Embed Size (px)

Citation preview

Issued on: 28 June 2013

Granting of Credit Facilities

BNM/RH/GL 010-18 Prudential Financial Policy Department / Islamic Banking and Takaful Department

Granting of Credit Facilities

Issued on: 28 June 2013

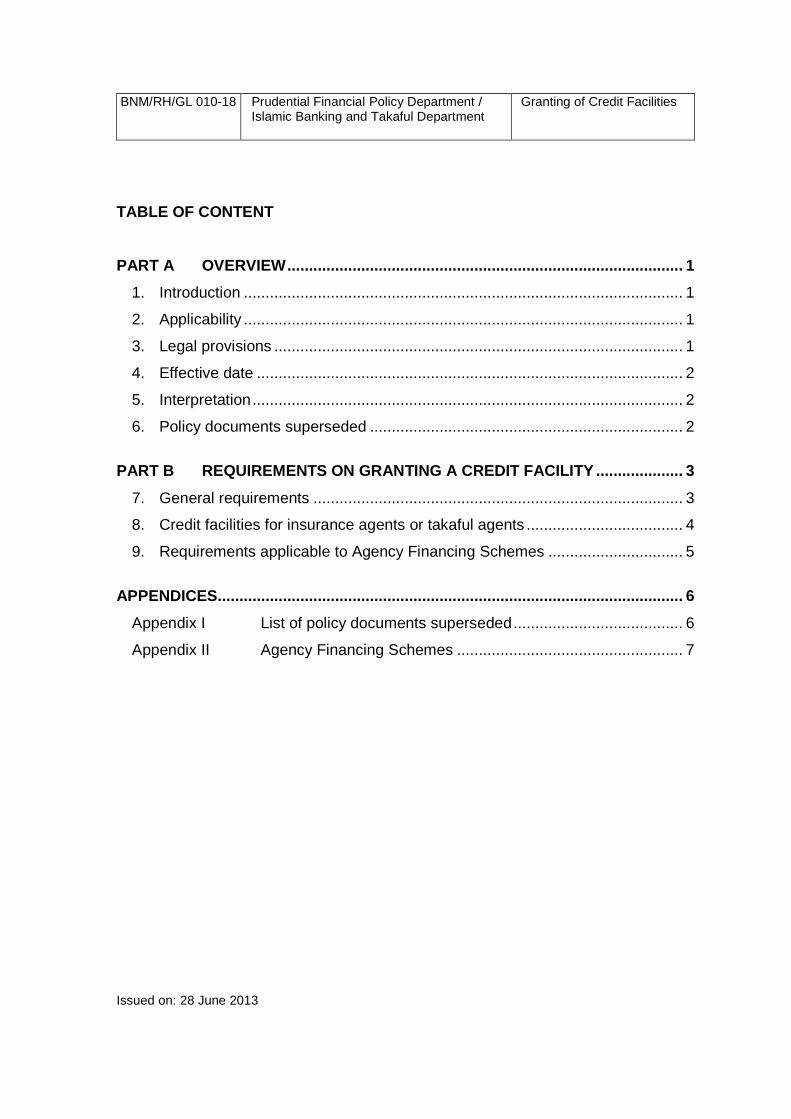

TABLE OF CONTENT

PART A OVERVIEW ........................................................................................... 1

1. Introduction ..................................................................................................... 1

2. Applicability ..................................................................................................... 1

3. Legal provisions .............................................................................................. 1

4. Effective date .................................................................................................. 2

5. Interpretation ................................................................................................... 2

6. Policy documents superseded ........................................................................ 2

PART B REQUIREMENTS ON GRANTING A CREDIT FACILITY ........ ............ 3

7. General requirements ..................................................................................... 3

8. Credit facilities for insurance agents or takaful agents .................................... 4

9. Requirements applicable to Agency Financing Schemes ............................... 5

APPENDICES........................................................................................................... 6

Appendix I List of policy documents superseded ....................................... 6

Appendix II Agency Financing Schemes .................................................... 7

BNM/RH/GL 010-18 Prudential Financial Policy Department / Islamic Banking and Takaful Department

Granting of Credit Facilities

1/12

Issued on: 28 June 2013

PART A OVERVIEW

1. Introduction

Scope of policy

1.1 This policy document sets out the requirements and conditions to be complied

with by a licensed insurer and licensed takaful operator for granting a credit

facility, including:

(a) specific conditions relating to agents; and

(b) specific requirements on Agency Financing Schemes for life insurers and

family takaful operators.

2. Applicability

2.1 This policy document is applicable to all insurers licensed under the Financial

Services Act 2013 (FSA) and takaful operators licensed under the Islamic

Financial Services Act 2013 (IFSA).

