Embed Size (px)

Citation preview

1

G R O W I N G W I T H E F F E C T I V E D I S T R I B U T I O N E X PA N S I O N

BY NIELSEN SALESFORCE ACTIVATION TEAM - Nov 2016

BY TARGETING TOP 20 PROVINCES

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

2

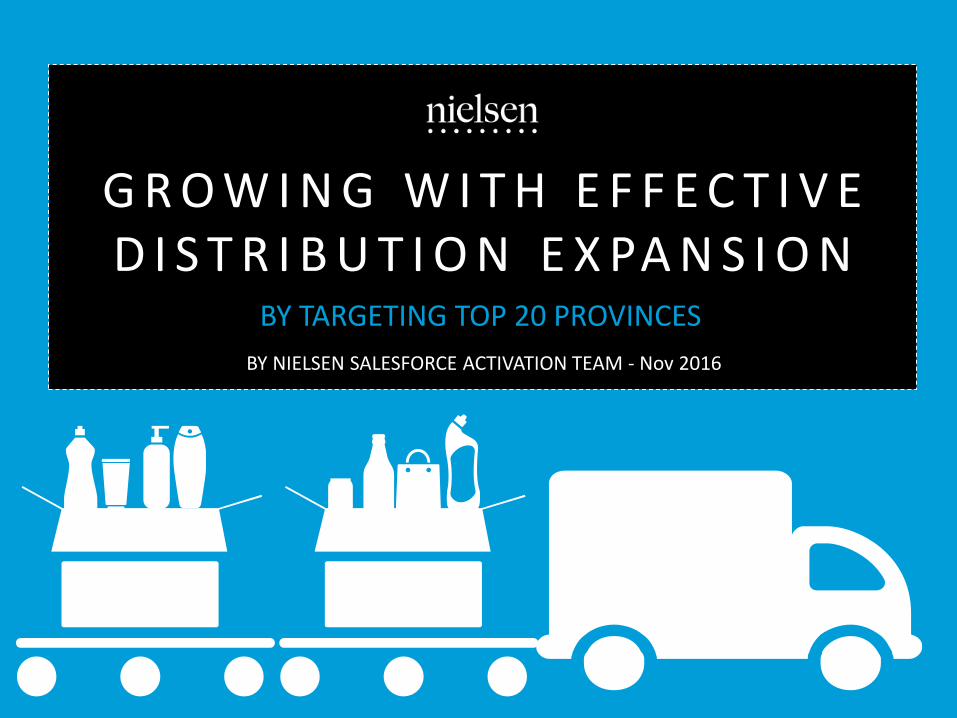

Traditional trade is potential

87%

Traditional Trade Value SOT

Avg. Customer/Day Avg. Trip/Week Per Person

33 4.1X

1.4M

FMCG Outlets

THE OPPORTUNITIES

Source: Nielsen RES 2014/ Shopper Trend 2014

450K TT stores

Accounts for

40% FMCG sales

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

3

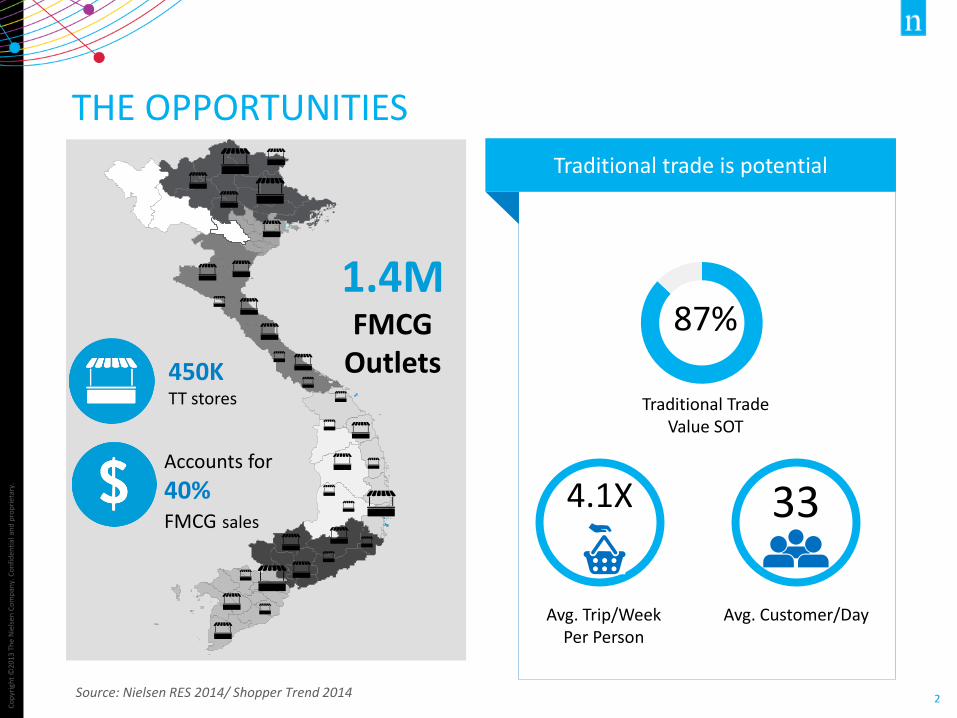

THE CHALLENGES

LIMITED CATEGORIES

LIMITED SPACE

F&B DOMINATE SPACE

Traditional outlets that have

account

50% of traditional

grocery universe.

40% 20%

>70% grocery outlets have selling area

LESS THAN

20m2

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

4

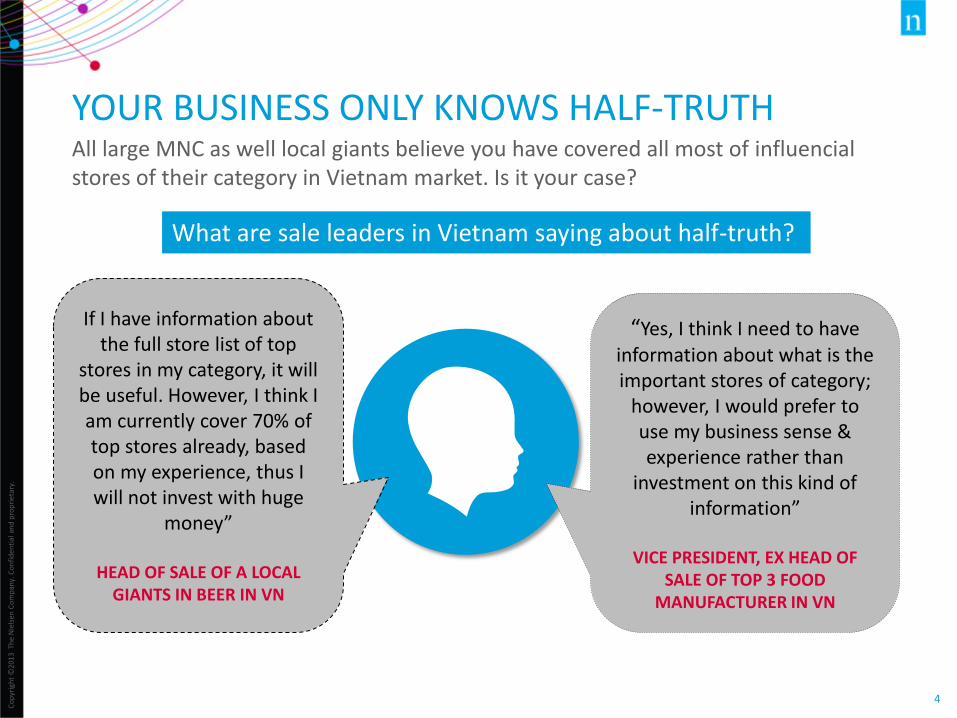

YOUR BUSINESS ONLY KNOWS HALF-TRUTH All large MNC as well local giants believe you have covered all most of influencial stores of their category in Vietnam market. Is it your case?

What are sale leaders in Vietnam saying about half-truth?

