Embed Size (px)

Citation preview

Mirvac Grouphalf-yearly report 1999

DEVELOPMENT

INVESTMENT

HOTELS

indexC h a i r m a n ’ s R e p o r t 1

M a n a g i n g D i r e c t o r ’ s C o m m e n t a r y 2

D i r e c t o r s ’ S t a t e m e n t 4

P r o f i t a n d L o s s S t a t e m e n t 6

B a l a n c e S h e e t 7

C o m b i n e d C a s h F l o w s S t a t e m e n t 8

N o t e s t o t h e F i n a n c i a l S t a t e m e n t s 9

D i r e c t o r s ’ D e c l a r a t i o n 1 6

I n d e p e n d e n t R e v i e w R e p o r t 1 7

All Securityholder enquiries should be directed to:

The Registrar Mirvac Group Locked Bag A14Sydney South NSW 1232Telephone 1800 356 444.

In all communications please quote your Securityholder Reference Number (SRN) located at thetop right-hand corner of your statement. Written enquiries and amendments to holdings must besigned by all registered Securityholders for that holding.

Change of name or address: Notification of all changes must be made in writing. Proof of namechange will be necessary. If you are a registered CHESS participant, please advise yourstockbroker of the changes.

Tax File Numbers (TFNs): The registrar is obliged to deduct tax at the highest marginal ratefrom distribution payments to those Securityholders who are resident in Australia and have notprovided their tax file number or exemption details. In case of a joint holding, TFNs or exemptiondetails must be provided for both/all parties.

Website: the Mirvac Group has now established a fully functional and informative web site,Mirvac Online. Mirvac Online is being designed to not only showcase the Group’s manyinvestments, development projects and Hotels but to also provide important, up to the minuteinformation to Securityholders. Please visit Mirvac Online at www.mirvac.com.au

securityholder support

chairman’s report

TH

E M

IRV

AC

GR

OU

P H

AL

F-Y

EA

R R

EP

OR

T 1

99

9

I am pleased to advise Securityholders that forthe six-month period ending 31 December1999, the Mirvac Group achieved an after taxprofit of $77.4 million. This result representsan increase of 28% over the previouscorresponding period on a pro-forma basis.

Importantly for Securityholders, the result alsorepresents a 21% increase in both operatingearnings and distribution per security over theprevious corresponding period on a pro-formabasis.

It has now been eight months since theformation of the Mirvac Group and byeffectively maintaining the momentumgenerated, we have positioned the Group toexceed the profit forecasts made at that time.

Over the latter part of 1999 and into this year,management has worked extremely hard insecuring a number of opportunities that willadd value for Securityholders and reflects theimplementation of our strategies to furtherenhance investor returns.

At the Annual General Meetings held inNovember 1999, several members requestedclarification of Securityholder benefitsavailable throughout Mirvac’s range of fourand five star Hotels. Please find enclosed withthis report a complete listing of the Group’sHotels and special rates available to allSecurityholders. It is important to note thatthese rates are subject to availability, andowing to the imposition of the GST in July,are valid to 30 June 2000.

I would also like to draw your attention to thelisting of the key dates for the coming year.

Finally, all this information and more detailedSecurityholder information is availablethrough the Mirvac Group’s website atwww.mirvac.com.au

Adrian Lane

Chairman

1

Shoremark, St Leonards

The Mirvac Group has now realised theoperating efficiencies brought about by themerger and we continue to capitalise on aplatform for growth provided across allDivisions.

PROPERTY INVESTMENT

During the period to 30 December 1999, on apro-forma basis over the same period last yearthe Investment Division realised an increase inits contribution to Group profits of 16%.

Essentially, the growth of the InvestmentDivision was achieved through the full yearimpact of several key assets including theComo Centre, No. 1 Castlereagh Street andthe Group’s 50% stake in Westpac Plaza.

The performance of the Investment Divisionhas been very pleasing, particularly the growthachieved within our retail portfolio, whichshowed a 9.3% increase in moving annualturnover, and the recent completion of theextension and refurbishment of the GippslandCentre in the Victorian regional centre of Salecertainly assisted this.

The Division also successfully leased orrenegotiated tenancies over a total of 15% ofthe entire portfolio during the six months to30 December, which effectively increased totalGroup occupancy to over 98.2%.

As a Group, we will continue to seekinvestment opportunities that providedevelopment or redevelopment potential thathas the capacity to add value and henceinvestment returns from our diverse portfolio.

PROPERTY DEVELOPMENT

During the six months to December, theProperty Development Division contributed atotal of 32.5% of the Group’s profits which isessentially in line with our objectives that wereoutlined at the time of the merger.

The Development Division, particularly ourhouse-and-land packaging operations havebenefited from a ‘pull forward’ in demandbrought about by the imminent introductionof the GST. Although the recent interest rateincreases and the run-up to the GST has seenan overall market slow down, the market hasgenerally returned to more sensible andsustainable levels.

Over the latter part of 1999 and during thefirst two months of 2000, we have been able tocomplement our existing major projects withseveral excellent long-term opportunities.These include a major residential andcommercial development site immediately tothe north of Chatswood railway station, aJoint Venture arrangement with Landcom todevelop the 1,800 lot Stanhope Gardens estatein Sydney’s north-west, and the purchase of CSR’s former sugar refinery on the Brisbane River. Including these opportunities,the Mirvac Group now controls sites for over 11,000 dwellings and 80,000 m2 ofcommercial space.

In terms of current projects, I am pleased toreport that the Group is currently holdingexchanged contracts of sale, totalling over$423 million. Importantly, revenue that willnot be brought to account until settlement.

Notwithstanding the current industrialdifficulties being experienced in Victoria, thesustainability of the Group’s forward workloadhas been enhanced, and we are well placed tocontinue to grow our development earnings.

HOTEL MANAGEMENT

During the period to 30 December 1999, on apro-forma basis over the same period last yearthe Hotel Division increased its contributionto total Group profits by 36%.

