Embed Size (px)

Citation preview

Health

“Health is wealth” is a common

phrase, yet we understand the true

meaning of the expression only

when we fall sick or get hospitalized

Need of Health Insurance

• No one plans to get sick or hurt, but most people need medical

care at some point. Health insurance covers these costs and

offers many other important benefits.

• Health insurance protects you from unexpected, high medical

expenses.

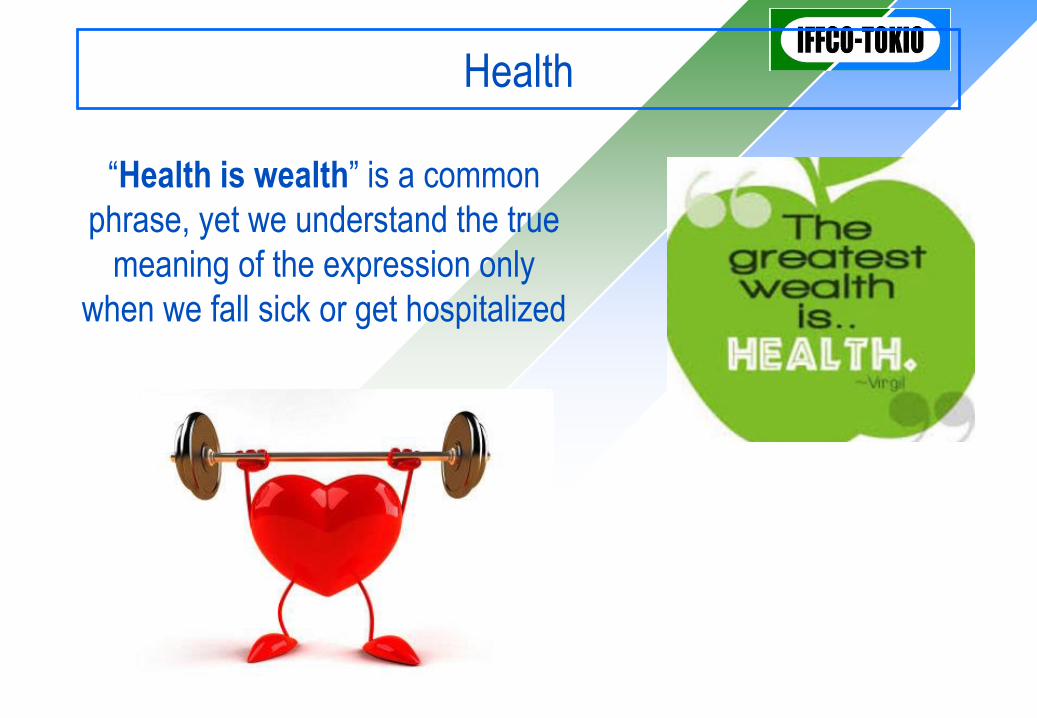

Survey on Medical Requirements

According to World Bank Report in the coming years

• 1 in 3 Person

Will develop some life threatening cancer.

• 1 in 4 Person

Will contact heart disease before they retire.

• 1 in 20 Person

Risk the chance of having stroke before the age of 70

Survey on Medical Requirements

• 85 % of the working population in India DO NOT have Rs.

5,00,000 as instant cash.

• 14 % have Rs. 5,00,000 instantly BUT will subsequently face a

financial crunch

• Only 1% can afford to spend Rs. 5,00,000 instantly and easily.

• 99 % of Indians will face financial crunch in case of any critical

illness.

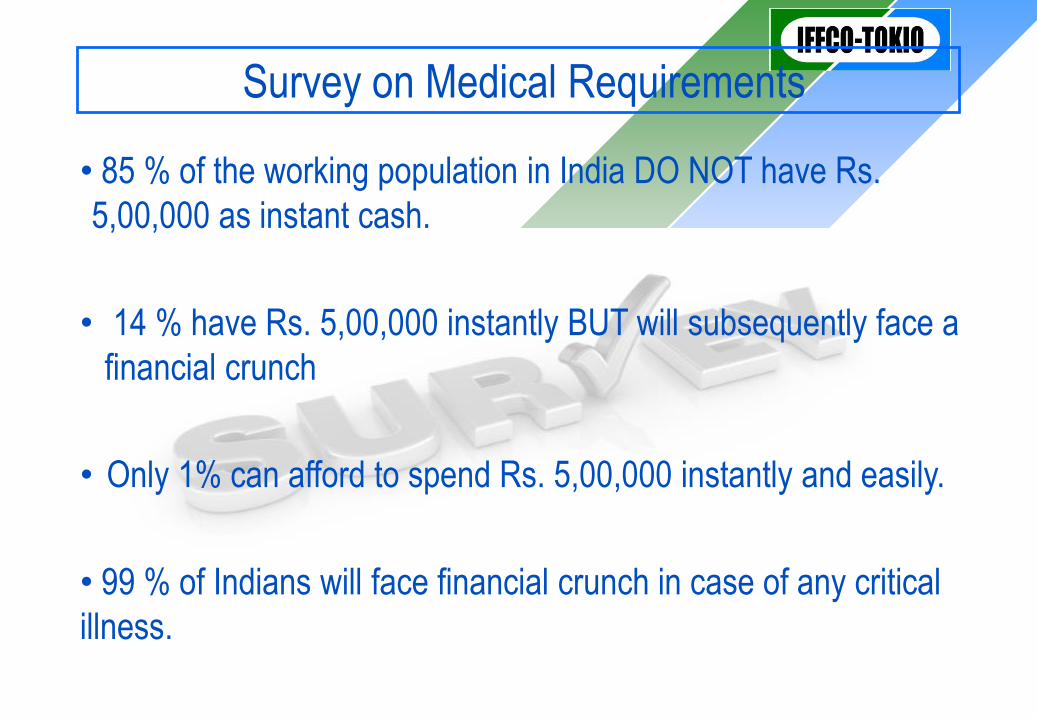

Overview of Treatment Cost

• Angioplasty

Rs. 3,00,000 to Rs. 6,00,000

• Open heart surgery

Rs. 3,50,000 to Rs. 7,50,000

• Liver Transplant

Rs. 30,00,000

• Kidney Transplant

Rs. 18,00,000 to 30,00,000

**** Imagine what will be the cost in the coming 10 to 15 years.

Benefits of Health Insurance

Ensure peace of mind

Flexible insurance cover

You can avail the facilities up to old age by renewing the

policy every year

No need to carry cash to the hospital because one can avail

the cashless treatment facilities

Income tax benefits under section 80D

Health Insurance Portability

Insurance Portability is a facility whereby a

policyholder can shift the existing health

insurance policy to another insurance company

providing better services and added benefits.

Health Policies of IFFCO TOKIO GENERAL

INSURANCE

HEALTH PROTECTOR (HP)

FAMILY HEALTH PROTECTOR (FHP) (Also known as

Family Floater)

HEALTH PROTECTOR PLUS (HPP)

Health Protector

This Policy offers a health protection

cover for you and your family for any

illness, disease or injury related

emergencies like hospitalization,

medical expenses, surgical expenses,

organ transplantation, etc.

Key Features

• Individual Sum Insured for each member

• Sum Insured from Rs. 50000 to Rs. 20 Lakhs

• *Critical Illness-Double your Sum Insured at additional premium of 30%

of basic premium

• Cashless Claim facility available at 4000 network hospitals across India

• Directly serviced by ITGI without any Third Party Administrator

• Portability Benefits

• Income Tax benefits under Section 80D

• *Day care surgeries covered

• Hospitalization more than 12 hours but less than 24 Hours: Up to 50% of

entitled room rent per day

Who Can be Covered

Person of any nationality, but primarily resident of India.

Unlimited no of members of family can be covered.

Entry age:18-65 years. Children from the age of 91 days

onward can be covered only if one or more parents are

covered.

Benefits under the Policy

*Hospitalization expenses

• Terrorism

In respect of SUM INSURED* less than Rs.5 (five) lakhs, room rent

expenses subject to following limits:

*Normal Room Rent Expenses :

• Class A Cities – Up to 1.75% of the Basic Sum Insured

• Other Cities – Up to 1.50% of the Basic Sum Insured

Benefits under the Policy

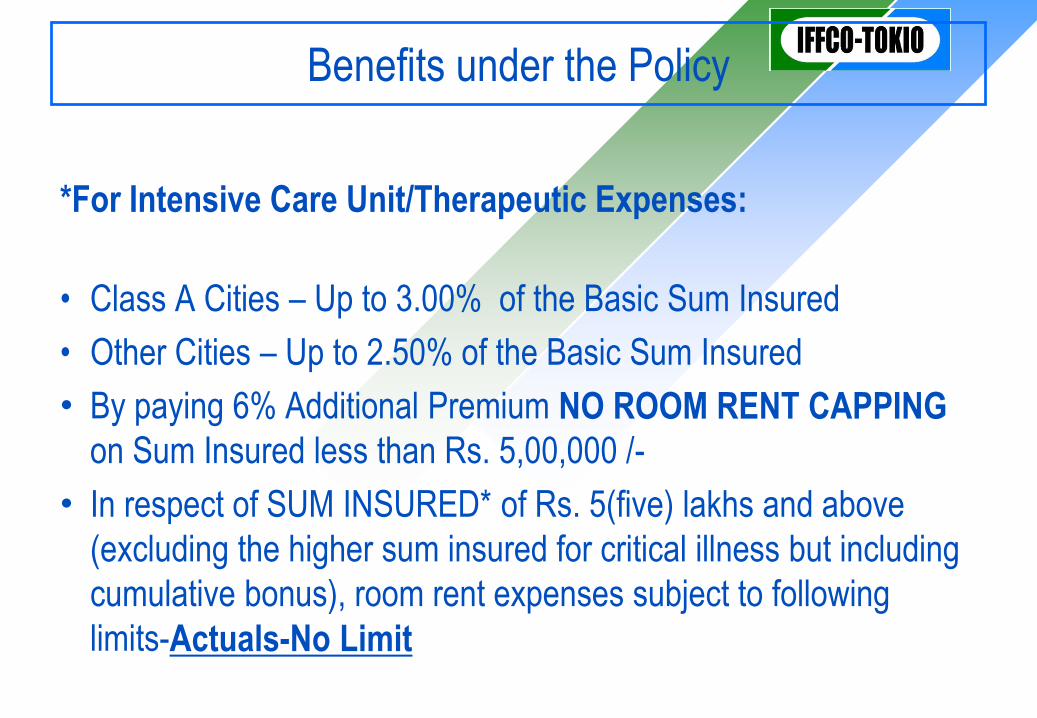

*For Intensive Care Unit/Therapeutic Expenses:

• Class A Cities – Up to 3.00% of the Basic Sum Insured

• Other Cities – Up to 2.50% of the Basic Sum Insured

• By paying 6% Additional Premium NO ROOM RENT CAPPING

on Sum Insured less than Rs. 5,00,000 /-

• In respect of SUM INSURED* of Rs. 5(five) lakhs and above

(excluding the higher sum insured for critical illness but including

cumulative bonus), room rent expenses subject to following

limits-Actuals-No Limit

Additional Benefits at no Extra cost

Daily Allowance - 0.20% of Sum Insured per day, for the duration

of hospitalisation

Ambulance Charges - 1% of Sum Insured or Rs. 2500 whichever

is less for each hospitalisation.