If I have information about the full store list of top

stores in my category, it will be useful. However, I think I am currently cover 70% of top stores already, based on my experience, thus I will not invest with huge

money”

HEAD OF SALE OF A LOCAL GIANTS IN BEER IN VN

“Yes, I think I need to have information about what is the important stores of category;

however, I would prefer to use my business sense & experience rather than

investment on this kind of information”

VICE PRESIDENT, EX HEAD OF

SALE OF TOP 3 FOOD MANUFACTURER IN VN

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

5

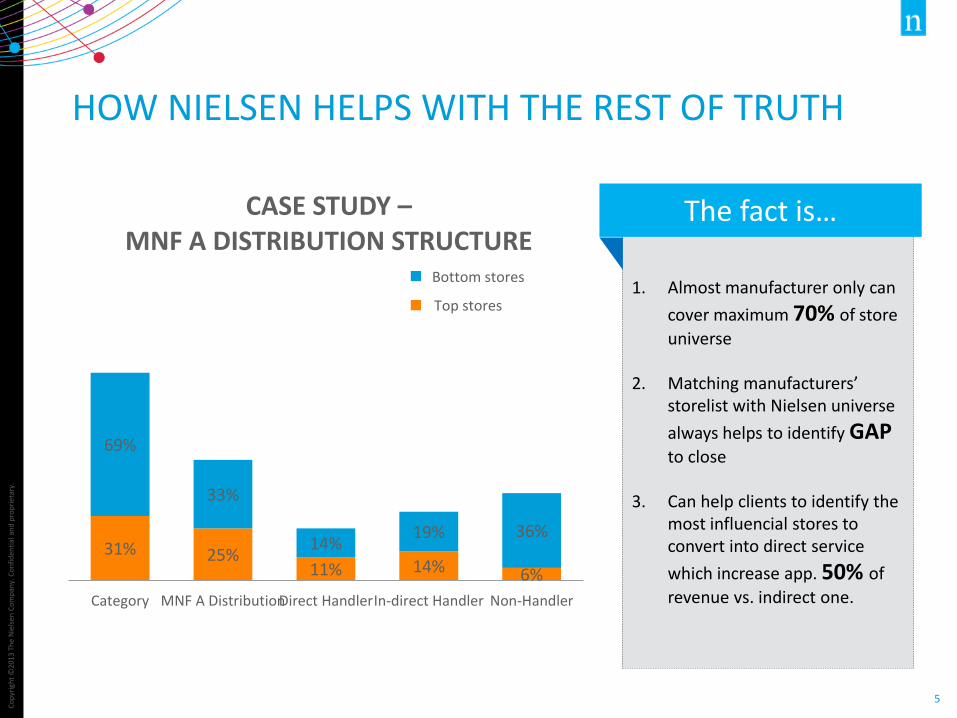

HOW NIELSEN HELPS WITH THE REST OF TRUTH

31% 25% 11% 14% 6%

69%

33%

14% 19% 36%

Category MNF A DistributionDirect HandlerIn-direct Handler Non-Handler

CASE STUDY – MNF A DISTRIBUTION STRUCTURE

Series2

Series1Top stores

Bottom stores 1. Almost manufacturer only can

cover maximum 70% of store

universe

2. Matching manufacturers’ storelist with Nielsen universe

always helps to identify GAP

to close

3. Can help clients to identify the most influencial stores to convert into direct service

which increase app. 50% of

revenue vs. indirect one.

The fact is…

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

6

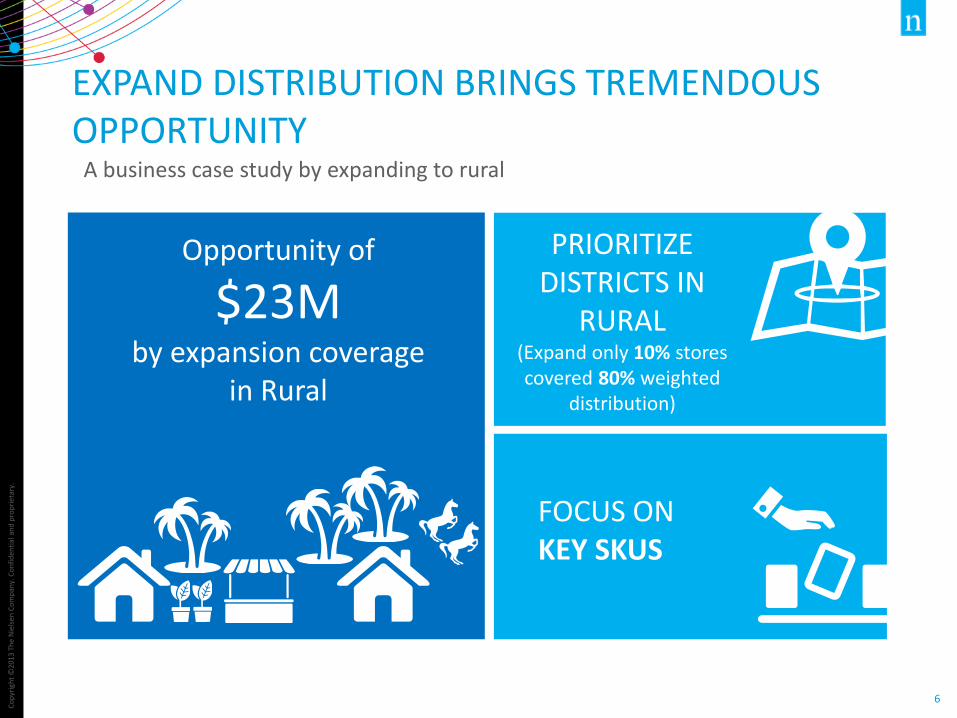

EXPAND DISTRIBUTION BRINGS TREMENDOUS OPPORTUNITY

A business case study by expanding to rural

Opportunity of

$23M by expansion coverage

in Rural

FOCUS ON KEY SKUS

PRIORITIZE DISTRICTS IN

RURAL (Expand only 10% stores covered 80% weighted

distribution)

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

8

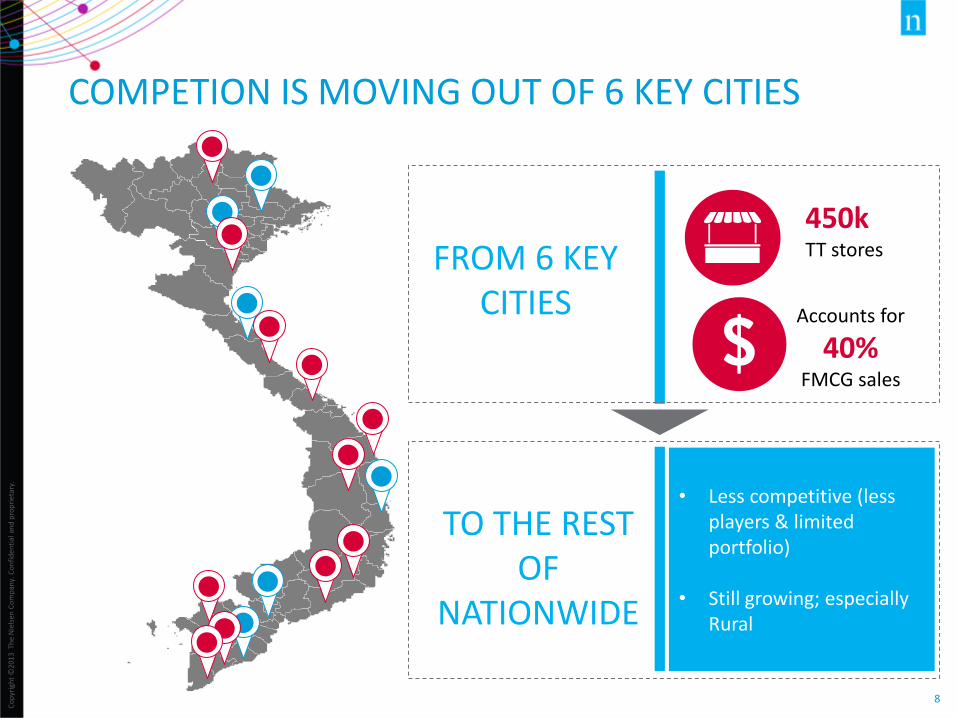

COMPETION IS MOVING OUT OF 6 KEY CITIES

FROM 6 KEY CITIES

TO THE REST OF

NATIONWIDE

450k TT stores

Accounts for

40% FMCG sales

• Less competitive (less players & limited portfolio)

• Still growing; especially Rural

9

BUT HOW TO EXPAND

DISTRIBUTION STRATEGICALLY

OUTSIDE 6 CITIES?

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

10

NIELSEN APPROACH TO DEVELOP A TARGETED DISTRIBUTION STRATEGY 5-step approach to expand distribution outside 6 cities

