Embed Size (px)

Citation preview

ISSUE PAPER ERRA TARIFF/PRICING

COMMITTEE

2006

GREEN ENERGY PRICING

ERRA Köztársaság tér 7

Budapest 1081, Hungary http://www.erranet.org

Issue Paper on Green Energy Pricing

© ERRA 2006 1

This publication was prepared by the members of ERRA Tariff/Pricing

Committee:

Mr. Kastriot Sulka (Albania)

Mr. Armen Arshakyan (Armenia) Mr. Almir Imamovic (Bosnia and Herzegovina)

Commissioner Svetla Todorova (Bulgaria)

Commissioner Ivona Štritof (Croatia)

Ms. Klarika Siegel (Estonia)

Mr. Iveri Shalamberidze (Georgia)

Mr. Ede Treso (Hungary)

Mr. Anatoly Shkarupa (Kazakhstan) Mr. Djeksenbek Sydykov (Kyrgyz Republic)

Mr. Ainars Cunculis (Latvia)

Ms. Aistija Zubaviciute (Lithuania)

Ms. Evgenija Kiprovska (Macedonia)

Ms. Lidia Zestrea (Moldova)

Ms. Ganchimeg Mujaan (Mongolia) Mr. Branko Kotri (Montenegro) Mr. Tomasz Kowalak (Poland)

Mr. Adrian Borotea (Romania)

Mr. Maxim Peshkov (Russian Federation)

Mr. Çetin Kayabaş (Turkey)

Commissioner Yuriy Kyyashko (Ukraine)

This publication was made possible through support provided by the Energy and Infrastructure Division of the Bureau of Europe and Eurasia under the terms of its Cooperative Agreement with the National Association of Regulatory Utility Commissioners, No. EE-N-00-99-00001-00. The opinions expressed herein are those of the authors and do not necessarily reflect the views of the U.S. Agency for International Development or the National Association of Regulatory Utility Commissioners.

Issue Paper on Green Energy Pricing

© ERRA 2006 2

TABLE OF CONTENT

TABLE OF CONTENT...................................................................................................... 2 Green Energy Pricing.......................................................................................................... 3

1. Background ................................................................................................................. 3 2. European Directive on renewable energy ................................................................... 4

2.1. National targets .................................................................................................... 5 2.2. Support schemes .................................................................................................. 5 2.3. Guarantees of origin............................................................................................. 6 2.6. External costs and subsidies/Summary report on implementation ...................... 7

3. Green pricing .............................................................................................................. 8 3.1. History of green pricing ....................................................................................... 8 3.2. Policy mechanisms............................................................................................. 11 3.3. Feed-in pricing ................................................................................................... 13 3.4. Net metering system .......................................................................................... 15 3.5. Quota system...................................................................................................... 16 3.6. Comparison between the two major supporting systems................................... 20 3.7. Requirements for successful green pricing policy ............................................. 26 3.8. Importance of consistent, long-term policies..................................................... 27

4. Conclusions and Recommendations ......................................................................... 28 4.1. General ............................................................................................................... 28 4.2. Developing Countries ........................................................................................ 30

