Embed Size (px)

DESCRIPTION

Part of the overall reform of the United Nations, this plan covering the years 2008-2013, provides a new shared vision. It is forged in the collaboration of all parties, from Governments to Local authorities and other Habitat Agenda partners, to the beneficiaries themselves. UN-HABITAT sees a way forward in five key areas of focus: advocacy, monitoring and partnerships; participatory urban planning, management and governance; affordable land and housing; environmentally-sound and affordable basic infrastructure and services; and, most importantly, strengthening human settlements finance systems.

Citation preview

A look at Global Migration Problems

U N I T E D N A T I O N S H U M A N S E T T L E M E N T S P R O G R A M M E

In this issue: Slums.....................................6

Gender and microfinance......................... 8

The German example............11

Nobel laureate..................... 14

Kumari Selja ........................15

Pakistan field dispatch..........20

Habitat Debate

March 2007 • Vol. 13, No. 1

Financing for the urban poor

� Habitat Debate March 2007

The year 2007 marks a historic cross-roads in human history because it is

the year in which, for the first time, half of humanity will be living in towns and cities.

We are at the dawn of the new urban era. And our research shows that by 2030, this figure will rise to two-thirds. We thus live at a time of unprecedented, rapid, ir-reversible urbanisation. The cities growing fastest are those of the developing world. And the fastest growing neighbourhoods are the slums. Indeed, 2007 will also be the year in which the global number of slum dwellers is forecast to reach the 1 bil-lion mark.

It is patently clear to all of us in the United Nations system as a whole, that if we fail to achieve the Millennium Development Goals in towns and cities, we will simply fail to achieve them at all.

But it comes down to a question of reaching as many people as possible. A cornerstone of UN-HABITAT’s new Medium-term Strategic and Institutional Plan is partnerships. We have no choice but to catalyze new partnerships between government and the private sector.

This is the only way to finance infra-structure and housing at the required scale – the scale needed to stabilize the rate of slum formation, and subsequently reduce and ultimately reverse the number of people living in life-threatening slum conditions.

Yet there is every likelihood that in the coming 20 years, conventional sources of funds will simply be unavailable for in-vestment at the scale required to meet the projected demand for urban infrastruc-ture and housing.

Many countries around the world con-tinue to face deficits in public budgets and weak financial sectors. Local govern-ments have started to seek finance in na-tional and global markets, but this is only in its initial phase.

New mortgage providers have emerged, including commercial financial institu-tions and mortgage companies. But only middle and upper income households have access to such finance, while the poor are generally excluded.

Although social housing is becoming less important in Europe and in countries with economies in transition, the need to provide shelter that is affordable to low-

income households still exists, including in developing countries.

The majority of urban poor households can only afford to build incrementally in stages, as and when financial resources be-come available. In response, microfinance institutions have started lending for low-income shelter development and have be-come very important in the last decade.

Guarantee schemes can, by providing credit enhancement, go far in broadening the appeal of microfinance institutions to lenders. Another important trend in the last decade is community funds, which are often linked to housing cooperatives as well as rotating savings and credit so-cieties. Community-based financing of housing and services has been used for both settlement upgrading and for build-ing new housing on serviced sites. These funds have many advantages for low in-come households because of the success of small loans and the increasing urbaniza-tion of poverty.

Constraints to mobilizing financial re-sources for investment in shelter develop-ment are both financial and non-financial in nature. Non-financial constraints in-clude land legislation that makes it diffi-cult to use real estate as effective collateral, as well as inappropriate national and lo-cal regulatory frameworks governing land use, occupancy and ownership.

Finance is only one dimension of secur-ing sustainable solutions that can fill the gap between the two extremes of current processes: inadequate, affordable shelter; and unaffordable adequate shelter.

Experience in both developed and de-veloping countries shows that such efforts contribute effectively to the objective of reducing poverty by creating jobs, attract-ing investments, improving health and raising economic productivity. Such ef-forts typically include: n Good urban management, planning

and governance to ensure that all cit-izens, particularly women, the young and the elderly, have a strong voice in decisions that affect their lives;

n Efficient land markets and property administration that prevent land spec-ulation and urban sprawl and provide sufficient affordable land for the urban poor;

n Enforceable zoning and land use reg-ulations that facilitate compact and mixed-use urban development and re-duce the ecological footprint of cities;

n Affordable and environmentally sound infrastructure including transport, en-ergy, water and sanitation;

n Financial markets and systems that can provide affordable housing credit and long-term municipal finance. As the only United Nations body vest-

ed with responsibility for promoting the sustainable development of the built en-vironment, UN-HABITAT needs all the support it can garner for its new reform plan.

Part of the overall reform of the United Nations, this plan covering the years 2008-2013, provides a new shared vision. It is forged in the collaboration of all par-ties, from Governments to Local author-ities and other Habitat Agenda partners, to the beneficiaries themselves.

UN-HABITAT sees a way forward in five key areas of focus: advocacy, monitor-ing and partnerships; participatory urban planning, management and governance; affordable land and housing; environmen-tally-sound and affordable basic infrastruc-ture and services; and, most importantly, strengthening human settlements finance systems.

Anna Tibaijuka Executive Director

A Message from the Executive Director

�Habitat Debate March 2007

Cover Photo

Slum area in Bukit Duri, Jarkata, IndonesiaPhoto © Suzi Mutter 2005

EditorRoman Rollnick

Editorial Assistance

Tom Osanjo

Design & Layout

Irene Juma

Editorial Board

Vincent KitioLucia KiwalaAnantha KrishnanEduardo López MorenoJane NyakairuEdlam YemeruMariam Yunusa

Published by

UN-HABITATP.O. Box 30030, GPONairobi 00100, KENYA;Tel: (254-20) 762 1234Fax: (254-20) 762 4266/7, 762 3477, 762 4246Telex: 22996 UNHABKE E-mail: [email protected]: http://www.unhabitat.org/

ISSN 1020-3613

Opinions expressed in signed articles are those of the authors and do not necessarily reflect the official views and policies of the United Nations Human Settlements Programme (UN‑HABITAT). All material in this publication may be freely quoted or reprinted, provided the authors and Habitat Debate are credited.

Contents

A MESSAGE FROM THE EXECUTIVE DIRECTOR ............................................2

OVERVIEW Financing for the urban poor..............................................4, 5

FORUM Three things we should know about slums.......................6

Employer-provided housing finance....................................7

Gender and microfinance .........................................................8

Promoting inclusive and effective local economic development .................................................................................9

Microfinance for the world’s poorest people..................10

SPECIAL REPORT Financing for urban development in the Asia-Pacific...............................................................................12,13

OPINION Home-financing in Africa........................................................11

Economic growth, rapid urbanisation and poverty............................................................................................14

Nobel laureate says ..................................................................15

