Embed Size (px)

Citation preview

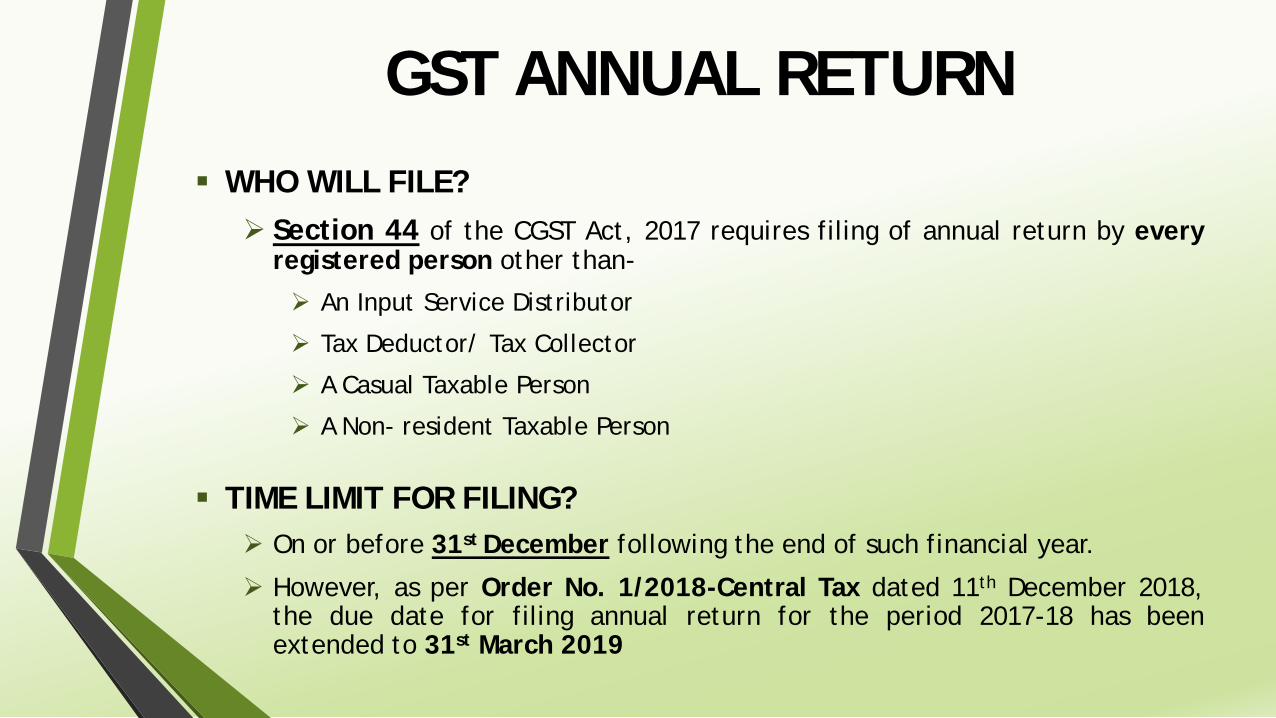

GST ANNUAL RETURN WHO WILL FILE? Section 44 of the CGST Act, 2017 requires filing of annual return by every

registered person other than-

An Input Service Distributor

Tax Deductor/ Tax Collector

A Casual Taxable Person

A Non- resident Taxable Person

TIME LIMIT FOR FILING? On or before 31st December following the end of such financial year.

However, as per Order No. 1/2018-Central Tax dated 11th December 2018,the due date for filing annual return for the period 2017-18 has beenextended to 31st March 2019

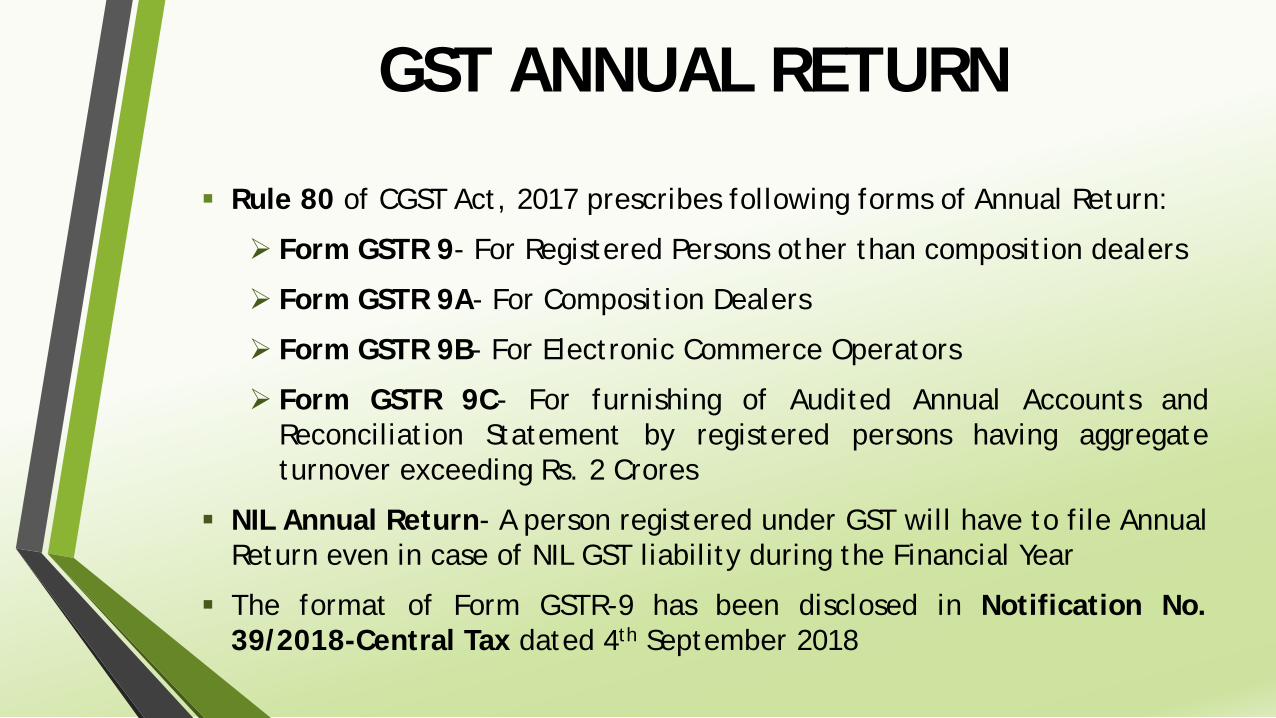

GST ANNUAL RETURN

Rule 80 of CGST Act, 2017 prescribes following forms of Annual Return:

Form GSTR 9- For Registered Persons other than composition dealers

Form GSTR 9A- For Composition Dealers

Form GSTR 9B- For Electronic Commerce Operators

Form GSTR 9C- For furnishing of Audited Annual Accounts andReconciliation Statement by registered persons having aggregateturnover exceeding Rs. 2 Crores

NIL Annual Return- A person registered under GST will have to file AnnualReturn even in case of NIL GST liability during the Financial Year

The format of Form GSTR-9 has been disclosed in Notification No.39/2018-Central Tax dated 4th September 2018

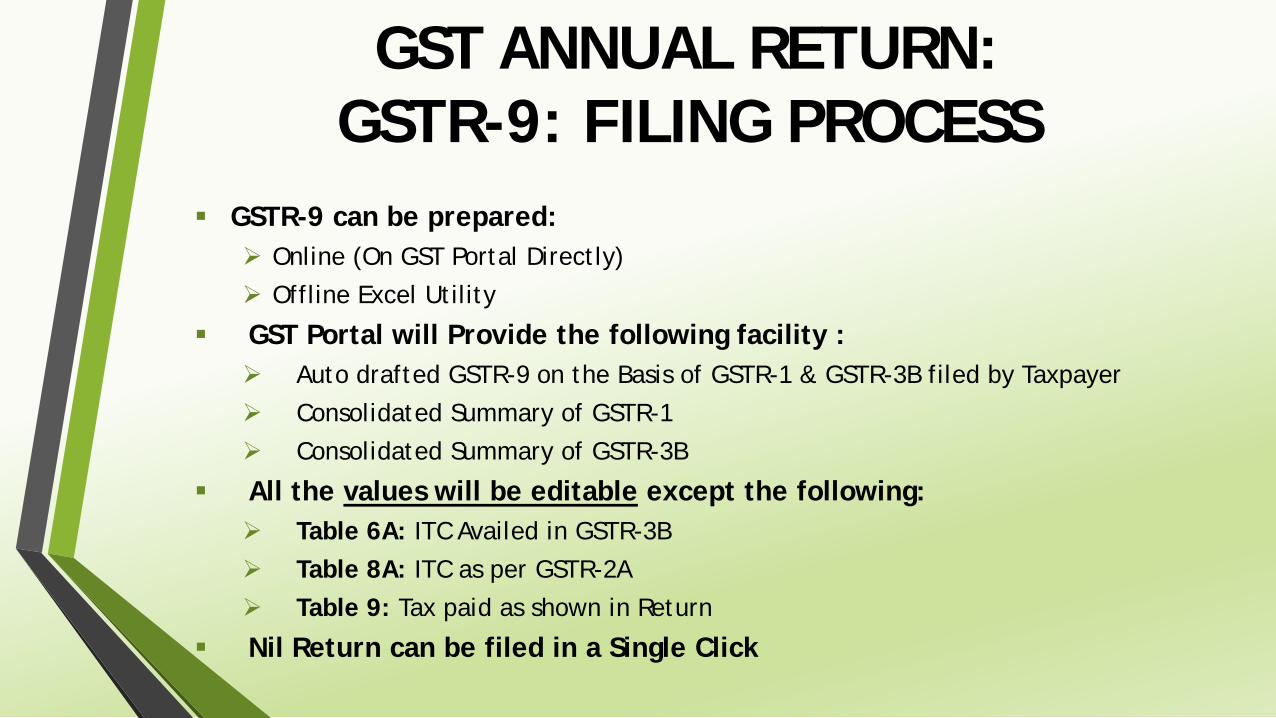

GST ANNUAL RETURN: GSTR-9: FILING PROCESS

GSTR-9 can be prepared: Online (On GST Portal Directly) Offline Excel Utility

GST Portal will Provide the following facility : Auto drafted GSTR-9 on the Basis of GSTR-1 & GSTR-3B filed by Taxpayer Consolidated Summary of GSTR-1 Consolidated Summary of GSTR-3B

All the values will be editable except the following: Table 6A: ITC Availed in GSTR-3B Table 8A: ITC as per GSTR-2A Table 9: Tax paid as shown in Return

Nil Return can be filed in a Single Click

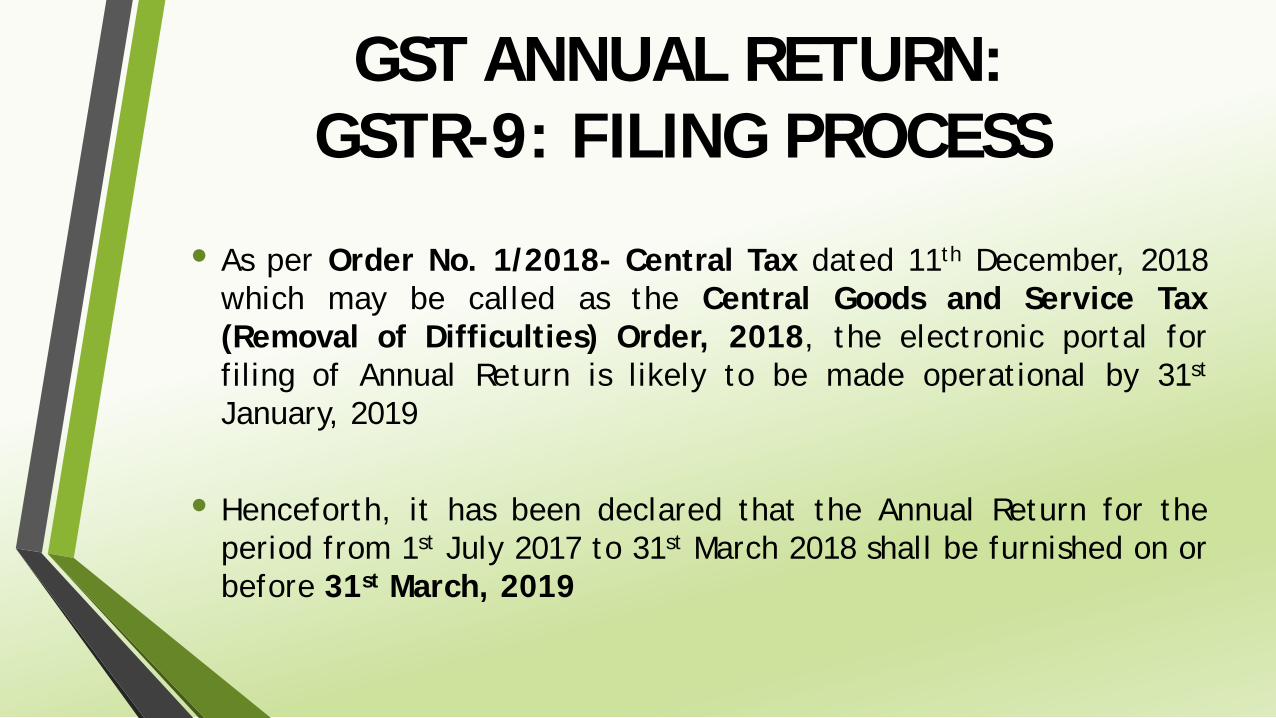

GST ANNUAL RETURN: GSTR-9: FILING PROCESS

• As per Order No. 1/2018- Central Tax dated 11th December, 2018which may be called as the Central Goods and Service Tax(Removal of Difficulties) Order, 2018, the electronic portal forfiling of Annual Return is likely to be made operational by 31st

January, 2019

• Henceforth, it has been declared that the Annual Return for theperiod from 1st July 2017 to 31st March 2018 shall be furnished on orbefore 31st March, 2019