District Prioritization

Top Store Profiling

2 3

Full Scan of Universe & detect target

stores

Matching with Client’s Direct

Stores

1 4 5

Snowballing to identify the Wholesaler

Detect top stores of the category to

identify the opportunity to

reallocate resources and manage SKUs

Replace the subjective

guesswork by statistical technique

to target right provinces &districts

Scan the prioritized districts & provinces

to know size of opportunity

Identify semi-retailers/wholesalers

to penetrate small retailers

Match census result with client’s direct

store list to find out gap

For each category Syndicated census By client Syndicated

census/ by client

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

11

CLIENT’S BENEFIT FROM THE APPROACH

ALLOCATE ENOUGH SALES RESOURCES BY TARGETING RIGHT WHOLESALER

SAVING TIME BY TAPPING TOP CATEGORY SALES

OPTIMIZE COST BY SYNDICATION

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

12

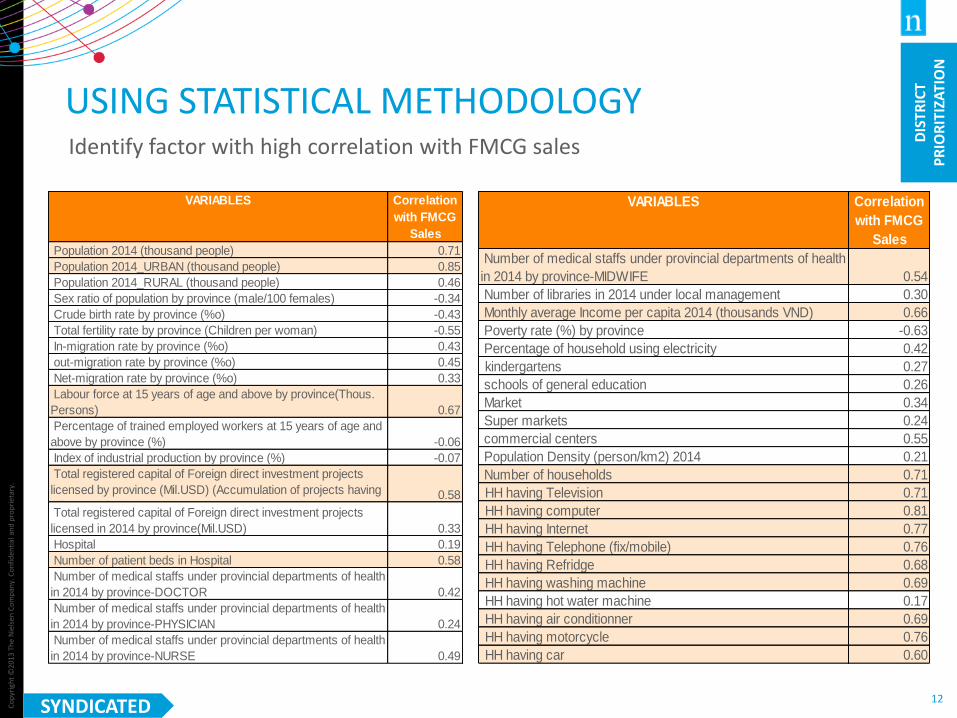

USING STATISTICAL METHODOLOGY Identify factor with high correlation with FMCG sales

VARIABLES Correlation

with FMCG

Sales

Population 2014 (thousand people) 0.71

Population 2014_URBAN (thousand people) 0.85

Population 2014_RURAL (thousand people) 0.46

Sex ratio of population by province (male/100 females) -0.34

Crude birth rate by province (%o) -0.43

Total fertility rate by province (Children per woman) -0.55

In-migration rate by province (%o) 0.43

out-migration rate by province (%o) 0.45

Net-migration rate by province (%o) 0.33

Labour force at 15 years of age and above by province(Thous.

Persons) 0.67

Percentage of trained employed workers at 15 years of age and

above by province (%) -0.06

Index of industrial production by province (%) -0.07

Total registered capital of Foreign direct investment projects

licensed by province (Mil.USD) (Accumulation of projects having

effect as of 31/12/2014) 0.58

Total registered capital of Foreign direct investment projects

licensed in 2014 by province(Mil.USD) 0.33

Hospital 0.19

Number of patient beds in Hospital 0.58

Number of medical staffs under provincial departments of health

in 2014 by province-DOCTOR 0.42

Number of medical staffs under provincial departments of health

in 2014 by province-PHYSICIAN 0.24

Number of medical staffs under provincial departments of health

in 2014 by province-NURSE 0.49

VARIABLES Correlation

with FMCG

Sales

Number of medical staffs under provincial departments of health

in 2014 by province-MIDWIFE 0.54

Number of libraries in 2014 under local management 0.30

Monthly average Income per capita 2014 (thousands VND) 0.66

Poverty rate (%) by province -0.63

Percentage of household using electricity 0.42

kindergartens 0.27

schools of general education 0.26

Market 0.34

Super markets 0.24

commercial centers 0.55

Population Density (person/km2) 2014 0.21

Number of households 0.71

HH having Television 0.71

HH having computer 0.81

HH having Internet 0.77

HH having Telephone (fix/mobile) 0.76

HH having Refridge 0.68

HH having washing machine 0.69

HH having hot water machine 0.17

HH having air conditionner 0.69

HH having motorcycle 0.76

HH having car 0.60

SYNDICATED

DIS

TRIC

T P

RIO

RIT

IZA

TIO

N

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

13

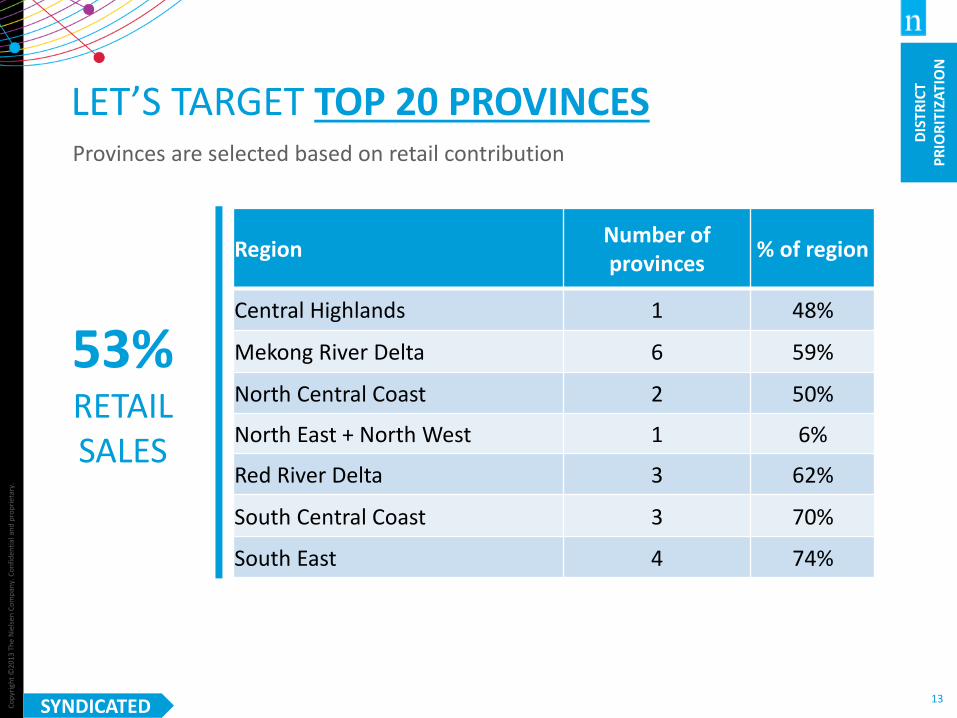

LET’S TARGET TOP 20 PROVINCES Provinces are selected based on retail contribution

Region Number of provinces

% of region

Central Highlands 1 48%

Mekong River Delta 6 59%

North Central Coast 2 50%

North East + North West 1 6%

Red River Delta 3 62%

South Central Coast 3 70%

South East 4 74%

53% RETAIL SALES

DIS

TRIC

T P

RIO

RIT

IZA

TIO

N

SYNDICATED

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

14

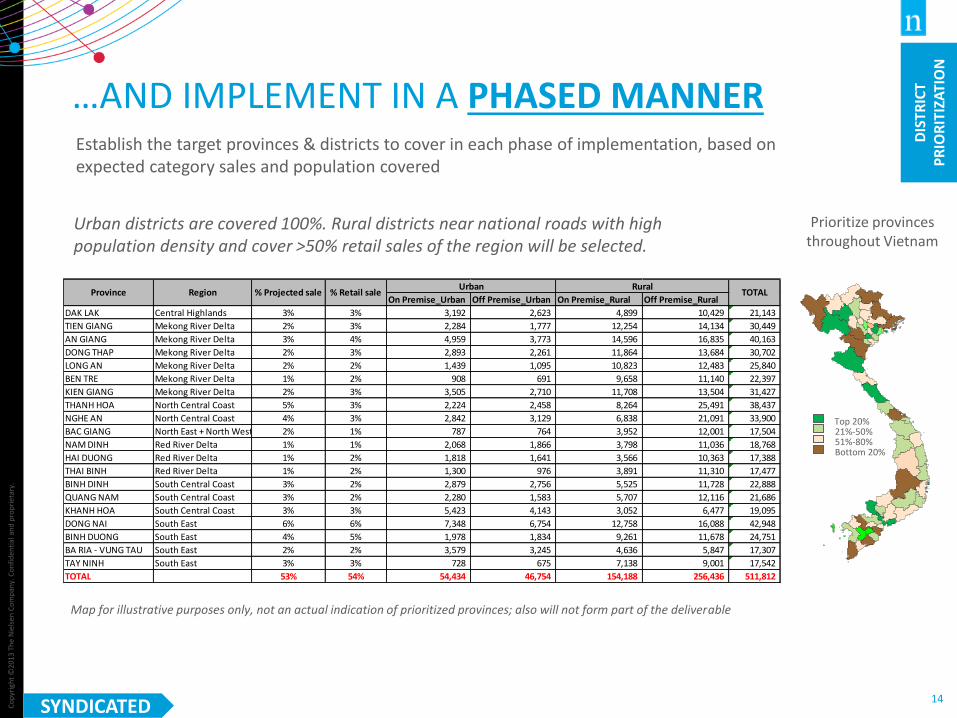

Urban districts are covered 100%. Rural districts near national roads with high population density and cover >50% retail sales of the region will be selected.

