Embed Size (px)

Citation preview

April 2014

Health Care Reform: Top Employer Questions

Health Care Reform

• Enacted in March 2010 • Makes significant changes to health care system • Implemented over several years

Affordable Care Act

• Health care providers • Government programs • Health insurance issuers • Employers/plan sponsors • Individuals

Provisions that impact:

Most employers that offer health plans will be impacted in some way

Q: What is a grandfathered plan (and do I have one)?

Grandfathered Plans

• Health plan or health insurance coverage that covered individuals on March 23, 2010

• Determination made separately for each benefit package

Definition

• Do not significantly change costs or benefits • Provide notice to participants and

beneficiaries in plan materials • Keep records of plan terms

Requirements

• Depends on each plan • New plans are not grandfathered • Check with your broker or carrier • Does not automatically expire

Status

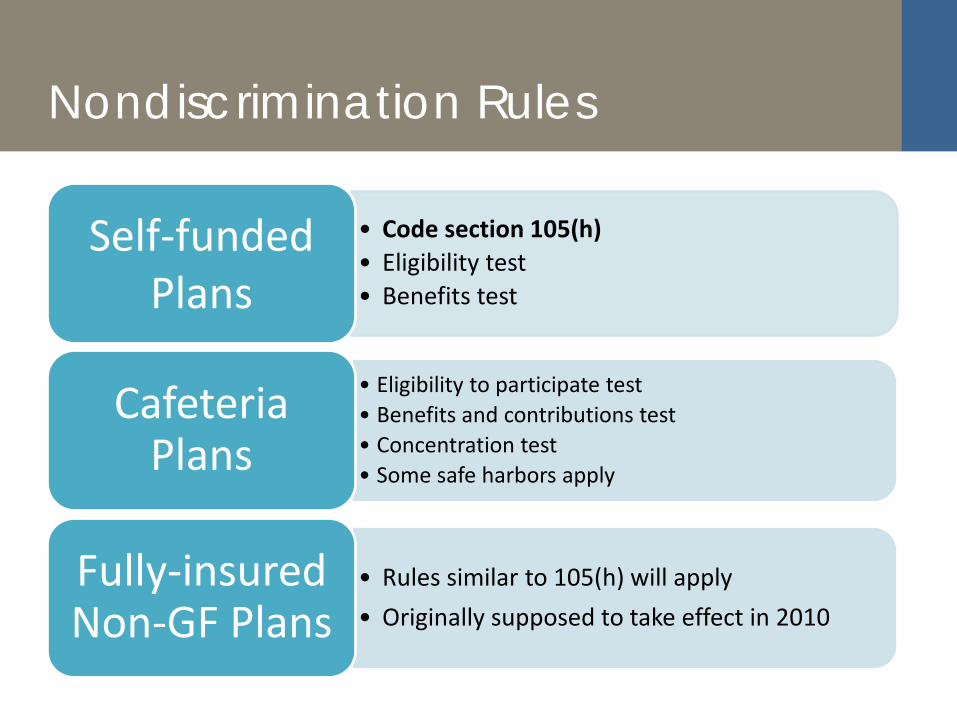

Nondiscrimination Rules

• Code section 105(h) • Eligibility test • Benefits test

Self-funded Plans

• Eligibility to participate test • Benefits and contributions test • Concentration test • Some safe harbors apply

Cafeteria Plans

• Rules similar to 105(h) will apply • Originally supposed to take effect in 2010

Fully-insured Non-GF Plans

Q: Do I have to offer health coverage to my employees?

Employer Shared Responsibility Rules (Pay or Play)

• No requirement to offer coverage • Can get tax credits for providing

coverage

Small Employers (fewer than 50

FT/FTE employees)

• Must make coverage available to FT employees and dependents

• Coverage must be affordable and adequate

• Penalties delayed until 2015 (2016 for 50-99)

Large Employers (50+ FT/FTE

employees)

Employer penalties triggered if any full-time employee receives subsidized coverage in an Exchange

Potential Penalties

• Employer did not offer coverage to substantially all FT employees and dependents (children)

• $2,084 x (all FT employees – 30)

Penalty A - Available

• Employer offered coverage to substantially all FT employees/dependents

• But, for some employee’s coverage is not affordable (9.5%) or adequate (60% or more AV)

