Embed Size (px)

Citation preview

H&A IDT Share - November 2012

Contents Job work under Central Excise Res Judicata relating to taxation matters Seminar in Bangalore – Cenvat Credit, Reverse and Joint

Charge – on December 22, 2012 In News Recent judicial decisions Training Corner Bangalore Seminar brochure

Highlights Job Work under Central Excise Res Judicata Workshop in Bangalore – Cenvat Credit, Reverse Charge &

Joint Charge - December 22, 2012 Workshop in Hyderabad - Cenvat Credit, Reverse Charge &

Joint Charge – January 05, 2013

(For private circulation to clients of Hiregange & Associates and Chartered Accountants only)

Contact:-Hiregange & Associates#1010, 1st floor, 26th main,(Above Corporation Bank)4th ‘T’ Block, Jayanagar,Bangalore 560 041Website – www.hiregange.com

Branch Office:-"Basheer Villa"H.No.8-2-268/1/16/B,2nd Floor, Sriniketan Colony,Road No.3, Banjara Hills,Hyderabad-500 034

2

Job Work Under Central Excise

Job work is one of the important aspects that amanufacturer registered under Central Exciseshould be familiar with not just because it enableshim to plan his processes in order to optimise thebenefits available under the Central Excise Act,1944 but would also enable him to cut costs on hismanufacturing. This is so as the processes whichpose problems or which are not cost effective athis end [ due to economies of scale] can be sub-contracted or delegated to another manufactureror processor who is referred to here as the jobworker. Many a time, the job worker may be moreefficient both in terms of the quality and cost ascompared to the main manufacturer due topursuance of core competencies. Most of the bigmanufacturers in fact make very good use of thisconcept and assign processes to more than onevendor which enables them to cut down onmanufacturing costs.

In the context of the Central Excise law, job workhas been defined under Rule 2(n) of the CenvatCredit Rules, 2004 to mean processing or workingupon of raw material or semi-finished goodssupplied to the job worker, so as to complete apart or whole of the process resulting in themanufacture or finishing of an article or anyoperation which is essential for aforesaid processand the expression “job worker” shall be construedaccordingly. It is vital to note here that the processundertaken by the job worker on the goods thatare supplied to him for job work, may or may notamount to manufacture.

If one were to go by the definition of the term “jobwork”, it is evident the raw materials have to besupplied by another person. In PrestigeEngineering India Ltd v CCE Meerut, (1994 (09) LCX0110), the Supreme Court held that when the jobworker contributed his own material to the goodssupplied by the customer and engaged inmanufacturing, the activity was not one of jobwork. However, minor additions by the job workerwould not take away the fact that the activity wasone of job work.

Job Work and Manufacturing

Since excise duty is on ‘manufacture’, duty liabilityarises only when the goods are manufacturedduring job work. The test as to whether theprocess amounts to manufacture or not would bedetermined by analyzing whether a new articlehaving a distinctive name, character or useemerges or not from the said process in …………

(For private circulation to clients of Hiregange & Associates and Chartered Accountants only)

……. accordance with the decision of the HonorableSupreme Court in Delhi Cloth and General Mills Co.Ltd Vs UOI (1962(10) LCX 0001). Where the goodsare manufactured during job work, the job workerwould be liable to pay duty of excise on the goodsso manufactured unless the principal manufacturerwho has supplied him the goods for job work,furnishes a declaration under Notification 214/86dated 25.03.1986 which exempts goodsmanufactured by a job worker from duty of exciseprovided the said goods after job work arereturned to the principal or cleared for export orcleared for home consumption on payment of dutyof excise. Where the goods are returned to theprincipal, the principal should either clear it onpayment of duty or use it in his manufacturingprocess which should result in a dutiable productbeing manufactured. The declaration as statedabove should be given to the AssistantCommissioner of Central Excise who hasjurisdiction over the factory of the job worker.

Job work & SSI exemptionNotification 214/86 CE (NT) has anothersignificance and that is where the job worker alsoavails the benefit of notification 8/2003 CE (NT)dated 01.03.2003, the job work done under thisnotification would not be included for the purposeof determining whether or not his turnover hasexceeded the said limit of Rs. 150 lakhs for thepurpose of determining duty liability if any or Rs.400 lakhs for the purpose of determining eligibilityto exemption u/n 8/2003 CE in the subsequentfinancial year. If working under this notificationthen job work done of even 10 crores would not besubjected to duty of excise in the hands of the jobworker.

Job work – Central Excise v Service TaxWhere the processing undertaken by the jobworker does not amount to manufacture, the saidjob worker would be liable to service tax evenunder the new regime of service tax. The liability interms of job work can arise where the processing isdone for the client. However one should note thatwhere the processing amounts to manufacture, thesame would not be taxable under service tax asthe same has been specifically included in thenegative list and the liability if any would have tobe studied under Central Excise. The entry in thenegative list reads as ‘any process amounting tomanufacture or production of goods’.

PTO

3

Job Work Under Central Excise Contd..