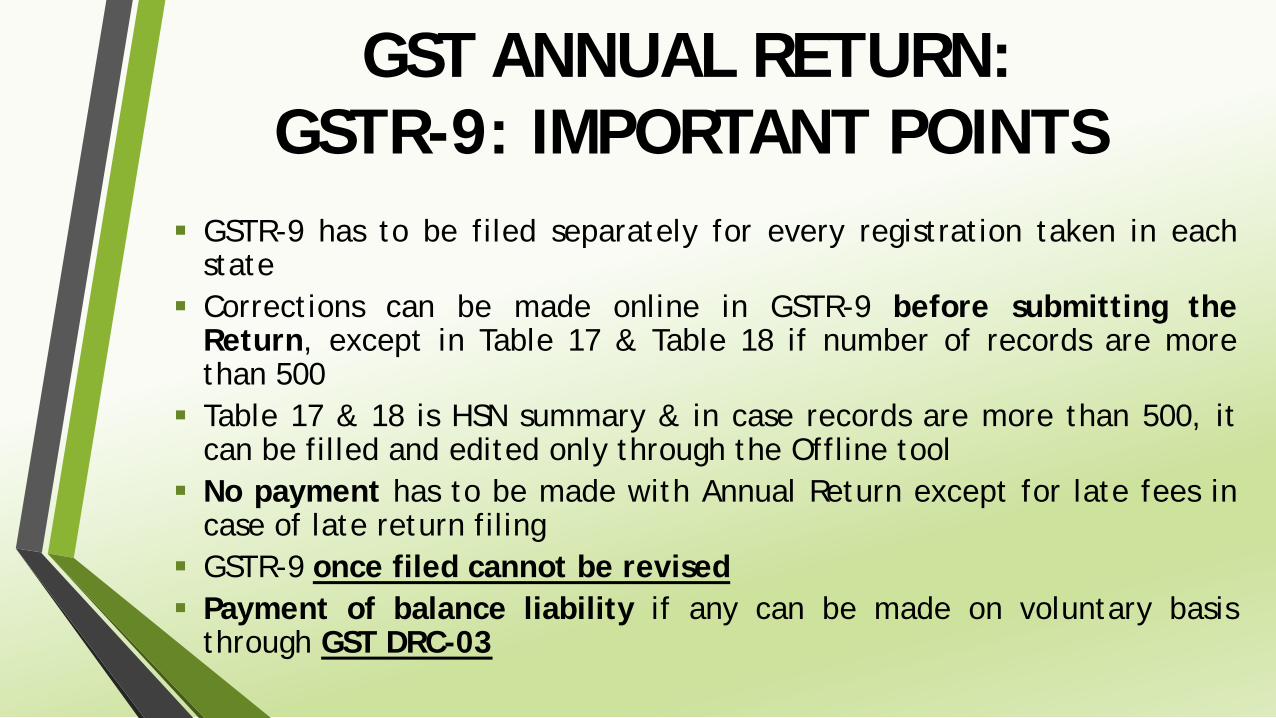

GST ANNUAL RETURN:GSTR-9: IMPORTANT POINTS

GSTR-9 has to be filed separately for every registration taken in eachstate

Corrections can be made online in GSTR-9 before submitting theReturn, except in Table 17 & Table 18 if number of records are morethan 500

Table 17 & 18 is HSN summary & in case records are more than 500, itcan be filled and edited only through the Offline tool

No payment has to be made with Annual Return except for late fees incase of late return filing

GSTR-9 once filed cannot be revised Payment of balance liability if any can be made on voluntary basis

through GST DRC-03

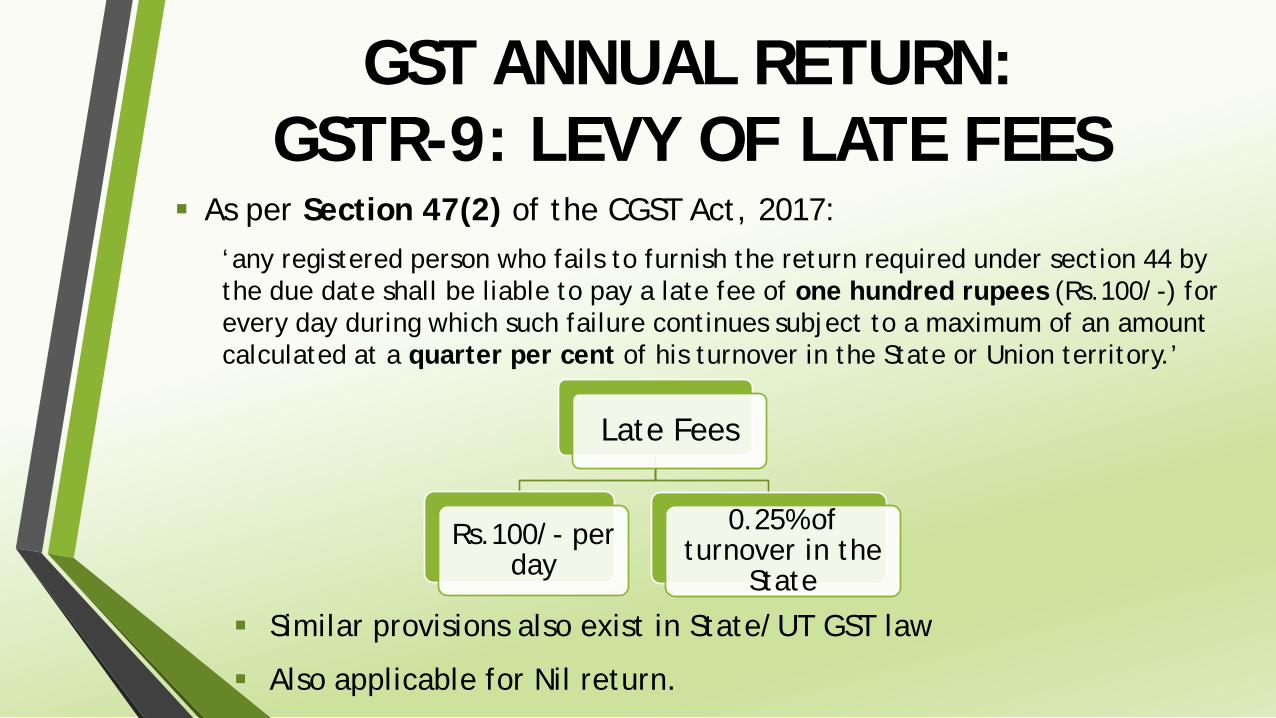

GST ANNUAL RETURN:GSTR-9: LEVY OF LATE FEES

As per Section 47(2) of the CGST Act, 2017:‘any registered person who fails to furnish the return required under section 44 by the due date shall be liable to pay a late fee of one hundred rupees (Rs.100/-) for every day during which such failure continues subject to a maximum of an amount calculated at a quarter per cent of his turnover in the State or Union territory.’

Late Fees

Rs.100/- per day

0.25% of turnover in the

State

Similar provisions also exist in State/UT GST law

Also applicable for Nil return.

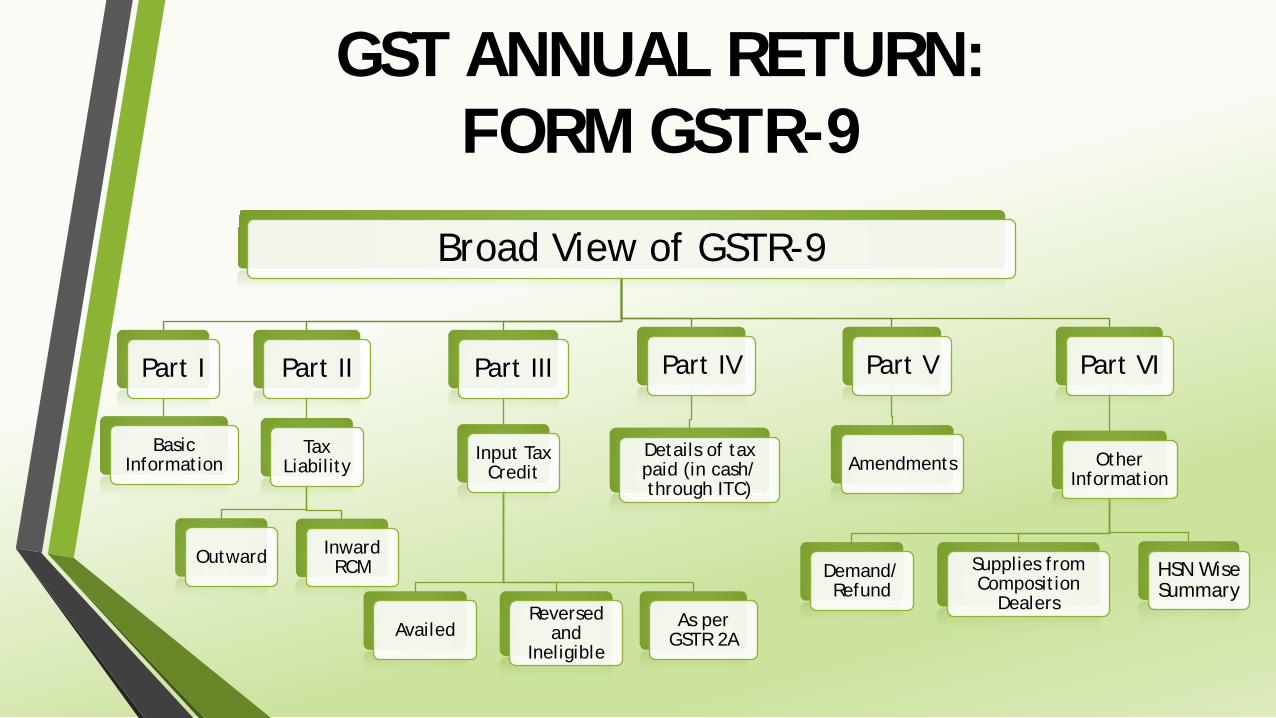

GST ANNUAL RETURN:FORM GSTR-9

Broad View of GSTR-9

Part I

Basic Information

Part II

Tax Liability

Outward Inward RCM

Part III

Input Tax Credit

AvailedReversed

and Ineligible

As per GSTR 2A

Part IV

Details of tax paid (in cash/ through ITC)