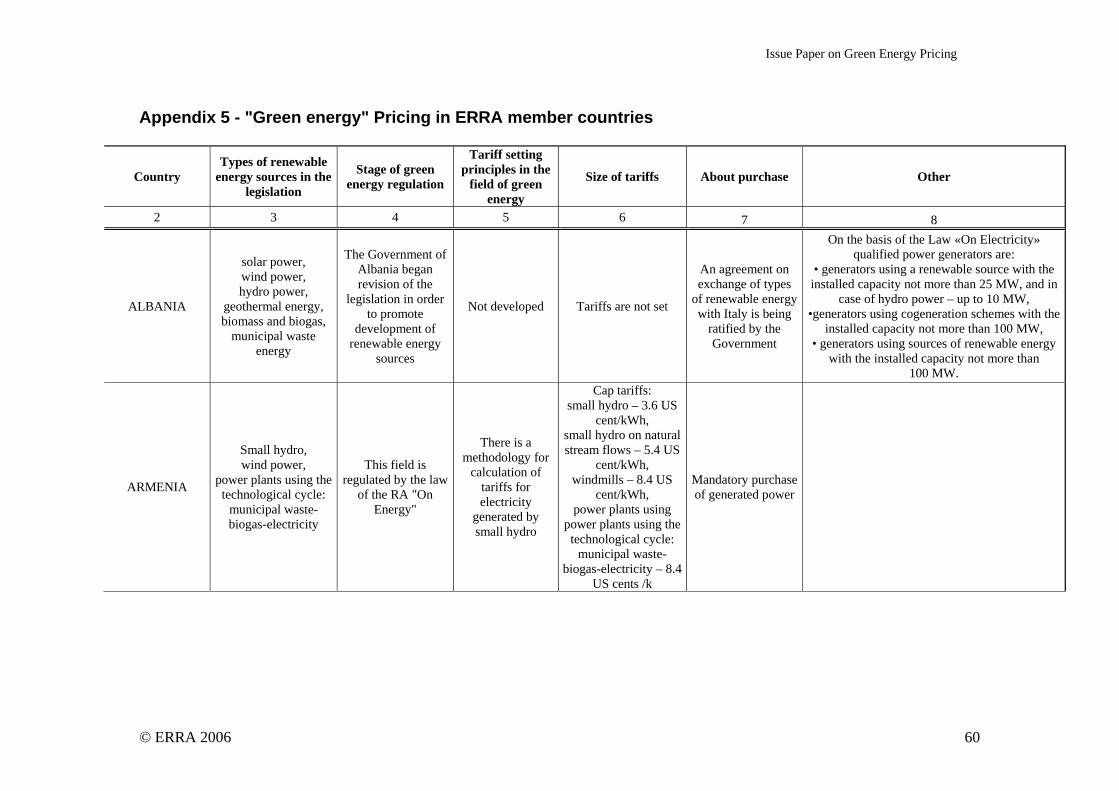

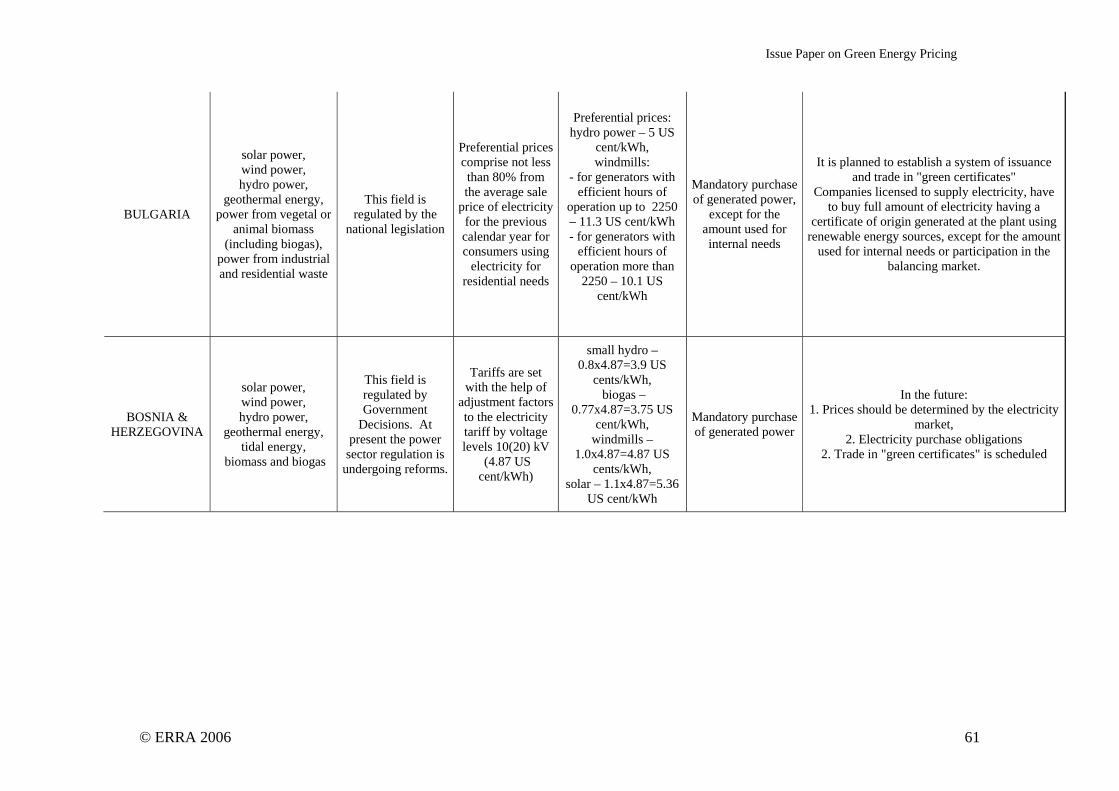

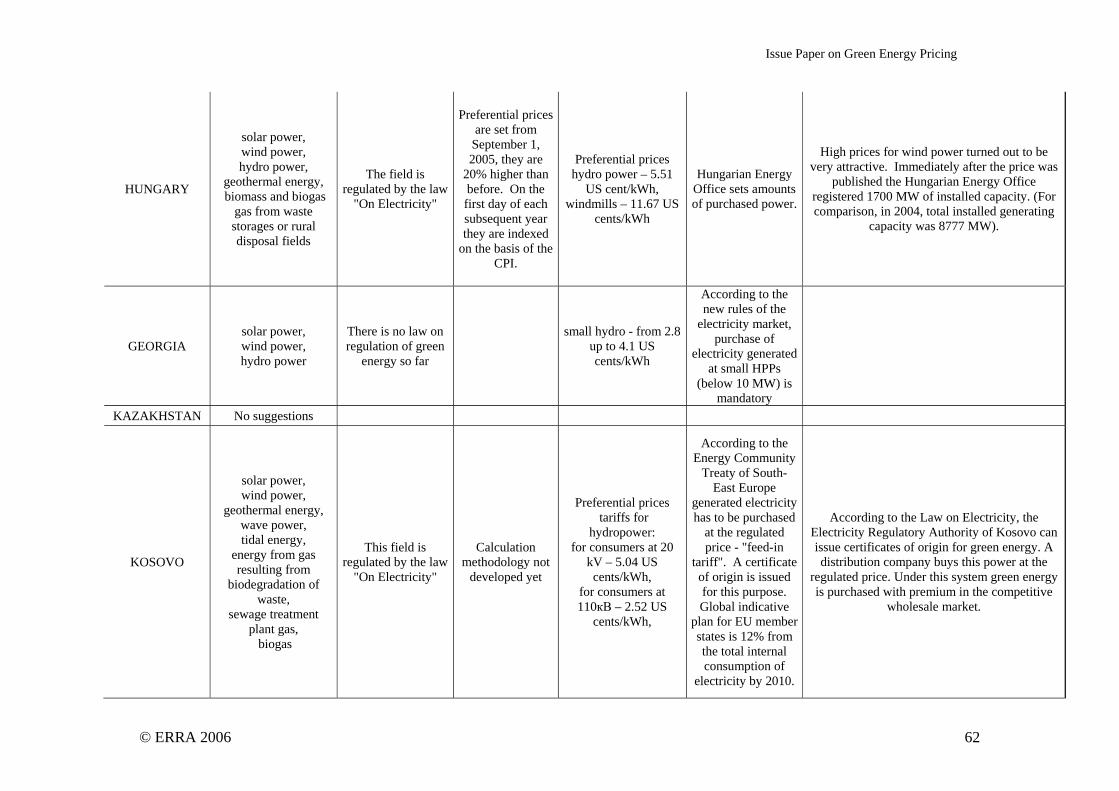

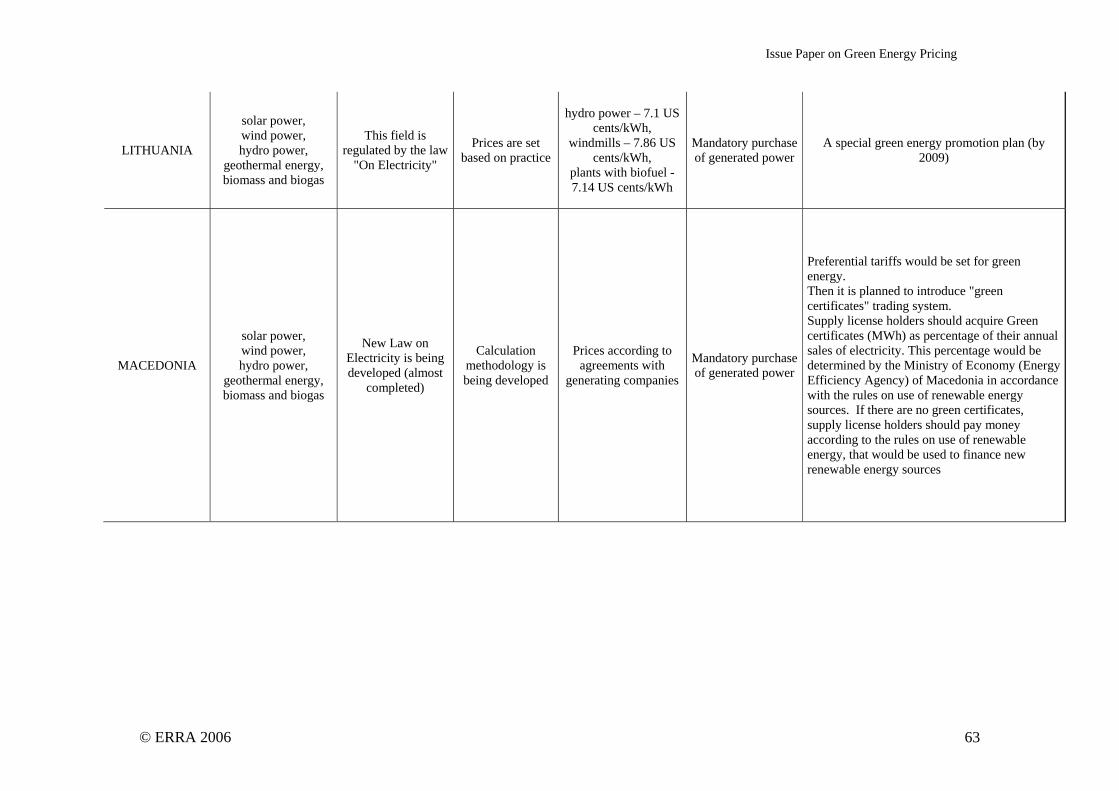

5. Green Energy Pricing in ERRA Member Countries................................................. 32 5.1. By Countries ...................................................................................................... 32 5.2. Benchmarking .................................................................................................... 44

