Embed Size (px)

Citation preview

page 2

page 2

1. Executive Summary

VSAT penetration of the maritime and offshore markets has continued unabated since our last report, despite trying economic conditions:

At the end of 2011 there were almost 12,300 vessels of all types with a stabilised VSAT service with the five year compound annual growth rate running at 19 per cent.

Annually, the number of new vessels has grown by more than 21 per cent for the past two years.

Revenue growth has also been impressive at more than 9 per cent in 2010 and 2011 and is now close to $1 billion, despite the downward pressure on service rates. This has been largely due to increased demand for bandwidth.

Crew welfare continues to consume the largest proportion of any VSAT connection although purchase decisions are now primarily driven by the need to support corporate and operational applications.

COMSYS believes that the maritime VSAT market continues to hold huge opportunities at all levels and our most likely forecast suggests that the number of vessels in service will double by 2016 and annual revenues will exceed $1.2 billion.

iDirect has continued to lead, both in terms of technological innovation and market share. The company has been the first to introduce many key features that have become de facto standards for maritime VSAT operators.

iDirect systems currently account for almost half of all VSATs installed in the marine environment – shipping and offshore services – and at an installation rate more than twice any other vendor.

Of the 20 largest maritime VSAT service providers by revenue, 70 per cent use iDirect’s technology and these companies lead the way in almost all of the major segments. All of the top five operators, as well as seven of the top 10, and 13 of the top 20 use iDirect’s system as their primary, if not sole, platform.

Higher data rates are not only maintaining revenue growth, they are pushing VSAT vendors to develop and introduce new product models able to support the services that customers are demanding. iDirect’s new X7 modem significantly raises the performance of its Evolution system and now threatens even SCPC as the solution of choice for bandwidth intense applications.

New satellite deployments – Global Xpress from Inmarsat and Intelsat EpicNG in particular – promise enhanced service, higher speeds and lower costs. In both cases iDirect is the chosen as strategic ground infrastructure partner for these solutions and, in the case of Inmarsat’s Global Xpress system, it is the exclusive VSAT platform supplier.

