Embed Size (px)

Citation preview

Hankou Bank Co., Ltd.

2019 Annual Report

2019 Annual Report of Hankou Bank Co., Ltd.

I

Contents

Chapter I Important Notice................................................................................................................ 1

Chapter II Basic Information..............................................................................................................2

I. Terms and Definitions......................................................................................................................................... 2

II. Company Profile................................................................................................................................................ 2

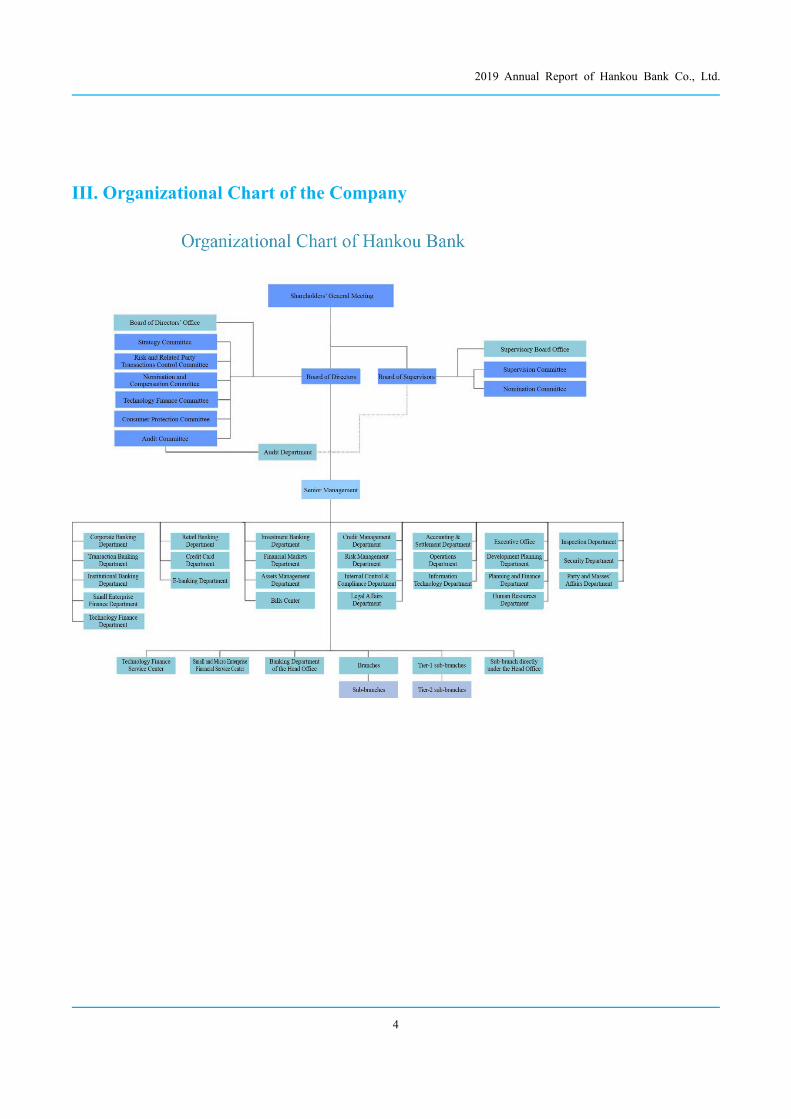

III. Organizational Chart of the Company..............................................................................................................4

Chapter III Summary of Accounting & Business Data.................................................................... 5

I. Major Financial Data for the Reporting Period.................................................................................................. 5

II. Major Accounting Data and Financial Indicators for the Three Years before the End of the Reporting

Period...................................................................................................................................................................... 6

III. Return on Equity and Earnings per Share........................................................................................................ 7

IV. Supplementary Financial Data for the Three Years before the End of the Reporting Period.......................... 8

V. Supplementary Financial Indicators for the Three Years before the End of the Reporting Period...................9

VI. Changes in Shareholder’s Equity during the Reporting Period.....................................................................10

VII. Composition of Capital and Its Changes...................................................................................................... 11

VIII. Liquidity Coverage Ratio at the End of the Period..................................................................................... 12

Chapter IV Report of the Board of Directors..................................................................................14

I. Management Discussion and Analysis..............................................................................................................14

i. Business review during the reporting period............................................................................................ 14

ii. Analysis of financial position and operating results during the reporting period....................................23

iii. Assets and liabilities during the reporting period................................................................................... 29

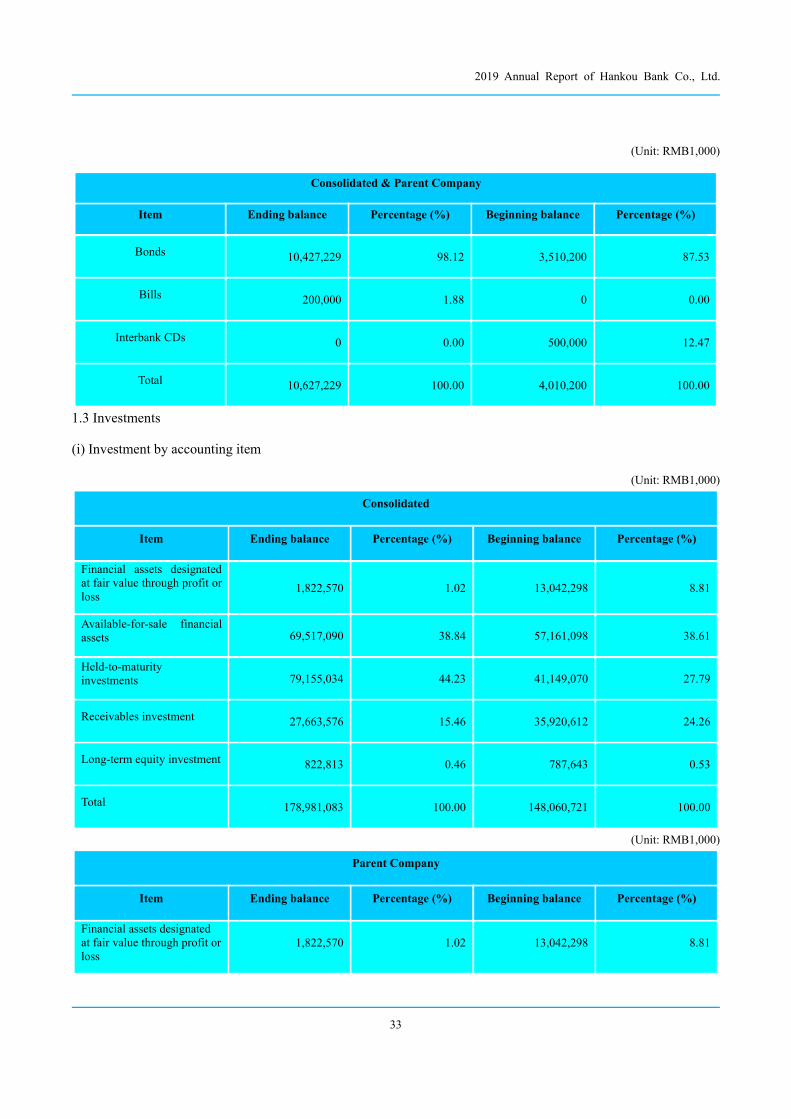

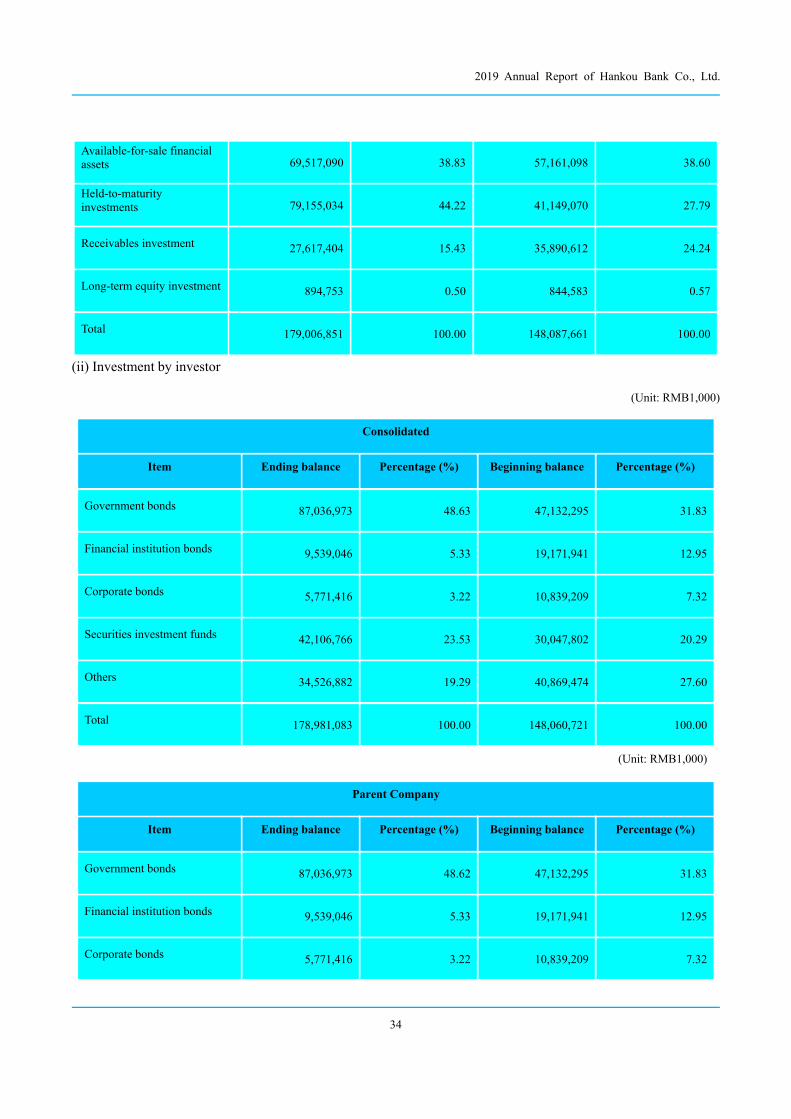

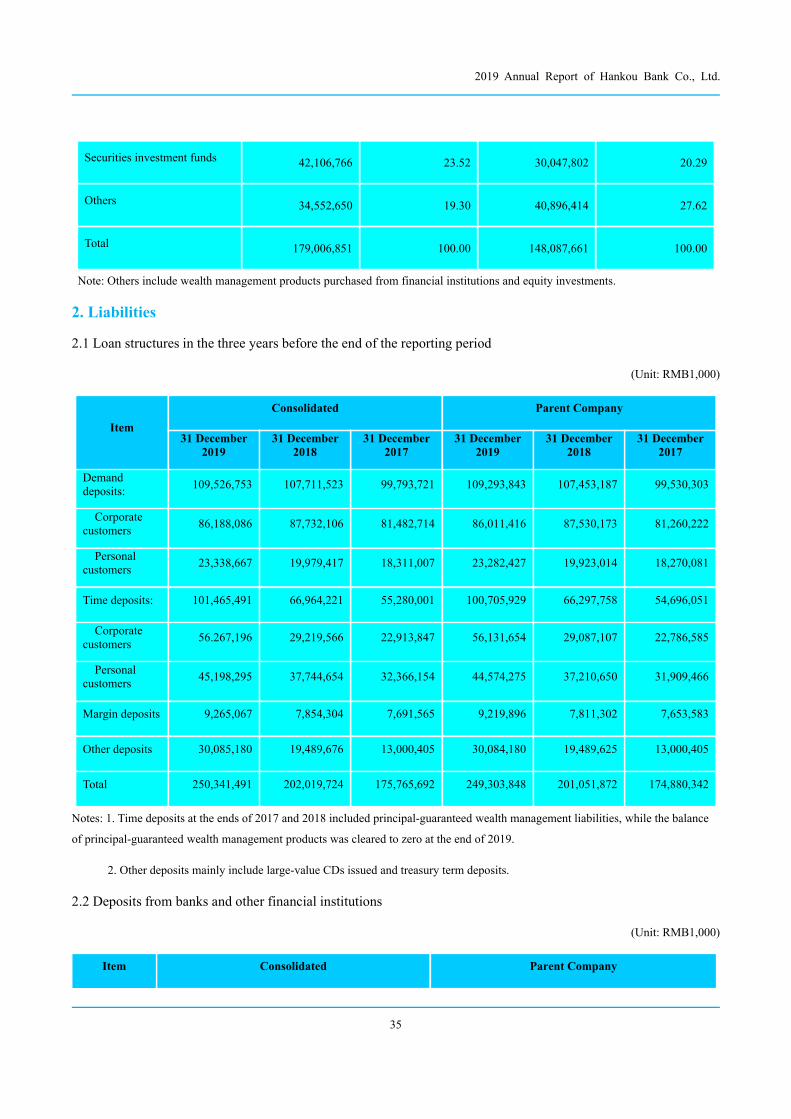

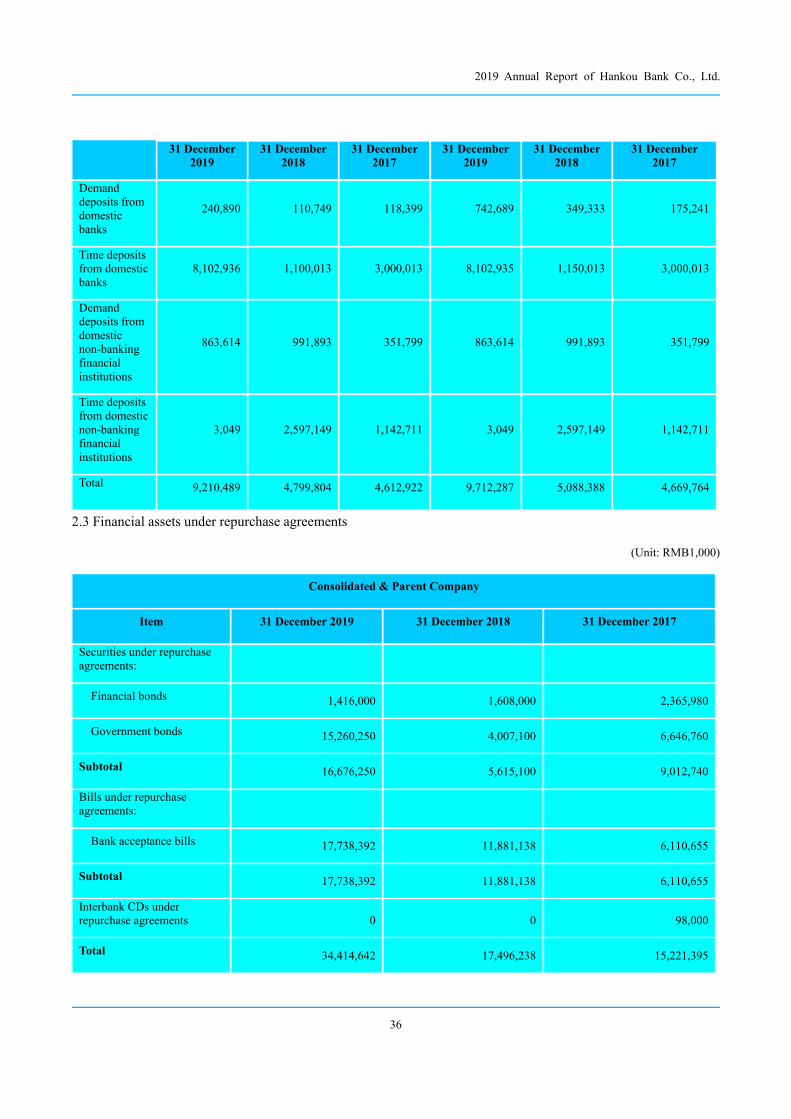

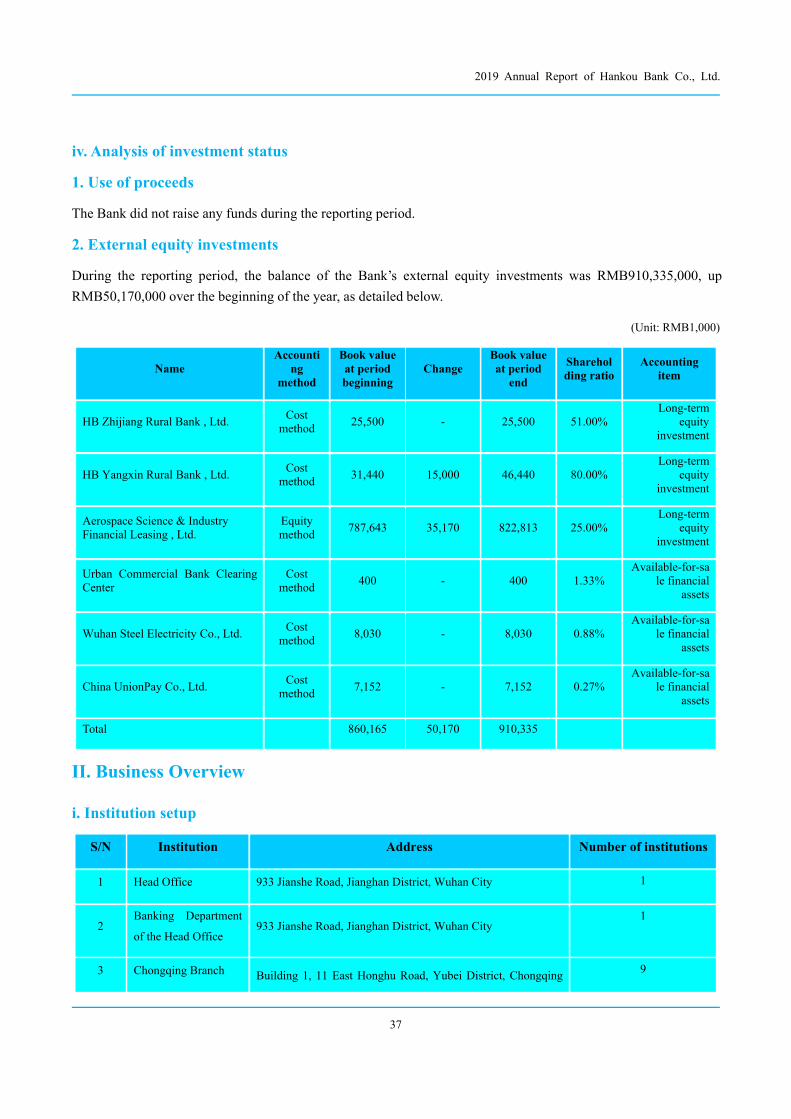

iv. Analysis of investment status.................................................................................................................. 37

II. Business Overview...........................................................................................................................................37

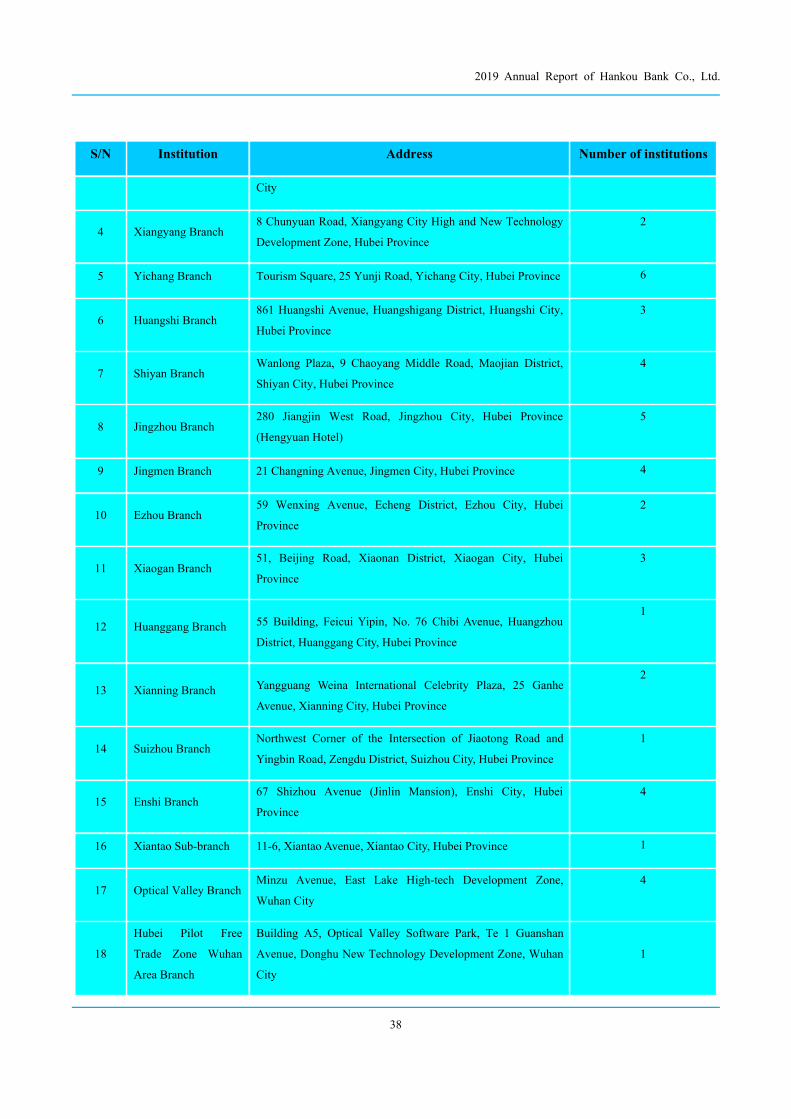

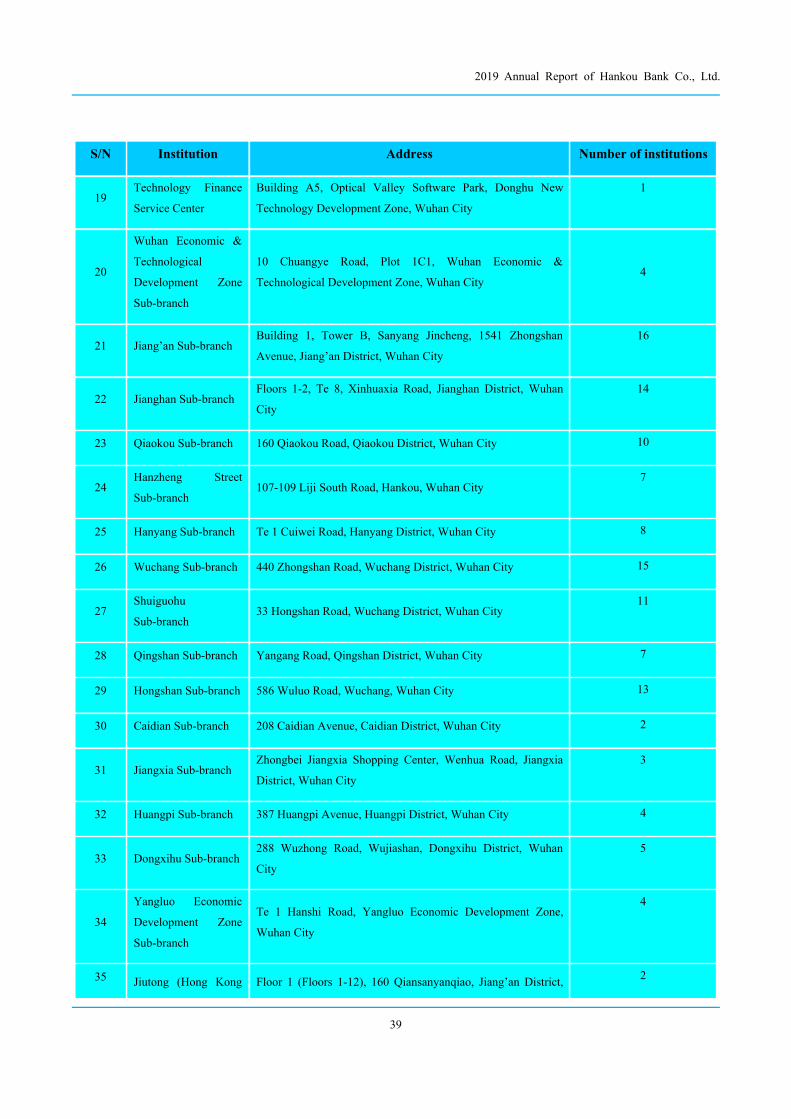

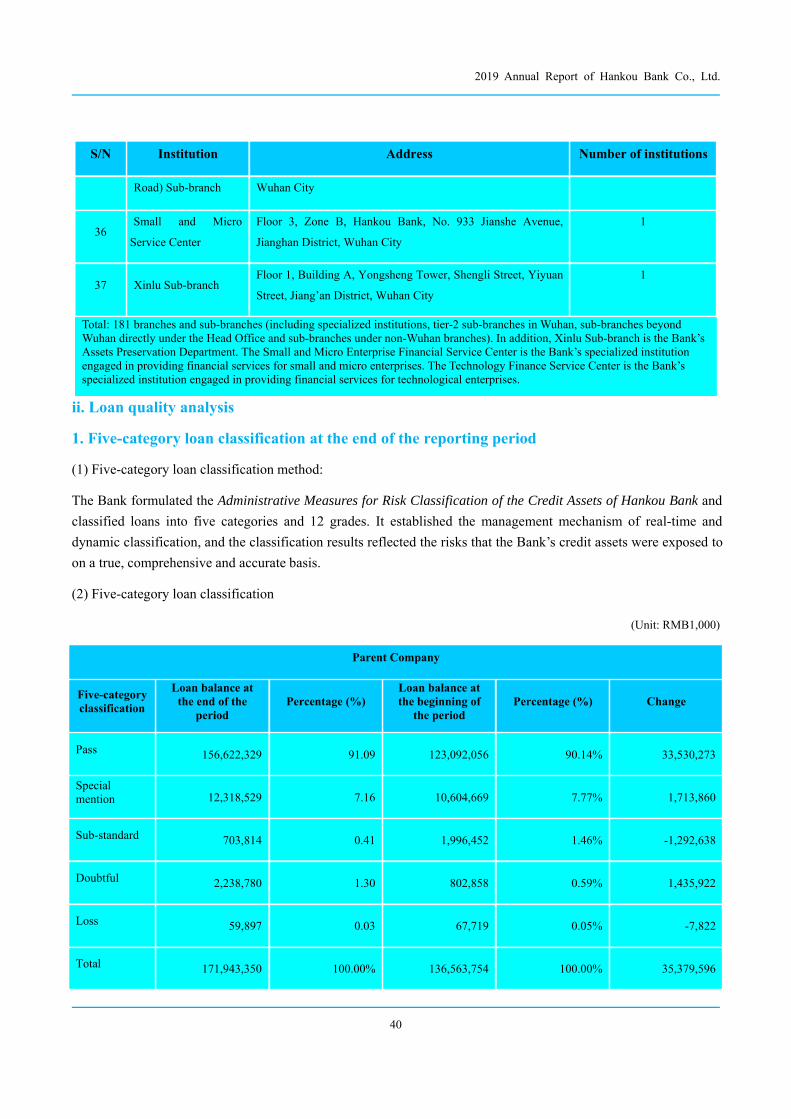

i. Institution setup......................................................................................................................................... 37