Therefore, the criteria is whether the processundertaken by the job worker amounts tomanufacture or production or not. If the processamounts to manufacture, but the final product iseither exempted by virtue of any notification or isnil rated, even then the said activity will beexempted under the new regime as the criteria isthat the process undertaken by the job workershould amount to manufacturer production ofgoods which has been fulfilled.Where the job work does not amount tomanufacture it would amount to a service andunless exempted would be liable to service tax.

Job work & Cenvat CreditCenvat credit can be availed on materials sent forjob work as per rule 4(5)(a) of the Cenvat CreditRules, 2004. It has to be established from therecords, challans or memos or any other documentproduced by the manufacturer taking the Cenvatcredit that the goods have been received back inthe factory within one hundred and eighty days ofgoods being sent to the job worker. Somaintenance of proper inventory accountingrecords, job work register, details of nature ofprocessing undertaken and quantities receivedback along with scrap generated would gainimportance. The movement should be under achallan giving the particulars as to the Rule underwhich the same is being sent. The challan would bein triplicate with two copies of the sameaccompanying the goods to the job worker whowould return one copy with the goods being sentback to the principal after completion of theprocess. Where the goods are sent back in lots, heis free to send his own delivery challan with thegoods and send back the original delivery challanreceived from the principal, with the finalconsignment being sent to the said principal.

If the inputs or the capital goods are not receivedback within one hundred and eighty days, themanufacturer shall pay an amount equivalent tothe Cenvat credit attributable to the inputs orcapital goods by debiting the Cenvat credit accountwith the amount so attributable to the inputs orcapital goods not received. But the manufacturercan take once again the Cenvat credit so debitedwhen the inputs or capital goods are received backin his factory.

The Cenvat credit shall also be allowed in respectof jigs, fixtures, moulds and dies sent by amanufacturer of final products to another ………..

…… manufacturer for the production of goods or to ajob worker for the production of goods on his behalfand according to his specifications. The restrictionwith regard to the requirement of receiving the goodsback within 180 days from the date of sending wouldnot apply to such tools, dies, fixtures and moulds.

Valuation issues in job workOne of the common issues confronting job workerspaying duty of excise is that of valuation. Untilrecently the valuation had been in accordance withthe decision of the Honorable Supreme Court inUjagar Prints Ltd Vs Union of India (1989 (01)LCX0047) where the assessable value for the purposeof charging excise duty was said to comprise thevalue of raw materials supplied by the principal plusthe conversion charges or job charges incurred by thejob worker plus his profit margin. The margin of theprincipal on those goods manufactured by the jobworker even if he merely traded in those goods wasnot to be subjected to duty of excise. But this positionunderwent a change from 01.04.2007 because of anamendment to the Central Excise Valuation(Determination of Price of Excisable Goods) Rules2000. A new Rule 10A was inserted in the said Ruleswhich stipulates that where the goods are sold by theprincipal manufacturer from the factory of jobworker, the value would have to be the transactionvalue of the goods so sold by the principalmanufacturer. This will apply only when the principalmanufacturer and the buyer of the goods are notrelated and price is the sole consideration for the saleand the goods are sold for delivery at the time ofremoval from the job worker's factory.

In a case where the goods are not sold by theprincipal manufacturer at the time of removal ofgoods from the factory of job-worker, but aretransferred to some other place from where the saidgoods are to be sold after their clearance from thefactory of the job worker, the normal transactionvalue of such goods sold from such other place at orabout the same time has to be adopted. This, in otherwords follows the principle of depot based valuationunder Central Excise applicable where goods arecleared to depots of manufacturers and soldtherefrom. Where such goods are not sold at orabout the same time, then the normal transactionvalue of such goods at the time nearest to the time ofremoval of said goods from the factory of job-worker,is to be adopted. The cost of transport from thepremises where from the goods are sold, to the placeof delivery, would not be included in assessable value.

- Team Hiregang & Associates

(For private circulation to clients of Hiregange & Associates and Chartered Accountants only)

4

Res Judicata relating to taxation matters

IntroductionFinality to assessment facilitates the assessee to planhis affairs and to decide the business planning forlong term strategies. The doctrine of Res Judicata is apotent tool in the hands of an assessee who wants toprevent the Assessing Officer from shifting his standyear – to – year on whimsical grounds.

However, tax authorities feel that there is no finalityto any assessment as the principle of Res Judicata isnot applicable to tax proceedings.

MeaningThe word ‘Res Judicata’ is derived from Latin. Itliterally means, a thing adjudged. It is a rule that saysa final judgment on the merits by a court havingjurisdiction is conclusive between the parties to a suitas to all matters that were litigated or that could havebeen litigated in that suit. The principle of ResJudicata, in the eye of law, is that if on any factsand/or law, a particular decision is made, thensubsequently if any suit on similar facts and/or law isto be decided between the same parties, it should besame as made earlier.

As per The Law Lexicon “Res adjudicata” means “Amatter adjudged; a thing judicially acted upon ordecided; a thing or matter settled by judgment; athing definitely settled by judicial decision, the thingadjudged”.

