Embed Size (px)

Citation preview

Hammerson Full-Year Results

1 March 2013

Hammerson

Full-Year Results

1 March 2013

Creating winning

retail locations

1

Today’s presentation

Overview and operations David Atkins – CEO

Financials Timon Drakesmith – CFO

Our business in France Jean-Philippe Mouton – MD France

Capital allocation Peter Cole – CIO

Conclusion David Atkins – CEO

2

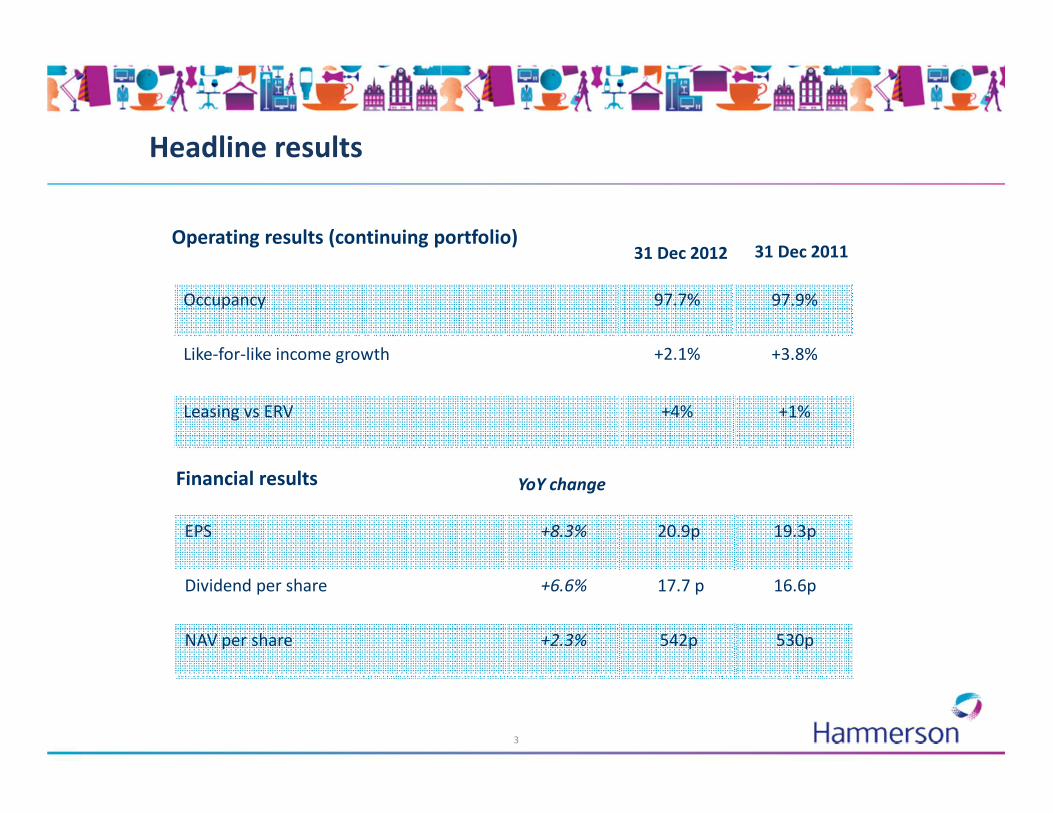

Headline results

Operating results (continuing portfolio)

Financial results

Occupancy 97.7% 97.9%

Like-for-like income growth +2.1% +3.8%

Leasing vs ERV +4% +1%

31 Dec 201131 Dec 2012

EPS +8.3% 20.9p 19.3p

Dividend per share +6.6% 17.7 p 16.6p

NAV per share +2.3% 542p 530p

3

YoY change

Vision

Our vision is to be the best owner-manager

and developer of retail property within Europe

By capitalising on our strengths we aim to provide

industry-leading shareholder returns

4

Our strategy in action...

Recycling capital

Managing interest expense

Reducing costs

� £541m re-invested into winning retail locations

High Occupancy Positive NRI Growth

1

5

4

� 7% YoY savings in operating costs� £6.8m reduction, well ahead of target� Cost/income ratio improved by 130

bps

� 11% reduction in finance costs� €220m bond buy back� Increasing use of floating rates� €500m unsecured bond� 20bps reduction average interest cost

Maximising income

3

� Completion of office disposal programme

� 7% premium to book value

2.1%

1.0%

2.5%

Group

France

UK

A pure retail player

Year-End 2011 Year-End 2012 (1)