…AND IMPLEMENT IN A PHASED MANNER

Map for illustrative purposes only, not an actual indication of prioritized provinces; also will not form part of the deliverable

Top 20% 21%-50% 51%-80% Bottom 20%

Establish the target provinces & districts to cover in each phase of implementation, based on expected category sales and population covered

Prioritize provinces throughout Vietnam

On Premise_Urban Off Premise_Urban On Premise_Rural Off Premise_Rural

DAK LAK Central Highlands 3% 3% 3,192 2,623 4,899 10,429 21,143

TIEN GIANG Mekong River Delta 2% 3% 2,284 1,777 12,254 14,134 30,449

AN GIANG Mekong River Delta 3% 4% 4,959 3,773 14,596 16,835 40,163

DONG THAP Mekong River Delta 2% 3% 2,893 2,261 11,864 13,684 30,702

LONG AN Mekong River Delta 2% 2% 1,439 1,095 10,823 12,483 25,840

BEN TRE Mekong River Delta 1% 2% 908 691 9,658 11,140 22,397

KIEN GIANG Mekong River Delta 2% 3% 3,505 2,710 11,708 13,504 31,427

THANH HOA North Central Coast 5% 3% 2,224 2,458 8,264 25,491 38,437

NGHE AN North Central Coast 4% 3% 2,842 3,129 6,838 21,091 33,900

BAC GIANG North East + North West 2% 1% 787 764 3,952 12,001 17,504

NAM DINH Red River Delta 1% 1% 2,068 1,866 3,798 11,036 18,768

HAI DUONG Red River Delta 1% 2% 1,818 1,641 3,566 10,363 17,388

THAI BINH Red River Delta 1% 2% 1,300 976 3,891 11,310 17,477

BINH DINH South Central Coast 3% 2% 2,879 2,756 5,525 11,728 22,888

QUANG NAM South Central Coast 3% 2% 2,280 1,583 5,707 12,116 21,686

KHANH HOA South Central Coast 3% 3% 5,423 4,143 3,052 6,477 19,095

DONG NAI South East 6% 6% 7,348 6,754 12,758 16,088 42,948

BINH DUONG South East 4% 5% 1,978 1,834 9,261 11,678 24,751

BA RIA - VUNG TAU South East 2% 2% 3,579 3,245 4,636 5,847 17,307

TAY NINH South East 3% 3% 728 675 7,138 9,001 17,542

TOTAL 53% 54% 54,434 46,754 154,188 256,436 511,812

% Projected saleRegionProvince TOTALUrban Rural

% Retail sale

DIS

TRIC

T P

RIO

RIT

IZA

TIO

N

SYNDICATED

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

15

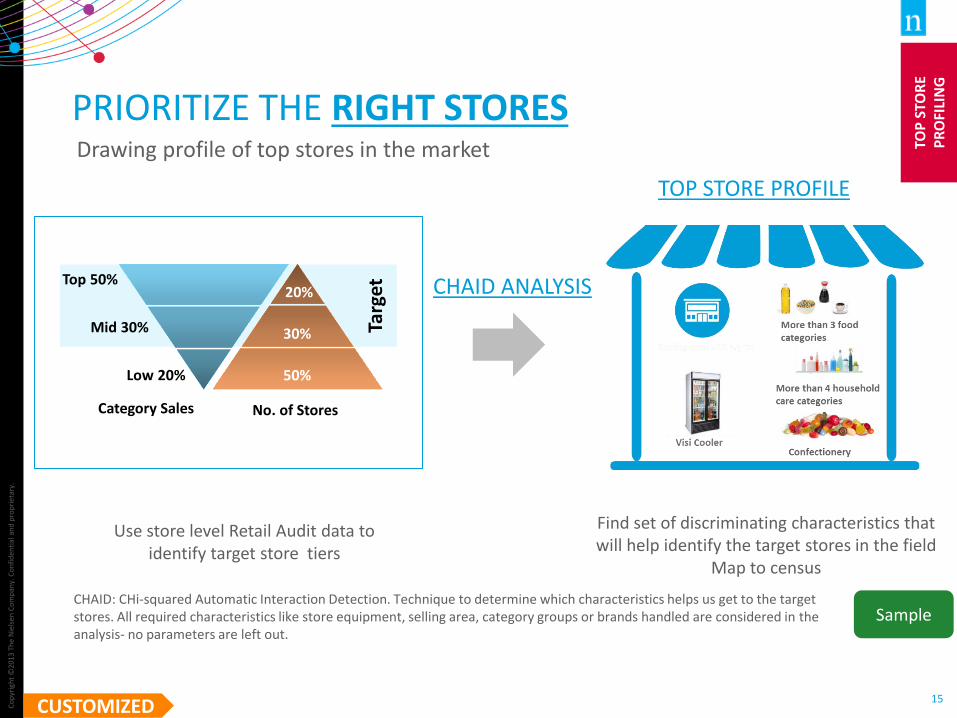

PRIORITIZE THE RIGHT STORES Drawing profile of top stores in the market

CHAID: CHi-squared Automatic Interaction Detection. Technique to determine which characteristics helps us get to the target stores. All required characteristics like store equipment, selling area, category groups or brands handled are considered in the analysis- no parameters are left out.

Sample

20%

30%

50%

Top 50%

Mid 30%

Low 20%

Category Sales No. of Stores

Targ

et

Use store level Retail Audit data to identify target store tiers

Find set of discriminating characteristics that will help identify the target stores in the field

Map to census

TOP STORE PROFILE

CHAID ANALYSIS

TOP

STO

RE

PR

OFI

LIN

G

CUSTOMIZED

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

16

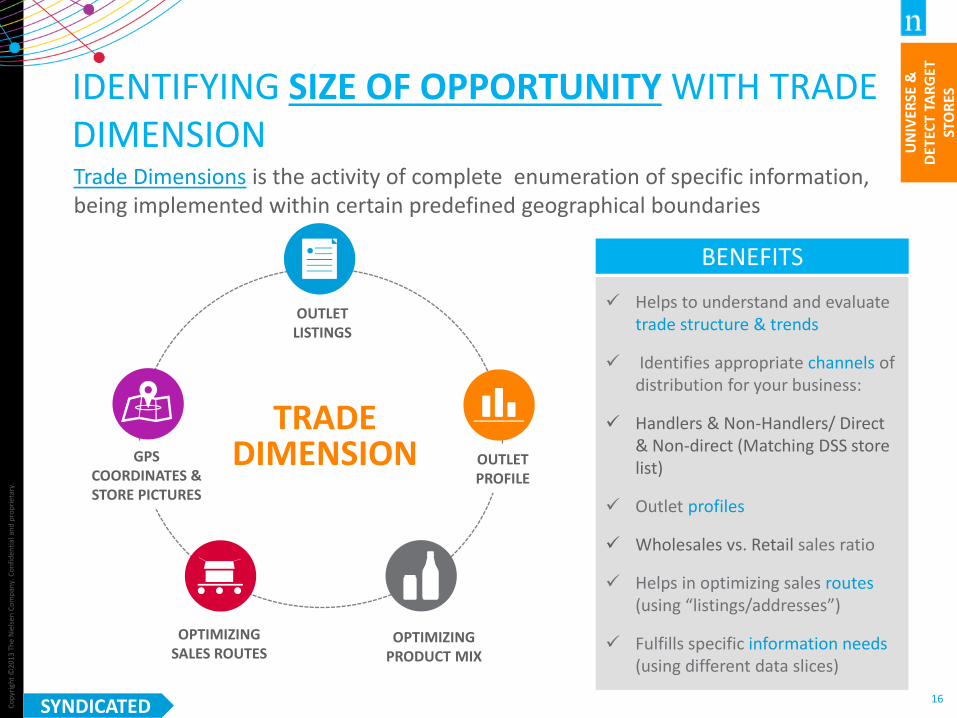

IDENTIFYING SIZE OF OPPORTUNITY WITH TRADE DIMENSION Trade Dimensions is the activity of complete enumeration of specific information, being implemented within certain predefined geographical boundaries

TRADE DIMENSION

OUTLET LISTINGS

OUTLET PROFILE

OPTIMIZING PRODUCT MIX

GPS COORDINATES & STORE PICTURES

OPTIMIZING SALES ROUTES

Helps to understand and evaluate trade structure & trends

Identifies appropriate channels of distribution for your business:

Handlers & Non-Handlers/ Direct & Non-direct (Matching DSS store list)

Outlet profiles

Wholesales vs. Retail sales ratio

Helps in optimizing sales routes (using “listings/addresses”)

Fulfills specific information needs (using different data slices)

