Embed Size (px)

Citation preview

Board of Directors

Audit Committee

13th November 2013

GSTS Pathology Review

Status: A Paper for Consideration

History: Final Review Report

Commercial in Confidence

Amanda Pritchard, Chief Operating Officer

Martin Shaw, Director of Finance

Victoria Cheston, Commercial Director

Doc 15

Commercial In Confidence

Audit Committee September 2013 2 Draft GSTS Pathology Review

GSTS Pathology Review

A paper prepared by , presented by Amanda Pritchard, Chief Operating Officer, Martin Shaw, Finance

Director and Victoria Cheston, Commercial Director

1. EXECUTIVE SUMMARY

1.1 In February 2013 The Audit Committee of GSTT agreed to commission an internal review of GSTS Pathology Services to determine:

If the ambitions that lay behind the establishment of GSTS have been realised.

If the current service has been transformed and offers value for money to the Trust.

1.2 A cross-directorate Project Team was established with membership from

Clinical Operations, Finance and Commercial. In early July 2013 a work plan and terms of reference (appendix 1) were agreed with the respective Executive Directors.

1.3 The review was undertaken over the period July to August 2013 by examining

documents as listed in the legend of documents (appendix 2), surveys of users at GSTT and of staff at GSTS, interviews with GSTS managers, and discussion groups with user directorates at GSTT. Requests for further information were submitted to GSTS and the Project Team acknowledges the cooperative and helpful responses of the GSTS team.

1.4 A draft review paper was sent to the September Audit Committee for

information. This draft was then sent to GSTS for review of accuracy and amendments have now been made on matters of factual accuracy..

1.5 Due to the limited time available the review has focussed on providing a

report that will support the Audit Committee when considering any decisions regarding the future of GSTS. It is acknowledged that further work may be required to revisit some of the issues in more detail once the Audit Committee has considered this initial draft report.

Review of Original Business Case Objectives

1.6 The review identified that the overall financial benefit to GSTT over the first 5 years of operation was £8.8m compared to £17.1m in the Business Case. The additional investment of £3m made by the Trust needs to be set alongside this. The main reasons for the shortfall were:

Low level achievement of transformation plans.

Doc 15

s.40(2)

Commercial In Confidence

Audit Committee September 2013 3 Draft GSTS Pathology Review

Expenditure by GSTS on bid activity with limited success mainly due to the low level of market activity in NHS pathology.

1.7 With regard to other objectives the review found that:

The trust received rental and service income as per the plan.

GSTS has achieved its objective of business growth in the period achieving turnover close to plan and securing Bedford Hospital as a customer and KCH as a member.

GSTS has managed its risks adequately with the exception of liquidity and clinician engagement.

1.8 The cash requirement from GSTT was increased by up to £3m in the

refinancing. GSTS achieved a small profit (£303k) in 2012 and is forecasting a profit of £3.8m for 2013. The GSTS forecast suggests that the JV will be able to repay loans to members by year 8 and fund its required investment including implementation of a new Laboratory Information System (LIMS).

1.9 Risks to this forecast have been identified along with proposals to mitigate the

risks. The team identified a range of strategic issues that should be considered in relation to the future of the success of the joint venture:

Innovation Research and Development of New tests.

Future of Transformation.

NHS pathology Market and market focus of GSTS.

VAT Position. 1.10 In undertaking this review the team has had the opportunity to undertake a

high level post implementation evaluation which has identified the following learning areas for future projects:

The complexity and novelty of the GSTS transaction.

The selection of a JV partner.

Processes for contract management. 1.11 Recommendations re: Business Case Objectives

Agree financial risk mitigation plan for future of GSTS covering investment IT Implementation risk, VAT and Direct Access contracts.

Clarify acceptable areas for transformation with JV members.

Agree refocused marketing plan on specialist tests, overseas market and possibly PRUH.

Develop joint action plan processes with GSTS KCL and GSTT to facilitate translation of research and innovation into new tests on the market.

Billing, Activity Reporting, Over-Performance and Unit Pricing

1.12 This section reviews the basis for GSTS’ charges to GSTT and how activity is reported. It also considers some of the concerns that have arisen from the operation of this area of the contract, in particular the challenge of apparent

Doc 15

Commercial In Confidence

Audit Committee September 2013 4 Draft GSTS Pathology Review

“over-performance” in the early years of the contract and more recently, the Internal Audit review of activity reporting in some specialist labs which called into the question charging for some activity by GSTS. The systemic weaknesses underlying activity reporting are described. Finally, unit prices and the opportunities for benchmarking are discussed.

1.13 Overall the review concluded that GSTS has not (yet) delivered the

anticipated transformation in LIMS systems, activity reporting and pricing which formed a key objective of the contract. This means that the shortcomings in these areas that GSTS inherited have not been resolved. As a consequence many of the commercial risks associated with these shortcomings are currently borne by GSTT. It is essential that these shortcomings are resolved if the adoption of “price per test” is to be successful.

1.14 Recommendations re: Billing, Activity and Pricing

GSTT needs to:

Take steps to manage the commercial risks associated with the shortcomings in the systems and processes that underpin activity reporting.

Ensure that these shortcomings are not allowed to undermine the adoption of price per test.

Detailed recommendations are set out in section 4.

Customer Satisfaction and Regulatory Compliance

1.15 In an effort to provide the Audit Committee with a balanced perspective, meetings took place with members of the GSTS clinical and managerial teams and all GSTS staff were encouraged to participate in a confidential on-line survey.

1.16 Participation from both Trust and GSTS staff was excellent and, whilst a

number of concerns were raised, the overall impression was one of a desire to move forward.

1.17 There is little doubt that the early years of the joint venture have failed to

deliver the logistical and clinical transformation that both organisations had hoped for. A number of factors ‘conspired’ to create this situation and both the Trust and GSTS have undertaken a range of initiatives to resolve the underlying problems in an attempt to build a strong platform for future development.

1.18 The strengthening of the corporate team and the introduction of shared

accountability of service delivery across the clinical, scientific and management teams would appear to place GSTS in a good position for future development.

1.19 The clinical teams within GSTT have been disappointed and frustrated by the

slow pace of change and in particular the lack of GSTS responsiveness in dealing with operational concerns. In simple terms they feel that it is now ‘make or brake’. However there is still sufficient enthusiasm from the clinical teams to continue to work in partnership with GSTS in order to deliver a

Doc 15

Commercial In Confidence

Audit Committee September 2013 5 Draft GSTS Pathology Review

world-class service. What is important is that this enthusiasm is nurtured and the clinical teams are given the confidence that the service can respond to clinical needs.

1.20 General compliance with the CQC and CPA standard has improved under

GSTS. 1.21 It should be noted that joint working has already commenced between GSTS

and GSTT to resolve a number of outstanding clinical issues. Senior members of the respective management teams are working on an urgent action plan which aims to agree a way forward on:

A&E

Phlebotomy

Implementing the investment in Next Generation Sequencing at Guys 1.21 Recommendations re: Customer Satisfaction and Regulatory Compliance:

The PSA Contract Manager should lead a cross-organisational team to develop revised KPIs to enable the Trust to measure the effectiveness of various elements of the GSTS service, including response to innovation and financial indicators.

The Joint Pathology Committee (JPC) should continue but with increased representation from the clinical team. The TOR should be revisited to with increased emphasis on joint-working to overcome the ‘cultural and practical challenges to pathology transformation’.

