Embed Size (px)

Citation preview

Page 1 of 21

14 December 2016

HLIB Research

PP 9484/12/2012 (031413)

Greater KL’s Catalytic Developments

MARKET VIEW

14 December 2016

Game changer or spoiler?

Highlights Boosting Greater KL. Greater KL is the most populated region in

Malaysia with 7m people (26% of the nation). Since 2010, 9

projects under the Economic Transformation Program (ETP) have

kick started in Greater KL. Its public transport system is being

improved via the BRT, LRT ext, MRT 1&2 and HSR. Road

connectivity will also be enhanced through new highways such as

DASH, SUKE and DUKE3.

Rise of catalytic developments. As a result of Greater KL’s

rejuvenation, several large scale catalytic developments have

emerged. These include the Tun Razak Exchange (TRX), Warisan

Merdeka, Bukit Bintang City Centre (BBCC), Bandar Malaysia,

Kwasa Damansara and Cyberjaya City Centre (CCC). Collectively,

these 6 catalytic developments have a GDV of at least RM275bn

over 3,355 acres of land.

Backed by the government. All the catalytic developments have

government participation as the master developer, be it directly

(e.g. MoF) or indirectly via its related entities (e.g. EPF and PNB).

As such, we reckon that much effort will be accorded to ensure its

success. Tax incentives will be given for developments such as

TRX and Bandar Malaysia. Take up rates will also be supported by

the relocation of government offices there (e.g. EPF relocating its

HQ to Kwasa Damansara and PNB to Warisan Merdeka).

The age of TOD. These catalytic developments will be integrated

to a public transport network, giving them an advantage as Transit

Oriented Developments (TOD). The case of KL Sentral as a TOD is

anecdotal evidence on the importance of public transport

connectivity towards a development’s success. We believe the

appeal of TODs will be even more prevalent once the MRT1 is

completed in July 2017.

Sector

Impact

Positive for construction. Assuming 50% of GDV constitutes

construction cost, these catalytic developments would present

contractors with RM137bn worth of jobs to undertake over the next

20 years. Potential beneficiaries are (i) WCT and Gadang for their

track record in earthworks, (ii) IJM, Pesona, Mitrajaya and SunCon

for urban high rise buildings and (iii) pilling contractors such as

Pintaras, Econpile and Ikhmas Jaya.

Negative for property… KL city is experiencing a potential excess

supply situation within the condo and office segments. Traditional

developments will have to compete with the catalytic ones which

have an edge as TODs and government backing. Nonetheless,

most developers under our coverage have a diversified product mix

spread across several states. For risk of concentrated exposure,

we highlight UOA within the office segment.

…and REITs as well. KL city’s retail space per capita (17sq ft) is

already above Bangkok (9 sq ft) and Singapore (12 sq ft).

Additional malls under the catalytic developments will further

increase this, capping upside to rental reversion. Despite this,

established malls in prime locations such as Pavilion (PREIT) and

Suria KLCC (KLCCSS) should continue stay relevant. On offices,

the influx of new space will place downward pressure on

occupancy and rent. MQREIT has 80% of its revenue from office

and KLCCSS at 44%.

Jeremy Goh, CFA

(603) 2168 1138

Jason Tan, CFA

(603) 2176 2751

Lee Meng Horng

(603) 2168 1121

Catalytic developments

Development Acres GDV (RM bn)

Tun Razak Exchange 70 40

Warisan Merdeka 19 5

Bukit Bintang City Centre 19 9

Bandar Malaysia 486 160

Kwasa Damansara 2,620 50

Cyberjaya City Centre 141 11

Total 3,355 275

Source: HLIB estimates

Potential construction winners

Stock Rating Price Target

IJM BUY 3.37 3.92 WCT HOLD 1.80 1.99 Pesona BUY 0.585 0.81 Mitrajaya BUY 1.23 1.95 SunCon BUY 1.70 1.93 Pintaras Not Rated 3.50 n.a. Econpile Not Rated 1.85 n.a. Ikhmas Not Rated 0.58 n.a.

Potential property and REIT losers

Stock Rating Price Target

MQREIT BUY 1.30 1.34 KLCCSS BUY 7.81 8.35 UOA Dev Not Rated 2.30 n.a.

HLIB Research | Greater KL Catalytic Developments

www.hlebroking.com

Page 2 of 21

14 December 2016

Prelude

Enter Greater KL. Klang Valley is an area centred in Kuala Lumpur (KL) along with its

adjourning cities and towns in Selangor. Rebranded in recent times as Greater KL, the

area covers 2,793 sq km and is governed by 10 local authorities. It is Malaysia’s most

populated region with 7.2m people or 26% of the national population. Greater KL’s

population is projected to hit 10m by the turn of the decade.

Figure #1 Area coverage of Greater KL

PEMANDU

Key area under ETP. In Sept 2010, Malaysia’s Economic Transformation Programme

(ETP) was launched with the aim to elevate it to a “developed nation” status by 2020

with GNI per capita of US$15k. Greater KL has been identified as one of the ETP’s

National Key Economic Areas (NKEA) which targets to achieve the top-20 ranking in

city economic growth while also being the global top-20 most liveable cities by 2020. A

total of 9 Entry Point Projects (EPPs) have been identified for Greater KL.

Figure #2 Entry Point Projects (EPP) for Greater KL

Entry Point Project (EPP) 2020 GNI (m) Jobs Status

Attracting 100 of the world's most dynamic firms 41,441 234,001 Operational

Attracting internal and external talent 118,212 560 Operational

Connecting KL to Singapore v ia HSR 6,224 28,700 WIP

Building an integrated urban MRT system 24,630 20,000 WIP

Revitalising Klang and Gombak rivers 4,281 17,041 WIP

Greening Greater KL 992 2,817 Operational

Creating iconic places and attractions 460 13,500 WIP

Creating a comprehensive pedestrian network 6 279 Operational

Efficient solid waste management system 157 NA WIP

PEMANDU

Enhancing connectivity. Greater KL’s public transport landscape is currently

undergoing a massive upgrade. This began with the completion of the Sunway BRT in

June 2015, followed by the Ampang and Kelana LRT extensions totalling 35km in June

2016. Phase 1 of the MRT1 (Sg Buloh-Kajang) is set to be finished by Dec 2016 and

fully operational by July 2017. For the MRT2 (Sg Buloh-Serdang-Putrajaya), major

contracts have been awarded and work has begun. Lastly, implementation of the High

Speed Rail would greatly enhance connectivity between KL and Singapore. In terms of

road networks, major highways such as DASH (Damansara-Shah Alam), SUKE (Sg

Besi-Ulu Kelang) and DUKE3 (Setiawangsa-Pantai) are being implemented.

Greater KL is the most

populated region in M’sia

Several ETP projects have

been implemented in Greater

KL

Transportation upgrade via

BRT, LRT ext, MRT1&2, HSR,

DASH, SUKE and DUKE3

HLIB Research | Greater KL Catalytic Developments

www.hlebroking.com

Page 3 of 21

14 December 2016

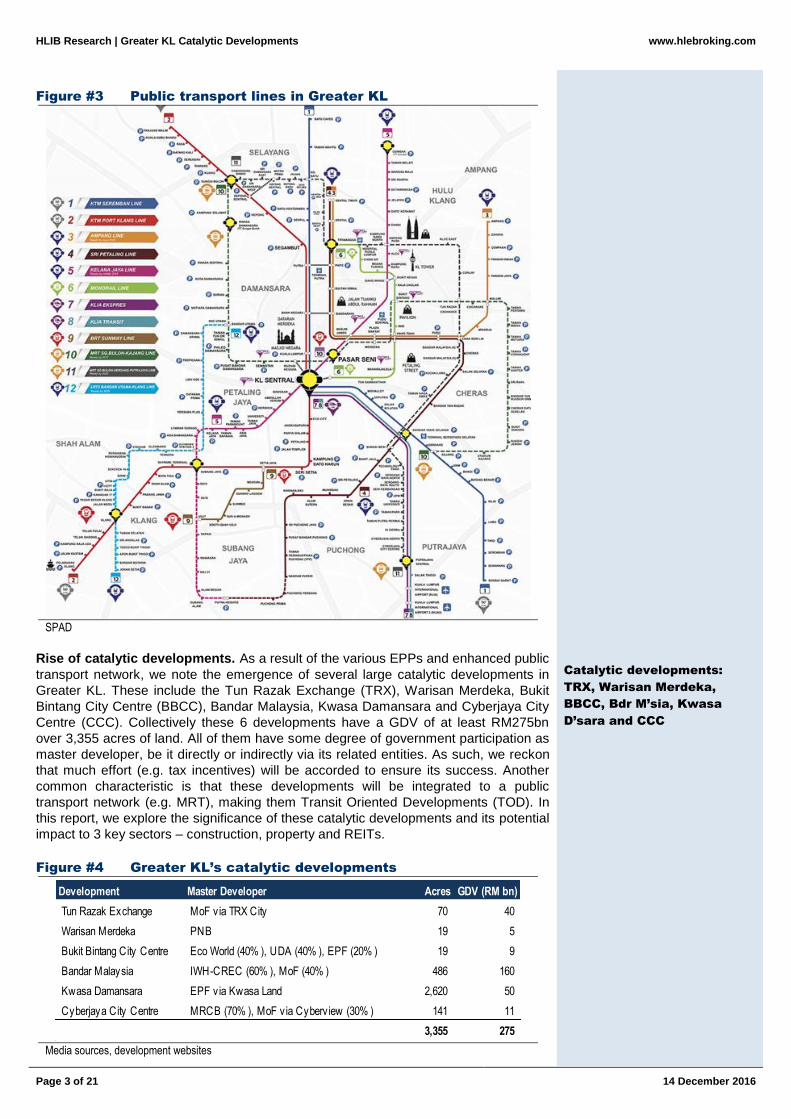

Figure #3 Public transport lines in Greater KL

SPAD

Rise of catalytic developments. As a result of the various EPPs and enhanced public

transport network, we note the emergence of several large catalytic developments in

Greater KL. These include the Tun Razak Exchange (TRX), Warisan Merdeka, Bukit

Bintang City Centre (BBCC), Bandar Malaysia, Kwasa Damansara and Cyberjaya City

Centre (CCC). Collectively these 6 developments have a GDV of at least RM275bn

over 3,355 acres of land. All of them have some degree of government participation as

master developer, be it directly or indirectly via its related entities. As such, we reckon

that much effort (e.g. tax incentives) will be accorded to ensure its success. Another

common characteristic is that these developments will be integrated to a public

transport network (e.g. MRT), making them Transit Oriented Developments (TOD). In

this report, we explore the significance of these catalytic developments and its potential

impact to 3 key sectors – construction, property and REITs.

