Embed Size (px)

Citation preview

Half year report at 30 June 2009

MISSIONSnam Rete Gas is an integrated group heading

the regulated gas sector in Italy and a major player

in Europe in terms of its regulatory asset base (RAB).

It transports and dispatches natural gas, regasifies

liquefied natural gas and distributes and stores

natural gas, with acknowledged expertise.

At Snam Rete Gas, our aim is to create value that

will fulfil our shareholders’ expectations.

This is achieved by providing our customers with services

that offers utmost security and operational reliability

and by ensuring that the domestic gas system’s

infrastructure is improved and is flexible,

assisting the development of competition in the Italian

gas market and a safe supply system.

Rete Gas pursues a sustainable model of growth

and is committed to in-depth evaluation

of the environmental impact of its activities and to

the development of new and more efficient technologies.

The company counts on the expertise of its staff

and on their constant advancement to successfully

achieve these goals.

OUR BACKGROUND

Snam Rete Gas S.p.A. was set up on 15 November 2000. On 1 July 2001,

the company became operational and received the natural gas transportation

and dispatching and the liquefied natural gas regasification lines of business

from Snam S.p.A. (now Eni S.p.A.).

On 30 June 2009, it acquired the entire share capital of Italgas S.p.A.,

the main natural gas distributor in Italy, and of Stogit, the leading natural gas

storage operator in Italy.

Snam Rete Gas shares have been listed on the Italian stock exchange

since 6 December 2001.

Half year reportat 30 June 2009

DisclaimerThis report includes forward-looking statements, especially in the section on the group’s outlook about future gas demand,investment plans and future performance. Such statements are, by their very nature, subject to risk and uncertainty as theydepend on the fact that certain events and developments will take place. The actual results may differ from those communi-cated due to different reasons, such as foreseeable trends in demand, offer and natural gas prices, general macro-economicconditions, the effect of new energy and environment legislation, the successful development and implementation of new tech-nologies, changes in the stakeholders’ expectations and other changes in business conditions.

Half year report at 30 June 2009 Directors’ report4 Acquisition of Italgas and Stogit7 Consolidation policies and scope9 Highlights

10 Key figures12 Operating review17 Financial review31 Other information35 Performance of the acquirees40 Business risk management and outlook42 Glossary

Condensed interim consolidated financial statements46 Condensed interim consolidated financial statements51 Basis of preparation and accounting policies54 Notes

77 Statement on the half year reportpursuant to article 154-bis of the Consolidated Finance Act

78 Independent auditors’ report

By Snam Rete Gas is meant Snam Rete Gas S.p.A. and the consolidated companies.

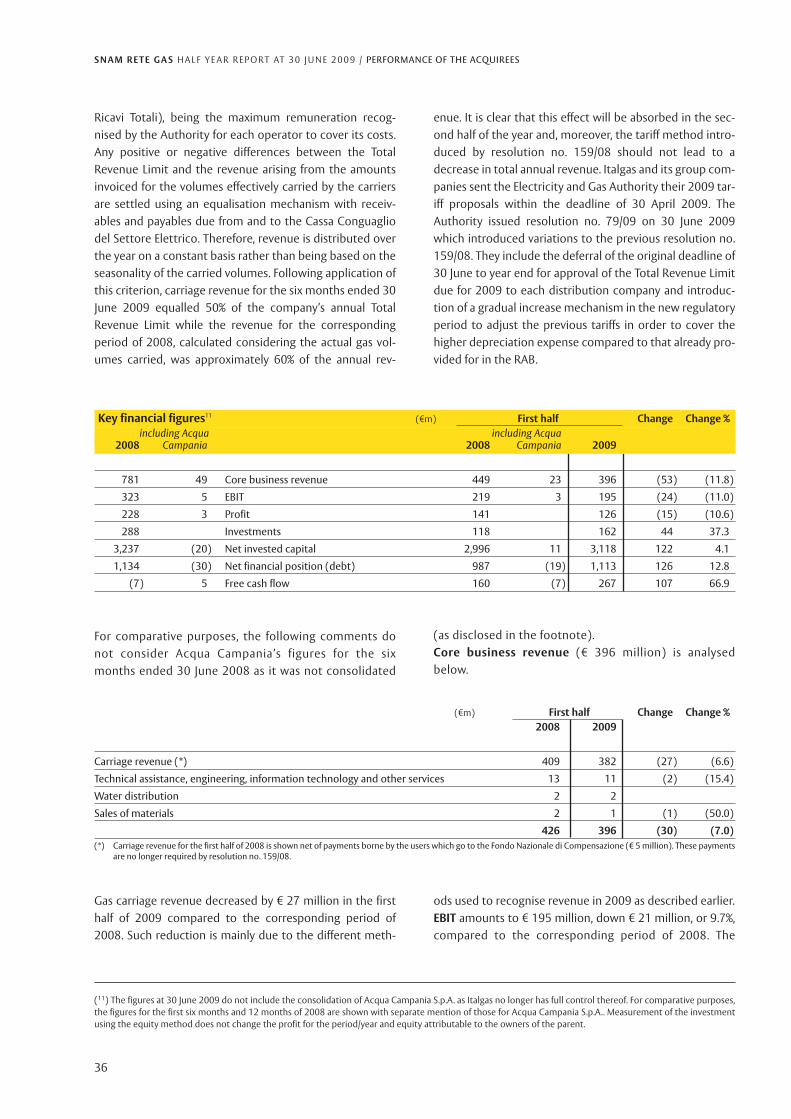

Gas of a consideration of € 4,509 million1, including €2,922 million for Italgas and € 1,587 million for Stogit. Thedifference compared to the price agreed when signing theacquisition contracts of € 148 million and € 63 million for

On 30 June 2009, the acquisition of the entire share capitalof Italgas S.p.A. and Stogit S.p.A., the major players in theItalian natural gas distribution and storage sectors, respec-tively, from Eni was carried out with payment by Snam Rete

4

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / AC Q U I S I T I O N O F I TA LG A S A N D S TO G I T

Acquisition of Italgas and Stogit

(1) This consideration is subject to possible future adjustments for both acquisitions, which were not considered when determining the price given the objectivedifficulty in making forecasts based on the currently available information. Disclosures about the price adjustment mechanisms are given in note 21 “Guarantees,commitments and risks” to the condensed interim consolidated financial statements.

5

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / AC Q U I S I T I O N O F I TA LG A S A N D S TO G I T

(2) Includes collection of the options not exercised during the offering period and auctioned on the stock exchange.(3) On 23 April 2009, Mediobanca, Morgan Stanley and UBS Investment Bank, as global coordinators and joint bookrunners, BNP PARIBAS, Credit Suisse, Merril LynchInternational and Unicredit Group (HVP), as co-bookrunners, agreed to subscribe the share capital increase for which the options had not been taken up at theclose of the stock exchange auction.(4) The predecessor values method entails recognition of amounts equal to those that would have been obtained had the acquired assets and liabilities assumedalways been included in the purchaser’s financial statements.

During the offering period, which commenced on 27 April2009 and closed on 15 May 2009, 1,756,673,448 optionswere exercised and, therefore, 1,610,283,994 new ordinarySnam Rete Gas shares were subscribed, equal to 99.75% ofthe shares offered. The unexercised 4,372,800 options, thatcould have been used to subscribe 4,008,400 new ordinaryshares, were auctioned by the company on the stockexchange, pursuant to article 2441.3 of the Italian Civil Codeduring the period from 21 to 27 May 2009. All the optionswere exercised3; therefore, 1,614,292,394 new ordinaryshares were subscribed, equal to 100% of the shares offered.

Effects of the acquisition on the half year reportThe 2009 half year report includes the effects of consolidat-ing Italgas and Stogit from the acquisition date, ie, from the

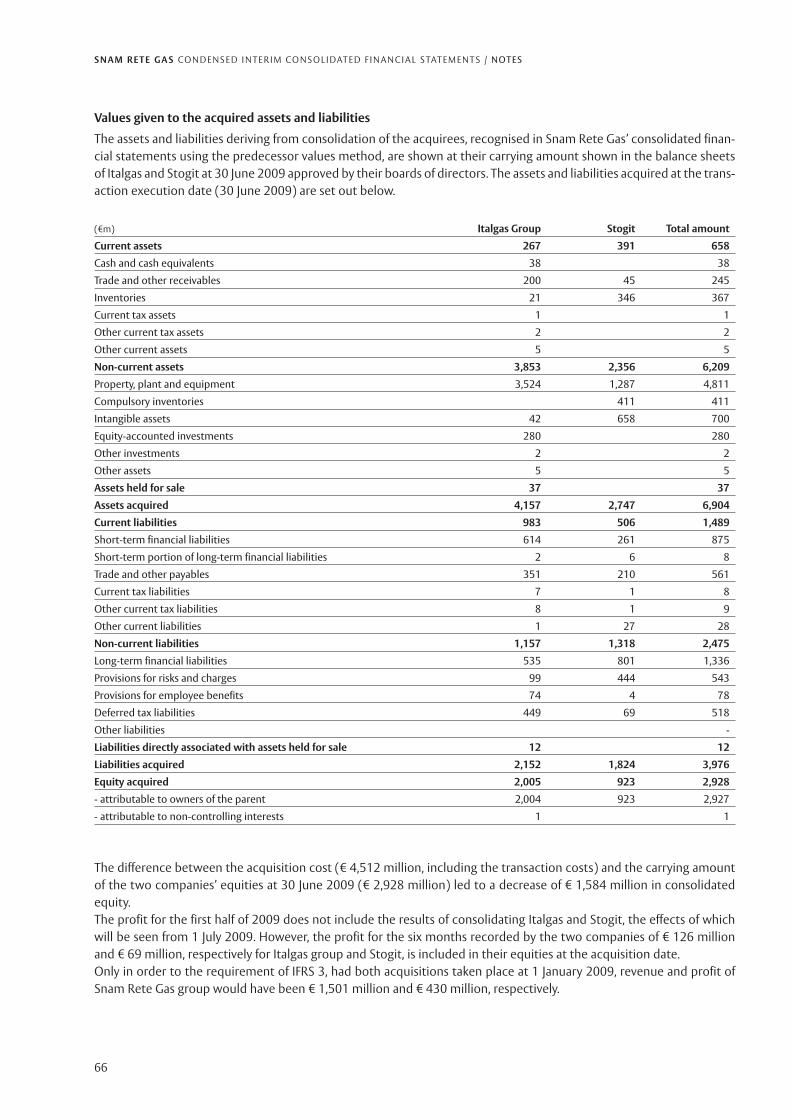

date of acquisition of title to the investments by Snam ReteGas S.p.A., ie 30 June 2009. Given the investment structure(Snam Rete Gas, Italgas and Stogit are under the commoncontrol of Eni S.p.A.), the transaction falls under the“Business combination of entities under common control” cat-egory, which is not covered by IFRS 3 “Business combinations”or other standards. The assets and liabilities deriving fromconsolidation of the acquirees, recognised in the consoli-dated financial statements of Snam Rete Gas using thepredecessor values method4, were recognised at the carry-ing amounts in the interim balance sheets at 30 June 2009approved by the acquirees’ directors. The acquisition ofItalgas and Stogit led to the consolidation of the followingassets and liabilities existing at the acquisition executiondate.

Number of ordinay shares offered 1,614,292,394

Exchange ratio no. 11 new shares for each 12 rights

Offering price per share (€) 2.15

Total amount of share capital increase (€) (*) 3,474,139,431

Number of shares composing Snam Rete Gas share capital 3,570,768,494

Snam Rete Gas share capital post offering 3,570,768,494(*) Includes collection of the options not exercised during the offering period and auctioned on the stock exchange.

Italgas and Stogit, respectively, is due to contractually pro-vided-for price adjustment mechanisms which consider,inter alia, the acquirees’ final net financial position, the2008 dividends distributed by Italgas and Stogit to EniS.p.A. and the financial expense accrued from the datewhen the transaction became effective for financial pur-poses (1 January 2009) to the date of its execution (30June 2009). The acquisitions were financed by means of ashare capital increase, issuing shares to be offered underoption to the Snam Rete Gas shareholders, of € 3,474 mil-lion, including the share premium2, and, for the remainder,by new loans disbursed by the ultimate parent Eni S.p.A..The share capital increase was approved by the board of

directors of Snam Rete Gas S.p.A. in its meeting of 23March 2009 when the board resolved to execute the proxy,given to it by the shareholders in their extraordinary meet-ing of 17 March 2009, to increase share capital in one ormore instalments for a maximum of € 3,500 million,including the premium, by issuing ordinary shares againstconsideration with a nominal amount of € 1 and regularrights to dividends to be offered to the Snam Rete Gasshareholders in proportion to their shares.In its meeting of 23 April 2009, the board of directorsapproved the final issue conditions for the share capitalincrease. The key figures for the offering of shares are setout below.