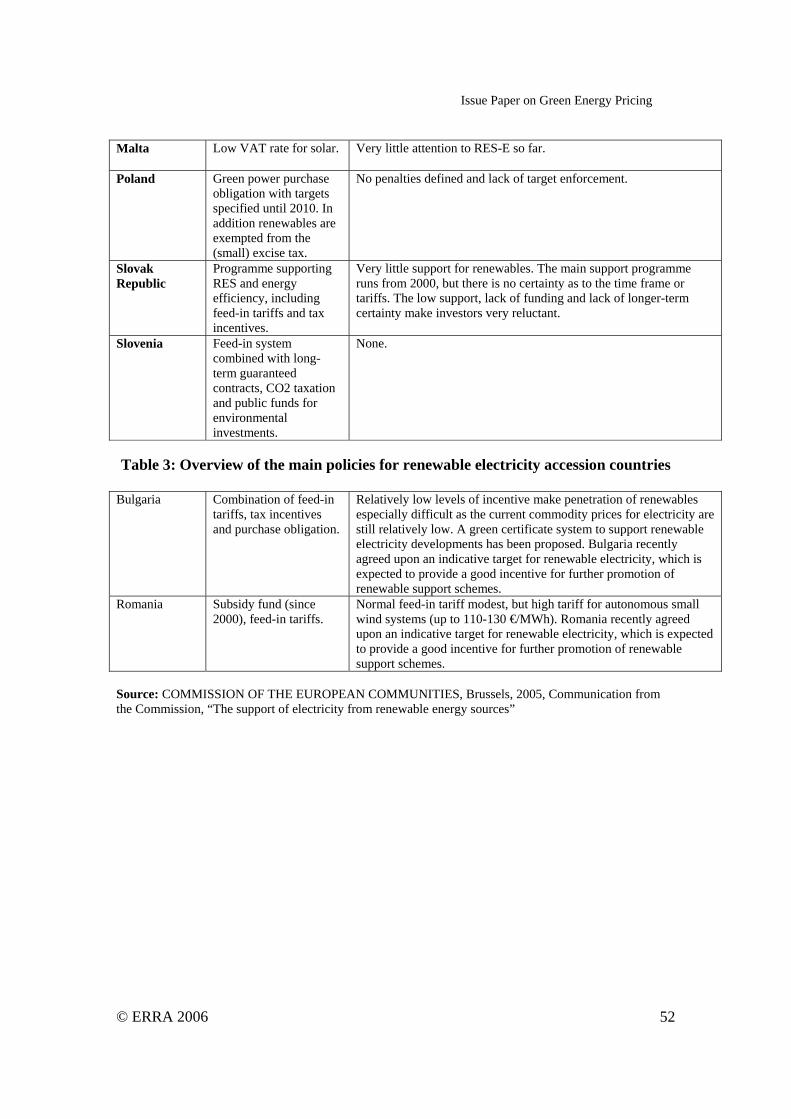

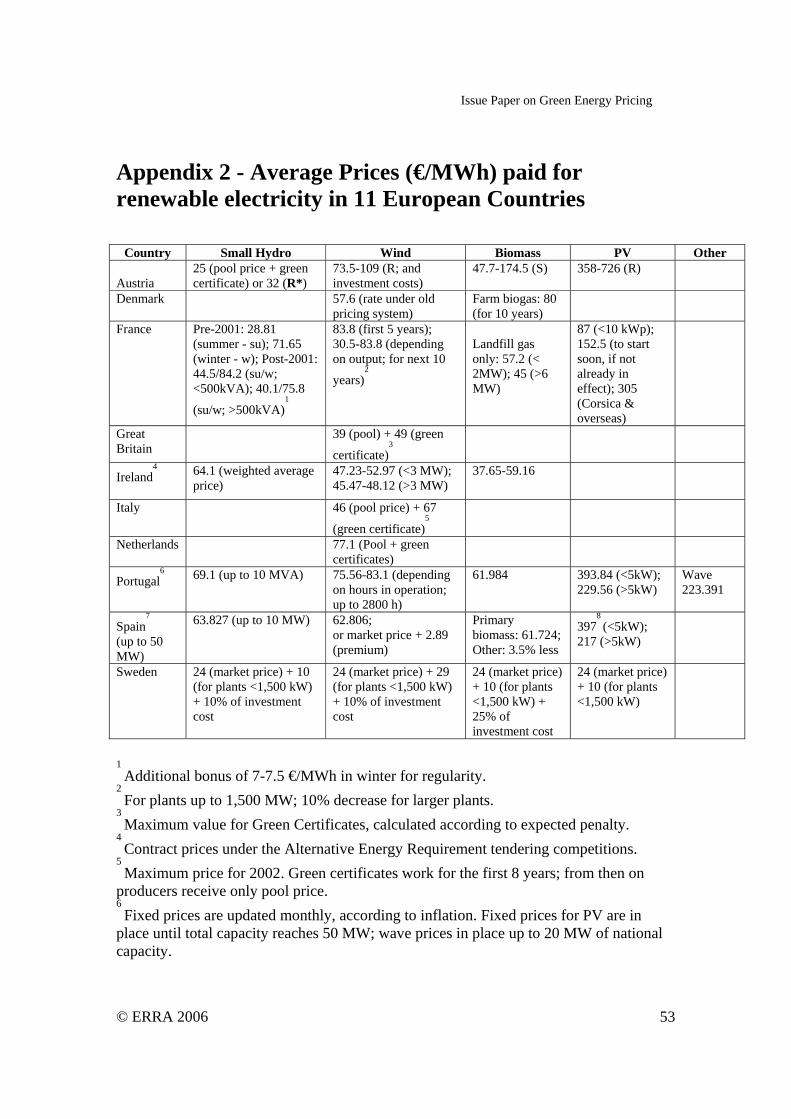

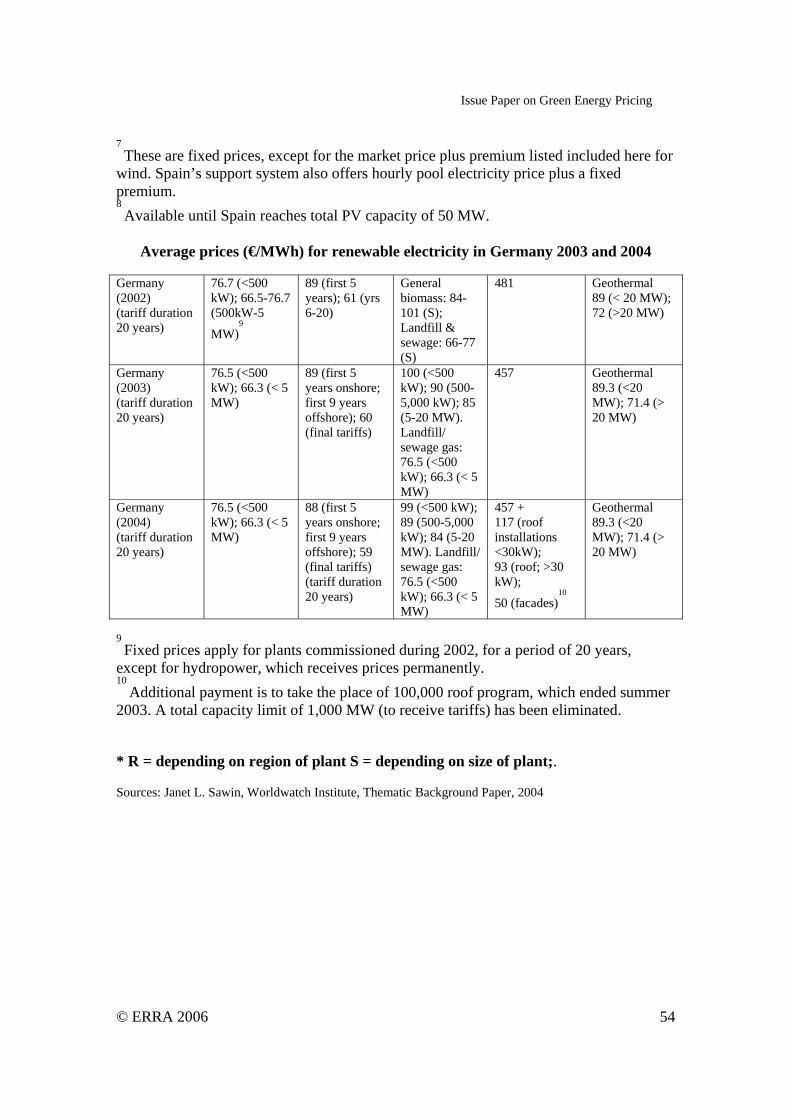

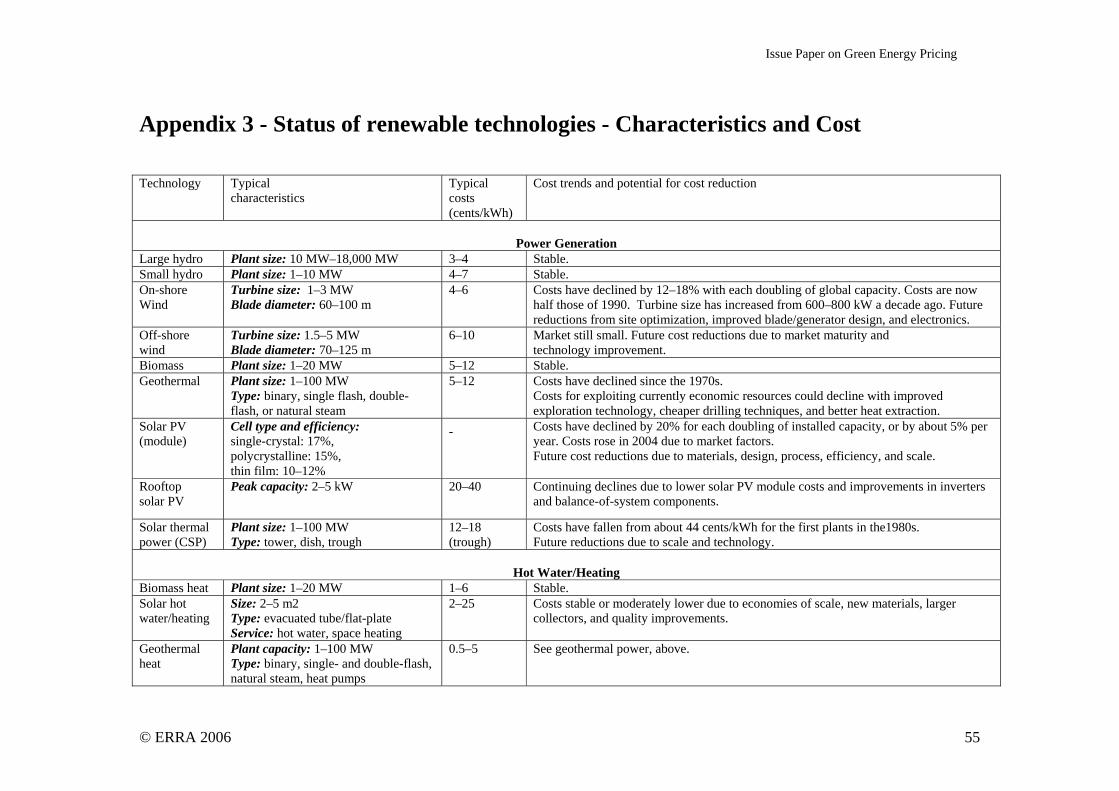

6. References................................................................................................................. 49 Appendix 1 - Current support systems.......................................................................... 50 Appendix 2 - Average Prices (€/MWh) paid for renewable electricity in 11 European Countries ....................................................................................................................... 53 Appendix 3 - Status of renewable technologies - Characteristics and Cost ................. 55

Appendix 4 - Renewable Energy Promotion Policies............................................... 57 Appendix 5 - "Green energy" Pricing in ERRA member countries ......................... 60

Issue Paper on Green Energy Pricing

© ERRA 2006 3

Green Energy Pricing Prepared by:

Ms. Svetla Todorova State Energy and Water Regulatory Commission (SEWRC) of Bulgaria, and

Mr. Armen Arshakyan Public Services Regulatory Commission of Armenia

1. Background It is widely known and accepted by experts that current levels of dependence on

fossil fuels are unsustainable. The main driving forces that necessitate a change in our energy consumption patterns include natural resource depletion, climate change, a need for security of supply, lack of access to basic energy services by one third of the world’s population and the predicted economic growth of emerging markets, especially in the BRIC countries1.

Regardless that "greenhouse theory'' is not accepted by all scientists2, most of the

literate world today regards global warming as both real and dangerous. The transition to a sustainable global energy system is one of the largest challenges to face mankind in the present century. Increased electricity generation from renewable energy sources (RES) contributes substantially to the easing of geo-, climate- and energy-political areas of conflict and should therefore be prioritized at all levels - local, national and global.

The European Union has set an ambitious target of 21 % of RES in 2010, obliging

all member states to intensify efforts and reach the common objective. The European Commission’s report entitled “The share of renewable energy in the EU” concludes however that: “Only a few member states have until now implemented an attractive framework for renewable energy sources. In view of the meager results so far the Commission calls on member states to ensure the fulfillment of the 2010 targets by the implementation of appropriate measures”.

During the past decade, the world has witnessed double-digit growth in the wind

and photovoltaic (PV) industries, significant advances in these technologies, and dramatic cost reductions. Today half a dozen countries represent roughly 80 percent of the world market for these technologies. Those countries have demonstrated that it is possible to

1 BRIC is a term used to refer to the combination of Brazil, Russia, India, and China. General consensus is that the term was first prominently used in the thesis of the Goldman Sachs investment bank. The main point of this 2003 paper was to argue that the economies of the BRICs are rapidly developing and by the year 2050 will eclipse most of the current richest countries of the world.

2 Richard S. Lindzen, Professor of Meteorology at the Massachusetts Institute of Technology “Global Warming: The Origin and Nature of the Alleged Scientific Consensus”

Issue Paper on Green Energy Pricing

© ERRA 2006 4

create vibrant markets for renewable energy and to do so very rapidly; but the record also shows that the renewable energy policies of most countries have been unsuccessful to date.

This paper gives an overview of the “green pricing history and examines which

policies have been most effective in promoting renewable energy around the world. It focuses also on the current practices in the South-East countries.

2. European Directive on renewable energy The idea of an internal market for energy appeared on the agenda of the European

Community in the mid-1980s with the Delors3 report and began to be transposed in the 1990s. Since that time, many directives have been adopted in this area, with the emphasis clearly on increasing competition; this process is far from being finished.

It is in this context that electricity from renewable energy sources appeared on the

agenda, partly because it was clear that renewable energy sources (RES) had little chance to develop under intensified competition and therefore needed a special regime, partly because climate change as well as considerations of security of supply – i.e. growing import dependence on fossil energy resources in the first decades of the 21

st century –

made it desirable to merge and harmonize national support policies which already existed in quite a few member states.

After defining renewable energy sources the directive sets national indicative

targets for the consumption of RES by 2010, lays down some principles for national support systems and provides for a guarantee of origin of RES-electricity. It requires member states to introduce simplified, transparent and non-discriminatory administrative and grid practices. Finally, it provides for a report on implementation referring to external costs.

The directive defines renewable energy sources as “non-fossil energy sources

(“wind, solar, geothermal, wave, tidal, hydropower, biomass, landfill gas, sewage treatment plant gas and biogases”). The original Commission proposal (2000) limited hydro to 10 MW; later this provision was eliminated. Biomass is further specified to mean “the biodegradable fraction of products, waste and residues from agriculture (including vegetal and animal substances), forestry and related industries, as well as the biodegradable fraction of industrial and municipal waste”. This was included upon the 3 Jacques Lucien Jean Delors (born July 20, 1925 in Paris) is a French economist and politician, the only person who served two terms as President of the European Commission (1985 - 1995). Delors became the President of the European Commission in 1985. During his presidency, he oversaw important budgetary reforms and laid the groundwork for the introduction of a single market within the European Community, which came into effect on January 1, 1993.

