Embed Size (px)

Citation preview

Gross IncomeChapter 6

1

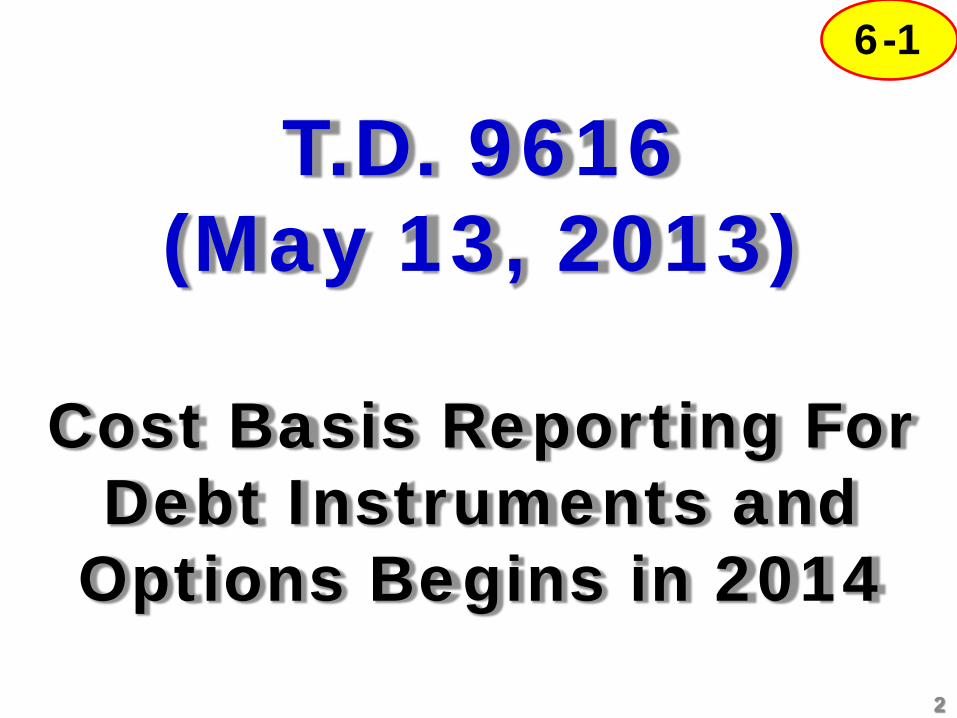

T.D. 9616 (May 13, 2013)

Cost Basis Reporting For Debt Instruments and

Options Begins in 2014

6-1

2

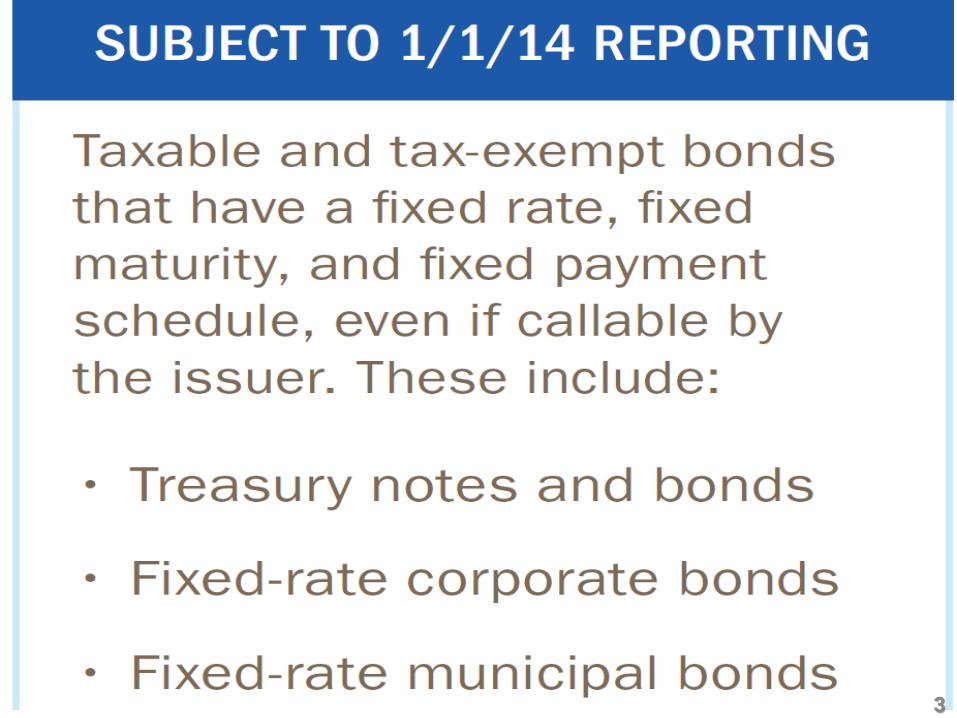

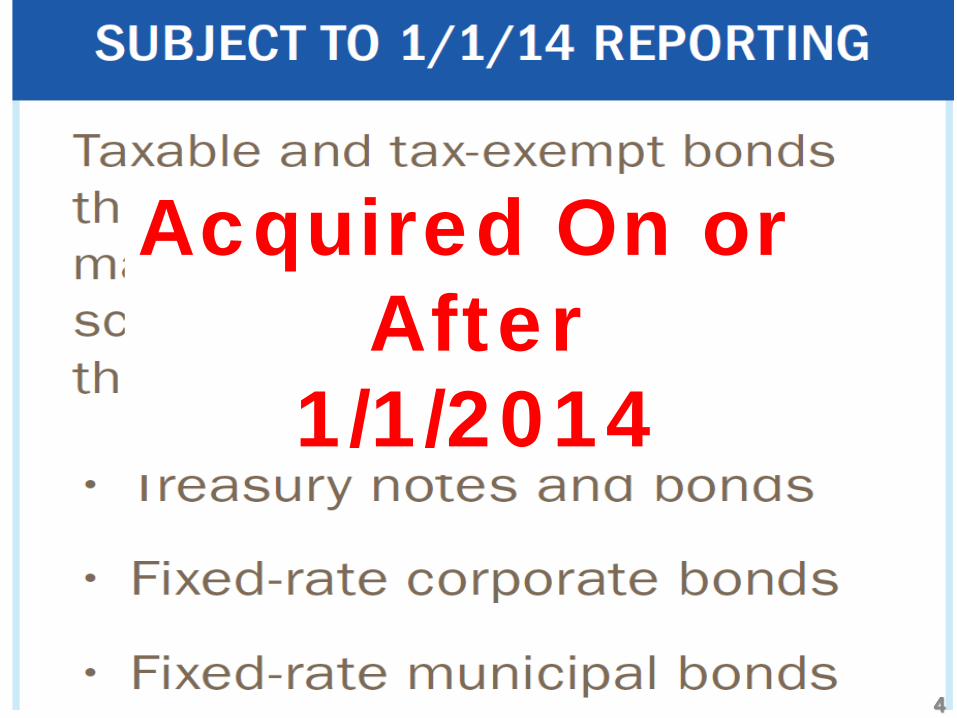

3

Acquired On or After

1/1/2014

4

5

The tax law default is no amortization

Taxpayer must affirmatively elect (all taxable bonds)