6

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / AC Q U I S I T I O N O F I TA LG A S A N D S TO G I T

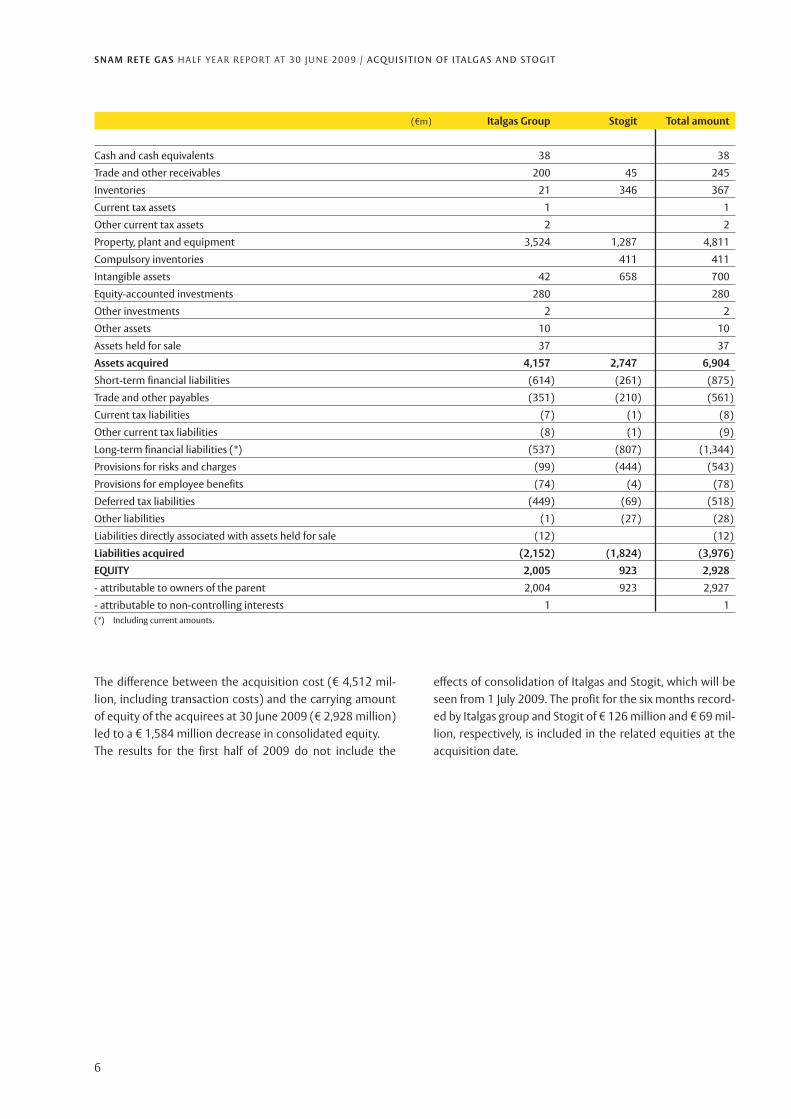

effects of consolidation of Italgas and Stogit, which will beseen from 1 July 2009. The profit for the six months record-ed by Italgas group and Stogit of € 126 million and € 69 mil-lion, respectively, is included in the related equities at theacquisition date.

The difference between the acquisition cost (€ 4,512 mil-lion, including transaction costs) and the carrying amountof equity of the acquirees at 30 June 2009 (€ 2,928 million)led to a € 1,584 million decrease in consolidated equity.The results for the first half of 2009 do not include the

(€m) Italgas Group Stogit Total amount

Cash and cash equivalents 38 38

Trade and other receivables 200 45 245

Inventories 21 346 367

Current tax assets 1 1

Other current tax assets 2 2

Property, plant and equipment 3,524 1,287 4,811

Compulsory inventories 411 411

Intangible assets 42 658 700

Equity-accounted investments 280 280

Other investments 2 2

Other assets 10 10

Assets held for sale 37 37

Assets acquired 4,157 2,747 6,904

Short-term financial liabilities (614) (261) (875)

Trade and other payables (351) (210) (561)

Current tax liabilities (7) (1) (8)

Other current tax liabilities (8) (1) (9)

Long-term financial liabilities (*) (537) (807) (1,344)

Provisions for risks and charges (99) (444) (543)

Provisions for employee benefits (74) (4) (78)

Deferred tax liabilities (449) (69) (518)

Other liabilities (1) (27) (28)

Liabilities directly associated with assets held for sale (12) (12)

Liabilities acquired (2,152) (1,824) (3,976)

EQUITY 2,005 923 2,928

- attributable to owners of the parent 2,004 923 2,927

- attributable to non-controlling interests 1 1(*) Including current amounts.

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / C O N S O L I DAT I O N P O L I C I E S A N D S C O P E

7

Consolidation policies and scope

Following acquisition of Italgas and Stogit, Snam Rete Gas isan integrated group heading in the regulated gas sector anda major gas operator in Europe in terms of its regulatoryasset base (RAB). The group operates in the natural gastransportation and dispatching sectors via the parent SnamRete Gas S.p.A., the liquefied natural gas (LNG) regasifica-

tion sector via the subsidiary GNL Italia S.p.A. and in the nat-ural gas distribution and storage sectors via Italgas andStogit S.p.A., respectively. The group also carries out otherless significant non-regulated activities, mainly consisting oftechnical and commercial services and the distribution ofwater.

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / C O N S O L I DAT I O N P O L I C I E S A N D S C O P E

8

Consolidation scope

The group’s consolidation scope at 30 June 2009 is shown in the following graph.

Distribution

Regasification Storage

SNAM RETE GAS S.p.A.

ITALGAS S.p.A.

100%

NAPOLETANA GAS S.p.A.

99.69%

GNL ITALIA S.p.A.

100%

STOGIT S.p.A.

100%

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / H I G H L I G H T S

9

Highlights

› Snam Rete Gas recorded a profit of € 234 million and EBITof € 444 million for the first half of 2009, down by € 25million (-9.7%) and € 56 million (-11.2%) on the sameperiod of 2008, respectively.

› The CEO intends to propose to the parent’s directors thatthe shareholders receive an interim dividend for 2009 of€ 0.06 per share (€ 0.09 per share in 2008) with an ex-dividend date of 19 October 2009 and payment from 22October 2009. This recommendation is subject to theapproval of the independent auditors as required byarticle 2433-bis of the Italian Civil Code.

› Investments of € 438 million (-8.2% on the first half of2008) were made in the period to develop and maintainthe natural gas transportation network. They specificallyrelated to the new transportation infrastructure along theAdriatic side (Puglia - Basilicata) and the upgrading of theimport infrastructure in Sicily, Calabria and the Po valley.

› Natural gas volumes injected into the transportationnetwork equalled 38.10 billion cubic metres, down 7.28billion cubic metres or 16% on the first half of 2008.Regasified LNG volumes were 0.64 billion cubic metres,

an 0.27 billion cubic metre decrease (-29.7%) on the sameperiod of 2008.

› Natural gas volumes carried on the Group’s distributionnetwork in the period came to 4,432 million cubic metres,compared to 4,376 million cubic metres in the first half of2008, an increase of 56 million cubic metres or 1.3%.

› During the first half of 2009, 10.35 billion cubic metres ofgas were moved in the Group’s storage system, up 3.24billion cubic metres (+45.6%) on the 2008 first half figureof 7.11 billion cubic metres.

› The Snam Rete Gas share closed the period at the officialprice of € 3.12. During the six months, the companyincreased its share capital involving the issue of1,614,292,394 new ordinary shares offered under optionto its shareholders in proportion to the shares alreadyheld by them. The share’s period-end official pricecompared to the adjusted price at the end of 2008, asrequired by the stock exchange regulations forextraordinary transactions, decreased by 4.3%, mainly dueto the entire European Utilities sector’s negativeperformance (Eurostoxx Utilities index -11.5%).

10

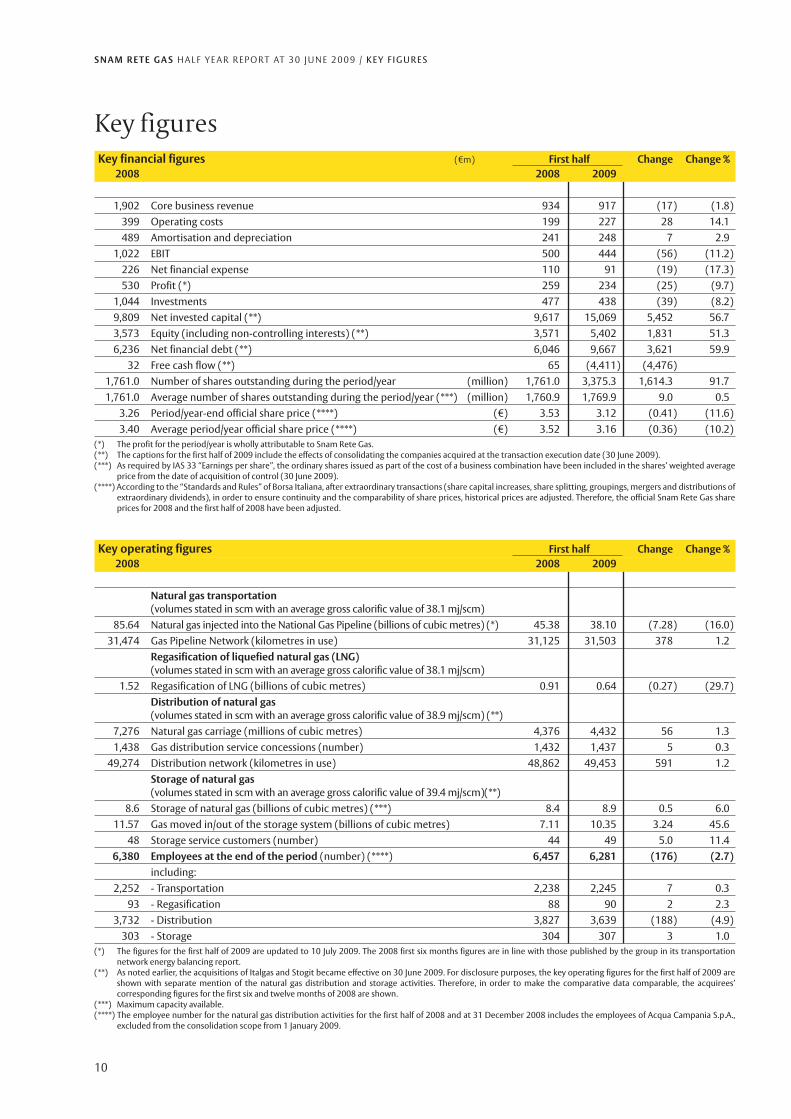

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / K E Y F I G U R E S

Key financial figures (€m) First half Change Change %2008 2008 2009

1,902 Core business revenue 934 917 (17) (1.8)399 Operating costs 199 227 28 14.1489 Amortisation and depreciation 241 248 7 2.9

1,022 EBIT 500 444 (56) (11.2)226 Net financial expense 110 91 (19) (17.3)530 Profit (*) 259 234 (25) (9.7)

1,044 Investments 477 438 (39) (8.2)9,809 Net invested capital (**) 9,617 15,069 5,452 56.73,573 Equity (including non-controlling interests) (**) 3,571 5,402 1,831 51.36,236 Net financial debt (**) 6,046 9,667 3,621 59.9

32 Free cash flow (**) 65 (4,411) (4,476)1,761.0 Number of shares outstanding during the period/year (million) 1,761.0 3,375.3 1,614.3 91.71,761.0 Average number of shares outstanding during the period/year (***) (million) 1,760.9 1,769.9 9.0 0.5

3.26 Period/year-end official share price (****) (€) 3.53 3.12 (0.41) (11.6)3.40 Average period/year official share price (****) (€) 3.52 3.16 (0.36) (10.2)

(*) The profit for the period/year is wholly attributable to Snam Rete Gas.(**) The captions for the first half of 2009 include the effects of consolidating the companies acquired at the transaction execution date (30 June 2009).(***) As required by IAS 33 “Earnings per share”, the ordinary shares issued as part of the cost of a business combination have been included in the shares’ weighted average

price from the date of acquisition of control (30 June 2009).(****) According to the “Standards and Rules” of Borsa Italiana, after extraordinary transactions (share capital increases, share splitting, groupings, mergers and distributions of

extraordinary dividends), in order to ensure continuity and the comparability of share prices, historical prices are adjusted. Therefore, the official Snam Rete Gas shareprices for 2008 and the first half of 2008 have been adjusted.

Key figures

Key operating figures First half Change Change %2008 2008 2009

Natural gas transportation(volumes stated in scm with an average gross calorific value of 38.1 mj/scm)

85.64 Natural gas injected into the National Gas Pipeline (billions of cubic metres) (*) 45.38 38.10 (7.28) (16.0)31,474 Gas Pipeline Network (kilometres in use) 31,125 31,503 378 1.2

Regasification of liquefied natural gas (LNG)(volumes stated in scm with an average gross calorific value of 38.1 mj/scm)

1.52 Regasification of LNG (billions of cubic metres) 0.91 0.64 (0.27) (29.7)Distribution of natural gas(volumes stated in scm with an average gross calorific value of 38.9 mj/scm) (**)

7,276 Natural gas carriage (millions of cubic metres) 4,376 4,432 56 1.31,438 Gas distribution service concessions (number) 1,432 1,437 5 0.3

49,274 Distribution network (kilometres in use) 48,862 49,453 591 1.2Storage of natural gas(volumes stated in scm with an average gross calorific value of 39.4 mj/scm)(**)

8.6 Storage of natural gas (billions of cubic metres) (***) 8.4 8.9 0.5 6.011.57 Gas moved in/out of the storage system (billions of cubic metres) 7.11 10.35 3.24 45.6

48 Storage service customers (number) 44 49 5.0 11.46,380 Employees at the end of the period (number) (****) 6,457 6,281 (176) (2.7)

including:2,252 - Transportation 2,238 2,245 7 0.3

93 - Regasification 88 90 2 2.33,732 - Distribution 3,827 3,639 (188) (4.9)

303 - Storage 304 307 3 1.0(*) The figures for the first half of 2009 are updated to 10 July 2009. The 2008 first six months figures are in line with those published by the group in its transportation

network energy balancing report.(**) As noted earlier, the acquisitions of Italgas and Stogit became effective on 30 June 2009. For disclosure purposes, the key operating figures for the first half of 2009 are

shown with separate mention of the natural gas distribution and storage activities. Therefore, in order to make the comparative data comparable, the acquirees’corresponding figures for the first six and twelve months of 2008 are shown.

(***) Maximum capacity available.(****) The employee number for the natural gas distribution activities for the first half of 2008 and at 31 December 2008 includes the employees of Acqua Campania S.p.A.,

excluded from the consolidation scope from 1 January 2009.

