be sold through the insurance exchanges, and Medicaid plans.

marketplace.cms.gov/getofficialresources/training-materials/the-health-insurance-marketplace-101.zip

marketplace.cms.gov/getofficialresources/training-materials/the-health-insurance-marketplace-101.zip

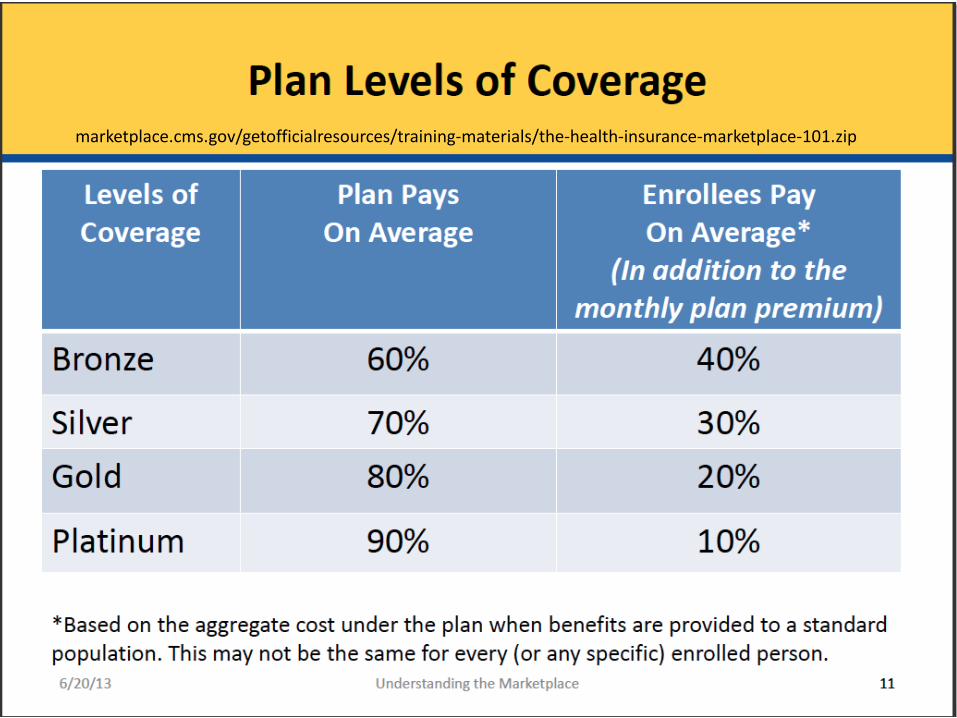

Bottom Line

• The lower the premium, the higher the out-of-pocket costs when you need care;

• The higher the premium, the lower the out-of-pocket costs when you need care.

• Note: The Marketplace also offers "catastrophic" plans to people under 30 years old and to some people with very low incomes.

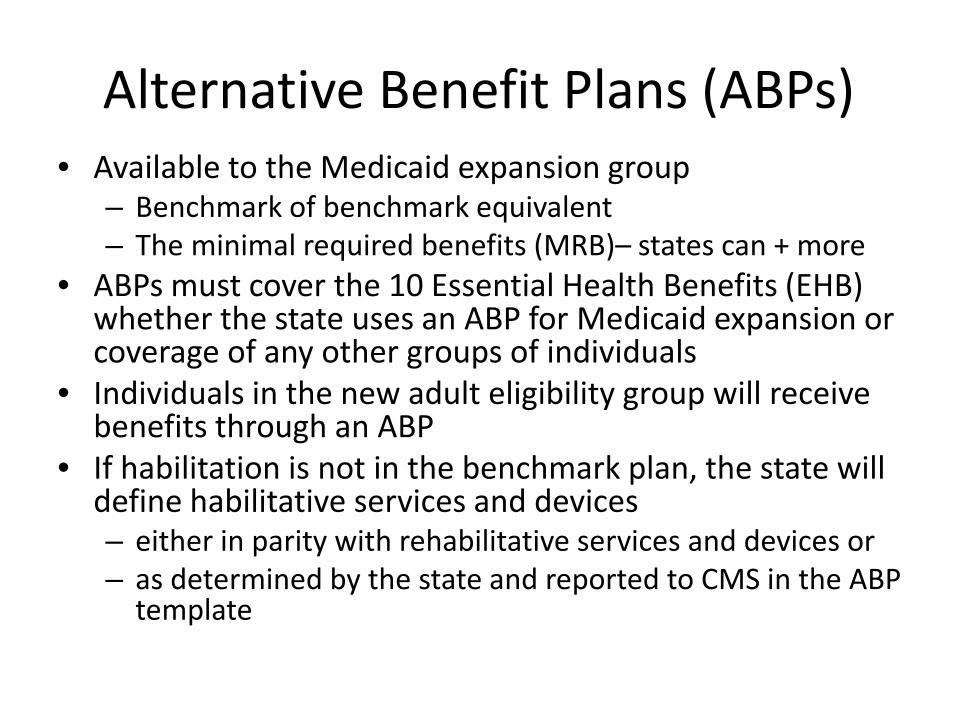

Alternative Benefit Plans (ABPs) • Available to the Medicaid expansion group

– Benchmark of benchmark equivalent – The minimal required benefits (MRB)– states can + more

• ABPs must cover the 10 Essential Health Benefits (EHB) whether the state uses an ABP for Medicaid expansion or coverage of any other groups of individuals

• Individuals in the new adult eligibility group will receive benefits through an ABP

• If habilitation is not in the benchmark plan, the state will define habilitative services and devices – either in parity with rehabilitative services and devices or – as determined by the state and reported to CMS in the ABP

template

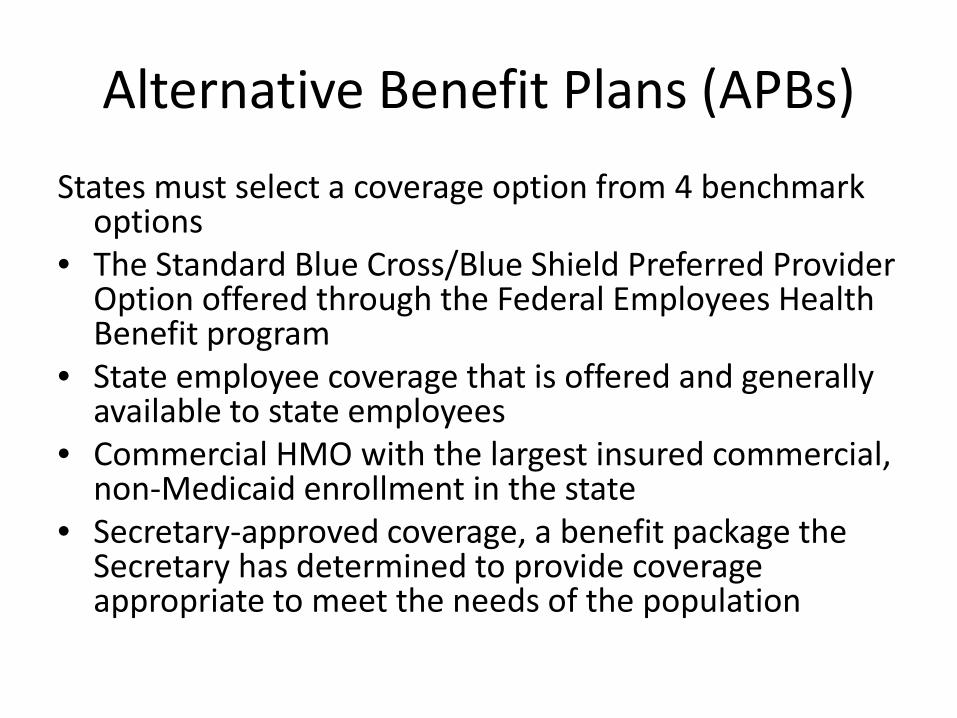

Alternative Benefit Plans (APBs) States must select a coverage option from 4 benchmark

options • The Standard Blue Cross/Blue Shield Preferred Provider

Option offered through the Federal Employees Health Benefit program

• State employee coverage that is offered and generally available to state employees

• Commercial HMO with the largest insured commercial, non-Medicaid enrollment in the state

• Secretary-approved coverage, a benefit package the Secretary has determined to provide coverage appropriate to meet the needs of the population