Part V

Amendments

Part VI

Other Information

Demand/ Refund

Supplies from Composition

Dealers

HSN Wise Summary

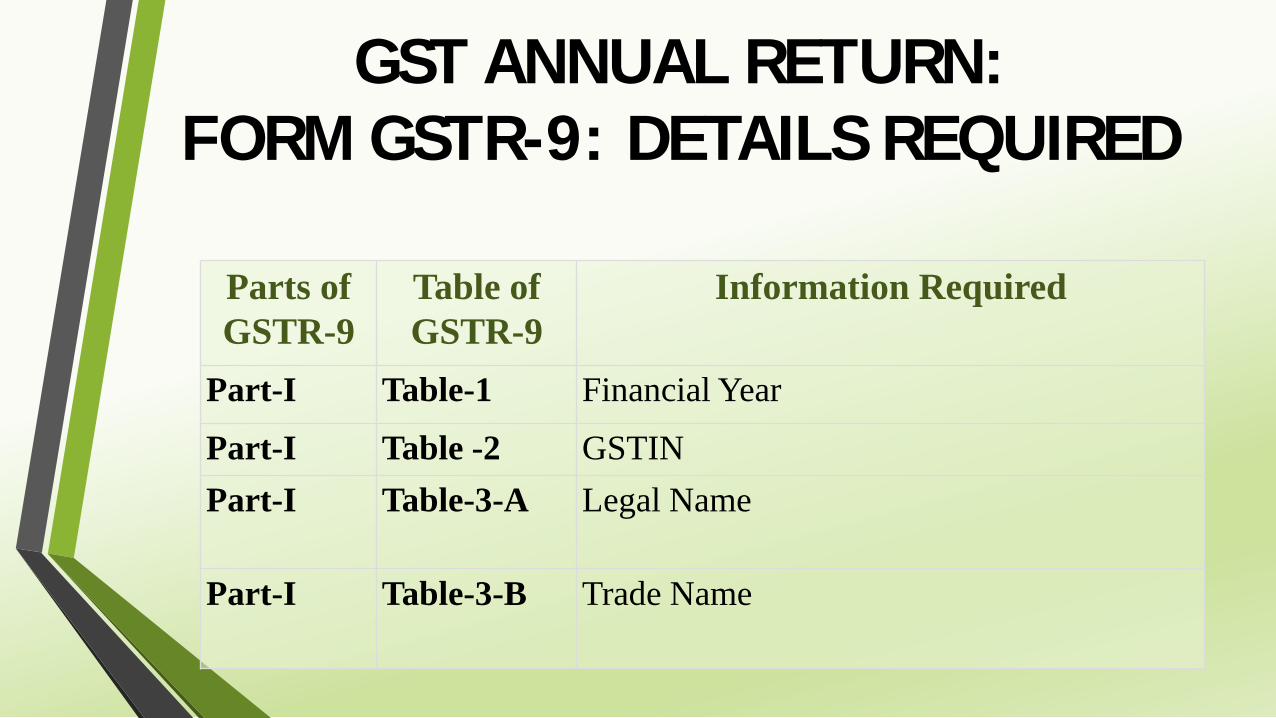

GST ANNUAL RETURN:FORM GSTR-9: DETAILS REQUIRED

Parts of GSTR-9

Table of GSTR-9

Information Required

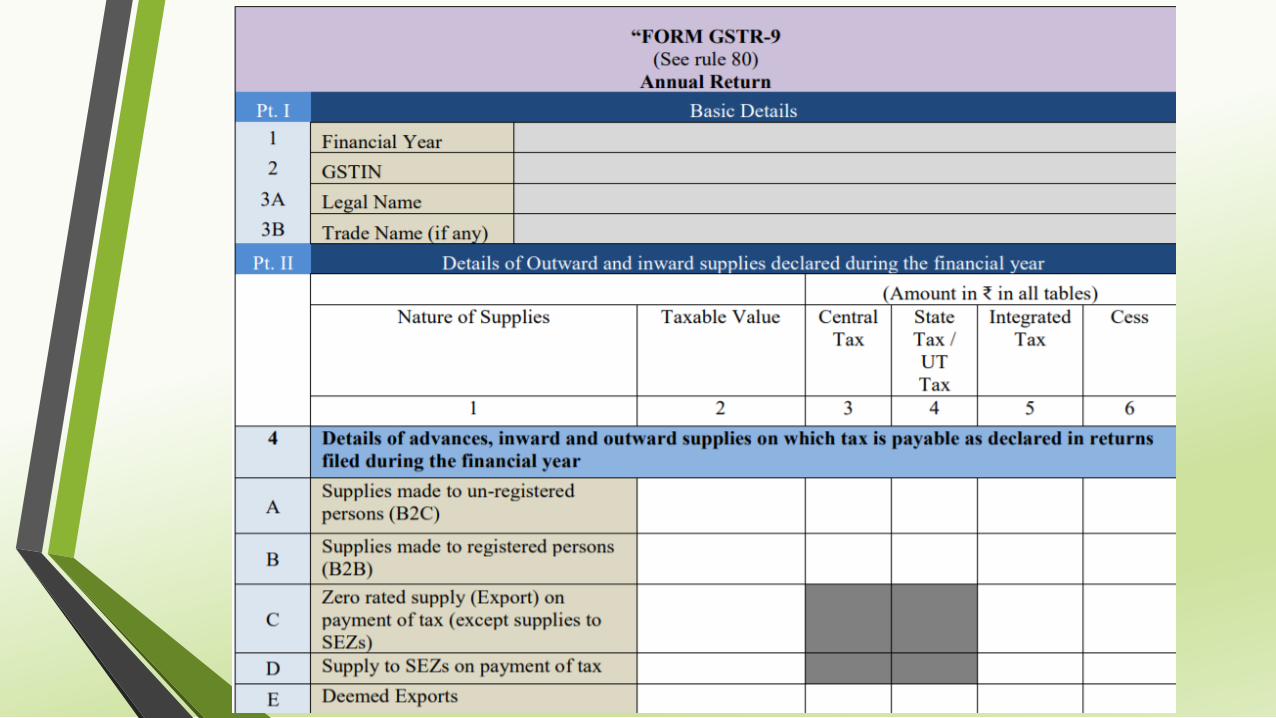

Part-I Table-1 Financial Year

Part-I Table -2 GSTINPart-I Table-3-A Legal Name

Part-I Table-3-B Trade Name

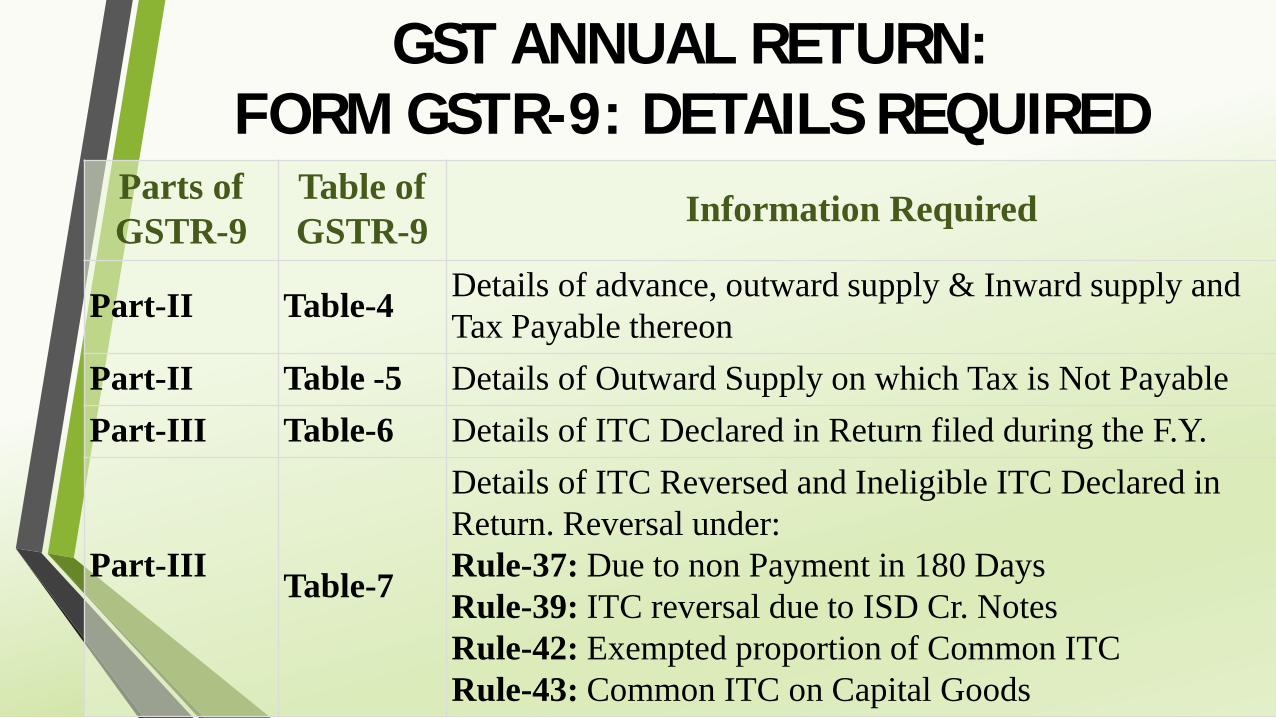

Parts of GSTR-9

Table of GSTR-9 Information Required

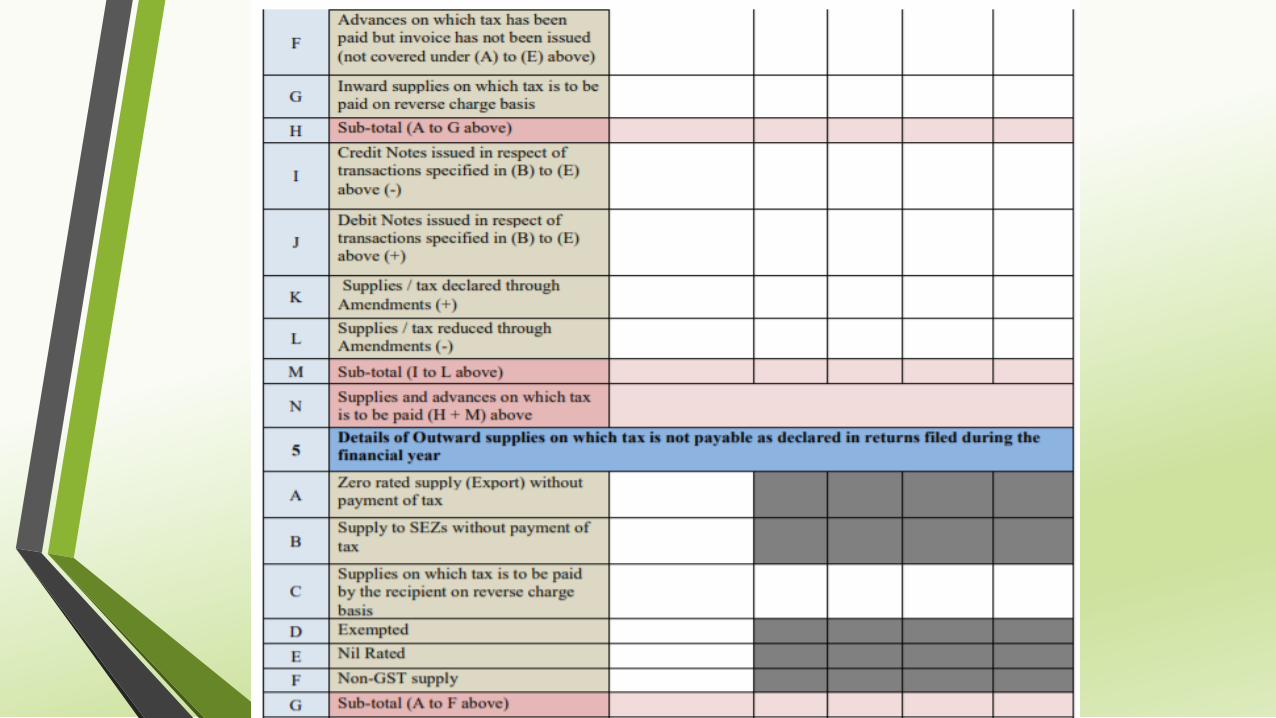

Part-II Table-4 Details of advance, outward supply & Inward supply and Tax Payable thereon

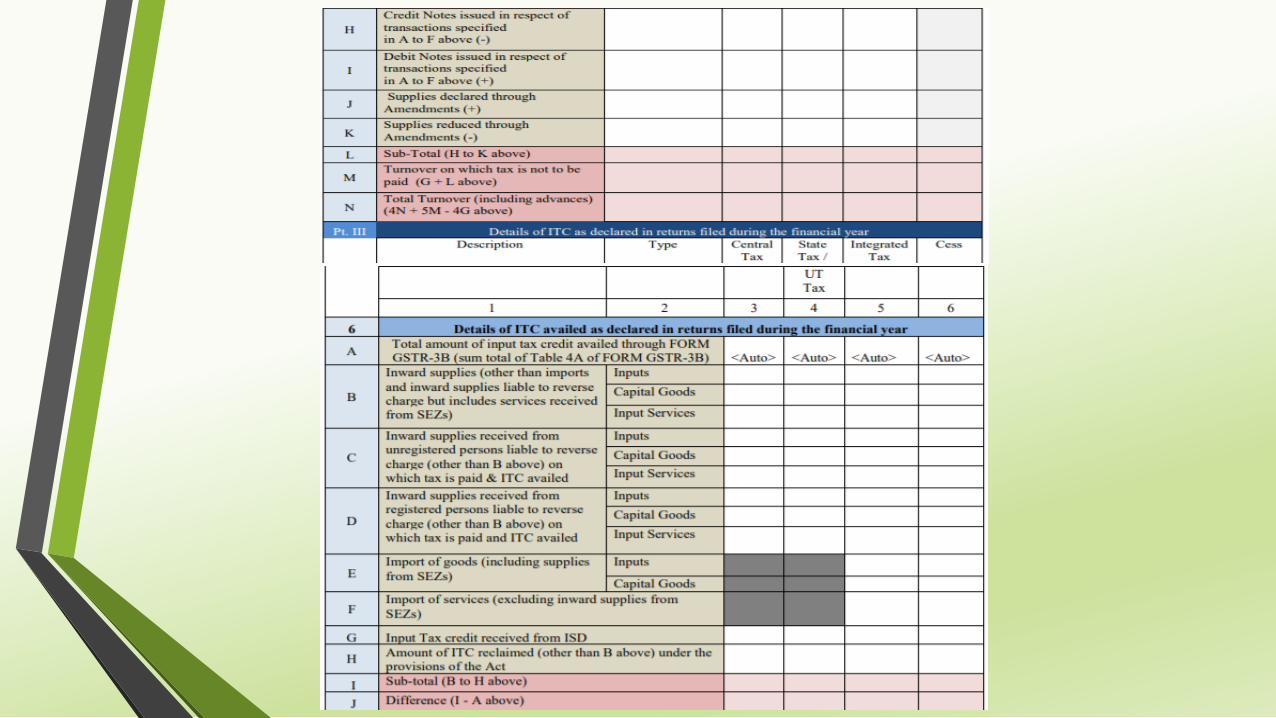

Part-II Table -5 Details of Outward Supply on which Tax is Not Payable Part-III Table-6 Details of ITC Declared in Return filed during the F.Y.

Part-III Table-7

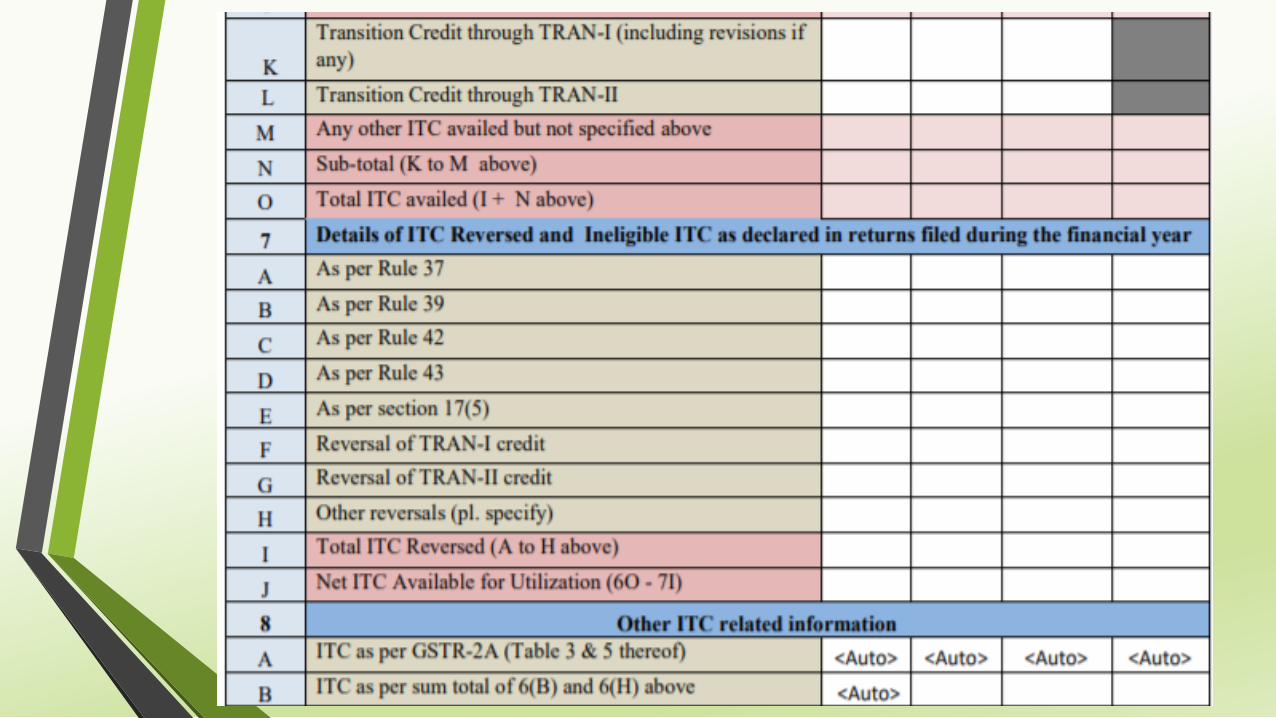

Details of ITC Reversed and Ineligible ITC Declared in Return. Reversal under:Rule-37: Due to non Payment in 180 DaysRule-39: ITC reversal due to ISD Cr. NotesRule-42: Exempted proportion of Common ITCRule-43: Common ITC on Capital Goods