6

Failure to amortize bond premium means a higher

bond basis and a capital loss at

maturity 7

IRS Pub 550

8

IRS Pub 550

9

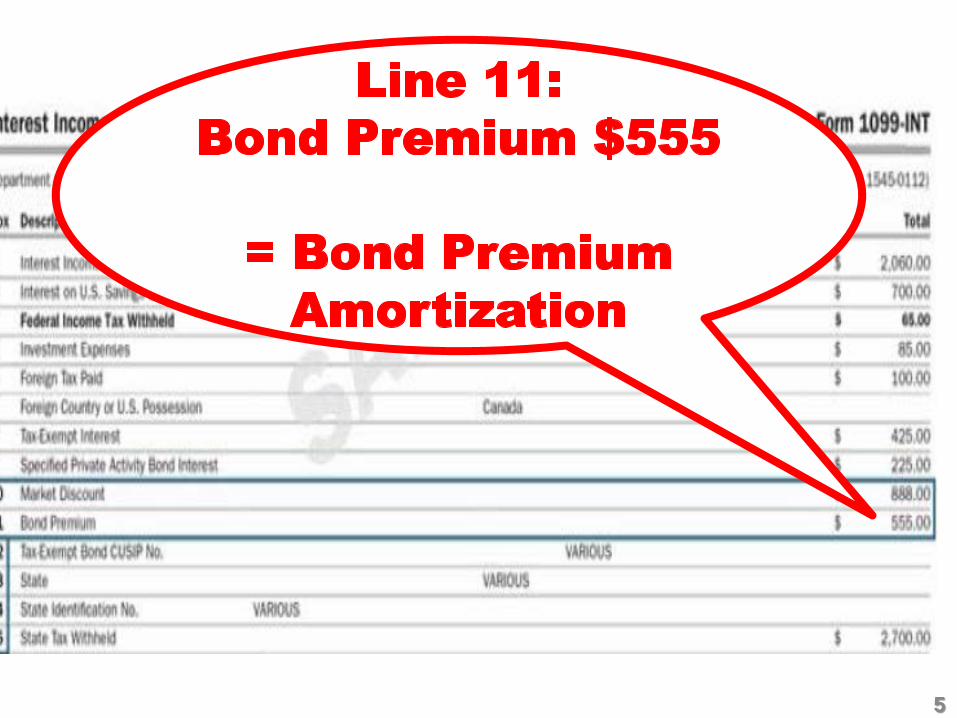

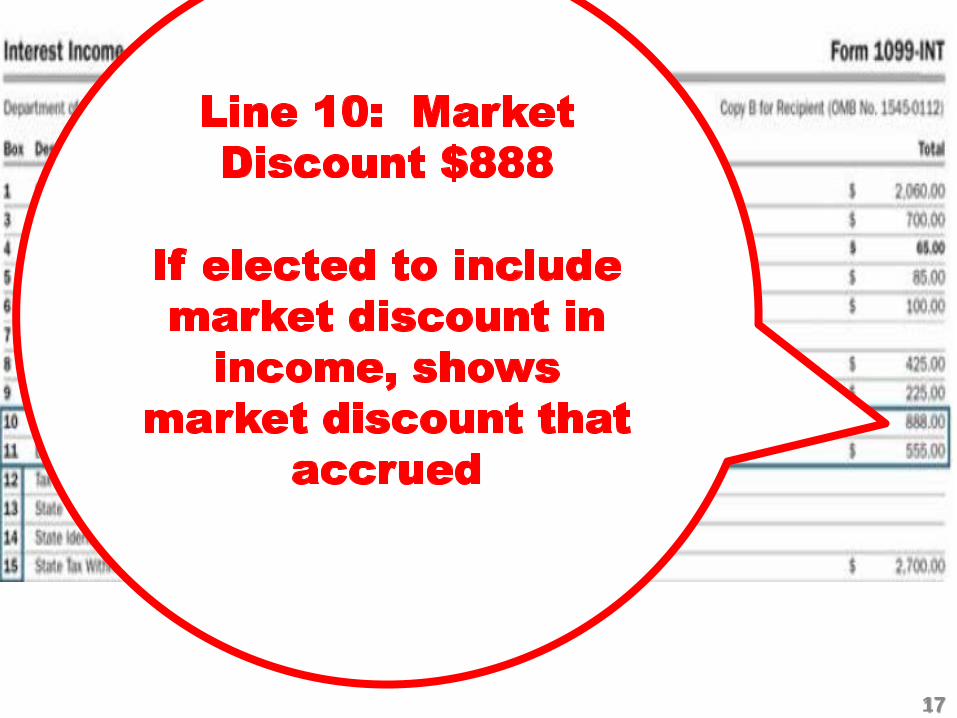

10

11

12

The tax law default is no annual

income/accrual for market discount

Taxpapayer can affirmatively elect

(bond by bond) 13

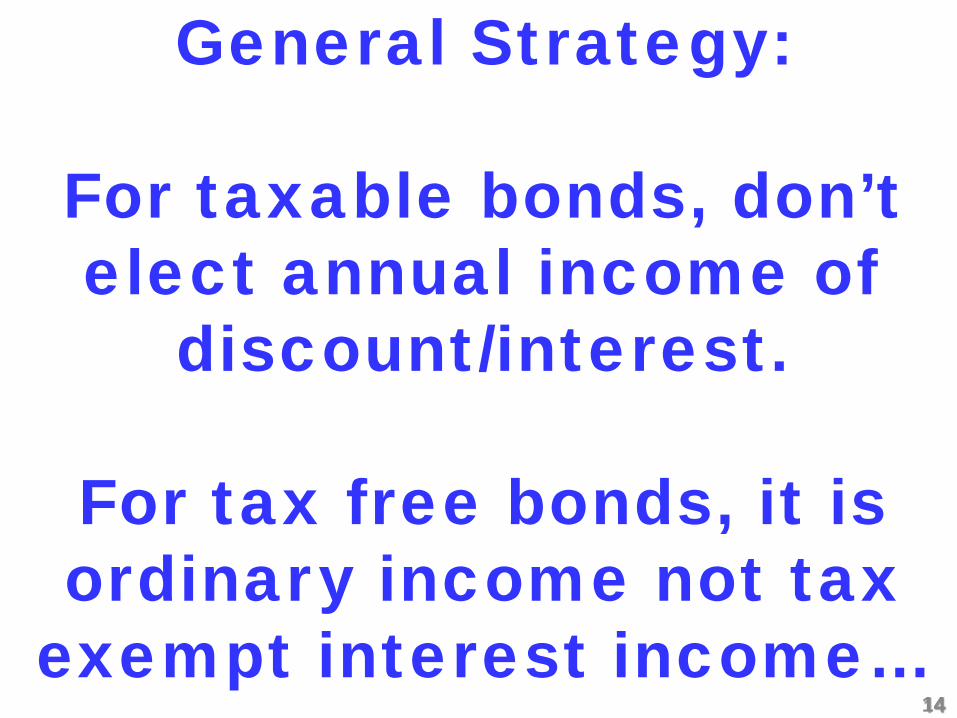

General Strategy:

For taxable bonds, don’t elect annual income of

discount/interest.