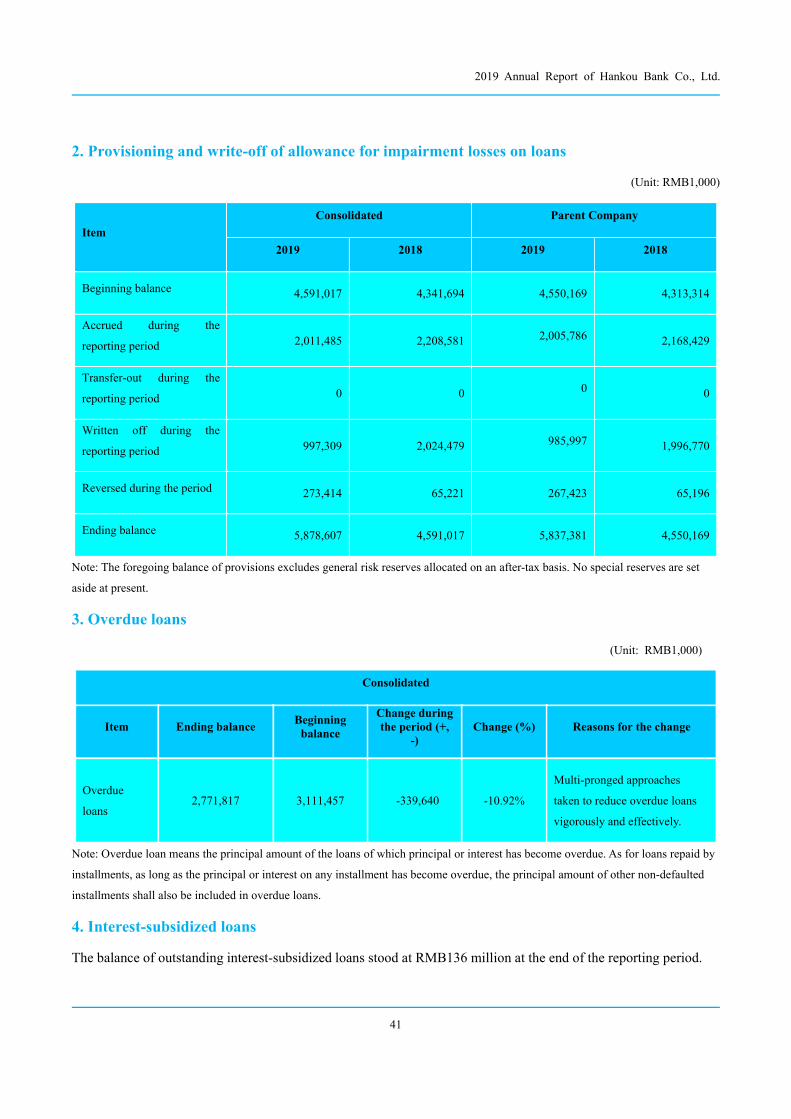

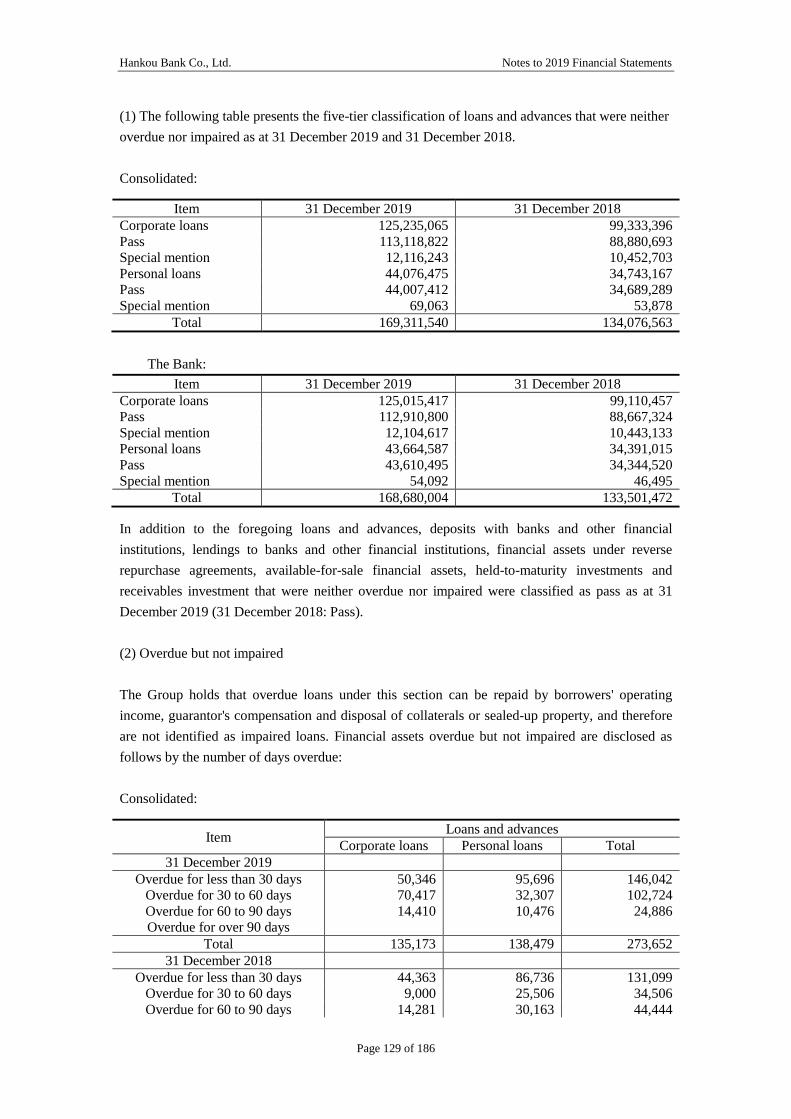

ii. Loan quality analysis................................................................................................................................40

iii. Group customer credit business and its risk management......................................................................42

iv. NPA changes and management measures................................................................................................42

2019 Annual Report of Hankou Bank Co., Ltd.

II

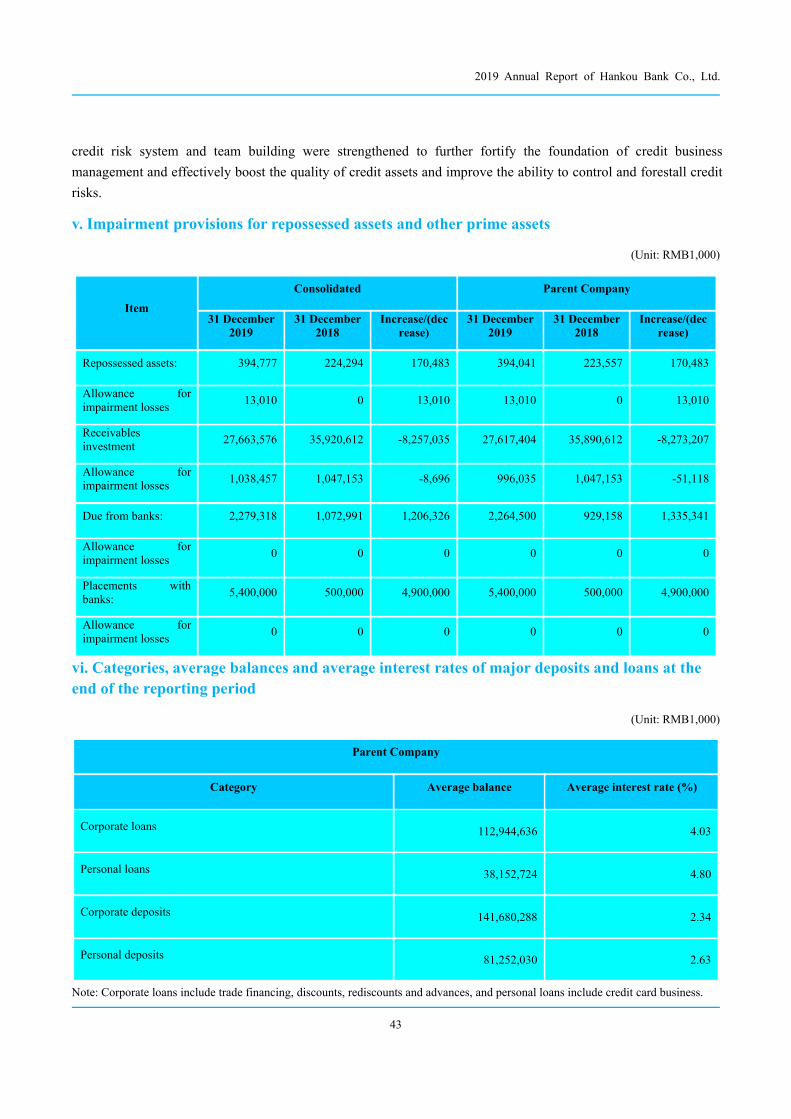

v. Impairment provisions for repossessed assets and other prime assets.....................................................43

vi. Categories, average balances and average interest rates of major deposits and loans at the end of the

reporting period............................................................................................................................................ 43

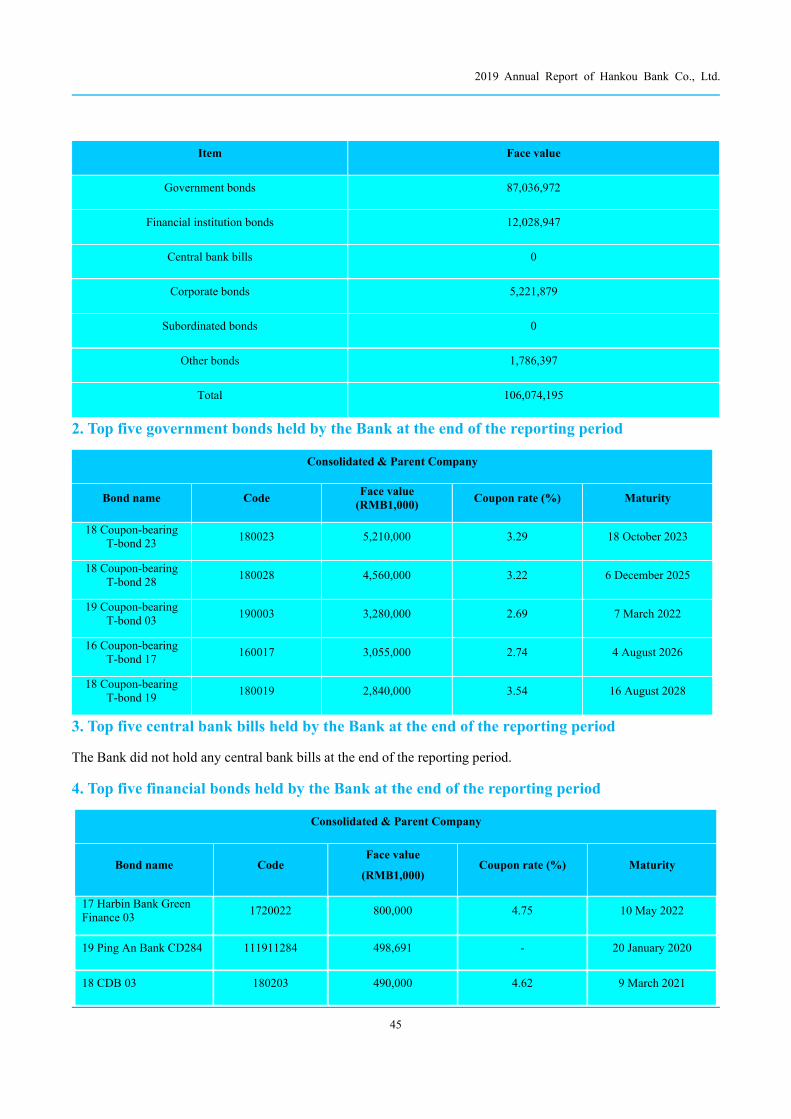

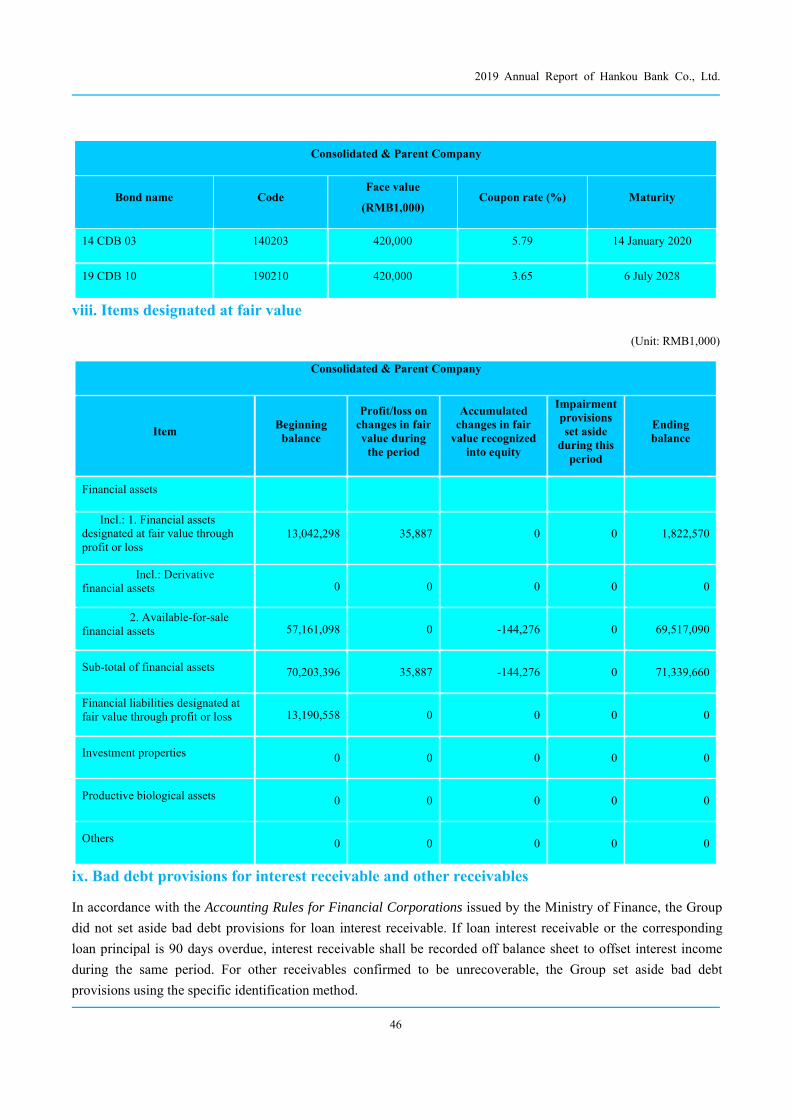

vii. Debt securities investment..................................................................................................................... 44

viii. Items designated at fair value................................................................................................................46

ix. Bad debt provisions for interest receivable and other receivables..........................................................46

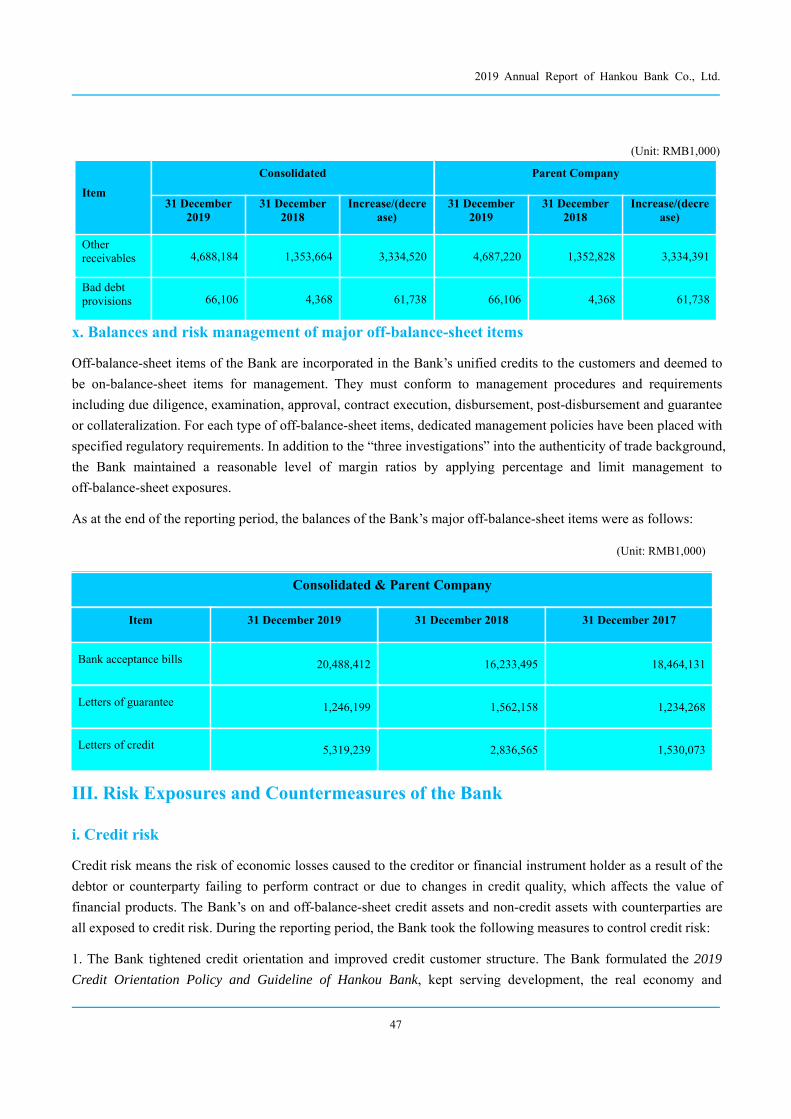

x. Balances and risk management of major off-balance-sheet items...........................................................47

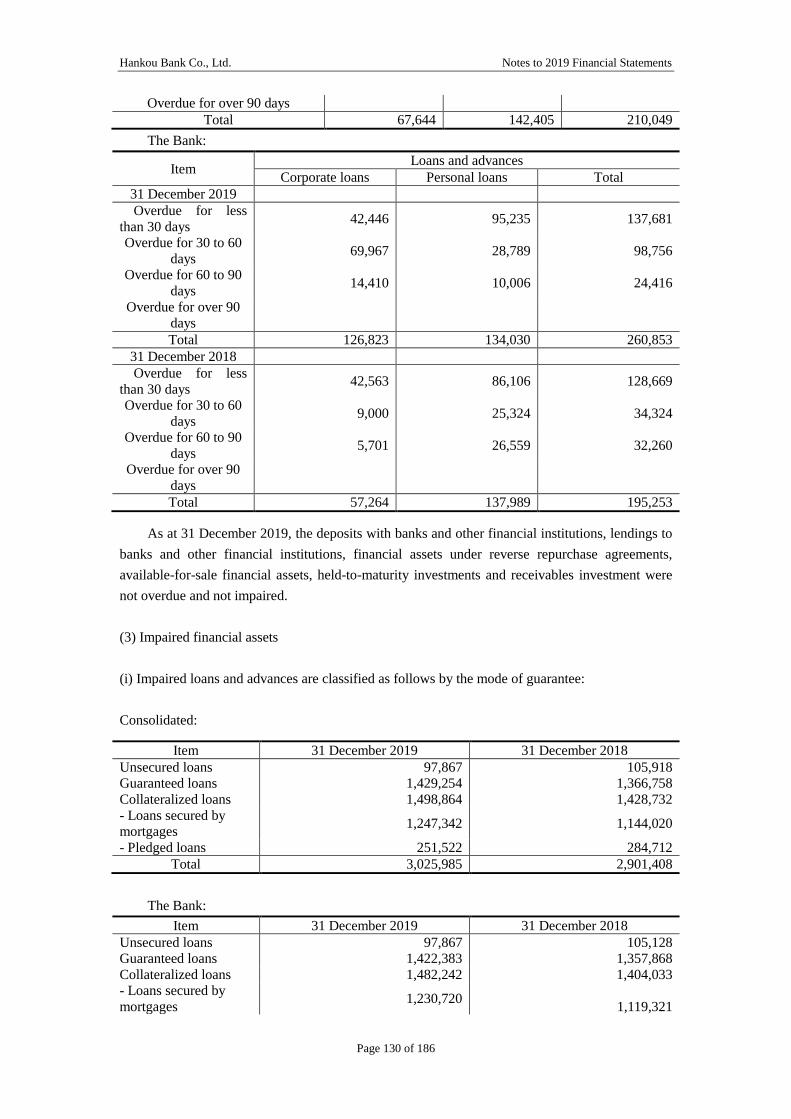

III. Risk Exposures and Countermeasures of the Bank........................................................................................47

i. Credit risk.................................................................................................................................................. 47

ii. Market risk................................................................................................................................................48

iii. Operational risk....................................................................................................................................... 49

iv. Compliance risk....................................................................................................................................... 50

v. Liquidity risk.............................................................................................................................................50

vi. Reputational risk......................................................................................................................................52

IV. Changes in the Business Environment and Macro Policies, Laws and Regulations and Influences thereof 52

i. Influence of macro control........................................................................................................................ 52

ii. Influence of reform in financial supervision............................................................................................53

V. Outlook............................................................................................................................................................. 53

i. Industry development pattern and trend....................................................................................................53

ii. Possible external risks in future operation............................................................................................... 54

iii. Challenges and opportunities in future operation................................................................................... 54

iv. Operating plan..........................................................................................................................................54

VI. Work of the Board of Directors during the Reporting Period........................................................................56

i. Meetings of the Board of Directors and resolutions during the reporting period.....................................56

ii. Implementation of the resolutions of Shareholders’ General Meeting by the Board of Directors..........57

iii. Performance of duties by the special committees of the Board of Directors......................................... 58

iv. Performance of strategic management functions by the Board of Directors.......................................... 59

v. Development of policies and procedures of the Board of Directors........................................................59

2019 Annual Report of Hankou Bank Co., Ltd.

III

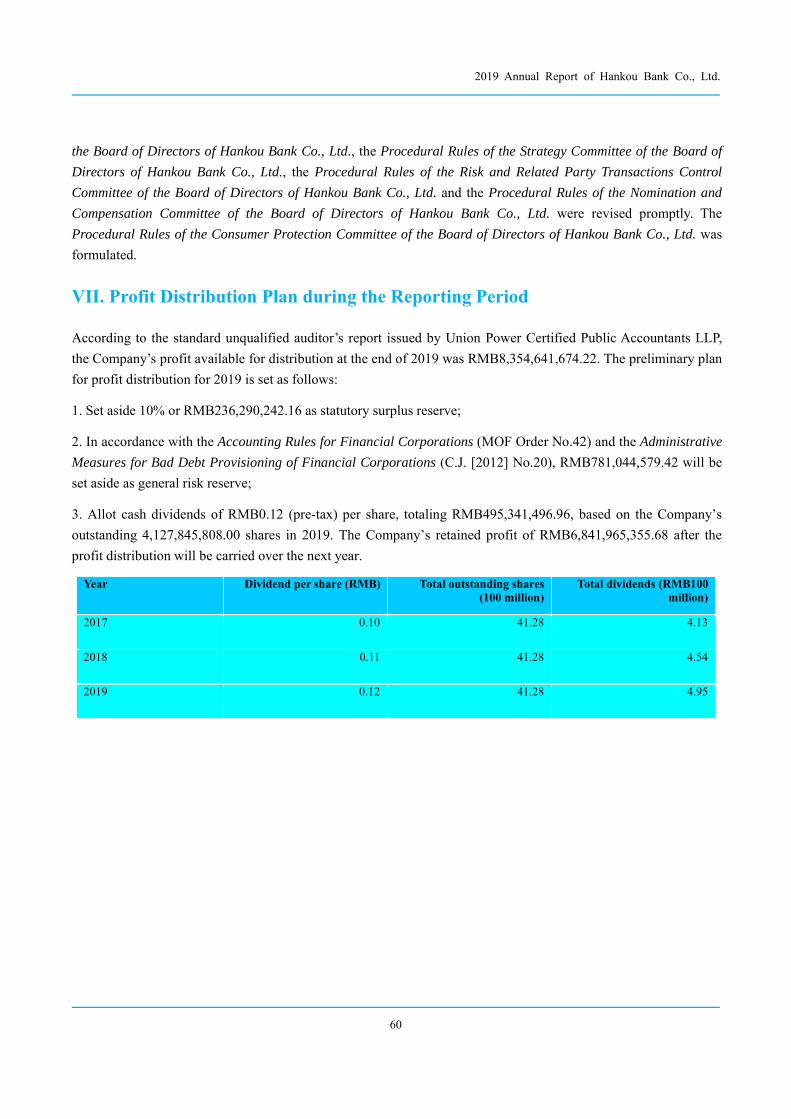

VII. Profit Distribution Plan during the Reporting Period...................................................................................60

Chapter V Report of the Board of Supervisors............................................................................... 61

I. Work of the Board of Supervisors during the Reporting Period.......................................................................61

i. Meetings of the Board of Supervisors and Resolutions............................................................................61

ii. Performance of duties by the special committees of the Board of Supervisors...................................... 62

iii. Supervisors’ attendance of the general meetings and the meetings of the Board of Directors as

non-voting delegates.....................................................................................................................................62

iv. Supervision of duty performance............................................................................................................ 62

iv. Special work done....................................................................................................................................63

v. Development of policies and procedures..................................................................................................63

vi. Application of supervision findings........................................................................................................ 64

vii. Studies.................................................................................................................................................... 64

II. Independent Opinions of the Board of Supervisors on Relevant Issues......................................................... 64

i. Compliant operation of the Company....................................................................................................... 64

ii. Authenticity of the financial statements of the Company........................................................................64

iii. Acquisitions and sales of assets.............................................................................................................. 64

iv. Related party transactions........................................................................................................................64

v. Implementation of resolutions made by the general meetings.................................................................64

vi. Risk management and internal control....................................................................................................64

Chapter VI Significant Events.......................................................................................................... 66

I. Material Legal Proceedings and Arbitrations................................................................................................... 66

II. Increase or Decrease of Registered Capital, Split-off and Merger..................................................................66

III. Material Asset Acquisition and Sale, Merger and Acquisition...................................................................... 66