Figure #4 Greater KL’s catalytic developments

Development Master Developer Acres GDV (RM bn)

Tun Razak Exchange MoF v ia TRX City 70 40

Warisan Merdeka PNB 19 5

Bukit Bintang City Centre Eco World (40% ), UDA (40% ), EPF (20% ) 19 9

Bandar Malaysia IWH-CREC (60% ), MoF (40% ) 486 160

Kwasa Damansara EPF v ia Kwasa Land 2,620 50

Cyberjaya City Centre MRCB (70% ), MoF v ia Cyberv iew (30% ) 141 11

3,355 275

Media sources, development websites

Catalytic developments:

TRX, Warisan Merdeka,

BBCC, Bdr M’sia, Kwasa

D’sara and CCC

HLIB Research | Greater KL Catalytic Developments

www.hlebroking.com

Page 4 of 21

14 December 2016

Highlights

Tun Razak Exchange

KL’s next financial district. Launched by the Prime Minister in July 2012, the Tun

Razak Exchange (TRX) sits on a 70-acre land plot located at KL’s southern gateway.

The development aspires to be KL’s financial and business district with GDV of

RM40bn over a period of 15-20 years. Essentially, TRX can be viewed as an extension

of KL’s Golden Triangle with direct connectivity via the largest MRT interchange station

(Line 1 and 2) and major highways such as SMART, MRR2, Jln Tun Razak, Jln Bukit

Bintang and Jln Sultan Ismail. TRX has been identified as a strategic priority for

Malaysia and a special task force has been assembled to facilitate its execution.

Figure #5 Location of TRX

TRX

Shareholding reshuffling. Previously, the master developer for TRX was 1MDB Real

Estate (1MDB-RE), a subsidiary of 1Malaysia Development Bhd (1MDB) which in turn,

is wholly owned by the Ministry of Finance (MoF). However, following a minor

shareholding reshuffling, 1MDB-RE was renamed to TRX City and is now directly

owned by the MoF with no ties to 1MDB. We view this change positively given the

ongoing controversies surrounding its previous direct parent-co, 1MDB.

Offerings on the plate. The TRX masterplan consist of 26 buildings with over 21m sq

ft of GFA spread across office (10m sq ft), residential (3.8k units), hotel (2m sq ft),

retail, F&B and cultural offerings. An allocation of 24% (16.8 acres) of the site will be

dedicated for parks and open spaces. Phase 1 which will be completed in 2018

comprises (i) 4 office towers, (ii) retail mall, (iii) 2 hotels and (iv) 6 residential towers.

KL’s next financial district is

an ext of the Golden Triangle

TRX no longer 1MDB,

directly under MoF

26 buildings with GFA of 21m

sq ft

HLIB Research | Greater KL Catalytic Developments

www.hlebroking.com

Page 5 of 21

14 December 2016

Figure #6 TRX masterplan

The Star

Attractive tax incentives. To attract investors into TRX, the government has granted

tax incentives for qualifying TRX marquee status companies operating in the financial

subsectors of banking (retail, merchant and Islamic), insurance, Takaful and capital

markets. These incentives include (i) industrial building allowances on purchase or

construction of property in TRX for use of their business at 10% p.a., (ii) accelerated

capital allowances of 100% over 2 years for renovation costs, (iii) deductions for

relocation costs, (iv) 150% deductions on rental of TRX premises for 10 years and (v)

stamp duty exemption (including on loan and services agreement). Besides, qualifying

developers will receive a 70% tax exemption on income derived from sale or rental of

properties in TRX for a period of 5 years.

Several commitments made. Since the TRX’s inception in mid-2012, there have been

5 notable investment commitments made with known land transaction values ranging

between RM2,774 to RM4,683 psf. These include

Lendlease: Australian based Lendlease will jointly develop the Lifestyle

Quarters with TRX City on a 60:40 basis. The RM8bn GDV quarters will span

16.8 acres, featuring a mall, hotel and 3 residential towers.

Mulia Group: The Indonesian property developer purchased a 3.4 acre land

for RM665m (RM4,490 psf) to undertake the Signature Tower (GDV: RM3.5bn)

with a height that approximates that of the Petronas Twin Towers.

Affin Bank: The bank acquired 1.25 acres of TRX land for RM255m (RM4,683

psf) to house its new 35-storey headquarter with GFA of 823k sq ft.

WCT Holdings: WCT (HOLD, TP: RM1.99) acquired several plots of TRX land

totalling 1.65 acres for RM223m (RM3,011 psf) which will be paid for via

contract works. It intends to develop a service residence (GDV: RM1.1bn).

Lembaga Tabung Haji: The pilgrimage fund (LTH) purchased 1.6 acres of

TRX land for RM189m (RM2,774 psf). Earlier plans to sell the land have been

aborted by LTH which now says it will be developing residential apartments

(GDV: RM828m).

Tax incentives for TRX

marquee status companies

and qualifying developers

Land transactions ranged

from RM2,700-4,700 psf

HLIB Research | Greater KL Catalytic Developments

www.hlebroking.com

Page 6 of 21

14 December 2016

Figure #7 Land transactions at TRX

Acquirer Acres Price RM psf Plot Ratio Est GDV

Lendlease 16.80 n.a. n.a. n.a. 8,000

Mulia Group 3.40 665 4,490 18.5 3,500

Affin Bank 1.25 255 4,683 15.2 n.a.

WCT Holdings 1.70 223 3,011 10.8 1,100

Lembaga Tabung Haji 1.56 189 2,774 10.5 828

Average (ex. Lendlease) 3,740 TRX, Media sources

Works ongoing, WCT the biggest beneficiary. Construction works at TRX are

currently ongoing with WCT emerging as the biggest beneficiary from its job flows thus

far. Since 2013, WCT has managed to secure 3 contracts at TRX totalling RM994m

involving earthworks, infrastructure and roads. According to an article by The Edge last

month, foundation works on the Signature Tower were completed in May and the

superstructure is now underway. AWC (not rated) was awarded an RM18m contract to

install and maintain the tower’s cold water and plumbing.

Figure #8 TRX site progress as at 30 June 2016

TRX

More incoming job flows. An article by The Edge in Oct stated that the entire

underground infrastructure works for TRX would amount to RM1bn. The job is said to

also involve the KL City Council but TRX City has decided to kick start its own portion

first by calling for RM350-400m worth of tenders. Work scope on the underground

infrastructure is regarded to be complex as a portion of it will run below the SMART

Tunnel and the MRT interchange station also needs to be accounted for. The deadline

for bids was closed on 1st July which required bidders to have (i) at least 10 years of

experience, (ii) CIDB G7 license, (iii) track record in rock excavation, tunnel concrete

structures, underpass and elevated structures, (iv) main contractor role for at least a

RM200m job and (v) foreign equity (if any) to be capped at 49% for JV. Track record

wise, Gamuda (BUY, TP: RM5.65) stands out as a contender for the job given its

tunnelling experience beneath KL for SMART and MRT1. Other contractors with

experience for heavy infrastructure include IJM (BUY, TP: RM3.92), SunCon (BUY, TP:

RM1.93) and WCT.

WCT has won 3 TRX

contracts worth RM1bn

Underground infra works for

TRX worth RM1bn

HLIB Research | Greater KL Catalytic Developments

www.hlebroking.com

Page 7 of 21

14 December 2016

Warisan Merdeka

Sky-scraping new heights. Warisan Merdeka is a mixed development undertaken by

Pemodalan Nasional Bhd (PNB) which will house the iconic Merdeka PNB118 tower.

Upon completion, Merdeka PNB118 will be the tallest building in Malaysia at 630m or

178m higher than the Petronas Twin Towers. It will also be the 2nd tallest tower in Asia

and 5th in the list of “mega-tall” buildings globally.

Connected by 3 rail lines. The development is located on a 19 acre land plot adjacent

to the historic Stadium Merdeka and Stadium Negara. Connectivity wise, Warisan

Merdeka will have its own dedicated MRT station (dubbed the “Merdeka station”) as

part of the MRT1. The Merdeka station will also serve as an interchange for the LRT

Ampang line and Monorail.

Figure #9 Location of Warisan Merdeka

KiniBiz , The Star

Phase 1: Tower and mall. Phase 1 of Warisan Merdeka will have a GDV of RM5bn

comprising Merdeka PNB118 tower and a shopping mall. The 118-storey tower will be

allocated as follows: (i) 82 floors (1.7m sq ft) of office space in which companies under

the PNB Group will take up 60 floors, (ii) 18 floors (435k sq ft) for a 6-star hotel with

236 rooms and (iii) 18 floors for an observation deck, sky lobby and to accommodate

M&E facilities. As for the proposed mall, it will have a GFA of 900k sq ft with over 200

stores and a 12-screen cinema.

Figure #10 Floor allocation for Merdeka PNB118

Office - PNB Group

60

Office - Others22

Hotel18

Deck & Sky Lobby

2

M&E16

Malay Mail

PNB118 will be the tallest

building in M’sia, 5th globally

Connected vi MRT, LRT and

monorail

Phase 1 comprising tower

and mall has GDV of RM5bn

HLIB Research | Greater KL Catalytic Developments

www.hlebroking.com

Page 8 of 21

14 December 2016

Contracts dished out. The foundation works (RM74m) for Merdeka PNB118 was

completed by Pintaras Jaya (not-rated) in 3Q15. Last Oct, the main tower contract was

awarded to the Samsung-UEM JV for RM2.1bn. Other job flows related to the tower

include (i) 2 contracts worth RM72m for plumbing and solid waste handling system

awarded to AWC, (ii) structural steel works (RM328m) secured by Eversendai (HOLD,

TP: RM0.54) and (iii) Finnish company, KONE to supply 105 units of elevators and

escalators. Looking ahead, our channel checks reveal that other potential contracts

from Warisan Merdeka would include the mall, access roads and infrastructure works.

Bukit Bintang City Centre

Pudu Jail’s transformation. The Pudu Jail was constructed in 1895 on a former

Chinese burial ground where it served as a prison for over a century until 1996. By Dec

2012, all buildings within the Pudu Jail were demolished to pave way for a

redevelopment plan to be led by UDA Holdings (not rated). The Pudu Jail site is

regarded as one of the last huge land parcels remaining in the heart of KL. Early last

year, a JV was established between UDA (40%), Eco World (40%) and the Employees

Provident Fund (20%) to jointly develop the said land in what is now known as Bukit

Bintang City Centre (BBCC). As the landowner, UDA will charge the JV a development

fee totalling RM1bn.