For tax free bonds, it is ordinary income not tax

exempt interest income… 14

If no election, then recognize accrued market discount as

interest at maturity or on disposition.

15

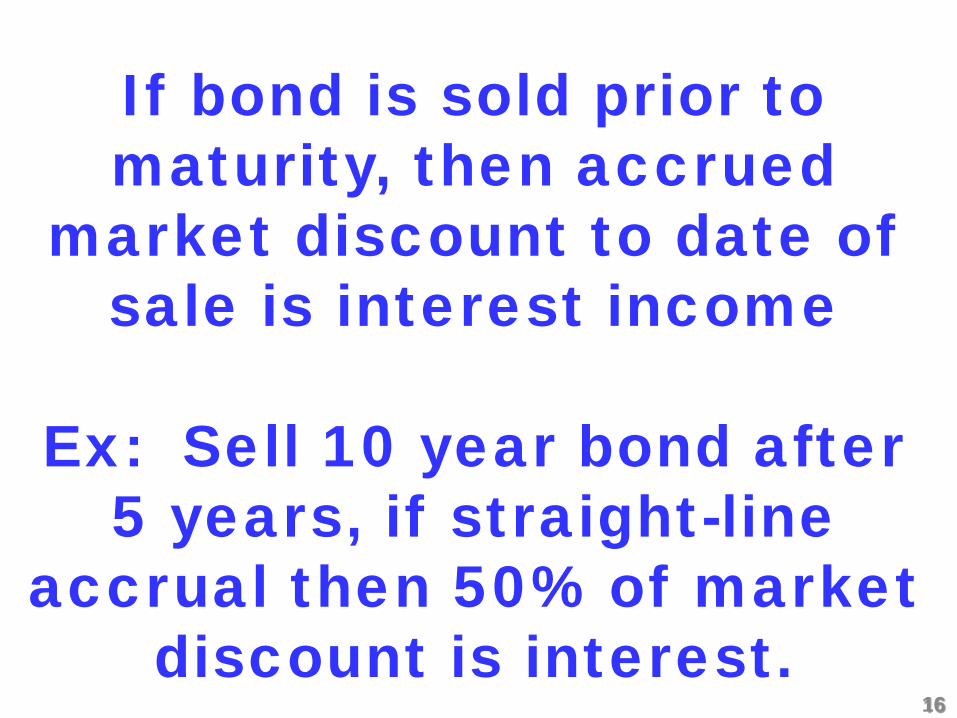

If bond is sold prior to maturity, then accrued

market discount to date of sale is interest income

Ex: Sell 10 year bond after 5 years, if straight-line

accrual then 50% of market discount is interest.

16

17

Broker may include net interest in Form

1099 Int box 1 instead of showing

gross interest in box 1 and market

discount. 18

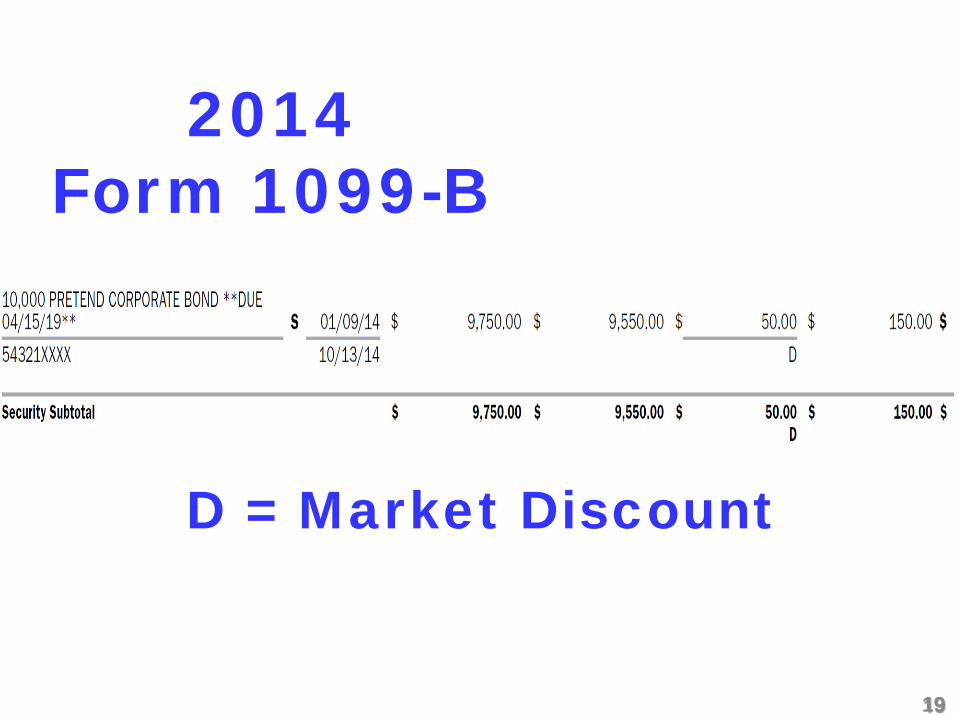

2014Form 1099-B

D = Market Discount

19

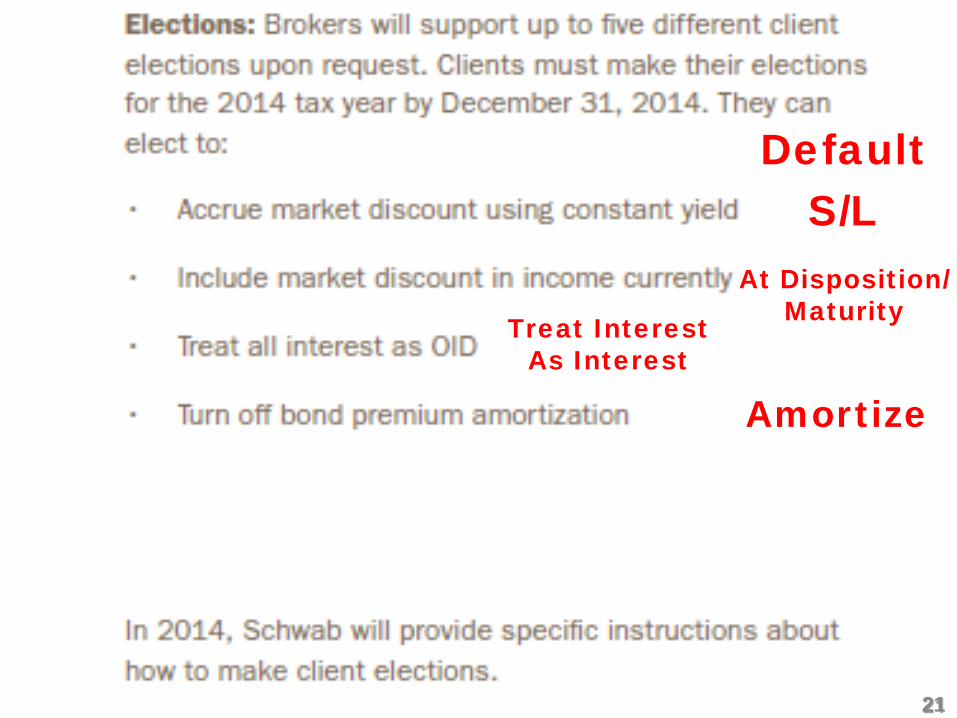

DefaultS/L

At Disposition/MaturityTreat Interest

As Interest

Amortize

21

22

Cooper143 TC No. 10

Patent Holder's Control of Corporate Transferee Eliminates Long-Term

Capital Gain Treatment

6-4

23

T.D. 9659; Reg. § 1.83-3 (02/25/2014)

Final Regs Tighten Deferral Rules Involving Receipt of

Property with Substantial Risk of Forfeiture – See Examples

6-4

24

The only provision of the securities law that defers income under IRC sec. 83

is section 16(b) of theSecurities Exchange Act

25

• Section 16(b) causes disgorgement of insider profits on all purchases and sales within six months;

• With stock options, the six month clock begins on the date the option is granted.