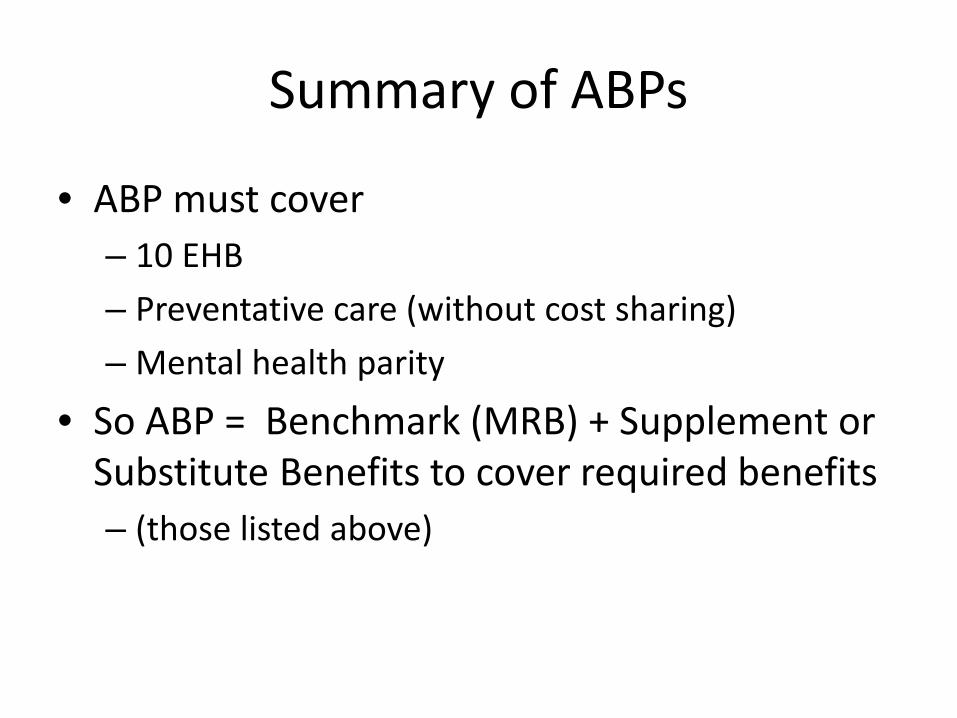

Summary of ABPs

• ABP must cover – 10 EHB – Preventative care (without cost sharing) – Mental health parity

• So ABP = Benchmark (MRB) + Supplement or Substitute Benefits to cover required benefits – (those listed above)

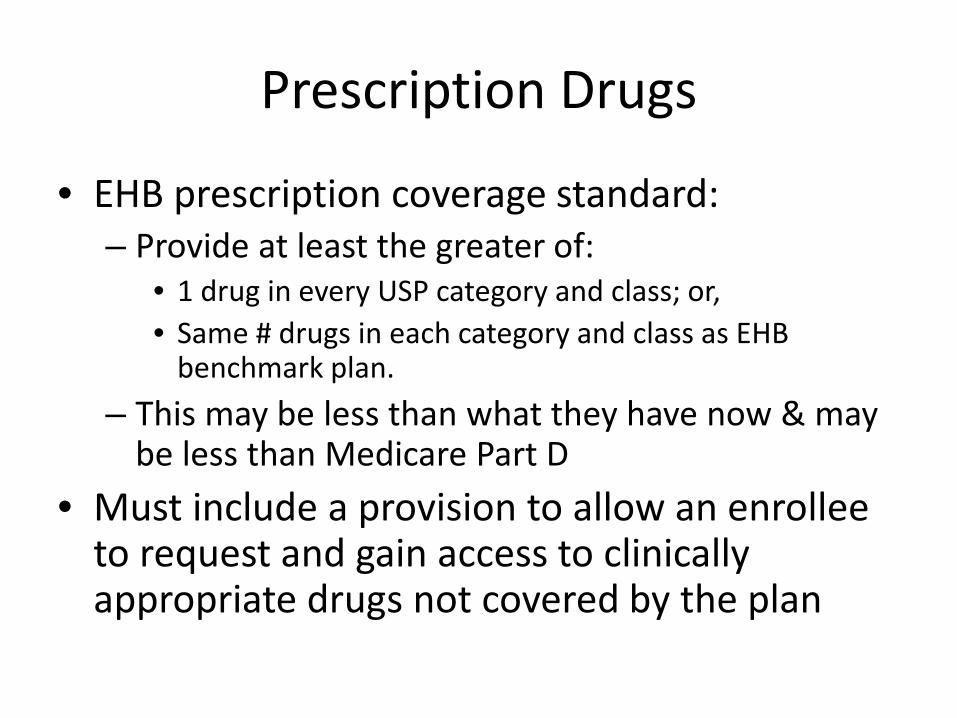

Prescription Drugs

• EHB prescription coverage standard: – Provide at least the greater of:

• 1 drug in every USP category and class; or, • Same # drugs in each category and class as EHB

benchmark plan. – This may be less than what they have now & may

be less than Medicare Part D • Must include a provision to allow an enrollee

to request and gain access to clinically appropriate drugs not covered by the plan

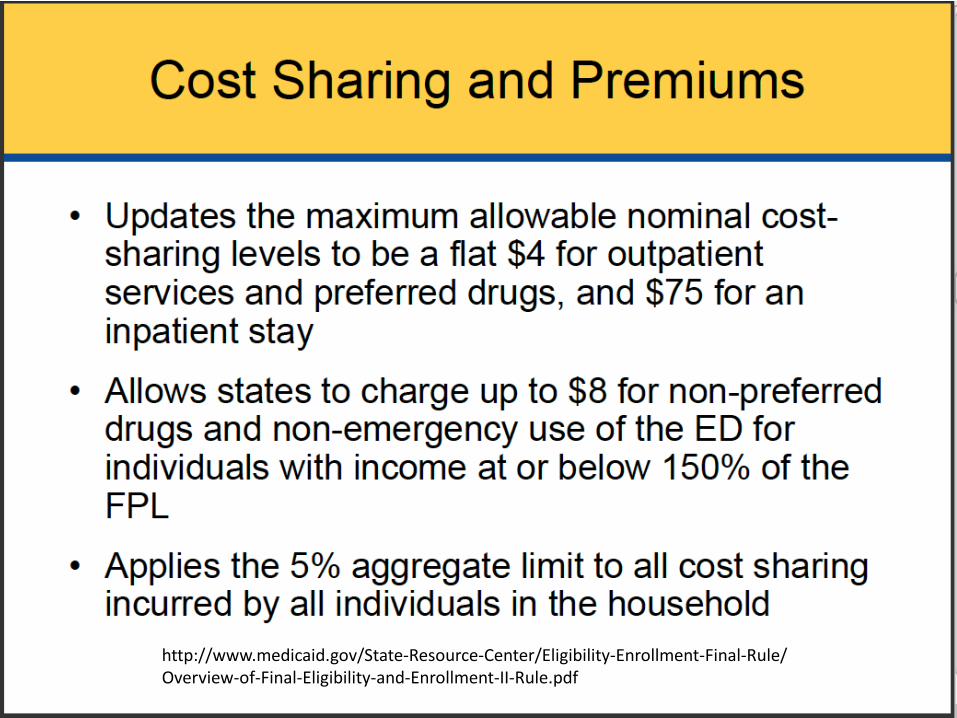

http://www.medicaid.gov/State-Resource-Center/Eligibility-Enrollment-Final-Rule/ Overview-of-Final-Eligibility-and-Enrollment-II-Rule.pdf

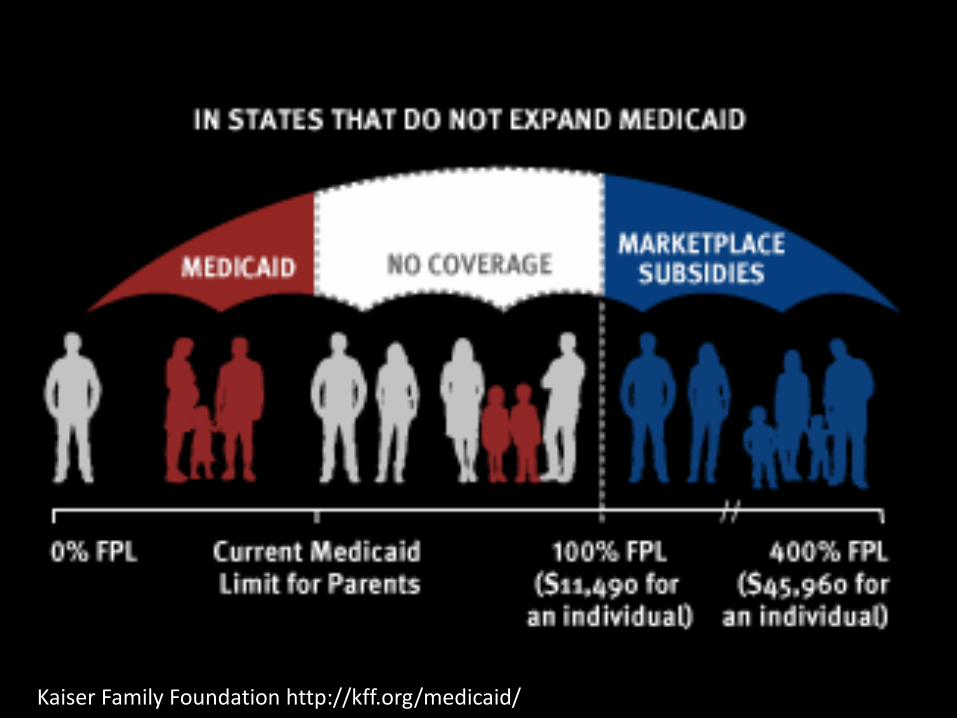

Medicaid Expansion

• ACA expands Medicaid coverage for most low-income adults to 138% of the federal poverty level (FPL) ($15,415 for an individual or $26,344 for a family of three in 2012)

• Supreme Court left some folks in limbo – said Medicaid expansion was optional for states

• Some states are talking about putting people in Medicaid in the exchanges/marketplaces via premium assistance – Establishes rules regarding premium assistance to support

enrollment of individuals eligible for Medicaid in health plans in the individual market, including enrollment in QHPs doing business on the Exchanges/Marketplaces