The GSTT COO should consider identifying a senior member of the Management Team to be the designated link with GSTS. This role could provide the vital support to both Trust and GSTS staff in order to establish effective working relationships foster a more open way of working and assist GSTS in successful delivery of their “One Organisation Programme”.

The General Manager of the GSTS Team should attend the weekly General Managers’ meetings.

The role of the PSA Manager should be revisited to ensure that there is a clear understanding of how this resource can be best utilised to provide a key ‘link’ between the two organisations. The PSA Contract Manager should have a clear operating brief especially in respect of the special circumstances whereby GSTT is both a Customer and a Share Holder.

In line with the PSA Contract, GSTS need to provide a suitable and authorised Contract Manager to work opposite the Trust Authorised Officer.

GSTS, possibly in conjunction with the PSA Manager and COO representative, should agree a proactive approach to the development of good working relationships with the Directorates. It is recommended that regular meetings take place with an emphasis on the quality of service delivery rather ad hoc meetings in response to complaints.

Doc 15

Commercial In Confidence

Audit Committee September 2013 6 Draft GSTS Pathology Review

Overall Conclusion of Review

1.22 The review found that the GSTS project had fallen short of the original GSTT objectives. However customers were generally satisfied with the services provided. Some of the anticipated financial benefits have accrued to the Trust. The inherited shortcomings in pricing and activity remain unresolved. Regulatory compliance has improved under GSTS. There is a general desire amongst GSTT staff members who work with GSTS to move forward with the current arrangement. GSTS has credible plans to address the shortcomings that have been identified.

Doc 15

Commercial In Confidence

Audit Committee September 2013 7 Draft GSTS Pathology Review

2. INTRODUCTION

2.1 In February 2013 The Audit Committee of GSTT commissioned a review of GSTS Pathology Services in order to establish if:

The ambitions that lay behind the establishment of GSTS have been realised.

The current service has been transformed and offers value for money to the Trust.

2.2 A cross-directorate Project Team was established with membership from

Clinical Operations, Finance and Commercial. In early July 2013 a work plan and terms of reference were agreed with the respective Executive Directors.

2.3 The terms of reference were developed in detail from the original referral from

the audit committee and are attached at appendix 1. The sections of the report reflect the items in the Terms of Reference. The review was undertaken over the period July and August 2013 by examining documents as listed in the legend of documents, surveys of users at GSTT and of staff at GSTS, interviews with GSTS managers, and discussion groups with user directorates at GSTT. Requests for further information were submitted to GSTS and the Project Team acknowledges the cooperative and helpful responses of the GSTS team.

2.4 The layout of the report reflects the terms of reference so that section 3

relates to business plan objectives, section 4 billing activity and pricing and section 5 to customer satisfaction and regulatory compliance.

2.5 Due to the limited time available the review has focussed on providing a

report that will support the Audit Committee when considering any major decisions regarding the future of GSTS. It is acknowledged that further work may be required to revisit some of the detailed issues once the Audit Committee has considered this initial report.

Background - The Carter Report

2.6 ‘The Carter Report’ was published in August 2006 and laid out an agenda for the transformation of NHS Pathology services. The main recommendations of the Carter Report were:

The creation of freestanding pathology providers.

The introduction of a commissioner provider split in pathology services.

Integrated service improvement.

Workforce changes. 2.7 It was thought that a combination of the above would improve service quality,

manage the annual 10% increase in volumes and deliver cost savings. 2.8 ‘The Pilot Sites Report’ followed in June 2008 and gave an indication of the

level of potential savings available. The pilot site studies suggested that savings of between 10% and 20% of overall costs were possible and that the greater the scale of consolidation the greater the level of savings that could be achieved. The process of consolidation had also been observed in the US and Australia.

Doc 15

Commercial In Confidence

Audit Committee September 2013 8 Draft GSTS Pathology Review

2.9 Timeline of Key Events

January 2007 In 2007 GSTT commenced the procurement process to identify a commercial third party provider to be a shareholder in a joint venture with GSTT.

March 2007 Pre qualification Issued

May 2007 Request for Proposals Issued

Late 2007 Serco selected as preferred bidder

December 2008 Final approval by the GSTT Board to establish the GSTS joint venture as an LLP company.

January 2009 GSTS Pathology Established

December 2009 GSTS contracted to provide the Pathology services for Bedford Hospital

September 2010 LLP membership extended to include Kings College Hospital

November 2011 Refinancing arrangements agreed

July 2013

Tax Issues

2.10 The creation of the joint venture required careful tax planning to ensure that the transactions between GSTT and GSTS would be tax neutral and not attract additional VAT and increase costs to GSTT. Extensive professional advice was obtained and all parties then approached HMRC independently to seek confirmation. Written rulings from HMRC were obtained which confirmed the advice received that the transactions between GSTT and GSTS were VAT neutral. Towards the end of 2012 HMRC declared that they had made an error when providing these confirmations. GSTS are now challenging this change of position at a VAT tribunal which is expected to rule during September 2013.

Employment Issues

2.11 The transaction took account of NHS employment issues at the time. Technical and scientific members of staff working for the Trust in Pathology services were seconded to GSTS using the retention of employment model (ROE). Consultant pathologists were not seconded under ROE but sessions of their time (PAs) were purchased by GSTS from the Trust. The ROE model was approved by the Department of Health. Subsequently the ROE model

Doc 15

s.43

Commercial In Confidence

Audit Committee September 2013 9 Draft GSTS Pathology Review

was constrained and is no longer available for new transactions of this type. The alternative of Direction Status is still to be authorised.

Property Issues

2.12 The Trust agreed to lease the existing laboratory space to GSTS on cost neutral terms.

Doc 15

Commercial In Confidence

Audit Committee September 2013 10 Draft GSTS Pathology Review

3. ACHIEVEMENT OF BUSINESS CASE OBJECTIVES

3.1 The objectives to be reviewed were identified from the requirements listed in the request for the Best and Final Offer document of September 2007 together with the business case approved by the GSTT Board in December 2008, set in the context of the two Carter reports on Pathology Services. In determining the extent to which these have been met consideration has been given to the impact of the entry of KCH into the LLP in 2009 and the financial restructuring that took place in 2011.

Objectives were categorised into:

Financial Objectives

Commercial Objectives

Service Quality Objectives

Other Objectives

Risk Management Objectives

The findings were mapped against the particular role of the Trust: M = Role of LLP Member i.e. owner investor C = Customer requiring services from the LLP S = Supplier providing services to the LLP

Financial Objectives

3.2 The financial objectives applied to the Trust in its member role. The financial objectives have not been met in full and in the first 5 years the actual financial benefit to the Trust was £8.8m against plan of £17.1m. This gap represents a shortfall in dividends plus the loss of one year’s worth of the price deflator (an adverse position to GSTT of £0.5m for that year) and, in addition the value of the PSA for GFSTT did not increase by the rate projected in the business plan, creating a cumulative effect over the period that is lower in terms of the deflator than was envisaged. These elements increased the gap in comparison to the original business plan over the five years to £0.6m, although the Trust did not incur the level of pathology costs modelled in the original business plan.

3.3 Shortfalls in performance (mainly within the cost base of GSTS) drove the need for refinancing. The financial difficulties in those early years became the focus of management and member attention to the detriment of other dimensions of the project.

