Embed Size (px)

Citation preview

H1 2016 Results

7 September 2016

Confidential

This Presentation has been prepared by Zegona Communications plc (the “Company”) in connection with the financial performance of the Company for the 3 months and 6 months ended 30 June 2016. The forecast financial information contained herein was prepared expressly for use herein and is based on certain assumptions and management’s analysis of information available at the time that this presentation was prepared. No reliance may be placed, for any purposes whatsoever, on the information contained in this Presentation or on its completeness. While the information provided herein is believed to be accurate, no representation or warranty, express or implied, is given by or on behalf of the Company, or any of its directors, partners, officers, employees, advisers or any other persons as to the accuracy, fairness or sufficiency of the information or opinions contained in this presentation and (to the extent permitted by law) no responsibility is accepted by any of them for the accuracy or completeness of such information or for omissions from the presentation or for any other written or oral information transmitted or made available. Accordingly, save in the case of fraud, no liability is accepted for any errors, omissions or inaccuracies in such information or opinions. The information and opinions provided in this Presentation are provided as of the date of this Presentation and are subject to change. Certain statements in this Presentation are forward-looking statements. The forward-looking statements include statements typically containing the words “intends”, “expects”, “anticipates”, “targets”, “plans”, “estimates” and words of similar import. These forward-looking statements speak only as at the date of this Presentation. These statements are based on current expectations and beliefs and, by their nature, are subject to a number of known and unknown risks, uncertainties and assumptions that could cause actual results, performances and achievements of the Company and its subsidiaries to differ. The forward-looking statements are based on numerous assumptions regarding the Company’s present and future business strategies and environments in which the Company may operate in the future and such assumptions may or may not prove to be correct. No statement in this Presentation is intended, nor may it be construed, as a profit forecast. No one undertakes to update or revise such forward-looking statements.

Disclaimer

Summary

Zegona’s Strategy

Telecable H1 2016 Results

Shareholder Returns

Agenda

1

2

3

1

4

Zegona continues to see many attractive investment opportunities in European TMT

Telecable acquisition performing well • Results fully in line with full year guidance • 4.4% revenue growth • 10.6% Cash Flow growth*

Strong cash returns to shareholders • 4.5p dividend for 2016 confirmed

Opportunity to further improve cash flows with debt refinancing • Significant reduction in interest costs • Material impact on free cash flow

Significant shareholder value upside potential

Summary Telecable acquisition continues to deliver strong performance, on track for full year guidance

2

2

3

4

5

1

* Cash Flow is EBITDA minus Capex

Zegona’s Strategy…. A Reminder

Significant sector expertise

Extensive real world senior operational and public company management experience

Executive leadership over last 10 years in businesses that have created $25bn of shareholder value

Experienced Team with Proven Track Record

Investor friendly Buy-Fix-Sell strategy in European TMT

Focus on businesses that require active change and fundamental improvement to realise full value

Target significant long term growth in shareholder value

Buy-Fix-Sell Strategy

Attractive Market Opportunity

Changing market dynamics in telecommunications and media industry create multiple investment opportunities

Driven by consumer consumption, industry consolidation and convergence in European TMT

Over 60 companies of desired scale identified

Targeting acquisitions in £1-3bn EV range

Telecable 1st acquisition and early performance very encouraging

Many attractive additional opportunities but very disciplined approach as shareholder value No 1 priority

Well Positioned to Access Attractive Deals

Zegona acquired Telecable in 2015 for €640m and continues to see many attractive investment opportunities

