Embed Size (px)

Citation preview

GreeceTax Guide

2012

PKF Worldwide Tax Guide 2012I

foreword

A country’s tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there double tax treaties in place? How will foreign source income be taxed?

Since 1994, the PKF network of independent member firms, administered by PKF International Limited, has produced the PKF Worldwide Tax Guide (WWTG) to provide international businesses with the answers to these key tax questions. This handy reference guide provides clients and professional practitioners with comprehensive tax and business information for 100 countries throughout the world.

As you will appreciate, the production of the WWTG is a huge team effort and I would like to thank all tax experts within PFK member firms who gave up their time to contribute the vital information on their country’s taxes that forms the heart of this publication. I would also like thank Richard Jones, PKF (UK) LLP, Kevin Reilly, PKF Witt Mares, and Kaarji Vaughan, PKF Melbourne for co-ordinating and checking the entries from countries within their regions.

The WWTG continues to expand each year reflecting both the growth of the PKF network and the strength of the tax capability offered by member firms throughout the world.

I hope that the combination of the WWTG and assistance from your local PKF member firm will provide you with the advice you need to make the right decisions for your international business.

Jon HillsPKF (UK) LLPChairman, PKF International Tax Committee [email protected]

PKF Worldwide Tax Guide 2012 II

important disclaimer

This publication should not be regarded as offering a complete explanation of the taxation matters that are contained within this publication.

This publication has been sold or distributed on the express terms and understanding that the publishers and the authors are not responsible for the results of any actions which are undertaken on the basis of the information which is contained within this publication, nor for any error in, or omission from, this publication.

The publishers and the authors expressly disclaim all and any liability and responsibility to any person, entity or corporation who acts or fails to act as a consequence of any reliance upon the whole or any part of the contents of this publication.

Accordingly no person, entity or corporation should act or rely upon any matter or information as contained or implied within this publication without first obtaining advice from an appropriately qualified professional person or firm of advisors, and ensuring that such advice specifically relates to their particular circumstances.

PKF International is a network of legally independent member firms administered by PKF International Limited (PKFI). Neither PKFI nor the member firms of the network generally accept any responsibility or liability for the actions or inactions on the part of any individual member firm or firms.

PKF Worldwide Tax Guide 2012III

preface

The PKF Worldwide Tax Guide 2012 (WWTG) is an annual publication that provides an overview of the taxation and business regulation regimes of 100 of the world’s most significant trading countries. In compiling this publication, member firms of the PKF network have based their summaries on information current as of 30 September 2011, while also noting imminent changes where necessary.

On a country-by-country basis, each summary addresses the major taxes applicable to business; how taxable income is determined; sundry other related taxation and business issues; and the country’s personal tax regime. The final section of each country summary sets out the Double Tax Treaty and Non-Treaty rates of tax withholding relating to the payment of dividends, interest, royalties and other related payments.

While the WWTG should not to be regarded as offering a complete explanation of the taxation issues in each country, we hope readers will use the publication as their first point of reference and then use the services of their local PKF member firm to provide specific information and advice.

In addition to the printed version of the WWTG, individual country taxation guides are available in PDF format which can be downloaded from the PKF website at www.pkf.com

PKF INTERNATIONAL LIMITEDAPRIL 2012

©PKF INTERNATIONAL LIMITEDALL RIGHTS RESERVEDUSE APPROVED WITH ATTRIBUTION

PKF Worldwide Tax Guide 2012 IV

about pKf international limited

PKF International Limited (PKFI) administers the PKF network of legally independent member firms. There are around 300 member firms and correspondents in 440 locations in around 125 countries providing accounting and business advisory services. PKFI member firms employ around 2,200 partners and more than 21,400 staff.

PKFI is the 10th largest global accountancy network and its member firms have $2.6 billion aggregate fee income (year end June 2011). The network is a member of the Forum of Firms, an organisation dedicated to consistent and high quality standards of financial reporting and auditing practices worldwide.