Doc 15

Commercial In Confidence

Audit Committee September 2013 11 Draft GSTS Pathology Review

Objective Objective

owner Expected Outcome Actual Outcome

Net Financial Benefit to Trust over 5 years

M

Total £17.1m

Total £8.8m

Dividend to Trust

M

EBT M

EBIT M

Revenue M

ROCE M

3.3 The initial plan was based on assumptions around market growth and service

transformation.

Market Growth

Doc 15

s.43s.43

s.43 s.43

s.43 s.43

s.43 s.43

s.43 s.43

s.43 s.43

Commercial In Confidence

Audit Committee September 2013 12 Draft GSTS Pathology Review

Initial growth was achieved via the Bedford Hospital contract and KCH joining the LLP by 2010. Turnover for the 5 years has been close to the original plan (actual £372m plan £379m). Since 2010 further growth has been delayed by lack of completed market procurements and annual earnings depressed by around £1m in business development and bid costs.

Service Transformation

No detailed transformation plan has been identified but the following items suggest the scale envisaged.

The Serco BAFO response offered;

The financial objectives were not achieved in full due to:

Transformation has not been achieved to the extent envisaged.

SERCO skills not effective in transformation and achievements promised in the BAFO not delivered.

The NHS Pathology Market has not developed at the pace envisaged.

Expenditure on Bid activity by GSTS with limited success.

Transactions

3.4 The table below summarises the transactions between GSTT and GSTS under the two operating agreements:

The Trust Service Agreement (TSA) – where GSTT receives income for services supplied.

The Pathology Service Agreement (PSA) – where GSTS incurs expenditure on Pathology services.

2009

£000

2010

£000

2011

£000

2012

£000

Grand Total

£000

Income: Invoice to GSTS under the TSA

26,776 30,609 28,900 22,624 108,908

Expenditure: Payments to GSTS under the PSA

45,110 46,524 47,436 48,720 187,789

Net 18,334 15,915 18,535 26,096 78,881

The majority of the income received by GSTT is for staff who have remained employees of GSTT, but are seconded to GSTS under the retention of employment arrangements (RoE). In 2009, this represented 81% of the TSA income. By 2012, this had fallen to 71% of the TSA income, reflecting the reduction in numbers from 550 at the start of the contract to 350 currently. Between 2009 and 2012, income for ROE staff fell by £5m. Every pound GSTT receives from GSTS for these staff is matched by equivalent

Doc 15

s.43

Commercial In Confidence

Audit Committee September 2013 13 Draft GSTS Pathology Review

expenditure. So this change in income is not significant for GSTT's bottom line.

Doc 15

Commercial In Confidence

Audit Committee September 2013 14 Draft GSTS Pathology Review

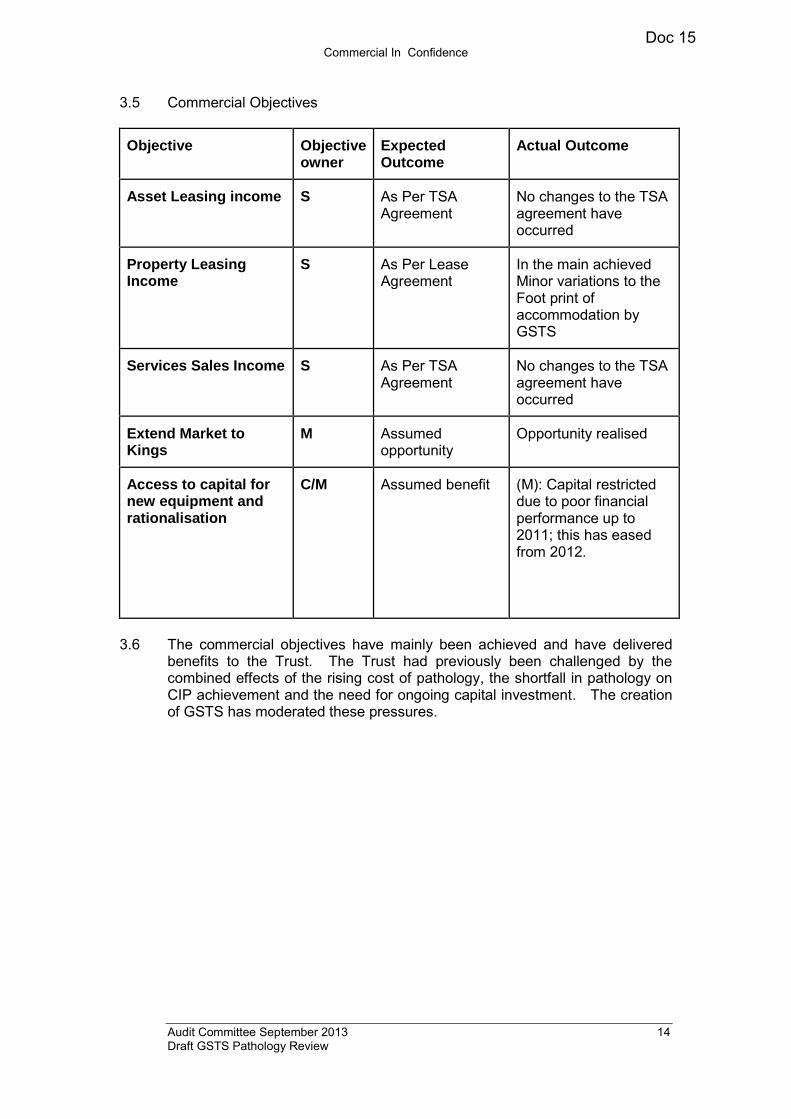

3.5 Commercial Objectives

Objective Objective owner

Expected Outcome

Actual Outcome

Asset Leasing income S As Per TSA Agreement

No changes to the TSA agreement have occurred

Property Leasing Income

S As Per Lease Agreement

In the main achieved Minor variations to the Foot print of accommodation by GSTS

Services Sales Income S As Per TSA Agreement

No changes to the TSA agreement have occurred

Extend Market to Kings

M Assumed opportunity

Opportunity realised

Access to capital for new equipment and rationalisation

C/M Assumed benefit (M): Capital restricted due to poor financial performance up to 2011; this has eased from 2012.

3.6 The commercial objectives have mainly been achieved and have delivered

benefits to the Trust. The Trust had previously been challenged by the combined effects of the rising cost of pathology, the shortfall in pathology on CIP achievement and the need for ongoing capital investment. The creation of GSTS has moderated these pressures.

Doc 15

Commercial In Confidence

Audit Committee September 2013 15 Draft GSTS Pathology Review

3.7 Service Quality Objectives

Objective Objective Owner

Expected Outcome

Actual Outcome

Enhance GSTT academic medical centre status reputation through supporting Research Development and Teaching

T Serco proposed 10% of free cash to be invested in research and development

Key strategic objective Not driven by pricing model nor PSA agreement Needs differential commercial approach

Provide a working environment which attracts and retains staff at all levels and which supports professional excellence through the provision of training and professional development

M Successful Recruitment of replacement staff by GSTS

Partial achievement Issues identified with attracting academic career clinical scientists Have recruited other staff to GSTS employment

3.8 There are significant shortfalls with strategic implication for one of these

objectives and the other has in the main been achieved:

The support for research development and teaching has not been demonstrated.

The provision of a working environment that will attract and retain staff is still a challenge. However the GSTS spend on agency staff for operational staff although rising is only 5.3% of the payroll cost and this suggests effective recruitment capability for most roles. The GSTS management have plans in place on identity branding and employment terms to strengthen the employer role. For some key positions flexibility of employer and terms may need to be available to secure top quality recruits.

