Embed Size (px)

Citation preview

Grant Budgeting Basics

Donna Marano

Director of Finance & Administration

Civil & Environmental Engineering

Denise Murrin Macey

Business Manager

Engineering and Public Policy

October 31, 2005 ©Sharon McCarl

Session Focus

Theory-What is a good budget?

Practical-What are the pieces and how do I put it together?

Routing and Approvals

What is a good proposal?

A good idea, well expressed, with a clear indication of methods for pursuing the idea, evaluating the findings, and making them known to all who need to know - NSF

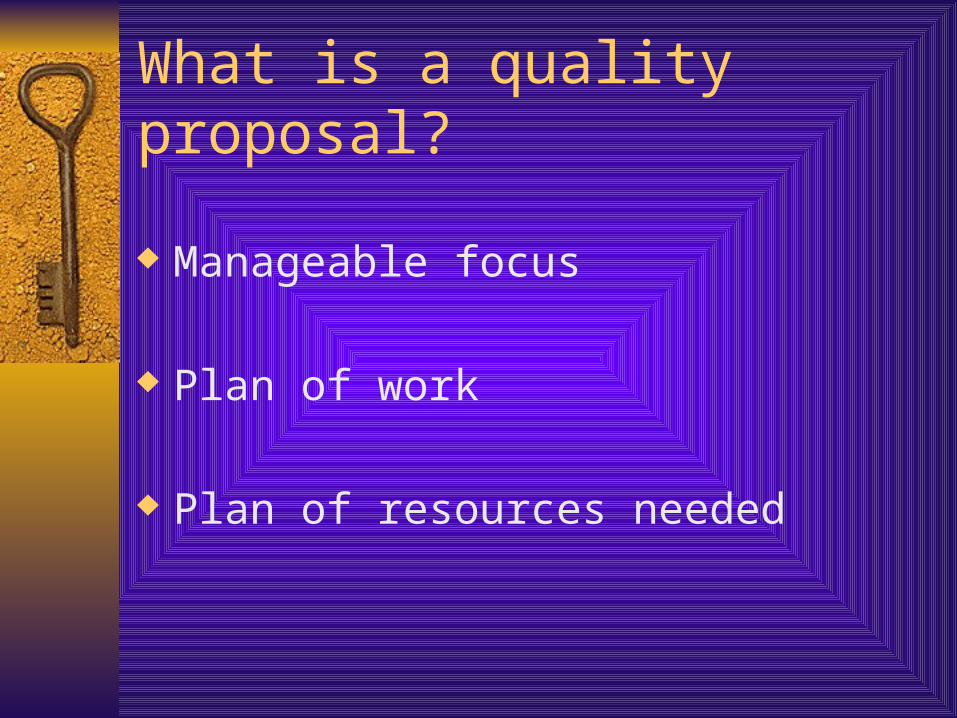

What is a quality proposal?

Manageable focus

Plan of work

Plan of resources needed

Point to Remember

Throughout It All, Remember, Proposals Are Approved Based on the Science, Then Whether the Budget Is Justified. A Good Budget Requires Justification but It Is Not the Primary Factor in Evaluation.

Budgeting Defined

“The Budget Plan is the Financial Expression of the Project or Program as Approved During the Award Process” (OMB Circular A-110, Subpart C, Section _.25).

Business Side-What do I need to accomplish the goals of this project?

Budgeting Principles

ALL costs (direct and F&A) that can be identified with a particular sponsored project should be identified and budgeted (somewhere) AT THE PROPOSAL STAGE

ALL costs (direct and F&A) of a particular sponsored project should be borne by the sponsor (to the maximum extent possible)

Costing Defined

The Process Used to Determine the Amount Required to Acquire the Goods and Services Necessary to Achieve Project Objectives

Pricing Defined

The Process Used to Determine the Amount Requested from the Sponsor to Acquire the Goods and Services Necessary to Achieve Project Objectives

Guiding Regulations

Office of Management and Budget (OMB) Circular A-21 http://www.whitehouse.gov/omb/circulars/a021/a021.html

Cost Accounting Standards Board http://www.whitehouse.gov/omb/procurement/casb.html

22 Standards for Industry

4 Apply to Educational Institutions OMB Circular A110

http://www.whitehouse.gov/omb/circulars/a110/a110.html)

Institutional Policies

Characteristics of Costs

Reasonable Allocable Allowable Treated Consistently

Reasonableness

Test - Is the expense reasonable? Logical? Reasonable person test Is it normal for this type and level of

expense to be charged on projects of a similar nature?

Market Value-Appropriate Bids

Allocable

Was the cost incurred solely for the advancement of the project?

Can the expense be clearly identified with the project?