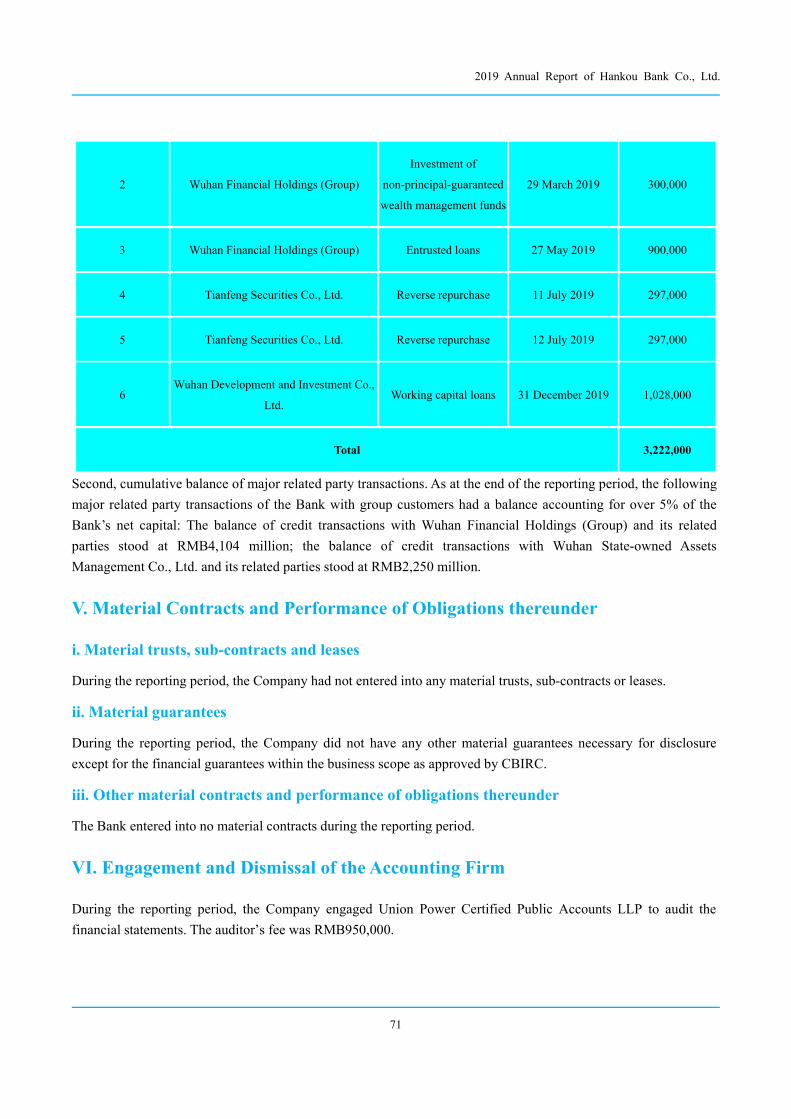

IV. Related Party Transactions..............................................................................................................................66

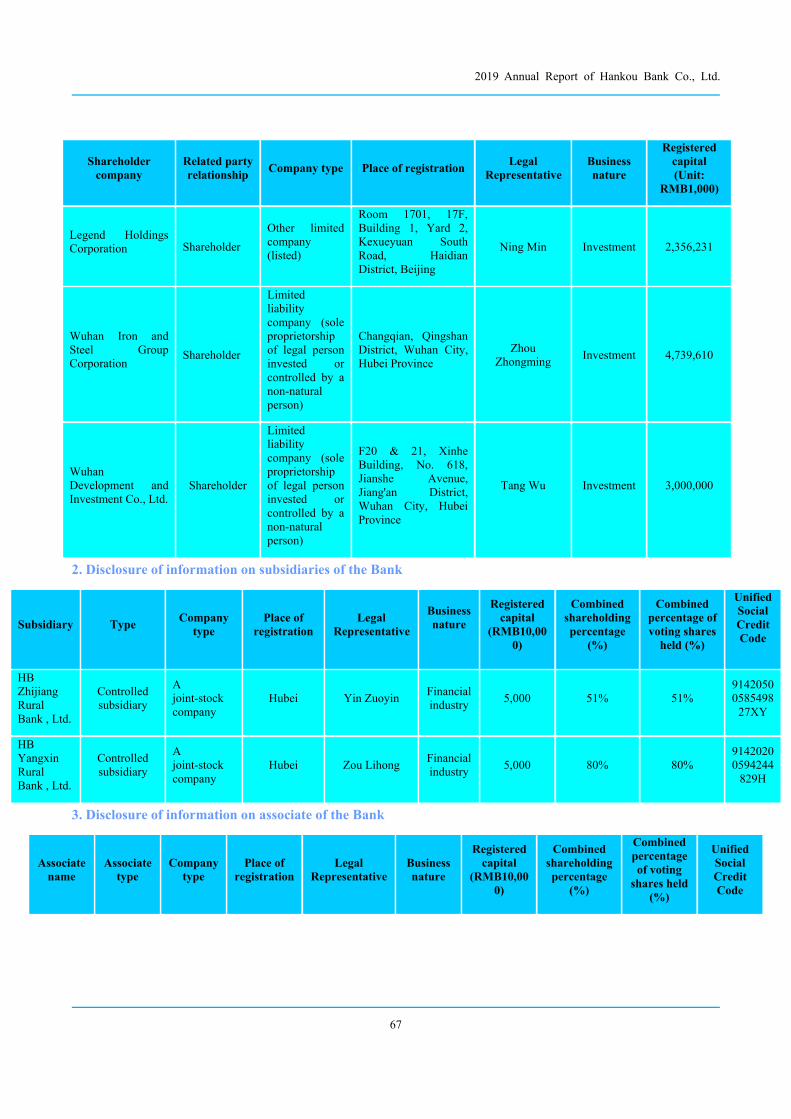

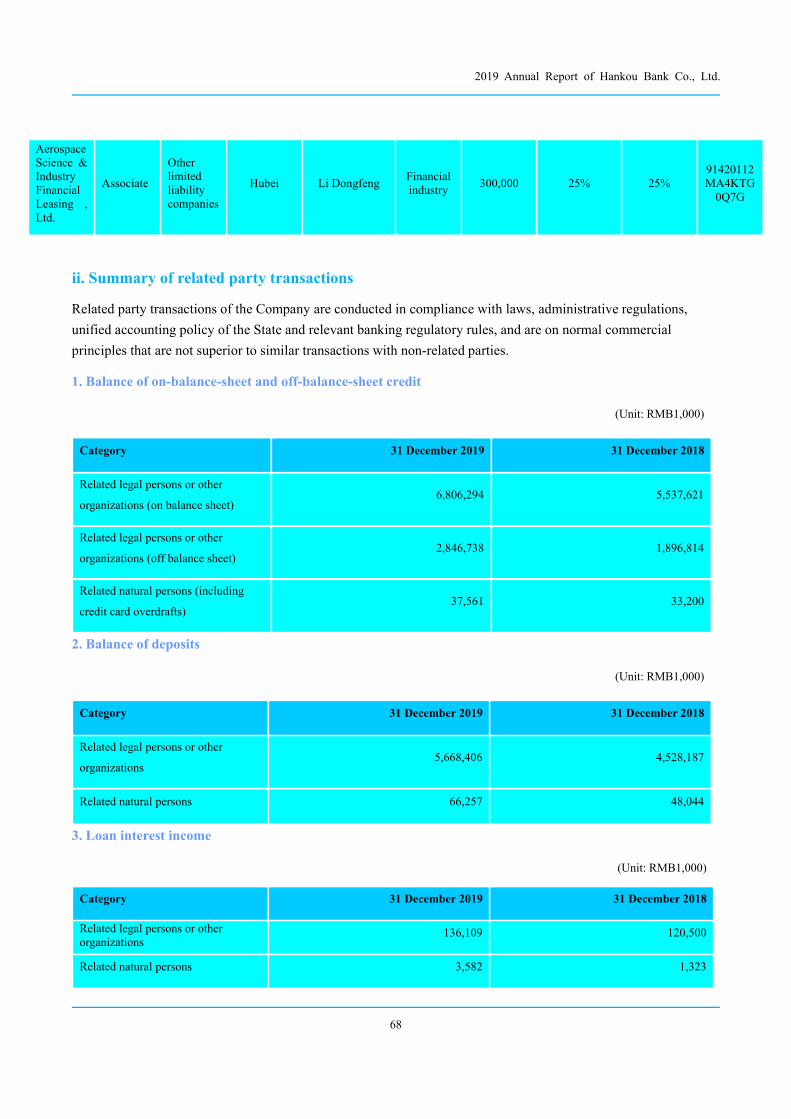

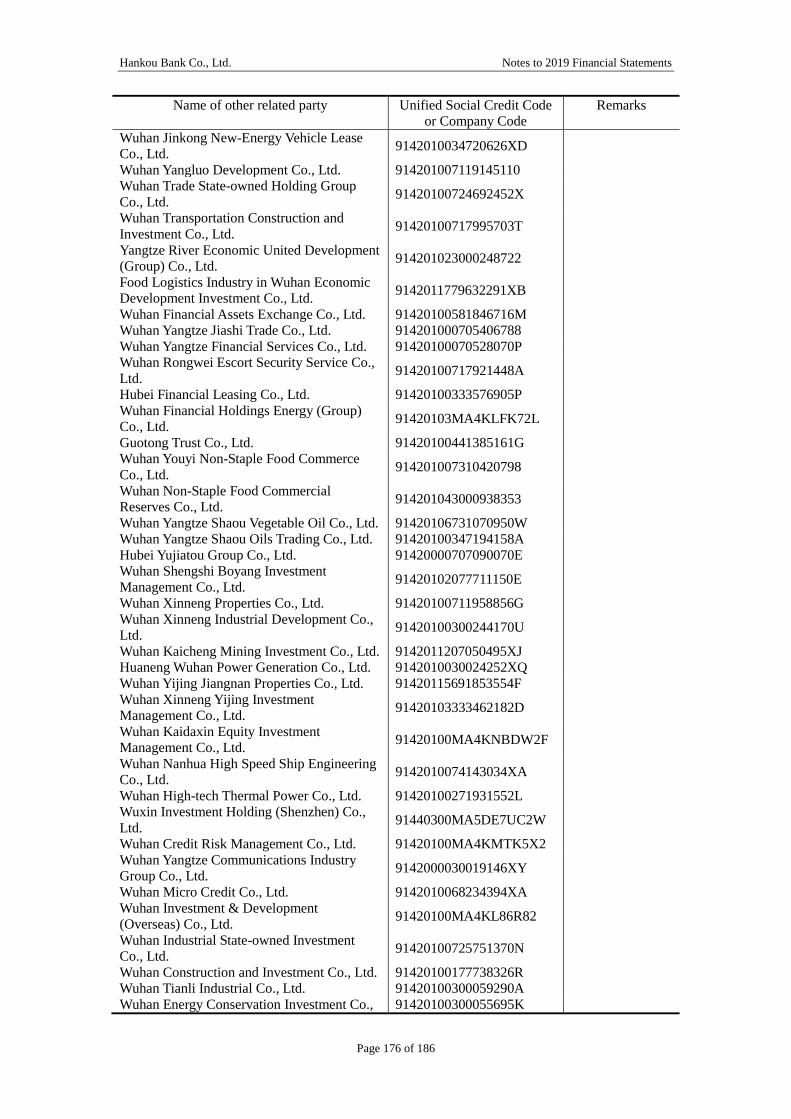

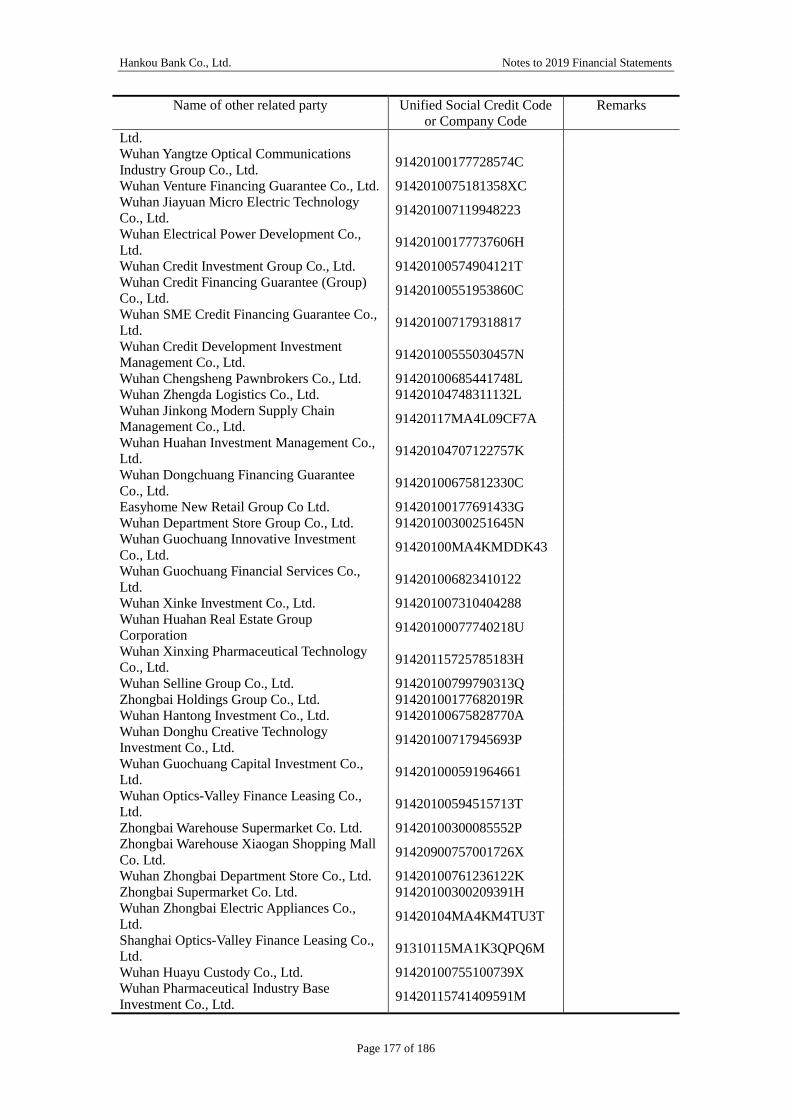

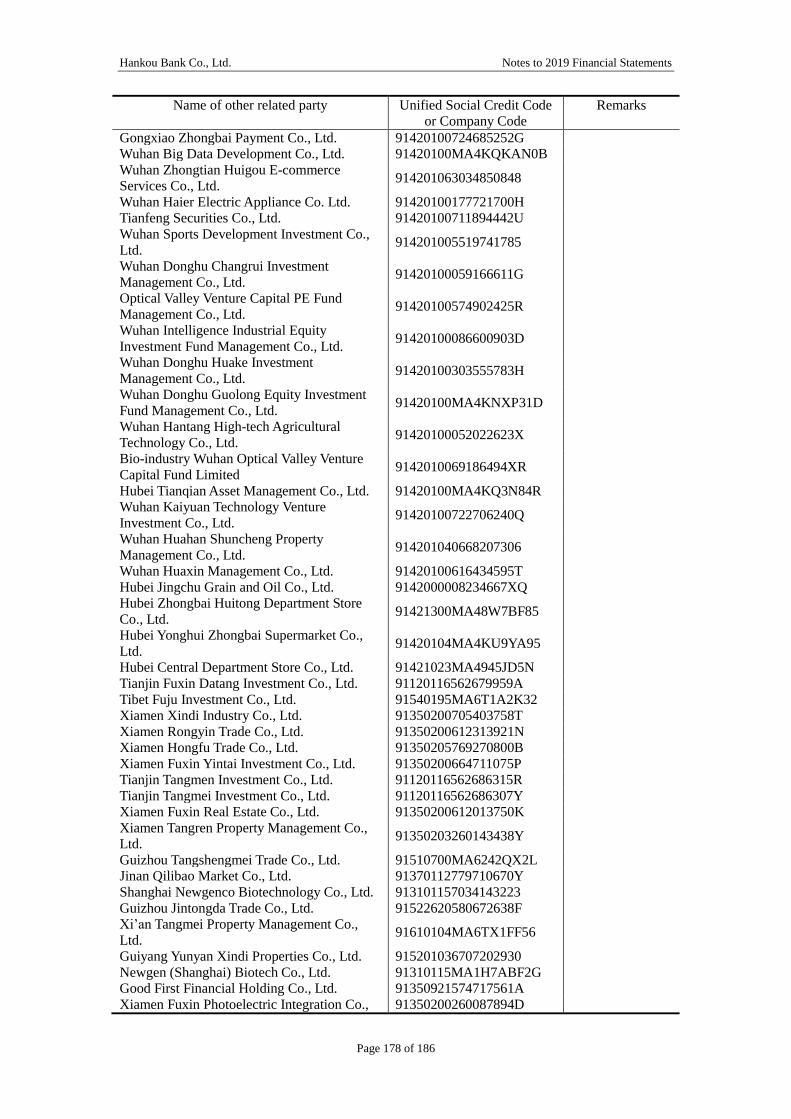

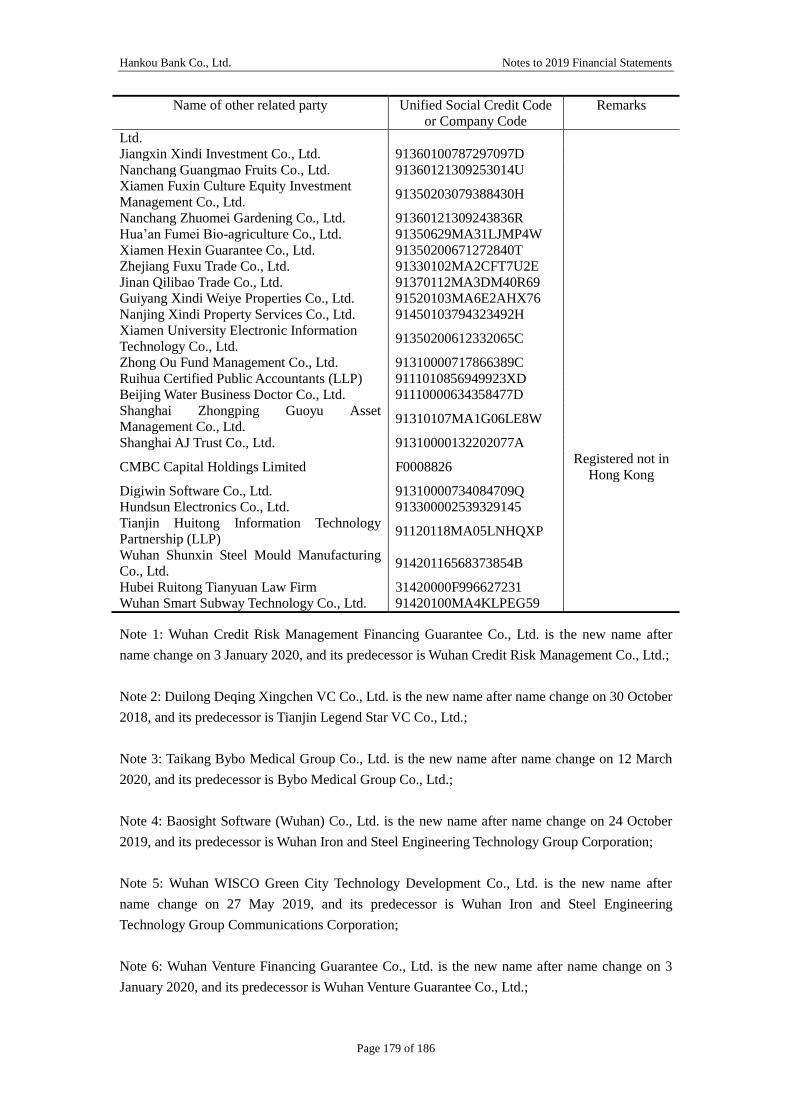

i. Related parties........................................................................................................................................... 66

ii. Summary of related party transactions.....................................................................................................68

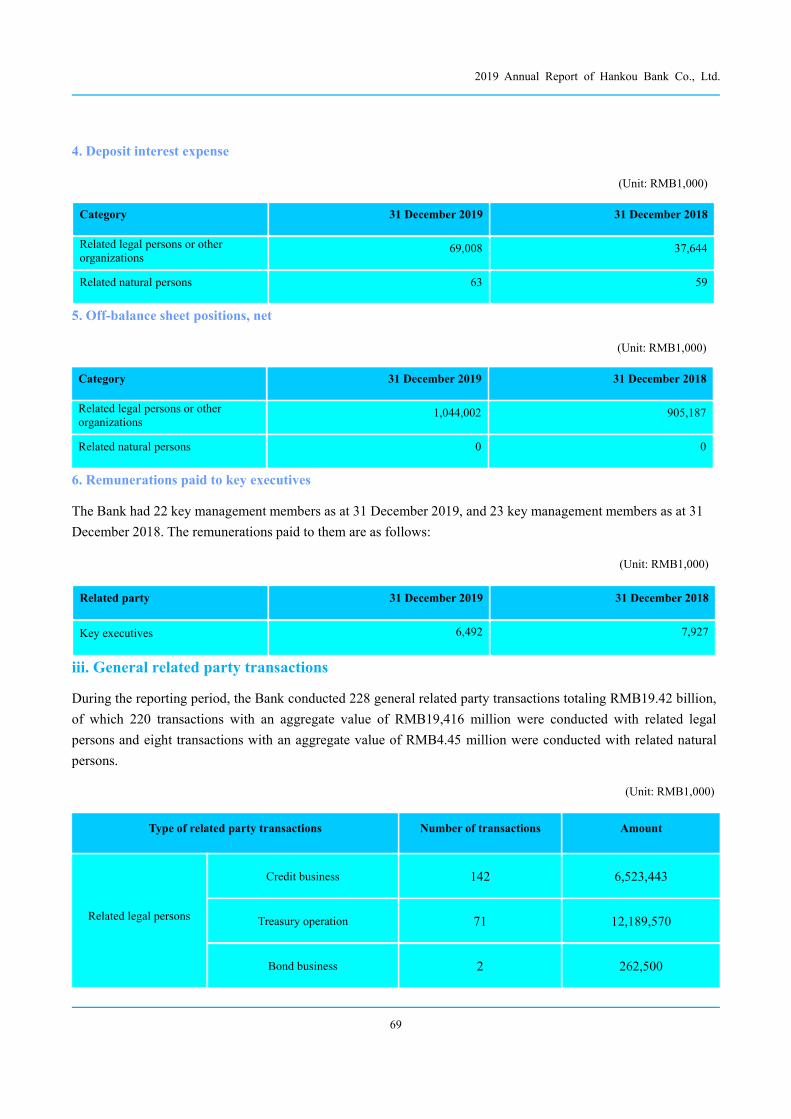

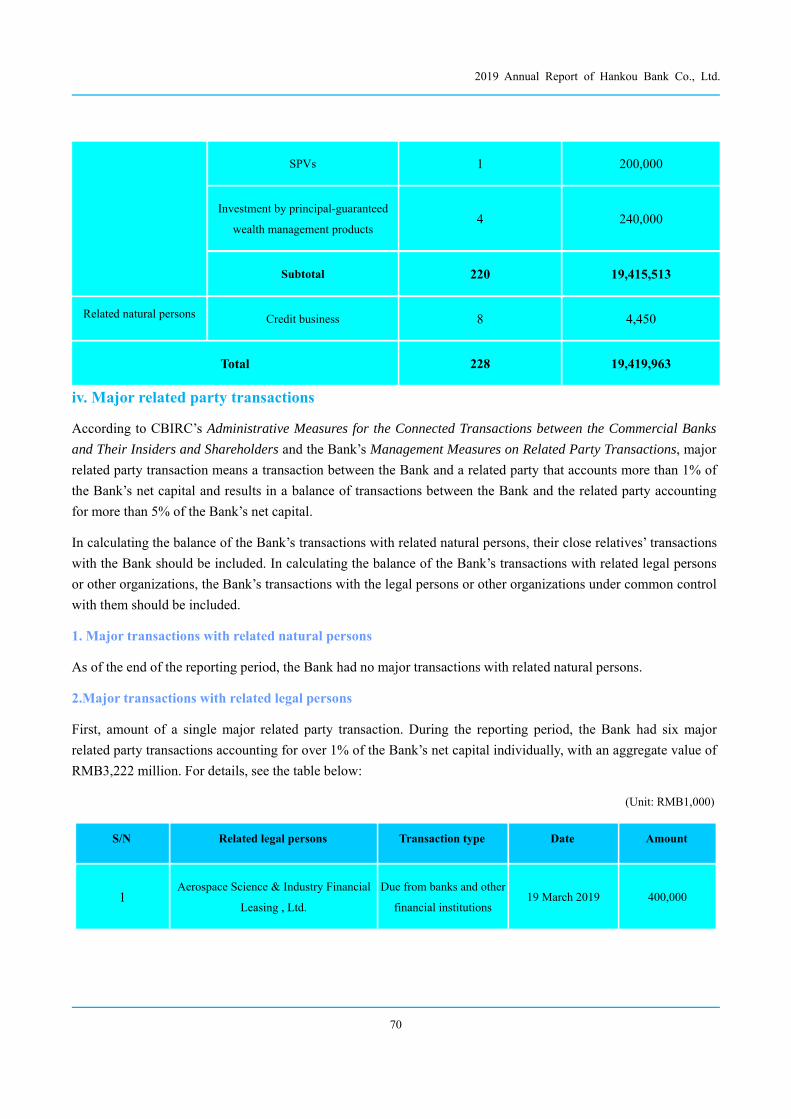

iii. General related party transactions...........................................................................................................69

iv. Major related party transactions.............................................................................................................. 70

2019 Annual Report of Hankou Bank Co., Ltd.

IV

V. Material Contracts and Performance of Obligations thereunder..................................................................... 71

i. Material trusts, sub-contracts and leases...................................................................................................71

ii. Material guarantees.................................................................................................................................. 71

iii. Other material contracts and performance of obligations thereunder.................................................... 71

VI. Engagement and Dismissal of the Accounting Firm......................................................................................71

VII. Regulatory Penalties on Directors, Supervisors and Senior Executives of the Company........................... 72

VIII. Other Important Information Necessary to Inform the Public.................................................................... 72

i. Acquisition of business access qualifications........................................................................................... 72

ii. Establishment of institutions.................................................................................................................... 72

iii. Other important information................................................................................................................... 72

Chapter VII Share Capital Changes and Shareholders................................................................. 74