Pre and Post Hospitalization expenses for 45 days and 60 days

respectively

Cumulative Bonus - 5% of basic sum Insured subject to maximum

of 50% for claim free policy.

Additional Benefits at no Extra cost

Cost of Health Checkup - Up to 1% of the basic Sum Insured at

the end of block of four continuous claim free policies with us.

Vaccination Expenses - Up to 10% of the Total Premium paid at

the end of block of 2 continuous claim free policies

Ayurvedic, Homeopathic, Unani and Sidha (AYUSH)

hospitalisation treatments covered up to full Sum Insured

Emergency Assistance Services

ITGI provides the following Emergency Assistance Services to the

insured when he is traveling within India, 150 kilometers or more,

away from the residential address as mentioned in the policy

schedule for less than 90 days.

Medical consultation, evaluation and referral

to qualified physicians

Emergency medical evacuation to the nearest

medical facility capable of providing the required care.

Repatriation under medical supervision to insured person

Emergency Assistance Services :

Transportation to meet patient

Care and/or transportation of minor

children

Emergency message transmission

Return of dead body

Emergency cash coordination

Major Exclusions

Pre-Existing disease until 36months of continuous coverage has

elapsed

Any expense on hospitalization which incepts

during first 30 days of commencement of

cover

Any expense incurred in 1st year of operation of cover on

treatment of certain disease

Major Exclusions

Expense on diagnostic, X-ray, or laboratory examinations mainly

done in outpatient department.

Dental treatment or surgery of any kind

Maternity expenses, childbirth, miscarriage

including caesarean section and any infertility

treatment

Any expenses related to the disease due

to chronic alcohol consumption/self inflicted

toxic or drug consumption

Major Exclusions

Any expense related to injury suffered whilst engaged in speed

contest or racing like bungee jumping etc.

Any non medical expenses external medical equipment used at

home as post hospitalization care, like wheelchairs crutches etc.

Any expense on treatment related to HIV,

AIDS and all related medical condition

Plastic Surgery and Rehabilitation expenses

Free Lookup Period

You will be allowed a period of at least 15 (fifteen) days from the

date of receipt of the policy to review the terms and conditions of

the policy and to return the same if not acceptable stating the

reasons therein for doing so.

Free look period is not applicable for

renewal policies.

Quiz

1. Pre Existing Disease is not covered till

A) 24 Months

B) 36 Months

C) 48 Months

2. Ambulance Charges are covered

A) 1% of Sum Insured

B) 5% of Sum Insured

C) 10% of Sum Insured

Quiz

3. Korean came to India on Work Visa is he eligible for Health

Insurance

A) Yes

B) No

4. Sum Insured Limit in Health Protector Policy

A) 20 Lakhs

B) 30 Lakhs

C) 15 Lakh

Quiz

5) Loading Charged for Critical Illness

A) 10% B) 20%

C) 30% D) 40%

6) Registration and service charges are charged at

A) 1% B) 0.5%

C) 3% D) 5%

7) Normal Room Rent Expenses

A) 1.75% B)1.5%

C) 3% D) 2.5%

Quiz

8) Waiver of Room rent at no additional premium is applicable at what

Sum Insured

A) 500000 B) 200000

C) 300000 D) 100000

9) Pre & Post Hospitalisation

A) 40/60 days B)45/60 days

C) 60/90 days D) 50/60 days

10) Cumulative Bonus Applicable for claim free year

A) 5% B)7%

C) 6% D) 10%

Quiz

11) IT benefit cab be taken under which section

A) 80D B) 80C

B) 100A D) 102

12) Maximum No. of Family Members can be covered

A) 4 B) 3

C) Unlimited D) 5

13) By paying _______ extra premium Room Rent Capping can be

waived.

A) 6% B) 5%

C) 4% D)7%

Quiz

14) Room Rent expenses for ICU in Other Cities

A) 1.75% B)1.5%

C) 3% D)2.5%

15) Hospitalisation expenses in how many days is covered

A) 30 Days B)45 Days

C) 50 Days D) 60 Days

16) Entry Age in Health Protector Policy

A) 91 Days B) 18 Years

C) 23 Years D) 25 Years

This Policy offers a protection cover for you and your family for any

injury or disease related contingencies like hospitalisation, medical

expenses, surgical expenses, organ transplantation etc.

The Policy covers the members of the family consisting of you, your

spouse and dependent parent and children, brother, sister, brother-

in-law, sister-in-law, nephew, niece or any other relation who is

dependent or relatives living together

Coverage is under a single sum insured and no separate sum

insured is required for each covered member. Thus each covered

member draws claim from the single limit of indemnity.

FAMILY HEALTH PROTECTOR (FHP)

(Family Floater)

Key Features

Floater Sum Insured for Entire Family

Sum Insured from Rs. 150000 to 30 Lakhs

*Critical Illness-Double your Sum Insured at additional premium of

30% of basic premium

Cashless Claim facility available at 4000 network hospitals across

India

Directly serviced by ITGI without any Third Party Administrator

Portability Benefits

Income Tax benefits under Section 80D

Day Care Surgeries Covered

Who Can be Covered

Person of any nationality, but primarily resident of India.

Unlimited no of members of family can be covered.

Entry age:18-65 years. Children from the age of 91 days onward

can be covered only if one or more parents are covered.

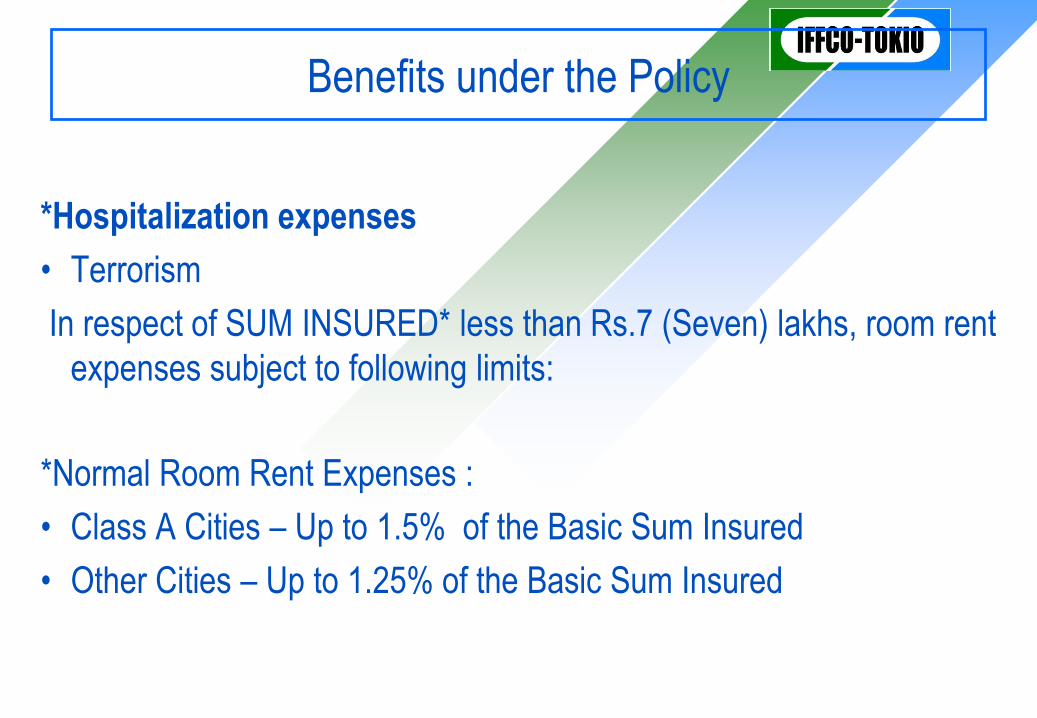

Benefits under the Policy

*Hospitalization expenses

• Terrorism

In respect of SUM INSURED* less than Rs.7 (Seven) lakhs, room rent

expenses subject to following limits:

*Normal Room Rent Expenses :