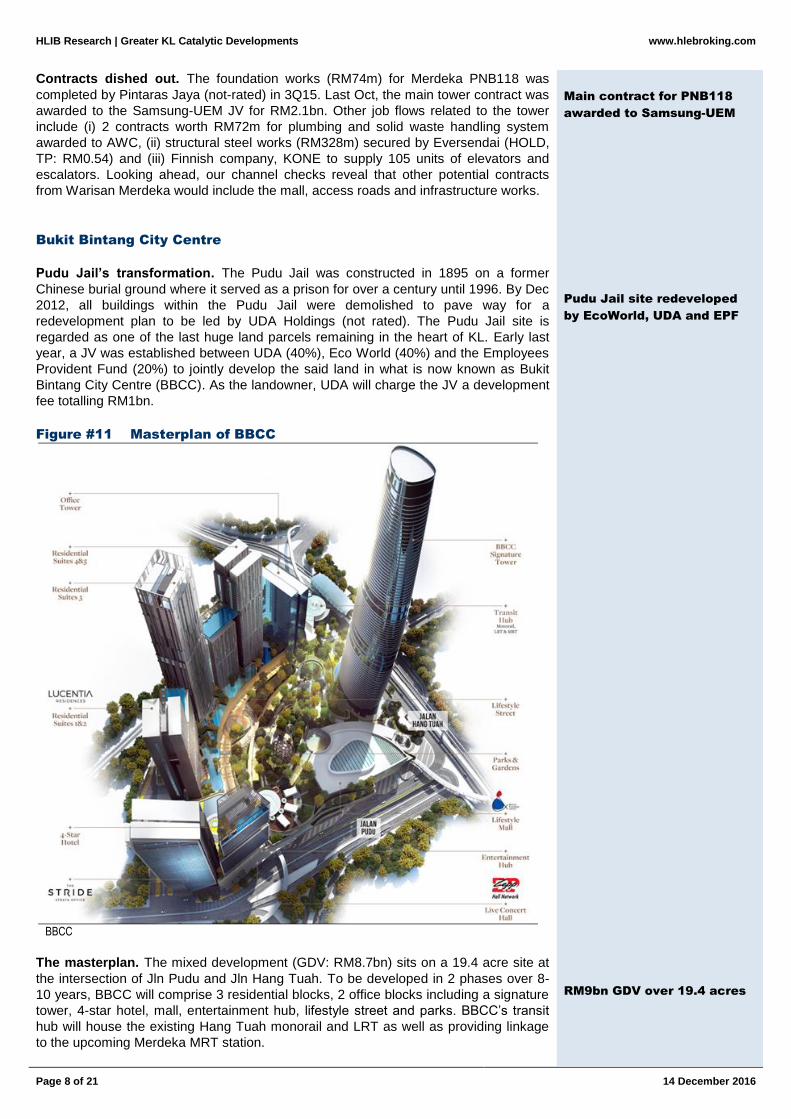

Figure #11 Masterplan of BBCC

BBCC

The masterplan. The mixed development (GDV: RM8.7bn) sits on a 19.4 acre site at

the intersection of Jln Pudu and Jln Hang Tuah. To be developed in 2 phases over 8-

10 years, BBCC will comprise 3 residential blocks, 2 office blocks including a signature

tower, 4-star hotel, mall, entertainment hub, lifestyle street and parks. BBCC’s transit

hub will house the existing Hang Tuah monorail and LRT as well as providing linkage

to the upcoming Merdeka MRT station.

Main contract for PNB118

awarded to Samsung-UEM

Pudu Jail site redeveloped

by EcoWorld, UDA and EPF

RM9bn GDV over 19.4 acres

HLIB Research | Greater KL Catalytic Developments

www.hlebroking.com

Page 9 of 21

14 December 2016

Plans for Phase 1. For the office portion of Phase 1, The Stride will consist of a 45-

storey tower with 347 strata units and build-ups ranging from 917-1,152 sq ft. As for the

residential component, there will be 2 blocks of 47 and 33-storeys totalling 680 units

with sizes from 450-850 sq ft. The residential units are said to be priced around

RM1,600 psf. Launches were initially scheduled for Oct 2016 but our channel checks

indicate that an official one has not happened. Our site check reveals that BBCC’s

show units are currently opened for viewing.

Figure #12 GDV breakdown for BBCC (RM bn)

Phase 1 - office and residential

2.0

Mall1.6

Entertainment hub0.4

Phase 24.7

The Star, HLIB estimates

Japanese roped in. In March 2016, the BBCC JV consortium inked an agreement with

Japan based Mitsui Fudosan Asia and Zepp Hall Network. Mitsui will be undertaking its

largest retail investment outside Japan by jointly building BBCC’s mall with the JV

consortium, each holding a 50% stake. Work on the RM1.6bn mall is expected to start

in 2017. The 1.4m sq ft mall with 300 stores will bring in popular Japanese brands and

is expected to open in 2021. On the other hand, BBCC’s RM400m entertainment hub

will house a concert hall which will be run by Sony’s Zepp Hall via a 20-year lease.

Bandar Malaysia

Redevelopment of Sg Besi Airport. Sg Besi Airport served as KL’s main airport from

1952 to 1965 and was subsequently used by the Royal Malaysian Air Force (RMAF).

The RMAF base is being relocated to Sendayan, Negeri Sembilan to pave way for a

redevelopment in what would be known as Bandar Malaysia. The redevelopment

covers 16 adjacent land plots totalling 486 acres located along Jln Sg Besi and 7km

from KL city centre.

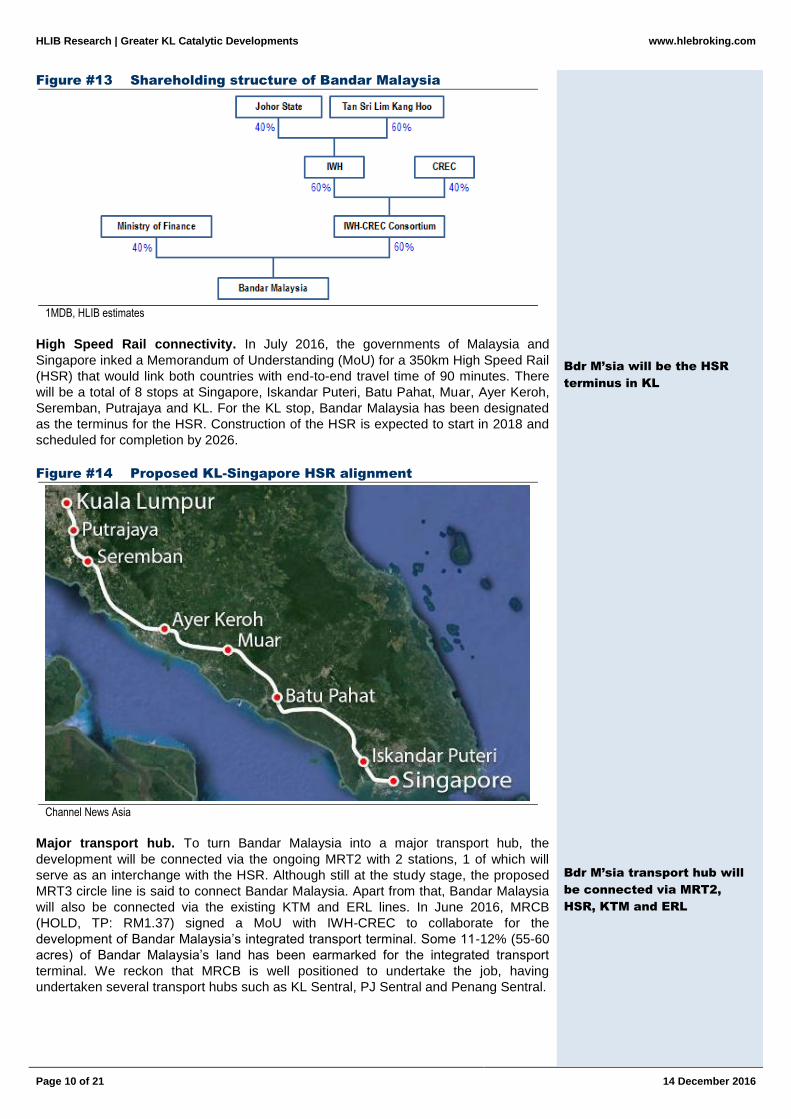

New master developer enters. Initially, 1MDB was supposed to be the master

developer for Bandar Malaysia. However, following 1MDB’s restructuring plan, an

agreement was inked in Dec 2015 to sell the land to an SPV comprising MoF (40%)

and IWH-CREC Consortium (60%). The consortium is in turn, 60% held by Iskandar

Waterfront Holdings (IWH) and 40% by construction giant, China Railway Engineering

Corp (CREC). To dwell further, the shareholders of IWH are state owned Kumpulan

Prasarana Rakyat Johor (40%) and Credence Resources (60%). The latter is a vehicle

wholly owned by Tan Sri Lim Kang Hoo who also owns several listed entities such as

Iskandar Waterfront City (not-rated) and Ekovest (not-rated). A detailed shareholding

structure of Bandar Malaysia is depicted in the following page.

Land valuation. IWH-CREC’s 60% stake in Bandar Malaysia was acquired at a

consideration of RM7.4bn or RM5.3bn if liabilities (Sukuk and RMAF base relocation

cost) are assumed. Using the former number (i.e. free of encumbrances), this

effectively values the entire Bandar Malaysia land at RM12.4bn or RM583 psf.

Phase 1 consist strata office

and condos, show units open

Japanese names such as

Mitsui and Sony to

participate

Sg Besi Airport to be

redeveloped into Bdr M’sia

1MDB out, now developed by

IWH-CREC and MoF

Land sold to new master

developer at RM583 psf

HLIB Research | Greater KL Catalytic Developments

www.hlebroking.com

Page 10 of 21

14 December 2016

Figure #13 Shareholding structure of Bandar Malaysia

1MDB, HLIB estimates

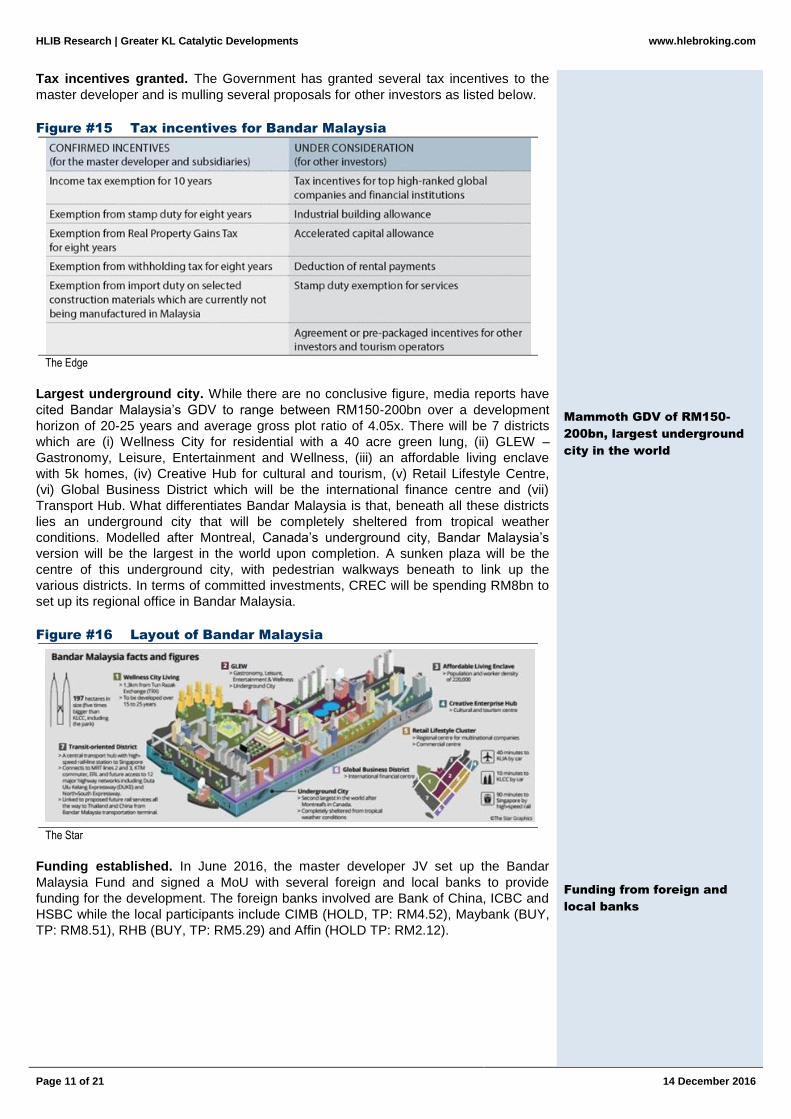

High Speed Rail connectivity. In July 2016, the governments of Malaysia and

Singapore inked a Memorandum of Understanding (MoU) for a 350km High Speed Rail

(HSR) that would link both countries with end-to-end travel time of 90 minutes. There

will be a total of 8 stops at Singapore, Iskandar Puteri, Batu Pahat, Muar, Ayer Keroh,

Seremban, Putrajaya and KL. For the KL stop, Bandar Malaysia has been designated

as the terminus for the HSR. Construction of the HSR is expected to start in 2018 and

scheduled for completion by 2026.