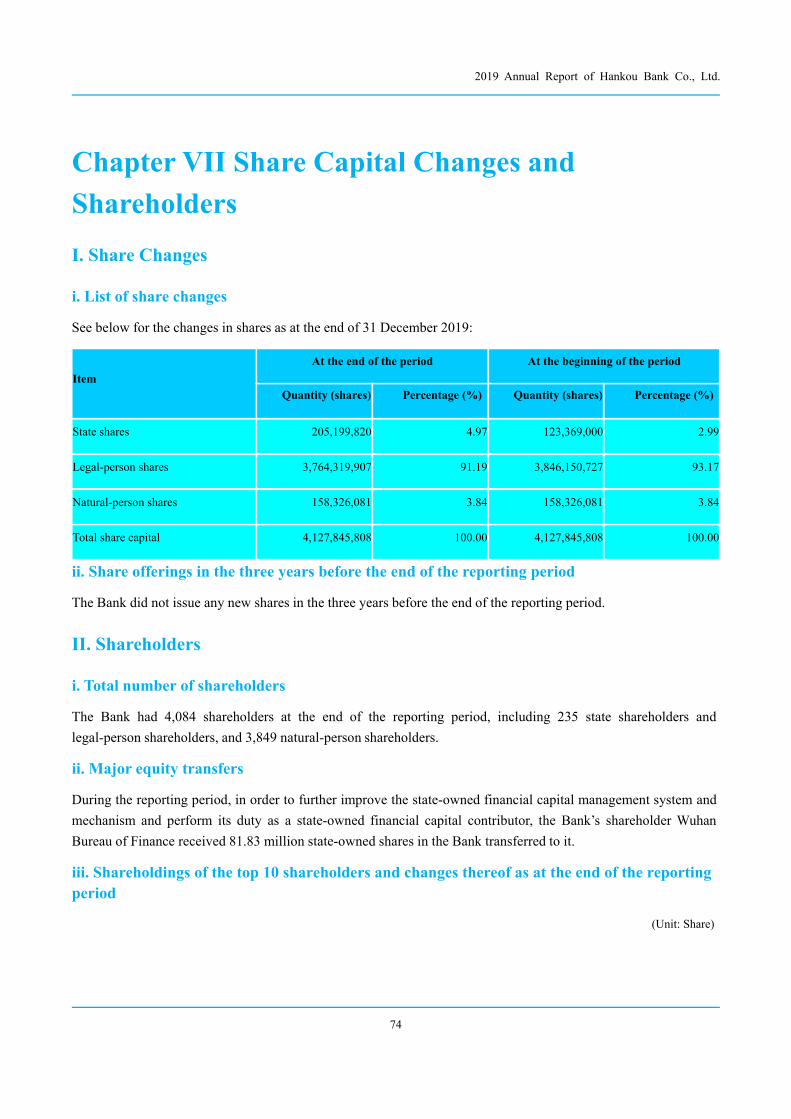

I. Share Changes................................................................................................................................................... 74

i. List of share changes................................................................................................................................. 74

ii. Share offerings in the three years before the end of the reporting period............................................... 74

II. Shareholders.....................................................................................................................................................74

i. Total number of shareholders.................................................................................................................... 74

ii. Major equity transfers.............................................................................................................................. 74

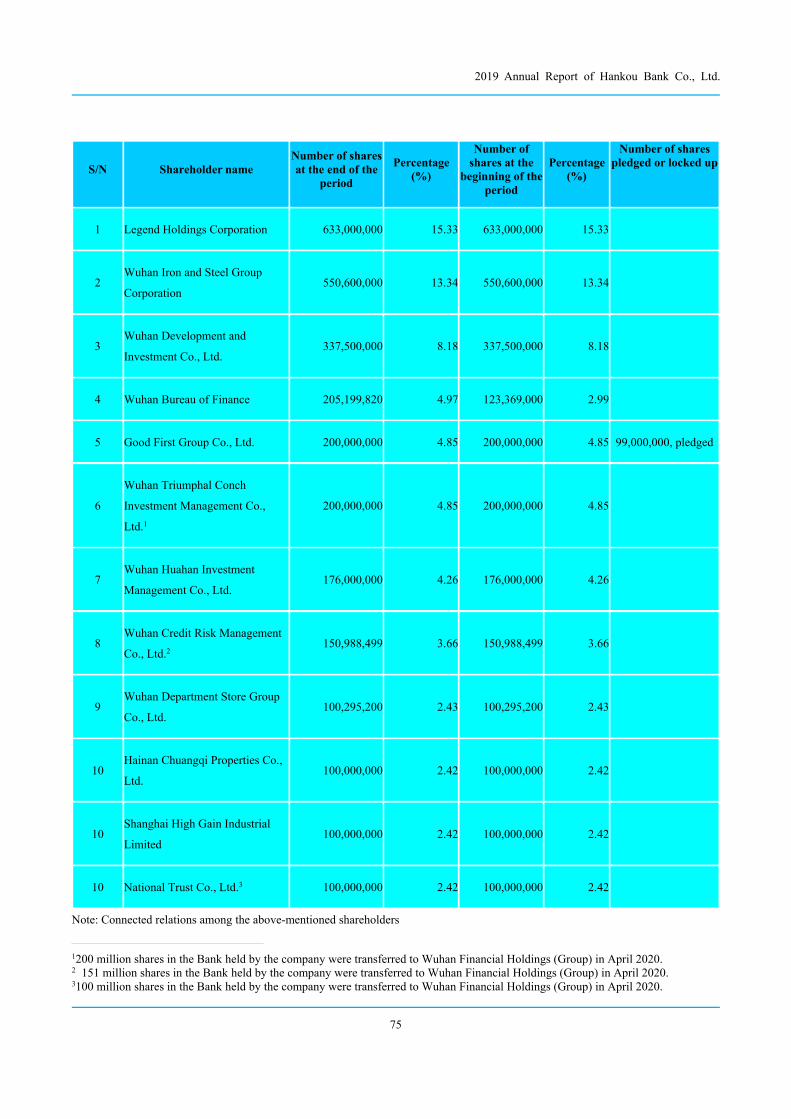

iii. Shareholdings of the top 10 shareholders and changes thereof as at the end of the reporting period... 74

iv. Substantial shareholders.......................................................................................................................... 76

Chapter VIII Directors, Supervisors, Senior Executives and Employees.....................................79

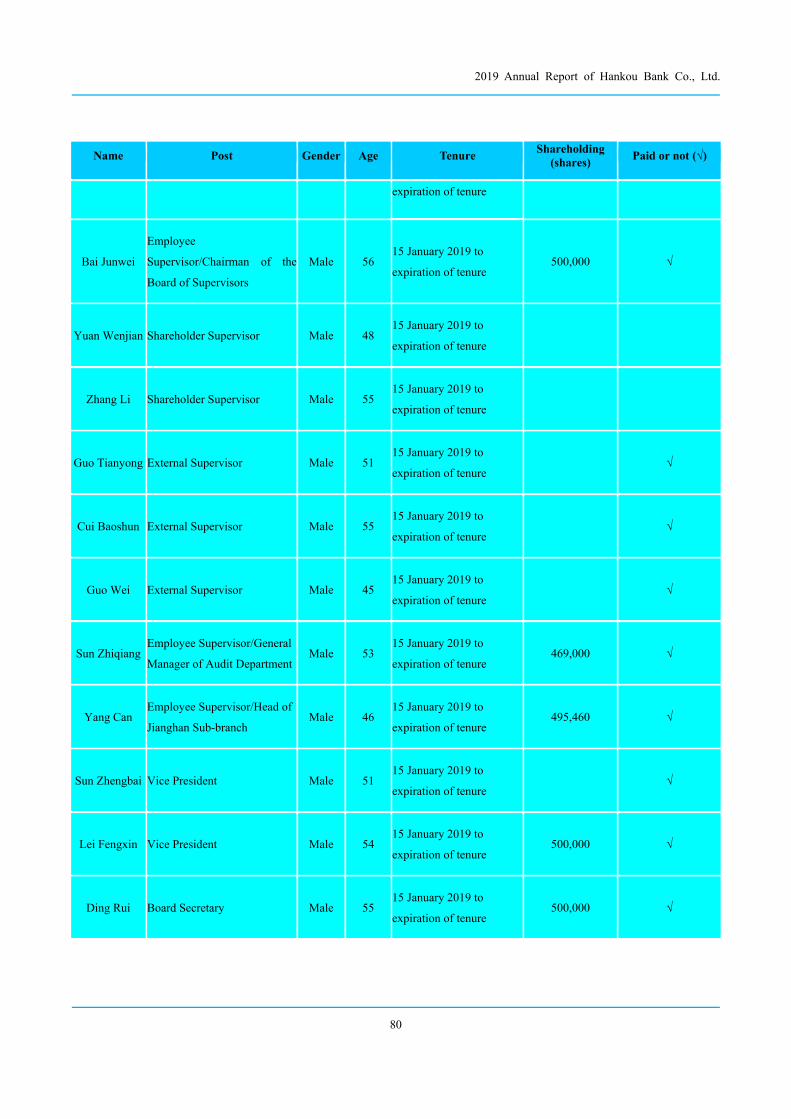

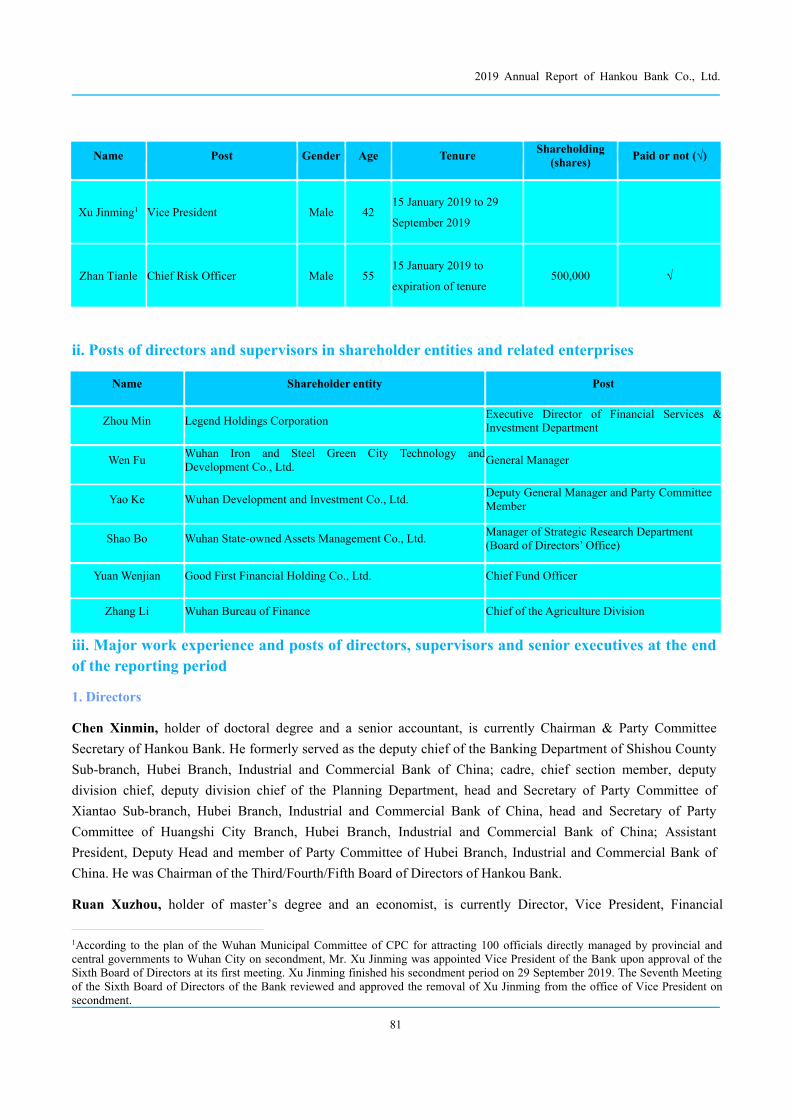

I. Directors, Supervisors and Senior Executives.................................................................................................. 79

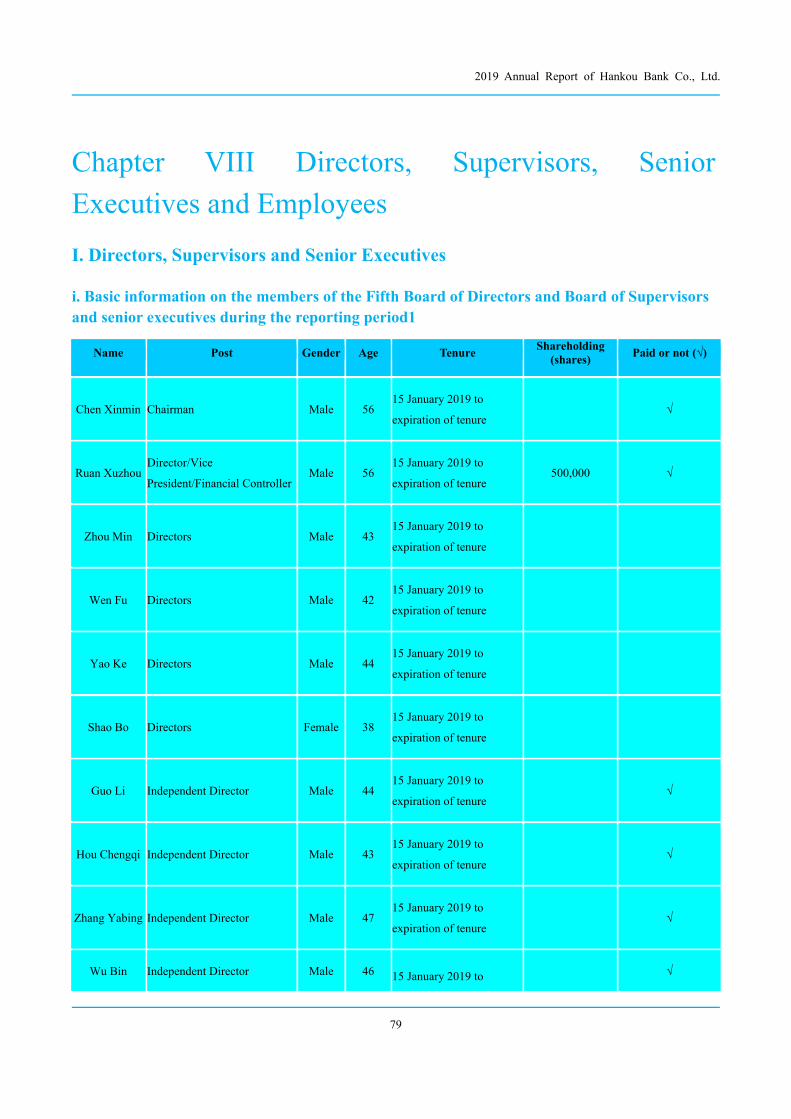

i. Basic information on the members of the Fifth Board of Directors and Board of Supervisors and senior

executives during the reporting period1.......................................................................................................79

ii. Posts of directors and supervisors in shareholder entities and related enterprises.................................. 81

iii. Major work experience and posts of directors, supervisors and senior executives at the end of the

reporting period............................................................................................................................................ 81

iv. Changes in directors, supervisors and senior executives during the reporting period............................85

II. Remunerations of Directors, Supervisors, Senior Executives and Key Management Personnel................... 86

2019 Annual Report of Hankou Bank Co., Ltd.

V

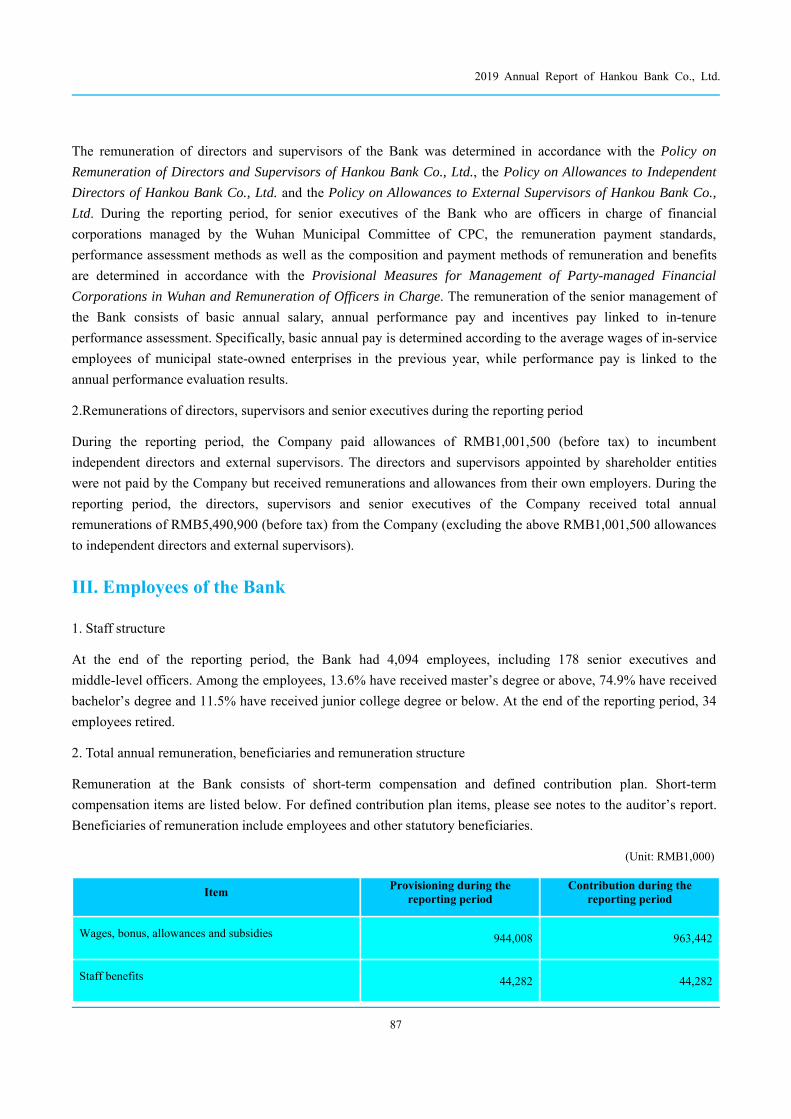

III. Employees of the Bank...................................................................................................................................87

Chapter IX Corporate Governance Practice...................................................................................90

I. Corporate Governance during the Reporting Period........................................................................................ 90

i. About shareholders and the Shareholders’ General Meeting....................................................................90

ii. About directors, the Board of Directors and special committees............................................................ 91

iii. About supervisors, the Board of Supervisors and special committees...................................................91

iv. About information disclosure and investor relations management.........................................................92

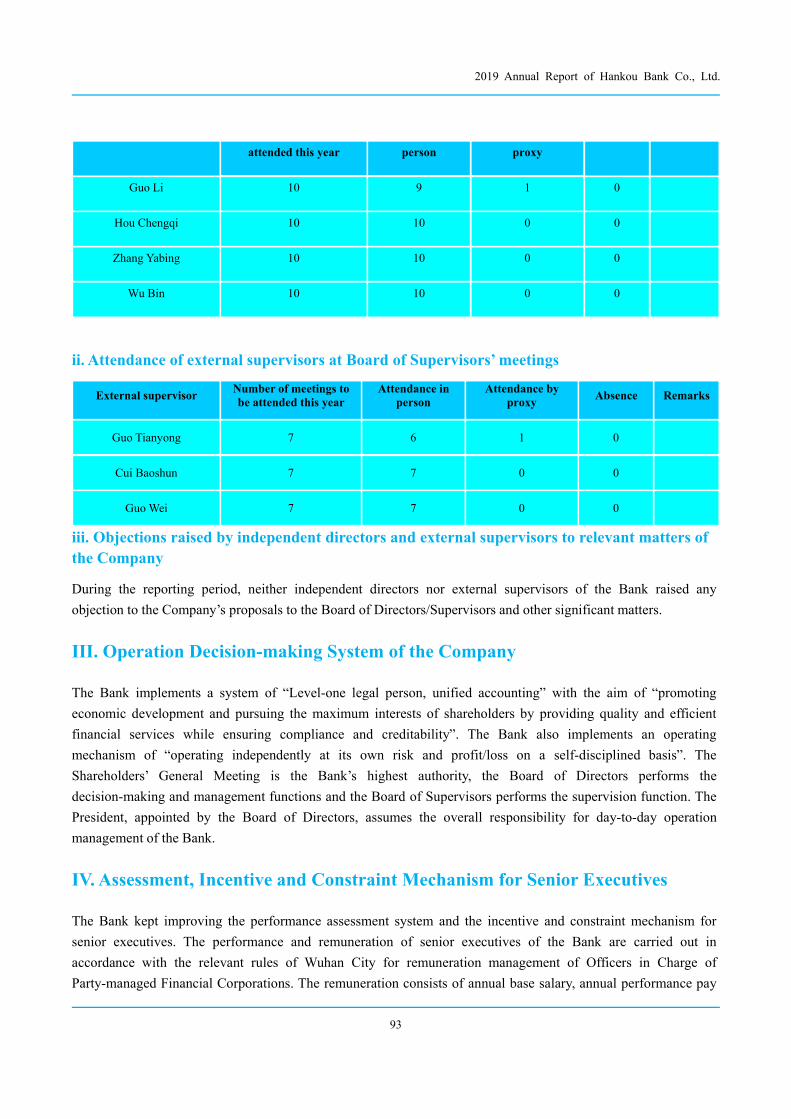

II. Duty Performance of Independent Directors and External Supervisors......................................................... 92

i. Attendance of independent directors at Board of Directors’ meetings..................................................... 92

ii. Attendance of external supervisors at Board of Supervisors’ meetings.................................................. 93

iii. Objections raised by independent directors and external supervisors to relevant matters of the

Company.......................................................................................................................................................93

III. Operation Decision-making System of the Company....................................................................................93

IV. Assessment, Incentive and Constraint Mechanism for Senior Executives.................................................... 93

Chapter X Internal Control.............................................................................................................. 95

I. Statement of the Board of Directors on Internal Control Responsibilities.......................................................95

II. Basis of Internal Control over Financial Reporting and Internal Control System Development................... 95

i. Basis of establishing internal control over financing reporting................................................................95

ii. General plan on the establishment of internal control............................................................................. 95

iii. Establishment and improvement of internal control system...................................................................96

iv. Operation of internal control supervision mechanism............................................................................ 96

v. Internal control self-assessment................................................................................................................97

vi. Development and improvement of internal control................................................................................ 97

Chapter XI Financial Report............................................................................................................ 98

Chapter XII List of Documents for Reference................................................................................ 98

Chapter XIII Annexes........................................................................................................................98

Written Confirmation of Directors and Senior Management of Hankou Bank Co., Ltd. on theCompany’s 2019 Annual Report.......................................................................................................99

2019 Annual Report of Hankou Bank Co., Ltd.

VI

2019 Auditor’s Report of Hankou Bank Co., Ltd. ...................................................................... 100

2019 Annual Report of Hankou Bank Co., Ltd.

1

Chapter I Important Notice

The Board of Directors, and the Board of Supervisors, as well as the directors, supervisors and senior executives

of the Company warrant that the information contained herein does not contain any false records, misleading

statements or material omissions, and shall bear the joint and several liabilities for the authenticity, accuracy and

integrity of its contents.

The 2019 Annual Report of the Company and its summary were reviewed and approved at the 12th Meeting of the

Sixth Board of Directors of the Company on 29 May 2019. Of the 10 directors supposed to attend the meeting, 10

directors were present. Eight supervisors of the Company attended the meeting as non-voting delegates.

The annual financial report of the Company has been audited by Union Power Certified Public Accountants LLP

in accordance with the PRC Auditing Standards with a standard unqualified auditor’s report issued.

The Board of Directors of Hankou Bank Co., Ltd.

Chen Xinmin, Chairman, Ruan Xuzhou, Vice President & Financial Controller, and Li Daquan, Principal of the

Planning and Finance Department, warrant the authenticity and integrity of the financial report herein.

2019 Annual Report of Hankou Bank Co., Ltd.

2

Chapter II Basic Information

I. Terms and Definitions

i. The Company, the Bank or Hankou Bank: Hankou Bank Co., Ltd.

ii. Our Group or the Group: Hankou Bank Co., Ltd. and its subsidiaries

iii. Articles of Association: Articles of Association of the Company

iv. Shareholders’General Meeting: The Shareholders’ General Meeting of the Company

v. Board of Directors: The Board of Directors of the Company

vi. Board of Supervisors: The Board of Supervisors of the Company

II. Company Profile

i. The Company’s legal Chinese name: 汉口银行股份有限公司

Legal English name: Hankou Bank Co., Ltd. (“HKB” in short)

ii. Legal Representative of the Company: Chen Xinmin

iii. Board Secretary: Ding Rui

Address: 933 Jianshe Road, Jianghan District, Wuhan City, Hubei Province

Postal Code: 430015

Tel: 027-82656263

Fax: 027-82656099

iv. Registered/office address: 933 Jianshe Road, Jianghan District, Wuhan City, Hubei Province

Postal Code: 430015

Tel: 027-82656263

Fax: 027-82656099

Customer service hotline: 96558 (Wuhan), 4006096558 (Nationwide)

Website: http://www.hkbchina.com

Email: [email protected]

v. Newspaper designated for information disclosure: Financial Times

Website designated for publication of annual report: http://www.hkbchina.com

2019 Annual Report of Hankou Bank Co., Ltd.

3

Place where the Annual Report can be obtained: Office of the Board of Directors of the Company

vi. Other relevant information:

Date of First Registration: 15 December 1997

Date of change of registration: 26 December 2012

Place of initial registration: 21 Jianghan Road, Jianghan District, Wuhan City

Place of registration changed to: 933 Jianshe Road, Jianghan District, Wuhan City

Unified Social Credit Code: 91420100300248067P

Name of domestic accounting firm engaged: Union Power Certified Public Accounts (Special General

Partnership)

Office address: F/2-9, Donghu Road, Wuchang District, Wuhan City

vii. This report is prepared in both Chinese and English. The Chinese version shall prevail in case of any

discrepancy between the two versions.