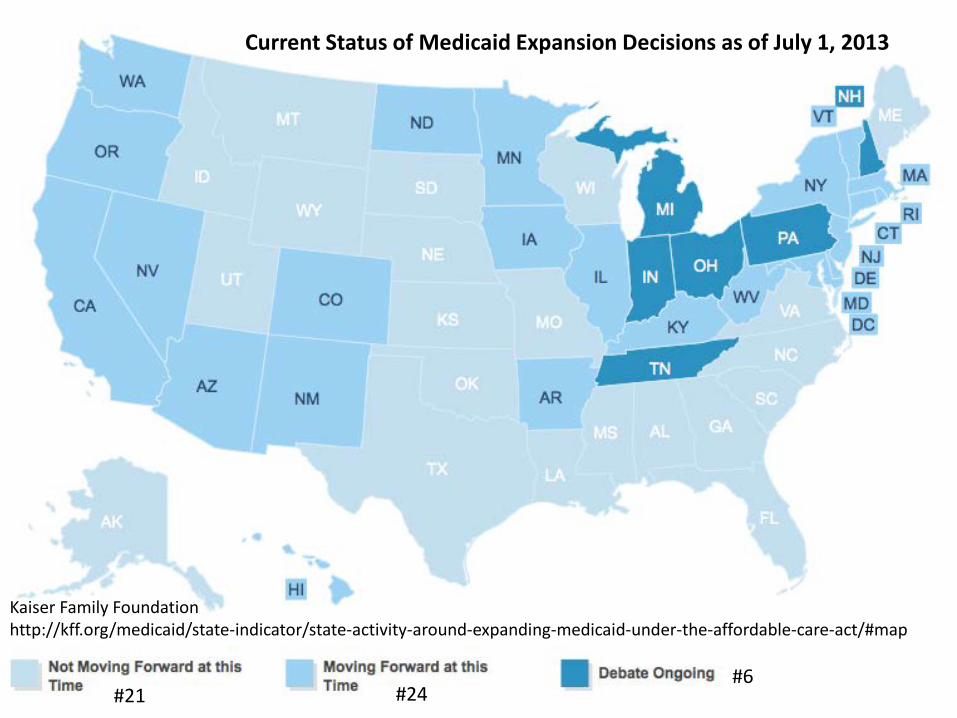

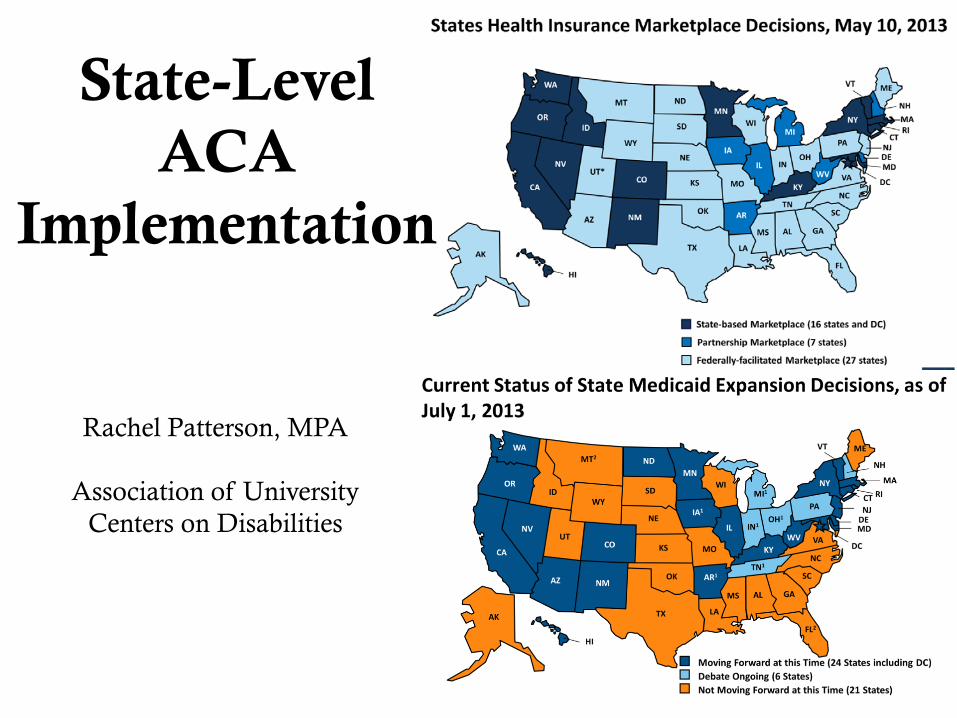

Current Status of Medicaid Expansion Decisions as of July 1, 2013

Kaiser Family Foundation http://kff.org/medicaid/state-indicator/state-activity-around-expanding-medicaid-under-the-affordable-care-act/#map

#6 #24 #21

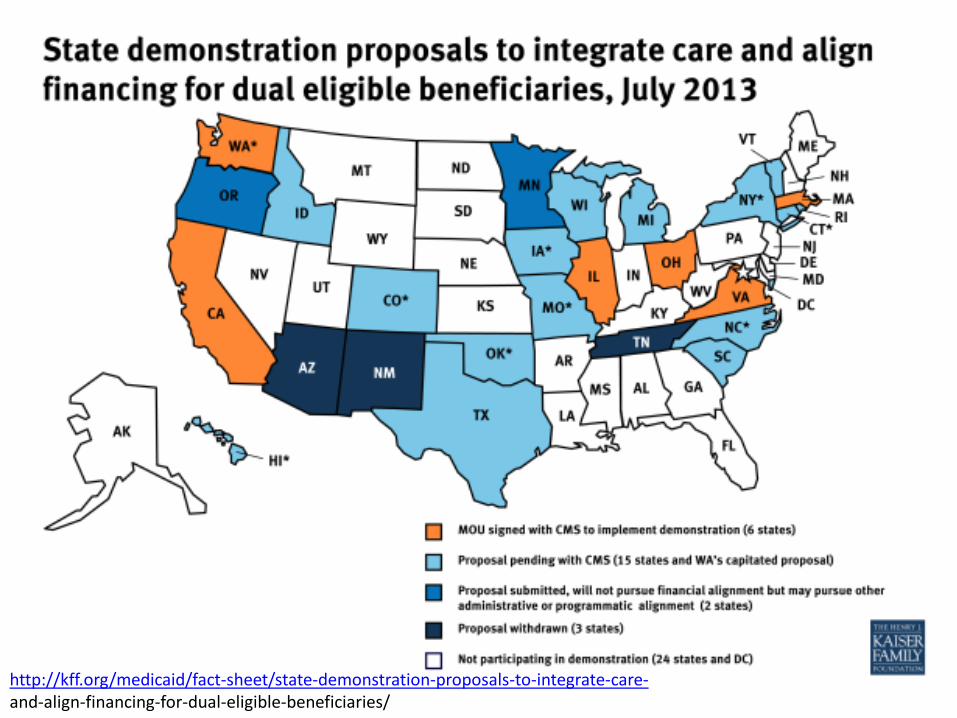

Kaiser Family Foundation http://kff.org/medicaid/

http://kff.org/medicaid/fact-sheet/state-demonstration-proposals-to-integrate-care- and-align-financing-for-dual-eligible-beneficiaries/

