Embed Size (px)

DESCRIPTION

Baldwin Bicycle Company

Citation preview

7/14/2019 Group8-Baldwin Bicycle Company

http://slidepdf.com/reader/full/group8-baldwin-bicycle-company 1/9

Baldwin Bicycle Company

Group 8

12P194 Chandrachuda12P229 Santosh Garbham

12P206 Kartik Maheswari

12P208 Kawaljeet Singh

7/14/2019 Group8-Baldwin Bicycle Company

http://slidepdf.com/reader/full/group8-baldwin-bicycle-company 2/9

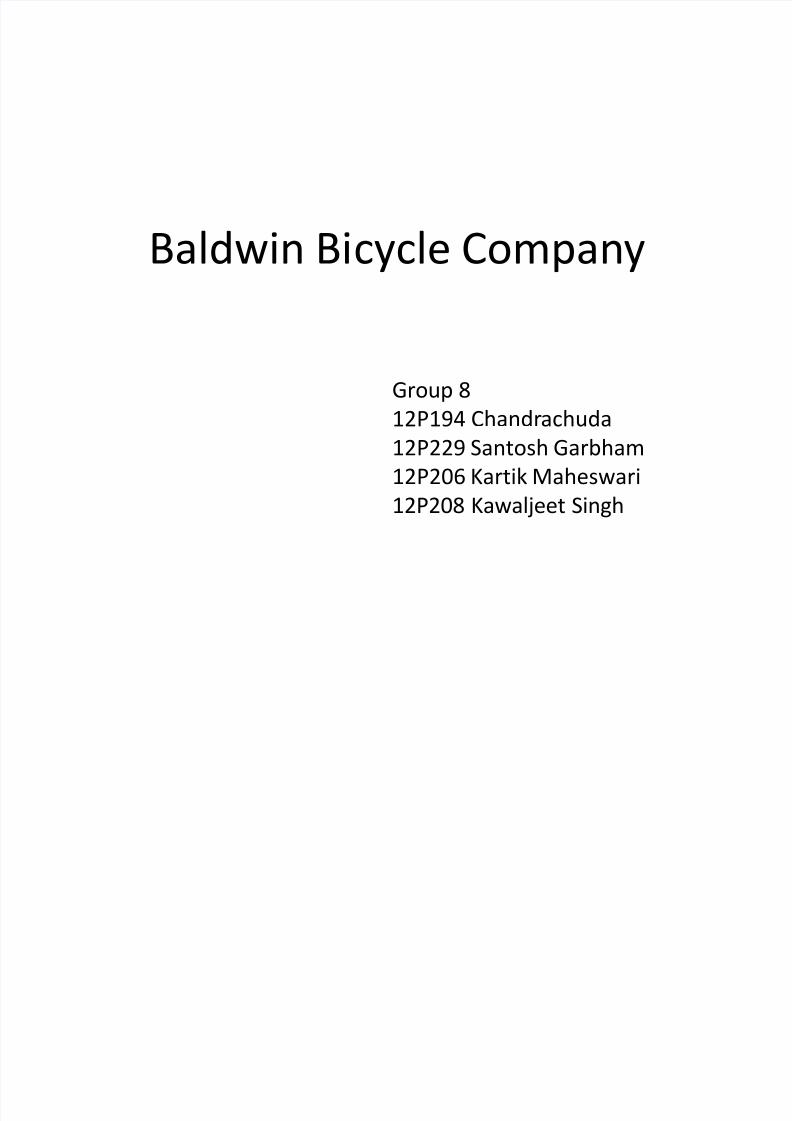

Added inventory costs

Work In process 1000 bikes 41950.000

Finished goods 500 bikes 41950.000