3. Legal provisions

3.1 The requirements in this policy document are specified pursuant to section

47(1) of the FSA and section 57(1) of the IFSA

3.2 The requirements in this policy document must be read together with section

133 of the Companies Act 1965.

BNM/RH/GL 010-18 Prudential Financial Policy Department / Islamic Banking and Takaful Department

Granting of Credit Facilities

2/12

Issued on: 28 June 2013

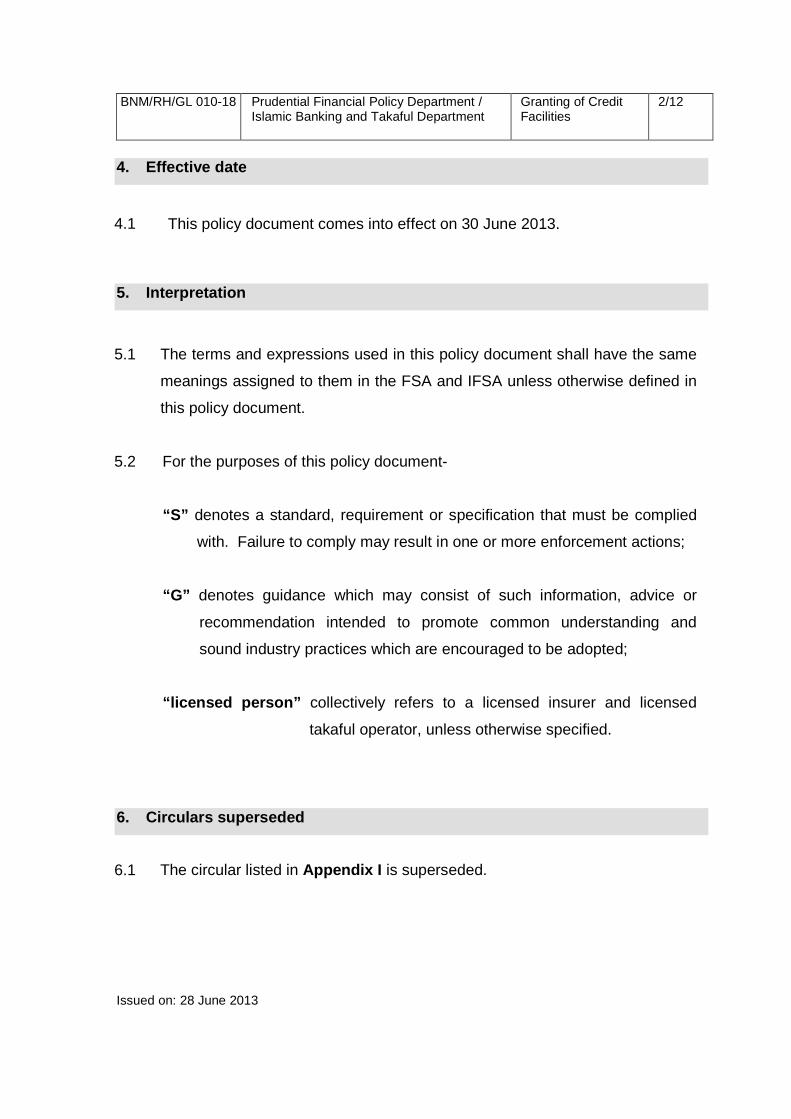

4. Effective date

4.1 This policy document comes into effect on 30 June 2013.

5. Interpretation

5.1 The terms and expressions used in this policy document shall have the same

meanings assigned to them in the FSA and IFSA unless otherwise defined in

this policy document.

5.2 For the purposes of this policy document-

“S” denotes a standard, requirement or specification that must be complied

with. Failure to comply may result in one or more enforcement actions;

“G” denotes guidance which may consist of such information, advice or

recommendation intended to promote common understanding and

sound industry practices which are encouraged to be adopted;

“licensed person” collectively refers to a licensed insurer and licensed

takaful operator, unless otherwise specified.

6. Circulars superseded

6.1 The circular listed in Appendix I is superseded.

BNM/RH/GL 010-18 Prudential Financial Policy Department / Islamic Banking and Takaful Department

Granting of Credit Facilities

3/12

Issued on: 28 June 2013

PART B REQUIREMENTS ON GRANTING A CREDIT FACILITY

7. General requirements

S 7.1 A licensed person must obtain the prior written approval of the Bank to:

(a) act, or arrange with any person to act, as a guarantor for a credit facility

granted to any person; and

(b) grant a credit facility to any person specified in paragraph 7.2, subject to

section 133.