Figure #14 Proposed KL-Singapore HSR alignment

Channel News Asia

Major transport hub. To turn Bandar Malaysia into a major transport hub, the

development will be connected via the ongoing MRT2 with 2 stations, 1 of which will

serve as an interchange with the HSR. Although still at the study stage, the proposed

MRT3 circle line is said to connect Bandar Malaysia. Apart from that, Bandar Malaysia

will also be connected via the existing KTM and ERL lines. In June 2016, MRCB

(HOLD, TP: RM1.37) signed a MoU with IWH-CREC to collaborate for the

development of Bandar Malaysia’s integrated transport terminal. Some 11-12% (55-60

acres) of Bandar Malaysia’s land has been earmarked for the integrated transport

terminal. We reckon that MRCB is well positioned to undertake the job, having

undertaken several transport hubs such as KL Sentral, PJ Sentral and Penang Sentral.

Bdr M’sia will be the HSR

terminus in KL

Bdr M’sia transport hub will

be connected via MRT2,

HSR, KTM and ERL

HLIB Research | Greater KL Catalytic Developments

www.hlebroking.com

Page 11 of 21

14 December 2016

Tax incentives granted. The Government has granted several tax incentives to the

master developer and is mulling several proposals for other investors as listed below.

Figure #15 Tax incentives for Bandar Malaysia

The Edge

Largest underground city. While there are no conclusive figure, media reports have

cited Bandar Malaysia’s GDV to range between RM150-200bn over a development

horizon of 20-25 years and average gross plot ratio of 4.05x. There will be 7 districts

which are (i) Wellness City for residential with a 40 acre green lung, (ii) GLEW –

Gastronomy, Leisure, Entertainment and Wellness, (iii) an affordable living enclave

with 5k homes, (iv) Creative Hub for cultural and tourism, (v) Retail Lifestyle Centre,

(vi) Global Business District which will be the international finance centre and (vii)

Transport Hub. What differentiates Bandar Malaysia is that, beneath all these districts

lies an underground city that will be completely sheltered from tropical weather

conditions. Modelled after Montreal, Canada’s underground city, Bandar Malaysia’s

version will be the largest in the world upon completion. A sunken plaza will be the

centre of this underground city, with pedestrian walkways beneath to link up the

various districts. In terms of committed investments, CREC will be spending RM8bn to

set up its regional office in Bandar Malaysia.

Figure #16 Layout of Bandar Malaysia

The Star

Funding established. In June 2016, the master developer JV set up the Bandar

Malaysia Fund and signed a MoU with several foreign and local banks to provide

funding for the development. The foreign banks involved are Bank of China, ICBC and

HSBC while the local participants include CIMB (HOLD, TP: RM4.52), Maybank (BUY,

TP: RM8.51), RHB (BUY, TP: RM5.29) and Affin (HOLD TP: RM2.12).

Mammoth GDV of RM150-

200bn, largest underground

city in the world

Funding from foreign and

local banks

HLIB Research | Greater KL Catalytic Developments

www.hlebroking.com

Page 12 of 21

14 December 2016

Kwasa Damansara

From rubber estate to township. In Aug 2011, an S&P agreement was inked

between Kwasa Land with the MoF and Malaysian Rubber Board (MRB) for the former

to purchase 2,620 acres of rubber estate land in Sg Buloh owned by MRB. The transfer

of ownership was concluded in Oct 2012. Kwasa Land is a wholly owned subsidiary of

the Employees Provident Fund (EPF) and has been tasked as the master developer for

the said land which is today known as Kwasa Damansara. Following the sale of 290

acres to MRT Corp for the MRT depot to be constructed, the land size of Kwasa

Damansara was reduced slightly to 2,330 acres.

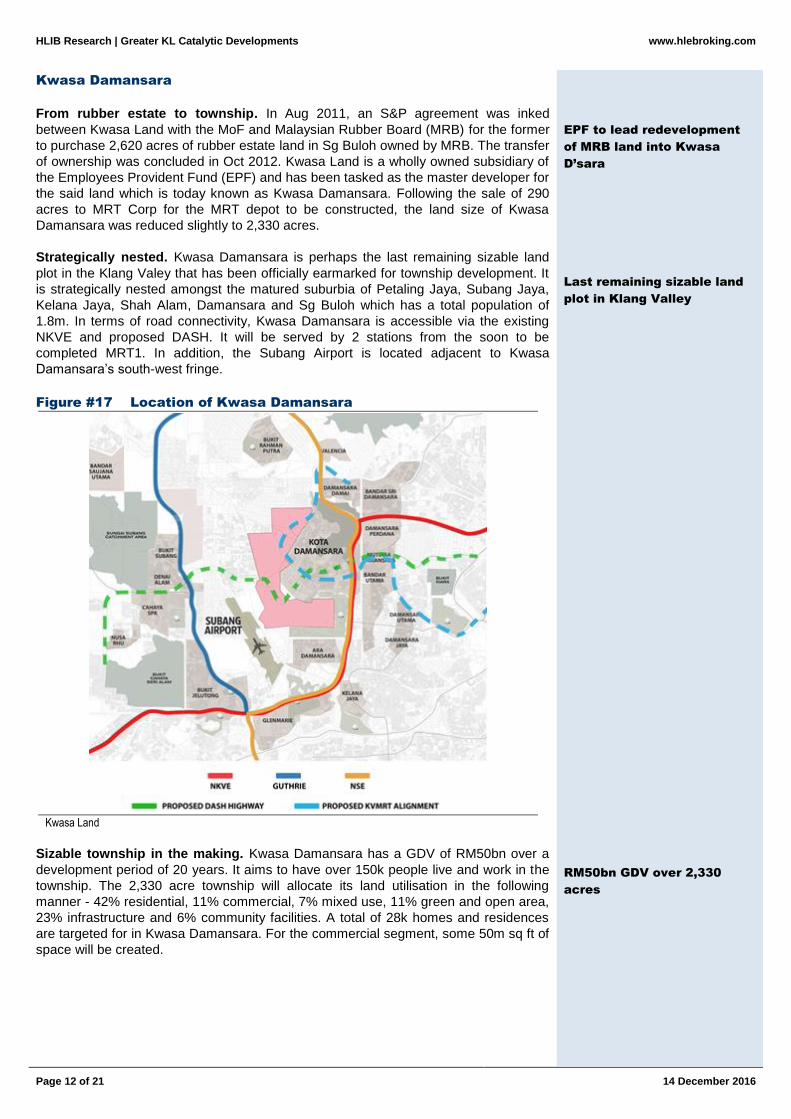

Strategically nested. Kwasa Damansara is perhaps the last remaining sizable land

plot in the Klang Valey that has been officially earmarked for township development. It

is strategically nested amongst the matured suburbia of Petaling Jaya, Subang Jaya,

Kelana Jaya, Shah Alam, Damansara and Sg Buloh which has a total population of

1.8m. In terms of road connectivity, Kwasa Damansara is accessible via the existing

NKVE and proposed DASH. It will be served by 2 stations from the soon to be

completed MRT1. In addition, the Subang Airport is located adjacent to Kwasa

Damansara’s south-west fringe.

Figure #17 Location of Kwasa Damansara

Kwasa Land

Sizable township in the making. Kwasa Damansara has a GDV of RM50bn over a

development period of 20 years. It aims to have over 150k people live and work in the

township. The 2,330 acre township will allocate its land utilisation in the following

manner - 42% residential, 11% commercial, 7% mixed use, 11% green and open area,

23% infrastructure and 6% community facilities. A total of 28k homes and residences

are targeted for in Kwasa Damansara. For the commercial segment, some 50m sq ft of

space will be created.

EPF to lead redevelopment

of MRB land into Kwasa

D’sara

Last remaining sizable land

plot in Klang Valley

RM50bn GDV over 2,330

acres

HLIB Research | Greater KL Catalytic Developments

www.hlebroking.com

Page 13 of 21

14 December 2016

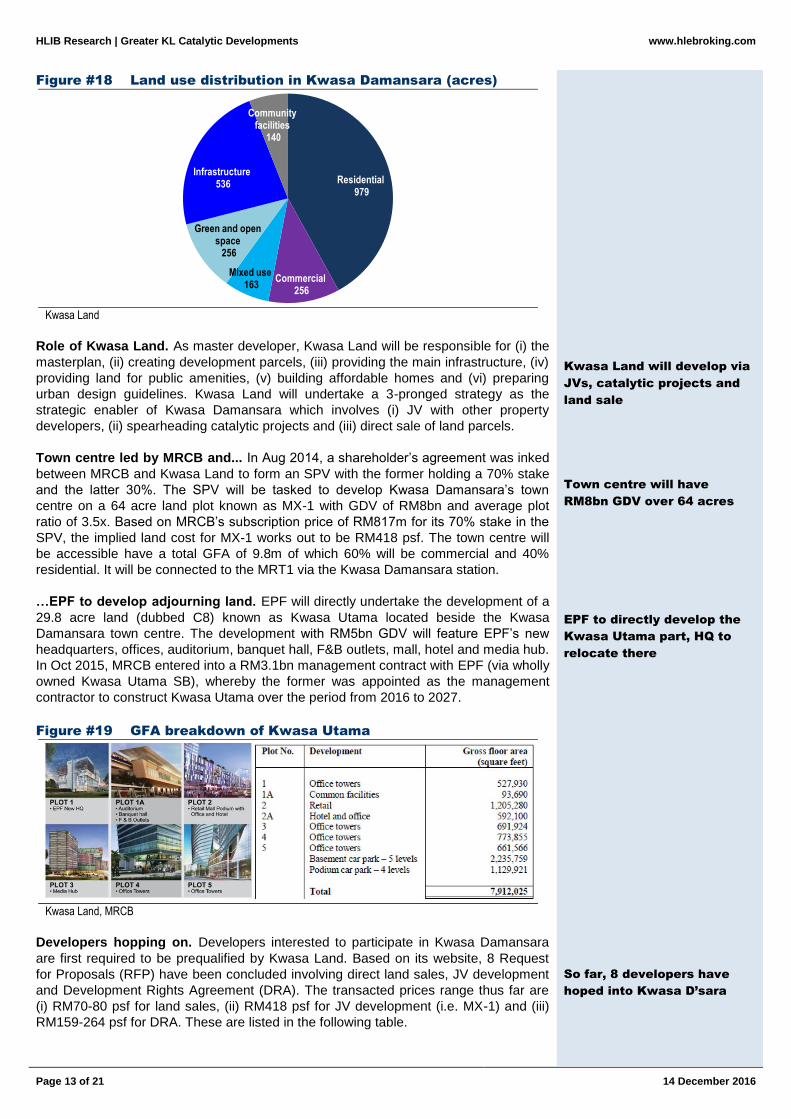

Figure #18 Land use distribution in Kwasa Damansara (acres)