Issue Paper on Green Energy Pricing

© ERRA 2006 5

insistence of the Dutch, British, Italian and Spanish governments against the opposition of both Commission and Parliament. The proportion of electricity produced by renewable energy sources in such plants may now also be considered as RES if the waste treatment hierarchy is respected.

2.1. National targets Historically, national commitments to renewable energy varied greatly with the

vagaries of the oil market. Crash programs in the 1970s and early 80s were generally followed by a decline in activities following the oil price decrease in 1986. The progress of renewable energy technologies also differed significantly among member states; breakthroughs were rare and incomplete. One of the ideas of the green and white papers on renewable energy sources was to reduce the costs of these technologies by achieving mass production on a European level (reinforced by exports once leadership was reached in this area); this in turn required a Community-wide effort. To achieve this effect, mandatory targets were seen as an appropriate instrument. This case was argued with great perseverance by the European Parliament. On the other hand, nearly all member states were unwilling to accept such targets (Denmark and later on Germany were the only exceptions).

Art. 3 of the directive proposes only indicative targets, with member states required

to “take the appropriate steps ... in proportion to the objective to be attained” and to document their efforts in regular reports (no later than 27 Oct 2003, the date by which the directive is to be transposed into national law, and thereafter every two years) which the Commission shall evaluate. If member states fail to live up to their targets without valid reasons, the Commission shall make appropriate proposals which may include mandatory targets.

The table in Annex 1 represents reference values for Member States’ national

indicative targets for the contribution of electricity from renewable energy sources to gross electricity consumption by 2010.

2.2. Support schemes

Besides the issue of targets, this was one of the most hotly contested provisions of the directive. At first, it was planned to progressively liberalize the area of RES in order to arrive at a community-wide harmonized regime fairly soon. It was also a conflict over renewable energy certificates combined with quotas versus fixed feed-in tariffs. The first draft proposals submitted by commissioner Christos Papoutsis 4 made clear that only support schemes which relied on “competition” were judged compatible with electricity liberalization. This referred to the tendering systems practiced at that time in some member states and ignored that there is competition also under fixed feed-in tariffs. These

4 Energy commissioner, representative of Greece

Issue Paper on Green Energy Pricing

© ERRA 2006 6

tendering schemes consisted in prospective RES-generators submitting competitive bids for fixed-price contracts. Such a system was practiced in Britain (where the NFFO5 system was no great success in expanding production of RES), France (where results were simply dismal) and Ireland (where this system still exists). Britain and France in particular had low rate of completion of accepted projects, even though they dispose of the best wind resources in the EU. This contrasted with the successful market introduction of RES achieved by those states which relied on fixed feed-in tariffs, i.e. Denmark, Germany and Spain, responsible for about 80-90 percent of wind power installations in the EU.

Later on, Papoutsis seems to have favored a quota/tradable certificate approach.

Under such an approach, generators of RES-electricity would sell, on the one hand, the physical electricity they produced; on the other, they would sell certificates embodying the “greenness” of that electricity, which could then be traded on an exchange so that a market price would result. This in turn would promote trade of RES-electricity within the EU, encourage its development in those regions where conditions were most favorable and thus reduce costs. At the time the directive was discussed, such a system was favored by Denmark, the Netherlands, the United Kingdom, Italy and the Flemish part of Belgium; it also had supporters in Sweden and Austria. It was opposed mostly by Germany.

The directive now provides that the Commission shall evaluate the various national

support mechanisms and present a report on their success (by October 2005), including their cost-effectiveness. If necessary, it shall at this point make a proposal for a Community framework with regard to support schemes which shall promote RES-electricity in a simple and effective way. This proposal will have to provide for transitional period of at least seven years, so that no harmonized regulation can enter into force before 2012.

2.3. Guarantees of origin Art. 5 of the directive, regulates the way in which member states shall set up

systems of guaranteeing the authenticity of RES-electricity. The term “certificates” was avoided as some member states viewed this as a first step towards introducing a system of tradable certificates/quota-based support schemes.

5 The NFFO (Non-Fossil Fuel Obligation) was introduced in England and Wales by the 1989 Electricity Act. The Act allowed the Secretary of State to order the Public Electricity Suppliers (PES) to purchase a certain amount of electricity produced from non-fossil fuels and also established a mechanism, the Fossil Fuel Levy (FFL), to compensate the PES for the NFFO.

Issue Paper on Green Energy Pricing

© ERRA 2006 7

2.4. Administrative procedures Art. 6 provides that member states shall evaluate their regulatory frameworks for

RES-electricity (authorizations, permits, support decisions etc.) with a view to reducing regulatory barriers, streamlining procedures and ensuring that rules are objective, transparent and non-discriminatory, taking into account the particularities of the various renewable energy technologies. 2.5. Grid access

Art. 7 regulates the relation between RES-electricity producers and operators of the

transmission and distribution system. Its purpose is to make sure that there is no discrimination against such producers taking into account all the costs and benefits of RES-E, e.g. in grid access, connection costs or transmission and distribution fees. Prospective connection costs must be communicated to RES generators and standard rules on costs published. The original Commission proposal – supported by Parliament provided for priority access. The Council changed this to “guaranteed access”, although priority access may still be granted. In dispatching generating installations, transmission system operators shall give priority to RES producers insofar as the operation of the national electricity system permits. This clause is important as in many areas grid operators are hostile to RES and try to impede its deployment. Member states shall report on measures taken to facilitate access to the grid in the report referred to in the preceding subsection.

2.6. External costs and subsidies/Summary report on implementation Art. 8 provides for the Commission to submit a summary report on implementation

on the basis of the member states’ reports at the end of 2005, and thereafter every five years. Such a report “shall consider the progress made in reflecting external costs of electricity from non-renewable sources and the impact of public support granted to electricity production” as well as progress on achieving national targets and discrimination between different energy sources.

The chief purpose of the directive is to make RES competitive for the internal

electricity market. Now the competitiveness of this form of electricity is greatly inhibited by the fact that the generation of electricity from conventional sources is not charged with its full external costs, and often receives subsidies on top of that. Research conducted for the EU in the ExternE project shows that the cost of electricity generated from coal and oil in the EU would on average double if external costs to environment and health were included; from gas, it would increase by 30%. In addition, fossil and nuclear generation is often subsidized by a variety of mechanisms. Without these market distortions, RES would not need the same amount of support.

Issue Paper on Green Energy Pricing

© ERRA 2006 8

3. Green pricing

3.1. History of green pricing The story of Green Pricing began in the 1970s, when the President Jimmy Carter

decided to solve the United State’s energy problems by encouraging energy conservation and a decreased dependence on foreign energy sources. As a means to reach that goal, the Public Utility Regulatory Policies Act of 1978 (PURPA) was signed into law on November 9, 1978.

PURPA created a market for power from non-utility power producers, known as

“qualifying facilities.” Before that law, only utilities could own and operate power generating plants. PURPA also required utilities to interconnect with and buy energy from “qualifying facilities,” including renewable energy plants, at incremental or avoided costs of production.

Since PURPA was enacted, the cost of green power has decreased, but expansion

still has not occurred as quickly as previously expected. Power price trends, especially falling generating costs, can be blamed for impeding green power introduction. Also, the push towards electricity deregulation has urged electric utilities to restructure to improve efficiency, which puts even more prices on electricity prices. These factors have worked unfavorably for RES by undermining their competitiveness in the electricity market.

One new way to introduce more green power into the market is by embracing the

spirit of “greenness.” Now more than ever, the public is making its preference for environmentally conscious products clear. It is a revolution known as green consumerism. Symbolic behaviors of green consumerism include recycling, preferential buying of products made out of recycled materials, and buying low-chemical farm products among others. Electric utilities are joining the movement through green pricing programs. This advent of green consumerism is intersecting with the introduction of deregulation of the electricity industry, which is providing consumers with choices as to who their power supplier will be and the content of the power product. Ironically, as the ongoing wave of electric utility deregulation forces utilities to scramble for the lowest-cost power, some companies have found they can sell power at a higher economic cost if it has a low environmental cost. More and more utilities are starting green pricing programs, which offer RES to interested customers at a premium price. In other words, one kilowatt-hour is suddenly different from another. Since green power is generally more costly, in terms of production, than conventional coal or gas-fired power, customers who participate in green pricing programs usually agree to pay a premium on their electricity bill to cover the extra expense.

Issue Paper on Green Energy Pricing

© ERRA 2006 9

In a green pricing program, the power provider gives customers the option to buy electricity generated from clean, environmentally friendlier sources such as solar, wind, geothermal and some types of biomass and hydro energy resources. These programs are based on the principal that consumers are voluntarily willing to pay more for electricity which is produced in an environmentally neutral manner. Consumers can usually choose to purchase all or a percentage of their electricity as “green.” The electricity supplier, in return, guarantees that each unit of electricity corresponds to a unit entering the electricity supply network from a green power plant.

Green pricing programs provide numerous benefits. Among them are: 1. Education - Utilities can act as a vital resource to consumers seeking information

about energy sources, efficiency, and conservation. Many utilities successfully market their green power product as part of an energy efficiency or conservation campaign. Through this type of education, consumers are able to make wiser choices about their energy use and become more knowledgeable about energy in general.

2. Investments - By encouraging environmentally-oriented people to put their

money in clean, renewable power sources and in the same time encouraging electricity marketers to develop national educational campaigns that promote clean energy. As utilities come under increasing pressure to reduce emissions that contribute to acid rain and global climate change, green pricing programs offer a golden opportunity to offset some of the adverse environmental effects of conventional power generation. In addition, investing in renewable power diversifies the energy mix, reducing dependence on fossil fuels and their inherent price fluctuations, and providing long-term rate stability.

In the same time pioneering utilities are faced with various marketing challenges

when it comes to green pricing programs: 1. While a few consumers are willing to pay a premium for green goods, most are

not. This apprehension stems from the fact that such environmental benefits as cleaner air or water are difficult to immediately see, feel or experience. With renewable forms of power, the product itself is not seen. Also, because the renewable energy is simply added to the communal power grid in place of fossil fuel-generated electricity, consumers do not actually receive the product they pay the premium for.

2. Many consumers lack awareness of exactly what types of energy are harnessed in

producing the electricity coming into their homes and are even less aware of the environmental issues associated with its production. Examples of such misleading beliefs are that electricity won't be available if the wind doesn't blow, renewable energy requires channeling a second set of power lines into homes, or tapping wind energy in a major way will somehow upset global climate patterns.