26

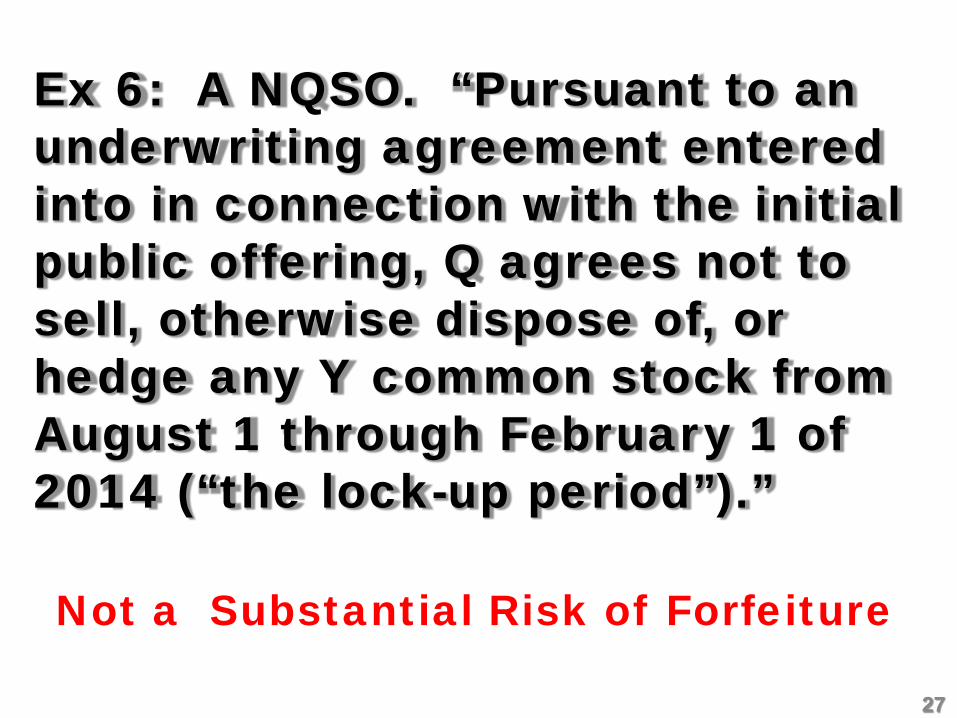

Ex 6: A NQSO. “Pursuant to an underwriting agreement entered into in connection with the initial public offering, Q agrees not to sell, otherwise dispose of, or hedge any Y common stock from August 1 through February 1 of 2014 (“the lock-up period”).”

Not a Substantial Risk of Forfeiture

27

Ex 7: NQSO. “The exercise of the option occurs … and, on the date of exercise, Q is in possession of material nonpublic information concerning Y that would subject him to liability under Rule 10b–5 under the Securities Exchange Act of 1934 if Q sold the Y shares while in possession of such information.”

Not a Substantial Risk of Forfeiture28

Brinkley, TC Memo 2014-227

(Oct. 30, 2014) –

Tech Company Co-Founder Has Mostly Ordinary Income When

Company is Acquired by Google

6-7

29

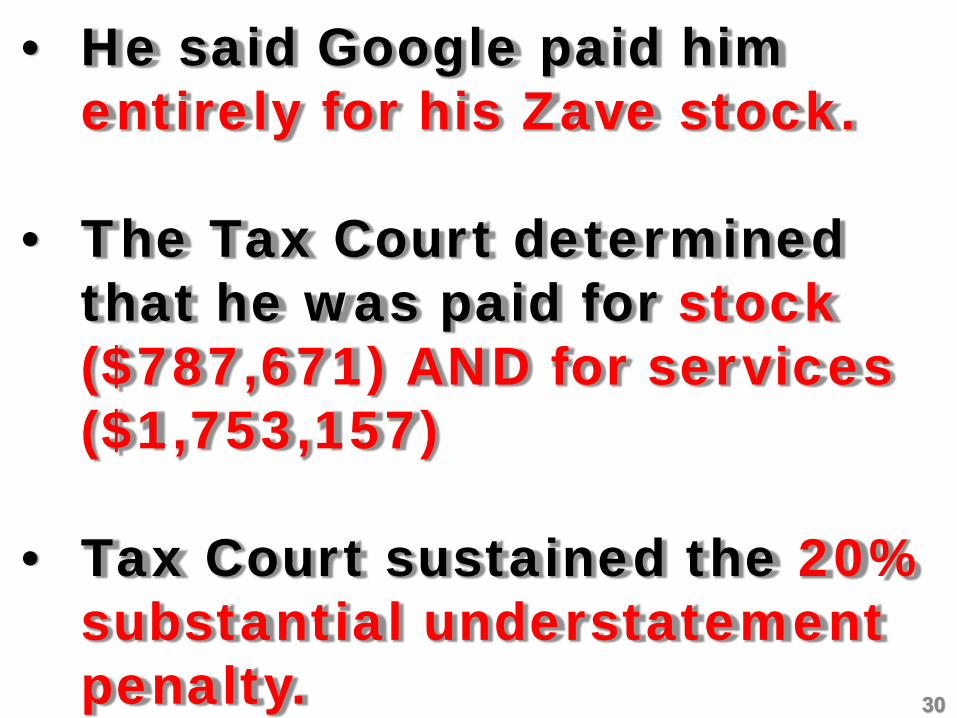

• He said Google paid him entirely for his Zave stock.