11

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / K E Y F I G U R E S

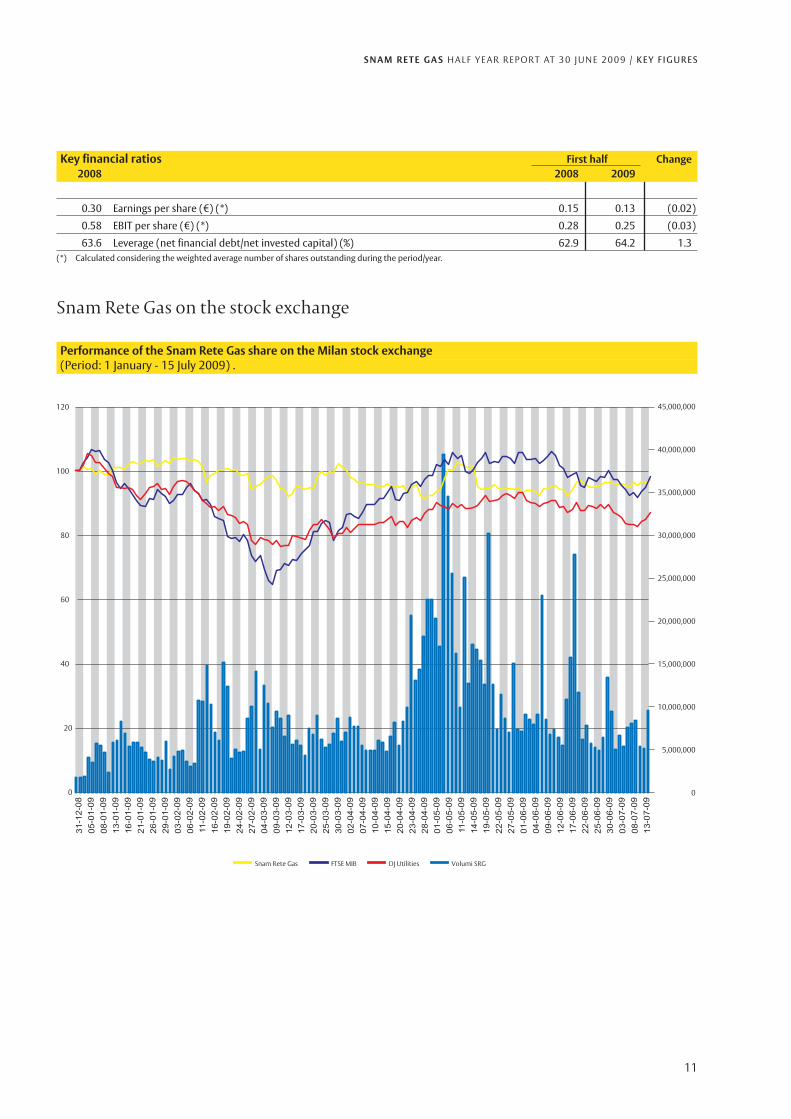

Key financial ratios First half Change2008 2008 2009

0.30 Earnings per share (€) (*) 0.15 0.13 (0.02)

0.58 EBIT per share (€) (*) 0.28 0.25 (0.03)

63.6 Leverage (net financial debt/net invested capital) (%) 62.9 64.2 1.3(*) Calculated considering the weighted average number of shares outstanding during the period/year.

80

100

120

60

40

20

0

Snam Rete Gas FTSE MIB DJ Utilities Volumi SRG

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

45,000,000

Performance of the Snam Rete Gas share on the Milan stock exchange(Period: 1 January - 15 July 2009) .

Snam Rete Gas on the stock exchange

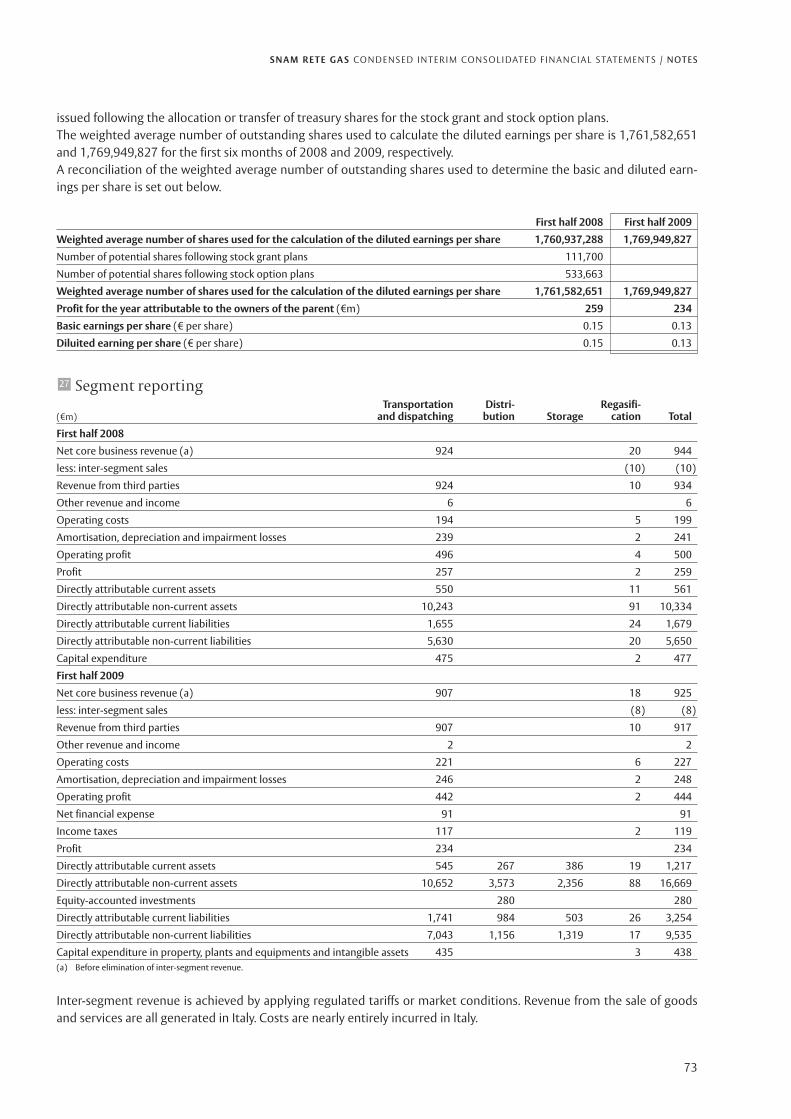

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / O P E R AT I N G R E V I E W

12

Operating review

Introduction

The key performance indicators are shown below by busi-ness segment5. The main income statement captions arenot given for the natural gas distribution and storage activ-

ities as the effects of the consolidation of Italgas and Stogitwill be seen from 1 July 2009, as disclosed in the section ontheir acquisition. Their performance in the entire sixmonths is described in the section on the “Performance ofthe acquirees” in order to properly assess their operations.

(5) The business segments (natural gas transportation, LNG regasification, natural gas distribution and storage) are identified, in line with internal reports, by man-agement, and mainly refer to the activities of Snam Rete Gas, GNL Italia, Italgas and its subsidiaries and Stogit, respectively.

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / O P E R AT I N G R E V I E W

13

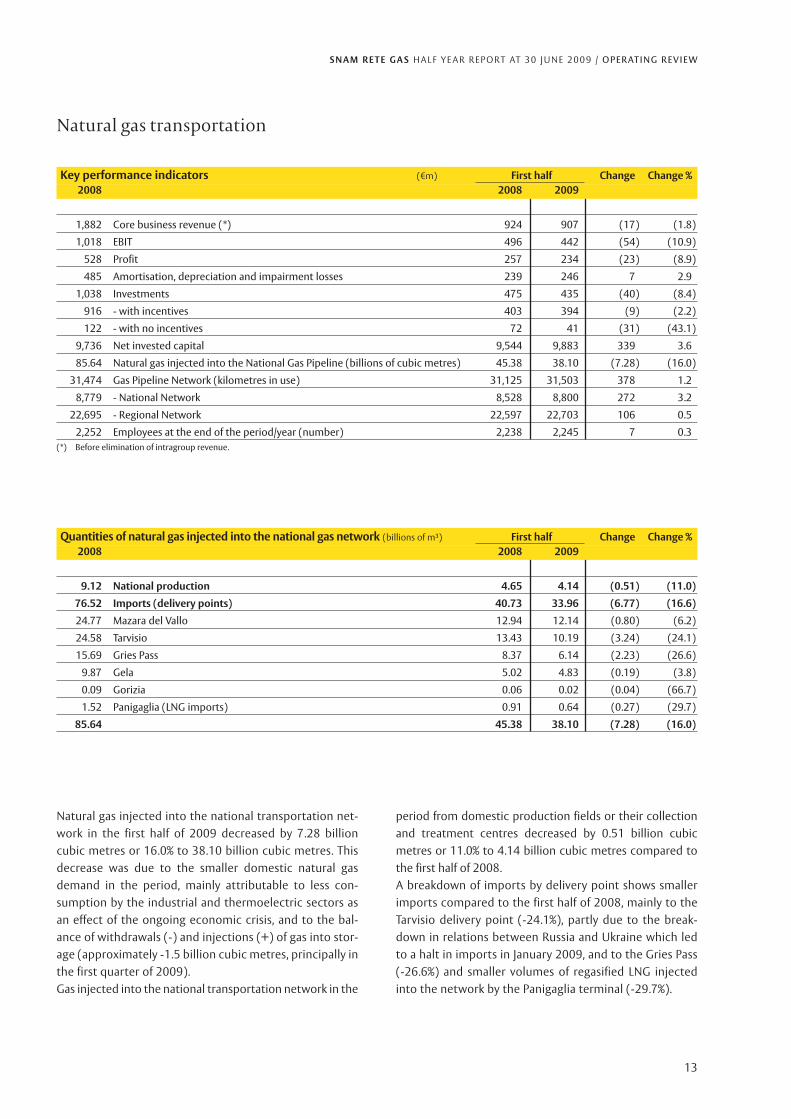

Natural gas transportation

Quantities of natural gas injected into the national gas network (billions of m³) First half Change Change %2008 2008 2009

9.12 National production 4.65 4.14 (0.51) (11.0)

76.52 Imports (delivery points) 40.73 33.96 (6.77) (16.6)

24.77 Mazara del Vallo 12.94 12.14 (0.80) (6.2)

24.58 Tarvisio 13.43 10.19 (3.24) (24.1)

15.69 Gries Pass 8.37 6.14 (2.23) (26.6)

9.87 Gela 5.02 4.83 (0.19) (3.8)

0.09 Gorizia 0.06 0.02 (0.04) (66.7)

1.52 Panigaglia (LNG imports) 0.91 0.64 (0.27) (29.7)

85.64 45.38 38.10 (7.28) (16.0)

Key performance indicators (€m) First half Change Change %2008 2008 2009

1,882 Core business revenue (*) 924 907 (17) (1.8)

1,018 EBIT 496 442 (54) (10.9)

528 Profit 257 234 (23) (8.9)

485 Amortisation, depreciation and impairment losses 239 246 7 2.9

1,038 Investments 475 435 (40) (8.4)

916 - with incentives 403 394 (9) (2.2)

122 - with no incentives 72 41 (31) (43.1)

9,736 Net invested capital 9,544 9,883 339 3.6

85.64 Natural gas injected into the National Gas Pipeline (billions of cubic metres) 45.38 38.10 (7.28) (16.0)

31,474 Gas Pipeline Network (kilometres in use) 31,125 31,503 378 1.2

8,779 - National Network 8,528 8,800 272 3.2

22,695 - Regional Network 22,597 22,703 106 0.5

2,252 Employees at the end of the period/year (number) 2,238 2,245 7 0.3(*) Before elimination of intragroup revenue.

Natural gas injected into the national transportation net-work in the first half of 2009 decreased by 7.28 billioncubic metres or 16.0% to 38.10 billion cubic metres. Thisdecrease was due to the smaller domestic natural gasdemand in the period, mainly attributable to less con-sumption by the industrial and thermoelectric sectors asan effect of the ongoing economic crisis, and to the bal-ance of withdrawals (-) and injections (+) of gas into stor-age (approximately -1.5 billion cubic metres, principally inthe first quarter of 2009).Gas injected into the national transportation network in the

period from domestic production fields or their collectionand treatment centres decreased by 0.51 billion cubicmetres or 11.0% to 4.14 billion cubic metres compared tothe first half of 2008.A breakdown of imports by delivery point shows smallerimports compared to the first half of 2008, mainly to theTarvisio delivery point (-24.1%), partly due to the break-down in relations between Russia and Ukraine which ledto a halt in imports in January 2009, and to the Gries Pass(-26.6%) and smaller volumes of regasified LNG injectedinto the network by the Panigaglia terminal (-29.7%).

14

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / O P E R AT I N G R E V I E W

Investments (€m) First half Change Change %2008 2008 2009

813 Development 359 351 (8) (2.2)

578 Investments with 3% incentive 232 243 11 4.7

235 Investments with 2% incentive 127 108 (19) (15.0)

225 Maintenance and other 116 84 (32) (27.6)

103 Investments with 1% incentive 44 43 (1) (2.3)

122 Investments with no incentives 72 41 (31) (43.1)

1,038 475 435 (40) (8.4)

Volumes injected by shipper (billions of m³) First half Change Change %2008 2008 2009

51.80 Eni 27.23 20.04 (7.19) (26.4)

9.82 Enel Trade 5.05 4.18 (0.87) (17.2)

24.02 Others 13.10 13.88 0.78 6.0

85.64 45.38 38.10 (7.28) (16.0)

Investments made in the first half of 2009 of € 435 millionshow an 8.4% decrease on the same period of 2008.In order to provide a consistent comparison of the differenttypes of investment made in the first halves of 2009 and2008, the investments of the first half of 2009 have beenclassified in accordance with resolution no. 166/05 issued bythe Electricity and Gas Authority. The Authority identifiedseparate project categories which have different incentives.Investments made in the first half of 2009 will be remuner-ated applying the Authority’s standards for the third regula-tory period, which may differ from those of the current reg-ulatory period, which expires on 30 September 2009.