3. Credibility represents another challenge. Customers question paying a premium

for "green electricity" because they feel current rates are high enough. They want to know precisely how funds will be used. But customers aren’t the only people hesitant to fully

Issue Paper on Green Energy Pricing

© ERRA 2006 10

embrace the concept of green pricing. Some renewable energy advocates have taken opposing stances as well. They say that increased use of renewable energy provides benefits to all customers, and therefore all customers should share in the cost of development.

Preconditions for successful green pricing programs are numerous: specifics of

program design, product pricing, the extent and quality of market research, the credibility of the utility, the simplicity of the program, the tangibility and visibility of the RES projects, and program implementation and marketing efforts, particularly with community organization partnerships.

1. The design and marketing of the "green power" product is considered a crucial

element of success. Product design involves several different elements such as the type of program offered, whether customers can obtain all of their electricity from RES, and exactly how much of the premium paid by customers actually goes toward developing new renewable energy sources.

2. Another key factor is whether the program creates "personal value" for customers. Customers are more apt to accept some additional cost for RES as long as they perceive some gain in personal value. Otherwise, customers may wonder why they are being singled out to pay for something that they perceive benefits all customers. Since utilities with green pricing programs are essentially asking individual customers to pay the cost of providing the benefits of a cleaner environment to all customers, many utilities are finding ways to add value to their green pricing products and generate private benefits for participating customers. Those benefits include tax deductibility of the extra charges, personal recognition in program newsletters and advertisements, instilling civic and community pride and price protection from fuel price increases.

3. Pricing is another vital element that is linked to success. A utility’s green pricing program should reflect the difference between the utility’s cost of acquiring the renewable energy and its alternative cost of power. The increased availability of state and federal subsidies and incentives is allowing many utilities to reduce their green pricing program premiums. Tax incentives can directly lower the costs of green power and can improve profit margins for marketers, enabling them to more easily compete in the market and undertake more aggressive marketing campaigns. Despite the numerous variables involved in determining premiums, one thing remains certain - pricing should be tied directly to the investment promised for new projects. Customers want to know that the dollars they are contributing result in additional and meaningful renewable energy development6. A similar scenario can be observed in charitable giving. Those contributing want the assurance that the money they donate is supporting the actual cause being solicited for rather than fundraising and program administration.

6 Swezey Blair and Lori Bird. NREL, “Utility Green Pricing Programs: What Defines Success?”, September 2001.

Issue Paper on Green Energy Pricing

© ERRA 2006 11

4. Another critical factor to its success is the way a green pricing program is implemented. Successful implementation not only demands creative and continuous marketing efforts to build awareness, but also requires ease of participation and a long term commitment to expanding the program to meet customer demand. While many consumers seem to favor RES, the majority may not know very much about renewable energy technologies. Programs that are overly complicated or that combine different environmental objectives may confuse already uncertain customers.

5. Another key issue program organizers must consider involves deciding which customers to target. While residential customers are generally the focus, a green pricing program's ability to attract business customers could determine its ultimate impact. Business and other non-residential customers such as governments, institutions, faith-based groups, and non-profits who were initially considered too price sensitive to pay more for green power, are now recognizing that purchasing green power can help meet both corporate and institutional goals related to environmental improvement and sustainable business practices. Some programs have drawn as much as half of their support from businesses. About a quarter of the total power sold through green power programs is to non-residential customers. The study also suggests that by carefully analyzing the motivations and preferences of potential participants, utilities can target specific green pricing programs to appeal to wide segments of their customer base. The extent to which a utility partners with the community and other outside groups to publicize the program is also important.

All these potential success factors are focused on what the green power supplier can

do to get customers. However, another problem exists for the customers of utilities that want green power, but whose markets aren’t deregulated or whose utilities don’t offer green pricing options.

3.2. Policy mechanisms Governments have a number of options that they can use to promote renewables.

The first is to support the use of voluntary measures, particularly through education and information dissemination. This option has varying and limited effects. Second are environmental standards or energy taxes. The third option is to promote renewable energies through direct support, which is the focus of this paper. Generally, a mix of instruments is essential and a key to success. The combination of policies needed depends on the costs of the technology used, location and conditions.

There are five major categories of relevant policy mechanisms:

• Regulations that govern capacity access to the market/electric grid and

production or purchase obligations; • Financial incentives; • Industry standards, permitting and building codes; • Education and information dissemination;

Issue Paper on Green Energy Pricing

© ERRA 2006 12

• Stakeholder involvement. There is not necessarily a direct link between these policy mechanisms and specific

obstacles to greater use of renewable energy, as some of the policy options tackle a combination of barriers. An additional critical element is the need or a general change in government perspective and approach to energy policy. Government investments in research and development are important as well.

Following are key points to frame the policy mechanisms. The concluding section

includes more findings and policy recommendations. 1) Experience to date has demonstrated that considerable intervention in energy

markets is required to introduce significant amounts of renewable energy into the mix. Every country that has succeeded thus far in developing renewable energy on a substantial scale has been committed over the long-term to this goal, with consistent policies that include a package of policy mechanisms (consisting of all of the above-mentioned types).

2) The effectiveness of government policies depends on how well they are designed

and whether or not they are enforced. The use of a particular policy type does not guarantee success. In addition, policy makers must be cognizant of the projects and technologies they are trying to promote as such decisions determine the policy framework that is needed. For example, to promote technologies such as PV, solar thermal, heat pumps and wind turbines on a small-scale, distributed basis, support should be granted to the end customer; to promote large wind, biomass, geothermal, or marine technologies, the investment is more likely to be channeled through a large entity or company. Further, each country has unique circumstances and must design its own system, and enact a combination of policies, based on needs, circumstances and available resources.

3) The experiences of countries such as Denmark, Germany, Japan, Spain and

Brazil have demonstrated that the key to steady and significant cost reductions is the development of consistent and reliable markets. Such conditions allow for the entry and maturation of small- and medium-scale enterprises, which have provided the bulk of the technological innovation that has driven down renewable energy costs. In addition to the “global learning curve” that exists for technologies such as wind turbines and PV cells, there is a “national learning curve” as individual countries develop domestic industries that are able to manufacture, install and maintain renewable energy systems using local equipment and labor. Those countries that do not yet have sizeable industries in place can expect dramatic price reductions in the first few years after effective new policies are introduced.

4) Most of the policies involve some sort of subsidy, direct or indirect. Energy

markets are not now and never have been fully competitive and open, and today’s markets include substantial institutional barriers, as well as long-term subsidies for conventional energy, that act as obstacles to renewable energy. Even market-oriented countries such as the United States and United Kingdom now agree that subsidizing

Issue Paper on Green Energy Pricing

© ERRA 2006 13

renewable energy makes sense. Support for RES is important not only to incorporate the external costs (environmental, social and security) of energy production and use, and make up for decades of past support for conventional energy. It is also essential to account for the environmental, social and security benefits associated with RES — including the reduced risk of fuel price volatility, a more diversified portfolio of energy options, a cleaner environment and better health, and job creation and economic development. Well-designed, modest production-based subsidies provided up front can work rapidly to close the cost gap between RES and conventional energy systems.

5) To date, feed-in pricing has been responsible for most of the additions in

renewable electricity capacity and generation, while driving down costs through technology advancement and economies of scale, and developing domestic industries. The record of quota systems is more uneven thus far, with a tendency of stop-and-go, and boom and bust markets. It is important to recognize that both quota and pricing systems involve subsidies. But pricing systems have provided increased predictability and consistency in markets, which in turn have encouraged banks and other financial institutions to provide the capital required for investment.

6) In developing countries, markets are apt to be particularly sensitive to the need

for relatively uncomplicated access to the electric grid and low transaction costs. Pricing laws allow for ease of entry into the marketplace and tend to favor smaller companies and incremental investment, making them particularly suited to developing countries, where power markets are often small and dispersed. As in the industrial world, it is critical to focus on models of development that are viable, sustainable, and replicable, and that emphasize local participation and ownership; to date, donor aid projects have tended to reduce the perceived value of renewable energy while inhibiting commercial markets.

3.3. Feed-in pricing The precursor to the pricing law was enacted in California during the 1980s. In that

state, the implementation of PURPA involved the use of standardized long-term contracts with fixed (and, in some cases, increasing) payments for all or part of the contract term. The costs of the contracts were covered through higher electric rates for consumers. While these contracts proved costly, it is widely believed that the alternative (nuclear power) would have been even more expensive. The time length of the contracts (15 to 30 years for wind projects), combined with fixed energy prices for much of that time, assured producers of a market for their product and finally gave them something they could take to the bank to obtain financing. While most other U.S. states saw little development during the 1980s, California for a time became the world’s leader in renewable energy use. General description of Standard Offer Contracts in California during the 1980s is presented in Appendix 2.

In the late 1980s German Federal Ministry for Research and Technology (known by

its German abbreviation, BMFT) established 250 MW research program with a premium for the environmental and research value of new wind generating capacity. Initially 100

Issue Paper on Green Energy Pricing

© ERRA 2006 14

MW, the program was so popular that it was increased to 250 MW before it was superseded by the law on feeding-in electricity in 1991.

The Aachen model of premium payments, that is payments above "avoided cost",

was introduced in Aachen Germany for photovoltaics in 1989. At that time that was the highest payment per kWh for renewable energy generation anywhere in the world. The tariffs were limited to the city of Aachen, but the process was eventually repeated in other German cities, including Bonn and Nuremberg.

In 1991 the German Parliament adopts the law on feeding-in electricity

(Stromeinspeisungsgesetz). Germany's ground breaking Renewable Energy Tariffs or Feed-in law specified that renewable generators had the right to connect and how they would be paid for their generation based on a percentage of the retail price of electricity. Wind energy generation was paid 90% of the full retail rate; hydro and biomass - 75%. In 1994 the German Feed-in law was modified and hydros' and biomass' payment increased to 80% of the retail rate.

Between 1980s and 1990s Denmark uses a complex mix of Renewable Energy

Tariffs (RET), exemptions from the carbon dioxide tax, and tax benefits to pay for wind generation. The Renewable Energy Tariff was 85% of the retail rate. This system was used until the introduction of a Renewable Portfolio Standard (RPS) and renewable energy credit trading system in 2000. The RPS eventually led to the collapse of the Danish domestic demand for wind turbines and was abandoned in 2004.