This principle operates as a bar to try the same issueonce over. The Apex Court in the case of SulochanaAmma vs. Narayanan Nair - (2002-TIOL-292-SC-MISC)held that this principle aims to prevent multiplicity ofproceedings and accords finality to an issue, whichdirectly and substantially had arisen in the former suitbetween the same parties or their privies, decidedand became final, so that parties are not vexed twiceover; vexatious litigation would be put to an end andthe valuable time of the Court is saved. It is based onpublic policy as well as private justice.

Res Judicata does not merely prevents futurejudgments from contradicting earlier ones, but alsoprevents them from multiplying judgments, so aprevailing plaintiff could not recover damages fromthe defendant twice for the same injury.

Origin of Res Judicata"Res Judicata pro veritate accipitur" is the full Latinmaxim which has, over the years, shrunk to mere"Res Judicata”.The concept of Res Judicata finds its evolvement fromthe English Common Law system, being derived fromthe overriding concept of judicial economy, …………..

consistency, and finality. The rule of Res Judicata hasa very ancient history it was accepted by the Romans,Hindu jurists, Mohammedan jurists and commonwealth countries. It was known to Romans as ‘onesuit and one decision was enough for any singledispute’. To the Hindu jurists res Judicata was knownas ‘Purva Nyaya’ (former judgment)

Basis of Res JudicataThe doctrine of Res Judicata is based on threemaxims:1. Nemo debet lis vaxari pro eadem causa (no man

should be vexed twice for the same cause);2. Interest republicae ut sit finis litium (it is in the

interest of the state that there should be an endto a litigation); and

3. Re judicata pro veritate accipitur (a judicialdecision must be accepted as correct).

Pre-requisites for Res JudicataThe pre-requisites which are necessary for ResJudicata are:1. There must be a final judgment;2. The judgment must be on the merits;3. The claims must be the same in the first and

second suits;4. The parties in the second action must be the

same as those in the first, or have beenrepresented by a party to the prior action.

Constructive Res Judicata‘Constructive' means ‘implied', “that which has notthe character assigned to it in its own essentialnature, but acquires such character in consequenceof the way in which it is regarded by a rule or policy oflaw” (Black). If a matter which might or ought to havebeen raised in an earlier proceeding, is not raised, theprinciple of constructive Res Judicata applies.

Source of Res Judicata in Indian LawSection 11 of The Code of Civil Procedure, 1908,defines “Res Judicata” as under:-

“No court shall try any suit or issue in which thematter directly and substantially in issue has beendirectly and substantially in issue in a former suitbetween the same parties, or between parties underwhom they or any of them claim, litigating under thesame title, in a court competent to try suchsubsequent suit or the suit in which such issue hasbeen subsequently raised, and has been heard andfinally decided by such court.”From the Civil Procedure Code, the AdministrativeLaw witnessed its applicability. Then, slowly butsteadily the other acts and statutes also started toadmit the concept of Res Judicata within its ambit.

PTO

(For private circulation to clients of Hiregange & Associates and Chartered Accountants only)

5

Res Judicata relating to taxation matters contd..

Principle of Res Judicata in tax matters

The general principle of law is that no one shouldblow hot and cold on the same set of facts to reachdifferent conclusions / findings in different years. Theneed for consistency is as important for revenueauthorities as it is expected from the assessee. Thecommon understanding is that, notwithstanding thepublic policy behind the rule, it has no relevance totax disputes. It is said that a finding or an opinionrecorded by an authority or even by a court of law forone assessment year has no binding effect on theissues in subsequent assessment years.

Views of High Court

The Bombay High Court, in H.A. Shah and Co. vs. CIT(1956) 30 ITR 618 (Bom.) has held that “the principleof estoppel or res judicata does not strictly apply tothe Income Tax authorities” and yet declared that “Anearlier decision on the same question cannot bereopened if that decision is not arbitrary or perverse,if it had been arrived at after due inquiry, if no freshfacts are placed before the Tribunal giving the laterdecision and if the Tribunal giving the earlier decisionhas taken into consideration all material evidence.”

In CIT vs. L. G. Ramamurthy (1977) 110 ITR 453(Mad.), the court laid down the principle that “…whatis relevant is not the personality of officers presidingover the Tribunal but the Tribunal as an institution. Ifit is conceded that simply because of the change inthe personnel who manned the Tribunal, it is open tothem to a conclusion totally contradictory to theconclusion which had been reached by earlier officersmanning the tribunal on same set of facts it will notonly shake the confidence of the public in judicialprocedure as such, but it will totally destroy suchconfidence…….that will be destructive of theinstitutional integrity itself”.