The key development investments related to:- as part of the project for the new transportation infra-

structure along the Adriatic side (€ 140 million), the pur-chase of materials to construct the Massafra-Biccaripipeline in Puglia and Basilicata;

- as part of the project to upgrade the import infrastruc-ture in Sicily and Calabria (€ 54 million): (i) constructionof the Montalbano-Messina pipeline and the Bronte-Montalbano section of the Enna-Montalbano pipeline inSicily and the Rende-Tarsia pipeline in Calabria; and (ii)

work to complete the Mazara-Menfi and Tarsia-Moranopipelines in Sicily and Calabria, respectively;

- as part of the project to improve the import infrastruc-ture from the North East (€ 19 million): (i) assembly of anew turbocompressor to upgrade the Malborghetto sta-tion in Friuli Venezia Giulia; and (ii) construction of theTarvisio-Malborghetto pipeline and assembly of the gascooler at the Istrana station;

- as part of the project to upgrade the transportation infra-structure in the Po valley (€ 27 million): (i) acquisition ofmaterials and labour to construct the Poggio Renatico-Cremona pipeline in Emilia Romagna and Lombardy; and(ii) delivery of spare parts and work to complete thePoggio Renatico station in Emilia Romagna;

- upgrading of the pipeline network in South Piedmont (€12 million), including construction of the Cherasco-Cuneo and Oviglio-Ponti pipelines.

The maintenance and other investments covered a num-ber of works aimed at ensuring adequate safety and qualitylevels of the systems, the replacement of assets and plants,the introduction of new IT systems, the development ofexisting ones and the purchase of other operating assets.

15

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / O P E R AT I N G R E V I E W

The Panigaglia (SP) LNG terminal regasified 0.64 billion cubicmetres of natural gas in the first half of 2009 compared to 0.91billion cubic metres in the same period of 2008. Different sized

methane tankers unloaded 20 loads (including two spot loads)compared to 26 in the first quarter of 2008. The decrease inregasified LNG of 0.27 billion cubic metres equals 29.7%.

LNG regasification

Quantities of regasified gas (billions of m³) First half Change Change %2008 2008 2009

1.23 Enel Trade 0.64 0.50 (0.14) (21.9)

0.29 Eni 0.27 0.08 (0.19) (70.4)

Others 0.06 0.06

1.52 0.91 0.64 (0.27) (29.7)

Key performance indicators (€m) First half Change Change %2008 2008 2009

37 Core business revenue (*) 20 18 (2) (10.0)

4 EBIT 4 2 (2) (50.0)

2 Profit 2 (2) (100.0)

4 Amortisation, depreciation and impairment losses 2 2

6 Investments 2 3 1 50.0

73 Net invested capital 73 77 4 5.5

1.52 Regasification of LNG (billions of cubic metres) 0.91 0.64 (0.27) (29.7)

42 Tankers of unloaded gas (number) 26 20 (6) (23.1)

93 Employees at the end of the period/year (number) 88 90 2 2.3(*) Core business revenue includes the recharging of the costs of transporting gas by Snam Rete Gas S.p.A. from the regasification facility to the entry point in the Panigaglia

network to customers. For consolidation purposes, this revenue is eliminated together with the transportation costs incurred by GNL Italia S.p.A. to present thetransaction’s substance.

Natural gas distribution

Key performance indicators6 First half Change Change %2008 2008 2009

3,237 Net invested capital (€m) 2,996 3,118 122 4.1

7,276 Natural gas carriage (millions of cubic metres) 4,376 4,432 56 1.3

1,438 Gas distribution service concessions (number) 1,432 1,437 5 0.3

49,274 Distribution Network (kilometres in use) 48,862 49,453 591 1.2

5,676,105 Meters in use (number) 5,635,039 5,718,660 83,621 1.5

132 Customers (number) 129 146 17 13.2

3,732 Employees at the end of the period/year (number) 3,827 3,639 (188) (4.9)

(6) The acquisition of Italgas became effective on 30 June 2009. In order to facilitate a comparison between the key performance indicators of the periods shown,the data for the corresponding first six and twelve months of 2008 are shown.

Quantities of natural gas moved in/out of the storagesystemGas moved in/out of the storage system in the six monthsamounted to 10.35 billion cubic metres, a 3.24 billioncubic metres, or 45.6%, increase compared to the sameperiod of 2008.This increase is due to:- the extraordinary supply crisis in January 2009 due to the

Russia-Ukraine situation, during which (6-20 January) 2.2billion standard cubic metres were supplied;

16

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / O P E R AT I N G R E V I E W

Gas carriageDuring the first half of 2009, 4,432 million cubic metres ofgas were carried, up 56 million cubic metres or 1.3% on thesame period of 2008, mainly due to the different weatherconditions. At period end, the group has concessions forgas distribution services in 1,437 municipalities (31December 2008: 1,438) with 5,718,660 active meters at gasredelivery points to end users (households, businesses,etc.) compared to 5,676,105 at the end of 2008.

Distribution networkThe group’s gas distribution network at period end spans49,453 km and is split into pipes, depending on the pres-sure category:- main feed pipes (greater than 12 bar);- medium pressure pipes (up to 5 bar);- low pressure pipes (up to 0.04 bar).The 179 km increase on 31 December 2008 is due to thebalance of increases and decreases in the network. The

increases are due to:- acquisition of the tendered gas distribution concession

in the Cerro Maggiore municipality;- acquisition of the business unit which distributes gas in

the Settimo Torinese and Brandizzo municipalities;- construction of new networks;- extension of networks to meet commitments deriving

from concession contracts;- service access requests from end users (households,

businesses, etc.).The decreases are mainly attributable to the sale of gas net-works in the Bussolengo, Liscate, Castiglione delle Stiviereand Capriolo municipalities to other operators followingdiscontinuation of distribution services.

CustomersAt 30 June 2009, the group transports the gas of 146 retailcompanies in its networks compared to 132 companies at31 December 2008.

- significant gas withdrawals for the residential sector dueto the harsh winter;

- the related greater injections to restore the volumeswithdrawn and gradually fill up the additional capacitymade available for the thermal year 2009-2010.

CustomersAt period end, the group provides gas storage and modula-tion services to 49 companies (31 December 2008: 48),including 47 non-Eni group companies.

Storage of natural gas

Key performance indicators7 First half Change Change %2008 2008 2009

1,874 Net invested capital (€m) 1,784 1,991 207 11.6

10 Gas storage service concessions (number) 10 10

11.57 Gas moved in/out of the storage system (billions of cubic metres) 7.11 10.35 3.24 45.6

6.30 - for injection 3.39 4.30 0.91 26.8

5.27 - for withdrawal 3.72 6.05 2.33 62.6

8.6 Storage of natural gas (billions of cubic metres) (*) 8.4 8.9 0.5 6.0

3.4 - for Eni 3.2 3.2

5.2 - for other operators 5.2 5.7 0.5 9.6

48 Customers (number) 44 49 5 11.4

303 Employees at the end of the period/year (number) 304 307 3 1.0(*) Maximum capacity available.

(7) The acquisition of Stogit became effective on 30 June 2009. In order to facilitate a comparison between the key performance indicators of the periods, the datafor the corresponding first six and twelve months of 2008 are shown.

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / F I N A N C I A L R E V I E W

17

Financial review

RECLASSIFIED CONSOLIDATED INCOME STATEMENT

(€m) First half Change Change %2008 2008 2009

1,902 Core business revenue 934 917 (17) (1.8)

8 Other revenue and income 6 2 (4) (66.7)

1,910 Total revenue 940 919 (21) (2.2)

(399) Operating costs (*) (199) (227) (28) 14.1

1,511 EBITDA 741 692 (49) (6.6)

(489) Amortisation, depreciation and impairment losses (241) (248) (7) 2.9

1,022 EBIT 500 444 (56) (11.2)

(226) Net financial expense (110) (91) 19 (17.3)

796 Profit before tax 390 353 (37) (9.5)

(266) Income taxes (131) (119) 12 (9.2)

530 Profit (**) 259 234 (25) (9.7)(*) Operating costs include the captions “Purchases, services and other costs” and “Personnel expense” of the consolidated income statement included in the condensed

interim consolidated financial statements.(**) The profit for the period is wholly attributable to Snam Rete Gas.

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / F I N A N C I A L R E V I E W

18

The profit (€ 234 million) decreased by € 25 million(9.7%) compared to the same period of 2008, due to thedecrease in EBIT (-€ 54 million) recorded by the trans-portation business, partly offset by the smaller net finan-cial expense (+€ 19 million), thanks to the cutting of mar-ket interest rates, and the downturn in income taxes (+€

12 million), related to the smaller profit before tax.

Non-recurring significant events and transactions andother special itemsNo non-recurring significant transactions and other specialitems took place in either the first half of 2009 or 2008.

Core business revenue (€ 917 million) decreased by € 17million (1.8%), mainly due to the smaller volumes of gastransported (-7.28 billion cubic metres; -16%) following thedownturn in gas demand in the first six months of the year.Revenue from the natural gas transportation business (€907 million) decreased by € 17 million due to the smaller

volumes of gas transported (-€ 47 million) and revision ofthe transportation tariffs (-€ 11 million), the effects ofwhich were partly offset by the investments made in 2007(+€ 38 million).Transportation revenue (€ 900 million) by shipper isanalysed in the following table.

Regasification revenue (€ 18 million) comprises the fee forthe LNG regasification service carried out at the Panigaglia(SP) terminal (€ 10 million) and charges for the transporta-tion capacity and the variable fee that the companyacquires from Snam Rete Gas and subsequently charges to

the regasification service users (€ 8 million). The € 2 milliondecrease on the first half of 2008 is due to the lower chargesfor the transportation service acquired from Snam Rete Gasand subsequently recharged to the regasification serviceusers.

(€m) First half Change Change %2008 2008 2009

1,882 Transportation 924 907 (17) (1.8)

37 Regasification 20 18 (2) (10.0)

(17) Consolidation adjustments (10) (8) 2 (20.0)

1,902 934 917 (17) (1.8)

(€m) First half Change Change %2008 2008 2009

1,081 Eni 553 489 (64) (11.6)

254 Enel Trade 129 121 (8) (6.2)

603 Other 305 348 43 14.1

(74) Revenue and fine adjustment (47) (34) 13 (27.7)

(34) Interruptibility fee as per resolution no. 277/07 (18) (19) (1) 5.6

(8) Regional network transportation fee as per resolution no. 45/07 - Equalisation (4) (5) (1) 25.0

45 Additional fee to cover the greater cost of purchasing gas

1,867 918 900 (18) (2.0)

Core business revenue

Core business revenue by business segment is analysed below.

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / F I N A N C I A L R E V I E W

19

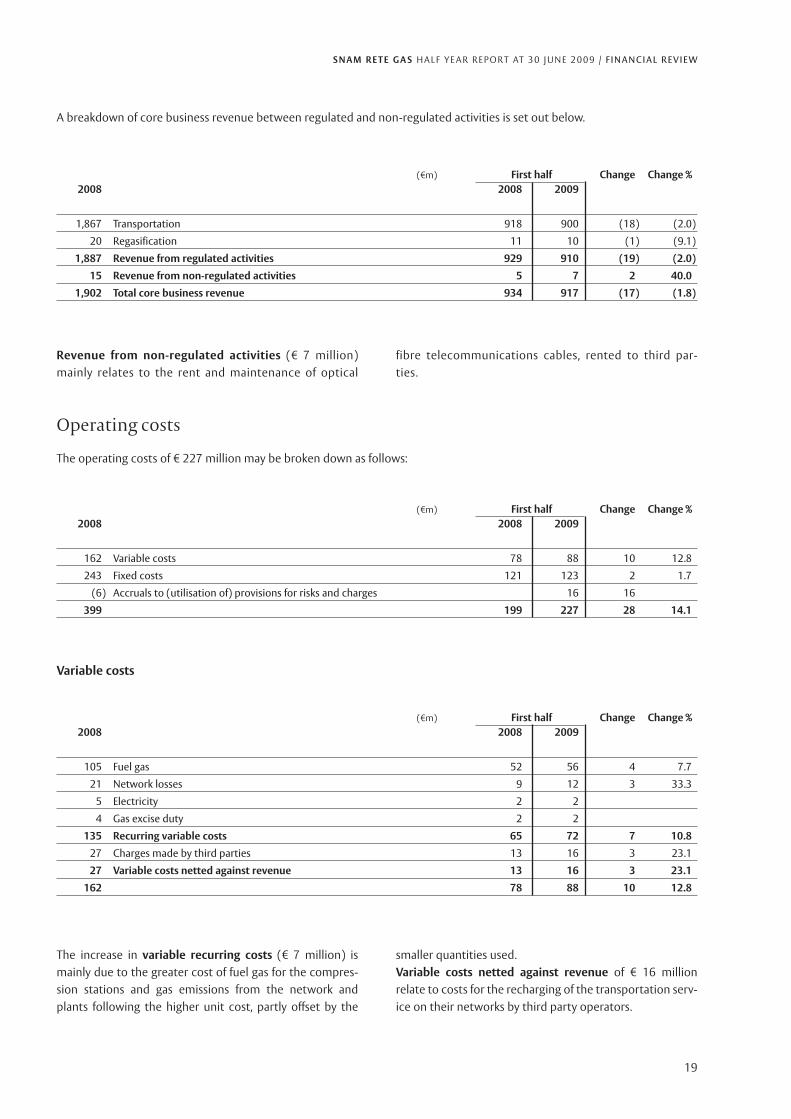

A breakdown of core business revenue between regulated and non-regulated activities is set out below.