Materials 2 months of Materials 165833.333

7/14/2019 Group8-Baldwin Bicycle Company

http://slidepdf.com/reader/full/group8-baldwin-bicycle-company 3/9

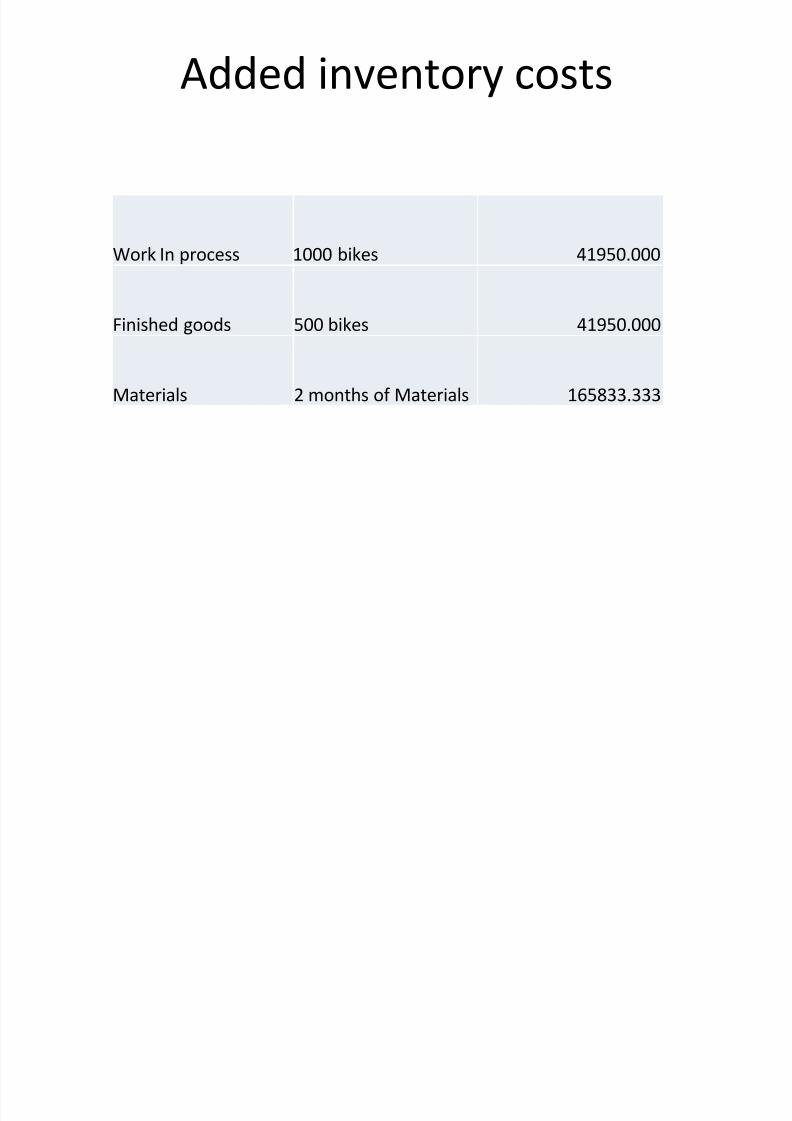

Asset Related Costs

Receivables for 5 months =92.9*25000/12*5 967708.333

Inventory =WIP,FinishedGoods,Materials 249733.333

Asset Related costs

Pretax cost of funds 140005.792

Record Keeping Costs 24348.833

Inventory Insurance 1498.400

State Property tax on inventory 1748.133Inventory handling labor and

equipment 14984.000

Pilferage,obsolescence,damage 5494.133

