Embed Size (px)

Citation preview

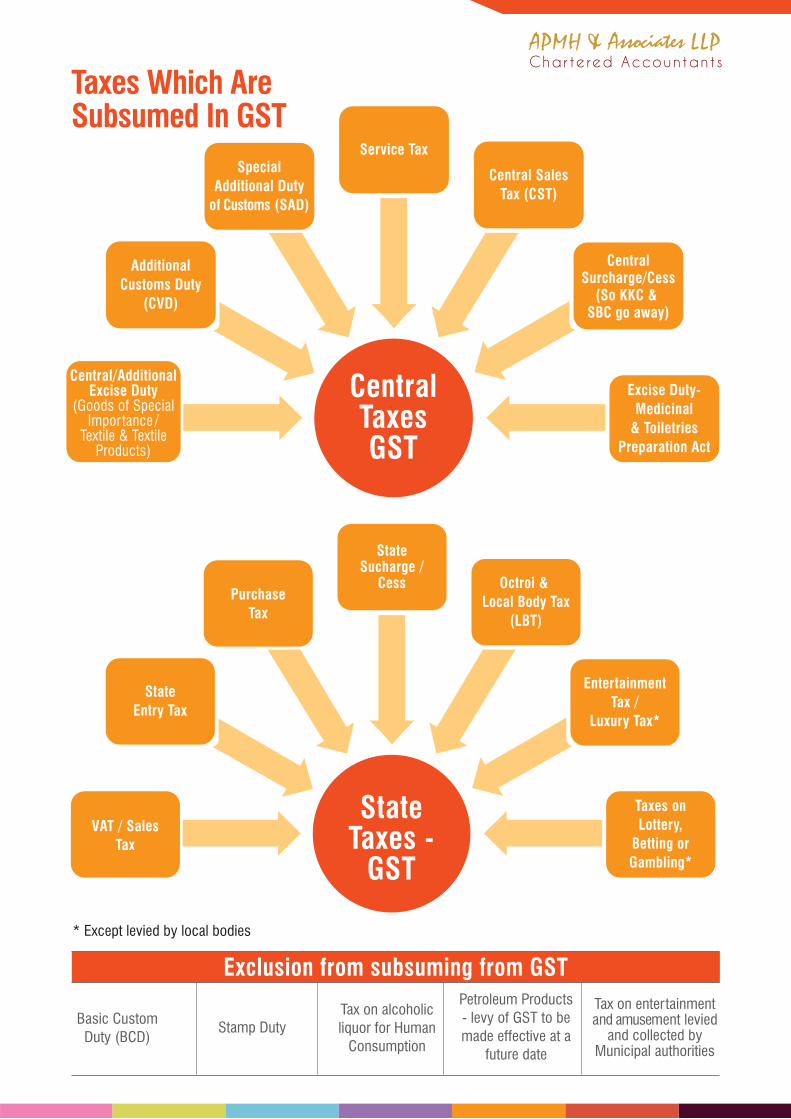

⇒ TAXES WHICH ARE SUBSUMED IN GST

⇒ PROPOSED TAX STRUCTURE POST GST

⇒ BENEFITS OF GST - FOR BUSINESS, GOVERNMENT & CONSUMERS

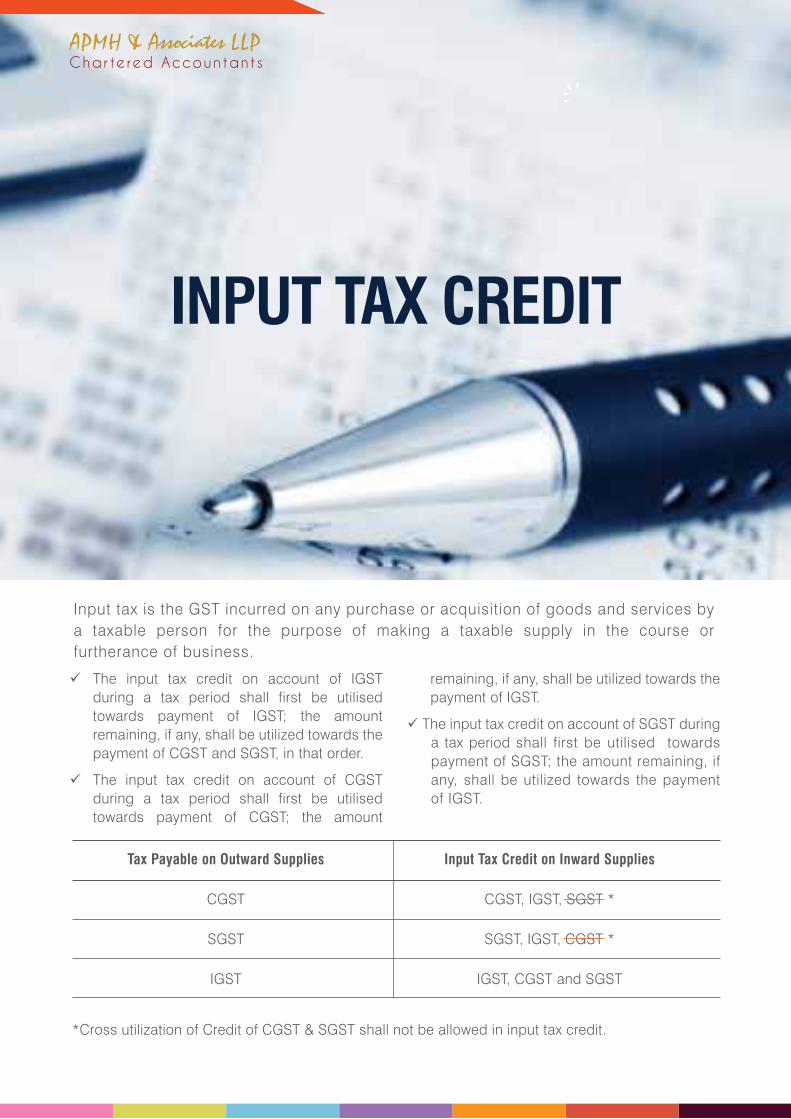