• Class A Cities – Up to 1.5% of the Basic Sum Insured

• Other Cities – Up to 1.25% of the Basic Sum Insured

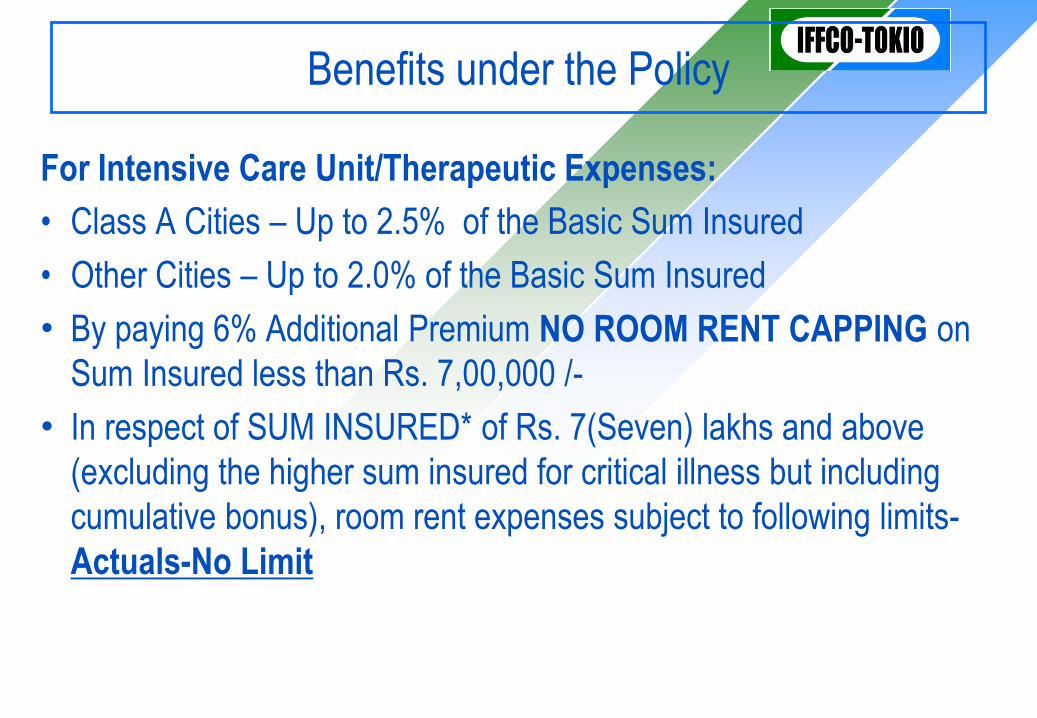

Benefits under the Policy

For Intensive Care Unit/Therapeutic Expenses:

• Class A Cities – Up to 2.5% of the Basic Sum Insured

• Other Cities – Up to 2.0% of the Basic Sum Insured

• By paying 6% Additional Premium NO ROOM RENT CAPPING on

Sum Insured less than Rs. 7,00,000 /-

• In respect of SUM INSURED* of Rs. 7(Seven) lakhs and above

(excluding the higher sum insured for critical illness but including

cumulative bonus), room rent expenses subject to following limits-

Actuals-No Limit

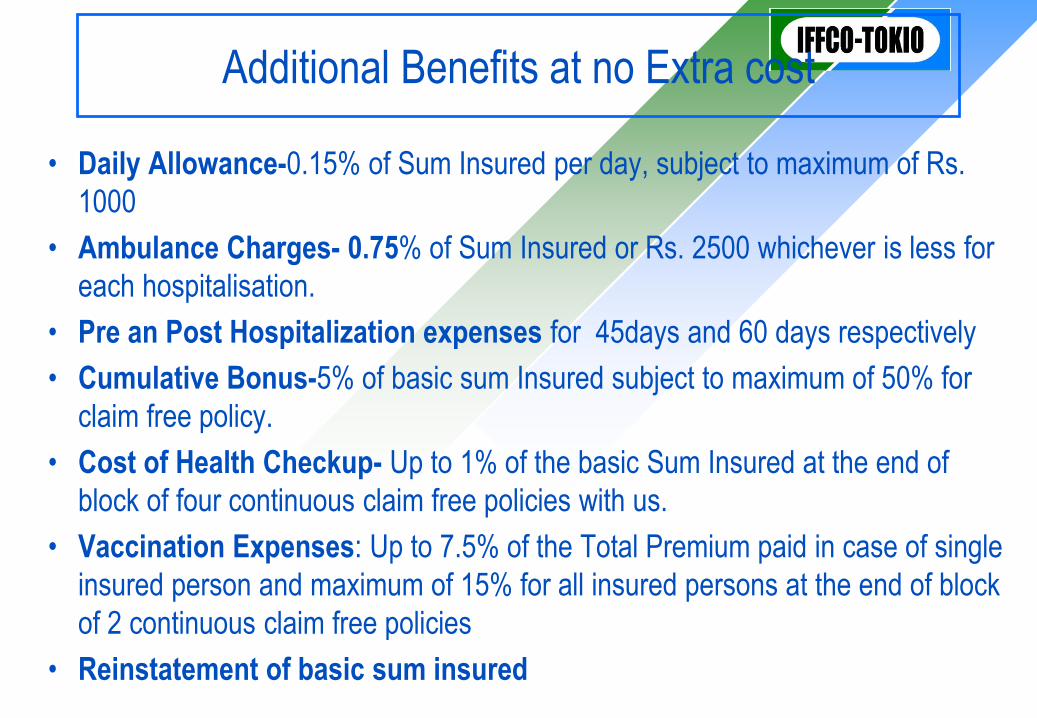

Additional Benefits at no Extra cost

• Daily Allowance-0.15% of Sum Insured per day, subject to maximum of Rs.

1000

• Ambulance Charges- 0.75% of Sum Insured or Rs. 2500 whichever is less for

each hospitalisation.

• Pre an Post Hospitalization expenses for 45days and 60 days respectively

• Cumulative Bonus-5% of basic sum Insured subject to maximum of 50% for

claim free policy.

• Cost of Health Checkup- Up to 1% of the basic Sum Insured at the end of

block of four continuous claim free policies with us.

• Vaccination Expenses: Up to 7.5% of the Total Premium paid in case of single

insured person and maximum of 15% for all insured persons at the end of block

of 2 continuous claim free policies

• Reinstatement of basic sum insured

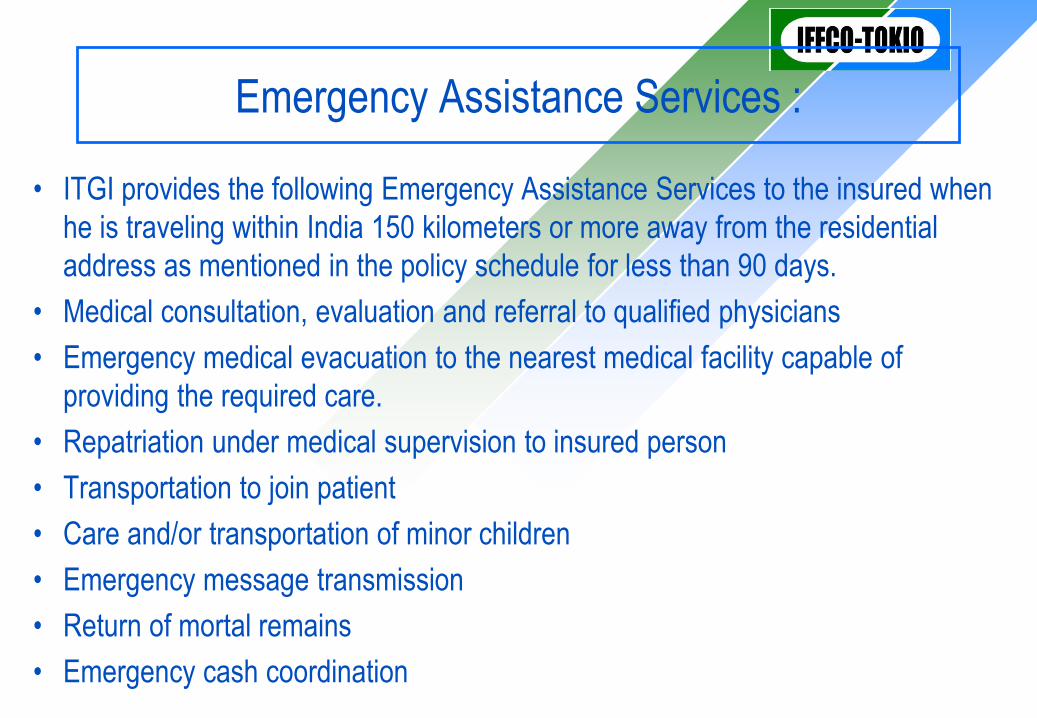

Emergency Assistance Services :

• ITGI provides the following Emergency Assistance Services to the insured when

he is traveling within India 150 kilometers or more away from the residential

address as mentioned in the policy schedule for less than 90 days.

• Medical consultation, evaluation and referral to qualified physicians

• Emergency medical evacuation to the nearest medical facility capable of

providing the required care.

• Repatriation under medical supervision to insured person

• Transportation to join patient

• Care and/or transportation of minor children

• Emergency message transmission

• Return of mortal remains

• Emergency cash coordination

Major Exclusions

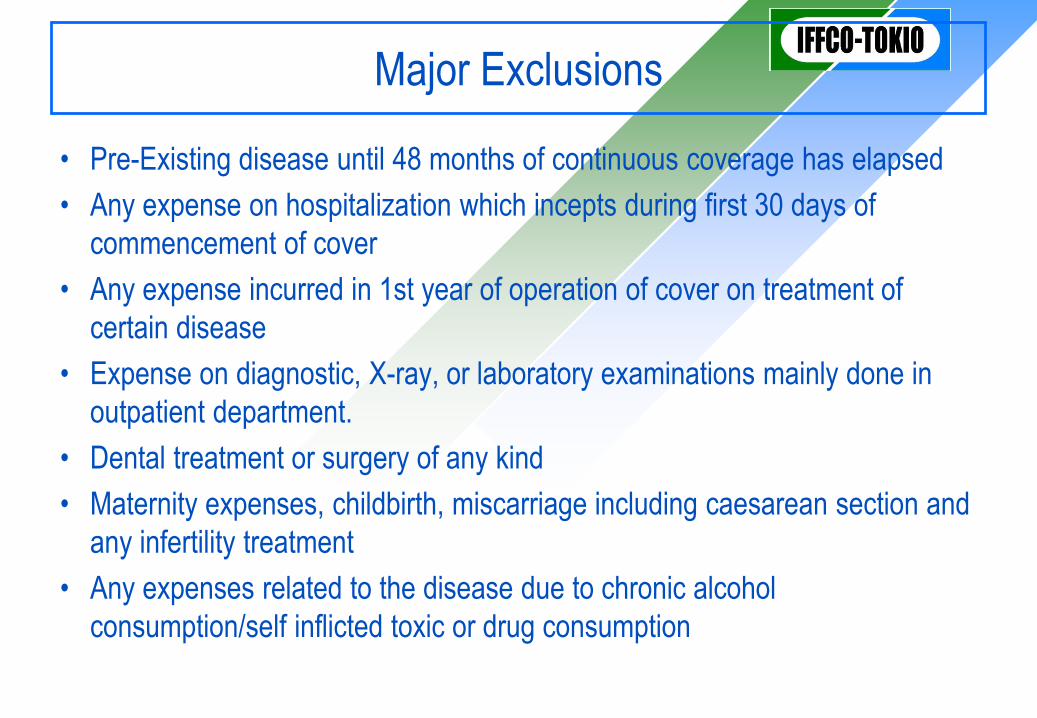

• Pre-Existing disease until 48 months of continuous coverage has elapsed

• Any expense on hospitalization which incepts during first 30 days of

commencement of cover

• Any expense incurred in 1st year of operation of cover on treatment of

certain disease

• Expense on diagnostic, X-ray, or laboratory examinations mainly done in

outpatient department.