Revenue from non-regulated activities (€ 7 million)mainly relates to the rent and maintenance of optical

The operating costs of € 227 million may be broken down as follows:

fibre telecommunications cables, rented to third par-ties.

Operating costs

Variable costs

(€m) First half Change Change %2008 2008 2009

1,867 Transportation 918 900 (18) (2.0)

20 Regasification 11 10 (1) (9.1)

1,887 Revenue from regulated activities 929 910 (19) (2.0)

15 Revenue from non-regulated activities 5 7 2 40.0

1,902 Total core business revenue 934 917 (17) (1.8)

(€m) First half Change Change %2008 2008 2009

162 Variable costs 78 88 10 12.8

243 Fixed costs 121 123 2 1.7

(6) Accruals to (utilisation of) provisions for risks and charges 16 16

399 199 227 28 14.1

(€m) First half Change Change %2008 2008 2009

105 Fuel gas 52 56 4 7.7

21 Network losses 9 12 3 33.3

5 Electricity 2 2

4 Gas excise duty 2 2

135 Recurring variable costs 65 72 7 10.8

27 Charges made by third parties 13 16 3 23.1

27 Variable costs netted against revenue 13 16 3 23.1

162 78 88 10 12.8

The increase in variable recurring costs (€ 7 million) ismainly due to the greater cost of fuel gas for the compres-sion stations and gas emissions from the network andplants following the higher unit cost, partly offset by the

smaller quantities used.Variable costs netted against revenue of € 16 millionrelate to costs for the recharging of the transportation serv-ice on their networks by third party operators.

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / F I N A N C I A L R E V I E W

20

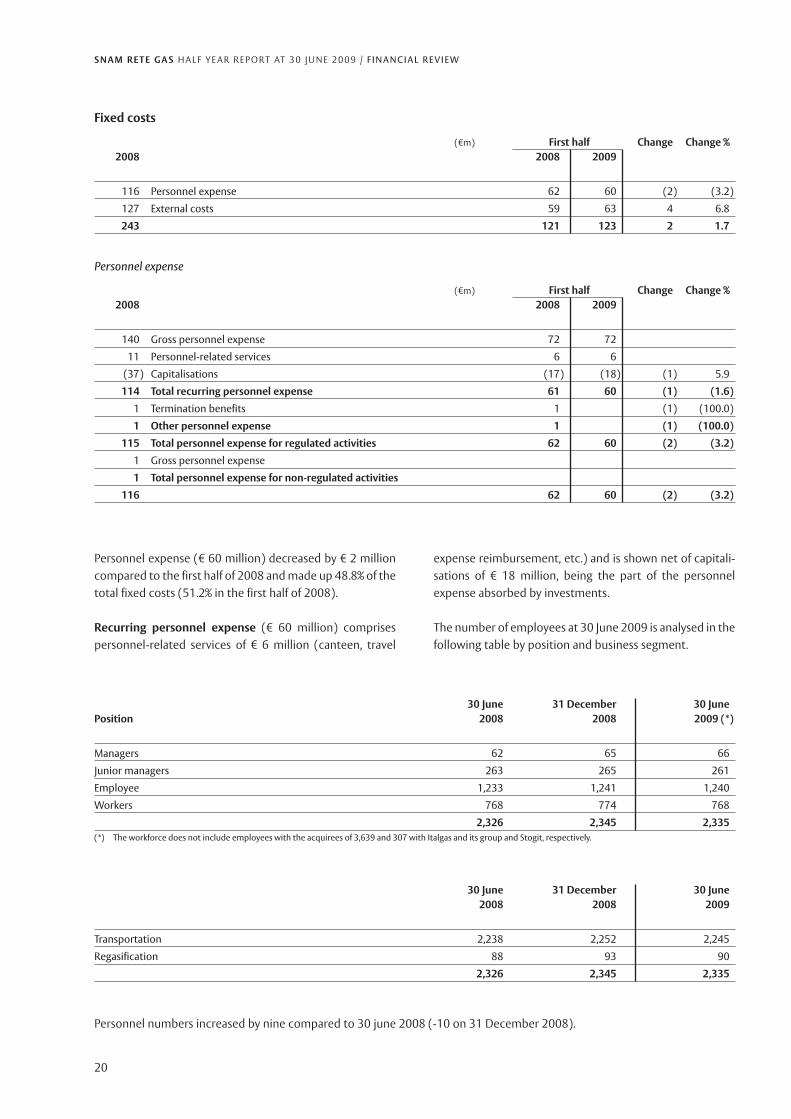

Personnel expense (€ 60 million) decreased by € 2 millioncompared to the first half of 2008 and made up 48.8% of thetotal fixed costs (51.2% in the first half of 2008).

Recurring personnel expense (€ 60 million) comprisespersonnel-related services of € 6 million (canteen, travel

expense reimbursement, etc.) and is shown net of capitali-sations of € 18 million, being the part of the personnelexpense absorbed by investments.

The number of employees at 30 June 2009 is analysed in thefollowing table by position and business segment.

Personnel expense

Fixed costs

(€m) First half Change Change %2008 2008 2009

116 Personnel expense 62 60 (2) (3.2)

127 External costs 59 63 4 6.8

243 121 123 2 1.7

(€m) First half Change Change %2008 2008 2009

140 Gross personnel expense 72 72

11 Personnel-related services 6 6

(37) Capitalisations (17) (18) (1) 5.9

114 Total recurring personnel expense 61 60 (1) (1.6)

1 Termination benefits 1 (1) (100.0)

1 Other personnel expense 1 (1) (100.0)

115 Total personnel expense for regulated activities 62 60 (2) (3.2)

1 Gross personnel expense

1 Total personnel expense for non-regulated activities

116 62 60 (2) (3.2)

30 June 31 December 30 JunePosition 2008 2008 2009 (*)

Managers 62 65 66

Junior managers 263 265 261

Employee 1,233 1,241 1,240

Workers 768 774 768

2,326 2,345 2,335(*) The workforce does not include employees with the acquirees of 3,639 and 307 with Italgas and its group and Stogit, respectively.

30 June 31 December 30 June2008 2008 2009

Transportation 2,238 2,252 2,245

Regasification 88 93 90

2,326 2,345 2,335

Personnel numbers increased by nine compared to 30 june 2008 (-10 on 31 December 2008).

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / F I N A N C I A L R E V I E W

21

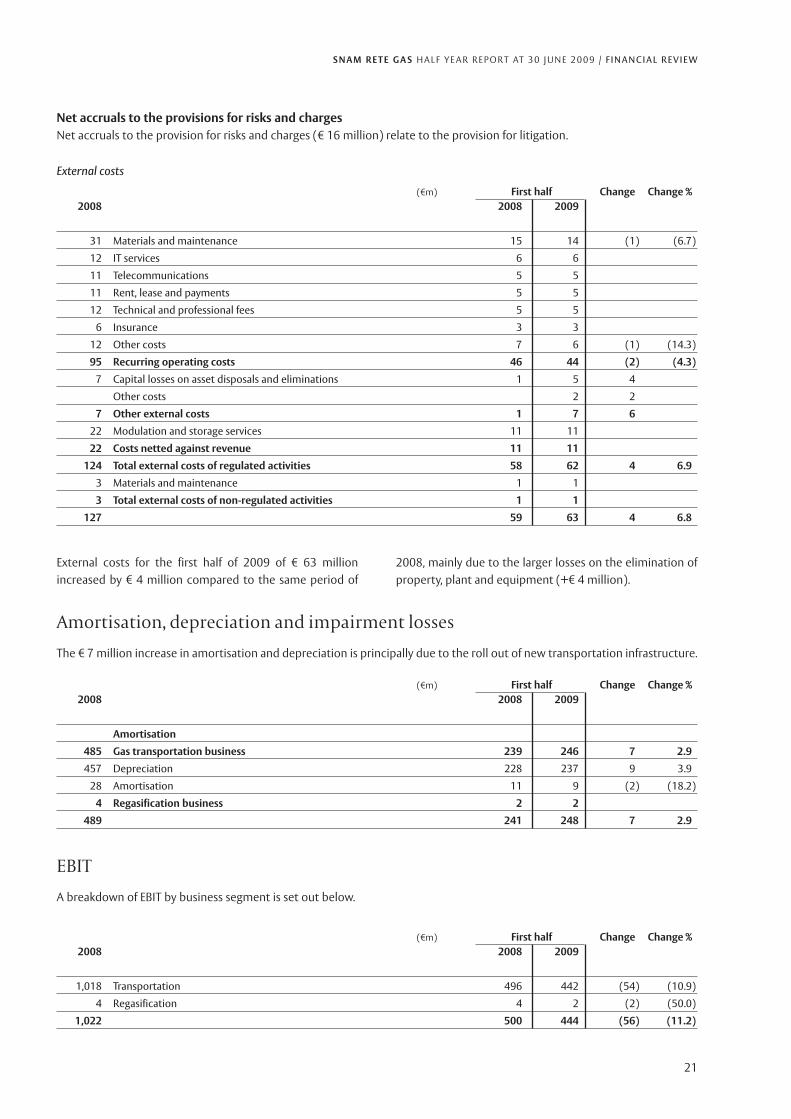

External costs for the first half of 2009 of € 63 millionincreased by € 4 million compared to the same period of

Amortisation, depreciation and impairment losses

The € 7 million increase in amortisation and depreciation is principally due to the roll out of new transportation infrastructure.

External costs

(€m) First half Change Change %2008 2008 2009

31 Materials and maintenance 15 14 (1) (6.7)

12 IT services 6 6

11 Telecommunications 5 5

11 Rent, lease and payments 5 5

12 Technical and professional fees 5 5

6 Insurance 3 3

12 Other costs 7 6 (1) (14.3)

95 Recurring operating costs 46 44 (2) (4.3)

7 Capital losses on asset disposals and eliminations 1 5 4

Other costs 2 2

7 Other external costs 1 7 6

22 Modulation and storage services 11 11

22 Costs netted against revenue 11 11

124 Total external costs of regulated activities 58 62 4 6.9

3 Materials and maintenance 1 1

3 Total external costs of non-regulated activities 1 1

127 59 63 4 6.8

(€m) First half Change Change %2008 2008 2009

Amortisation

485 Gas transportation business 239 246 7 2.9

457 Depreciation 228 237 9 3.9

28 Amortisation 11 9 (2) (18.2)

4 Regasification business 2 2

489 241 248 7 2.9

EBIT

A breakdown of EBIT by business segment is set out below.

(€m) First half Change Change %2008 2008 2009

1,018 Transportation 496 442 (54) (10.9)

4 Regasification 4 2 (2) (50.0)

1,022 500 444 (56) (11.2)

Net accruals to the provisions for risks and chargesNet accruals to the provision for risks and charges (€ 16 million) relate to the provision for litigation.

2008, mainly due to the larger losses on the elimination ofproperty, plant and equipment (+€ 4 million).

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / F I N A N C I A L R E V I E W

EBIT8 recorded for the first half of 2009 amounts to € 444million, down € 56 million or 11.2%, on the correspondingperiod of 2008, mainly due to: (i) smaller transportationactivities (-€ 54 million) attributable to lower transporta-tion revenue (-€ 20 million, net of revenue offset againstcosts) principally due to the decreased volumes of naturalgas transported; (ii) higher operating costs (-€ 25 million,net of costs offset against revenue), principally due to thesmaller accruals to the provisions for risks and charges (-€

16 million) and the rise in variable costs for the purchase offuel gas used by the compression stations and network andsystem losses (-€ 7 million); and (iii) greater amortisationand depreciation expense (-€ 7 million) following the roll-out of new transportation infrastructure during the period.

EBIT of the regasification business (€ 2 million) decreasedby € 2 million following the smaller income from the sale ofgas and smaller LNG regasification revenue.

22

(8) EBIT is analysed by considering only those elements that have led to a change therein, as application of the gas sector tariff regulations generate costs and rev-enue which are netted.

Net financial expense

(€m) First half Change Change %2008 2008 2009

(276) Interest expense on net financial debt (134) (76) 58 (43.3)

(276) - Interest expense on short-term and long-term financial liabilities (134) (76) 58 (43.3)

27 Gains (losses) on derivatives 12 (21) (33)

(2) - Adjustment to fair value (1) (2) (1) 100.0

29 - Interest accrued during the year 13 (19) (32)

(3) Other financial income (expense) (1) (2) (1) 100.0

2 - Other income 1 1

(1) - Discounting interest

(4) - Other financial expense (2) (3) (1) 50.0

26 Financial expense on internal work capitalised 13 8 (5) (38.5)

(226) (110) (91) 19 (17.3)

Net financial expense (€ 91 million) decreased by € 19 mil-lion, mainly due to the market interest rate cuts. The average

cost of borrowing decreased from 4.2% in the first half of2008 to 3.2% following the sharp cut in market interest rates.

Income taxes(€m) First half Change Change %

2008 2008 2009

291 Current taxes 145 137 (8) (5.5)

Deferred tax (income) expense

(37) Deferred tax expense (19) (16) 3 (15.8)

12 Deferred tax income 5 (2) (7)

(25) (14) (18) (4) 28.6

266 131 119 (12) (9.2)

Income taxes (€ 119 million) decreased by € 12 millioncompared to the corresponding period of 2008, mainly dueto the smaller profit before tax.

The tax rate is 33.7% compared to 33.6% in the same periodof 2008.