$400

$500

$600

$700

$800

$900

$1,000

2,000

4,000

6,000

8,000

10,000

12,000

14,000

06 07 08 09 10 11

Mar

itim

e V

SAT

Re

ven

ues

Ves

sels

wit

h V

SAT

page 3

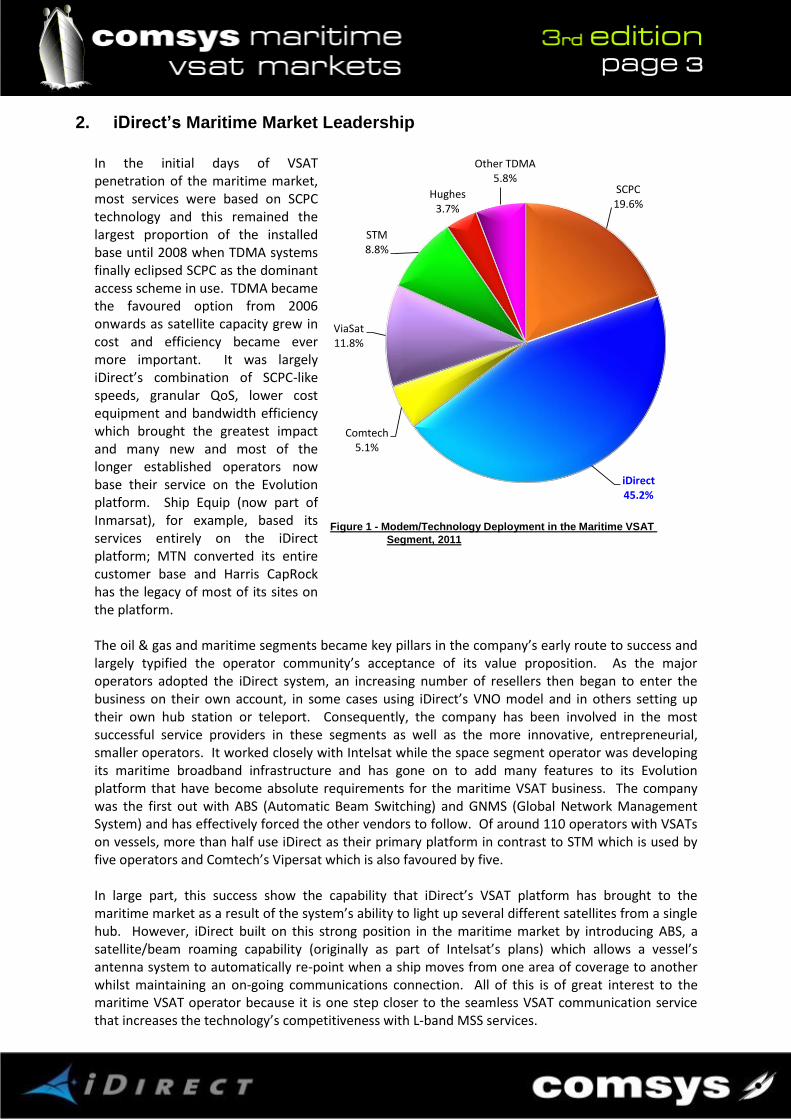

2. iDirect’s Maritime Market Leadership

In the initial days of VSAT penetration of the maritime market, most services were based on SCPC technology and this remained the largest proportion of the installed base until 2008 when TDMA systems finally eclipsed SCPC as the dominant access scheme in use. TDMA became the favoured option from 2006 onwards as satellite capacity grew in cost and efficiency became ever more important. It was largely iDirect’s combination of SCPC-like speeds, granular QoS, lower cost equipment and bandwidth efficiency which brought the greatest impact and many new and most of the longer established operators now base their service on the Evolution platform. Ship Equip (now part of Inmarsat), for example, based its services entirely on the iDirect platform; MTN converted its entire customer base and Harris CapRock has the legacy of most of its sites on the platform. The oil & gas and maritime segments became key pillars in the company’s early route to success and largely typified the operator community’s acceptance of its value proposition. As the major operators adopted the iDirect system, an increasing number of resellers then began to enter the business on their own account, in some cases using iDirect’s VNO model and in others setting up their own hub station or teleport. Consequently, the company has been involved in the most successful service providers in these segments as well as the more innovative, entrepreneurial, smaller operators. It worked closely with Intelsat while the space segment operator was developing its maritime broadband infrastructure and has gone on to add many features to its Evolution platform that have become absolute requirements for the maritime VSAT business. The company was the first out with ABS (Automatic Beam Switching) and GNMS (Global Network Management System) and has effectively forced the other vendors to follow. Of around 110 operators with VSATs on vessels, more than half use iDirect as their primary platform in contrast to STM which is used by five operators and Comtech’s Vipersat which is also favoured by five. In large part, this success show the capability that iDirect’s VSAT platform has brought to the maritime market as a result of the system’s ability to light up several different satellites from a single hub. However, iDirect built on this strong position in the maritime market by introducing ABS, a satellite/beam roaming capability (originally as part of Intelsat’s plans) which allows a vessel’s antenna system to automatically re-point when a ship moves from one area of coverage to another whilst maintaining an on-going communications connection. All of this is of great interest to the maritime VSAT operator because it is one step closer to the seamless VSAT communication service that increases the technology’s competitiveness with L-band MSS services.

Figure 1 - Modem/Technology Deployment in the Maritime VSAT

Segment, 2011

SCPC19.6%

iDirect45.2%

Comtech5.1%

ViaSat11.8%

STM8.8%

Hughes3.7%

Other TDMA5.8%

page 4

Today, of the top 20 maritime VSAT operators ranked by revenues, only six do not use iDirect as part of their service and 13 of the top 20 have adopted iDirect’s system as their primary, if not sole, platform. VSAT Platform Market Ranking Segment Specialization

Operator Primary Secondary Revenues Vessels Primary Secondary

MTN 1 5 Cruise Yachts

Harris CapRock SCPC 2 4 O&G Rigs Commercial

Vizada SCPC 3 3 O&G Maritime Commercial

Inmarsat 4 2 Commercial O&G Maritime

RigNet SCPC 5 7 O&G Rigs O&G Maritime

KVH ViaSat 6 1 Commercial Leisure

NSSL STM 7 6 Commercial Military

Orange 8 9 Commercial O&G Maritime

Elektrikom Comtech 9 8 Commercial Government

DTS 10 10 O&G Maritime O&G Rigs

Eutelsat ViaSat 11 15 Commercial Leisure

STMI STM 12 11 Commercial O&G Maritime

Telespazio SCPC Hughes 13 26 O&G Rigs Commercial

SpeedCast 14 12 Commercial Leisure

Globecomm/Mach6 Comtech 15 13 Commercial Fishing

Radio Holland/Imtech 16 14 Commercial Mega-Yachts

OmniAccess 17 33 Mega-Yachts Cruise

Telemar STM 18 16 Commercial Government

SingTel 19 20 Commercial O&G Rigs

ITC Global SCPC 20 34 O&G Rigs Commercial

Table 1 - Ranked Operator VSAT Platform Choice

page 5

3. Market Information

Industry Drivers & Trends

On the face of it little has changed in the maritime VSAT industry over the past two years – despite the economic downturn and tough conditions in the commercial maritime market customers have continued to adopt VSAT solutions over the traditional MSS products. The satellite industry generally, and VSAT technology more specifically, has brought incremental changes, but the services sold in 2012 appear little different than those we reported on in 2010. However, underneath this calm and gently progressing surface the reality is very different:

Stabilised antenna products, once the preserve of just a few companies and an area of angst for almost all operators frustrated by the lack of viable alternatives to Sea Tel, have seen a plethora of new platforms from a variety of ambitious and aggressive manufacturers.

Service providers in the oil & gas and maritime segments have seen huge consolidation – at least huge consolidation of the huge companies – at great valuations. From a point when the largest and most profitable operators would be almost unknown outside of the satcoms industry, the big consolidators are well-known giants – Harris, EADS, Inmarsat.

Marine system suppliers, most of which are well-known within the maritime industry, have begun to enter the market. Furuno, Radio Holland (Imtec) and InterSchalt all now have a stake in the maritime communications market in one way or another.

Satellite capacity, for so long one of the most reliable areas of staid conservatism, noted as a business of careful steps and incremental change has blossomed with new initiatives.

Sales channels at all levels face unprecedented change. Whatever the title – value added reseller, distribution partner, LESO, Inmarsat Service Provider (ISP) or VSAT operator – some major decisions now feature heavily on most companies’ horizon. ISPs have to face the possibility of a valueless business a few years from now, VSAT operators have to consider whether tens of millions in infrastructure investment will be redundant and everyone has to decide whether Ka-band is the ultimate future, if value added services will shift to the control of the satellite system provider and maritime service will simply become just one more commoditised service distinguished by whoever is prepared to live with the lowest margins.

To say that the maritime communications industry stands on the brink of a major upheaval, a tipping point in its development, is not an exaggeration. And, as is always the case with the satellite industry which has to place big upfront investment bets, the dice have been rolled. There will be winners and there will be losers. Finally, it should also be noted that this will have a major impact for the maritime industry itself – like it or not, vessel owners are about to be dragged wholesale into the information age. Satellite capacity has become a big issue in the market. From a period a few years ago when satellite system operators questioned the viability of ocean coverage and most of the beams in use offered only spill-over coverage from footprints designed for land applications, SES, Telesat and Intelsat have found that specific maritime capacity designed into a spacecraft has sold robustly and at good prices. iDirect’s Virtual Network Operator (VNO) innovation, which allowed operators to tie multiple uplinks from one or more hubs using often diverse satellite beams into a seamless global network undoubtedly helped enable the spread of maritime VSAT services. Through NewWave Broadband, Ship Equip constructed quite comprehensive coverage through a network of VNO arrangements with SES, Intelsat, Arqiva and other teleport operators which positioned their facilities as hosts, or HNOs. Many other VSAT operators followed on with this same model, including MTN, Harris CapRock and

page 6

Marlink/Astrium Services, although all of these companies mix VNOs supported from third party facilities with hubs at their own teleports. Other operators, often coming from land services backgrounds, have also built networks based on VNO platforms hosted in different regions. These include some of the fastest growing operators including SpeedCast, Elektrikom, Mach6/Globecomm, ION and ITC Global. The net result is widespread coverage of the major shipping routes and coastal zones proving to be a very attractive way for new resellers to enter the market, such as Imtech/Radio Holland which recently signed up with ITC Global.