Views of the Apex Court

The Supreme Court in Amalgamated Coalfields vs.Janapada Sabha AIR 1964 SC 1013 have evinced ahighly, balanced approach: “In considering thisquestion, it may be necessary to distinguish betweendecision on questions of law which directly andsubstantially arise in any dispute about the liability fora particular year, and questions of law which ariseincidentally or in a collateral manner … the effect oflegal decisions establishing the law would be adifferent matter. If, for instance, the validity of ataxing statute is impeached by an assessee who iscalled upon to pay a tax for a particular year and thematter is taken to the High Court or brought beforethis Court and it is held that the taxing statute is valid,it may not be easy to hold that the decision on thisbasic and material issue would not operate as res -

judicata against the assessee for a subsequent year”.

In Radhasoami Satsang vs. CIT (1992) 193 ITR 321(SC) the Hon’ble Apex Court observed as under:“So far as the proposition of law is concerned, it iswell settled and needs no further discussion. Intaxation matters, the strict rule of res Judicata asenvisaged by Section 11 of the Code of CivilProcedure, 1908 has no application. As a general rule,each year's assessment is final only for that year anddoes not govern later years, because it determinesthe tax for a particular period. It is, therefore, open tothe Revenue/Taxing Authority to consider theposition of the assessee every year for the purpose ofdetermining and computing the liability to pay tax oroctroi on that basis in subsequent years.”However, in an interesting comment, the Apex Courtsaid, “We are aware of the fact that strictly speakingres judicata does not apply to income taxproceedings. Again, each assessment year being aunit, what is decided in one year may not apply in thefollowing year but where a fundamental aspectpermeating through the different assessment yearshas been found as a fact one way or the other andparties have allowed that position to be sustained bynot challenging the order, it would not be at allappropriate to allow the position to be changed in asubsequent year”.

Not pressing the groundThere is no estoppel against law. No concession oflaw is permissible. An appellant having not pressed anissue before lower authorities, can still raise andagitate the same before the Tribunal-CIT vs. VMRPFirm (1965) 56 ITR 67 (74) (SC).

Conflicting stands by revenueThe revenue cannot take conflicting stands. It has gotthe assistance of technical persons and should beconsistent. It cannot discriminate between theassessees. Seshasayee Paper and Boards Ltd. vs. CIT(2003) 260 ITR 419 (Mad.)

ConclusionFrom the above discussion, it is evident that, as ageneral rule, Res Judicata does not apply in taxmatters, be it direct tax or indirect tax. As apparent,we come across periodical show cause notices withrespect to same assessee on the same matter.However, the principles of consistency, natural justiceand comity apply. Based on these, the tax payers canbe ascertained of certain aspects in their favour.Further, we can also understand that, the counter forRes Judicata can be appeal to a higher judicial forum.

- Compiled by CA Dhanashree PrabhuAcknowledgements – ARTHA Study Circle

(For private circulation to clients of Hiregange & Associates and Chartered Accountants only)

6

In News

McDonalds’ soft serve should be classified as ice-cream for determining excise duty: Supreme Court -The Supreme Court has ruled that the 'soft serve' soldat McDonalds India's outlets should be classified asice-cream for the purpose of determining excise duty,upholding the excise department's claim. Thedepartment had issued three show-cause notices tothe fast-food restaurant chain for April 1997-March2000, saying 'soft serve' would attract the 16% dutyplus an additional duty levied on ice-cream.McDonalds India (Ms/ Connaught Plaza Restaurant(Pvt) Ltd) had opposed the classification, leading tothe dispute. In a judgement last week, the apex courtruled, "We are unable to accept the argument thatsince 'soft serve' is distinct from 'ice-cream' due to adifference in its milk fat content, the same must beconstrued in the scientific sense for the purpose ofclassification.“

Source: The Economics Times

FIU asked to track service tax evaders - The FinancialIntelligence Unit (FIU), country’s nodal agency forgathering, analysing and disseminating informationrelated to suspicious financial transaction, has beenasked to work with the Directorate General of CentralExcise Intelligence (DGCEI) to go after over 65,000non-filers of service tax returns, who have managedto escape the scrutiny of the government so far.Finance minister P Chidambaram has also asked theDGCEI “to make available some unique identifier” totrack evaders of both the service tax and centralexcise duty.

ITAT: Four new e-courts to be launched, hearingthrough video-conferences - The Income TaxAppellate Tribunal will launch e-courts in four citiesfrom December 10 to facilitate hearing of cases viavideo-conferencing. The tribunal, a quasi-judicialbody, has set up webcast facilities at Delhi, Mumbai,Nagpur and Ahmedabad, a first in the history of taxjudiciary in India. In a note, ITAT said the e-courts willfollow the procedures that are laid out for the benchfor hearing appeals in an open court. "There is nodifference in procedures except that the bench andbar are at different places connected electronically,"the note said.

Source: The Economics Times

Cadbury India probed over R213-cr tax evasioncharge - Tax authorities have detected alleged taxevasion of Rs 213 crore by the Indian arm ofconfectionery multinational Cadbury, now owned byKraft Foods, in two separate cases and have realisedRs 12.6 crore in one of the cases, minister of state forfinance SS Palanimanickam said in the Rajya Sabha.

