Embed Size (px)

Citation preview

HB Litigation Conferences Presents:

Reinsurance Outlook 2010February 9, 2010 | 30 Rockefeller Plaza, 36th Floor, New YorkConference Chairs: Scott Birrell, Esq., Vice President and Associate General Counsel, Travelers, Hartford, CT John Finnegan, Esq., Chadbourne & Parke, LLP, New York Wendy Shapss, CPA, CFE, Senior Managing Director, FTI Consulting, Inc., New York

8:00 Registration & Continental Breakfast

8:45 Welcome and Introductory Remarks

9:00 Dealing with Major Recurring Issues •Productv.OperationsClaims•NetRetainedLinesProvision•Warranties•Allocation•Aggregation•LateNotice•LegallyObligatedToPay•ChallengesToUnderwritingProcess•FollowTheFortunesModerator: Kenneth Levine, Esq., Nelson Levine deLuca & Horst, Blue Bell, PAJessica Pardi, Esq., Morris Manning & Martin, LLP, Atlanta Benjamin Gonson, Esq., Nicoletti Gonson Spinner Owen LLP, New York

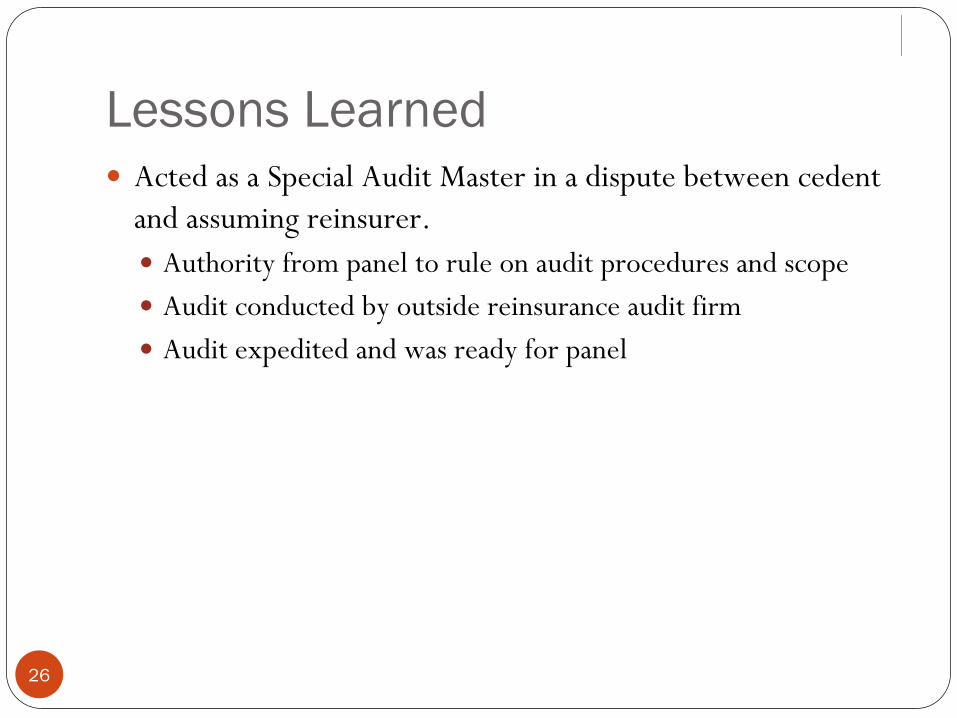

10:00 Reinsurance Audits – A Cedent and Reinsurer View •Interpretingtheaccesstorecordsclause•Preparingforareinsuranceclaimaudit•Preparingforatransactionalaudit•Lessonslearnedandthevalueofauditsforbothcompanies Richard Hershman, Senior Managing Director, Leader of Insurance Services, FTI Consulting, Inc., New York John O’Connor, Senior Vice President and Head of Claims, Endurance Services Limited, New York

11:00 Morning Break

11:15 Preserving Privileges: Ethical Issues Confronting Reinsurers, Insurers, Policyholders & Counsel (ABA Model Rule 1.6) •HowToDistinguishBetween“Defense”Communicationsand“Coverage”Communications•HowCoverageDenialsOrReservationsOfRightsAffectPrivileges•HowPresenceOfMultipleInsuredsWithConflictingInterestsCouldAffectPrivileges•HowInsuranceCompaniesCanEvaluateCoverageClaimsWithoutWaivingPrivileges•CommunicationsBetweenInsurerandReinsurer:AreTheyPrivilegedStephen Weisbrod, Esq., Gilbert LLP, Washington, DC Robert Van Kirk, Esq., Williams & Connolly LLP, Washington, DC Bryce Friedman, Esq., Simpson Thacher & Bartlett LLP, New York John Finnegan, Esq., Chadbourne & Parke LLP, New York

12:15 Networking Luncheon Sponsored by FTI Consulting, Inc.

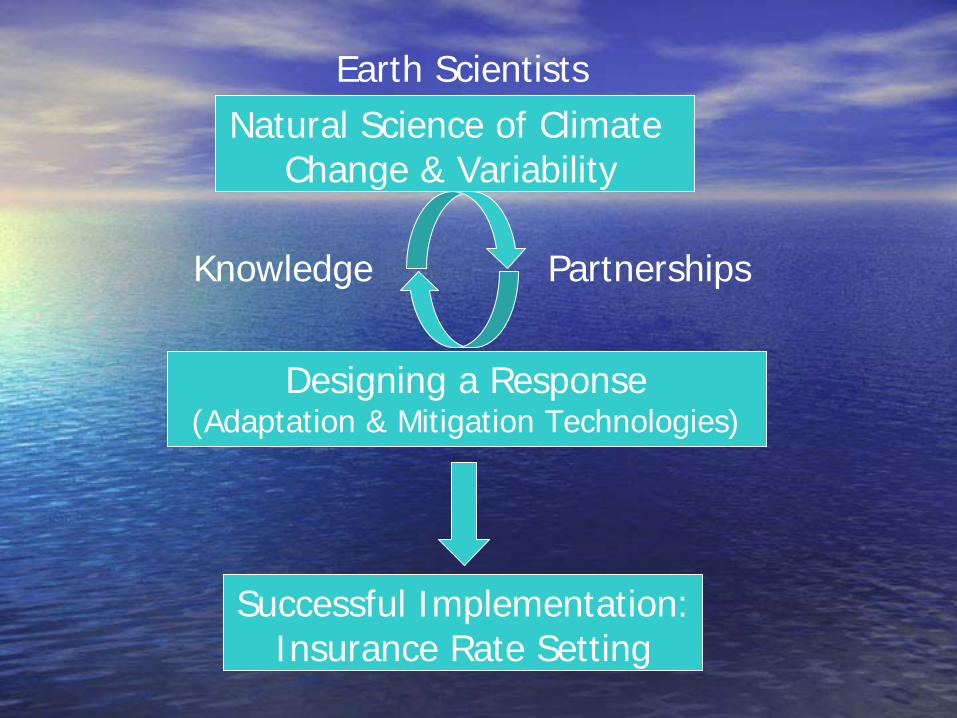

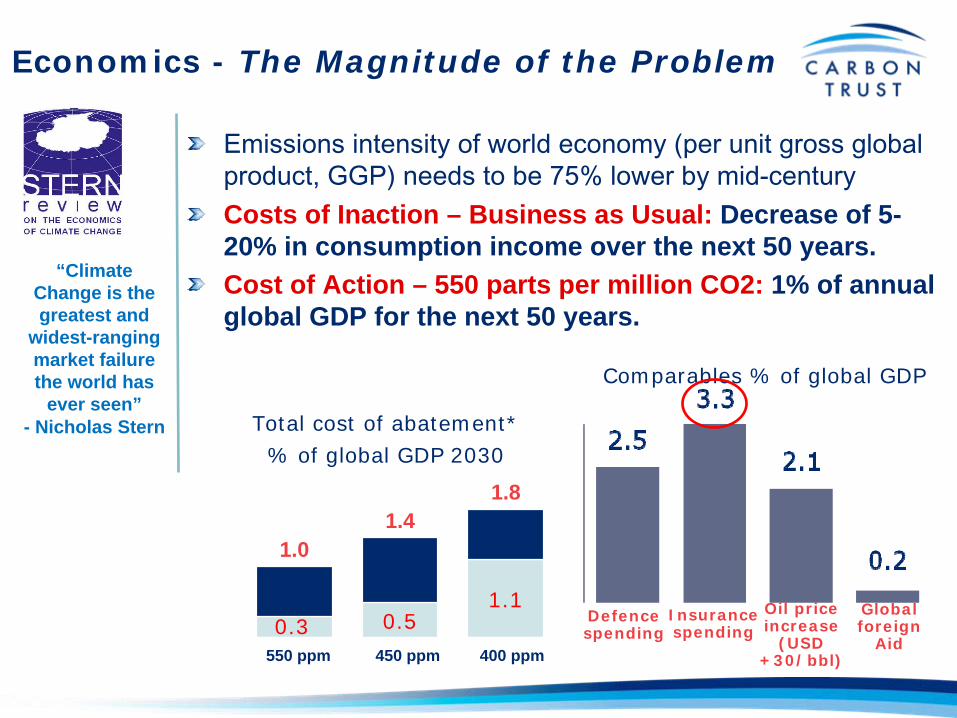

1:15 Climate Change: Reinsurance Risks & Opportunities •TheImportanceoftheInsuranceAssetInTheProcessOfAcceleratingDeliveryofNewTechnologyToMarketToCombatClimateChange Lewis Rothstein, PhD, Principal Scientist, WeatherPredict Consulting, Inc., and Professor of Oceanography, University of Rhode Island Graduate School of Oceanography, Narragansett, RI Chris Walker, Chief Executive Officer, The Carbon Trust, New York Michael Cohen, Vice President, Government Affairs, Ren Re, Washington, DC

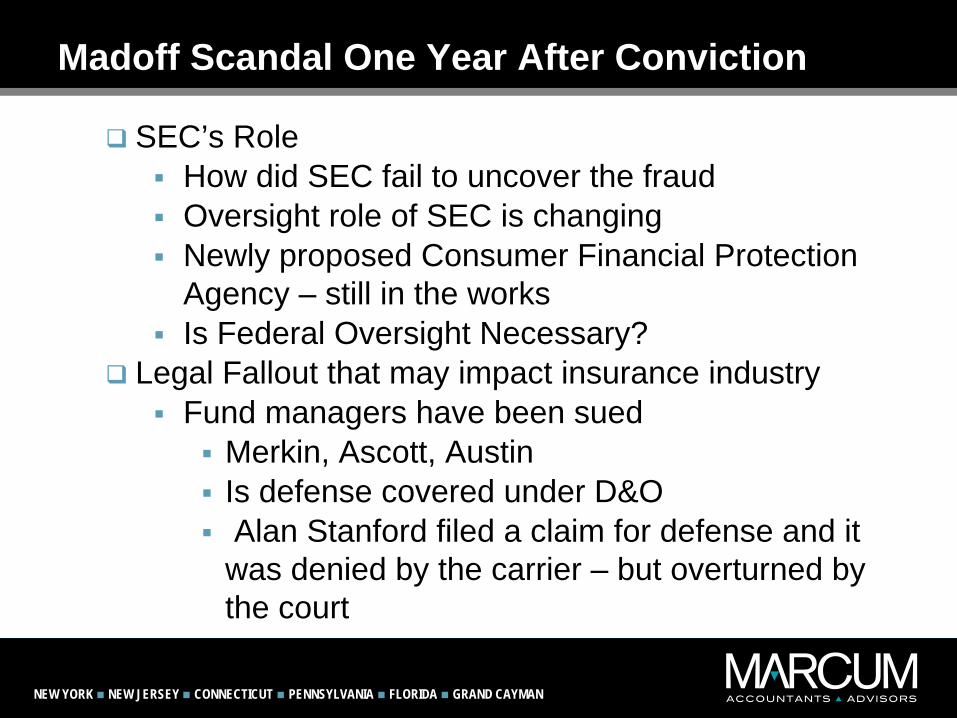

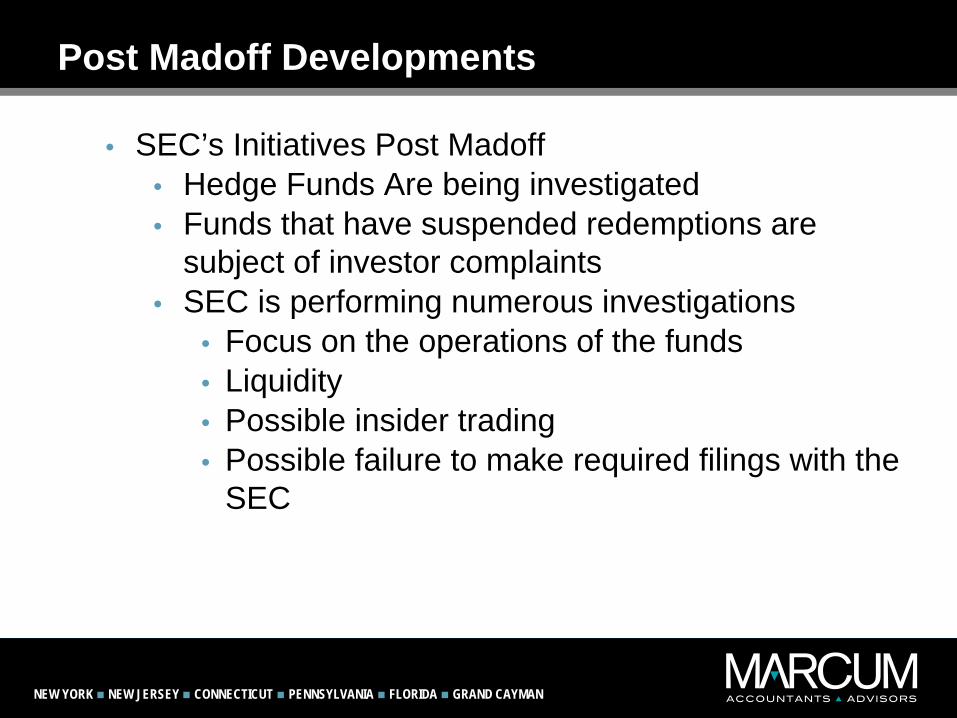

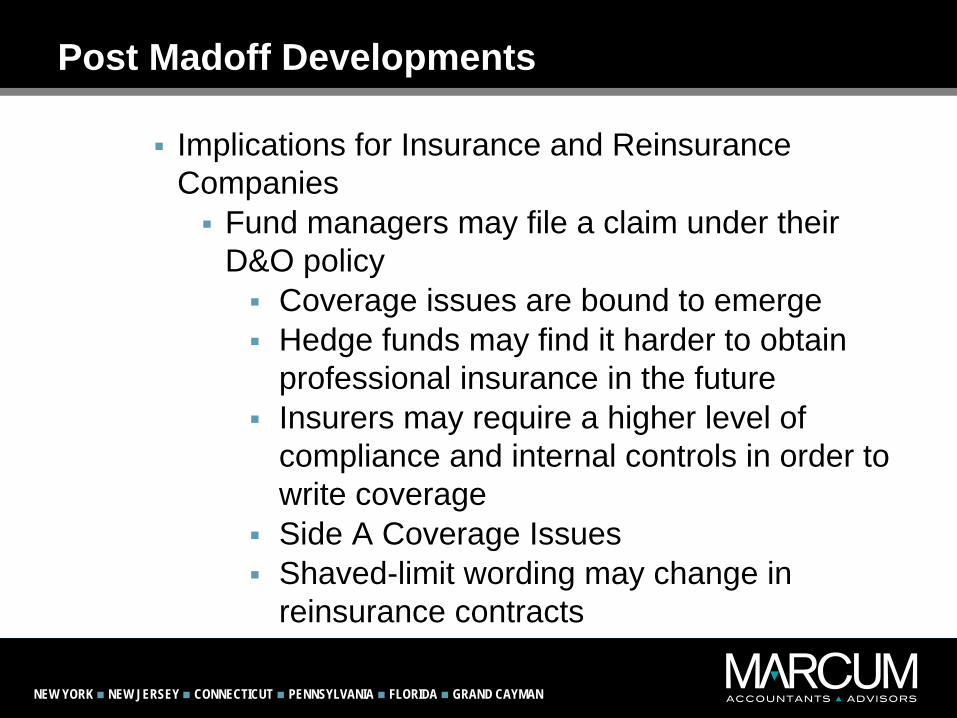

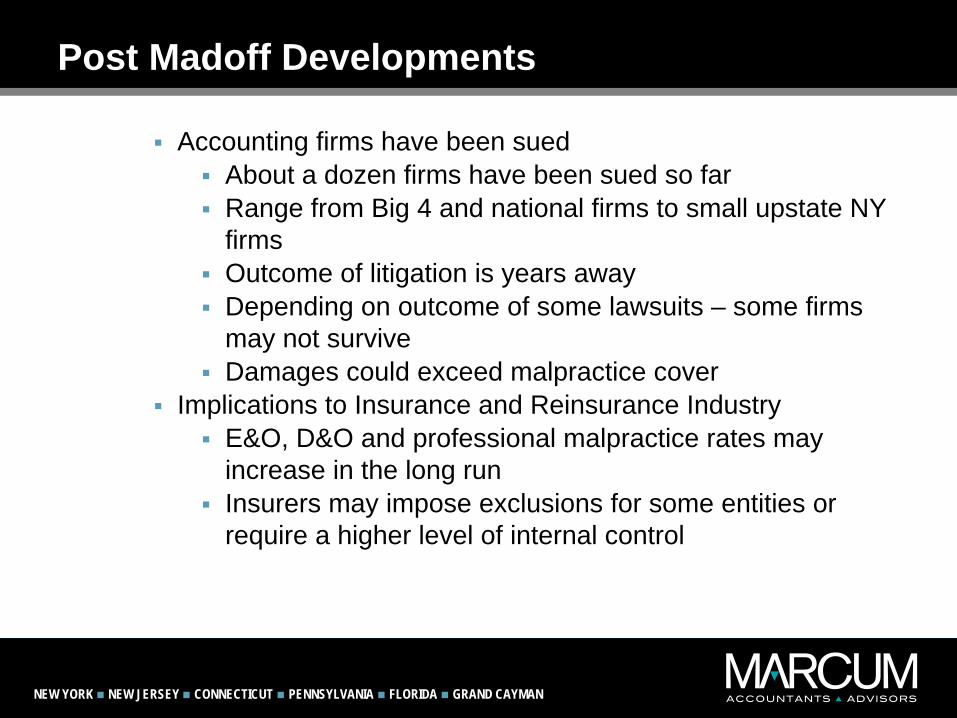

2:00 Global Financial Crisis/Madoff Scandal: Reinsurance Implications •EvolutionoftheU.S.SubprimeLendingCrisisIntoAWorldwideFinancialCrisis•ImpactToDateOnTheReinsuranceIndustry•ClaimTrendsToDate•IncreasedCedingCompanySecurityRequirements•U.S.LegislativeReactions•OutlookForReinsurers Peter Chaffetz, Esq., Chaffetz Lindsey LLP, New York John Green, Partner-in-Charge, Insurance Industry Group, Marcum LLP, Melville, NY

