Embed Size (px)

Citation preview

PA International Property Consultants Sdn Bhd

GUIDELINES

1. EPF WITHDRAWALS FOR HOUSING USE

2. GUIDELINE ON THE ACQUISITION OF PROPERTIES

BY FOREIGN INTERESTS

3. MALAYSIA MY SECOND HOME (MM2H)

4. REAL PROPERTY GAINS TAX

5. MY FIRST HOME SCHEME

PA International Property Consultants Sdn Bhd

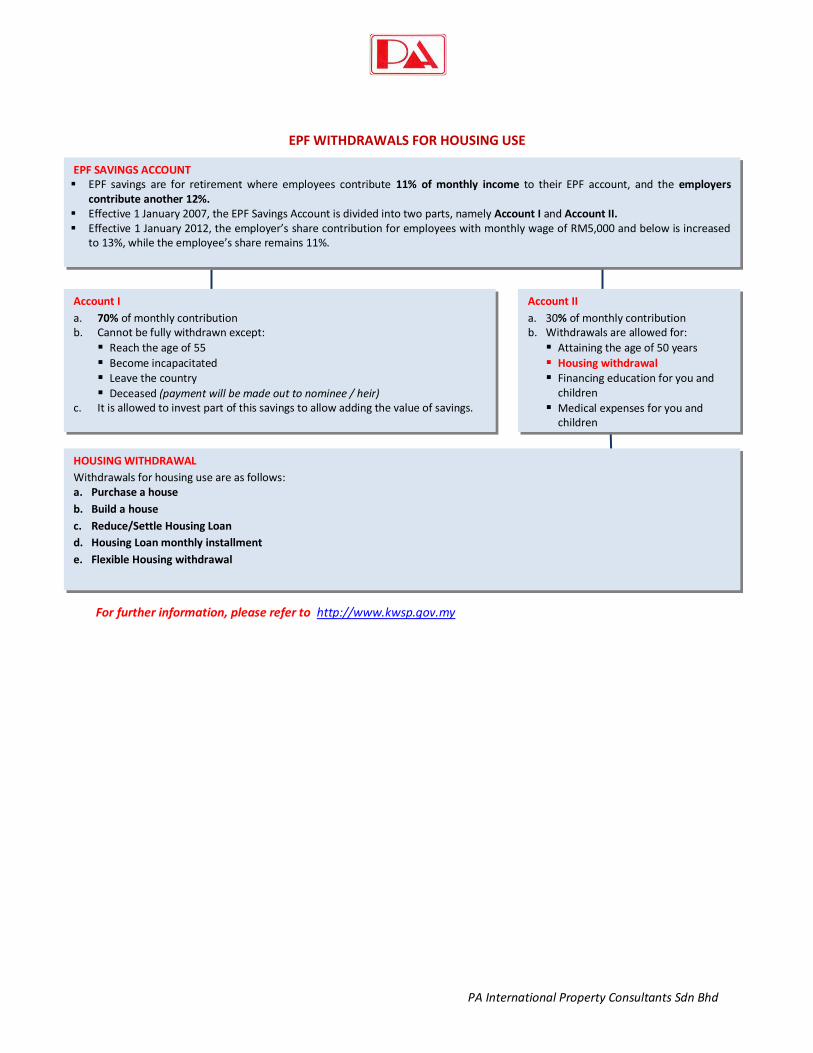

EPF WITHDRAWALS FOR HOUSING USE

For further information, please refer to http://www.kwsp.gov.my

Account I

a. 70% of monthly contribution b. Cannot be fully withdrawn except:

Reach the age of 55

Become incapacitated Leave the country

Deceased (payment will be made out to nominee / heir) c. It is allowed to invest part of this savings to allow adding the value of savings.

Account II

a. 30% of monthly contribution b. Withdrawals are allowed for:

Attaining the age of 50 years

Housing withdrawal Financing education for you and

children

Medical expenses for you and children

HOUSING WITHDRAWAL

Withdrawals for housing use are as follows: a. Purchase a house

b. Build a house

c. Reduce/Settle Housing Loan

d. Housing Loan monthly installment

e. Flexible Housing withdrawal

EPF SAVINGS ACCOUNT EPF savings are for retirement where employees contribute 11% of monthly income to their EPF account, and the employers

contribute another 12%. Effective 1 January 2007, the EPF Savings Account is divided into two parts, namely Account I and Account II. Effective 1 January 2012, the employer’s share contribution for employees with monthly wage of RM5,000 and below is increased

to 13%, while the employee’s share remains 11%.

PA International Property Consultants Sdn Bhd

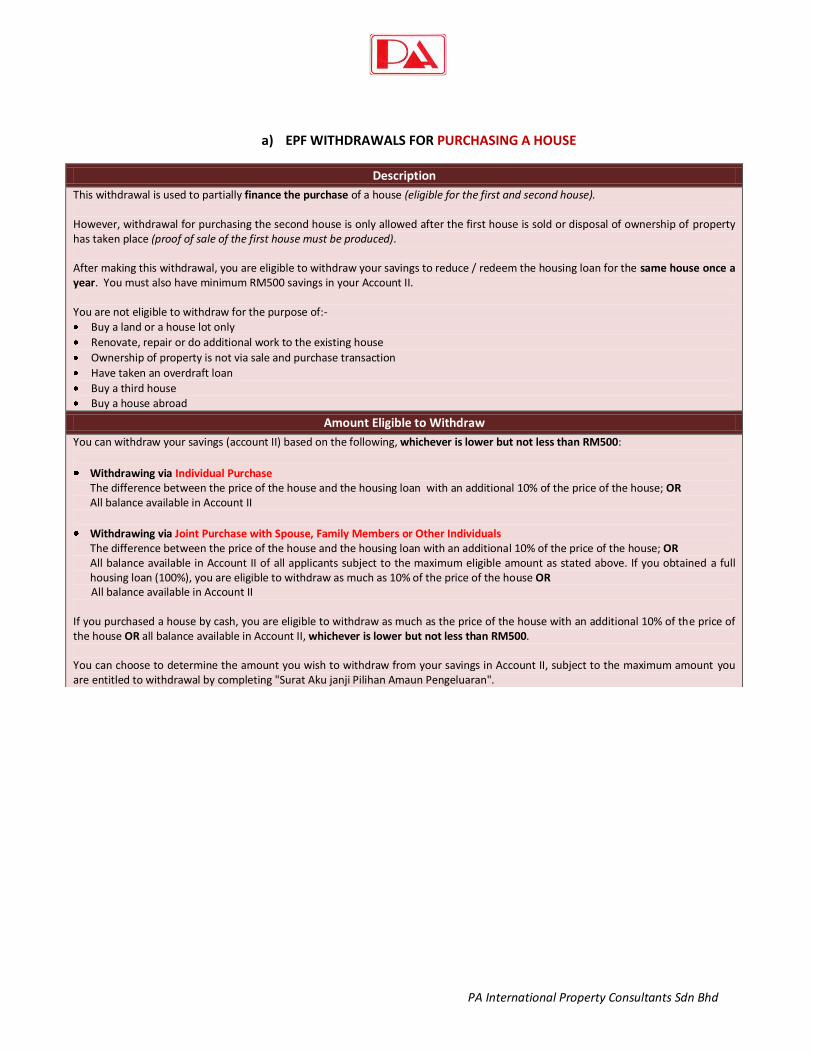

a) EPF WITHDRAWALS FOR PURCHASING A HOUSE

Description

This withdrawal is used to partially finance the purchase of a house (eligible for the first and second house). However, withdrawal for purchasing the second house is only allowed after the first house is sold or disposal of ownership of property has taken place (proof of sale of the first house must be produced). After making this withdrawal, you are eligible to withdraw your savings to reduce / redeem the housing loan for the same house once a year. You must also have minimum RM500 savings in your Account II. You are not eligible to withdraw for the purpose of:- Buy a land or a house lot only