“Two cases of tax evasion by Cadbury India Ltd havebeen detected by the Directorate General of CentralExcise Intelligence during the years 2009-10 to 2012-13 up to October 31, 2012,” the minister said in replyto a question in the Upper House.Source: The Financial Express

Carmaker Fiat India seeks review of Supreme Courtorder on excise duty payment - Carmaker Fiat Indiahas sought review of a Supreme Court order directingit to pay about 360 crore as additional excise duty onsales of its Uno cars between 1996 and 2001. "Wehave filed a review petition," said V LakshmiKumaran, lawyer for Italian carmaker Fiat's Indianunit, without giving further details. The court hadpassed the order on August 29. The case pertains toFiat's joint venture with Mumbai-based PremierAutomobiles at the time. Fiat was importingcompletely-knocked-down kits of its popular Unohatchback and selling them in the country below costprice. This prompted the tax authorities to levy theduty on the cost price of the company's Unohatchbacks.

Tax bumps ahead for diesel cars - At a time whendiesel-powered vehicles have been driving sales inthe country’s otherwise sluggish automobile market,the industry has been hit by a double whammy. First,a proposal to levy an additional annual road tax of upto Rs 50,000 on diesel sports utility vehicles. Second,a suggestion before the Supreme Court to impose anenvironment tax of 25 per cent (of the cost of thevehicle) on diesel vehicles to curb the growing levelsof pollution in the Delhi-National Capital Region.These have raised concerns in the domesticautomobile industry, battling slow sales and highinterest rates and fuel prices. “On an average, dieselvehicles are tagged 20-23 per cent higher than ex-showroom prices of petrol variants. Once Euro-Vemission norms come into effect, vehicle priceswould automatically rise Rs 40,000. If there areadditional levies, it would certainly putmanufacturers’ investments to increase dieselcapacity in jeopardy,” said a senior industryexecutive.

Old service specific accounting codes for payment ofservice tax restored - A list of 120 descriptions ofservices for the purpose of registration andaccounting codes corresponding to each descriptionof service for payment of tax has been provided. Thedescription provided is only for the purpose ofstatistical analysis. The sub-head “other receipts” ismeant only for payment of interest payable ondelayed payment of service tax.

(For private circulation to clients of Hiregange & Associates and Chartered Accountants only)

7

Recent judicial decisions

INDIAN ACRYLIC LTD. VERSUS COMMISSIONER OFC.EXCISE, CHANDIGARH-II 2012 (28) S.T.R. 354 (TRI-DEL)

Background: The appellant is a manufacturer ofacrylic fibre, acrylic top etc. and were availing thefacility of Cenvat credit of duty paid on inputs, capitalgoods and Service Tax paid on inputs services used inor in relation to manufacture of final products. Theappellants are availing the services of foreign agentsand were paying commission on said agents locatedoutside India. They were discharging the Service Taxliability in respect of such commission paid to theforeign agents in terms of provisions of Rule2(1)(d)(iv) and (v). The lower authorities have deniedthe utilization of Cenvat credit availed by theappellant on the capital goods, for the purpose ofdischarging their Service Tax liability on the groundthat the appellant cannot be treated as provider oftaxable service. The stand of the Revenue is that afterthe deletion of Explanation appearing in Rule 2(p) ofCenvat Credit Rules, which conferred status of outputservice provider to an assessee, the assessee cannotbe held to be provider of output services andappellants are not entitled to utilize the credit.

Issue: The issue required to be decided in presentappeal is as to whether the appellant can utilize theCenvat credit so earned by them for discharge ofService Tax liability in respect of overseas commissionagent.

Decision: Utilization of Cenvat credit is in accordancewith the law inasmuch as the Rule 2(r) of CenvatCredit Rules conferred status of service provider to anassessee who paid the Service Tax as a recipient ofservice. If the appellant is the person liable to payservice tax, he would be deemed to be provider oftaxable service by fiction of law and therefore, theservice provided by him will be deemed to be outputservice under Rule 2(p) of the Rules. It is held thatthe appellant is entitled to utilize the Cenvat creditfor discharge of Service Tax for the commission paidto the overseas agents.

INDIA TRIMMINGS PVT LTD VERSUS COMMISSIONEROF C.EX. COIMBATORE 2012 (28) S.T.R. 401 (TRICHENNAI)

Background: The appellants are manufacturer andexporter. They have taken the services of GTA andpaid commission to overseas service provider. Noservice tax was paid under reverse charge mechanismand on pointing out the same by the Department, theappellants paid service tax along with interest.Thereafter, the appellant was issued SCN for ……..

…. appropriation of the amount of service tax andinterest paid and proposing penalty u/s 78 of theFinance Act 1994. Counsel for the appellantsubmitted that they were under a bona fide beliefthat they are not required to pay service tax on aboveservices as they were not a service provider and if atall they had paid service tax they would have entitledto take credit of the same and there will be asituation of revenue neutrality and thereforeallegation of suppression is not sustainable.Reference was made to the case of Amman SteelCorporation Vs CCE, Trichy. Revenue contended thatas the appellant is dealing with excisable and taxableservice, they must be aware of law.