• The Tax Court determined that he was paid for stock ($787,671) AND for services ($1,753,157)

• Tax Court sustained the 20% substantial understatement penalty. 30

Pool, TC Memo 2014-3 (1/8/14)

Developer is a Dealer Not an Investor in

Real Estate

6-8

31

Frederic Allen v. U.S., (DC CA 05/28/14)

California District Court Holds Land Sale Triggered

Ordinary Income, Not Capital Gain – Intent to

Develop Not Hold

6-8

32

Long v. Comm’r(CA 11 Nov. 20, 2014)

Developer Entitled to Long-Term Capital Gain

on Sale of Right to Purchase Real Estate

Supp

33

Patrick, 142 TC No. 5 (2/24/14)

$6,856,000 on Form 1099-MISC for

Whistleblower Award is Ordinary Income Not

Capital Gain

6-9

34

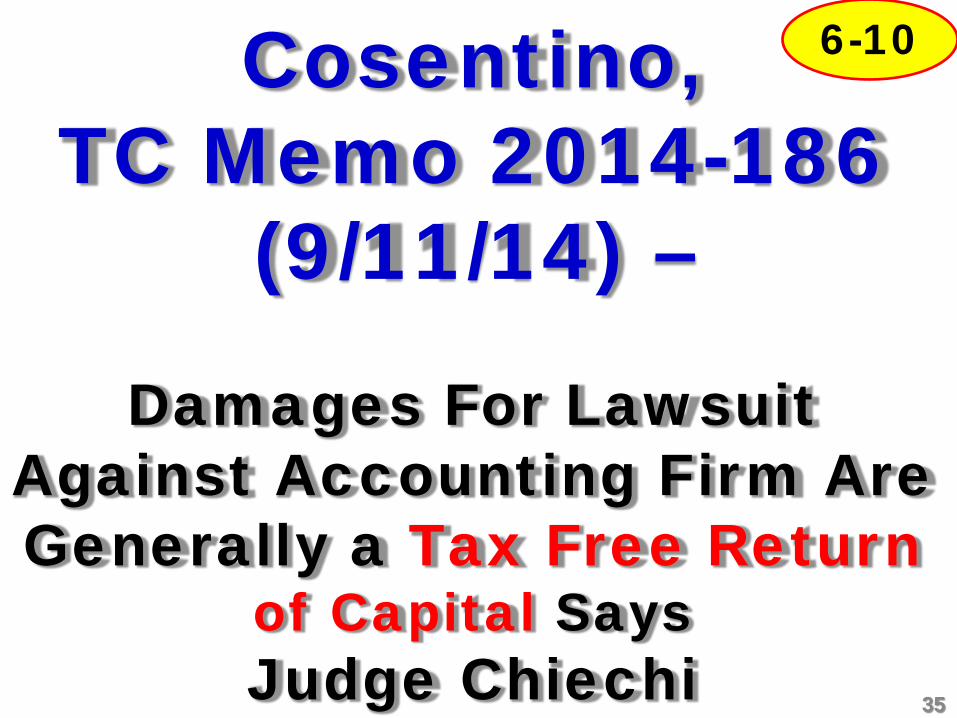

Cosentino, TC Memo 2014-186

(9/11/14) –

Damages For Lawsuit Against Accounting Firm Are Generally a Tax Free Return

of Capital SaysJudge Chiechi

6-10

35

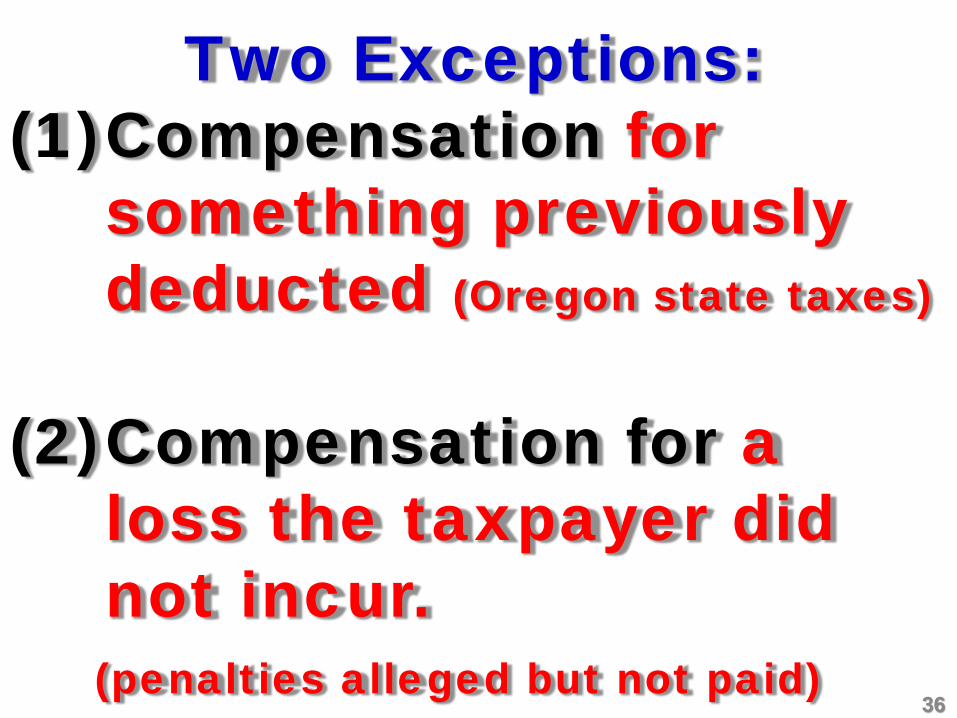

Two Exceptions:(1)Compensation for

something previously deducted (Oregon state taxes)

(2)Compensation for a loss the taxpayer did not incur. (penalties alleged but not paid)

36

Ann Carrino, T.C. Memo. 2014-34

(February 25, 2014)

6-13

• In 2002, she separated from H, but H funded a partnership with community funds.

• In 2003, they remained married and filed MFS.

Holding: Whether or not Ann was considered a partner in 2003, she had income from the partnership in that year based on her community property interest in H’s partnership interest (IRC sec. 66).

• The Tax Court noted Ann's failure to argue for innocent-spouse relief in IRC sec. 66 on MFS returns.

• Innocent spouse relief in IRC sec. 66 is not available to California RDPs (unmarried) per IRS website Q&As.

1-23

What about employment tax on her half of the community income?

IRC sec. 1402(a)(5)(B) pushes 100% of community property income, for spouses, to the partner – H.If Ann is also a partner, then 50/50.

IRS website FAQ declares that

IRC sec. 1402(a)(5) does not apply to non-spouse RDPs.

