Embed Size (px)

Citation preview

HALF YEAR FINANCIAL REPORTJanuary-June 2016

July 29, 2016

Martin à Porta, President and CEOJukka Pahta, CFO

COPYRIGHT©PÖYRY

CONTENTS

1. January – June overview

2. Continuous improvement

3. Key project and contract wins

4. Outlook

Martin à PortaPresident & CEO

5. Financial performance

6. Appendices

Jukka PahtaCFO

JULY 29, 2016Q2/2016 PRESENTATION 2

COPYRIGHT©PÖYRYJULY 29, 2016

Q2/2016 PRESENTATION 3

JANUARY – JUNEOVERVIEW1

COPYRIGHT©PÖYRY

MARKET REVIEW: OVERVIEW

JULY 29, 2016Q2/2016 PRESENTATION 4

• The economic and market outlook for our sectors in 2016 remains challenging• Slowing growth in China, reasonable in the rest of the Asia• Robust economic growth in the US• Our key regions in particular are impacted by fewer investments• However, there are still opportunities in many markets

COPYRIGHT©PÖYRY

MANAGEMENT CONSULTING• Improvement in Central and Southern Europe• Challenging market situation in Northern Europe

REGIONAL OPERATIONS• Challenging market situation continues with respect to our business portfolio• Public sector investment decisions may open opportunities• Despite slight signs on economic recovery the situation in Brazil remains uncertain

INDUSTRY• Production line conversions in forest industry• Pulp-mill equipment relocation projects in Asia• Other parts of Asian market are generally slowing down

ENERGY• Positive development especially in hydro business in Asian market• Low oil prices delay investment decision making in Middle East• Tight market situation in Northern and Central Europe

MARKET REVIEW: BUSINESS LINES

JULY 29, 2016Q2/2016 PRESENTATION 5

COPYRIGHT©PÖYRY

Continued strengthening of sales focus

Reduced number of legal cases

Progress in streamlining the organisation in Energy, Management Consulting

and Latin America

Q2 ORDER INTAKE STABLE, PERFORMANCE FAR BELOWEXPECTATIONS

JULY 29, 2016Q2/2016 PRESENTATION 6

Net sales• Decreased across all business lines partly explained by missing larger EPC-

projects

Order stock• Remained stable compared to 2015 year end• Stable in Management Consulting and the Regional Operations• Decreased in Energy and Industry

• Improved in the Regional Operations• Decreased in other Business Lines

Adjustedoperating result

COPYRIGHT©PÖYRY

LOWER FIGURES AGAINST COMPARABLE PERIOD

JULY 29, 2016Q2/2016 PRESENTATION 7

MEUR 1-6/2016 1-6/2015 Change

Order stock 457.8 502.4 -8.9%Net sales 271.9 297.6 -8.6%Operating result -4.2 2.8 n.a.Adjusted operating result -1.7 4.3 n.a.Net result -5.6 -1.5 n.a.

COPYRIGHT©PÖYRYJULY 29, 2016

Q2/2016 PRESENTATION 8

CONTINUOUSIMPROVEMENT2

COPYRIGHT©PÖYRY

WE CONTINUE IMPLEMENTING OUR OPERATIONALFRAMEWORK AND ENHANCING CLIENT FOCUS

JULY 29, 2016Q2/2016 PRESENTATION 9

2013 2014 2015

Driving sales focus and performance in project management

Improving profitability

Addressing structural and administrative challenges

Strengthening client focus1. Simplify and empower2. Strengthen the core3. Scale up

2016

COPYRIGHT©PÖYRYJULY 29, 2016

Q2/2016 PRESENTATION 10

KEY PROJECT AND CONTRACT WINS3

COPYRIGHT©PÖYRY

ASSIGNMENT FOR RECONSTRUCTION AND EXTENSION OF ATRANSMISSION SYSTEM SUBSTANTION IN AUSTRIA

JULY 29, 2016Q2/2016 PRESENTATION 11

· Client – Austrian Power Grid AG, Austria· Scope – Modernisation and extension of existing 220/380kV switchgears at Lienz

substation, Austria. The frame agreement includes detailed design engineering, projectmanagement and installation services as well as the supply of equipment. Dismantlingof the existing 220kV switchgear and installation of the new components will bemanaged step by step, in close co-operation with the client.