Issue: The issue for consideration is that whether notshowing the amount of GTA availed and commissionpaid from overseas by the appellant in their ST-3Returns and nonpayment of service tax on the sameamounts to suppression and whether proposingpenalty u/s 78 is sustainable in the above case.

Decision: If appellant have paid the service tax theyare entitled to credit of the same and in this view, itcannot be said that by suppressing the fact that theappellants are going to get extra benefit on accountof suppression. Penalty u/s 78 was waived.

COMMISSIONER OF CENTRAL EXCISE, JAIPURVERSUS KEC INTERNATIONAL LTD. 2012 (28) S.T.R.399 (TRI DEL)

Background: The respondent were engaged in themanufactuer of galvanized parts of transmissiontower and lining falling under Chpater 73 of theSchedule to the Central Excise Tariff Act, 1985. Theraw material for the said final product is billet and it ispurchased from outside and sent directly to thefactory of job worker who converts the same intoangles and channels. Revenue’s contention is thatService Tax paid on GTA service received is notavailable to them as credit

Issue: The issue in consideration is that whethercenvat credit can be availed on service tax paid onGTA as the raw materials were not brought into therespondents’ factory and are directly sent to the jobworker.

Decision: Held that billets are admittedly the rawmaterial for the respondent’s final product and if thesaid billets are brought to the factory by therespondents and then sent to the job workers, therecould be no dispute about the availability of credit ofservice tax paid on GTA service.

(For private circulation to clients of Hiregange & Associates and Chartered Accountants only)

8

Training Corner

Recently CA Roopa Nayak, CA Akbar Basha and CAGaurav Shah conducted a training session in M/sBalakrishna & Co. The training program was very wellappreciated by the qualified Chartered Accountantsof the firm as well as the articled assistants.

With the objective of holistic learning, we have comeup with the training modules.

Training Program for Chartered Accountants FirmsThis program would be conducted to enlighten andempower the Practicing Chartered Accountants inconducting the statutory, internal & tax auditswherein value additive suggestions to clients may getappreciation. This will be conducted at the respectiveoffices of Chartered Accountants by qualified andskilled staff of Hiregange & Associates.

Program Highlights• Focus on impact of indirect taxes during statutory

audit, internal audit and other areas of practice• Use of case studies and practical aspects• To enlighten and empower the Practicing CAs in the

field of Indirect Taxation• Program will be conducted at your respective office• Topics for the program will be of your selection

from the Annexure• Programs will be conducted by qualified and

experienced staff of Hiregange & AssociatesWho are eligible for the program• Chartered Accountant company/firms at Bangalore

who do not currently practice in the field of IndirectTaxation

• Chartered Accountant company/firms at Bangalorewho wish to enter the field but with soundfundamental knowledge of the subject or add thiscompetency

Proposed Modules are:-• Major aspects to be checked in the Statutory Audit,

Internal Audit, Tax Audit having implications underindirect tax (IDT)

• How to provide Value Addition to the auditee inStatutory/ Internal Audit with respect to IDT

• Impact of Joint and Reverse Charge• Reconciliation between Excise / Service Tax returns

to financials and other statutory returns.• Common errors made by assessee in Central Excise

/ Service Tax.• How to fill Central Excise Returns & ST returns• Introduction on Central Excise viz.- Concept of

manufacture, Levy of Excise duty, Classification ofgoods, Exemption, Valuation Implication, Exports.

• Introduction on Service Tax viz.- Negative List, Levyof Service Tax, Exemption, Valuation aspects, Pointof Taxation Rules, Place of Provision of ServiceRules and Aspects related to filing of Returns.

Training Program for Clients of Hiregange &AssociatesClient Specific Training:This is for specific clients in specific areas such asBasic Accounting, Tax Planning and Impact of IndirectTaxes in their day-to-day working. This programwould be conducted to enlighten and empower thefinance team of the company in the field of IndirectTaxation.We have devised two approaches to this programme.• To conduct it at H&A premises fortnightly (on

Saturdays)• To conduct it at your respective office (on the date

and time mutually agreed)

Program Highlights• Focus of indirect taxes in the effective day-to-day

working.• Use of case studies and practical aspects• To enlighten and empower our Clients in the field

of Indirect Taxation• Topics for the program will be of your selection

from the Annexure• Programs will be conducted by qualified and

experienced staff of Hiregange & Associates

Who are eligible for the programThe Indirect Taxation Training Programs areexclusively for the Clients of Hiregange & Associates

Proposed Modules are:-• Introduction on Central Excise• Introduction on Service Tax• Availment of credit under Central Excise/Service

Tax & VAT• Impact of indirect tax on cost• Means of ensuring maximum credit (CE/ST/VAT)• Accounting entries in Indirect Tax• Impact of Joint and Reverse charge to the entity• Filling of Excise Returns• Filling of New format of Service Tax returns• Common errors under Central Excise & Service Tax• Preventive measures to avoid common errors• Strengthening Internal Control with respect to

Indirect Taxation• Reconciliation between Excise / Service Tax return

with financials and other statutory returns• Point of Taxation Rules• Place of Provision of Service Rules• How to make a refund application?

