Embed Size (px)

Citation preview

© 2013 The Hackett Group, Inc.; All Rights Reserved. | CR_6000131 Procurement Executive Insight I The Hackett Group I 1

2013 Procurement Key Issues: Going Deeper and Broader to Deliver Borderless Procurement Services

In 2013, enterprises are trying to not just grow globally, but to balance local agility with global scale in their value chains. To do so, internal business services that support them must be equally borderless, from the geographic, organizational, technology and other standpoints.

Four imperatives were identified by participants in our 2013 Enterprise Key Issues Study:

• Fostering the agility required to achieve profit goals when revenue falls short of expectations, and to add value to procurement services without additional headcount or budget.

• Continuing to move toward a more standardized and global approach to the business and to procurement operations.

• Maturing the concepts of process ownership beyond the basics of process standardization, and creating value by working across functional, business unit and geographic borders.

• Obtaining insights, intelligence and actionable strategies from data generated by procurement activities.

It is likely that growth will always be the top priority for CEOs, but for the other senior executives (including procurement leaders) who participated in the study, improving operating margin actually overtook increasing revenue compared to 2012 (Fig. 1).

By Michel Janssen, Pierre Mitchell and Lynne Schneider

Procurement Executive Insight

January, 2013

Executive SummaryOf all the Hackett Key Issues Studies conducted in the last five years, the 2013 edition shows the greatest year-over-last change in priorities for both performance and capability-related issues. Procurement executives expect to be extremely busy in the coming year supporting the enterprise focus on profitable growth. In response, they are working to expand the quantity and quality of their organization’s spend influence via sourcing, category management and increasingly, supplier relationship management. Many of their priorities in the coming year will require greater cross-functional collaboration with business units, functional partners, Global Business Services groups and third parties. While priorities may vary based on individual enterprise strategies, in 2013 the overarching goal is to deliver more value without more resources.

Complim

entary Research

© 2013 The Hackett Group, Inc.; All Rights Reserved. | CR_6000131 Procurement Executive Insight I The Hackett Group I 2

The enterprise is looking under every stone for improvement opportunities. This of course helps set the agenda for procurement organizations to support. On the revenue and growth enablement front alone, procurement organizations have a broad spectrum of supplier engagement options planned to support enterprise strategies in 2013 (Fig. 2).

FIG. 1 Summary: Enterprise key issues in 2013

Source: Enterprise Key Issues Study, The Hackett Group, 2013

Improve operating margin 90%

88%

88%

83%

82%

82%

77%

77%

74%

68%

49%

Accelerate revenue growth

Largest increase

Improve customerservice/satisfaction

Reduce overhead cost

Increase operational agilityand flexibility

Enhance employee/talentretention and development

Improve cash flow/working capital

Reduce total supply chain cost

Manage enterprise risk

Grow emerging market presence

Achieve non-financial, social responsibilityand sustainability-related objectives

0 20 40 60 80 100

+/- 3% CHANGE FROM 2012

Percent of companies ranking issue as “important" or "extremely important"

FIG. 2 Procurement initiatives planned for next 12-24 months in support of the enterprise strategy

Source: Revenue/Growth Enablement Study, The Hackett Group, 2012

Joint ventures/strategic partnerships

Mergers & acquisitions

Ensuring value chain partners'ability to scale for growth

Improving brand perception(e.g., sustainability, diversity, etc.)

A strategic/business planning processeffectively supporting growth

and related initiatives

Finding new target industries, channelsand channel partners

Penetrating international markets

Pursuing game-changinginnovation/technology

Improving sales & marketingeffectiveness in existing channels

Developing/improving traditionalproducts and services

Strategic supplier partnering (e.g., JVs, joint IP licensing)