1-28

IRS Information Letter

2014-0018 (June 2014) -- Mortgage

Forgiveness in California; Boxer Letter Version 2.0

6-16

43

Backgroundon

NonrecourseDebt With

Short Sales44

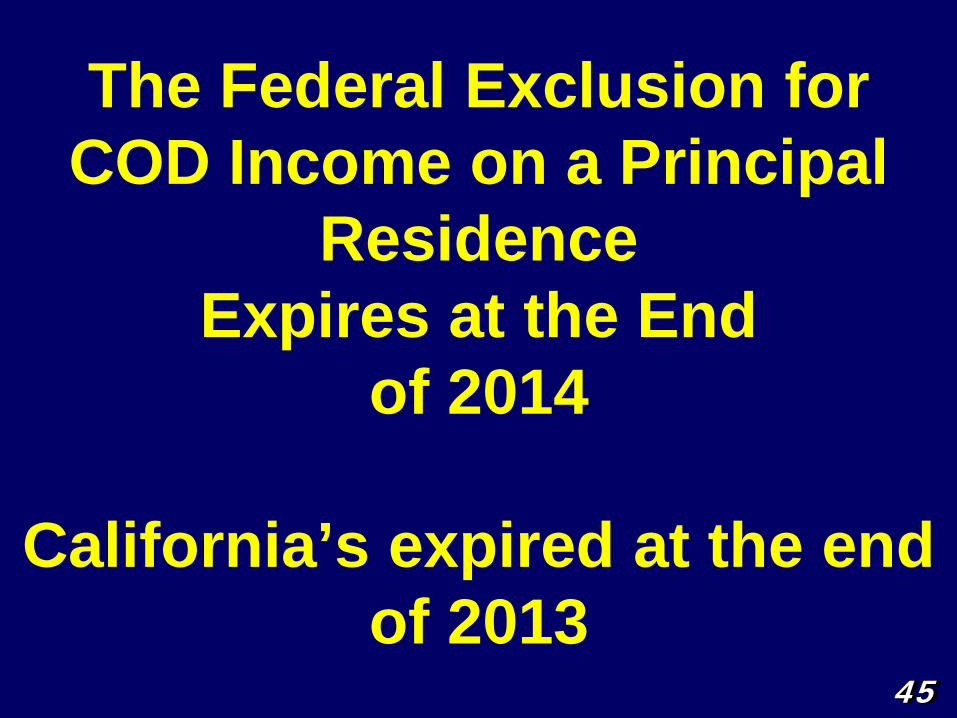

The Federal Exclusion for COD Income on a Principal

ResidenceExpires at the End

of 2014

California’s expired at the end of 2013

45

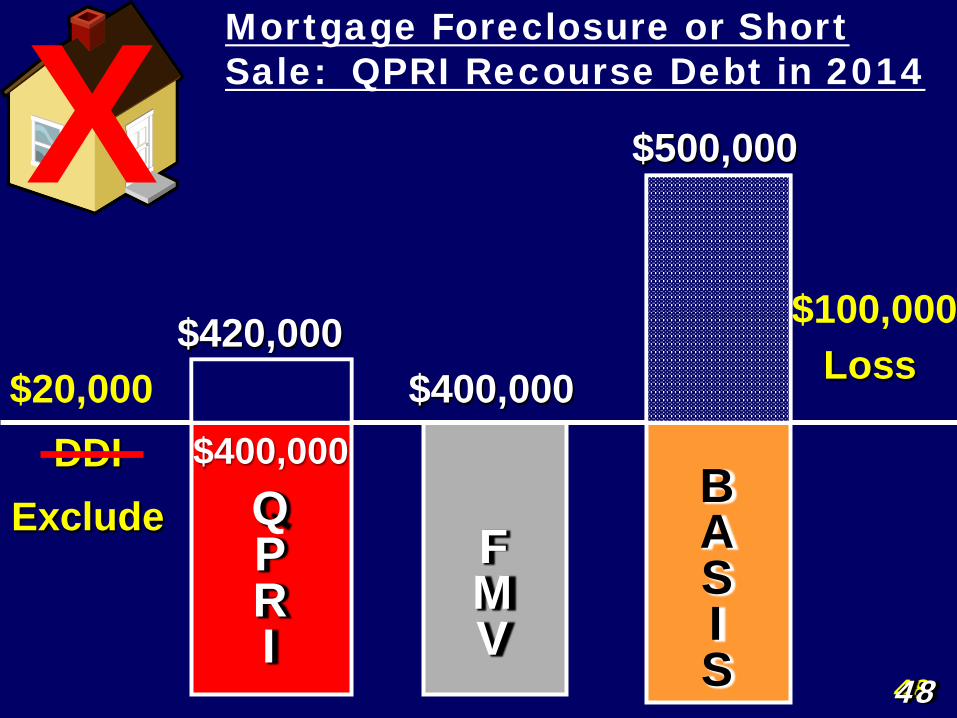

48

QPRI

FMV

BASIS

$500,000

$400,000$420,000

$20,000DDI

Exclude

Mortgage Foreclosure or Short Sale: QPRI Recourse Debt in 2014X

$100,000Loss

$400,000

48

49

QPRI

FMV

BASIS

$500,000

$400,000$420,000

$20,000COD

Income

Mortgage Foreclosure or Short Sale: QPRI Recourse Debt in 2015X

$100,000Loss

$400,000

49

If the QPRI COD Exclusion is Not Extended to

2015….Nonrecourse debt is

the only escape route

50

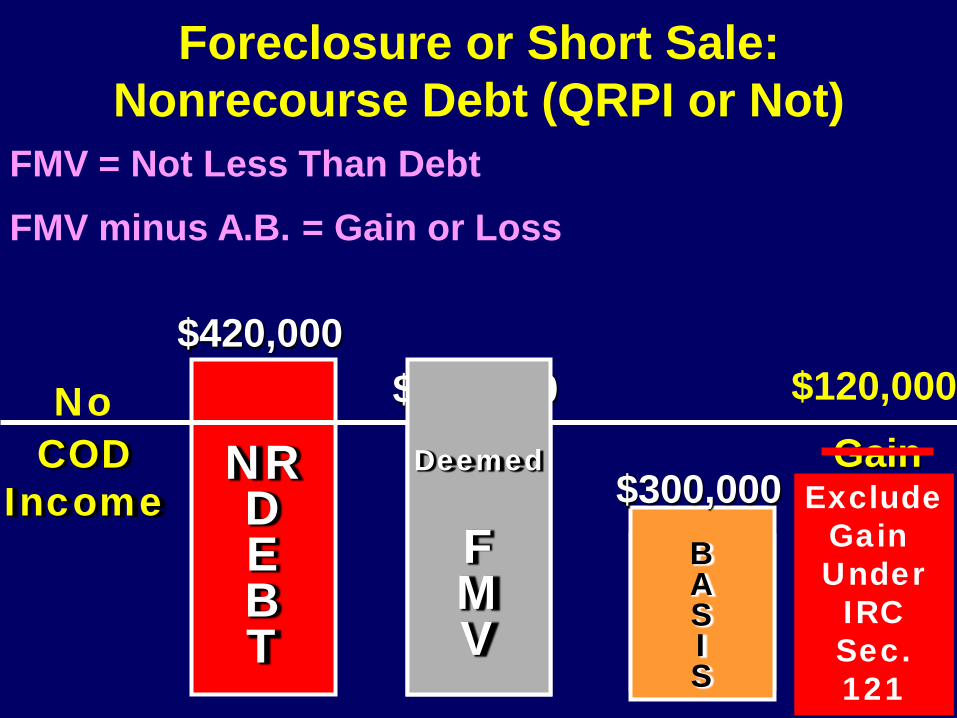

7701(g), provides that “in determining the amount of gain or loss … the fair market value of such property shall be treated as being not less than the amount of any nonrecourse indebtedness to which such property is subject.”

Foreclosure or Short-Sale With Nonrecourse Debt

51

No COD income with nonrecourse debt on a foreclosure or short sale.

52

53

NRDEBT

FMV

BASIS

$500,000

$400,000$420,000

$80,000Loss

Foreclosure or Short Sale:Nonrecourse Debt (QRPI or Not)

Deemed

FMV

No COD

Income

53

FMV = Not Less Than DebtFMV minus A.B. = Gain or Loss

54

NRDEBT

FMV

BASIS

$300,000

$400,000$420,000

$120,000Gain

Foreclosure or Short Sale:Nonrecourse Debt (QRPI or Not)

Deemed

FMV

No COD

Income

54

FMV = Not Less Than DebtFMV minus A.B. = Gain or Loss

ExcludeGain Under

IRCSec.121

• CCP 580e debt is nonrecourse debt so a short-sale results in gain or loss not COD income.