⇒ INPUT TAX CREDIT

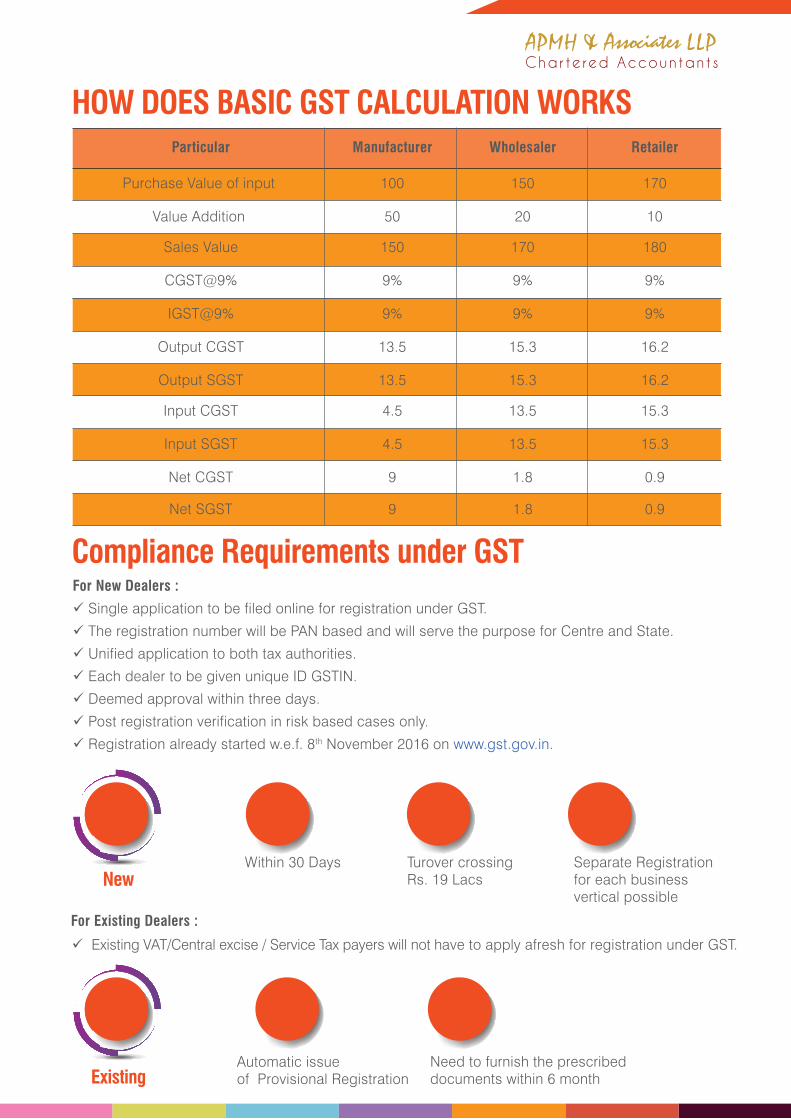

⇒ HOW DOES BASIC GST CALCULATION WORKS

⇒ COMPLIANCE REQUIREMENTS UNDER GST

⇒ ROUTINE COMPLIANCE

⇒ GST IMPACT ANALYSIS

⇒ BUSINESS DECISIONS NEEDING RE-CONSIDERATION IN GST REGIME

⇒ FINAL GST RATES