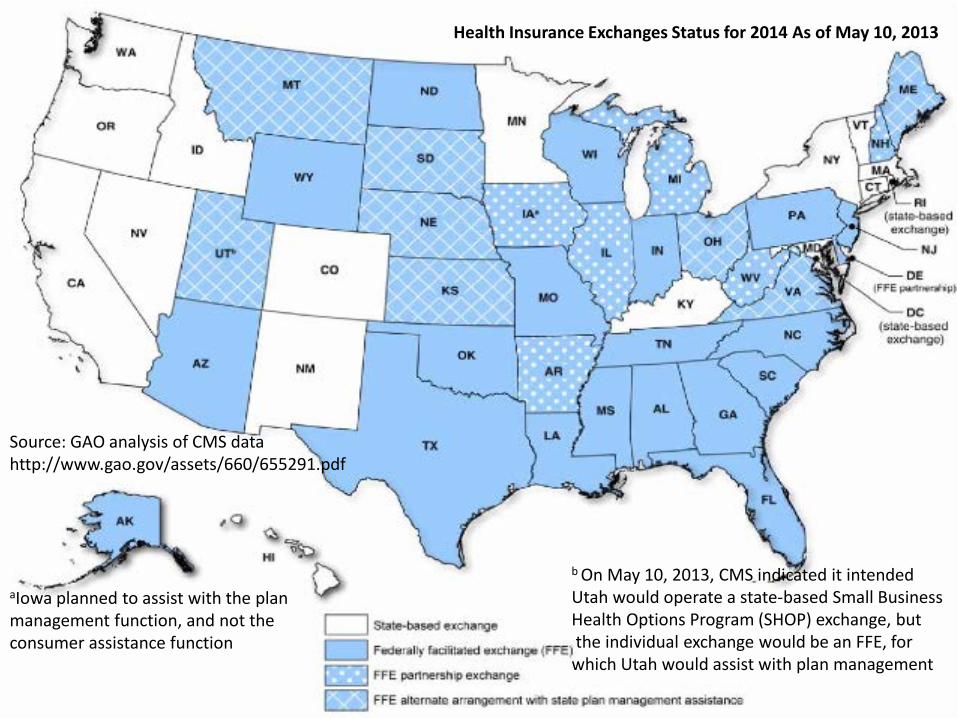

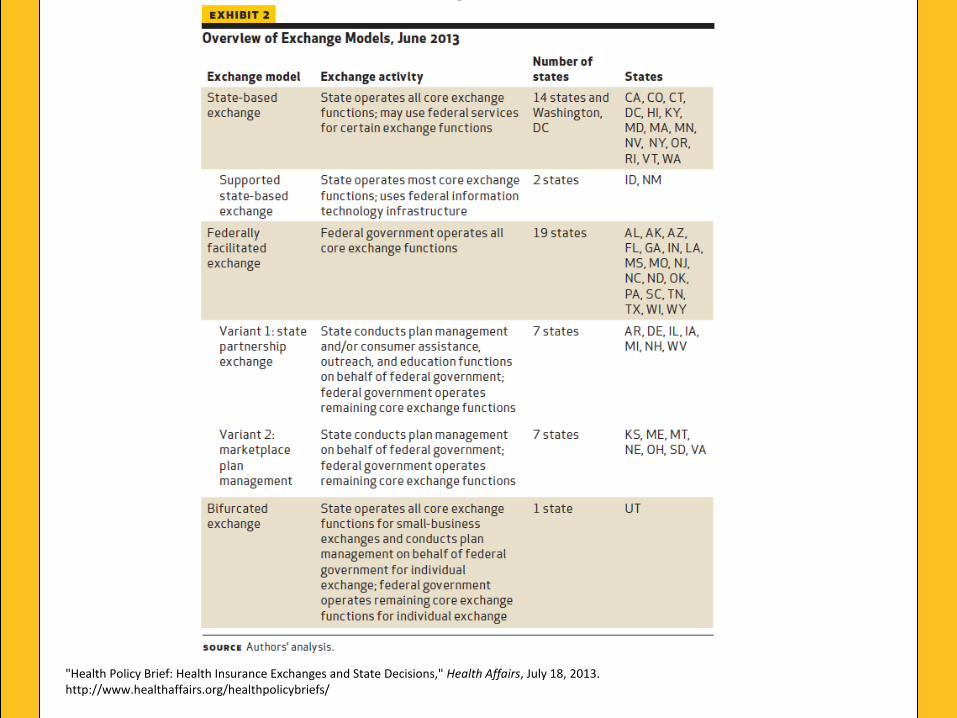

Source: GAO analysis of CMS data http://www.gao.gov/assets/660/655291.pdf

Health Insurance Exchanges Status for 2014 As of May 10, 2013

aIowa planned to assist with the plan management function, and not the consumer assistance function

b On May 10, 2013, CMS indicated it intended Utah would operate a state-based Small Business Health Options Program (SHOP) exchange, but the individual exchange would be an FFE, for which Utah would assist with plan management

"Health Policy Brief: Health Insurance Exchanges and State Decisions," Health Affairs, July 18, 2013. http://www.healthaffairs.org/healthpolicybriefs/

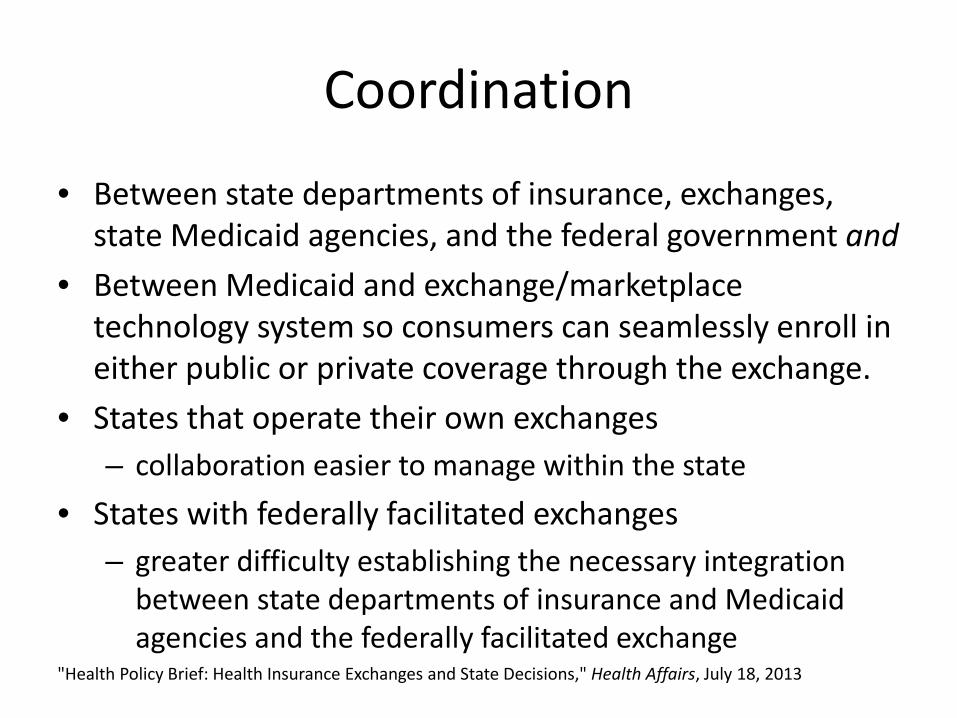

Coordination

• Between state departments of insurance, exchanges, state Medicaid agencies, and the federal government and

• Between Medicaid and exchange/marketplace technology system so consumers can seamlessly enroll in either public or private coverage through the exchange.

• States that operate their own exchanges – collaboration easier to manage within the state

• States with federally facilitated exchanges – greater difficulty establishing the necessary integration

between state departments of insurance and Medicaid agencies and the federally facilitated exchange

"Health Policy Brief: Health Insurance Exchanges and State Decisions," Health Affairs, July 18, 2013

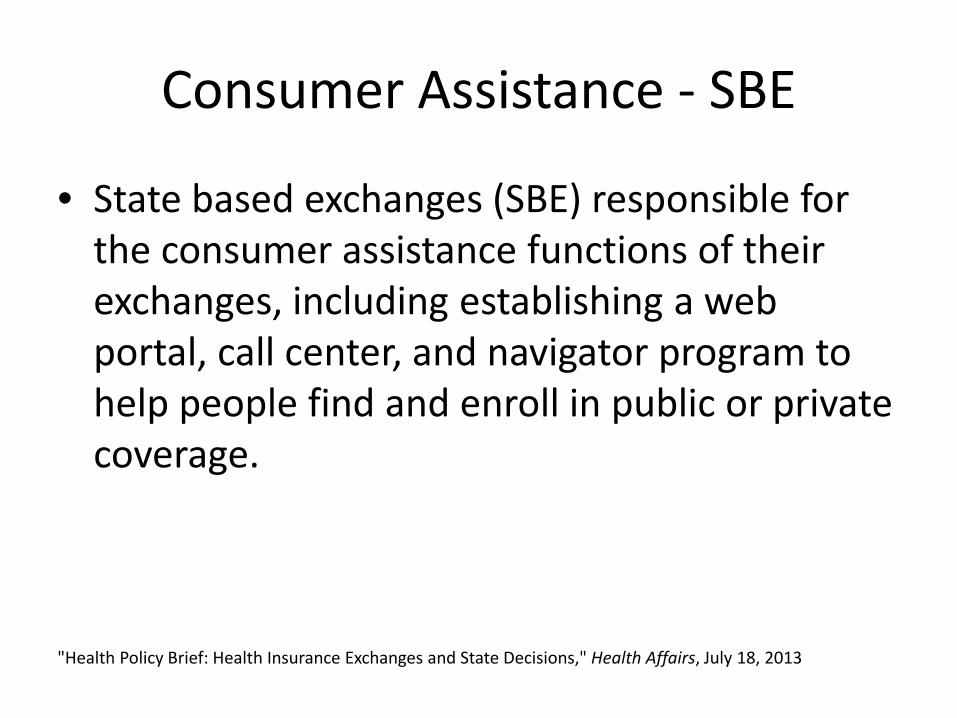

Consumer Assistance - SBE

• State based exchanges (SBE) responsible for the consumer assistance functions of their exchanges, including establishing a web portal, call center, and navigator program to help people find and enroll in public or private coverage.

"Health Policy Brief: Health Insurance Exchanges and State Decisions," Health Affairs, July 18, 2013

Consumer Assistance SBE & SPE

• Can choose to use federal funds to establish in-person assistance programs to supplement their navigator programs, which cannot be fully funded by exchange establishment grants--thus helping to ensure that there will be enough assisters to help people enroll in coverage.

"Health Policy Brief: Health Insurance Exchanges and State Decisions," Health Affairs, July 18, 2013

Consumer Assistance - FFE

• Federally facilitated exchange states will have limited assistance since states must rely on a limited federal funding stream for grants to navigators and will not have in-person assistance programs to supplement the work.