Services provided by member firms include:

Assurance & AdvisoryCorporate FinanceFinancial PlanningForensic AccountingHotel ConsultancyInsolvency – Corporate & PersonalIT ConsultancyManagement ConsultancyTaxation

PKF member firms are organised into five geographical regions covering Africa; Latin America; Asia Pacific; Europe, the Middle East & India (EMEI); and North America & the Caribbean. Each region elects representatives to the board of PKF International Limited which administers the network. While the member firms remain separate and independent, international tax, corporate finance, professional standards, audit, hotel consultancy, insolvency and business development committees work together to improve quality standards, develop initiatives and share knowledge and best practice cross the network.

Please visit www.pkf.com for more information.

PKF Worldwide Tax Guide 2012V

structure of country descriptions

a. taXes payable

FEDERAL TAXES AND LEVIES COMPANY TAX CAPITAL GAINS TAX BRANCH PROFITS TAX SALES TAX/VALUE ADDED TAX FRINGE BENEFITS TAX LOCAL TAXES OTHER TAXES

b. determination of taXable income

CAPITAL ALLOWANCES DEPRECIATION STOCK/INVENTORY CAPITAL GAINS AND LOSSES DIVIDENDS INTEREST DEDUCTIONS LOSSES FOREIGN SOURCED INCOME INCENTIVES

c. foreiGn taX relief

d. corporate Groups

e. related party transactions

f. witHHoldinG taX

G. eXcHanGe control

H. personal taX

i. treaty and non-treaty witHHoldinG taX rates

PKF Worldwide Tax Guide 2012 VI

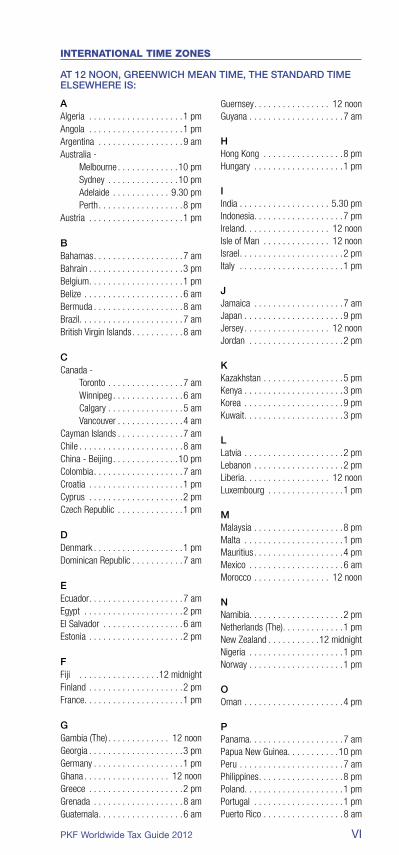

AAlgeria . . . . . . . . . . . . . . . . . . . .1 pmAngola . . . . . . . . . . . . . . . . . . . .1 pmArgentina . . . . . . . . . . . . . . . . . .9 amAustralia - Melbourne . . . . . . . . . . . . .10 pm Sydney . . . . . . . . . . . . . . .10 pm Adelaide . . . . . . . . . . . . 9.30 pm Perth . . . . . . . . . . . . . . . . . .8 pmAustria . . . . . . . . . . . . . . . . . . . .1 pm

BBahamas . . . . . . . . . . . . . . . . . . .7 amBahrain . . . . . . . . . . . . . . . . . . . .3 pmBelgium . . . . . . . . . . . . . . . . . . . .1 pmBelize . . . . . . . . . . . . . . . . . . . . .6 amBermuda . . . . . . . . . . . . . . . . . . .8 amBrazil. . . . . . . . . . . . . . . . . . . . . .7 amBritish Virgin Islands . . . . . . . . . . .8 am