Other Objectives

3.9 The objectives of Novation of contracts, introduction of new LIMS and market testing remain unachieved.

Doc 15

Commercial In Confidence

Audit Committee September 2013 16 Draft GSTS Pathology Review

Objective Objective Owner

Expected Outcome Actual Outcome

It is also intended that the joint venture LLP will become a major supplier of pathology services to NHS and private organisations both regionally, nationally and internationally

M Continuous bidding activity to assist in revenue growth to drive up profit gains and gain market share assumed.

Partially Achieved Continuous bidding activity has taken place gained Bedford Hospital pathology work early on. Bidding for EoE and SE London work has proved slow and problematic, mainly due to market conditions. Little progress in international market.

Achieve ROE Model S ROE staff would gradually reduce

Achieved to date Number of GSTT ROE staff reduced from 550 to 350

Novation of Contracts / Manage Price Pressure AQP

C/M Novation would occur in year 1

Not Achieved GSTS delayed Novation in view of financial situation Novation target date now April 14 Lack of transformation leaves risk of price pressure in AQP high

Manage VAT position restructure / Direction Status

M VAT ruling given at commencement of LLP at fully VAT able.

HMRC tribunal in September. To date the VAT issue has been well managed and there will be no retrospective charges and a period of transition will be provided if case lost.

Introduce New LIMS M/C Occur in Years 1-2 Need to replace pathnet system remains. Minor progress in integration of systems

Doc 15

Commercial In Confidence

Audit Committee September 2013 17 Draft GSTS Pathology Review

Objective Objective Owner

Expected Outcome Actual Outcome

Market Test C By Benchmarking No Benchmarking processes have taken place. No reliable benchmarking sources have been identified

Accurate Invoicing of Tests

C Occur in Years 1-2 Progress only made in year 5 (no progress in years 1-4)

Risk Management Objectives

3.10 The Pathology Services business case contained a risk register and this section reviews the extent to which those risks were mitigated and reviews subsequently identified risks.

3.11 It is clear that the majority of the risks identified in the risk register have been

managed effectively and that where risks have impacted the effect has not been dramatic. The key outstanding areas for concern are:

Clinician engagement.

Future progress on productivity targets.

Objective Objective Owner

Expected Outcome Actual Outcome

Risks taken from Business Case Risk register

Volume of activity in business plan not achieved

M Volumes to be achieved

Volumes broadly achieved

More than 20 Trust staff opting to TUPE

S More then 20 Trust staff, would pressure on the redundancy provision.

Less then 20 Staff Transferred over under TUPE, however the mix of Staff, did mean that the provision for redundancy costs was breached.

Doc 15

Commercial In Confidence

Audit Committee September 2013 18 Draft GSTS Pathology Review

Objective Objective Owner

Expected Outcome Actual Outcome

Direct access volumes increase materially at current contract terms for marginal revenue

C General increase in pathology use, Third party Customers expected to move to GSTS in year 1.

Most Third Party Customers have stayed with GSTT, as GSTS, due to data integrity problems have not been able to take over direct billing.

A national tariff reduction

C/M Expected reduction in Pathology Prices.

Due to the lack of consistency in Nomenclature in Pathology the anticipated downwards pressure on Pathology Prices has not occurred.

Productivity targets in the business plan are not met

M Assumed lab consolidation, plus pay and non-pay efficiencies reduce cost base and contribute to EBIT from year 1

Gains in this area not seen until 2012 (year 4) , so well behind expectations

Liquidity constraints might hinder the smooth management of the LLP

M Assumed risk This did occur in 2011, with a financial crisis, which was resolved at member level, and the business put on a consolidation track to achieve stable financial base

Trust exposure if the LLP commences without Insurance

T/M Assumed risk Insurance was in place

Doc 15

s.43

Commercial In Confidence

Audit Committee September 2013 19 Draft GSTS Pathology Review

Objective Objective Owner

Expected Outcome Actual Outcome

If for any reason the Trust need to make alternative procurement of pathology services due to failure of LLP

C With the management of Pathology passing to a different body, a risk of non-supply was identified.

The addition of both Kings and Bedford as customers (with production capability) has given further production contingency for GSTS. Risk has not materialised

Partner wishes to sell share of JV

M Assumed risk Not materialised

Investment agreed not made by JV partner

M Assumed risk Not materialised

Accreditation not maintained

C/M Assumed risk ALL Labs now CPA accredited

Inaccurate results C With the management of Pathology passing to a different body, a risk of inaccurate results.

Occasionally problems with results have been identified (normal). But problems have been identified and fixed.

Failure to provide services required for Trust delivery of clinical key performance indicators

C Initial KPI regime would change after year 1 of the contract.

There has been no change in the KPI regime, which remains the originally KPI regime, that was agreed to be temporary. GSTS do declare the results on a monthly basis.

Failure to meet internal SLA for Trust services

S New SLA documents would be created and agreed in the 1st Year of the contract.

No TSA SLAs have been agreed.

Unclear framework for residual Trust Pathology activities

S GSTT would maintain control/influence of some of the pathology services.

With the exception of Point of Care Testing, no agreements have been reached to more closely define these areas.

Doc 15

Commercial In Confidence

Audit Committee September 2013 20 Draft GSTS Pathology Review

Objective Objective Owner

Expected Outcome Actual Outcome

Lack of engagement with JV by clinical consultants

C Clinicians show disinterest in JV

Clinicians have engaged, but unfortunately the responses from GSTS to date have been below expectations. (This area is not defined contractually)

Interruption of services, e.g. fire, IT failure, strikes, etc

C Assumed risk There have been numerous floods in St Thomas’ of which some have not affected the GSTS services. In spite of this services were maintained.

Changes in political direction

All Assumed risk The 2010-2015 Government has not had any affect on the contracts with the exception of a retrospective review of the VAT treatment.

Equal pay claims M Assumed Risk No claims identified

Retention and Recruitment of qualified staff

M Assumed Risk LLP has suffered some key operational staff leaving the business in the last 2-3 years. Not entirely clear whether this directly relates to financial and/or leadership issues within GSTS. Agency use within reasonable expectation

If ROE and secondment of staff unable to maintain consistency in behaviour standards and discipline

M Assumed Risk No evidence of impact

Doc 15

Commercial In Confidence

Audit Committee September 2013 21 Draft GSTS Pathology Review

BUSINESS PLAN OBJECTIVES - CONCLUSIONS AND RECOMMENDATIONS

Financial Objectives

3.12 The financial objectives have only been partially achieved. The short fall in financial objectives is a matter of historic costs that can not be reversed.. Accurate and creditable financial projections are the more important information for GSTT in making decision about the future of GSTS.

3.13 GSTS achieved a small profit (£303k) in 2012 and is forecasting a profit of

£3.8 m for 2013. The GSTS forecasts suggest that the JV will be able repay loans to members by year 8 and fund its required investment.

3.14 There are risks to the GSTS forecasts and the subsequent years’ profitability

that could result in delays to loan repayment and the possibility of GSTS needing further capital from its members namely:

Some of the cost savings that were achieved in 2012 were non recurrent and further recurrent savings will be needed to maintain the 2012 cost baseline.

The impact of the VAT Issue in the event of an unfavourable tribunal ruling which will result in both one off costs and after restructuring, an ongoing reduction in profitability due to non recoverable VAT.

The need to replace the LIMS and the possibility of an investment requirement deliver the new system and the potential for cost overruns during implementation.

