Embed Size (px)

Citation preview

8/6/2019 Gray & Needles Pp 24-26

http://slidepdf.com/reader/full/gray-needles-pp-24-26 1/3

24 1/ ACCOUNTING INFORMATION, DECISION MAKING, AN D THE USES OF FDIANCIAL STATEMENTS

auditor's opinion when deciding to invest in a company or to make loans to a firm

that has been audited. The independent audit is an important factor in the worldwide/ ' growth of financial markets.

.......

,N1"f0,i">--",

Factors That Influence Accounting tandardsfiNAN" It(.. I } c ~ , J " r , N c .

While a varietyof

economic, social, political, legal,and

cultural factors influence theA C : ( . ~ 4 , U A ,DJ"ftl.k formulation of ac.counting standards, the most important factors would seem to be

the enterprise's sources of finance and the nature of capital markets, taxation, the( l i1f accounting profession, the nature of accounting regulation, national cultures and tra

ditions, and international economic and political relationships (see Figure 1-6).110 4M .re'N j111''''-' 1'-/.

/- ources ofFinance and Capital Markets

The sources of finance for an enterprise exert an important influence because the

more capital that is raised from the public or external shareholders the more pressure

there will be for public accountability and information disclosure. This is the case

especially In countr ies such as the United States and the United Kingdom where stock

markets are highly developed and substantial numbers of corporations are owned by

a broad base of shareholders. In this way, investor interests have been perceived by

management to be significant and have become the predominant influence on finan

cial statements. In contrast, banks are a much more important source of finance in

countries such as Germany, Japan, and Switzerland, and hence their concerns have

tended to influence the preparation of financial statements more than those of

investors.

Taxation

Another major influence on accounting standards is taxation, such as in France,

Germany, and Japan, where the financial statements of business enterprises prepared

F IGURE 1 -6 Factors That Inf luence Acco unt ing Standards

InternationalSources of Finance

Economic and Politicaland C ~ p i t a l Markets

Relationships

National Culturesand Traditions ..._T_axa_tion_.....