⇒ UNDERSTANDING GST IMPACT - AN EXAMPLE

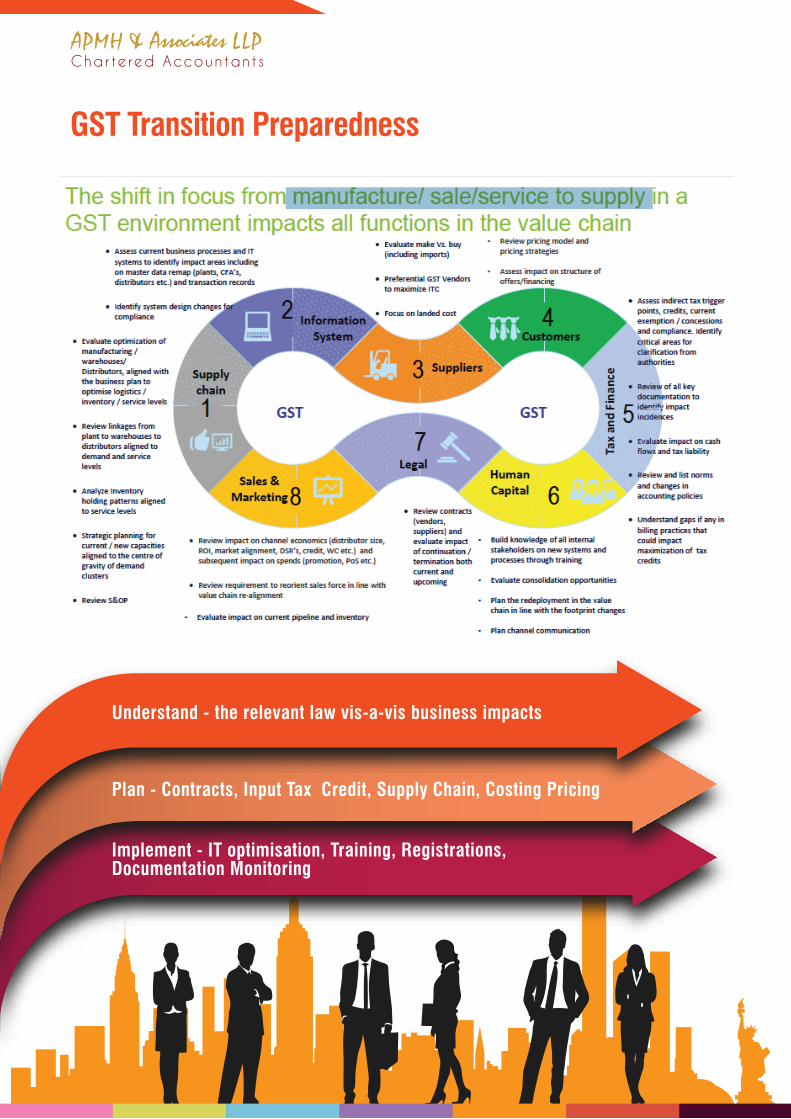

⇒ GST TRANSITION PREPAREDNESS

⇒ ABOUT APMH

Char te red AccountantsAPMH & Associates LLP

Taxes Which AreSubsumed In GST

Service TaxSpecial

Additional Dutyof Customs (SAD)