"Health Policy Brief: Health Insurance Exchanges and State Decisions," Health Affairs, July 18, 2013

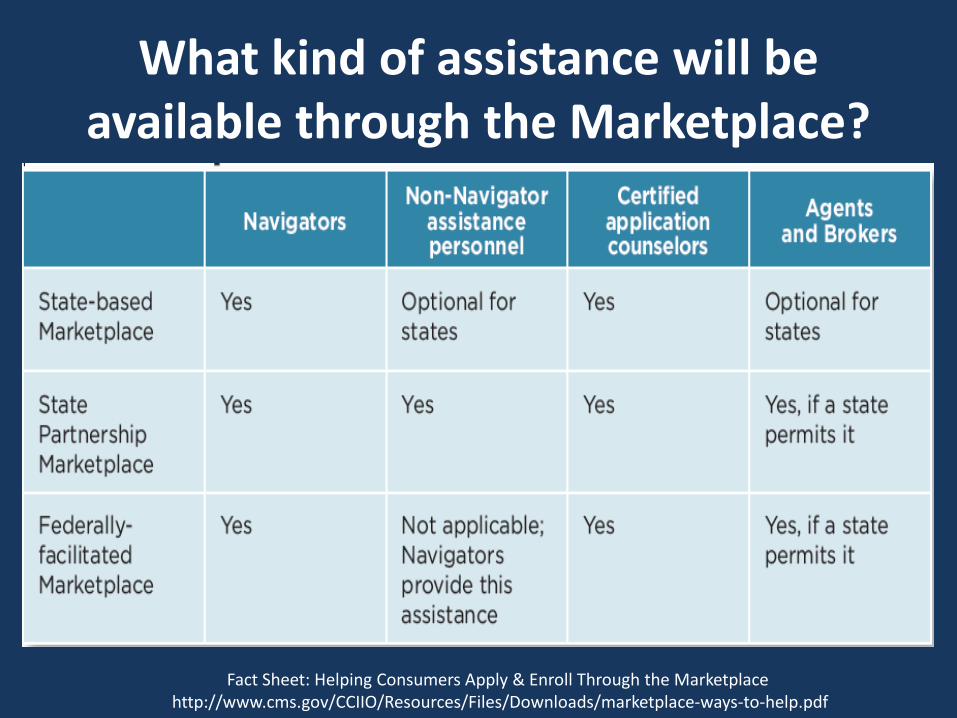

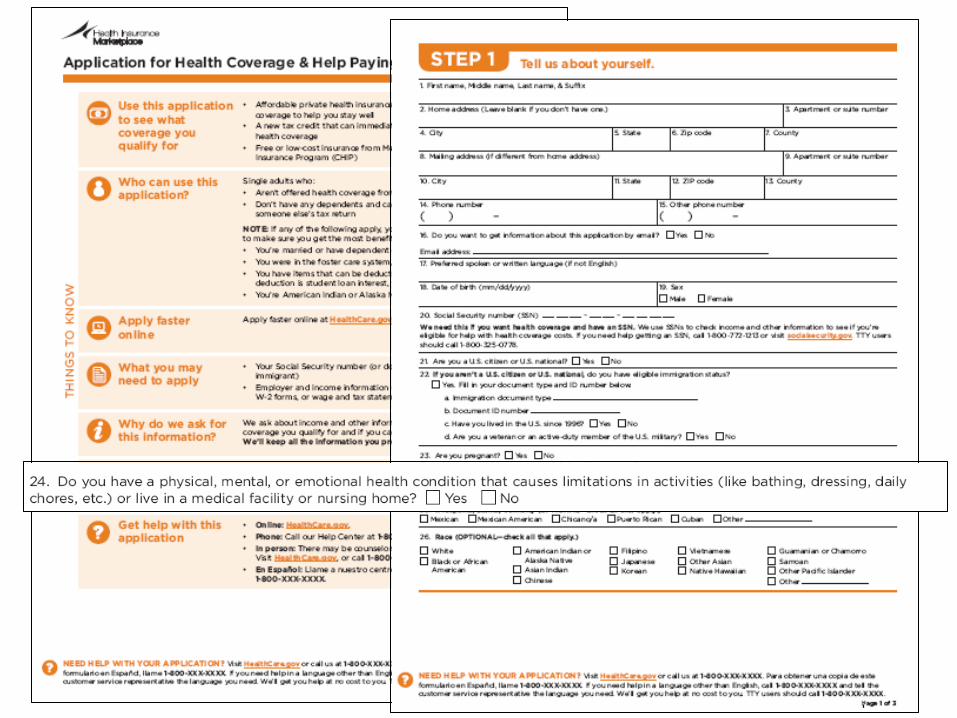

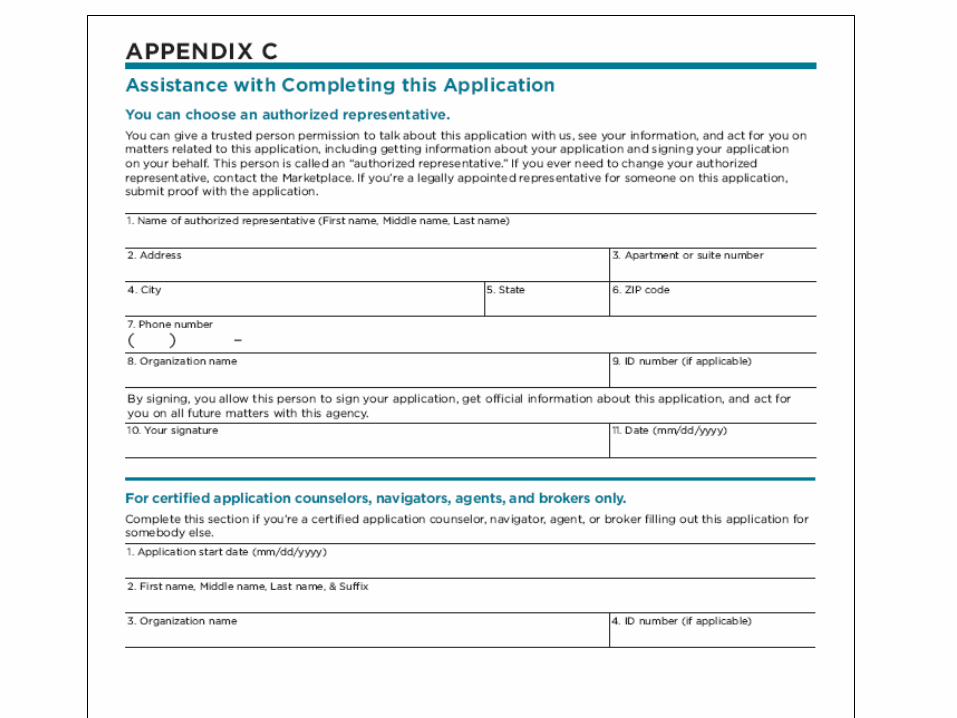

What kind of assistance will be available through the Marketplace?

Fact Sheet: Helping Consumers Apply & Enroll Through the Marketplace http://www.cms.gov/CCIIO/Resources/Files/Downloads/marketplace-ways-to-help.pdf

Marketplaces/Exchanges • Health Navigators

– Major impact on participation by PWD – CMS announced grants RFP for navigator programs

• 45 CFR 155.210(e)(5) and 155.205(d) and (e) require Navigators and non-Navigator assistance programs to provide meaningful access to people with disabilities

• Certified application counselors can provide information with reasonable accommodations for those with disabilities through referrals to Navigators, non-Navigator assistance personnel, and/or the Exchange call center. – 42826 Federal Register / Vol. 78, No. 137 / Wednesday, July 17, 2013 /

Rules and Regulations

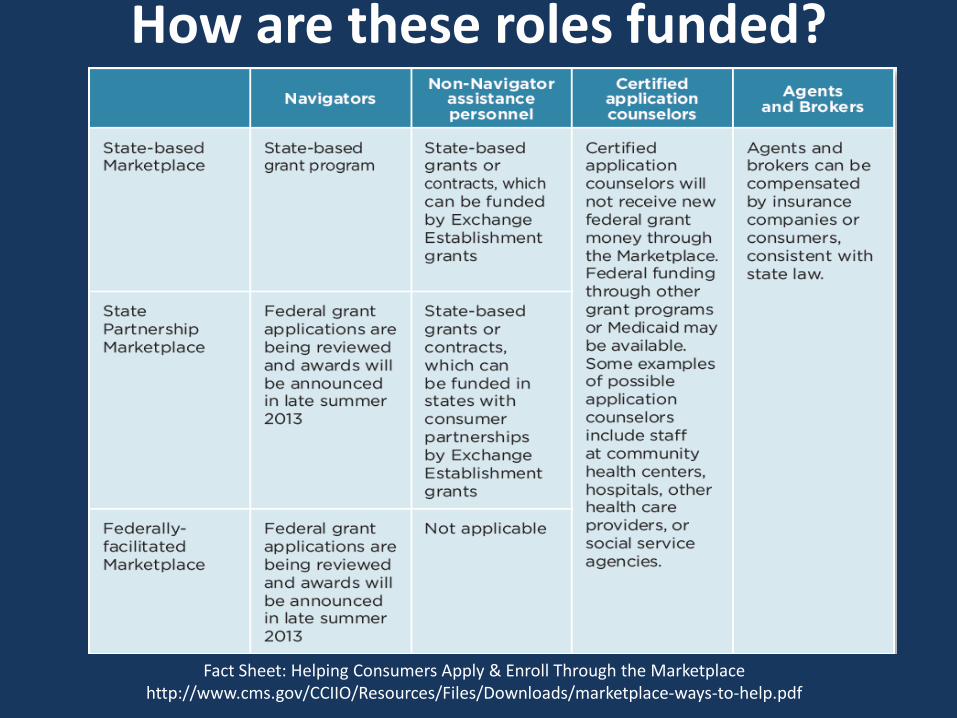

How are these roles funded?