• Dental treatment or surgery of any kind

• Maternity expenses, childbirth, miscarriage including caesarean section and

any infertility treatment

• Any expenses related to the disease due to chronic alcohol

consumption/self inflicted toxic or drug consumption

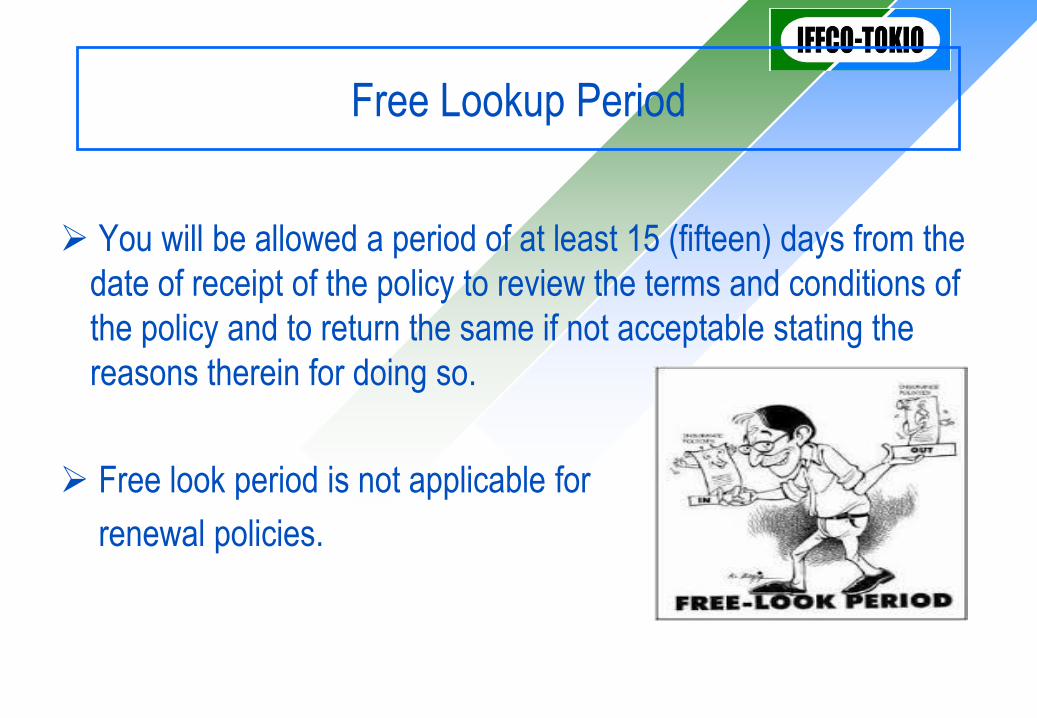

Free Lookup Period

You will be allowed a period of at least 15 (fifteen) days from the

date of receipt of the policy to review the terms and conditions of

the policy and to return the same if not acceptable stating the

reasons therein for doing so.

Free look period is not applicable for

renewal policies.

HEALTH PROTECTOR

Individual sum insured policy

Unlimited number of persons can be

covered

No restriction on relations covered

No Room rent capping – above Rs. 5

lacs sum insured

Lesser Sum Insured – Option to waive

room rent capping

12 – 24 hrs of hospitalization covered

Vaccination charges paid once in two

years

FAMILY HEALTH PROTECTOR

Floater insurance policy

Unlimited number of persons can be

covered

No restriction on relations covered

No Room rent capping – above Rs. 7 lacs

sum insured

Lesser Sum Insured – Option to waive

room rent capping

12 – 24 hrs of hospitalization covered

Vaccination charges paid once in two

years

Brief Description of Both Products

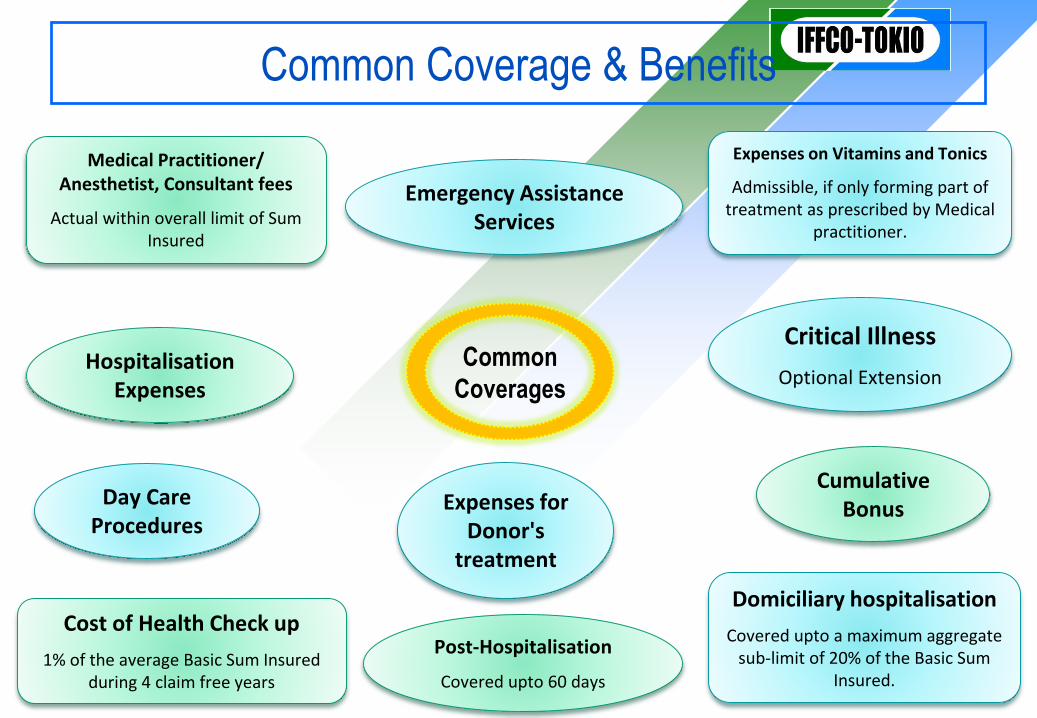

Common

Coverages

Expenses on Vitamins and Tonics

Admissible, if only forming part of treatment as prescribed by Medical

practitioner.

Post-Hospitalisation

Covered upto 60 days

Cost of Health Check up

1% of the average Basic Sum Insured during 4 claim free years

Domiciliary hospitalisation

Covered upto a maximum aggregate sub-limit of 20% of the Basic Sum

Insured.

Day Care Procedures

Medical Practitioner/ Anesthetist, Consultant fees

Actual within overall limit of Sum Insured

Cumulative Bonus

Emergency Assistance Services

Critical Illness

Optional Extension

Expenses for Donor's

treatment

Hospitalisation Expenses

Common Coverage & Benefits

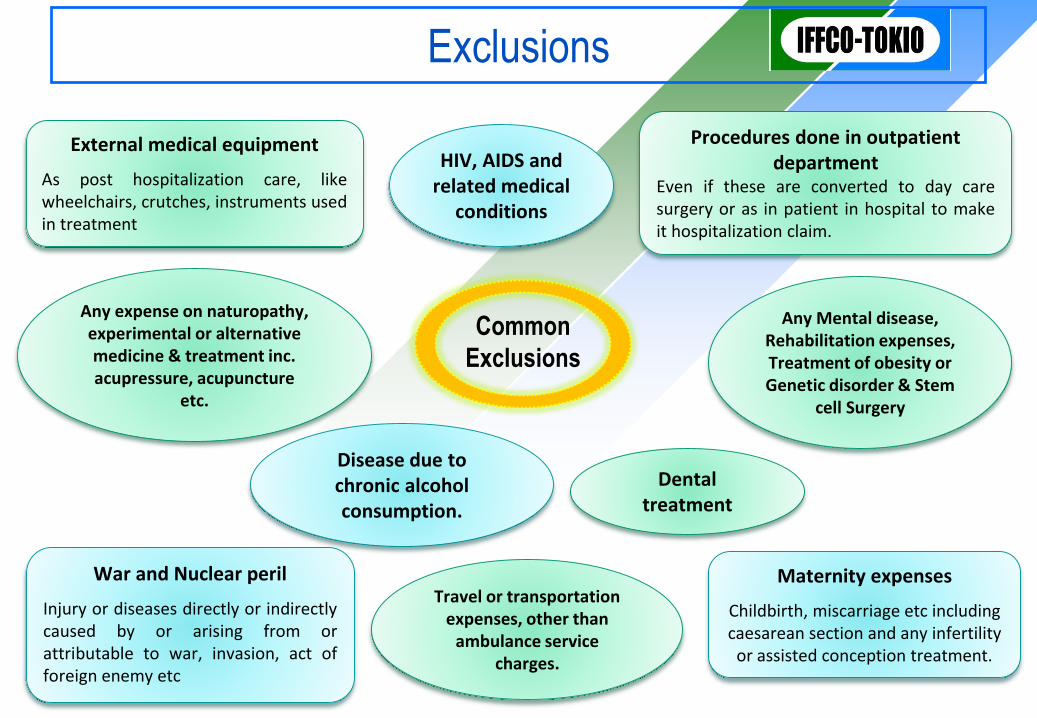

Common

Exclusions

Any expense on naturopathy, experimental or alternative medicine & treatment inc. acupressure, acupuncture

etc.