For further information please contactCA Akbar [email protected] Dhanashree [email protected]

(For private circulation to clients of Hiregange & Associates and Chartered Accountants only)

Workshop on

Saturday, 22nd December, 2012

Between 09 am & 06 pm

@ Springs Hotel & Spa#19, H. Siddaiah Road, Bangalore – 02

(Next to Urvashi Theatre and near BBMP pay & park)

“CENVAT CREDIT –UNDER NEW ST LAW”

Contact :-Hiregange & Associates

# 1010, 1st Floor, 26th Main, (Above Corporation Bank)4th ‘T’ Block, Jayanagar, Bangalore – 560 041

Ph No. 4121 0703 / 2653 6404Web : www.hiregange.com

CA. Prateek Marlecha– +91 99000 68911Email: [email protected]

CA. Dhanashree Prabhu – +91 99000 68920Email: [email protected]

(Only for CAs and clients of Hiregange & Associates)

Similar seminar in Hyderabad will be held on January 05, 2013

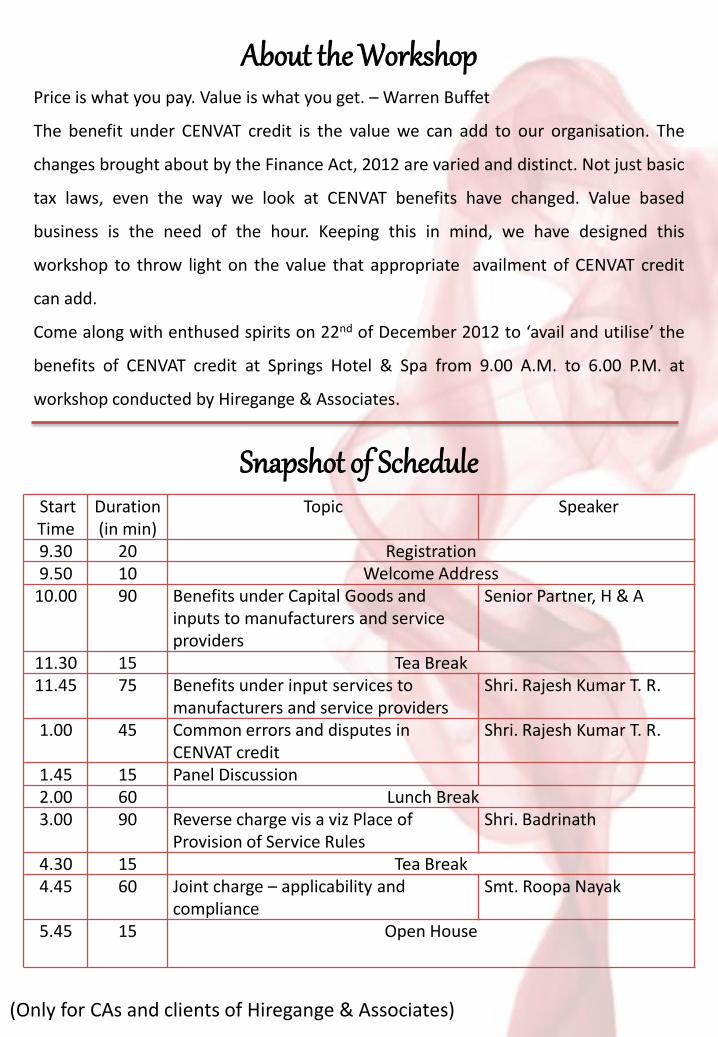

Price is what you pay. Value is what you get. – Warren Buffet

The benefit under CENVAT credit is the value we can add to our organisation. The

changes brought about by the Finance Act, 2012 are varied and distinct. Not just basic

tax laws, even the way we look at CENVAT benefits have changed. Value based

business is the need of the hour. Keeping this in mind, we have designed this

workshop to throw light on the value that appropriate availment of CENVAT credit

can add.

Come along with enthused spirits on 22nd of December 2012 to ‘avail and utilise’ the

benefits of CENVAT credit at Springs Hotel & Spa from 9.00 A.M. to 6.00 P.M. at

workshop conducted by Hiregange & Associates.

Start Time

Duration (in min)

Topic Speaker

9.30 20 Registration9.50 10 Welcome Address

10.00 90 Benefits under Capital Goods and inputs to manufacturers and service providers

Senior Partner, H & A

11.30 15 Tea Break11.45 75 Benefits under input services to

manufacturers and service providersShri. Rajesh Kumar T. R.

1.00 45 Common errors and disputes in CENVAT credit

Shri. Rajesh Kumar T. R.