CASE STUDIES The municipal finance system in Germany.....................16

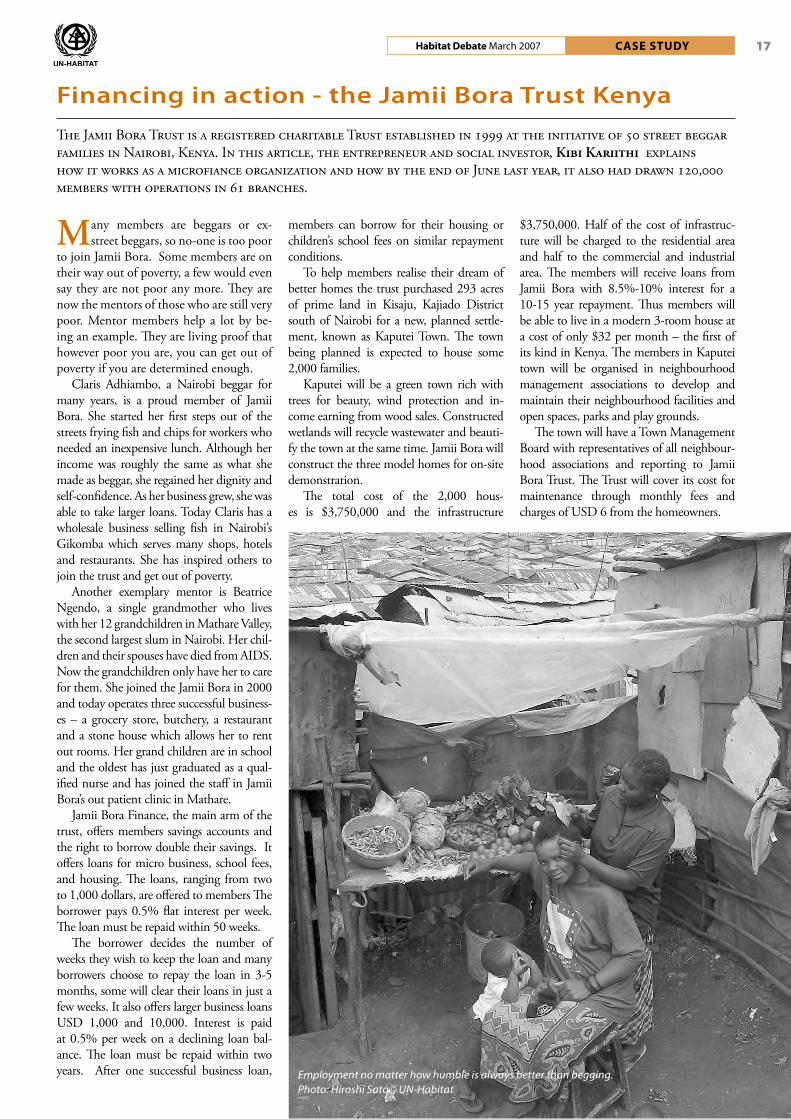

Financing in action - the Jamii Bora Trust Kenya...........17

BEST PRACTICES ....................................................................18,19

FIELD REPORT Building back better in Pakistan...........................................20

NEW PUBLICATIONS ...................................................................21

NEWS & EVENTS ..............................................................22,23

� Habitat Debate March 2007OVERVIEW

In an era of neo-liberal econom-ics predicated on market-led

growth, interest in financing reflects recognition of the limits of public expenditure. It also reflects the fail-ure of public planning and deliv-ery systems to keep pace with rapid urbanization. It further reflects the initiatives of non-State actors to in-crease the supply of housing and infrastructure in the absence of ade-quate public intervention.

The shift in emphasis from pub-lic to private sources of finance rais-es questions about the role of the State in housing and urban devel-opment and, by extension, about the future policies of international development cooperation agencies and financial institutions.

In the 1970s, most member States in the developing world ex-perienced in the 1970s an econom-ic and political crisis that led many to implement structural adjustment policies in the next decade. Governments devalued their currencies to promote ex-ports, eliminated price supports, aligned their economies with global markets, cut public expenditures on social services, privatized state-owned enterprises, and liberalized financial markets. National housing corporations in many countries either collapsed or scaled back operations. Public expenditure on hous-ing dropped, as did public investment in urban infrastructure. By the 1990s, pub-lic finance for housing and urban infra-structure was all but eliminated, save ad hoc programmes of development coopera-tion agencies and NGOs designed to min-imize the social consequences of structural adjustment.

The advent of rapid urbanization coin-cided with economic crisis and structural adjustment. First in Latin America, then in South and Southeast Asia, and more recently in Africa, rural-urban migration combined with population growth to in-crease the size of cities. Urbanization with-out requisite economic growth resulted in urban unemployment; urbanization with-out public services resulted in inadequate

shelter, water and sanitation; urbanization without economic growth and public ser-vices resulted in the urbanization of pover-ty and slums. Municipal authorities barely capable of meeting their payrolls, were vulnerable to corruption, unable to col-lect revenues, or plan, let alone finance the burgeoning housing and service needs.

The demand for services in the absence of public supply created two types of in-novation and corresponding sources of fi-nance: Private entrepreneurs who saw in slums a business opportunity and urban poor organizations keen to improve their living and working conditions. The entre-preneurs built shacks without services for rent, or provided unofficial services (wa-ter, credit, sanitation, electricity, security, etc.). Rates were calibrated on capacity to pay, small unit provision, high unit cost, and on high volume.

The organized poor mobilized sav-ings and acted collectively or individual-ly to secure land, build homes, and gain access to services. Microfinance institu-tions emerged to offer credit to entrepre-neurs and the organized poor. Rather than rely on public finance, slums generated in-

vestment, fostered rent-seeking op-portunities and offered a source of cheap labour to industry, upscale residential neighbourhoods and the central business districts.

The combination of structur-al adjustment, rapid urbanization, weak municipal planning and ser-vices, and distinct slum economies has created conditions for radical changes in the formal private sector – and hence, a new source of finance for housing and urban infrastruc-ture. The banking sector and private utility companies are two important examples of finance. The flip side of structural adjustment has been that banks have grown in number with the advent of market liberalization, privatization and related financial sector reforms.

While many banks have confined lending to traditional, higher-in-come markets, others have diversi-fied lending to reach rapidly growing

urban populations, building upon prec-edents set in slums by entrepreneurs and urban poor organizations. Innovation of this kind has been accelerated by compe-tition among banks for traditional, high-er-income markets, the lucrative business of microfinance, and downward pressure on interest rates. Primary mortgage in-stitutions have also emerged especially in countries with established domestic capital markets that can subscribe to debt instru-ments as a source of long-term financing so essential for housing finance.

For private service providers, structural adjustment has had unanticipated conse-quences in countries with rapidly expand-ing urban populations. Privatized utility companies see in slums a large, untapped market—a population of slum dwellers who pay more per unit cost of service than higher income households. By working with entrepreneurs and urban poor orga-nizations, private utilities are developing innovative systems to extend their services to slum dwellers and the urban poor.

The shift from public to private sourc-es of finance for housing and urban infra-structure in cities of Africa, Asia and Latin

Financing for the urban poorThe way housing and urban infrastructure are financed is a topic of renewed debate and a source of creative innovation, write Chris Williams, Political Advisor, and Nicholas You, Special Advisor on Policy and Strategic Planning, both in the Office of the Executive Director at UN-HABITAT. Here they examine financing in Africa, Asia and Latin America, where the demand for shelter and basic services far outstrips supply, and where most urban populations live in slums.

Paragraph 47 of the Habitat Agenda commits member states to:“… strengthening existing financial mechanisms and, where appropriate, developing innovative approaches for financing the implementation of the Habitat Agenda, which will mobilize additional resources from various sources of finance – public, private, multilateral and bilateral – at the international, regional, national and local levels, and which will promote the efficient, effective and accountable allocation and management of resources, recognizing that local institutions involved in micro‑credit may hold the most potential for housing the poor.”

Commitments on shelter finance, Habitat Agenda, 1996

�Habitat Debate March 2007 OVERVIEW

America would suggest that governments no longer have a significant role to play in financing human settlements devel-opment. On the contrary, the role of the State has never been more pertinent. Only government policy, public investment and municipal planning can ensure financial sector reforms that translate into private investment in affordable housing and ba-sic services.

Government legislation on pension funds, for example, can create a source of long-term capital and trigger institutional investment in debt instruments to finance municipal infrastructure and/or mort-gage facilities. Targeted public investment is also crucial. It is estimated that 30 per-cent of the cost of home construction is made up of expenditure in water and san-itation. By dedicating public expenditure to infrastructure, the State can spur mas-sive private investment in housing—a vol-ume of shelter hundreds of times greater than could be constructed by government funds. Municipal planning is a pre-requi-site for mainstreaming private investment, particularly approaches to planning that build upon, rather than exclude the dyna-mism of the slum economy and the inte-gral role it plays in urban development.