Potential write down of investment in the blood sciences consolidation if this is not brought to fruition.

Price deflation in the direct access market.

3.15 The review recommends that GSTT mitigate these risks through; Restructuring the business into two separate companies to enable most

input VAT to be reclaimed. This involves the transfer of employees of both Trusts from the ROE model to employment by GSTS Newco under Direction Status for NHS pension eligibility. The scale of the staff transfer is significant and will be a major HR challenge.

Seeking to involve new sources of capital through relationships with other companies to fund the LIMS and to transfer the implementation risk.

Agreement with KCH on a transformation plan to achieve further savings. OTHER OBJECTIVES

ROE Model and Transfer of Employees 3.16 The staff turnover over the 5 years has reduced the number of staff employed

by GSTT and seconded to GSTS from 550 to 350. The GSTT employment risk is steadily decreasing through time.

Doc 15

s.43

Commercial In Confidence

Audit Committee September 2013 22 Draft GSTS Pathology Review

New LIMS System 3.17 Scheduled for implementation in years 1 to 2 financial difficulties caused

delay to the implantation. Preparatory plans are in progress and GSTS will seek approval for the replacement investment and plan in October 2014. The complexity of this project indicates a potential cost overrun risk above the already significant investment cost. Strategic Issues

3.18 In addition to the overall review of the BC objectives the team also identified s range of Strategic issues that should be considered in relation to the future of GSTS:

Innovation Research and the Development of New Tests

3.19

Future of Transformation

3.20 The potential gains from transformation remain significant but will require an increase in single site working for routine tests. The difficulties of agreeing a transformation plan between the sites is exacerbated by the uncertain position over possible organisational merger and the future of Princess Royal Hospital. There is an argument to delay transformation planning until this

Doc 15

s.43

Commercial In Confidence

Audit Committee September 2013 23 Draft GSTS Pathology Review

landscape is clearer but to do so fails to mitigate the risk in direct access business. The member Trusts, in their role as customers, need to make clear their priorities in this area.

Novation of Direct Access Contracts

3.21

NHS Pathology Market

3.22 The NHS pathology market has not emerged as quickly as expected and there have been difficulties that have resulted in contracts not being awarded.

A judgement is required as to the likely market activity in the coming years and whether the Carter agenda is now abandoned. If that judgement indicates a low level of potential contracts then consideration could be given to both refocusing the sales efforts of GSTS and reducing the overall level of committed spend. The business development agenda could be refocused on international opportunities and the specialist tests market. The reduction in budget could be held in a contingent budget only authorised by members for release in the light of a significant contract prospect being identified. VAT

3.23 The VAT status of the Sales by GSTS to the Trusts is being challenged by HMRC and if upheld in Tribunal will mean that VAT inputs to GSTS will not be recoverable under the present structure. To enable most of this issue to be mitigated it will require the transfer of ROE staff from both Trusts to GSTS employment under Directive status.

Doc 15

s.43

s.43

Commercial In Confidence

Audit Committee September 2013 24 Draft GSTS Pathology Review

Lessons to Be Learned For Future Joint Venture Projects

The Transaction

3.24 The transactions that established GSTS were complex and took account of issues and advice on specifics of Tax, employment, property. It was an ambitious and novel step. The complexity and novelty for the Trust of the transaction meant that the final contract closure process extended for 12 months despite both parties commitment. There was no similar agreement in pathology services existing elsewhere. It is likely that such novel agreements inherently involve greater risks. Selecting the Right Partner

3.25 The process used to select a partner deliberately chose to look at organisations with out a track record in pathology. This implied a significant level of management input to the JV from GSTT. The underlying assumption on transferability of skills is now questionable. Where the selection process is for a true partner rather than a supplier the relationship cannot be managed by contract alone and issues of corporate culture and compatibility require to be given greater weight in selection. Contract Management

3.26 Although the PSA is detailed and extensive when the financial problems emerged the other areas of contract management were given a back seat and it was not possible to maintain the fire walls between the different GSTS roles. Stronger separation of function and governance would help ameliorate this. An independent chair of GSTS has been appointed and consideration could be given to the appointment of Independent Non Executives to further strengthen the GSTS Board.

Doc 15

Commercial In Confidence

Audit Committee September 2013 25 Draft GSTS Pathology Review

4. FINANCIAL REVIEW OF BILLING, ACTIVITY REPORTING, OVER-PERFORMANCE AND UNIT PRICING

Overview

4.1

Terms of Reference

4.2

Terms of reference Relevant paragraphs

4.3

s.43

s.43

Commercial In Confidence

Audit Committee September 2013 26 Draft GSTS Pathology Review

4.6 :

4.7

4.8

4.9

4.10

2 Source: GSTT Test List.xlsx, supplied by GSTS, 1/8/2013 3 This summarises the actual operation of the contract in practice. There are more complex formulas for large scale variances from baseline - these have never needed to be invoked.

Doc 15

s.43

s.43

s.43

s.43

s.43

s.43

s.43

s.43

Commercial In Confidence

Audit Committee September 2013 27 Draft GSTS Pathology Review

Table 4.3: full and marginal cost per unit of activity per DU

Departmental Unit Full cost per unit

Variable cost per

unit

Blood Sciences Cellular Pathology Haemostasis Infection and Immunology Genetics Oral Pathology Renal Tissue Typing Spec Derm Labs Specialised Lab Medicine DU

4.11

New Tests

4.12

4.13

4.14

4.15 4.16

Activity Definition

4.17

Doc 15

s.43

s.43

s.43

s.43

s.43

s.43

s.43

s.43

Commercial In Confidence

Audit Committee September 2013 28 Draft GSTS Pathology Review

4.18

4.19

4.20

Chargeable Activity

4.21

4.22

Doc 15

s.43

s.43

s.43

s.43

s.43

s.43

s.43

s.43

Commercial In Confidence

Audit Committee September 2013 29 Draft GSTS Pathology Review

Best Practice

4.23

4.24

4.25

4.26

4.27

4.28

Activity Reporting & Over-performance

Activity Reporting

4.29 .

Doc 15

s.43

s.43

s.43

s.43

s.43

s.43

s.43

Commercial In Confidence

Audit Committee September 2013 30 Draft GSTS Pathology Review

4.30

4.31

4.32

4.33

4.34

Activity Reporting Systems and Processes

4.35

4.36

4.37 4.38

Doc 15

s.43

s.43

s.43

s.43

s.43

s.43

s.43

s.43

s.43

Commercial In Confidence

Audit Committee September 2013 31 Draft GSTS Pathology Review

4.39

4.40

4.45

4.46

4.47

4 Review of the Financial, Commercial and Customer Service Aspects of the Pathology Services Contract with

GSTS, Richard Jones, GSTS CEO, 1 August 2013

Doc 15

s.43

s.43

s.43

s.43

s.43

Commercial In Confidence

Audit Committee September 2013 32 Draft GSTS Pathology Review

Over-performance

4.48

Table 4.4: GSTS contract activity for GSTT by DU

Graph 4.1: GSTS contract activity for GSTT by DU

4.49

Doc 15

s.43

s.43

s.43

s.43

Commercial In Confidence

Audit Committee September 2013 33 Draft GSTS Pathology Review

Table 4.5: Year on year percentage change in GSTS activity by DU

Graph 4.2: GSTS contract activity changes by DU

4.50

4.51

5 In year 1, the percentage change reflects the increase above contract baseline activity, not the activity of the previous year; in years 2, 3 and 4 the percentage change is the change when compared with the activity of the previous year.