3:00 Afternoon Break

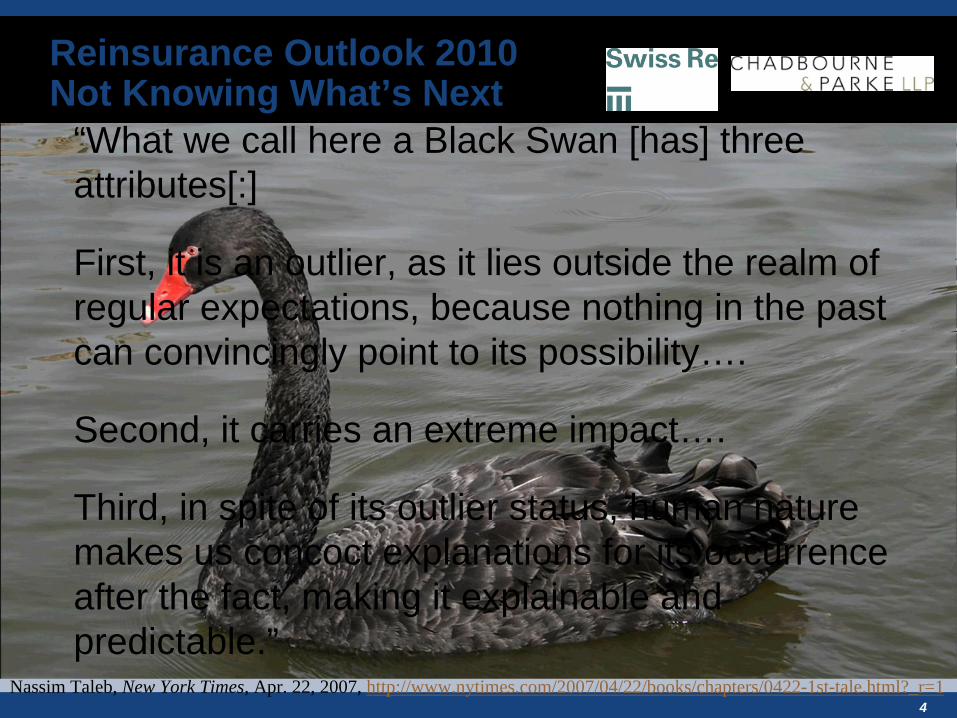

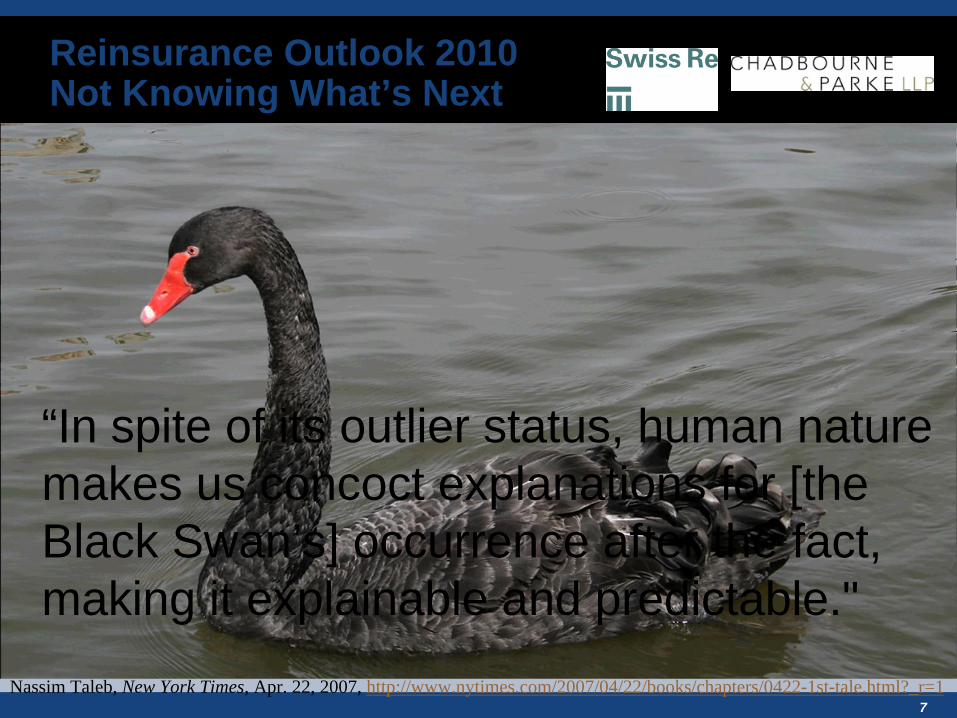

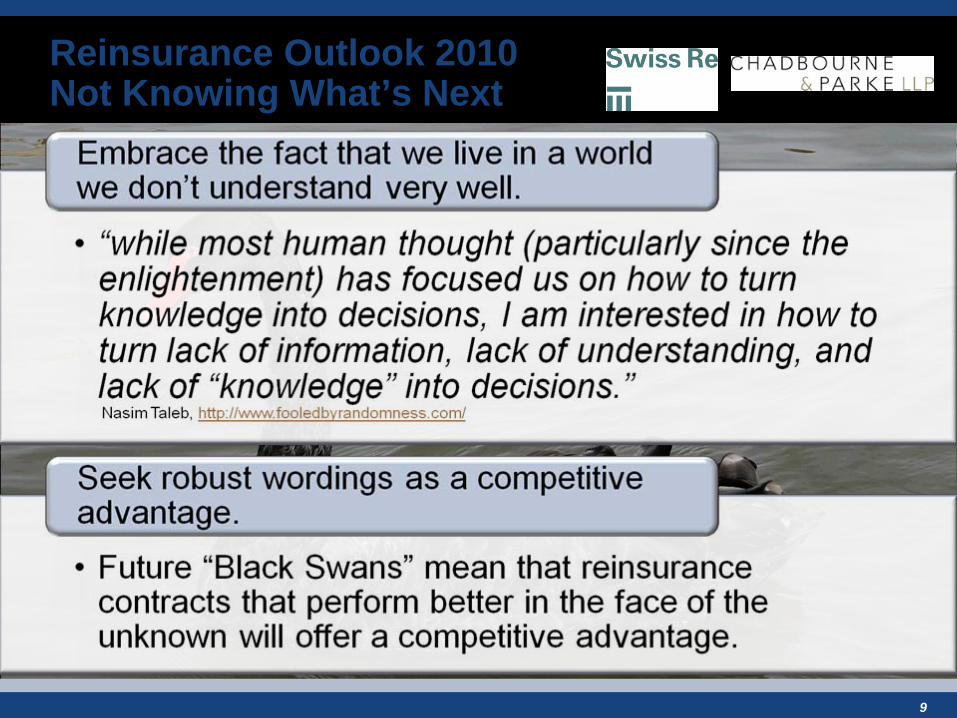

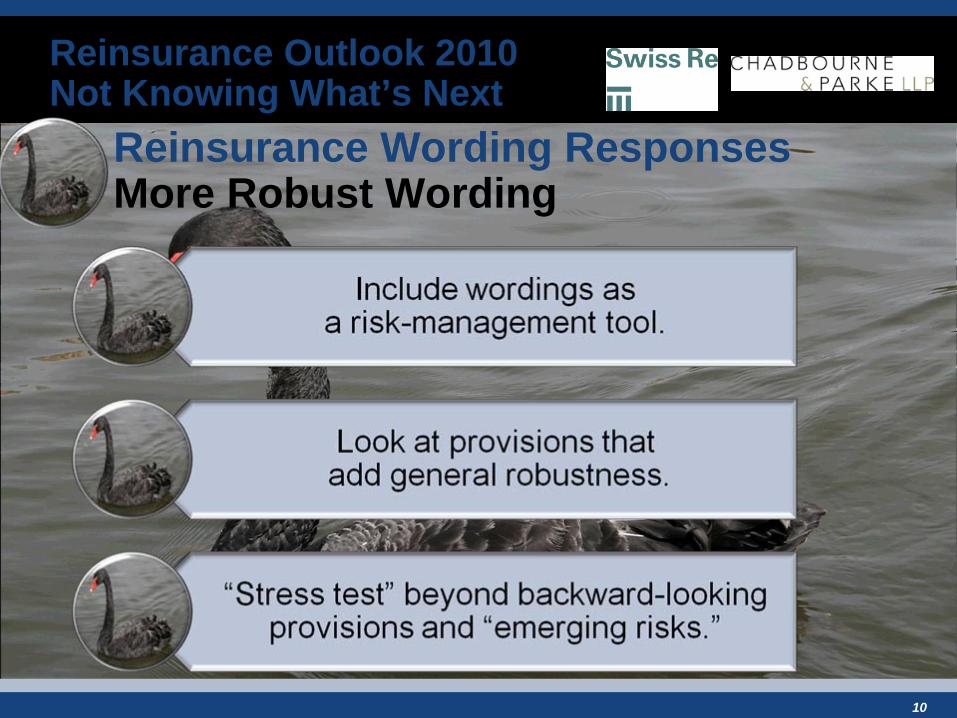

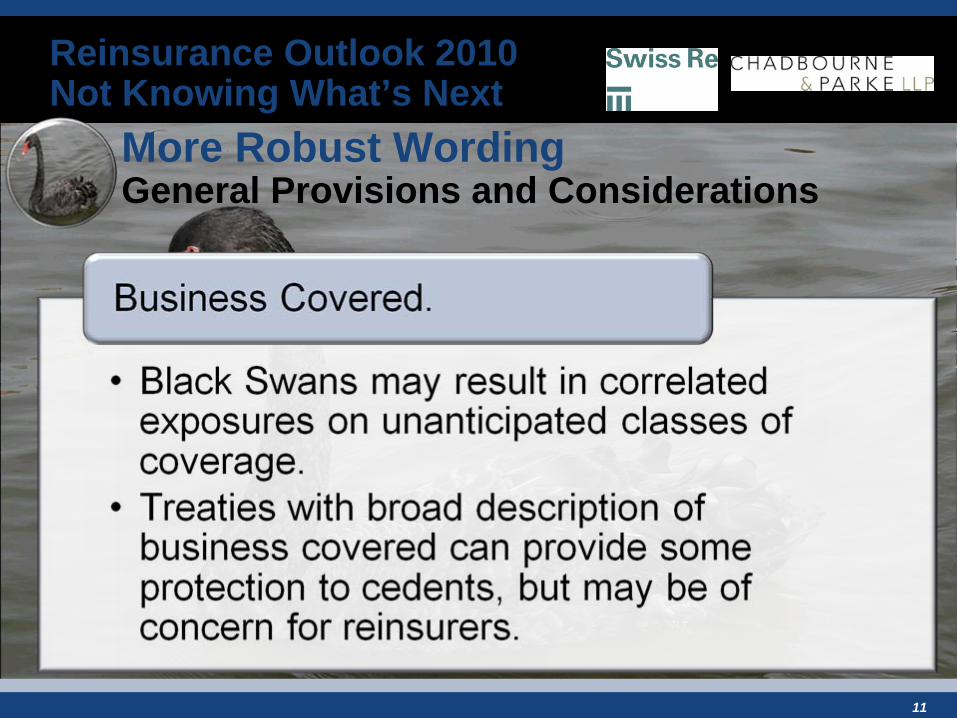

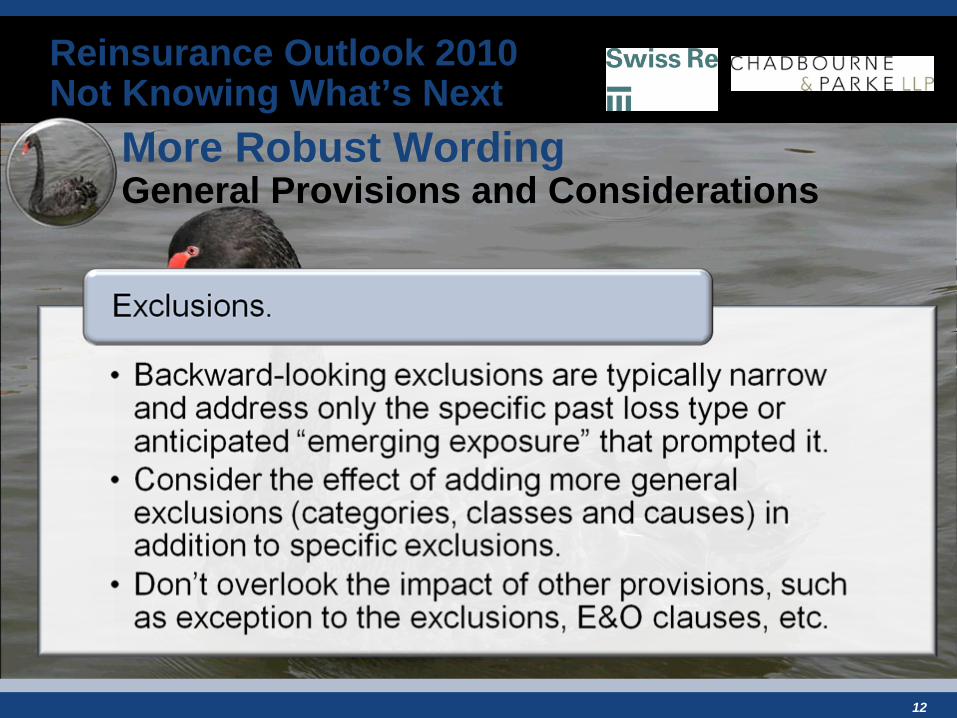

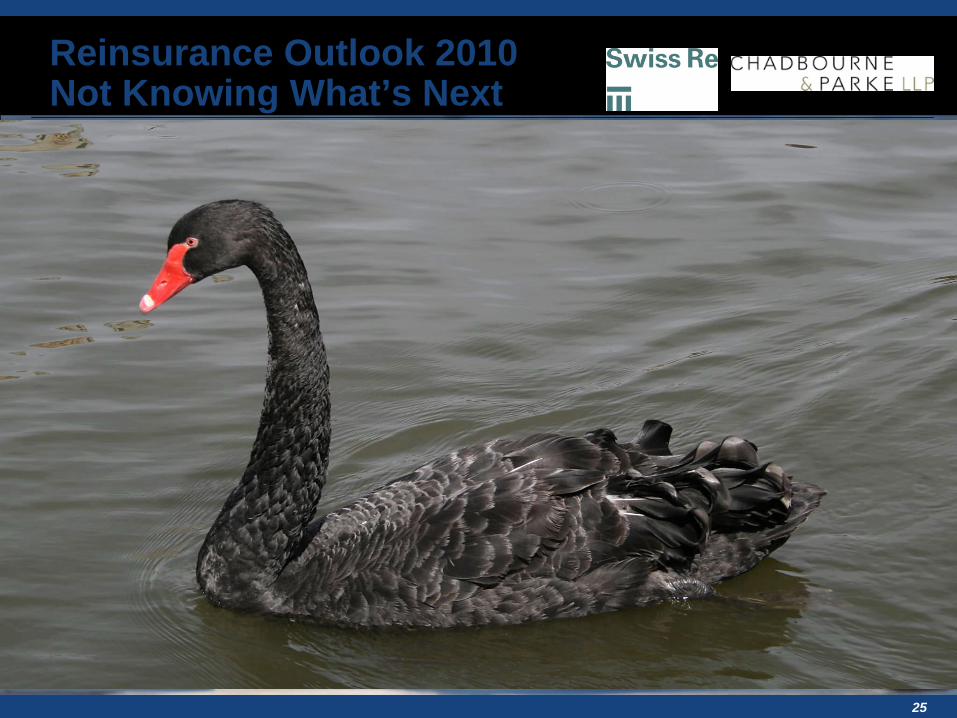

3:15 Not Knowing What’s Next: Are Reinsurance Wordings Ready for the Era of the “Black Swan”? •Are“100yearevents”(socalled“BlackSwans”)occurringmorefrequentlythatanticipated?•Eitherway,doyourcurrentwordingsadequatelyaddressuncertainfutureevents?Carey Child, Esq., Chadbourne & Parke LLP, Washington, DC Reka Koerner, Senior Vice President, Legal, Swiss Reinsurance America Corporation, Armonk, NY

4:00 Resolution Without Arbitration/Decreasing Cost of Arbitration •HandlingResolutionWithRun-offCompanies•ImportanceofSecurity•AvoidingMotionsToVacate•Consolidation•SummaryJudgmentModerator: Scott Birrell, Esq., Vice President and Associate General Counsel, Travelers, Hartford, CT William Goldsmith, Esq., Assistant General Counsel, American International Group Ltd., New York Jonathan Rosen, Arbitration, Mediation and Expert Witness Services, New York William Perry, Esq., Chadbourne & Parke LLP, Washington, DC

5:00 Networking Reception

Dealing with Dealing with Major Recurring IssuesMajor Recurring Issues

Kenneth LevineKenneth Levine Nelson Levine de Luca & Horst, Blue Bell, PANelson Levine de Luca & Horst, Blue Bell, PA

Jessica Jessica PardiPardi Morris Manning & Martin, LLP, Atlanta, GAMorris Manning & Martin, LLP, Atlanta, GA

Benjamin Benjamin GonsonGonson NicolettiNicoletti GonsonGonson Spinner & Owen LLP, New York, NYSpinner & Owen LLP, New York, NY

Follow the Settlements

An Historical Overview and Discussion of Recent

Developments

Jessica F. Pardi, Esq. Morris, Manning & Martin, LLP

1600 Atlanta Financial Center 3343 Peachtree Road, NE Atlanta, GA 30326-1044

(404) 504-7662 [email protected]

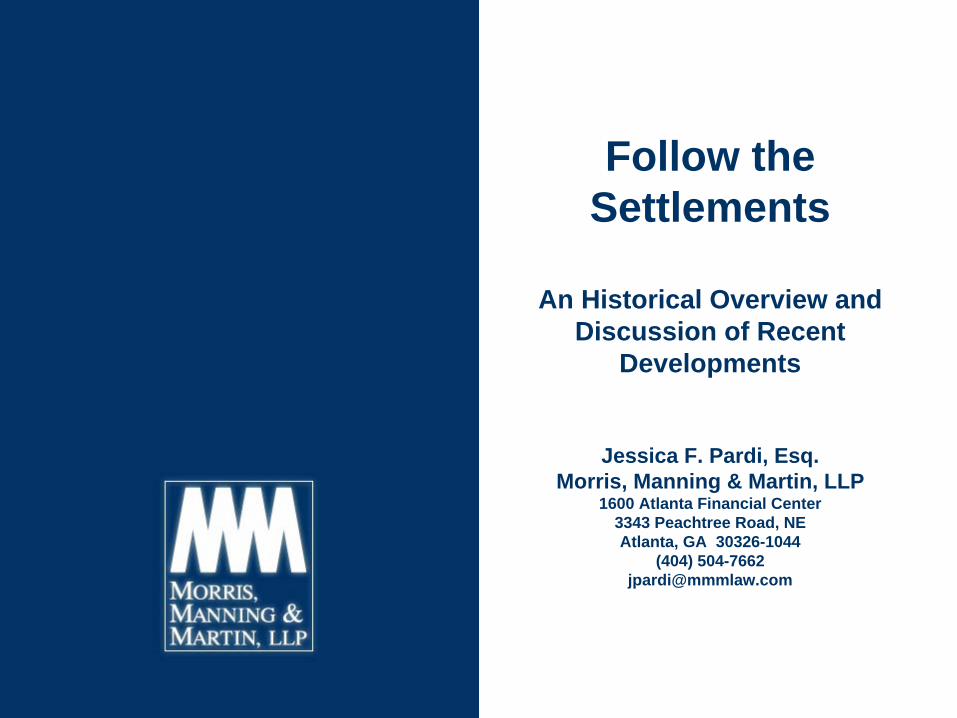

A. Statement of the rule: A contractual obligation by the reinsurer to indemnify the ceding company for claim payments or settlements it makes under its policy provided the payment is not fraudulent, made in bad faith or otherwise ex gratia.

B. “Follow the Settlements” is meant to be narrower in scope than “Follow the Fortunes.”

C. Purpose of Follow the Settlements:

1. To prevent second-guessing by the reinsurer;

2. To avoid litigation of coverage disputes; and

3. To promote good faith settlements.

FOLLOW THE SETTLEMENTS

SAMPLE CLAUSES

“Reinsurer agrees to abide by the loss settlements of the reinsured.”

To this may be added a notice provision mandating the reinsured notify the reinsurer of claims to which the reinsurance applies [or may apply or likely will apply] and an opportunity for the reinsurer to associate in the defense and/or settlement of the claim [typically at the reinsurer’s expense].

The “Honorable Undertaking” clause in an arbitration provision may also contain language regarding follow the settlements:

“The Treaty(ies) shall be construed as an honorable undertaking between the parties hereto not to be defeated by technical legal constructions, it is the intention of the Treaty(ies) that the fortunes of the reinsurer shall follow the fortunes of the reinsured.”

Should Follow the Settlements be implied in reinsurance contracts?

International Surplus Lines Ins. Co. v. Certain Underwriters & Underwriting Syndicates at Lloyd’s of London, 868 F.Supp. 917 (S.D. Ohio 1994) (follow the settlements implied into all reinsurance contracts).

necessary to preserve the cedant-reinsurer relationship

maximize coverage

overruled by American Ins. Co. v. Am Re-Ins. Co., 2006 U.S. Dist. LEXIS 95801 (N.D. Cal. Nov. 27, 2006).

Aetna Cas. & Surety Co. v. Home Ins. Co., 882 F.Supp. 1328, 1348-51 (S.D.N.Y. 1995) (implying follow the settlements into reinsurance contract based upon custom and practice).

Eight years later, the Second Circuit, in British Int’l. Ins. Co. v. Seguros La Republica, S.A., 342 F.3d 78 (2nd Cir. 2003), strictly limited “custom and practice” evidence. This strict standard would not have allowed the evidence in Aetna v. Home.

The majority of courts no longer imply follow the settlements into reinsurance contracts. See e.g. The Am. Ins. Co. v. Am. Re-Ins. Co., 2006 U.S. Dist. LEXIS 95801 (N.D. Cal. Nov. 27, 2006) (tracing the history of implying follow the settlements and refusing to do so); Employer Reins. Corp. v. Laurier Indem. Co., 2007 U.S. Dist. LEXIS 45670 (M.D. Fla. June 25, 2007) (the absence of a follow the settlements clause does not create an ambiguity permitting parole evidence regarding custom and usage).

When can reinsurers avoid following the settlements of the cedant?

1. Fraud

2. Bad faith

a) Includes improper claims handling and “manifest manipulation” of allocations

b) Typically a high standard requiring at least gross negligence or recklessness

3. Ex gratia payments

4. Differing scopes of insurance and reinsurance, i.e., the coverage is not “back to back”

Importance of “governing law” clause

ALLOCATION

“Allocation” refers to the assignment of losses by an insurer to particular policy periods, categories of losses and/or number of occurrences.