· Duration – Six years

COPYRIGHT©PÖYRY

DETAILED DESIGN SERVICES ASSIGNMENT FORHYDROELECTRIC POWER PLANT, TURKEY

JULY 29, 2016Q2/2016 PRESENTATION 12

· Client – Kalehan Genç Enerji Üretim A.S.· Project – Pöyry has been awarded a detailed design services assignment for the

Lower Kaleköy Hydroelectric Power Plant and Dam in Turkey. The assignment includesthe execution of the detail design for the civil engineering of the powerhouse, andstructural reviews, including the roller-compacted concrete (RCC) dam, power intakeand penstocks, piano-key weir spillway solution, diversion structures with two tunnelsand bottom.

· Expected completion – By the end of 2017

COPYRIGHT©PÖYRY

FINANCIAL ADVISORY SERVICES TO DELTA PACKAGING ON ITSACQUISITION BY HUHTAMÄKI

JULY 29, 2016Q2/2016 PRESENTATION 13

· Client – Delta Print & Packaging· Project – On 19th May 2016 Huhtamäki announced its acquisition of Delta Print &

Packaging. Based in Belfast, Northern Ireland, Delta is a manufacturer of folding cartonpackaging, supplying major food service brands including KFC, Kellogg's, McDonald'sand United Biscuits. The company has recently expanded its manufacturing operationsby building a factory in southern Poland.

· Pöyry acted as financial adviser to Delta and its owners.

COPYRIGHT©PÖYRY

BASIC ENGINEERING ASSIGNMENT FOR THE NEW WASTEWATERSOLUTION IN LAPPEENRANTA, FINLAND

JULY 29, 2016Q2/2016 PRESENTATION 14

· Client – Lappeenrannan Lämpövoima Oy· Project – Pöyry has been awarded the basic engineering assignment for the new

Lappeenranta wastewater treatment plant and its wastewater transfer system. Theassignment also includes identification and comparison of process solutions, piloting ofthe selected solution, optimisation of the wastewater balancing and pumping systemsand preparation of the building permit documents.

· Expected completion - Summer 2021

COPYRIGHT©PÖYRY

DETAILED ENGINEERING ASSIGNMENTS FOR BLOMINMÄKIWASTEWATER TREATMENT PLANT IN FINLAND

JULY 29, 2016Q2/2016 PRESENTATION 15

· Client – Helsinki Region Environmental Services (HSY)· Project – Pöyry has been awarded detailed engineering assignments for the

Blominmäki wastewater treatment plant to be built in Espoo, Finland. The assignmentsinclude the structural and architectural design of the treatment plant, electrical,instrumentation and automation design, area planning, and the geotechnicalengineering of aboveground structures.

· Expected completion – 2020

COPYRIGHT©PÖYRYJULY 29, 2016

Q2/2016 PRESENTATION 16

OUTLOOK4

COPYRIGHT©PÖYRY

OUTLOOK FOR 2016

JULY 29, 2016Q2/2016 PRESENTATION 17

Asian market for Industry business slowingdown

Opportunities in Energy sector especiallyin Asia, South-America and Africa

In Europe public sector investments oninfrastructure in order to stimulate economic

growth.

For energy and other industrial sectors relevantto Pöyry’s business, the prospects are

expected to be challenging

The Group’s adjusted operating result is expected to be positive.

Market conditions

Despite some signs for economicrecovery in Brazil, economic and political

situation still uncertain

Decline in structural consumptionof graphic paper continues, outlookreasonable for other forest product

industry sectors

COPYRIGHT©PÖYRYJULY 29, 2016

Q2/2016 PRESENTATION 18

FINANCIALPERFORMANCE5

COPYRIGHT©PÖYRY

0

100

200

300

400

500

600

2012 2013 2014 2015 Q2/2016

Energy Industry Regional Operations Management Consulting

ORDER STOCK

JULY 29, 2016Q2/2016 PRESENTATION 19

457.8 (502.4) MEUR· Order stock remained stable

compared to 2015 year-end.