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / F I N A N C I A L R E V I E W

RECLASSIFIED CONSOLIDATED BALANCE SHEET (*)

23

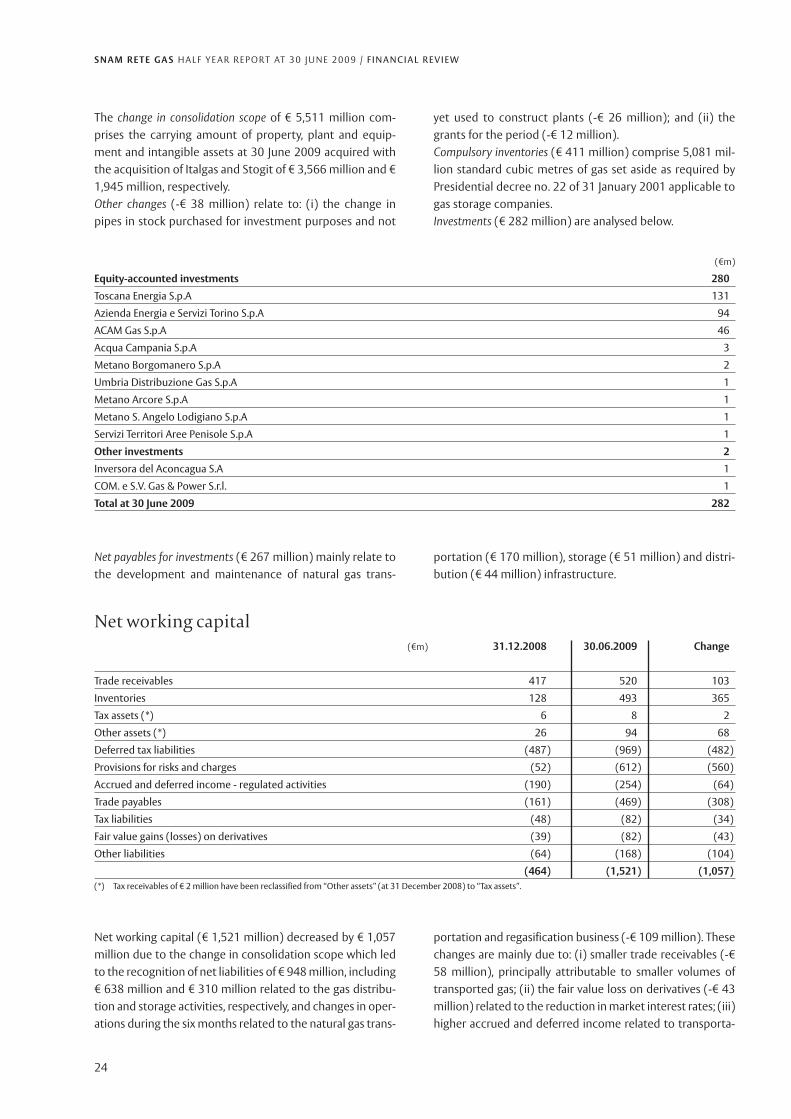

Net invested capital (€ 15,069 million) increased by €5,260 million compared to 31 December 2008 due to therise in non-current assets (+€ 6,371 million), partly offset bythe reduction in net working capital (-€ 1,057 million).Non-current assets (€ 16,673 million) increased by € 6,371million, mainly due to the change in consolidation scope(+€ 6,110 million).Assets held for sale and the directly related liabilities of €25 million relate to: (i) a property owned by Italgas (€ 17

million, net of the environmental provisions for the proper-ty’s restoration)9; and (ii) sale of an investment (17.77%)held by Italgas S.p.A. in the gas distribution companyToscana Energia Clienti S.p.A. to Eni S.p.A. (€ 8 million). Thistransaction is part of the ongoing restructuring plan, toconcentrate the gas distribution activities in Italgas.

Changes in property, plant and equipment and intangibleassets (+€ 5,658 million) are analysed below:

(€m) 31.12.2008 30.06.2009 Change

Property, plant and equipment 10,549 15,508 4,959

Compulsory inventories 411 411

Intangible assets 39 738 699

Investments 282 282

Financial receivables held for operating activities 1 1

Net payables for investments (286) (267) 19

Non-current assets 10,302 16,673 6,371

Net working capital (464) (1,521) (1,057)

Provision for employee benefits (29) (108) (79)

Assets held for sale and directly related liabilities 25 25

NET INVESTED CAPITAL 9,809 15,069 5,260

Equity (including non-controlling interests) 3,573 5,402 1,829

Net financial debt 6,236 9,667 3,431

COVERAGE 9,809 15,069 5,260(*) Reference should be made to the paragraph on the reconciliation of the reclassified consolidated balance sheet with the legally-required consolidated balance sheet.

Reclassified consolidated balance sheet

The reclassified consolidated balance sheet combines theassets and liabilities of the balance sheet format included inthe annual consolidated financial statements and con-densed interim financial statements in accordance withtheir function, split into the three basic functions: invest-ment, operations and financing.

Group management holds that this format presents addi-tional information useful for investors as it allows identifica-tion of the sources of financing (own and third party funds)and the application of such funds for non-current assetsand working capital.

The reclassified balance sheet format is used by manage-ment to calculate the key leverage ratios.

(€m) Property, plant Intangible Totaland equipment assets

Opening balance at 31 December 2008 10,549 39 10,588

Investments 430 8 438

Effect of changes in consolidation scope 4,811 700 5,511

Amortisation, depreciation and impairment losses (239) (9) (248)

Sales, eliminations and disposals (5) (5)

Other changes (38) (38)

Closing balance at 30 June 2009 15,508 738 16,246

(9) Note 21 “Guarantees, commitments and risks – commitments deriving from the acquisition of Italgas and Stogit from Eni” sets out the commitments taken on by the parties.

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / F I N A N C I A L R E V I E W

The change in consolidation scope of € 5,511 million com-prises the carrying amount of property, plant and equip-ment and intangible assets at 30 June 2009 acquired withthe acquisition of Italgas and Stogit of € 3,566 million and €1,945 million, respectively.Other changes (-€ 38 million) relate to: (i) the change inpipes in stock purchased for investment purposes and not

yet used to construct plants (-€ 26 million); and (ii) thegrants for the period (-€ 12 million).Compulsory inventories (€ 411 million) comprise 5,081 mil-lion standard cubic metres of gas set aside as required byPresidential decree no. 22 of 31 January 2001 applicable togas storage companies.Investments (€ 282 million) are analysed below.

24

Net payables for investments (€ 267 million) mainly relate tothe development and maintenance of natural gas trans-

portation (€ 170 million), storage (€ 51 million) and distri-bution (€ 44 million) infrastructure.

Net working capital(€m) 31.12.2008 30.06.2009 Change

Trade receivables 417 520 103

Inventories 128 493 365

Tax assets (*) 6 8 2

Other assets (*) 26 94 68

Deferred tax liabilities (487) (969) (482)

Provisions for risks and charges (52) (612) (560)

Accrued and deferred income - regulated activities (190) (254) (64)

Trade payables (161) (469) (308)

Tax liabilities (48) (82) (34)

Fair value gains (losses) on derivatives (39) (82) (43)

Other liabilities (64) (168) (104)

(464) (1,521) (1,057)(*) Tax receivables of € 2 million have been reclassified from “Other assets” (at 31 December 2008) to “Tax assets”.

(€m)

Equity-accounted investments 280

Toscana Energia S.p.A 131

Azienda Energia e Servizi Torino S.p.A 94

ACAM Gas S.p.A 46

Acqua Campania S.p.A 3

Metano Borgomanero S.p.A 2

Umbria Distribuzione Gas S.p.A 1

Metano Arcore S.p.A 1

Metano S. Angelo Lodigiano S.p.A 1

Servizi Territori Aree Penisole S.p.A 1

Other investments 2

Inversora del Aconcagua S.A 1

COM. e S.V. Gas & Power S.r.l. 1

Total at 30 June 2009 282

Net working capital (€ 1,521 million) decreased by € 1,057million due to the change in consolidation scope which ledto the recognition of net liabilities of € 948 million, including€ 638 million and € 310 million related to the gas distribu-tion and storage activities, respectively, and changes in oper-ations during the six months related to the natural gas trans-

portation and regasification business (-€ 109 million). Thesechanges are mainly due to: (i) smaller trade receivables (-€58 million), principally attributable to smaller volumes oftransported gas; (ii) the fair value loss on derivatives (-€ 43million) related to the reduction in market interest rates; (iii)higher accrued and deferred income related to transporta-

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / F I N A N C I A L R E V I E W

25

tion revenue (-€ 38 million); (iv) larger accruals to the provi-sions for risks and charges for litigation (-€ 16 million); and(v) smaller other assets (-€ 13 million), mainly due to the useof the VAT advance paid to the ultimate parent in December

2008. These factors were partly offset by: (i) the smallerdeferred tax liabilities (+€ 36 million); (ii) smaller tradepayables (+€ 22 million); and (iii) smaller tax liabilities (+€ 9million) as a result of the smaller profit before tax.

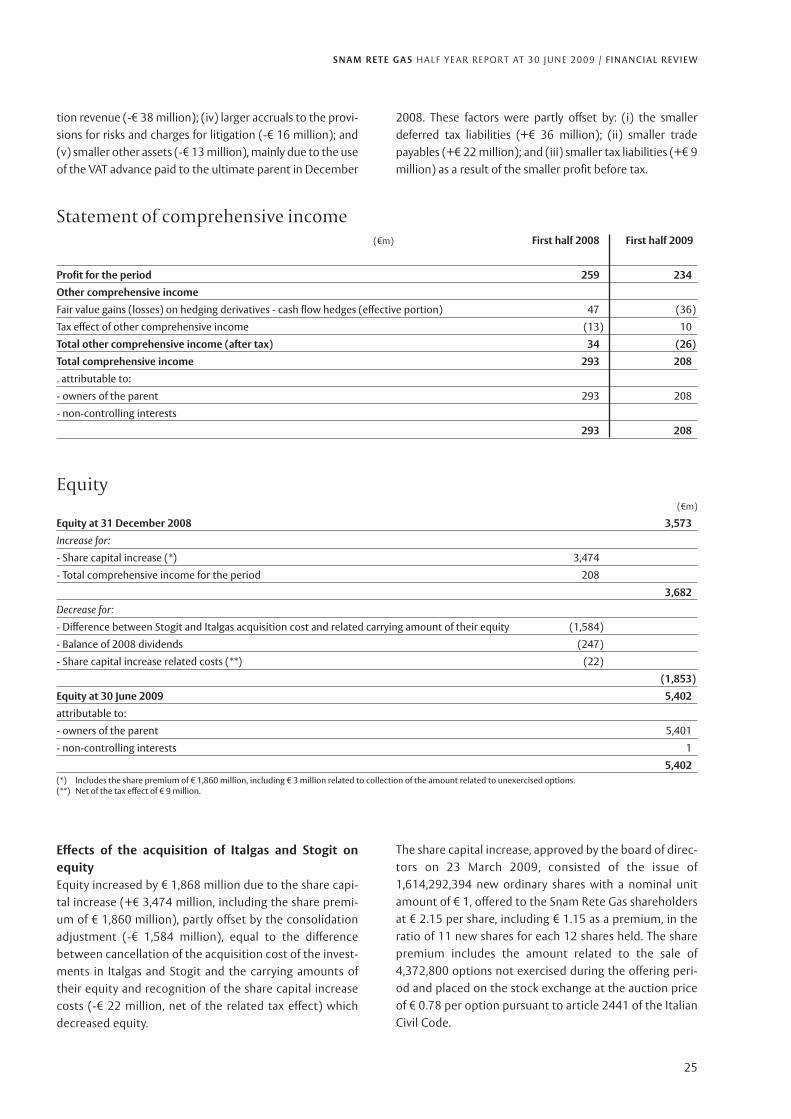

Statement of comprehensive income(€m) First half 2008 First half 2009

Profit for the period 259 234

Other comprehensive income

Fair value gains (losses) on hedging derivatives - cash flow hedges (effective portion) 47 (36)

Tax effect of other comprehensive income (13) 10

Total other comprehensive income (after tax) 34 (26)

Total comprehensive income 293 208

. attributable to:

- owners of the parent 293 208

- non-controlling interests

293 208

(€m)

Equity at 31 December 2008 3,573

Increase for:

- Share capital increase (*) 3,474

- Total comprehensive income for the period 208

3,682

Decrease for:

- Difference between Stogit and Italgas acquisition cost and related carrying amount of their equity (1,584)

- Balance of 2008 dividends (247)

- Share capital increase related costs (**) (22)

(1,853)

Equity at 30 June 2009 5,402

attributable to:

- owners of the parent 5,401

- non-controlling interests 1

5,402(*) Includes the share premium of € 1,860 million, including € 3 million related to collection of the amount related to unexercised options.(**) Net of the tax effect of € 9 million.

Equity

Effects of the acquisition of Italgas and Stogit onequityEquity increased by € 1,868 million due to the share capi-tal increase (+€ 3,474 million, including the share premi-um of € 1,860 million), partly offset by the consolidationadjustment (-€ 1,584 million), equal to the differencebetween cancellation of the acquisition cost of the invest-ments in Italgas and Stogit and the carrying amounts oftheir equity and recognition of the share capital increasecosts (-€ 22 million, net of the related tax effect) whichdecreased equity.

The share capital increase, approved by the board of direc-tors on 23 March 2009, consisted of the issue of1,614,292,394 new ordinary shares with a nominal unitamount of € 1, offered to the Snam Rete Gas shareholdersat € 2.15 per share, including € 1.15 as a premium, in theratio of 11 new shares for each 12 shares held. The sharepremium includes the amount related to the sale of4,372,800 options not exercised during the offering peri-od and placed on the stock exchange at the auction priceof € 0.78 per option pursuant to article 2441 of the ItalianCivil Code.