The change in the way affordable hous-ing and urban infrastructure is financed at country level has significant implications for development cooperation. Official de-

Paragraph 48 of the Habitat Agenda commits member states to:(a) [Stimulating] national and local economies through promoting economic development, social development

and environmental protection that will attract domestic and international financial resources and private investment, generate employment and increase revenues, providing a stronger financial base to support adequate shelter and sustainable human settlements development.

(b) [Strengthening] fiscal and financial management capacity at all levels, so as to fully develop the sources of revenue.

(c) [Enhancing] public revenue through the use, as appropriate, of fiscal instruments that are conducive to environmentally sound practices in order to promote direct support for sustainable human settlements development.

(d) [Strengthening] regulatory and legal frameworks to enable markets to work, overcome market failure and facilitate independent initiative and creativity, as well as to promote socially and environmentally responsible corporate investment and reinvestment in, and in partnership with, local communities and to encourage a wide range of other partnerships to finance shelter and human settlements development.

(e) [Promoting] equal access to credit for all people.(f ) [Adopting], where appropriate, transparent, timely, predictable and performance based mechanisms for the

allocation of resources among different levels of government and various actors.(g) [Fostering] the accessibility of the market for those who are less organized and informed or otherwise

excluded from participation by providing subsidies, where appropriate, and promoting appropriate credit mechanisms and other instruments to address their needs.

velopment assistance will never finance the massive housing and service deficit in cit-ies in Africa, Asia and Latin America, nor should it.

The accumulated savings and purchasing power of urban poor and the capital housed in pension funds and among private inves-tors as well as dedicated public investment constitute sources of finance that make offi-cial development aid pale by comparison.

The future of development cooperation is to channel funds in ways that accelerate the actions of local actors to harness these sources of finance. This includes a combi-nation of targeted technical assistance and credit enhancements, equity investments, and bridging finance that preferably can build local capacity and leverage multiple sources of finance.

It also involves creative partnerships be-tween multilateral and bilateral develop-ment agencies and international finance institutions geared toward fast-tracking in-vestment for infrastructure.

More fundamentally, development co-operation will require coming to terms with the social and economic consequenc-es of rapid urbanization and addressing ur-ban poverty by drawing on the potential of innovations in financing.

Newly completed houses, self-build housing project Jinja, Uganda 2005. Photo: © Suzi Mutter

� Habitat Debate March 2007FORUM

According to UN-HABITAT, slums represent one-third of the world's ur-

ban population. This ratio is not going down in spite of all political declarations and official commitments. Why? Why do slums exist? Are they a planning mistake? Do they reflect the inefficiency or mal-functioning of land markets?

Let’s think for a second why we have so many slums and shanty towns. Of course, we know: slums are the best way found by many countries to provide cheap housing to the urban poor. And cheap housing means a cheap labour force, low-income workers. Slums are the physical expression and con-dition of urban poverty: in many countries they are necessary to ensure profitable eco-nomic growth!

Before being a problem, slums are there-fore a solution at a particular stage of eco-nomic development. They were a solution in Victorian London as they are a solution in Mumbai today. Slums are not a market fail-ure, they are a market success. This is the first thing we should know about slums: they are economically useful, sometimes extremely use‑ful, because they offer low‑cost housing options to the poor.

But all informal settlements are not equal-ly squalid. In Latin America, Southeast Asia, Sub-Saharan Africa, and the Indian sub-con-tinent, slums are very different, particularly in terms of overcrowding.

Some are built on public land, some on private land, some are squatter settlements, and others provide rental housing options. Some areas are extremely dense (3 people or more sharing a small bedroom and more than 1,000 persons per ha). For instance in South Asia, 150 million people live in over-crowded units. In West Africa on the other hand, most slums have relatively low densi-ties (less than 500 persons per ha).

The degree of shelter deprivation is di-rectly correlated to the degree of urban in-equities. Thus the worst slums are found in the most inequitable cities. These are cities where the poor pay more than the rich for land and urban services, where land is mo-nopolized by the upper classes, the cities that are physically divided into poor areas and gated communities.

The existence of slums is always a re-flection of urban poverty but the intensity of shelter deprivation is usually a reflection

of urban inequity. For example, Nairobi is richer than Kinshasa but more than 50 per-cent of its population lives in slums - the same percentage as in Kinshasa. Nairobi’s slums are worse than those of Kinshasa, be-cause Nairobi is more inequitable than the Congolese capital. Nairobi’s poor slum dwellers are squeezed into only 5 percent of the total city area. The largest slum, Kibera occupies less than 1 percent of the city area and accommodates 20 percent of the city population. Its density reaches 3,000 per-sons per ha. This is the second thing we should know about slums: they are a manifes‑tation of social injustice, a reflection of a social divide which excludes the poor from the bene‑fits of urban life.

But the urban poor are not only victims, they are also actors. In fact slums and in-formal settlements demonstrate everyday how the urban poor fight for survival, how they innovate, how they find resources and energy, how they create their own employ-ment opportunities and transform their environment.

In some cities they form com-munity groups to defend their interests. Slum-dwellers may be the most dynam-ic “entrepreneurs” of our time – the real “Private Sector” about which we talk so much. Good at survival strategies, slum peo-ple rarely reach the accumulation and devel-opment stage. They need support, or at least they need to be left alone, away from public harassment.

Slum life shows that the concentration of people in cities is in itself a positive de-velopment factor, simply because concentra-tion means more exchange, more markets, more opportunities, and more risks. This is the third thing we should know about slums: they are a manifestation of human resilience, a reflection of social dynamics, of fantastic hu‑man energy. Sometimes they are places of solidarity, often they are places of urban vi-olence, always they are places of urban life, of multiple struggles for survival and human dignity.

From these three points, we can derive a few basic principles for the reduction of ur-ban poverty. Firstly, the absolute necessity to adopt a holistic approach to address urban development challenges. This means bring-ing together policy makers from economy and finance ministries with housing and lo-

cal government departments, to ensure that the key contribution of urbanisation to eco-nomic development is well understood, that resources are properly mobilized and allocat-ed, that employment policies are associated with slum upgrading policies. In a word this means advocacy campaigns to strengthen or create enough political will at all levels.

Much remains to be done. Only a few governments have a comprehensive slum up-grading strategy, national targets are rarely es-tablished and the Millennium Development Goals are largely ignored. We should pop-ularize success stories demonstrating that good policies bring economic and social advantages.

The second principle is affirmative ac‑tion to secure the urban poor access to land, housing, credit and basic services. This means identifying urban inequities in these areas and correcting them. The poor should pay less, not more, than the wealthy for the comparative benefits of city life. Inequity should be replaced by solidarity, the divided city by the inclusive city. Of course political will is required but technical solutions are available, they have been tested, they work.

The third principle – participatory and transparent governance – is the means to de-liver on any dimension of urban development, on the three components of sustainable de-velopment (economic, social and ecological). Efficiency in municipal finance (resource mo-bilization and allocation) constitutes one of the best indicators of good urban governance. Since the Istanbul City Summit of 1996 this third principle is widely accepted in the inter-national arena. But it needs to be implemented more systematically at country level.

Indeed, a number of governments have adopted reasonable and effective urban poli-cies in the last 10 years. South Africa, Brazil, Mexico, Egypt, and China come to mind.

In the meantime, international assistance to urban development has remained stagnant, but this has had little impact on these large middle-income economies which can work on their own. The urban crisis is now concentrating on the Least Developed Countries which are ur-banizing rapidly without sufficient institution-al resources. These countries should be the top priority of the UN system.

Three things we should know about slumsSlums are economically useful, a reflection of the urban social divide, and a bedrock of human resilience. And writes Daniel Biau, Director of UN-HABITAT’s Regional and Technical Cooperation Division, they are not a market failure, but a market success…

�Habitat Debate March 2007 FORUM

Employer-provided housing played a major role in accommodating the

work force in European cities as a result of the industrial revolution. It was aimed at improving the productivity of employ-ees because employers realized that well housed employees were healthier, better rested and more disciplined – all of which enhanced labour productivity.