The seminal case applying follow the settlements to allocations is Commercial Union Ins. Co. v. Seven Provinces Ins. Co., Ltd., 9 F.Supp. 2d 49 (D. Mass. 1998) aff’d 217 F.3d 33 (1st Cir. 2000) (follow the settlements requires reinsurer to follow the reinsured’s good faith and reasonable allocation of settlement dollars between different policies and sites).

“[The reinsurer] attempts to avoid the effect of the “follow the settlements” doctrine by arguing that what it is challenging is the good faith of the allocation, rather than of the settlement. This is a distinction without a difference. . . .”

ALLOCATION (Cont’d)

Seven Provinces is followed by two cases involving large payments to Owens Corning Fiberglas for asbestos liabilities:

1. North River Ins. Co. v. ACE Am. Reins. Co., 2002 U.S. Dist. LEXIS 5536 (S.D.N.Y. Mar. 29, 2002) aff’d in part, vacated in part, remanded by, 361 F.3d 134 (2nd Cir. 2004) (reinsurers not allowed to second- guess allocations among policies and layers).

2. Travelers Cas. & Sur. Co. v. Gerling Global Reins. Corp. of Am., 285 F.Supp. 2d 200 (D. Conn. 2003), rev’d, 419 F.3d 181 (2nd Cir. 2005) (reinsurer obligated to abide by insurer’s determination of number of occurrences even though number was not determined as part of settlement with insured).

Treatment of Allocations Under Treaty As Opposed to Facultative

Reinsurance

Facultative reinsurance typically is governed by a one or two page, standard form with coverage terms following the underlying policy. Here a cedant’s allocations generally must be followed if they are reasonable and in good faith and the coverage is arguably within the policy.

Treaty reinsurance typically involves a detailed contract with its own coverage terms pertaining to numerous and varied underlying policies. Here, the treaty’s terms generally govern whether the allocation is followed.

Treatment of Allocations Under Treaty As Opposed to Facultative

Reinsurance (Cont’d)FACULTATIVE REINSURANCE

Some courts examining good faith and reasonableness of allocations involving facultative reinsurance have created a high standard for a reinsurer to challenge a cedant’s settlement allocation. National Union Fire Ins. Co. v. Am. Reins. Co., 441 F.Supp. 2d 646 (S.D.N.Y. 2006) (even indifference to proper allocation does not rise to the necessary showing of “extraordinary bad faith”).

Treatment of Allocations Under Treaty As Opposed to Facultative

Reinsurance (Cont’d)

Suter v. Gen. Acc. Ins. Co., 2006 U.S. Dist. LEXIS 51853 (D.N.J. July 17, 2006) vacated by Goldman v. General Acc. Ins. Co., 2007 U.S. Dist. LEXIS 70406 (D.N.J. May 24, 2007) (“Bad faith in this context amounts to a showing of gross negligence, recklessness or a showing that the settlement was not even arguably within the scope of the reinsurance coverage”).

Some rulings have favored reinsurers:

Allstate Ins. Co. v. Am. Home Assurance Co., 837 N.Y.S. 2d 138 (N.Y. App. Div. 2007) (reinsurer not required to follow reinsurance loss allocations that are unreasonable). The Court held as follows:

Treatment of Allocations Under Treaty As Opposed to Facultative

Reinsurance (Cont’d)[North River and Travelers] do not require a reinsurer, under the follow-the- fortunes doctrine, to accept the reinsured’s post-settlement loss allocation even if that allocation is contrary to the reinsured’s pre-allocation position and treatment of the loss allocation issue with its own insured, i.e., its treatment of deductibles. While the cases unequivocally hold that the doctrine extends to a post-settlement allocation despite ‘an inconsistency between that allocation and the [reinsured’s] pre-settlement assessments of risk,’ it applies only ‘as long as the allocation meets the typical follow-the- settlements requirements, i.e., is in good faith, reasonable, and within the applicable policies.’ Here, unlike North River, the inconsistency is not between defendant’s post-settlement allocation and its pre-settlement assessments of the risk, but between its pre-settlement allocation of loss with its insured (UTC) and its post-settlement allocation with its reinsurer.

Treatment of Allocations Under Treaty As Opposed to Facultative

Reinsurance (Cont’d)TREATY REINSURANCE

Follow the Settlements as applied to allocations under treaty insurance typically relies on analysis of the terms of the treaty.

In Travelers v. Lloyds, the Supreme Court of New York held as follows:

“While a follow the fortunes clause in most reinsurance agreements leaves reinsurers little room to dispute the reinsured’s conduct of the case, we agree with the rationale of the . . . Second Circuit that such a clause does not alter the terms or override the language of reinsurance policies.”

“To hold that these ‘follow the fortunes’ clauses supplant the definition of ‘disaster and/or casualty’ in the reinsurance treaties and allow Travelers to recover under its single allocation theory would effectively negate the phrase. The practical result of such an application would be that a reinsurance contract interpreted under New York law that contains a ‘follow the fortunes’ clause would bind a reinsurer to indemnify a reinsured whenever it paid a claim, regardless of the contractual language defining loss.” Travelers Cas. & Sur. Co. v. Lloyd’s, 760 N.E.2d 319 (N.Y. 2001); see also Hartford Acc. & Indem. Co. v. ACE, 2005 Conn. Super. LEXIS 3576 (Dec. 14, 2005).

RECENT DEVELOPMENTS

An insurer cannot use a declaratory judgment action to test the application of Follow the Settlements prior to paying a claim. The Tall Tree Ins. Co. v. Munich Reins. Am., Inc., 2008 U.S. Dist. LEXIS 60499 (N.D. Cal. July 29, 2008).

Commutations and contingent liabilities allocated to reinsurer based upon actuarial studies are losses covered under the reinsurance treaties. Global Reins. Corp. of Am. v. Argonaut Ins. Co., 2009 U.S. Dist. LEXIS 37460 (S.D.N.Y. March 23, 2009).

“Follow the fortunes” applies only to reinsurance contracts. Idaho Counties Risk Mgmt Program Underwriters v. Northland Ins. Cos., 205 P.3d 1220 (Idaho 2009).

RECENT DEVELOPMENTS (Cont’d)

Differences in governing law between and among insurance and reinsurance contracts may result in paid claims for which there is no reinsurance despite a follow the settlements clause. Wasa v. Lexington [2009] UKL 40 (July 30, 2009).

Follow the fortunes cannot be used to expand reinsurance coverage to renewals. Arrowood Surplus Lines Ins. Co. v. Westport Ins. Corp., Slip Copy, 2010 U.S. Dist. LEXIS 426 (D.Ct., January 6, 2010).

LATE NOTICELATE NOTICE

Benjamin Benjamin GonsonGonson NicolettiNicoletti GonsonGonson Spinner Owen LLP, New York, NYSpinner Owen LLP, New York, NY

THE PROMPT NOTICE REQUIREMENTTHE PROMPT NOTICE REQUIREMENT

-- IN ALL FACULATIVE CERTIFICATESIN ALL FACULATIVE CERTIFICATES

-- IN MOST EXCESS OF LOSS TREATIESIN MOST EXCESS OF LOSS TREATIES

-- PERMITS REINSURERS TO RESERVE PERMITS REINSURERS TO RESERVE PROPERLY; TO ADJUST PREMIUMS AND TO PROPERLY; TO ADJUST PREMIUMS AND TO DECIDE WHETHER TO ASSOCIATE IN DECIDE WHETHER TO ASSOCIATE IN HANDLING OF CLAIMHANDLING OF CLAIM

WHEN IS NOTICE LATE ?WHEN IS NOTICE LATE ?

-- PROMPT NOTICE TYPICALLY REQUIRED PROMPT NOTICE TYPICALLY REQUIRED WHEN CLAIM APPEARS LIKELY TO INVOLVE WHEN CLAIM APPEARS LIKELY TO INVOLVE THE REINSURANCE OR WHEN RESERVES SET THE REINSURANCE OR WHEN RESERVES SET BY CEDENT REACH 50% OF RETENTIONBY CEDENT REACH 50% OF RETENTION

-- WHEN IS CLAIM LIKELY TO INVOLVE THE WHEN IS CLAIM LIKELY TO INVOLVE THE REINSURANCE REINSURANCE –– OBJECTIVE VS. SUBJECTIVE OBJECTIVE VS. SUBJECTIVE TESTTEST

-- PROMPT NOTICE SOMETIMES REQUIRED PROMPT NOTICE SOMETIMES REQUIRED FOR SPECIFIC TYPES OF INJURIESFOR SPECIFIC TYPES OF INJURIES

PREJUDICE REQUIREMENTPREJUDICE REQUIREMENT

-- UNDER NEW YORK LAW, REINSURER UNDER NEW YORK LAW, REINSURER REQUIRED TO SHOW REQUIRED TO SHOW ““TANGIBLE ECONOMIC TANGIBLE ECONOMIC INJURYINJURY”” TO PREVAIL ON LATE NOTICE TO PREVAIL ON LATE NOTICE GROUNDSGROUNDS

-- PREJUDICE IS REQUIRED IN ALMOST EVERY PREJUDICE IS REQUIRED IN ALMOST EVERY STATE THAT HAS ADDRESSED SUBJECTSTATE THAT HAS ADDRESSED SUBJECT

-- PREJUDICE NOT REQUIRED IF NOTICE IS A PREJUDICE NOT REQUIRED IF NOTICE IS A CONDITION PRECEDENT CONDITION PRECEDENT -- MUST BE CLEARLY MUST BE CLEARLY STATED IN CERTIFICATE / TREATYSTATED IN CERTIFICATE / TREATY

WHAT IS PREJUDICE?WHAT IS PREJUDICE?

-- ECONOMIC INJURY DUE TO LOW ECONOMIC INJURY DUE TO LOW COMMUTATIONS WITH RETROCESSIONAIRESCOMMUTATIONS WITH RETROCESSIONAIRES

-- TAX RAMFICATIONSTAX RAMFICATIONS

-- IMPACT OF LATE NOTICE ON SUBSEQUENT IMPACT OF LATE NOTICE ON SUBSEQUENT RENEWALS RENEWALS

-- ARBITRATION VS. LITIGATION ARBITRATION VS. LITIGATION –– EQUITY AND EQUITY AND CUSTOM & PRACTICE (DAMAGES)CUSTOM & PRACTICE (DAMAGES)

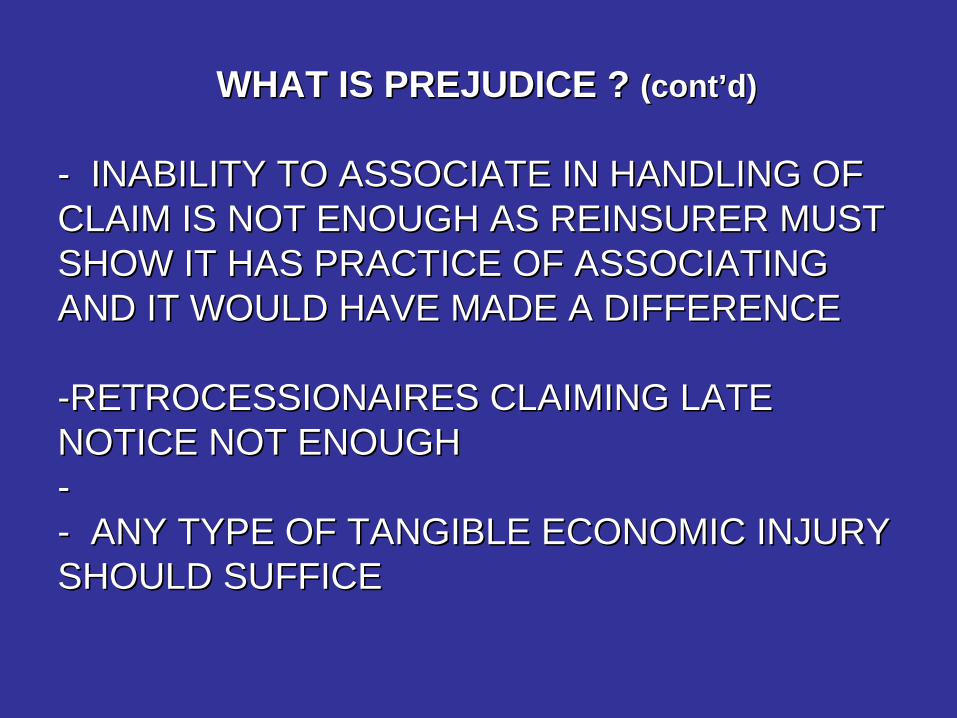

WHAT IS PREJUDICE ? WHAT IS PREJUDICE ? (cont(cont’’d)d)

-- INABILITY TO ASSOCIATE IN HANDLING OF INABILITY TO ASSOCIATE IN HANDLING OF CLAIM IS NOT ENOUGH AS REINSURER MUST CLAIM IS NOT ENOUGH AS REINSURER MUST SHOW IT HAS PRACTICE OF ASSOCIATING SHOW IT HAS PRACTICE OF ASSOCIATING AND IT WOULD HAVE MADE A DIFFERENCEAND IT WOULD HAVE MADE A DIFFERENCE

--RETROCESSIONAIRES CLAIMING LATE RETROCESSIONAIRES CLAIMING LATE NOTICE NOT ENOUGHNOTICE NOT ENOUGH---- ANY TYPE OF TANGIBLE ECONOMIC INJURY ANY TYPE OF TANGIBLE ECONOMIC INJURY SHOULD SUFFICESHOULD SUFFICE

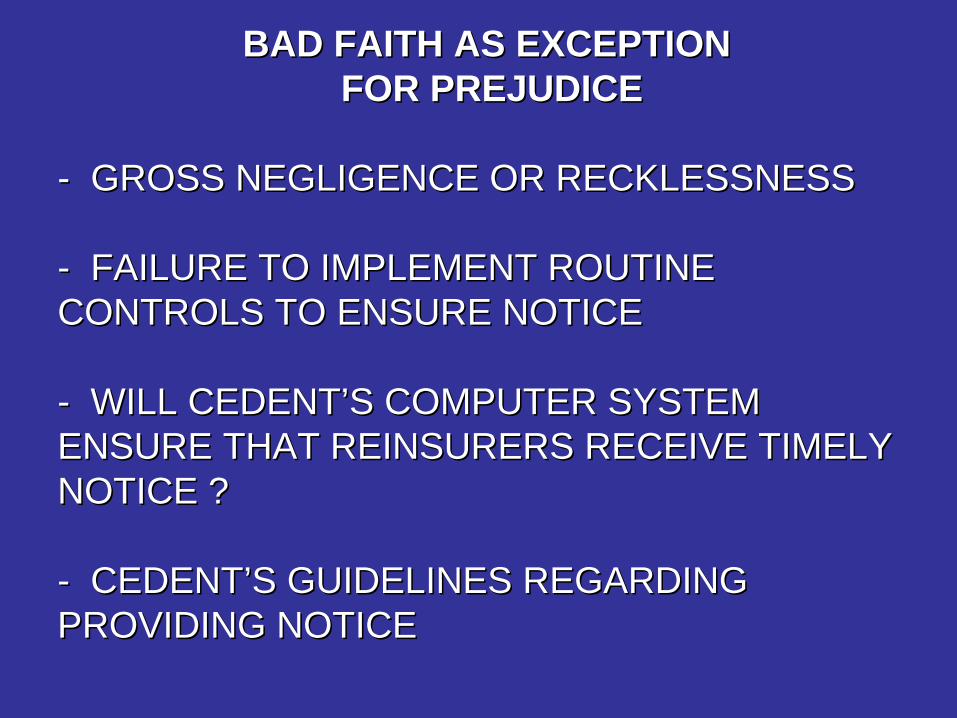

BAD FAITH AS EXCEPTIONBAD FAITH AS EXCEPTIONFOR PREJUDICEFOR PREJUDICE

-- GROSS NEGLIGENCE OR RECKLESSNESSGROSS NEGLIGENCE OR RECKLESSNESS

-- FAILURE TO IMPLEMENT ROUTINE FAILURE TO IMPLEMENT ROUTINE CONTROLS TO ENSURE NOTICECONTROLS TO ENSURE NOTICE

-- WILL CEDENTWILL CEDENT’’S COMPUTER SYSTEM S COMPUTER SYSTEM ENSURE THAT REINSURERS RECEIVE TIMELY ENSURE THAT REINSURERS RECEIVE TIMELY NOTICE ?NOTICE ?

-- CEDENTCEDENT’’S GUIDELINES REGARDING S GUIDELINES REGARDING PROVIDING NOTICE PROVIDING NOTICE

RESCISSIONRESCISSION

Benjamin Benjamin GonsonGonson NicolettiNicoletti GonsonGonson Spinner & Owen, New York, NYSpinner & Owen, New York, NY

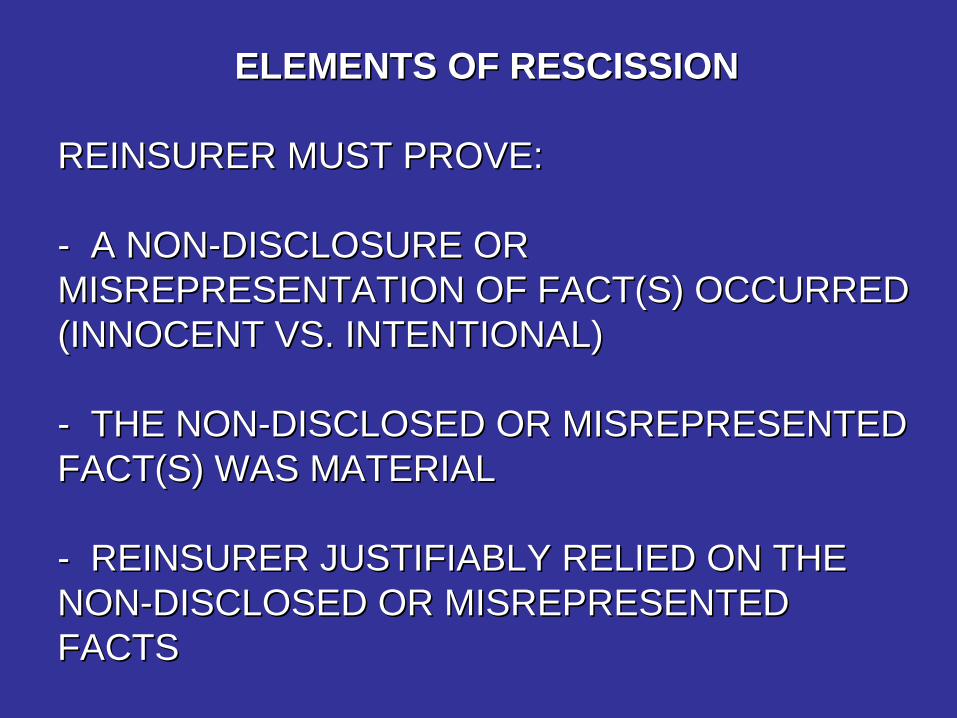

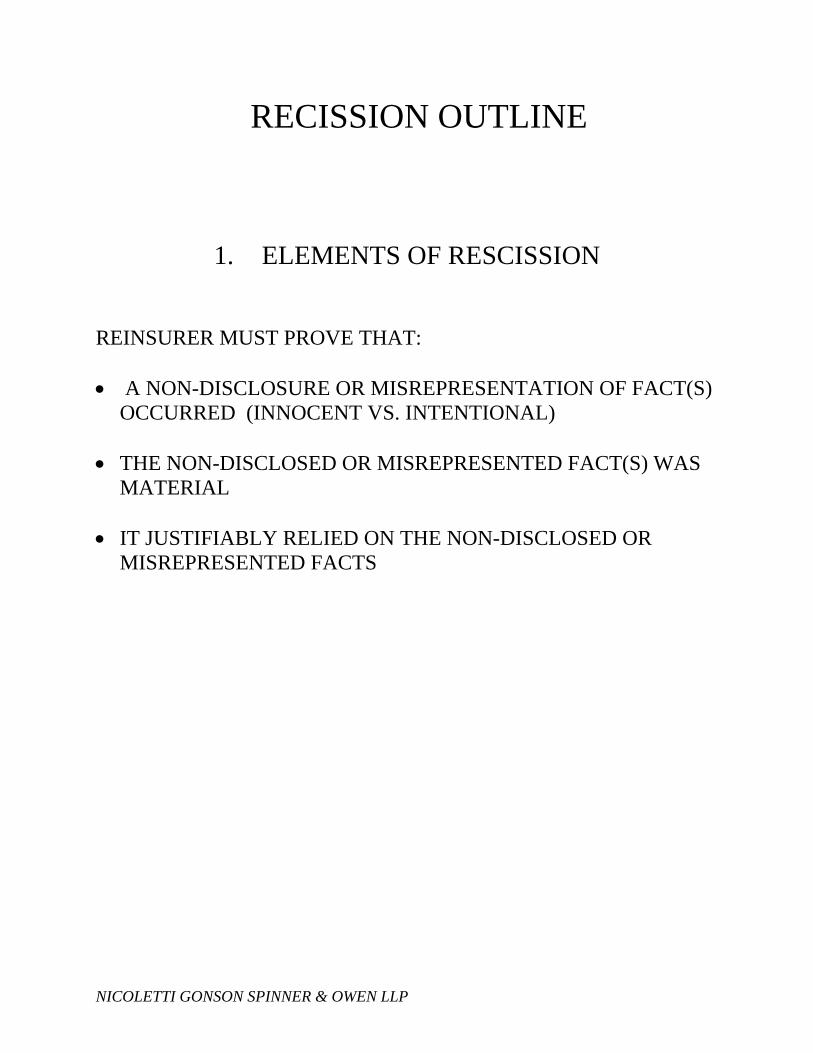

ELEMENTS OF RESCISSION ELEMENTS OF RESCISSION

REINSURER MUST PROVE:REINSURER MUST PROVE:

-- A NONA NON--DISCLOSURE OR DISCLOSURE OR MISREPRESENTATION OF FACT(S) OCCURRED MISREPRESENTATION OF FACT(S) OCCURRED (INNOCENT VS. INTENTIONAL)(INNOCENT VS. INTENTIONAL)

-- THE NONTHE NON--DISCLOSED OR MISREPRESENTED DISCLOSED OR MISREPRESENTED FACT(S) WAS MATERIALFACT(S) WAS MATERIAL

-- REINSURER JUSTIFIABLY RELIED ON THE REINSURER JUSTIFIABLY RELIED ON THE NONNON--DISCLOSED OR MISREPRESENTED DISCLOSED OR MISREPRESENTED FACTS FACTS

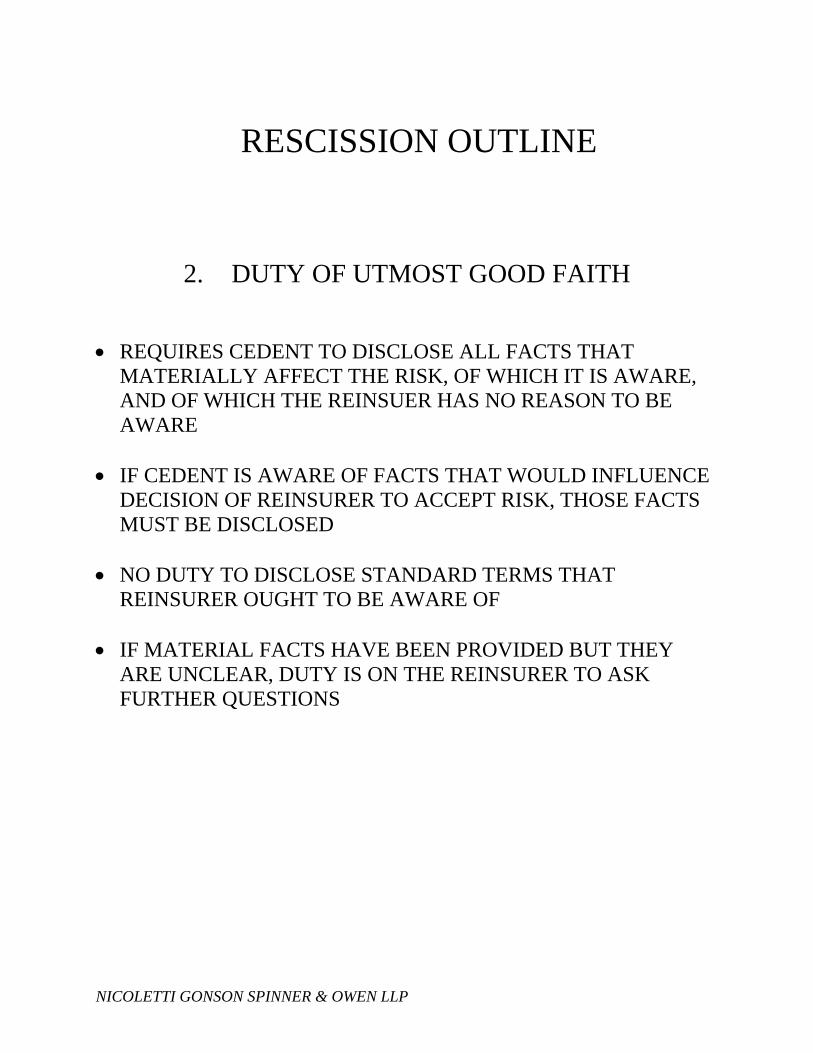

DUTY OF UTMOST GOOD FAITHDUTY OF UTMOST GOOD FAITH

-- REQUIRES CEDENT TO DISCLOSE ALL REQUIRES CEDENT TO DISCLOSE ALL FACTS OF WHICH IT IS AWARE THAT FACTS OF WHICH IT IS AWARE THAT MATERIALLY AFFECT THE RISK, AND OF MATERIALLY AFFECT THE RISK, AND OF WHICH THE REINSURER HAS NO REASON TO WHICH THE REINSURER HAS NO REASON TO BE AWARE BE AWARE

-- IF CEDENT IS AWARE OF FACTS THAT IF CEDENT IS AWARE OF FACTS THAT WOULD INFLUENCE DECISION OF REINSURER WOULD INFLUENCE DECISION OF REINSURER TO ACCEPT RISK, THOSE FACTS MUST BE TO ACCEPT RISK, THOSE FACTS MUST BE DISCLOSED DISCLOSED

DUTY OF UTMOST GOOD FAITH (contDUTY OF UTMOST GOOD FAITH (cont’’d):d):

-- NO DUTY TO DISCLOSE STANDARD TERMS NO DUTY TO DISCLOSE STANDARD TERMS THAT REINSURER OUGHT TO BE AWARE OFTHAT REINSURER OUGHT TO BE AWARE OF

-- IF MATERIAL FACTS HAVE BEEN PROVIDED IF MATERIAL FACTS HAVE BEEN PROVIDED BUT THEY ARE UNCLEAR, DUTY IS ON THE BUT THEY ARE UNCLEAR, DUTY IS ON THE REINSURER TO ASK FURTHER QUESTIONSREINSURER TO ASK FURTHER QUESTIONS

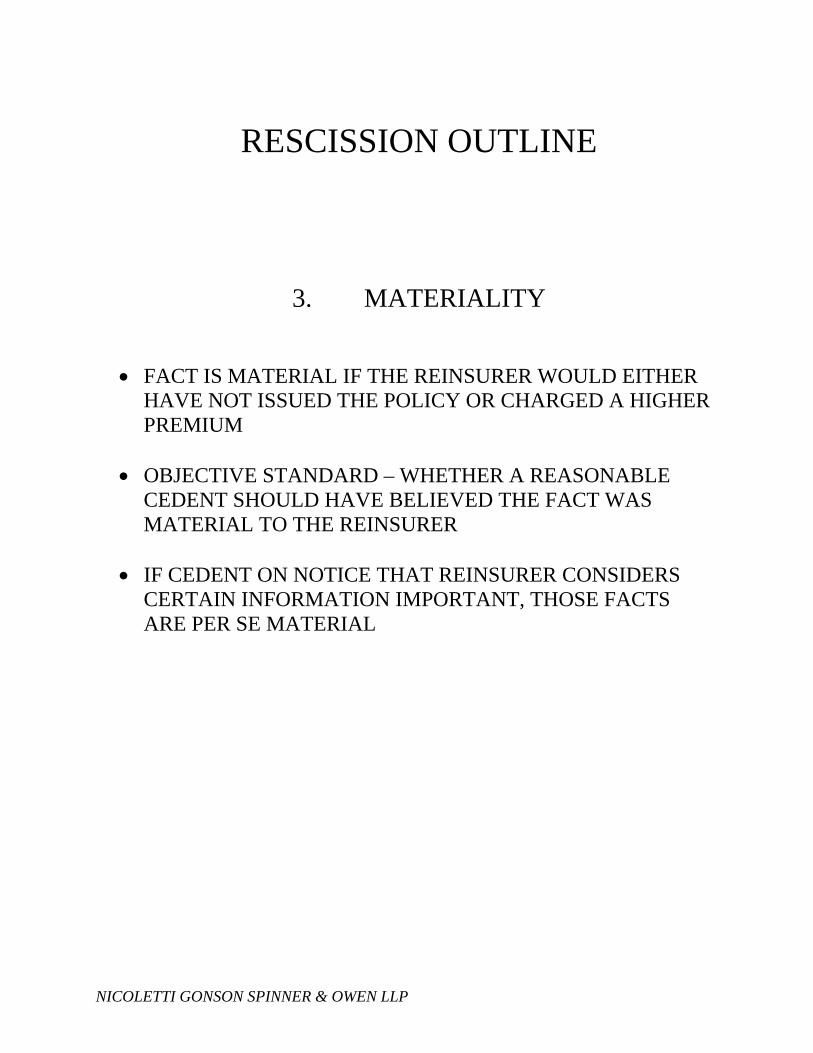

MATERIALITY MATERIALITY

-- MATERIAL IF REINSURER WOULD NOT HAVE MATERIAL IF REINSURER WOULD NOT HAVE ISSUED POLICY OR PAID HIGHER PREMIUM ISSUED POLICY OR PAID HIGHER PREMIUM

-- OBJECTIVE STANDARD OBJECTIVE STANDARD –– WHETHER WHETHER REASONABLE CEDENT SHOULD HAVE REASONABLE CEDENT SHOULD HAVE BELIEVED FACT WAS MATERIAL TO BELIEVED FACT WAS MATERIAL TO REINSURER REINSURER

-- IF CEDENT ON NOTICE THAT REINSURER IF CEDENT ON NOTICE THAT REINSURER CONSIDERS CERTAIN INFO IMPORTANT, CONSIDERS CERTAIN INFO IMPORTANT, THOSE FACTS ARE PER SE MATERIALTHOSE FACTS ARE PER SE MATERIAL

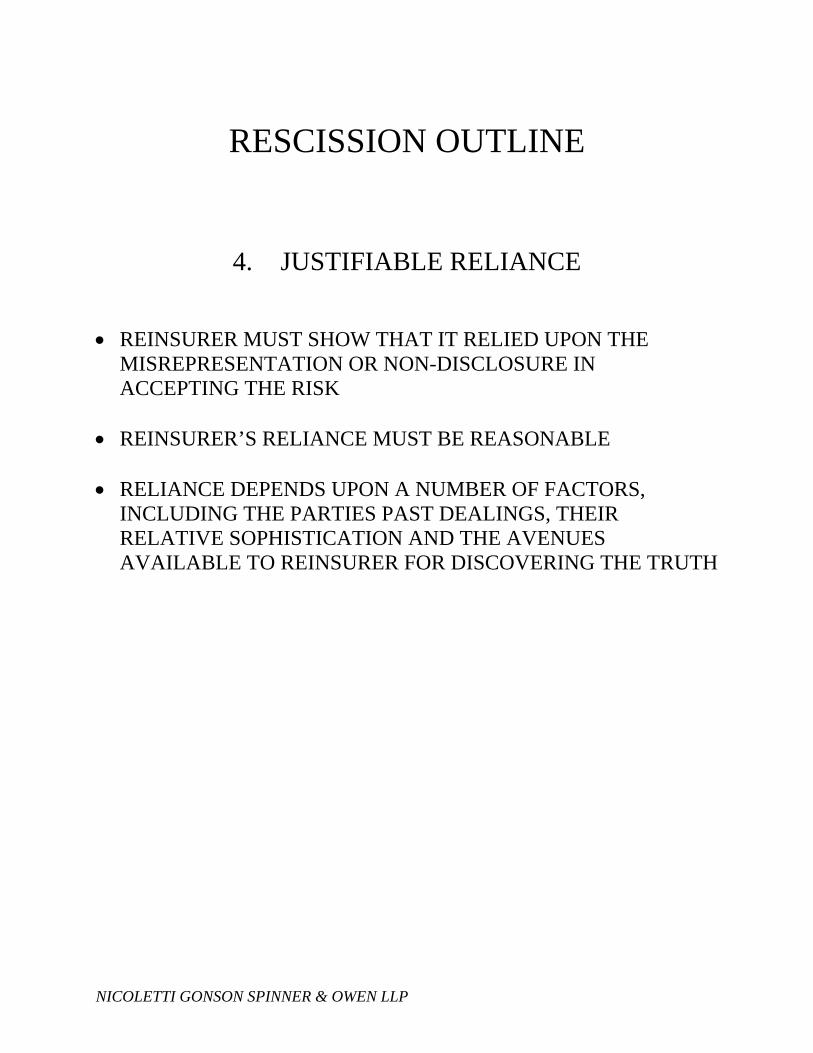

JUSTIFIABLE RELIANCE JUSTIFIABLE RELIANCE

-- REINSURER MUST SHOW IT RELIED UPON REINSURER MUST SHOW IT RELIED UPON MISREPRESENTATION OR NONMISREPRESENTATION OR NON--DISCLOSURE DISCLOSURE IN ACCEPTING RISKIN ACCEPTING RISK

-- REINSURERREINSURER’’S RELIANCE MUST BE S RELIANCE MUST BE REASONABLEREASONABLE

-- RELIANCE DEPENDS UPON NUMBER OF RELIANCE DEPENDS UPON NUMBER OF FACTORS, INCLUDING: PARTIESFACTORS, INCLUDING: PARTIES’’ PAST PAST DEALINGS, RELATIVE SOPHISTICATION AND DEALINGS, RELATIVE SOPHISTICATION AND AVENUES AVAILABLE TO REINSURER FOR AVENUES AVAILABLE TO REINSURER FOR DISCOVERING TRUTH.DISCOVERING TRUTH.

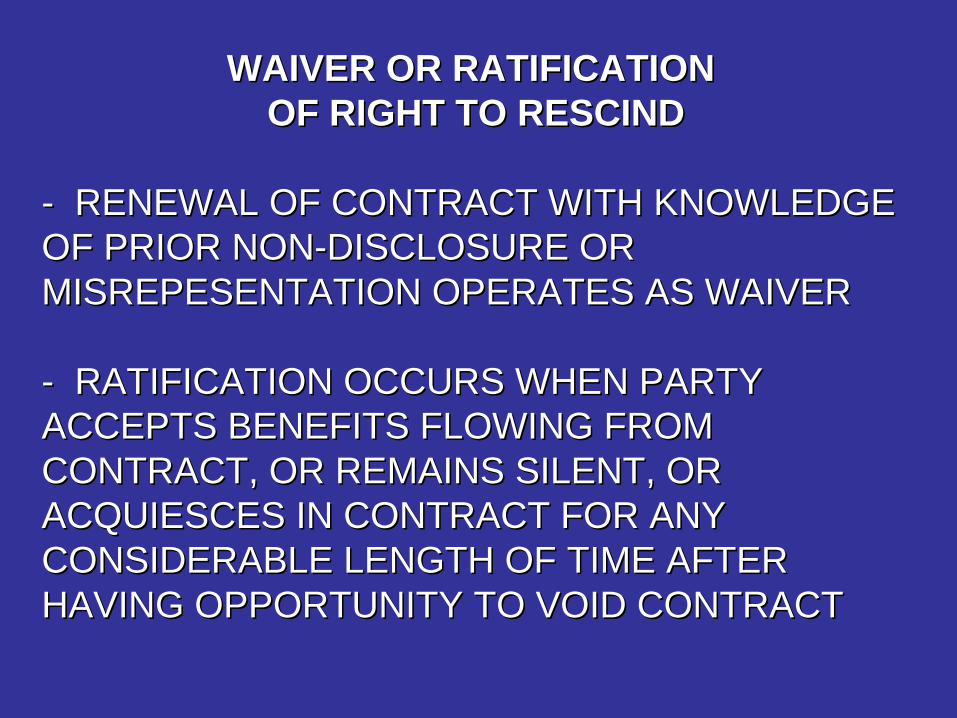

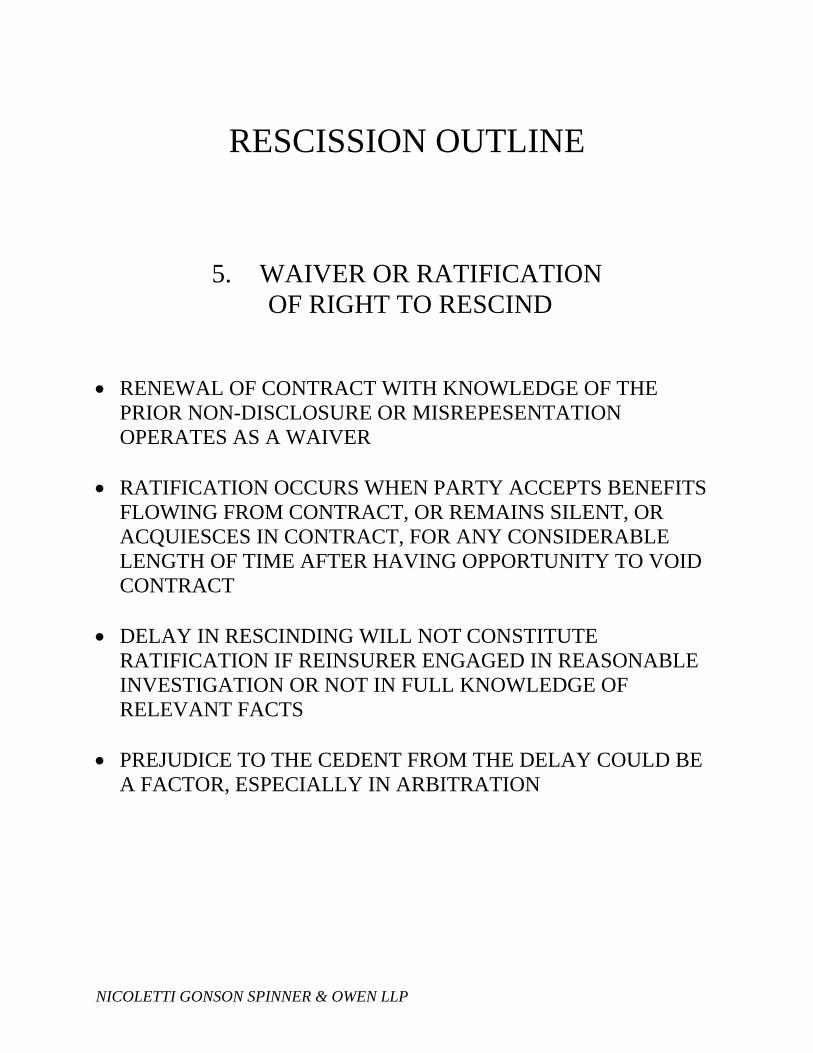

WAIVER OR RATIFICATIONWAIVER OR RATIFICATIONOF RIGHT TO RESCIND OF RIGHT TO RESCIND

-- RENEWAL OF CONTRACT WITH KNOWLEDGE RENEWAL OF CONTRACT WITH KNOWLEDGE OF PRIOR NONOF PRIOR NON--DISCLOSURE OR DISCLOSURE OR MISREPESENTATION OPERATES AS WAIVERMISREPESENTATION OPERATES AS WAIVER

-- RATIFICATION OCCURS WHEN PARTY RATIFICATION OCCURS WHEN PARTY ACCEPTS BENEFITS FLOWING FROM ACCEPTS BENEFITS FLOWING FROM CONTRACT, OR REMAINS SILENT, OR CONTRACT, OR REMAINS SILENT, OR ACQUIESCES IN CONTRACT FOR ANY ACQUIESCES IN CONTRACT FOR ANY CONSIDERABLE LENGTH OF TIME AFTER CONSIDERABLE LENGTH OF TIME AFTER HAVING OPPORTUNITY TO VOID CONTRACTHAVING OPPORTUNITY TO VOID CONTRACT

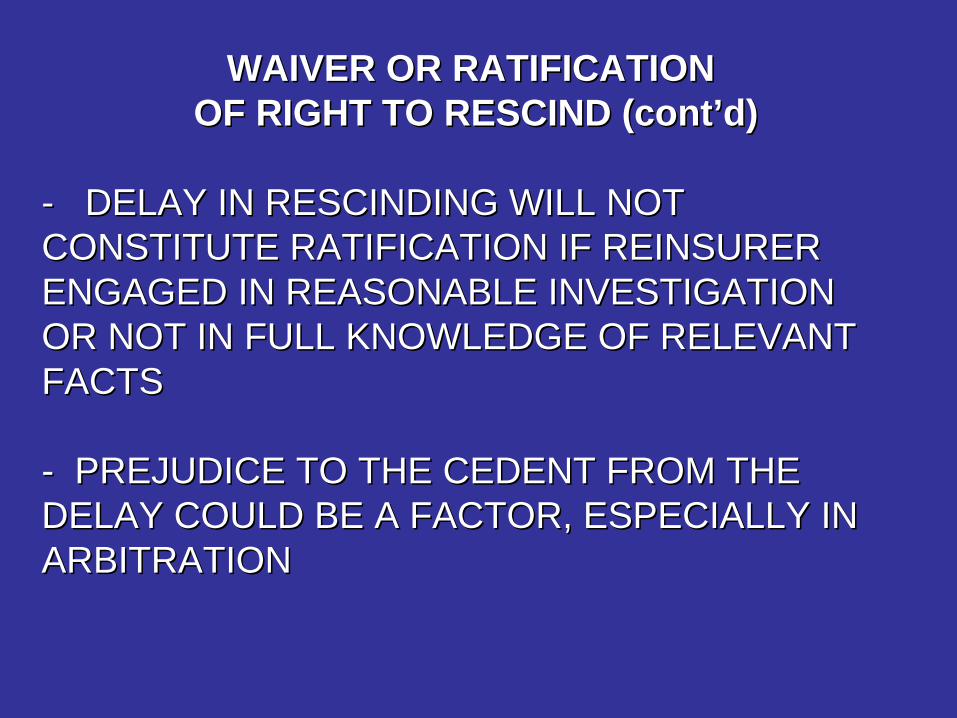

WAIVER OR RATIFICATIONWAIVER OR RATIFICATIONOF RIGHT TO RESCIND (contOF RIGHT TO RESCIND (cont’’d) d)

