Embed Size (px)

Citation preview

Research

H2 2012

WARSAW Office market report

Highlights• While growth has slowed, the Polish economy has remained relatively resilient

in the face of the Eurozone crisis which has been reflected in the level of leasing

activity. Indeed, 2012 was another record year for take-up, which reached

608,000 sq m.

• Pricing for prime stock has stabilised, although investor demand has remained

buoyant. An exceptionally strong H2 pushed full year transaction volumes

(including hotels) to €2.7bn – virtually unchanged on 2011.

• In Euro terms, prime rents remain in the €22-28 per sq m per month range,

but the tone of average asking rents softened over the year, in line with

a more cautious economic outlook.

• The capital also saw a marked increase in office stock, with 260,000 sq m of new

space delivered to the market – more than double the amount recorded in 2011.

H2 2012WarsawOffice market report

2

Table 1

Major leasing transactions signed in H2 2012

Property Submarket Tenant Size (sq m) Transaction type

Sector

Wilanów Office Park A Służewiec Przemysłowy Asseco 20,400 new professional services

Warsaw Spire CBD Frontex 14,580 new professional services

Domaniewska 37C Służewiec Przemysłowy Poczta Polska 12,600 new public

Green Corner CBD GDDKiA 11,700 new public

Feniks CBD BOŚ Bank 8,940 new financial/banking

Grzybowska 81 Wola Bank Polskiej Spółdzielczości

8,920 pre- let financial/banking

Marynarska Point Służewiec Przemysłowy Generali 7,700 renewal financial

Source: Knight Frank

0

100

200

300

400

500

600

0

4

8

12

16

20

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Figure 1

Warsaw office take-up and vacancy rate000s sq m %

Source: Knight Frank

Take-up Vacancy rate

Market overviewPoland avoided the recent recession and remains one of Europe’s best performing economies. However, in line with the sluggish outlook for much of Europe, recent data show that the economy has slowed and growth is expected to be just over 2% for 2012 – around half the rate seen in 2011. A similar pace of growth is forecast for 2013.

Nonetheless, leasing activity in the capital was brisk in 2012, with total take-up rising by 6% on 2011 to reach a record level of 608,000 sq m. The split between pre-lets and new leases was more or less equal at 35% and 34% of the total respectively, while existing lease renewals accounted for another 23%. As in recent years, most of the space was leased in locations outside the main CBD area, mainly as a result of lower asking rents, in addition to the large number of office schemes being developed in non-central areas.

At the end of 2012, the weighted average asking rent for Warsaw office space amounted to €17.50 per sq m per month. Prime rents in the CBD vary from €22-28 per sq m per month, while rents for good quality space outside central locations range from €14-16 per sq m per month. Expectations for the coming months suggest modest downward pressure on asking rents, resulting from the sizeable development pipeline.

Indeed, in terms of space, Warsaw remains

the largest and fastest growing office market

in Poland. Some 260,000 sq m of new space

– a 121% increase on 2011 – was completed

in 2012, taking the city’s supply of modern

offices to 3.14 million sq m by the year-end.

Invariably, the most popular locations for

development remain the CBD, Służewiec

Przemysłowy and Wola.

However, the CBD has seen a steady decline

in its share of total office space in recent

years. In 2007 it accounted for 44% of

Warsaw’s office stock, which had fallen

to 35% by the end of last year. An analysis

of a number of recently started projects

suggests that there is potential for the

market to become over-supplied in the

next 12 months. Approximately 140,000

sq m of modern office space was under

construction at the start of 2012, which had

risen to 520,000 sq m by the end of the year,

of which 59% will be completed this year.

As a result of this development activity,

the vacancy rate increased to 10.8% as at

December, an increase of 2.4 percentage

points on a year earlier. The large volume

of new supply anticipated for this year is

likely to push the vacancy rate up further over

the coming months, although the precise

impact will clearly depend on the strength

of occupier demand for this space.