Supplier acquisitions

Supplier capability/capacity development

Supplier diversity;supplier sustainability

Supplier business reviews;supplier eventst

Supplier market intelligence

Supply base localization

Open innovation

Joint promotions;demand pull tactics

Early supplier involvementin design

Enterprise growth strategies

Related initiatives

Supplier-related activity

0 20 40 60 80 100

HIGH MODERATE

43%

36%

34%

28%

22%

25%

43%

36%

14%

14%

39%

43%

31%

34%

33%

46%

25%

32%

34%

21%

82%

79%

65%

62%

55%

71%

68%

68%

48%

35%

© 2013 The Hackett Group, Inc.; All Rights Reserved. | CR_6000131 Procurement Executive Insight I The Hackett Group I 3

The challenge will be finding a way to fund these strategic pursuits when staffing and budgets remain tight. Although revenue is expected to grow during 2012-2013, albeit slowing relative to 2011-2012, procurement budgets will be flat going into 2013, with operating budgets expected to drop by 0.40% and FTE levels by 0.50% (Fig. 3).

Since procurement, like other functions, is being required to do more with less, it will need to do things differently. Based on the Key Issues Study findings, there is plenty of change on the horizon:

• Globalizing value chains means globalizing direct as well as indirect procurement re-sources that are increasingly part of a broader business services delivery group, such as a Global Business Services organization.1 Companies have average of 12% of their FTEs already located in low-cost regions, a number that is expected to reach 21% in within two years.

• Roughly one-third to one-half of companies have created a global design for policy/strategy standards, process designs, technology platforms, KPIs and master data man-agement (MDM) – with plans to increase those levels to 50-60% within three years.

• KPIs, MDM and near-real-time analytics are key to enabling closed-loop performance management processes for the enterprise (i.e., enterprise performance management, or EPM) or for procurement/supply chain (which Hackett calls “supply performance management”).2 Timely analytics are not always easy to come by in large, global en-terprises. In our recent globalization study, we found that 80% of top-quartile perform-ers offer visibility in near real-time or within one day, compared to only 28% of the peer group.

• Since a one-size-fits-all procurement Service Delivery Model (SDM) is insufficient for the complex needs of large organizations, the ability to mass-customize procurement processes as services by category, stakeholder, contract type, buy-pay channel, ge-ography, etc., is paramount. Using a procurement SDM to design tailored services for end-to-end processes is a key principle behind enterprise process ownership (some-times known as “global process ownership”) and Global Business Services strategies. In the study, we found that 21% of procurement organizations are scoping their enter-prise process ownership to cross-functional, end-to-end processes (e.g., purchase-to-pay or source-to-settle).

Building these new capabilities is not easy, and procurement, perhaps more than any other function, realizes the importance of tailoring its approach to influence stakeholders and help them gain better performance outcomes. This means helping to maximize the

FIG. 3 Projected changes in revenue, procurement budgets and headcount

Overall revenue growth Procurement operatingbudget

Number of staff (FTEs) in the procurement function

Source: Key Issues Study, The Hackett Group, 2013

7.9%

6.5%

1.16%0.31%

-0.40%

2012 COMPARED TO 2011

-0.50% -1012345678

2013 COMPARED TO 2012

1 In 2012, The Hackett Group conducted a globalization research study and created an associated Globaliza-tion Index to measure the extent of globalization of the enterprise operating model; globalization of business services delivery (including procurement); and finally, the degree of alignment between the two.

© 2013 The Hackett Group, Inc.; All Rights Reserved. | CR_6000131 Procurement Executive Insight I The Hackett Group I 4