· Stable in Regional Operations andManagement Consulting

· Decreased in Energy and Industry

Comparable figures after divestments

MEUR

512

462 472 465 458

COPYRIGHT©PÖYRY

NET SALES

JULY 29, 2016Q2/2016 PRESENTATION 20

MEUR

Comparable figures after divestments

271.9 (297.6) MEUR· Net sales decreased partly due to

missing larger EPC-projects

· Remained stable in Industry

· Decreased in other BusinessLines

Q2: 135.9 (150.9) MEUR

706

602552

575 565 550

298272

0

100

200

300

400

500

600

700

800

COPYRIGHT©PÖYRY

ADJUSTED OPERATING RESULT

JULY 29, 2016Q2/2016 PRESENTATION 21

MEUR

-1.7 (4.3) MEUR· Increased in Industry

· Decreased in other BusinessLines

Q2: -1.1 (1.2) MEUR

*) 2013 includes a gain of EUR 14 million from thedivestment of the office real estate in Vantaa

9

11

-5

9

6

3 4

-2

-6

-4

-2

0

2

4

6

8

10

12

14

• Adjusted items -2.6 MEUR (-1.5 MEUR) are mainlyrestructuring expenses and expenses related tolabour claims customary in one of the Groupsoperating countries as well as losses relating toprojects from former Urban Business Group and fromprojects finalized over two years ago.

COPYRIGHT©PÖYRY

NET SALES AND HEADCOUNT 1-6/2016 BY BUSINESS LINE

JULY 29, 2016Q2/2016 PRESENTATION 22

Net salesEUR 271.9 (297.6) million

Headcount5,685 (5,803)

EnergyIndustry

Regional OperationsManagement ConsultingFTEs at the end of period 4,879

26%

8%

54%

12%22%

10%

60%

7%24%

10%

54%

12%21%

11%

61%

7%

COPYRIGHT©PÖYRY

ENERGY BUSINESS GROUP: NET SALES DOWN

JULY 29, 2016Q2/2016 PRESENTATION 23

Adjusted operatingresult 0.7 (1.8) MEUR• Operating result 0.5 (1.8) MEUR• Adjusted items include

restructuring expenses inNorthern Europe

Q2: 0.0 (0.6) MEUR

Sales 65.3 (71.8) MEUR

Q2: 31.7 (37.3) MEUR• Decreased especially in Northern

and Central Europe and inPhilippines where a larger projectwas in execution phase in 2015

Rolling 12 months

Net sales & adjusted operating margin, %MEUR

129

142 141

6%

2%

3%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0

20

40

60

80

100

120

140

160

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16

Net sales Adjusted operating margin, %

COPYRIGHT©PÖYRY

INDUSTRY BUSINESS GROUP: NET SALES STABLE

JULY 29, 2016Q2/2016 PRESENTATION 24

Adjusted operating result2.7 (2.1) MEUR• Adjusted items include profit related

to a project on which losses wererecorded in 2014 and reported as anadjusted item