2019 Annual Report of Hankou Bank Co., Ltd.

4

III. Organizational Chart of the Company

2019 Annual Report of Hankou Bank Co., Ltd.

5

Chapter III Summary of Accounting & Business

Data

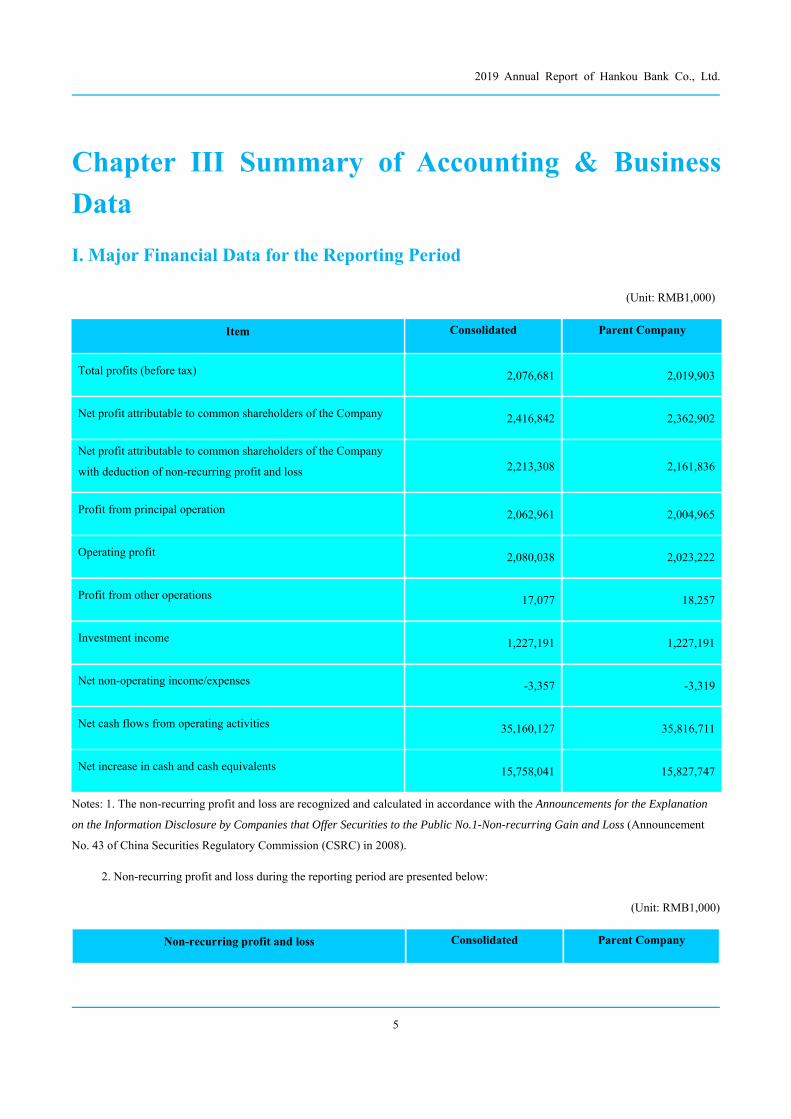

I. Major Financial Data for the Reporting Period

(Unit: RMB1,000)

Item Consolidated Parent Company

Total profits (before tax) 2,076,681 2,019,903

Net profit attributable to common shareholders of the Company 2,416,842 2,362,902

Net profit attributable to common shareholders of the Company

with deduction of non-recurring profit and loss 2,213,308 2,161,836

Profit from principal operation 2,062,961 2,004,965

Operating profit 2,080,038 2,023,222

Profit from other operations 17,077 18,257

Investment income 1,227,191 1,227,191

Net non-operating income/expenses -3,357 -3,319

Net cash flows from operating activities 35,160,127 35,816,711

Net increase in cash and cash equivalents 15,758,041 15,827,747

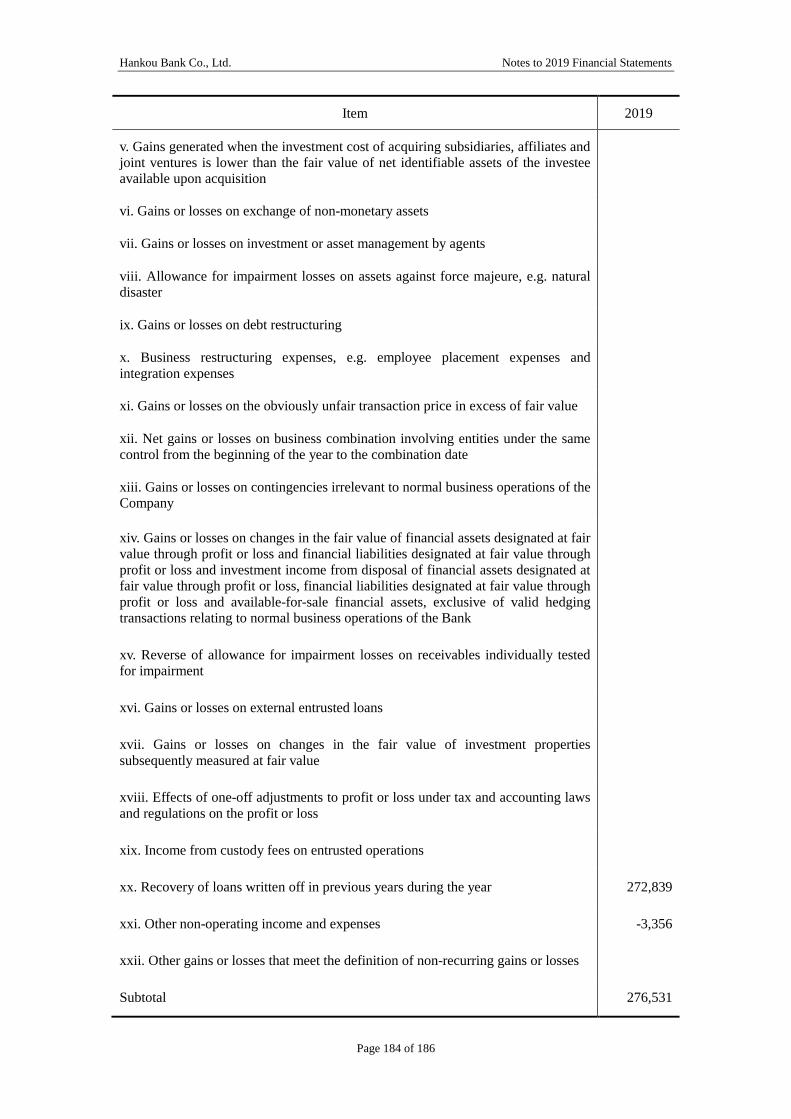

Notes: 1. The non-recurring profit and loss are recognized and calculated in accordance with the Announcements for the Explanation

on the Information Disclosure by Companies that Offer Securities to the Public No.1-Non-recurring Gain and Loss (Announcement

No. 43 of China Securities Regulatory Commission (CSRC) in 2008).

2. Non-recurring profit and loss during the reporting period are presented below:

(Unit: RMB1,000)

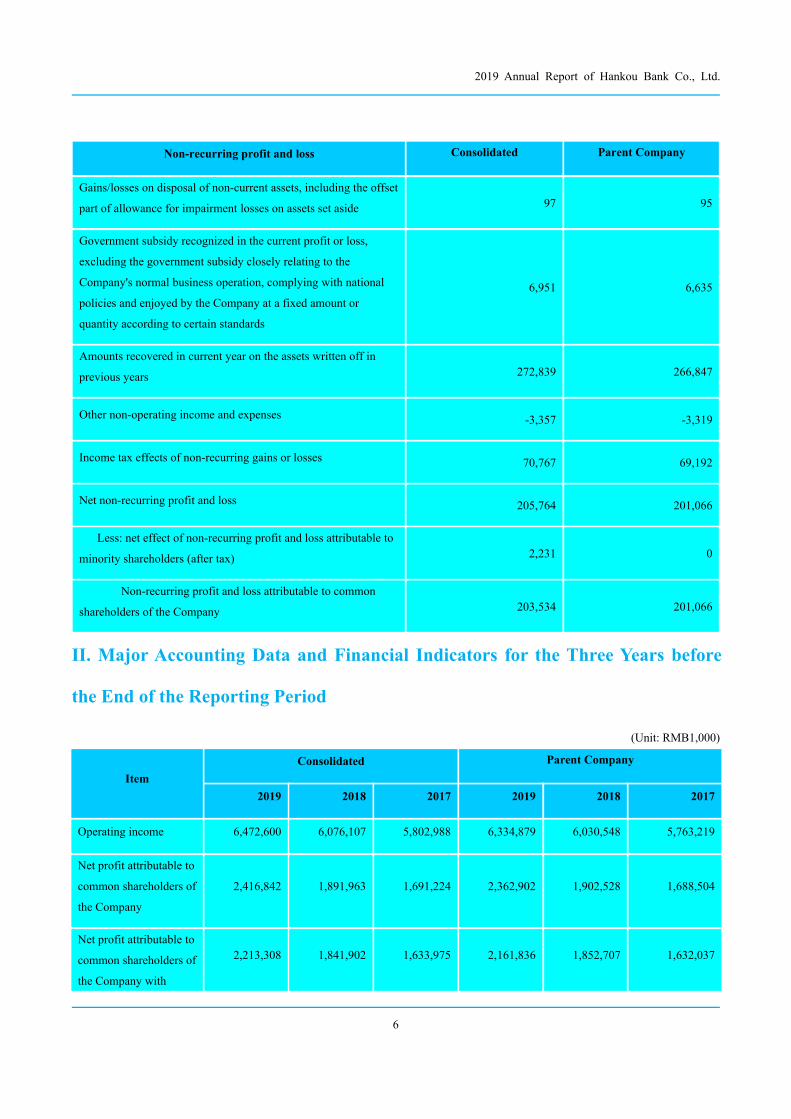

Non-recurring profit and loss Consolidated Parent Company

2019 Annual Report of Hankou Bank Co., Ltd.

6

Non-recurring profit and loss Consolidated Parent Company

Gains/losses on disposal of non-current assets, including the offset

part of allowance for impairment losses on assets set aside 97 95

Government subsidy recognized in the current profit or loss,

excluding the government subsidy closely relating to the

Company's normal business operation, complying with national

policies and enjoyed by the Company at a fixed amount or

quantity according to certain standards

6,951 6,635

Amounts recovered in current year on the assets written off in

previous years 272,839 266,847

Other non-operating income and expenses -3,357 -3,319

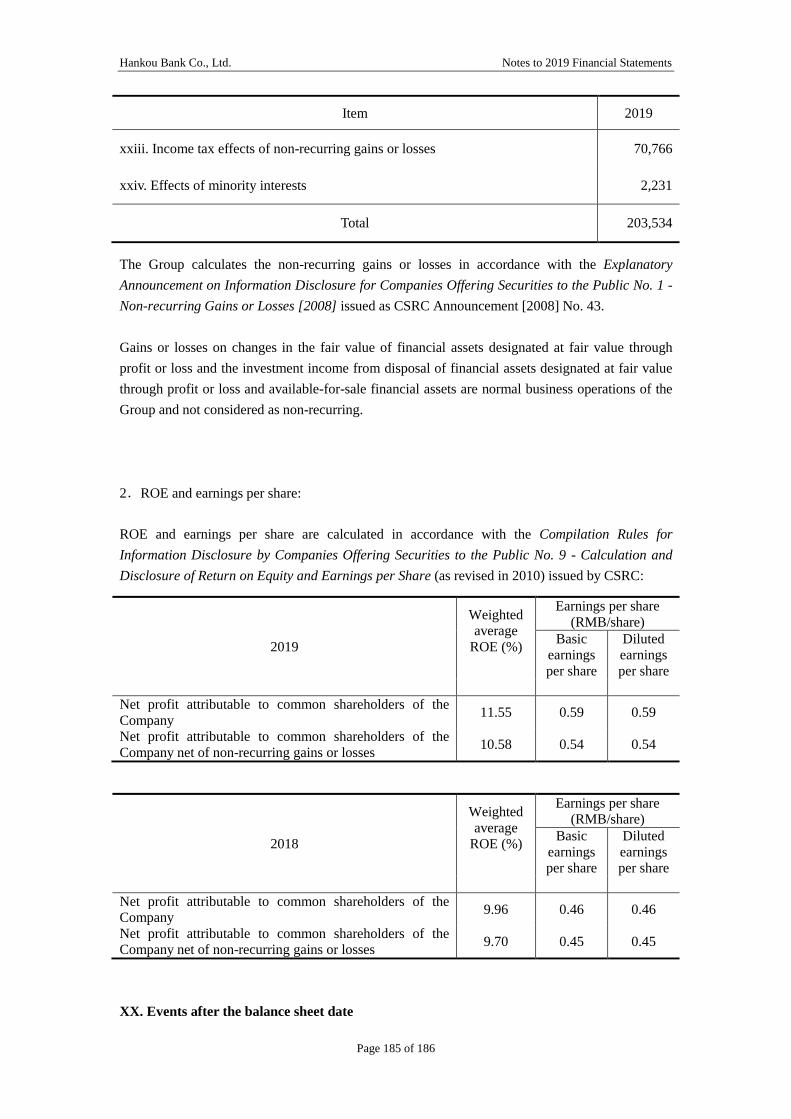

Income tax effects of non-recurring gains or losses 70,767 69,192

Net non-recurring profit and loss 205,764 201,066

Less: net effect of non-recurring profit and loss attributable to

minority shareholders (after tax) 2,231 0

Non-recurring profit and loss attributable to common

shareholders of the Company 203,534 201,066

II. Major Accounting Data and Financial Indicators for the Three Years before

the End of the Reporting Period

(Unit: RMB1,000)

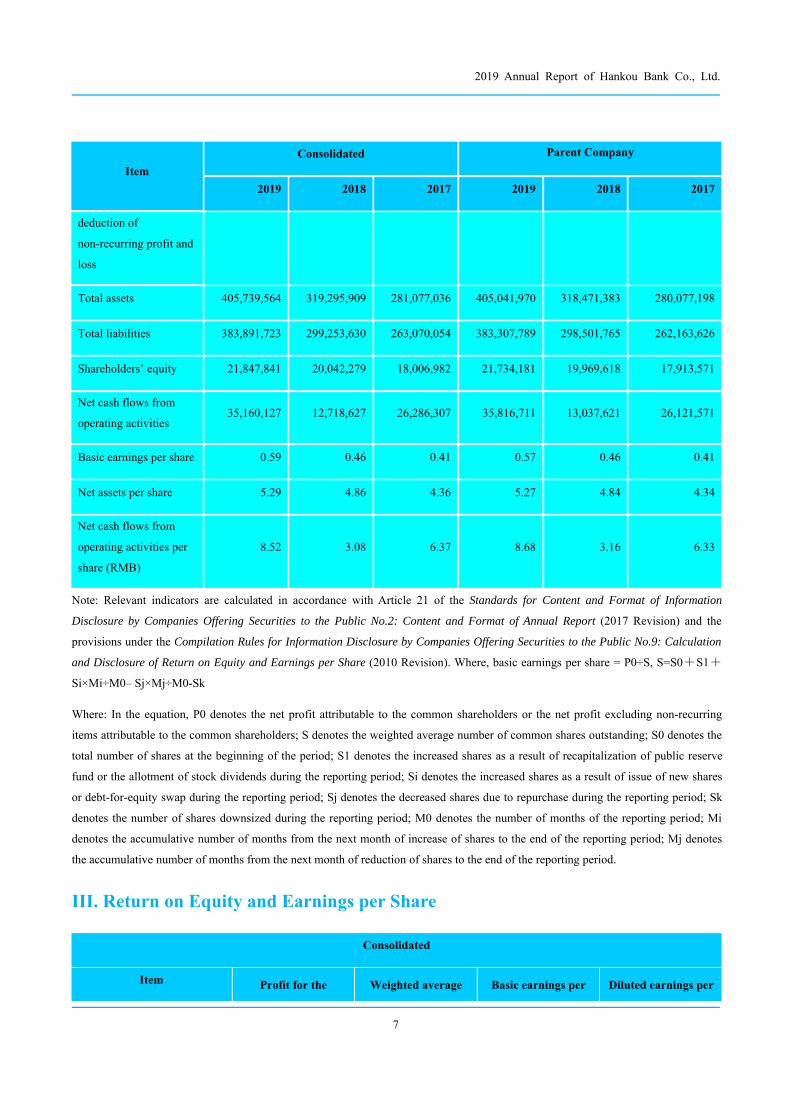

Item

Consolidated Parent Company

2019 2018 2017 2019 2018 2017

Operating income 6,472,600 6,076,107 5,802,988 6,334,879 6,030,548 5,763,219

Net profit attributable to

common shareholders of

the Company

2,416,842 1,891,963 1,691,224 2,362,902 1,902,528 1,688,504

Net profit attributable to

common shareholders of

the Company with

2,213,308 1,841,902 1,633,975 2,161,836 1,852,707 1,632,037

2019 Annual Report of Hankou Bank Co., Ltd.

7

Item

Consolidated Parent Company

2019 2018 2017 2019 2018 2017

deduction of

non-recurring profit and

loss

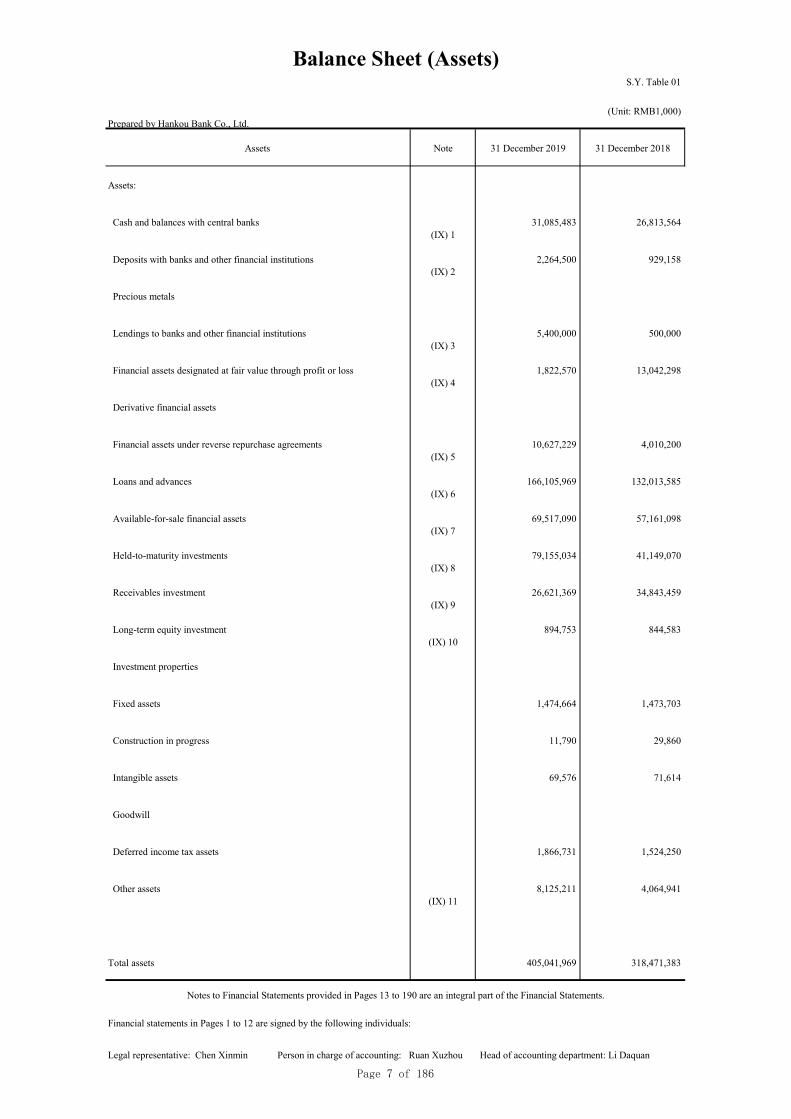

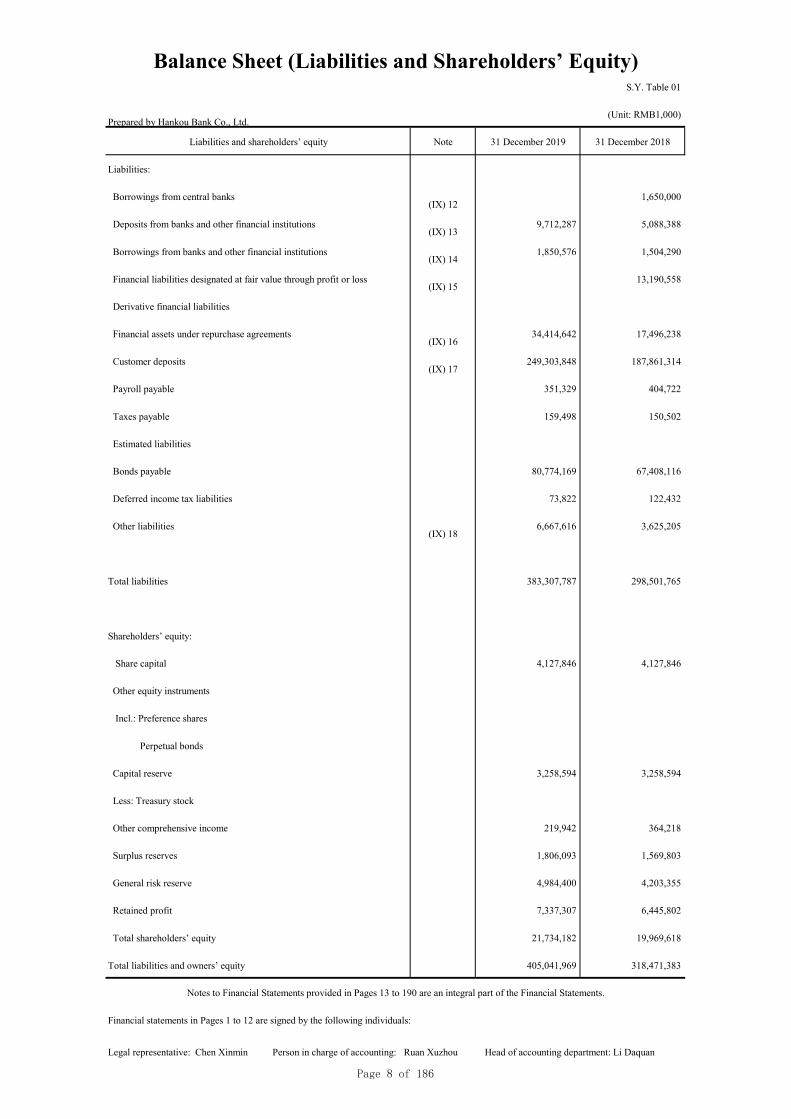

Total assets 405,739,564 319,295,909 281,077,036 405,041,970 318,471,383 280,077,198

Total liabilities 383,891,723 299,253,630 263,070,054 383,307,789 298,501,765 262,163,626

Shareholders’ equity 21,847,841 20,042,279 18,006,982 21,734,181 19,969,618 17,913,571

Net cash flows from

operating activities35,160,127 12,718,627 26,286,307 35,816,711 13,037,621 26,121,571

Basic earnings per share 0.59 0.46 0.41 0.57 0.46 0.41

Net assets per share 5.29 4.86 4.36 5.27 4.84 4.34

Net cash flows from

operating activities per

share (RMB)

8.52 3.08 6.37 8.68 3.16 6.33

Note: Relevant indicators are calculated in accordance with Article 21 of the Standards for Content and Format of Information

Disclosure by Companies Offering Securities to the Public No.2: Content and Format of Annual Report (2017 Revision) and the

provisions under the Compilation Rules for Information Disclosure by Companies Offering Securities to the Public No.9: Calculation

and Disclosure of Return on Equity and Earnings per Share (2010 Revision). Where, basic earnings per share = P0÷S, S=S0+S1+

Si×Mi÷M0– Sj×Mj÷M0-Sk

Where: In the equation, P0 denotes the net profit attributable to the common shareholders or the net profit excluding non-recurring

items attributable to the common shareholders; S denotes the weighted average number of common shares outstanding; S0 denotes the

total number of shares at the beginning of the period; S1 denotes the increased shares as a result of recapitalization of public reserve

fund or the allotment of stock dividends during the reporting period; Si denotes the increased shares as a result of issue of new shares

or debt-for-equity swap during the reporting period; Sj denotes the decreased shares due to repurchase during the reporting period; Sk

denotes the number of shares downsized during the reporting period; M0 denotes the number of months of the reporting period; Mi

denotes the accumulative number of months from the next month of increase of shares to the end of the reporting period; Mj denotes

the accumulative number of months from the next month of reduction of shares to the end of the reporting period.

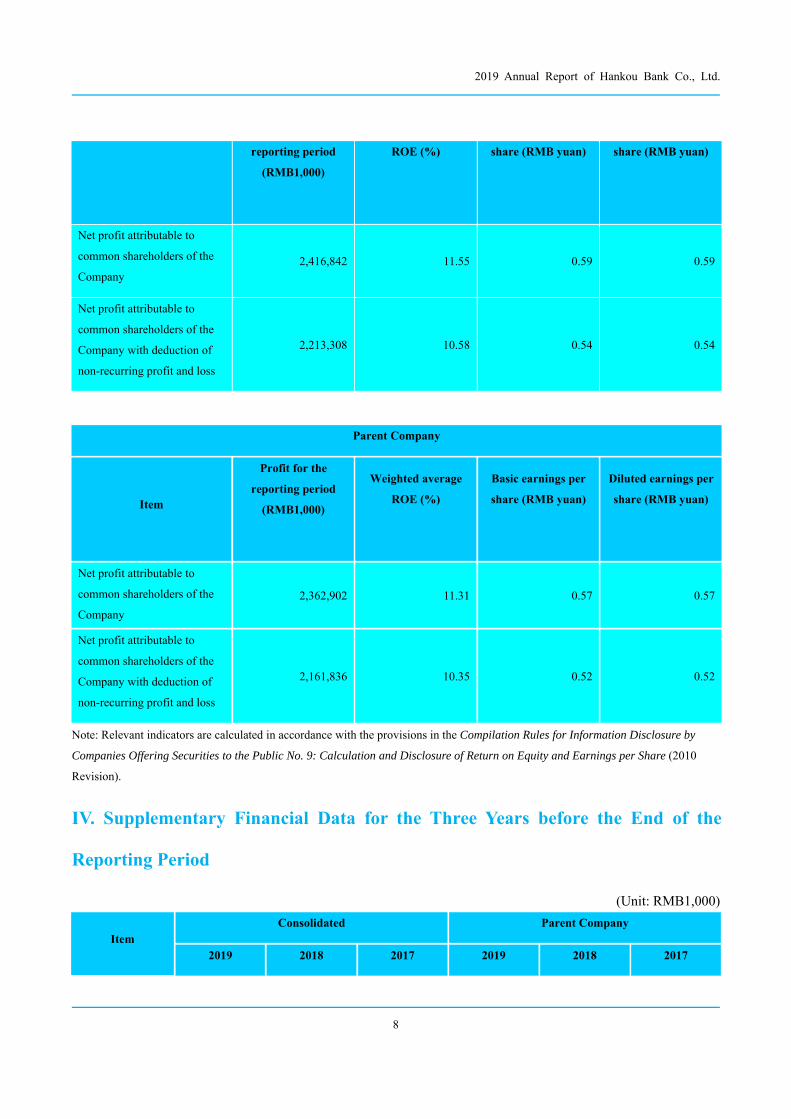

III. Return on Equity and Earnings per Share

Consolidated

Item Profit for the Weighted average Basic earnings per Diluted earnings per

2019 Annual Report of Hankou Bank Co., Ltd.

8

reporting period

(RMB1,000)

ROE (%) share (RMB yuan) share (RMB yuan)

Net profit attributable to

common shareholders of the

Company2,416,842 11.55 0.59 0.59

Net profit attributable to

common shareholders of the

Company with deduction of

non-recurring profit and loss

2,213,308 10.58 0.54 0.54

Parent Company

Item

Profit for the

reporting period

(RMB1,000)

Weighted average

ROE (%)

Basic earnings per

share (RMB yuan)

Diluted earnings per

share (RMB yuan)

Net profit attributable to

common shareholders of the

Company

2,362,902 11.31 0.57 0.57

Net profit attributable to

common shareholders of the

Company with deduction of

non-recurring profit and loss

2,161,836 10.35 0.52 0.52

Note: Relevant indicators are calculated in accordance with the provisions in the Compilation Rules for Information Disclosure by

Companies Offering Securities to the Public No. 9: Calculation and Disclosure of Return on Equity and Earnings per Share (2010

Revision).