TH

E M

IRV

AC

GR

OU

P H

AL

F-Y

EA

R R

EP

OR

T 1

99

9

2

managing director’s commentary

TH

E M

IRV

AC

GR

OU

P H

AL

F-Y

EA

R R

EP

OR

T 1

99

9

3

operational overview

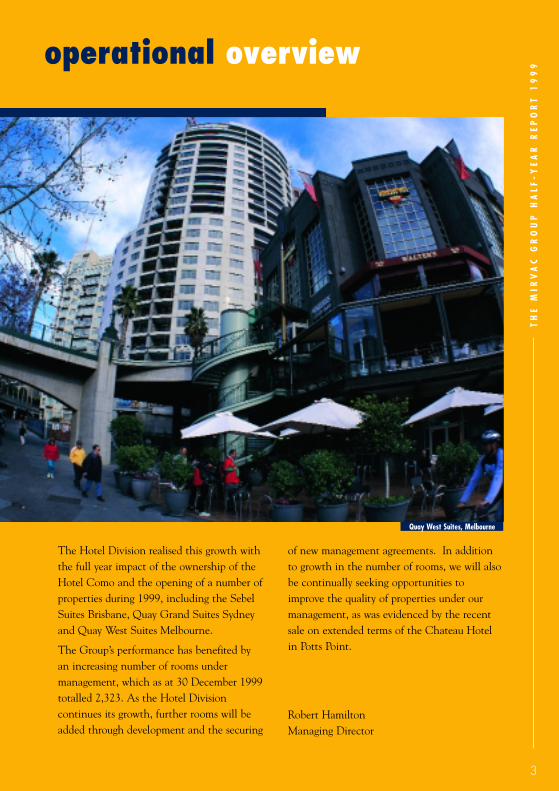

Quay West Suites, Melbourne

The Hotel Division realised this growth withthe full year impact of the ownership of theHotel Como and the opening of a number ofproperties during 1999, including the SebelSuites Brisbane, Quay Grand Suites Sydneyand Quay West Suites Melbourne.

The Group’s performance has benefited by an increasing number of rooms undermanagement, which as at 30 December 1999totalled 2,323. As the Hotel Divisioncontinues its growth, further rooms will beadded through development and the securing

of new management agreements. In additionto growth in the number of rooms, we will alsobe continually seeking opportunities toimprove the quality of properties under ourmanagement, as was evidenced by the recentsale on extended terms of the Chateau Hotelin Potts Point.

Robert HamiltonManaging Director

TH

E M

IRV

AC

GR

OU

P H

AL

F-Y

EA

R R

EP

OR

T 1

99

9

4

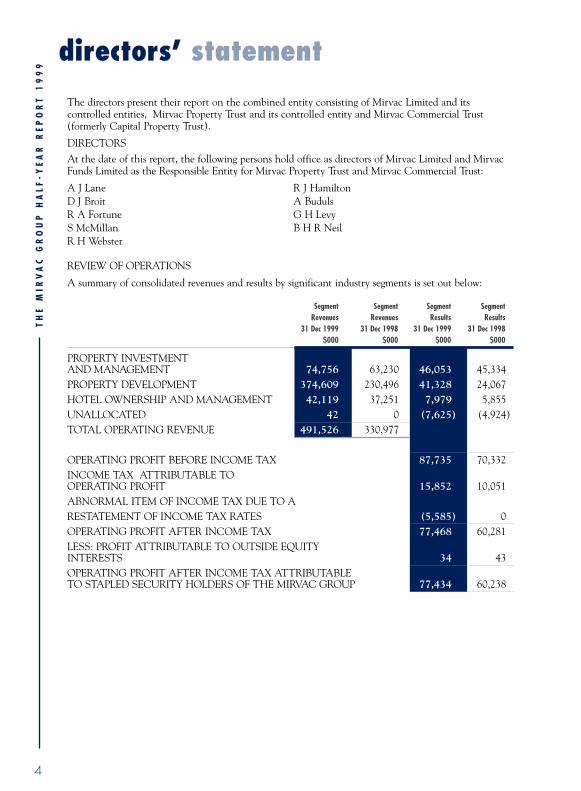

directors’ statement

The directors present their report on the combined entity consisting of Mirvac Limited and itscontrolled entities, Mirvac Property Trust and its controlled entity and Mirvac Commercial Trust(formerly Capital Property Trust).

DIRECTORS

At the date of this report, the following persons hold office as directors of Mirvac Limited and MirvacFunds Limited as the Responsible Entity for Mirvac Property Trust and Mirvac Commercial Trust:

A J Lane R J HamiltonD J Broit A BudulsR A Fortune G H LevyS McMillan B H R NeilR H Webster

REVIEW OF OPERATIONS

A summary of consolidated revenues and results by significant industry segments is set out below:

Segment Segment Segment SegmentRevenues Revenues Results Results

31 Dec 1999 31 Dec 1998 31 Dec 1999 31 Dec 1998$000 $000 $000 $000

PROPERTY INVESTMENT AND MANAGEMENT 74,756 63,230 46,053 45,334 PROPERTY DEVELOPMENT 374,609 230,496 41,328 24,067 HOTEL OWNERSHIP AND MANAGEMENT 42,119 37,251 7,979 5,855 UNALLOCATED 42 0 (7,625) (4,924)TOTAL OPERATING REVENUE 491,526 330,977

OPERATING PROFIT BEFORE INCOME TAX 87,735 70,332INCOME TAX ATTRIBUTABLE TO OPERATING PROFIT 15,852 10,051ABNORMAL ITEM OF INCOME TAX DUE TO A RESTATEMENT OF INCOME TAX RATES (5,585) 0 OPERATING PROFIT AFTER INCOME TAX 77,468 60,281 LESS: PROFIT ATTRIBUTABLE TO OUTSIDE EQUITYINTERESTS 34 43OPERATING PROFIT AFTER INCOME TAX ATTRIBUTABLETO STAPLED SECURITY HOLDERS OF THE MIRVAC GROUP 77,434 60,238

TH

E M

IRV

AC

GR

OU

P H

AL

F-Y

EA

R R

EP

OR

T 1

99

9

5

Comments on the operations and the results of those operations are set out below:

(a) Property Investment

The division increased its operating revenue by 18.2%, while operating profit before tax and revaluationof investment properties increased by 16.1%. The growth of the division was achieved through the fullyear impact of several key assets including the Como Centre, No. 1 Castlereagh Street and the Group’s50% stake in Westpac Plaza. The division also successfully leased or negotiated tenancies over a total of15% of the entire portfolio during the period, which effectively increased occupancy to over 98.2%.

(b) Property Development

The division achieved a 62.5% increase in operating revenue and a 71.7% increase in operating profitbefore tax. House and land packages have benefited from the pre-GST activity, and while the overallmarket has slowed somewhat due to recent interest rate increases and the run up to the GSTimplementation, activity has returned to more sustainable levels.