7/14/2019 Group8-Baldwin Bicycle Company

http://slidepdf.com/reader/full/group8-baldwin-bicycle-company 4/9

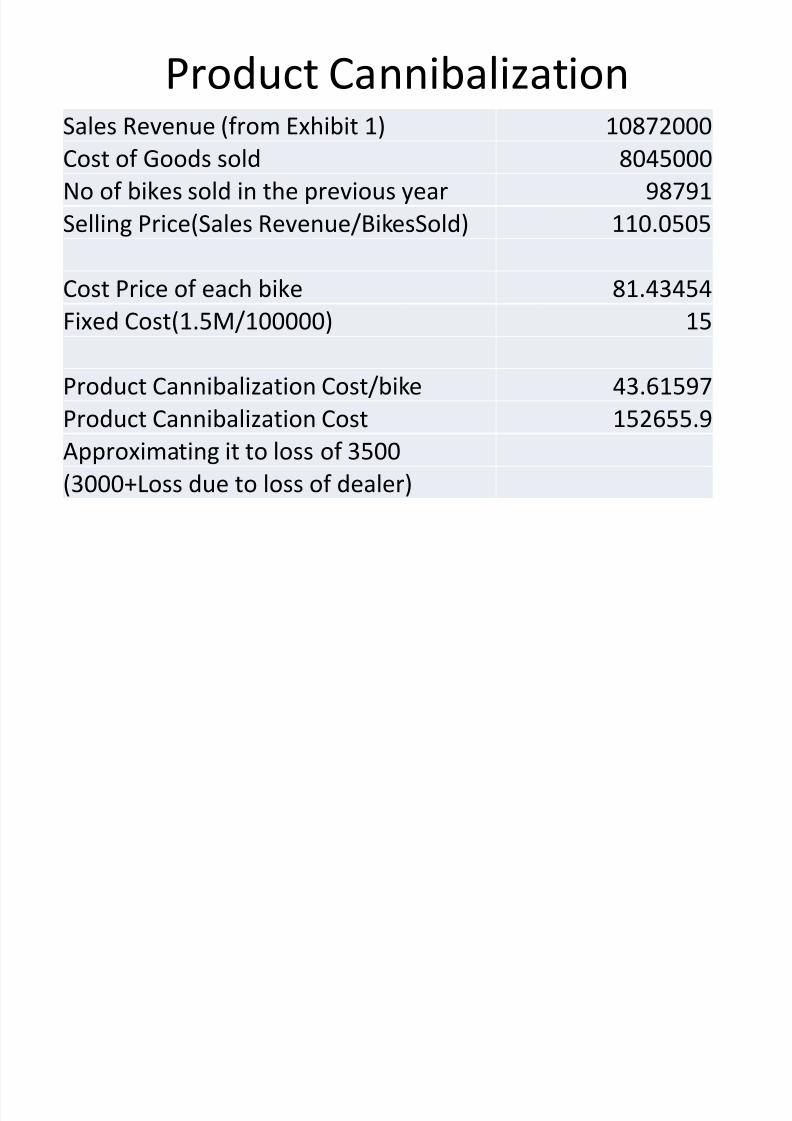

Product Cannibalization

Sales Revenue (from Exhibit 1) 10872000Cost of Goods sold 8045000

No of bikes sold in the previous year 98791

Selling Price(Sales Revenue/BikesSold) 110.0505

Cost Price of each bike 81.43454

Fixed Cost(1.5M/100000) 15

Product Cannibalization Cost/bike 43.61597

Product Cannibalization Cost 152655.9Approximating it to loss of 3500

(3000+Loss due to loss of dealer)