BENEFITS

SYNDICATED

FULL

SC

AN

OF

UN

IVER

SE &

D

ETEC

T TA

RG

ET

STO

RES

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

17

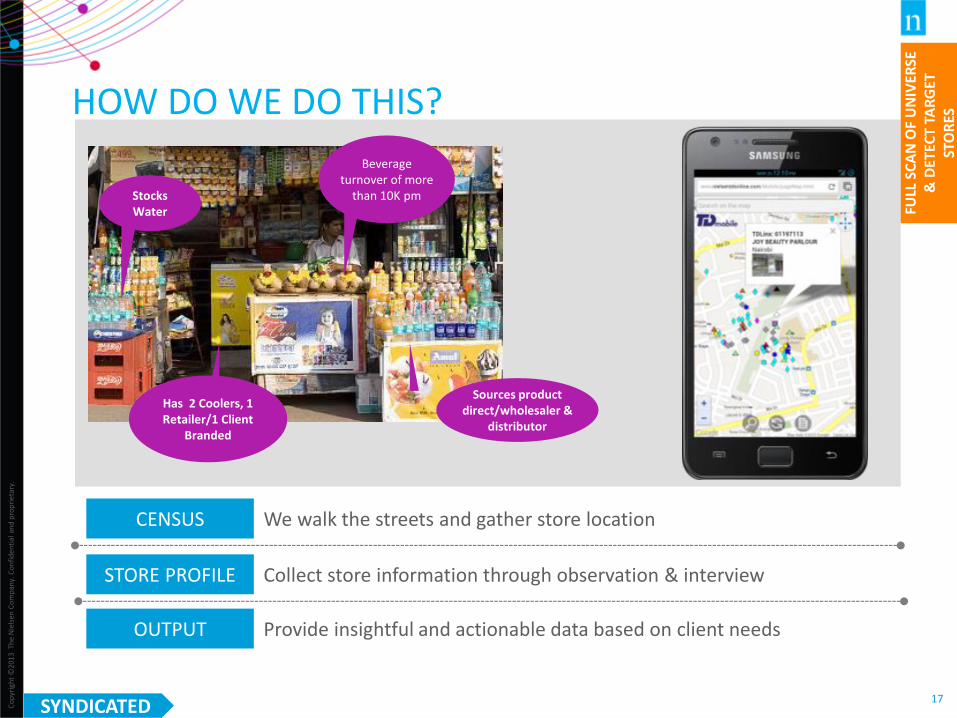

Stocks Water

Has 2 Coolers, 1 Retailer/1 Client

Branded

Sources product direct/wholesaler &

distributor

Beverage turnover of more

than 10K pm

HOW DO WE DO THIS?

CENSUS We walk the streets and gather store location

STORE PROFILE Collect store information through observation & interview

OUTPUT Provide insightful and actionable data based on client needs

FULL

SC

AN

OF

UN

IVER

SE

& D

ETEC

T TA

RG

ET

STO

RES

SYNDICATED

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

18

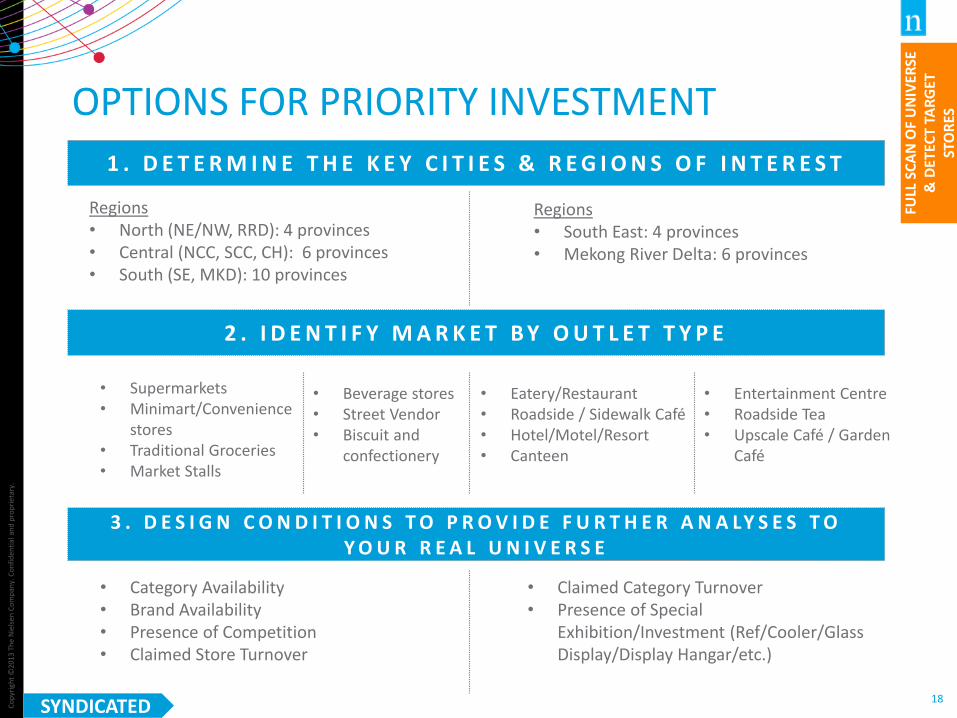

1 . D E T E R M I N E T H E K E Y C I T I E S & R E G I O N S O F I N T E R E S T

Regions • North (NE/NW, RRD): 4 provinces • Central (NCC, SCC, CH): 6 provinces • South (SE, MKD): 10 provinces

• Supermarkets • Minimart/Convenience

stores • Traditional Groceries • Market Stalls

• Eatery/Restaurant • Roadside / Sidewalk Café • Hotel/Motel/Resort • Canteen

• Category Availability • Brand Availability • Presence of Competition • Claimed Store Turnover

• Beverage stores • Street Vendor • Biscuit and

confectionery

• Entertainment Centre • Roadside Tea • Upscale Café / Garden

Café

2 . I D E N T I F Y M A R K E T B Y O U T L E T T Y P E

3 . D E S I G N C O N D I T I O N S T O P R O V I D E F U R T H E R A N A LY S E S T O Y O U R R E A L U N I V E R S E

• Claimed Category Turnover • Presence of Special

Exhibition/Investment (Ref/Cooler/Glass Display/Display Hangar/etc.)

Regions • South East: 4 provinces • Mekong River Delta: 6 provinces

OPTIONS FOR PRIORITY INVESTMENT

FULL

SC

AN

OF

UN

IVER

SE

& D

ETEC

T TA

RG

ET

STO

RES

SYNDICATED

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

19

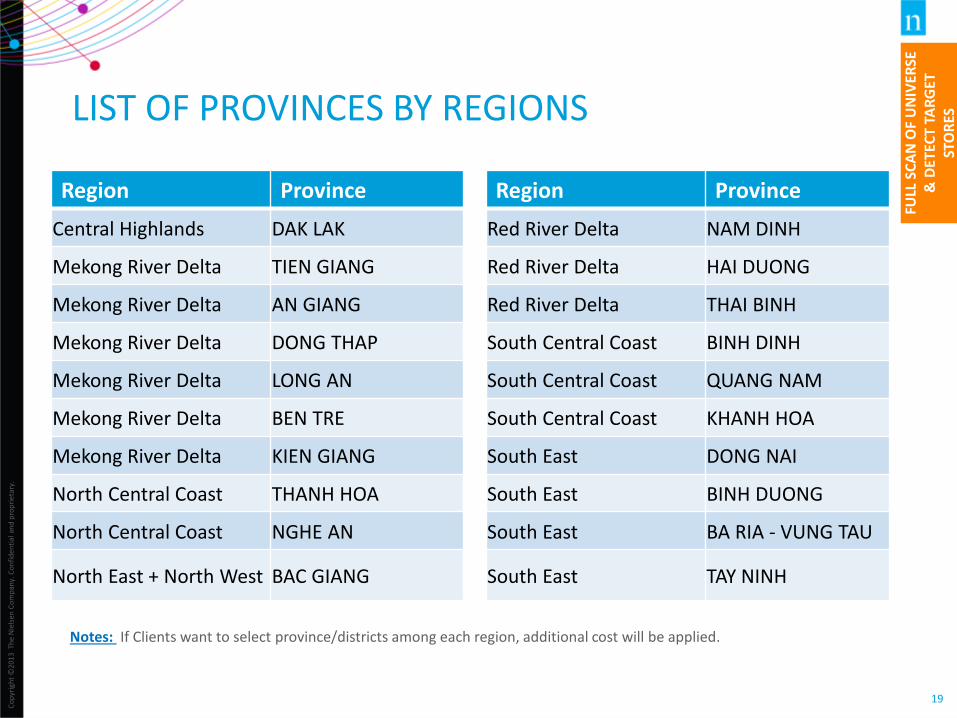

LIST OF PROVINCES BY REGIONS

Notes: If Clients want to select province/districts among each region, additional cost will be applied.