Doc 15

s.43

s.43

s.43

s.43

Commercial In Confidence

Audit Committee September 2013 34 Draft GSTS Pathology Review

4.52

4.53

4.54

Table 4.6 the weighted % increase of the aggregate volume of

activity (using the contract price base)

4.55

4.56

Doc 15

s.43

s.43

s.43

s.43

s.43

s.43

Commercial In Confidence

Audit Committee September 2013 35 Draft GSTS Pathology Review

4.57

Table 4.7: GSTT Activity increase by calendar year6

4.58

4.59

6 Source: Information Department: Trust Activity as reported in the annual accounts, adjusted to calendar years; activity includes A&E activity, consultant outpatients, admitted spells, all specialties

Doc 15

s.43

s.43

s.43

s.43

s.43

Commercial In Confidence

Audit Committee September 2013 36 Draft GSTS Pathology Review

4.60

4.61

Other concerns relating to the reporting of activity

4.62

4.63

4.64

Doc 15

s.43

s.43

s.43

s.43

s.43

s.43

Commercial In Confidence

Audit Committee September 2013 37 Draft GSTS Pathology Review

4.65

4.66

Unit Prices, benchmarking and price per test

The reasonableness of GSTS Unit Prices

4.67

4.68

Benchmarking

4.69

. 4.70

Doc 15

s.43

s.43

s.43

s.43

s.43

s.43

s.43

Commercial In Confidence

Audit Committee September 2013 38 Draft GSTS Pathology Review

4.71

Price per test

4.72

4.73

Billing, Activity and Pricing - Conclusions & Recommendations

Conclusions

4.74

4.75

4.76

4.77

7 Challenges relating to benchmarking of pathology services, GSTS, August 2013

Doc 15

s.43

s.43

s.43

s.43

s.43

s.43

s.43

s.43

Commercial In Confidence

Audit Committee September 2013 39 Draft GSTS Pathology Review

4.78

4.79

4.80

4.81

4.82

Recommendations 4.83

4.84

4.85

Doc 15

s.43

s.43

s.43

s.43

s.43

s.43

s.43

s.43

Commercial In Confidence

Audit Committee September 2013 40 Draft GSTS Pathology Review

4.86

4.87

4.88

4.89

Doc 15

s.43

s.43

s.43

s.43

s.43

s.43

s.43

s.43

Commercial In Confidence

Audit Committee September 2013 41 Draft GSTS Pathology Review

5. CUSTOMER SATISFACTION AND REGULATORY COLLABORATION

5.1 The Clinical Operations element of the audit focused on reviewing the

Operational Effectiveness of the GSTS Pathology Service. A User Satisfaction Questionnaire was undertaken during August, focusing on the quality of the clinical service with particular emphasis around timeliness and accuracy. Meetings took place with the Directorate Management Teams in order to complement the survey and provide the opportunity for the teams to raise specific issues around quality of service together with more management related issues such as the quality of activity data, response to innovation and commercial opportunities. Other specific areas covered by this section of the review include:

Review of GSTS compliance with CQC Standards.

Adherence to Trust policies.

Effectiveness of formal and informal systems of communication.

Appropriateness of Key Performance Indicators (KPIs).

Governance of the contract from a clinical operations perspective.

5.2 In order to try and provide the Audit Committee with a balanced perspective, meetings also took place with members of the GSTS clinical and managerial teams and all GSTS staff were encouraged to participate in a confidential on-line survey.

5.3 Participation from both Trust and GSTS staff was excellent and whilst a

number of concerns were raised the overall impression was one of a desire to move forward.

User Survey

5.4 The online survey was distributed to all medical staff, ward managers, matrons, and AHPs using the Trust email address lists. This population represents more than 3,000 members of staff although a high proportion of these will not be pathology users. The survey opened on 30 July and closed on 20 August, allowing users 3 weeks to complete the survey.

5.5 A total of 134 responses were received (compared to approximately 60 in

2012), of which 119 (89%) were clinicians and 14 (10%) were nurses. 74% of respondents were based at St Thomas’ Hospital with the remainder based at Guy’s.

5.6 The majority of the questions were multiple choices, with answers ranging

from very satisfied to very dissatisfy. Users were asked to provide narrative comments where they had answered dissatisfied or very dissatisfied only.

5.7 It is interesting to note that for each question at least 50% of responses were

either neutral or positive. For pathology services by lab, 90% of responses ranged from neutral to positive, with 10% responding negatively. At a lab level, the highest scores were for Microbiology and Immunology (at 97% ranging from neutral to positive) with Blood Transfusion and Cytology (at 96% ranging from neutral to positive) while the lowest scores were Chemistry (81%

Doc 15

Commercial In Confidence

Audit Committee September 2013 42 Draft GSTS Pathology Review

ranging from neutral to positive) and Phlebotomy (80% ranging from neutral to positive).

5.8 A high proportion of respondents (79%) believe the service has either stayed

the same or improved in the past 6 months. The question with the most positive result was Question 10 relating to the quality of professional clinical and scientific advice where only 1 respondent was dissatisfied and 1 extremely dissatisfied. The most negative result was Question 14, relating to the reliability of getting specimens to the lab, where 35% of respondents were dissatisfied and 14.3% were very dissatisfied. The key areas that respondents feel should be improved are:

Communications:

There were a number of points relating to the difficulties in getting hold of the correct people in the labs, finding the correct telephone numbers, ensuring there are sufficient knowledgeable staff to respond to phone calls and politeness of staff on the phone. In response to this GSTS are planning to continue their work in developing a customer service team to ensure that the correct contact numbers are easily accessible on both the Trust Intranet and the GSTS website.

Portering and Air Chute issues Users are experiencing ongoing problems with the reliability of the air chute coupled with issues of poor response from portering staff. This has a significant impact on the ability of the labs to meet turnaround times and provide an efficient service. As both portering and the chute system are run by GSTT for GSTS as part of the TSA the Trust needs to resolve these as a matter of urgency.

Electronic reporting

Respondents generally feel that there are delays and inefficiencies for the areas where results are not available on EPR (genetics and molecular most frequently noted).

Test Turnaround Times and Service Variability Specific tests where the turnaround times require improvement are D-Dimers and Troponin for A&E. A number of respondents believe that there is variability and inconsistency in the levels of service in some areas, particularly out of hours and at weekends.

5.9 Based on the results of this survey, it would appear that users appear to be

satisfied with the service overall. However there are specific areas where further effort is required in order to address challenges and ensure the service is fit for purpose and improves on an ongoing basis. The full survey is attached at appendix 3.

Directorate Meetings

5.10 The Meetings with the Directorate Management Teams were designed to provide the opportunity to raise not only general areas of concern also but specific issues relating to service provision. Three Directorates had no

Doc 15

Commercial In Confidence

Audit Committee September 2013 43 Draft GSTS Pathology Review

concerns to raise and were relatively happy with the services provided. The remaining Directorates raised anything from one to multiple issues that had been outstanding for some time. All felt that the benefits expected via the Joint Venture had not been realised. The table below is not exhaustive but provides an indication of general areas of concern:

Issues Implications

Unavailability of all results on EPR

Difficult to find results

Can lead to repeat testing

Down time of air chutes Delays in receipt of results

Possible delays in discharge

Lack of continuity of GSTS Staff and knowing who to contact

Frustration from Directorate staff at constant repetition of issues

Leads to Directorates ‘living’ with the problem rather than seeking resolution

Problems with billing: Concerns that Directorates are paying for services not ordered by their staff

Problems with patient level reporting

Work undertaken by Oral Pathology includes work requested by ENT and Cancer however Dental are billed for the total service. The lack of patient level information results in an inability to align budgets correctly

Delays in the implementation of Price per test:

Changes in clinical practice i.e. using cheaper/fewer tests can not be translated into directorate savings

Concerns from Directorate Teams that reduction in the number of tests requested will result in an increase in GSTS prices

Poor Turn around times Delays in clinical decision making

Decisions taking unilaterally without consultation with the local clinical team

15 minutes as the maximum time to bleed a child.