Employers also provided housing that was predominantly rental, hence, rent was deducted from salaries. The availabil-ity of land close to factories was an add-ed opportunity for workers to live nearby. In addition, some governments provid-ed increased fiscal incentives by allowing high rates of depreciation on housing in-vestments which made housing produc-tion even more attractive and profitable to companies.

In the post-war period, companies provided low-interest, long-term hous-ing loans for workers to buy or build their own homes, or to buy the homes they were renting, an approach often referred to as employer-assisted housing.

Governments in Western Europe also invented a whole range of housing pol-icies focusing on income tax relief for prospective home owners, for housing co-operatives, and subsidies for developers of social housing. Although these poli-cies seem to have responded to the hous-ing crisis in Western Europe since the mid 1970s, their success was also a function of increased incomes.

In the United States, employer-assisted housing became a well-known practice at the beginning of the 1990s when relative-

ly high economic growth in some regions resulted in a shortage of labor owing to a general shortage of housing combined with high housing costs. Employers decid-ed to provide assistance to their employees by helping homeowners with down-pay-ments and closing costs. Employers also partnered with housing finance com-panies as guarantors which essentially reduced mortgage costs. For renters, sup-port was provided in the form of initial deposits or a monthly fixed contribution towards rent payment.

Efforts towards employer-assisted housing resulted in the Housing America’s Workforce Act 2005. It provides incen-tives to increase private sector investment in housing through tax credits to employ-ers who contributed towards employee’s home purchase, as well as rental assis-tance. Housing assistance is also regarded as a non-taxable benefit, similar to health, dental and life insurance.

In developing countries, housing fi-nance is severely constrained because of prevailing or perceived high default risk. These risks limit lending to high-in-come groups and also increase mortgage costs considerably. With financial lib-eralization, housing finance institutions are increasingly resorting to the employ-er-employee contractual relationship, and using security of tenure as a form of risk reduction as well as a source of guarantee for loans. Lenders view the relationship between employer and employee as the collateral to ensure loan repayment.

This approach still occurring on an ad hoc basis could have a better impact

if approached in a more comprehensive and systematic manner. The government should support the mainstreaming of this approach by developing specific tax in-centives for the employer.

The concept can also be applied to slums. In Kenya, for instance, in the Kibera slum, approximately 20-30 per-cent of the slum dwellers have regular formal sector employment. Such an ap-proach could provide an alternative sup-ply of housing, reduce the rate of growth and overcrowding in slums, while provid-ing low-income earners with an opportu-nity to own a tangible asset.

This can only be achieved if the gov-ernment takes up that important task of adopting appropriate housing policies and legislation, and fiscal measures to en-courage employers to help their employ-ees finance their housing.

Lessons from developed countries in-dicate the important role played by em-ployer provided and employer assisted housing. These lessons can prove to be significant in the growth of affordable housing finance in developing countries. Its wider application, that is, in order to reach the low-income groups including slum dwellers is only possible if govern-ment adopts a more holistic approach to housing and urban development, rather than the current piece-meal application of sectoral policies that fail to reconcile busi-ness and economic development with the welfare and productivity of people, and their housing needs in particular.

Employer provided housing financeThe widespread proliferation of slums affecting many developing country cities is not a new phenomenon in economic and social history. The late 19th and early 20th century saw great social change in the U.K. and Continental Europe caused by unbearable living conditions, especially among the industrial workforce. Guenter Karl, a UN-HABITAT expert, and Margaret Gachuru, a lecturer at the University of Nairobi, say a major factor that contributed to the better housing was the role played by employers.

Housing in Sheikh, Somalia . Photo: © UN-Habitat

� Habitat Debate March 2007FORUM

Gender and microfinance: one step forward, two steps back?Microfinance is widely regarded as a ‘magic bullet’ capable of resolving an array of development problems including poverty, gender inequality as well as financing development from the bottom-up, writes Kavita Datta, a lecturer in the Department of Geography, Queen Mary, University of London. Yet, while a focus on women has often been interpreted as illustrating the capacity of microfinance programmes to promote women’s empowerment, it is important not to conflate the two.

Such is the popularity of microfinance, that 2005 was named the UN Year of

Microfinance, while the founder of the Grameen Bank, Professor Mohammed Yunus, was awarded the Nobel Prize in 2006. Perhaps unsurprisingly then, a di-verse range of organisations are involved in these programmes including international financial institutions, bi-lateral donor agen-cies, national governments, civil society, banks and other financial organisations.

In turn, women have emerged as key targets of microfinance programmes. In their 2002 report for UNIFEM, Empowering women through microfinance, Susy Cheston, Senior Vice President of Policy and Research for Opportunity International and Executive Director Emeritus of the Women’s’ Opportunity Fund, and Lisa Kuhn, Program Analyst for Opportunity International, note that women’s access to microfinance has in-creased substantially over the last ten years. As such, women account for nearly 14.2 million (or 74 percent) of the 19.3 million poor people being served by microfinance institutions. Yet, while a focus on women has often been interpreted as illustrating the capacity of microfinance programmes to promote gender equality and wom-en’s empowerment, it is important not to conflate the two, says Susan Johnson in an article in the European Journal of Development Research in 2005. Even while microfinance programmes target women explicitly, they do so for a variety of rea-sons reflecting quite diverse understand-ings of gender and resulting in a variety of gender outcomes, including potentially the disempowerment of women.

Linda Mayoux, in her work, Women’s empowerment through sustainable micro‑finance: rethinking ‘best practice’ (2005), identifies three different approaches to mi-crofinance even while acknowledging that there are considerable over-laps between them. They are the financial self-sustain-ability, poverty alleviation and feminist empowerment paradigms.

Taking these in turn, the financial sus-tainability model is essentially premised

upon a liberal perspective that gender in-equalities are harmful for economic growth and development. Proponents argue that increasing women’s access to financial re-sources has two inter-related positive im-pacts: it enhances women’s productivity and the overall economic development of communities and countries in the Global South. The efficiency and sustainability of programmes which target women also un-derwrite the interest in extending financial services to them. Research indicates that schemes which target women have poten-tially higher repayment rates.

As such, one could argue that this ap-proach essentially focuses on women due to an interest in economic growth, finan-cial sustainability and efficiency, and is driven by what women can do for micro-finance and development rather than the other way around.

The poverty alleviation approach is based upon a consensus that meanings, experienc-es and processes of poverty are fundamentally gendered. The 1995 UN Human Development Report estimated that 70 percent of the world’s 1.3 billion poor were women and led to the coining of the phrase the feminisation of poverty. Widely popularised by subsequent internation-al women’s conferences, the prevalence of pov-erty among women informs the Millennium Development Goals which centred upon the need to eradicate poverty.

While more recent research has identi-fied key deficiencies in the feminisation of poverty thesis, the aim of microfinance to extend financial services to the poor means that a focus on women is justified on the grounds that it can reduce their vulnerabil-ity to poverty. At the same time, women’s greater investment in the household which

is partly attributable to a ‘feminisation of responsibility and obligation’ (Sylvia Chant 2006) also means that targeting women has potentially beneficial impacts upon their dependents and households.

Arguably, the focus on women here is also related to wider concerns about pov-erty rather than women or gender relations per se. As Ms. Johnson argues, gender rela-tions determine the effects that loans have on women, some of which may work in favour of women while others may not. Furthermore, neo-liberal restructuring means that women’s responsibilities and duties within and beyond the household have intensified, adversely affecting their health.

Finally, and perhaps most significantly, the feminist empowerment paradigm ex-plicitly views microfinance as an effective entry point to achieving gender equality and women’s empowerment. This view-point is supported by the Convention on the Elimination of Discrimination Against Women (CEDAW) and the Beijing Platform for Action (BPFA). It is also firmly rooted in initiatives located in the Global South including the Self Employed Women’s Association in India with pro-grammes attempting to address both mac-ro- and micro-level obstacles to gender empowerment.