Satellite System Innovations

During the first part of 2010 news leaked out that Inmarsat was contemplating the possibility of launching a new generation of spacecraft that would provide Ka-band coverage for the maritime market. The company officially announced its $1.2 billion investment in three Inmarsat-5 Ka-band satellites and the associated ground infrastructure in August 2010 to support a new service named Global Xpress. Based on the launch schedule with the first satellites being placed in orbit in 2013, Global Xpress is expected to come into full operation towards the end of 2014. Our view of the system was (and is) extremely positive. The Ka/L-band hybrid approach leapfrogs existing capabilities and leverages Inmarsat’s key L-band spectrum. In theory the service would have the critical attributes of access to large amounts of bandwidth as well as almost bullet-proof reliability. The difficulty of obtaining frequency assignments for Ku or C-band is a huge obstacle for new operators, so Ka-band has emerged as the new frontier for the satellite industry and for Inmarsat to use it in a future system makes a lot of sense. Inmarsat then went on to make a series of (in our opinion) smart choices – selecting the next generation iDirect platform for its ground segment and Cobham’s Sea Tel subsidiary as its primary provider of antennas. The iDirect modem, known as the “core module” for Global Xpress, will essentially be the same as a standard next generation iDirect modem, but with the addition of a second demodulator to facilitate beam-switching. Our judgement was that these were smart decisions because they indicated that Inmarsat planned to take an inclusive approach to marketing the service, possibly allowing maritime VSAT operators already running an iDirect platform to roam in and out of the Global Xpress system. This, we believed, would attract operators to the system and allow them to gradually migrate their services to the platform as they gained confidence in the system and wrote down the investment in their existing infrastructure. We also believed that this strategy would help alleviate the potential congestion in the system over some of the high traffic routes in areas such as the North Atlantic, North Sea, Mediterranean and Caribbean. However, Inmarsat took a different direction based on the view that the Global Xpress service would be so compelling that it could be a closed platform – effectively giving independent maritime VSAT service providers no option other than to sign up to resell the service. Inmarsat’s stance initially was uncompromising, but as of mid-2012 there were indications that some of the less acceptable elements of its value proposition were likely to be modified to allow some greater flexibility and, with iDirect’s renowned platform flexibility and investment in advanced network management systems, the option to work with an open architecture will always be available to Inmarsat. By contrast, Intelsat has been working to develop a stronger presence in the maritime segment for a number of years. The company has focused on a 2.4 metre global C-band solution alongside a regional Ku-band service which makes use of smaller antennas. These offerings are constructed on top of Intelsat’s global iDirect HNO platform that now comprises 37 Direct hubs with access to 42 satellites. In total we believe that Intelsat’s maritime VNOs now support more than 500 vessels on the service. However, the company had also been working on its wider mobility strategy – a series of tailored Ku-band beams designed to support all mobility applications, but with a particular emphasis

page 7

on the maritime market. Intelsat’s plan, announced in 2011, was to consolidate supply and strategically position the company with an integrated series of beams covering the major shipping routes with optimised Ku-band payloads on seven satellites launched between 2011 and 2013. This programme is now firmly underway, but rumours about a new satellite initiative from Intelsat had been circulating around some parts of the industry for some time and in mid-2012 the company finally announced plans for two EpicNG spacecraft. If Intelsat is able to deliver on its promises, EpicNG could be a game changer. In essence, Intelsat plans to initially launch two satellites supporting a series of targeted, high powered Ku and C-band spot beams designed to support a range of applications, of which one is maritime. The Intelsat EpicNG spacecraft will allow for very small antennas to be deployed in an open architecture – effectively an operator can use any VSAT system from any hub located in the footprint – with transparent switching on the spacecraft, carrier-by-carrier between different beams and even in different frequencies. The final kicker to the system is the bandwidth supported. Based on an assumed aeronautical antenna size of 40 centimetres, each satellite should be able to support at least 25 Gbps of capacity and, with larger antennas, as much as 60 Gbps, perhaps more. The two EpicNG spacecraft promise smaller antennas, lower powered RF, high data rates and all at a lower cost per bit. The coverage provided by the EpicNG satellites needs also to be considered overlaid with the company’s mobility beam coverage. Together, Intelsat can claim to have near global coverage, perhaps not too dissimilar to Inmarsat’s Global Xpress, but with the differentiating factor of capacity loaded in high traffic areas.

VSAT Operators

The maritime VSAT market is led by just a few key operators. These companies divide broadly into two – those that have built a service offering around the offshore oil & gas market and those that are entirely focused on ships. The former – Harris CapRock being the best example – branched out into vessels other than rigs as it supplied service to the oil & gas support structure. Dive support, seismic survey, supply ships and shuttle tankers are all examples of types of seagoing vessels that the O&G communications operators class as oil & gas. There are, however, some companies which have offshore installations, but few vessels of this type – the best example being RigNet, although the OSV market is now a target for the company’s future expansion.