Region Province

Central Highlands DAK LAK

Mekong River Delta TIEN GIANG

Mekong River Delta AN GIANG

Mekong River Delta DONG THAP

Mekong River Delta LONG AN

Mekong River Delta BEN TRE

Mekong River Delta KIEN GIANG

North Central Coast THANH HOA

North Central Coast NGHE AN

North East + North West BAC GIANG

Region Province

Red River Delta NAM DINH

Red River Delta HAI DUONG

Red River Delta THAI BINH

South Central Coast BINH DINH

South Central Coast QUANG NAM

South Central Coast KHANH HOA

South East DONG NAI

South East BINH DUONG

South East BA RIA - VUNG TAU

South East TAY NINH

FULL

SC

AN

OF

UN

IVER

SE

& D

ETEC

T TA

RG

ET

STO

RES

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

20

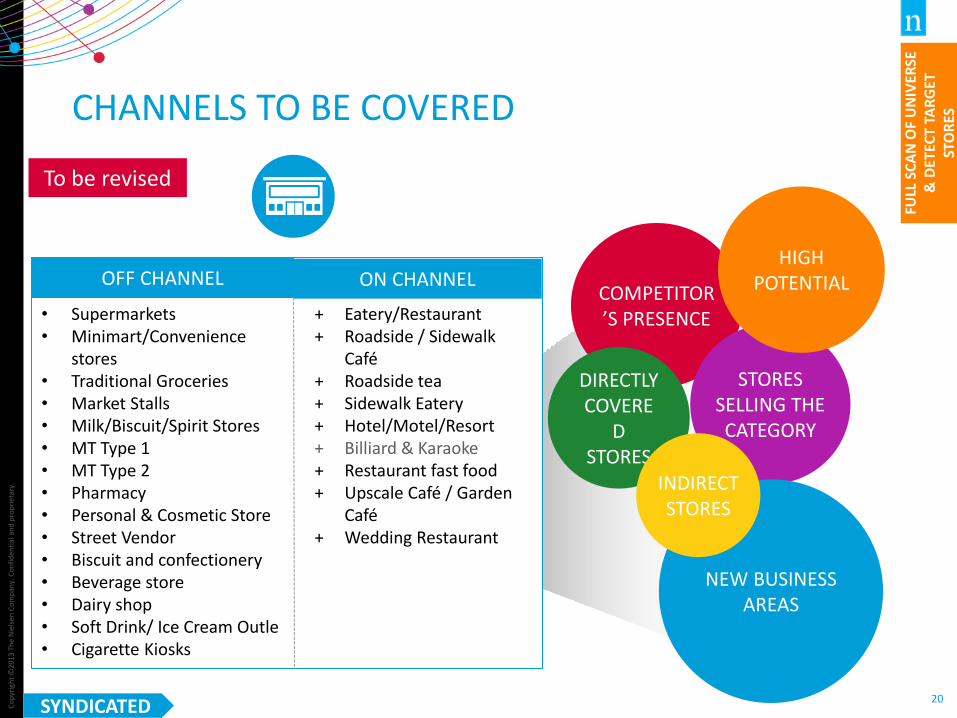

OFF CHANNEL

• Supermarkets • Minimart/Convenience

stores • Traditional Groceries • Market Stalls • Milk/Biscuit/Spirit Stores • MT Type 1 • MT Type 2 • Pharmacy • Personal & Cosmetic Store • Street Vendor • Biscuit and confectionery • Beverage store • Dairy shop • Soft Drink/ Ice Cream Outle • Cigarette Kiosks

ON CHANNEL

+ Eatery/Restaurant + Roadside / Sidewalk

Café + Roadside tea + Sidewalk Eatery + Hotel/Motel/Resort + Billiard & Karaoke + Restaurant fast food + Upscale Café / Garden

Café + Wedding Restaurant

COMPETITOR’S PRESENCE

STORES SELLING THE CATEGORY

DIRECTLY COVERE

D STORES

NEW BUSINESS AREAS

HIGH POTENTIAL

INDIRECT STORES

CHANNELS TO BE COVERED

To be revised

FULL

SC

AN

OF

UN

IVER

SE

& D

ETEC

T TA

RG

ET

STO

RES

SYNDICATED

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

21

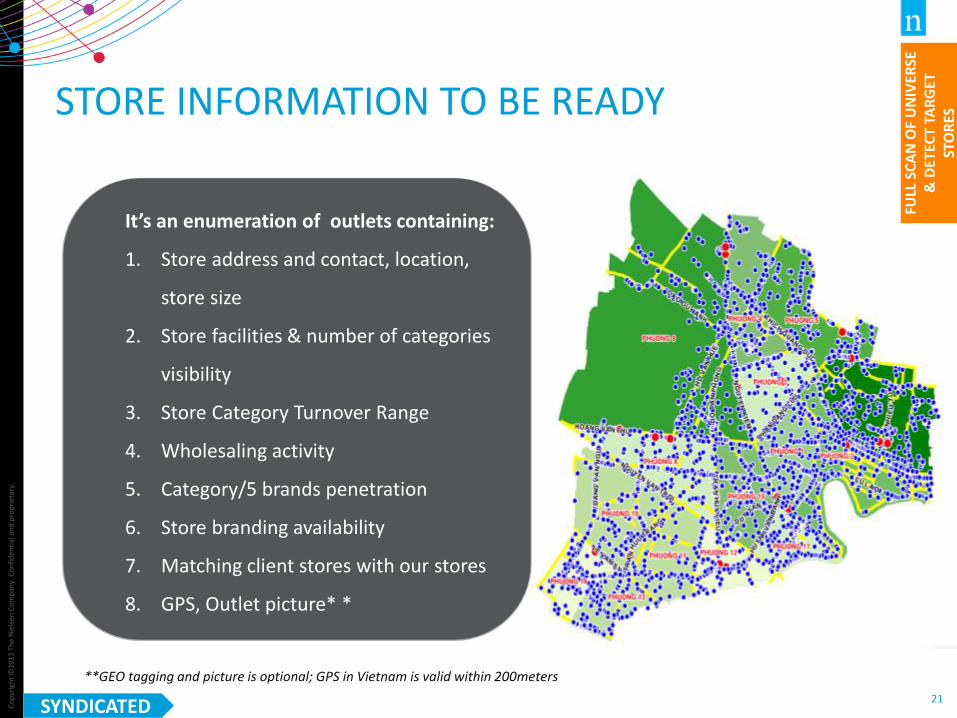

It’s an enumeration of outlets containing:

1. Store address and contact, location,

store size

2. Store facilities & number of categories

visibility

3. Store Category Turnover Range

4. Wholesaling activity

5. Category/5 brands penetration

6. Store branding availability

7. Matching client stores with our stores

8. GPS, Outlet picture* *

**GEO tagging and picture is optional; GPS in Vietnam is valid within 200meters

STORE INFORMATION TO BE READY

FULL

SC

AN

OF

UN

IVER

SE

& D

ETEC

T TA

RG

ET

STO

RES

SYNDICATED

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

22

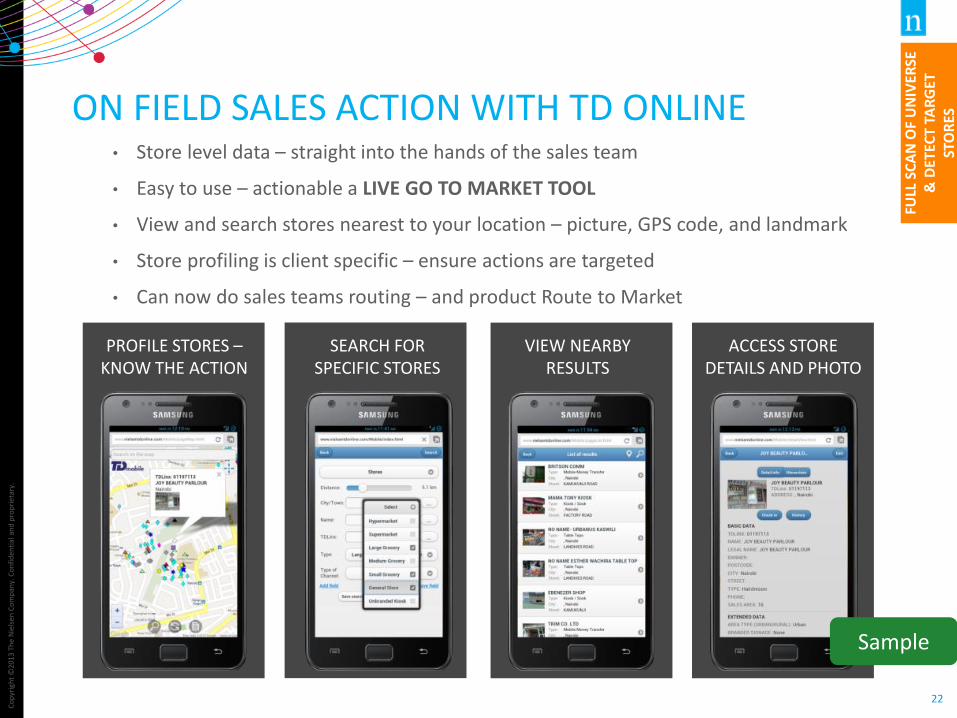

ON FIELD SALES ACTION WITH TD ONLINE • Store level data – straight into the hands of the sales team