But the challenge remains of how eco-nomic empowerment can be linked to wider social and political empowerment, and whether ironically, increasingly wom-en’s access to economic resources endan-gers their existing networks while also taking them away from other social and political activities.

As such, significant challenges remain in realising the potential of microfinance to promote greater gender equality and empowerment. There must be a renewed initiative to move away from simply tar-geting women to explicitly focusing on gender roles, relations and empowerment which must be the starting point of all interventions.

The aim of microfinance to extend financial services to the poor means that a focus on women is justified on the grounds that it can reduce

their vulnerability to poverty.

�Habitat Debate March 2007 FORUM

Figure 1: ‘Objective’ Based vs. Traditional Approach to LED

Promoting inclusive and effective local economic development - A strategic planning approachThe prosperity and welfare of cities depend on their ability to exploit sustainable economic development and to minimise the problems associated with global economic integration and urban growth. This makes strategic thinking and planning for Local Economic Development (LED) crucial write UN-HABITAT Human Settlements Officer Gulelat Kebede and William Trousdale, President of EcoPlan International in Canada.

Sound economic development strategies constitute one of the key pillars of sus-

tainable local development. One reason for the recent gains in pop-

ularity of Local Economic Development is the fact that it is evolving past the tra-ditional economic development model that focused almost exclusively on promotion, attracting investment and strengthening of physical infrastructure.

It is emerging as a new model that in-tegrates economic, social and environmen-tal objectives; a system where all types of community capital (human, social, cultur-al physical, economic, and natural) are in-cluded and strengthened. It is a process that integrates the soft infrastructure, such as local business and entrepreneurial sup-port, leadership, partnerships, networks, capacity building and innovation with the hard infrastructure – buildings, commu-nications and transportation. It takes into account the role of natural capital that sup-ports economic activity – resources, ecosys-tem services (e.g., clean water, flood control from wetlands and forests) and other envi-ronmental values.

It places a stronger focus on the ba-sic conditions required for development, the comparative advantages of an area, and the economic needs of local citizens and businesses. Key aspects include a thor-ough understanding of the economic fab-ric of a local area and the key forces for its improvement.

LED is now defined as a participatory process in which local people work togeth-er to stimulate local commercial activity,

resulting in a resilient and sustainable econ-omy. It helps create jobs and improve the quality of life for everyone, including the poor and marginalized. Local economic de-velopment encourages the public, private and civil-society sectors to establish part-nerships and collaboratively find local solu-tions to common economic problems.

Its strategies embrace local values for poverty reduction, basic human needs, lo-cal jobs, social and environmental integra-tion; it utilizes economic drivers forged in value-added resource use, local skills train-ing, retention of income, regional cooper-ation; and it considers development in the role of structural change, and the quality of development.

Traditional approaches that are not stra-tegic generally rely on identifying problems and then choosing solutions that address those problems. When issues are used to elucidate ‘community objectives’ as a key step driving the new development, two es-sential outcomes result: more creative al-ternatives are developed that have a greater chance of consensus-based, broadly sup-ported and workable solutions; and sus-tainable, systemic and long-lasting change is achieved, as opposed to quick fixes.

The engagement of stakeholders is es-sential to develop community objectives. A process centred on properly defined com-munity objectives ensures that the activities taken under the aegis of LED are founded on community values.

For LED to succeed, there are a num-ber of conditions which need to be met. Local commitment, especially that of the

political leadership is critical. Bringing in the right people and resources requires a lo-cal champion. Appropriate tools for infor-mation gathering, assessment and analysis should be carefully selected and calibrated to ensure that important aspects of the local economy are covered, and understood.

In the context of many developing countries, for example, the role of the in-formal economy is so crucial, its inclusion is a must. Like all planning exercises, stra-tegic planning is worthless unless translat-ed to implementation. The LED process is meant to be action oriented. Often there is “hanging-fruit” to be reaped with less challenging or controversial interventions, and these could provide a stepping stone to move to the more complex and demanding ones as well as providing the necessary vis-ible results to keep stakeholders and citi-zens engaged.

There are significant economic develop-ment opportunities to be gained by cutting red tape, removing barriers to business and the informal sector and creating account-able and transparent governance structure, and generally by addressing market and government failures.

Creating this business-enabling envi-ronment is as important for local entrepre-neurs as it is for outside investors. The LED strategic planning from this perspective is both a framework and catalyst for action. Ultimately, the measure of success in LED revolves around focus, innovation, and im-plementation, and its impact on the lives of the citizens, including the poor and the marginalized.

10 Habitat Debate March 2007FORUM

Microfinance for the world’s poorest people The world’s urban population is expected to increase dramatically by over 800 million households between 2005 and 2030. In effect, this implies an average daily increase of 100,000 households in urban areas. This article was prepared on the basis of UN-HABITAT’s 2005 Global Report on Human Settlements entitled ‘Financing Urban Shelter’.

Cities around the world, especially those in developing countries where

the bulk of urban growth will occur in coming decades, are faced with the un-precedented challenge of providing ade-quate shelter for their inhabitants.

Shelter has become a commodity for increasing numbers of low income ur-ban households, especially those in urban areas of developing countries. Yet these households, which rely mainly on income from the informal economy, cannot bor-row money easily from the formal financial sector. This remains a key obstacle to the improvement of shelter conditions and ul-timately poverty reduction in urban areas.

Low income households are not an at-tractive clientele for formal sector institu-tions that provide shelter finance primarily because they have limited assets and can only build their homes in stages.

Indeed, an estimated 70 percent of housing investment in developing coun-tries occurs through such progressive build-ing. Yet, incremental shelter investment is not favoured by formal finance institutions due to the risks associated with the build-ing processes.

The formal financial institutions do not make a profit out of low income house-holds, which in turn do not have the collat-eral required to get a loan. Thus, a majority of low income households finance their shelter investments through their own sav-ings or informal credit from various sources (relatives, friends, money lenders).

The realisation that hundreds of millions of low income urban households remain largely excluded from borrowing, has therefore led to the exploration of innovative finance mecha-nisms. In particular, shelter microfinance and

community funds have grown considerably in recent decades, through multiple explora-tions and innovations predominantly in Asia and Latin America.

Shelter microfinance programmes pro-vide small-scale lending to individuals for housing investments (constructions, im-provements and extensions). Community funds are provided by institutions to groups or community organisations for collective housing construction or development of land, infrastructure or services.

Both approaches are better designed to help poor urban households address their shelter needs because they involve small-scale lending suitable to incremental shelter investment strategies common among low income households.

There is also a growing trend of combin-ing loan provision through shelter micro-finance and community fund programmes with more comprehensive neighbour-hood improvement and poverty reduction initiatives such as settlement upgrading (infrastructure and services), land develop-ment and enterprise lending. Community funds are particularly appropriate for slum upgrading.

However, in their efforts to target low income households, both approaches are faced with two particular challenges. The first involves the risk of excluding the poor-est households from being able to get loans. Shelter microfinance programmes often target the higher income urban poor such as those with formal employment or diver-sified livelihood strategies. In the case of community fund mechanisms, the poor-est households, most of which rely on daily savings, may not be able to contribute to-wards group or community savings, there-

by facing exclusion.Tenants without secure tenure rights

and women are also at risk of being de-nied loans through community funds. Moreover, community funds require rela-tively stable communities which may not be the case for the poorest neighbourhoods of many urban areas.

Institutions involved in shelter micro-finance, for their part, also have difficulty in securing sufficient loan capital, there-by curbing their outreach. Longer loan re-payment terms create greater term risk for shelter microfinance providers. Shelter mi-crofinance agencies also find it difficult to set low interest rates and small loan sizes that weigh the borrower’s demands against their own financial needs. Similarly, com-munity fund programmes often struggle to secure subsidies from state funds, NGOs and international development agencies, without which they are unable to maintain low interest rates.

Despite this, shelter microfinance and community funds strategies flourish and more agencies are becoming involved, in-cluding municipal and central government agencies as well as private sector agencies not previously engaged.