-- DELAY IN RESCINDING WILL NOT DELAY IN RESCINDING WILL NOT CONSTITUTE RATIFICATION IF REINSURER CONSTITUTE RATIFICATION IF REINSURER ENGAGED IN REASONABLE INVESTIGATION ENGAGED IN REASONABLE INVESTIGATION OR NOT IN FULL KNOWLEDGE OF RELEVANT OR NOT IN FULL KNOWLEDGE OF RELEVANT FACTSFACTS

-- PREJUDICE TO THE CEDENT FROM THE PREJUDICE TO THE CEDENT FROM THE DELAY COULD BE A FACTOR, ESPECIALLY IN DELAY COULD BE A FACTOR, ESPECIALLY IN ARBITRATIONARBITRATION

Dealing with Dealing with Major Recurring IssuesMajor Recurring Issues

Kenneth LevineKenneth Levine Nelson Levine de Luca & Horst, Blue Bell, PANelson Levine de Luca & Horst, Blue Bell, PA

Jessica Jessica PardiPardi Morris Manning & Martin, LLP, Atlanta, GAMorris Manning & Martin, LLP, Atlanta, GA

Benjamin Benjamin GonsonGonson NicolettiNicoletti GonsonGonson Spinner Owen LLP, New York, NYSpinner Owen LLP, New York, NY

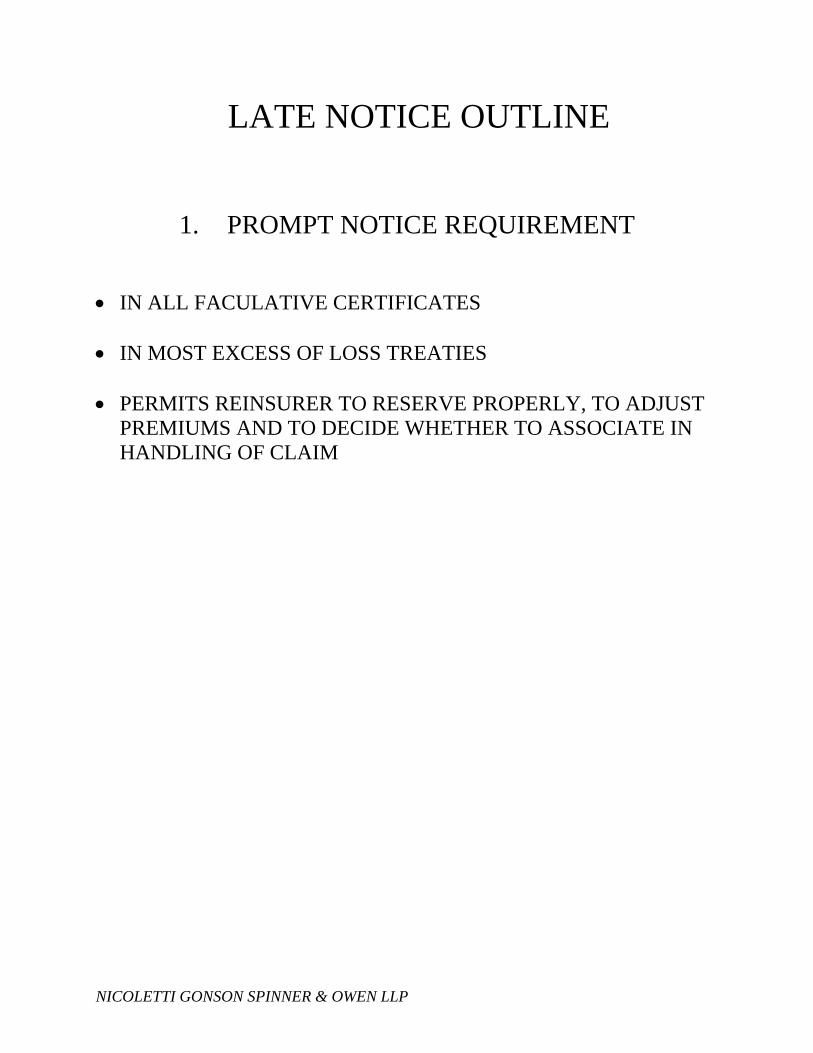

LATE NOTICE OUTLINE

1. PROMPT NOTICE REQUIREMENT

IN ALL FACULATIVE CERTIFICATES IN MOST EXCESS OF LOSS TREATIES PERMITS REINSURER TO RESERVE PROPERLY, TO ADJUST

PREMIUMS AND TO DECIDE WHETHER TO ASSOCIATE IN HANDLING OF CLAIM

NICOLETTI GONSON SPINNER & OWEN LLP

LATE NOTICE OUTLINE

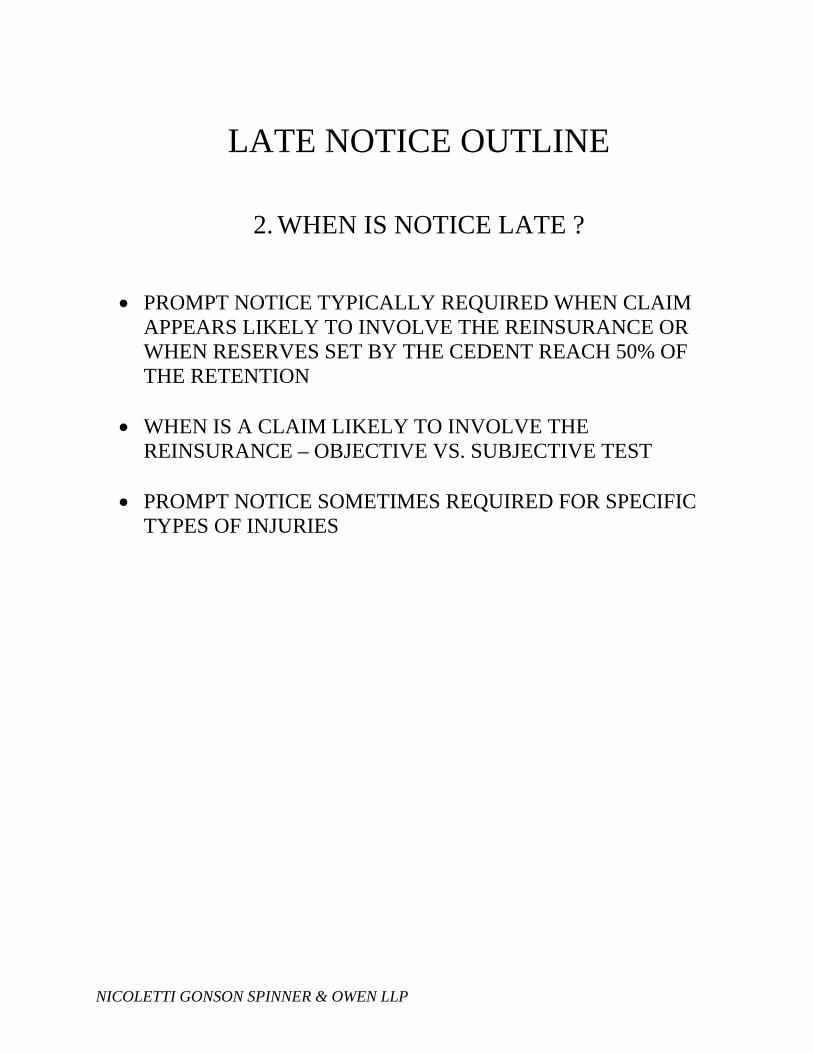

2. WHEN IS NOTICE LATE ?

PROMPT NOTICE TYPICALLY REQUIRED WHEN CLAIM

APPEARS LIKELY TO INVOLVE THE REINSURANCE OR WHEN RESERVES SET BY THE CEDENT REACH 50% OF THE RETENTION

WHEN IS A CLAIM LIKELY TO INVOLVE THE

REINSURANCE – OBJECTIVE VS. SUBJECTIVE TEST

PROMPT NOTICE SOMETIMES REQUIRED FOR SPECIFIC TYPES OF INJURIES

NICOLETTI GONSON SPINNER & OWEN LLP

LATE NOTICE OUTLINE

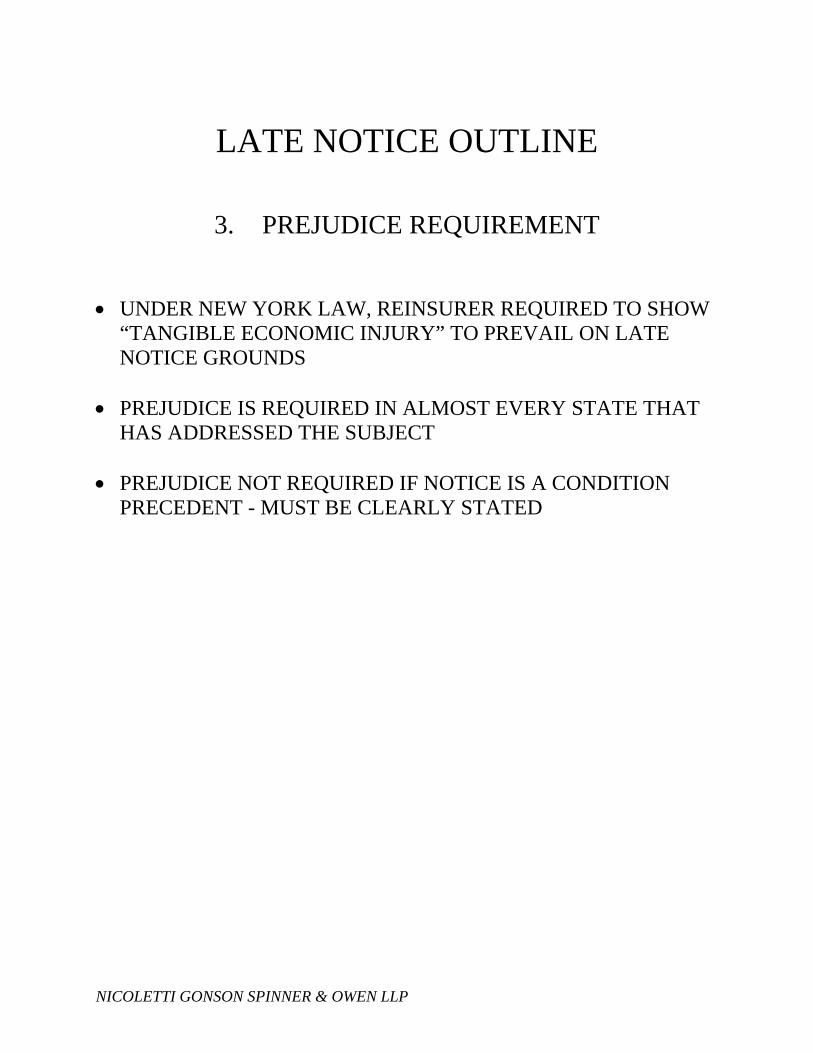

3. PREJUDICE REQUIREMENT

UNDER NEW YORK LAW, REINSURER REQUIRED TO SHOW “TANGIBLE ECONOMIC INJURY” TO PREVAIL ON LATE NOTICE GROUNDS

PREJUDICE IS REQUIRED IN ALMOST EVERY STATE THAT

HAS ADDRESSED THE SUBJECT PREJUDICE NOT REQUIRED IF NOTICE IS A CONDITION

PRECEDENT - MUST BE CLEARLY STATED

NICOLETTI GONSON SPINNER & OWEN LLP

LATE NOTICE OUTLINE

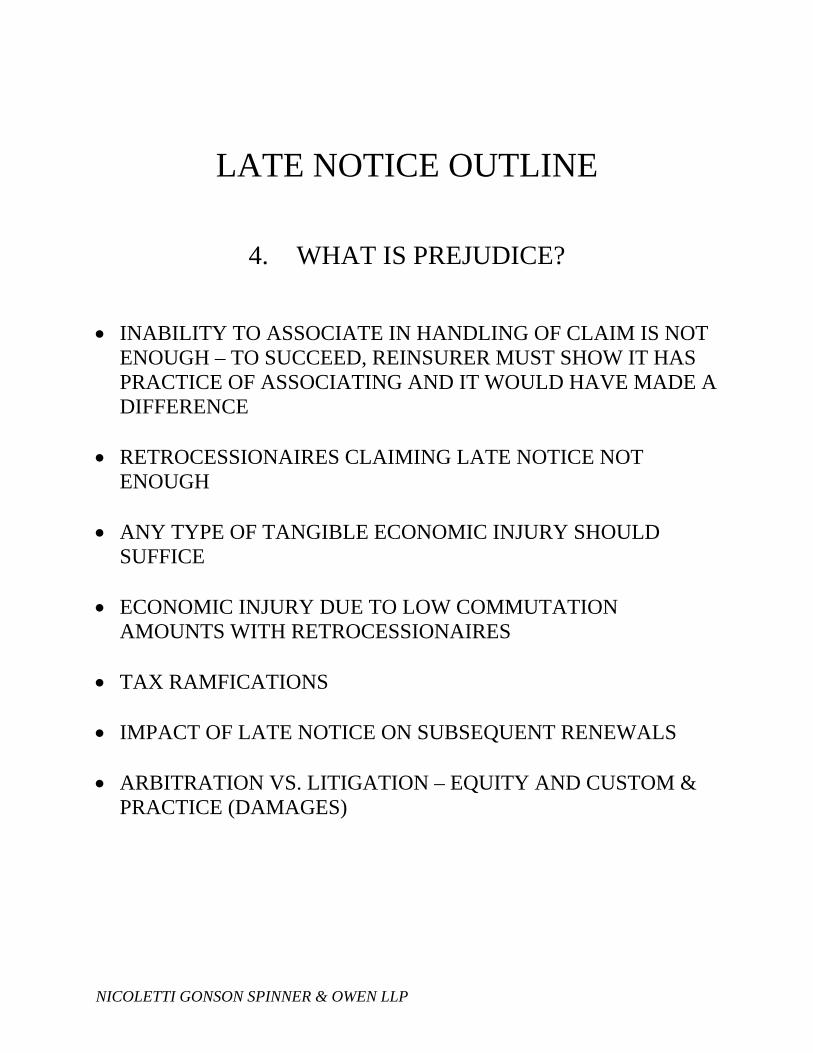

4. WHAT IS PREJUDICE?

INABILITY TO ASSOCIATE IN HANDLING OF CLAIM IS NOT ENOUGH – TO SUCCEED, REINSURER MUST SHOW IT HAS PRACTICE OF ASSOCIATING AND IT WOULD HAVE MADE A DIFFERENCE

RETROCESSIONAIRES CLAIMING LATE NOTICE NOT

ENOUGH ANY TYPE OF TANGIBLE ECONOMIC INJURY SHOULD

SUFFICE ECONOMIC INJURY DUE TO LOW COMMUTATION

AMOUNTS WITH RETROCESSIONAIRES TAX RAMFICATIONS IMPACT OF LATE NOTICE ON SUBSEQUENT RENEWALS ARBITRATION VS. LITIGATION – EQUITY AND CUSTOM &

PRACTICE (DAMAGES)

NICOLETTI GONSON SPINNER & OWEN LLP

NICOLETTI GONSON SPINNER & OWEN LLP

LATE NOTICE OUTLINE

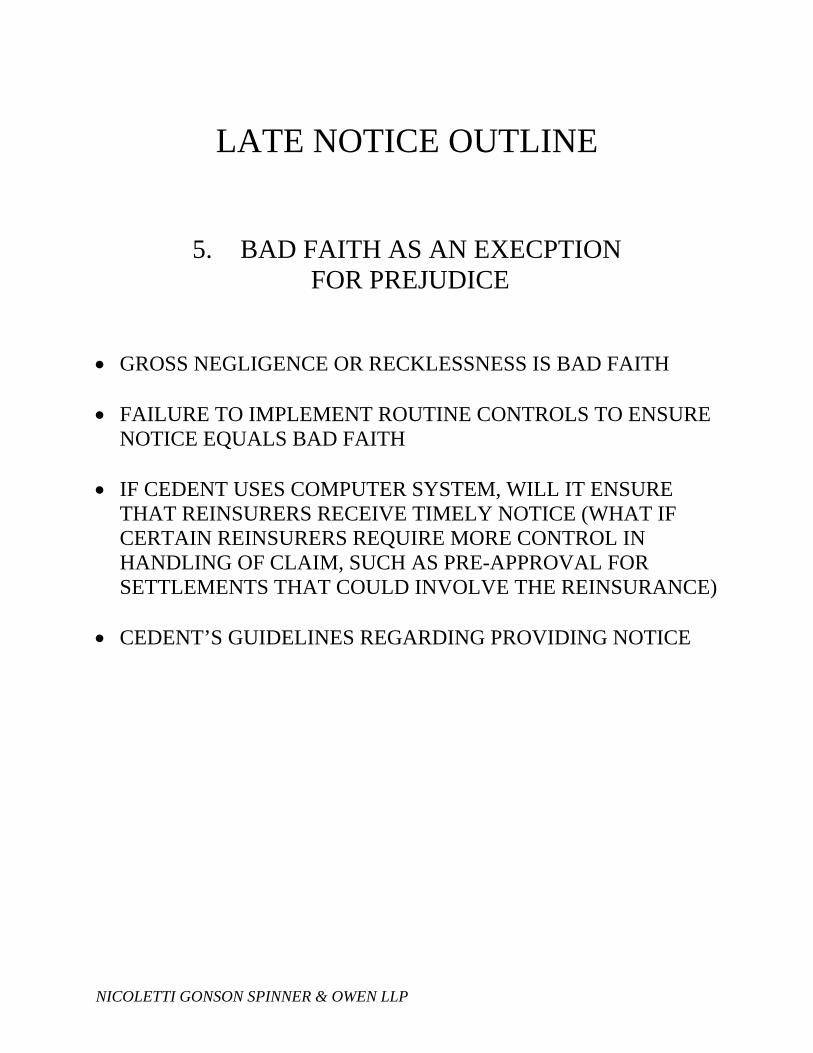

5. BAD FAITH AS AN EXECPTION FOR PREJUDICE

GROSS NEGLIGENCE OR RECKLESSNESS IS BAD FAITH FAILURE TO IMPLEMENT ROUTINE CONTROLS TO ENSURE

NOTICE EQUALS BAD FAITH IF CEDENT USES COMPUTER SYSTEM, WILL IT ENSURE

THAT REINSURERS RECEIVE TIMELY NOTICE (WHAT IF CERTAIN REINSURERS REQUIRE MORE CONTROL IN HANDLING OF CLAIM, SUCH AS PRE-APPROVAL FOR SETTLEMENTS THAT COULD INVOLVE THE REINSURANCE)

CEDENT’S GUIDELINES REGARDING PROVIDING NOTICE

RECISSION OUTLINE

1. ELEMENTS OF RESCISSION REINSURER MUST PROVE THAT: A NON-DISCLOSURE OR MISREPRESENTATION OF FACT(S)

OCCURRED (INNOCENT VS. INTENTIONAL) THE NON-DISCLOSED OR MISREPRESENTED FACT(S) WAS

MATERIAL IT JUSTIFIABLY RELIED ON THE NON-DISCLOSED OR

MISREPRESENTED FACTS

NICOLETTI GONSON SPINNER & OWEN LLP

RESCISSION OUTLINE

2. DUTY OF UTMOST GOOD FAITH

REQUIRES CEDENT TO DISCLOSE ALL FACTS THAT MATERIALLY AFFECT THE RISK, OF WHICH IT IS AWARE, AND OF WHICH THE REINSUER HAS NO REASON TO BE AWARE