In 1997 Spain permits private power production. Spain introduces Renewable

Energy Tariffs with Royal Decree in 1998. The early pricing laws in Europe, in Denmark and Germany required that utilities

give small wind and other private generators access to the electric grid, and they guaranteed producers a minimum share of the retail rate.

The German system was revised in 2000. Renewable Energy Sources Act

(Erneuerbare Energien Gesezt, EEG) replaced the first Feed-in law and introduced Advanced Renewable Energy Tariffs. These differed from the simpler approach of the original Stromeinspeisungsgesetz by specifying the actual prices that would be paid for generation from each of several different renewable technologies independent of the retail price for electricity. Different prices were also introduced within each technology band depending upon the size of the project or the resource base. For example, there were several prices for biomass plants of varying size. This strategy allowed premiums sufficient for developing all renewable technologies, including photovoltaics.

In 2004 Germany's EEG and Spain's Royal Decree on renewable generation

included tariffs for offshore wind. Laws similar to Germany’s pricing law have been enacted in several other European

countries, including France, Austria, Portugal, and Greece, in addition to South Korea.

Issue Paper on Green Energy Pricing

© ERRA 2006 15

Recently, Brazil enacted a law that combines pricing laws and quotas (specific capacity targets).

Today most pricing laws provide a fixed payment for renewable electricity that

varies by technology type, plant size, and occasionally by location (e.g., wind energy), and is generally based on the costs of generation. Payments guaranteed to new projects decline annually, and are adjusted periodically. The tariffs last for 15-20 years from date of project installation.

The costs of higher payments to RES are covered by an additional per kilowatt-hour

(kWh) charge on all consumers according to their level of use (e.g., Spain, Germany as of 2000), a charge on those customers of utilities required to purchase green electricity (e.g., Germany until 2000), or by taxpayers, or a combination of both (Denmark through feed-in rates and reimbursement of the carbon tax).

It is important to note that pricing laws have not succeeded in every country that has

enacted them. At the same time, to date, those countries that have experienced the most significant market growth and have created the strongest domestic industries have had pricing laws. In order to succeed, tariffs must be high enough to cover costs and encourage development of particular technologies; they also must be guaranteed for a time period long enough to assure investors of a high enough rate of return. The success of pricing laws is also determined by factors such as charges for access to the electric grid, limits set on qualifying capacity and the ease of permitting (influenced by the existence and specifics of national or regional standards).

3.4. Net metering system A variation on pricing laws, “net metering,” permits consumers to install small

renewable systems at their homes or businesses and then to sell their excess electricity into the grid. This excess electricity must be purchased at wholesale market prices by the utility. In some cases, producers are paid for every kilowatt hour (kWh) they feed into the grid; in other cases they receive credit only to the point where their production equals their consumption. This option is available in Japan, Thailand, Canada, and many U.S. states. It is of benefit to electricity providers as well as system owners, particularly in the case of PV, because excess power generated during peaking times can improve system load factors and offset the need for new peak load generating plants.

Net metering differs from the access and pricing laws in Europe primarily in scale

and implementation. Success in attracting new renewable energy investments and capacity depends on limits set on participation (capacity caps, number of customers, or share of peak demand); on the price paid, if any, for net excess generation; on the existence of grid connection standards; and on enforcement mechanisms. Without other financial incentives, net metering is not enough to advance market penetration. Neither California nor Texas saw much benefit from net metering for wind power, let alone for more costly RES like solar PVs, until other incentives were added to the mix. However,

Issue Paper on Green Energy Pricing

© ERRA 2006 16

net metering might have a greater impact if private generators were to receive time-of-use rates for the electricity they put into the grid—particularly in the case of PVs, which generate electricity at peak demand times when the value of their power is highest. Mandated targets or quotas, discussed below, and net metering can be used simultaneously.

3.5. Quota system 3.5.1. General principles

Pricing laws establish the price and let the market determine capacity and

generation. Under Quota system model the government sets a target and lets the market determine the price. Typically, governments mandate a minimum share of capacity or generation of electricity (generally grid-connected only), or a share of fuel, to come from renewable sources. The share required often increases gradually over time, with a specific final target and end-date. The mandate can be placed on producers, distributors or consumers.

The simplest form of quota system is one in which the government imposes a

mandate on one producer/supplier. For example, during the 1990s, the Minnesota Public Utilities Commission ordered the electric utility Northern States Power to install successive amounts of wind energy capacity, thereby helping to open up the wind market in that U.S. state. Quotas have also been used to promote the use of RES off the grid, including alternative fuels. Several European countries now require that a specific share of diesel fuel contain biodiesel, and Brazil has become the world leader in ethanol production and use by requiring that ethanol make up a set share of all fuel sold (in combination with other support).

Quota system for renewable electricity is a relatively new type of policy, first

introduced in the late 1990s, so there is relatively little experience with quota systems to date. 3.5.2. Main types of quota systems

There are two main types of quota systems used today for electricity generation: 1. Obligation/certificate. The Renewable Portfolio Standard (RPS), widely used

in U.S. states, is in the former category. Under an RPS, a political target is established for the minimum amount of capacity or generation that must come from RES, with the amount generally increasing over time. Investors and generators then determine how they will comply - the type of technology to be used (except in the case where specific targets are established by technology type), the developers to do business with, and the price and contract terms they will accept. At the end of the target period, electricity generators (or suppliers, depending on the policy design) must demonstrate, through the ownership of credits that they are in compliance in order to avoid paying a penalty. Producers receive

Issue Paper on Green Energy Pricing

© ERRA 2006 17

credit - in the form of “Green Certificates”, “Green Labels”, “Green Tags” or “Renewable Energy Credits” - for the renewable electricity they generate. Such credits can be tradable or sellable, to serve as proof of meeting the legal obligation and to earn additional income. (Some countries have set floors and/or ceilings for the value that these certificates can achieve.) Those with too many certificates can trade or sell them; those with too few can build their own renewable capacity, buy electricity from other renewable plants (which generally involves a bidding process), or buy credits from others. Once the system has been established, government involvement includes the certifying of credits, and compliance monitoring and enforcement.

2. Tendering systems. Under those systems, regulators specify an amount of

capacity or share of total electricity to be achieved, and the maximum price per kWh. Project developers then submit price bids for contracts. The UK’s Non Fossil Fuel Obligation was an early example of this type of policy. Governments set the desired level of generation from each resource, and the growth rates required over time. The criteria for evaluation are established prior to each round of bidding. In some cases, governments will require separate bids for different technologies, so that solar PV is not competing against wind energy projects, for example. Generally, proposals from potential developers are accepted starting with the lowest bid and working upwards, until the level of capacity or generation required is achieved. Those who win the bid are guaranteed their price for a specified period of time; on the flip side, electricity providers are obligated to purchase a certain amount of renewable electricity from winning producers at a premium price. The government covers the difference between the market reference price and the winning bid price. Each bidding round is a one-time competition for funds and contracts. In contrast, under the RPS, companies and projects must constantly compete in the marketplace, with existing and new projects, unless they have signed long-term contracts.

Both types of quota systems give customers who want to invest in green power the

opportunity to do so, even if their own utility doesn’t offer such a program. Green certificates represent the environmental and social attributes of green power.

Green power costs more than conventional power, but also provides environmental

benefits. Therefore, it’s possible to say that customers who purchase green power are really getting two things: the electricity needed to power their home or facility, and the environmental benefits associated with this power. In the same manner, a customer who is willing to pay more for an organic apple is really paying for the apple and then paying extra for the environmental benefits such as decreased fertilizers and pesticides in the ground.

The electricity generated from green power can be sold at that same price as

conventional power in the wholesale market if the environmental attributes are separated out. This power is then said to be generic, null or commodity power. However, it still costs more to generate green power. Selling the environmental attributes as green tags can make up the extra cost.

Issue Paper on Green Energy Pricing

© ERRA 2006 18

The green certificates correspond to an amount of green power that was generated and sold into the market where it originated. They represent the real savings in carbon dioxide (CO2) and other pollutants that occur when green power replaces the burning of fossil fuels. 3.5.3. How Green certificates work

Utilities that offer a green power alternative sell the power and the environmental benefits in one package at a higher price than conventional power is sold. In this case, the utility handles all transactions with the generating facilities. Conversely, utilities are not involved in green certificate transactions. Green certificates are either sold directly to the customer by the green power generating facility, by a nonprofit organization working with the generating facility, or by a private business hoping to take advantage of the financial opportunities presented by green tags. These organizations are collectively called green certificate marketers.

The customer makes a payment to their electric utility for the market cost of the

power, and also makes a payment to their green certificate marketer to promote the flow of more green power into the power grid. 3.5.4. Challenges Facing Green Tags

Green tags face challenges that fall into three basic categories. Among them are: legal property rights to the intangible environmental attributes; customer protection from misrepresentations and fraud; development of a system that will protect against double counting or double selling of the same green certificate.

In the absence of an accepted set of rules, laws, policies or other guidelines to direct

the legalities of owning and trading green tags, many issues arise. In some cases, groups entering into green certificate deals create their own specific contracts to handle the transaction. This may work for commercial customers, but it’s impractical for residential and small business customers that lack sophistication in legal matters.

Green certificates will only simplify the process of selling green power as long as

there is a third party to certify that there are only as many green tags as there is green power being generated. Otherwise the market will be bogged down with uncertainty.

Customers won’t be confident they’re getting what they’re paying for and green

certificate marketers won’t be sure what their rights are in handling disputes. In such a situation, lawsuits will inevitably crop up. Currently, there is no official set of standardized definitions, processes, or rules that govern the green certificate market.

Ownership is one issue that standards need to address. One solution could be that a

green certificate’s existence should be recognized either when the meter output of the generating facility is read or when the electricity is delivered into the power grid. At that

Issue Paper on Green Energy Pricing

© ERRA 2006 19

time, the green certificate should belong to the owner of the green power generating facility.

The transfer of green certificates should be handled through the use of specific

contractual agreements. This is useful in determining ownership and recording and maintaining records of transfers. The ideal solution would be a cradle to grave tracking system. While this would probably add administrative costs, it may be necessary to maintain customer confidence and prevent double counting.