(c) Hotels

The hotels division, through a combination of acquisitions and new managements, has benefited fromthe increasing number of rooms under management. Operating revenue increased by 13.1%, whileoperating profit before tax increased by 36.3%, reflecting the less than full period impact of newacquisitions and managements.

ROUNDING OF AMOUNTS TO NEAREST THOUSAND DOLLARS

Mirvac Limited, Mirvac Commercial Trust and Mirvac Property Trust are entities of the kind referred toin Class Order 98/0100 issued by the Australian Securities & Investments Commission, relating to the“rounding off” of amounts in the financial report. Amounts in the financial report have been roundedoff to the nearest thousand dollars in accordance with that Class Order.

This statement is made in accordance with a resolution of the directors of Mirvac Limited and MirvacFunds Limited.

Signed at Sydney this twenty-fourth day of February 2000.

AJ LANE RJ HAMILTONDirector Director

6

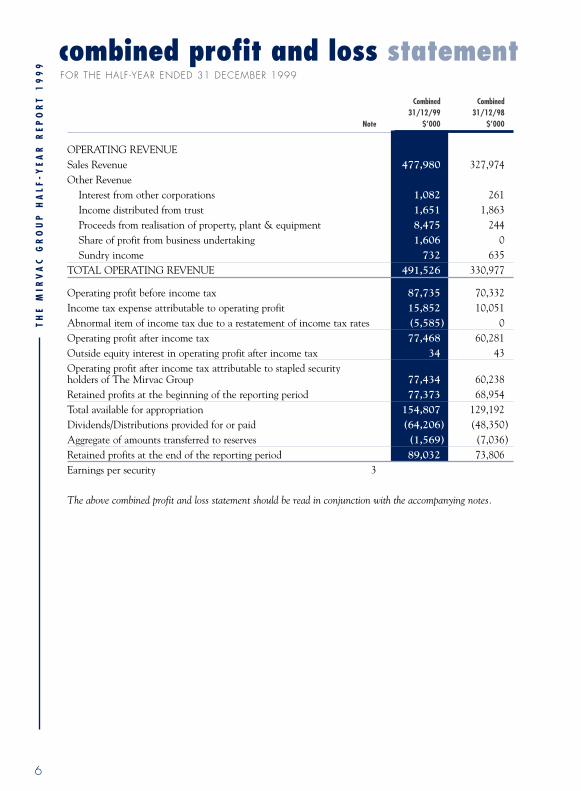

combined profit and loss statementFOR THE HALF-YEAR ENDED 31 DECEMBER 1999

Combined Combined31/12/99 31/12/98

Note $’000 $’000

OPERATING REVENUESales Revenue 477,980 327,974 Other Revenue

Interest from other corporations 1,082 261Income distributed from trust 1,651 1,863Proceeds from realisation of property, plant & equipment 8,475 244 Share of profit from business undertaking 1,606 0 Sundry income 732 635

TOTAL OPERATING REVENUE 491,526 330,977

Operating profit before income tax 87,735 70,332Income tax expense attributable to operating profit 15,852 10,051Abnormal item of income tax due to a restatement of income tax rates (5,585) 0Operating profit after income tax 77,468 60,281Outside equity interest in operating profit after income tax 34 43 Operating profit after income tax attributable to stapled securityholders of The Mirvac Group 77,434 60,238 Retained profits at the beginning of the reporting period 77,373 68,954Total available for appropriation 154,807 129,192 Dividends/Distributions provided for or paid (64,206) (48,350)Aggregate of amounts transferred to reserves (1,569) (7,036)Retained profits at the end of the reporting period 89,032 73,806 Earnings per security 3

The above combined profit and loss statement should be read in conjunction with the accompanying notes.

TH

E M

IRV

AC

GR

OU

P H

AL

F-Y

EA

R R

EP

OR

T 1

99

9

7

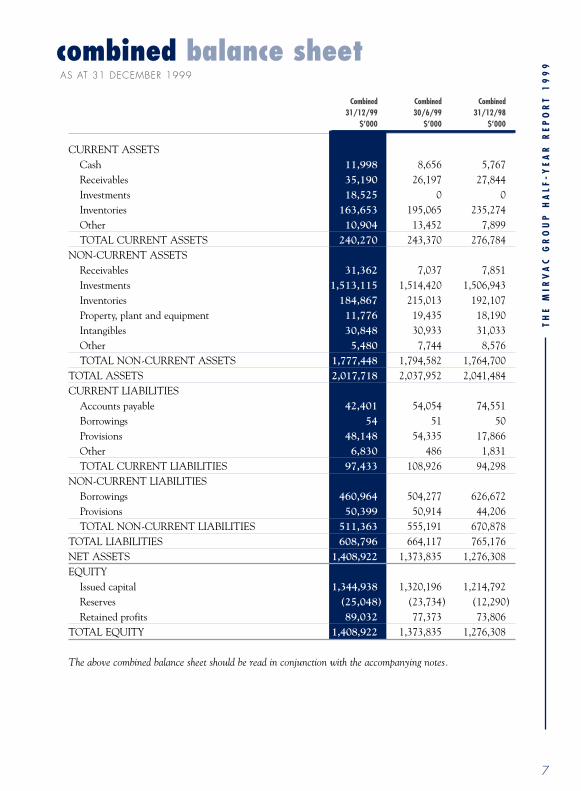

combined balance sheetAS AT 31 DECEMBER 1999

TH

E M

IRV

AC

GR

OU

P H

AL

F-Y

EA

R R

EP

OR

T 1

99

9

Combined Combined Combined31/12/99 30/6/99 31/12/98

$’000 $’000 $’000

CURRENT ASSETSCash 11,998 8,656 5,767 Receivables 35,190 26,197 27,844 Investments 18,525 0 0 Inventories 163,653 195,065 235,274 Other 10,904 13,452 7,899 TOTAL CURRENT ASSETS 240,270 243,370 276,784

NON-CURRENT ASSETSReceivables 31,362 7,037 7,851Investments 1,513,115 1,514,420 1,506,943 Inventories 184,867 215,013 192,107 Property, plant and equipment 11,776 19,435 18,190 Intangibles 30,848 30,933 31,033 Other 5,480 7,744 8,576 TOTAL NON-CURRENT ASSETS 1,777,448 1,794,582 1,764,700

TOTAL ASSETS 2,017,718 2,037,952 2,041,484 CURRENT LIABILITIES

Accounts payable 42,401 54,054 74,551 Borrowings 54 51 50 Provisions 48,148 54,335 17,866 Other 6,830 486 1,831 TOTAL CURRENT LIABILITIES 97,433 108,926 94,298

NON-CURRENT LIABILITIESBorrowings 460,964 504,277 626,672 Provisions 50,399 50,914 44,206 TOTAL NON-CURRENT LIABILITIES 511,363 555,191 670,878

TOTAL LIABILITIES 608,796 664,117 765,176 NET ASSETS 1,408,922 1,373,835 1,276,308EQUITY

Issued capital 1,344,938 1,320,196 1,214,792Reserves (25,048) (23,734) (12,290)Retained profits 89,032 77,373 73,806

TOTAL EQUITY 1,408,922 1,373,835 1,276,308

The above combined balance sheet should be read in conjunction with the accompanying notes.