Residential979

Commercial256

Mixed use163

Green and open space

256

Infrastructure536

Community facilities

140

Kwasa Land

Role of Kwasa Land. As master developer, Kwasa Land will be responsible for (i) the

masterplan, (ii) creating development parcels, (iii) providing the main infrastructure, (iv)

providing land for public amenities, (v) building affordable homes and (vi) preparing

urban design guidelines. Kwasa Land will undertake a 3-pronged strategy as the

strategic enabler of Kwasa Damansara which involves (i) JV with other property

developers, (ii) spearheading catalytic projects and (iii) direct sale of land parcels.

Town centre led by MRCB and... In Aug 2014, a shareholder’s agreement was inked

between MRCB and Kwasa Land to form an SPV with the former holding a 70% stake

and the latter 30%. The SPV will be tasked to develop Kwasa Damansara’s town

centre on a 64 acre land plot known as MX-1 with GDV of RM8bn and average plot

ratio of 3.5x. Based on MRCB’s subscription price of RM817m for its 70% stake in the

SPV, the implied land cost for MX-1 works out to be RM418 psf. The town centre will

be accessible have a total GFA of 9.8m of which 60% will be commercial and 40%

residential. It will be connected to the MRT1 via the Kwasa Damansara station.

…EPF to develop adjourning land. EPF will directly undertake the development of a

29.8 acre land (dubbed C8) known as Kwasa Utama located beside the Kwasa

Damansara town centre. The development with RM5bn GDV will feature EPF’s new

headquarters, offices, auditorium, banquet hall, F&B outlets, mall, hotel and media hub.

In Oct 2015, MRCB entered into a RM3.1bn management contract with EPF (via wholly

owned Kwasa Utama SB), whereby the former was appointed as the management

contractor to construct Kwasa Utama over the period from 2016 to 2027.

Figure #19 GFA breakdown of Kwasa Utama

Kwasa Land, MRCB

Developers hopping on. Developers interested to participate in Kwasa Damansara

are first required to be prequalified by Kwasa Land. Based on its website, 8 Request

for Proposals (RFP) have been concluded involving direct land sales, JV development

and Development Rights Agreement (DRA). The transacted prices range thus far are

(i) RM70-80 psf for land sales, (ii) RM418 psf for JV development (i.e. MX-1) and (iii)

RM159-264 psf for DRA. These are listed in the following table.

Kwasa Land will develop via

JVs, catalytic projects and

land sale

Town centre will have

RM8bn GDV over 64 acres

EPF to directly develop the

Kwasa Utama part, HQ to

relocate there

So far, 8 developers have

hoped into Kwasa D’sara

HLIB Research | Greater KL Catalytic Developments

www.hlebroking.com

Page 14 of 21

14 December 2016

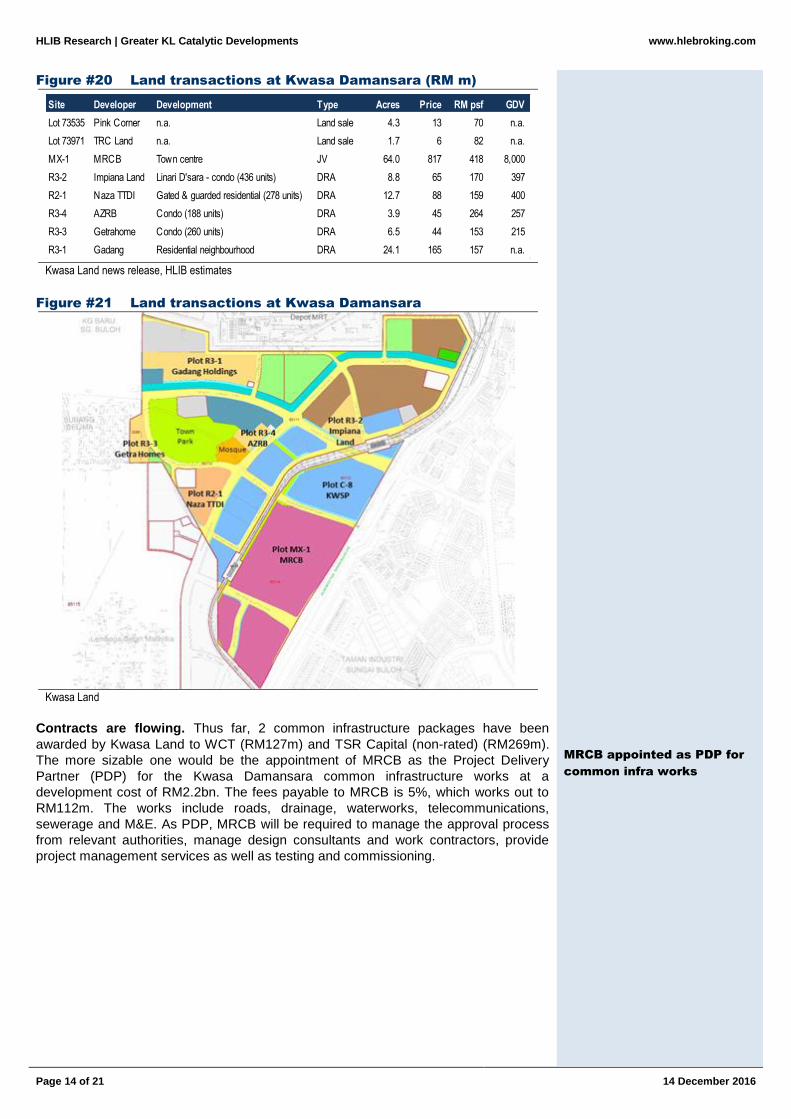

Figure #20 Land transactions at Kwasa Damansara (RM m)

Site Developer Development Type Acres Price RM psf GDV

Lot 73535 Pink Corner n.a. Land sale 4.3 13 70 n.a.

Lot 73971 TRC Land n.a. Land sale 1.7 6 82 n.a.

MX-1 MRCB Town centre JV 64.0 817 418 8,000

R3-2 Impiana Land Linari D'sara - condo (436 units) DRA 8.8 65 170 397

R2-1 Naza TTDI Gated & guarded residential (278 units) DRA 12.7 88 159 400

R3-4 AZRB Condo (188 units) DRA 3.9 45 264 257

R3-3 Getrahome Condo (260 units) DRA 6.5 44 153 215

R3-1 Gadang Residential neighbourhood DRA 24.1 165 157 n.a.

Kwasa Land news release, HLIB estimates

Figure #21 Land transactions at Kwasa Damansara

Kwasa Land

Contracts are flowing. Thus far, 2 common infrastructure packages have been

awarded by Kwasa Land to WCT (RM127m) and TSR Capital (non-rated) (RM269m).

The more sizable one would be the appointment of MRCB as the Project Delivery

Partner (PDP) for the Kwasa Damansara common infrastructure works at a

development cost of RM2.2bn. The fees payable to MRCB is 5%, which works out to

RM112m. The works include roads, drainage, waterworks, telecommunications,

sewerage and M&E. As PDP, MRCB will be required to manage the approval process

from relevant authorities, manage design consultants and work contractors, provide

project management services as well as testing and commissioning.

MRCB appointed as PDP for

common infra works

HLIB Research | Greater KL Catalytic Developments

www.hlebroking.com

Page 15 of 21

14 December 2016

Cyberjaya City Centre

Origins of Cyberjaya. Spearheaded by Cyberview (now wholly owned by MoF),

Cyberjaya was launched in 1997 to become Malaysia’s ICT hub. Today, the city is

home to over 800 firms including 40 MNCs. Its day time population is estimated to be

100k and this is expected to increase to 210k by 2020 given its development pipeline.

Cyberjaya also has a large student population, driven by 4 universities and 2 colleges.

Since 2014, efforts have been made by the government to reposition Cyberjaya as a

global technology hub. To achieve this, the 141 acre Cyberjaya City Centre (CCC)

development was mooted as one of the key projects during Budget 2016.

MRCB to spearhead CCC. In Oct 2015, MRCB entered into an agreement with

Cyberview to set up a JV whereby the former will hold a 70% stake and the latter 30%.

The purpose of the JV is to (i) develop a 53.4 acre land within CCC and (ii) have first

right of refusal over another 59.9 acre adjourning land. The JV will purchase the 53.4

acre land from Cyberview for RM349m or RM150 psf.