S 7.2 For the purposes of paragraph 7.1(b) a specified person is-

(a) any of a licensed person’s directors;

(b) a company or firm in which a licensed person has any interest as

controller, manager or agent;

(c) a company or firm in which any of a licensed person’s directors has any

interest as director, partner, controller, manager or agent;

(d) an individual for whom or a company or firm for which any of a licensed

person’s directors is a guarantor;

(e) a company in which a licensed person, or any one or more of its

directors has an interest in voting shares of 20% or more;

(f) a company which has an interest in voting shares of 20% or more in a

licensed person; and

(g) a company in which the company in paragraph 7.2(f) above has an

interest in voting shares of 20% or more.

S 7.3 The Bank’s prior written approval under paragraph 7.1(b) is not required for the

grant of a credit facility to a director of a licensed person if the credit facility is

secured in full by a life policy or family takaful certificate held by the director

which does not exceed the surrender value of the policy or certificate.

BNM/RH/GL 010-18 Prudential Financial Policy Department / Islamic Banking and Takaful Department

Granting of Credit Facilities

4/12

Issued on: 28 June 2013

S 7.4 For the purposes of paragraphs 7.2 and 7.3, “director” includes a relative of a

director.

G 7.5 The purchase of private debt securities or Islamic private debt securities in the

secondary market is not deemed to be the granting of credit facilities.

8. Credit facilities for insurance agents or takafu l agents

S 8.1 Any credit facility granted by a licensed person to its insurance agent or takaful

agent, as the case may be, may only be granted from the licensed person’s

shareholders’ funds.

S 8.2 In granting an unsecured credit facility to its insurance agent or takaful agent,

as the case may be, a licensed person must comply with the following

requirements:

(a) for loans or financing for the purchase of-

(i) a new vehicle, the loan or financing must not exceed 80% of the

cost of the vehicle or RM120,000, whichever amount is lower; and

(ii) a second hand vehicle, the loan or financing must not exceed 70%

of the value of the vehicle or RM80,000, whichever amount is

lower;

(b) loans or financing for the purchase of computers must not exceed the

purchase price of the computer or RM5,000, whichever amount is lower;

and

(c) requirements as may be specified by the Bank to be applied to loans or

financing provided under an Agency Financing Scheme.

BNM/RH/GL 010-18 Prudential Financial Policy Department / Islamic Banking and Takaful Department

Granting of Credit Facilities

5/12

Issued on: 28 June 2013

9. Requirements applicable to Agency Financing Sch emes

S 9.1 For the purposes of the requirements on Agency Financing Schemes, “licensed

person” refers to a licensed life insurer and a licensed family takaful operator

collectively.

S 9.2 Pursuant to paragraph 8.2 (c) of this document, a licensed person must comply

with the requirements recommended by the Life Insurance Association of

Malaysia (LIAM) and the Malaysian Takaful Association (MTA), and approved

by the Bank in relation to the Agency Development Financing and Personal

Development Financing Schemes, as attached in Appendix II .

BNM/RH/GL 010-18 Prudential Financial Policy Department / Islamic Banking and Takaful Department

Granting of Credit Facilities

6/12

Issued on: 28 June 2013

APPENDICES

Appendix I Circular superseded

1. Grant of Credit Facilities By Licensed Insurers and Takaful Operators

(Consolidated) issued on 31 December 2012

BNM/RH/GL 010-18 Prudential Financial Policy Department / Islamic Banking and Takaful Department

Granting of Credit Facilities

7/12

Issued on: 28 June 2013

Appendix II Agency Financing Schemes

1. General requirements for Agency Financing Scheme s

1.1 A licensed person may only provide an Agency Financing Scheme (AFS) for its

insurance agents or takaful agents, as the case may be, for the purposes of

Agency Development Financing, as set out in Section 2 of Appendix II and

Personal Development Financing, as set out in Section 3 of Appendix II .

1.2 An insurance agent or takaful agent is only eligible to participate in an AFS if

the agent-

(a) is at least 18 years old;

(b) has completed the SPM/MCE or 11 years of formal education;

(c) is not a bankrupt;

(d) is not involved in criminal acts and has not been dismissed for

malpractices or fraud in his previous employment1;

(e) complies with LIAM's Code of Ethics / MTA’s Code of Ethics;

(f) is registered with the licensed person;

(g) is involved in selling life insurance or marketing family takaful; and

(h) provides at least one guarantor who is either an agency manager (AM),

agency supervisor (AS) or any person who directly reports to the licensed

person and is approved by the licensed person to be the guarantor.