CCanada - Toronto . . . . . . . . . . . . . . . .7 am Winnipeg . . . . . . . . . . . . . . .6 am Calgary . . . . . . . . . . . . . . . .5 am Vancouver . . . . . . . . . . . . . .4 amCayman Islands . . . . . . . . . . . . . .7 amChile . . . . . . . . . . . . . . . . . . . . . .8 amChina - Beijing . . . . . . . . . . . . . .10 pmColombia . . . . . . . . . . . . . . . . . . .7 amCroatia . . . . . . . . . . . . . . . . . . . .1 pmCyprus . . . . . . . . . . . . . . . . . . . .2 pmCzech Republic . . . . . . . . . . . . . .1 pm

DDenmark . . . . . . . . . . . . . . . . . . .1 pmDominican Republic . . . . . . . . . . .7 am

EEcuador . . . . . . . . . . . . . . . . . . . .7 amEgypt . . . . . . . . . . . . . . . . . . . . .2 pmEl Salvador . . . . . . . . . . . . . . . . .6 amEstonia . . . . . . . . . . . . . . . . . . . .2 pm

FFiji . . . . . . . . . . . . . . . . .12 midnightFinland . . . . . . . . . . . . . . . . . . . .2 pmFrance. . . . . . . . . . . . . . . . . . . . .1 pm

GGambia (The) . . . . . . . . . . . . . 12 noonGeorgia . . . . . . . . . . . . . . . . . . . .3 pmGermany . . . . . . . . . . . . . . . . . . .1 pmGhana . . . . . . . . . . . . . . . . . . 12 noonGreece . . . . . . . . . . . . . . . . . . . .2 pmGrenada . . . . . . . . . . . . . . . . . . .8 amGuatemala . . . . . . . . . . . . . . . . . .6 am

Guernsey . . . . . . . . . . . . . . . . 12 noonGuyana . . . . . . . . . . . . . . . . . . . .7 am

HHong Kong . . . . . . . . . . . . . . . . .8 pmHungary . . . . . . . . . . . . . . . . . . .1 pm

IIndia . . . . . . . . . . . . . . . . . . . 5.30 pmIndonesia. . . . . . . . . . . . . . . . . . .7 pmIreland . . . . . . . . . . . . . . . . . . 12 noonIsle of Man . . . . . . . . . . . . . . 12 noonIsrael . . . . . . . . . . . . . . . . . . . . . .2 pmItaly . . . . . . . . . . . . . . . . . . . . . .1 pm

JJamaica . . . . . . . . . . . . . . . . . . .7 amJapan . . . . . . . . . . . . . . . . . . . . .9 pmJersey . . . . . . . . . . . . . . . . . . 12 noonJordan . . . . . . . . . . . . . . . . . . . .2 pm

KKazakhstan . . . . . . . . . . . . . . . . .5 pmKenya . . . . . . . . . . . . . . . . . . . . .3 pmKorea . . . . . . . . . . . . . . . . . . . . .9 pmKuwait . . . . . . . . . . . . . . . . . . . . .3 pm

LLatvia . . . . . . . . . . . . . . . . . . . . .2 pmLebanon . . . . . . . . . . . . . . . . . . .2 pmLiberia . . . . . . . . . . . . . . . . . . 12 noonLuxembourg . . . . . . . . . . . . . . . .1 pm

MMalaysia . . . . . . . . . . . . . . . . . . .8 pmMalta . . . . . . . . . . . . . . . . . . . . .1 pmMauritius . . . . . . . . . . . . . . . . . . .4 pmMexico . . . . . . . . . . . . . . . . . . . .6 amMorocco . . . . . . . . . . . . . . . . 12 noon

NNamibia. . . . . . . . . . . . . . . . . . . .2 pmNetherlands (The) . . . . . . . . . . . . .1 pmNew Zealand . . . . . . . . . . .12 midnightNigeria . . . . . . . . . . . . . . . . . . . .1 pmNorway . . . . . . . . . . . . . . . . . . . .1 pm