Retail

Office

89%

11%

Recycling capital

Strategic focus

Maximising income

Managing interest expense

Reducing Costs

1

Retail

100%

5

2012 TSR

+41%Creating winning retail venues

97.0%97.7%

Min target Dec-12

2

2

34

5

...And plenty more to come

Investment &

Development

Leasing & Asset

Management

Leasing & Asset

Management

Financing &

Operations

Commitment to start Le Jeu de Paume, Beauvais

Deliver Les Terrasses du Port – Spring 2014

Advance development pipeline of c.520,000 sq. m

Further selective acquisitions

Commitment to start Le Jeu de Paume, Beauvais

Deliver Les Terrasses du Port – Spring 2014

Advance development pipeline of c.520,000 sq. m

Further selective acquisitions

Advance UK extension and refurbishment

programme of c.200,000 sq. m

Complete €100m French SC refurbishment

Drive LfL NRI growth

Advance UK extension and refurbishment

programme of c.200,000 sq. m

Complete €100m French SC refurbishment

Drive LfL NRI growth

Aim to further reduce cost/income ratio

Reduce average interest rate to below 5%

Maintain LTV below 40% and high liquidity

6

Supports future

EPS and DPS

growth

Shopping centres: Experience and excitement

Our market position

• 22 Shopping Centres

• 2,200 shops / 250m visitors pa

• 1.25m sq. m

• Top three operator in both UK and France

7

2012 highlights

• Occupancy 97.8%

• 160 new leases / £12m rents pa at +4% ERV

• Limited impact of administrations

• Tenants’ sales: UK +0.4%/France -3.0%

• Footfall: UK -2.3%/France-3.4%

• 33 new retail brands to the group secured in 2012

• mobile website use +190%

• online dwell time +150%

Retail Parks: Bringing together clicks and bricks

8

Our market position

• £260million acquisition of Junction Fund

• UK’s largest direct owner / 400,000 sq. m

• 65% of open A1, £17 sq. ft. average rents

• 11% units let to catering operators

2012 highlights

• Occupancy 98.2%

• 13 leases / £1.6m annual rent at +8.4% ERV

• Pre-letting to M&S at Merthyr Tydfil

• Pre-letting to Debenhams at Rugby

• Planning applications submitted at Merthyr and Rugby

• Cinema redevelopment at Cramlington

Designer outlets; Luxury and tourism

9

Our market position

• 9 villages in Europe’s major cities, 165,000 sq. m floor space

• 22% stake in VR holding companies

• Total brand sales £1.3bn

• 30 million annual shoppers

2012 highlights

• Additional £100m invested

• Tenants’ sales +13%

• Extension completed at La Vallee / floor space +20%

• Burberry flagship opened at La Vallee

• Planning permission granted for additional 5,800 sq. m at La

Roca

• 25% floor space re-let / remerchandised

• Village valuations +18%, driven by income growth

Financial Results

Timon Drakesmith

10

Financial highlights

Net Rental Income (£m) (1) 258.8 +2.1%(2)

Adjusted Profit Before Tax (£m) 152.5 +7.7%

Adjusted EPS (pence) 20.9 +8.3%

Final Dividend (pence per share)10.0 7.5%

31 Dec 2012 Change vs

31 Dec 2011

Income statement

Portfolio Value (£m) (1) 5,458 -0.5%

NAV (pence per share) 542 +2.3%

LTV (%) 36 n/a

Balance sheet

Notes:

(1) For continuing portfolio

(2) For continuing portfolio on a like for like basis

Change vs

31 Dec 2011

11

31 Dec 2012

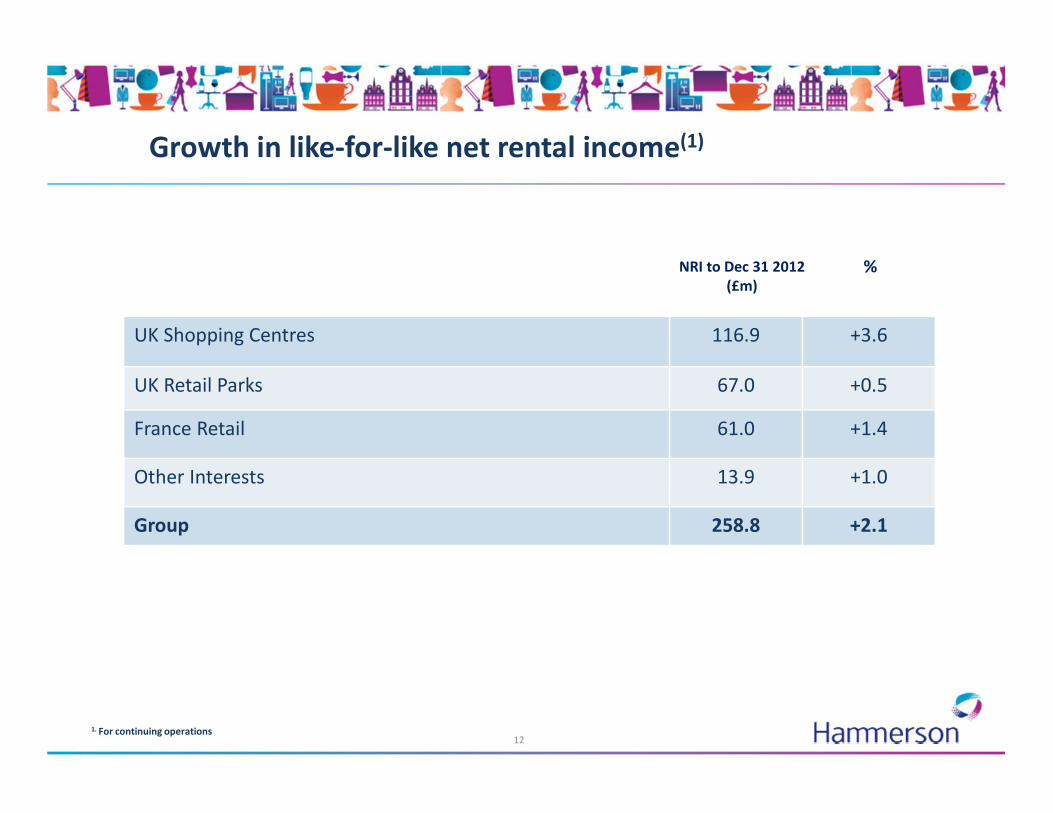

Growth in like-for-like net rental income(1)

UK Shopping Centres 116.9 +3.6

UK Retail Parks 67.0 +0.5

France Retail 61.0 +1.4

Other Interests 13.9 +1.0

Group 258.8 +2.1

%NRI to Dec 31 2012

(£m)