Lack of flexibility to respond to fluctuations in demand

Problems with lack of appropriate support during peaks in activity demand

GSTS structure is difficult to understand

Unable to identify who to go to

Lost Samples Late delivery

Impact on A&E waiting times

Doc 15

Commercial In Confidence

Audit Committee September 2013 44 Draft GSTS Pathology Review

Issues Implications

On-going issues around accountability for the Stat Lab in STH Critical Care:

The Directorate Management Team are in discussions with the 4th management team from GSTS

Pathologists felt disenfranchised Disconnected staff base

Review of GSTS compliance with CQC Standards

5.11 There are 16 essential standards that relate most directly to the quality and safety of care within Pathology services. The CQC inspected GSTS Pathology Services in July 2012 and found that in most respects they were meeting the standards required. However, there were some shortcomings in the training and support provided to staff in the phlebotomy department. In particular they felt that staff were not fully protected against the risks of unsafe care and treatment as the provider did not have in place suitable arrangements to ensure that staff were appropriately supported in relation to the their responsibilities.

5.12 In response to this GSTS implemented a range of initiatives including:

The appointment of a training co-ordinator to manage training in the Phlebotomy department.

The production of standard operating procedures for staff.

A workshop for staff on customer services and complaints handling.

Detailed competence assessment and tutorials for staff.

Focus groups to review values and behaviours.

Introduction of regular staff meetings. 5.13 The CQC revisited the service in March 2013 and found that the service had

now met the standard.

CPA Accreditation

5.14 GSTS have achieved progress in CPA accreditation. On establishment in 2009 two laboratories had only conditional accreditation and one was not accredited. As per the table below progress has been made and all laboratories now have full accreditation. The remaining two laboratories the Haemostasis & Thrombosis: Vitamin K EQA scheme organiser and the Clinical Transplant Unit are accredited on a non ISO 15489 basis.

Doc 15

Commercial In Confidence

Audit Committee September 2013 45 Draft GSTS Pathology Review

Laboratory/ CPA Lab No

Current Status

2012 2011 2010 2009 2008

Blood Sciences 0799

Accredited Conditional

Cellular Pathology 0800

Accredited Conditional Jul 12-Apr

13

Conditional Jan 09-Apr

10 Infection &

Immunology 0803 Accredited

Haemostasis & Thrombosis 0909

Accredited

Oral Pathology 1608

Accredited Conditional Oct 12-Jan

13

Clinical Transplant Unit

1696

Accredited

Genetics Centre (DNA &

Biochemistry labs) 1770

Accredited

Biochemical Sciences 1867

Accredited Conditional Nov 12-Feb 13

Cytogenetics1993 Accredited St. Johns

Histopathology 2008

Accredited Conditional Oct 09-Mar

10 Withdrawn St. Johns: EB lab,

Mycology, Skin Tumour Unit 4008

Accredited Not

Accredited Not

Accredited Not

Accredited Not

Accredited Not

Accredited

Adherence to Trust Policies

5.15 GSTS provides Pathology services on three sites, and historically, adopted the local policies and procedures in force when the JV was formed and for the new sites when these services were acquired. From the perspective of GSTT, the policies and procedures are followed in the following areas for all services provided on GSTT sites:

Health, safety and environment

IT

Finance and commercial

Governance, conduct and ethics

Human Resources

Procurement and supply chain

Quality management

Security

Doc 15

Commercial In Confidence

Audit Committee September 2013 46 Draft GSTS Pathology Review

5.16 GSTS has a board, committee and management structure that provides assurance on compliance with GSTT policies and procedures. There is evidence of a Quality Management System for the labs, independent scrutiny by the specialist Laboratory Accreditation organisation (UKAS), a sophisticated Operational Performance Management System, regular audit of compliance with policies and procedures at laboratory level, and an Audit Committee. The Audit Committee conducts audits to ensure that GSTS is operating effectively and risks are being managed in line with the relevant policies and standards. GSTS corporate staff and all GSTS staff working on GSTT sites have access to GTi and the full suite of GSTT policies and procedures.

Effectiveness of Formal and Informal Systems of Communication

5.17 Whilst a range of issues were raised by the Directorates, at the core of the concerns was the perceived lack of responsiveness by the GSTS team. In most examples examined, the Directorate Teams had undertaken multiple conversations with a number of GSTS staff but felt that in most cases very little or no headway had been made towards a resolution.

5.18 There was little evidence of any proactive behaviour on the part of GSTS

towards customer care and most Directorate Teams have no idea who to contact within GSTS if they have any issues. As a consequence opportunities for joint working are missed and there appears to be a lack of understanding on both sides of the strategic and operational aspirations of each organisation.

5.19 It is also apparent that the clinical teams fail to include GSTS in service

developments and the annual business planning cycle. 5.20 Recommendations:

The General Manager of the GSTS Team should attend the weekly General Managers’ meetings.

The role of the PSA Manager should be revisited to ensure that there is a clear understanding of how this resource can be best utilised to provide a key ‘link’ between the two organisations. The PSA Contract Manager should have a clear operating brief especially in respect of the special circumstances whereby GSTT is both a Customer and a Share Holder.

GSTS also in line with the PSA Contract, need to provide a suitable and authorised Contract Manager to work opposite the Trust Authorised Officer (in line with the PSA Contract.

GSTS possibly in conjunction with the PSA Manager should agree a proactive approach to the development of good working relationships with the Directorates. It is recommended that regular meetings take place with an emphasis on the quality of service delivery rather ad hoc meetings in response to complaints.

Clinical Services should include GSTS fully in the Business Planning cycle.

Appropriateness of KPIs

5.21 The contract between the Trust and GSTS contains 18 KPIs focused on test turn around times and PIs predominately covering Phlebotomy Waiting

Doc 15

Commercial In Confidence

Audit Committee September 2013 47 Draft GSTS Pathology Review

Times. The KPIs agreed reflected the Trust’s then ability to demonstrate evidence based measures on which to base future performance rather than a robust set of quantifiable measurements that reflect the critical success factors of the organisation.

5.22 There is a joint appreciation from GSTS and GSTT that the current KPIs need

to be reviewed urgently and attempts have been made over the last two years to agree a set that are robust enough to indicate the success or otherwise of the service being provided.

Recommendation: The PSA Contract Manager should lead a cross-organisational team to develop revised KPIs to enable the Trust to measure the effectiveness of various elements of the GSTS service, including response to innovation and financial indicators.

Operational Governance of the Contract

5.23 The Chief Operating Officer was keen that this review attempted to identify any action that the clinical teams could take to improve the efficiency of the customer provider interface. During the meetings with both the Directorate and GSTS teams it became clear that there is a genuine lack of understanding of where and how operational and strategic decisions are taken. Although there is a formal governance structure the process and responsibility for taking action when local resolution is unsuccessful is ambiguous.