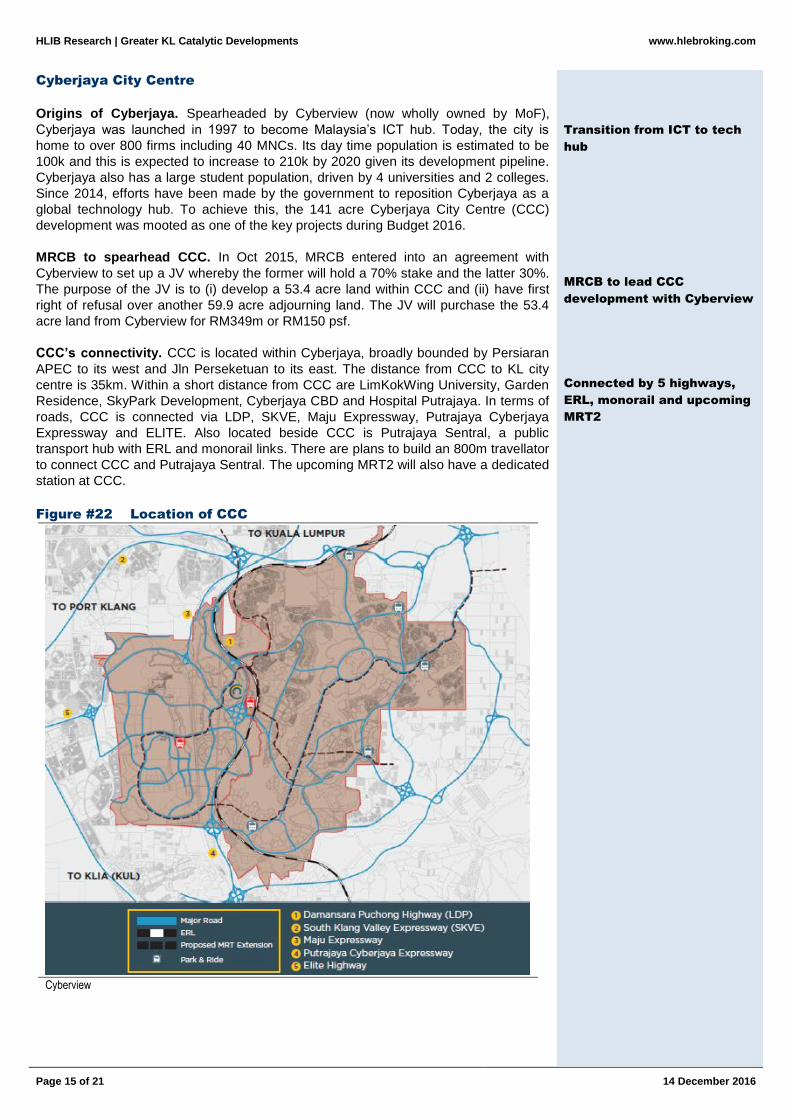

CCC’s connectivity. CCC is located within Cyberjaya, broadly bounded by Persiaran

APEC to its west and Jln Perseketuan to its east. The distance from CCC to KL city

centre is 35km. Within a short distance from CCC are LimKokWing University, Garden

Residence, SkyPark Development, Cyberjaya CBD and Hospital Putrajaya. In terms of

roads, CCC is connected via LDP, SKVE, Maju Expressway, Putrajaya Cyberjaya

Expressway and ELITE. Also located beside CCC is Putrajaya Sentral, a public

transport hub with ERL and monorail links. There are plans to build an 800m travellator

to connect CCC and Putrajaya Sentral. The upcoming MRT2 will also have a dedicated

station at CCC.

Figure #22 Location of CCC

Cyberview

Transition from ICT to tech

hub

MRCB to lead CCC

development with Cyberview

Connected by 5 highways,

ERL, monorail and upcoming

MRT2

HLIB Research | Greater KL Catalytic Developments

www.hlebroking.com

Page 16 of 21

14 December 2016

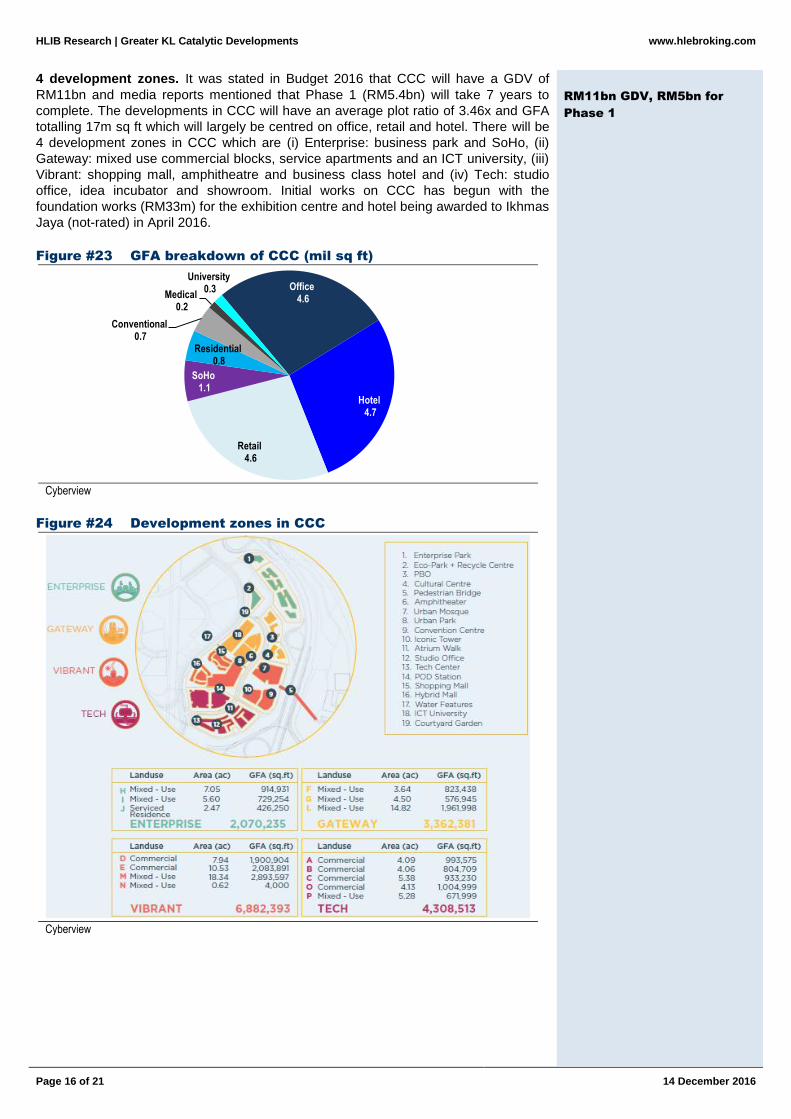

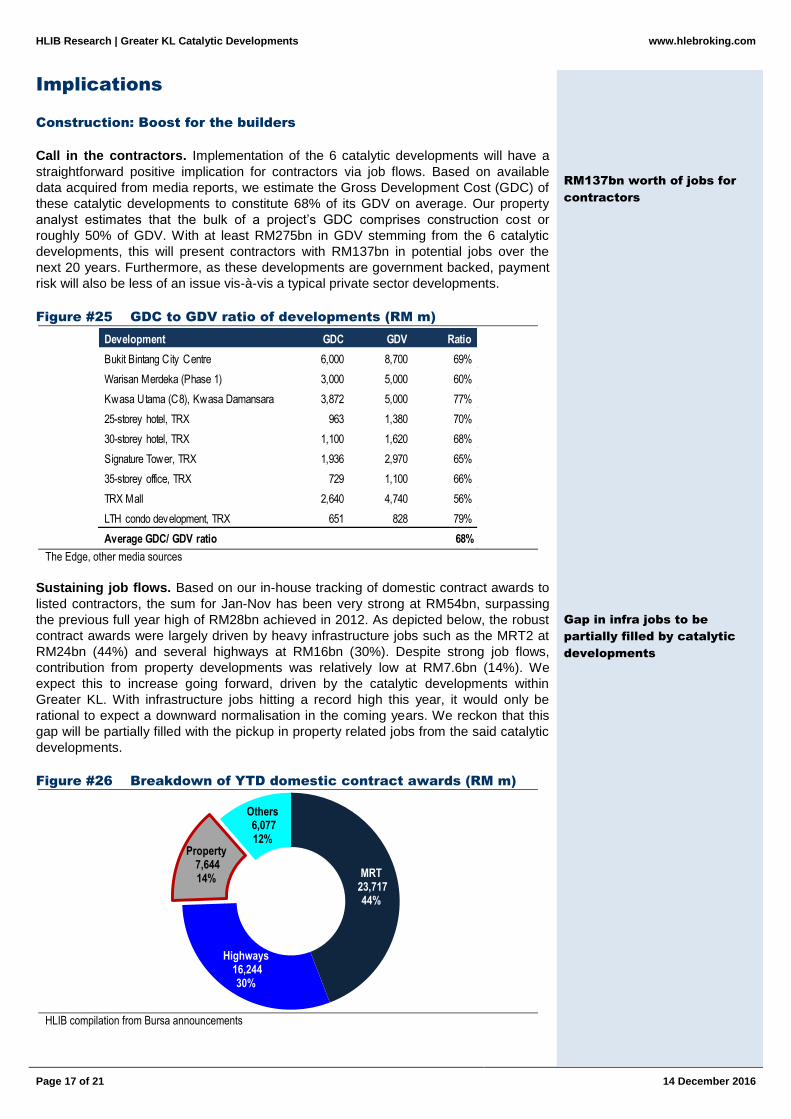

4 development zones. It was stated in Budget 2016 that CCC will have a GDV of

RM11bn and media reports mentioned that Phase 1 (RM5.4bn) will take 7 years to

complete. The developments in CCC will have an average plot ratio of 3.46x and GFA

totalling 17m sq ft which will largely be centred on office, retail and hotel. There will be

4 development zones in CCC which are (i) Enterprise: business park and SoHo, (ii)

Gateway: mixed use commercial blocks, service apartments and an ICT university, (iii)

Vibrant: shopping mall, amphitheatre and business class hotel and (iv) Tech: studio

office, idea incubator and showroom. Initial works on CCC has begun with the

foundation works (RM33m) for the exhibition centre and hotel being awarded to Ikhmas

Jaya (not-rated) in April 2016.

Figure #23 GFA breakdown of CCC (mil sq ft)

Office 4.6

Hotel 4.7

Retail4.6

SoHo1.1

Residential0.8

Conventional0.7

Medical0.2

University0.3

Cyberview

Figure #24 Development zones in CCC

Cyberview

RM11bn GDV, RM5bn for

Phase 1

HLIB Research | Greater KL Catalytic Developments

www.hlebroking.com

Page 17 of 21

14 December 2016

Implications

Construction: Boost for the builders

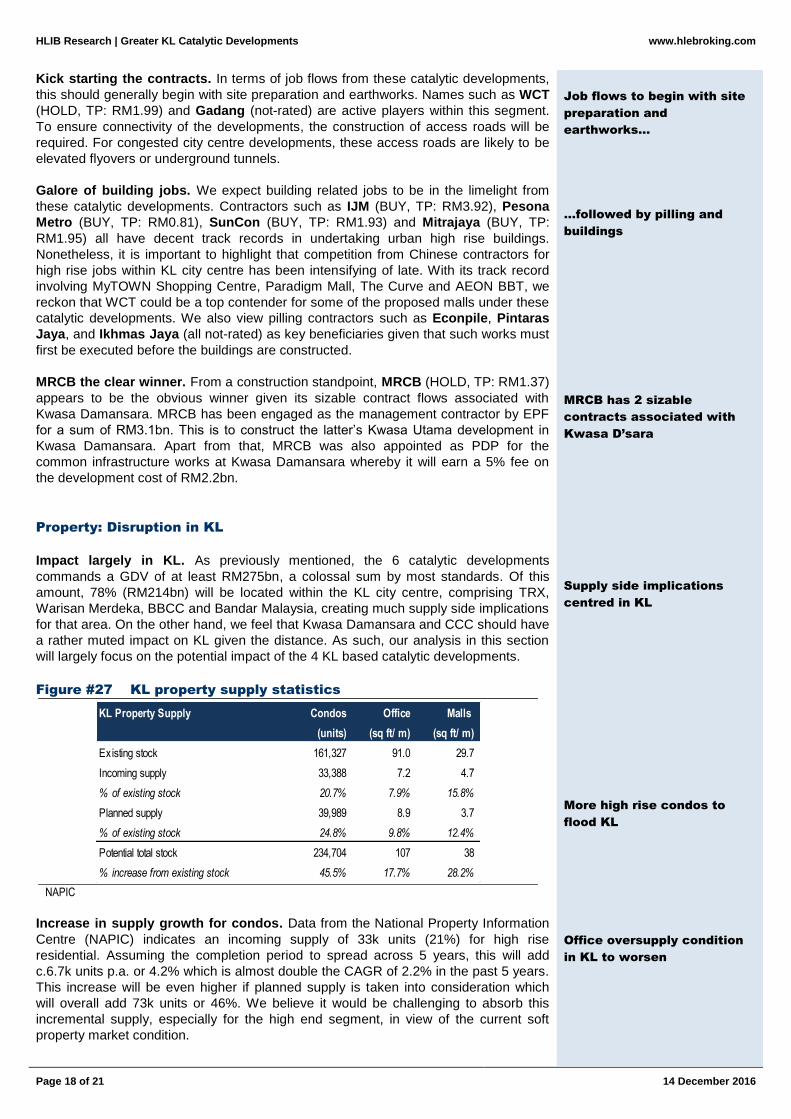

Call in the contractors. Implementation of the 6 catalytic developments will have a