Those companies that specialise in the pure maritime segment – Vizada, MTN, Inmarsat and NSSL for example – have generally done so for many years and have built quite sizeable businesses that cross over with the O&G suppliers. They have picked up maritime customers from the O&G industry and, in some instances, attempted to diversify into serving rigs. At the same time, most of the largest O&G VSAT operators have begun to diversify into the maritime segment. The intense specialisation

Figure 2 - Oil & Gas and Maritime Stabilised Antenna VSAT Service

Provider Market Share, Vessels in Service 2011

KVH12.3%

Inmarsat10.2%

Vizada10.0%

Harris CapRock

7.7%

MTN6.2%

NSSL 5.7%

Elektrikom3.3%

Rignet2.9%

Orange2.5%

DTS2.5%

STMI2.5%

Speedcast2.2%

Others31.9%

iDirectOperators

page 8

that operators reserved for the maritime market meant that for many years sales were strong, but relatively low in volume. Revenues and margins were also premium and contributed to a strong performance by almost all of the companies associated with stabilised VSAT services. As a highly specialised segment of the technology, barriers to entry into the High End Commercial markets were considered significant for other operators because the various niches are both demanding and require a great deal of inside knowledge to be successful. This was further reinforced by the additional demands placed by customers in the highest value segments. All stabilised antenna VSAT services have shown robust long term revenue growth. This had traditionally run at rates of between 15-20 per cent per year up to 2007. The economic crisis of 2008 saw the rate fall to 10 per cent and this remained true for 2009. However, the reasons behind the slowdown were not all related to the economy and were a great deal more complex than might first appear. As previously mentioned, the customer base has broadened quite considerably and neither average prices nor margins are as high as they were in the late 1990s and early 2000s. Most recently, there have been two opposing trends with growth in installations based on more economical services using sub-metre antennas tending to push down the lowest prices available in the market and drag down those above them to some degree whilst the inexorable demand for bandwidth has brought growth in many segments, but disproportionately to those who focus on the High-End Commercial customers. The nature of the operator market has also changed as consolidation has taken hold – two years ago four of the top twelve revenue earners were primarily focused on the oil & gas industry. Today it is three, arguably only two, primarily due to the acquisition by Harris of CapRock and Schlumberger’s GCS unit. As the segment has become saturated and revenue growth became harder many of the major players progressively moved towards the broader maritime industry in their search for growth in verticals they know and have some expertise in. Harris CapRock has since begun to make more of an impact on the wider maritime business and even RigNet, which has been very adamant about its desire to maintain its oil & gas focus, has been more active in the O&G maritime segments. However, both companies reported strong growth in their energy related businesses, with rates substantially exceeding 10 per cent in 2011. We believe that a major driver behind this growth was increased bandwidth consumption rather than new sites. Considering the fact that depressed shipping rates have resulted in a general tightening of belts and restrictions on capital expenditure by fleet operators, the continued growth of the maritime VSAT market is impressive. Additionally, it should also be noted that Inmarsat’s aggressive promotion of its Fleet Broadband product has also meant that many potential customers have chosen FBB as a broadband replacement for their lower rate Inmarsat products rather than jumping to VSAT. With typical usage rates by ships with VSAT running at between 20 and 50GB per month, we believe that the limited capacity on offer from FBB means that these are postponed, not lost, opportunities. However, the VSAT operators have responded by opening up new areas using smaller, lower cost antennas whilst, at the same time, there have been more antenna choices available to them, both in the form of a greater number of qualified suppliers and more variation in product ranges.

page 9

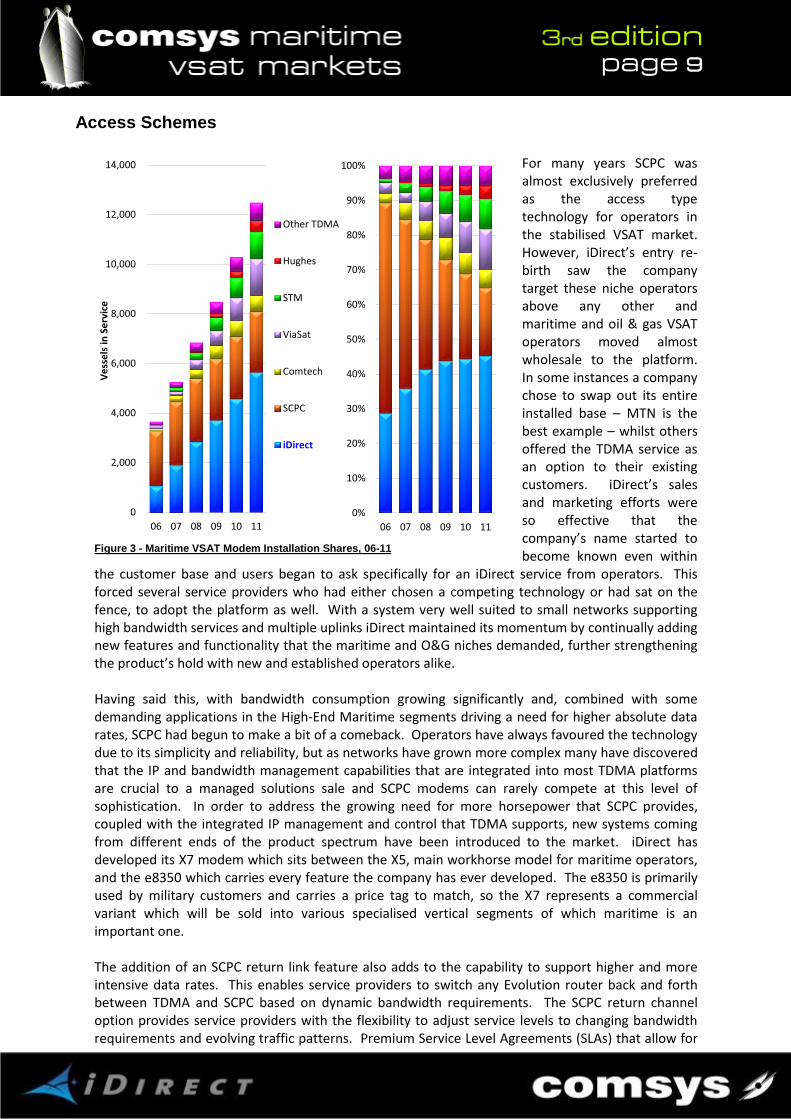

Access Schemes

For many years SCPC was almost exclusively preferred as the access type technology for operators in the stabilised VSAT market. However, iDirect’s entry re-birth saw the company target these niche operators above any other and maritime and oil & gas VSAT operators moved almost wholesale to the platform. In some instances a company chose to swap out its entire installed base – MTN is the best example – whilst others offered the TDMA service as an option to their existing customers. iDirect’s sales and marketing efforts were so effective that the company’s name started to become known even within