OOman . . . . . . . . . . . . . . . . . . . . .4 pm

PPanama. . . . . . . . . . . . . . . . . . . .7 amPapua New Guinea. . . . . . . . . . .10 pmPeru . . . . . . . . . . . . . . . . . . . . . .7 amPhilippines . . . . . . . . . . . . . . . . . .8 pmPoland. . . . . . . . . . . . . . . . . . . . .1 pmPortugal . . . . . . . . . . . . . . . . . . .1 pmPuerto Rico . . . . . . . . . . . . . . . . .8 am

international time Zones

AT 12 NOON, GREENwICH MEAN TIME, THE sTANDARD TIME ELsEwHERE Is:

PKF Worldwide Tax Guide 2012VII

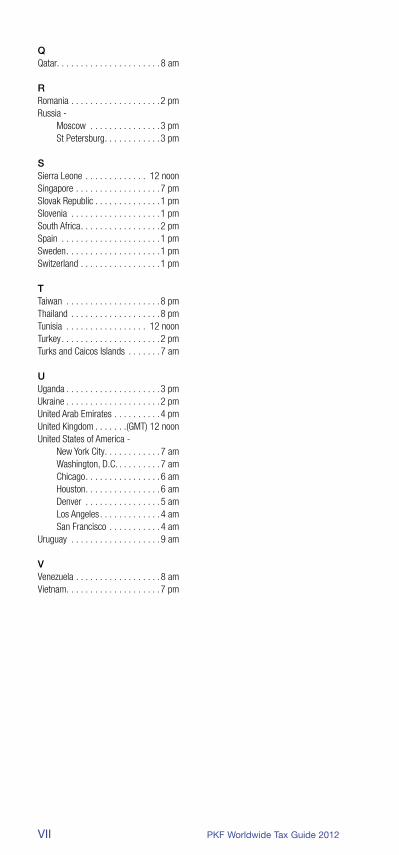

QQatar. . . . . . . . . . . . . . . . . . . . . .8 am

RRomania . . . . . . . . . . . . . . . . . . .2 pmRussia - Moscow . . . . . . . . . . . . . . .3 pm St Petersburg . . . . . . . . . . . .3 pm

sSierra Leone . . . . . . . . . . . . . 12 noonSingapore . . . . . . . . . . . . . . . . . .7 pmSlovak Republic . . . . . . . . . . . . . .1 pmSlovenia . . . . . . . . . . . . . . . . . . .1 pmSouth Africa . . . . . . . . . . . . . . . . .2 pmSpain . . . . . . . . . . . . . . . . . . . . .1 pmSweden . . . . . . . . . . . . . . . . . . . .1 pmSwitzerland . . . . . . . . . . . . . . . . .1 pm

TTaiwan . . . . . . . . . . . . . . . . . . . .8 pmThailand . . . . . . . . . . . . . . . . . . .8 pmTunisia . . . . . . . . . . . . . . . . . 12 noonTurkey . . . . . . . . . . . . . . . . . . . . .2 pmTurks and Caicos Islands . . . . . . .7 am

UUganda . . . . . . . . . . . . . . . . . . . .3 pmUkraine . . . . . . . . . . . . . . . . . . . .2 pmUnited Arab Emirates . . . . . . . . . .4 pmUnited Kingdom . . . . . . .(GMT) 12 noonUnited States of America - New York City . . . . . . . . . . . .7 am Washington, D.C. . . . . . . . . .7 am Chicago . . . . . . . . . . . . . . . .6 am Houston . . . . . . . . . . . . . . . .6 am Denver . . . . . . . . . . . . . . . .5 am Los Angeles . . . . . . . . . . . . .4 am San Francisco . . . . . . . . . . .4 amUruguay . . . . . . . . . . . . . . . . . . .9 am

VVenezuela . . . . . . . . . . . . . . . . . .8 amVietnam . . . . . . . . . . . . . . . . . . . .7 pm