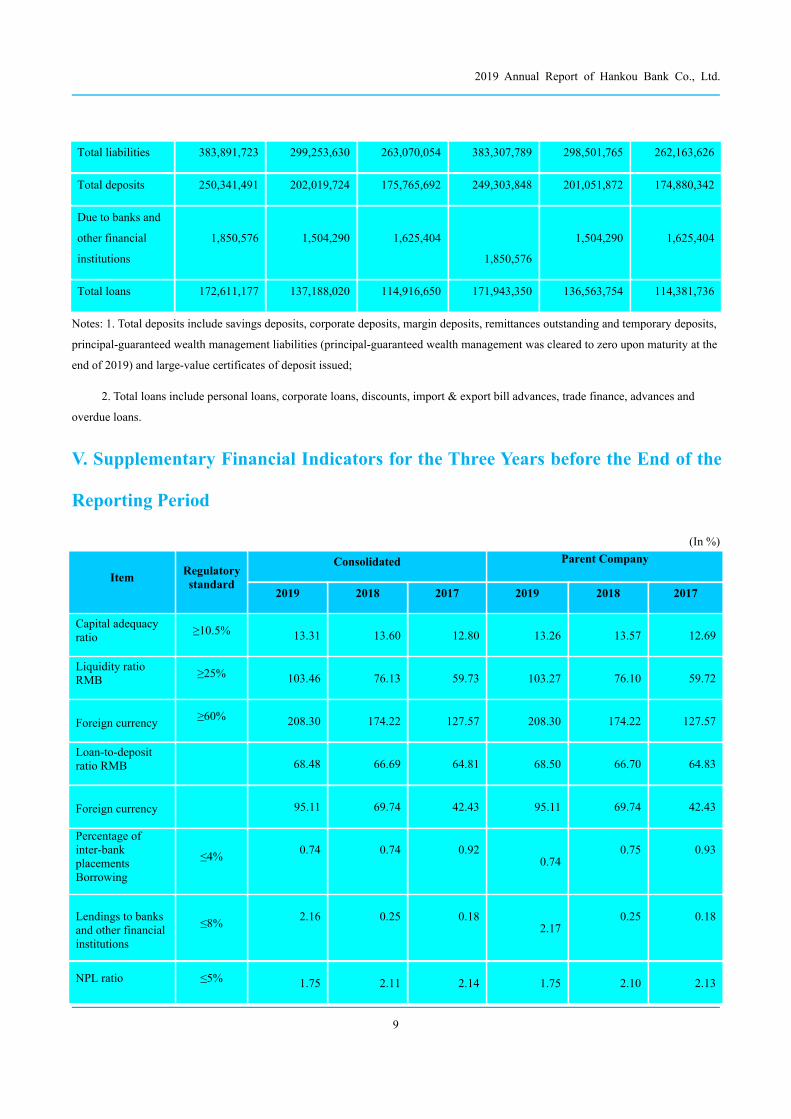

IV. Supplementary Financial Data for the Three Years before the End of the

Reporting Period

(Unit: RMB1,000)

ItemConsolidated Parent Company

2019 2018 2017 2019 2018 2017

2019 Annual Report of Hankou Bank Co., Ltd.

9

Total liabilities 383,891,723 299,253,630 263,070,054 383,307,789 298,501,765 262,163,626

Total deposits 250,341,491 202,019,724 175,765,692 249,303,848 201,051,872 174,880,342

Due to banks and

other financial

institutions

1,850,576 1,504,290 1,625,404

1,850,576

1,504,290 1,625,404

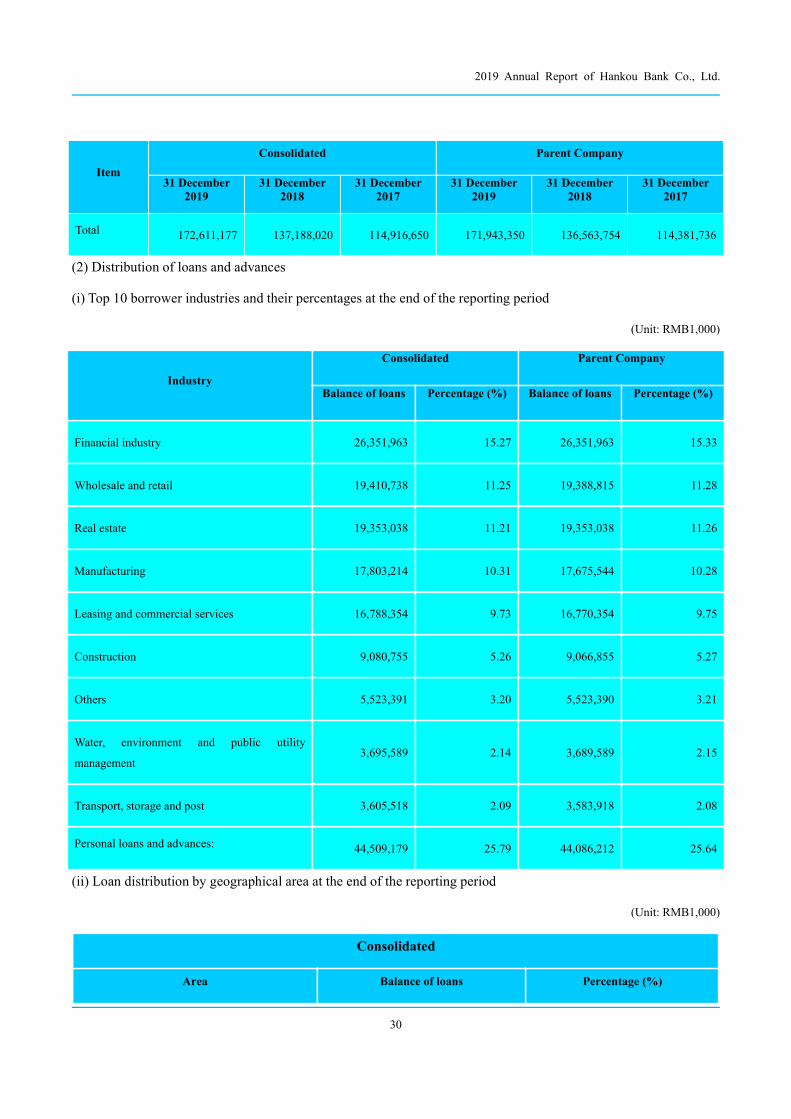

Total loans 172,611,177 137,188,020 114,916,650 171,943,350 136,563,754 114,381,736

Notes: 1. Total deposits include savings deposits, corporate deposits, margin deposits, remittances outstanding and temporary deposits,

principal-guaranteed wealth management liabilities (principal-guaranteed wealth management was cleared to zero upon maturity at the

end of 2019) and large-value certificates of deposit issued;

2. Total loans include personal loans, corporate loans, discounts, import & export bill advances, trade finance, advances and

overdue loans.

V. Supplementary Financial Indicators for the Three Years before the End of the

Reporting Period

(In %)

ItemRegulatorystandard

Consolidated Parent Company

2019 2018 2017 2019 2018 2017

Capital adequacyratio

≥10.5% 13.31 13.60 12.80 13.26 13.57 12.69

Liquidity ratioRMB

≥25% 103.46 76.13 59.73 103.27 76.10 59.72

Foreign currency≥60% 208.30 174.22 127.57 208.30 174.22 127.57

Loan-to-depositratio RMB 68.48 66.69 64.81 68.50 66.70 64.83

Foreign currency 95.11 69.74 42.43 95.11 69.74 42.43

Percentage ofinter-bankplacementsBorrowing

≤4%0.74 0.74 0.92

0.740.75 0.93

Lendings to banksand other financialinstitutions

≤8%2.16 0.25 0.18

2.170.25 0.18

NPL ratio ≤5% 1.75 2.11 2.14 1.75 2.10 2.13

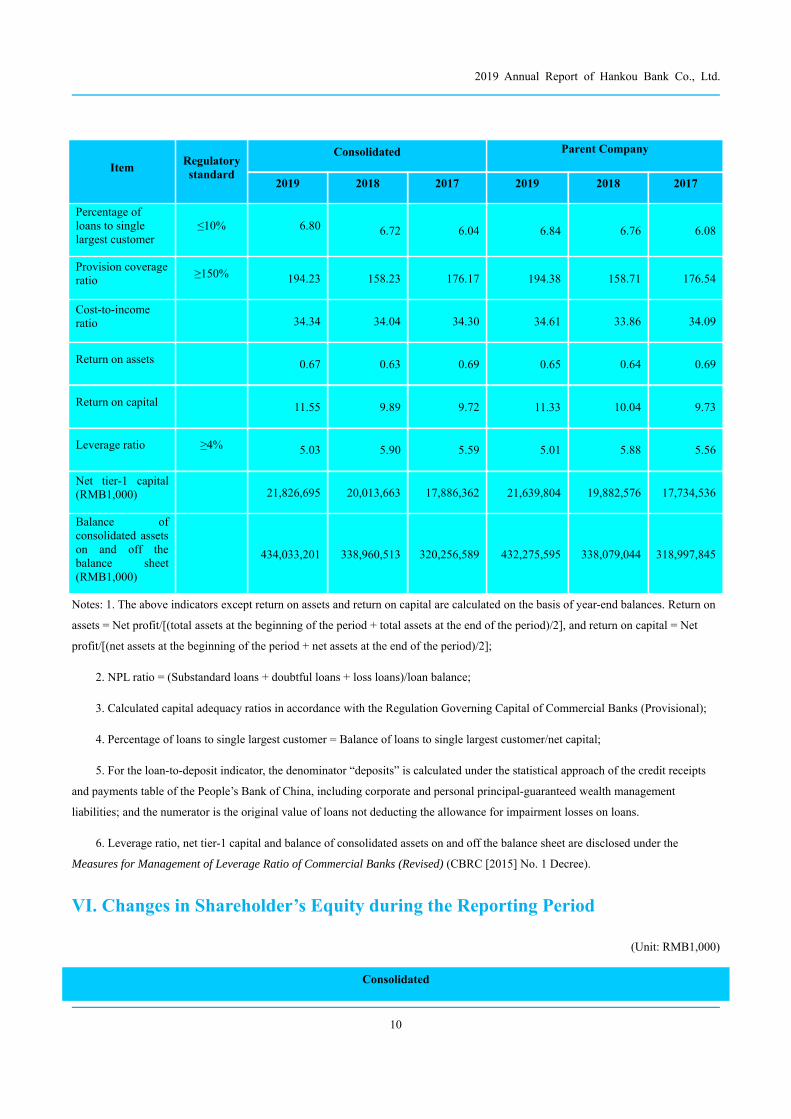

2019 Annual Report of Hankou Bank Co., Ltd.

10

ItemRegulatorystandard

Consolidated Parent Company

2019 2018 2017 2019 2018 2017

Percentage ofloans to singlelargest customer

≤10% 6.80 6.72 6.04 6.84 6.76 6.08

Provision coverageratio

≥150% 194.23 158.23 176.17 194.38 158.71 176.54

Cost-to-incomeratio 34.34 34.04 34.30 34.61 33.86 34.09

Return on assets 0.67 0.63 0.69 0.65 0.64 0.69

Return on capital 11.55 9.89 9.72 11.33 10.04 9.73

Leverage ratio ≥4% 5.03 5.90 5.59 5.01 5.88 5.56

Net tier-1 capital(RMB1,000) 21,826,695 20,013,663 17,886,362 21,639,804 19,882,576 17,734,536

Balance ofconsolidated assetson and off thebalance sheet(RMB1,000)

434,033,201 338,960,513 320,256,589 432,275,595 338,079,044 318,997,845

Notes: 1. The above indicators except return on assets and return on capital are calculated on the basis of year-end balances. Return on

assets = Net profit/[(total assets at the beginning of the period + total assets at the end of the period)/2], and return on capital = Net

profit/[(net assets at the beginning of the period + net assets at the end of the period)/2];

2. NPL ratio = (Substandard loans + doubtful loans + loss loans)/loan balance;

3. Calculated capital adequacy ratios in accordance with the Regulation Governing Capital of Commercial Banks (Provisional);

4. Percentage of loans to single largest customer = Balance of loans to single largest customer/net capital;

5. For the loan-to-deposit indicator, the denominator “deposits” is calculated under the statistical approach of the credit receipts

and payments table of the People’s Bank of China, including corporate and personal principal-guaranteed wealth management

liabilities; and the numerator is the original value of loans not deducting the allowance for impairment losses on loans.

6. Leverage ratio, net tier-1 capital and balance of consolidated assets on and off the balance sheet are disclosed under the

Measures for Management of Leverage Ratio of Commercial Banks (Revised) (CBRC [2015] No. 1 Decree).

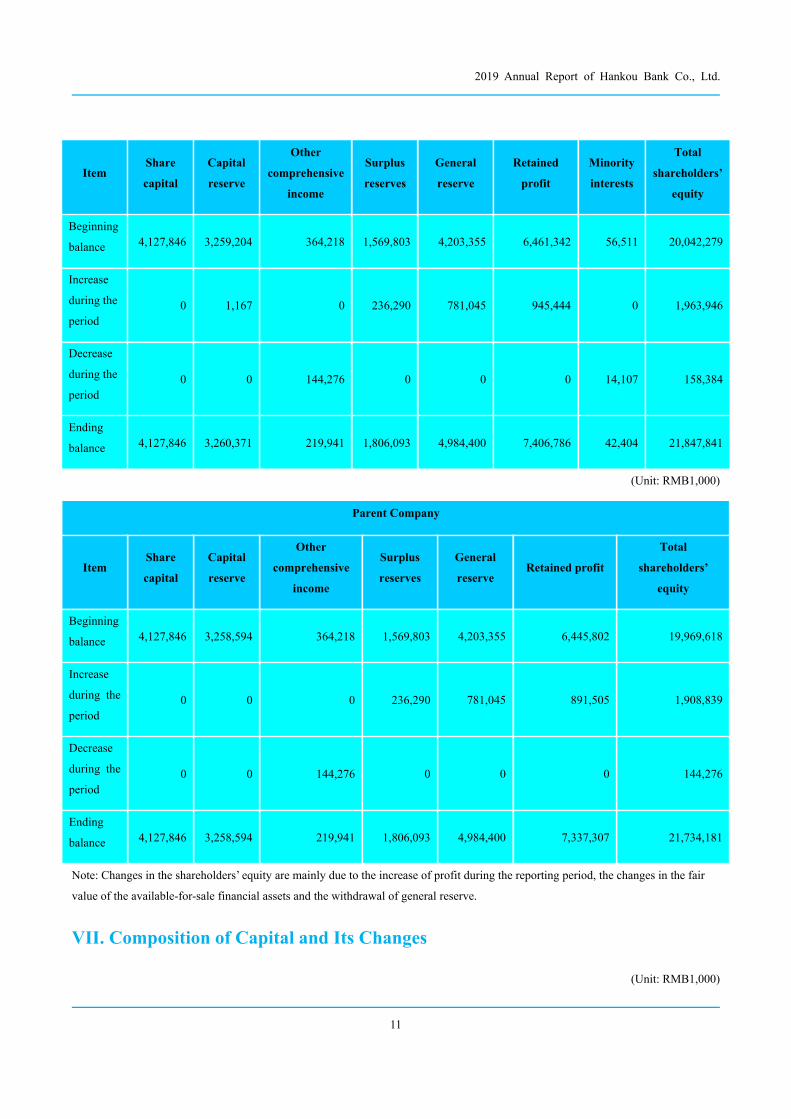

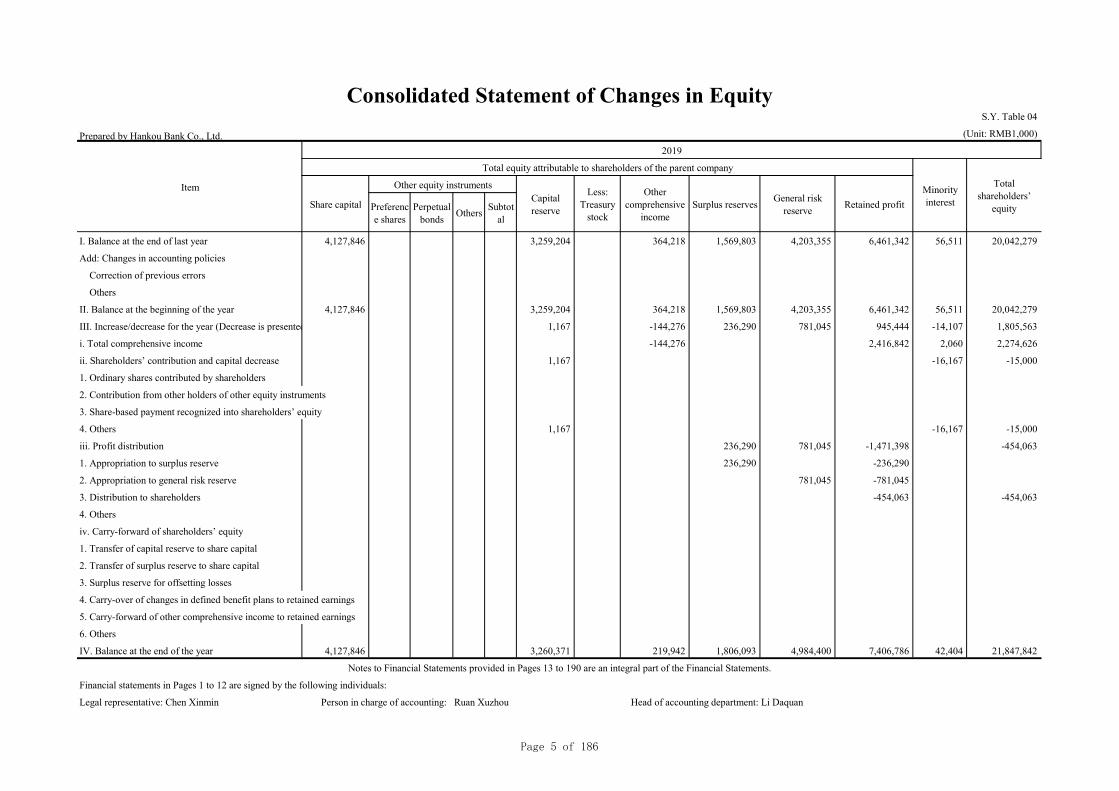

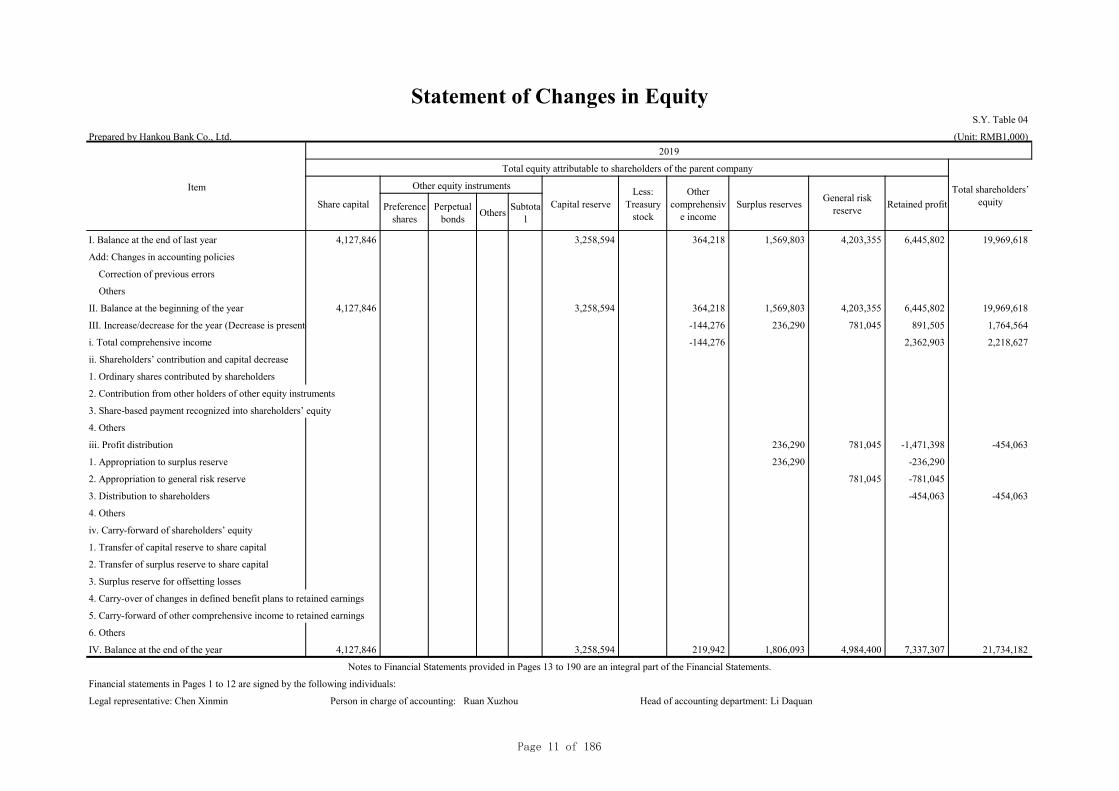

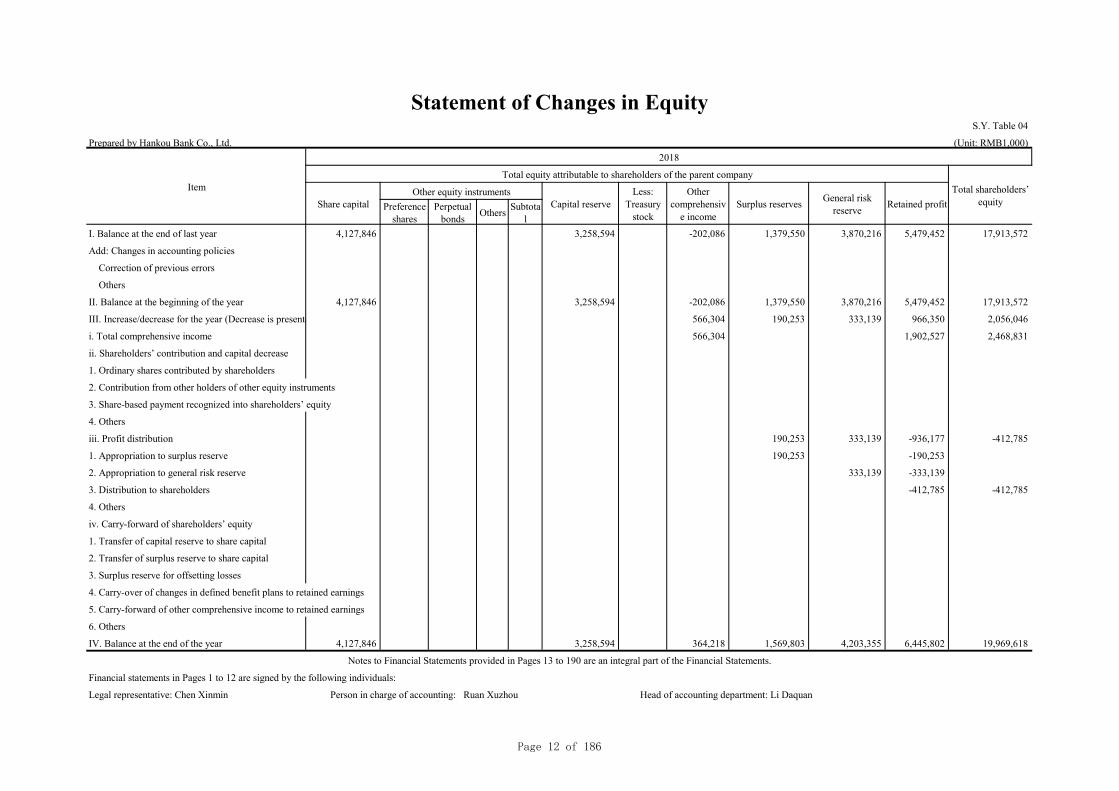

VI. Changes in Shareholder’s Equity during the Reporting Period

(Unit: RMB1,000)

Consolidated

2019 Annual Report of Hankou Bank Co., Ltd.

11

ItemShare

capital

Capital

reserve

Other

comprehensive

income

Surplus

reserves

General

reserve

Retained

profit

Minority

interests

Total

shareholders’

equity

Beginning

balance 4,127,846 3,259,204 364,218 1,569,803 4,203,355 6,461,342 56,511 20,042,279

Increase

during the

period0 1,167 0 236,290 781,045 945,444 0 1,963,946

Decrease

during the

period0 0 144,276 0 0 0 14,107 158,384

Ending

balance 4,127,846 3,260,371 219,941 1,806,093 4,984,400 7,406,786 42,404 21,847,841

(Unit: RMB1,000)

Parent Company

ItemShare

capital

Capital

reserve

Other

comprehensive

income

Surplus

reserves

General

reserveRetained profit

Total

shareholders’

equity

Beginning

balance 4,127,846 3,258,594 364,218 1,569,803 4,203,355 6,445,802 19,969,618

Increase

during the

period0 0 0 236,290 781,045 891,505 1,908,839

Decrease

during the

period0 0 144,276 0 0 0 144,276

Ending

balance 4,127,846 3,258,594 219,941 1,806,093 4,984,400 7,337,307 21,734,181

Note: Changes in the shareholders’ equity are mainly due to the increase of profit during the reporting period, the changes in the fair

value of the available-for-sale financial assets and the withdrawal of general reserve.