• $3,126 x each employee who gets subsidized coverage (capped at Penalty A amount)

Penalty B – Affordable & Adequate

Avoiding Penalties

Offer coverage to FT employees and dependents that:

Affordable

•Employee’s contribution for self-only coverage does not exceed 9.5% of income

•Safe harbors for what income and premium amount to use

Adequate

•Plan covers at least 60% of costs on average

•MV calculator or design-based checklists

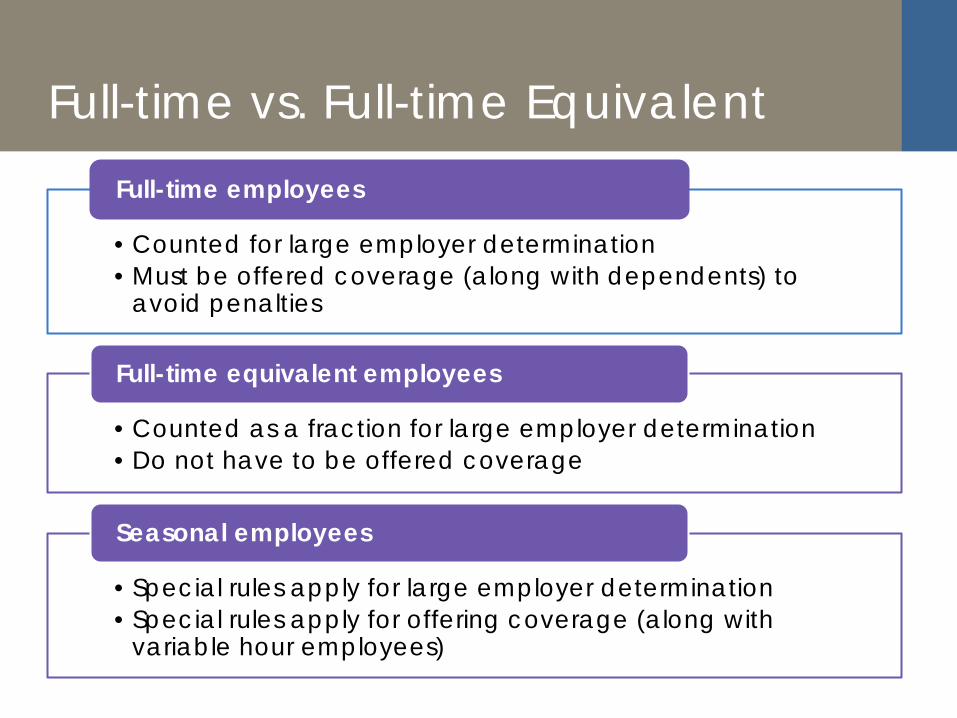

Q: Who is a full-time employee?

Full-time vs. Full-time Equivalent

•Counted for large employer determination •Must be offered coverage (along with dependents) to

avoid penalties

Full-time employees

•Counted as a fraction for large employer determination •Do not have to be offered coverage

Full-time equivalent employees

•Special rules apply for large employer determination •Special rules apply for offering coverage (along with

variable hour employees)

Seasonal employees

Q: What is an Exchange?

American Health Benefits Exchange

Public health insurance exchange required by ACA

Primarily online marketplace for purchasing health insurance (Qualified Health Plans)

Run by state or federal government with consumer assistance from other entities

For individuals and small employers (generally up to 50 employees)