AdditionalCustoms Duty

(CVD)

Central/AdditionalExcise Duty

(Goods of SpecialImportance /

Textile & TextileProducts)

Excise Duty-Medicinal

& ToiletriesPreparation Act

CentralSurcharge/Cess

(So KKC & SBC go away)

Central SalesTax (CST)

CentralTaxesGST

StateSucharge /

CessPurchase

Tax

StateEntry Tax

VAT / SalesTax

Taxes onLottery,

Betting orGambling*

EntertainmentTax /

Luxury Tax*

Octroi & Local Body Tax

(LBT)

StateTaxes -

GST

Exclusion from subsuming from GST

Basic Custom Duty (BCD)

Stamp Duty

* Except levied by local bodies

Tax on alcoholic liquor for Human

Consumption

Petroleum Products - levy of GST to be made effective at a

future date

Tax on entertainment and amusement levied

and collected by Municipal authorities

Char te red AccountantsAPMH & Associates LLP

Proposed TaxStructure Post GST

Tax Structure

Direct Tax

Income Tax

Indirect TaxGST

(Except customs)

ImportTransaction

Inter StateIntra- state

Customs Duty+

IGST (Central)

IGST (Central)SGST (State)CGST (Central)

Export (Zero Rated)

Import

Factory

CGST+SGST

Purchase

BCD - Cost

IGST - Credit

Sale

CGST+

SGST

Warehouse

IGST

Purchase

IGST

Trf in Maharashtra

No Tax

Warehouse

CGST+SGST

Sale

Transfer

Outside India

Overseas Supplier

Overseas Customer

Maharashtra

India

OMS(Outside Maharashtra State)

Distributor

Supplier

Distributor

Supplier

Char te red AccountantsAPMH & Associates LLP

For the Centre and the States

According to experts, by implementing the GST, India will gain $15 billion a year. This is because, it will promote more exports, create more employment opportunities and boost growth. It will divide the burden of tax between manufacturing and services.

For individuals and companies

In the GST system, taxes for both Centre and State will be collected at the point of sale. Both will be charged on the manufacturing cost. Individuals will be benefited by this as prices are likely to come down and lower prices mean more consumption, and more consumption means more production, thereby helping in the growth of the companies.

Benefits of GST - Know Who Gains What-Industry, Government, Consumers

BUSINESS GOVERNMENT FINALCONSUMER

Reduction inmultiplicity ofIndirect taxes

Increased taxcollections due to

wider tax base

Rate reductionin prices possible.

Reduced cascading effect due to cross tax credit mechanism under GST

Bettercompliance Reduction intaxes if Govt. tax

collection increases

Non creditable CST to be removed will lead to

cost reduction

The input tax credit on account of IGST during a tax period shall first be utilised towards payment of IGST; the amount remaining, if any, shall be utilized towards the payment of CGST and SGST, in that order.

The input tax credit on account of CGST during a tax period shall first be utilised towards payment of CGST; the amount

*Cross utilization of Credit of CGST & SGST shall not be allowed in input tax credit.

Tax Payable on Outward Supplies Input Tax Credit on Inward Supplies

CGST CGST, IGST, SGST *

SGST SGST, IGST, CGST *

IGST IGST, CGST and SGST

INPUT TAX CREDIT

Input tax is the GST incurred on any purchase or acquisition of goods and services by a taxable person for the purpose of making a taxable supply in the course or furtherance of business.

remaining, if any, shall be utilized towards the payment of IGST.

The input tax credit on account of SGST during a tax period shall first be utilised towards payment of SGST; the amount remaining, if any, shall be utilized towards the payment of IGST.