the customer base and users began to ask specifically for an iDirect service from operators. This forced several service providers who had either chosen a competing technology or had sat on the fence, to adopt the platform as well. With a system very well suited to small networks supporting high bandwidth services and multiple uplinks iDirect maintained its momentum by continually adding new features and functionality that the maritime and O&G niches demanded, further strengthening the product’s hold with new and established operators alike. Having said this, with bandwidth consumption growing significantly and, combined with some demanding applications in the High-End Maritime segments driving a need for higher absolute data rates, SCPC had begun to make a bit of a comeback. Operators have always favoured the technology due to its simplicity and reliability, but as networks have grown more complex many have discovered that the IP and bandwidth management capabilities that are integrated into most TDMA platforms are crucial to a managed solutions sale and SCPC modems can rarely compete at this level of sophistication. In order to address the growing need for more horsepower that SCPC provides, coupled with the integrated IP management and control that TDMA supports, new systems coming from different ends of the product spectrum have been introduced to the market. iDirect has developed its X7 modem which sits between the X5, main workhorse model for maritime operators, and the e8350 which carries every feature the company has ever developed. The e8350 is primarily used by military customers and carries a price tag to match, so the X7 represents a commercial variant which will be sold into various specialised vertical segments of which maritime is an important one. The addition of an SCPC return link feature also adds to the capability to support higher and more intensive data rates. This enables service providers to switch any Evolution router back and forth between TDMA and SCPC based on dynamic bandwidth requirements. The SCPC return channel option provides service providers with the flexibility to adjust service levels to changing bandwidth requirements and evolving traffic patterns. Premium Service Level Agreements (SLAs) that allow for

Figure 3 - Maritime VSAT Modem Installation Shares, 06-11

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

06 07 08 09 10 11

Ve

sse

ls in

Se

rvic

e

Other TDMA

Hughes

STM

ViaSat

Comtech

SCPC

iDirect

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

06 07 08 09 10 11

page 10

temporary bursts in traffic support applications like file transfer, data back-up and HD video, as well as seasonal bandwidth requirements common to maritime, oil and gas, and other markets. In addition, when customer sites grow larger, service providers can up-sell their customers to a dedicated SCPC link. iDirect believes that this allows operators economically to grow networks for cellular backhaul, Internet access and other services where subscribers tend to be limited at launch and then expand steadily. By integrating SCPC onto iDirect’s shared TDMA platform, service providers can also pool total capacity and distribute it more cost-effectively across their customer base. Untapped SCPC bandwidth can be re-allocated instead of being wasted. And service providers can expand the size of an SCPC link by simply sourcing bandwidth from the overall bandwidth pool without needing to lease new space segment.

The onward march of TDMA systems into the segment can be seen clearly in Figure 4. Prior to 2003 over 80 per cent of all deployments were SCPC versus around one third today. We remarked in our last report that the type of system in use was likely to be a crucial factor in any future consolidation – something that we believed to be inevitable in the light of the extreme fragmentation of the market. We considered that consolidators would be attracted to the easy integration and potential synergies of combining multiple iDirect platforms, but

this would also put pressure on iDirect to ensure that its system and support structures could smoothly facilitate this. The acquisition of CapRock and GCS by Harris, already an iDirect operator; Vizada by EADS Astrium, both operators of the iDirect system; Broadpoint by ITC Global, both operators of iDirect, begins to show the truth behind our remarks. COMSYS continues to believe that the type of system deployed will have a bearing on the attractiveness and valuation of future acquisition opportunities driven by the desire to consolidate that is being driven by several interested private equity firms and the larger integrator/manufacturers, such as EADS and Harris, as they look to build service-based businesses to diversify their revenue streams.

Figure 4 - Access Schemes in Service in the Maritime VSAT Segment, 07-11

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

07 08 09 10 11

Ve

sse

ls in

Se

rvic

e

SCPC

DVB-RCS

DAMA

CDMA

TDMA

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

07 08 09 10 11

page 11

Maritime Market Segmentation

From a handful of very specialised operators, we now track almost 140 service providers all interested or providing some form of VSAT service to the maritime industry. COMSYS analysis indicates there were about 12,300 vessels equipped with VSAT solutions from more than 100 different service providers at the end of 2011. The total as of mid-2012 is believed to be in excess of 13,200. The maritime market is highly fragmented and we have segmented it as follows:

Oil & Gas Rigs and Platforms – service to rigs is highly specialised and very well defined, so we have separated it from ships. Very few new rigs and platforms are constructed each year leaving a relatively static number of addressable locations, but whilst global procurements to leverage purchase power led to general price reductions, an overall increase in bandwidth requirements has, over the past two to three years reversed a slow and slight decline in revenues.

High End Commercial segments – oil & gas offshore service vessels, ferries and cruise lines – have provided the mainstay for VSAT operators for around 20 years. Whilst this area of the market continues to grow, it now only does so at very low rates and price pressure is intense.

Commercial shipping lines account for about 100,000 vessels greater than 100gt in weight (according to Lloyds Register) and most participants in the maritime VSAT market agree that there is an immediately addressable market of around 10,000 ships. In most cases this measure is based on traffic requirements and the capability of supporting a stabilised antenna of 1.2 metres or greater.

Fishing is a very large market, but to date penetration has been relatively small. Much of the demand in the local fishing fleets has been served with voice and limited low-rate data services from the MSS operators including Iridium, Thuraya, ACeS and MSV as well as Inmarsat’s Standard-C services. Vessels that do not wander far from the coast often rely solely on cellular service when in coverage.

Government and Military naval vessels are a difficult segment to understand in terms of their accessibility. The application for the military is usually not tactical, effectively opening the market out to any operator. In most cases, the customer will almost certainly opt for a local provider who is able to land traffic directly in their own country. Many navies also have tactical systems based on custom-designed, very expensive antennas developed by specialist military integrators, but this is not a part of the market that we include in this analysis. There are also government research and support vessels which represent a potential market.

Leisure or the “White Boat” market is of interest to some. The typical large yacht customer rarely requires global coverage – seasonal between the Mediterranean and the Caribbean is usually considered enough to cover the majority of the demand. However, our analysis shows that this segment can be split into three sub-segments that have very different characteristics and that are therefore likely to respond to different value propositions. Smaller stabilised antennas with a diameter of less than one metre have emerged as a key to success in the broader leisure market.