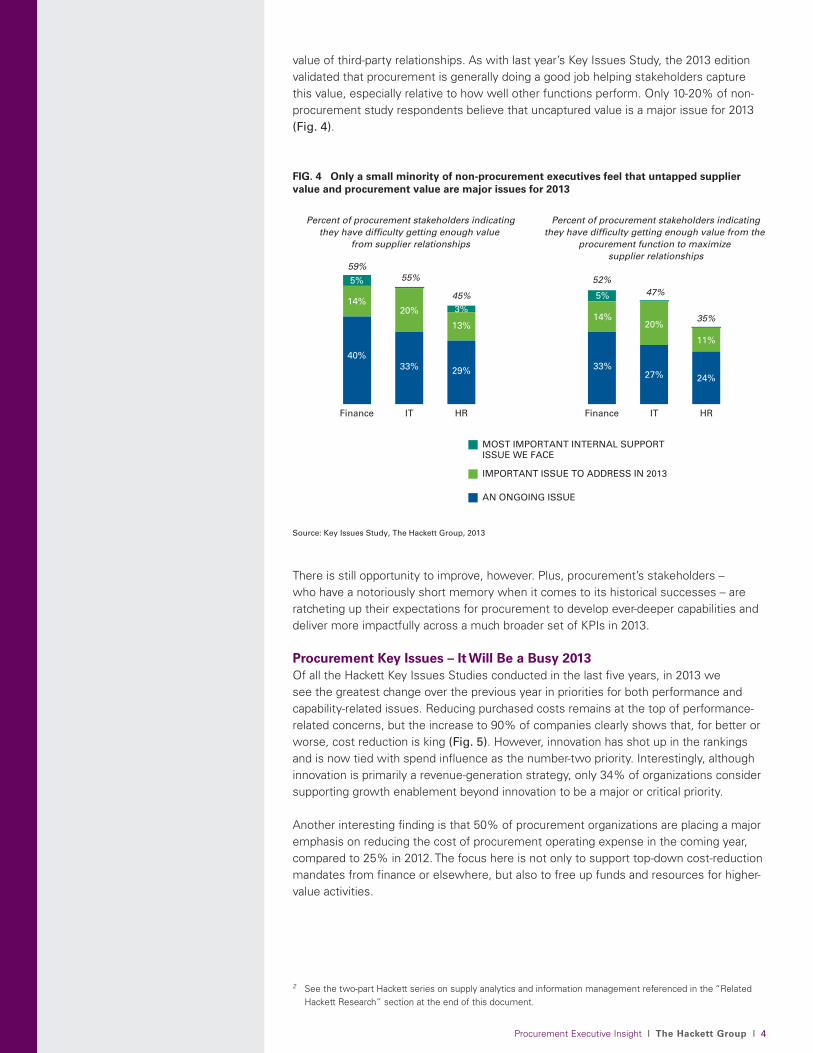

value of third-party relationships. As with last year’s Key Issues Study, the 2013 edition validated that procurement is generally doing a good job helping stakeholders capture this value, especially relative to how well other functions perform. Only 10-20% of non-procurement study respondents believe that uncaptured value is a major issue for 2013 (Fig. 4).

There is still opportunity to improve, however. Plus, procurement’s stakeholders – who have a notoriously short memory when it comes to its historical successes – are ratcheting up their expectations for procurement to develop ever-deeper capabilities and deliver more impactfully across a much broader set of KPIs in 2013.

Procurement Key Issues – It Will Be a Busy 2013Of all the Hackett Key Issues Studies conducted in the last five years, in 2013 we see the greatest change over the previous year in priorities for both performance and capability-related issues. Reducing purchased costs remains at the top of performance-related concerns, but the increase to 90% of companies clearly shows that, for better or worse, cost reduction is king (Fig. 5). However, innovation has shot up in the rankings and is now tied with spend influence as the number-two priority. Interestingly, although innovation is primarily a revenue-generation strategy, only 34% of organizations consider supporting growth enablement beyond innovation to be a major or critical priority.

Another interesting finding is that 50% of procurement organizations are placing a major emphasis on reducing the cost of procurement operating expense in the coming year, compared to 25% in 2012. The focus here is not only to support top-down cost-reduction mandates from finance or elsewhere, but also to free up funds and resources for higher-value activities.

2 See the two-part Hackett series on supply analytics and information management referenced in the “Related Hackett Research” section at the end of this document.