• FTB quickly agreed.

Boxer Letter V1(9/19/13) 6-16

55

California CCP 580eFor short-sales after July 5, 2011, CCP §580e provides

that if the lender consents toa short sale the lender

cannot pursue the borrower for any excess debt over the

sales proceeds.

56

• The property needs to be a dwelling unit of 1 to 4 units (so no good for commercial property)

• Does not require owner occupancy, so it applies to a residential rental.

57

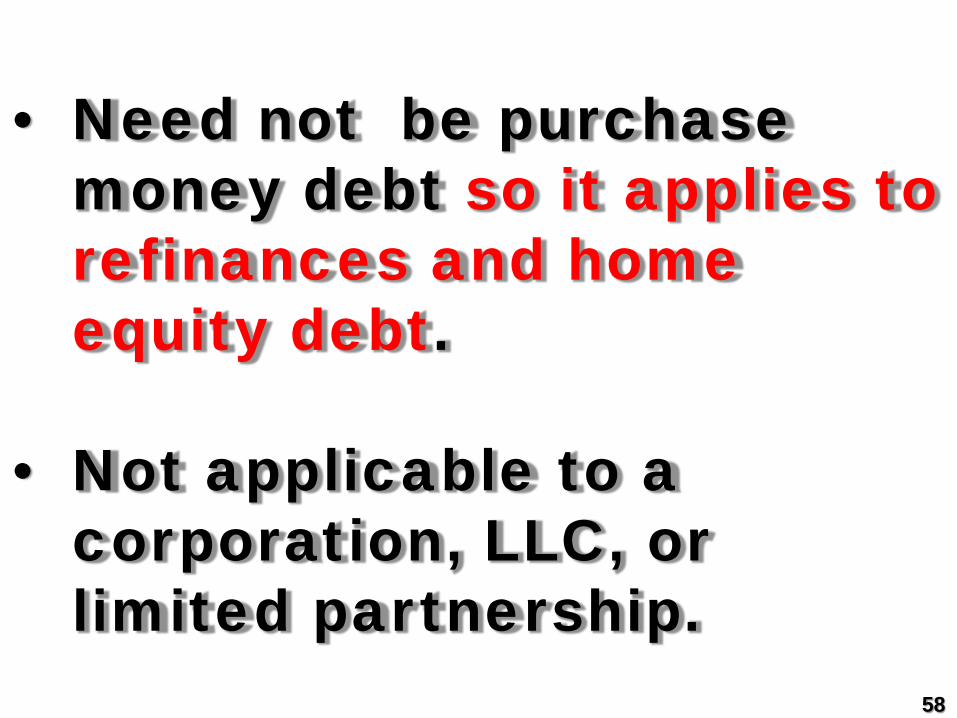

• Need not be purchase money debt so it applies to refinances and home equity debt.

• Not applicable to a corporation, LLC, or limited partnership.

58

So 580(e) debt can start out recourse debt

and flip to nonrecourse on the short sale.

59

• Please Ignore Version 1

• It was OVERLY BROAD

Boxer Letter V2: April 2014

60

CCP 580b(a)(3) purchase money debt on

an owner-occupied residence, NR debt from

the start, generates gain or loss but no COD

income.

What We Mean’t To Say

61

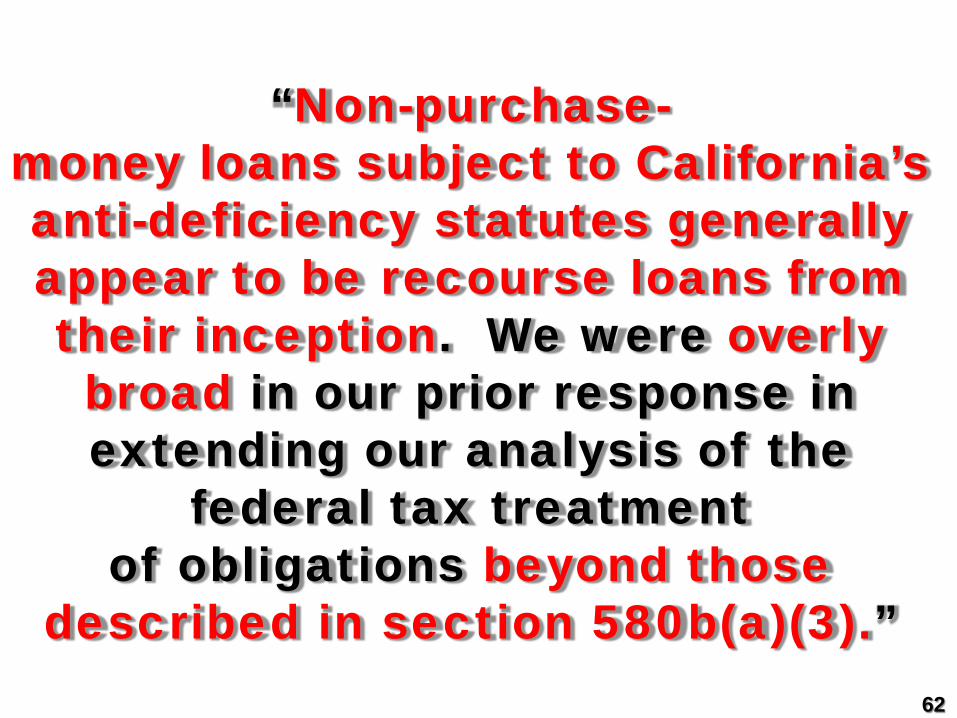

“Non-purchase-money loans subject to California’s anti-deficiency statutes generally appear to be recourse loans from their inception. We were overly broad in our prior response in extending our analysis of the