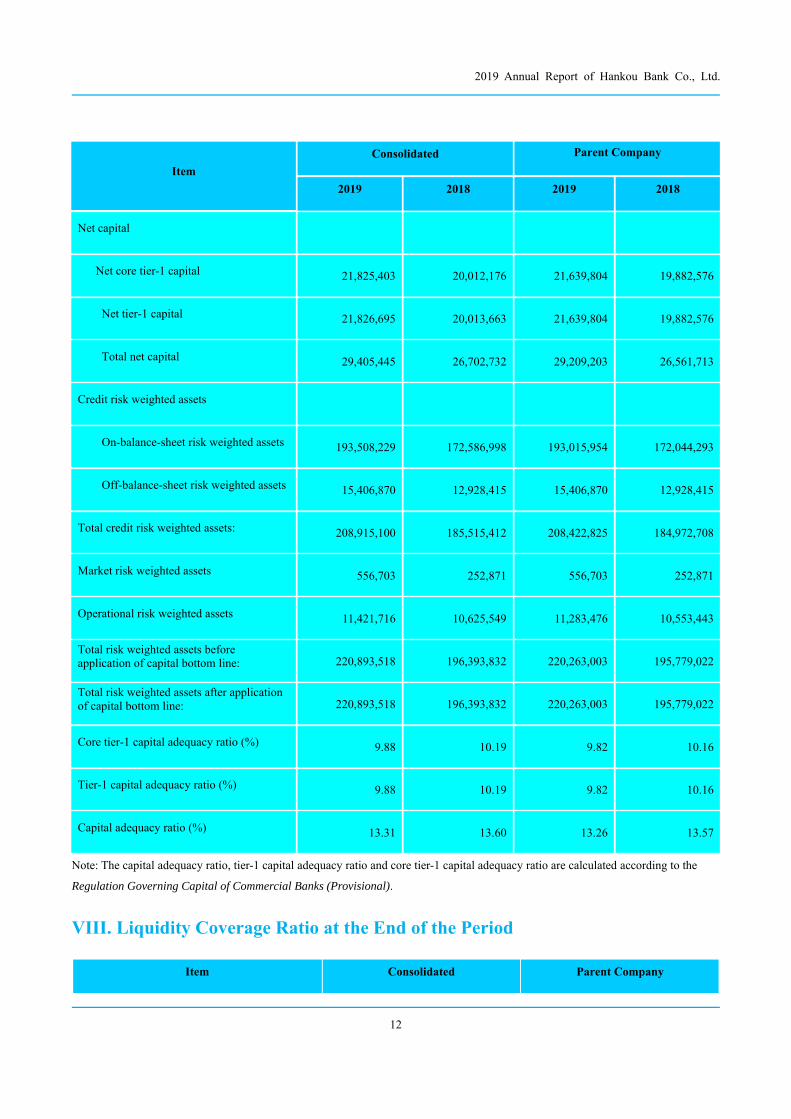

VII. Composition of Capital and Its Changes

(Unit: RMB1,000)

2019 Annual Report of Hankou Bank Co., Ltd.

12

Item

Consolidated Parent Company

2019 2018 2019 2018

Net capital

Net core tier-1 capital 21,825,403 20,012,176 21,639,804 19,882,576

Net tier-1 capital 21,826,695 20,013,663 21,639,804 19,882,576

Total net capital 29,405,445 26,702,732 29,209,203 26,561,713

Credit risk weighted assets

On-balance-sheet risk weighted assets 193,508,229 172,586,998 193,015,954 172,044,293

Off-balance-sheet risk weighted assets 15,406,870 12,928,415 15,406,870 12,928,415

Total credit risk weighted assets: 208,915,100 185,515,412 208,422,825 184,972,708

Market risk weighted assets 556,703 252,871 556,703 252,871

Operational risk weighted assets 11,421,716 10,625,549 11,283,476 10,553,443

Total risk weighted assets beforeapplication of capital bottom line: 220,893,518 196,393,832 220,263,003 195,779,022

Total risk weighted assets after applicationof capital bottom line: 220,893,518 196,393,832 220,263,003 195,779,022

Core tier-1 capital adequacy ratio (%) 9.88 10.19 9.82 10.16

Tier-1 capital adequacy ratio (%) 9.88 10.19 9.82 10.16

Capital adequacy ratio (%) 13.31 13.60 13.26 13.57

Note: The capital adequacy ratio, tier-1 capital adequacy ratio and core tier-1 capital adequacy ratio are calculated according to the

Regulation Governing Capital of Commercial Banks (Provisional).

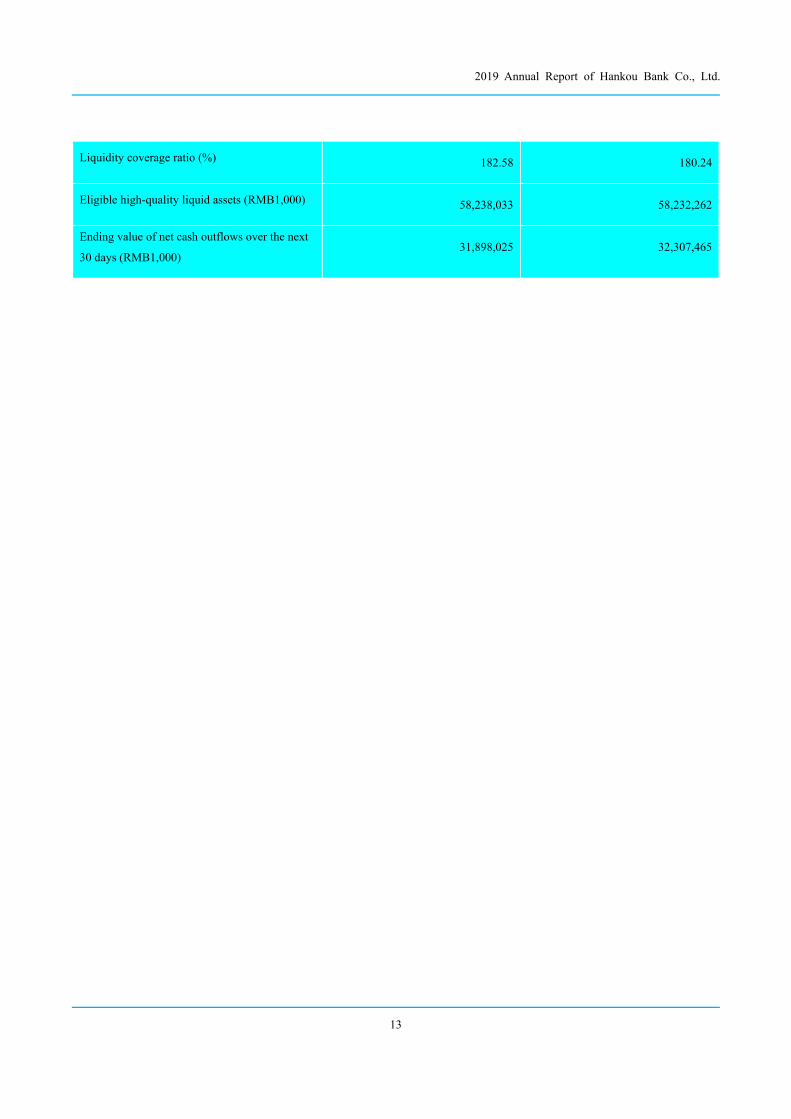

VIII. Liquidity Coverage Ratio at the End of the Period

Item Consolidated Parent Company

2019 Annual Report of Hankou Bank Co., Ltd.

13

Liquidity coverage ratio (%) 182.58 180.24

Eligible high-quality liquid assets (RMB1,000) 58,238,033 58,232,262

Ending value of net cash outflows over the next

30 days (RMB1,000)31,898,025 32,307,465

2019 Annual Report of Hankou Bank Co., Ltd.

14

Chapter IV Report of the Board of Directors

I. Management Discussion and Analysis

i. Business review during the reporting period

1. Scope of principal operations

Principal operations of the Company are deposits taking, extension of short, medium and long-term loans, domestic

settlement, bill discounting, issuance of financial bonds, commissioned issuance, honoring and underwriting of

government bonds, trading over government bonds, interbank lending, provision of security, agency

collection/payment and insurance, provision of safety deposit box services, entrusted deposits and loans on behalf

of local public finance, foreign exchange deposits, foreign exchange loans, foreign exchange remittance, foreign

currency conversion, foreign exchange guarantee, credit reference, inquiry and witness services, international

settlement, interbank foreign exchange lending, foreign exchange settlement, foreign exchange sales, foreign

exchange trading on its own behalf and as an agent, foreign exchange borrowings, trading or agency trading over

non-stock foreign currency securities, policy-related housing finance services, and other services approved by the

CBIRC Hubei Office and the State Administration of Foreign Exchange.

2. Performance review during the reporting period

In 2019 with economic and financial complexities and tough market environment, the Bank overcame difficulties

under self-inflicted pressure according to the work plan that “take leading peers as benchmark, fighting three tough

battles”, delivering good results based on the high comparison level in 2018.

2.1 Fulfillment of operating targets across the Bank

At the end of 2019, the Bank’s total assets reached RMB405,042 million, an increase of RMB86,571 million or

27.18% over the previous year. The balance of deposits amounted to RMB249,304 million1, an increase of

RMB48,252 million or 24.00% over the previous year. The balance of loans amounted to RMB171,943 million, an

increase of RMB35,380 million or 25.91% over the previous year. The balance of net assets totaled RMB21,734

million, an increase of RMB1,765 million or 8.84% over the previous year.

In 2019, the Bank reported a net profit of RMB2,363 million, an increase of RMB460 million or 24.20% over the

previous year.

Accumulated intermediary business income registered RMB963 million, accounting for 15.20% of net operating

income.

As at the end of the reporting period, the balance and ratio of non-performing loans were RMB3,003 million and

1.75% respectively. Provision coverage ratio was 194.38%, better than regulatory standard.

2.2 Progress was made in the transition from old to new growth drivers

1 According to the PBOC statistical criteria, the balance of deposits at the end of 2018 included RMB13.2 billion of principal-guaranteed wealthmanagement products. The accounting firm restated them in “financial liabilities designated at fair value through profit or loss”. At the end of 2019, thebalance of principal-guaranteed wealth management products was cleared to zero.

2019 Annual Report of Hankou Bank Co., Ltd.

15

The corporate customer base was restructured vigorously. The number of trade finance customers grew by 178%

year-on-year. 77 supply chain projects were implemented in the year, with the first ever independent lead

underwriting deal accomplished and the first residential mortgage-backed security (RMBS) successfully issued.

Investment banking, trade finance, transaction banking, wealth management and credit card business were

developed with vigor, pushing intermediary business income up by 35% year-on-year. The Bank worked hard to

address regional imbalance in development and structural imbalance in business, with a focus on major business

areas and weaker fields of management, such as quality and compliance.

2.3 The way of serving the real economy was increasingly enriched.

The Bank served major government strategies, cumulatively granting RMB231.3 billion of credits, on or off

balance sheet, and held RMB21,547 million of local government bonds with a focus on high-quality development

areas in Hubei and the “Two Points” positioning of Chongqing. In serving emerging industries, the Bank became

the first banking lender to the PPP project of the Wuhan National Aerospace Industry Base, extended integrated

credit to Yangtze Memory Technologies Co., Ltd. and supported 35 major investment promotion projects. In

serving the private-sector economy, the Bank took actions to serve private enterprises with financial services and

introduced measures to improve the business environment. The balance of loans to private enterprises increased by

RMB10,231 million over the beginning of the year. The Bank’s case of serving the private-sector real economy

won the first prize for excellent cases awarded by the Asian Financial Cooperation Association. In serving poverty

alleviation, the Bank carried out financial service-based precision poverty alleviation with vigor and further

performed its duty. The Bank’s balance of precision poverty alleviation loans was RMB362 million, up 31.49%

from the beginning of the year.

2.4 The pursuit of innovation-driven development yielded new results

In terms of technology finance, the Bank developed the “STAR IPO Loan” for seeded enterprises for the Star

Market of Shanghai Stock Exchange. A total of 40 STAR seeded enterprises in Hubei were served, including the

enterprise supported by the first “venture loan” in China’s banking industry that successfully went public on the

STAR Market. In terms of MSE finance, an innovative integrated inclusive finance business system was launched,

with nearly 4,000 new customers added and over RMB1 billion of new loans granted, achieving the “Two Increases,

Two Curbs” regulatory targets. In terms of Internet finance, 30 Internet finance innovations were introduced,

bringing personal financial assets in direct banking to a level beyond RMB10 billion. In terms of everyday financial

services, the Bank strengthened “Financial Plus” everyday, government and consumer services by rolling out over

30 everyday financial products. In terms of services for the 7th CISM Military World Games, the Bank enhanced

support during key time intervals and at major outlets during the event, including online customer service

representatives and offline “bilingual” guides at outlets, extending service recipients to players, staff, volunteers

and foreign guests to the Games.

2.5 Comprehensive risk management took on a new look

In the battle for asset quality enhancement, a multi-level supervision mechanism was implemented to monitor

organizations, people and projects according to plan and schedule. In the battle for compliance, a register focused

on “three fields, one priority” was established, “account closure” management was carried and the “troubleshooting

project” as advanced to crack down on non-compliances. In terms of building the comprehensive risk management

2019 Annual Report of Hankou Bank Co., Ltd.

16

system, the new-generation credit risk management system development was accelerated.

2.6 IT development made new progress

The three-year plan for FinTech of the Bank was further implemented. The leading group on major information

system projects was established to ensure major projects are completed to schedule and quality criteria. FinTech

penetration into business was carried out continuously to boost business innovation. The online supply chain

platform, the MSE inclusive finance system and the integrated investment banking platform were built successively

in 2019. The existing big data platform was further exploited to provide decision-making support for customer

acquisition and marketing. The Bank’s data governance system began to reap the harvest. The Data Governance

Committee and the working group on data governance were established to promote fine-grained implementation of

all data governance work. The Internet security was enhanced through increasingly strengthened top-level design of

information security, and certified for ISO 27001. The information security system was comprehensively enhanced.

The dynamic security protection platform and the threat intelligence analysis platform were imported. As at the end

of 2019, the Bank had 127 IT staff, representing 3.1% of total headcount. The Bank spend RMB159 million in

information technology this year.

2.7 The foundation of operation and management was further reinforced.

Corporate governance was improved, with the Board of Directors, the Board of Supervisors and the senior

management re-elected. Another round of share capital increase was advanced. The quality and efficiency of

swindle prevention work were enhanced, with the responsibility for swindle prevention well assigned to

management personnel at each level and coordinated efforts made on annual key work on swindle prevention.

Bank-wide safety and stability were assured by formulating contingency plans against some bank risk incidents,

nipping problems in the bud and strengthening market monitoring. The “wartime” mechanism requirement was

implemented for the 7th CISM Military World Games. The Bank strengthened team building and sent young

officers to branches and sub-branches on secondment to strengthened their leadership staffing.

2.8 Development led by Party building went deeper

The Bank carried out the “Staying True to Our Founding Mission” themed education program and a range of

required activities, including studies, surveys, topical Party classes and topical democratic meetings under the

guiding principle of studying and implementing the Xi Jinping Thought on Socialism with Chinese Characteristics

for a New Era. The Bank cemented the outputs of the “Year of Development Led by Party Building” program,

increased the depth of “Party Building Plus”, improved the primary-level Party building assessment measures and

built the “Red Smelter” of amateur Party schools. To further improve Party conduct and uphold integrity, a conduct

supervision group was established to cement the outcomes of strict bank governance. The total-process

accountability mechanism for credit business was improved to further enforce accountability for credit

non-compliances.

3. Operation of main businesses

3.1 Corporate banking

3.1.1 Corporate business

2019 Annual Report of Hankou Bank Co., Ltd.

17

During the reporting period, the Bank deepened the philosophy of “serving you with idea” in line with the

regulatory orientation and stayed true to its principal responsibility and business. By serving the real economy,

broadening the mind, enhancing professional capabilities, boosting development vitality and promoting business

transformation, the Bank managed to make solid progress in high-quality development. SME financial services

achieved the “Two Increases, Two Curbs” regulatory targets. The Bank strictly abided by the rules for “Two Bans,

To Restrictions”, “Seven Nos” and “Four Opens”, provided strong support for the development of private MSEs

and established Hankou Bank’s financial service system supporting SME development.

(1) Corporate deposits: As at the end of the reporting period, the balance of the Bank’s corporate deposits reported

RMB160,639 million, an increase of RMB27,821 million or 20.95% over the beginning of the year.

(2) Corporate loans: As at the end of the reporting period, the balance of the Bank’s corporate loans reported

RMB127,857 million, an increase of RMB26,263 million or 25.85% over the beginning of the year. Among those,

the balance of loans to small and micro enterprises reached RMB38,708 million, an increase of RMB5,291 million

or 15.83% over the beginning of the year.

(3) International banking: As at the end of the reporting period, the Bank reported an international settlement

volume of USD2,423 million, an increase of USD229 million or 10.41% over the beginning of the year.

(4) Intermediary business income: As at the end of the reporting period, the Bank generated an intermediary

corporate business income of RMB462 million, an increase of RMB125 million or 37.14% year-on-year.

3.1.2 Investment banking

During 2019, the Bank adhered to the economic and financial policies. The investment banking business returned

to the original mission of serving the real economy, working as an engine for transformation of corporate business.

They adhered to the development path of “light capital, pursuit of reform, and strict risk management”. It continued

to innovate services and products, enriched service methods, enhanced the capability of post-investment risk

prevention, and effectively and efficiently promoted collaboration with multiple lines in the Bank.

As at the end of the reporting period, balance of investment banking assets stood at RMB33.7 billion. RMB11.6

billion of financing was granted in the year and balance of investment banking assets rose by RMB3.3 billion.

Financing under debt financing plans stood at RMB5.13 billion, ranking first across Hubei Province. The Bank

underwrote 21 debt financing instruments as lead underwriter in the year, ranking third province-wide, and

underwriting shares amounted to RMB6.51 billion, ranking eighth province-wide and up RMB1.46 billion from the

previous year. 395 bonds were distributed with an aggregate value of RMB35 billion, the highest across Hubei

Province.

(1) Adhering to product innovation

During the reporting period, the Bank issued RMB3,511 million of residential mortgage-backed security (RMBS).

Its successful issuance helped expand the Bank’s sources of funding, accelerate turnover of credit funds and

optimize allocation of resources across the Bank.

(2) A number of “first-of-its-kind” lead underwriting deals were accomplished

During the reporting period, the Bank issued the 2019 commercial paper of Wuhan Municipal Construction Group

2019 Annual Report of Hankou Bank Co., Ltd.

18

Co., Ltd. as independent lead underwriter for the first time. Subsequently the commercial paper of Hongshan City

Construction Investment, the super-short-term commercial paper of Tus Environmental, the super-short-term

commercial paper of Humanwell Healthcare and the super-short-term commercial paper of Jointown

Pharmaceutical, for which the Bank served as independent lead underwriter, were registered and issued. These

independent lead underwriting deals marked a new milestone in the Bank’s capability of “solicitation, undertaking

and underwriting” in the lead underwriting business.

(3) New channels were developed for non-standard business

In 2019, the Bank successfully had a number of peer institutions participate in a RMB1,615 million debt financing

plan registered and issued by it. The project served customers of the Bank, generated light-capital income and

pointed to a new direction of investment banking development.

3.2 Retail banking

3.2.1 Overview

During the reporting period, the Bank continued to foster the “neighborhood finance” brand, carried forward the

local “neighborhood culture” under the traditional Chinese philosophy that “a far-off relative is not as helpful as a

near neighbor” and built an online-offline integrated service system featuring “hearty finance” and “neighbor

service”. The Bank furthered the social security card-based inclusive finance services, tapped deep into distinctive

community banking services and launched a wide variety of innovative “Jointown” series products. Retail banking

maintained good momentum of growth, showing continuous improvements in professional value and regional

competitiveness. “Neighborhood finance” and “Jointown” brands became increasingly influential in market.

3.2.2 Personal financial assets

The Bank adapted itself to customers’ demand for diversity of financial assets and met their wealth management

needs in terms of earning, liquidity and safety. By improving business structure and attracting target customers, the

Bank steadily expanded the size of personal financial assets. At the end of 2019, personal financial assets grew by

24.78%, with a three-year compound annual growth rate of over 18%. The Bank continued to enhance its deposit

taking capacity by providing distinctive products and services, maintaining stable growth in savings deposits. The

balance of savings deposits grew by 29.85%. The balance of principal-guaranteed wealth management products

were reduced to zero.

3.2.3 Personal consumption loans

The Bank integrated online and offline development of personal consumer loans to serve the diverse consumer

needs. The Bank implemented the real estate regulation policy of the State, strictly implemented the differentiated

housing credit policy and gave priority to the needs of first-time homebuyers while supporting the loan demand of

home upgraders and curbing speculative trading in housing market. LPR was steadily applied to residential

mortgages. The Bank developed online high-quality channels for cooperation, enriched online business varieties,

enhanced fine-grained operation and management and enhanced online service capacity. The Bank issued the

RMB3,511 million Jointown 2019 Residential Mortgage-Backed Security Tranche I, in a bid to increase the return

on asset operation, liquidize remnant assets and improve the credit structure. At the end of 2019, personal

consumption loans grew by 35.57%.

2019 Annual Report of Hankou Bank Co., Ltd.

19

3.2.4 Credit cards

The Bank continued to improve the credit card business structure, carried out business innovation, diversified

customer acquisition channels and kept enhancing the service capacity. Under the “micro and decentralized”

principle of credit card business, the Bank made solid moves in marketing toward “demand depositors” and

developed distinctive credit card installment facilities. As at the end of 2019, credit card overdrafts grew by

35.27%.

3.2.4 Debit cards

The Bank attached importance to reinforcing the foundation of debit card business, upgrading payment channels

and fostering a secure and convenient environment for debit card users. Such special customer groups as social

security card holders, Jointown co-branded card holders and Jointown themed card holders were expanded

vigorously to win broad market recognition. At the end of 2019, the total number of debit cards issued grew by

8.68%.

3.2.5Entrusted loans under housing provident funds

The Bank implements the local and national policies on entrusted loans under housing provident funds, persistently

regards entrusted loans under housing provident funds as a service for people’s wellbeing, introduces innovative

service models, improves business processes, enhances improves the quality and efficiency of service to boost its

market position. As at the end of 2019, the balance of entrusted loans under housing provident fund grew by 84.3%.

3.3 Financial market business

3.3.1 Main operating results

During the reporting period, the Bank’s financial market business was sound and developed in compliance with

regulations. While continuing to develop bond investment, interbank investment, wealth management agency,

foreign exchange, bills, etc., the Bank also integrated market channel resources, optimized the structure of assets

and liabilities, and strengthened internal control & compliance efforts. In the complex and ever-changing financial

market environment, the Bank ensured continuous improvement in operating capacity and market influence.

(1) Treasury operation

During the reporting period, the Bank recorded RMB4.53 trillion in pledge-type repurchases and RMB3.52 trillion

in spot bond transactions. It won such awards and honors as Top 300 Interbank RMB Market Dealers 2019, Active

Dealers in the Interbank RMB Market, ChinaBond Excellent Proprietary Trader, ChinaBond Excellent Market

Making Settlement Agency for Treasury Bonds, ChinaBond Excellent Market Making and Settlement Agency for

Local Government Bonds and ChinaBond Outstanding Contributor to Collateral Business.

(2) Asset management business

At the end of the reporting period, the Bank registered RMB55,796 million in balance of proprietary wealth

management products, down RMB136 million or 0.24% year-on-year.

(3) Bills business

2019 Annual Report of Hankou Bank Co., Ltd.

20

During the reporting period, the Bank registered nearly RMB1 trillion in bills financing, making itself a vibrant city

commercial bank in the bills market. Through imposing control at both front and middle offices, reasonably

arranging the business operation strategy and harnessing the role of Bills Appraisal Committee, the Bank ensured

scientific and complying major decisions under the guiding principle of “Shared Wisdom and Joint Risk

Identification” and in pursuit of sustained, steady business development and transformation. The Bank maintained

the record of six zeros (zero case, zero incident, zero fake bill, zero non-performing asset, zero advance and zero

penalty). In 2019, nearly ten major product series were launched, including “Discounting-Counter-discounting

Link”, “Discounting-Rediscounting Link”, “Bills ABS” and “Treasury Link”, running across the primary,

secondary and tertiary bills markets. Corporate customers and financial institutions were provided with a wide

variety of multi-tiered bills services.

3.4 Characteristic businesses -- technology finance

3.4.1 Operating results

As of the end of the reporting period, the Bank had served 2,713 high-tech firms, including 518 credit customers.

The balance of on- and off- balance sheet credits to high-tech enterprises stood at RMB27,974 million. Specifically,

the balance of on-balance-sheet loans (including discounted bills) to high-tech enterprises reached RMB17,398

million, an increase of RMB6,632 million or 61.6% over the beginning of the year. Technology finance made

breakthroughs, giving stronger impetus and support for the Bank’s business transformation.

3.4.2 Business development initiatives

(1) The action plan for the “Hundred, Thousand and Ten Thousand” Hi-tech Program was further implemented. The

three project pipelines (basic, select and core) were established, putting focus on enterprises in the strategic

emerging industries, participants in the “venture loan” program and capital market players. 443 enterprises were

added to the high-tech customer base in the year. As of the end of the reporting period, 71 of Hubei-based listed

companies were customers of the Bank. All the five Hubei applicants for listing on the STAR Market were

customers of the Bank.

(2) The technology finance business system was strengthened. Asset allocations to strategic emerging industries

were strengthened in the exploration for transforming to an asset trading bank. The Bank advanced the reform and

innovation in the technology finance system to improve the performance assessment and staff development policies

for technology finance. The banker-investor-business starter matchmaking business was strengthened under the

“venture loan” program to further improve the cooperation mechanism for technology finance channels.

(3) The research and development of new products were strengthened. The Bank approached government agencies

and capital markets, launched such innovative products as “STAR Listing Loan” and “Proportional Re-guarantee”

to meet the particular financing needs of high-tech businesses in different life stages and enterprises applying for

listing. These products enriched the Bank’s methods to foster high-tech enterprises and serve seeded enterprises for

listing.

3.5 Distribution channels

The Bank rendered products and services through a variety of channels which mainly consist of physical outlets

and e-banking means.

2019 Annual Report of Hankou Bank Co., Ltd.

21

3.5.1 Physical outlet channels

(1) Establishment of institutions

As at the end of the reporting period, the Bank had established 181 institutions, including the Banking Department

of the Head Office, 15 branches, one sub-branch directly under the Head Office, 16 tier-1 sub-branches, two

specialized institutions and 146 tier-2 sub-branches (27 of which were community sub-branches). So far, the Bank

had its outlet layout almost cover the entire Hubei Province and set up a branch in Chongqing.

(2) New institutions and changes in existing ones

During the reporting period, the Bank established eight institutions in total, among which one branch and two

sub-branches were sub-branches beyond Wuhan and five sub-branches in Wuhan. During the reporting period, the

Bank established Suizhou Branch, Shiyan Shanghai Road Sub-branch and Xianing Xian’an Sub-branch outside

Wuhan, and established Shuguang Xingcheng Sub-branch, Yuanlin Road Sub-branch, Yongqing Sub-branch, Youyi

Road Sub-branch and Taizihu Sub-branch in Wuhan.

3.5.2 E-banking channels

(1) Operating results

As at the end of the reporting period, personal Internet banking customers reached 2,126,100, an increase of

17.92%; mobile banking customers reached 2,028,500, an increase of 19.78%; corporate Internet banking

customers reached 57,300, an increase of 5.72%; and new direct banking customers increased by 262,700. The

transaction volume of e-banking reached RMB2.18 trillion, an increase of 12.37%. In the year, the replacement rate

of counter-based transactions by e-banking arrived at 92.51%. There were 1,179 self-service equipment across the

Bank, 119 units more than the beginning of the year. The Bank established a total of 191 self-service banks, an

increase of three over the beginning of the year. Intelligent equipment at outlets recorded 126.09 transactions a day

on average, up 64.93% year-on-year. 833,000 passbook-based cash withdrawals were made on self-service

equipment, accounting for 52.57% of total passbook-based cash withdrawals, up 24.69% year-on-year.

(2) Channel innovation

First, online financial services were deepened to accelerate Internet banking transformation. 20 innovations were

completed in E-channel and Internet finance, with the versions of personal Internet banking, mobile banking and

direct banking updated 28 times. Both quantity and quality of mobile banking customers were improved. As of the

end of the reporting period, the customers with effective changes in balance of mobile banking accounts saw

year-on-year growth of 19.95% in number of transactions, or 39.62% in value of transactions. Direct banking

recorded over RMB10 billion in personal financial assets, maintaining high-quality growth.

Second, business innovation and upgrading gained pace and core competitiveness of channels was enhanced.