Renovate, repair or do additional work to the existing house

Ownership of property is not via sale and purchase transaction

Have taken an overdraft loan

Buy a third house Buy a house abroad

Amount Eligible to Withdraw

You can withdraw your savings (account II) based on the following, whichever is lower but not less than RM500:

Withdrawing via Individual Purchase The difference between the price of the house and the housing loan with an additional 10% of the price of the house; OR All balance available in Account II

Withdrawing via Joint Purchase with Spouse, Family Members or Other Individuals The difference between the price of the house and the housing loan with an additional 10% of the price of the house; OR All balance available in Account II of all applicants subject to the maximum eligible amount as stated above. If you obtained a full housing loan (100%), you are eligible to withdraw as much as 10% of the price of the house OR All balance available in Account II

If you purchased a house by cash, you are eligible to withdraw as much as the price of the house with an additional 10% of the price of the house OR all balance available in Account II, whichever is lower but not less than RM500. You can choose to determine the amount you wish to withdraw from your savings in Account II, subject to the maximum amount you are entitled to withdrawal by completing "Surat Aku janji Pilihan Amaun Pengeluaran".

PA International Property Consultants Sdn Bhd

b) EPF WITHDRAWALS TO BUILD A HOUSE

Description

This withdrawal is used to finance the construction of a house (eligible for the first and second house). However, withdrawal for purchasing the second house is only allowed after the first house is sold or disposal of ownership of property has taken place (proof of sale of the first house must be produced). After making this withdrawal, you are eligible to withdraw your savings to reduce / redeem the housing loan for the same house once a year. You must also have minimum RM500 savings in your Account II. You are not eligible to withdraw for the purpose of:- Buy a land or a house lot only

Renovate, repair or do additional work to the existing house

Have taken an overdraft loan

Build a third house

Build a house abroad

Amount Eligible to Withdraw

You can withdraw your savings based on the following, whichever is lower but not less than RM500:

Withdrawing via Individual Construction The difference between the construction cost of the house and the housing loan with an additional 10% of the construction cost ; OR All balance available in Account II.

Withdrawing via Joint Construction with Spouse The difference between the construction cost of the house and the housing loan with an additional 10% of the construction cost; OR All balance available in Account II of all applicants, subject to the maximum eligible amount as stated above.

If you obtained a full housing loan (100%), you are eligible to withdraw as much as 10% of the cost of construction of the house or all balance available in Account II, whichever is lower but not less than RM500. If you self-financed the construction of the house (by cash), you are eligible to withdraw as much as the construction cost of the house with an additional 10% of the construction cost or all balance available in Account II, whichever is lower but not less than RM500. You can choose to determine the amount you wish to withdraw from your savings in Account II, subject to the maximum amount you are entitled to withdrawal by completing "Surat Aku janji Pilihan Amaun Pengeluaran".

PA International Property Consultants Sdn Bhd

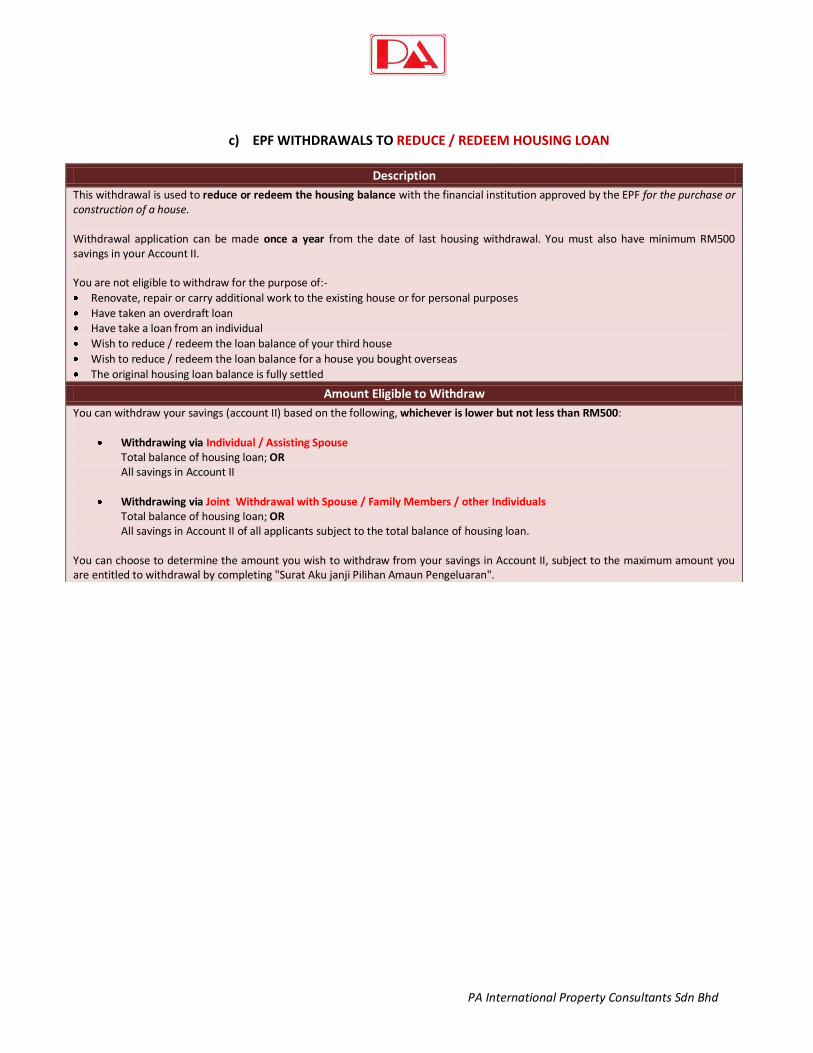

c) EPF WITHDRAWALS TO REDUCE / REDEEM HOUSING LOAN

Description

This withdrawal is used to reduce or redeem the housing balance with the financial institution approved by the EPF for the purchase or construction of a house. Withdrawal application can be made once a year from the date of last housing withdrawal. You must also have minimum RM500 savings in your Account II. You are not eligible to withdraw for the purpose of:-

Renovate, repair or carry additional work to the existing house or for personal purposes

Have taken an overdraft loan Have take a loan from an individual

Wish to reduce / redeem the loan balance of your third house

Wish to reduce / redeem the loan balance for a house you bought overseas

The original housing loan balance is fully settled

Amount Eligible to Withdraw

You can withdraw your savings (account II) based on the following, whichever is lower but not less than RM500:

Withdrawing via Individual / Assisting Spouse Total balance of housing loan; OR All savings in Account II

Withdrawing via Joint Withdrawal with Spouse / Family Members / other Individuals Total balance of housing loan; OR All savings in Account II of all applicants subject to the total balance of housing loan.