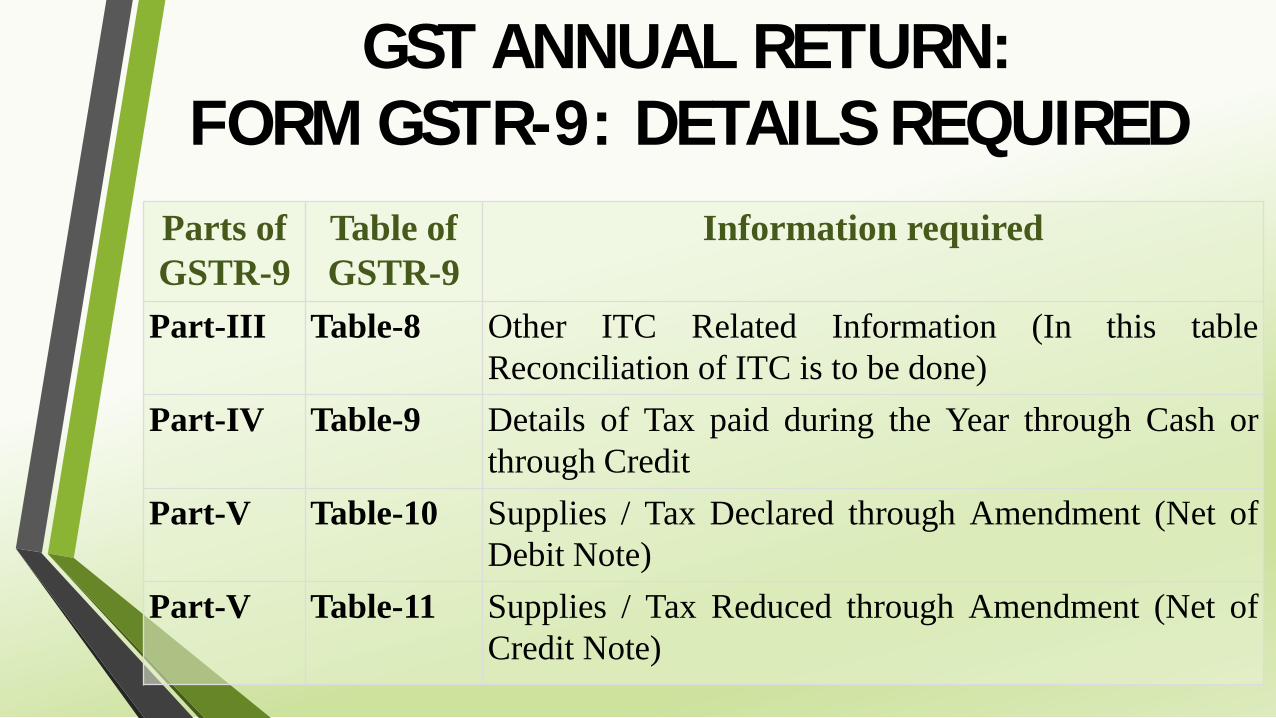

GST ANNUAL RETURN:FORM GSTR-9: DETAILS REQUIRED

GST ANNUAL RETURN:FORM GSTR-9: DETAILS REQUIRED

Parts of GSTR-9

Table of GSTR-9

Information required

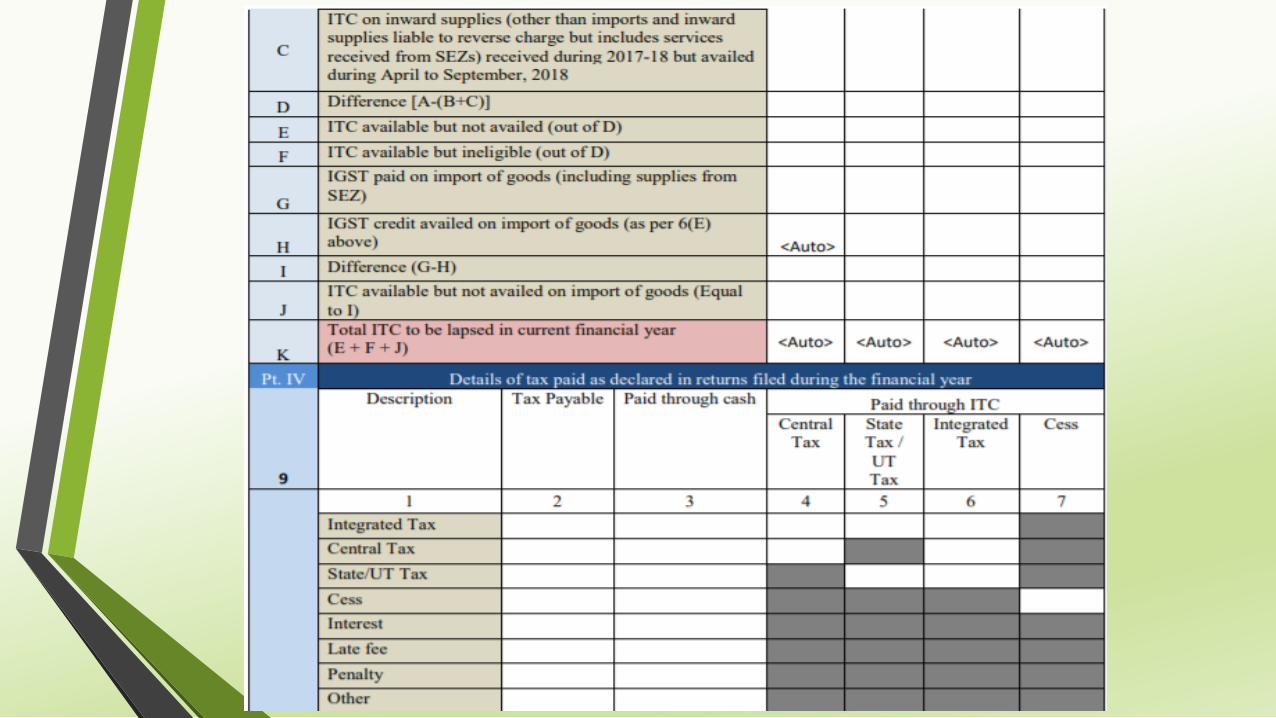

Part-III Table-8 Other ITC Related Information (In this tableReconciliation of ITC is to be done)

Part-IV Table-9 Details of Tax paid during the Year through Cash orthrough Credit

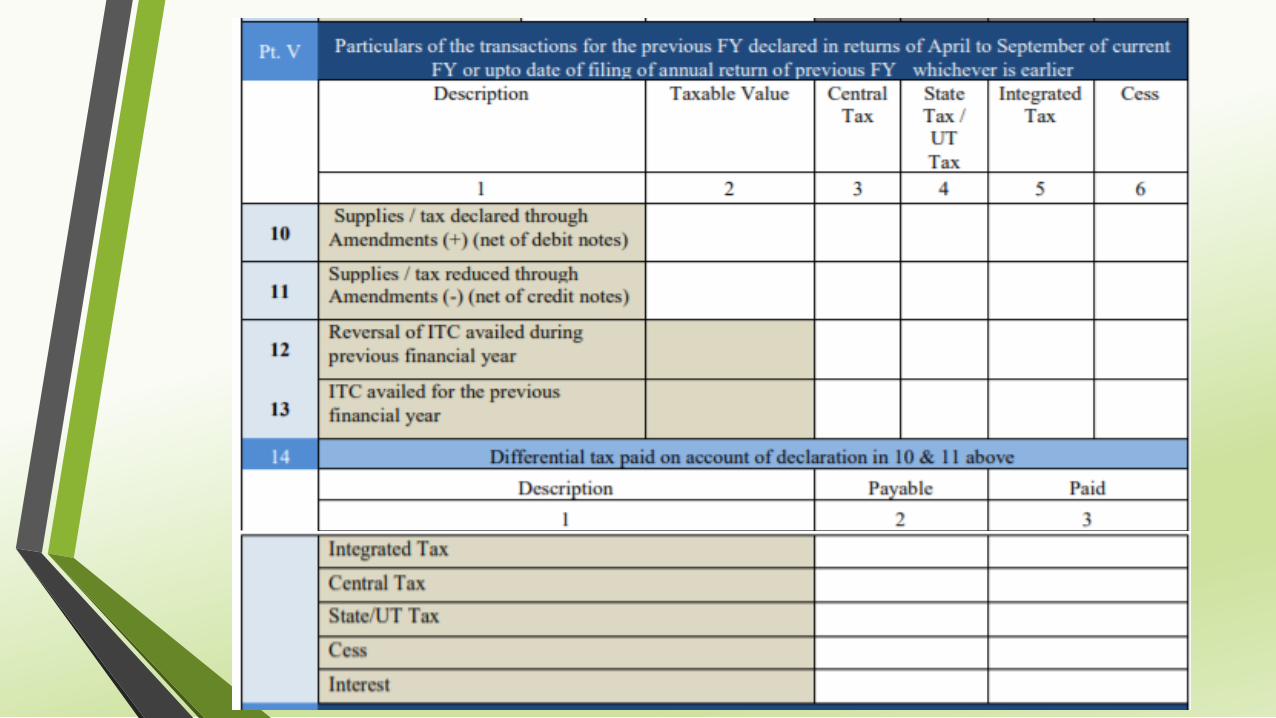

Part-V Table-10 Supplies / Tax Declared through Amendment (Net ofDebit Note)

Part-V Table-11 Supplies / Tax Reduced through Amendment (Net ofCredit Note)

GST ANNUAL RETURN:FORM GSTR-9: DETAILS REQUIRED

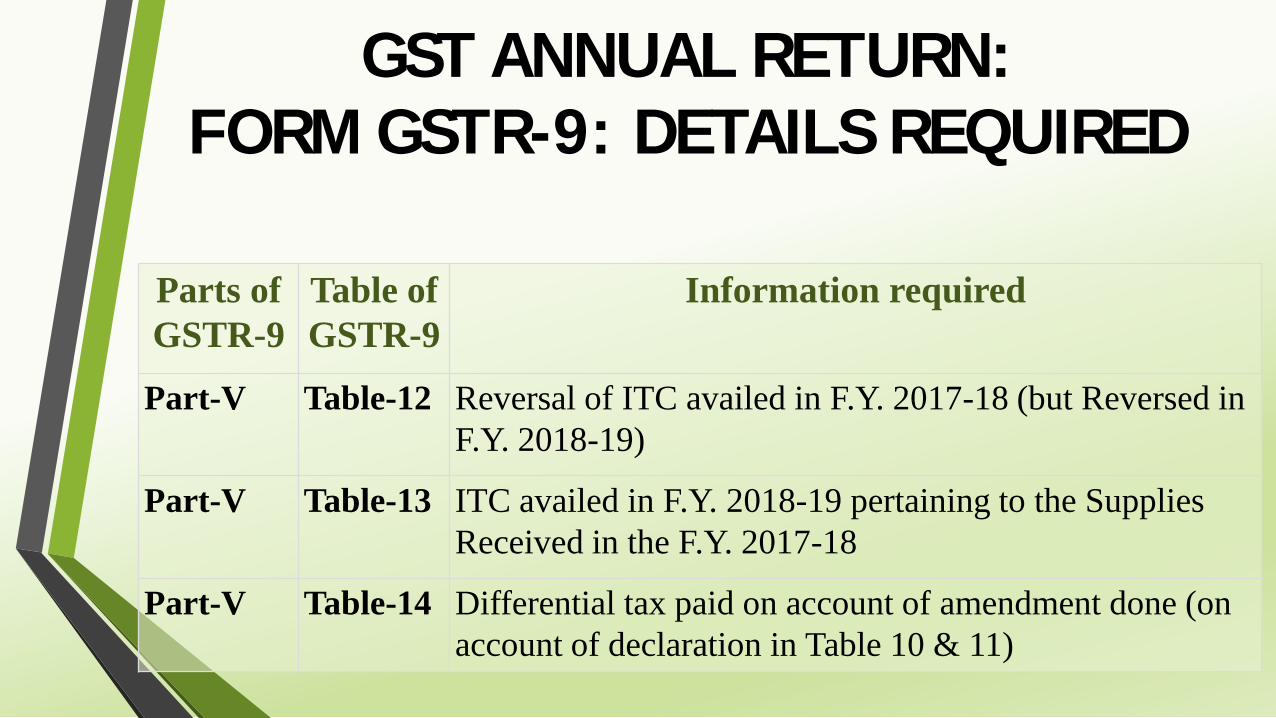

Parts of GSTR-9

Table of GSTR-9

Information required

Part-V Table-12 Reversal of ITC availed in F.Y. 2017-18 (but Reversed in F.Y. 2018-19)

Part-V Table-13 ITC availed in F.Y. 2018-19 pertaining to the Supplies Received in the F.Y. 2017-18

Part-V Table-14 Differential tax paid on account of amendment done (on account of declaration in Table 10 & 11)