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / F I N A N C I A L R E V I E W

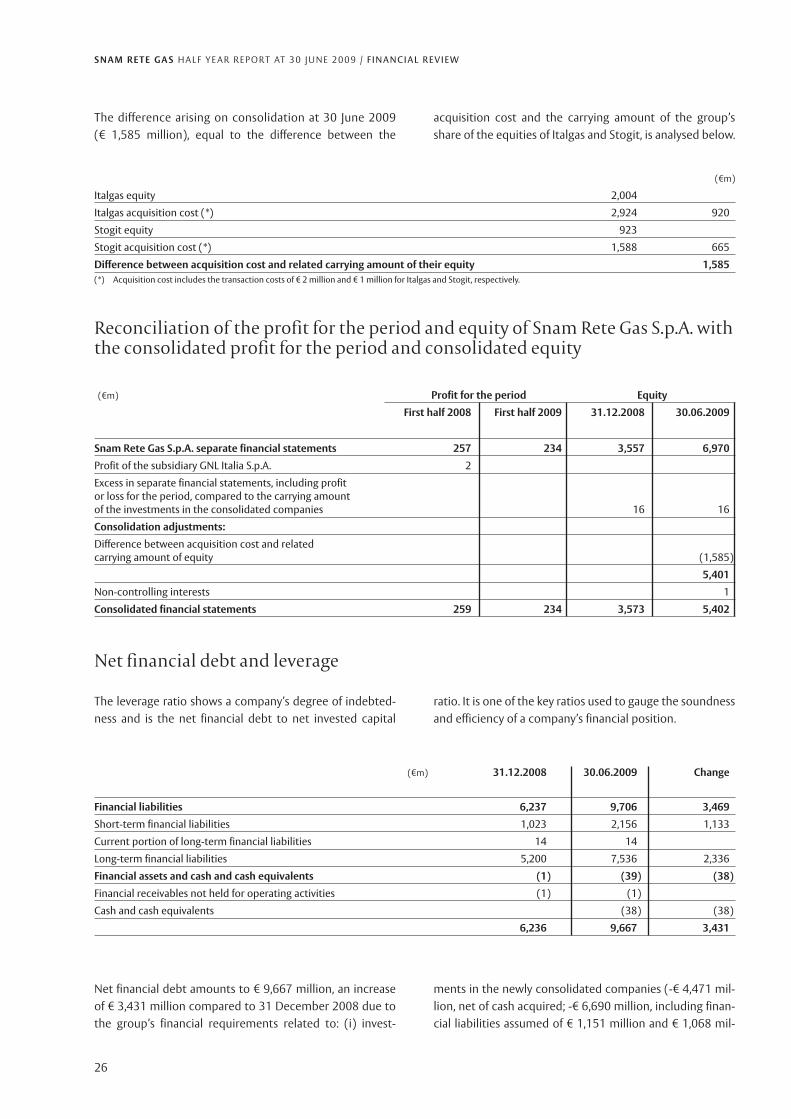

The difference arising on consolidation at 30 June 2009(€ 1,585 million), equal to the difference between the

acquisition cost and the carrying amount of the group’sshare of the equities of Italgas and Stogit, is analysed below.

26

(€m)

Italgas equity 2,004

Italgas acquisition cost (*) 2,924 920

Stogit equity 923

Stogit acquisition cost (*) 1,588 665

Difference between acquisition cost and related carrying amount of their equity 1,585(*) Acquisition cost includes the transaction costs of € 2 million and € 1 million for Italgas and Stogit, respectively.

Reconciliation of the profit for the period and equity of Snam Rete Gas S.p.A. withthe consolidated profit for the period and consolidated equity

(€m) Profit for the period Equity

First half 2008 First half 2009 31.12.2008 30.06.2009

Snam Rete Gas S.p.A. separate financial statements 257 234 3,557 6,970

Profit of the subsidiary GNL Italia S.p.A. 2

Excess in separate financial statements, including profitor loss for the period, compared to the carrying amountof the investments in the consolidated companies 16 16

Consolidation adjustments:

Difference between acquisition cost and relatedcarrying amount of equity (1,585)

5,401

Non-controlling interests 1

Consolidated financial statements 259 234 3,573 5,402

The leverage ratio shows a company’s degree of indebted-ness and is the net financial debt to net invested capital

ratio. It is one of the key ratios used to gauge the soundnessand efficiency of a company’s financial position.

Net financial debt and leverage

(€m) 31.12.2008 30.06.2009 Change

Financial liabilities 6,237 9,706 3,469

Short-term financial liabilities 1,023 2,156 1,133

Current portion of long-term financial liabilities 14 14

Long-term financial liabilities 5,200 7,536 2,336

Financial assets and cash and cash equivalents (1) (39) (38)

Financial receivables not held for operating activities (1) (1)

Cash and cash equivalents (38) (38)

6,236 9,667 3,431

Net financial debt amounts to € 9,667 million, an increaseof € 3,431 million compared to 31 December 2008 due tothe group’s financial requirements related to: (i) invest-

ments in the newly consolidated companies (-€ 4,471 mil-lion, net of cash acquired; -€ 6,690 million, including finan-cial liabilities assumed of € 1,151 million and € 1,068 mil-

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / F I N A N C I A L R E V I E W

27

(€m) 31.12.2008 % 30.06.2009 % Change

. Floating rate 2,524 40 4,541 47 2,017

. Fixed rate 3,713 60 5,165 53 1,452

6,237 100 9,706 100 3,469

All the financial liabilities are due to Eni and they are almostall in Euros.Floating rate financial liabilities (€ 4,541 million) increasedby € 2,017 million, partly due to the change in consolidationscope (€ 1,461 million) and the taking out of a new floatingrate loan from the ultimate parent, Eni S.p.A., of € 300 mil-lion to be repaid in 2016 and to be used by Snam Rete Gasto finance part of the acquisition of Stogit and Italgas.Fixed rate financial liabilities (€ 5,165 million) increased by€ 1,452 million, mainly due to the liabilities deriving fromconsolidation of the acquirees (€ 758 million) and the tak-ing out of a new floating rate loan from Eni S.p.A. of € 700

million. This was converted into a fixed rate loan by an inter-est rate swap.Fixed rate financial liabilities at 30 June 2009 include sevenfloating rate loans converted into fixed rate loans by inter-est rate swaps for a total notional amount of € 3,500 mil-lion. Note 14 “Other current liabilities” gives informationabout these derivatives.The leverage ratio, ie, the ratio of net financial debt to netinvested capital, is 64.2% (63.6% at 31 December 2008).There are no financial liabilities subject to covenants.Cash and cash equivalents (€ 38 million) relate to thechange in consolidation scope.

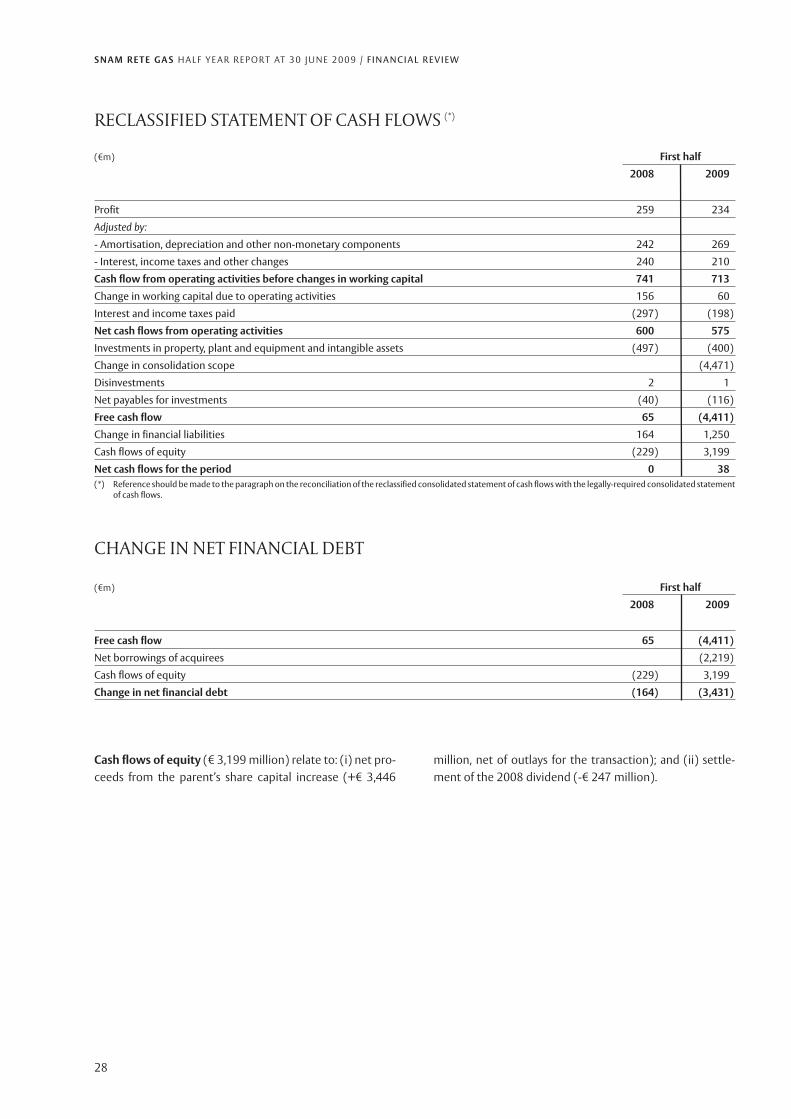

Reclassified consolidated statement of cash flows

The reclassified consolidated statement of cash flows set outbelow summarises the legally-required format. This reclassi-fied consolidated statement of cash flows shows the open-ing and closing cash and cash equivalents and the change innet financial debt during the period. The two statements arereconciled through the free cash flow, ie the cash surplus ordeficit left over after servicing capital expenditure. The free

cash flow closes either: (i) with the change in cash and cashequivalents for the period, after adding/deducting all cashflows related to financial liabilities/assets (takingout/repayment of loans) and equity (payment of divi-dends/capital injections); or (ii) with the change in net finan-cial debt for the period, after adding/deducting the debt flowsrelated to equity (payment of dividend/capital injections).

lion for Italgas and Stogit, respectively); (ii) net investmentsfor the period (-€ 515 million); (iii) settlement of the 2008dividend of € 0.14 per share, paid from 23 May 2008 (-€ 247million). These factors were partly offset by: (i) net cashflows of equity related to the share capital increase (+€3,446 million, including the share premium and net of out-flows to cover the transaction costs); and (ii) cash inflowsfrom operating activities (+€ 575 million).

Long-term financial liabilities of € 7,536 million make up78% of net financial debt (83% at 31 December 2008). Theaverage maturity of the long-term financing, including thecurrent portion, is just over four years (unchanged from 31December 2008).

A breakdown of the liabilities by type of interest rate at 30June 2009 is as follows:

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / F I N A N C I A L R E V I E W

28

Cash flows of equity (€ 3,199 million) relate to: (i) net pro-ceeds from the parent’s share capital increase (+€ 3,446

million, net of outlays for the transaction); and (ii) settle-ment of the 2008 dividend (-€ 247 million).

(€m) First half

2008 2009

Profit 259 234

Adjusted by:

- Amortisation, depreciation and other non-monetary components 242 269

- Interest, income taxes and other changes 240 210

Cash flow from operating activities before changes in working capital 741 713

Change in working capital due to operating activities 156 60

Interest and income taxes paid (297) (198)

Net cash flows from operating activities 600 575

Investments in property, plant and equipment and intangible assets (497) (400)

Change in consolidation scope (4,471)

Disinvestments 2 1

Net payables for investments (40) (116)

Free cash flow 65 (4,411)

Change in financial liabilities 164 1,250

Cash flows of equity (229) 3,199

Net cash flows for the period 0 38(*) Reference should be made to the paragraph on the reconciliation of the reclassified consolidated statement of cash flows with the legally-required consolidated statement

of cash flows.

CHANGE IN NET FINANCIAL DEBT

RECLASSIFIED STATEMENT OF CASH FLOWS (*)

(€m) First half

2008 2009

Free cash flow 65 (4,411)

Net borrowings of acquirees (2,219)

Cash flows of equity (229) 3,199

Change in net financial debt (164) (3,431)

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / F I N A N C I A L R E V I E W

29

RECONCILIATION OF THE RECLASSIFIED BALANCE SHEET FORMATS WITHTHE LEGALLY-REQUIRED FORMATS

(€m)

Reclassified consolidated balance sheet items 31.12.2008 30.06.2009(where not expressly stated, the component is taken directly Notes to the condensed Partial amount Amount from Partial amount Amount fromfrom the legally-required format) interim consolidated from legally- reclassified from legally- reclassified

financial statements required format format required format format

Non-current assetsProperty, plant and equipment 10,549 15,508Compulsory inventories 411Intangible assets 39 738Investments 282Financial receivables and securities held for operating activities (see note 2) 1Net payables for investments, consisting of: (286) (267)- Payables for investments (see note 12) (298) (292)- Receivables for investments/disinvestments (see note 2) 12 25Total non-current assets 10,302 16,673Net working capitalTrade receivables (see note 2) 417 520Inventories 128 493Tax assets, consisting of: 6 8- Current tax assets 1 1- Other current tax assets (*) 2 4- IRES receivables to parent for national consolidated tax scheme (see note 2) 3- Receivable to parent for group consolidated VAT scheme (see note 2) 3Trade payables (see note 12) (161) (469)Tax liabilities, consisting of: (48) (82)- Current tax liabilities (1) (11)- Other current tax liabilities (4) (12)- IRES payables to parent for national consolidated tax scheme (see note 12) (3) (42)- Payable to parent for group consolidated VAT scheme (see note 12) (40) (17)Deferred tax liabilities (487) (969)Provisions for risks and charges (52) (612)Other current assets (liabilities) consisting of: (267) (410)- Other receivables (see note 2) 20 74- Other current assets 52 58- Other non-current assets 3 9- Payments on account and advances, Other payables (see note 12) (34) (138)- Other current liabilities (52) (103)- Other non-current liabilities (256) (310)Total net working capital (464) (1,521)Provisions for employee benefits (29) (108)Net assets available for sale including related liabilities 25- Assets held for sale (see note 10) 37- Liabilities directly related to assets held for sale (see note 10) (12)NET INVESTED CAPITAL 9,809 15,069Equity 3,573 5,402Net financial debtFinancial labilities, consisting of: 6,237 9,706- Long-term financial liabilities 5,200 7,536- Current portion of long-term financial liabilities 14 14- Short-term financial liabilities 1,023 2,156Financial receivables, cash and cash equivalents consisting of: (1) (39)- Other financial assets (1) (1)- Cash and cash equivalents (38)Total net financial debt 6,236 9,667COVERAGE 9,809 15,069(*) VAT receivables of € 2 million have been reclassified from “Other assets” to “Tax assets” compared to 31 December 2008.