FIG. 4 Only a small minority of non-procurement executives feel that untapped supplier value and procurement value are major issues for 2013

Percent of procurement stakeholders indicatingthey have difficulty getting enough value

from supplier relationships

Percent of procurement stakeholders indicatingthey have difficulty getting enough value from the

procurement function to maximize supplier relationships

Source: Key Issues Study, The Hackett Group, 2013

0

10

20

30

40

50

60

0

10

20

30

40

50

6040%

Finance IT HR Finance IT HR

33% 29% 33%27% 24%

11%

20%14%

5%

13%

3%20%14%

5%

AN ONGOING ISSUE

IMPORTANT ISSUE TO ADDRESS IN 2013

MOST IMPORTANT INTERNAL SUPPORT ISSUE WE FACE

59%55%

45%

52%47%

35%

© 2013 The Hackett Group, Inc.; All Rights Reserved. | CR_6000131 Procurement Executive Insight I The Hackett Group I 5

Managing supply risk has also increased in priority as a means of profit protection. Supplier compliance is receiving particular attention, with an emphasis on efficient management of cross-functional workflows relating to regulatory requirements and supplier compliance with performance expectations. These processes create headaches for suppliers and buyers alike, and can detract from strategic value creation when participants are bogged down in processing paper and spreadsheets. Building such capabilities is a combination of process change (e.g., using supplier stratification to tailor workflows and information), master data management, analytics, measurement systems and more, and leads naturally to the topic of improving procurement capabilities in 2013 (Fig. 6).

FIG. 5 Key procurement performance-related issues in 2013

Percent of organizations citing issue as “major” or “critical”

Source: The Hackett Group 2013 Key Issues Study

0 20 40 60 80 100

Reduce/avoid purchased costs72%

90%

53%

76%

44%

76%

51%

69%

42%

56%

39%

52%

40%

52%

25%

50%

32%

34%

20%

26%

Expand purchasing’s scope/influence

Increase innovation and product/service support

Deepen influence on complex indirectspend categories

Reduce supply risk

Drive more value frompurchase-to-pay process

Free up cash

Reduce procurementoperating cost

Enable growthbeyond innovation

Environmental sustainabilityor supplier diversity

20132012

© 2013 The Hackett Group, Inc.; All Rights Reserved. | CR_6000131 Procurement Executive Insight I The Hackett Group I 6

As episodic sourcing activity is broadening to a life cycle-based category management approach, new capabilities must be built, including broader supplier relationship management (SRM), deeper supplier/market intelligence (and associated analytics), and the way in which these knowledge-based processes can be delivered as services in a scalable way. The idea is to set up a “one-to-many” approach through a Center of Excellence (CoE) serving both procurement and its stakeholders. A good example is supply market intelligence (SMI), in which a CoE supports multiple value objectives including reducing risk, speeding up sourcing, improving negotiations, supporting new-market entry and competitive intelligence scenarios. It might be provided to category managers who then use it to serve their stakeholders; alternatively, it might serve enterprise strategic planning staff or others. Building such a major capability requires a major effort involving implementation of many lower-level capabilities (Fig. 7).

FIG. 6 Strategic priority of capability-related issues in 2013

Percent of organizations citing issue as “major” or “critical”

Source: Key Issues Study, The Hackett Group, 2013

0 20 40 60 80 100

Strategic sourcing 71%

88%

58%

81%

53%

64%

52%

64%

43%

57%

34%

56%

38%

50%

32%

45%

26%

43%

19%

34%

17%

33%

23%

14%

Category management

Supplier relationship management (SRM)

Value contribution visibility

Upgrade of talent/skills

Supply market intelligence

Continuous imprvovement

Upgrading technology tools

Procurement shared services/CoEs/BPO/globalization

Upgrading information capabilities

Process sourcing/placement

20132012

Knowledge management

© 2013 The Hackett Group, Inc.; All Rights Reserved. | CR_6000131 Procurement Executive Insight I The Hackett Group I 7

Of course, SMI is only one type of capability that is being established in CoEs (Fig. 8). Sourcing workflow support (including tactical sourcing and “buying desks”), analytics, knowledge management, benchmarking, training and other areas are similarly popular. CoEs can be run in the procurement organization, corporate headquarters, the Global Business Services organization or even in business units (the latter via a virtual model, in which resources report through the CoE but remain at their normal work location).