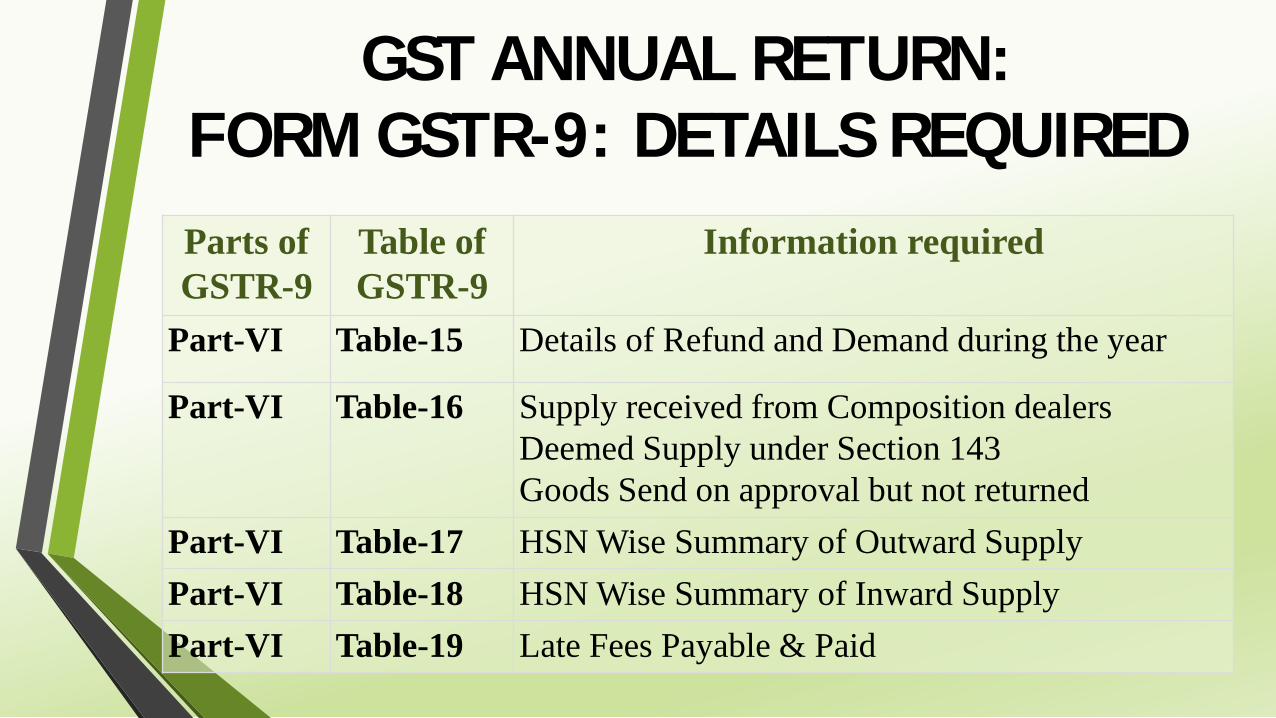

GST ANNUAL RETURN:FORM GSTR-9: DETAILS REQUIREDParts of GSTR-9

Table of GSTR-9

Information required

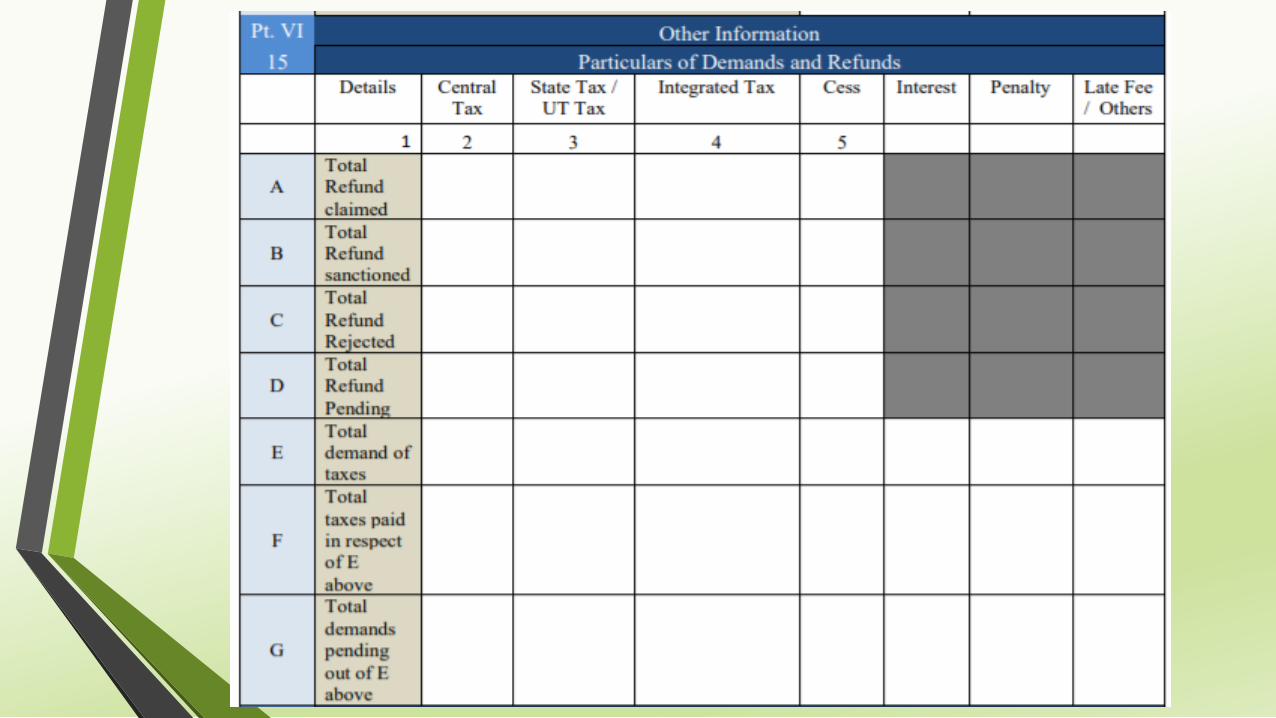

Part-VI Table-15 Details of Refund and Demand during the year

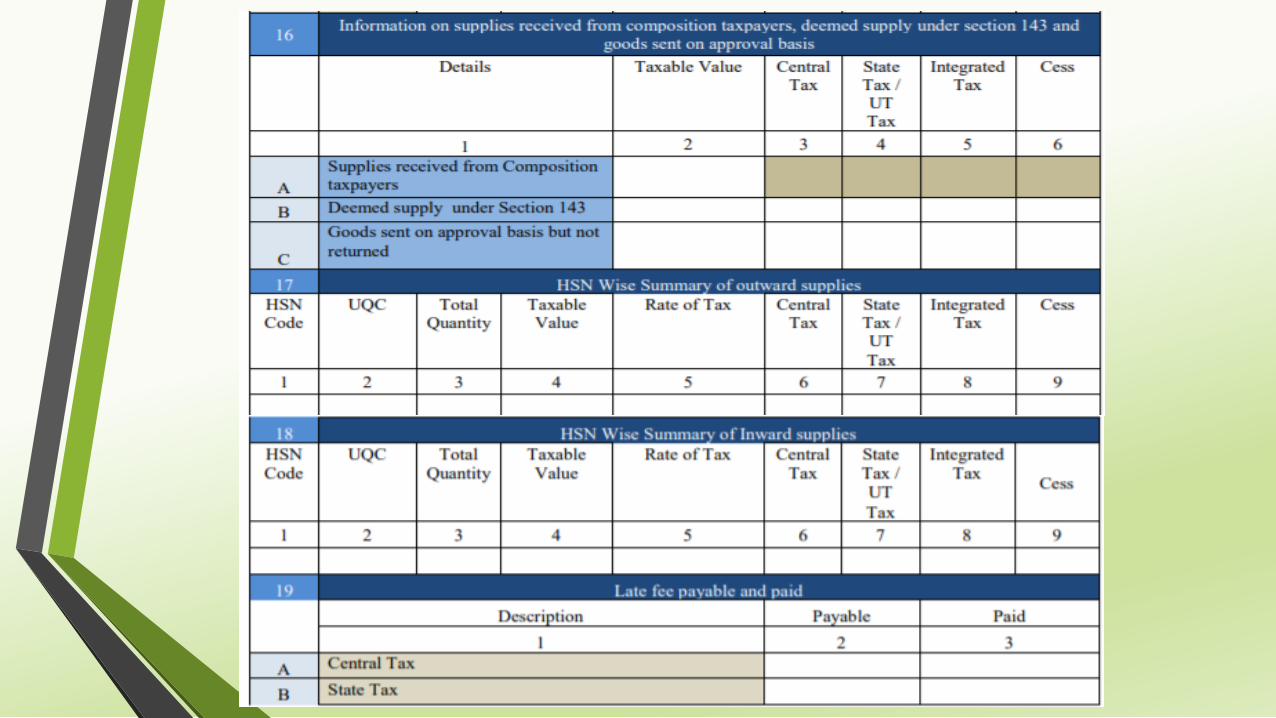

Part-VI Table-16 Supply received from Composition dealersDeemed Supply under Section 143Goods Send on approval but not returned

Part-VI Table-17 HSN Wise Summary of Outward SupplyPart-VI Table-18 HSN Wise Summary of Inward SupplyPart-VI Table-19 Late Fees Payable & Paid

GSTR-9 FORMAT

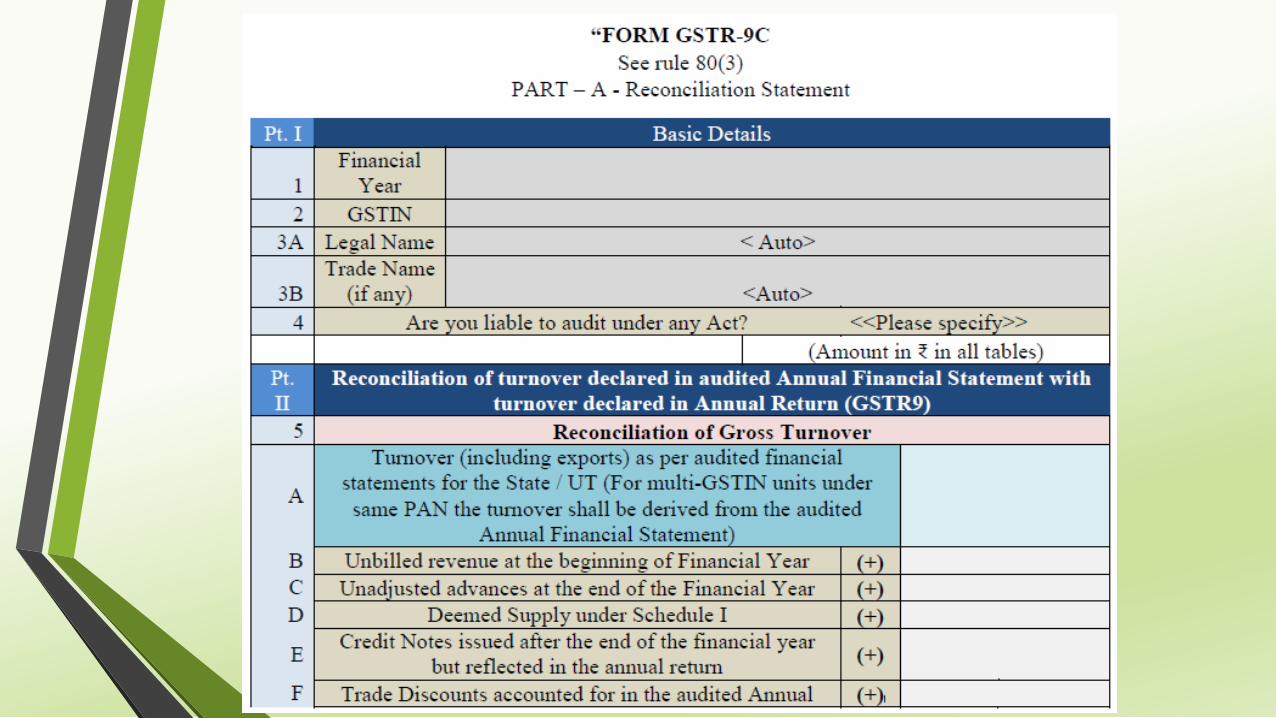

GST ANNUAL RETURN:FORM GSTR-9C

• Form GSTR-9C is the GST Reconciliation Statement for a particularFY to be filed by taxpayers after being certified by CharteredAccountant(s).

• It must be filed along with the GSTR-9 (Annual Return) and theAudited Financial Statements on the GST Portal directly or be filedthrough the facilitation centre

• This statement is applicable to all those taxpayers who must gettheir Annual Accounts audited under the GST law

• Audit applies to those registered persons whose annual aggregateturnover exceeds Rs 2 crores in a financial year

• The format of GSTR-9C was notified vide Notification No. 49/2018-Central Tax dated 13th September 2018

GST ANNUAL RETURN:FORM GSTR-9C: IMPORTANT POINTS• A person required to file Form GSTR-9C shall also file Annual Return

along with the Reconciliation Statement and copy of auditedfinancial statements.

• For the purpose of GSTR 9C,as per Section 2(6), aggregate turnovermeans the aggregate value of all taxable supplies, exempt supplies,export of goods and services and interstate supplies of personshaving the same PAN, to be computed on all India basis but excludesCGST, SGST/UTGST, IGST and Cess and Inward supply on which tax ispaid on Reverse Charge Basis.

• As per Auditor’s Recommendation, taxpayer shall have to pay anyshort tax liability in case of excess refund/ credit taken and vice-versa.