Another issue is “banking” of green tags. Banking is a tool that gives utilities or

marketers flexibility in compliance with specific renewable program mandates. It essentially allows the obligated party to purchase the RES in advance of their obligation and hold or bank the green certificates to be applied at a later date. For example if a state has an energy-based renewable portfolio standard, then a utility might be allowed to purchase green certificates in 2005 to be applied toward their obligation in 2006. Similarly, a utility might be allowed to purchase enough green tags in one quarter to meet their green pricing demand for the entire year. The converse, borrowing, could be allowed to facilitate compliance, e.g. applying 2006 purchases toward the 2005 obligation.

Generally, some period of green certificate banking is necessary to overcome

problems created by the seasonality of renewable energy generation and the necessity of maintaining a competitive and liquid market. Some RES, such as wind, solar and hydro, experience seasonal output fluctuations. Therefore, allowing some amount of banking between periods of high output and low output can help utilities and marketers meet their obligations with renewable resources by allowing green certificates to be banked in periods of high output and applied toward the obligation in periods of low output.

Green certificates also present many customer protection concerns. Green

certificates present a potential problem for abuse because they are an intangible product that customers may have difficulty understanding. A lack of customer sophistication leaves customers open to misrepresentations and fraud. Add this to the fact that the definitions and information associated with green tags, and the rules and processes for working with green certificates are not standardized and customer misunderstandings become a huge risk.

Customer education and disclosure is of utmost importance if the market will be

successful. The problem is that there are many kinds of customers and they all have very different reasons for purchasing green tags. So, the information needed by particular customers may vary widely. In addition, it is possible to give a customer more information than they can handle, leading to confusion and distrust.

Some green certificate advocates believe that customers should be told the type of

technology they are supporting and where power is being generated. Some say customers should know if certain attributes like CO2 benefits have been unbundled from the other attributes on their green tag. Some think it would be a good idea to inform the customer

Issue Paper on Green Energy Pricing

© ERRA 2006 20

of when the plant that generated the green power was built as well as when that specific power was generated. All told, advocates are consumers might feel cheated by green tag purchases that don’t meet their expectations.

One obvious way customers could be cheated through the use of green certificates

is by double counting. Double counting is the sale of one green tag to more than one customer. Every green certificate should be equivalent to an amount of green power that was generated and sold into the market. Otherwise, the green certificate is essentially worthless. Double counting can either be purposeful, as in outright fraud, or it can be accidental, such as through computer error or confusion. Whether it’s purposeful or not, it can cause severe damage to the green certificate market. Customers are already skeptical of new power companies that are emerging in restructured markets. Even the perception of double counting could push these customers to a point where they never trust that they’ll get what they’re paying for.

Green certificates also face many of the same challenges that other green markets

have faced in the past. Namely, definitions of which renewable resources are valuable in the market and eligible for various programs often cause disagreement. The relationship between green certificates and RPS or emissions credit trading is not clear. On the same note, multi-state independent system operators (ISOs) each have different regulations with different approaches, definitions and procedures for credit trading.

So far, only the UK seems to have introduced a quota/certificates system that is

clearly attractive to RES industry – and even here many important issues remain unsolved. As a result, many observers conclude that market-based instruments have not really proven their worth so far.

3.6. Comparison between the two major supporting systems 3.6.1. Costs, prices and competition

It had been argued that it is difficult to control the costs of pricing laws over the

short term, whereas subsidies can be controlled under bidding or quota systems. For example, if tariffs are set too high, they can encourage significant development and dramatically increase electric rates; if they are not high enough, the policy will bring about little development. The pricing law could be more expensive than tendering programs or an RPS per kWh of electricity produced.

In addition, it is argued there is less competition and cost minimization under

pricing laws than with quota systems, in which developers must compete to win bids or gain contracts. Historically, it has been assumed that pricing laws do not inherently encourage cost or price reductions, and do not ensure least-cost development. The pricing law can drive down costs by driving economies of scale and innovation, and manufacturers and developers will compete for the lowest possible costs in order to achieve higher profit margins, which promote cost reductions. Yet, developers have little

Issue Paper on Green Energy Pricing

© ERRA 2006 21

incentive to pass these cost savings onto consumers as long as tariffs remain unchanged. Furthermore, under pricing systems, utilities and customers in resource-rich areas can experience the brunt of costs associated with renewable energy development.

However, most of these limitations can be overcome depending on how pricing

systems are set up. Pricing policies can address cost and price issues through regular adjustments to tariffs for renewable energy in response to changes in technologies and the marketplace. This is now the case in Germany, where the law was changed from a percentage of the retail rate to fixed tariffs; the French and Portuguese pricing laws have also adopted many of these features. In addition, they can be established with help from research institutes (neutral consulting) and the RES industry (with insight into the costs of production) as in Germany. The introduction of declining tariffs has brought the costs of the pricing and quota systems much closer together. And, at least one analyst believes that pricing laws have delivered renewable electricity more cheaply than have quota or green-certificate policies7.

There is also some evidence, that it may be cheaper to provide significant national

investment for renewable energy (through the German pricing law, for example) over a period of perhaps 15-20 years to bring renewable energy technologies rapidly down their learning curves8, and thus reduce costs very quickly, rather than to introduce renewable energy relatively slowly and over a longer period of time - with an associated slower reduction in costs.

Further, pricing systems encourage development of local manufacturing industries,

which leads to a large number of companies and in it creates competition. And even where pricing laws are more expensive per unit of energy produced, they drive technological development and strengthen or establish new businesses, thereby supporting industry and agriculture (biomass), leading to job creation and furthering economic growth. The use of well-designed pricing laws can avoid the need for a host of other additional subsidies. They also help to “internalize external costs” of conventional energy and compensate for the benefits of renewable energy. Pricing laws encourage higher growth rates in early years than quota systems generally do, and encourage long-term innovation. Finally, concerns about heavy burdens in resource-rich areas can be addressed, as was the case in Germany, by spreading the costs around the entire country so that each region pays according to its total electricity consumption, rather than according to its resource base.

Quota systems are generally credited with encouraging competition and

dramatically driving down the cost and price of renewable energy. This appears to be true in a number of cases. One example often cited is the decline in wind energy prices under 7 Environment Daily, 2003 8 The learning curve effect and the closely related experience curve effect express the relationship between experience and efficiency. As individuals and/or organizations get more experienced at a task, they usually become more efficient at them. Both concepts originate in the old adage, "practice makes perfect", and both concepts are opposite to the popular notion that a "steep" learning curve means that something is hard to learn. In fact, a "steep" learning curve implies that something gets easier quickly.

Issue Paper on Green Energy Pricing

© ERRA 2006 22

the UK’s Non-Fossil Fuel Obligation. Wind bids declined dramatically, from US$ 0.189/kWh in the first round to US$ 0.043/kWh in the last9. At the same time, it is unclear whether these reductions came about through the quota system. There is evidence that at least part of the reductions were due to the pricing policies of other countries, which drove technological improvements and brought down costs. In addition, some of the later cost reductions under the NFFO were due to changing terms and conditions, including a longer contract period.

There is also speculation that the low costs and prices driven by the RPS in parts of

the United States and Australia are due, at least in part, to the availability of wide-open spaces with good resources. This would explain the difference in wind energy costs between those countries and Germany and Spain. Taking into account the relationship between wind speeds and the resultant power output (wind power is proportional to the cube of wind speed), costs under quota systems will come more in line with those of pricing laws once the best resources are no longer available.

Particularly early on, when a country has few domestic manufacturers or

developers, only a small number of companies might respond to bidding rounds, limiting choice and competition. According to some sources, a high degree of concentration of participants can lead to cartels and the abuse of market power. And if the price of credits or certificates is high, this can increase the electricity price paid by consumers, as is the case with pricing laws. However, this would likely be a short-term situation as higher certificate prices would encourage more development, thereby reducing certificate prices. Finally, if purchase obligations are large enough, quotas can lead to economies of scale, thereby reducing both costs and prices.

There is some evidence that in quota systems which lack differentiation among

technologies, such as the current Renewable Obligation Certificate (ROC) program in the United Kingdom, there is a tendency to over-subsidize lower-cost renewables such as onshore wind and biomass waste-to-power, a factor that will lead to higher costs10. Under the ROC system, the price paid for renewable electricity (most of which is wind power, in a country with the best winds in Europe) is similar to payments for wind energy in Germany. As a result, a great deal of development is underway. But this makes it clear that the costs of renewably generated power are at least as dependent on how a particular policy is structured as they are on the system that is chosen. Quota based systems are not inherently cheaper, nor are pricing systems inherently more costly; the costs per unit of electricity produced depend on the details of those systems. 3.6.2. Financial security

Under a pricing system, the long-term certainty that results from guaranteed prices

over perhaps 20 years means that companies are willing to invest in technology, to train staff, and establish other services and resources with a longer-term perspective. This certainty also makes it easier to obtain financing, as banks and other investors are assured 9 Wiser et al, 2000 10 Kleiburg, 2003

Issue Paper on Green Energy Pricing

© ERRA 2006 23

a guaranteed rate of return over a specified period of time. In fact, even banks in Germany lobbied the Bundestag for a continuation of pricing laws in 2000.

With quota systems, there are potential uncertainties through many steps in the

process from project planning to operation. For example, there can be substantial preparation costs for projects submitted for bids, adding an element of risk and uncertainty that many potential developers cannot afford. Without long-term contracts, under quota systems existing developers could be undersold by future projects, and will always be competing against new developments. While some see this is as a disadvantage, others view this as an incentive to reduce costs. This challenge has been resolved in Texas with 10-25 year contract requirements. But unless such contracts are standardized, renewable energy developers must negotiate contracts with utilities or suppliers on an individual basis. While this could be a problem, to date in several U.S. states and elsewhere this does not seem to be a major drawback.

Under quota systems potential investors must assess future supply and demand

balance during the lifetime of the project (often 20 years or more) by developing a forward price curve. Yet, demand is created by political targets, which could change, thereby resulting in a degree of uncertainty. In addition, estimating supply is a complex process that requires an understanding of a broad range of factors. These include the current competitiveness of all eligible energy technologies; future costs – determined by learning curve effects; cost-resource curves, or the impact on costs when the best resources are no longer available and projects must be sited where wind speeds are lower, or rely on more expensive biomass feedstock, for example. All of these factors add to the level of uncertainty. Finally, if renewable technologies enjoy subsidies or other types of support (e.g., grid connection costs, tax credits, accelerated depreciation), whose continuation over the project lifetime is also uncertain, the risks to investors will be higher, requiring a higher projected rate of return. Under these circumstances, banks will also be less willing to provide financing for RES projects.