FIG. 7 Supply market intelligence (SMI) capability-building priorities

SM

I typ

esS

MI s

trat

egie

s

Source: Key Issues Study, The Hackett Group, 2013

Other

Tying SMI to broader corporatecompetitive/MI efforts

Increasing executive awareness,buy-in and funding

Mining social media and other external sitesfor specific intelligence

Ensuring the company minimizes its footprintin intelligence posted externally

Communicating of SMI externally to interested stakeholders

Communicating of SMI internallywithin procurement

Using third-party content more cost-effectively

Building custom internal intelligence/KM platform

Integrating analytic applications toexternal intelligence

Improving how intelligence is tied toprocesses and job roles

Category-specific pricing indices

Monitoring supply marketsfor innovation/growth possibilities

Category/industry trends and events

Third-party category knowledge/intelligence reports

Supplier-specific financial/risk intelligence

0 10 20 30 40 50 60 70 80

SOME FOCUS IN 2013 MAJOR FOCUS IN 2013

31%

35%

23%

32%

31%

35%

39%

42%

40%

31%

35%

37%

40%

31%

34%

31%

31%

23%

34%

24%

24%

16%

11%

8%

8%

16%

11%

8%

5%

13%

8%

2%

62%

58%

57%

56%

55%

51%

50%

50%

48%

47%

46%

45%

44%

42%

33%

45%

© 2013 The Hackett Group, Inc.; All Rights Reserved. | CR_6000131 Procurement Executive Insight I The Hackett Group I 8

Strategic ImplicationsIt is clear from the 2013 Key Issues Study that procurement is going to be very busy in the coming year, not only just to stay in step with the business, but also to build capabilities for the longer term. The three areas of capability-building receiving the most attention are category management, supplier relationship management (SRM) and improving the source-to-settle operating model. Most procurement organizations have a weaker formal mandate than they would like in these areas, but the smartest among them have learned to be opportunistic, using external events and internal business initiatives to provide the impetus for building new capabilities. They are also more deliberate in systematizing newly built capabilities in order to extend them to additional areas of spend and stakeholder engagement.

Unquestionably, this continual process of broadening procurement’s value objectives, scorecard and capabilities is arduous. More than brute strength, flexibility will help the procurement organization go global in step with the business.

FIG. 8 Competencies and services offered in procurement Centers of Excellence(percent of companies)

Source: The Hackett Group, 2012

IN PLACE, WORKING WELL

A FOCUS IN 2013 A FOCUS IN 2013 (TO INTEGRATE WITH CORPORATE CoE/GBS)

NOT A FOCUS AREA

Supplier support/help-desk

Specialized domains(e.g., logistics, asset disposition)

Talent management

Finance-specific(e.g., costing, auditing, working capital)

Contract/commercial excellence

Program/project management

Continuous improvement support(e.g., Lean/Six Sigma)

Benchmarking, KPIs,value measurement/tracking

Technology support

Knowledge management

Regulatory compliance(if different from supply risk)

Supply market intelligence (SMI)

Analytics

Specialized sourcing support

0 20 40 60 80 100 120

28%

29%

35%

35%

39%

42%

43%

45%

47%

47%

52%

54%

58%

59%

15%

14%

33%

11%

26%

19%

24%

35%

19%

35%

12%

25%

29%

22%

7%

5%

7%

4%

9%

7%

6%

7%

9%

6%

7%

4%

4%

4%

50%

52%

25%

50%

27%

32%

27%

12%

25%

11%

28%

18%

8%

16%

© 2013 The Hackett Group, Inc.; All Rights Reserved. | CR_6000131 Procurement Executive Insight I The Hackett Group I 9

About the Advisors

Michel Janssen

Principal and Chief Research Officer

Mr. Janssen is responsible for developing The Hackett Group’s core intellectual property, including thought leadership. He works with the company’s Executive Advisory Council to understand the strategic impact of new and emerging trends on the business functions. He also heads Hackett’s team of researchers and analysts in the US, Europe and India in the design and implementation of research studies; analysis of

results; and production of resulting findings. Previously Mr. Janssen was president of Supplier Solutions for Everest Group and co-founded the Everest Research Institute. In addition, he provided strategic oversight for Everest’s Outsourcing Center, the world’s largest outsourcing community and vehicle for identifying early industry trends. He was also a senior director in Gartner Group’s Strategic Sourcing practice and held numerous management positions with EDS.