1.3 The licensed person must assess the ability of the guarantor to meet the

guarantee commitments in the event of default of the insurance agent or takaful

agent in respect of whom the guarantee has been given. The licensed person

must exercise appropriate care to ensure maximum recovery of a loan or

financing extended under an AFS. This includes setting appropriate internal

1 Any non-disclosure on past conduct would result in termination

BNM/RH/GL 010-18 Prudential Financial Policy Department / Islamic Banking and Takaful Department

Granting of Credit Facilities

8/12

Issued on: 28 June 2013

loan or financing exposure limits for every guarantor and taking into

consideration relevant factors such as the financial resources of the guarantor.

1.4 The licensed person must put in place internal policies and procedures to

ensure that the ongoing eligibility criteria for an AFS set out in paragraphs 2.2

and 3.6 of Appendix II are met.

2. Agency Development Financing

2.1 An AFS includes an Agency Development Financing Scheme (ADF) and a

Personal Development Financing Scheme (PDF). An ADF serves to assist newly

recruited insurance agents or takaful agents, as the case may be, and newly

appointed agency leaders, to stabilise their income during the initial stages of

their career and to encourage part-time agents to become full-time agents, by

providing qualified agents with profit-free or subsidised unsecured loans or

financing.

2.2 In addition to the criteria set out in paragraph 1.2 of Appendix II , only an

insurance agent or takaful agent who meets the following criteria is eligible for

an ADF:

(a) for a newly appointed agent:

(i) a minimum production quota of three insurance policies or takaful

certificates and RM4,000 annualised first year premiums or

contributions (FYP) at the end of the second quarter and each quarter

thereafter; and

(ii) a minimum persistency rate of 85%, if the agent has been in service for

more than one year; and

(b) for a newly appointed agency leader:

(i) a minimum of three new agents; and

BNM/RH/GL 010-18 Prudential Financial Policy Department / Islamic Banking and Takaful Department

Granting of Credit Facilities

9/12

Issued on: 28 June 2013

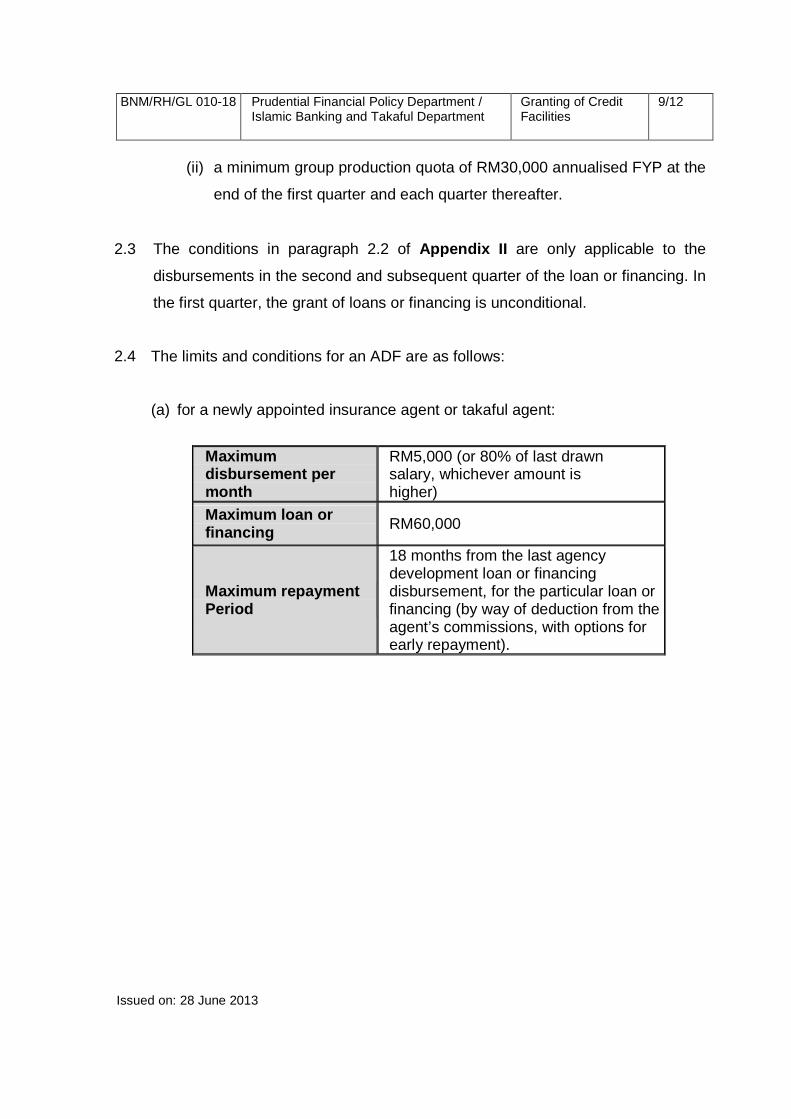

(ii) a minimum group production quota of RM30,000 annualised FYP at the

end of the first quarter and each quarter thereafter.