Sources of income are two-fold under a certificate-based quota system: first, is

payment for the sale of renewably generated electricity and, second is income from the sale or trade of renewable energy certificates. The price of credits or certificates can fluctuate significantly with changes in the marketplace or meteorological variability, rising when there is a shortage of renewable electricity and falling when there is a surplus. Diversifying sources and location of projects can also reduce fluctuations due to meteorological variability. Establishing minimum and maximum certificate prices can help, but does not eliminate investor uncertainty. Trading in international markets can also work to stabilize prices, and risks can be limited through long-term contracts, or borrowing or banking of credits. Some of these solutions, however, can increase the complexity of the system. Seasonal variations in output lead to variations in income from fixed tariffs as well, and market fixes are not built into the pricing system as they are with certificate models. Over time, however, these variations will also be smoothed out. Further, under quota systems financial security is reduced if there is uncertainty around rules relating to green certificate trading. For instance, as system designs are altered—such as changes in penalties, borrowing or banking provisions, and the status of

Issue Paper on Green Energy Pricing

© ERRA 2006 24

imports—prices can be affected dramatically. In general, many believe that the higher risks and lower profits associated with quota systems make them less attractive for investors than pricing laws.

Some analysts believe that quota systems provide more regulatory and financial

stability and security than do pricing systems, which could change with the political winds11. For example, long-term purchasing contracts with private entities are enforceable under the law, which might be safer than relying on consistency of government policy.

Others believe that pricing systems provide a greater sense of security than quota

systems, particularly in developing countries, because there is not the same assurance that a market for renewable energy credits will exist and that they will be of value. Targets established under quota systems are also policy dependent and can change over time, affecting the value of certificates and creating uncertainty. In addition, payment systems and levels are known at the outset under a pricing system; this is not necessarily the case under a quota system with certificate trading. What is most important is political stability, and long-term, credible, consistent policies.

3.6.3. Ease of implementation In general, pricing laws are easy to administer and enforce, and they are highly

transparent. As with quota systems, policy makers are required to establish targets and timetables, and to determine which technologies are qualified (type and scale). Pricing laws also require the setting of tariffs for each technology type, which can be done with the help of research institutes and industries, as in Germany. Once the system is established, the only government follow-up required is regular adjustments of tariffs.

Under quota systems, many of the requirements are far more challenging. Picking

optimal target levels is critical (if they are set too high, they can push prices up dramatically; if they are too low, they will not produce the economies of scale needed to reduce costs), as is the choice of timetables. The same can be said for the setting of tariffs under pricing laws. However, they can be established with input from research institutes and industries, and pricing laws can be created to allow for adjustments as necessary. As discussed below, targets set under quota systems are not as flexible. In addition, policy makers must decide which technologies are eligible, and if there should be technology-specific targets—this will depend on the readiness of technologies, their costs, available resources, and other factors. In order to make successful choices, it is also important to understand the cost and learning curves for the relevant renewable technologies. Policy makers also need to determine which category of parties must meet the obligation (e.g., retail suppliers, grid companies, or distribution companies), and whether all or just a few of those parties are required to meet the targets. The penalty for non-compliance must be established, and the tradability, life-span and price (floor- or ceiling-prices?) of certificates or credits chosen. These decisions will all determine the impact of the quota

11 Lauber, 2003

Issue Paper on Green Energy Pricing

© ERRA 2006 25

system. Once these matters are resolved, government agencies (or other bodies, e.g. Regulator) must certify renewable energy producers, issue and control certificates, monitor compliance, and collect penalties, all of which increases administrative requirements, complexities and costs.

Some argue that quota/certificate systems tend, by their very nature, to be more

complex than pricing systems, difficult to administer, and open to utility manipulation, and that such problems could be even more significant in developing countries. On the other hand, others have noted that the system for cost-equalization under the German Renewable Energy Law is neither simple nor transparent. Finally, it has been argued that bidding processes are bureaucratic, have significant transaction costs, and are time-consuming for authorities and renewable energy developers.

3.6.4. Flexibility

Historically, pricing laws have been criticized for being inflexible. For example, once tariffs are established, it could be difficult to reduce them. However, it is possible to set up the system such that payments can be adjusted on a regular basis to reflect changes in technologies and market conditions. This flexibility was incorporated into the German system in 2000, and is now featured in other national pricing systems as well. Thus, once a government sets the price to be paid for RES electricity, it is possible in the future to adjust these payments up or down to affect the amount of new capacity coming on line as desired.

On the other hand, with a quota system, once targets and timetables are established,

they are difficult to adjust. Even as markets change and technologies advance, experiencing major breakthroughs in efficiency and/or cost, it is highly unlikely that targets or timetables can be altered - or, at least made more ambitious—particularly without lead-times of several years.

3.6.5. Summary of pricing and quota systems analysis

Pricing systems

Arguments in favor

Arguments against

• To date, they have been most successful at developing renewables markets and domestic industries, and achieving the associated social, economic, environmental, and security benefits • Flexible – can be designed to account for changes in technology and the marketplace • Encourage steady growth of small- and medium-scale producers • Low transaction costs • Ease of financing • Ease of entry.

• If tariffs are not adjusted over time, consumers may pay unnecessarily high prices for renewable power • Can involve restraints on renewable energy trade due to domestic production requirements.

Issue Paper on Green Energy Pricing

© ERRA 2006 26

Quota systems

Arguments in favor Arguments against

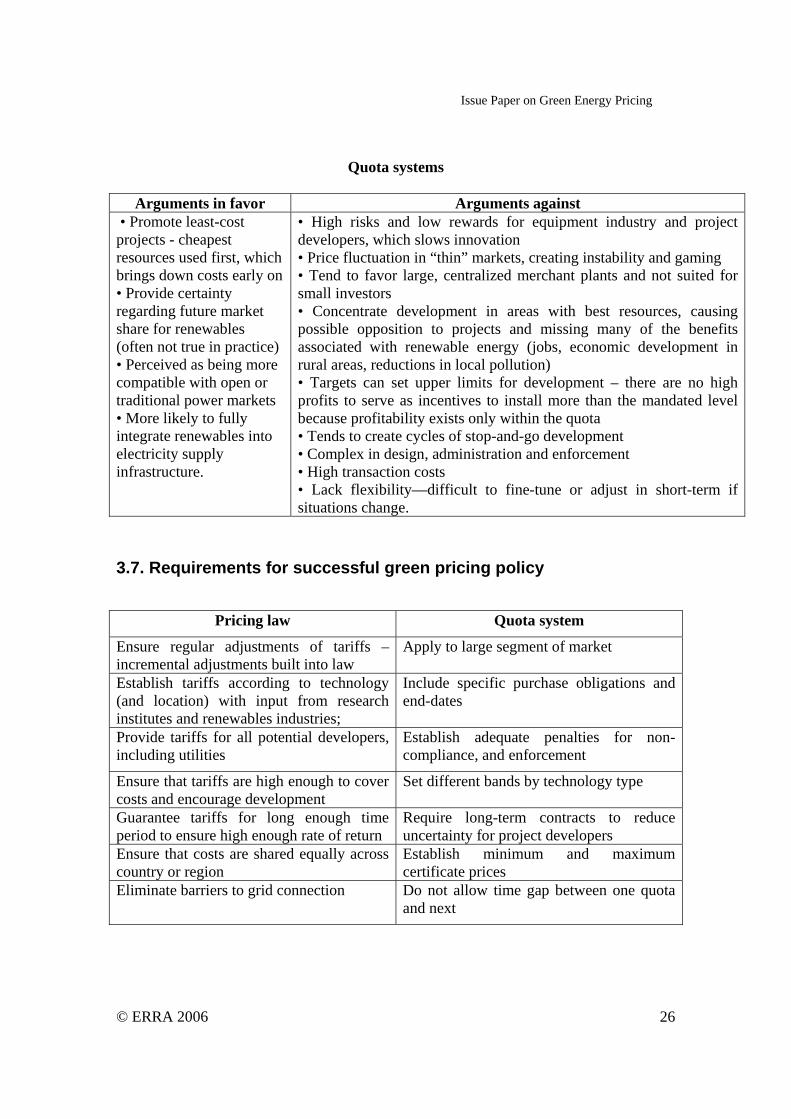

• Promote least-cost projects - cheapest resources used first, which brings down costs early on • Provide certainty regarding future market share for renewables (often not true in practice) • Perceived as being more compatible with open or traditional power markets • More likely to fully integrate renewables into electricity supply infrastructure.

• High risks and low rewards for equipment industry and project developers, which slows innovation • Price fluctuation in “thin” markets, creating instability and gaming • Tend to favor large, centralized merchant plants and not suited for small investors • Concentrate development in areas with best resources, causing possible opposition to projects and missing many of the benefits associated with renewable energy (jobs, economic development in rural areas, reductions in local pollution) • Targets can set upper limits for development – there are no high profits to serve as incentives to install more than the mandated level because profitability exists only within the quota • Tends to create cycles of stop-and-go development • Complex in design, administration and enforcement • High transaction costs • Lack flexibility—difficult to fine-tune or adjust in short-term if situations change.

3.7. Requirements for successful green pricing policy

Pricing law Quota system

Ensure regular adjustments of tariffs – incremental adjustments built into law

Apply to large segment of market

Establish tariffs according to technology (and location) with input from research institutes and renewables industries;

Include specific purchase obligations and end-dates

Provide tariffs for all potential developers, including utilities

Establish adequate penalties for non-compliance, and enforcement

Ensure that tariffs are high enough to cover costs and encourage development

Set different bands by technology type

Guarantee tariffs for long enough time period to ensure high enough rate of return

Require long-term contracts to reduce uncertainty for project developers

Ensure that costs are shared equally across country or region

Establish minimum and maximum certificate prices

Eliminate barriers to grid connection

Do not allow time gap between one quota and next

Issue Paper on Green Energy Pricing

© ERRA 2006 27

The most important for both systems is political stability, and long-term, credible, enforceable and consistent policies.

3.8. Importance of consistent, long-term policies It is important to note that policies enacted to advance renewable energy can slow