GSTS Governance Structure

5.24 Although there is a formal governance structure within GSTS this not so clearly defined within the Trust. As a consequence the route for communicating and implementing decisions taken at both the Members’ and

Operational Boards is ambiguous. There is a misconception from both Trust and GSTS staff that if an issue is discussed at the Member or Operations Boards there is an automatic route to cascade this information to the relevant Trust departments for action. This is not the case. The ‘disconnect’ of formal

decision making and internal Trust delivery is a major risk to the smooth delivery of the contract.

Members Board

Operating Board

Governance Risk and Quality Committee

Executive Group Audit Committee Remuneration

Committee

Doc 15

Commercial In Confidence

Audit Committee September 2013 48 Draft GSTS Pathology Review

Trust Governance Structure for GSTS

5.25 The Joint Pathology Committee (JPC) is the only nominated body for monitoring delivery of the contract including KPI performance. It is defined in the PSA Contract as the Pathology Review Meeting and was previously called “Pathology Performance Review & Assurance Committee” (PPRAC). However it is not defined in the PSA Contract as to where this Committee reports to in the Trust nor does there appear to have been any governance follow up to confirm accountability; in effect it just “exists”. As a consequence this has likely been the main factor as to why “Governance” of the Customer Function has been somewhat diluted.

Recommendation

Whilst this report recommends strengthening both the governance and communication structures within the Trust it does not suggest that a further body be created but rather the existing mechanisms be reviewed and strengthened. In particular it is recommended that:

The Trust’s Director of Operations should became a member of the Operations Board

The JPC should be formally accountable to the Trust Management Executive

The JPC should be chaired by the Trust’s Director of Operations

The TOR should be revisited to provide greater emphasis on joint-working to overcome the ‘cultural and practical challenges to pathology transformation’.

The ToR of the JPC should be reviewed to ensure a clear governance system to monitor performance of the contract

Membership should be increased to include The Trust Chief Accountant or nominee.

5.26 The COO should consider identifying a senior member of the Management

Team to be the designated link with GSTS. This role could provide the vital support to both Trust and GSTS staff in order to establish effective working relationships foster a more open way of working and assist GSTS in successful delivery of their “One Organisation Programme”.

Joint Pathology

Committee

Joint Pathology Finance

and Commercial

Committee

Joint Pathology

Operational Meeting

Joint Third Party

Customer Group with

KCH

Doc 15

Commercial In Confidence

Audit Committee September 2013 49 Draft GSTS Pathology Review

GSTS Staff Satisfaction Survey

5.27 The Audit Committee was keen to gain an idea of how GSTS staff saw the first 5 years of the JV and in particular whether there had been any impact on staff morale and retention.

5.28 In order to achieve as broad a perspective as possible, GSTS encouraged their staff to complete an on-line confidential questionnaire. Around 550 people were invited to participate via an email link and 120 people took part. There was a representative mix of participants across roles, departments, employment types and length of service.

5.29 Less than 28% of people still feel they are aligned with the Trust rather than GSTS. 16 people didn’t choose any of the options listed with question with

the majority of these stating they don’t feel they belong to either organisation as there is a sense that neither party are interested in their well being.

5.30 While almost 27% of respondents were not employed prior to GSTS being formed and offered no view, of the remainder nearly 35% of employees feel the service has improved/stayed the same with nearly 39% feeling it has got worse.

5.31 Staff were asked for examples of how the service has improved since GSTS was formed. The key themes from this question were acknowledgement that there has been investment in new equipment and that there had been improvements to the service and turnaround times. IT and systems improvement (OPMS, SAP, GSTS IT Service desk) were also mentioned. There was also a mention that things had generally improved over the last two years.

5.32 An open response to the problem areas that people still feel GSTS need to address was provided, largely the key themes were as expected with many of them already having action plans associated with them as part of the One Organisation programme.

Understaffing and retaining experienced/skilled people was the main issue and the affect this is having on staff morale.

Providing training and more opportunities to develop Pressure for more funding for equipment and investment in R&D and IT The survey supports the perception that there is a lack of understanding

between the role of the corporate team and what happens in the laboratories.

5.33 Other comments

There is a sense that people would like to see GSTT and GSTS work much more collaboratively and that having ROE/GSTS employed people working together is neither efficient or fair given the disparity in terms of pay and benefits

Doc 15

Commercial In Confidence

Audit Committee September 2013 50 Draft GSTS Pathology Review

GSTS management were also asked to listen more to the people in the laboratories – specifically about equipment, processes and when testing new ideas. A copy of the full questionnaire is attached at appendix 4.

Customer Satisfaction Conclusion & Recommendations

5.34 There is little doubt that the early years of the joint venture have failed to deliver the logistical and clinical transformation that both organisations had hoped for. A number of factors ‘conspired’ to create this situation and both the Trust and GSTS have undertaken a range of initiatives to resolve the underlying problems in an attempt to build a strong platform for future development.

5.35 GSTS are planning to launch the One Organisation Programme aimed at aligning stakeholders around their vision, purpose and values. The Programme encompasses 9 key work streams:

Shareholders Align the JV partners (GSTT, KCH and Serco) around a renewed vision and purpose for GSTS

Rebranding Develop, launch and gain full acceptance of a new brand for GSTS

Clinical and Scientific Leadership Develop, consult and implement a new model of clinical and scientific leadership within GSTS.

Operational Leadership and Delivery Align operational leadership and service delivery to ensure tangible actions on the ground.

Laboratory Structure, Resourcing and Performance Develop optimal laboratory staffing and management structure and supporting framework.

Customer Sales, Marketing and Contract Management Implement effective sales and marketing plan, an approach to account management and increase the capability of the Commercial function.

Employee Proposition Implement and employee proposition that will ensure the attraction, development and retention of a unified, aligned and motivated workforce.

Web Site Develop and launch a powerful new web site that communicates the new brand and supports sales and staff recruitments.

Communications Framework Establish effective internal and external communication channels and key messages for engaging with stakeholders including strengthening the employee proposition, rebranding, clinical and scientific leadership and website development.

5.36 The strengthening of the corporate team and the introduction of shared accountability of service delivery across the clinical, scientific and management teams would appear to place GSTS in a good position for future development. It is positive to note that the issues raised by the clinical teams can be mapped to action plans within the 9 work streams of

Doc 15

Commercial In Confidence

Audit Committee September 2013 51 Draft GSTS Pathology Review

the One Organisation Programme. This will hopefully deliver some ‘quick-win’ solutions.

5.37 The clinical teams within GSTT have been disappointed and frustrated by

the slow pace of change and in particular the lack of GSTS responsiveness in dealing with operational concerns. In simple terms they feel that it is now ‘make or brake’. However there is still sufficient enthusiasm from the clinical teams to continue to work in partnership with GSTS to deliver a world-class service. What is important that this enthusiasm is nurtured and the clinical teams are given the confidence that GSTS will be responsive to their clinical needs.

5.38 Joint working has already commenced between GSTS and GSTT to

resolve a number of outstanding clinical issues. Senior members of the respective management teams are working on an urgent action plan which aims to agree a way forward on:

A&E

Phlebotomy

Implementing the investment in Next Generation Sequencing at Guys 5.39 In response to the first draft of this review a joint action plan has been

developed between GSTS and GSTT that captures the recommendations in this report and agrees a joint approach to their resolution.

Doc 15