121. For continuing operations

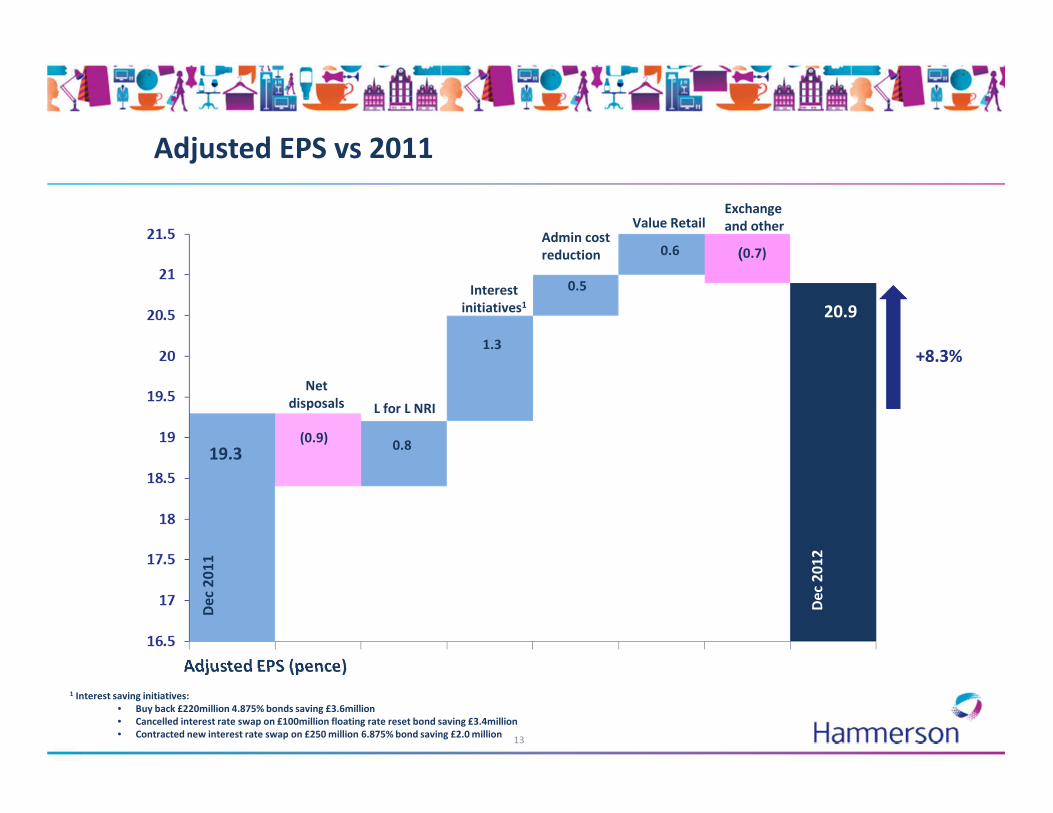

Adjusted EPS vs 2011

Adjusted EPS (pence)

Interest

initiatives1

Exchange

and other

L for L NRI

Net

disposals

De

c 2

01

1

20.9

((((0.7)

(0.9)0.8

19.3

1.3

De

c 2

01

2

0.5

0.6

+8.3%

Value RetailAdmin cost

reduction

13

1 Interest saving initiatives:

• Buy back £220million 4.875% bonds saving £3.6million

• Cancelled interest rate swap on £100million floating rate reset bond saving £3.4million

• Contracted new interest rate swap on £250 million 6.875% bond saving £2.0 million

Cost management

14

Operating

Costs(1) (£m)

(LHS)

Cost/income(1)(2)

ratio (%)

(RHS)

Net interest

expense (£m)

(LHS)

WAIR(3) (%)

(RHS)

(1) Continuing operations

(2) Cost ratio is defined as: net service charge expense + property outgoings + administration expenses – management fees receivable / Gross rental income

(3) WAIR: Weighted average interest rate

Operating cost control - £6.3m saving Interest expense management - £11.6m saving

2011 20122011 2012

Portfolio value capital movement

UK Shopping Centres 2,413 -0.8

UK Retail Parks 1,423 -2.5

France Retail 1,188 +0.8

Current Developments 275 +11.5

Other UK interests(1) 159 -8.3

Discontinued Operations(2) 195 +5.3

Total(3)(4) 5,653 +0.1

IPD UK Index-

-2.8%

Value at 31

Dec 2012

£m

% Change

From Dec

2011

15

Notes:

(1) Principally assets held for redevelopment

(2) The remaining London office portfolio has been contracted for sale. Excludes 10 Grosvenor Street and The Goodsyard that have been retained

(3) Excludes Value Retail

(4) Continuing portfolio had capital movement of -0.5%

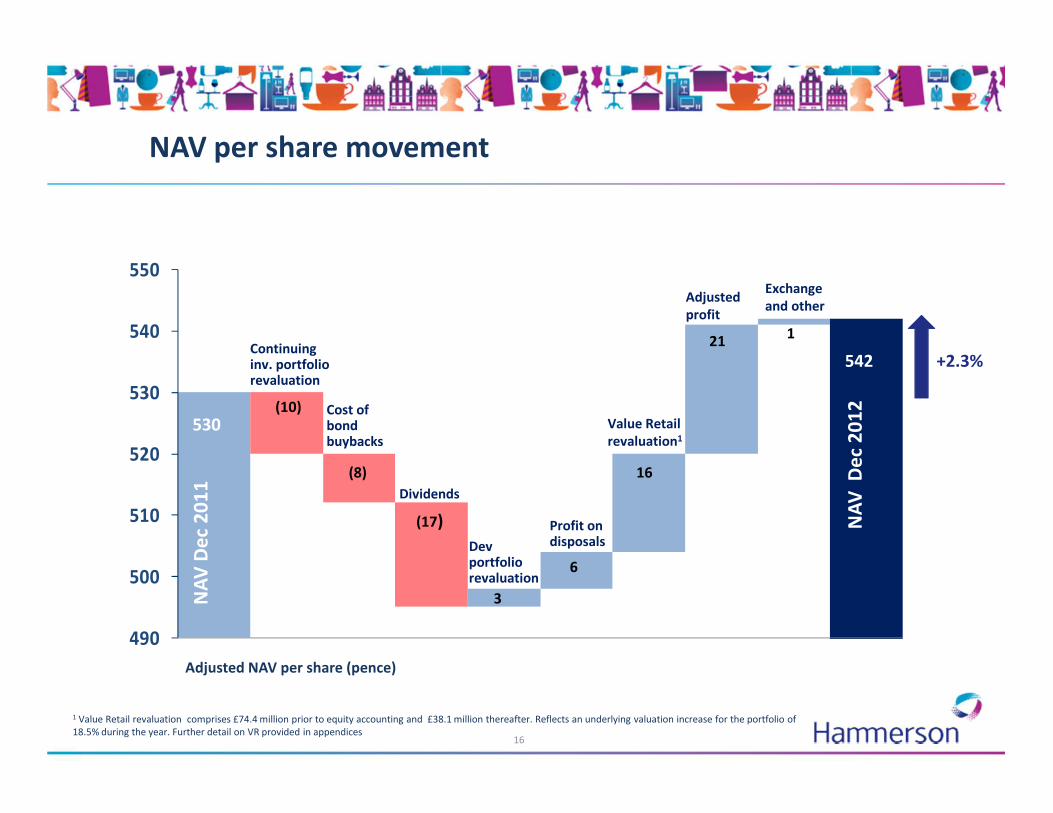

NAV per share movement

16

Adjusted NAV per share (pence)