Mobile banking and direct banking were remodeled to optimize business processes. Mobile banking and direct

banking were integrated. The new version of mobile banking allows trusted login to the direct banking APP. The

mobile number-based payment project was completed. Application scenarios were actively developed to attract user

traffic. The mobile traffic fine payment service was launched.

Third, business scenarios were enriched to expand the everyday finance market. Based on the electronic social

2019 Annual Report of Hankou Bank Co., Ltd.

22

security cards, the Bank entered local social security markets to increase deposits from social security agencies and

also expand the individual customers and corporate customers through pharmacies. The Bank partnered with China

UnionPay in the QuickPass-based marketing. 27,000 effective users of UnionPay APP were added to the customer

base, expanding the sources of intermediary service income. The online housing provident fund withdrawal service

was promoted. Direct banking rolled out nine new services, including transfer and withdrawal by home-buying

railway workers, withdrawal for commercial loan repayment and withdrawal under hybrid loan, pushing the

housing provident fund withdrawals up by 240% year-on-year. The unconscious pay parking scenarios were

developed, covering 64 Park & Ride parking areas. The Bank competed for the education and training tuition

collection market, achieving nearly RMB100 million in tuition collection service.

Fourth, smart outlet development was advanced. 16 outlets completed the upgrading of their intelligent

equipment-based service areas. The intelligent equipment systems were improved. 49 new features went online and

63 programs were optimized in the year The Bank accelerated the upgrading of self-service passbook-based

withdrawal features at outlets and enhanced the elderly customer service capability. Passbook-based withdrawals

increased by 24.69% year-on-year in Wuhan. The social security self-service process was optimized. 366,700

third-generation social security cards were issued through intelligent equipment and self-service card replacement

machines, representing a substitution ratio of 71.81%.

Fifth, the Bank strictly prohibited crossing the line for compliance and strengthened channel risk control. The

E-banking policies and procedures were improved to enhance compliance of business and standardize the risk

prevention and control for incremental business. Business continuity drills were conducted for all E-banking

channels. Business risk training was intensified.

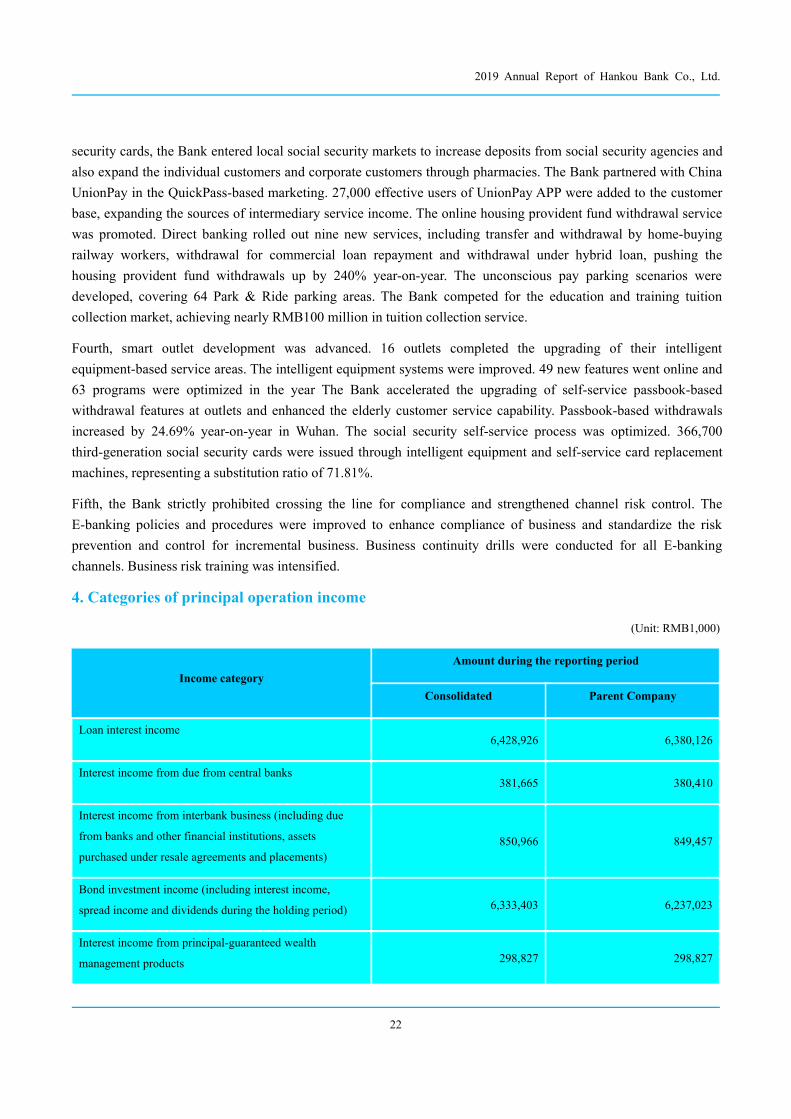

4. Categories of principal operation income

(Unit: RMB1,000)

Income category

Amount during the reporting period

Consolidated Parent Company

Loan interest income6,428,926 6,380,126

Interest income from due from central banks381,665 380,410

Interest income from interbank business (including due

from banks and other financial institutions, assets

purchased under resale agreements and placements)850,966 849,457

Bond investment income (including interest income,

spread income and dividends during the holding period) 6,333,403 6,237,023

Interest income from principal-guaranteed wealth

management products 298,827 298,827

2019 Annual Report of Hankou Bank Co., Ltd.

23

Income category

Amount during the reporting period

Consolidated Parent Company

Fee and commission income963,520 963,497

Total15,257,307 15,109,341

5. Market shares of main products or services

According to the statistics in RMB terms from the Operation Management Department of Wuhan Branch of the

People’s Bank of China, at the end of 2019, the Bank accounted for 9.49% of the total RMB deposits in Wuhan,

ranking third in the banking industry. Specifically, the Bank’s market share in the corporate deposit segment was

7.74%, ranking fourth; the market share in the savings deposit segment was 8.78%, ranking fifth. The Bank

accounted for 5.02% of the total RMB loans in Wuhan, ranking the seventh. The market share in the corporate loan

segment was 3.72%, ranking ninth; the market share in discounting segment was 32.99%, ranking first; and the

market share in personal loan market segment was 4.24%, ranking eighth.

ii. Analysis of financial position and operating results during the reporting period

1. Changes in major financial indicators and reasons

(Unit: RMB1,000)

Item

Consolidated Parent Company

Main reason31 December

2019

31December2018

Change31 December

2019

31December2018

Change

Total assets 405,739,564 319,295,909 27.07% 405,041,970318,471,383

27.18%

Increase in loans

and investments

Total liabilities 383,891,723 299,253,630 28.28% 383,307,789 298,501,765 28.41% Increase in deposits

Shareholders’

equity 21,847,841 20,042,279 9.01% 21,734,18119,969,618

8.84%

Increase in net

profit

Total profit 2,076,681 1,715,761 21.04% 2,019,9031,737,377

16.26%

Increase in

operating income

Net profit 2,418,902 1,882,378 28.50% 2,362,9021,902,528

24.20%

Increase in

operating income

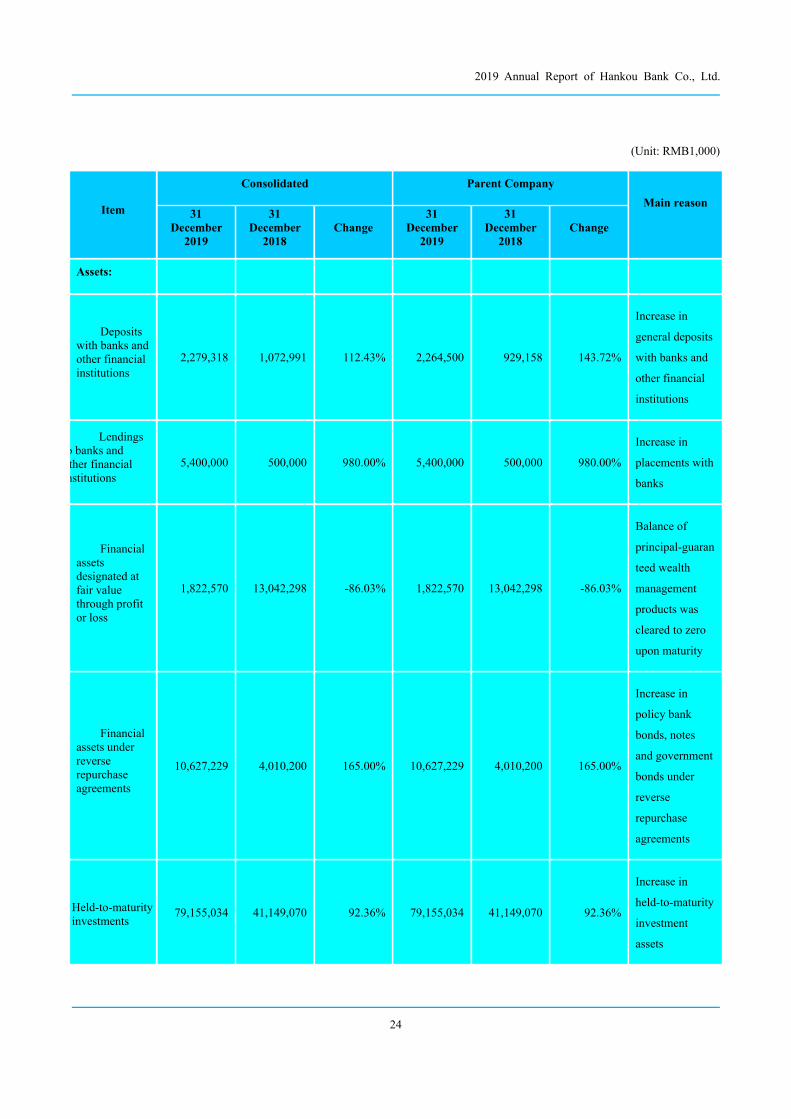

2. Items with 30% or more changes in the financial report and reasons

2019 Annual Report of Hankou Bank Co., Ltd.

24

(Unit: RMB1,000)

Item

Consolidated Parent Company

Main reason31

December2019

31December2018

Change31

December2019

31December2018

Change

Assets:

Depositswith banks andother financialinstitutions

2,279,318 1,072,991 112.43% 2,264,500 929,158 143.72%

Increase in

general deposits

with banks and

other financial

institutions

Lendingso banks andther financialnstitutions

5,400,000 500,000 980.00% 5,400,000 500,000 980.00%

Increase in

placements with

banks

Financialassetsdesignated atfair valuethrough profitor loss

1,822,570 13,042,298 -86.03% 1,822,570 13,042,298 -86.03%

Balance of

principal-guaran

teed wealth

management

products was

cleared to zero

upon maturity

Financialassets underreverserepurchaseagreements

10,627,229 4,010,200 165.00% 10,627,229 4,010,200 165.00%

Increase in

policy bank

bonds, notes

and government

bonds under

reverse

repurchase

agreements

Held-to-maturityinvestments

79,155,034 41,149,070 92.36% 79,155,034 41,149,070 92.36%

Increase in

held-to-maturity

investment

assets

2019 Annual Report of Hankou Bank Co., Ltd.

25

Item

Consolidated Parent Company

Main reason31

December2019

31December2018

Change31

December2019

31December2018

Change

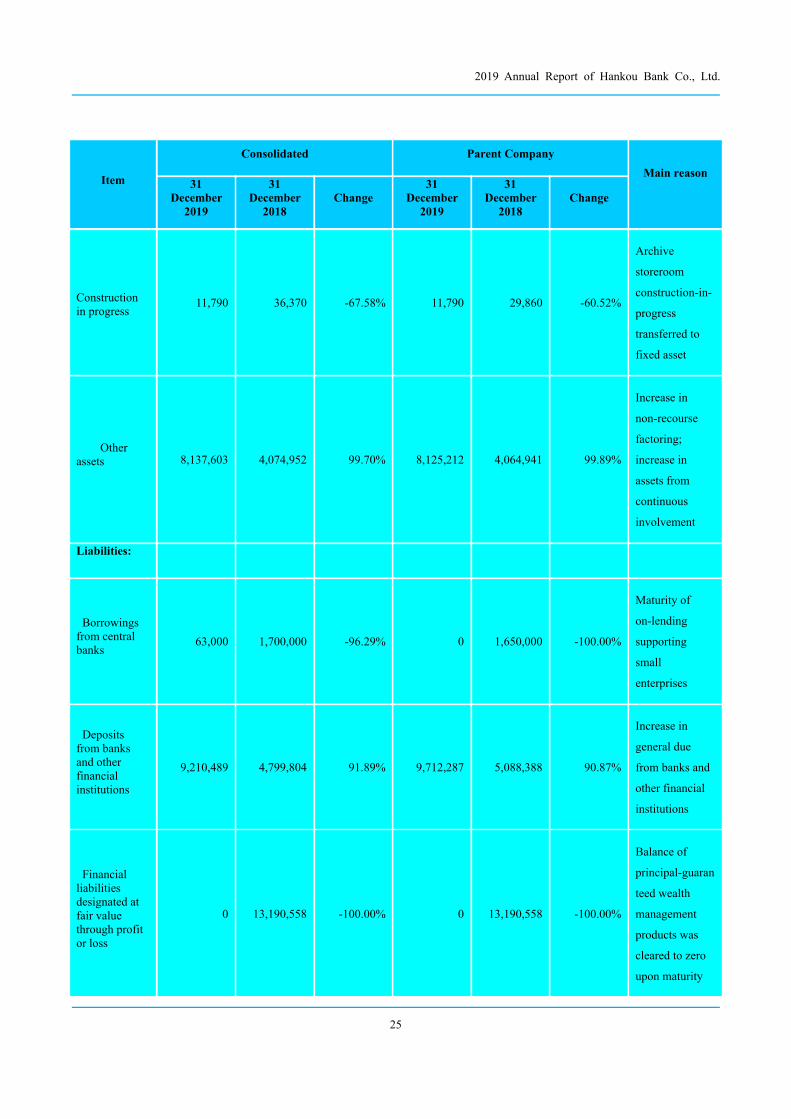

Constructionin progress

11,790 36,370 -67.58% 11,790 29,860 -60.52%

Archive

storeroom

construction-in-

progress

transferred to

fixed asset

Otherassets 8,137,603 4,074,952 99.70% 8,125,212 4,064,941 99.89%

Increase in

non-recourse

factoring;

increase in

assets from

continuous

involvement

Liabilities:

Borrowingsfrom centralbanks

63,000 1,700,000 -96.29% 0 1,650,000 -100.00%

Maturity of

on-lending

supporting

small

enterprises

Depositsfrom banksand otherfinancialinstitutions

9,210,489 4,799,804 91.89% 9,712,287 5,088,388 90.87%

Increase in

general due

from banks and

other financial

institutions

Financialliabilitiesdesignated atfair valuethrough profitor loss

0 13,190,558 -100.00% 0 13,190,558 -100.00%

Balance of

principal-guaran

teed wealth

management

products was

cleared to zero

upon maturity

2019 Annual Report of Hankou Bank Co., Ltd.

26

Item

Consolidated Parent Company

Main reason31

December2019

31December2018

Change31

December2019

31December2018

Change

Financialassets underrepurchaseagreements

34,414,642 17,496,238 96.70% 34,414,642 17,496,238 96.70%

Increase in

government

bonds and bills

under

repurchase

agreements

Customerdeposits 250,341,491 188,829,166 32.58% 249,303,848 187,861,314 32.71%

Increase in

customer

deposits

Deferredincome taxliabilities

73,822 122,432 -39.70% 73,822 122,432 -39.70%

Decrease in

changes in fair

value of

available-for-sal

e financial

assets

Otherliabilities 6,648,892 3,646,474 82.34% 6,667,618 3,625,206 83.92%

Increase in

customer

deposits and

interest payable;

increase in

on-lending

funds; increase

in liabilities

from continuous

involvement

Shareholders’equity:

Othercomprehensiveincome

219,941 364,218 -39.61% 219,941 364,218 -39.61%

Decrease in fair

value of

available-for-sal

e financial

assets

2019 Annual Report of Hankou Bank Co., Ltd.

27

Item

Consolidated Parent Company

Main reason31

December2019

31December2018

Change31

December2019

31December2018

Change

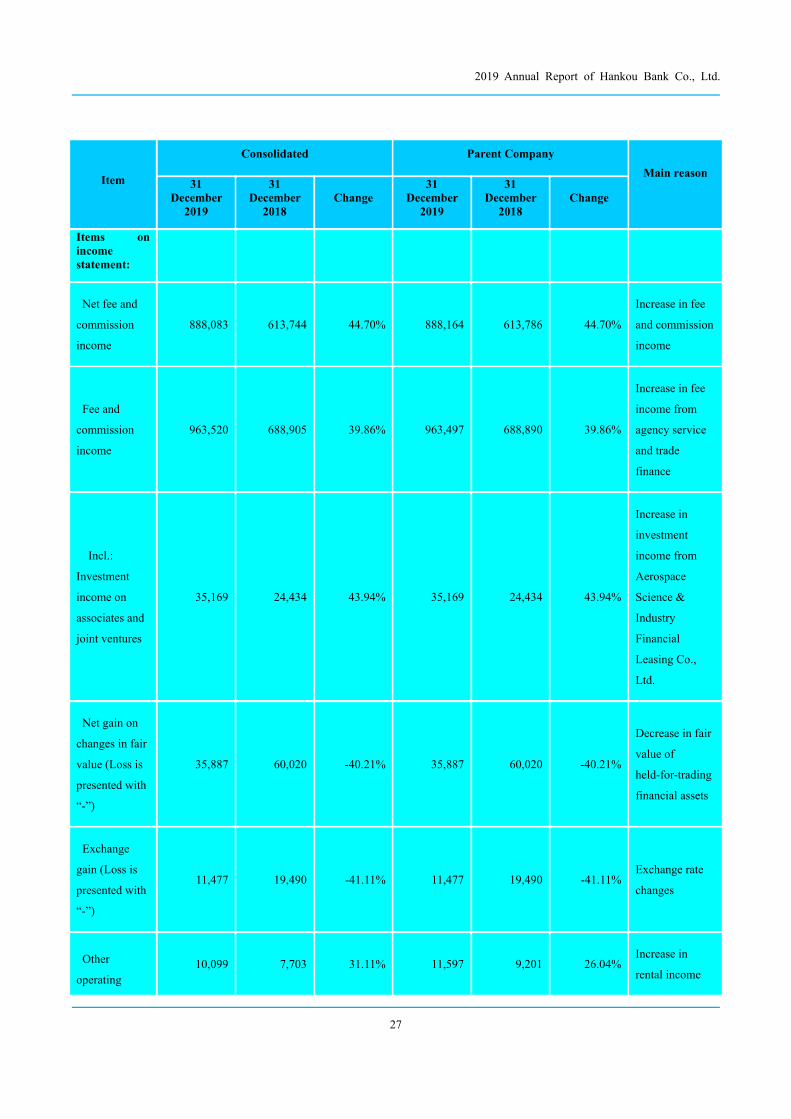

Items onincomestatement:

Net fee and

commission

income

888,083 613,744 44.70% 888,164 613,786 44.70%

Increase in fee

and commission

income

Fee and

commission

income

963,520 688,905 39.86% 963,497 688,890 39.86%

Increase in fee

income from

agency service

and trade

finance

Incl.:

Investment

income on

associates and

joint ventures

35,169 24,434 43.94% 35,169 24,434 43.94%

Increase in

investment

income from

Aerospace

Science &

Industry

Financial

Leasing Co.,

Ltd.

Net gain on

changes in fair

value (Loss is

presented with

“-”)

35,887 60,020 -40.21% 35,887 60,020 -40.21%

Decrease in fair

value of

held-for-trading

financial assets

Exchange

gain (Loss is

presented with

“-”)

11,477 19,490 -41.11% 11,477 19,490 -41.11%Exchange rate

changes

Other

operating10,099 7,703 31.11% 11,597 9,201 26.04%

Increase in

rental income

2019 Annual Report of Hankou Bank Co., Ltd.

28

Item

Consolidated Parent Company

Main reason31

December2019

31December2018

Change31

December2019

31December2018

Change

income

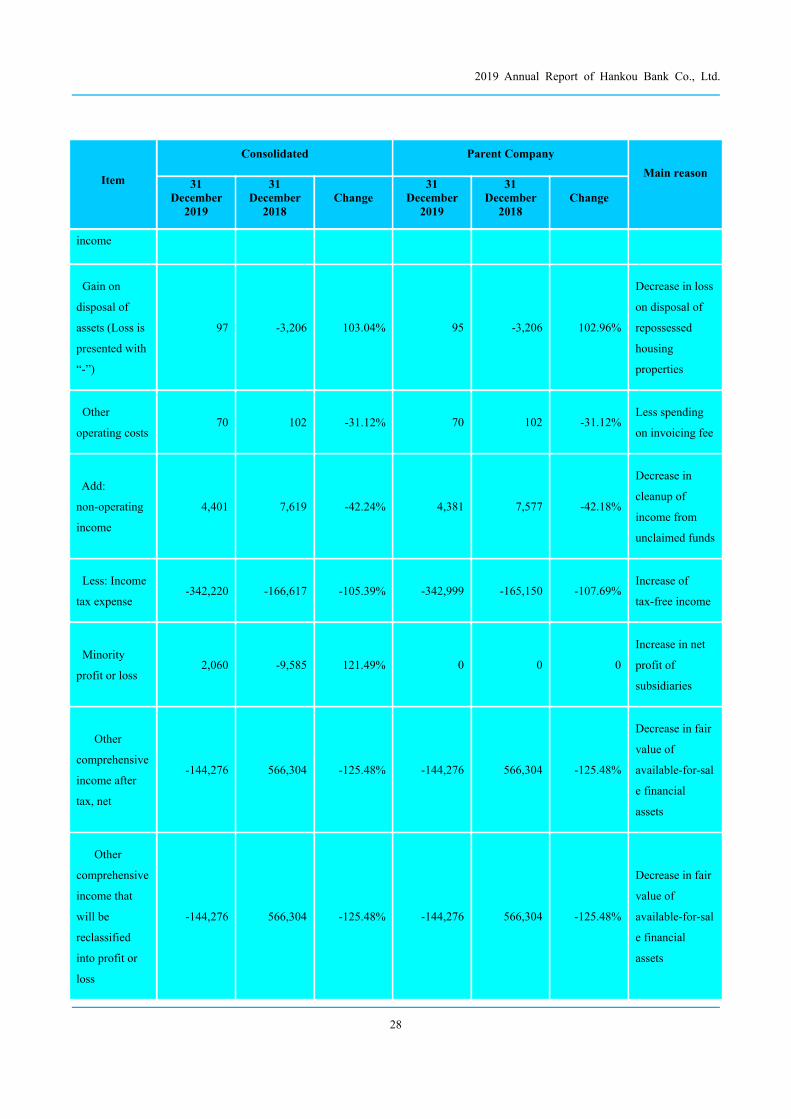

Gain on

disposal of

assets (Loss is

presented with

“-”)

97 -3,206 103.04% 95 -3,206 102.96%

Decrease in loss

on disposal of

repossessed

housing

properties

Other

operating costs70 102 -31.12% 70 102 -31.12%

Less spending

on invoicing fee

Add:

non-operating

income

4,401 7,619 -42.24% 4,381 7,577 -42.18%

Decrease in

cleanup of

income from

unclaimed funds

Less: Income

tax expense-342,220 -166,617 -105.39% -342,999 -165,150 -107.69%

Increase of

tax-free income

Minority

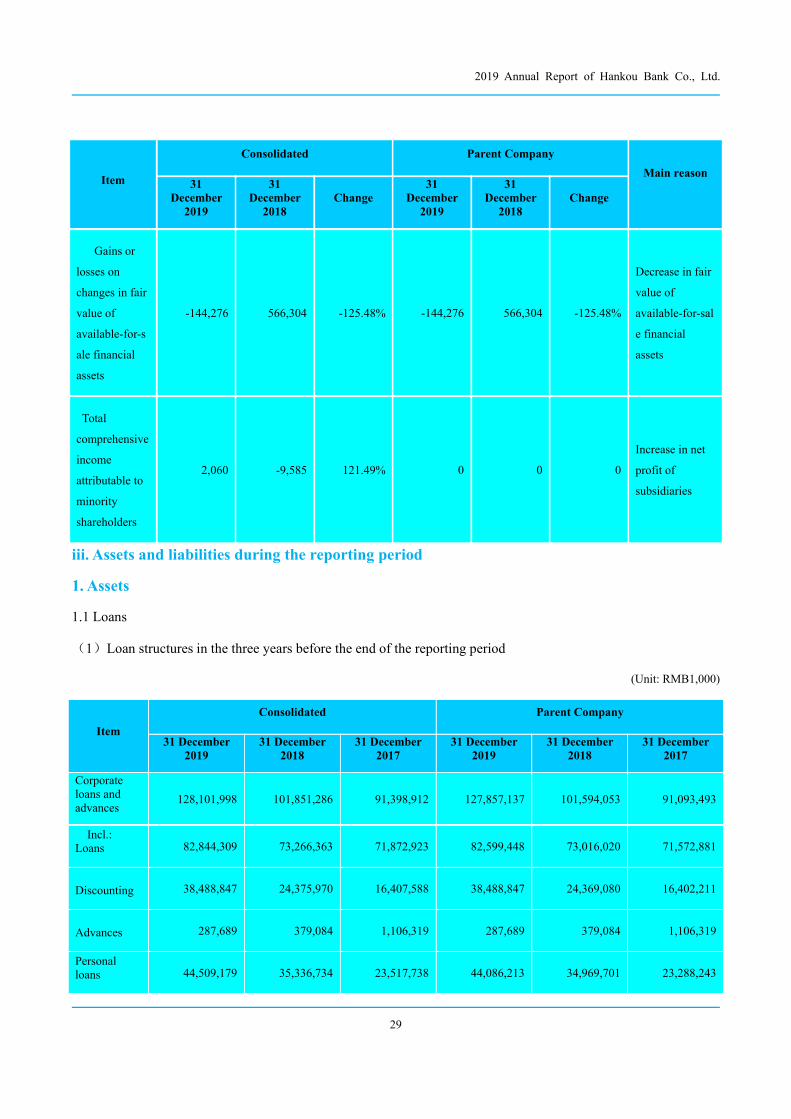

profit or loss2,060 -9,585 121.49% 0 0 0

Increase in net

profit of

subsidiaries

Other

comprehensive

income after

tax, net

-144,276 566,304 -125.48% -144,276 566,304 -125.48%

Decrease in fair

value of

available-for-sal

e financial

assets

Other

comprehensive

income that

will be

reclassified

into profit or

loss

-144,276 566,304 -125.48% -144,276 566,304 -125.48%

Decrease in fair

value of

available-for-sal

e financial

assets

2019 Annual Report of Hankou Bank Co., Ltd.

29

Item

Consolidated Parent Company

Main reason31

December2019

31December2018

Change31

December2019

31December2018

Change

Gains or

losses on

changes in fair

value of