IF CEDENT IS AWARE OF FACTS THAT WOULD INFLUENCE

DECISION OF REINSURER TO ACCEPT RISK, THOSE FACTS MUST BE DISCLOSED

NO DUTY TO DISCLOSE STANDARD TERMS THAT

REINSURER OUGHT TO BE AWARE OF IF MATERIAL FACTS HAVE BEEN PROVIDED BUT THEY

ARE UNCLEAR, DUTY IS ON THE REINSURER TO ASK FURTHER QUESTIONS

NICOLETTI GONSON SPINNER & OWEN LLP

RESCISSION OUTLINE

3. MATERIALITY

FACT IS MATERIAL IF THE REINSURER WOULD EITHER

HAVE NOT ISSUED THE POLICY OR CHARGED A HIGHER PREMIUM

OBJECTIVE STANDARD – WHETHER A REASONABLE

CEDENT SHOULD HAVE BELIEVED THE FACT WAS MATERIAL TO THE REINSURER

IF CEDENT ON NOTICE THAT REINSURER CONSIDERS

CERTAIN INFORMATION IMPORTANT, THOSE FACTS ARE PER SE MATERIAL

NICOLETTI GONSON SPINNER & OWEN LLP

RESCISSION OUTLINE

4. JUSTIFIABLE RELIANCE REINSURER MUST SHOW THAT IT RELIED UPON THE

MISREPRESENTATION OR NON-DISCLOSURE IN ACCEPTING THE RISK

REINSURER’S RELIANCE MUST BE REASONABLE RELIANCE DEPENDS UPON A NUMBER OF FACTORS,

INCLUDING THE PARTIES PAST DEALINGS, THEIR RELATIVE SOPHISTICATION AND THE AVENUES AVAILABLE TO REINSURER FOR DISCOVERING THE TRUTH

NICOLETTI GONSON SPINNER & OWEN LLP

NICOLETTI GONSON SPINNER & OWEN LLP

RESCISSION OUTLINE

5. WAIVER OR RATIFICATION OF RIGHT TO RESCIND

RENEWAL OF CONTRACT WITH KNOWLEDGE OF THE PRIOR NON-DISCLOSURE OR MISREPESENTATION OPERATES AS A WAIVER

RATIFICATION OCCURS WHEN PARTY ACCEPTS BENEFITS

FLOWING FROM CONTRACT, OR REMAINS SILENT, OR ACQUIESCES IN CONTRACT, FOR ANY CONSIDERABLE LENGTH OF TIME AFTER HAVING OPPORTUNITY TO VOID CONTRACT

DELAY IN RESCINDING WILL NOT CONSTITUTE

RATIFICATION IF REINSURER ENGAGED IN REASONABLE INVESTIGATION OR NOT IN FULL KNOWLEDGE OF RELEVANT FACTS

PREJUDICE TO THE CEDENT FROM THE DELAY COULD BE

A FACTOR, ESPECIALLY IN ARBITRATION

DEALING WITH MAJOR RECURRING ISSUES

Reinsurance Outlook 2010 Conference 30 Rockefeller Plaza, NY, NY

February 9, 2010 Kenneth Levine, Esquire, Moderator Nelson Levine de Luca & Horst 518 Township Line Rd., Ste 300 Blue Bell, PA 19422 215.358.5170 www.nldhlaw.com Jessica Pardi, Esquire Morris, Manning & Martin, LLP 1600 Atlanta Financial Center, 3343 Peachtree Rd., NE Atlanta, GA 30326-1044 404.504.7662 www.mmmlaw.com Ben Gonson, Esquire Nicoletti Gonson Spinner & Owen, LLP 555 Fifth Avenue, 8th Floor New York, NY 10017 (212) 730-7750 www.nicolettilaw.com

REINSURANCE OUTLOOK 2010

DEALING WITH MAJOR RECURRING ISSUES

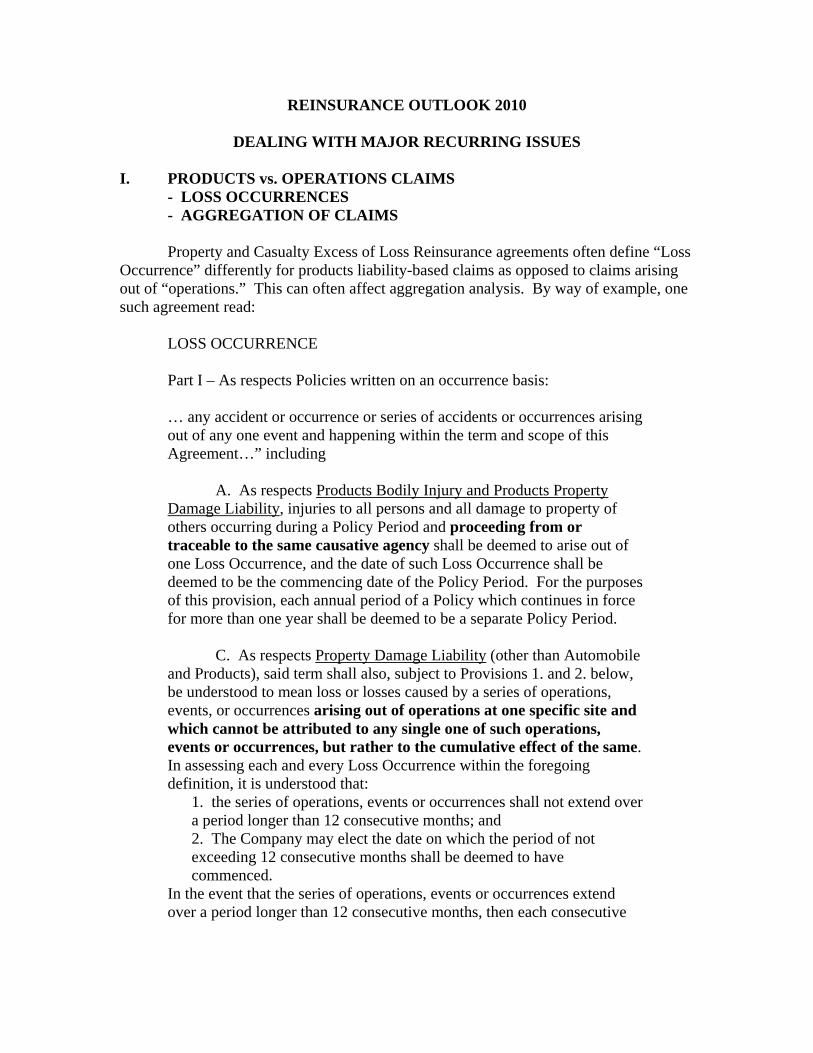

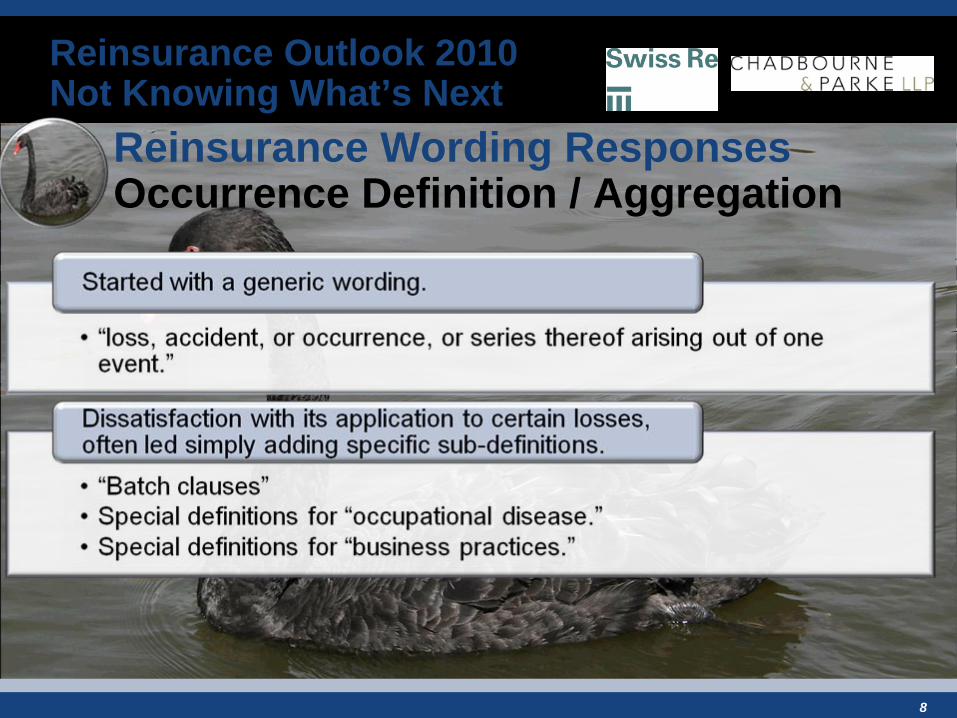

I. PRODUCTS vs. OPERATIONS CLAIMS - LOSS OCCURRENCES - AGGREGATION OF CLAIMS Property and Casualty Excess of Loss Reinsurance agreements often define “Loss Occurrence” differently for products liability-based claims as opposed to claims arising out of “operations.” This can often affect aggregation analysis. By way of example, one such agreement read:

LOSS OCCURRENCE Part I – As respects Policies written on an occurrence basis: … any accident or occurrence or series of accidents or occurrences arising out of any one event and happening within the term and scope of this Agreement…” including A. As respects Products Bodily Injury and Products Property Damage Liability, injuries to all persons and all damage to property of others occurring during a Policy Period and proceeding from or traceable to the same causative agency shall be deemed to arise out of one Loss Occurrence, and the date of such Loss Occurrence shall be deemed to be the commencing date of the Policy Period. For the purposes of this provision, each annual period of a Policy which continues in force for more than one year shall be deemed to be a separate Policy Period. C. As respects Property Damage Liability (other than Automobile and Products), said term shall also, subject to Provisions 1. and 2. below, be understood to mean loss or losses caused by a series of operations, events, or occurrences arising out of operations at one specific site and which cannot be attributed to any single one of such operations, events or occurrences, but rather to the cumulative effect of the same. In assessing each and every Loss Occurrence within the foregoing definition, it is understood that: 1. the series of operations, events or occurrences shall not extend over

a period longer than 12 consecutive months; and 2. The Company may elect the date on which the period of not

exceeding 12 consecutive months shall be deemed to have commenced.

In the event that the series of operations, events or occurrences extend over a period longer than 12 consecutive months, then each consecutive

period of 12 months … shall form the basis of claim under this Agreement.

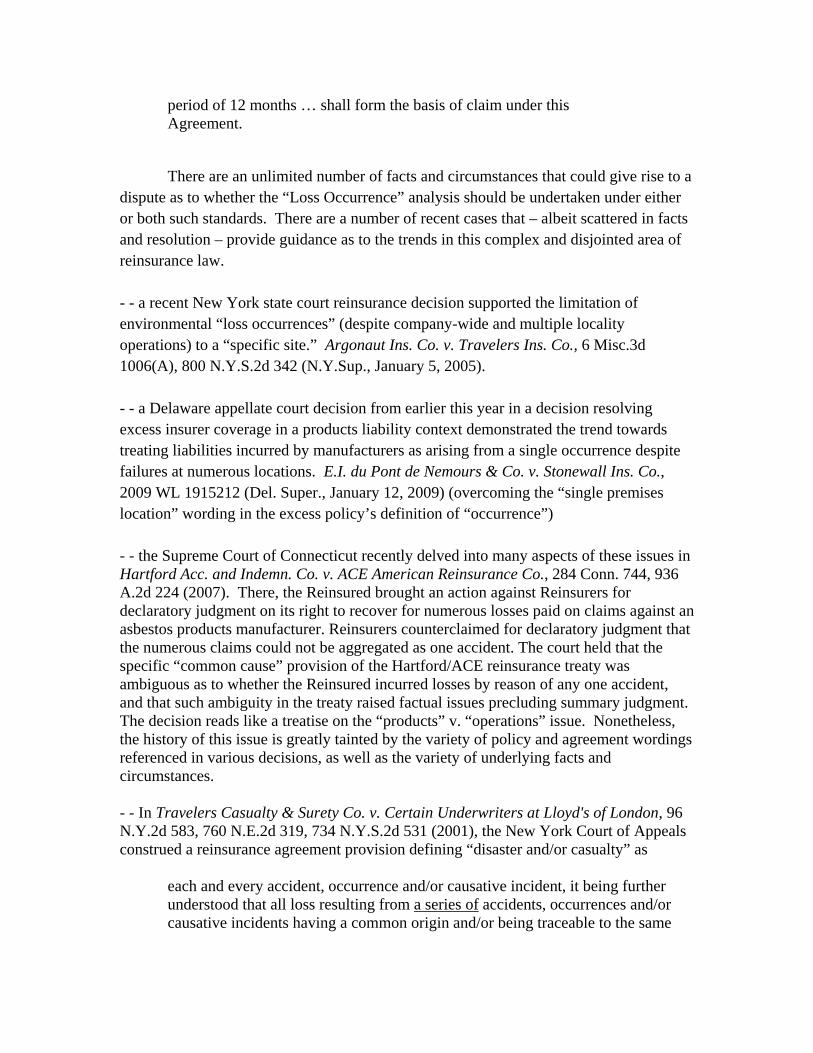

There are an unlimited number of facts and circumstances that could give rise to a dispute as to whether the “Loss Occurrence” analysis should be undertaken under either or both such standards. There are a number of recent cases that – albeit scattered in facts and resolution – provide guidance as to the trends in this complex and disjointed area of reinsurance law. - - a recent New York state court reinsurance decision supported the limitation of environmental “loss occurrences” (despite company-wide and multiple locality operations) to a “specific site.” Argonaut Ins. Co. v. Travelers Ins. Co., 6 Misc.3d 1006(A), 800 N.Y.S.2d 342 (N.Y.Sup., January 5, 2005). - - a Delaware appellate court decision from earlier this year in a decision resolving excess insurer coverage in a products liability context demonstrated the trend towards treating liabilities incurred by manufacturers as arising from a single occurrence despite failures at numerous locations. E.I. du Pont de Nemours & Co. v. Stonewall Ins. Co., 2009 WL 1915212 (Del. Super., January 12, 2009) (overcoming the “single premises location” wording in the excess policy’s definition of “occurrence”) - - the Supreme Court of Connecticut recently delved into many aspects of these issues in Hartford Acc. and Indemn. Co. v. ACE American Reinsurance Co., 284 Conn. 744, 936 A.2d 224 (2007). There, the Reinsured brought an action against Reinsurers for declaratory judgment on its right to recover for numerous losses paid on claims against an asbestos products manufacturer. Reinsurers counterclaimed for declaratory judgment that the numerous claims could not be aggregated as one accident. The court held that the specific “common cause” provision of the Hartford/ACE reinsurance treaty was ambiguous as to whether the Reinsured incurred losses by reason of any one accident, and that such ambiguity in the treaty raised factual issues precluding summary judgment. The decision reads like a treatise on the “products” v. “operations” issue. Nonetheless, the history of this issue is greatly tainted by the variety of policy and agreement wordings referenced in various decisions, as well as the variety of underlying facts and circumstances. - - In Travelers Casualty & Surety Co. v. Certain Underwriters at Lloyd's of London, 96 N.Y.2d 583, 760 N.E.2d 319, 734 N.Y.S.2d 531 (2001), the New York Court of Appeals construed a reinsurance agreement provision defining “disaster and/or casualty” as

each and every accident, occurrence and/or causative incident, it being further understood that all loss resulting from a series of accidents, occurrences and/or causative incidents having a common origin and/or being traceable to the same

act, omission, error and/or mistake shall be considered as having resulted from a single accident, occurrence and/or causative incident.

Travelers had separate coverage litigations paid two corporations for claims against them arising from pollution at numerous hazardous waste sites that they had operated for decades. Travelers then sought reimbursement from the defendant Reinsurers claiming that all of the claims against each separate corporation could be aggregated because the waste sites “shared a ‘common origin,’ namely, a managerial failure ... in the implementation and enforcement of [the corporations'] company-wide environmental policy.” Id., at 592, 734 N.Y.S.2d 531, 760 N.E.2d 319. The Court of Appeals concluded that because the word “series” implied a spatial or temporal relationship between the members of the series, the events at the separate waste sites were not a “series of accidents” and could not be aggregated for purposes of reinsurance. Id., at 594, 734 N.Y.S.2d 531, 760 N.E.2d 319.

There remains a rather unsettled issue in this area, that being whether premises operations claims that do not come within the products hazard provision of an underlying asbestos liability insurance policy (because they arose before the product had been relinquished by the insured) can nevertheless come within a reinsurance treaty's common cause provision because they “arose out of products.” Certain recent cases have attempted to deal with this issue: - - the New York Court of Appeals in Frontier Insulation Contractors, Inc. v. Merchants Mutual Ins. Co., 91 N.Y.2d 169, 690 N.E.2d 866, 667 N.Y.S.2d 982 (1997), provided some guidance on the issue. The case involved a coverage dispute between an asbestos insulation contractor and its insurers involving multiple asbestos related personal injury claims. The insurers contended that all of the claims fell within the policies' exclusions for products hazards. The court redirected the focus: “it is not simply whether an insured's product caused the loss at issue, but rather is dependent on the location of the accident and the possession of the product.... [The insurers'] argument fails to appreciate that an exclusion for product hazards governs only one subset of product liability claims.” Id., at 175-76, 667 N.Y.S.2d 982, 690 N.E.2d 866. The court concluded that the insurers would be relieved of their duty to defend the claims only if they established both that the claims fell squarely within the products hazard provisions (that the claims arose away from the insured's premises) and after possession of the asbestos had been relinquished. The court in Frontier Insulation Contractors, Inc., implicitly recognized that, although product hazard claims and operations claims are mutually exclusive, some operations claims may “arise out of products.” - - in Commercial Union Ins. Co. v. Porter Hayden Co., 116 Md.App. 605, 692-93, 698 A.2d 1167 (1996) , cert. denied, 348 Md. 205, 703 A.2d 147 (1997) the Maryland state court found that liability for injuries resulting from exposure to asbestos products could arise under the “operations” clause if exposure occurred before product was relinquished by insured.

- - the court in Continental Casualty Co. v. Employers Ins. Co. of Wausau, 16 Misc.3d 223, 230-31, 839 N.Y.S.2d 403 (2007) noted in a reinsurance context that the “products hazard” provision covers risks due to defective products that have been put into stream of commerce while premises/operations provision covers “risks that arise due to injuries from the defective product at the insured's premises or while the work with the product is still in progress.” - - the Supreme Court of Connecticut also addressed this issue in Hartford Acc. and Indemn. Co. v. ACE American Reinsurance Co., 284 Conn. 744, 936 A.2d 224 (2007), noting that products hazard claims constitute only a subset of claims that can be said to “arise from products.” The court acknowledged though that there was a close linguistic similarity between the language of the reinsurance treaty's “common cause” provision and the “products hazard” provision of the underlying policies – and that such connection suggested some correspondence in meaning between the two provisions. It concluded though that the “arising out of products” portion of the “common cause” provision in the reinsurance treaty was ambiguous as to whether it refers to liability arising out of the “products hazard” provision of the underlying liability policies or, instead, refers to any claim arising from a product, regardless of whether the manufacturer had relinquished physical possession of the product at the time that liability was incurred. The court determined in turn that the meaning of the provision must be determined by the finder of fact on remand. II. NET RETAINED LINES PROVISION

An excess of loss reinsurance agreement’s Net Retained Lines clause compels a Reinsured to “tap” other reinsurances first so that the treaty only protects the net excess loss, operating as protection only after proportional treaty or facultative cessions. In turn, the excess of loss reinsurance applies only to those losses that apply to the ceding insurer's net retentions. The excess of loss contract does not apply to losses otherwise covered by other reinsurance or above the insured's net retention, whether collectible or not, as well as net of salvages and all other recoveries due the Reinsured.

By way of example, one such agreement read, in part:

NET RETAINED LINES This Agreement shall protect only that portion of any insurance or reinsurance which the Reinsured, acting in accordance with its established practices at the time of the commencement of this Agreement, retains net for its own account. The Reinsurer's liability hereunder shall not be increased due to any error or omission which results in the Reinsured's net retention being larger than it would normally have been nor by the Reinsured's failure to reinsure and maintain reinsurance in accordance with its established practice as aforesaid, nor by the inability of the

Reinsured to collect from any other Reinsurers any amounts which may have become due from them for any reason whatsoever.

There are no known reported US decisions that address any issues arising from such concept or such applicable provisions.

There is a distinction between “Net Retained Lines” and “Net Loss Retention” that should be noted. “Net Loss Retention” is the amount of loss which a Reinsured keeps for its own account and does not pass on to another Reinsurer. In excess of loss reinsurance, the term "first loss retention" is sometimes used. A further discussion of Net Loss Retention is contained in the Warranties section immediately below. III. WARRANTIES

Certain provisions in reinsurance agreements may be construed as “warranties” or “conditions precedent” - obligations that the Cedent must meet before it may recover under the agreement.

A. NET LOSS RETENTION WARRANTY The most discussed such warranty is the Net Loss Retention Warranty.

In Stonewall Ins. Co. v. Fortress Reinsurers Managers, Inc., 83 N.C.App. 263,

350 S.E.2d 131 (1986), disc. rev. denied, 319 N.C. 410, 354 S.E.2d 728 (1987), the court construed a facultative reinsurance contract containing the following “net loss retention” language:

The company warrants to retain for its own account the amount of liability specified in Item 3 [$500,000] unless otherwise provided herein, and the liability of the Reinsurer specified in Item 4 shall follow that of the Company, except as ... provided herein, and shall be subject in all respects to all the terms and conditions of the Company's policy.