8

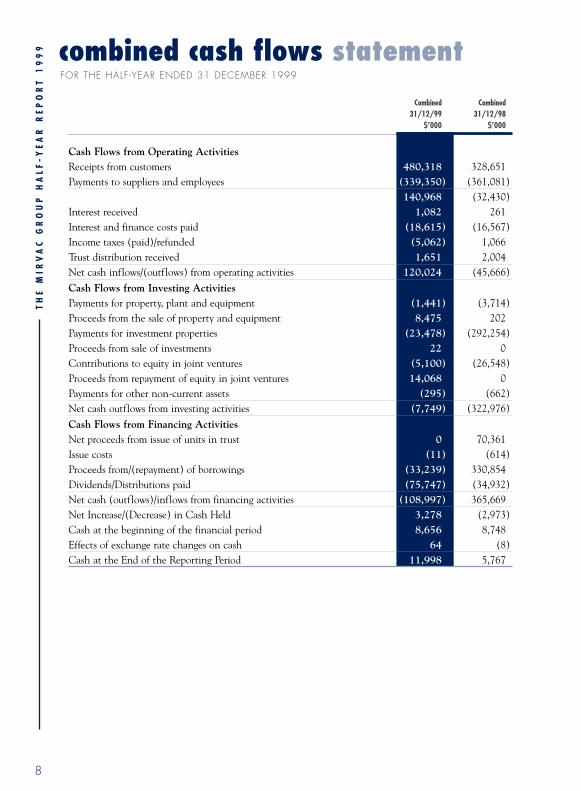

combined cash flows statementFOR THE HALF-YEAR ENDED 31 DECEMBER 1999

TH

E M

IRV

AC

GR

OU

P H

AL

F-Y

EA

R R

EP

OR

T 1

99

9

Combined Combined31/12/99 31/12/98

$’000 $’000

Cash Flows from Operating ActivitiesReceipts from customers 480,318 328,651 Payments to suppliers and employees (339,350) (361,081)

140,968 (32,430)Interest received 1,082 261 Interest and finance costs paid (18,615) (16,567)Income taxes (paid)/refunded (5,062) 1,066Trust distribution received 1,651 2,004 Net cash inflows/(outflows) from operating activities 120,024 120,024 (45,666)

Cash Flows from Investing ActivitiesPayments for property, plant and equipment (1,441) (3,714)Proceeds from the sale of property and equipment 8,475 202 Payments for investment properties (23,478) (292,254)Proceeds from sale of investments 22 0 Contributions to equity in joint ventures (5,100) (26,548)Proceeds from repayment of equity in joint ventures 14,068 0Payments for other non-current assets (295) (662)Net cash outflows from investing activities (7,749) (322,976)

Cash Flows from Financing ActivitiesNet proceeds from issue of units in trust 0 70,361 Issue costs (11) (614)Proceeds from/(repayment) of borrowings (33,239) 330,854 Dividends/Distributions paid (75,747) (34,932)Net cash (outflows)/inflows from financing activities (108,997) 365,669Net Increase/(Decrease) in Cash Held 3,278 (2,973)Cash at the beginning of the financial period 8,656 8,748Effects of exchange rate changes on cash 64 (8)Cash at the End of the Reporting Period 11,998 5,767

9

NOTE 1. BASIS OF PREPARATION OF HALF-YEAR FINANCIAL STATEMENTSThe Mirvac Group - Stapling of Securities

The Mirvac Group was formed by the stapling of the securities of three listed entities comprisingMirvac Limited, Mirvac Commercial Trust and Mirvac Property Trust.

The resulting Mirvac Group Stapled Securities, quoted and traded together on the Australian StockExchange, comprise one Consolidated Mirvac Limited share, one Consolidated Mirvac CommercialTrust unit and one Consolidated Mirvac Property Trust unit.

The stapled securities cannot be traded or dealt with separately.

Trading of the stapled securities (with deferred settlement) commenced on 18 June 1999.

With the establishment of The Mirvac Group and its common investors, the combined group hascommon directors and common business objectives, and operates as a combined entity with three corebusinesses:

- Property investment and management

- Property development

- Hotel management

The three Mirvac entities comprising the stapled group, remain separate legal entities in accordancewith the Corporations Law, and are each required to comply with the reporting and disclosurerequirements of Accounting Standards and the Corporations Regulations.

The Stapled Security structure will cease to operate on the first to occur of:

- any of Mirvac Limited, Mirvac Commercial Trust or Mirvac Property Trust resolving by specialresolution in general meeting and in accordance with its constitution to terminate the staplingprovisions; or

- the commencement of the winding up of Mirvac Limited, Mirvac Commercial Trust or MirvacProperty Trust.

The Australian Stock Exchange reserves the right (but without limiting its absolute discretion) toremove one or more entities of the same class with stapled securities from the official list if any of theirsecurities are issued by one entity which are not stapled to equivalent securities in the other entity orentities.

Basis of Accounting

The financial statements of The Mirvac Group consist of the aggregated financial statements of thecombined entity comprising Mirvac Limited and its controlled entities, Mirvac Property Trust and itscontrolled entity and Mirvac Commercial Trust. None of the entities whose securities are stapled is aparent of the other entities and the entities do not have a common parent.

The financial statements are a general purpose financial report, which have been prepared to satisfy therequirements of the Urgent Issues Group Consensus View 13, “The Presentation of the FinancialReport of Entities Whose Securities are Stapled”, and in accordance with Accounting Standard AASB1029: Half-Year Accounts and Consolidated Accounts, and other mandatory professional reportingrequirements (Urgent Issues Group Concensus Views).

It is recommended that this report should be read in conjunction with the Annual Report for the yearended 30 June 1999 and any public announcements made by The Mirvac Group during the half-year inaccordance with the continuous disclosure requirements of the Listing Rules of the Australian StockExchange.