Char te red AccountantsAPMH & Associates LLP

HOW DOES BASIC GST CALCULATION WORKS

Compliance Requirements under GST

Char te red AccountantsAPMH & Associates LLP

Particular Manufacturer Wholesaler Retailer

Purchase Value of input 100 150 170

Value Addition 50 20 10

Sales Value 150 170 180

CGST@9% 9% 9% 9%

IGST@9% 9% 9% 9%

Output CGST 13.5 15.3 16.2

Output SGST 13.5 15.3 16.2

Input CGST 4.5 13.5 15.3

Input SGST 4.5 13.5 15.3

Net CGST 9 1.8 0.9

Net SGST 9 1.8 0.9

For New Dealers :

Single application to be filed online for registration under GST.

The registration number will be PAN based and will serve the purpose for Centre and State.

Unified application to both tax authorities.

Each dealer to be given unique ID GSTIN.

Deemed approval within three days.

Post registration verification in risk based cases only.

Registration already started w.e.f. 8th November 2016 on www.gst.gov.in.

Existing VAT/Central excise / Service Tax payers will not have to apply afresh for registration under GST.

Existing

New

For Existing Dealers :

Automatic issueof Provisional Registration

Within 30 Days Turover crossingRs. 19 Lacs

Separate Registrationfor each businessvertical possible

Need to furnish the prescribeddocuments within 6 month

“GST is a significant move, but implementation is key”- RC Bhargava, Chairman of Maruti Suzuki

Business Decisions needingre-consideration in GST regime

Routine Compliance

Annual Compliance

Type of Dealers

Periodical returns

GSTR 8 -Annual Return By

31st Dec.next year

Special Cases For Normal

Dealers(Monthly)

GSTR 4 / 5 / 6 / 7 for special filings

in prescribed frequency

GSTR 2 -Inward

Supplies

GSTR 3-MonthlyReturn

GSTR 1 - Outward Supplies

Supply chain

o Sourcing strategy - Make v/s Buy

Distribution strategy – Stock transfer/Depot vs. Distributor/Dealer

o Sourcing pattern – availability of increased credits to vendors on services like renting of

immovable property, securities services, housekeeping services etc.

o Supply/Inventory management

Capital Expenditure

Impact on Margin and thereby Selling Price –IGST, No Retention

Sales in Transit to be done away with

Impact on Works Contract / EPC / Maintenance Contracts currently subject to dual taxes non

procurement/sale side

Char te red AccountantsAPMH & Associates LLP

Goods and Services Tax is on the fast track for roll out. Looking at coordination of GST Networks & GST council, the speed at which the decisions are being taken and things are being implemented, we can envisage that GST will be a reality w.e.f. 1st of April 2017.

Larger business groups have already studied the draft provisions, analysed the impact on their complex business models & multistate presence and started the march towards “ahead of curve” implementation. With Impact Analysis and different business scenarios envisaged in the future, people are being trained, supply chain is being redesigned, IT systems are being tweaked, contracts are being redrafted and so on.

It’s need of the hour for the visionary companies to start working on the impact analysis of GST on it’s business model & industry, to ideate their best foot forward and take the transition to their advantage.

A specialized GST team at APMH has developed the IT enabled models suiting various industry specific businesses to generate empirical impact analysis in the GST era. This is a onetime exerciseworth undergoing for assessing the tax impact, P & L impact, Cashflow impact, Working Capital impact in “As is” and various strategic scenarios to catalyse objective decision making for being “ahead of curve”. Our endeavour is to leave behind a smart modelling tool for scenario analysis even in times to come.

Team APMH consists of collaborative experience of legal aspects of GST and business understanding in combination with the cutting edge Technology capabilities for making viable this modelling exercise.