3

1

4 3

2

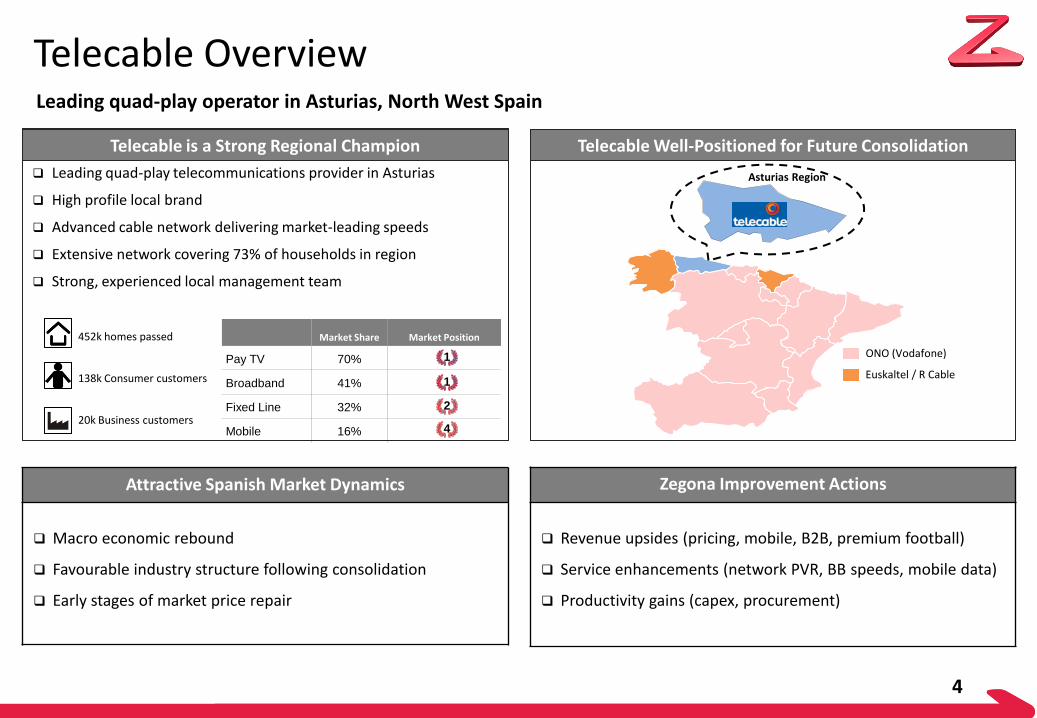

Attractive Spanish Market Dynamics

Macro economic rebound

Favourable industry structure following consolidation

Early stages of market price repair

Telecable Overview

Leading quad-play telecommunications provider in Asturias

High profile local brand

Advanced cable network delivering market-leading speeds

Extensive network covering 73% of households in region

Strong, experienced local management team

Telecable is a Strong Regional Champion Telecable Well-Positioned for Future Consolidation

452k homes passed

138k Consumer customers

20k Business customers

Market Share Market Position

Pay TV 70%

Broadband 41%

Fixed Line 32%

Mobile 16%

Asturias Region

1

1

2

4

Zegona Improvement Actions

Revenue upsides (pricing, mobile, B2B, premium football)

Service enhancements (network PVR, BB speeds, mobile data)

Productivity gains (capex, procurement)

4

Euskaltel / R Cable

ONO (Vodafone)

Leading quad-play operator in Asturias, North West Spain

€m

YoY Growth

€m

YoY Growth

Revenue 34.3 3.1% 69.2 4.4%

EBITDA 16.7 0.2% 33.3 1.9% % Revenue 49% 48%

Capex 5.1 - 16.7% 12.9 - 9.3% % Revenue 15% 19%

Cash Flow* 11.6 10.2% 20.4 10.6% % Revenue 34% 29%

Telecable Financial Results

Q2 2016 H1 2016

5

Note: A reconciliation between Telecable’s unaudited results and Zegona’s interim condensed consolidated financial statements for the six months ended 30 June 2016 is provided in Appendix C of Zegona’s Earnings Release

* Cash Flow is EBITDA minus Capex

In line with expectations, with continuing growth in Revenue, EBITDA and Cash flow

Telecable Operational Results Product and service enhancements driving KPI improvements