Fact Sheet: Helping Consumers Apply & Enroll Through the Marketplace http://www.cms.gov/CCIIO/Resources/Files/Downloads/marketplace-ways-to-help.pdf

Required Training & Certification

Fact Sheet: Helping Consumers Apply & Enroll Through the Marketplace http://www.cms.gov/CCIIO/Resources/Files/Downloads/marketplace-ways-to-help.pdf

Misc Provisions

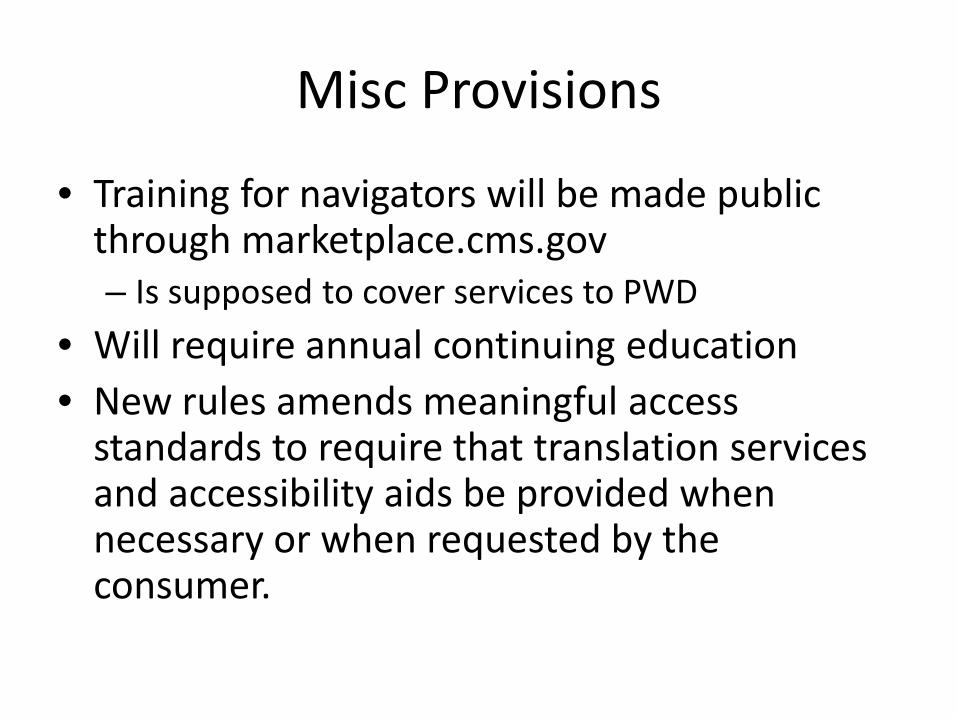

• Training for navigators will be made public through marketplace.cms.gov – Is supposed to cover services to PWD

• Will require annual continuing education • New rules amends meaningful access

standards to require that translation services and accessibility aids be provided when necessary or when requested by the consumer.

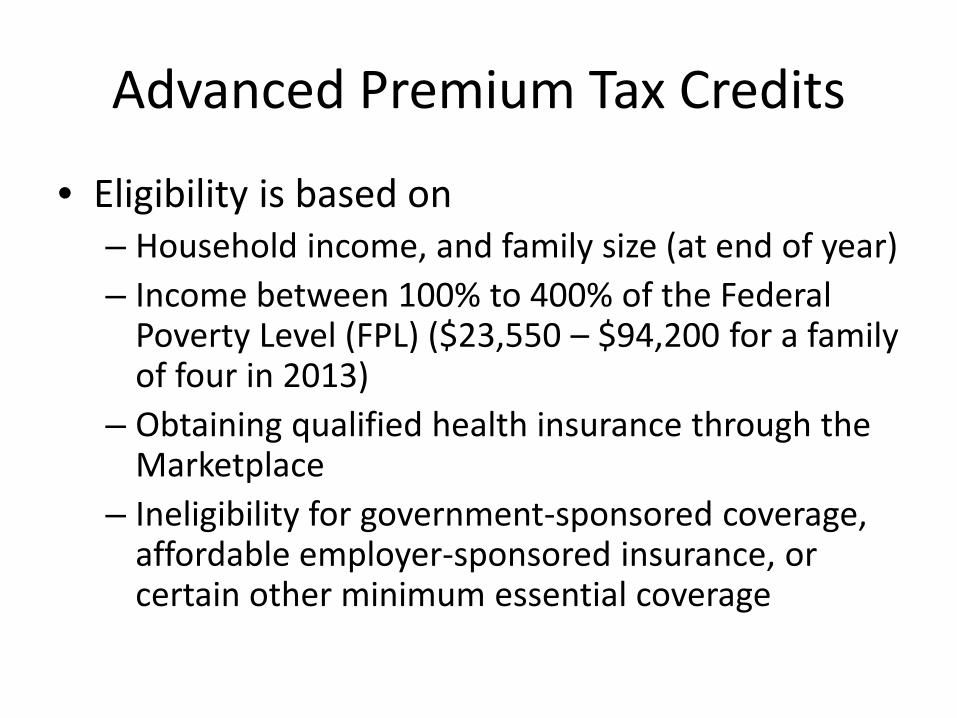

Advanced Premium Tax Credits

• Eligibility is based on – Household income, and family size (at end of year) – Income between 100% to 400% of the Federal

Poverty Level (FPL) ($23,550 – $94,200 for a family of four in 2013)

– Obtaining qualified health insurance through the Marketplace

– Ineligibility for government-sponsored coverage, affordable employer-sponsored insurance, or certain other minimum essential coverage

"Health Policy Brief: Premium Tax Credits," Health Affairs, August 1, 2013. http://www.healthaffairs.org/healthpolicybriefs/

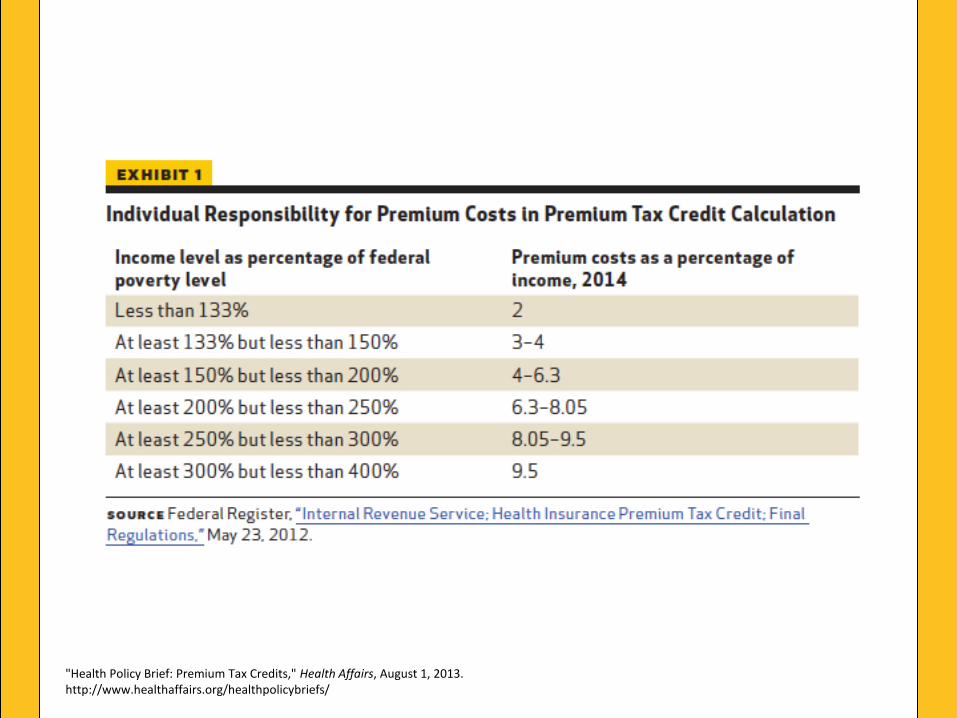

Advanced Premium Tax Credits • This tax credit is paid up front directly to the insurer.

– Advanced each month when premiums are due. • The advance payment of the tax credit is based on the

consumer’s anticipated annual income. • This is reconciled at the end of the year with the

annual filing of the income tax return when actual income is known.