7/14/2019 Group8-Baldwin Bicycle Company

http://slidepdf.com/reader/full/group8-baldwin-bicycle-company 5/9

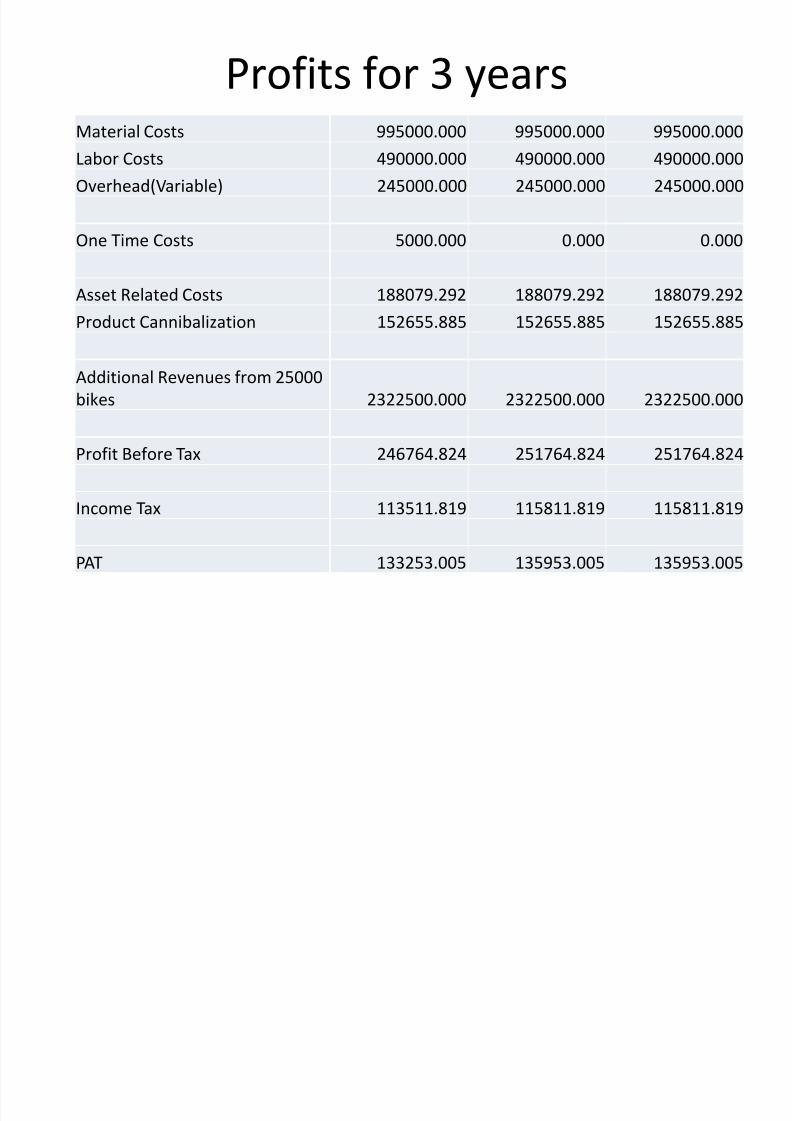

Profits for 3 years

Material Costs 995000.000 995000.000 995000.000Labor Costs 490000.000 490000.000 490000.000