490

500

510

520

530

540

550

530

(17)

6

16

211

542

Profit on disposals

Dividends

Adjusted

profit

Dev portfolio revaluation

Exchange

and other

Value Retail

revaluation1

NA

V D

ec

20

11

NA

V D

ec

20

12

Continuinginv. portfolio revaluation

3

(10) Cost of bond buybacks

(8)

+2.3%

1 Value Retail revaluation comprises £74.4 million prior to equity accounting and £38.1 million thereafter. Reflects an underlying valuation increase for the portfolio of

18.5% during the year. Further detail on VR provided in appendices

£m£m

EPRA Net assets2

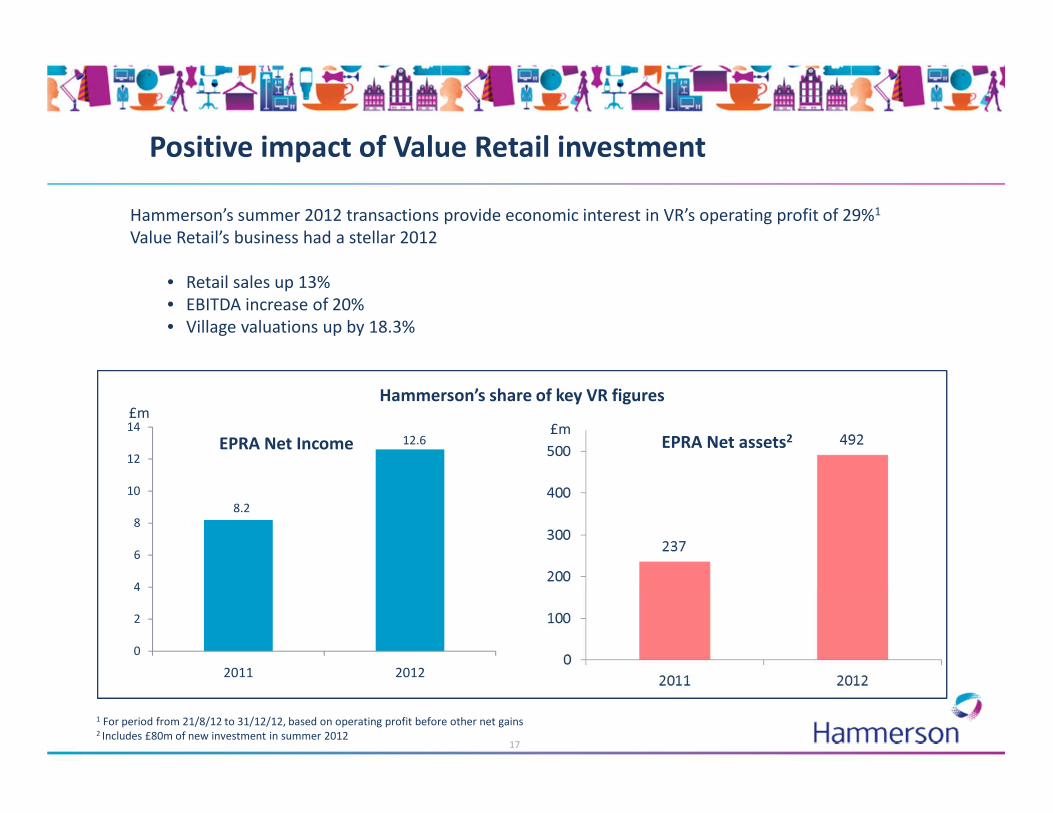

Positive impact of Value Retail investment

Hammerson’s summer 2012 transactions provide economic interest in VR’s operating profit of 29%1

Value Retail’s business had a stellar 2012

• Retail sales up 13%

• EBITDA increase of 20%

• Village valuations up by 18.3%

EPRA Net Income

17

Hammerson’s share of key VR figures

8.2

12.6

0

2

4

6

8

10

12

14

2011 2012

1 For period from 21/8/12 to 31/12/12, based on operating profit before other net gains2 Includes £80m of new investment in summer 2012

Healthy financing ratios

Net debt £2,036m £1,964m

Gearing <85% 53% 52%

Loan to value <40% 36% 34%

Cash/undrawn facilities £696m £696m(1)

Weighted average (cost of finance) 5.0% 5.2%

Interest cover >2.0x 2.8x 2.6x

Net debt/EBITDA <10x 7.9x 7.7x

Debt fixed/hedged 80% 88%

31 Dec

2011

Note:

(1) Restated to exclude FX swaps. Previously reported at £711million

31 Dec 2012

18

Financing policies

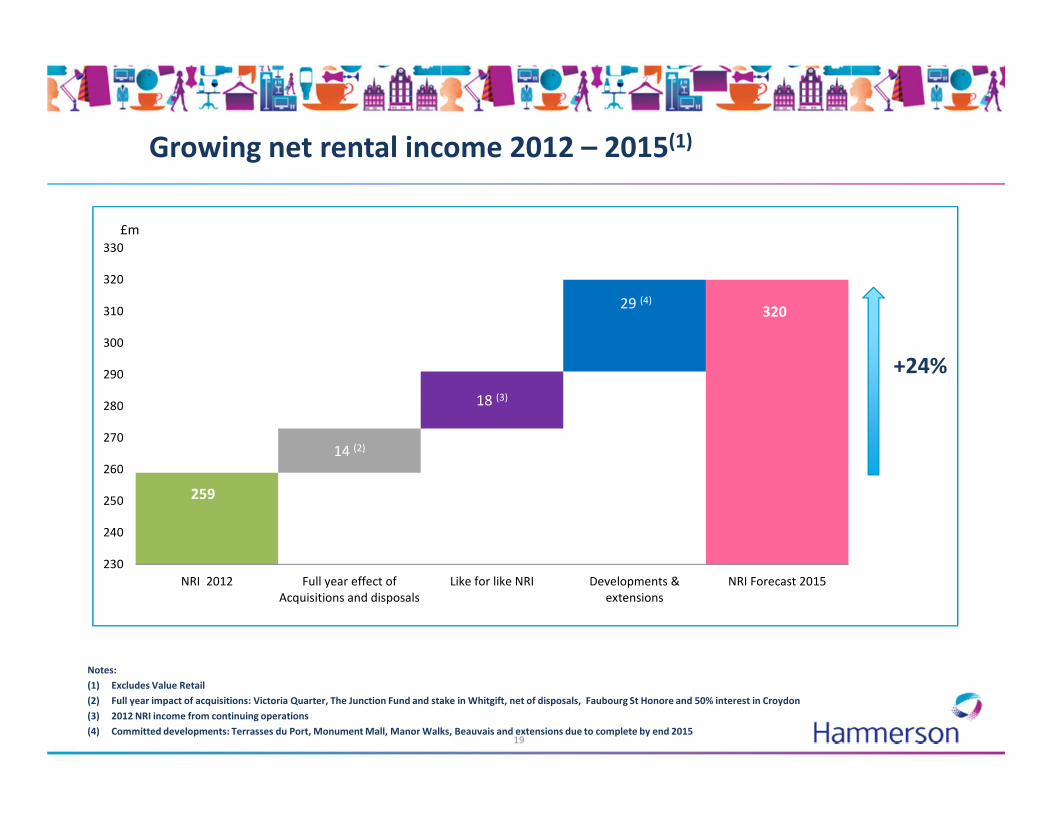

Growing net rental income 2012 – 2015(1)

19

+24%

Notes:

(1) Excludes Value Retail

(2) Full year impact of acquisitions: Victoria Quarter, The Junction Fund and stake in Whitgift, net of disposals, Faubourg St Honore and 50% interest in Croydon

(3) 2012 NRI income from continuing operations

(4) Committed developments: Terrasses du Port, Monument Mall, Manor Walks, Beauvais and extensions due to complete by end 2015

14 (2)

18 (3)

29 (4)

259

320

230

240

250

260

270

280

290

300

310

320

330

NRI 2012 Full year effect of

Acquisitions and disposals

Like for like NRI Developments &

extensions

NRI Forecast 2015

£m

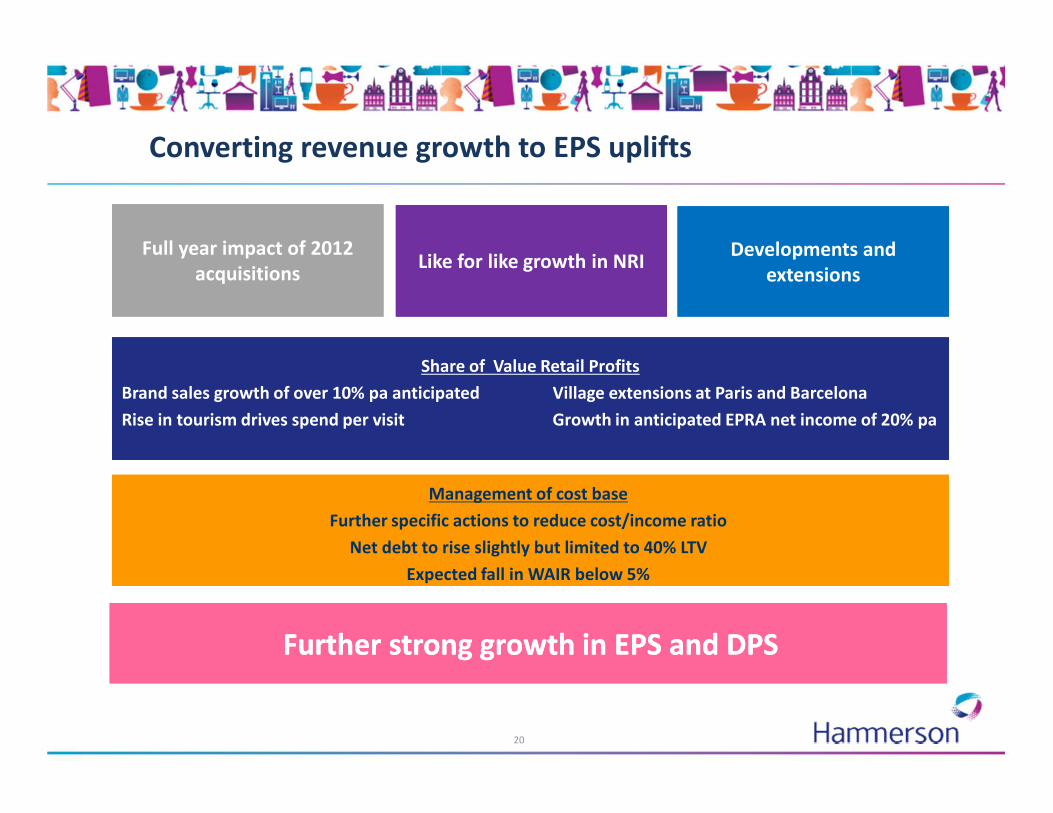

Converting revenue growth to EPS uplifts

Management of cost base

Further specific actions to reduce cost/income ratio

Net debt to rise slightly but limited to 40% LTV

Expected fall in WAIR below 5%

Like for like growth in NRILike for like growth in NRIDevelopments and

extensions

Developments and

extensions

Share of Value Retail Profits

Brand sales growth of over 10% pa anticipated Village extensions at Paris and Barcelona

Rise in tourism drives spend per visit Growth in anticipated EPRA net income of 20% pa