Inland Waterway Vessels are an undefined segment of the market that some small operators are specifically targeting. It is clear that several sub-segments also exist in the Inland Waterways sector – river cruises is a small niche, but one that has grown well and is readily accessible both in terms of demand and ability to serve. Commercial vessels on the other hand, are far more numerous in Europe and North America, but with continually growing GPRS and 3G cellular services, viability of this sub-segment has to be questionable.

page 12

Application Demands

In 2007 and early 2008 as the shipping boom reached its height the overwhelmingly dominant market driver was crew welfare which had moved from being “nice to have” to important or even critical in some instances. Crew recruitment and retention had emerged as a major problem for the fleet operators and broadband service was seen as an effective way to combat the problem. In part, this need for connectivity is driven simply by the fact that we have all grown used to being in contact almost all of the time and ship crews are no different. In some ways, the need for connectivity is even greater as a result of the isolation that a crew member experiences when spending weeks or even months at sea. The economic downturn hit the maritime business hard, and since then priorities have definitely changed within the broad sphere of the shipping fleet market. To place the change in perspective, at the height of the shipping boom in 2007/8 perhaps eight out of ten decisions to implement VSAT on board ship were driven primarily by crew welfare requirements. Today, the proportion is probably nearer to half, so the change has been significant. Having said this, there is a wrinkle to the story because whilst operational and corporate applications seem to be the primary reasons behind buying decisions, crew usage accounts for the greatest proportion of the bandwidth consumption and by some margin. Vessel owners and operators inform us that only around 5 to 10 per cent of bandwidth is ever used for corporate applications in the commercial segment. This rises to 60 per cent or more in the High-End Commercial and specialised Oil & Gas segments, but crew welfare use remains very significant. The growth of other application demands has come from three main sources which we classify as administrative, operational and regulatory. These applications have all been talked about for many years as areas of business process improvement, but most usually need a persistent, cost-effective broadband connection. It is our view – and the view of many of the operators – that, as broadband VSAT services take hold in the maritime market, the major fleet operators will increasingly find themselves forced into implementing a broadband solution simply as a defensive measure, as their early-adopting competitors gain a substantial advantage in the search for new crews and maintenance of their existing staff. The combination of software, implementation, integration and a new broadband satellite system, which is often required for full functionality of a management system, with its associated service charges is believed to have been one of the major inhibitors of the market for management and ERP systems in the marine industry over the past few years. However, this state of affairs has begun to change over the past two years as true broadband service becomes more widespread. There is growing evidence that ship owners are making greater use of the capability by taking the plunge and implementing more advanced ship management systems – all applications that their proponents claim will save a ship-owner money with fuel savings, quicker turnaround times and reduced lay-ups for repairs and maintenance amongst other things. Maritime VSAT operators and software system providers consequently believe that the long-expected up-sell opportunity is finally beginning to be seen.

page 13

4. Market Expectations

Over the course of this study COMSYS conducted 175 separate interviews with service providers, equipment manufacturers, satellite operators, resellers and experts in the maritime market. In previous years, we have interviewed many other companies with large stabilised antenna businesses, visited teleports and manufacturing plants and spoken with customers in both the maritime and oil & gas industries. During the research for our 2008 and 2010 reports, where an opinion was given, the view was almost always that a conservative estimate on the number of commercial vessels adopting a stabilised VSAT service by 2015 was most likely to be between 10,000 and 20,000. This generic estimate would include the Fishing and High-End Commercial markets, but not take into account the Military and Leisure segments. The Inland Waterway segment is something of an unknown quantity to us and most others in the industry, but of those companies that expressed their opinion, we do not believe that any would have taken this niche of the market into consideration. Today, with almost 12,500 vessels recorded as having a VSAT onboard, the segments included in these estimates account for just over 9,000. As a consequence, our belief is that the 20,000 estimate is likely to be closer to the final result, especially as Inmarsat’s Global Xpress service takes hold, and this will grow further as operators make use of Intelsat’s EpicNG capacity within their service. Given all this, it is hard to see how iDirect could be in a better position to take advantage of this forecasted growth. Not only is the company the exclusive VSAT platform supplier of Inmarsat’s Global Xpress system, the Evolution platform also forms the basis of Intelsat’s mobility infrastructure. As we have mentioned previously, 14 of the largest maritime VSAT service providers by revenue also use iDirect’s technology and these companies lead the way in almost all of the major segments:

Cruise: MTN and Astrium/Marlink

Oil & Gas: Harris CapRock and RigNet

Ferries: Astrium/Marlink

Commercial: Astrium and Inmarsat

Offshore Supply: DTS and Inmarsat

Fishing: Inmarsat

Mega Yachts: OmniAccess and MTN

River Cruise: OmniAccess MTN and Harris CapRock have already committed themselves to significant contracts with Intelsat’s Epic system, worth in excess of $2 billion, and will almost certainly enjoy a significant market advantage in their chosen segments for the foreseeable future. Others, including RigNet, Astrium, DTS and OmniAccess, have developed deep relationships and defensible market positions within their primary target segments and so look set to maintain their momentum. Inmarsat has a clear objective to convert its existing VSAT customer base to its Global Xpress system when it comes fully online in 2014 and, we believe that it will be very successful in many of the segments where alternative operators are currently building their businesses – fishing, smaller yachts and the wider commercial market. Whilst the future looks like it will be increasingly polarised for many in the industry, with operators having to choose between committing to Intelsat’s EpicNG satellites and leverage their existing infrastructure investment or move to Inmarsat’s Global Xpress reseller model, iDirect is one of the few companies that will benefit regardless of which direction these companies take. We believe that the majority of businesses that choose to sign up with Global Xpress will be existing Inmarsat resellers, bringing further business to the iDirect maritime machine. With the strong financial