You can choose to determine the amount you wish to withdraw from your savings in Account II, subject to the maximum amount you are entitled to withdrawal by completing "Surat Aku janji Pilihan Amaun Pengeluaran".

PA International Property Consultants Sdn Bhd

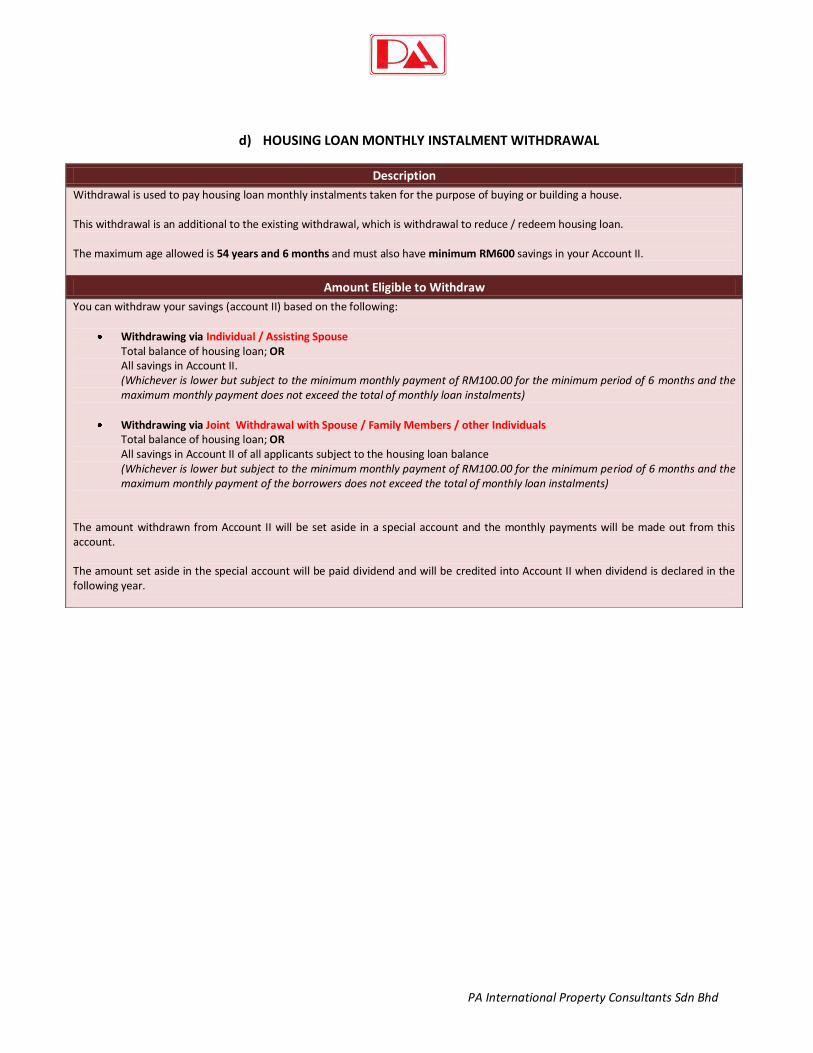

d) HOUSING LOAN MONTHLY INSTALMENT WITHDRAWAL

Description

Withdrawal is used to pay housing loan monthly instalments taken for the purpose of buying or building a house. This withdrawal is an additional to the existing withdrawal, which is withdrawal to reduce / redeem housing loan. The maximum age allowed is 54 years and 6 months and must also have minimum RM600 savings in your Account II.

Amount Eligible to Withdraw

You can withdraw your savings (account II) based on the following:

Withdrawing via Individual / Assisting Spouse Total balance of housing loan; OR All savings in Account II. (Whichever is lower but subject to the minimum monthly payment of RM100.00 for the minimum period of 6 months and the maximum monthly payment does not exceed the total of monthly loan instalments)

Withdrawing via Joint Withdrawal with Spouse / Family Members / other Individuals Total balance of housing loan; OR All savings in Account II of all applicants subject to the housing loan balance (Whichever is lower but subject to the minimum monthly payment of RM100.00 for the minimum period of 6 months and the maximum monthly payment of the borrowers does not exceed the total of monthly loan instalments)

The amount withdrawn from Account II will be set aside in a special account and the monthly payments will be made out from this account. The amount set aside in the special account will be paid dividend and will be credited into Account II when dividend is declared in the following year.