• Easy to use – actionable a LIVE GO TO MARKET TOOL

• View and search stores nearest to your location – picture, GPS code, and landmark

• Store profiling is client specific – ensure actions are targeted

• Can now do sales teams routing – and product Route to Market

PROFILE STORES – KNOW THE ACTION

SEARCH FOR SPECIFIC STORES

VIEW NEARBY RESULTS

ACCESS STORE DETAILS AND PHOTO

Sample

FULL

SC

AN

OF

UN

IVER

SE

& D

ETEC

T TA

RG

ET

STO

RES

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

23

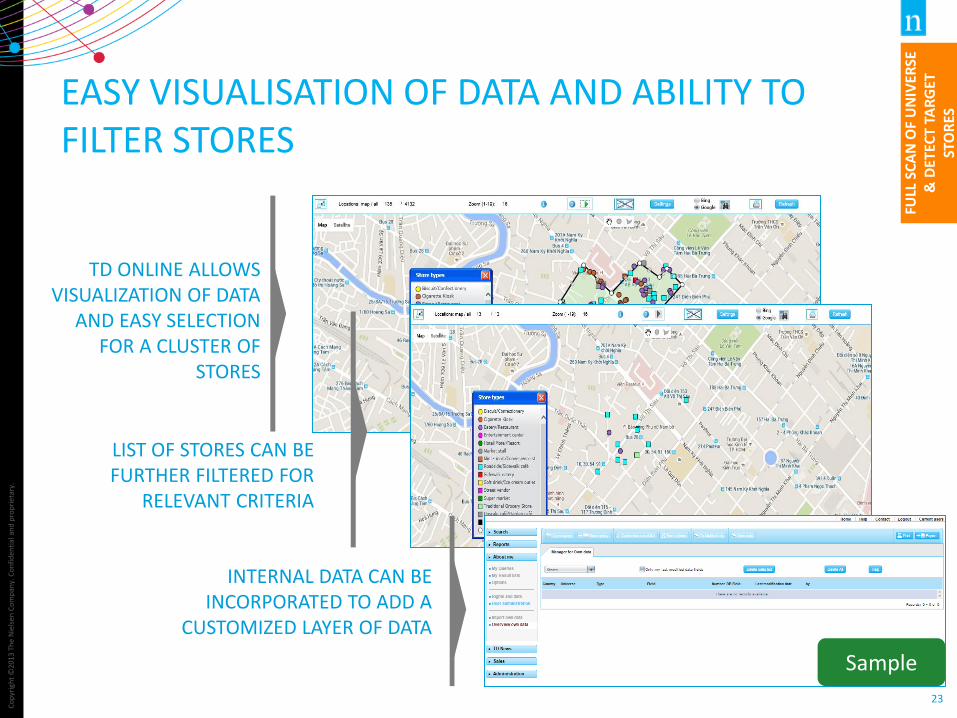

EASY VISUALISATION OF DATA AND ABILITY TO FILTER STORES

TD ONLINE ALLOWS VISUALIZATION OF DATA

AND EASY SELECTION FOR A CLUSTER OF

STORES

INTERNAL DATA CAN BE INCORPORATED TO ADD A

CUSTOMIZED LAYER OF DATA

Sample

FULL

SC

AN

OF

UN

IVER

SE

& D

ETEC

T TA

RG

ET

STO

RES

LIST OF STORES CAN BE FURTHER FILTERED FOR

RELEVANT CRITERIA

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

24

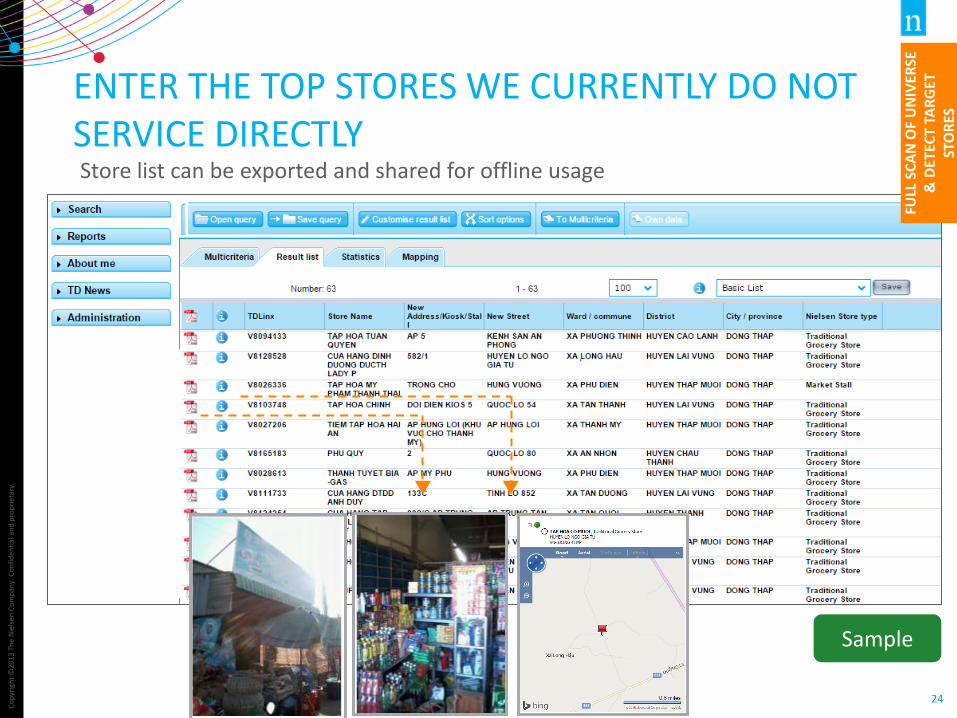

ENTER THE TOP STORES WE CURRENTLY DO NOT SERVICE DIRECTLY Store list can be exported and shared for offline usage