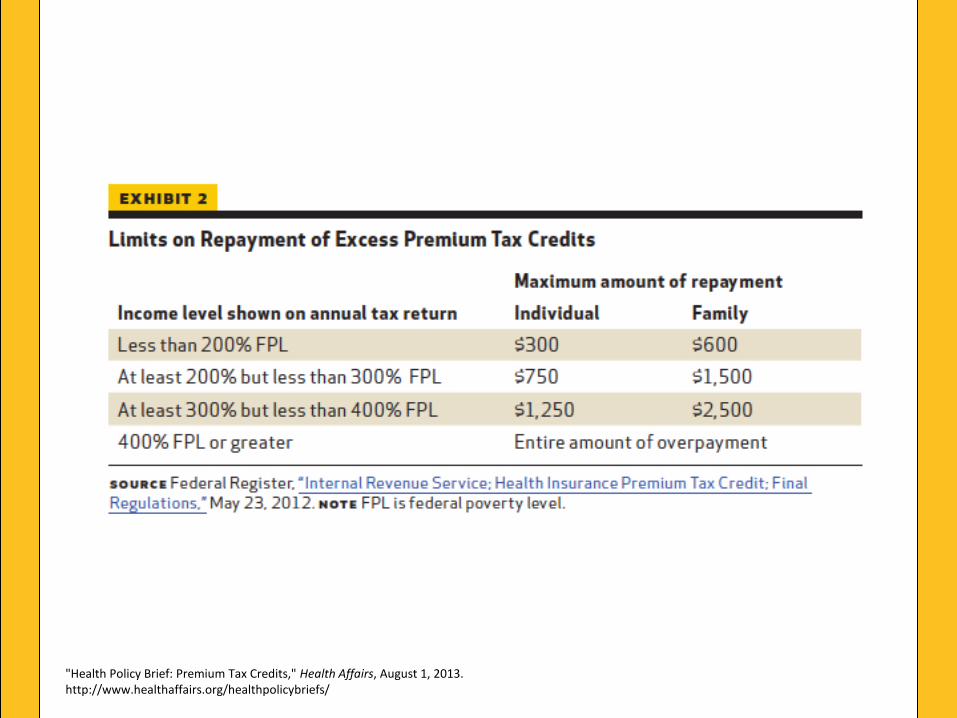

• If the family’s income (or other circumstances, such as family size) changes from the original estimate for the credit amount, the family gets a refund or repays the excess amount up to $1,500, the maximum amount for their income level (see Exhibit 2).

"Health Policy Brief: Premium Tax Credits," Health Affairs, August 1, 2013. http://www.healthaffairs.org/healthpolicybriefs/

Rachel Patterson, MPA

Association of University Centers on Disabilities

State-Level ACA

Implementation

State Decisions on Exchanges

• Benchmark Plan Selection • Essential Health Benefits

– Habilitation

• Non-discrimination standards

State Decisions on Medicaid Expansion

• Alternative Benefits Package – Benchmark plan

• Essential Health Benefits – Habilitation

– Exemption process

UCEDD Involvement: Arkansas

UCEDD Involvement: Michigan

UCEDD Involvement: Wisconsin

We still have work to do

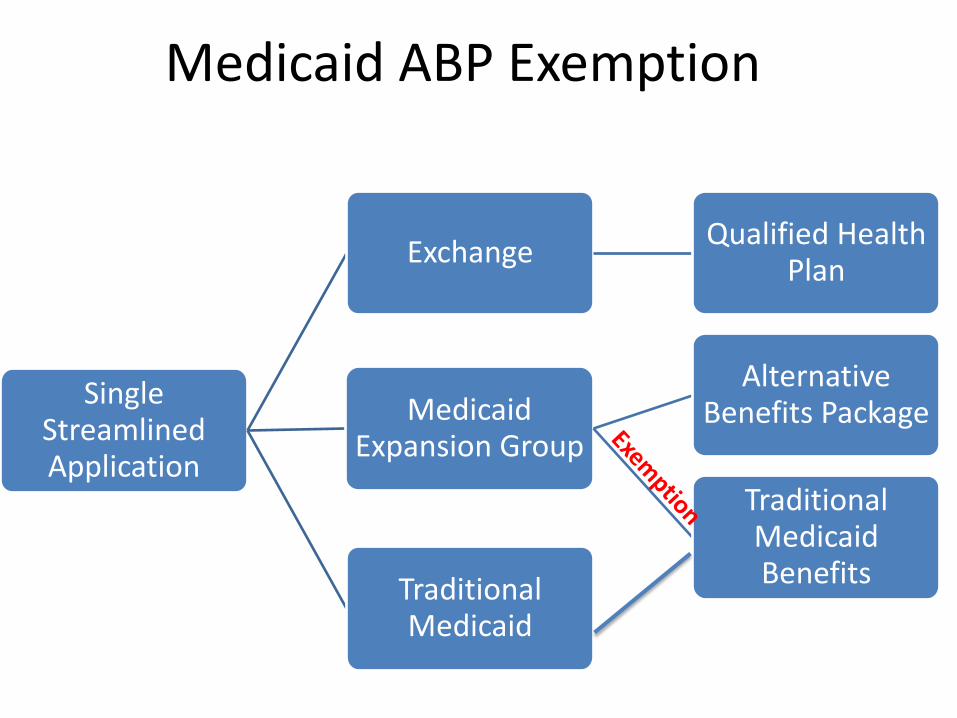

Single Streamlined Application

Exchange Qualified Health Plan

Medicaid Expansion Group

Alternative Benefits Package

Traditional Medicaid Benefits Traditional

Medicaid

Medicaid ABP Exemption

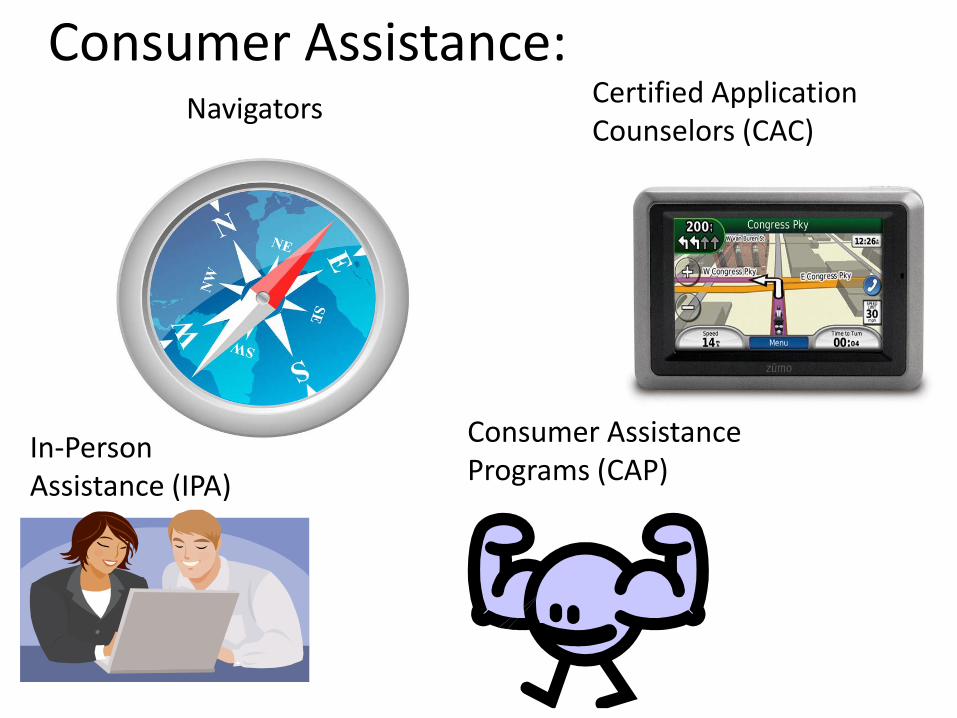

Consumer Assistance: Navigators Certified Application

Counselors (CAC)

In-Person Assistance (IPA)

Consumer Assistance Programs (CAP)

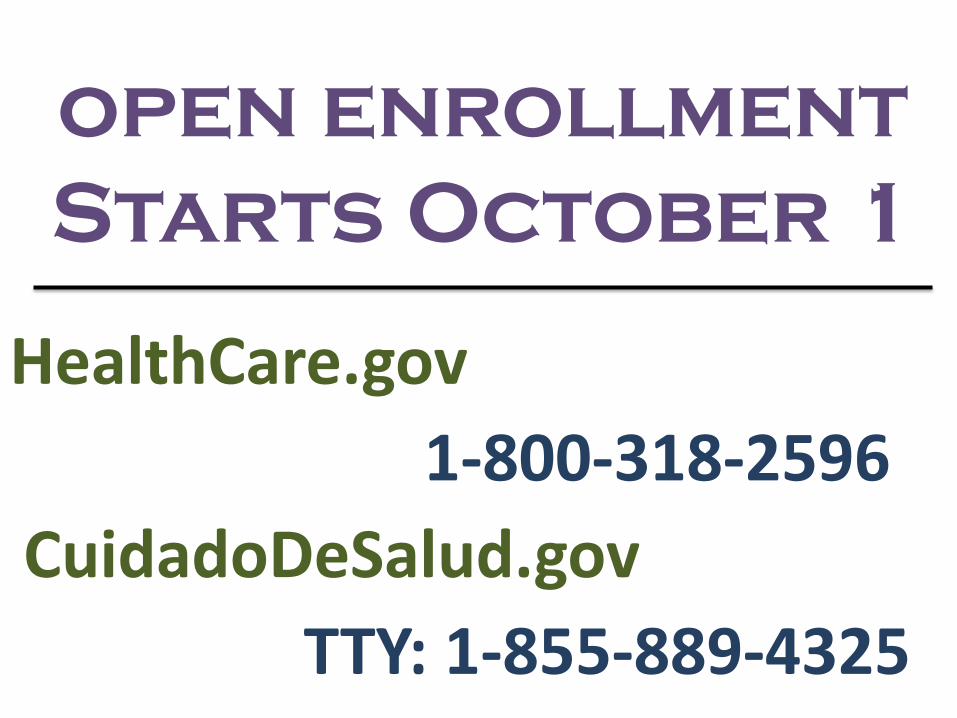

open enrollment Starts October 1

HealthCare.gov

CuidadoDeSalud.gov 1-800-318-2596

TTY: 1-855-889-4325

Niketa Sheth, MPA Senior Vice President, Quality of Life Christopher & Dana Reeve Foundation