There is an urgent need to increase the scale of operations of shelter microfinance and community fund operations. Scale and sustainability can be realised through concerted efforts of financial institutions, governments and donors. It is particularly important that governments encourage the expansion of microfinance and communi-ty fund lending for shelter investments by creating the necessary legal and regulatory environment.

Poverty reduction strategy papersWhile the dire shortage of affordable housing has been recognized internationally as a deep and pervasive problem, strat-egies to address this have not been thoroughly addressed in existing mechanisms, such as poverty reduction strategy pa-pers (PRSPs).These are documents that the International Monetary Fund (IMF) and the World Bank require from national governments detailing their plans to reduce poverty in order to qualify for debt relief under the Heavily Indebted Poor Countries (HIPC) initiative. Out of the 54 countries with PRSPs or interim PRSPs, many of them address housing, but with varying degrees of commitment or specificity with regard to resource requirements. Many of the PRSPs discuss housing as a problem and some have conducted surveys to identify housing needs more exactly. Some countries propose build-ing a few hundred or few thousand units, while others propose public–private partnerships and land reform measures. However, it is disappointing that many do not include clear measurable goals or budget information.

11Habitat Debate March 2007

OPINION

The African continent, particularly sub-Saharan Africa, is characterised

by the enormous differentiation in the economies of South Africa and the rest of the continent. This is also evident in the housing market and developments in housing finance and delivery.

The housing market is very well de-veloped in South Africa, despite severe challenges in the low-income housing market.

However, the market is not well de-veloped in most other parts of Africa, with the exception of Ghana where there is a developing mortgage mar-ket. Other parts of Africa are still de-veloping policies and mechanisms for housing delivery, with a virtually non-existent mortgage market.

The South African government is also very active in housing delivery and has developed a mass of policies to en-able particularly low-income housing delivery.

South Africa The mortgage market in South Africa

is dominated by the banking sector, which is responsible for more than 90 percent of mortgage lending. Mortgage advances in South Africa grew by 29.6 percent year-on-year in September 2006. The total of mortgage advanc-es as at September 2006 was R640.4bn ($91.5bn). The critical challenge for South Africa is the existence of a dual market.

The bulk of the mortgage advances are in a very well developed middle to upper income market. A significant part of the population is in the lower-income market, and this sector experiences chal-lenges in housing delivery.

The critical challenge is for those in the monthly income category between R1,500 and R7,900. There are issues of affordability, supply and product in this market. Construction costs have in-creased significantly in South Africa, as in most parts of the world, and this is ex-acerbated by severe holding costs for de-velopers as a result of delays at municipal level in the processing of registrations and provision of bulk infrastructure.

The affordability issue is critical in a context of rising interest rates. A house-hold earning R3,500 per month only has a cushion of about R120 after basic household costs. A 2 percent increase in rates would make the mortgage payment unaffordable. The prohibitive holding costs have resulted in developers exiting the low-income housing market, thus leading to a lack of supply.

The country needs about 160,000 houses in the low-income market per year to make an impact on the back-log, but is constructing about 19,000 per year.

These are some of the challenges that South Africa faces.

However, there is a very healthy en-gagement between government, its agencies and the banking sector to try to address these challenges. The South African government has been exem-plary in its efforts to raise the issue of low-income housing to the top of the agenda in the country. The government has instituted a capital subsidy scheme that has benefited 2.9 million benefi-ciaries since 1994.

Subsidy-linked housing delivery has reached about 2.2 million people since 1994. The government is also engag-ing the banking sector to develop risk mitigation and sharing mechanisms to enable the sector to lend to lower in-come people. The banking sector and government are also engaging the con-struction sector to begin to address the supply issues. And the banking sector is engaging municipal government to address the capacity constraints in that level of government on land registra-tion, bulk infrastructure and other rel-evant matters.

The banking sector has been active in the area of low-income housing. It has done mortgage lending of about R17bn in the 2005 calendar year to the R1,500- R7,500 per month income category.

The South African government es-tablished a wholesale financing facili-ty called the National Housing Finance Corporation in 1996. Its mandate is to provide wholesale finance to retail

housing intermediaries servicing the low-income market. The coporation has approved R2.3bn in finance and has disbursed about R1.9bn since its incep-tion. This has resulted in 1.1 million people getting access to shelter.

The South African government also established an initiative called the People’s Housing Process. It brings peo-ple together in groups and enhances the government subsidy by organising people to contribute “sweat equity” by building their own homes.

There are significant developments in inner city housing development in South Africa. The government has in-troduced an Urban Development Zone tax incentive scheme. About 100 com-panies have registered to access it, with a total investment in inner city regener-ation, particularly in housing, of about R1.5bn.

East Africa A current initiative in East Africa is

an example of the positive results of re-gional cooperation on the continent. Kenya, Uganda and Tanzania have co-operated to undertake a major housing project to address a shortfall of about 3.8 million units in the region.

The 20-year project will eventual-ly lead to the development of about 28 million units. The East African Development Bank (EADB) is expect-ed to raise $120m in the next two years for the project. It will expect the three countries to raise $20m each in the next two years for seed capital. The balance will be raised from the private sector in the region and offshore investors will be invited to subscribe to half of the cap-ital needs.

The East African Development Bank estimates the region will need to invest some $12bn over the next 20 years to keep pace with demand. The project is a good start to meeting this need and will go some way towards addressing the severe problems of informal settle-ments in the region.

Home-financing in Africa One of Africa’s biggest challenges is home delivery. But except for South Africa, Ghana and a handful of East African countries, Cas Coovadia, Managing Director of the Banking Association of South Africa, says the home-financing sector in the rest of Africa remains in its infancy. In an article first published in The Banker, he highlights the good examples set by those countries leading the way.

1� Habitat Debate March 2007SPECIAL REPORT

Financing for urban development in the Asia-PacificWorld Development Indicators show that East Asia and the Pacific, and the South Asia sub-regions account for 864 and 1,064 million people, respectively, living on less than $2 a day. This article is derived from a special paper prepared for first Asia-Pacific Ministerial Conference on Housing and Urban Development (APMCHUD) 13-16 December, 2006, in New Delhi by experts of UN-HABITAT’s Human Settlements Financing Division.

A large proportion of the popula-tion in Asian countries is vulnera-

ble to internal and external economic shocks such as the Asian financial crisis of 1997. In addition, widening income inequalities are likely to create social un-rest, which need to be addressed with-out delay.

Based on lessons from 1997 and buoyed by the sustained econom-ic growth, many governments in the re-gion are building social safety nets, and undertaking massive urban investments. Similarly, the private sector is making an attempt to create business solutions that provide affordable services to the urban poor. The conditions for improving the quality of life for the majority of the poor by the 2020 Millennium Development Goals deadline set by world leaders are positive, if urgent action is taken.

Civil Society more demanding Today many believe it is their right to

demand a better quality of life. Given the structure of the economies of the coun-tries in the region and integration with world markets, Asian cities will have to be competitive on a global scale both in terms of quality and cost efficiency of ur-ban management. There is also signifi-cant pressure to create Asian world class cities. This augurs well for creating sus-tainable urban centres.

Community mobilisation Community and civil society move-

ments in the region are relatively strong, and slowly gaining ground as a result of efforts by NGOs such as Slum Dwellers International and the Asian Coalition of Human Rights. The community-led de-velopment processes are being promot-ed by many countries such as Thailand, the Philippines, Sri Lanka, India, Pakistan, Nepal, Cambodia, Indonesia, etc. However, in many other countries, community movements and community-led development processes are weak. This must change.

The region is also very strong in co-operative movements as well as having a savings culture. Many governments have encouraged community mobilisation, savings and cooperative movements. The Philippines, Thailand, Cambodia, Sri Lanka, India, and Indonesia, to cite some, have developed pro-poor urban develop-ment strategies. This is a vital strength for many countries in the region.