Overhead(Variable) 245000.000 245000.000 245000.000

One Time Costs 5000.000 0.000 0.000

Asset Related Costs 188079.292 188079.292 188079.292

Product Cannibalization 152655.885 152655.885 152655.885

Additional Revenues from 25000

bikes 2322500.000 2322500.000 2322500.000

Profit Before Tax 246764.824 251764.824 251764.824

Income Tax 113511.819 115811.819 115811.819

PAT 133253.005 135953.005 135953.005

7/14/2019 Group8-Baldwin Bicycle Company

http://slidepdf.com/reader/full/group8-baldwin-bicycle-company 6/9

Risks and Rewards

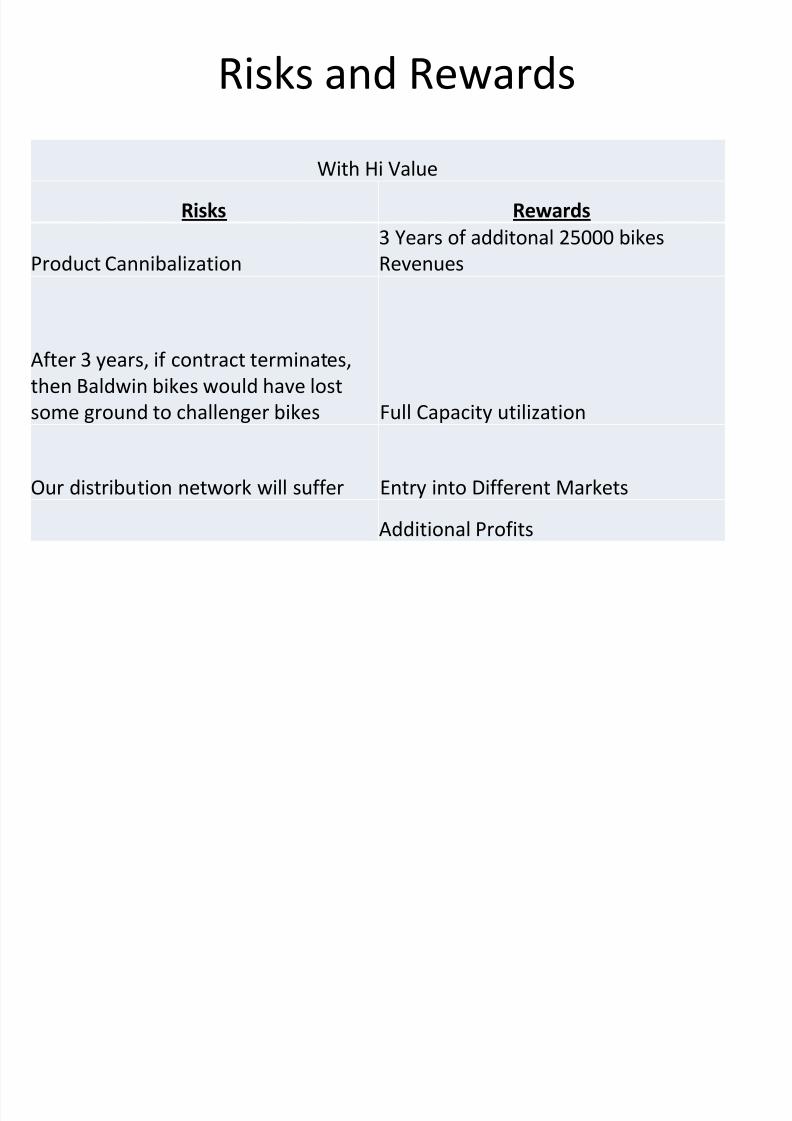

With Hi Value

Risks Rewards

Product Cannibalization

3 Years of additonal 25000 bikes