PA International Property Consultants Sdn Bhd

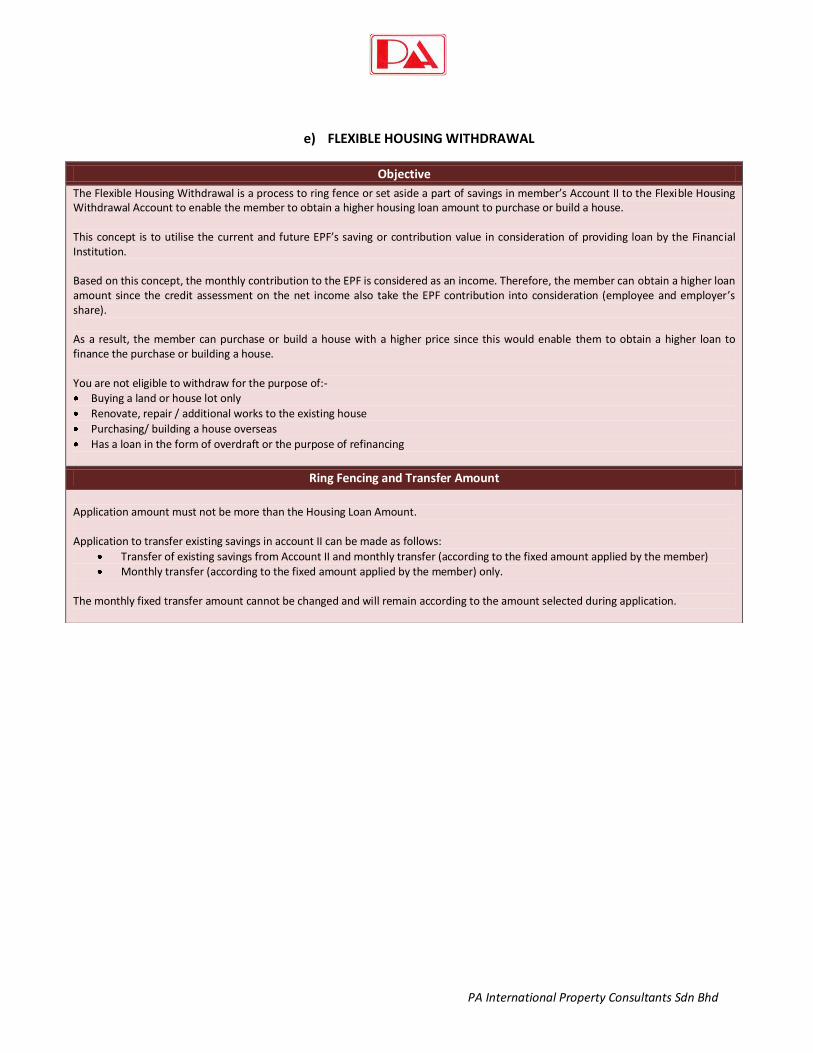

e) FLEXIBLE HOUSING WITHDRAWAL

Objective

The Flexible Housing Withdrawal is a process to ring fence or set aside a part of savings in member’s Account II to the Flexible Housing Withdrawal Account to enable the member to obtain a higher housing loan amount to purchase or build a house. This concept is to utilise the current and future EPF’s saving or contribution value in consideration of providing loan by the Financial Institution. Based on this concept, the monthly contribution to the EPF is considered as an income. Therefore, the member can obtain a higher loan amount since the credit assessment on the net income also take the EPF contribution into consideration (employee and employer’s share). As a result, the member can purchase or build a house with a higher price since this would enable them to obtain a higher loan to finance the purchase or building a house. You are not eligible to withdraw for the purpose of:- Buying a land or house lot only

Renovate, repair / additional works to the existing house

Purchasing/ building a house overseas

Has a loan in the form of overdraft or the purpose of refinancing

Ring Fencing and Transfer Amount

Application amount must not be more than the Housing Loan Amount. Application to transfer existing savings in account II can be made as follows:

Transfer of existing savings from Account II and monthly transfer (according to the fixed amount applied by the member) Monthly transfer (according to the fixed amount applied by the member) only.

The monthly fixed transfer amount cannot be changed and will remain according to the amount selected during application.

PA International Property Consultants Sdn Bhd

GUIDELINE ON THE ACQUISITION OF PROPERTIES

BY FOREIGN INTERESTS

This Guideline is to clarify the procedure on the acquisition of properties.

Foreign interest means any interest, associated group of interests or parties acting in concert which comprises:

Non Malaysian citizen; or

Permanent Resident (Non Malaysian citizen and has been granted Permanent Resident status by the

Malaysia Government); or

Foreign companies or institution; or

Companies incorporated in Malaysia with more than 50% owned by the above three definitions

The guideline is divided into the following categories: -

a) ACQUISITION OF PROPERTY

b) EXEMPTIONS / RESTRICTION

For further information, please refer to http://www.epu.jpm.my/

PA International Property Consultants Sdn Bhd

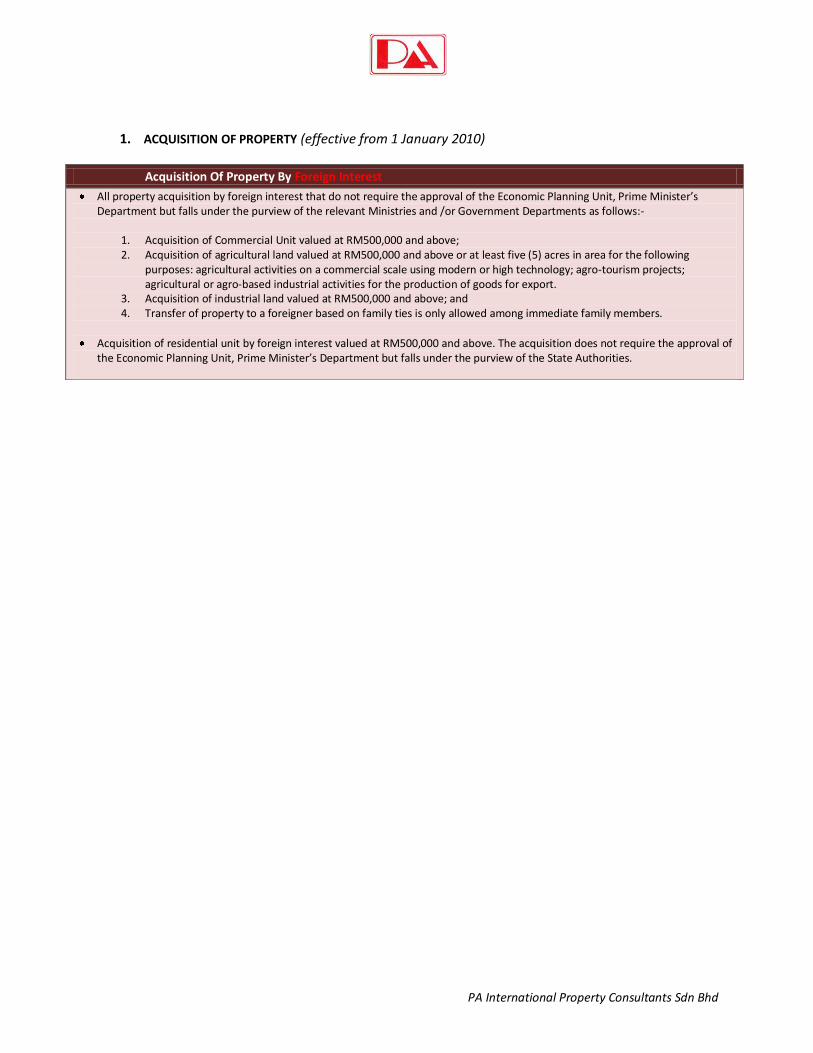

1. ACQUISITION OF PROPERTY (effective from 1 January 2010)

Acquisition Of Property By Foreign Interest

All property acquisition by foreign interest that do not require the approval of the Economic Planning Unit, Prime Minister’s Department but falls under the purview of the relevant Ministries and /or Government Departments as follows:-

1. Acquisition of Commercial Unit valued at RM500,000 and above; 2. Acquisition of agricultural land valued at RM500,000 and above or at least five (5) acres in area for the following

purposes: agricultural activities on a commercial scale using modern or high technology; agro-tourism projects; agricultural or agro-based industrial activities for the production of goods for export.

3. Acquisition of industrial land valued at RM500,000 and above; and 4. Transfer of property to a foreigner based on family ties is only allowed among immediate family members.