PKF Worldwide Tax Guide 2012 1

Greece

Greece

Currency: Euro Dial Code To: 30 Dial Code Out: 00 (EUR)

Member Firm:City: Name: Contact Information:Athens Alexandros Sfarnas 210 748 0600 [email protected]

a. taXes payable

FEDERAL TAxEs AND LEVIEsCOMPANy TAxCompanies resident in Greece are subject to corporate income tax on their worldwide income and capital gains. Non-resident companies that have a permanent establishment in Greece are subject to corporate income tax on income and capital gains derived through the permanent establishment. A financial period is 12 months and usually coincides with the calendar year. In certain cases, however, it may start on 1 July and end on 30 June of the following year. Also, the financial period of a company in which a foreign enterprise has at least a 50% capital participation may coincide with that of the foreign enterprise.

The tax rates applicable to undistributed profits are as follows:

Public limited companies (SA) -20%

Banks 20% as above

Limited liability companies (EPE) 20% as above

Branches of foreign companies 20% as above

Distributed profits are subject to an additional income tax at 25%. Dividends paid to parent companies based in European countries are exempted from such tax.

Note: Income tax is payable in eight equal monthly instalments commencing in the fifth month from the end of the financial period in which the tax return must be filed.

CAPITAL GAINs TAxCapital gains are not taxed separately but are added to the company’s taxable income except for the following cases:(1) Gains from the sales of shares quoted on a Stock Exchange are currently taxed

at a rate of 0.15% of the sales proceeds. From 1 April 2012 these gains will be taxed in the same way as any other income. However such taxation has been postponed several times up to now.

(2) Sales of shares not quoted on a Stock Exchange are taxed separately at a rate of 5% on the sale value (i.e. gross proceeds). If this income is gained by a company, the above 5% tax is considered as a prepayment and the profits are taxed as any other taxable income.

(3) Profit from sales of (a) interests in any kind of company (except a public limited company), and (b) an enterprise as a whole, is taxed separately at a rate of 20%.

(4) Profit from the sale of a right, relevant to the operation of the enterprise, is taxed separately at a rate of 20%.

In cases (3) and (4), the profit is taxed together with other income if the seller is a public limited company.

sALEs TAx/VALUE ADDED TAx (VAT)VAT is charged on every supply of goods and services by a commercial enterprise, with the exception of the Aghion Oros area. The VAT rate is 23%, except for specific categories of goods and services for which the tax rate is 13% and 6.5% respectively. The above rates are reduced by 30% in certain circumstances. Public services (health, education, insurance etc.) are not subject to VAT. These services are considered VAT exempt. Exports of goods and services are zero-rated. VAT is collected at each stage of the process of production or distribution of goods and services. The burden of the tax falls on the ultimate consumer.

OTHER TAxEsInsurance business income is not subject to VAT but to turnover tax at a rate of 10%.

Each transfer of real estate is subject to transfer tax computed on the market value of the real estate at a rate of 10%. This tax is borne by the buyer. From 1 January 2006,

PKF Worldwide Tax Guide 20122

buildings (sale of new buildings only) are subject to VAT at 23%. Other buildings are subject to transfer tax at 10%.

Taxpayers are subject to a yearly charge based on the value of real property held. Starting from 2010, the tax rates applicable to companies are as follows: • Propertiesingeneral6/1000• Buildingsownedandusedforthepurposesofacommercialactivity1/1000• Hotels,forthebusinessyears2010,2011and2012,usedforbusiness

purposes 0.33/1000• Buildingsownedandusedbynot-for-profitlegalentities1/100• Individualsaresubjecttothechargeonaprogressivescale• TransactionsnotsubjecttoVATaresubjecttostampdutyatratesfrom1.2%

to 3.6%.