page 14

synergies that a common platform brings, as long as iDirect continues to innovate with developments like its Global NMS, Automatic Beam-Switching, Open AMIP standard and, most recently, its X.7 modem, there is likely to be very little resistance from those that use the company’s platform. Our forecasts for this report have to take in to account a much more complex future now we know that Inmarsat will launch their Global Xpress Ka-band system in 2014 and Intelsat will substantially bolster its mobility beam coverage with the EpicNG satellites in 2016. Perhaps the biggest question is just how much these future service platforms might delay a customer’s buying decision over the next two years. Inmarsat’s very aggressive pricing during 2011/12 on its XpressLink “bridge” to Global Xpress has undoubtedly made VSAT service more attractive with lower price points, but also actually scared some customers into deferring a decision lest they commit to a solution that proves to be a long term mistake when the new services arrive. We suspect that a slight depression is the most likely scenario, followed by a two stage release of decisions – first when Global Xpress has proved its capabilities in 2015 and then second when EpicNG capacity begins to come online. Our expectation is that a combination of future service uncertainty and tough economic conditions are likely to restrict new growth in 2013 and 2014 and contribute to a reduction in the net new vessels converted to VSAT. When the new services come online, growth will accelerate and by 2016 our Most Likely forecasts expect to see net new adds at more than twice the level of 2011 bringing the total number of VSATs in service in the maritime market to more than 26,000. This analysis covers all maritime segments, but the main commercial segments account for 68 per cent of annual sales with almost 19,000 vessels in service by 2016. As in previous years, we believe this to be a relatively conservative estimate and our more optimistic scenario sees the entire market grow to around 32,000 vessels by 2016 with the main commercial segments accounting for approximately 22,000 vessels and almost 70 per cent of the market.

Conclusion

For many years, communications at sea effectively meant Inmarsat’s L-band service which grew from its creation in 1979 to serve almost 240,000 maritime installations by the end of 2011. However, Inmarsat faces a huge issue not of its making – use of communications and bandwidth consumption by individuals and businesses has risen dramatically over the past ten years across the globe, so much so that even FSS satellite capacity providers have begun to take dramatic steps to ensure that their businesses will remain relevant in the future. Inmarsat’s limited L-band spectrum is simply not sufficient to cater for the increase in demand, even after the company invested in its advanced spot beam I-4 spacecraft and despite the fact that many maritime fleet operators have tried to keep the lid on demand for communications from their vessels and crew. VSAT services are, without doubt, the future for the maritime communications market. The next few years will, however, be a stormy sea which the successful companies will have to cross. Operators and resellers will have to choose between higher margins from value creation versus faster top line revenue growth based on volume sales; satellite operators will dispute independence over network ownership; antenna manufacturers will need to develop technology differentiators or restructure their product strategies; VSAT system vendors need to find the balance between cost and performance for a small niche market; and, customers will need to educate themselves to the degree that they can make an informed decision as to which service will be the right one for their particular needs. Of one thing they can be sure – there will be plenty of choice.

page 15

5. The COMSYS Maritime VSAT Report

The foundations for this study were laid in 2006 when several companies requested COMSYS to look in more detail at the market for maritime VSATs. We had already established an extensive understanding of the maritime VSAT market, but even with research which was conducted for the VSAT Report, it was clear that a study focused on stabilised services also required a far greater understanding of the maritime and oil & gas markets themselves. Between the end of 2007 and the beginning of 2008 we undertook a great deal of specific research into stabilised antenna VSAT services and subsequently published the 1st Edition of this report in April 2008. The 3rd Edition builds on that knowledge base and is supplemented by our research

during most of 2011 for the 12th Edition of the VSAT Report as well as specific research conducted between the end of 2011 and the first half of 2012. It comprised data from over 170 interviews with current and potential maritime VSAT operators, MSS L-band operators and resellers, stabilised platform manufacturers, VSAT and L-band system manufacturers, industry associations and experts in the maritime industry, several with key expertise in important segments. We would like to take this opportunity to thank all those that shared their experiences and information with us and contributed to the high level of detail we have been able to provide. The full report details the growth of maritime VSAT services, analysing the number of vessels in service and market revenues by operator, region, technology and segment. Almost 120 pages containing 41 tables and 84 charts and figures provide a statistical analysis of the service market by number of vessels in service and revenues, both historically and forecast over the next five years. As always, COMSYS bases its information on primary research and builds from the ground up. The COMSYS Maritime VSAT Report includes:

Current VSAT penetration by operator and maritime segment type by number of vessels and revenues.

Competing technologies to VSAT.

Analysis of the stabilised VSAT antenna manufacturers, production, technology trends, pricing, market shares and revenues.

Size of the maritime market segmented as O&G Rigs & Platforms; High-End Commercial; Mainstream Commercial; Fishing; Leisure; Military & Government; and, Inland Waterways.

Total available and addressable markets for stabilised VSAT services.

Market drivers and inhibitors.

Five year "Most Likely" and "Optimistic" forecasts by number of vessels and revenues by maritime segment.

It considers different stabilised antenna systems, their availability, price points, strengths and weaknesses as well as future development. The total size of the maritime market is assessed and the