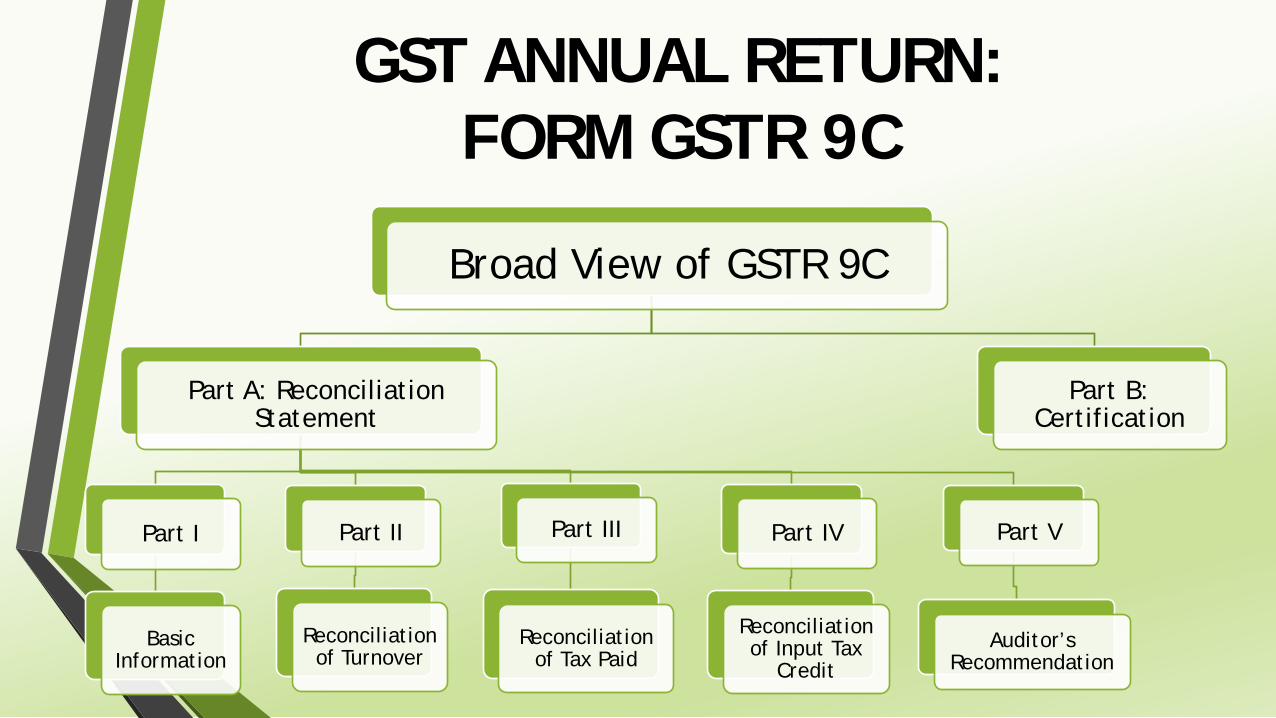

GST ANNUAL RETURN:FORM GSTR 9C

Broad View of GSTR 9C

Part A: Reconciliation Statement

Part I

Basic Information

Part II

Reconciliation of Turnover

Part III

Reconciliation of Tax Paid

Part IV

Reconciliation of Input Tax

Credit

Part V

Auditor’s Recommendation

Part B: Certification

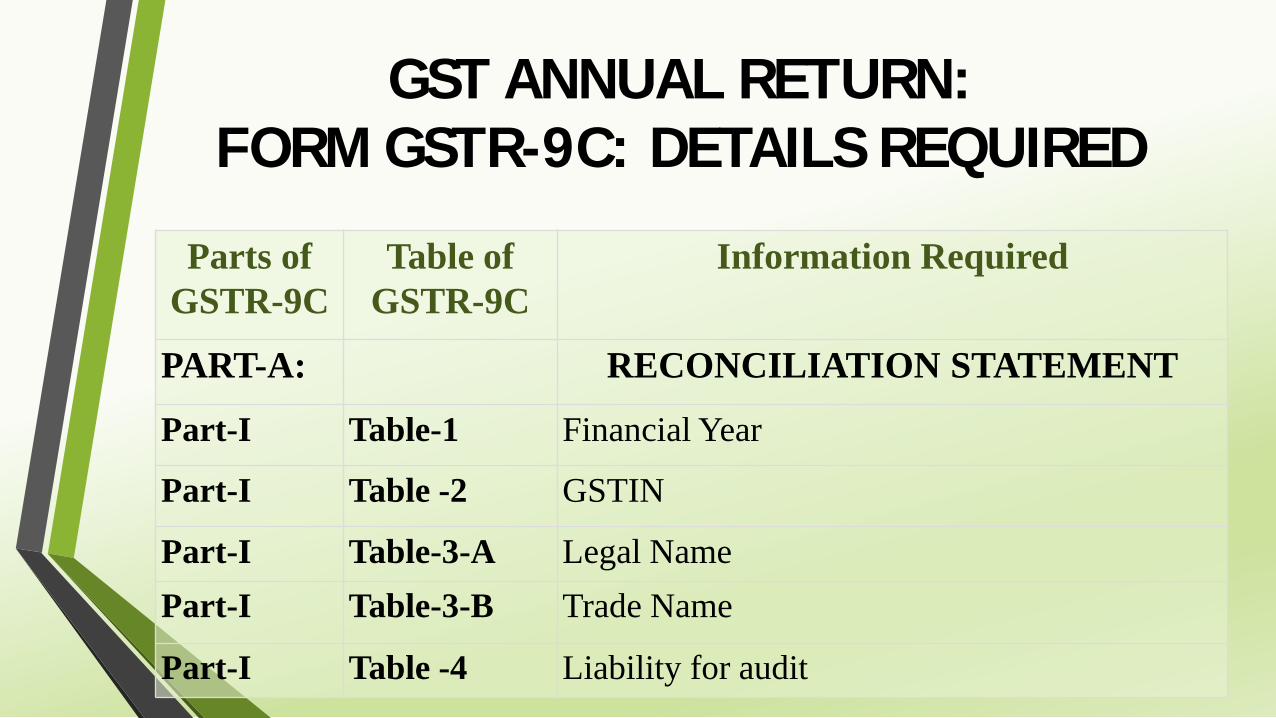

GST ANNUAL RETURN:FORM GSTR-9C: DETAILS REQUIRED

Parts of GSTR-9C

Table of GSTR-9C

Information Required

PART-A: RECONCILIATION STATEMENT

Part-I Table-1 Financial Year

Part-I Table -2 GSTIN

Part-I Table-3-A Legal NamePart-I Table-3-B Trade Name

Part-I Table -4 Liability for audit

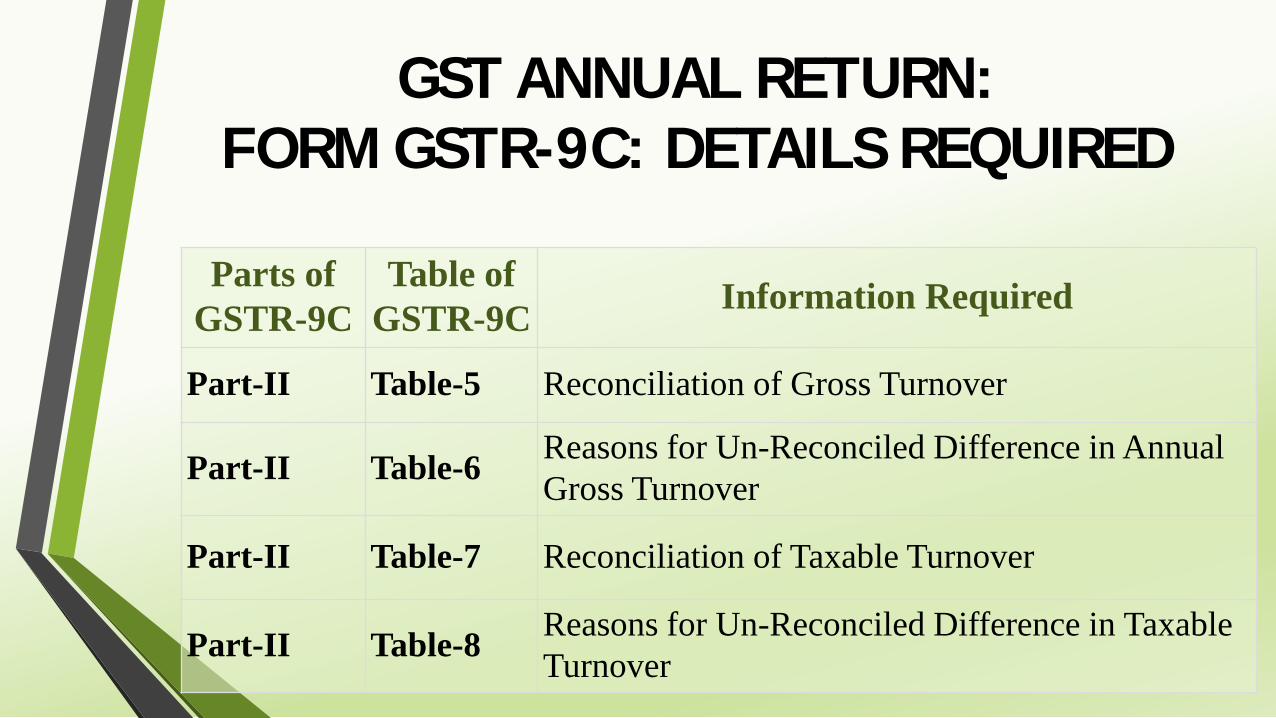

Parts of GSTR-9C

Table of GSTR-9C Information Required

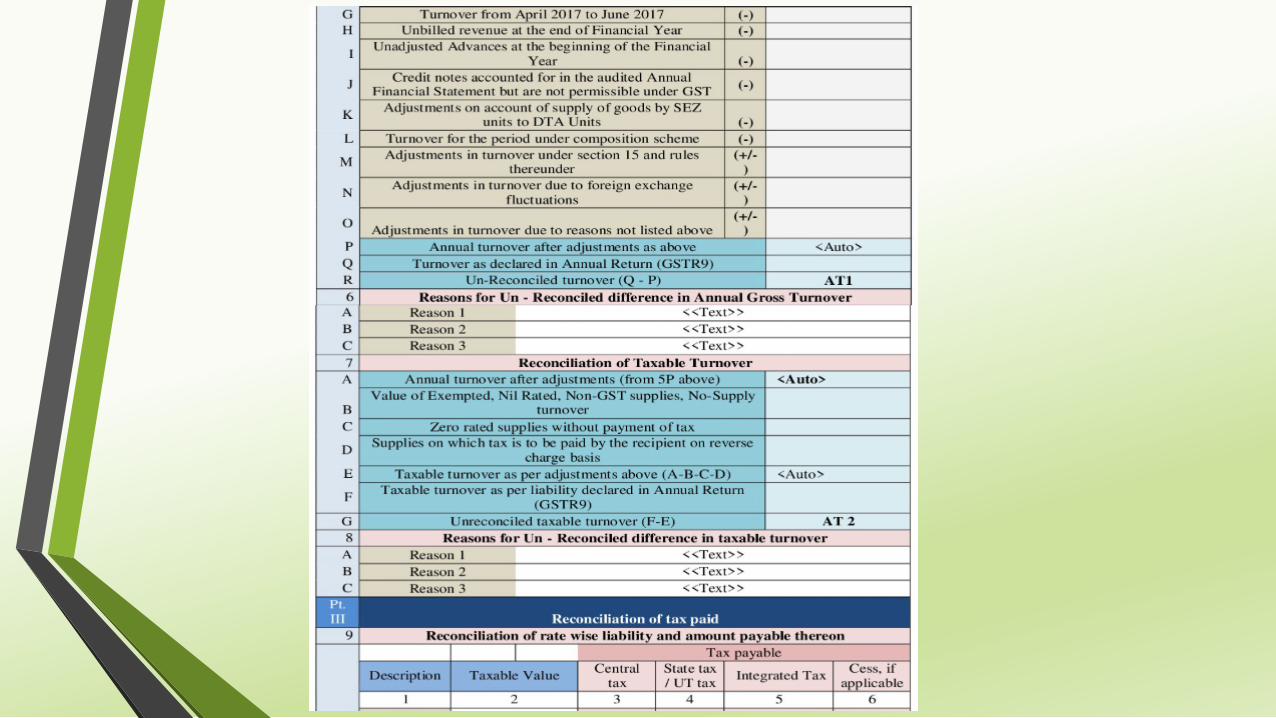

Part-II Table-5 Reconciliation of Gross Turnover

Part-II Table-6 Reasons for Un-Reconciled Difference in Annual Gross Turnover

Part-II Table-7 Reconciliation of Taxable Turnover

Part-II Table-8 Reasons for Un-Reconciled Difference in Taxable Turnover

GST ANNUAL RETURN:FORM GSTR-9C: DETAILS REQUIRED

GST ANNUAL RETURN:FORM GSTR-9C: DETAILS REQUIRED

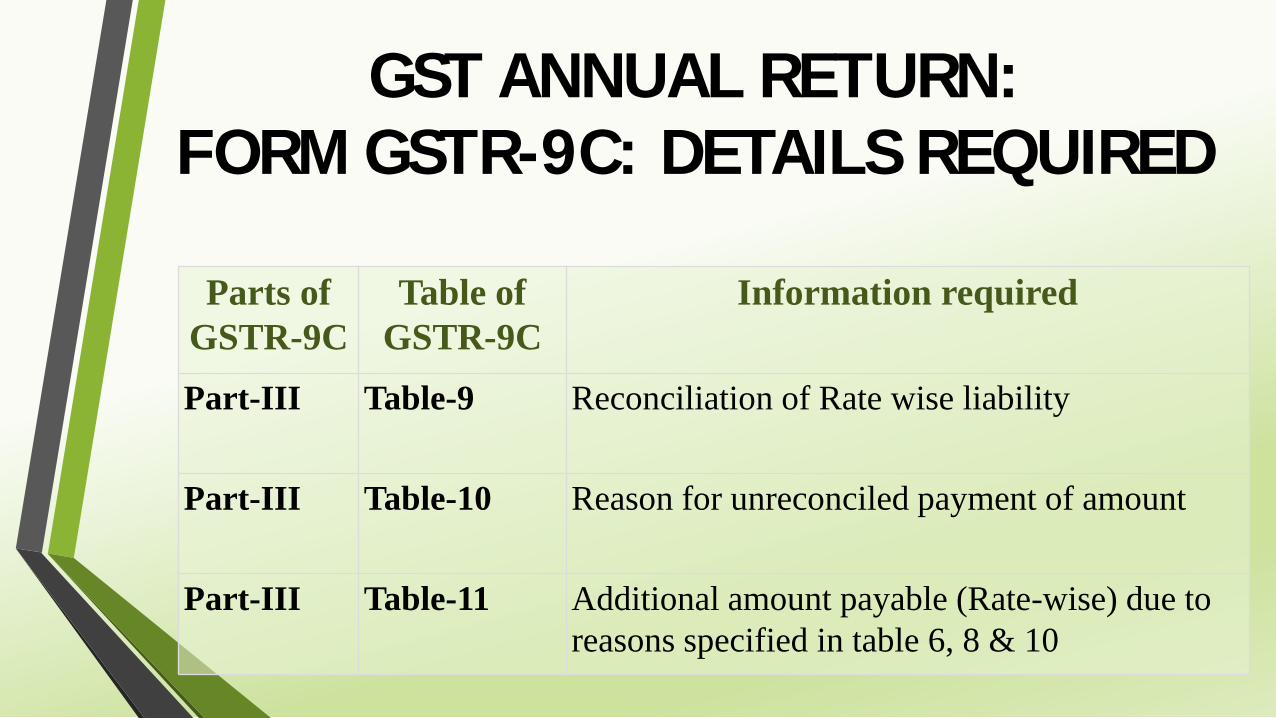

Parts of GSTR-9C

Table of GSTR-9C

Information required

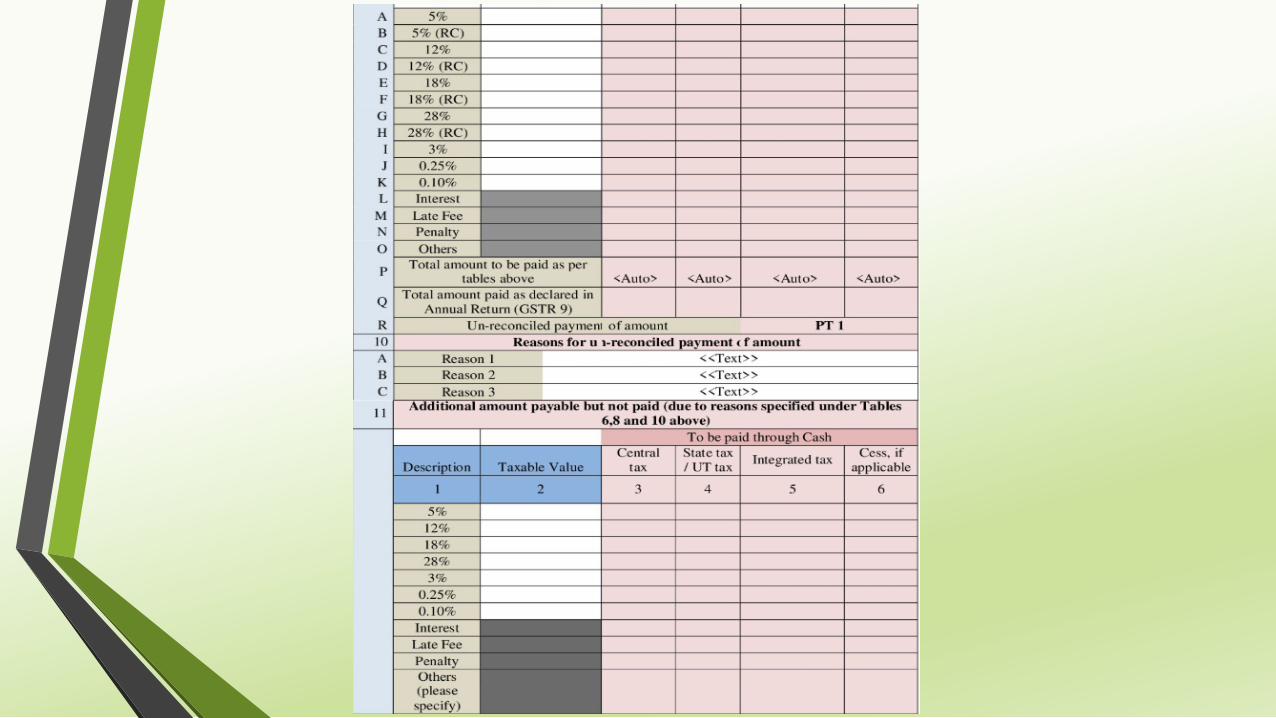

Part-III Table-9 Reconciliation of Rate wise liability

Part-III Table-10 Reason for unreconciled payment of amount

Part-III Table-11 Additional amount payable (Rate-wise) due to reasons specified in table 6, 8 & 10