Acquisition of residential unit by foreign interest valued at RM500,000 and above. The acquisition does not require the approval of the Economic Planning Unit, Prime Minister’s Department but falls under the purview of the State Authorities.

PA International Property Consultants Sdn Bhd

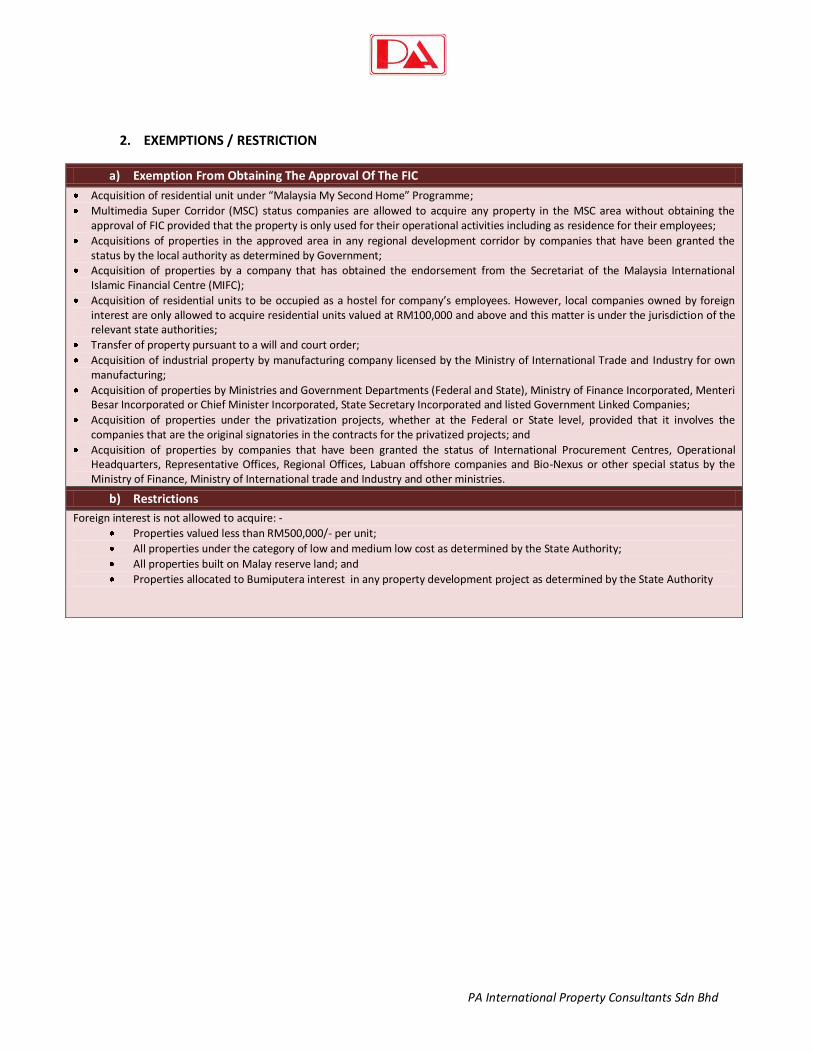

2. EXEMPTIONS / RESTRICTION

a) Exemption From Obtaining The Approval Of The FIC

Acquisition of residential unit under “Malaysia My Second Home” Programme;

Multimedia Super Corridor (MSC) status companies are allowed to acquire any property in the MSC area without obtaining the approval of FIC provided that the property is only used for their operational activities including as residence for their employees;

Acquisitions of properties in the approved area in any regional development corridor by companies that have been granted the status by the local authority as determined by Government;

Acquisition of properties by a company that has obtained the endorsement from the Secretariat of the Malaysia International Islamic Financial Centre (MIFC);

Acquisition of residential units to be occupied as a hostel for company’s employees. However, local companies owned by foreign interest are only allowed to acquire residential units valued at RM100,000 and above and this matter is under the jurisdiction of the relevant state authorities;

Transfer of property pursuant to a will and court order;

Acquisition of industrial property by manufacturing company licensed by the Ministry of International Trade and Industry for own manufacturing;

Acquisition of properties by Ministries and Government Departments (Federal and State), Ministry of Finance Incorporated, Menteri Besar Incorporated or Chief Minister Incorporated, State Secretary Incorporated and listed Government Linked Companies;

Acquisition of properties under the privatization projects, whether at the Federal or State level, provided that it involves the companies that are the original signatories in the contracts for the privatized projects; and

Acquisition of properties by companies that have been granted the status of International Procurement Centres, Operational Headquarters, Representative Offices, Regional Offices, Labuan offshore companies and Bio-Nexus or other special status by the Ministry of Finance, Ministry of International trade and Industry and other ministries.

b) Restrictions

Foreign interest is not allowed to acquire: -

Properties valued less than RM500,000/- per unit;

All properties under the category of low and medium low cost as determined by the State Authority;

All properties built on Malay reserve land; and

Properties allocated to Bumiputera interest in any property development project as determined by the State Authority

PA International Property Consultants Sdn Bhd

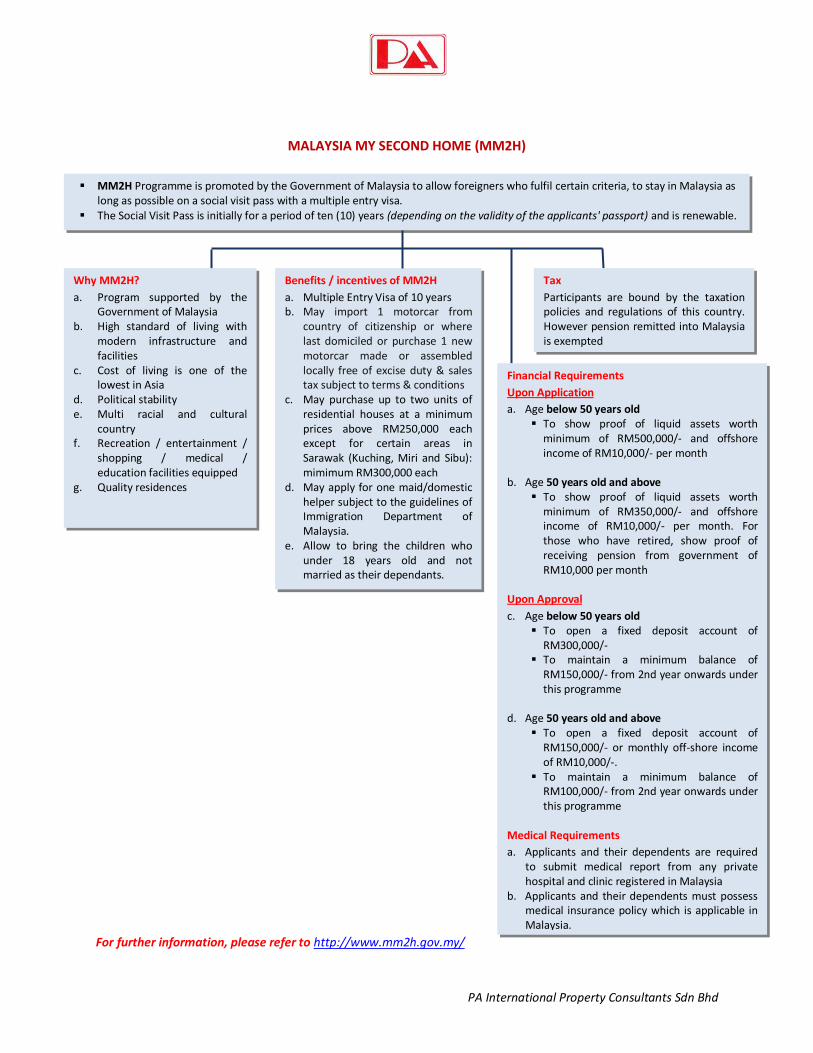

MALAYSIA MY SECOND HOME (MM2H)