War and Nuclear peril

Injury or diseases directly or indirectlycaused by or arising from orattributable to war, invasion, act offoreign enemy etc

Maternity expenses

Childbirth, miscarriage etc including caesarean section and any infertility

or assisted conception treatment.

Disease due to chronic alcohol consumption.

External medical equipment

As post hospitalization care, likewheelchairs, crutches, instruments usedin treatment

Procedures done in outpatient department

Even if these are converted to day caresurgery or as in patient in hospital to makeit hospitalization claim.

Dental treatment

Any Mental disease, Rehabilitation expenses, Treatment of obesity or Genetic disorder & Stem

cell Surgery

HIV, AIDS and related medical

conditions

Travel or transportation expenses, other than

ambulance service charges.

Exclusions

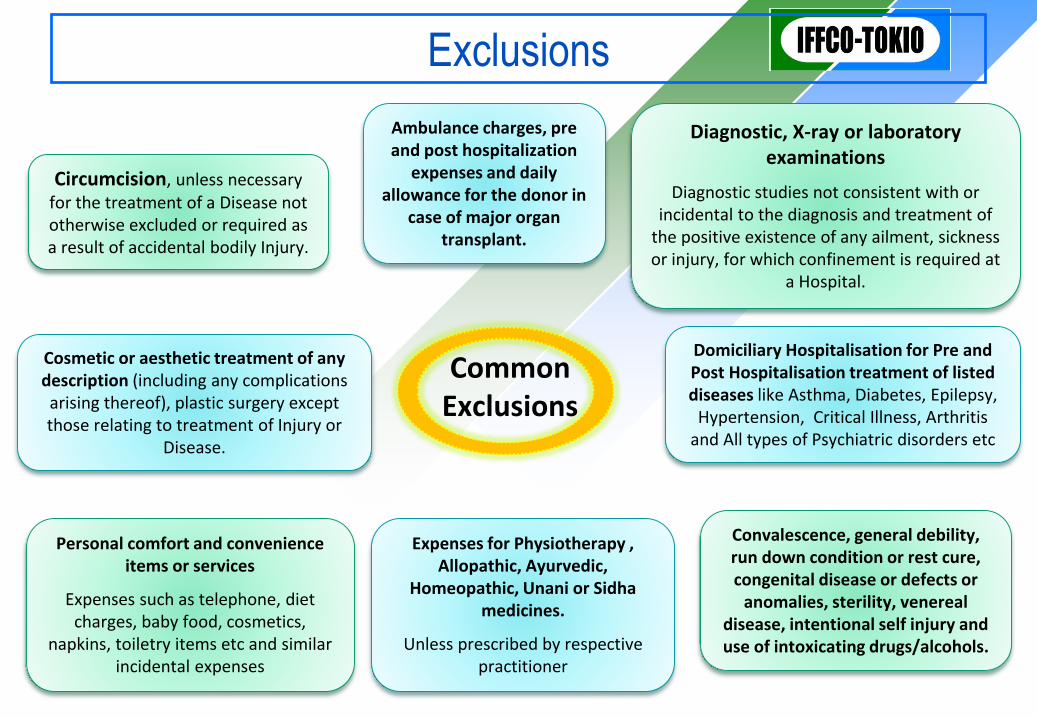

Common Exclusions

Ambulance charges, pre and post hospitalization

expenses and daily allowance for the donor in

case of major organ transplant.

Personal comfort and convenience items or services

Expenses such as telephone, diet charges, baby food, cosmetics,

napkins, toiletry items etc and similar incidental expenses

Convalescence, general debility, run down condition or rest cure, congenital disease or defects or

anomalies, sterility, venereal disease, intentional self injury and use of intoxicating drugs/alcohols.

Circumcision, unless necessary for the treatment of a Disease not otherwise excluded or required as a result of accidental bodily Injury.

Diagnostic, X-ray or laboratory examinations

Diagnostic studies not consistent with or incidental to the diagnosis and treatment of

the positive existence of any ailment, sickness or injury, for which confinement is required at

a Hospital.

Cosmetic or aesthetic treatment of any description (including any complications arising thereof), plastic surgery except those relating to treatment of Injury or

Disease.

Expenses for Physiotherapy , Allopathic, Ayurvedic,

Homeopathic, Unani or Sidha medicines.

Unless prescribed by respective practitioner

Domiciliary Hospitalisation for Pre and Post Hospitalisation treatment of listed diseases like Asthma, Diabetes, Epilepsy,

Hypertension, Critical Illness, Arthritis and All types of Psychiatric disorders etc