Pierre Mitchell

Senior Director, Procurement Research

Mr. Mitchell is responsible for leading the development of research and other intellectual property within Hackett’s Procurement Executive Advisory Program, where he also serves as an adjunct business advisor. He has over 20 years of industry and consulting experience in procurement, supply chain and information technology. Mr. Mitchell is quoted widely in the press and speaks at numerous industry events on

supply management trends and technologies. Previously he was vice president of supply management research at AMR Research and a manager at Arthur D. Little, where he led numerous supply chain and procurement transformations at Fortune 500 companies. Other industry positions include manufacturing project manager at The Timberland Company, materials manager at Krupp Companies and engineer at EG&G Torque Systems.

Related Research“Unlimited Options to Realize Borderless Business Services: Distilling the Key Issues of 2013,” January 2013

“Procurement Centers of Excellence,” December 2012

“The Case for Enterprise Process Ownership: Spotlight on the Purchase-to-Pay Process,” November 2012

“World-Class Supply Analytics and Information Management, Part 1: Analytics,” May 2012

“World-Class Supply Analytics and Information Management, Part 2: Supply Information Management,” May 2012

© 2013 The Hackett Group, Inc.; All Rights Reserved. | CR_6000131 Procurement Executive Insight I The Hackett Group I 10

For more papers, perspectives and research, please visit: www.thehackettgroup.com Or to learn more about The Hackett Group and how we can help your company sharply reduce costs while improving business effectiveness, please contact us at 1 866 614 6901 (U.S.) or +44 20 7398 9100 (U.K.).

The Hackett Group, a global strategic advisory firm, is a leader in best practice implementation, advisory, benchmarking, and transformation

consulting services, including shared services, offshoring and outsourcing advice. Utilizing best practices and implementation insights from

more than 7,500 benchmarking engagements, executives use The Hackett Group’s empirically based approach to quickly define and prioritize

initiatives to enable world-class performance. Through its REL brand, it offers working capital solutions focused on delivering significant cash flow

improvements. The Hackett Group offers business application consulting services that helps maximize returns on IT investments. It has worked

with 2,700 major corporations and government agencies, including 97% of the Dow Jones Industrials, 84% of the Fortune 100, 80% of the DAX

30 and 49% of the FTSE 100. Founded in 1991, The Hackett Group was acquired by Answerthink, which was renamed The Hackett Group in 2008.

The Hackett Group has global offices in the United States, Europe, Australia and India and is publicly traded on the NASDAQ as HCKT.

Email: [email protected]

www.thehackettgroup.com

Atlanta +1 770 225 3600 London +44 20 7398 9100

Amsterdam I Budapest | Atlanta I Chicago I Frankfurt I Hyderabad I London I Melbourne I New York I Paris I Philadelphia I San Francisco I Sydney

© 2013 The Hackett Group, Inc.; All Rights Reserved. | CR_6000131

This publication has been prepared for general guidance on the matters addressed herein. It does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice.

Procurement Executive Insight I The Hackett Group I 10

Lynne Schneider

Senior Research Director

Ms. Schneider is responsible for leading the development of research and other intellectual property for multiple programs. She has worked in consulting and related research for over 20 years. Her previous positions included Director of Research for Kennedy Consulting Research and Advisory, as well as a variety of internal and external consulting positions with international companies. As Director of Business Process

Improvement at American Greetings, Ms. Schneider managed a portfolio of strategic and operations projects, including both staff and line functions. She was also a senior consultant in Towers Watson’s Organization Effectiveness practice and a consultant in the Change Management practice at Accenture.