The court in Stonewall Ins. Co. held that the Cedent was not entitled to recover under the reinsurance agreement because (a) compliance with the warranty / net loss retention provision was a condition precedent to the Reinsurer's liability; (b) the Cedent had breached the warranty by ceding part of its retention to treaty Reinsurers; and (c) the Reinsurer had not waived the warranty and was not estopped from relying on its breach.

Similarly, in Fortress Re, Inc. v. Jefferson Insurance Company of New York, 465 F.Supp. 333 (E.D.N.C.1978), aff'd, 628 F.2d 860 (4th Cir.1980), the federal district court opined that “In the absence of any evidence as to the intent of the parties as to the meaning of the language in the [net loss] retention clause, a retention warranty was breached by the Reinsured company when it retained for its own account only a portion of the risk and reinsured the remainder in a reinsurance treaty with another reinsurance

company. Compliance with the retention warranty was a condition precedent to the Reinsured’s recovery. A North Carolina federal court reached the same conclusion based upon the exact same retention warranty language in Penn Re, Inc. v. Stonewall Ins. Co., 708 F.Supp. 123 (E.D.N.C., 1988), aff’d 894 F.2d 402.

In Commercial Union Ins. Co. v. Seven Provinces Ins. Co., Ltd., 217 F.3d 33 (1st Cir. (Mass.) July 6, 2000), a district court struggled to address the meaning of a net retention provision in a facultative reinsurance certificate. Although the policy called for the Reinsurer’s liability to be “proportionally reduced” to the extent that the Reinsured retained less than 50% of the risk, it permitted the Reinsured to obtain “general excess loss or excess catastrophe reinsurance” without violating the net retention requirement.

The parties acknowledged that “general excess loss or excess catastrophe reinsurance” were not common terms in the industry. The facultative reinsurance certificate was therefore deemed ambiguous as to whether quota share treaty reinsurance could cover Cedent’s share of the risk of loss or if it would violate the net retention requirement and entitle the Reinsurer to a reduction in its obligation. The district court considered extrinsic evidence to determine what the parties meant by the phrase “general excess loss or excess catastrophe reinsurance.” Evidence of the parties' actual intent was unavailable, but each side proffered an insurance expert who testified to what the terms must have meant in light of industry practice. The Reinsurer’s expert argued that the phrase “general excess loss or excess catastrophe reinsurance” was probably meant to prohibit the Reinsured from using quota share treaty reinsurance and to permit only the use of additional “excess loss” or “excess catastrophe” cover. Reinsured’s expert took the opposite view of the policy language and explained that (1) industry custom long has permitted treaty reinsurance on a risk insured by a facultative certificate absent unequivocal language to the contrary; (2) because the facultative certificate only imposed a net retention requirement “on the identical subject matter and risk and in identically the same proportion,” it did not preclude the use of a qualitatively different kind of additional coverage such as quota share treaty insurance; and (3) while the contract was ambiguous, it probably was meant to authorize “general” as well as “excess of loss” reinsurance - in which case the use of quota share treaty reinsurance would have been permissible without triggering a reduction in coverage. The district court found this latter opinion to be a more credible interpretation of the relevant language, emphasizing the expert’s more extensive experience in the reinsurance industry, his testimony’s consistency on direct and cross-examination, and his more comprehensive reasoning. The Court of Appeals found no basis to reverse this conclusion. Nonetheless, this decision demonstrates the importance of well written policy language in the warranty context, as well as others.

Similarly, in Penn Re, Inc. v. Stonewall Ins. Co., 708 F.Supp. 123 (E.D. N.C., Dec. 16, 1988) and Stonewall Ins. Co. v. Fortress Reinsurers Managers, Inc., 83 N.C.App. 263, 350 S.E.2d 131 (N.C. App., Nov. 18, 1986), the court reviewing the same facts noted how the Reinsured had violated its warranty (deemed a condition precedent)

where a facultative reinsurance certificate with a net retention warranty clause required retention of $500,000 of the risk for “its own account.” The Reinsured asserted that the clause was susceptible to interpretations other than a literal promise that it would not cede any portion of this sum to another carrier; that it was understood as a custom and practice in the reinsurance industry that the term, “for its own account,” permits the reinsurance of the retention by treaty reinsurance; and that the cession of $450,000 of the stated retention to another Reinsurer had been accomplished by treaty reinsurance. The court noted that the warranty was a condition precedent to liability; that it had been breached by the purchase of other treaty reinsurance.

B. UNDERWRITING WARRANTIES “Warranties” can also be used in reinsurance agreements to limit a Reinsurer’s

exposure to certain types of losses that would otherwise be covered under the reinsurance agreement. This is done by having the Reinsured “warrant” the limited coverage scope or amounts of its underlying insurance policies.

In the recent decision, Princeton Ins. Co. v. Converium Reinsurance (North

America) Inc., 2009 WL 2915092 (3d Cir., September 14, 2009), summary judgment was granted to the Cedent and against the Reinsurer where a warranty in the reinsurance agreement purported to limit the Reinsurer's exposure from Employer Liability claims to set limits. The underlying insurance policy appeared to comply with the warranty provision on its face, but the limitation that it imposed was prohibited under New York's Insurance Law. The Cedent and Reinsurer were thus exposed to far more risk than anticipated. The appellate court held that the wording of the agreement in this warranty was ambiguous and vacated the trial court’s summary judgment ruling – leaving the matter to be decided as a factual issue of broader contract interpretation.

As in the Princeton Ins. Co. matter, other courts have held that if Reinsurers want

warranties or other assurances, they should be explicit as to their parameters. For example, in PXRE Reinsurance Co. v. Lumbermens Mut. Cas. Co., 330 F.Supp.2d 981 (N. D. Ill., Aug. 10, 2004), an Aggregate Excess of Loss Retrocessional Reinsurance Agreement contained a warranty negation clause that read in part:

This Stop Loss Cover … constitute the entire agreement between the parties … and supersede all prior and contemporaneous agreements, understandings, negotiations, and discussions, … and there are no general or specific warranties, representations or other agreements by or among the parties in connection with the entering into this Stop Loss Cover … except as specifically set forth or contemplated herein.

The court rejected the Retrocessionaire’s assertion that uberrimae fidae (“utmost good faith” responsibility) operated as a powerful public policy doctrine that trumped any express boundaries the parties elected to circumscribe their contractual relationship, and that certain false assurances had been made by the Retrocedent that should have negated

the retrocession. The court read the no warranties provision literally, and foreclosed any argument of implied warranty via “uberrimae fidae.” These and other such decisions demonstrate the important need to explicitly and clearly include all guarantees or warranties expected by parties into their reinsurance agreements.

IV. ALLOCATION

Any discussion as to allocation these days ties ever so closely into a discussion as to the “Follow the Fortunes” doctrine – as most of the recent cases of such reinsurance doctrine deal with post-settlement allocations. These require that the allocation must be reasonable, in good faith and within the coverage provided by the reinsurance agreement. V. “LEGALLY OBLIGATED TO PAY”

A Reinsurer's obligations under an agreement with respect to the amounts incurred by the Cedent in connection with the underlying loss are not always clear or easy to discern. Most reinsurance agreements contain a clause limiting exposure to underlying payments made that the Reinsured was “legally obligated to pay.” This is in contrast to explicit or implied “follow the settlement” provisions. Additionally, time-wise, when a Reinsurer may be held liable to make payments (when the Cedent becomes obligated to pay, or when the Cedent has actually made payment) remains unclear under the law. In The Tall Tree Ins. Co. v. Munich Re, 2008 WL 2950098 (N.D. Cal., July 29, 2008), a federal court in California held that it was premature to decide the validity of reinsurance claims until the reinsured carrier had paid a claim that its insured had submitted or may in the future submit, or until a determination is otherwise made that the reinsured carrier “is obligated to pay any such claim.” Otherwise, the Reinsurer would not be in a position to decide if the Reinsured had paid a claim in good faith. In American Motorists Ins. v. American Re, 2007 WL 4197427 (N.D.Cal., Nov. 21, 2007), after a court determined that a “follow the settlements” provision was not included in a reinsurance agreement (and would not be implied as well), it held that the Reinsured bore the burden of establishing that the underlying claim settlement was covered by its obligations under the underlying policy. While it acknowledged that the agreement unambiguously provided the Reinsured the right to settle claims, it held that a “triable question of fact exists regarding whether the … claim was covered by the [policy, and that] Plaintiff bears the burden of establishing that it was liable for the … claim based on the [underlying policy].” Similarly, in The American Ins. Co. v. American Re, 2006 WL 3412079 (N.D.Cal., Nov. 27, 2006), after a California federal court refused to read an implied

“follow the fortunes” or “follow the settlements” provision into a reinsurance agreement, the court found that American Re may assert defenses that would have been available to the Reinsurer against the insured at the time of settlement as it only agreed to reinsure for losses or damages which the Cedent was legally obligated to pay on the underlying insurance policies. As both of the underlying excess policies at issue provided insurance in excess of $25 million of underlying insurance, the court held that there would be no obligation to pay reinsurance on the excess policies if and until the underlying insurance policies were exhausted. The court also found that there was a genuine issue of material fact as to whether the Reinsured could have prevailed on the validity and scope of an asbestosis exclusion in its liability policy. In North River Ins. Co. v. Ace American Reinsurance Co., 361 F.3d 134 (2d Cir. 2004), the Reinsurer took an aggressive stance that the Reinsured’s' settlement of its obligations to its insured asbestos manufacturer took into consideration its “risk of loss,” outside and above its layers of coverage reinsured by this Reinsurer and therefore the settlement was outside the definition of loss that this Reinsured was “legally obligated to pay.” The court held that the Reinsured's allocation of settlement loss, as opposed to “risk of loss,” to Reinsurer was within definition of “loss” covered by reinsurance contract. The fact that the Reinsured had considered the risk of loss to layers of coverage above Reinsurer's layer in settling its obligations to its insured asbestos manufacturer for underlying claims against such insured did not impact on Reinsurer's obligation to indemnify Reinsured for actual loss incurred under reinsurance contract. There will always be tension between the concepts of “follow the fortunes” / “follow the settlements” and the provision that requires the Reinsurer to only indemnify for monies that the Reinsured was “legally obligated to pay.” It will always be resolved by a balancing of these issues based upon the wording of the agreements, the relationship between the parties, and the underlying facts and circumstances. VI. LATE NOTICE

There are a number of legal decisions that have addressed the material effect of untimely notice as to reinsurance claims. Some of the following recent cases shed light of the recent court trends as to such issue.

In AIU Ins. Co. v. TIG Ins. Co., 2008 WL 5062030 (S.D.N.Y., Nov. 25, 2008), the

court addressed the issue in the context of an attorney client waiver dispute. New York law has historically strictly construed timely notice provisions in (direct) insurance policies. The federal court here noted, though, that by contrast, in a reinsurance contract, a contractual duty to give prompt notice “is not a condition precedent to coverage absent clear language to the contrary.” This was a direct application of an earlier New York state court decision in Unigard Sec. Ins. Co. v. N. River Ins. Co., 79 N.Y.2d 576, 582, 594 N.E.2d 571, 574, 584 N.Y.S.2d 290, 293 (1992). The court held that the “prompt-notice” clause in the subject reinsurance contract was not a condition precedent because

there was no express language in the contract indicating the parties' intent that this clause operate as such.

In another recent decision from a New York federal court, Global Reinsurance

Corp. v. Argonaut Ins. Co., 548 F.Supp.2d 104 (S.D.N.Y., April 28, 2008) the court noted that under New York law a reinsurance company may only avoid its obligation to pay claims for which it received late notice (1) if there is an express provision in the treaty making timely notice a condition precedent or (2) it can demonstrate that it was prejudiced by such late notice. The court in Global Reinsurance found support for this in another classic Unigard Sec. Ins. Co. late notice precedent (Unigard Sec. Ins. Co., Inc. v. North River Ins. Co., 4 F.3d 1049 (2d Cir. 1993).

These recent New York decisions are a bit unique though, as this issue (prompt

notice to a Reinsurer) has been very poorly developed. In fact, a recent federal court decision out of Florida, Employer Reinsurance Corp. v. Laurier Indem. Co., 2007 WL 1831775 (M.D. Fla., June 25, 2007) noted that “Georgia reinsurance law is practically non-existent with regard to the issue of timeliness of notice.” The court went on to review the issue by relying almost entirely on Georgia law in the context of excess insurance policies and notice provisions therein. The language of the subject notice provision controlled the decision, as it required the Reinsured to give prompt notice when “in the judgment of the [Reinsured],” it might result in a claim for indemnity under the reinsurance agreement. In turn, under this policy wording the time of notice was a subjective question of judgment and the Reinsured was “deemed to have provided sufficient notice as long as it used due diligence and took appropriate steps to make an informed judgment regarding the nature and amount of the claim.”

Despite these New York decisions requiring wording as to “condition precedent”

status, or demonstrable prejudice, the court in Allstate Ins. Co. v. Employers Reinsurance Corp., 441 F.Supp.2d 865 (N.D. Ill., Mar. 18, 2005) viewed the issue differently. In the face of some extensive untimely notice as to many reinsurance claims arising from underlying PIP claims, the court held that the law in Illinois is clear that a notice requirement, such as the one contained in the subject reinsurance treaty, was in fact a condition precedent to coverage. Consequently, when the Reinsured failed to comply with the notice requirement, the Reinsurer could deny liability, regardless of whether it has been prejudiced by the delay. The court did note that the United State Court of Appeals for the Seventh Circuit had interpreted Illinois law to distinguish between notice clauses that required parties to give “prompt” or “immediate” notice, as in the subject reinsurance treaty here, and those that require parties to give notice “as soon as practicable,” or “reasonable” notice. In this regard, in cases where the contract between the parties requires only reasonable notice, prejudice was a factor to be considered in assessing the reasonableness of notice. The problem with the court’s analysis though is that it was convinced that the Reinsurer had in fact been prejudiced, so the legal banter as to criteria seems superfluous (“The prejudice in this case, however, is clear: with regard to the seven claims that Allstate failed to report until after the Treaty was implicated, ERC had no opportunity to build adequate reserves to pay these claims or plan for its financial obligations.”)

As with so many of these reinsurance issues, a great deal of the interpretation and application will depend on the wording of the agreement prompt notice language, as well as the nature of the underlying loss.

“Late Notice” Presentation Outline Prepared and Presented by Ben Gonson, Esquire Nicoletti Gonson Spinner & Owen, LLP 555 Fifth Avenue, 8th Floor, New York, NY 10017 (212) 730-7750 www.nicolettilaw.com 1. Prompt Notice. Prompt notice requirements are typically seen in all

Facultative Certificates and in most Excess of Loss Treaties. These permit Reinsurers to properly reserve, to adjust premiums, and to decide whether to associate in handling claims.

2. When is Notice Late? Prompt notice is typically required when the claim

appears likely to involve the reinsurance or when reserves set by the Cedent reach 50% of the retention. When a claim is likely to involve the reinsurance is sometimes viewed as a subjective test and sometimes as an objective one. The “promptness” of the notice is sometimes based upon specific types of injuries.

3. Prejudice. Under New York Law, a Reinsurer is required to show “tangible

economic injury” to prevail on Late Notice defense. In re Liquidation of Midland Ins. Co., 18 Misc.3d 1117(A), 856 N.Y.S.2d 498 (N.Y. Sup., Jan. 14, 2008); Unigard Sec. Ins. Co. v. North River Ins. Co., 4 F.3d 1049, 1068 (2d Cir.1993). Prejudice is required in almost every state that has similarly addressed the subject. Most courts agree, though, that prejudice would not be required if prompt notice had been clearly stated to form a condition precedent in the reinsurance agreement

4. What Amounts to “Prejudice”? a. Inability to associate in handling claims is probably not in and of itself enough

to prevail unless reinsurer can demonstrate that it has a practice of associating on claims handling and it would have made a difference if it had;

b. Retrocessionaire claiming late notice is probably not enough; c. Any “tangible economic injury” should suffice, including:

i. Economic injury due to low commutation amounts received from Retrocessionaires should suffice;

ii. Tax Ramifications; iii. Impact on Subsequent Renewals

5. “Bad Faith” Conduct May Act as Exception to Prejudice. “Bad faith” in

this context equates to “gross negligence” or “recklessness.” It may be met by a failure to implement routine controls to ensure notice. This raises the issue as to a Cedent’s guidelines regarding Prompt Notice. For example, if a Cedent uses a computer system, does it ensure that Reinsurers will receive timely notice (what if certain Reinsurers

require greater control in claim handling, such as pre-approval for settlements that could involve reinsurance coverage). These all become factors.

VII. RESCISSION

“Rescission” Presentation Outline Prepared and Presented by Ben Gonson, Esquire Nicoletti Gonson Spinner & Owen, LLP 555 Fifth Avenue, 8th Floor, New York, NY 10017 (212) 730-7750 www.nicolettilaw.com

1. Elements of Rescission. A Reinsurer must prove: (1) a non-disclosure or

misrepresentation of fact(s) occurred (innocent or intentional); (2) the non-disclosed or misrepresented fact(s) was material; and (3) it justifiably relied on the non-disclosed or misrepresented facts. 2. Duty of Utmost Good Faith. This duty requires Cedent to disclose all facts that materially affect the risk of which it is aware, and of which the Reinsurer has no reason to be aware. If the Cedent is aware of facts that would influence decision of the Reinsurer to accept the risk, those facts must be disclosed. There is no duty to disclose standard terms of which Reinsurer should be aware. If material facts have been provided but they are unclear, the duty probably falls on the Reinsurer to ask further questions.

3. Materiality. Facts are “material” if the Reinsurer either would not have issued the policy or would have charged a higher premium. This is an objective standard; that being whether a reasonable Cedent should have believed the fact to be material to the Reinsurer. If a Cedent is on notice that a Reinsurer considers certain information important, those facts arguably become per se “material.”

4. Justifiable Reliance. A Reinsurer must show that it relied upon the misrepresentation or non-disclosure in accepting the risk, and that such reliance was reasonable. Reliance depends upon a number of factors, including the parties’ past dealings, their relative sophistication and the avenues available for the Reinsurer to discover or know the truth.

5. Waiver or Ratification of Right to Rescind. A renewal of the contract with knowledge of the prior non-disclosure or misrepresentation will usually operate as a waiver. “Ratification” occurs when a party accepts benefits flowing from a contract, or remains silent and/or acquiesces in a contract, for any considerable length of time after having an opportunity to void the contract. Delay in rescinding probably will not in and of itself constitute “ratification” if the Reinsurer engaged in reasonable investigation and/or did not have full knowledge of true material facts. Prejudice to the Cedent from such a delay could be a factor, especially in arbitration.

VIII. FOLLOW THE SETTLEMENTS

“Follow the Settlements” Presentation Outline Prepared and Presented by Jessica Pardi, Esquire Morris, Manning & Martin, LLP 1600 Atlanta Financial Center, 3343 Peachtree Rd., NE Atlanta, GA 30326-1044 404.504.7662 [email protected] www.mmmlaw.com

A. Generally The “Follow the Settlements” doctrine is a contractual obligation by a reinsurer to

indemnify a reinsured for claim payments or settlements made to its underlying insured provided the payment is not fraudulent, made in bad faith or otherwise ex gratia. This principle is meant to be narrower in scope than “Follow the Fortunes.” The purposes of the “Follow the Settlements” doctrine are: (1) to prevent second-guessing by the reinsurer; (2) to avoid re-litigation of coverage disputes; and (3) to promote good faith settlements.

A simple example of a clause enunciating such doctrine in a reinsurance agreement is: “Reinsurer agrees to abide by the loss settlements of the Reinsured.” To this may be added a notice provision mandating that the reinsured notify the reinsurer of claims to which the reinsurance applies (or may apply or likely will apply) and an opportunity for the reinsurer to associate in the defense and/or settlement of the underlying claim (typically at the reinsurer’s expense).

Similarly, the “Honorable Undertaking” clause in arbitration agreements may also contain language regarding follow the settlements such as the following: “The Treaty(ies) shall be construed as an honorable undertaking between the parties hereto, not to be defeated by technical legal constructions. It is the intention of the Treaty(ies) that the fortunes of the Reinsurer shall follow the fortunes of the Reinsured.” B. Implied “Follow the Settlements” in Reinsurance Agreements

A number of reported decisions have addressed whether or not the “follow the settlements” doctrine is implied in all reinsurance agreements.

In International Surplus Lines Ins. Co. v. Certain Underwriters & Underwriting

Syndicates at Lloyd’s of London, 868 F.Supp. 917 (S.D. Ohio 1994), the court held that the “follow the settlements” doctrine was implied into all reinsurance contracts. The court found that it was implicit because it was necessary to preserve the cedent-reinsurer relationship, and to maximize coverage. Shortly thereafter, the court in Aetna Cas. & Surety Co. v. Home Ins. Co., 882 F.Supp. 1328 (S.D.N.Y. 1995) found that “follow the

settlements” was implied in a reinsurance contract based upon parol evidence as to custom and practice in the industry.