GST ANNUAL RETURN:FORM GSTR-9C: DETAILS REQUIRED

Parts of GSTR-9C

Table of GSTR-9C

Information required

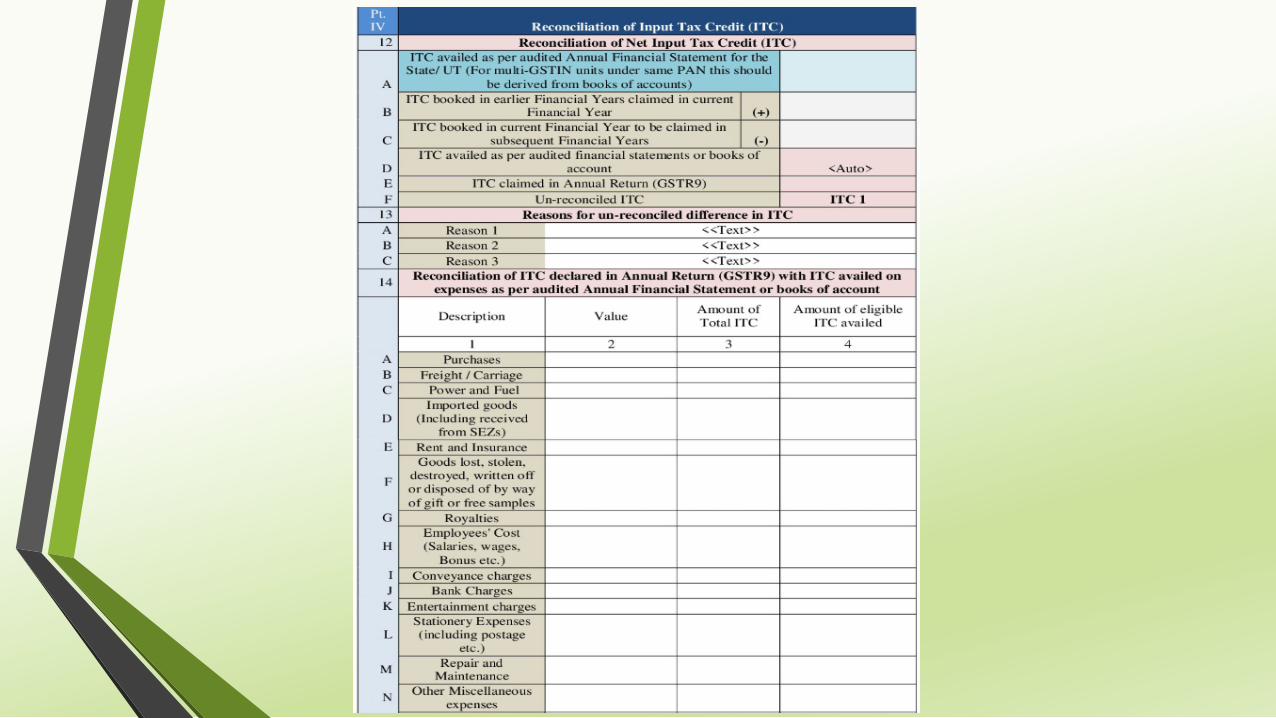

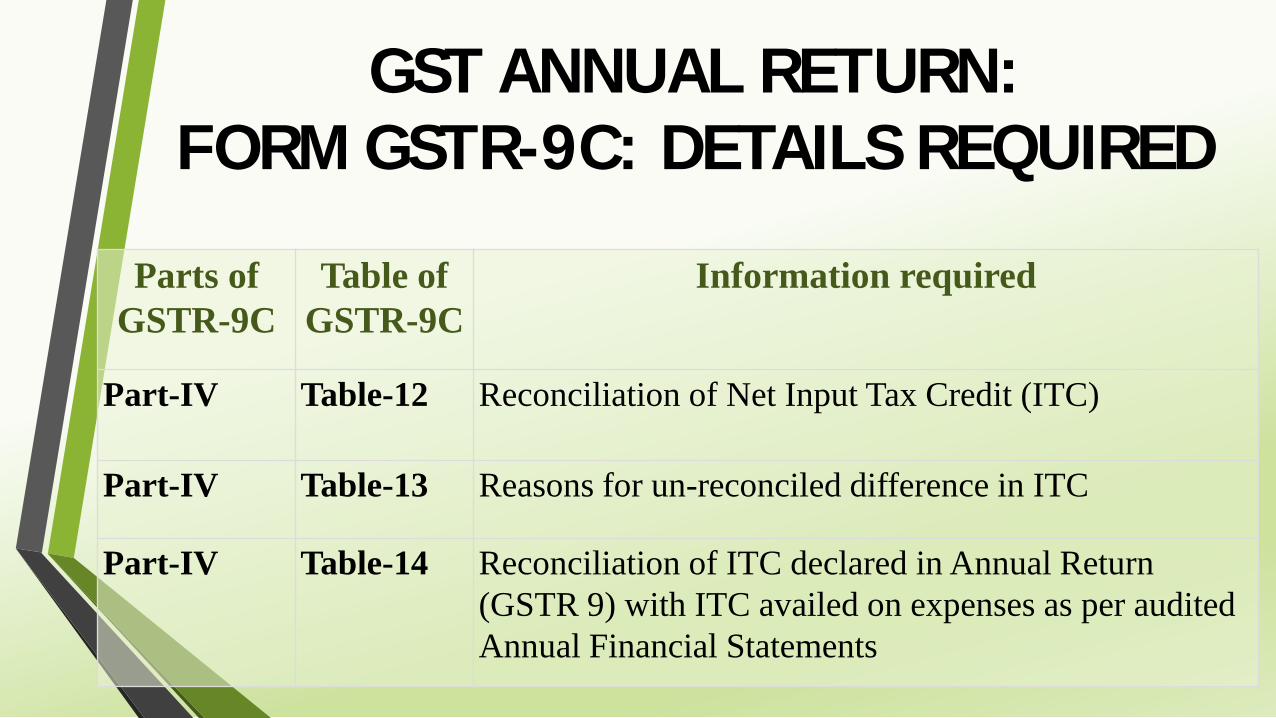

Part-IV Table-12 Reconciliation of Net Input Tax Credit (ITC)

Part-IV Table-13 Reasons for un-reconciled difference in ITC

Part-IV Table-14 Reconciliation of ITC declared in Annual Return (GSTR 9) with ITC availed on expenses as per audited Annual Financial Statements

GST ANNUAL RETURN:FORM GSTR-9C: DETAILS REQUIRED

Parts of GSTR-9C

Table of GSTR-9C Information required

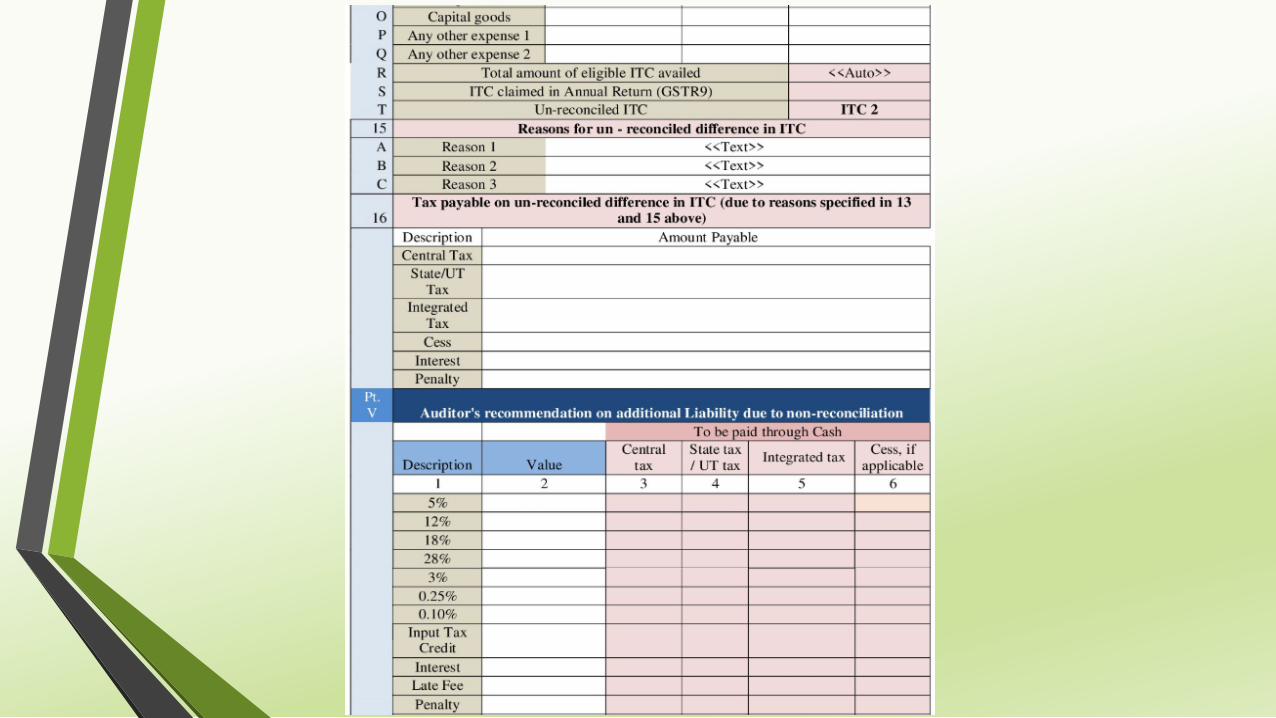

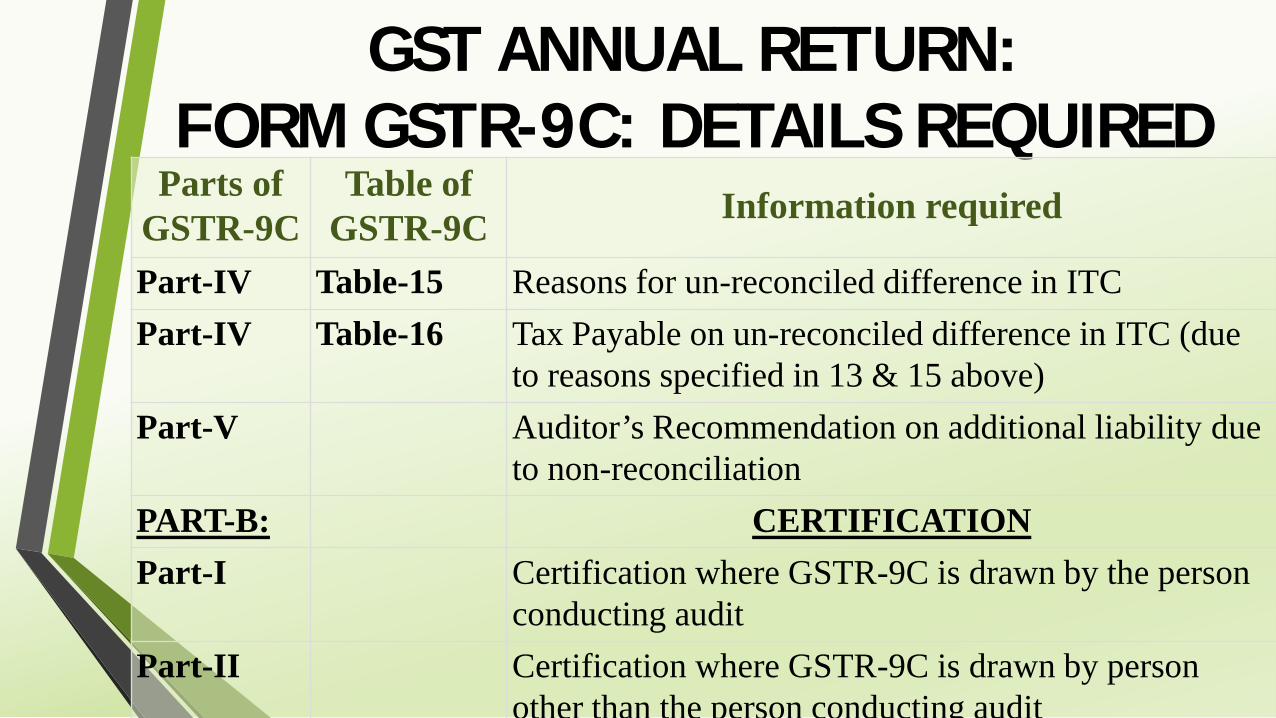

Part-IV Table-15 Reasons for un-reconciled difference in ITCPart-IV Table-16 Tax Payable on un-reconciled difference in ITC (due

to reasons specified in 13 & 15 above)Part-V Auditor’s Recommendation on additional liability due