POLAND’S ECONOMY SLOWED IN 2012, BUT OCCUPIER ACTIVITY WAS BUOYANT AND TAKE-UP EXCEEDED 600,000 SQ M

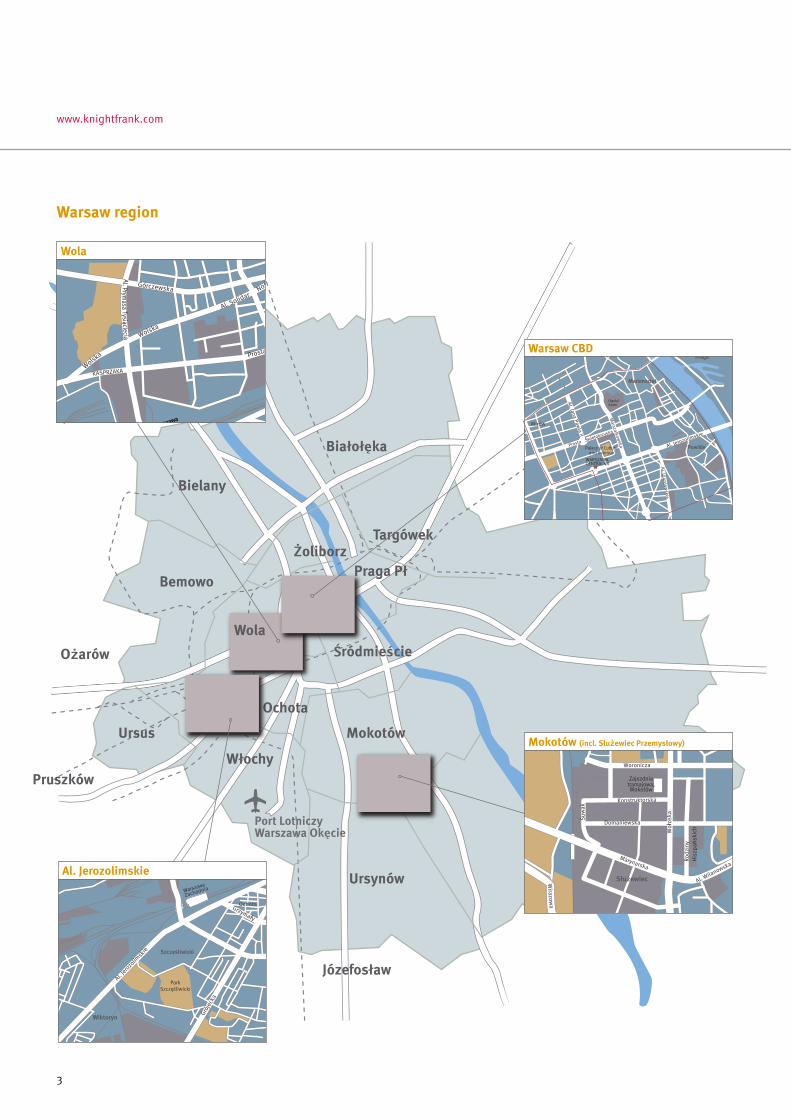

Łomianki

Bielany

Białołęka

Targówek

Praga PłBemowo

Mokotów

Śródmieście

Żoliborz

Ożarów

Pruszków

Janki

Piaseczno

Port LotniczyWarszawa Okęcie

Józefosław

Ursynów

Ursus

Włochy

Ochota

Wola

www.knightfrank.com

3

Mokotów (incl. Służewiec Przemysłowy)

Warsaw region

Zajezdniatramajowa,Mokotów

Marynarska

Woronicza

Rodz

iny

Wirazow

a

Al. Wilanowska

Konstruktorska

Domaniewska

Suw

ak

Woł

oska

Służewiec

His

zpań

skic

h

Warsaw CBD

Prosta

Ności

Wolska

Al. Prymasa Tysiącllecia

Górczewska

Al. Solidar

Wolska

Palace of Cultureand Science

OgródSaski

WARSZAWACENTRALNA

Praga

Mariensztat

Powisle

Mirów

Al. Jana Pawla II

Marszalkow

ska Al. Jerozolimskie

Prosta Świetokrzyska

Al. Ujazdow

skie

Wola

KASPRZAKA

Warszawa

ZachodniaWarszawa

Zachodnia

Prosta

Ności

Wolska

Al. Prymasa Tysiąclecia

Górczewska

Wolska

Al. Solidar

Al. Jerozolimskie

Prosta

Ności

Wolska

Al. Prymasa Tysiącllecia

Górczewska

Al. Solidar

Wolska

Wiktoryn

Warszawa

Zachodnia

ParkSzczesliwicki

Szczesliwicki

Ochota

Al. Jero

zolim

skie

Grój

ecka

Grzymały

4

0

200

400

600

800

1,000

1,200

1,400

CBD

Jero

zolim

skie Av

.

Mok

otów

(incl

. Służe

wie

c

Prze

msy

łow

y)

Wol

a

Oth

er

Figure 4

New supply by location000s sq m

Source: Knight Frank

0

5

10

15

20

25

30

35

40

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Figure 2

Prime office rents€ per sq m per month

Source: Knight Frank

Figure 3

Submarket vacancy rates%

0

5

10

15

20

25

to end 2003 2004 2005 2006

2007 2008 2009 2010

CBD

Jero

zolim

skie Av

.