Exclusions

Quiz

1)Normal Room Rent expenses for Class A cities

A) 1.5% B)1.25%

C) 2.5% D) 2%

2) Pre and Post Hospitalization

A) 45/60 Days B) 60/60 Days

C) 40/60 Days D) 60/90 Days

3) Pre Existing disease are covered after

A) 36 Months B) 48 Months

C) 12 Months D) 24 Months

Quiz

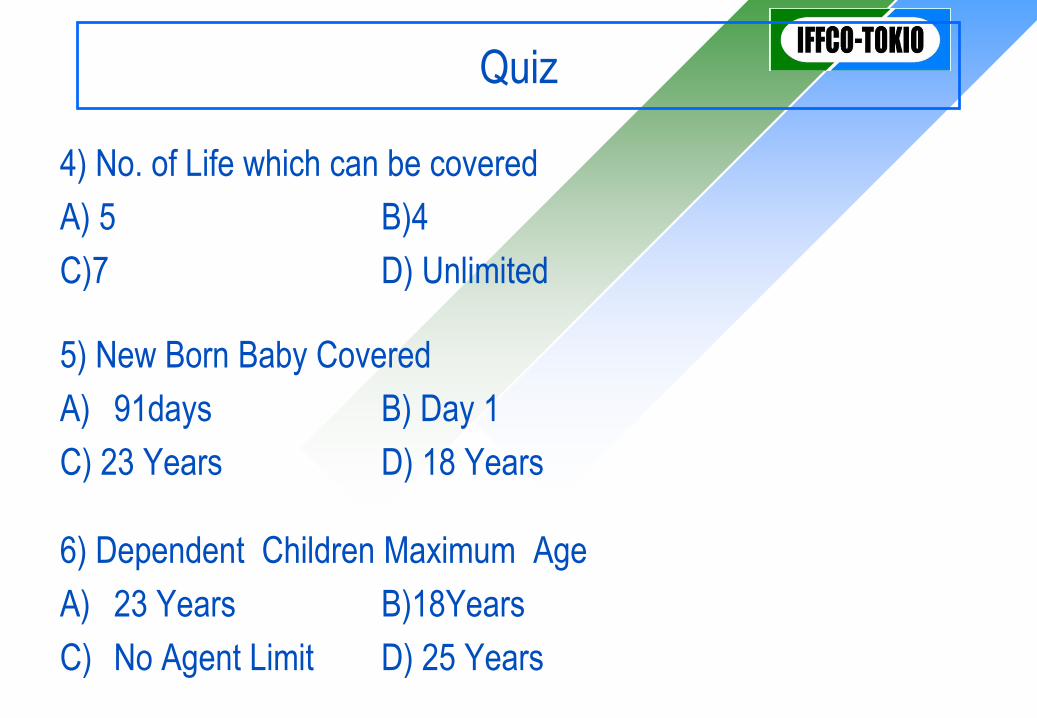

4) No. of Life which can be covered

A) 5 B)4

C)7 D) Unlimited

5) New Born Baby Covered

A) 91days B) Day 1

C) 23 Years D) 18 Years

6) Dependent Children Maximum Age

A) 23 Years B)18Years

C) No Agent Limit D) 25 Years

Quiz

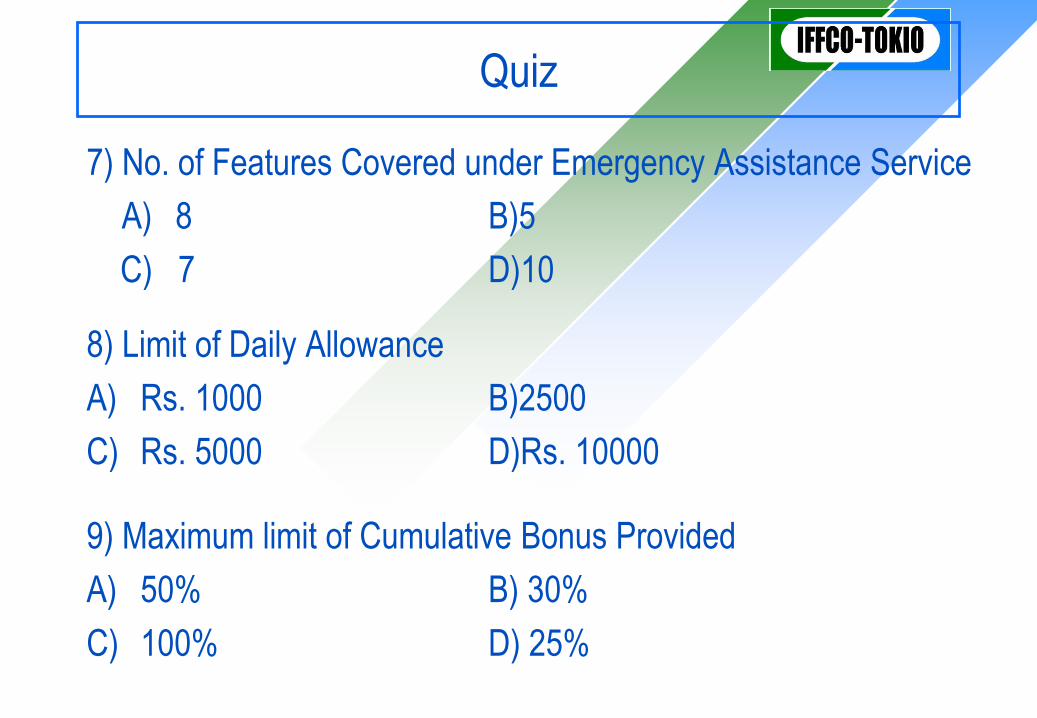

7) No. of Features Covered under Emergency Assistance Service

A) 8 B)5

C) 7 D)10

8) Limit of Daily Allowance

A) Rs. 1000 B)2500

C) Rs. 5000 D)Rs. 10000

9) Maximum limit of Cumulative Bonus Provided

A) 50% B) 30%

C) 100% D) 25%

Quiz

10) Cumulative Bonus Applicable for claim free year

A) 5% B)7%

C) 6% D) 10%

11) IT benefit cab be taken under which section

A) 80D B) 80C

C) 100A D) 102

12) Maximum No. of Family Members can be covered

A) 4 B) 3

C) Unlimited D)5

Quiz

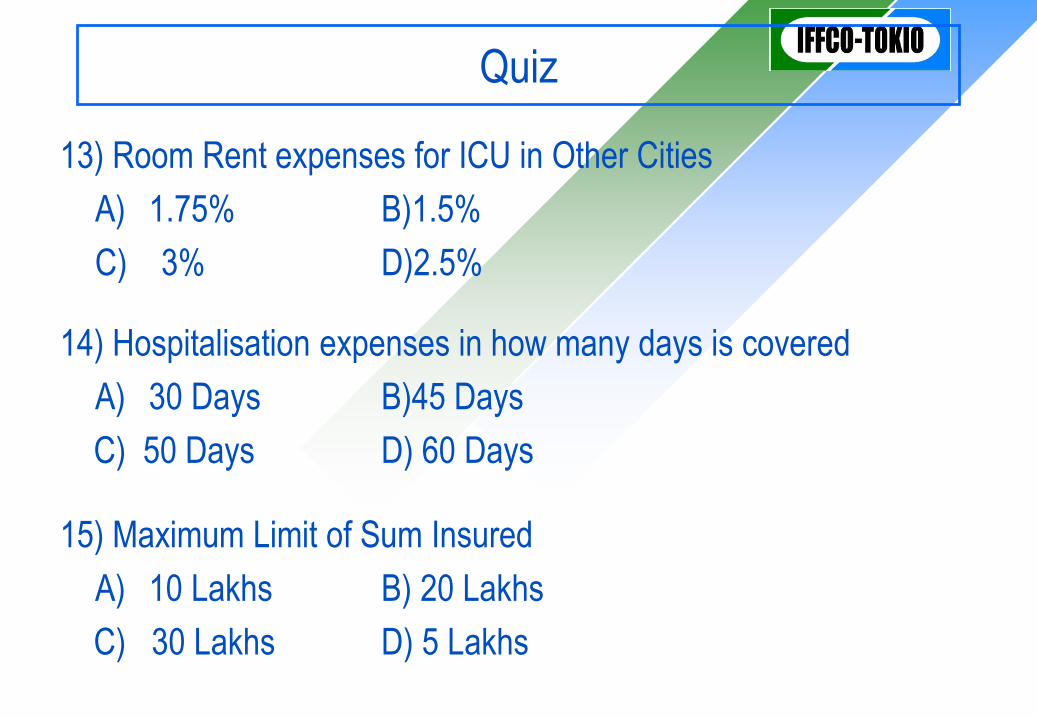

13) Room Rent expenses for ICU in Other Cities

A) 1.75% B)1.5%

C) 3% D)2.5%

14) Hospitalisation expenses in how many days is covered

A) 30 Days B)45 Days

C) 50 Days D) 60 Days

15) Maximum Limit of Sum Insured

A) 10 Lakhs B) 20 Lakhs

C) 30 Lakhs D) 5 Lakhs

Quiz

16) Ambulance Charges % and Minimum Amount

A) 0.5%/2500 B) 0.75%/2000

C) 0.75%/2500 D) 0.5%/2000

17) No Room Rent Capping is at what Sum Insured

A) 7 Lakh B) 5 Lakh

C) 3 Lakh D) 6 Lakh

18) By paying _______ extra premium Room Rent Capping can be waived.

A)6% B) 5%

C) 4% D) 7%

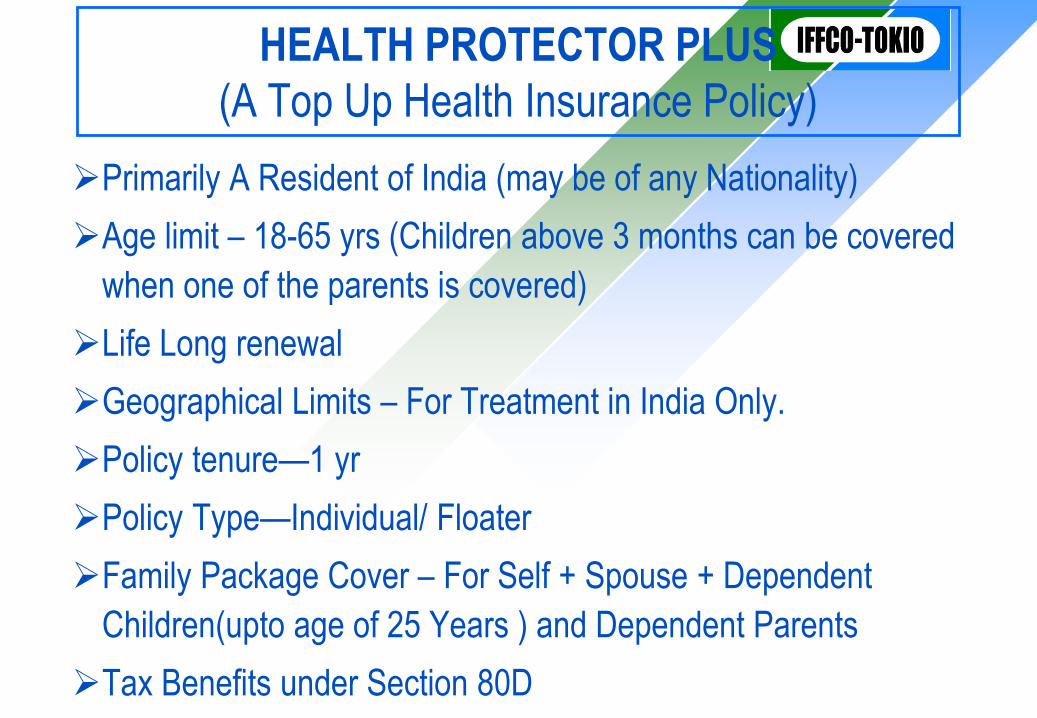

HEALTH PROTECTOR PLUS

(A Top Up Health Insurance Policy)

Primarily A Resident of India (may be of any Nationality)

Age limit – 18-65 yrs (Children above 3 months can be covered

when one of the parents is covered)

Life Long renewal

Geographical Limits – For Treatment in India Only.

Policy tenure—1 yr

Policy Type—Individual/ Floater

Family Package Cover – For Self + Spouse + Dependent

Children(upto age of 25 Years ) and Dependent Parents

Tax Benefits under Section 80D

Widest range of Plans to offer -- 8 different plans

Deductible* - It is a cost-sharing requirement that provides that the Insurer will not be liable for a specified rupee

amount in case of indemnity policies and for a specified number of days/ hours in case of hospital cash policies

which will apply before any benefits are payable by the Insurer. A deductible does not reduce the sum insured.

Top-Up Cover

Deductible applicable on “Per Event” Basis

Super Top Up cover

Deductible applicable on “Per Policy” basis

Plan A B C D E F G H

Sum Insured 200000 400000 500000 500000 750000 1000000 1500000 2500000

Deductible* 100000 200000 200000 300000 300000 500000 500000 500000

HEALTH PROTECTOR PLUS PLANS

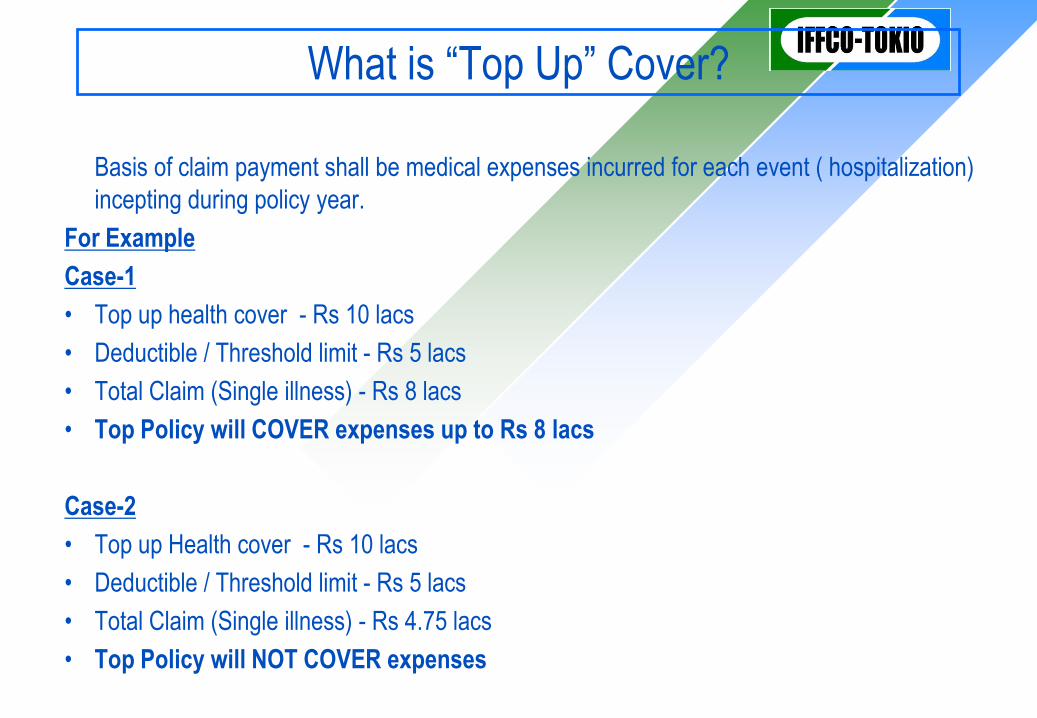

What is “Top Up” Cover?