Eight years later, the United States Court of Appeals for the Second Circuit, in British Int’l. Ins. Co. v. Seguros La Republica, S.A., 342 F.3d 78 (2d Cir. 2003), strictly limited “custom and usage” parol evidence in such instances (requiring that only evidence establishing that the allegedly implied provision was fixed and invariable throughout the entire industry in question). This strict evidentiary standard precluded the evidence employed in Aetna v. Home, and “follow the fortunes” (in that instance) was not implied into the agreement.

The majority of courts no longer imply “follow the settlements” into reinsurance contracts. See, e.g., The Am. Ins. Co. v. Am. Re-Ins. Co., 2006 U.S. Dist. LEXIS 95801 (N.D. Cal., Nov. 27, 2006) (tracing the history of the implication of “follow the settlements” and refusing to do so); Employer Reins. Corp. v. Laurier Indem. Co., 2007 U.S. Dist. LEXIS 45670 (M.D. Fla., June 25, 2007) (absence of “follow the settlements” clause does not create ambiguity permitting parol evidence regarding custom and usage).

C. Avoiding “Following the Settlements” of the Cedent “Follow the settlements” provisions generally do not apply in the following

instances: 1. Fraud; 2. Bad Faith, including “manifest manipulation” of allocations and improper

claims handling requiring at least gross negligence or recklessness; 3. Ex gratia payments; and 4. Differences of scope between the underlying insurance and the reinsurance

coverage, i.e., it is not “back to back.” The agreement’s “governing law” clause can have a significant impact on this issue.

D. Allocation

“Allocation” is the assignment of losses by an insurer to particular policy periods, categories of losses and/or numbers of occurrences. The most oft-cited decision applying “follow the settlements” to an underlying carrier’s allocations is Commercial Union Ins. Co. v. Seven Provinces Ins. Co., Ltd., 9 F.Supp. 2d 49 (D. Mass. 1998) aff’d 217 F.3d 33 (1st Cir. 2000) (“follow the settlements” requires reinsurer to follow its reinsured’s good faith and reasonable allocation of settlement dollars between different policies and sites). The court noted that the reinsurer “attempt[ed] to avoid the effect of the ‘follow the settlements’ doctrine by arguing that what it is challenging is the good faith [basis for] the allocation, rather than of the settlement. This is a distinction without a difference. . . .”

Seven Provinces was followed by two cases involving large payments to Owens Corning Fiberglas arising from asbestos liabilities. In North River Ins. Co. v. ACE Am. Reins. Co., 2002 U.S. Dist. LEXIS 5536 (S.D.N.Y. Mar. 29, 2002) aff’d in part, vacated

in part and remanded by 361 F.3d 134 (2d Cir. 2004) (reinsurers not allowed to second-guess allocations among policies and layers). Similarly, in Travelers Cas. & Sur. Co. v. Gerling Global Reins. Corp. of Am., 285 F.Supp. 2d 200 (D. Conn. 2003) rev’d 419 F.3d 181 (2nd Cir. 2005), the court also held that the reinsurer was obligated to accept and abide by the reinsured’s underlying determination as to the number of occurrences even though the number was not determined as part of its settlement with the underlying insured.

E. Treatment of Allocations under Facultative vs. Treaty Reinsurance

Facultative reinsurance is often comprised of only a short, standardized form with coverage terms following the underlying policy. In such context a Cedent’s allocations generally must be followed if they are reasonable, made in good faith, and the coverage is arguably within the policy. Conversely, treaty reinsurance usually involves a detailed contract with its own coverage terms pertaining to numerous and varied underlying policies, and the treaty’s terms often govern whether the allocation must be followed.

1. Facultative Reinsurance

Some courts reviewing facultative reinsurance contracts have created a high standard for a reinsurer to challenge a cedent’s settlement allocation. See, e.g., National Union Fire Ins. Co. v. Am. Reins. Co., 441 F.Supp. 2d 646 (S.D.N.Y. 2006) (indifference to proper allocation does not rise to necessary showing of “extraordinary bad faith”); Suter v. Gen. Acc. Ins. Co., 2006 U.S. Dist. LEXIS 51853 (D.N.J. July 17, 2006) vacated by stipulation in Goldman v. General Acc. Ins. Co., 2007 U.S. Dist. LEXIS 70406 (D.N.J. May 24, 2007) (bad faith in this context must amount to showing of gross negligence, recklessness or that settlement was not even arguably within the scope of reinsurance coverage).

The decision of the court in Allstate Ins. Co. v. Am. Home Assurance Co., 837

N.Y.S. 2d 138 (N.Y. App. Div. 2007) was far more favorable to reinsurers, who were not required by the court to follow reinsurance loss allocations that were unreasonable. The court held that although precedents have unequivocally held post-settlement allocations are binding even in the face of “an inconsistency between that allocation and the [Reinsured’s] pre-settlement assessments of risk,” such doctrine applies only “as long as the allocation meets the typical ‘follow the settlements’ requirements, i.e., is in good faith, reasonable, and within the applicable policies.” In Allstate, unlike North River, supra, the reinsured aggressively asserted the maximum number of occurrences of loss at each site to minimize its pre-settlement allocation of loss with its insured and then completely changed its position and asserted a one-occurrence-per-site allocation in post-settlement allocations with its reinsurer.

2. Treaty Reinsurance

“Follow the Settlements,” as applied to allocations under treaty insurance,

typically relies on analysis of the terms of the treaty.

In Travelers Cas. & Sur. Co. v. Lloyd’s, 760 N.E.2d 319 (N.Y. 2001), the

Supreme Court of New York held: “While a follow the fortunes clause in most reinsurance agreements leaves Reinsurers little room to dispute the Reinsured’s conduct in the case, we agree with the rationale of the . . . Second Circuit that such a clause does not alter the terms or override the language of reinsurance policies.”

The court continued: “To hold that these ‘follow the fortunes’ clauses supplant the definition of ‘disaster and/or casualty’ in the reinsurance treaties and allow Travelers to recover under its single allocation theory would effectively negate the phrase. The practical result of such an application would be that a reinsurance contract interpreted under New York law that contains a ‘follow the fortunes’ clause would bind a Reinsurer to indemnify a Reinsured whenever it paid a claim, regardless of the contractual language defining loss.” Travelers Cas. & Sur. Co. v. Lloyd’s, 760 N.E.2d 319 (N.Y. 2001); see also Hartford Acc. & Indem. Co. v. ACE, 2005 Conn. Super. LEXIS 3576 (Dec. 14, 2005).

F. Recent Developments

- An insurer cannot use a declaratory judgment action to test the application of “follow the settlements” prior to paying a claim. The Tall Tree Ins. Co. v. Munich Reins. Am., Inc., 2008 U.S. Dist. LEXIS 60499 (N.D. Cal. July 29, 2008).

- Commutations and contingent liabilities allocated to a reinsurer based upon actuarial studies are losses covered under the reinsurance treaties. Global Reins. Corp. of Am. v. Argonaut Ins. Co., 2009 U.S. Dist. LEXIS 37460 (S.D.N.Y. March 23, 2009).

- “Follow the fortunes” applies to only reinsurance contracts. Idaho Counties Risk Mgmt Program Underwriters v. Northland Ins. Cos., 205 P.3d 1220 (Idaho 2009).

- Differences in governing law between and among insurance and reinsurance contracts may result in paid claims for which there is no reinsurance despite a “follow the settlements” clause. Wasa v. Lexington [2009] UKL 40 (July 30, 2009).

- “Follow the settlements” cannot be used to expand reinsurance coverage to reimbursements for losses arising from “renewals” of underlying policies beyond the scope of the reinsurance contract (despite risk of such exposure to the underlying carrier). Arrowood Surplus Lines Ins. Co. v. Westport Ins. Corp., Slip Copy, 2010 U.S. Dist. LEXIS 426 (D.Conn., January 6, 2010).

Kenneth Levine, Esquire, Moderator Nelson Levine de Luca & Horst 518 Township Line Rd., Ste 300 Blue Bell, PA 19422 215.358.5170 www.nldhlaw.com Jessica Pardi, Esquire Morris, Manning & Martin, LLP 1600 Atlanta Financial Center, 3343 Peachtree Rd., NE Atlanta, GA 30326-1044 404.504.7662 [email protected] www.mmmlaw.com Ben Gonson, Esquire Nicoletti Gonson Spinner & Owen, LLP 555 Fifth Avenue, 8th Floor New York, NY 10017 (212) 730-7750 www.nicolettilaw.com February 9, 2010

Presented by:Richard Hershman, Senior Managing Director, Leader of Insurance Services, FTI Consulting, Inc., New York

John O’Connor, Senior Vice President, Head of Claims, Endurance Reinsurance of America, New York

Reinsurance Audits –

A Cedent and Reinsurer View

February 9, 2010

Audit “Triggers”

Why are audits conducted?

2

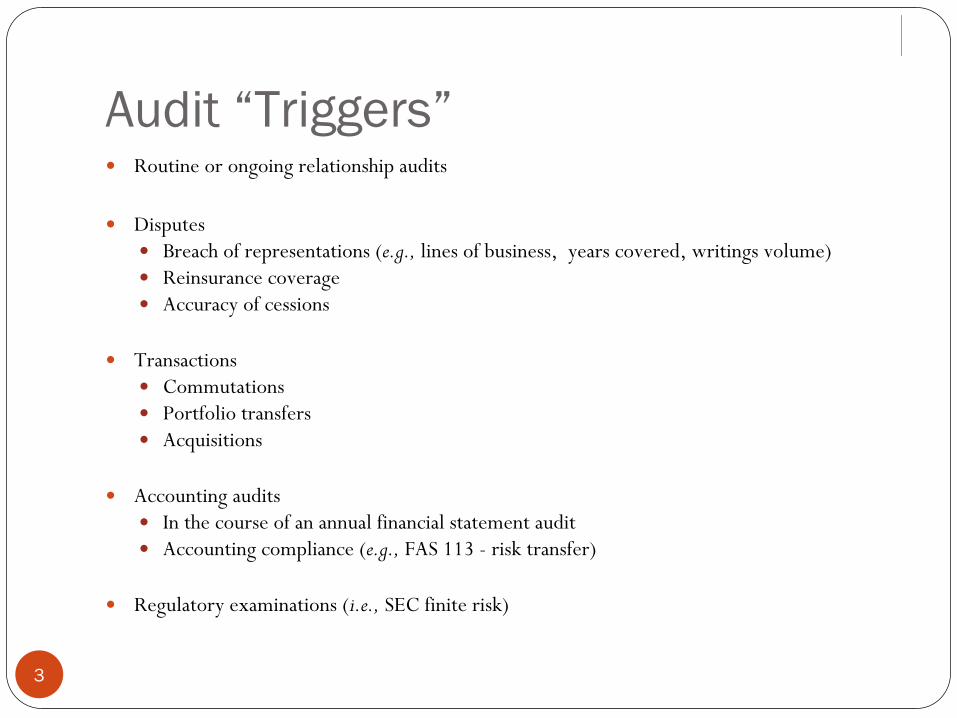

Audit “Triggers”

3

Routine or ongoing relationship audits

Disputes

Breach of representations (e.g., lines of business, years covered, writings volume)

Reinsurance coverage

Accuracy of cessions

Transactions

Commutations

Portfolio transfers

Acquisitions

Accounting audits

In the course of an annual financial statement audit

Accounting compliance (e.g., FAS 113 -

risk transfer)

Regulatory examinations (i.e., SEC finite risk)

Parties Involved in an Audit

4

What parties/entities are involved in an audit?

Parties Involved in an Audit

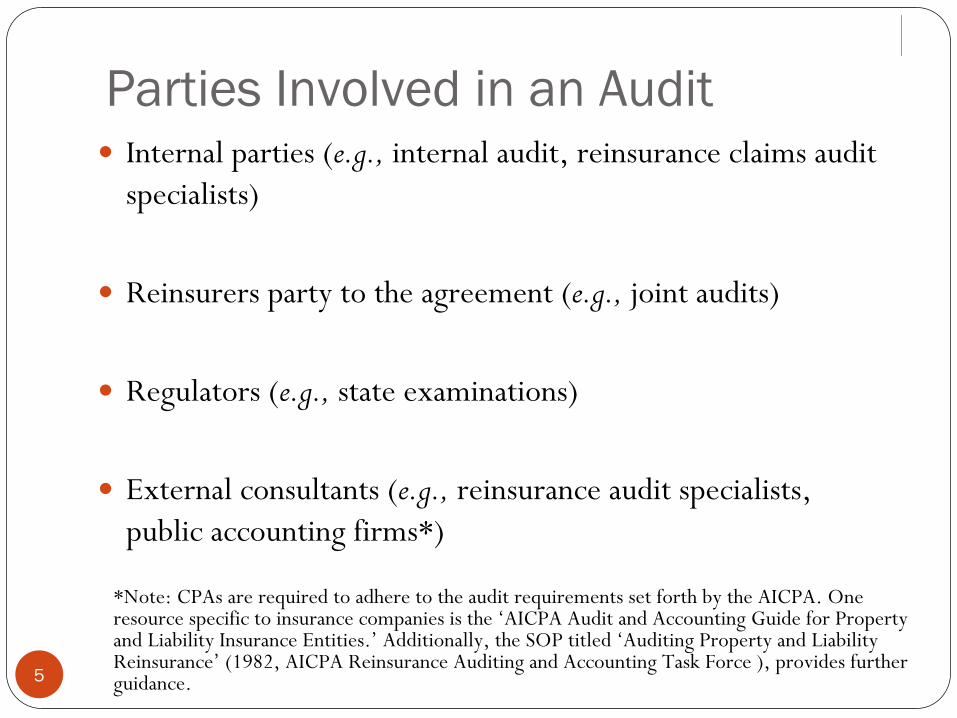

5

Internal parties (e.g., internal audit, reinsurance claims audit specialists)

Reinsurers party to the agreement (e.g., joint audits)

Regulators (e.g., state examinations)

External consultants (e.g., reinsurance audit specialists, public accounting firms*)

*Note: CPAs are required to adhere to the audit requirements set

forth by the AICPA. One resource specific to insurance companies is the ‘AICPA Audit and Accounting Guide for Property and Liability Insurance Entities.’

Additionally, the SOP titled ‘Auditing Property and Liability Reinsurance’

(1982, AICPA Reinsurance Auditing and Accounting Task Force ), provides further guidance.

Audit Areas

6

What are the different types of audits?

Audit Areas

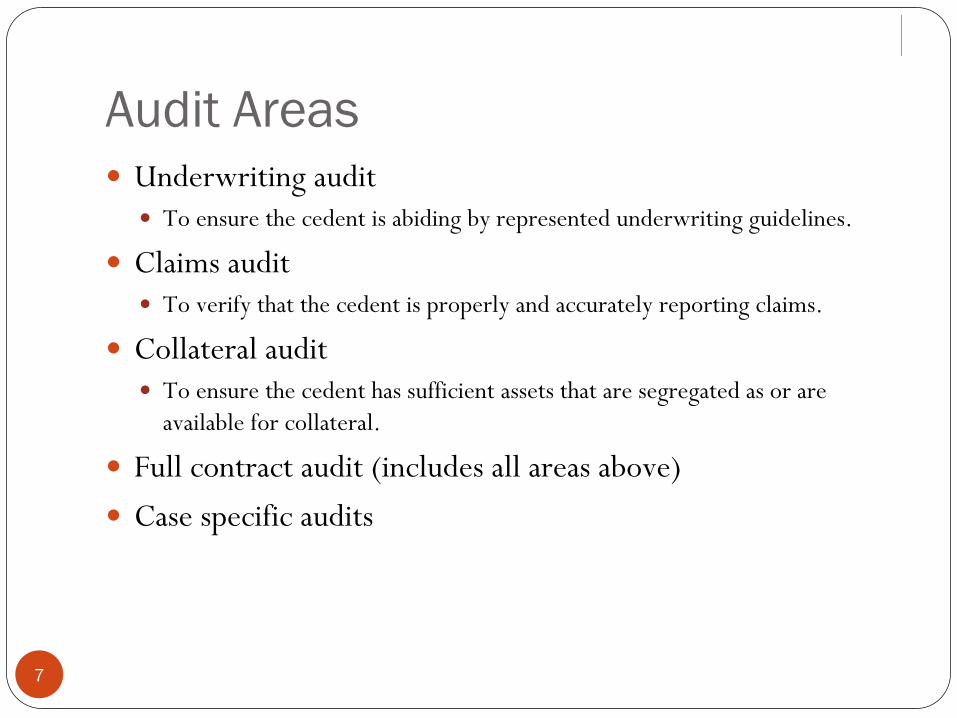

7

Underwriting audit

To ensure the cedent is abiding by represented underwriting guidelines.

Claims audit

To verify that the cedent is properly and accurately reporting claims.

Collateral audit

To ensure the cedent has sufficient assets that are segregated as or are available for collateral.

Full contract audit (includes all areas above)

Case specific audits

The Access to Records Clause

8

What are common issues related to obtaining access to a cedent’s records?

The Access to Records Clause

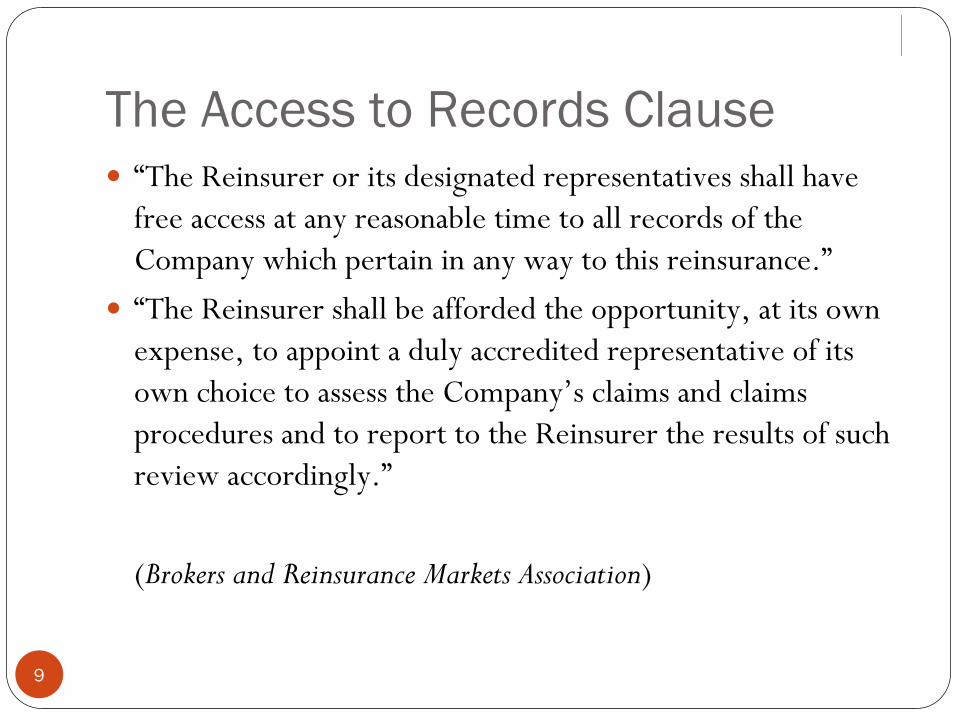

9

“The Reinsurer or its designated representatives shall have free access at any reasonable time to all records of the Company which pertain in any way to this reinsurance.”

“The Reinsurer shall be afforded the opportunity, at its own expense, to appoint a duly accredited representative of its own choice to assess the Company’s claims and claims procedures and to report to the Reinsurer the results of such review accordingly.”

(Brokers and Reinsurance Markets Association)

The Access to Records Clause

10

Purpose:

To identify unreported losses and verify the accuracy of the cedent’s reserves.

To ensure that the cedent is ceding losses and calculating reinsurance premium in accordance with the reinsurance agreement.

To assess the cedent’s practices and competence in terms of underwriting, claims handling and reporting.

The Access to Records Clause

11

This clause is one of the most important contract rights the reinsurer has in a ceding agreement.

Industry debate is ongoing over what level of access reinsurer should have to the cedant’s privileged files.

Vague clauses may lead to disagreements between the cedent and reinsurer in the future.

Cedent and reinsurer should work to set detailed terms within the contract to avoid future disputes.

Also may consider including a provision for an independent third party to make all decisions if the parties disagree.

Focus Point: The Claims Audit Process

12

A walk-through of the claims audit process and components.

Claims Audits -

Overview

13

A significant portion of the Claims Department’s time is spent conducting on-site audits of potential or existing clients. Claims audits support underwriting, actuarial and corporate goals through the meaningful review and analysis of ceding company claim operations and files. In conjunction with audits performed

by the Underwriting and Actuarial Departments, the claims audit enables the Company to evaluate our exposures in a more complete manner.

Claims Audits -

Overview

14

Proper evaluation of reported claims and the validity of their reported reserves is crucial to the continued success of the reinsurer. Identifying potential unreported claims exposures and establishing additional case reserves (ACR’s), on both reported and unreported claims if necessary, is fundamental to quality claim management. Proper auditing provides numerous insights into the claims-related risks that might be present under a reinsurance agreement. Claim audits continue to be a key component in the underwriting decision process.

Audit Protocol

15

Audits are typically initiated in three ways:

Directly from the underwriter

Broker –

Notification of a pre-scheduled group audit of the reinsurers