Mok

otów

(incl

. Służe

wie

c

Prze

msy

łow

y)

Wol

a

Oth

er

Source: Knight Frank

THE INVESTMENT MARKET HAD A SOLID 2012, WITH TOTAL VOLUMES JUST AHEAD OF 2011 AT €2.7BN

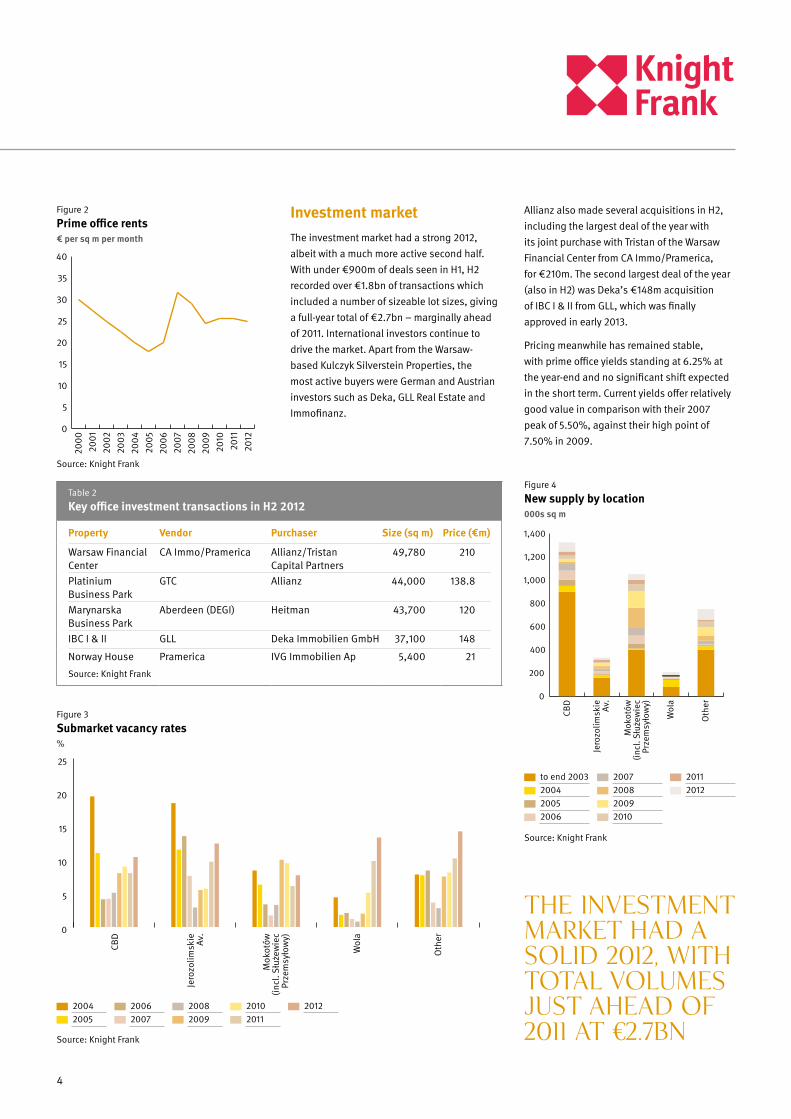

Investment marketThe investment market had a strong 2012, albeit with a much more active second half. With under €900m of deals seen in H1, H2 recorded over €1.8bn of transactions which included a number of sizeable lot sizes, giving a full-year total of €2.7bn – marginally ahead of 2011. International investors continue to drive the market. Apart from the Warsaw-based Kulczyk Silverstein Properties, the most active buyers were German and Austrian investors such as Deka, GLL Real Estate and Immofinanz.

Allianz also made several acquisitions in H2, including the largest deal of the year with its joint purchase with Tristan of the Warsaw Financial Center from CA Immo/Pramerica, for €210m. The second largest deal of the year (also in H2) was Deka’s €148m acquisition of IBC I & II from GLL, which was finally approved in early 2013.

Pricing meanwhile has remained stable, with prime office yields standing at 6.25% at the year-end and no significant shift expected in the short term. Current yields offer relatively good value in comparison with their 2007 peak of 5.50%, against their high point of 7.50% in 2009.