Figure 5 - Primary Research Interviews by Type

Operator59.2%

Vendor20.1%

Technology Competitor

4.0%

Maritime Industry

8.6%

O&G Industry

4.6%Reseller3.4%

Total 174 Interviews

page 16

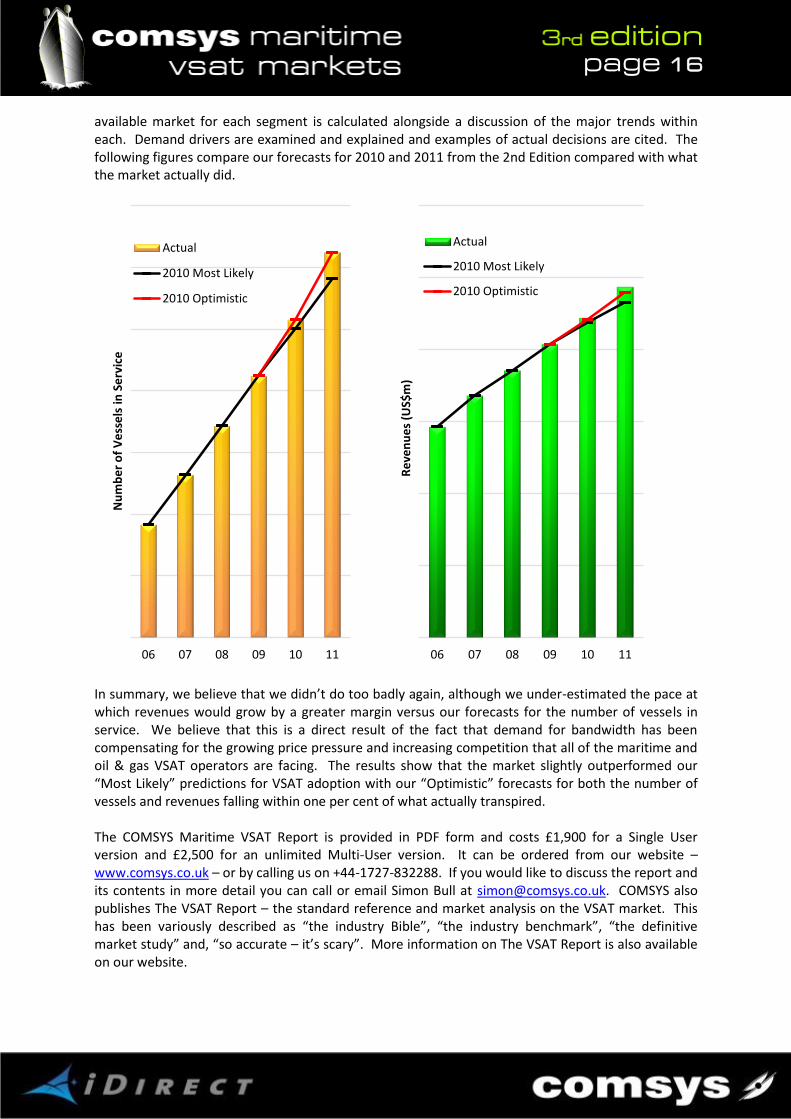

available market for each segment is calculated alongside a discussion of the major trends within each. Demand drivers are examined and explained and examples of actual decisions are cited. The following figures compare our forecasts for 2010 and 2011 from the 2nd Edition compared with what the market actually did.

In summary, we believe that we didn’t do too badly again, although we under-estimated the pace at which revenues would grow by a greater margin versus our forecasts for the number of vessels in service. We believe that this is a direct result of the fact that demand for bandwidth has been compensating for the growing price pressure and increasing competition that all of the maritime and oil & gas VSAT operators are facing. The results show that the market slightly outperformed our “Most Likely” predictions for VSAT adoption with our “Optimistic” forecasts for both the number of vessels and revenues falling within one per cent of what actually transpired. The COMSYS Maritime VSAT Report is provided in PDF form and costs £1,900 for a Single User version and £2,500 for an unlimited Multi-User version. It can be ordered from our website – www.comsys.co.uk – or by calling us on +44-1727-832288. If you would like to discuss the report and its contents in more detail you can call or email Simon Bull at [email protected]. COMSYS also publishes The VSAT Report – the standard reference and market analysis on the VSAT market. This has been variously described as “the industry Bible”, “the industry benchmark”, “the definitive market study” and, “so accurate – it’s scary”. More information on The VSAT Report is also available on our website.

06 07 08 09 10 11

Nu

mb

er

of

Ve

sse

ls in

Se

rvic

e

Actual

2010 Most Likely

2010 Optimistic

06 07 08 09 10 11

Re

ven

ue

s (U

S$m

)

Actual

2010 Most Likely

2010 Optimistic

page 17

About comsys

Communication Systems Limited (comsys) is a specialised telecommunications consultancy company which was founded in 1982. comsys performs a range of consultancy services in many areas of the telecommunications industry, but has concentrated its resources in the field of satellite technology and has developed expertise in business planning, regulatory, financial, competitive and operational analysis. Clients range from users and governments to operators and manufacturers. Over almost 30 years we have visited essentially all manufacturers of VSAT systems and most of the world’s operators of VSAT systems as part of the primary research we do in the industry. comsys is regularly consulted on VSAT industry matters (as well as the satellite communications business in general) by clients both within the satcom industry and outside it (including the financial community, regulators and larger consulting firms). We have also advised clients on present and future markets, new products, service introductions, application platforms and network procurements ranging in size from 50 to 3,000 sites. On the financial side our figures and analysis of the VSAT industry have been extensively used by Wall Street analysts for many years as well as in filings to the SEC and in support of other financial documents and business plans. comsys has been the primary industry advisor or part of advisory teams in the purchases of most of the major satellite-related sales over the past few years, including those of Inmarsat, PanAmSat, Hughes Network Systems and Intelsat. comsys has earned a reputation for objective, empirical analysis and is known in the industry as a primary source of market information. This reputation has been hard-earned by constant monitoring of the world market through visits to businesses in more than 70 countries.

Simon Bull, Senior Consultant, comsys

Simon Bull is a Senior Consultant with COMSYS. He has specialised in the VSAT market since 1985 and advises clients worldwide on all aspects of VSAT systems and satellite services. He is primarily responsible for the multi-client VSAT studies published by COMSYS during the last twenty years, including the company's VSAT Report and Maritime VSAT Report. He also advises clients on the regulatory, strategic and business planning, administrative and operational aspects of satellite communication systems. He has visited hundreds of VSAT companies in more than 70 countries worldwide and is regularly consulted by VSAT manufac-turers, operators and users. He has been actively involved, directly and as part of multi-disciplinary teams, advising clients with respect to acquisitions ranging in size from $5 million to over $1 billion. In 1997, Simon was instrumental in forming the Global VSAT Forum (GVF), an industry organisation which represents over 140 of the leading manufacturers and operators of VSAT systems around the world. He currently co-Chairs the GVF’s Maritime Industry Group.

![iSite Basics & VSAT* Commissioning iDS v6 - Ciberallciberall.net/idirect/3x-evolution-idirect/iSite_Basic_User_Guide[1].pdf · 3 RemoRemote Site te Basic Network Description NetModem](https://img.pdfslide.us/doc/110x75/5d65340688c993b8288b4a2c/isite-basics-vsat-commissioning-ids-v6-1pdf-3-remoremote-site-te-basic.jpg)