Bankability of CitiesSince the early 1990s, political decen-

tralisation has gradually gained ground in the Asia-Pacific, and is relatively strong in China, The Philippines, Indonesia and India. However, with few exceptions, many of the cities in the region manifest the paradox of rich citizens and poor city governments. City governments do not have the financial strength to meet the

requirements of even moderate invest-ments in services.

The institutional arrangements for ser-vice delivery are also fragmented – most of the local services are provided by na-tional level or parastatal utilities - depriv-ing the city governments a role in service delivery. Slum prevention requires that cities are equipped to plan and finance land development and service delivery that is affordable and efficient.

Despite this, many cities in China are creating world class infrastructure to pro-mote economic growth. Similarly, coun-tries such as India, The Philippines and Indonesia have supported local gov-ernment reforms related to better ac-countability, creditworthiness and own revenues. They are also introducing in-centive funds to promote reforms, stream-lining of inter-governmental transfers, encouraging market based investments, and, creating of municipal bond mar-kets. Many countries also initiated e-gov-ernance reforms to improve the quality of governance – thus helping to create value for money in public finance and helping to improve quality of service delivery.

Housing Finance SystemsHousing remains one of the most

pressing issues in the Asia-Pacific. A lack of infrastructure and long commuting distances exacerbate the problems. Public transport systems remain one of least de-veloped infrastructure systems in many

Enhanced fiscal capacity of local governments is the capacity to do development work at a large scale. It is essential that cities are made to work for all citizens –equitably and efficiently. There are several actions important in the immediate phase that include:

n Fiscal decentralisation aimed at improving own revenue base of cities;n Promoting land based revenue measures such as impact fees and valorisation charges to finance major infrastruc-

ture such as public transport;n Empowering cities to undertake land development with a pro-poor focus;n Enhancing the quantity and predictability of inter-governmental transfers, with special attention on output based

aid and incentives for reform;n Promoting credit rating of local governments;n Rule and market based municipal borrowing frameworks; andn Promoting efficiency in public expenditure.

Source: UN-HABITAT

1�Habitat Debate March 2007 SPECIAL REPORT

of the cities in the developing countries leading to very high commuting costs.

In Asia, according to UN-HABITAT’s State of the World’s Cities 2006—7 re-port, 73 per cent, of urban dwellers live in non-permanent housing. Over half of the world’s inadequate housing units are located in Asia-Pacific – at roughly 500 million units. The housing sector is also severely constrained by lack of ade-quate and appropriate housing finance systems. In fact, an Asian Development Bank study says Asia’s mortgage sector is the least developed in the world. In Asia, many countries’ mortgage financing per year is less than 2 per cent of GDP com-pared to 88 per cent in the UK.

Despite this gloomy picture, the re-gion also has excellent innovations in terms of shelter finance practices includ-ing through shelter microfinance and community funds.

Other Financial ServicesThe financial sector in the region is

comparatively well developed and in-tegrated intra-region wise and globally. Many countries have liberalized the fi-nancial markets. The financial sector in countries such as China, South Korea, Malaysia, Singapore, India and Indonesia are thriving. The stock markets in many of the countries are large and well devel-oped. The region is also experiencing sig-nificant growth of the Islamic banking system.

On the downside, many countries in the region have nascent and weak finan-cial markets. The participation of finan-cial markets in financing housing and urban infrastructure has been limited in many of the developing countries of the region. Similarly, the majority of the low-income households are also exclud-ed from the formal financial services in-

dustry – although efforts are being made to develop systems that provide finan-cial services for the poor. And, the State remains the main provider of shelter fi-nance in several Asian countries, such as The Philippines and Bangladesh.

For the last 30 years, and thanks in no small measure to Muhammad Yunus, the Bangladeshi banker and Nobel laureate, Bangladesh leads the way in creating fi-nancial products for the poor. The pen-etration of microfinance into the shelter finance sector is significant in many of the developing countries of the region. Significant efforts are underway to in-tegrate the informal (including microfi-nance) markets with formal ones in many of the countries in the region.

Innovations in capital markets – both formal and informal – present tremen-dous opportunities for introducing fi-nancial instruments for sustainable urbanization.

Urban developmentVery few countries (with the exception

of developed and emerging economies in the region) have housing and urban sec-tor policies for adequate, affordable shel-ter, including related infrastructure. Land ownership and titling is complex and ex-pensive. There are limited subsidies avail-able for housing and infrastructure. The urban sector does not feature highly in many of the national programmes and strategies. There is need for a better fo-cus on housing and urban development in several countries of the region.

Donor support In general, bi-lateral donors (from

within and outside the region) and multi-lateral banks have supported urban devel-opment in many developing countries of the region substantially during last three

Key innovations:

n Promoting affordable housing through provision of service delivery, competitive market development, private sec-tor involvement and cost reduction measures;

n Improved land use planning as well as provision of affordable and adequate public transport systems;n Introduction of smart subsidies for the needy;n Establishment of special purpose vehicles for intermediating market based housing finance and for improving the

management of housing stock;n Introduction of credit bureaus, foreclosure laws, etc;n Establishment of mortgage insurance, credit guarantee facilities and securitisation mechanisms;n Facilitating long term funds for housing and infrastructure;n Deepening of life and non-life insurance products; andn Promoting universal access to comprehensive financial services.

Source: UN-HABITAT

decades. Yet, aid flows to countries ac-count for small proportion of their GDP. The Asia 2015 Conference strongly sup-ported the increasing development as-sistance flows. The conference also recognised the need for strong technical assistance in deepening development in Asia. Future aid is likely to flow to lowest income countries in the region.

RecommendationsThere is a tremendous scope for cross-

learning across the countries of the region. However, many developing coun-tries in the region are also extremely im-poverished. Unless and until structural and fundamental changes in financing are initiated and sustained, the Millennium Development Goals will remain a dream in many of these countries. It is not just a question of initiating few measures, but also a matter of implementing decisions and sustaining them over a long period of time.

History has demonstrated that the success of slum upgrading initia-tives is greatest when community-driv-en. Community movements are gaining ground in the Asia-Pacific region. The en-ergy of the communities needs to be har-nessed to undertake slum upgrading and slum prevention. It is also necessary to promote business solutions that provide services to households at the bottom of the pyramid.

Given the innovations and improved economic growth in the region, there is significant scope for deepening of the housing finance markets and financial services industry, especially for low-to-middle income households in many of the developing countries of the region.

1� Habitat Debate March 2007

OPINION

The Asia-Pacific region is ex-periencing the triple dy-

namics of economic growth, rapid urbanisation and poverty. It accounts for 34 percent of the global urban population and is also home to over 40 percent of the slum populations.

Some major challenges of ur-banization and economic growth in this region are the growing ur-ban-urban divide, deteriorat-ing inner cities, unplanned and haphazard settlements, insuffi-cient urban infrastructure and basic services. The list also in-cludes land and housing shortag-es, environmental degradation, mounting poverty, unemploy-ment and social exclusion.

These problems have to be confronted by effective planning, appropriate strate-gies, action plans and a paradigm of good governance. This will include strategic vi-sion, consensus orientation, the rule of law, participation, equity, efficiency, effec-tiveness, transparency and accountability.

India with its initiatives and economic reforms has been able to achieve a growth rate of 8 percent per annum in the last few years and is now aiming a growth rate of 9 per cent in the next five years.

India has 286 million people living in over 5,000 cities and towns. Over 40 percent of them live in 60 metropolitan urban agglomerations. There are 61.7 million urban people living in slums and squatter settlements today. It is projected that the urban population of the country will grow to 468 million by 2020. This will have a serious impact on housing, civic infrastructure, basic amenities and employment.

Conscious of the issues of slums and poverty, the United Progressive Alliance (UPA) Government in India through the National Common Minimum Programme (NCMP) has committed itself to a com-prehensive approach to urban renewal with emphasis on social housing, inclusive city growth, slum upgrading and devel-opment. The Government has launched the Jawaharlal Nehru National Urban

Renewal Mission to address the problems of slums and civic amenities in an inte-grated manner and has allocated US$12.5 billion for institutional financing.