Reclassified consolidated balance

30

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / F I N A N C I A L R E V I E W

(€m)

First half

Reclassified captions and reconciliation with legally-required captions 2008 2009

Partial amounts Amounts from Partial amounts Amounts fromfrom legally- reclassified from legally- reclassified

required formats formats required formats formats

Profit for the period 259 234

Adjusted by:

Amortisation, depreciation and other non-monetary components 242 269

- Amortisation and depreciation 241 248

- Net impairment losses 1

- Change in provisions for risks and charges 17

- Losses on disinvestments, eliminations and derecognition 4

Interest, income taxes and other changes: 240 210

- Interest income (14) (2)

- Interest expense 122 91

- Income taxes 131 119

- Other adjustments 1 2

Cash flows from operating activities before changes in working capital 741 713

Change in working capital due to operating activities: 156 60

- Inventories (18) 1

- Trade and other receivables 130 69

- Other assets (5) (4)

- Trade and other payables 2 (41)

- Other liabilities 47 35

Cash flows from operating activities 897 773

Interest and income taxes collected (paid): (297) (198)

- Interest collected 25 4

- Interest paid (121) (85)

- Income taxes paid (201) (117)

Net cash flows from operating activities 600 575

Investments: (497) (4,871)

- Property, plant and equipment (484) (392)

- Intangible assets (13) (8)

- Change in consolidation scope (4,471)

Disinvestments: 2 1

- Property, plant and equipment 2 1

Net payables for investing activities (40) (116)

Free cash flow 65 (4,411)

Change in financial liabilities: 164 1,250

- Taking on long-term financial liabilities 311 9,306

- Repayments of long-term financial liabilities (14) (8,314)

- Increase (decrease) in short-term financial liabilities (133) 258

Cash flows of equity (229) 3,199

Net cash flows for the period 0 38

Reclassified statement of cash flows

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / O T H E R I N F O R M AT I O N

31

Other information

Incentive plans for managersinvolving Snam Rete Gas shares

Stock grant planAt 30 June 3009, Snam Rete Gas did not have any commit-ments to assign stock grants.

Stock option planReference should be made to the 2008 Annual Report forinformation on the 2002-2004, 2005 and 2006-2008 stockoption plans. No new stock option plans were issued in thefirst half of 2009. Variations that took place in the period aredescribed below.

In its meeting of 11 March 2009, the board of directorsset the exercise percentage for the stock optionsassigned in 2006 considering the company’s TSR posi-tioning in the three years 2006, 2007 and 2008 com-pared to that of the six leading European utilities compa-nies. At that date, 731,325 options related to 2006 hadbeen forfeited due to this positioning, calculated at theend of the vesting period.In April 2009, 30,500 shares were issued with a nominalvalue of € 1, subscribed by the managers benefitting fromthe 2004 stock option plan, as part of the resolutiontaken by the board of directors for the managers’ incen-tive plans.

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / O T H E R I N F O R M AT I O N

32

Year Option exercised Forfeited options (*) Exercised Existing options

2002 608,500 (21,000) (587,500)

2003 640,500 (433,000) 207,500

2004 677,000 (30,000) (286,500) 360,500

2005 658,000 (51,000) (69,000) 538,000

2006 2,597,500 (1,061,525) 1,535,975

2007 2,326,500 (242,900) 2,083,600

2008 2,235,000 2,235,000

9,743,000 (1,406,425) (1,376,000) 6,960,575(*) Includes forfeited options due to termination of employment relationship and, beginning from the 2006-2008 plan, the options forfeited as a result of the TSR positioning

at the end of the vesting period.

Changes in the stock option plans for each year of assignment are as follows:

Treasury shares

At 30 June 2009, Snam Rete Gas had 195,429,850 treasuryshares (unchanged from 31 December 2008), equal toapproximately 5.47% of the share capital. Their market valuewas roughly € 610 million at period end10.

Related party transactions

Snam Rete Gas S.p.A. is a subsidiary of Eni S.p.A..Transactions undertaken by Snam Rete Gas S.p.A. with relat-ed parties, as per IAS 24 “Related party disclosures”, mainlyinvolve the exchange of goods, provision of services and theprovision and utilisation of financial resources in addition totransactions to hedge interest rate risk with the ultimateparent, Eni S.p.A., and its subsidiaries and associates as wellas with Enel, a state-controlled company, and its sub-sidiaries. All these transactions are part of its ordinary busi-ness activities, usually take place at market conditions, ie,those conditions that would be applied between two inde-pendent parties, and are performed in the interests of theSnam Rete Gas group. Given the activities performed andthe nature of the relationship (company entirely or nearlyentirely owned by Eni), the services provided by certaincompanies are charged at rates agreed based on the specif-ic costs incurred and minimum profit margin to cover thegeneral costs and remuneration of invested capital. Theamounts of trade, other and financial transactions carriedout with related parties are disclosed in note 28 “Relatedparty transactions” to the condensed interim consolidatedfinancial statements. On 30 June 2009, as disclosed earlier,the acquisition of the entire share capital of Italgas andStogit from Eni was executed with payment by Snam ReteGas of a consideration of € 4,509 million, including € 2,922million for Italgas and € 1,587 million for Stogit. The acqui-sition represents a related party transaction as: (i) Eni is the

controlling shareholder of Snam Rete Gas; (ii) on 12February 2009, Snam Rete Gas received a commitment let-ter to enter into a contract, before the acquisition execu-tion date, for a long-term loan of a maximum of € 1,300 mil-lion to be used to pay part of the acquisition consideration;and (iii) on 12 February 2009, Eni agreed to subscribe theshares arising from the share capital increase. Informationon the transaction is given in the section on the“Acquisition of Italgas and Stogit” in this report to whichreference should be made.

Litigation

This section sets out developments in litigation comparedto the information given in the 2008 Annual Report and themost significant proceedings in which the acquirees areinvolved. Unless indicated otherwise, no provision has beenmade as Snam Rete Gas deems it improbable that the out-come of the proceedings will be unfavourable to it orbecause the accrual cannot be determined reliably.

Tax litigation

GNL Italia S.p.A. - Local property tax (ICI)With respect to the local property tax litigation betweenthe subsidiary GNL Italia S.p.A., the Porto Venere municipalauthorities and the La Spezia local body, the La Spezia taxcommission:- admitted the claims made by the local body whereby the

conditions for the application of the ICI tax would be inte-grated for the subsidiary in its ruling no. 136/7/08 of 18December 2008;

- accepted the claims made by GNL Italia in its ruling no.83/07/2009 of 9 April 2009 admitting that the greater taxassessed by the Porto Venere municipal authorities is duefrom 2007.

(10) Calculated by multiplying the number of treasury shares by the official price at 30 June 2009 (€ 3.12 per share).

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / O T H E R I N F O R M AT I O N

33

While awaiting filing of the rulings, the company has notused its provision for risks of € 2.6 million.

The key proceedings in which the acquirees are involved aresummarised below.

Penal cases

Italgas S.p.AIn May 2007, Italgas was served a search and seizure meas-ure as part of proceeding no. 1183/06 RGNR commencedby the public prosecutor before the Milan court. The deedwas also served to the company’s chairman. It set outalleged unlawful conduct beginning from 2003 withrespect to use of gas metering instruments, the relatedexcise duties, invoicing to customers and relationships withthe supervisory authorities. The alleged violations include,inter alia, crimes covered by Legislative decree no. 231 of 8June 2001, which envisages the company’s administrativeliability in the case of crimes committed by its employees inthe interests, or to the benefit of the company.Italgas is cooperating with the relevant authorities.

Tax litigation

Stoccaggi Gas Italia S.p.A. - Local property tax (ICI)On 26 February 2009, the subsidiary presented two appealsto the Chieti provincial tax commission against the assess-ment reports of the Chieti municipal local body and theCupello municipal authorities about payment of ICI on itscompression station.It has already recognised a provision of € 1.3 million for thislitigation.

Antitrust Authority

Italgas S.p.AOn 6 May 2009, the Antitrust Authority notified Italgas ofcommencement of an investigation into the possible abuseof a dominant position violating article 82 of the EU Treaty.This investigation also covers other companies in the gas sec-tor and is based on a communication made by another oper-ator, also active in the gas distribution sector. The latter com-pany communicated alleged blocking and time-wastingactions taken by Italgas when carrying out operating andcommercial switching procedures for the migration of cus-tomers from one company to another. The investigationshould end before 30 June 2010, Italgas obtained access tothe proceeding’s documents on 26 May 2009 in order to gaina clear understanding of the other operator’s allegations.

Stoccaggi Gas Italia S.p.AFinalisation of the preliminary investigation by the AntitrustAuthority and the Electricity and Gas Authority published

on 3 June 2009 wound up the procedure commenced inNovember 2007.The investigation covered: (i) discovering potential obsta-cles to the development of new storage capacity in financialand strategic terms; (ii) assessing the existence of alterna-tive flexibility instruments to storage and access thereto bynewcomers; and (iii) analysing the legislative and regulato-ry context, also to assess its impact on competition. Stogitcomplied with the formal requests for documents andinformation in July 2008 and provided additional informa-tion in October 2008 as requested.Upon concluding the investigation, the Authorities recog-nised that Stogit had conducted itself in line with the estab-lished legislative and regulatory requirements without preju-dice to other operators and that the existing framework of sys-tem balancing rules and access and use of storage capacityhave significantly influenced access to the gas distributionmarket, especially to industrial and thermoelectric customers.

Rome urban area

Following the sale by the French company Suez S.A. (nowGdF-Suez S.A. after their merger) of its Belgium subsidiaryDistrigaz, Eni agreed to sell Suez, on the basis of preliminarynegotiations with Italgas, the latter’s distribution activitiesin the Rome urban area together with other gas and elec-tricity business assets. On 29 May 2008, the related prelim-inary agreements were signed, including the sales terms forthe gas distribution activities. The final agreement for suchgas distribution activities was entered into by Italgas andGdF-Suez on 30 October 2008.The transaction relates to the business unit which distrib-utes gas in the municipalities of Rome, Fiumicino,Ciampino, Marino, Grottaferrata, Rocca di Papa and Frascati(the concession for Rome expires on 31 December 2009),including the distribution networks (spanning roughly5,300 km) and the related systems, approximately 1.3 mil-lion delivery points (equal to approximately 28% of theusers served), together with roughly 800 employees.The set price, based on 31 December 2008, is € 1,018 mil-lion.The contract provides that execution of the transactionshall take place with the transfer by Italgas of the businessunit to Rete Gas Roma S.r.l. (a newco set up on 26November 2008 wholly owned by Italgas) and is subject toattainment of approval by the Rome municipality authori-ties of transfer of the concession before 30 June 2009,which date the buyer may extend to 31 August 2009.The Rome municipal authorities agreed the transfer of theconcession contract to Rete Gas Roma with its communica-tion no. 1231 of 25 June 2009, acknowledging Italgas’ inten-tion to transfer its entire investment in this company to GdF-Suez. The concession covers the distribution of gas in Rome.

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / O T H E R I N F O R M AT I O N

34

On 6 July 2009, the Rome mayor subsequently specifiedthat this communication is the sole document necessary tolegitimately and effectively express the municipal authori-ty’s consent to the transaction and that the town councilwould be informed thereof.However, on 13 July 2009, GdF-Suez informed Italgas that itnot believe that the conditions for transfer of the Romeurban area gas distribution activities had been met in theestablished timeframe. Therefore, it decided not to contin-ue with finalisation of the acquisition as set out in the con-tract agreed by the parties on 30 October 2008.Snam Rete Gas is evaluating the contract’s content to assesswhat actions could be taken to best protect its interests.

Disclosure required by article 37 ofConsob regulation no. 16191/07

On 12 February 2009, the directors checked that the parentmeets the requirements set out in article 37.1 of Consobresolution no. 16191/07 for the listing of shares of sub-

sidiaries managed and coordinated by another company onan Italian regulated market as: a) it has complied with thedisclosure obligations set by article 2497-bis of the ItalianCivil Code; b) negotiates terms with its customers and sup-pliers independently; c) has a centralised treasury arrange-ment with its parent, Eni S.p.A., which meets its interests;and d) the board of directors has nine members, five ofwhom meet the independence requirements set for statu-tory auditors as per article 148.3 of Legislative decree no. 58of 24 February 1998 and article 3 of the Code of Conduct.No variations had taken place at 30 June 2009 with respectto the above information.

Subsequent events

The Electricity and Gas Authority published the secondpublic discussion document (DCO 24/09 dated 23 July2009) regarding the determination of the transport rev-enue and natural gas transportation and dispatching tariffsfor the third regulatory period.

S N A M R E T E G A S H A L F Y E A R R E P O RT AT 3 0 J U N E 2 0 0 9 / PERFORMANCE OF THE ACQUIREES