1.45 15 Panel Discussion2.00 60 Lunch Break3.00 90 Reverse charge vis a viz Place of

Provision of Service RulesShri. Badrinath

4.30 15 Tea Break4.45 60 Joint charge – applicability and

complianceSmt. Roopa Nayak

5.45 15 Open House

(Only for CAs and clients of Hiregange & Associates)

Snapshot of Schedule

About the Workshop

Featured SpeakersShri Rajesh Kumar T. R. - Apart from being a Chartered Accountant, he is a graduatein Law. Involved in providing strategic indirect tax consultancy and representationservices. Also written many articles on Central Excise and Service tax published invarious professional journals and co-authored many books. He is a visiting faculty forMBA course of M.P. Birla Institute for management Studies, Bangalore andSiddaganga School of Mangement, Tumkur.

Shri. Badrinath N. R. - Apart from being a Chartered Accountant, he is also a CostAccountant and specializes in Indirect Taxation. His area of expertise spans overCentral & State levies which include Central Excise, Customs, Service Tax, CommercialTaxes and Foreign Trade. He is very closely associated with the subject specializationand has addressed the officers at Central Board of Excise and Customs, members ofthe ICAI and Institute of Internal Auditors. He is a faculty for Indirect Taxation at MATSSchool of Business and IT.

Smt. Roopa Nayak - Is a Chartered Accountant by profession, qualified in 2008. Co-author of books like Central Excise Made Simple (e-book & KSCAA publication),background material for Indirect Taxes Certificate Course, ICAI. She is an activecontributor of articles to Peenya Industries Association and KSCAA.

Delegate Fee – Rs. 1,500/-For 3 or more delegates from the same organization fee – Rs. 1,250/- each

Includes service tax applicable @ 12.36%

The fee covers delegate kit, lunch and refreshments

Kindly issue Cheque/DD in favour of “Hiregange & Associates”, payable at Bangalore

Fee structure

(Only for CAs and clients of Hiregange & Associates)

Top level Company officials – For Strategic business decisionsMiddle level Company officials – For regular and day-to-day complianceChartered Accountants in practice – To update their knowledge and

educate their clients

The workshop would be of special interest to:-

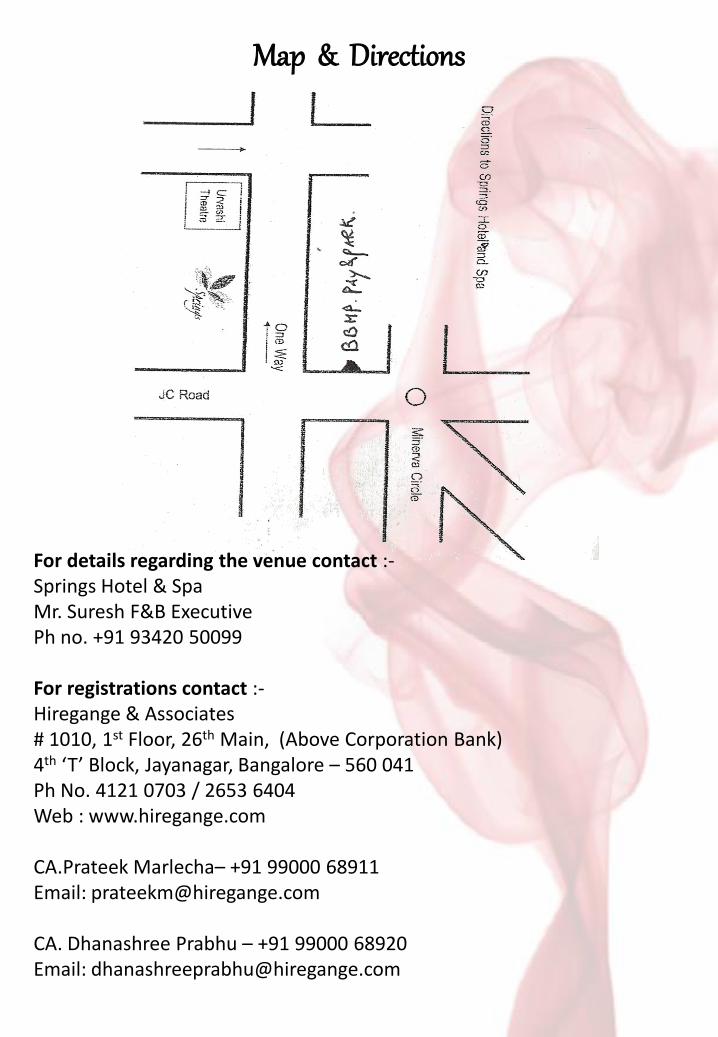

Map & Directions

For registrations contact :-Hiregange & Associates# 1010, 1st Floor, 26th Main, (Above Corporation Bank)4th ‘T’ Block, Jayanagar, Bangalore – 560 041Ph No. 4121 0703 / 2653 6404Web : www.hiregange.com

CA.Prateek Marlecha– +91 99000 68911Email: [email protected]

CA. Dhanashree Prabhu – +91 99000 68920Email: [email protected]

For details regarding the venue contact :-Springs Hotel & SpaMr. Suresh F&B ExecutivePh no. +91 93420 50099