straightforward positive implication for contractors via job flows. Based on available

data acquired from media reports, we estimate the Gross Development Cost (GDC) of

these catalytic developments to constitute 68% of its GDV on average. Our property

analyst estimates that the bulk of a project’s GDC comprises construction cost or

roughly 50% of GDV. With at least RM275bn in GDV stemming from the 6 catalytic

developments, this will present contractors with RM137bn in potential jobs over the

next 20 years. Furthermore, as these developments are government backed, payment

risk will also be less of an issue vis-à-vis a typical private sector developments.

Figure #25 GDC to GDV ratio of developments (RM m)

Development GDC GDV Ratio

Bukit Bintang City Centre 6,000 8,700 69%

Warisan Merdeka (Phase 1) 3,000 5,000 60%

Kwasa Utama (C8), Kwasa Damansara 3,872 5,000 77%

25-storey hotel, TRX 963 1,380 70%

30-storey hotel, TRX 1,100 1,620 68%

Signature Tower, TRX 1,936 2,970 65%

35-storey office, TRX 729 1,100 66%

TRX Mall 2,640 4,740 56%

LTH condo development, TRX 651 828 79%

Average GDC/ GDV ratio 68% The Edge, other media sources

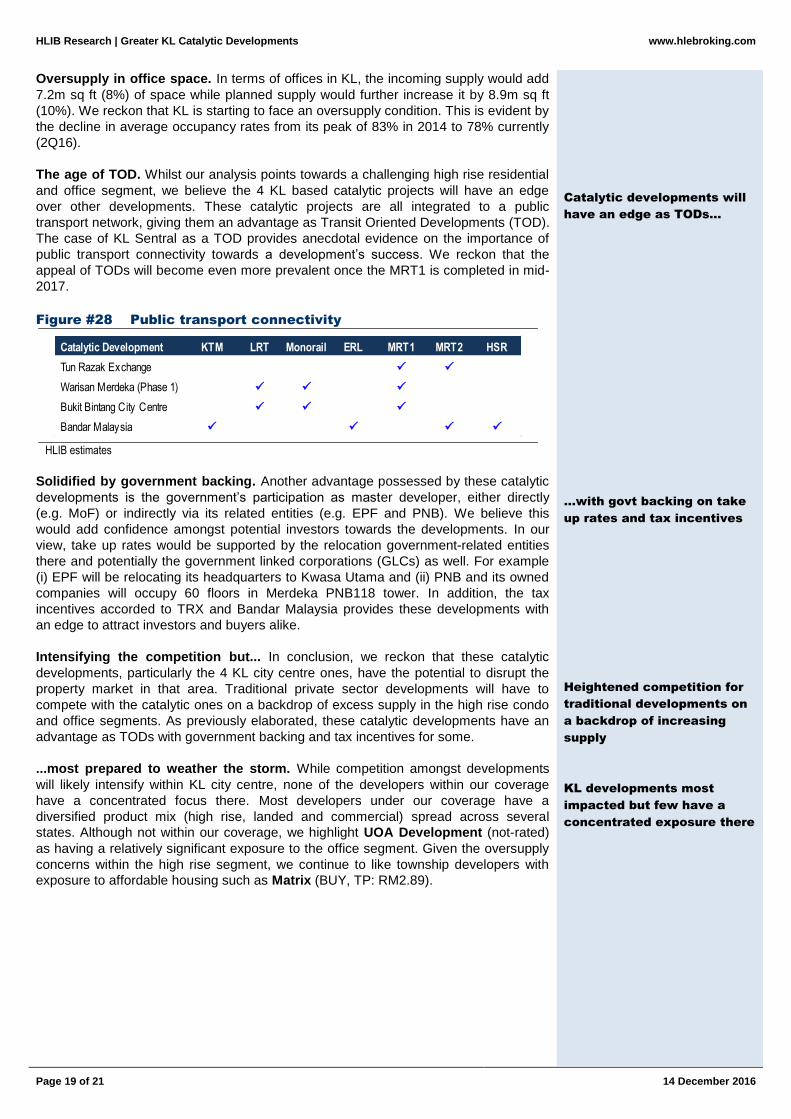

Sustaining job flows. Based on our in-house tracking of domestic contract awards to

listed contractors, the sum for Jan-Nov has been very strong at RM54bn, surpassing

the previous full year high of RM28bn achieved in 2012. As depicted below, the robust

contract awards were largely driven by heavy infrastructure jobs such as the MRT2 at

RM24bn (44%) and several highways at RM16bn (30%). Despite strong job flows,

contribution from property developments was relatively low at RM7.6bn (14%). We

expect this to increase going forward, driven by the catalytic developments within

Greater KL. With infrastructure jobs hitting a record high this year, it would only be

rational to expect a downward normalisation in the coming years. We reckon that this

gap will be partially filled with the pickup in property related jobs from the said catalytic

developments.

Figure #26 Breakdown of YTD domestic contract awards (RM m)

MRT23,717 44%

Highways16,244 30%

Property7,644 14%

Others6,077 12%

HLIB compilation from Bursa announcements

RM137bn worth of jobs for

contractors

Gap in infra jobs to be

partially filled by catalytic

developments

HLIB Research | Greater KL Catalytic Developments

www.hlebroking.com

Page 18 of 21

14 December 2016

Kick starting the contracts. In terms of job flows from these catalytic developments,

this should generally begin with site preparation and earthworks. Names such as WCT

(HOLD, TP: RM1.99) and Gadang (not-rated) are active players within this segment.

To ensure connectivity of the developments, the construction of access roads will be

required. For congested city centre developments, these access roads are likely to be

elevated flyovers or underground tunnels.

Galore of building jobs. We expect building related jobs to be in the limelight from

these catalytic developments. Contractors such as IJM (BUY, TP: RM3.92), Pesona

Metro (BUY, TP: RM0.81), SunCon (BUY, TP: RM1.93) and Mitrajaya (BUY, TP:

RM1.95) all have decent track records in undertaking urban high rise buildings.

Nonetheless, it is important to highlight that competition from Chinese contractors for

high rise jobs within KL city centre has been intensifying of late. With its track record

involving MyTOWN Shopping Centre, Paradigm Mall, The Curve and AEON BBT, we

reckon that WCT could be a top contender for some of the proposed malls under these

catalytic developments. We also view pilling contractors such as Econpile, Pintaras

Jaya, and Ikhmas Jaya (all not-rated) as key beneficiaries given that such works must

first be executed before the buildings are constructed.

MRCB the clear winner. From a construction standpoint, MRCB (HOLD, TP: RM1.37)

appears to be the obvious winner given its sizable contract flows associated with

Kwasa Damansara. MRCB has been engaged as the management contractor by EPF

for a sum of RM3.1bn. This is to construct the latter’s Kwasa Utama development in

Kwasa Damansara. Apart from that, MRCB was also appointed as PDP for the

common infrastructure works at Kwasa Damansara whereby it will earn a 5% fee on

the development cost of RM2.2bn.

Property: Disruption in KL

Impact largely in KL. As previously mentioned, the 6 catalytic developments

commands a GDV of at least RM275bn, a colossal sum by most standards. Of this

amount, 78% (RM214bn) will be located within the KL city centre, comprising TRX,

Warisan Merdeka, BBCC and Bandar Malaysia, creating much supply side implications

for that area. On the other hand, we feel that Kwasa Damansara and CCC should have

a rather muted impact on KL given the distance. As such, our analysis in this section

will largely focus on the potential impact of the 4 KL based catalytic developments.

Figure #27 KL property supply statistics

KL Property Supply Condos Office Malls

(units) (sq ft/ m) (sq ft/ m)

Existing stock 161,327 91.0 29.7

Incoming supply 33,388 7.2 4.7

% of existing stock 20.7% 7.9% 15.8%

Planned supply 39,989 8.9 3.7

% of existing stock 24.8% 9.8% 12.4%

Potential total stock 234,704 107 38

% increase from existing stock 45.5% 17.7% 28.2%

NAPIC

Increase in supply growth for condos. Data from the National Property Information

Centre (NAPIC) indicates an incoming supply of 33k units (21%) for high rise

residential. Assuming the completion period to spread across 5 years, this will add

c.6.7k units p.a. or 4.2% which is almost double the CAGR of 2.2% in the past 5 years.

This increase will be even higher if planned supply is taken into consideration which

will overall add 73k units or 46%. We believe it would be challenging to absorb this

incremental supply, especially for the high end segment, in view of the current soft

property market condition.

Job flows to begin with site

preparation and

earthworks…

…followed by pilling and

buildings

MRCB has 2 sizable

contracts associated with

Kwasa D’sara

Supply side implications

centred in KL

More high rise condos to

flood KL

Office oversupply condition

in KL to worsen

HLIB Research | Greater KL Catalytic Developments

www.hlebroking.com

Page 19 of 21

14 December 2016

Oversupply in office space. In terms of offices in KL, the incoming supply would add

7.2m sq ft (8%) of space while planned supply would further increase it by 8.9m sq ft

(10%). We reckon that KL is starting to face an oversupply condition. This is evident by

the decline in average occupancy rates from its peak of 83% in 2014 to 78% currently

(2Q16).

The age of TOD. Whilst our analysis points towards a challenging high rise residential

and office segment, we believe the 4 KL based catalytic projects will have an edge

over other developments. These catalytic projects are all integrated to a public

transport network, giving them an advantage as Transit Oriented Developments (TOD).

The case of KL Sentral as a TOD provides anecdotal evidence on the importance of

public transport connectivity towards a development’s success. We reckon that the

appeal of TODs will become even more prevalent once the MRT1 is completed in mid-

2017.