Basis of claim payment shall be medical expenses incurred for each event ( hospitalization)

incepting during policy year.

For Example

Case-1

• Top up health cover - Rs 10 lacs

• Deductible / Threshold limit - Rs 5 lacs

• Total Claim (Single illness) - Rs 8 lacs

• Top Policy will COVER expenses up to Rs 8 lacs

Case-2

• Top up Health cover - Rs 10 lacs

• Deductible / Threshold limit - Rs 5 lacs

• Total Claim (Single illness) - Rs 4.75 lacs

• Top Policy will NOT COVER expenses

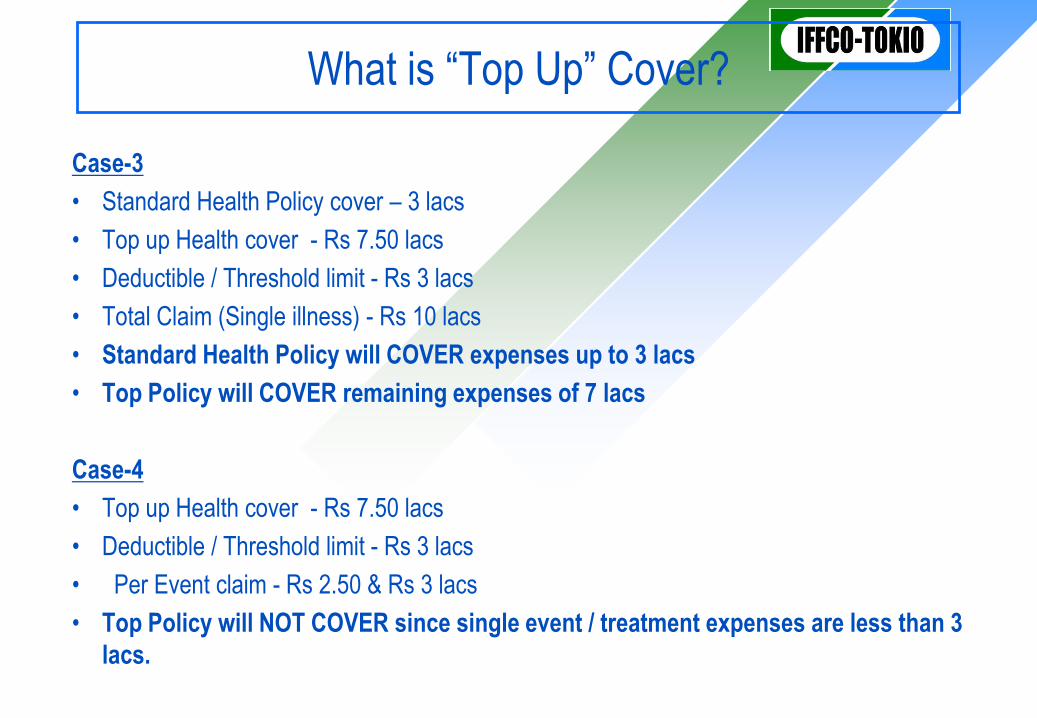

What is “Top Up” Cover?

Case-3

• Standard Health Policy cover – 3 lacs

• Top up Health cover - Rs 7.50 lacs

• Deductible / Threshold limit - Rs 3 lacs

• Total Claim (Single illness) - Rs 10 lacs

• Standard Health Policy will COVER expenses up to 3 lacs

• Top Policy will COVER remaining expenses of 7 lacs

Case-4

• Top up Health cover - Rs 7.50 lacs

• Deductible / Threshold limit - Rs 3 lacs

• Per Event claim - Rs 2.50 & Rs 3 lacs

• Top Policy will NOT COVER since single event / treatment expenses are less than 3

lacs.

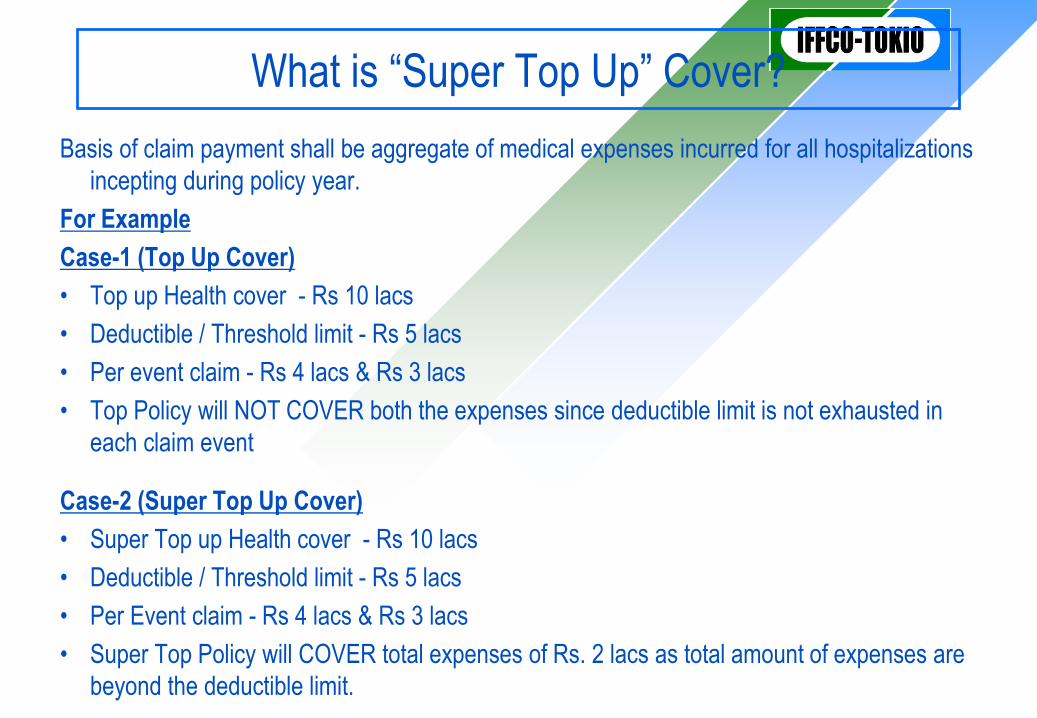

What is “Super Top Up” Cover?

Basis of claim payment shall be aggregate of medical expenses incurred for all hospitalizations

incepting during policy year.

For Example

Case-1 (Top Up Cover)

• Top up Health cover - Rs 10 lacs

• Deductible / Threshold limit - Rs 5 lacs

• Per event claim - Rs 4 lacs & Rs 3 lacs

• Top Policy will NOT COVER both the expenses since deductible limit is not exhausted in

each claim event

Case-2 (Super Top Up Cover)

• Super Top up Health cover - Rs 10 lacs

• Deductible / Threshold limit - Rs 5 lacs

• Per Event claim - Rs 4 lacs & Rs 3 lacs

• Super Top Policy will COVER total expenses of Rs. 2 lacs as total amount of expenses are

beyond the deductible limit.

Let’s take an example…..

But…What if the Hospitalization expenses exceeds 500,000?

What if he change his job and there is a gap before he joins new company?

What if he decides to quit his job and start his own work?

What will happen after his retirement?

Can he take tax benefit under section 80D?

Narendra and his family is covered under Employer’s Group Health Insurance for Rs.

500,000.

IFFCO Tokio Health Protector Plus provides the solutions at a very

low premium and even a lower cost after the Income Tax Benefits.

S.No.Name of

InsuredDate of Birth

Relationship

with InsuredGender Sum Insured Deductible

Waiver of

Deductible

1 Narendra 09-09-1984 Self Male

1000000 500000 90 Days

2 Madhuri 18-06-1986 Wife Female

3 Himanshu 27-06-2008 SonMale

4 Anjali 06-05-2010 DaughterFemale

Premium

S.Tax

Rs.

Rs.

7399

924

Rs.

Income Tax Benefit Under Sec 80 D @ 80% slab Rs.

Net cost for a Rs. 10 Lakhs cover for 4 people Rs.

8323

2497

5826

So many questions, one simple solution…

Salient Features

• High Coverage…… Low Premium

• Sum insured options (with deductible) – 8 plans ranging from Rs. 2

lacs to 25 lacs

• Individual & Family floater options available

• Family discounts under individual option : For 2 members - 5% and

for 3 or more - 10%

• Policy can be purchased as :

1. Independent policy without any basic health cover.

2. Top-up to the existing basic health policy of other insurance

company.

