Embed Size (px)

Citation preview

All rights reserved – 2012

Grupo Fleury announces the acquisition of Grupo Papaiz, entering the dental diagnostics market

September 28th, 2012

2

Disclaimer

This presentation may contain forward-looking statements. Such statements are not statements of historical facts and reflect the beliefs and expectations of the Company’s management. The words “anticipates”, “believes”, “estimates”, “expects”, “forecasts”, “plans”, “predicts”, “project”, “targets” and similar words are intended to identify these statements, which necessarily involve known and unknown risks and uncertainties. Known risks and uncertainties include but are not limited to the impact of competitive services and pricing market acceptance of services, service transactions by the Company and its competitors, regulatory approval, currency fluctuations, changes in service mix offered, and other risks described in the Company´s registration statement. Forward-looking statements speak only as of the date they are made and the Fleury Group does not undertake any obligation to

update them in light of new information or future developments.

Overview

Grupo Fleury announces the acquisition of Grupo Papaiz, a company with more than 30 years of tradition with leadership position in the São Paulo’s market of dental diagnostics.

The acquisition objective is to explore business opportunities in the dental diagnostics market, a still under penetrated market, with highly fragmented competition and high growth potential.

Grupo Papaiz offers dental diagnostics services through eight patient service centers (PSCs) located in São Paulo. In the last twelve months (LTM) ended in June, 2012, Net Revenues reached R$ 13.4 million and EBITDA amounted R$ 3.7 million (27,6% margin).

The negotiated enterprise value is R$ 18.4 million (5.0x EBITDA jun12 LTM). Net debt was estimated at R$ 260 thousand and will be deducted from the enterprise value. There will be retention of R$ 2.7 million as risks and contingencies.

Grupo Fleury will hold 51% of the Grupo Papaiz and will lead the business. Odontoprev will control the company that will hold the remaining 49%.

All the nine current shareholders are dentists and will continue to develop their current functions after the transaction conclusion. Three of them will remain with management activities.

The acquisition’s conclusion is conditioned to CADEs (Brazilian anti-trust entity) approval

3

Payers mix

About Grupo Papaiz

Grupo Papaiz operates through eight pacient service centers (PSCs) located at the city of São Paulo, that offers dental diagnostics services, such as tomography, intra and extraoral radiographs, ortodontic documentation, and dental arcade models.

Between 2006 and 2011, Papaiz Group achieved a 20% CAGR in Gross Revenue.

PSCs location

4

1

2

3

4

5

6 7

8

Jardins Santana Vila Mariana

Tatuapé Santo Amaro Lapa

São Miguel Av. Brasil

1

2

3

4

5

6

7

8

¹ Individuals: clients that pay for the service without intermediation of a DCO

² DCO: dental care organization’s

In the last twelve months ended in June of 2012, the company reached net revenues of R$ 13.4 millions and

R$ 3.7 millions EBITDA (27.6% margin).

Individuals¹ (out of pocket)

80%

DCOs²20%

Services offered by Grupo Papaiz

Sample of Pacient Service Centers (PSCs)

Services offered and sample of patient service centers (PSCs)

Imaging diagnostic method that allows the reproduction of the maxillomandibular complex in three-dimensional shapes

Tomography (dental)

Intraoral radiographs Radiographs performed with the film inside the patient's mouth

Extraoral radiographs Radiographs performed with the film outside the patient's mouth

Ortodontic documentation Grouping of different procedures results in a single condensed report (usually composed by dental arcade model, extraoral radiographs, photos and cephalometric tracing)

Dental arcade models Reproductions of dental arcade

5

Vila Mariana Av. Brasil Jardins São Miguel

Expected benefits

This acquisition expands Grupo Fleury’s role in the Brazilian healthcare value chain and presents successful opportunities in face of the still undeveloped potential of this market.

Addition of important intangible assets, including the employees, dental surgeons and qualified managers of Grupo Papaiz, which are recognized in the dental diagnostics market.

Reinforcement of Grupo Fleury's drivers to offer services based on differentiation and markets with growth potential.

Diversification of revenue sources. Only 20% of Grupo Papaiz gross revenue comes from DCOs.

Synergies in management and technology, and contribution to the further development of Grupo Papaiz on items related to excellence in service processes and customer intimacy.

Odontoprev: strategic partner.

6 ¹ DCO: dental care organization

The Brazilian private dental market benefits from favorable economic and sociodemographic factors. Among them,

the increasing income of the Brazilian population and formal job creation.

The dental plans segment achieved higher growth rates compared to medical-hospital plans. The penetration rate

¹ of exclusively dental plans is well below the penetration rate of medical-hospital plans (9% vs. 24% respectively in

December 2011).

With about 240 thousand professionals, Brazil presents the highest dentists concentration of the world.