For further information, please refer to http://www.mm2h.gov.my/

MM2H Programme is promoted by the Government of Malaysia to allow foreigners who fulfil certain criteria, to stay in Malaysia as long as possible on a social visit pass with a multiple entry visa.

The Social Visit Pass is initially for a period of ten (10) years (depending on the validity of the applicants' passport) and is renewable.

Benefits / incentives of MM2H

a. Multiple Entry Visa of 10 years b. May import 1 motorcar from

country of citizenship or where last domiciled or purchase 1 new motorcar made or assembled locally free of excise duty & sales tax subject to terms & conditions

c. May purchase up to two units of residential houses at a minimum prices above RM250,000 each except for certain areas in Sarawak (Kuching, Miri and Sibu): mimimum RM300,000 each

d. May apply for one maid/domestic helper subject to the guidelines of Immigration Department of Malaysia.

e. Allow to bring the children who under 18 years old and not married as their dependants.

Tax

Participants are bound by the taxation policies and regulations of this country. However pension remitted into Malaysia is exempted

Why MM2H?

a. Program supported by the Government of Malaysia

b. High standard of living with modern infrastructure and facilities

c. Cost of living is one of the lowest in Asia

d. Political stability

e. Multi racial and cultural country

f. Recreation / entertainment / shopping / medical / education facilities equipped

g. Quality residences

Financial Requirements

Upon Application

a. Age below 50 years old To show proof of liquid assets worth

minimum of RM500,000/- and offshore income of RM10,000/- per month

b. Age 50 years old and above

To show proof of liquid assets worth minimum of RM350,000/- and offshore income of RM10,000/- per month. For those who have retired, show proof of receiving pension from government of RM10,000 per month

Upon Approval

c. Age below 50 years old To open a fixed deposit account of

RM300,000/- To maintain a minimum balance of

RM150,000/- from 2nd year onwards under this programme

d. Age 50 years old and above

To open a fixed deposit account of RM150,000/- or monthly off-shore income of RM10,000/-.

To maintain a minimum balance of RM100,000/- from 2nd year onwards under this programme

Medical Requirements

a. Applicants and their dependents are required to submit medical report from any private hospital and clinic registered in Malaysia

b. Applicants and their dependents must possess medical insurance policy which is applicable in Malaysia.

PA International Property Consultants Sdn Bhd

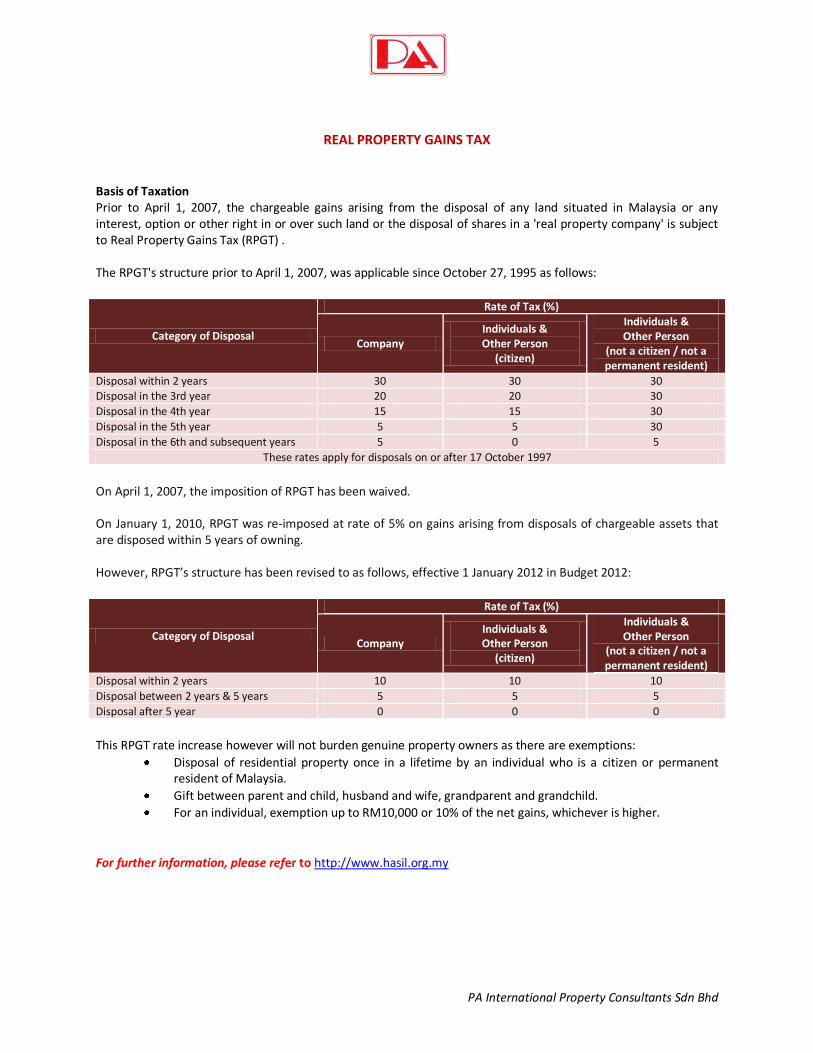

REAL PROPERTY GAINS TAX

Basis of Taxation Prior to April 1, 2007, the chargeable gains arising from the disposal of any land situated in Malaysia or any interest, option or other right in or over such land or the disposal of shares in a 'real property company' is subject to Real Property Gains Tax (RPGT) . The RPGT's structure prior to April 1, 2007, was applicable since October 27, 1995 as follows:

Category of Disposal

Rate of Tax (%)

Company Individuals & Other Person

(citizen)

Individuals & Other Person

(not a citizen / not a permanent resident)

Disposal within 2 years 30 30 30 Disposal in the 3rd year 20 20 30

Disposal in the 4th year 15 15 30

Disposal in the 5th year 5 5 30

Disposal in the 6th and subsequent years 5 0 5

These rates apply for disposals on or after 17 October 1997

On April 1, 2007, the imposition of RPGT has been waived. On January 1, 2010, RPGT was re-imposed at rate of 5% on gains arising from disposals of chargeable assets that are disposed within 5 years of owning. However, RPGT’s structure has been revised to as follows, effective 1 January 2012 in Budget 2012:

Category of Disposal

Rate of Tax (%)

Company Individuals & Other Person

(citizen)

Individuals & Other Person

(not a citizen / not a permanent resident)

Disposal within 2 years 10 10 10

Disposal between 2 years & 5 years 5 5 5

Disposal after 5 year 0 0 0

This RPGT rate increase however will not burden genuine property owners as there are exemptions:

Disposal of residential property once in a lifetime by an individual who is a citizen or permanent resident of Malaysia.