Figure #28 Public transport connectivity

Catalytic Development KTM LRT Monorail ERL MRT1 MRT2 HSR

Tun Razak Exchange

Warisan Merdeka (Phase 1)

Bukit Bintang City Centre

Bandar Malaysia

HLIB estimates

Solidified by government backing. Another advantage possessed by these catalytic

developments is the government’s participation as master developer, either directly

(e.g. MoF) or indirectly via its related entities (e.g. EPF and PNB). We believe this

would add confidence amongst potential investors towards the developments. In our

view, take up rates would be supported by the relocation government-related entities

there and potentially the government linked corporations (GLCs) as well. For example

(i) EPF will be relocating its headquarters to Kwasa Utama and (ii) PNB and its owned

companies will occupy 60 floors in Merdeka PNB118 tower. In addition, the tax

incentives accorded to TRX and Bandar Malaysia provides these developments with

an edge to attract investors and buyers alike.

Intensifying the competition but... In conclusion, we reckon that these catalytic

developments, particularly the 4 KL city centre ones, have the potential to disrupt the

property market in that area. Traditional private sector developments will have to

compete with the catalytic ones on a backdrop of excess supply in the high rise condo

and office segments. As previously elaborated, these catalytic developments have an

advantage as TODs with government backing and tax incentives for some.

...most prepared to weather the storm. While competition amongst developments

will likely intensify within KL city centre, none of the developers within our coverage

have a concentrated focus there. Most developers under our coverage have a

diversified product mix (high rise, landed and commercial) spread across several

states. Although not within our coverage, we highlight UOA Development (not-rated)

as having a relatively significant exposure to the office segment. Given the oversupply

concerns within the high rise segment, we continue to like township developers with

exposure to affordable housing such as Matrix (BUY, TP: RM2.89).

Catalytic developments will

have an edge as TODs…

…with govt backing on take

up rates and tax incentives

Heightened competition for

traditional developments on

a backdrop of increasing

supply

KL developments most

impacted but few have a

concentrated exposure there

HLIB Research | Greater KL Catalytic Developments

www.hlebroking.com

Page 20 of 21

14 December 2016

REIT: Supply, supply and more supply

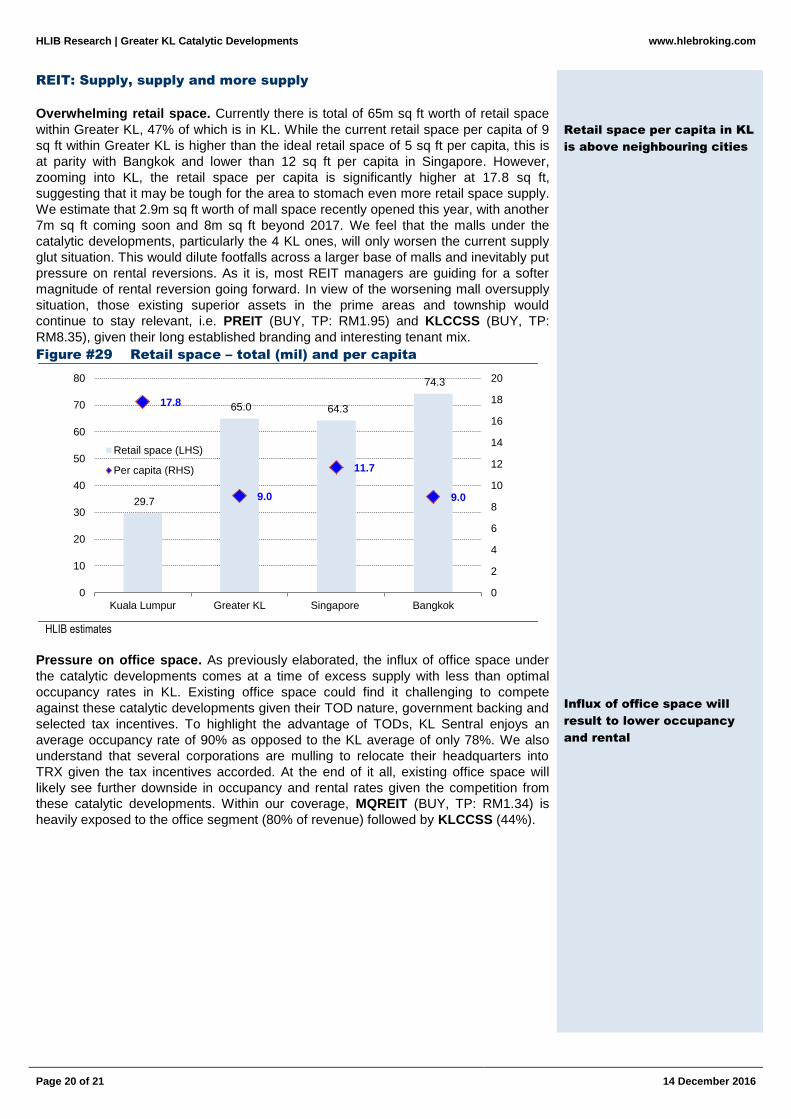

Overwhelming retail space. Currently there is total of 65m sq ft worth of retail space

within Greater KL, 47% of which is in KL. While the current retail space per capita of 9

sq ft within Greater KL is higher than the ideal retail space of 5 sq ft per capita, this is

at parity with Bangkok and lower than 12 sq ft per capita in Singapore. However,

zooming into KL, the retail space per capita is significantly higher at 17.8 sq ft,

suggesting that it may be tough for the area to stomach even more retail space supply.

We estimate that 2.9m sq ft worth of mall space recently opened this year, with another

7m sq ft coming soon and 8m sq ft beyond 2017. We feel that the malls under the

catalytic developments, particularly the 4 KL ones, will only worsen the current supply

glut situation. This would dilute footfalls across a larger base of malls and inevitably put

pressure on rental reversions. As it is, most REIT managers are guiding for a softer

magnitude of rental reversion going forward. In view of the worsening mall oversupply

situation, those existing superior assets in the prime areas and township would

continue to stay relevant, i.e. PREIT (BUY, TP: RM1.95) and KLCCSS (BUY, TP:

RM8.35), given their long established branding and interesting tenant mix.

Figure #29 Retail space – total (mil) and per capita

29.7

65.0 64.3

74.3

17.8

9.0

11.7

9.0

0

2

4

6

8

10

12

14

16

18

20

0

10

20

30

40

50

60

70

80

Kuala Lumpur Greater KL Singapore Bangkok

Retail space (LHS)

Per capita (RHS)

HLIB estimates

Pressure on office space. As previously elaborated, the influx of office space under

the catalytic developments comes at a time of excess supply with less than optimal

occupancy rates in KL. Existing office space could find it challenging to compete

against these catalytic developments given their TOD nature, government backing and

selected tax incentives. To highlight the advantage of TODs, KL Sentral enjoys an

average occupancy rate of 90% as opposed to the KL average of only 78%. We also

understand that several corporations are mulling to relocate their headquarters into

TRX given the tax incentives accorded. At the end of it all, existing office space will

likely see further downside in occupancy and rental rates given the competition from

these catalytic developments. Within our coverage, MQREIT (BUY, TP: RM1.34) is

heavily exposed to the office segment (80% of revenue) followed by KLCCSS (44%).

Retail space per capita in KL

is above neighbouring cities

Influx of office space will

result to lower occupancy

and rental

HLIB Research | Greater KL Catalytic Developments

www.hlebroking.com

Page 21 of 21

14 December 2016

Disclaimer

The information contained in this report is based on data obtained from sources believed to be reliable. However, the data and/or sources have not been independently verified and as such, no representation, express or implied, is made as to the accuracy, adequacy, completeness or reliability of the info or opinions in the report.

Accordingly, neither Hong Leong Investment Bank Berhad nor any of its related companies and associates nor person connected to it accept any liability whatsoever for any direct, indirect or consequential losses (including loss of profits) or damages that may arise from the use or reliance on the info or opinions in this publication.

Any information, opinions or recommendations contained herein are subject to change at any time without prior notice. Hong Leong Investment Bank Berhad has no obligation to update its opinion or the information in this report.

Investors are advised to make their own independent evaluation of the info contained in this report and seek independent financial, legal or other advice regarding the appropriateness of investing in any securities or the investment strategies discussed or recommended in this report. Nothing in this report constitutes investment, legal, accounting or tax advice or a representation that any investment or strategy is suitable or appropriate to your individual circumstances or otherwise represent a personal recommendation to you.

Under no circumstances should this report be considered as an offer to sell or a solicitation of any offer to buy any securities referred to herein.

Hong Leong Investment Bank Berhad and its related companies, their associates, directors, connected parties and/or employees may, from time to time, own, have positions or be materially interested in any securities mentioned herein or any securities related thereto, and may further act as market maker or have assumed underwriting commitment or deal with such securities and provide advisory, investment or other services for or do business with any companies or entities mentioned in this report. In reviewing the report, investors should be aware that any or all of the foregoing among other things, may give rise to real or potential conflict of interests.

This research report is being supplied to you on a strictly confidential basis solely for your information and is made strictly on the basis that it will remain confidential. All materials presented in this report, unless specifically indicated otherwise, is under copyright to Hong Leong Investment Bank Berhad. This research report and its contents may not be reproduced, stored in a retrieval system, redistributed, transmitted or passed on, directly or indirectly, to any person or published in whole or in part, or altered in any way, for any purpose.

This report may provide the addresses of, or contain hyperlinks to, websites. Hong Leong Investment Bank Berhad takes no responsibility for the content contained therein. Such addresses or hyperlinks (including addresses or hyperlinks to Hong Leong Investment Bank Berhad own website material) are provided solely for your convenience. The information and the content of the linked site do not in any way form part of this report. Accessing such website or following such link through the report or Hong Leong Investment Bank Berhad website shall be at your own risk. 1. As of 14 December 2016, Hong Leong Investment Bank Berhad has proprietary interest in the following securities covered in this report: (a) -. 2. As of 14 December 2016, the analysts, Jeremy Goh, who prepared this report, have interest in the following securities covered in this report: (a) -.

Published & Printed by

Hong Leong Investment Bank Berhad (10209-W)

Level 23, Menara HLA No. 3, Jalan Kia Peng 50450 Kuala Lumpur Tel 603 2168 1168 / 603 2710 1168 Fax 603 2161 3880

Equity rating definitions

BUY Positive recommendation of stock under coverage. Expected absolute return of more than +10% over 12-months, with low risk of sustained downside. TRADING BUY Positive recommendation of stock not under coverage. Expected absolute return of more than +10% over 6-months. Situational or arbitrage trading opportunity. HOLD Neutral recommendation of stock under coverage. Expected absolute return between -10% and +10% over 12-months, with low risk of sustained downside. TRADING SELL Negative recommendation of stock not under coverage. Expected absolute return of less than -10% over 6-months. Situational or arbitrage trading opportunity. SELL Negative recommendation of stock under coverage. High risk of negative absolute return of more than -10% over 12-months. NOT RATED No research coverage and report is intended purely for informational purposes.

Industry rating definitions

OVERWEIGHT The sector, based on weighted market capitalization, is expected to have absolute return of more than +5% over 12-months. NEUTRAL The sector, based on weighted market capitalization, is expected to have absolute return between –5% and +5% over 12-months. UNDERWEIGHT The sector, based on weighted market capitalization, is expected to have absolute return of less than –5% over 12-months.