Revenues

After 3 years, if contract terminates,

then Baldwin bikes would have lost

some ground to challenger bikes Full Capacity utilization

Our distribution network will suffer Entry into Different Markets

Additional Profits

7/14/2019 Group8-Baldwin Bicycle Company

http://slidepdf.com/reader/full/group8-baldwin-bicycle-company 7/9

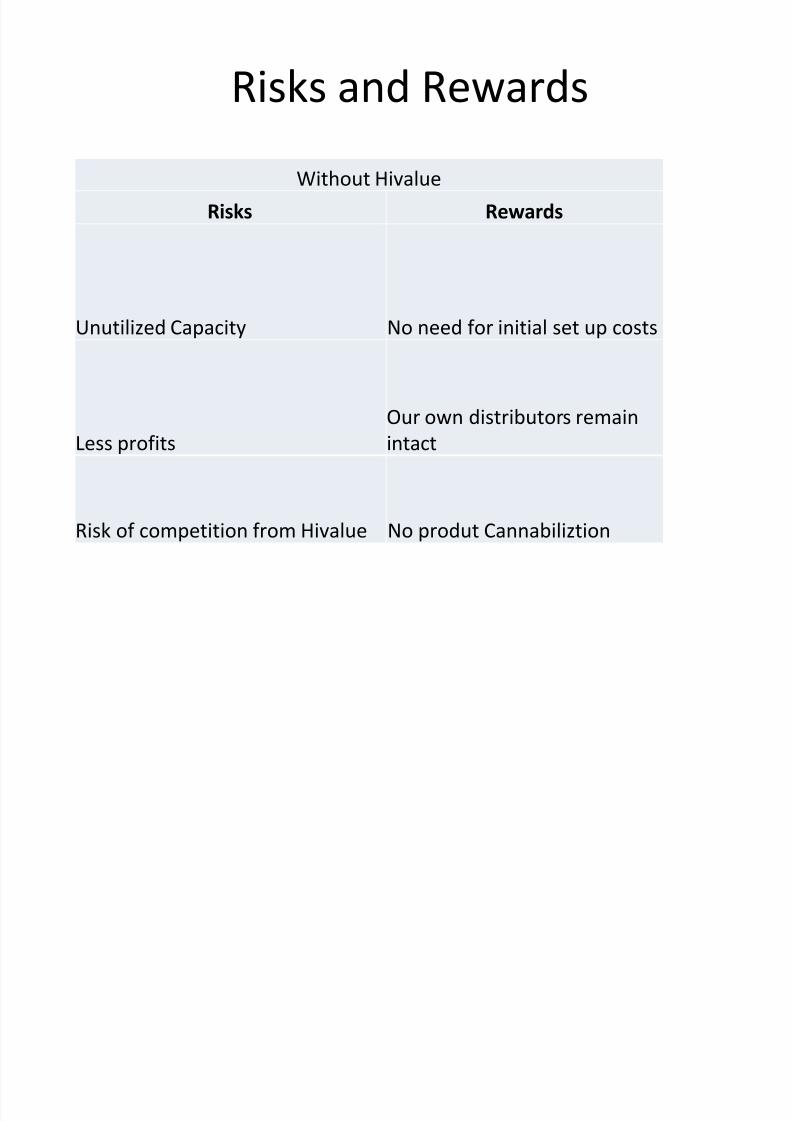

Without Hivalue

Risks Rewards

Unutilized Capacity No need for initial set up costs

Less profitsOur own distributors remainintact

Risk of competition from Hivalue No produt Cannabiliztion

Risks and Rewards

7/14/2019 Group8-Baldwin Bicycle Company