Sample

FULL

SC

AN

OF

UN

IVER

SE

& D

ETEC

T TA

RG

ET

STO

RES

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

25

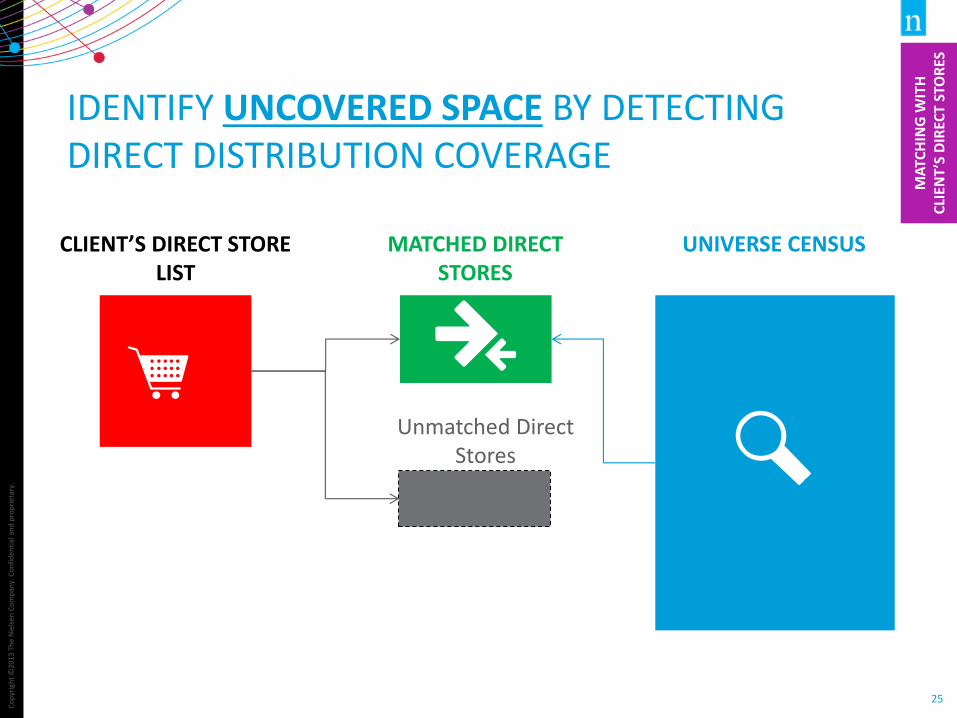

IDENTIFY UNCOVERED SPACE BY DETECTING DIRECT DISTRIBUTION COVERAGE

CLIENT’S DIRECT STORE LIST

UNIVERSE CENSUS MATCHED DIRECT STORES

Unmatched Direct Stores

Check this chart

MA

TCH

ING

WIT

H

CLI

ENT

’S D

IREC

T ST

OR

ES

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

26

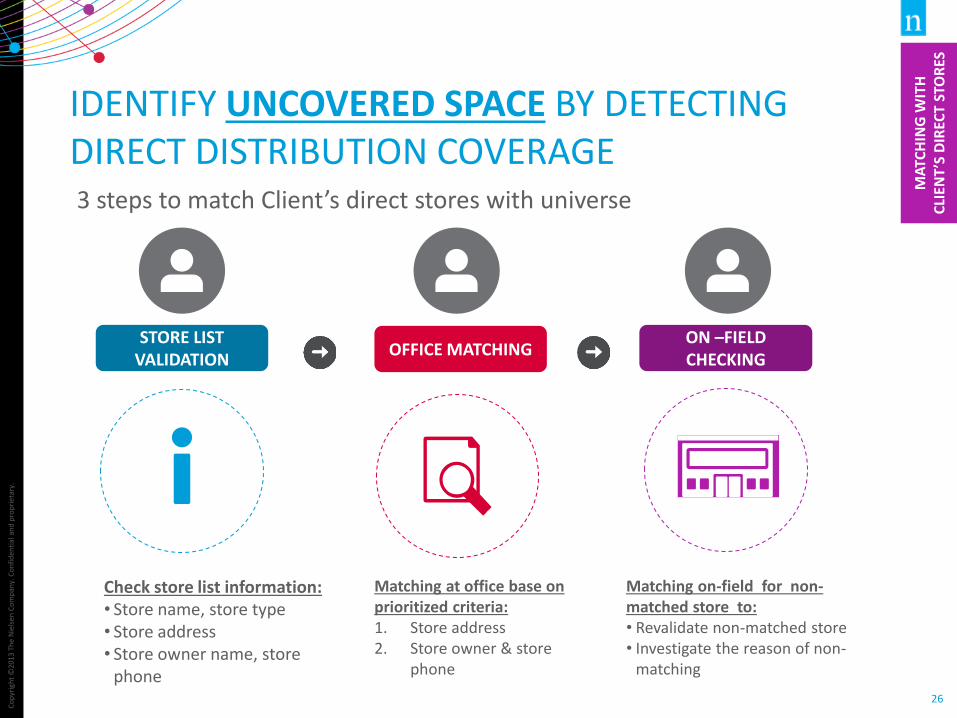

IDENTIFY UNCOVERED SPACE BY DETECTING DIRECT DISTRIBUTION COVERAGE 3 steps to match Client’s direct stores with universe

STORE LIST VALIDATION

Check store list information: • Store name, store type • Store address • Store owner name, store

phone

OFFICE MATCHING

Matching at office base on prioritized criteria: 1. Store address 2. Store owner & store

phone

ON –FIELD CHECKING

Matching on-field for non-matched store to: • Revalidate non-matched store • Investigate the reason of non-

matching

MA

TCH

ING

WIT

H

CLI

ENT

’S D

IREC

T ST

OR

ES

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

27

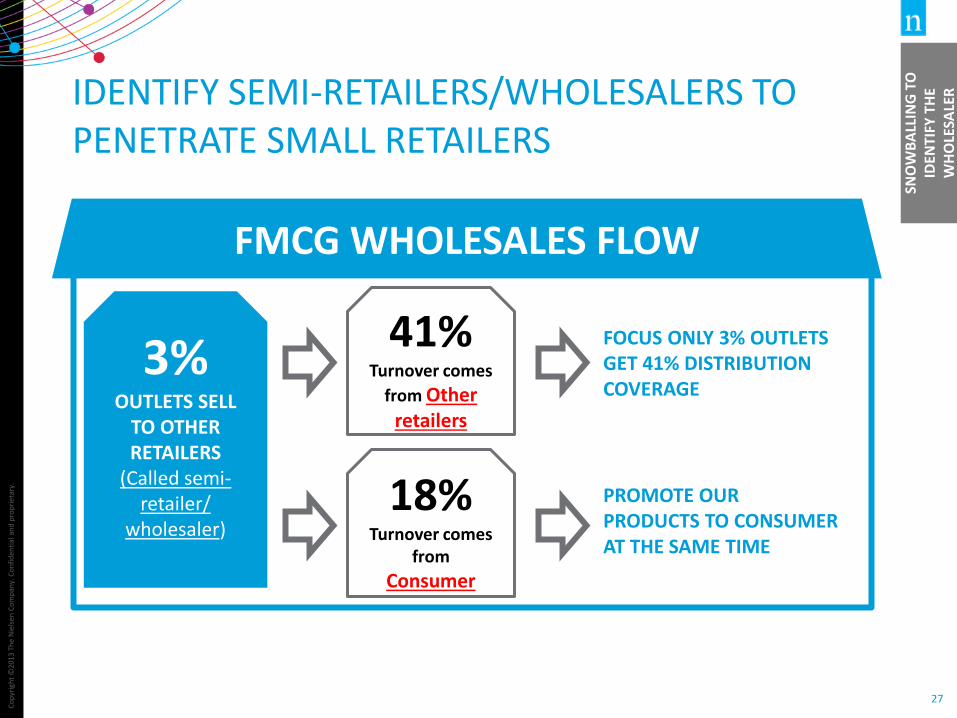

IDENTIFY SEMI-RETAILERS/WHOLESALERS TO PENETRATE SMALL RETAILERS

FMCG WHOLESALES FLOW

3% OUTLETS SELL

TO OTHER RETAILERS

(Called semi-retailer/

wholesaler)

41% Turnover comes

from Other retailers

18% Turnover comes

from

Consumer

FOCUS ONLY 3% OUTLETS GET 41% DISTRIBUTION COVERAGE

PROMOTE OUR PRODUCTS TO CONSUMER AT THE SAME TIME

Check this slide Source of

information

SNO

WB

ALL

ING

TO

ID

ENTI

FY T

HE

WH

OLE

SALE

R

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

28

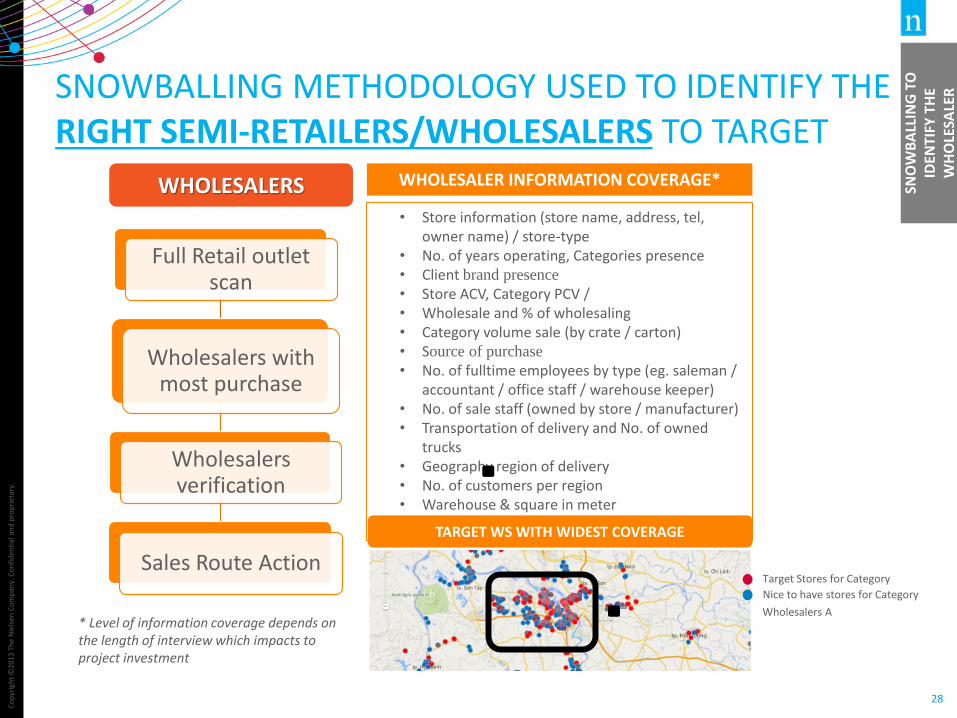

SNOWBALLING METHODOLOGY USED TO IDENTIFY THE RIGHT SEMI-RETAILERS/WHOLESALERS TO TARGET

WHOLESALERS

Full Retail outlet scan

Wholesalers with most purchase

Wholesalers verification

Sales Route Action

• Store information (store name, address, tel, owner name) / store-type

• No. of years operating, Categories presence • Client brand presence • Store ACV, Category PCV / • Wholesale and % of wholesaling • Category volume sale (by crate / carton) • Source of purchase • No. of fulltime employees by type (eg. saleman /

accountant / office staff / warehouse keeper) • No. of sale staff (owned by store / manufacturer) • Transportation of delivery and No. of owned

trucks • Geography region of delivery • No. of customers per region • Warehouse & square in meter • No. of offices & office facilities

WHOLESALER INFORMATION COVERAGE*

TARGET WS WITH WIDEST COVERAGE

Target Stores for Category

Nice to have stores for Category

Wholesalers A * Level of information coverage depends on the length of interview which impacts to project investment

SNO

WB

ALL

ING

TO

ID

ENTI

FY T

HE

WH

OLE

SALE

R

CLIENT INVESTMENT

TIMELINE TO GO!

34

T H A N K Y O U

BY NIELSEN SALESFORCE ACTIVATION TEAM - Nov 2016