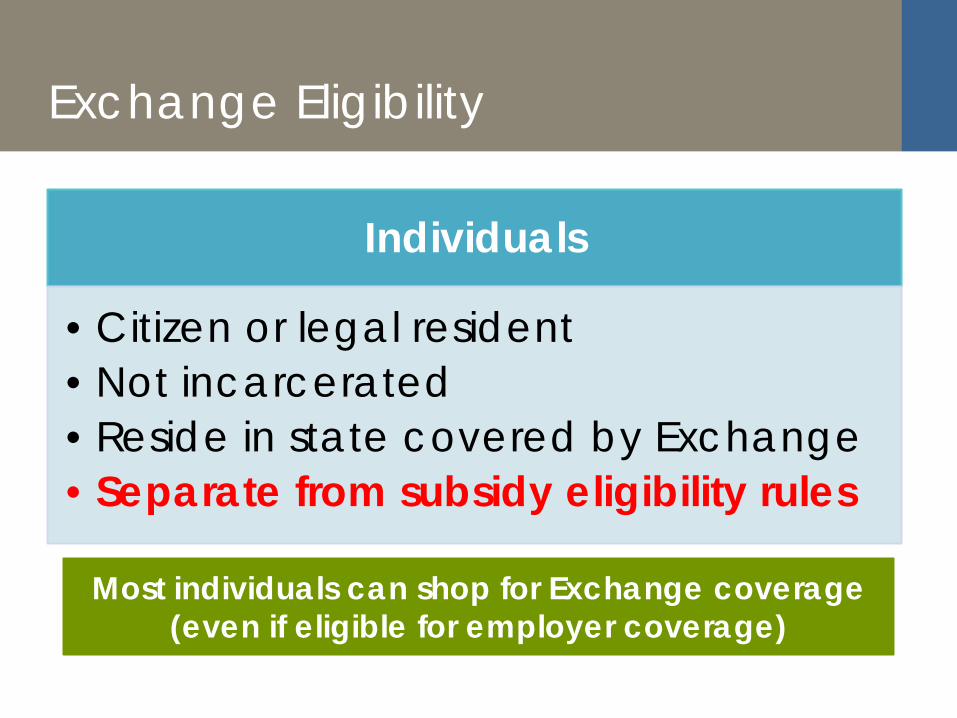

Exchange Eligibility

Individuals

•Citizen or legal resident •Not incarcerated •Reside in state covered by Exchange •Separate from subsidy eligibility rules

Most individuals can shop for Exchange coverage (even if eligible for employer coverage)

Exchange Subsidies

Provide assistance to low-income individuals: • 100%-400% of federal poverty level • Not eligible for government programs that provide

coverage

To help pay premiums or reduce cost-sharing

Not available to individuals who are: • Eligible for affordable, minimum-value employer

coverage or • Enrolled in an employer plan

Q: What fees do we have to pay under health care reform?

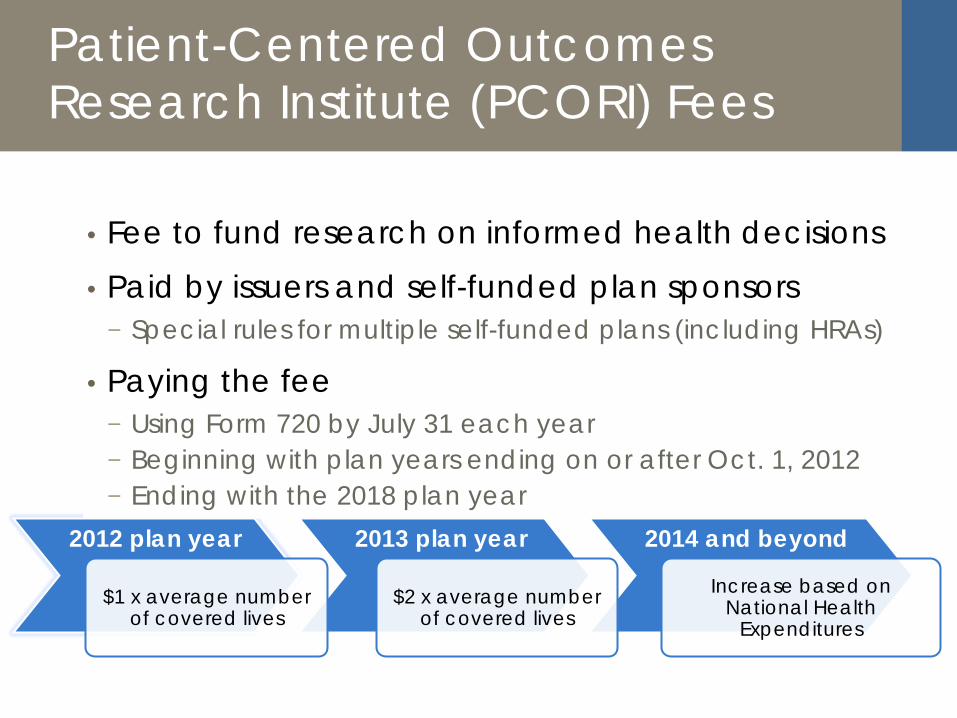

2014 and beyond 2013 plan year

Patient-Centered Outcomes Research Institute (PCORI) Fees

2012 plan year

$1 x average number of covered lives

$2 x average number of covered lives

Increase based on National Health

Expenditures

• Fee to fund research on informed health decisions • Paid by issuers and self-funded plan sponsors − Special rules for multiple self-funded plans (including HRAs)