Gift between parent and child, husband and wife, grandparent and grandchild.

For an individual, exemption up to RM10,000 or 10% of the net gains, whichever is higher.

For further information, please refer to http://www.hasil.org.my

PA International Property Consultants Sdn Bhd

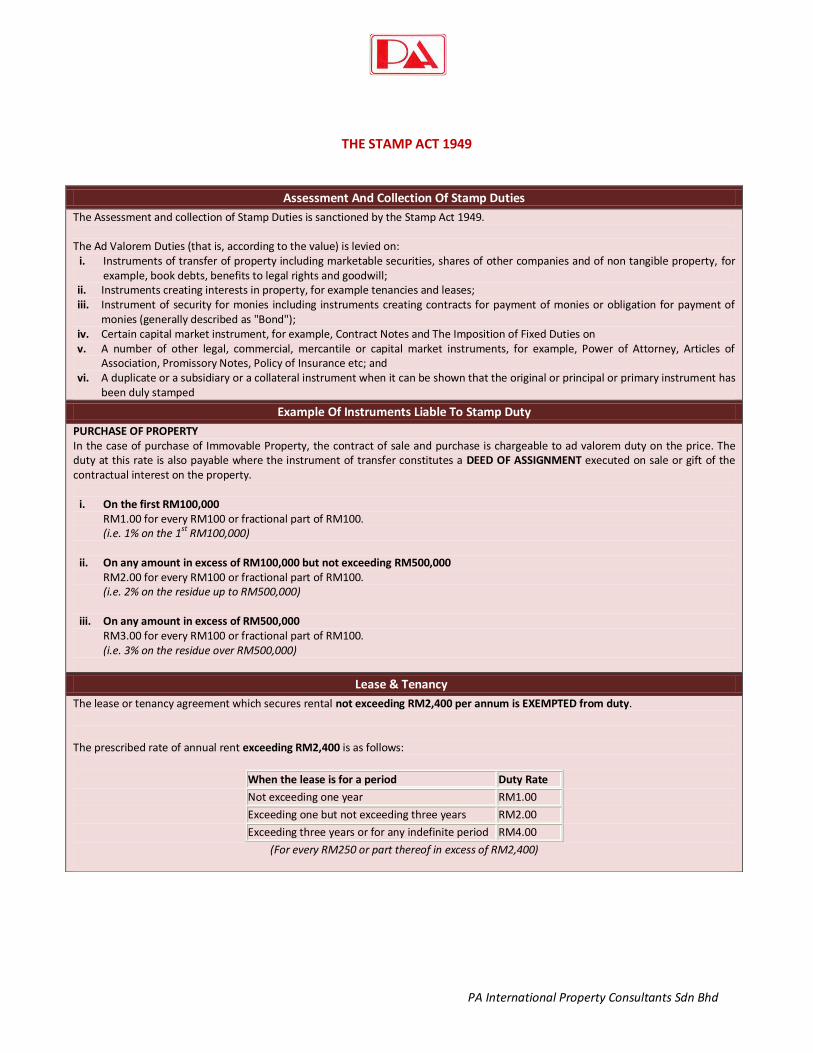

THE STAMP ACT 1949

Assessment And Collection Of Stamp Duties

The Assessment and collection of Stamp Duties is sanctioned by the Stamp Act 1949. The Ad Valorem Duties (that is, according to the value) is levied on:

i. Instruments of transfer of property including marketable securities, shares of other companies and of non tangible property, for example, book debts, benefits to legal rights and goodwill;

ii. Instruments creating interests in property, for example tenancies and leases; iii. Instrument of security for monies including instruments creating contracts for payment of monies or obligation for payment of

monies (generally described as "Bond"); iv. Certain capital market instrument, for example, Contract Notes and The Imposition of Fixed Duties on v. A number of other legal, commercial, mercantile or capital market instruments, for example, Power of Attorney, Articles of

Association, Promissory Notes, Policy of Insurance etc; and vi. A duplicate or a subsidiary or a collateral instrument when it can be shown that the original or principal or primary instrument has

been duly stamped

Example Of Instruments Liable To Stamp Duty

PURCHASE OF PROPERTY In the case of purchase of Immovable Property, the contract of sale and purchase is chargeable to ad valorem duty on the price. The duty at this rate is also payable where the instrument of transfer constitutes a DEED OF ASSIGNMENT executed on sale or gift of the contractual interest on the property.

i. On the first RM100,000 RM1.00 for every RM100 or fractional part of RM100. (i.e. 1% on the 1st RM100,000)

ii. On any amount in excess of RM100,000 but not exceeding RM500,000 RM2.00 for every RM100 or fractional part of RM100. (i.e. 2% on the residue up to RM500,000)

iii. On any amount in excess of RM500,000

RM3.00 for every RM100 or fractional part of RM100. (i.e. 3% on the residue over RM500,000)

Lease & Tenancy

The lease or tenancy agreement which secures rental not exceeding RM2,400 per annum is EXEMPTED from duty. The prescribed rate of annual rent exceeding RM2,400 is as follows:

When the lease is for a period Duty Rate

Not exceeding one year RM1.00

Exceeding one but not exceeding three years RM2.00

Exceeding three years or for any indefinite period RM4.00

(For every RM250 or part thereof in excess of RM2,400)

PA International Property Consultants Sdn Bhd

For further information, please refer to http://www.hasil.org.my/english/eng_NO2_1_4.asp