Companies pay contributions to the social security organisation (IKA) for their employees. The contribution is computed on the employee’s salaries at a rate of approximately 30%.

b. determination of taXable income

Taxable profits are determined by ascertaining total gross income and then subtracting allowable expenses. These expenses must be wholly incurred for the purposes of the enterprise. Below are some of the allowed deductions.

DEPRECIATIONFixed asset depreciation is computed annually at fixed rates, the most important of which are:• plantandotherbuildings5%–8%• machinery11%–15%• furniture15%–20%,officemachines15%–20%,computers24%–30% or 100%• privatecars11%–15%,trucksandbuses15%–20%.

sTOCK/INVENTORyStock is valued at the lower of acquisition cost or market value.

CAPITAL GAINs AND LOssEsCapital losses are deducted from the taxable trading income.

DIVIDENDsBefore 2011, no tax was charged on the receipt of dividends but distributed profits were subject to corporate tax at 40%.From 2011, dividends are subject to a dividend tax of 25% and the total of the company’s profits before distribution will be taxed at 20%.

INTEREsT DEDUCTIONsInterest on loans is generally tax deductible. Interest on loans from affiliated companies is tax deductible only to the extent that the loan does not exceed a debt:equity ratio of 3:1.

LOssEsLosses incurred in a financial year may be carried forward to be set off against profits of the following five financial years.

FOREIGN sOURCED INCOMEForeign sourced dividends are added to the taxable income of the company.

INCENTIVEsTax incentives are given if a company makes productive investments. There are two kinds of investments: state grants and tax reliefs.

The total amount of the support depends on the size of the enterprise and the geographical area.

Both incentives require a decision from the related authorities. The amount allocated every year for both grants and tax reliefs is limited.

c. foreiGn taX relief

The Greek tax liability is reduced by the tax actually paid in the foreign country on which the profits arose. Relief is restricted to the amount relating to the tax suffered on the profits in Greece.

Greece

PKF Worldwide Tax Guide 2012 3

d. corporate Groups

There are no special tax provisions for corporate groups.

e. related party transactions

When income from a related party transaction, at home or abroad, is not at arm’s length prices, a transfer pricing adjustment is carried out.

f. witHHoldinG taX

In the absence of Double Tax Treaties, withholding tax of 20% must be deducted from royalties paid to foreign enterprises or foreign persons not permanently established in Greece.

Withholding tax is also deducted from interest income at the following rates:• 10%onbankdepositsinEurodenominatedaccounts• 25%onanyothertypeofinterest.

Double taxation agreements contain specific provisions that confine the above mentioned withholding taxes.

G. eXcHanGe control

According to the EU Directives, there are no longer any exchange controls. Such controls still exist for transfers of capital to non-EU countries.

H. personal taX

An individual is subject to income tax on his total net income in Greece and abroad. Net income sourced in Greece is taxed irrespective of the residence of the individual. Income arising abroad is taxed if the relevant individual is a resident of Greece. The tax year is the calendar year.

Taxable income is established by deducting the following expenses, where applicable:- Social security contributions- Interest paid for buying a house (for the first time)- Medical care expenses.

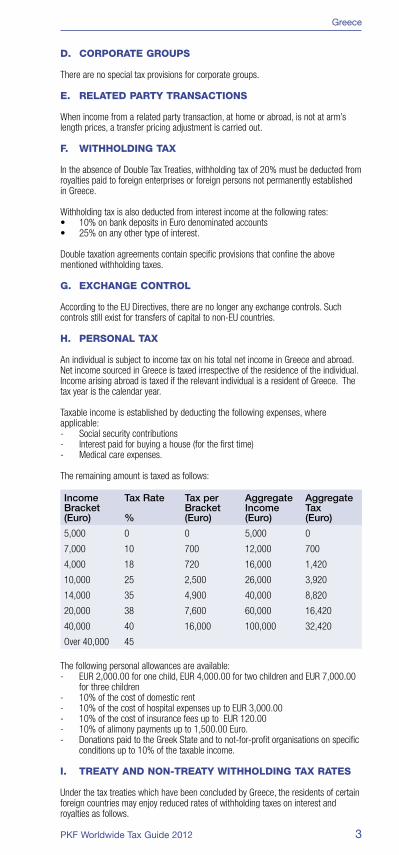

The remaining amount is taxed as follows:

Income Bracket(Euro)

Tax Rate

%

Tax per Bracket(Euro)

Aggregate Income(Euro)

Aggregate Tax(Euro)

5,000 0 0 5,000 0

7,000 10 700 12,000 700

4,000 18 720 16,000 1,420

10,000 25 2,500 26,000 3,920

14,000 35 4,900 40,000 8,820

20,000 38 7,600 60,000 16,420

40,000 40 16,000 100,000 32,420

Over 40,000 45

The following personal allowances are available:- EUR 2,000.00 for one child, EUR 4,000.00 for two children and EUR 7,000.00

for three children- 10% of the cost of domestic rent- 10% of the cost of hospital expenses up to EUR 3,000.00- 10% of the cost of insurance fees up to EUR 120.00 - 10% of alimony payments up to 1,500.00 Euro.- Donations paid to the Greek State and to not-for-profit organisations on specific

conditions up to 10% of the taxable income.

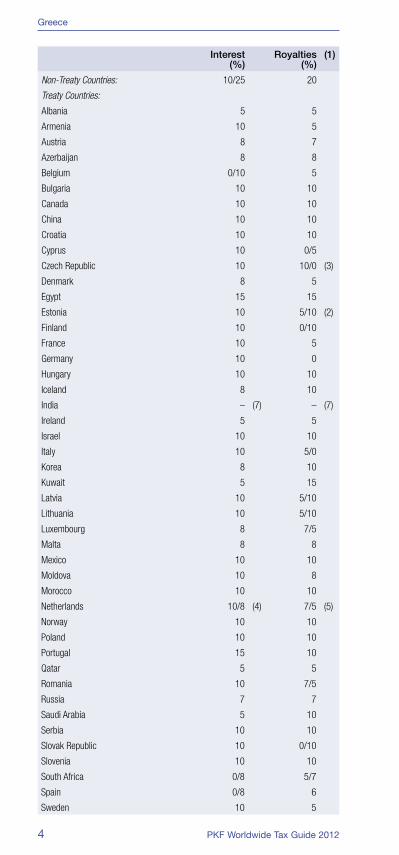

i. treaty and non-treaty witHHoldinG taX rates

Under the tax treaties which have been concluded by Greece, the residents of certain foreign countries may enjoy reduced rates of withholding taxes on interest and royalties as follows.

Greece

PKF Worldwide Tax Guide 20124

Interest(%)

Royalties(%)

(1)

Non-Treaty Countries: 10/25 20

Treaty Countries:

Albania 5 5

Armenia 10 5

Austria 8 7

Azerbaijan 8 8

Belgium 0/10 5

Bulgaria 10 10

Canada 10 10

China 10 10

Croatia 10 10

Cyprus 10 0/5

Czech Republic 10 10/0 (3)

Denmark 8 5

Egypt 15 15

Estonia 10 5/10 (2)

Finland 10 0/10

France 10 5

Germany 10 0

Hungary 10 10

Iceland 8 10

India – (7) – (7)

Ireland 5 5

Israel 10 10

Italy 10 5/0

Korea 8 10

Kuwait 5 15

Latvia 10 5/10

Lithuania 10 5/10

Luxembourg 8 7/5

Malta 8 8

Mexico 10 10

Moldova 10 8

Morocco 10 10

Netherlands 10/8 (4) 7/5 (5)