Resources for Patients and Organizations

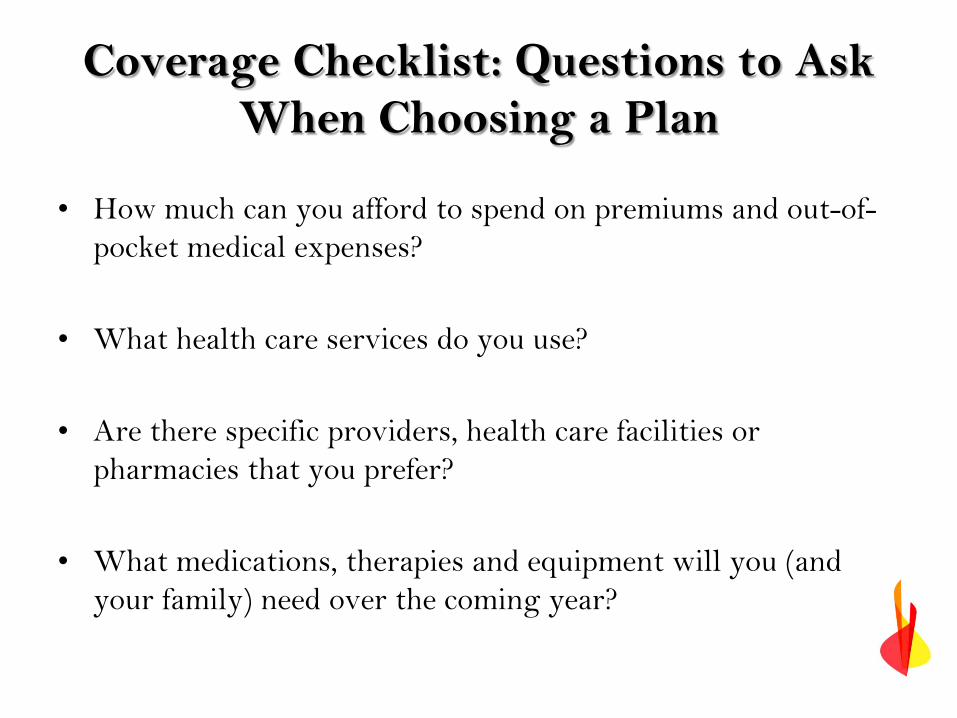

Coverage Checklist: Questions to Ask When Choosing a Plan

• How much can you afford to spend on premiums and out-of-pocket medical expenses?

• What health care services do you use?

• Are there specific providers, health care facilities or pharmacies that you prefer?

• What medications, therapies and equipment will you (and your family) need over the coming year?

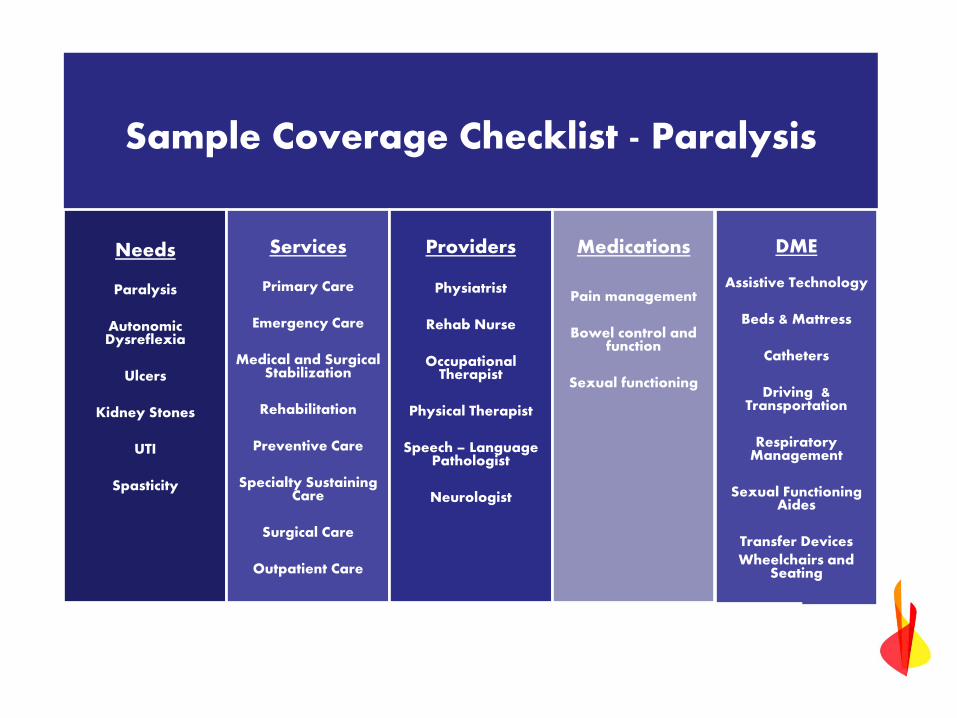

Sample Coverage Checklist - Paralysis

Needs

Paralysis

Autonomic Dysreflexia

Ulcers

Kidney Stones

UTI

Spasticity

Services

Primary Care

Emergency Care

Medical and Surgical Stabilization

Rehabilitation

Preventive Care

Specialty Sustaining Care

Surgical Care

Outpatient Care

Providers

Physiatrist

Rehab Nurse

Occupational Therapist

Physical Therapist

Speech – Language Pathologist

Neurologist

Medications

Pain management

Bowel control and function

Sexual functioning

DME

Assistive Technology

Beds & Mattress

Catheters

Driving & Transportation

Respiratory Management

Sexual Functioning Aides

Transfer Devices

Wheelchairs and Seating

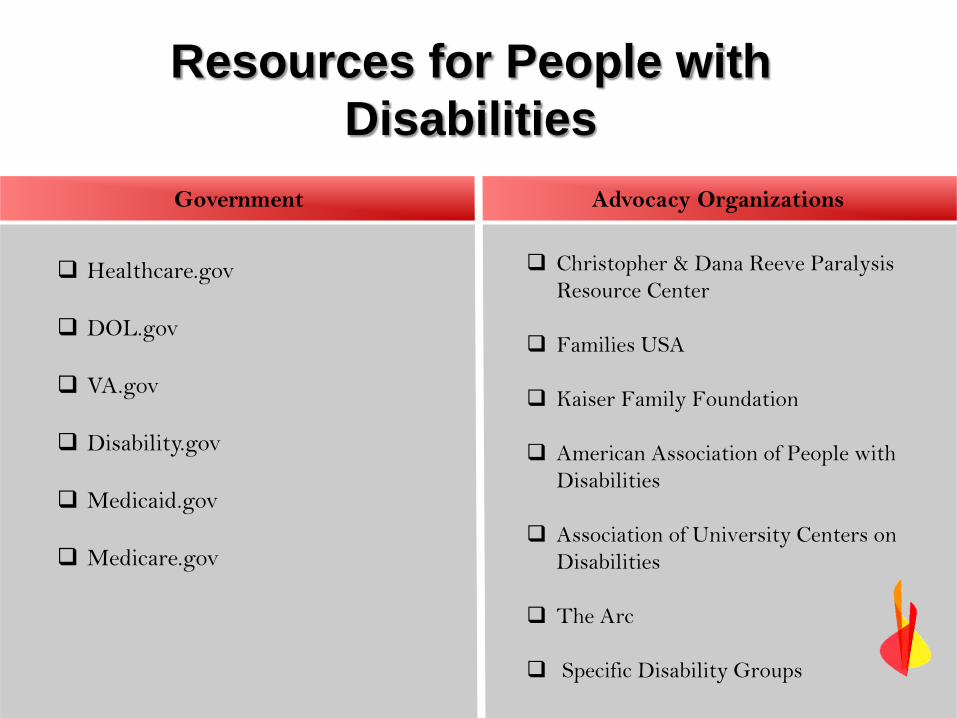

Resources for People with Disabilities

Government Advocacy Organizations

Healthcare.gov

DOL.gov

VA.gov

Disability.gov

Medicaid.gov

Medicare.gov

Christopher & Dana Reeve Paralysis

Resource Center

Families USA

Kaiser Family Foundation

American Association of People with Disabilities

Association of University Centers on Disabilities

The Arc

Specific Disability Groups

Tips to Communicate on the ACA

• Know the right questions to ask • Educate and engage your

audience – Timely email alerts and updates – Webinar Series – ACA Micro-Site – Social Media Tools

• Create a feedback mechanism

The Time Is Now

Ask a question! - Type your question in the “question box” on your webinar dashboard. - The moderator will read the question.

Q & A

Learn more about the Friends of NCBDDD! - www.friendsofncbddd.org Questions about the webinar? - Email Tory Christensen ([email protected])

Thank You

Please take a few minutes to complete the survey!