TH

E M

IRV

AC

GR

OU

P H

AL

F-Y

EA

R R

EP

OR

T 1

99

9

notes to the financial statementsFOR THE HALF-YEAR ENDED 31 DECEMBER 1999

10

notes to the financial statementsFOR THE HALF-YEAR ENDED 31 DECEMBER 1999

TH

E M

IRV

AC

GR

OU

P H

AL

F-Y

EA

R R

EP

OR

T 1

99

9

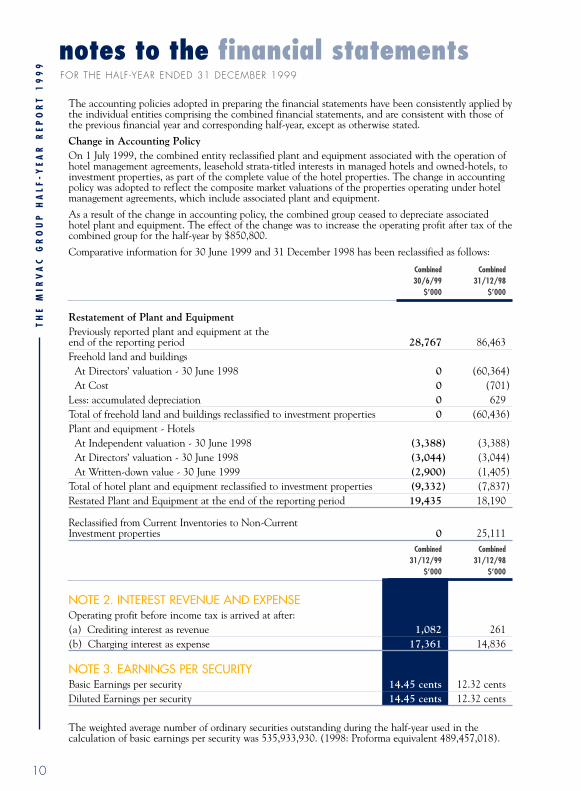

The accounting policies adopted in preparing the financial statements have been consistently applied bythe individual entities comprising the combined financial statements, and are consistent with those ofthe previous financial year and corresponding half-year, except as otherwise stated.

Change in Accounting PolicyOn 1 July 1999, the combined entity reclassified plant and equipment associated with the operation ofhotel management agreements, leasehold strata-titled interests in managed hotels and owned-hotels, toinvestment properties, as part of the complete value of the hotel properties. The change in accountingpolicy was adopted to reflect the composite market valuations of the properties operating under hotelmanagement agreements, which include associated plant and equipment.

As a result of the change in accounting policy, the combined group ceased to depreciate associatedhotel plant and equipment. The effect of the change was to increase the operating profit after tax of thecombined group for the half-year by $850,800.

Comparative information for 30 June 1999 and 31 December 1998 has been reclassified as follows:

Combined Combined30/6/99 31/12/98

$’000 $’000

Restatement of Plant and EquipmentPreviously reported plant and equipment at the end of the reporting period 28,767 86,463 Freehold land and buildings

At Directors’ valuation - 30 June 1998 0 (60,364)At Cost 0 (701)

Less: accumulated depreciation 0 629 Total of freehold land and buildings reclassified to investment properties 0 (60,436)Plant and equipment - Hotels

At Independent valuation - 30 June 1998 (3,388) (3,388)At Directors’ valuation - 30 June 1998 (3,044) (3,044)At Written-down value - 30 June 1999 (2,900) (1,405)

Total of hotel plant and equipment reclassified to investment properties (9,332) (7,837)Restated Plant and Equipment at the end of the reporting period 19,435 18,190

Reclassified from Current Inventories to Non-Current Investment properties 0 25,111

Combined Combined31/12/99 31/12/98

$’000 $’000

NOTE 2. INTEREST REVENUE AND EXPENSEOperating profit before income tax is arrived at after:(a) Crediting interest as revenue 1,082 261 (b) Charging interest as expense 17,361 14,836

NOTE 3. EARNINGS PER SECURITYBasic Earnings per security 14.45 cents 12.32 centsDiluted Earnings per security 14.45 cents 12.32 cents

The weighted average number of ordinary securities outstanding during the half-year used in thecalculation of basic earnings per security was 535,933,930. (1998: Proforma equivalent 489,457,018).

11

TH

E M

IRV

AC

GR

OU

P H

AL

F-Y

EA

R R

EP

OR

T 1

99

9

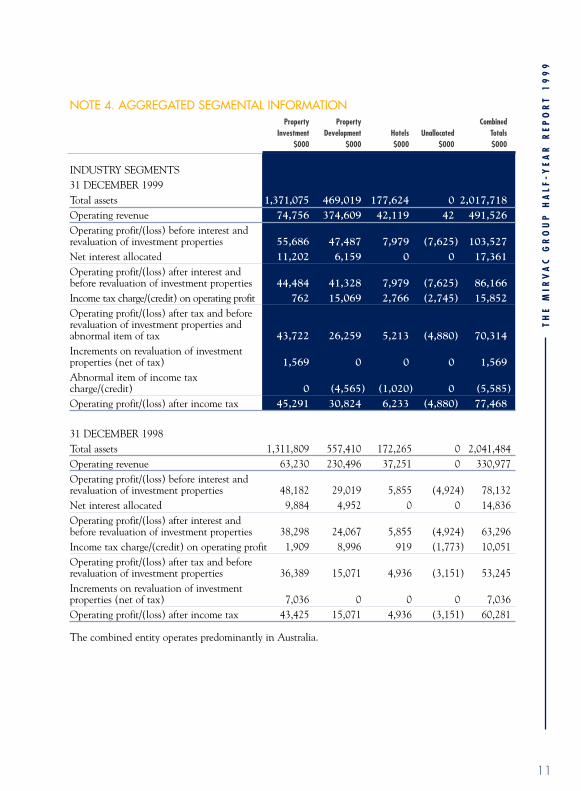

NOTE 4. AGGREGATED SEGMENTAL INFORMATIONProperty Property Combined

Investment Development Hotels Unallocated Totals$000 $000 $000 $000 $000

INDUSTRY SEGMENTS31 DECEMBER 1999Total assets 1,371,075 469,019 177,624 0 2,017,718 Operating revenue 74,756 374,609 42,119 42 491,526 Operating profit/(loss) before interest andrevaluation of investment properties 55,686 47,487 7,979 (7,625) 103,527 Net interest allocated 11,202 6,159 0 0 17,361 Operating profit/(loss) after interest and before revaluation of investment properties 44,484 41,328 7,979 (7,625) 86,166 Income tax charge/(credit) on operating profit 762 15,069 2,766 (2,745) 15,852 Operating profit/(loss) after tax and before revaluation of investment properties andabnormal item of tax 43,722 26,259 5,213 (4,880) 70,314 Increments on revaluation of investmentproperties (net of tax) 1,569 0 0 0 1,569 Abnormal item of income tax charge/(credit) 0 (4,565) (1,020) 0 (5,585)Operating profit/(loss) after income tax 45,291 30,824 6,233 (4,880) 77,468