Further strong growth in EPS and DPSFurther strong growth in EPS and DPS

20

Full year impact of 2012

acquisitions

Full year impact of 2012

acquisitions

21

Our Business in France

Jean-Philippe Mouton

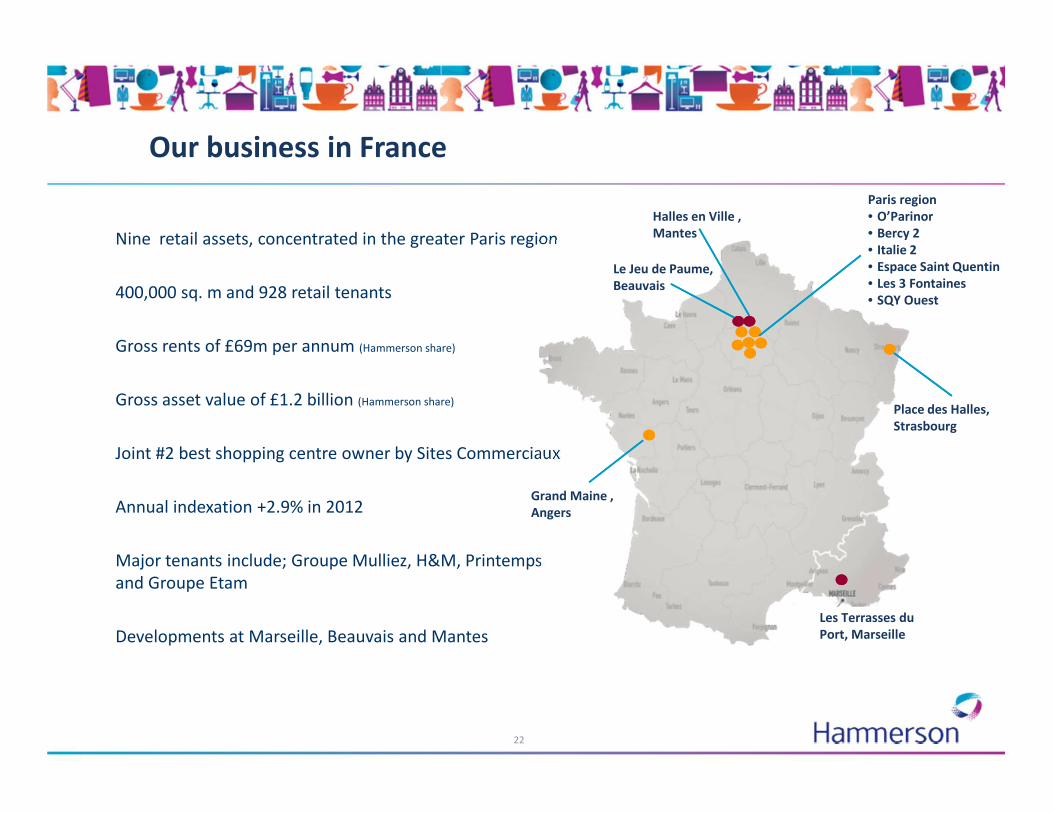

Our business in France

Nine retail assets, concentrated in the greater Paris region

400,000 sq. m and 928 retail tenants

Gross rents of £69m per annum (Hammerson share)

Gross asset value of £1.2 billion (Hammerson share)

Joint #2 best shopping centre owner by Sites Commerciaux

Annual indexation +2.9% in 2012

Major tenants include; Groupe Mulliez, H&M, Printemps

and Groupe Etam

Developments at Marseille, Beauvais and Mantes

Paris region

• O’Parinor

• Bercy 2

• Italie 2

• Espace Saint Quentin

• Les 3 Fontaines

• SQY Ouest

Grand Maine ,

Angers

Place des Halles,

Strasbourg

Les Terrasses du

Port, Marseille

Halles en Ville ,

Mantes

Le Jeu de Paume,

Beauvais

22

Investing in our assets

Italie 2 O’Parinor

Extension & redevelopmentRefurbishment

• Only Parisian shopping centre with a department store

• Adjacent one of Paris’ busiest metro stations

• Renovation to be complete by Q3 2013

• €17 million1 project

• Leases agreed with Adidas and Armand Thierry

• 7 further leases agreed +14% previous rents

• New 7,200 sq. m, 14 screen cinema and food court

extension

• Anchor letting exchanged with UGC

• Predicted to attract over 1 million visitors per annum

• €20million1 extension project

• 58% food court rent already secured

• Retail and building permits received

23

Note:

(1) Before recharged to tenant and JV partners

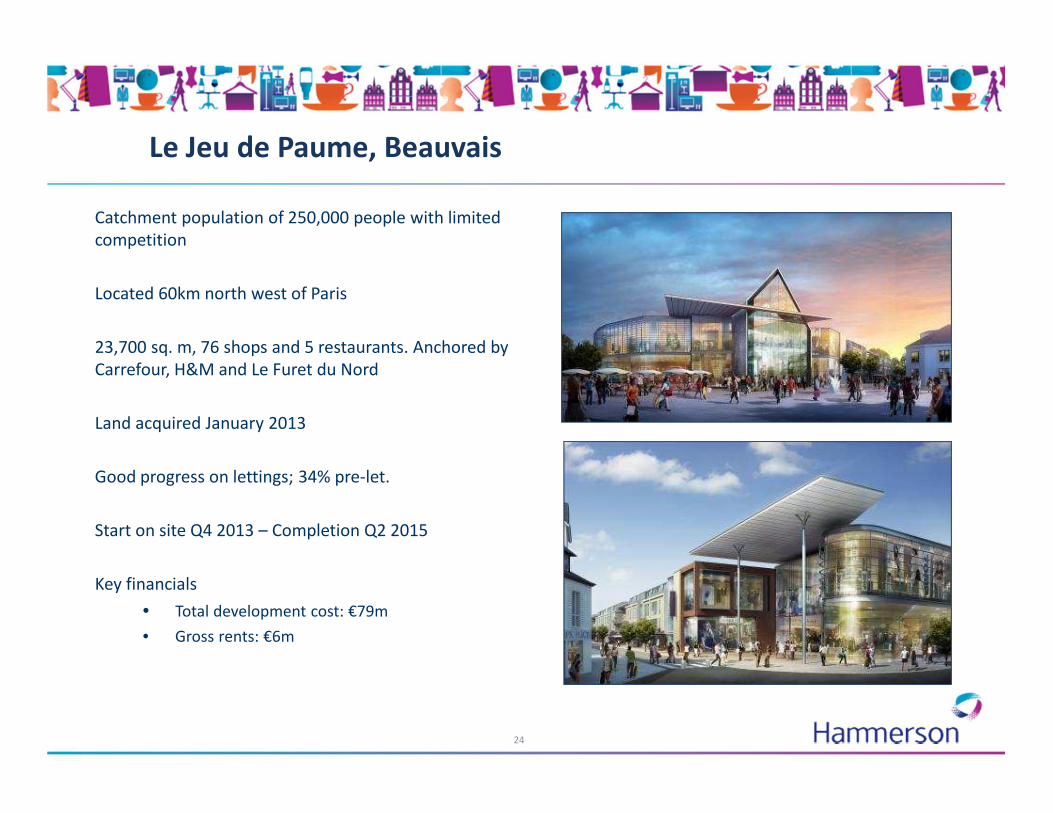

Le Jeu de Paume, Beauvais

Catchment population of 250,000 people with limited

competition

Located 60km north west of Paris

23,700 sq. m, 76 shops and 5 restaurants. Anchored by

Carrefour, H&M and Le Furet du Nord

Land acquired January 2013

Good progress on lettings; 34% pre-let.

Start on site Q4 2013 – Completion Q2 2015

Key financials

• Total development cost: €79m

• Gross rents: €6m

24

Les Terrasses du Port, Marseille

83% pre-let including all MSU’s

Construction 75% completed

Agreement for lease exchanged with Printemps

1,200 sq. m letting to Deltaccord completes letting of lower level

Lettings agreed with high quality fashion retailers; Sandro, Maje,

Michael Kors, G-Star

Key financials;

• Total development cost: €450m

• Gross rents: €33.6m

Focus on optimising tenant mix and driving rents

25

26

Multi-channel retail

Jean-Philippe Mouton

A busy year for digital engagement

April

Amazon lockers

introduced

Jan July

Ocado shopping wall

@Bullring

August

Full portfolio websites

launched/mobile enabled

October Nov

Google indoor

mapping – BX/WQ

Sept

Google product search live at The

Oracle

January 2013

Google product

search rolled out to

all UK centres

March 2013

Venteprivee.com

“Drive to store”

operation

Average basket :

+34%

Fidall Aps

partnership : digital

loyalty card

acquisition (40% of

new members /

100% opt in)

Trial web/mobile

platform live at Oracle

Dance Flashmob

in O’Parinor

displayed on

(23% footfall

increase)

Foursquare Aps

for each

shopping centerVenteprivee.com “Drive to

store” operation

Average basket : +30%

27

Portfolio student

events @ Highcross,

11k students attended

Free public

wifi across UK

shopping

centres

29

Capital Allocation

Peter Cole

Our investment criteria and recent acquisitions

30

• Principle cities and dominant market

positions

• Well anchored and strong tenant mix

• Sustainable rent:sales ratio

• Developments and acquisitions

• Value Retail investments

• City centres and tourist destinations

• Selective developments and

acquisitions

• Well located and good transport links

• Open A1 planning consents

• Low rents

• Development and asset management

situations

Luxury ConvenienceExperience

Our investment criteria

The Junction FundVictoria Quarter, LeedsWhitgift, Croydon

Whitgift, Croydon: The south London retail opportunity

• Joint venture announced January 2013

• 50% stake in Centrale sold to Westfield

• Outline planning anticipated Q2 2013

• 200,000 sq. m project

• £1 billion total forecast investment

• Accelerated programme targets 2015

start on site

• World class retail venue to open in 2018

31

Whitgift

Centrale

Commitment to Eastgate Quarters, Leeds

• Agreement for lease exchanged with John Lewis

• Outline planning consent already achieved

• Detailed planning application in Q2 2013

• Start on site Spring 2014 – Completion Autumn

2016

• 37,000 sq. m scheme initial phase

• £130m total development cost

• Gross rents £10m

• Linking Victoria and Eastgate Quarters

32

Excellent progress on Junction Fund

Thurrock

• Development of former UCI Cinema completed

• UK’s first Nike retail park store

• 6 hectare conditional land sale agreed for £18.5m

Paisley

• Former Comet re-let to CSL

• Planning permission secured for 5,000 sq. m. redevelopment

• Solicitors instructed with Wren Kitchens, Maplin and Dunelm

• Extension now >60% under offer

Performance

• £25m (10%) valuation uplift since acquisition

• 100,000 sq. m

• 70% floor space openly consented

• Low average rents of £19 psf

• 7% yield rising to 8% with fixed uplifts

33

Conclusion

David Atkins

34

Delivering against our vision

Reorientation to a specialist retail REIT complete

Operating expenses lower by 7%

Les Terrasses du Port 83% let

JV agreed for Whitgift, Croydon

NRI +2.1%

Leases agreed 4% above ERV

Digital engagement with consumers

Excellent contribution from Value Retail

8.3% EPS growth and 7.5% growth in final dividend

2012 total shareholder return of 41%

Strong growth in EPS and dividends

Acquisitions to further boost returns

Delivering on our

strategy

Focused on

winning retail

venues

Industry leading

shareholder

returns

35

36

QuestionsQuestions

Disclaimer

This presentation contains certain statements that are neither reported financial results nor other

historical information. These statements are forward-looking in nature and are subject to risks and

uncertainties. Actual future results may differ materially from those expressed in or implied by these

statements.

Many of these risks and uncertainties relate to factors that are beyond Hammerson's ability to

control or estimate precisely, such as future market conditions, currency fluctuations, the behaviour

of other market participants, the actions of governmental regulators and other risk factors such as

the Company's ability to continue to obtain financing to meet its liquidity needs, changes in the

political, social and regulatory framework in which the Company operates or in economic or

technological trends or conditions, including inflation and consumer confidence, on a global, regional

or national basis.