Table 2

Key office investment transactions in H2 2012

Property Vendor Purchaser Size (sq m) Price (€m)

Warsaw Financial Center

CA Immo/Pramerica Allianz/Tristan Capital Partners

49,780 210

Platinium Business Park

GTC Allianz 44,000 138.8

Marynarska Business Park

Aberdeen (DEGI) Heitman 43,700 120

IBC I & II GLL Deka Immobilien GmbH 37,100 148

Norway House Pramerica IVG Immobilien Ap 5,400 21

Source: Knight Frank

to end 2003 2004 2005 2006

2007 2008 2009 2010

2011 2012

2004 2005

2006 2007

2008 2009

2010 2011

2012

H2 2012WarsawOffice market report

5

Table 3

2012 Figures

Area Prime rent (€ per sq m per month)

Stock (sq m)1

Vacancy rate (%)2

Vacant space (sq m)

CBD 25.10 1,047,566 10.4 109,102

Mokotów (incl. Służewiec Przemysłowy) 15.50 947,072 7.7 73,334

Wola 16.20 194,983 13.3 26,009

Al. Jerozolimskie 15.00 331,179 12.4 40,956

Other 15.90 617,212 14.2 87,600

Warsaw total 3,138,012 10.8 337,0011 Excluding owner occupied stock 2 Vacancy rates reflect vacant space in leasable office premises, excluding owner occupied stock Source: Knight Frank

Figure 5

Offices under construction by submarket and completion date000s sq m

4

5

6

7

8

9

10

11

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Figure 6

Prime office yields %

Source: Knight Frank

0

1

2

3

4

5

620

05

2006

2007

2008

2009

2010

2011

2012

Figure 7

Poland commercial property investment volumes €bn

Source: Knight Frank

Griffin House

City skyline

0

100

200

300

400

500

600

War

saw

tota

l

CBD

Al. J

eroz

olim

skie

Mok

otów

(inc

l. Sł

użew

iec

Prze

mys

łow

y)

Wol

a

Oth

er

Poland data

Poland population 38.5 m

Warsaw metropolitan area population

2.7 m

Poland GDP growth 2013 (forecast)

2.1%

Poland inflation rate 2.4%

Poland unemployment rate 13.4%

Poland National Bank Reference rate

4.00%

PLN/EUR exchange rate 4.07

PLN/USD exchange rate 3.07Source: Poland Statistical Office/National Bank of Poland/IMF/OANDA. December 2012 data quoted unless otherwise stated.

2013 2014 2015

Source: Knight Frank

RESEARCH

Warsaw Joseph BorowskiManaging Partner +48 (22) 596 50 50 [email protected]

Monika A. DebskaChairman of the Board +48 (22) 596 50 50 [email protected]

Magdalena CzempińskaResearch +48 (22) 596 50 50 [email protected]

LondonChris BellManaging Director, Europe+44 (0) 207 629 [email protected]

Darren YatesPartner, International Research+44 (0) 207 629 [email protected]

Matthew ColbourneAssociate, International Research+44 (0) 207 629 [email protected]

Carly TompsettAnalyst, International Research+44 (0) 207 629 [email protected]

Knight Frank Research provides strategic advice, consultancy services and forecasting to a wide range of clients worldwide including developers, investors, funding organisations, corporate institutions and the public sector. All our clients recognise the need for expert independent advice customised to their specific needs.

Knight Frank Reports are also available at www.knightfrank.com

© Knight Frank LLP 2013

This report is published for general information only. Although high standards have been used in the preparation of the information, analysis, views and projections presented in this report, no legal responsibility can be accepted by Knight Frank Research or Knight Frank LLP for any loss or damage resultant from the contents of this document. As a general report, this material does not necessarily represent the view of Knight Frank LLP in relation to particular properties or projects. Reproduction of this report in whole or in part is allowed with proper reference to Knight Frank Research.

Knight Frank LLP is a limited liability partnership registered in England with registered number OC305934. Our registered office is 55 Baker Street, London, W1U 8AN, where you may look at a list of members’ names.

NewmarkKnight FrankGlobal

NewmarkKnight FrankGlobal

NewmarkKnight FrankGlobal

AmericasUSACanadaCaribbean

AustralasiaAustraliaNew Zealand

EuropeUKAustriaBelgiumCzech RepublicFranceGermanyIrelandItalyMonacoPolandPortugalRomaniaRussiaSpainSwitzerlandThe NetherlandsUkraine

AfricaBotswanaKenyaMalawiNigeriaSouth AfricaTanzaniaUgandaZambiaZimbabwe

AsiaCambodiaChinaHong KongIndiaIndonesiaMacauMalaysiaSingaporeSouth KoreaThailandVietnam

The GulfBahrainQatar UAE