H1 2016

YoY Growth

Consumer*

Revenue (€m) 50.4 2.8%

Customers (AOP K) 139 -3.7%

ARPU (€/mth) 60.3 6.7%

RGUs (K) 450 -1.7%

Consumer Mobile

Revenue (€m) 13.6 7.7%

Postpaid lines (AOP k) 116 19.0%

Postpaid ARPU (€/mth) 19.5 -9.5%

Business**

Revenue (€m) 18.7 9.8%

Customers (AOP K) 20 3.4%

RGUs (K) 93 6.2%

ARPU (€/mth) 152 6.1%

High value customer base

Stable RGUs

ARPU growing with recent price increase in line with market

Strong growth with further upside given low market share

Prepaid to postpaid customer conversion program

Converged customers have lower churn/higher value

Impressive Business revenue growth

Growing RGUs per customer

Significant further potential given relatively low market share

Note: Telecable results are unaudited and based on management accounts for the period from 1 January 2016 to 30 June 2016

* Includes Consumer Mobile ** Includes Business Mobile and excludes other revenues 6

Significant Progress on Key Strategic Initiatives

7

Enhance Mobile Experience

Doubled mobile data allowances in January 2016 Continued Wifisfera take-up to 61k customers, up 17% YoY 19k consumer mobile postpaid YoY line adds (19% growth) Mobile penetration increased to 55% (from 51% end of 2015) Quadplay customers at record high of 36%

Improve Capex Productivity

Focus on sales distribution, network maintenance, self install Invest savings into revenue growth initiatives, e.g. BB speed Capex % revenue 19% in H1 2016 vs 22% in 2015 EBITDA – Capex % revenue now 29% vs 27% in 2015

Grow Consumer Revenues

Doubled min. BB speed to 200Mbps, launched 500Mbps Investment in best-in-class football offering: customers

increased by 18k YoY to 30k* Increased consumer prices by €2/mth in January 2016 7% ARPU growth, now at record high of €60/mth

Renewed Focus on Business Clients

Comprehensive product and management changes Football expansion into bars/ restaurants 10% revenue growth in H1 2016 Customers and ARPU growing strongly

2 1

3 4

* Includes OTT

Shareholder Returns - Dividend Confirmed

8

4.5p per share dividend confirmed

£8.8m full year payment

Half (2.25p/ £4.4m) to be paid in Oct 2016, balance in March 2017

Current dividend yield of 4.5%*

Intention to grow dividend on a progressive basis

2

3

4

1

5

* Based on share price of 99.95p as per 2 September 2016

£4.4m to be paid in October 2016 and a further £4.4m in March 2017

Shareholder Returns - Reduced Interest Costs

9

We are exploring the opportunity to refinance existing debt to significantly reduce interest costs

Potential Benefits

Over €4m reduction in interest costs

Circa 10% reduction in cost of capital

Potential for double digit free cash

flow increase2

1 Excludes €20m undrawn revolver capacity

2 Based on pro forma Telecable 2015 normalised free cash flow of €28m

Current Debt

€274m

Bullet in Aug 2022

4.25%

c.€12m

Very limited

Possible Refinancing

€274m

Amortising but back-ended

<3.00%

<€8m

Limited

Amount:1

Maturity: Interest Rate: Annual Cost: Covenants:

Shareholder Returns - Valuation Perspectives

10

1 Based on last twelve months Telecable EBITDA to June 2016. Using Zegona share price of 99.95p, FX rate 1.19 €/ £ as at 2 Sep 2016

2 Based on last twelve months pro forma EBITDA to June 2016 (including R Cable). Using Euskaltel share price of €8.03 as at 2 Sep 2016

Valuation multiple: Zegona June 2016 LTM EBITDA valuation multiple is only 7.3x1 vs Euskaltel at 9.3x2

Circa 50% shareholder value upside compared to Euskaltel rating

Growth: Telecable revenue growing faster than peers - growth of circa 3% in 2015 with acceleration to

mid single digit in 2016

Cash flow: Telecable generating strong Cash Flow Incremental upside post potential debt refinancing

Shareholder returns: Zegona dividend of 4.5p provides attractive yield

Additional capital returns potential

Forex gain: €/£ rate has improved from 1.40 at acquisition to 1.19, a gain of c.18% for Zegona shareholders

2

3

4

1

5

Many attractive investment opportunities for Zegona in European TMT

Telecable performing well in 2016, building on a robust 2015 performance

Strong cash returns and shareholder value upside potential

Conclusions

11

2

3

1