Considering that reforms in cities are critical for sustainable urban develop-ment, the Mission aims to bring about mandatory reforms both at State and city levels to improve urban governance.

The repeal of the Urban Land Ceiling Act, the Rationalization of Stamp Duty, Amendment to Rent Control Act, Property Tax Reforms, Disclosure laws, and GIS mapping are some of the major reforms. We now have Seven Basic Services to the Poor – Land Tenure, Affordable Shelter, Water, Sanitation, Education, Health and Social. The Mission is a fast-track, de-mand-driven, participatory urban plan-ning and implementation mechanism.

The central Government will give at-tention to planning for sustainable cities and devising macro-economic policies so that resources can flow to the housing and civic infrastructure sectors. Government will also provide a more supportive en-vironment to Street Vendors through a comprehensive policy and a model Act.

However, there are three areas where critical intervention is required for pro-moting sustainable human settlements and sustainable cities in the Asia-Pacific region:

First, the traditional sys-tem of Master Planning of cit-ies based on the Western model of segregation of residential uses from commercial and institu-tional uses has led to social ex-clusion and unequal growth. There has been little planning in this system for the informal sec-tor including vendors, hawkers, construction workers and other vulnerable groups in cities. The Master Plans must be made in-clusive with provision of ade-quate space for housing the poor and informal sector activities.

Second, urban growth, mounting poverty, population concentration, and unplanned spatial activities have exacerbated

the complexities of urban administration. There is lack of institutional and mana-gerial capacities in implementing poverty alleviation and slum upgrading in urban civic bodies. City Governments should be enabled to have the capacities and skills to administer service outsourcing, public-private partnerships for infrastructure de-velopment, effective services delivery and poverty alleviation programmes.

Lastly, we must accept inclusion of the poor as the core in all urban policies and programmes. My Ministry has been em-phasizing the need for inclusive zoning, inclusive planning and inclusive cities and municipalities. I would urge this region to make inclusion the dominant paradigm in all our programmes.

India would be glad to support a “Forum for Inclusive Cities”, which could be a think tank – a bank of best practic-es in inclusive civic development and an agent of change for pro-poor governance and service delivery in cities.

The new Asia-Pacific conference is unique because it provides a platform for advancing the Habitat Agenda. It ena-bles Asia-Pacific countries to speak with one voice during regional and interna-tional meetings like World Urban Forum, the UN¬-HABITAT Governing Council and meetings of the Commission on Sustainable Development.

Economic growth, rapid urbanisation and povertyIn today’s fast developing and urbanising world, cities are integral contributors to economic growth. But says Kumari Selja, India’s Minister of State for Housing and Urban poverty Alleviation, we are also witnessing the negative consequences of this urbanisation such as slum growth, housing and civic infrastructure shortfalls. Here in a summary of remarks to the first Asia-Pacific Ministerial Conference on Housing and Urban Development she warns of the consequences of rising poverty.

The author, Kumari Selja, with Mrs. Tibaijuka, and President Abdul Kalam of India at the first Asia-Pacific Ministerial Conference on Housing and Urban Development in Delhi in December 2006. Photo: © UN-Habitat/N.Kihara

1�Habitat Debate March 2007

OPINION

By giving us this prize, the Norwegian Nobel Committee has given impor-

tant support to the proposition that peace is inextricably linked to poverty. Poverty is a threat to peace.

The World’s income distribution gives a very telling story. Ninety-four percent of the world income goes to 40 percent of the population while sixty percent of people live on only 6 per cent of world income. Half of the world population lives on two dollars a day. Over one billion people live on less than a dollar a day. This is no for-mula for peace.

The new millennium began with a great global dream. World leaders gathered at the United Nations in 2000 and adopt-ed, among others, a historic goal to reduce poverty by half by 2015. Never in human history had such a bold goal been adopted by the entire world in one voice, one that specified time and size.

Poverty is the denial of all human rights

Peace should be understood in a human way − in a broad social, political and eco-nomic way. Peace is threatened by unjust economic, social and political order, ab-sence of democracy, environmental degra-dation and absence of human rights.

Poverty is the absence of all human rights. The frustrations, hostility and anger gener-ated by abject poverty cannot sustain peace in any society. For building stable peace we must find ways to provide opportunities for people to live decent lives.

The creation of opportunities for the ma-jority of people − the poor − is at the heart of the work that we have dedicated ourselves to during the past 30 years.

Grameen Bank I became involved because poverty was all

around me, and I could not turn away from it. In 1974, I found it difficult to teach ele-gant theories of economics in the university classroom, in the backdrop of a terrible fam-ine in Bangladesh. Suddenly, I felt the empti-ness of those theories in the face of crushing hunger and poverty. I wanted to do some-thing immediate to help people around me, even if it was just one human being, to get

through another day with a little more ease. That brought me face to face with poor peo-ple’s struggle to find the tiniest amounts of money to support their efforts to eke out a living. I was shocked to discover a woman in the village, borrowing less than a dollar from the money-lender, on the condition that he would have the exclusive right to buy all she produces at the price he decides. This, to me, was a way of recruiting slave labor.

I decided to make a list of the victims of this money-lending “business” in the village next door to our campus.

When my list was done, it had the names of 42 victims who borrowed a total amount of US $27. I offered US $27 from my own pocket to get these victims out of the clutch-es of those money-lenders. The excitement that was created among the people by this small action got me further involved in it. If I could make so many people so happy with such a tiny amount of money, why not do more of it?

That is what I have been trying to do ever since. The first thing I did was to try to persuade the bank located in the campus to lend money to the poor. But that did not work. The bank said that the poor were not creditworthy. After all my efforts, over sev-eral months, failed I offered to become a guarantor for the loans to the poor. I was stunned by the result. The poor paid back their loans, on time, every time! But still I kept confronting difficulties in expand-ing the programme through the existing banks. That was when I decided to create a separate bank for the poor, and in 1983, I finally succeeded in doing that. I named it Grameen Bank or Village bank.

Today, Grameen Bank gives loans to nearly 7 million poor people, 97 percent of whom are women, in 73,000 villages in Bangladesh. Grameen Bank gives col-lateral-free income generating, housing, student and micro-enterprise loans to the poor families and offers a host of attractive savings, pension funds and insurance prod-ucts for its members. Since it introduced them in 1984, housing loans have been used to construct 640,000 houses. The le-gal ownership of these houses belongs to the women themselves. We focused on women because we found giving loans to

women always brought more benefits to the family.

In a cumulative way the bank has giv-en out loans totaling about US $6 bil-lion. The repayment rate is 99%. Grameen Bank routinely makes profit. Financially, it is self-reliant and has not taken donor mon-ey since 1995. Deposits and own resourc-es of Grameen Bank today amount to 143 percent of all outstanding loans. According to Grameen Bank’s internal survey, 58 per-cent of our borrowers have crossed the pov-erty line.

Grameen Bank was born as a tiny home-grown project run with the help of several of my students, all local girls and boys. Three of these students are still with me in Grameen Bank, after all these years, as its topmost ex-ecutives. This idea, which began in Jobra, a small village in Bangladesh, has spread around the world and there are now Grameen type programmes in almost every country. ‑‑ © THE NOBEL FOUNDATION 2006

Beggars Can Turn to Business''In Bangladesh 80 percent of the poor

families have already been reached with microcredit. We are hoping that by 2010, 100 per cent of the poor families will be reached. Three years ago we started an

exclusive programme focusing on the beggars. None of Grameen Bank’s rules apply to them. Loans are interest‑free; they can pay whatever amount they wish, whenever they wish. We

gave them the idea to carry small merchandise such as snacks, toys or household items, when they went from house to house for begging. The idea worked. There are now 85,000

beggars in the program. About 5,000 of them have already stopped begging completely.