3. Top-up for IFFCO Tokio standard health cover.

Salient Features

• Option to convert to standard health policy with continuity of

benefits after 04 continuous years with us

• Waiver of Deductible in case of change/loss of job

• Pre and Post hospitalization of 60 and 90 days respectively

• Income tax benefits under section 80D

• Lifelong renewal

• Portability

• Emergency Assistance Services

• Cashless Claim Facility

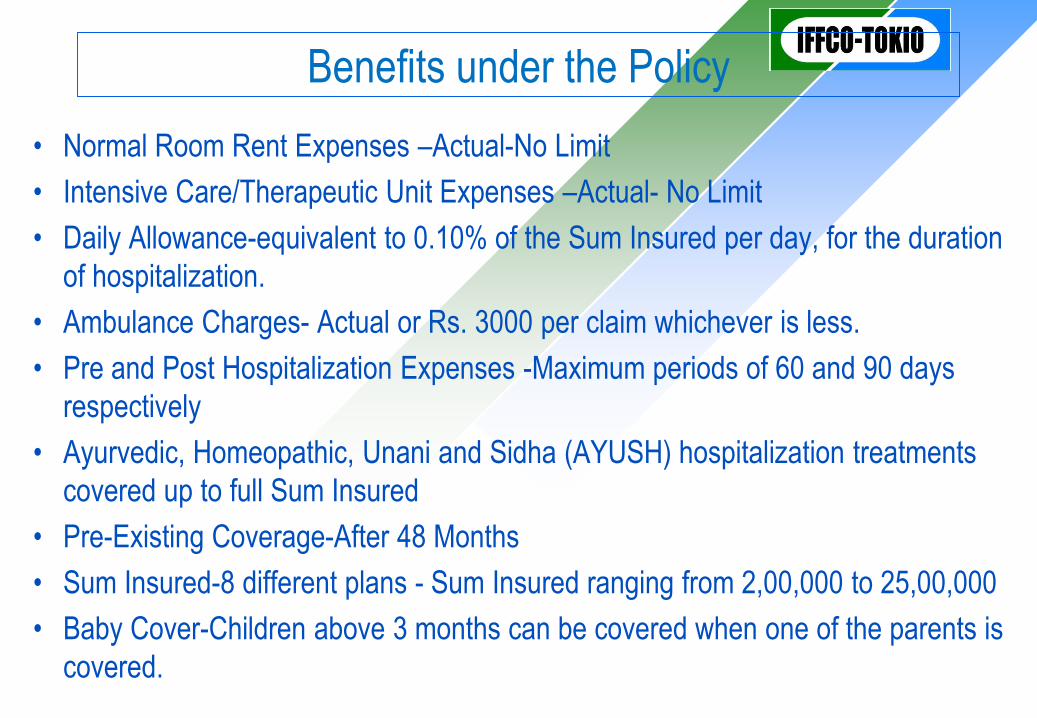

Benefits under the Policy

• Normal Room Rent Expenses –Actual-No Limit

• Intensive Care/Therapeutic Unit Expenses –Actual- No Limit

• Daily Allowance-equivalent to 0.10% of the Sum Insured per day, for the duration

of hospitalization.

• Ambulance Charges- Actual or Rs. 3000 per claim whichever is less.

• Pre and Post Hospitalization Expenses -Maximum periods of 60 and 90 days

respectively

• Ayurvedic, Homeopathic, Unani and Sidha (AYUSH) hospitalization treatments

covered up to full Sum Insured

• Pre-Existing Coverage-After 48 Months

• Sum Insured-8 different plans - Sum Insured ranging from 2,00,000 to 25,00,000

• Baby Cover-Children above 3 months can be covered when one of the parents is

covered.

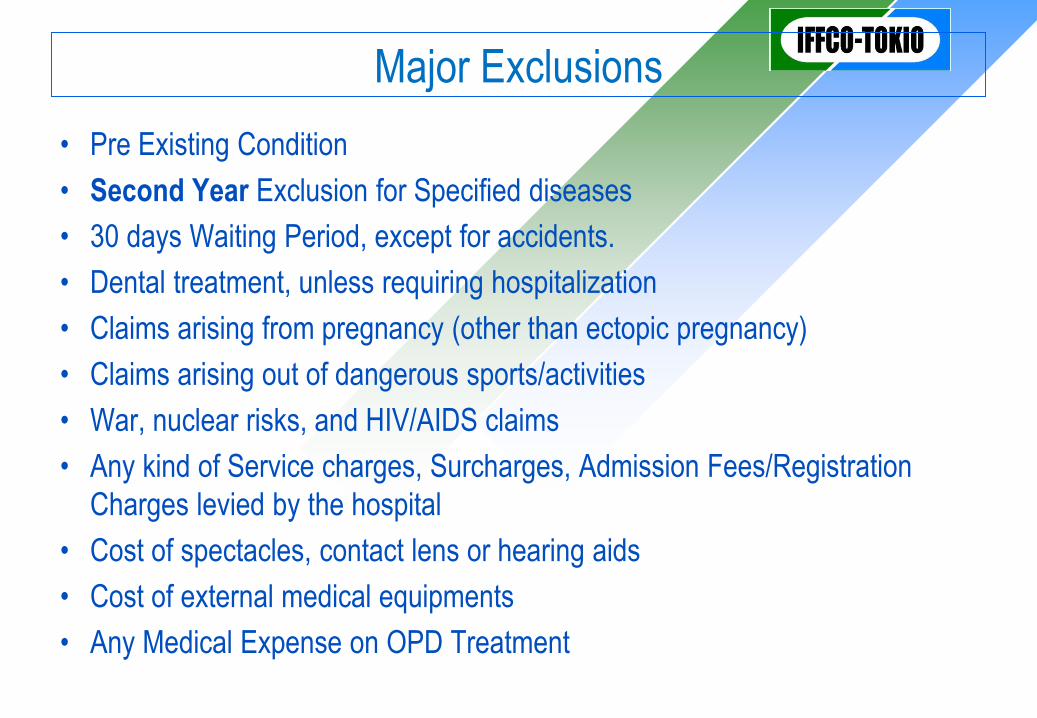

Major Exclusions

• Pre Existing Condition

• Second Year Exclusion for Specified diseases

• 30 days Waiting Period, except for accidents.

• Dental treatment, unless requiring hospitalization

• Claims arising from pregnancy (other than ectopic pregnancy)

• Claims arising out of dangerous sports/activities

• War, nuclear risks, and HIV/AIDS claims

• Any kind of Service charges, Surcharges, Admission Fees/Registration

Charges levied by the hospital

• Cost of spectacles, contact lens or hearing aids

• Cost of external medical equipments

• Any Medical Expense on OPD Treatment

Major Exclusions

• Expenses on Diagnostic, X-Ray, or Laboratory examinations

unless related to the active treatment of Disease or Injury falling

within ambit of Hospitalization claim.

• Genetic disorders and stem cell implantation/surgery.

• Expenses on naturopathy, experimental or alternative medicine,

acupressure, acupuncture, magnetic and similar therapies.

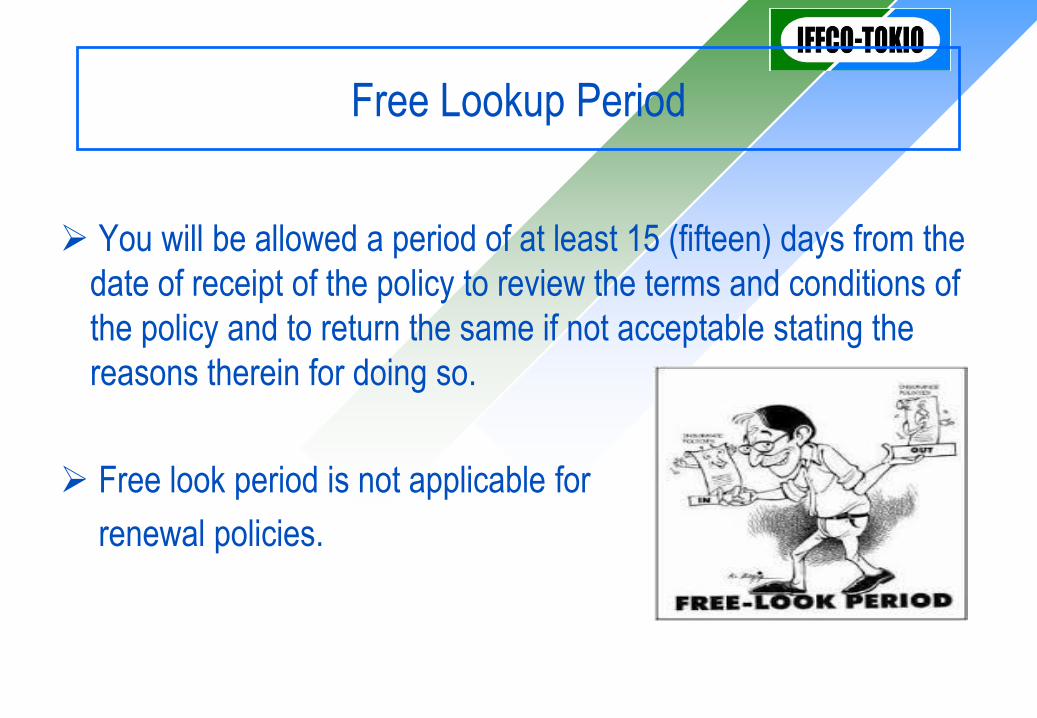

Free Lookup Period

You will be allowed a period of at least 15 (fifteen) days from the

date of receipt of the policy to review the terms and conditions of

the policy and to return the same if not acceptable stating the

reasons therein for doing so.

Free look period is not applicable for

renewal policies.

Quiz

1) Entry Age for HPP Policy

A) 18 Years B) 65 Years

C) 91 Days D) 25 Years

2) Geographical Limit in India

A) Anywhere in India B) Any where in World

C) Anywhere in Asia D) None of Above

Quiz

3) Type of policy

A) Individual B) Floater

C) Individual/Floater D) None

4) Minimum duration of hospitalisation required is

A) 24 Hours B) 48 Hours

C) 12 Hours D) 36 Hours

Quiz

5) Normal Room Rent Capping

A) No Limit B)1.75% of SI

C) 1.5% of SI D) 2% of SI

6) Ambulance Charges

A) 3000 B) 2000

C) 2500 D)None

Quiz

7) Pre and Post Hospitalisation

A) 60/90days B) 60/60days

C) 45/60Dayd D) 60/45 Days

8) Pre-Existing disease covered after

A) 18 Months B) 36 Month

C) 12 Months D) None

Quiz

9) Children Cover

A) Day 1 B) 18years

C) 91 Days D) None

10) Top-Up Cover Deductible applicable

A) on “Per Event” Basis B) Per Policy Basis

C) Per year basis D) None

Quiz

11. No, of Plans in HPP Policy

A) 8 B) 10

C) 15 D) 5

12) Range of Sum Insured in HPP Policy

A) 2 Lakh to 25 Lakh B) 1.5 Lakh to 30 Lakh

C) 2.5 Lakh to 20 Lakh D) 5 Lakh to 25 Lakh

Thank you