2.3 The conditions in paragraph 2.2 of Appendix II are only applicable to the

disbursements in the second and subsequent quarter of the loan or financing. In

the first quarter, the grant of loans or financing is unconditional.

2.4 The limits and conditions for an ADF are as follows:

(a) for a newly appointed insurance agent or takaful agent:

Maximum disbursement per month

RM5,000 (or 80% of last drawn salary, whichever amount is higher)

Maximum loan or financing RM60,000

Maximum repayment Period

18 months from the last agency development loan or financing disbursement, for the particular loan or financing (by way of deduction from the agent’s commissions, with options for early repayment).

BNM/RH/GL 010-18 Prudential Financial Policy Department / Islamic Banking and Takaful Department

Granting of Credit Facilities

10/12

Issued on: 28 June 2013

(b) for a newly appointed agency leader:

Maximum disbursement per month

RM10,000 (or 80% of last drawn salary, whichever amount is higher)

Maximum loan or financing RM120,000

Maximum repayment Period

18 months from the last agency development loan or financing disbursement, for the particular loan or financing (by way of deduction from agent’s commissions, with options for early repayment).

2.5 All disbursements of an ADF by a licensed person must be made directly to the

newly recruited insurance agent or takaful agent, as the case may be, or the

newly appointed agency leader.

2.6 A licensed person must not continue to extend the ADF to an insurance agent,

takaful agent or agency leader who does not meet the minimum production and

persistency requirements in paragraph 2.2 of Appendix II . Disbursement must

cease immediately if the requirements are not met.

3. Personal Development Financing

3.1 A Personal Development Financing Scheme (PDF) is used to assist insurance

agents or takaful agents, as the case may be, to finance their training or

development costs to enhance their knowledge, technical skills and quality of

service. Training or development programmes include courses that are offered

by the Malaysian Insurance Institute (MII), the Islamic Banking and Finance

Institute Malaysia (IBFIM) and those endorsed by the Life Insurance Association

of Malaysia (LlAM) or the Malaysian Takaful Association (MTA). Apart from

course fees, a PDF may cover related transportation and accommodation costs.

BNM/RH/GL 010-18 Prudential Financial Policy Department / Islamic Banking and Takaful Department

Granting of Credit Facilities

11/12

Issued on: 28 June 2013

3.2 A new insurance agent or takaful agent, as the case may be, that qualifies for an

ADF will also be eligible for a PDF.

3.3 In addition, an existing insurance agent or takaful agent must meet a minimum

persistency rate of 85% and the following criteria to be eligible for a PDF:

(a) for an AM, a minimum production of RM100,000 per annum annualised

FYP under his supervision; (b) for an AS, a minimum production of RM50,000 per annum annualised FYP

under his supervision; and (c) for an ordinary agent, a minimum of nine insurance policies or takaful

certificates or RM6,000 per annum annualised FYP.

3.4 The limits and conditions for a PDF are as follows: (a) the loan or financing must not exceed the actual amount of the training or

development costs incurred;

(b) the amount of the cumulative loan or financing to an insurance agent or

takaful agent at any one time must not exceed RM5,000; and

(c) the repayment period must not be more than 12 months, beginning from

the disbursement date, and must be deducted from the insurance agent or

takaful agent’s commissions, with options for early repayment.

3.5 Disbursements under this scheme must be made directly to the provider of the

training or development programme.

3.6 Subsequent disbursements of loans or financing under this scheme must be

subject to an insurance agent or takaful agent meeting the following

maintenance rules for each quarter:

(a) for an existing insurance agent or takaful agent, meeting the criteria set out

in paragraph 3.3 of Appendix II ; and (b) for a new insurance agent or takaful agent, meeting a continued minimum

BNM/RH/GL 010-18 Prudential Financial Policy Department / Islamic Banking and Takaful Department

Granting of Credit Facilities

12/12

Issued on: 28 June 2013

production quota of three insurance policies or takaful certificates or

RM2,000 annualised FYP.

3.7 A licensed person must not continue to extend the ADF to an insurance agent or

takaful agent who does not meet the minimum production and persistency

requirements in paragraph 3.6 of Appendix II . Disbursement must cease

immediately if the requirements are not met.