federal tax treatmentof obligations beyond those

described in section 580b(a)(3).” 62

NeitherLetter

Is Legal Authority

64

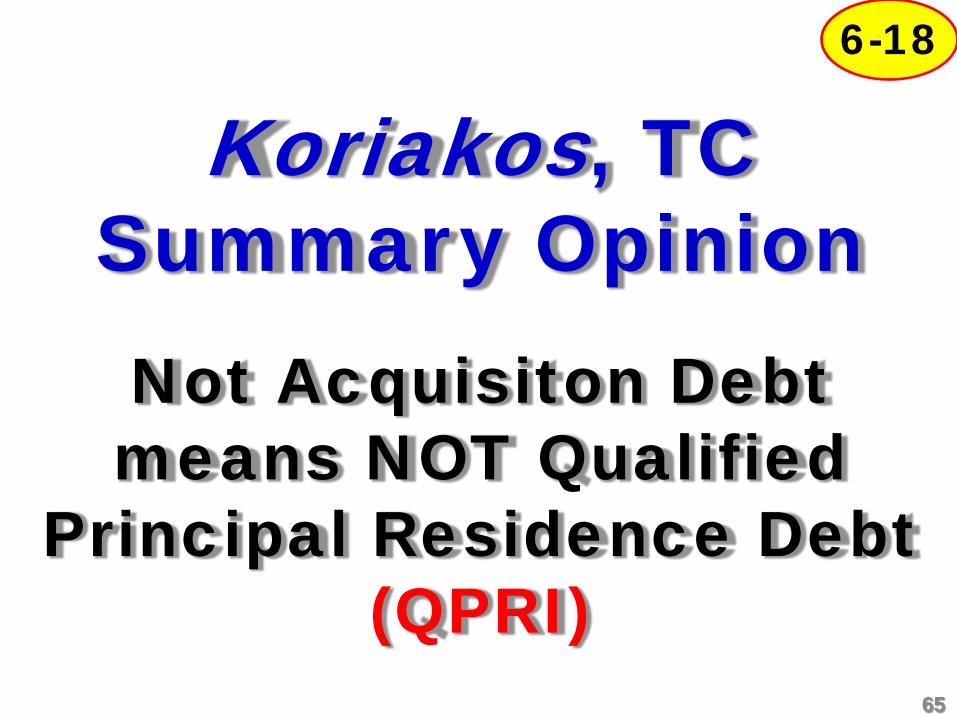

Koriakos, TC Summary Opinion Not Acquisiton Debt means NOT Qualified

Principal Residence Debt(QPRI)

6-18

65

Couple used the debt to construct property

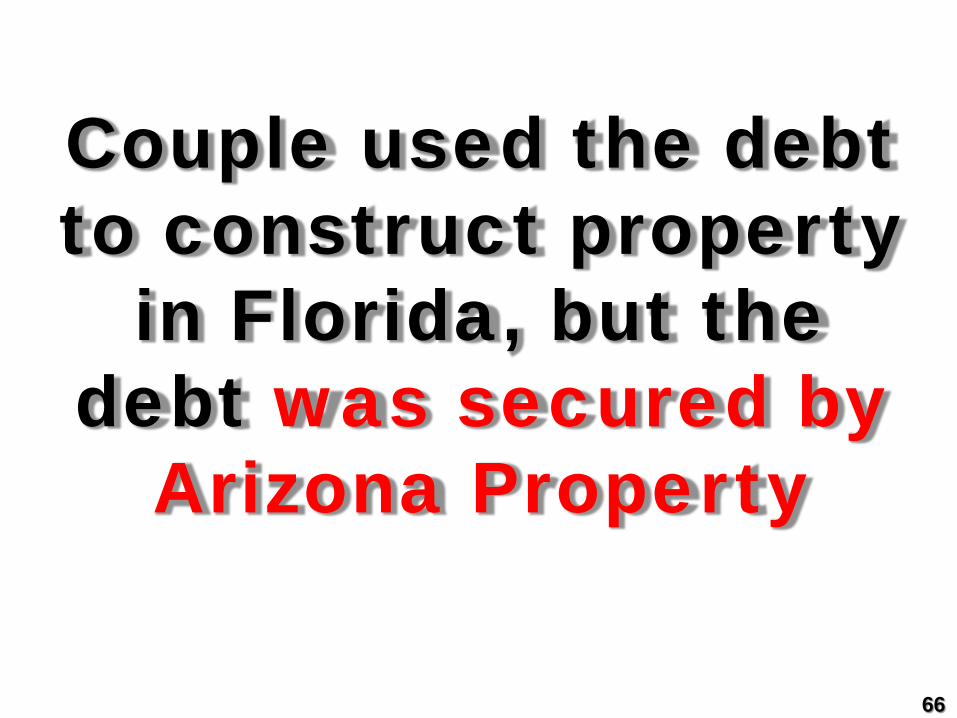

in Florida, but the debt was secured by

Arizona Property

66

Debough, 142 TC No. 17

Reacquisition of Principal Residence Eliminates Exclusion

6-20

67

• Debough sells his residence for $1,400,000 on the installment method.

• After sec. 121 exclusion, he recognizes $60,000

68

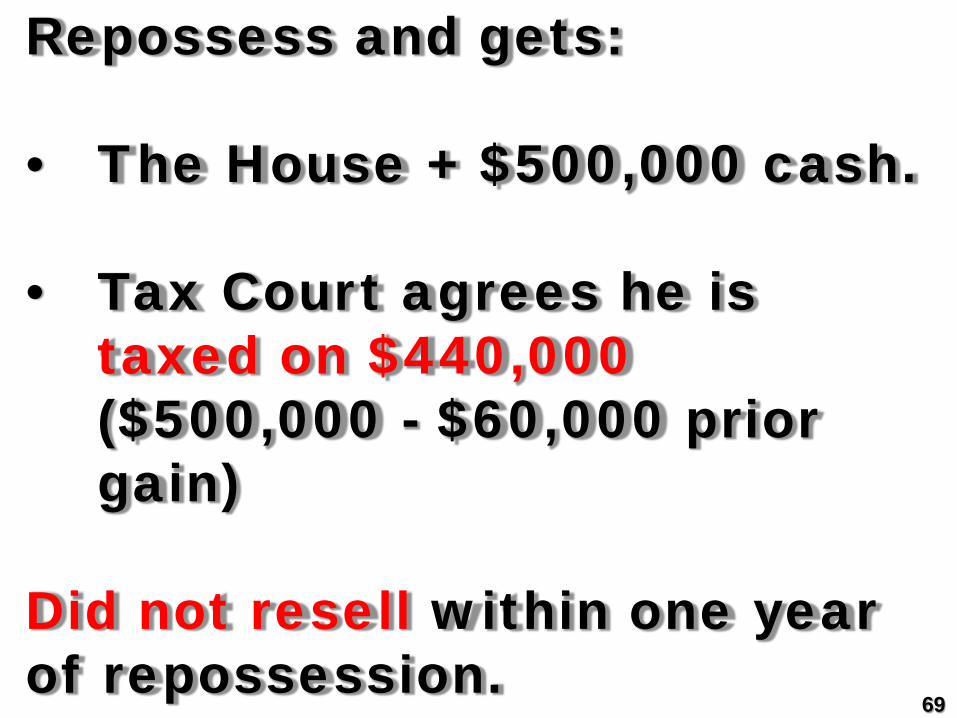

Repossess and gets:

• The House + $500,000 cash.

• Tax Court agrees he is taxed on $440,000 ($500,000 - $60,000 prior gain)

Did not resell within one year of repossession.

69

If he re-sold the house within one year of the repossession, he could have excluded the entire $440,000 gain under IRC sec. 121.

70

Blangiardo, TC Memo 2014-110

(6/9/14)

Son/Attorney Cannot Serve as a Qualified Intermediary

6-23

74

Notice 2014-68 (Oct. 24, 2014)

IRS Approves Leave-Sharing Programs to Help

West African Ebola Victims

6-24

75

Shankar, Bank’s “Thank You

Points” Converted to Free Airline

Ticket was Taxable

20

76

CompareIRS Announcement 2002-18: IRS grants audit protection for “the receipt or personal

use of frequent flyer miles or other in-kind promotional

benefits attributable to the taxpayer’s business or

official travel….”77

Information Letter 2014-0012

Treatment of Same-Sex Spouse Health Premiums Wrongly Included In W-2

Income

6-30

78