Q2: 0.8 (1.1) MEUR

Sales 26.8 (25.8) MEUR

Q2: 12.8 (14.1) MEUR• Decline mainly due to development in

Asia

Rolling 12 months

Net sales & adjusted operating margin, %MEUR

46 45

55

5% 5%

10%

0%

2%

4%

6%

8%

10%

12%

14%

0

10

20

30

40

50

60

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16

Net sales Adjusted operating margin, %

COPYRIGHT©PÖYRY

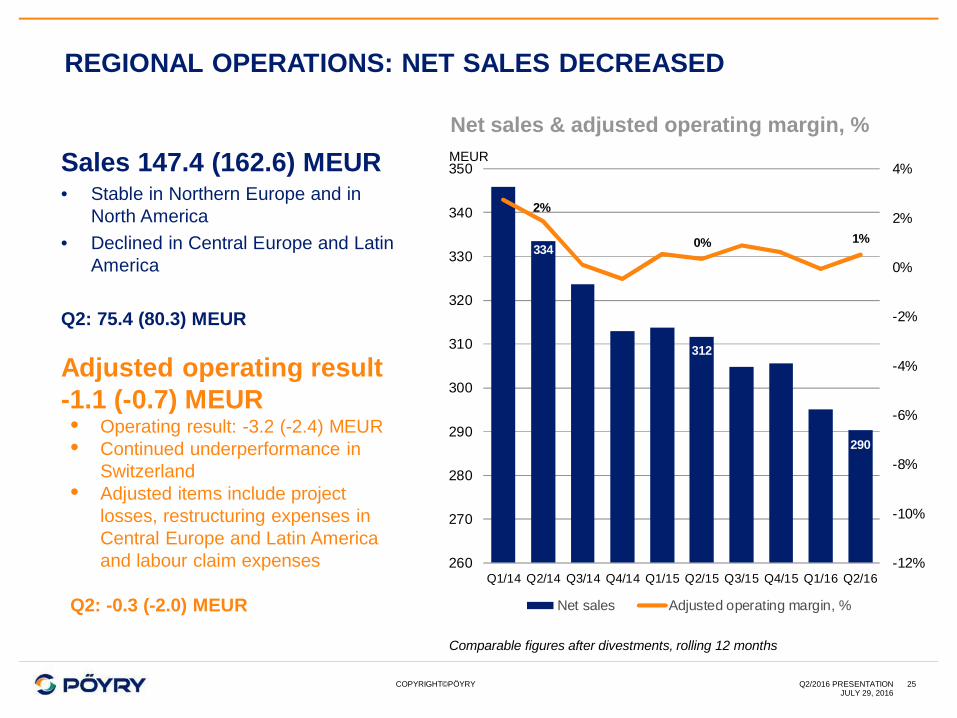

REGIONAL OPERATIONS: NET SALES DECREASED

JULY 29, 2016Q2/2016 PRESENTATION 25

Adjusted operating result-1.1 (-0.7) MEUR• Operating result: -3.2 (-2.4) MEUR• Continued underperformance in

Switzerland• Adjusted items include project

losses, restructuring expenses inCentral Europe and Latin Americaand labour claim expenses

Q2: -0.3 (-2.0) MEUR

Sales 147.4 (162.6) MEUR• Stable in Northern Europe and in

North America• Declined in Central Europe and Latin

America

Q2: 75.4 (80.3) MEUR

Comparable figures after divestments, rolling 12 months

Net sales & adjusted operating margin, %MEUR

334

312

290

2%

0% 1%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

260

270

280

290

300

310

320

330

340

350

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16

Net sales Adjusted operating margin, %

COPYRIGHT©PÖYRY

MANAGEMENT CONSULTING: NET SALES DOWN

JULY 29, 2016Q2/2016 PRESENTATION 26

Adjusted operatingresult 2.3 (3.0) MEUR• Operating result 1.8 (3.0) MEUR• Adjusted items include

restructuring expenses in Asiaand expenses related to projectsfinalized over two years ago

Q2: 0.8 (1.5) MEUR

Sales 31.9 (35.2) MEUR

Q2: 15.9 (17.9) MEUR

Q2

Rolling 12 months

Net sales & adjusted operating margin, %MEUR

66 6563

8%8%

6%

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

10

20

30

40

50

60

70

80

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16

Net sales Adjusted operating margin, %

COPYRIGHT©PÖYRY

CASH FLOW

JULY 29, 2016Q2/2016 PRESENTATION 27

Cash flow before financing-35.4 (-8.6) MEUR

Q2: -10.7 (-10.6) MEUR

Cash flow from operations-33.6 (-9.2) MEUR• Change in net working capital

- 28.2 MEUR including advancepayment of 5.0 MEUR for three years’software lease agreement andpayment of 7.7 (4.6) MEUR foraccrued bonuses

• Ongoing implementation of businessmanagement system had a negativeimpact on cash flow from operations

Q2:-10.1 (-12.9) MEUR

*) 2013 includes the divestment of the office real estate in Vantaa, Finland**) 2014 includes the divestment of real estate business in Finland