31 DECEMBER 1998Total assets 1,311,809 557,410 172,265 0 2,041,484 Operating revenue 63,230 230,496 37,251 0 330,977 Operating profit/(loss) before interest andrevaluation of investment properties 48,182 29,019 5,855 (4,924) 78,132 Net interest allocated 9,884 4,952 0 0 14,836 Operating profit/(loss) after interest and before revaluation of investment properties 38,298 24,067 5,855 (4,924) 63,296 Income tax charge/(credit) on operating profit 1,909 8,996 919 (1,773) 10,051 Operating profit/(loss) after tax and before revaluation of investment properties 36,389 15,071 4,936 (3,151) 53,245 Increments on revaluation of investment properties (net of tax) 7,036 0 0 0 7,036 Operating profit/(loss) after income tax 43,425 15,071 4,936 (3,151) 60,281

The combined entity operates predominantly in Australia.

12

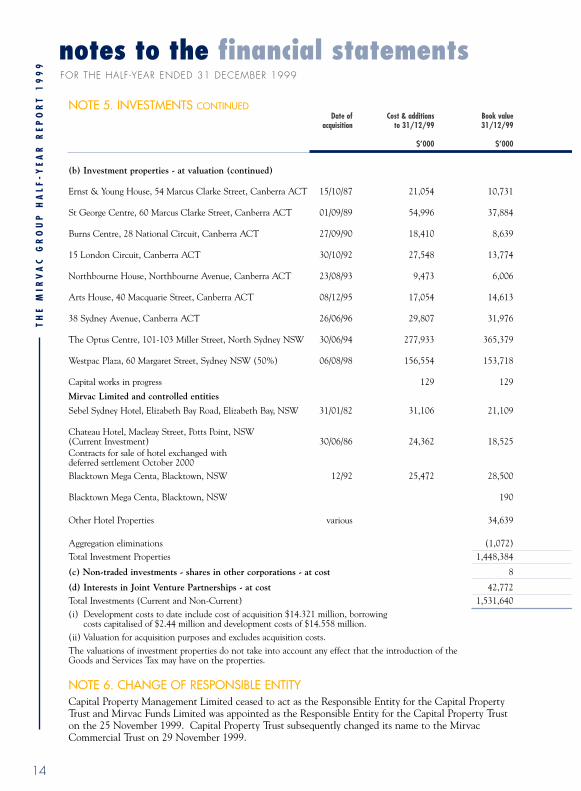

NOTE 5. INVESTMENTSDate of Cost & additions Book value

acquisition to 31/12/99 31/12/99

$’000 $’000

(a) Units in unlisted trusts - at valuation

St Kilda Road Trust - 40,238,686 units - 50% interest 04/10/95 40,305 40,476

Total units in unlisted trusts 40,476

(b) Investment properties - at valuation

Mirvac Property Trust

67 Albert Avenue, Chatswood, NSW 01/09/89 52,638 62,457

30 Cowper Street, Parramatta, NSW 01/09/88 15,670 17,250

Quay West Car Park, 111 Harrington Street, Sydney, NSW 30/11/89 36,995 38,012

Orange City, Orange, NSW 05/04/93 28,469 29,178

Kawana Shoppingworld, Buddina, QLD 09/12/93 74,956 85,667

Gippsland Centre, Cunningham Street, Sale, VIC 06/01/94 32,136 31,012

Como Centre, Cnr Toorak Road & Chapel Street, South Yarra, VIC. 18/08/98 102,405 106,534

Parramatta Industrial Estate, Boundary Road, Northmead, NSW 14/07/94 18,181 24,129

20-30 Scrivener Street, Warwick Farm, NSW 24/12/93 17,575 17,021

Aspley Hypermarket, 59 Albany Creek Road, Aspley, QLD 20/12/94 70,074 65,108

Woden Tower, Keltie Street, Phillip, ACT 14/07/94 46,617 36,903

The Marriott Hotel, College Street and Hargrave Street, Sydney, NSW 31/12/91 97,503 80,719

Miller Street Development, 40 Miller Street, North Sydney, NSW 31/03/98 31,208 31,319

1 Castlereagh Street, Sydney NSW 18/12/98 45,919 45,919

Mirvac Commercial Trust

24 Marcus Clarke Street, Canberra ACT 03/09/84 5,526 3,017

Cooyong Centre, Cnr Cooyong & Torrens Streets, Canberra ACT 01/07/81 5,071 3,628

8 Brisbane Avenue, Canberra ACT 28/06/85 12,103 9,138

Law Society Building, 11 London Circuit, Canberra ACT 09/03/87 9,487 6,701

Perpetual Trustees Building, 10 Rudd Street, Canberra ACT 15/10/87 18,918 9,932

TH

E M

IRV

AC

GR

OU

P H

AL

F-Y

EA

R R

EP

OR

T 1

99

9

notes to the financial statementsFOR THE HALF-YEAR ENDED 31 DECEMBER 1999

13

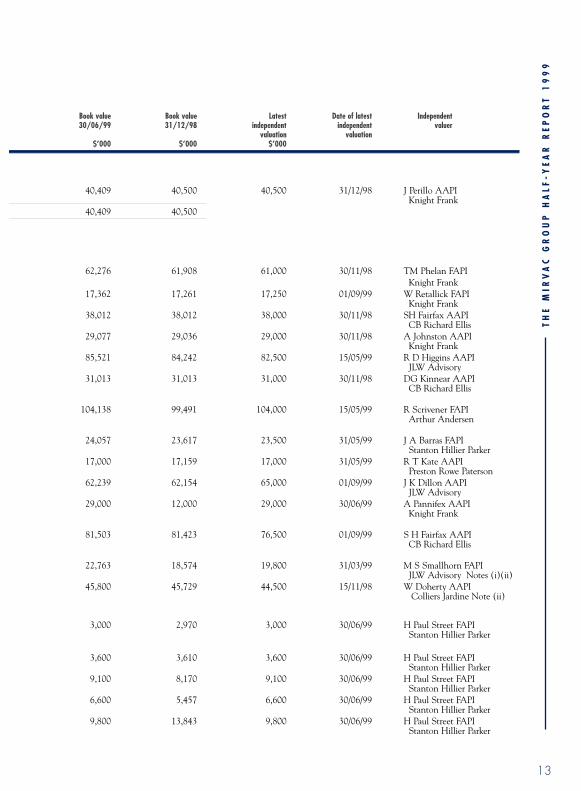

Book value Book value Latest Date of latest Independent 30/06/99 31/12/98 independent independent valuer