Our Team

Principal Consultant - GSTCA Pranav Kapadia

Management ConsultantCA Mitesh Katira

Director Internal AuditMr. Madhav Wagle

GST Impact Analysis

Collecting tax related data from various data sources

Straightening the Data for analysis

Predictive Analysis for GST ERA

Developing Beneficial Scenarios for business

Decision making and followup for implementation

Char te red AccountantsAPMH & Associates LLP

Understanding GST Impact - An ExampleParticulars Current Scenario GST

Base Price of Goods (Manufacturer) 100000 100000

Add: Excise / CGST 12500 9000

Add : VAT / SGST 16875 9000

Total Sale Value 129375 118000

Less: Input Tax Credit 16875 18000

Landed Cost (Distributor / Dealer) 112500 100000

Value Addition (Distributor / Dealer) 10000 10000

Basic Sale Value 122500 110000

Add: VAT / SGST 18375 19800

Cost to end Consumer 140875 129800

Differential Saving Due to Tax 11075

Percentile Saving on Manufacturer’s Price 11.07%

Char te red AccountantsAPMH & Associates LLP

Char te red AccountantsAPMH & Associates LLP

GST Rates Finalized by GST Council Meeting on 03.11.2016

Rate on Gold to be Decided Later

Luxury Car, Aerated Water and Tobacco may be taxed more than 28%

Additional Cess on Goods covered in 28%

0

5

12

18

28

Zero Tax Rate

Essential Food Items &Mass Consumption Items

Standard Rates

Maximum Goods &all the Services Standard Rate

May be Luxury Items,Pan Masala etc., Aerated Drinks

GST Transition Preparedness

Implement - IT optimisation, Training, Registrations,Documentation Monitoring

Plan - Contracts, Input Tax Credit, Supply Chain, Costing Pricing

Understand - the relevant law vis-a-vis business impacts

Char te red AccountantsAPMH & Associates LLP

Char te red AccountantsAPMH & Associates LLP

About APMH

APMH & Associates LLP is a leading Chartered Accountant Firm in Mumbai with it's network spread Pan-India for VAT, Service Tax, GST transition Consulting. The Firm is ideal Consulting, Audit, Outsourcing & Company Secretary firm for Corporate Houses, Multinationals, SMEs & Startups.

Our Objective is to synergize the expertise with information technology, in order to enhance the service delivery with strong client focus.

Pranav’s expertise lies in Advisory, Audit, Compliance, Corporate Training,

Litigation Matters on Value Added Tax (VAT), Central Sales Tax (CST), Profession

Tax (PT) and Service Tax. Pranav has been consultant to large corporates with

presence in Multiple States with complex structures in the Indirect Tax, especially

VAT. Pranav lucidly deals in complex legal matters like Works Contracts (WCT),

About the Author

DDQ (Determination Disputed Question) now called Advance Ruling (AR), Assessments and

Appeals relates to the VAT and other Sales Tax Laws. He is the Vice President of The Sales Tax

Practitioners Association of Maharashtra for 2015-16. Pranav is also part of the Indirect Tax

Research Committee of the WIRC of ICAI. He has been past Chairman of Indirect Tax Committee of

The Chamber of Tax Consultants for 2014-15 and past Convenor of Ghatkopar CPE Study Circle of

ICAI. Pranav has addressed various seminars and lectures on MVAT and CST at the STPAM,

Chamber of Tax Consultants, WIRC Study Circles of ICAI and various Industrial Associations in

Mumbai. Pranav is also Vice President of Sales Tax Practitioner Association of Maharashtra.

Write to [email protected] for further information.

Contact Us

To know more about APMH & Associates LLP, please visit www.apmh.in

Head OfficeD-613/614, Neelkanth Business Park, Opp. Railway Station, Vidyavihar (W),Near Ghatkopar, Mumbai 400 086

Mumbai Branch201, Bhaveshwar Complex, Station Road, Vidyavihar West, Mumbai 400 086

Roha Branch101, Landscape Apartment, Seva Dal Aali,Dhavir Chowk, Roha, Raigad - 402 109

Talk to UsEmail: [email protected]

Mumbai HO: 022-25146854/55 /56 /57

Mumbai Branch: 022-25146858

Roha Branch: 2194-234498, +91 986750 8556

Disclaimer: The information contained in this document has been compiled or arrived at from other sources believed to be reliable, but no representation or warranty is made to its accuracy, completeness or correctness. The information contained in this document is published for the knowledge of the recipient but is not to be relied upon as authoritative or taken in substitution for the exercise of judgment by any recipient. This document is not intended to be a substitute for professional, technical or legal advice or opinion and the contents in this document are subject to change without notice.

Whilst due care has been taken in the preparation of this document and information contained herein, neither APMH nor other legal entities in the group to which it belongs, accept any liability whatsoever, for any direct or consequential loss howsoever arising from any use of this document or its contents or otherwise arising in connection herewith.