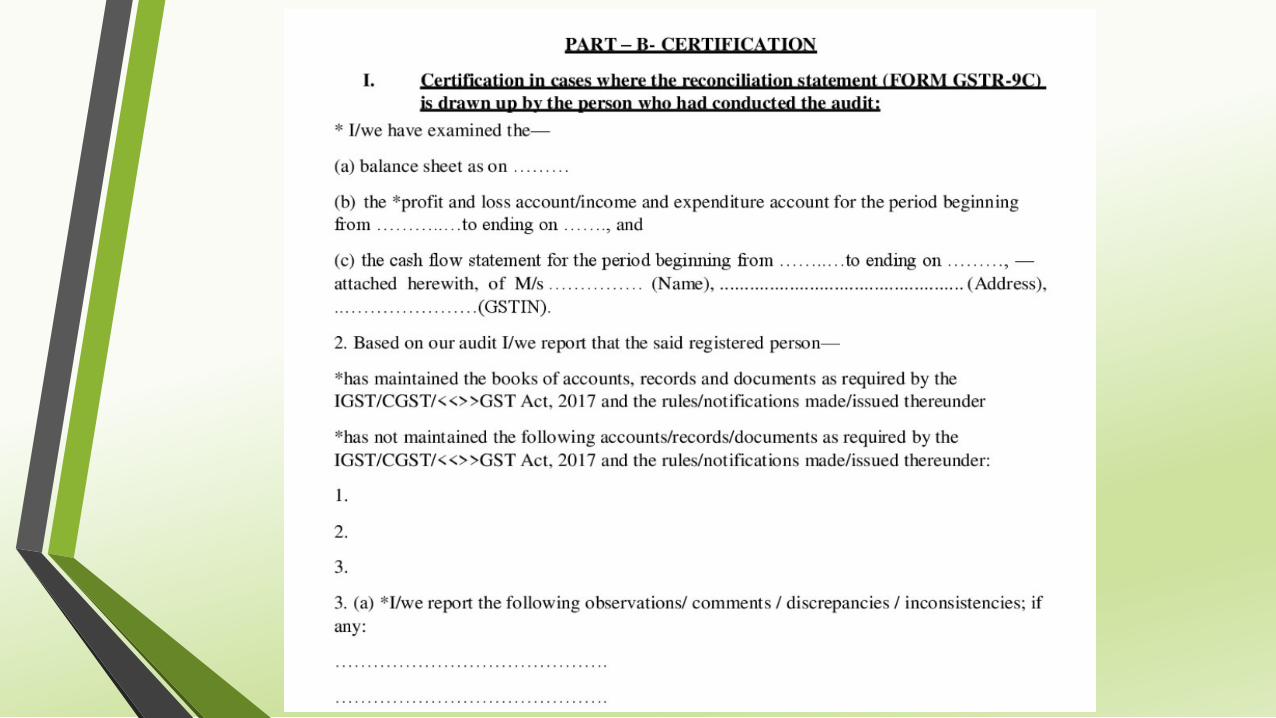

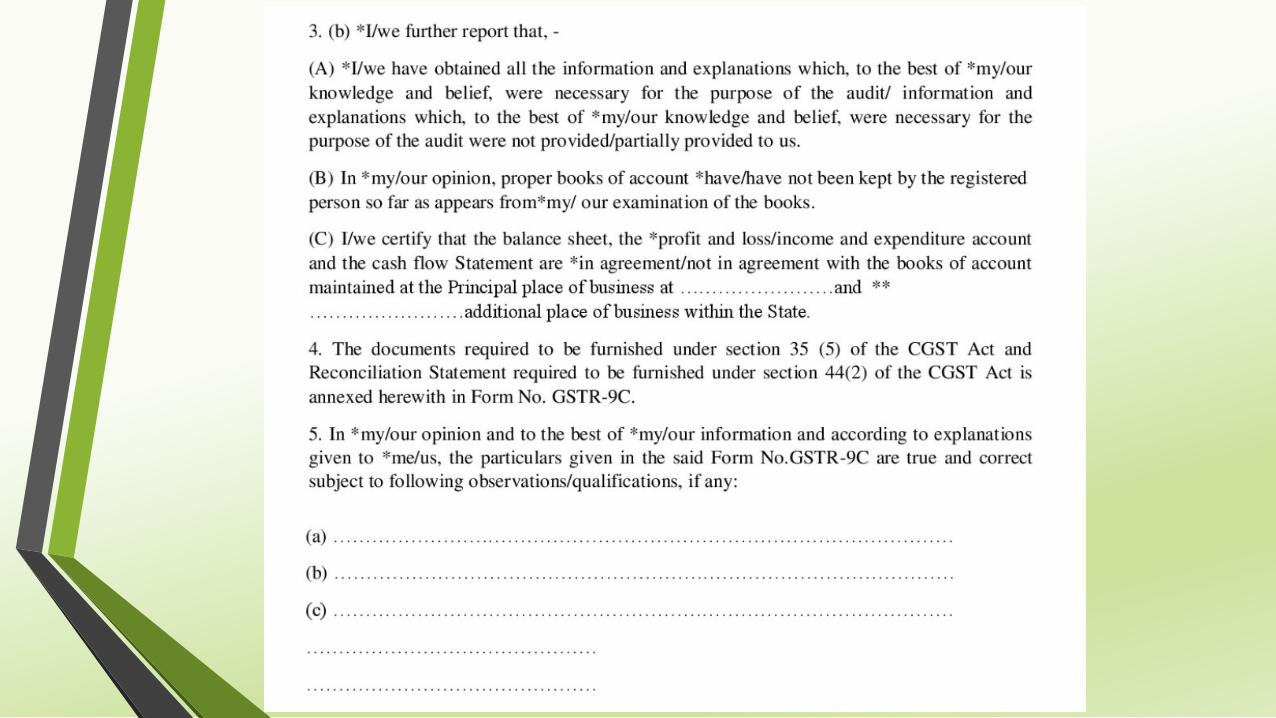

to non-reconciliationPART-B: CERTIFICATIONPart-I Certification where GSTR-9C is drawn by the person

conducting auditPart-II Certification where GSTR-9C is drawn by person

other than the person conducting audit

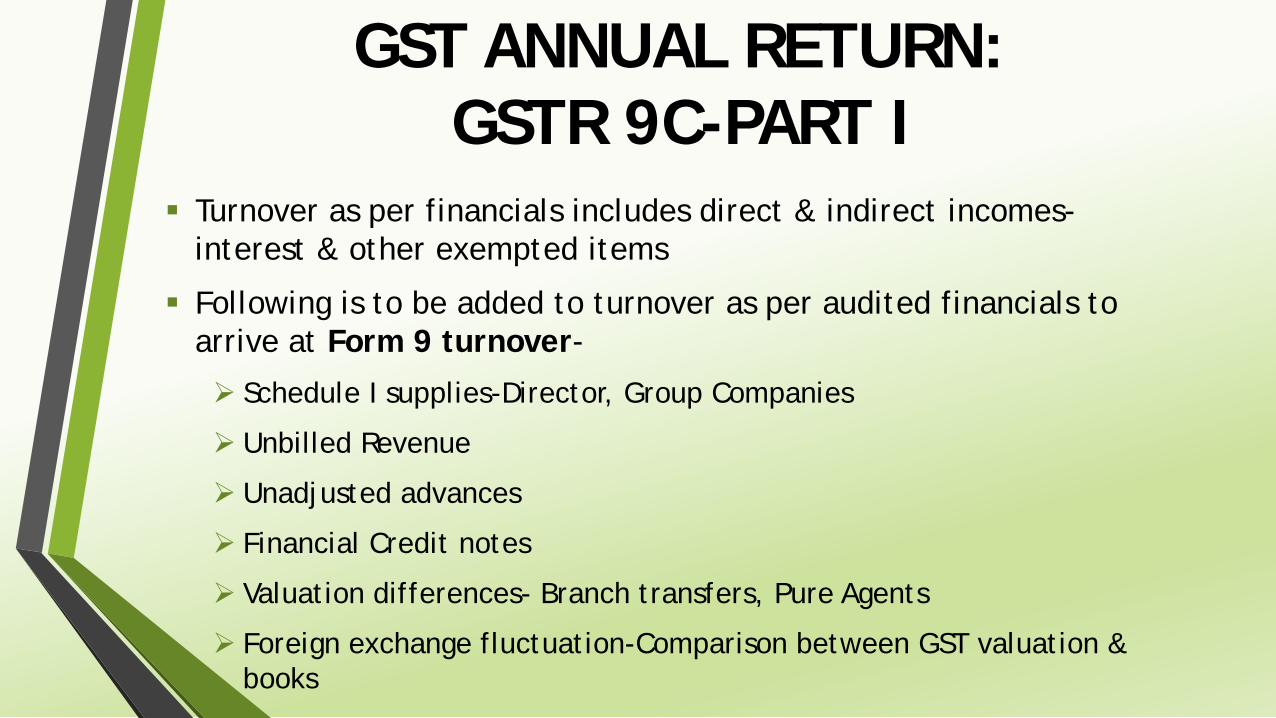

GST ANNUAL RETURN:GSTR 9C-PART I

Turnover as per financials includes direct & indirect incomes-interest & other exempted items

Following is to be added to turnover as per audited financials to arrive at Form 9 turnover-

Schedule I supplies-Director, Group Companies

Unbilled Revenue

Unadjusted advances

Financial Credit notes

Valuation differences- Branch transfers, Pure Agents

Foreign exchange fluctuation-Comparison between GST valuation & books

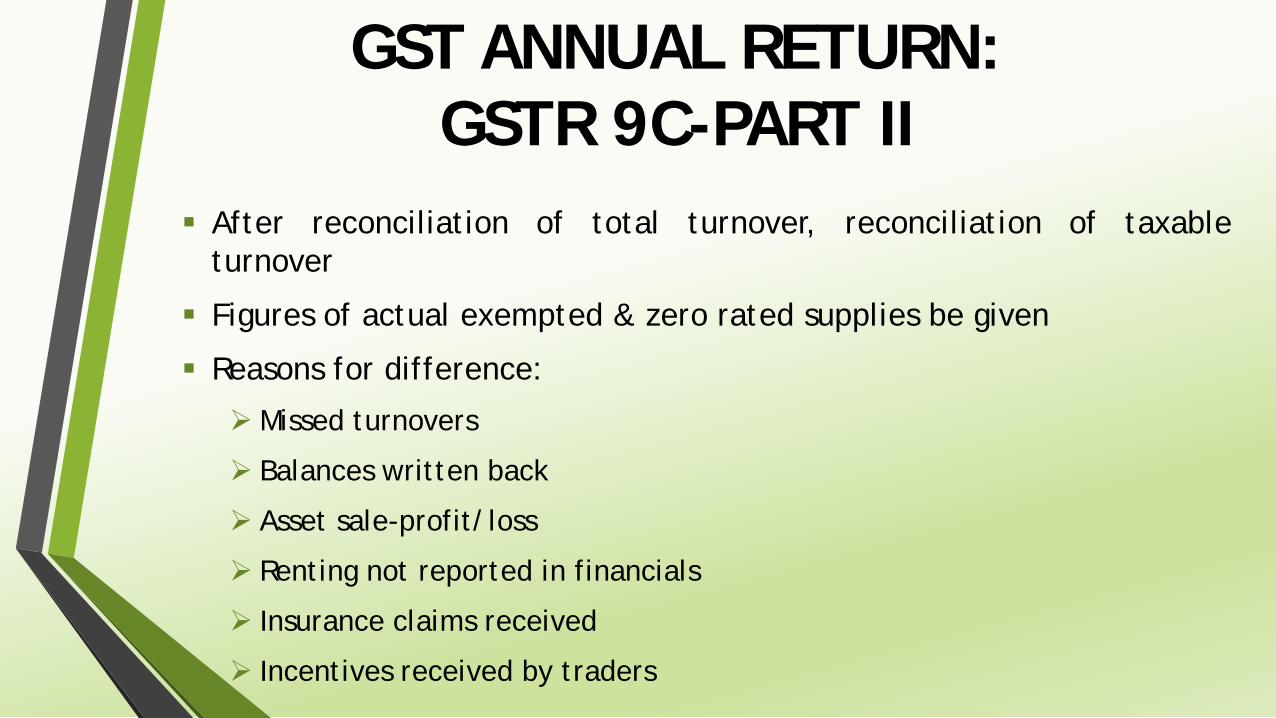

GST ANNUAL RETURN:GSTR 9C-PART II

After reconciliation of total turnover, reconciliation of taxableturnover

Figures of actual exempted & zero rated supplies be given

Reasons for difference:

Missed turnovers

Balances written back

Asset sale-profit/loss

Renting not reported in financials

Insurance claims received

Incentives received by traders

GST ANNUAL RETURN:GSTR 9C-PART III

Reconciliation of taxes paid- Payable vs paid

Additional tax payable- because of difference intotal/taxable turnover or tax payable

GST ANNUAL RETURN:GSTR 9C-PART IV

Reason for unreconciled ITC: ITC booked in current year but availed in returns of

subsequent year

Booked in books but not availed

Debited in financials as expense

GST ANNUAL RETURN:GSTR 9C-PART V

Auditor’s recommendation should be summarization & quantification oftax arising out of-

Non-reconciliation of turnover;

Non-reconciliation of ITC;

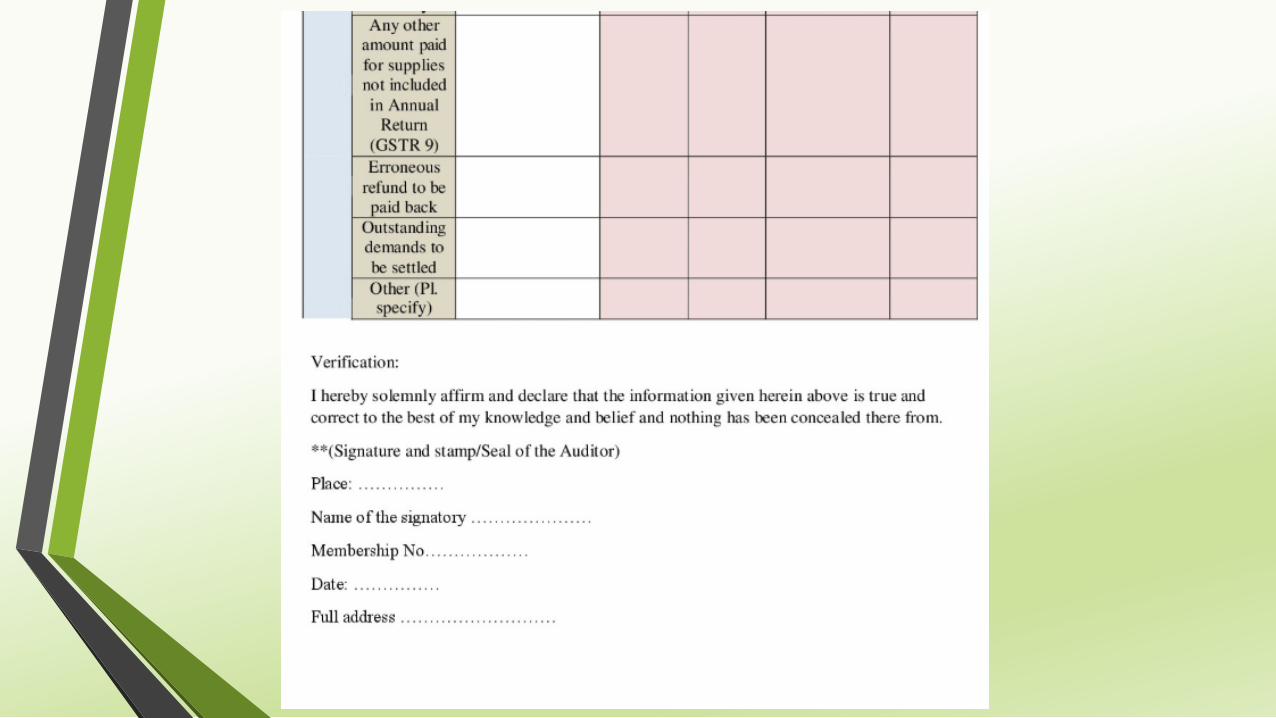

Any other amount to be paid for supplies not included in the Annualreturn

Any refund which has been erroneously taken & shall be paid back tothe Government

Any other outstanding demands which is recommended to be settledby the auditor