MEUR

- 2.2

-33.6

5.2

-35.4-40

-30

-20

-10

0

10

20

30

40

50

60

2012 2013*) 2014**) 2015 1-6/2016

From operations Before financing

COPYRIGHT©PÖYRY

NET DEBT, EQUITY AND GEARING

JULY 29, 2016Q2/2016 PRESENTATION 28

Gearing 32.7 (51.1)%

Net debt39.3 (47.5) MEUR

Equity120.2 (92.9) MEUR

The office real estate in Vantaa, Finland, was included in thebalance sheet in 2012 and sold in Q4-2013

MEUR Gearing-%

120.2

39.3

32.7%

0%

10%

20%

30%

40%

50%

60%

70%

0

20

40

60

80

100

120

140

2012 2013 2014 2015 End ofperiod

Equity Net debt Gearing -%

www.poyry.comConsulting. Engineering. Projects. Operations.

Thank you

COPYRIGHT©PÖYRYJULY 29, 2016

Q2/2016 PRESENTATION 30

APPENDICES6

COPYRIGHT©PÖYRY

RETURN ON INVESTMENT, %

JULY 29, 2016Q2/2016 PRESENTATION 31

-2.9%

-12%-10%-8%-6%-4%-2%0%2%4%6%8%

2012 2013 2014 2015 End of period

COPYRIGHT©PÖYRY

STATEMENT OF INCOME

JULY 29, 2016Q2/2016 PRESENTATION 32

MEUR 1-6/2016 1-6/2015Net sales 271.9 297.6Other operating income 0.5 0.8Materials and supplies -1.9 -6.9External charges, sub-consulting -20.7 -24.1Personnel expenses -184.7 -194.9Other operating expenses -69.4 -69.6

Operating result -4.2 2.8Net financial items -0.8 -3.9Share of associated companies’ andjoint ventures results 0.3 0.3

Result before taxes -4.8 -0.9Income taxes -0.8 -0.6

Net result for the period -5.6 -1.5

COPYRIGHT©PÖYRY

BALANCE SHEET

JULY 29, 2016Q2/2016 PRESENTATION 33

MEUR 30 Jun 2016 30 Jun 2015Goodwill 121.4 124.1Other non-current assets 56.1 48.8Work in progress 74.6 88.0Accounts receivable 108.2 113.0Other current assets 30.2 26.1Cash and cash equivalents 36.9 51.6Assets classified as held for sale - 4.6Total assets 427.5 456.3Equity 120.2 92.9Interest bearing liabilities 76.2 99.1Pension obligations and other non-current liabilities 53.6 52.9

Project advances 56.8 81.2Accounts payable 18.0 20.0Other current liabilities 102.6 110.2Total equity and liabilities 427.5 456.3

COPYRIGHT©PÖYRY

CASH FLOW

JULY 29, 2016Q2/2016 PRESENTATION 34

MEUR 1-6/2016 1-6/2015Net result for the period -5.6 -1.5AdjustmentsDepreciation and impairment losses 2.3 2.2Financial items and taxes 1.6 4.6Other adjustments 0.4 -1.3

Change in working capital -28.2 -8.8Paid financial items and taxes -4.2 -4.4Total from operating activities -33.6 -9.2Net cash flow from investing activities -1.8 0.7Net cash before financing -35.4 -8.6Net cash from financing 0.9 7.4Change in cash -34.6 -1.2

COPYRIGHT©PÖYRY

KEY FIGURES

JULY 29, 2016Q2/2016 PRESENTATION 35

1-6/2016 1-6/2015Earnings per share, EUR (diluted) -0.11 -0.03Earnings per share adjusted, EUR -0.07 -0.01Equity per share, EUR 1.98 1.53ROI-% -2.9 4.3ROE-% -10.0 -2.8Equity ratio-% 32.4 24.8Gearing-% 32.7 51.1Net debt, EUR million 39.3 47.5Capital expenditure, EUR million 2.2 3.2Personnel on average (FTE) 4 900 5 091