• Paying the fee − Using Form 720 by July 31 each year − Beginning with plan years ending on or after Oct. 1, 2012 − Ending with the 2018 plan year

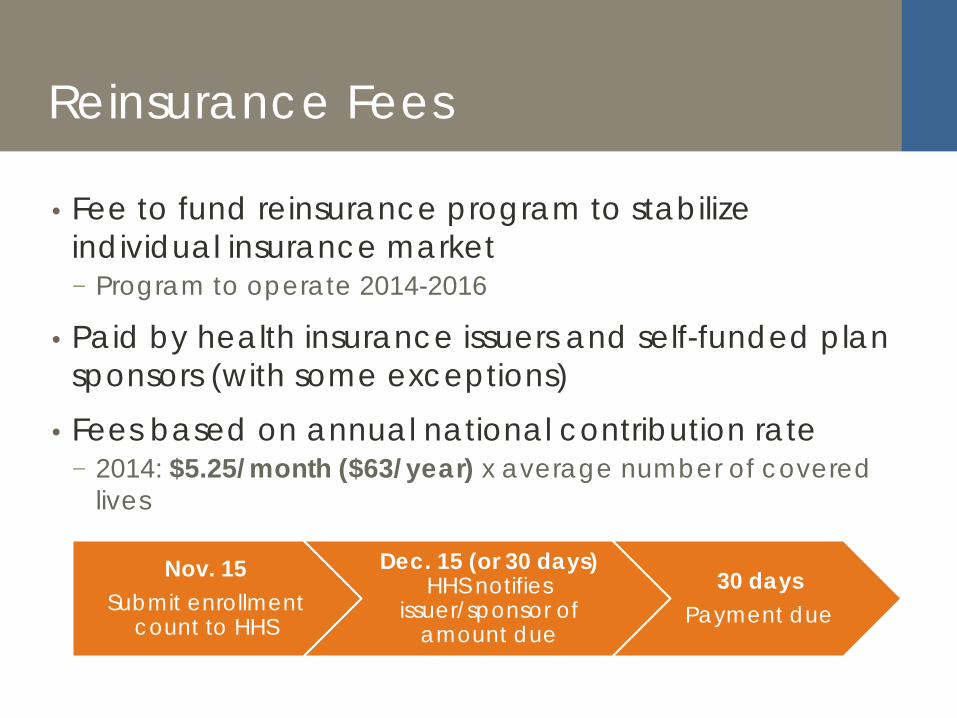

Reinsurance Fees

• Fee to fund reinsurance program to stabilize individual insurance market − Program to operate 2014-2016

• Paid by health insurance issuers and self-funded plan sponsors (with some exceptions)

• Fees based on annual national contribution rate − 2014: $5.25/month ($63/year) x average number of covered

lives

Nov. 15 Submit enrollment

count to HHS

Dec. 15 (or 30 days) HHS notifies

issuer/sponsor of amount due

30 days Payment due

Health Insurance Providers Fee • Annual fee on health insurance providers − Effective in 2014 − Due Sept. 30 each year − Allocated according to market share: $8B in 2014 - $14.3B in

2018 (based on premium growth in later years)

Applies to:

Covered Entities

Including health insurance issuers and

HMOs

Does not apply to: Companies with $25M or

less in net premiums

Self-insured employers

Government and non-profit entities

VEBAs

Ross & Yerger Resources Health Care Reform Access all the information you and your employees need, including legislative updates, timelines and explanations Compliance Hands on guidance to complex legislative topics HR & Legal Support Access to certified HR professionals and labor attorneys Documents on Command Instant access to a library of downloadable articles, brochures, forms and reports

Health & Wellness Education Newsletters that help employees understand important health care issues and educate them on making wise health care decisions Community Connect with other professionals in your field by entering group discussions, or posting a message of your own Benchmark Surveys Participate in benefit plan surveys & benchmark your plan to peers Training Center Provide ready-to-go HR training courses on a number of different topics to employees