Norway 10 10

Poland 10 10

Portugal 15 10

Qatar 5 5

Romania 10 7/5

Russia 7 7

Saudi Arabia 5 10

Serbia 10 10

Slovak Republic 10 0/10

Slovenia 10 10

South Africa 0/8 5/7

Spain 0/8 6

Sweden 10 5

Greece

PKF Worldwide Tax Guide 2012 5

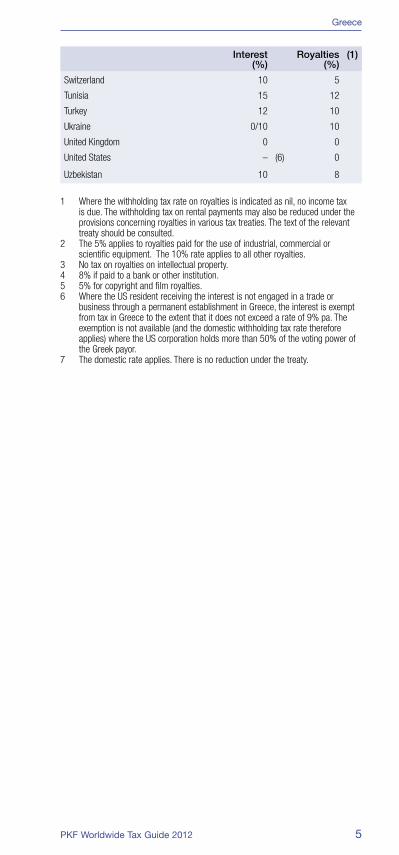

Interest(%)

Royalties(%)

(1)

Switzerland 10 5

Tunisia 15 12

Turkey 12 10

Ukraine 0/10 10

United Kingdom 0 0

United States – (6) 0

Uzbekistan 10 8

1 Where the withholding tax rate on royalties is indicated as nil, no income tax is due. The withholding tax on rental payments may also be reduced under the provisions concerning royalties in various tax treaties. The text of the relevant treaty should be consulted.

2 The 5% applies to royalties paid for the use of industrial, commercial or scientific equipment. The 10% rate applies to all other royalties.

3 No tax on royalties on intellectual property.4 8% if paid to a bank or other institution.5 5% for copyright and film royalties.6 Where the US resident receiving the interest is not engaged in a trade or

business through a permanent establishment in Greece, the interest is exempt from tax in Greece to the extent that it does not exceed a rate of 9% pa. The exemption is not available (and the domestic withholding tax rate therefore applies) where the US corporation holds more than 50% of the voting power of the Greek payor.

7 The domestic rate applies. There is no reduction under the treaty.

Grenada

Currency: Dollar Dial Code To: 1473 Dial Code Out: 011 (EC$)

Member Firm:City: Name: Contact Information:St George’s Henry A Joseph 440 4979 [email protected]

a. taXes payable

FEDERAL TAxEs AND LEVIEsCOMPANy TAxGrenadian resident companies are liable to income tax on all sources of non-exempt income wherever arising. A company is regarded as resident in Grenada if its central management and control is located and exercised in Grenada or if it was incorporated in Grenada. A non-resident company is taxed on income of a branch carrying on a trade or business in Grenada, i.e. the income arises in Grenada.

The rate of tax on companies is 30%. The tax year or ‘year of assessment’ is a period of 12 months commencing on 1 January in each year. Companies are assessed tax on their income that arises in the basis period. Where the company usually makes up its accounts for a period other than the calendar year, this period will be substituted for the calendar year. The company is expected to submit its tax return by the end of March or three months following the year of assessment and pay any balance of tax due. The company is required by law to make monthly advance payments of income tax based on the results of the preceding year (estimated tax). Any balance of tax is due and payable when the return is filed.

CAPITAL GAINs TAxThere is no income tax on capital gains secured on the disposal of capital assets. However, there is a transfer property tax of 5% of the value of property sold with or without improvement.

Aliens landholding tax: for foreign company buying into local company, the foreigner pays 15% and the local pays 10%.

Foreign buying into foreign: each pays 15%.

There is a 1% stamp duty charge

Greece

PKF Worldwide Tax Guide 2012 565

www.pkf.com$100