valuation valuation$’000 $’000 $’000

40,409 40,500 40,500 31/12/98 J Perillo AAPIKnight Frank

40,409 40,500

62,276 61,908 61,000 30/11/98 TM Phelan FAPI Knight Frank

17,362 17,261 17,250 01/09/99 W Retallick FAPIKnight Frank

38,012 38,012 38,000 30/11/98 SH Fairfax AAPICB Richard Ellis

29,077 29,036 29,000 30/11/98 A Johnston AAPIKnight Frank

85,521 84,242 82,500 15/05/99 R D Higgins AAPIJLW Advisory

31,013 31,013 31,000 30/11/98 DG Kinnear AAPICB Richard Ellis

104,138 99,491 104,000 15/05/99 R Scrivener FAPIArthur Andersen

24,057 23,617 23,500 31/05/99 J A Barras FAPIStanton Hillier Parker

17,000 17,159 17,000 31/05/99 R T Kate AAPIPreston Rowe Paterson

62,239 62,154 65,000 01/09/99 J K Dillon AAPIJLW Advisory

29,000 12,000 29,000 30/06/99 A Pannifex AAPIKnight Frank

81,503 81,423 76,500 01/09/99 S H Fairfax AAPICB Richard Ellis

22,763 18,574 19,800 31/03/99 M S Smallhorn FAPIJLW Advisory Notes (i)(ii)

45,800 45,729 44,500 15/11/98 W Doherty AAPIColliers Jardine Note (ii)

3,000 2,970 3,000 30/06/99 H Paul Street FAPIStanton Hillier Parker

3,600 3,610 3,600 30/06/99 H Paul Street FAPIStanton Hillier Parker

9,100 8,170 9,100 30/06/99 H Paul Street FAPIStanton Hillier Parker

6,600 5,457 6,600 30/06/99 H Paul Street FAPIStanton Hillier Parker

9,800 13,843 9,800 30/06/99 H Paul Street FAPIStanton Hillier Parker

TH

E M

IRV

AC

GR

OU

P H

AL

F-Y

EA

R R

EP

OR

T 1

99

9

14

TH

E M

IRV

AC

GR

OU

P H

AL

F-Y

EA

R R

EP

OR

T 1

99

9

NOTE 5. INVESTMENTS CONTINUEDDate of Cost & additions Book value

acquisition to 31/12/99 31/12/99

$’000 $’000

(b) Investment properties - at valuation (continued)

Ernst & Young House, 54 Marcus Clarke Street, Canberra ACT 15/10/87 21,054 10,731

St George Centre, 60 Marcus Clarke Street, Canberra ACT 01/09/89 54,996 37,884

Burns Centre, 28 National Circuit, Canberra ACT 27/09/90 18,410 8,639

15 London Circuit, Canberra ACT 30/10/92 27,548 13,774

Northbourne House, Northbourne Avenue, Canberra ACT 23/08/93 9,473 6,006

Arts House, 40 Macquarie Street, Canberra ACT 08/12/95 17,054 14,613

38 Sydney Avenue, Canberra ACT 26/06/96 29,807 31,976

The Optus Centre, 101-103 Miller Street, North Sydney NSW 30/06/94 277,933 365,379

Westpac Plaza, 60 Margaret Street, Sydney NSW (50%) 06/08/98 156,554 153,718

Capital works in progress 129 129

Mirvac Limited and controlled entities

Sebel Sydney Hotel, Elizabeth Bay Road, Elizabeth Bay, NSW 31/01/82 31,106 21,109

Chateau Hotel, Macleay Street, Potts Point, NSW (Current Investment) 30/06/86 24,362 18,525 Contracts for sale of hotel exchanged with deferred settlement October 2000Blacktown Mega Centa, Blacktown, NSW 12/92 25,472 28,500

Blacktown Mega Centa, Blacktown, NSW 190

Other Hotel Properties various 34,639

Aggregation eliminations (1,072)Total Investment Properties 1,448,384

(c) Non-traded investments - shares in other corporations - at cost 8

(d) Interests in Joint Venture Partnerships - at cost 42,772 Total Investments (Current and Non-Current) 1,531,640 (i) Development costs to date include cost of acquisition $14.321 million, borrowing

costs capitalised of $2.44 million and development costs of $14.558 million.(ii) Valuation for acquisition purposes and excludes acquisition costs.The valuations of investment properties do not take into account any effect that the introduction of the Goods and Services Tax may have on the properties.

NOTE 6. CHANGE OF RESPONSIBLE ENTITYCapital Property Management Limited ceased to act as the Responsible Entity for the Capital Property Trust and Mirvac Funds Limited was appointed as the Responsible Entity for the Capital Property Trust on the 25 November 1999. Capital Property Trust subsequently changed its name to the Mirvac Commercial Trust on 29 November 1999.

notes to the financial statementsFOR THE HALF-YEAR ENDED 31 DECEMBER 1999

15

TH

E M

IRV

AC

GR

OU

P H

AL

F-Y

EA

R R

EP

OR

T 1

99

9

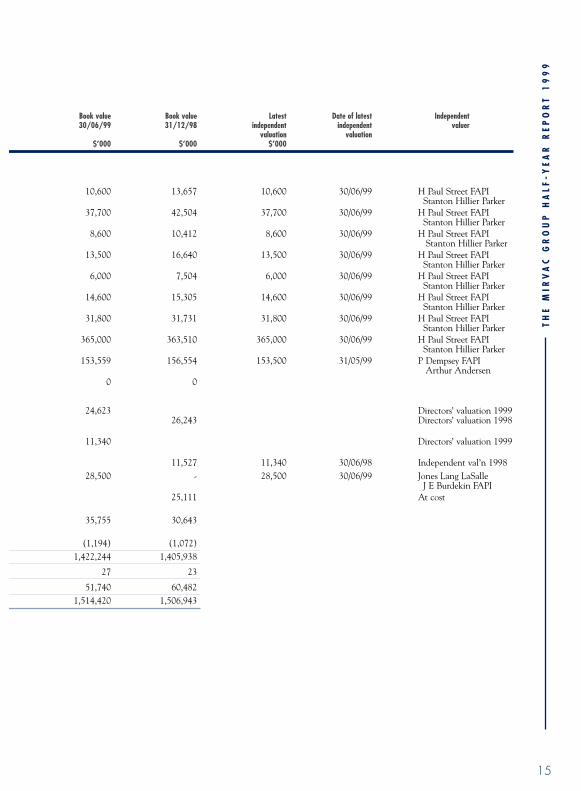

Book value Book value Latest Date of latest Independent 30/06/99 31/12/98 independent independent valuer