Readers are cautioned not to place undue reliance on these forward-looking statements, which

speak only as of the date of this document. Hammerson does not undertake any obligation to

publicly release any revisions to these forward-looking statements to reflect events or circumstances

after the date of these materials. Information contained in this presentation relating to the Company

or its share price, or the yield on its shares, should not be relied upon as a guide to future

performance.

37

38

AppendicesAppendices

Our assets

£5.5 billion property portfolio

Assets in UK and France

20 shopping centres

22 retail parks

Investment in Value Retail

2,800 shop units

250 million annual visitors

40

Developments and extensions

Notes: all costs and income are incremental, income is stated net of head rents and rent-free periods (€ converted at £1= €1.233)

% let comprises let or in solicitors hands by income at 25 February 2013

# Phase 1 only, area reflects retail space component

1 50% ownership interest

2 retail space only

3 41% interest

Scheme Lettable area

Earliest start Potential completion

Value at 31/12/12

Estimated costs to complete

Estimated annual income

Let

m2 £m £m £m %ON SITELes Terrasses du Port, Marseille 61,000 Commenced Q2 2014 229 178 27 83Manor Walks, Cramlington 5,900 Commenced Q2 2013 n/a 5 1 44Monument Mall, Newcastle 11,400 Commenced Q3 2013 37 11 1 38

78,300 194 29NEAR TERMAbbotsinch, Paisley 4,900 2013 2014 10 1 60Cyfarthfa, Methyr Tydfil 14,500 2013 2014 28 2 33Elliott's Field, Rugby 16,000 2013 2015 35 3 13Le Jeu de Paume, Beauvais 23,700 2013 2015 64 5 34Brent Cross Cinema, London NW43 9,000 2014 2015 20 2 -Eastgate Quarters (phase 1), Leeds 37,000 2014 2016 120 10 18Halle en Ville, Mantes 32,000 2014 2016 110 9 30Silverburn extension 10,700 2014 2015 12 1 37SQY Ouest 30,000 2014 2015 16 1 -Watermark, Southampton 19,400 2014 2016 70 5 -

197,200 485 39MEDIUM TERMCroydon town centre1 200,000 2015 2018 500 35 -Italie 2, Paris 13eme 6,000 2015 2017 26 2 -Orchard Centre, Didcot 21,000 2015 2016 50 4 -Sevenstone, Sheffield 60,500 2015 2017 285 24 -The Goodsyard, London# 1,2 5,750 2015 phased 100 - -Brent Cross extension, London NW43 87,000 2016 2019 350 26 -Eastgate Quarters (phase 2), Leeds 73,000 2016 2019 470 40 -

453,250 1,781 1312,460 199

Value Retail performance drivers (1)

41

Value Retail

Year ended 31 December

2012

Year ended 31 December

2011 £m £m Income statement Distributions received 4.9 6.1 Share of results of associate 47.5 - Interest receivable 3.4 2.1 Less: EPRA adjustments (43.2) - Total impact of VR on income statement – EPRA basis 12.6 8.2 Balance sheet Other investments - 214.0 Investment in associate 428.4 - Add: EPRA adjustments 16.2 - EPRA adjusted investment in associate 444.6 214.0 Loan to VR 47.0 23.4 Total impact of VR on balance sheet – EPRA basis 491.6 237.4

1. Share of result of associate, less EPRA adjustments, equals £4.3m, the net income from VR recognised from 21 August to 31

December 2012

Hammerson’s Investments in Value Retail

42

Holding Companies

22% equity

Holding Companies

22% equityHammerson

£47 m shareholder

loan

Bicester

Village

La Roca

Village

Las Rozas

Village

La Vallée

Village

Maasmechelen

Village

Fidenza

Village

Wertheim

Village

Ingolstadt

Village

Kildare

Village

Hammerson invests directly in Asset Companies at ‘Investor’ level.

Total Village

ownership (%)

Village Ownership

via LP’s (%)33 15 15 0 13 20 31 0 3

45 26 26 11 24 32 43 11 14

Value Retail investment to associate

200

240

280

320

360

400

440

Additions

Revaluation

31 Aug 2012

Associate

Share of

Income (1)

Distribution

EPRA

adjustments

1 Jan 2012

Investment

31 Dec 2012

Associate

94

214

74 382

48

(2)16

444

431. Includes £38 million portfolio revaluation uplift

£m

Debt maturity (1)

44

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028

£m

Bank debt drawn Secured debt Euro bonds Sterling bonds Undrawn facilities

1 Does not include new £175m credit facility with April 2018 maturity

2012 components of valuation change

45

(7.1)

(25.9)(30.4)

(6.6)

(70.0)

(9.2)

37.9

(15.6)

(6.7)

6.3

(4.9)

8.8

15.3

(4.0)

15.2

(21.2)

20.7

(30.7)

(17.3)

(48.6)

-80

-60

-40

-20

0

20

40

60

UK shopping centres France retail UK retail parks UK other Total continuing

portfolio

Yield

Income

Development and

other

Total

£m

Rental uplifts from reversions

46

Outstanding rent

reviews 2012 2013 2014 Total

£m £m £m £m £m

Expiries and breaks (UK and France)

ERV 45.8 19.5 17.4 82.7

Passing rents 40.0 19.3 16.8 76.1

Uplift 5.8 0.2 0.6 6.6

Rent reviews (UK only)

ERV 44.5 26.0 43.5 27.5 141.5

Passing rents 41.3 24.3 41.8 25.0 132.4

Uplift 3.2 1.7 1.7 2.5 9.1

Total uplift 3.2 7.5 1.9 3.1 15.7

Trading environment

47

27 Feb 2013

79 in administration (2.3% passing rent)

28 units unoccupied (0.7% passing rent)

UK Shopping Centres

Sales +0.4%

Footfall -2.3%

Rent:Sales 12.3% (Dec 2011: 13.2%)

France Shopping Centres

Sales -3.3%

Footfall -3.4%

Rent:Sales 10.3% (Dec 2011: 9.7%)

31 Dec 2012

63 units in administration (1.19% passing rent)

25 units unoccupied (0.5% passing rent)

Sales & Footfall

Group administrations – 2800 units in portfolio