Accounting The Accounting

Regulation Profession

8/6/2019 Gray & Needles Pp 24-26

http://slidepdf.com/reader/full/gray-needles-pp-24-26 2/3

8/6/2019 Gray & Needles Pp 24-26

http://slidepdf.com/reader/full/gray-needles-pp-24-26 3/3

the ethical responsibilities of

accountants

26 11 ACCOUNTING INFORMATION, DECISION MAKING, AND TH E USES OF FINANCIAL STATEMENTS

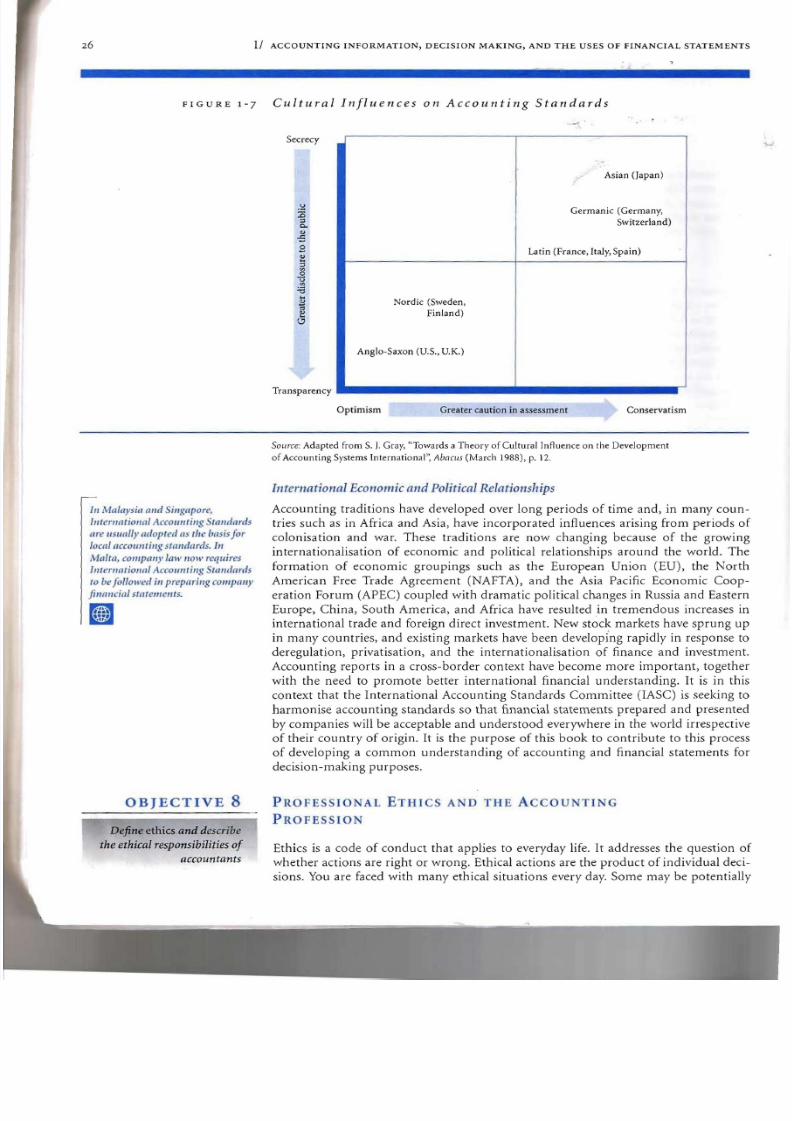

F IGURE 1 -7 Cultural Inf luences on Account ing Standards

-.'Secrecy

Transparency

Optimism Greater caution in assessment Conservatism

Asian (Japan)..

Germanic (Germany,

Switzerland)

Latin (France, Italy, Spain)

Nordic (Sweden.

Finland)

Anglo-Saxon (U.S., u.K.)

hI Malaysia and Sillgapore,

llltemntionni Accolllltillg Sttllldards

are /ls/lally adopted as tire basis for

local a,colII/tillg stal/dards. III

Malta, company law II0W requires

Il1fernatiol/al Accountillg Stlll/dnrds

to be followed ill preparillg compallY

jillnll,ial stalelllellts.

OBJECTIVE 8

Define ethics and describe

Source: Adapted from S. ). Gray, "Towards a Theory of Cultural Influence on the Development

of Accounting Systems International", Abacus (March 1988), p. 12.

International Economic and Political Relationships

Accounting traditions have developed over long periods of time and, in many coun

tries such as in Africa and Asia, have incorporated influences arising from periods of

colonisation and war. These traditions are now changing because of the growing

internationalisation of economic and political relationships around the world. The

formation of economic groupings such as the European Union (EU), the North

American Free Trade Agreement (NAFTA), and the Asia Pacific Economic Coop

eration Forum (APEC) coupled with dramatic political changes in Russia and Eastern

Europe, China, South America, and Africa have resulted in tremendous increases in

international trade and foreign direct investment. New stock markets have sprung up

in many countries, and existing markets have been developi'ng rapidly in response to

deregulation, privatisation, and the internationalisation of finance and investment.

Accounting reports in a cross-border context have become more important, together

with the need to promote better international financial understanding. It is in this

context that the International Accounting Standards Committee (lASC) is seeking to

harmonise accounting standards so that financial statements prepared and presented

by companies will be acceptable and understood everywhere in the world irrespective

of their country of origin. It is the purpose of this book to contribute to this process

of developing a common understanding of accounting and financial statements for

decision-making purposes.

PROFESSIO AL ETHICS A D TH E Acco TI G

PROFESSIO

Ethics is a code of conduct that applies to everyday life. It addresses the question of

whether actions are right or wrong. Ethical actions are the product of individual deci

sions. You are faced with many ethical situations every day. Some may be potentially