valuation valuation$’000 $’000 $’000

10,600 13,657 10,600 30/06/99 H Paul Street FAPIStanton Hillier Parker

37,700 42,504 37,700 30/06/99 H Paul Street FAPIStanton Hillier Parker

8,600 10,412 8,600 30/06/99 H Paul Street FAPIStanton Hillier Parker

13,500 16,640 13,500 30/06/99 H Paul Street FAPIStanton Hillier Parker

6,000 7,504 6,000 30/06/99 H Paul Street FAPIStanton Hillier Parker

14,600 15,305 14,600 30/06/99 H Paul Street FAPIStanton Hillier Parker

31,800 31,731 31,800 30/06/99 H Paul Street FAPIStanton Hillier Parker

365,000 363,510 365,000 30/06/99 H Paul Street FAPIStanton Hillier Parker

153,559 156,554 153,500 31/05/99 P Dempsey FAPIArthur Andersen

0 0

24,623 Directors’ valuation 199926,243 Directors’ valuation 1998

11,340 Directors’ valuation 1999

11,527 11,340 30/06/98 Independent val’n 1998 28,500 - 28,500 30/06/99 Jones Lang LaSalle

J E Burdekin FAPI25,111 At cost

35,755 30,643

(1,194) (1,072)1,422,244 1,405,938

27 23

51,740 60,482 1,514,420 1,506,943

16

TH

E M

IRV

AC

GR

OU

P H

AL

F-Y

EA

R R

EP

OR

T 1

99

9

The directors declare that the financial statements and notes set out on pages 6 to 15:

(a) comply with Accounting Standards and other mandatory professional reporting requirements; and

(b) give a true and fair view of the combined entity’s financial position as at 31 December 1999 and of its performance, as represented by the results of its operations and cash flows, for the half-yearended on that date.

In the directors’ opinion there are reasonable grounds to believe that the combined entity will be ableto pay its debts as and when they become due and payable.

This declaration is made in accordance with a resolution of the directors of Mirvac Limited and MirvacFunds Limited as the Responsible Entity for Mirvac Property Trust and Mirvac Commercial Trust.

Signed at Sydney this twenty-fourth day of February 2000

A J Lane RJ HamiltonDirector Director

directors’ declarationFOR THE HALF-YEAR ENDED 31 DECEMBER 1999

DE

SIG

NE

D A

ND

PR

OD

UC

ED

BY

AR

MST

RO

NG

MIL

LE

R+

MCL

AR

EN

, SY

DN

EY

AN

D M

EL

BO

UR

NE

, AU

STR

AL

IA. P

HO

TO

GR

AP

HY

BY

BO

B A

RM

STR

ON

G A

ND

MIK

EA

RM

STR

ON

G

TH

E M

IRV

AC

GR

OU

P H

AL

F-Y

EA

R R

EP

OR

T 1

99

9

Independent review report to the stapledsecurity holders of The Mirvac Group

SCOPEWe have reviewed the financial report of The Mirvac Group for the half-year ended 31 December 1999as set out on pages 6 to 16.

The financial report comprises the aggregated financial statements of Mirvac Limited and its controlledentities, Mirvac Property Trust and its controlled entity, and Mirvac Commercial Trust (formerlyCapital Property Trust).

The directors of Mirvac Limited and Mirvac Funds Limited as the Responsible Entity for both MirvacProperty Trust and Mirvac Commercial Trust are responsible for the financial report.

We have performed an independent review of the combined financial report in order for the stapledgroup to lodge the financial report with the Australian Stock Exchange. This review was performed inorder to state whether, on the basis of the procedures described, anything has come to our attentionthat would indicate that the combined financial report is not presented fairly in accordance withAccounting Standard AASB 1029: Half-Year Accounts and Consolidated Accounts, and othermandatory professional reporting requirements, so as to present a view which is consistent with ourunderstanding of The Mirvac Group’s financial position, and performance as represented by the resultsof its operations and its cash flows.

Our review has been conducted in accordance with Australian Auditing Standards applicable to reviewengagements. A review is limited primarily to inquiries of group personnel and analytical proceduresapplied to the financial data. These procedures do not provide all the evidence that would be requiredin an audit, thus the level of assurance provided is less than given in an audit. We have not performedan audit and, accordingly, we do not express an audit opinion.

STATEMENTBased on our review, which is not an audit, we have not become aware of any matter that makes usbelieve that the combined financial report of The Mirvac Group does not present fairly in accordancewith Accounting Standard AASB 1029: Half-Year Accounts and Consolidated Accounts and othermandatory professional reporting requirements, the financial position of The Mirvac Group as at 31December 1999 and the results of its operations and its cash flows for the half-year ended on that date.

PricewaterhouseCoopersChartered Accountants

B.K. Hunter SydneyPartner 24 February 2000

17

BOARD OF DIRECTORS

Adrian J Lane -

Chairman

Robert J Hamilton -Managing Director

Roger A Fortune

Barry H R Neil - CEO Investments

Dennis J Broit

Stephen R McMillan

Anna Buduls

Geoffrey H Levy

Robert J Webster

GROUP SECRETARY

Max Sheaffe

GROUP AUDITORS

PricewaterhouseCoopers

Chartered Accountants

REGISTERED OFFICE ANDPRINCIPAL OFFICE

99 Forbes Street

Woolloomooloo NSW 2011

Telephone: (02) 9357 9200

Facsimile: (02) 9380 2150

SHARE REGISTER

Perpetual RegistrarsLimited

Securities RegistrationServices

Locked Bag A14

Sydney South

NSW 1232

Telephone: (02) 9285 7111

Freecall: 1800 356 444

Facsimile: (02) 9261 8489

WEB SITEwww.mirvac.com.au

corporate directory