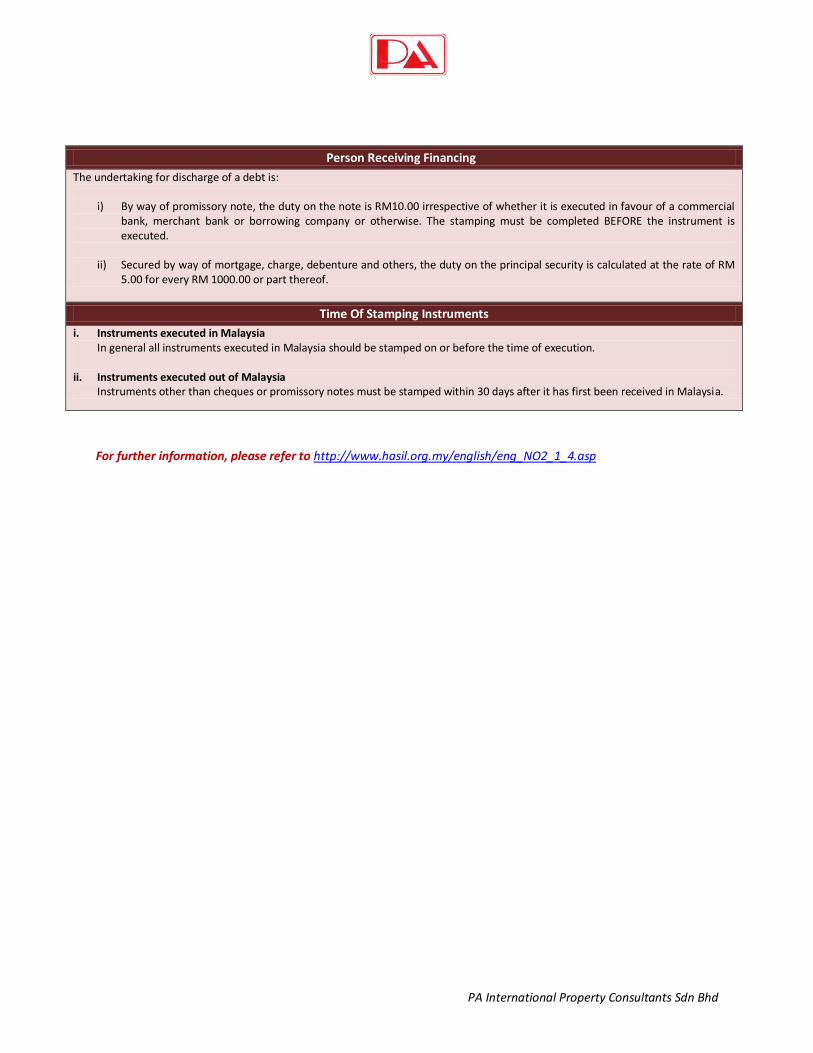

Person Receiving Financing

The undertaking for discharge of a debt is:

i) By way of promissory note, the duty on the note is RM10.00 irrespective of whether it is executed in favour of a commercial bank, merchant bank or borrowing company or otherwise. The stamping must be completed BEFORE the instrument is executed.

ii) Secured by way of mortgage, charge, debenture and others, the duty on the principal security is calculated at the rate of RM 5.00 for every RM 1000.00 or part thereof.

Time Of Stamping Instruments

i. Instruments executed in Malaysia In general all instruments executed in Malaysia should be stamped on or before the time of execution.

ii. Instruments executed out of Malaysia Instruments other than cheques or promissory notes must be stamped within 30 days after it has first been received in Malaysia.

PA International Property Consultants Sdn Bhd

Below are the PARTICIPATING BANKS:

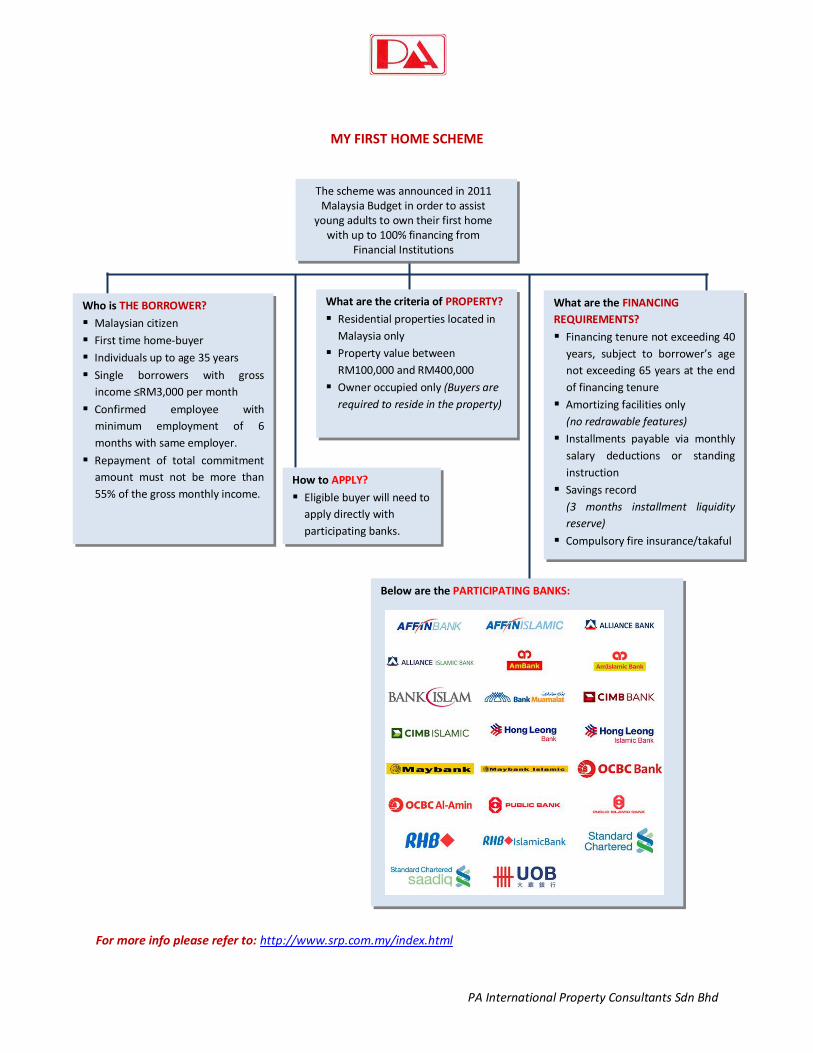

MY FIRST HOME SCHEME

For more info please refer to: http://www.srp.com.my/index.html

What are the criteria of PROPERTY?

Residential properties located in

Malaysia only

Property value between

RM100,000 and RM400,000

Owner occupied only (Buyers are

required to reside in the property)

What are the FINANCING

REQUIREMENTS?

Financing tenure not exceeding 40

years, subject to borrower’s age

not exceeding 65 years at the end

of financing tenure

Amortizing facilities only

(no redrawable features)

Installments payable via monthly

salary deductions or standing

instruction

Savings record

(3 months installment liquidity

reserve)

Compulsory fire insurance/takaful

The scheme was announced in 2011 Malaysia Budget in order to assist

young adults to own their first home with up to 100% financing from

Financial Institutions

Who is THE BORROWER?

Malaysian citizen

First time home-buyer

Individuals up to age 35 years

Single borrowers with gross

income ≤RM3,000 per month

Confirmed employee with

minimum employment of 6

months with same employer.

Repayment of total commitment

amount must not be more than

55% of the gross monthly income.

How to APPLY?

Eligible buyer will need to

apply directly with

participating banks.