http://slidepdf.com/reader/full/group8-baldwin-bicycle-company 8/9

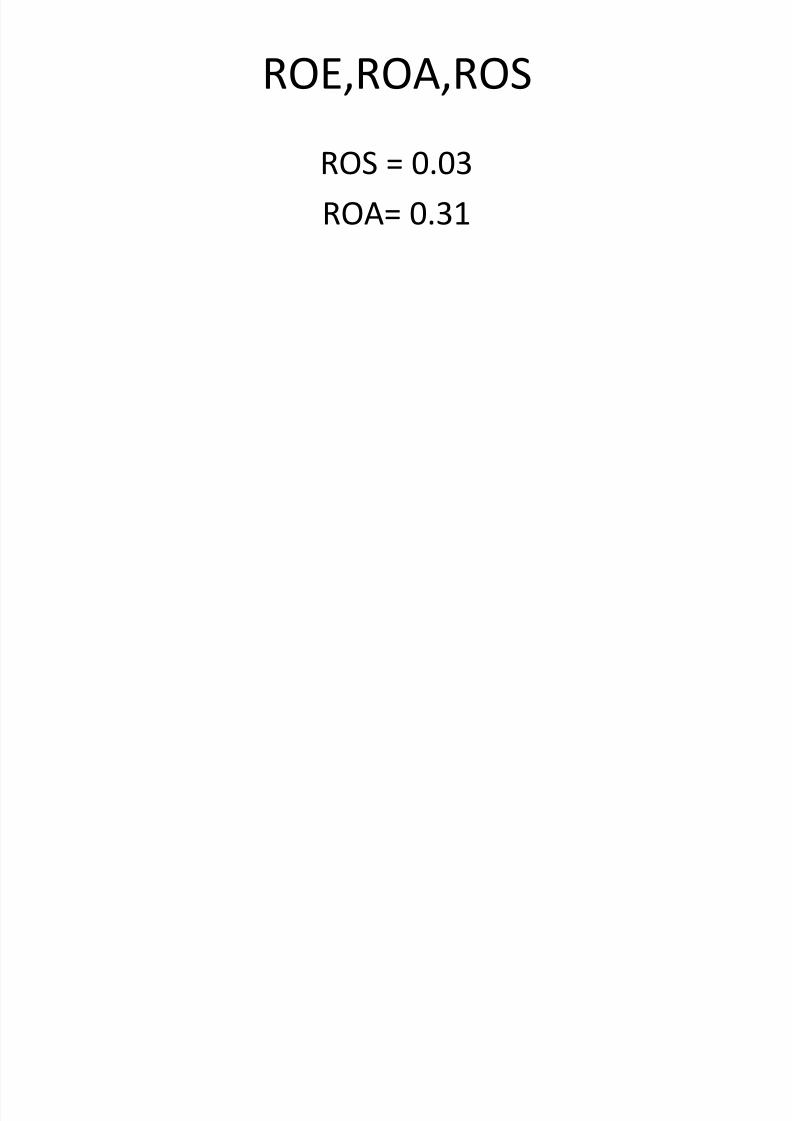

ROE,ROA,ROS

ROS = 0.03

ROA= 0.31

7/14/2019 Group8-Baldwin Bicycle Company

http://slidepdf.com/reader/full/group8-baldwin-bicycle-company 9/9

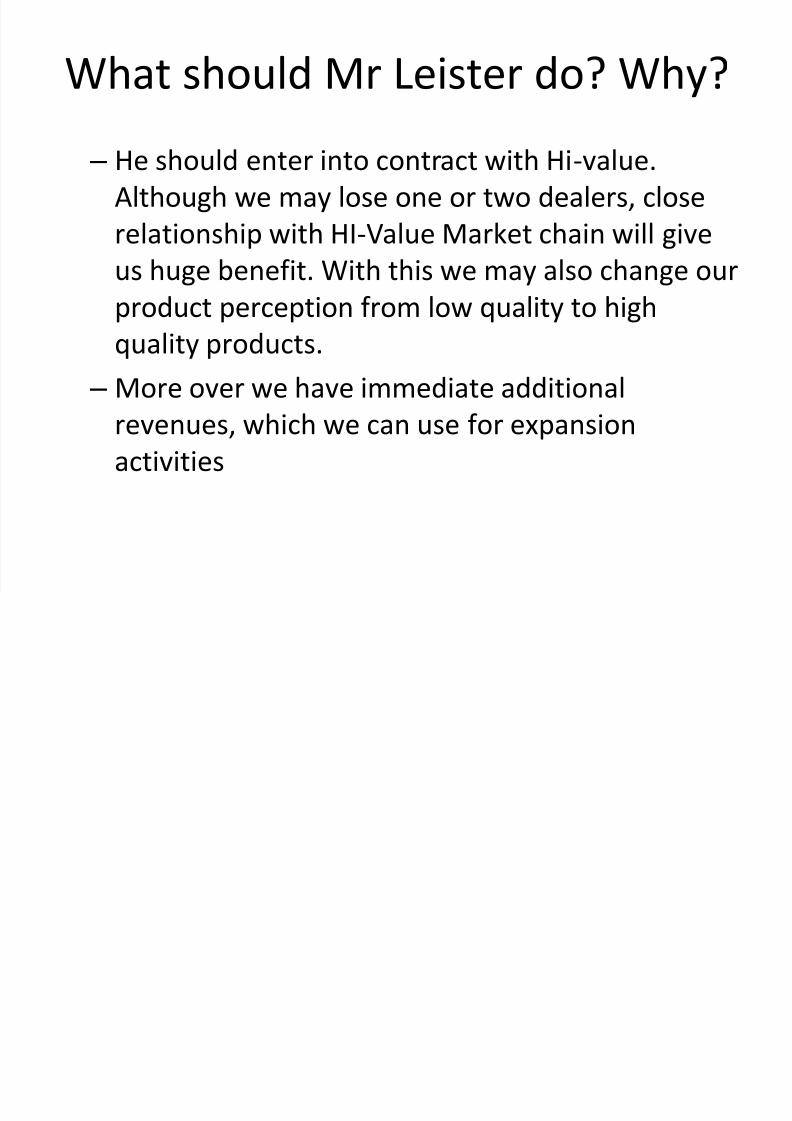

What should Mr Leister do? Why?

– He should enter into contract with Hi-value.

Although we may lose one or two dealers, close

relationship with HI-Value Market chain will give

us huge benefit. With this we may also change ourproduct perception from low quality to high

quality products.

– More over we have immediate additional

revenues, which we can use for expansionactivities