Private dental market in Brazil

¹ Penetration: ratio, expressed as a percentage, between the number of beneficiaries and the total population in a specific area 7

Formal jobs creation (millions) Source: Ministério do Trabalho e Emprego / CAGED

Middle class (“classe C”) participation on total brazilian population Source : Fundação Getúlio Vargas (FGV)

48% 50% 52% 53% 54% 55%

60%

2006 2007 2008 2009 2010 2011 2014 E

Dental plan beneficiaries (millions) Source: ANS

Penetration¹ of medical-hospital and dental plans Source: ANS / IBGE

1.51.9

1.71.4

2.6

2.0

1.5

1.0

2006 2007 2008 2009 2010 2011 1S11 1S12

3.9% 4.7% 5.5% 6.7% 7.6% 8.7%

20.0% 20.7% 21.5% 22.1%23.8% 24.6%

Dec/06 Dec/07 Dec/08 Dec/09 Dec/10 Dec/11

Dental medical-hospital

7.38.8

10.412.7

14.716.8 16.2

17.6

2006 2007 2008 2009 2010 2011 2Q11 2Q12

Total population per metropolitan region (millions) Source : CENSO 2010 - IBGE

The São Paulo metropolitan region

concentrates the biggest population in

Brazil, also presenting the highest quantity

of private dental plans

The growth of dental plans in the last five

years was higher in São Paulo than

anywhere else in Brazil.

8

Quantity of Dental plans beneficiaries per metropolitan regions – March/12 (thousands) Source: ANS

Private dental market in São Paulo

4,274

1,910

830 767 743 631 505 531

SP RJ BSB SALV BH CUR CAMP FORT

19,7

11,8

5,44,0 3,7 3,7 3,6 3,6

SP RJ BH P.ALEG DF REC FORT SALV

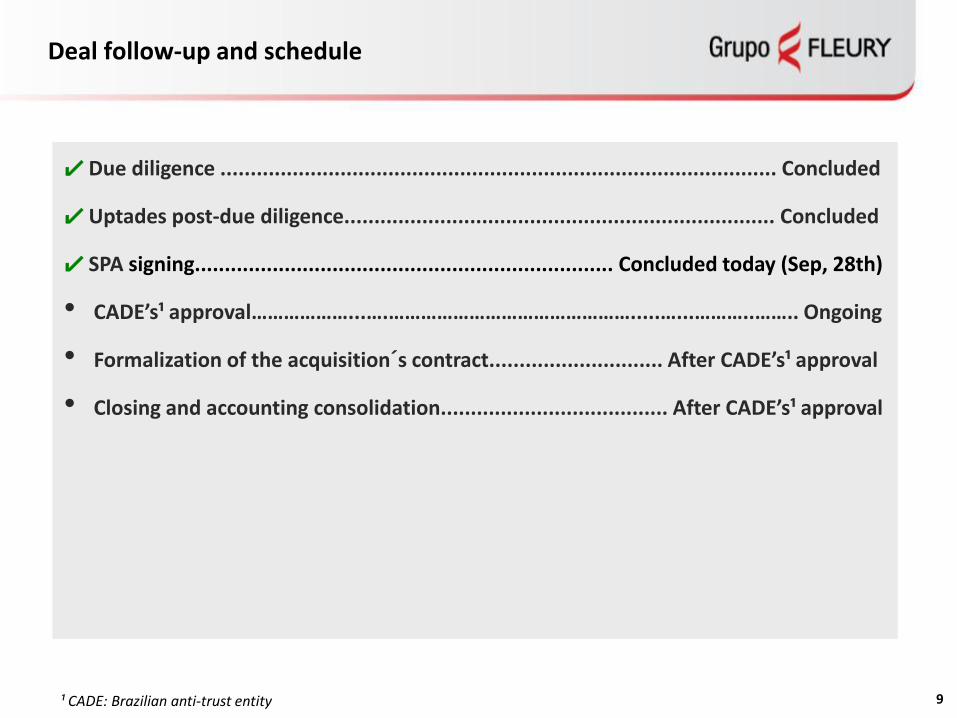

Deal follow-up and schedule

9

! Due diligence ............................................................................................. Concluded

! Uptades post-due diligence........................................................................ Concluded

! SPA signing...................................................................... Concluded today (Sep, 28th)

• CADE’s¹ approval………………...….……………………………………….....…...………..…….. Ongoing

• Formalization of the acquisition´s contract............................. After CADE’s¹ approval

• Closing and accounting consolidation...................................... After CADE’s¹ approval

¹ CADE: Brazilian anti-trust entity

27 acquisitions since 2002: Enhancing services diversification, geographical presence and knowledge base

Timeline of Acquisitions

10

2002 2004 2005 2007 2008

Paraná

Rio de Janeiro São Paulo Bahia

São Paulo Paraná Pernambuco Bahia Rio de Janeiro

São Paulo

2009

Rio de Janeiro

Rio Grande do Sul

2010

São Paulo

Rio de Janeiro

2011

Bahia

2012

São Paulo

![Lysias Fleury et al. v. Haiti - Loyola Law School · 2019. 12. 18. · 2014] Lysias Fleury et al. v. Haiti 1097 officers repeatedly kick and beat Mr. Fleury outside of his cell.24](https://img.pdfslide.us/doc/110x75/5fefaa41485eaa784f2b77e9/lysias-fleury-et-al-v-haiti-loyola-law-school-2019-12-18-2014-lysias-fleury.jpg)