Assigning inappropriate expenses is FRAUD!

Allowable

Reasonable and necessary A-21 section J In conformance with limitations/exclusions

(example foreign travel, equipment)

Treated Consistently

Cost Accounting Standards Must be able to defend cost estimates

Cost Accounting Standards

501-Estimating, Accumulating and Reporting costs

502-Consistency in Allocating Costs Incurred for the Same Purpose

505-Accounting for Unallowable Costs

506-Consistent use of Cost Accounting Period

OMB Circular A-110

Financial Management Standards– Rules for Accounting, Asset Management

Cost Sharing

Cost Sharing

“…that portion of project or program costs not borne by the Federal Government.” (OMB Circular A-110, Subpart A, Section _.2(i))

Know your department or college’s policy & procedures

NSF Statement 10/19/04 (NSB-04-157)

Questions???

Consider the Source of Funding

Sponsor Awarded Funding– State or Federal Government– Industry– Foundations

Institutionally Provided Funding– Start-up Fund– Seed Fund– Faculty Development– Cost Sharing

Assess Budget Needs

Budget matches narrative Amounts

– Reasonable for scope of work– Well justified– In-line with program– Allowable

Includes adjustments for future years

Types of Costs

Direct Costs– “…costs that can be identified specifically with

a particular sponsored project…” (OMB Circular A-21, Sec.D.1)

Facility and Administrative Costs– “…costs incurred for common or joint

objectives and [that] therefore cannot be identified readily and specifically with a sponsored project…” OMB Circular A-21, Sec.E.1

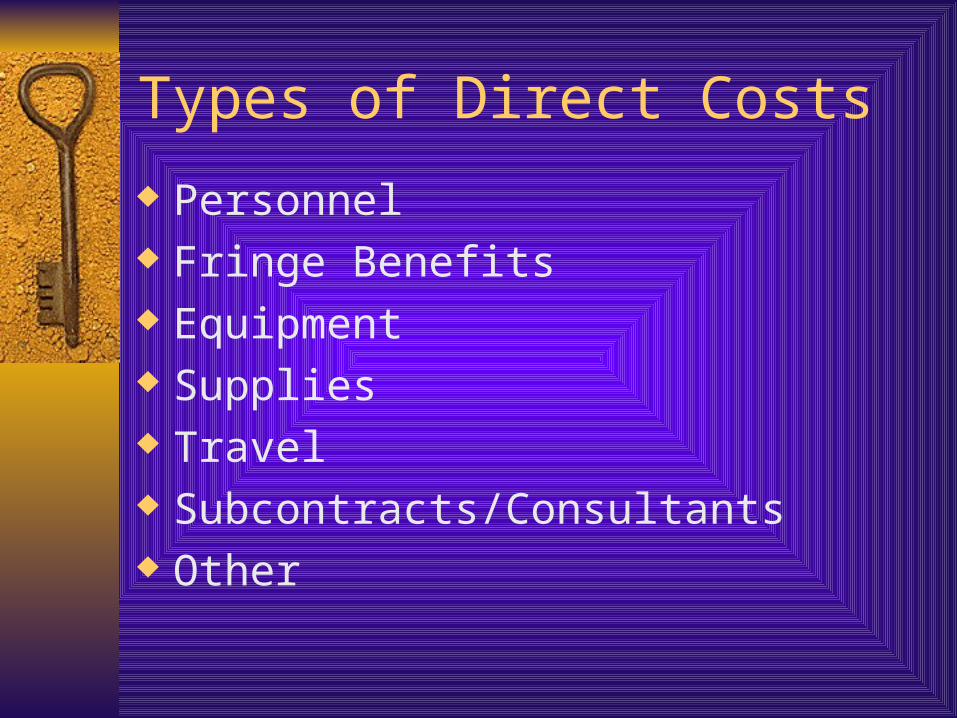

Types of Direct Costs

Personnel Fringe Benefits Equipment Supplies Travel Subcontracts/Consultants Other

Personnel

Individuals who are employees or students of Carnegie Mellon

Vacant Positions (to be named) Generally no administrative positions Funding in proportion to project effort using base

salary Include fringe benefits (full or part-time) Include salary increments Remember salary caps

Fringe Benefits

Pooled or composite rate Rates proposed by Carnegie Mellon and

approved by the Office of Naval Research– Full-time 37.5 hours 29.50%– Full-time 37.5 hours Federal 25.90%

• Issue: dependent tuition 3.60%

Fringe Benefits

– Part-time 17.5 and < 37.5 18.5%– Part-time Mandatory < 17.5 10%

• Mandatory (FICA, unemployment, worker’s comp)

• Non-CMU students

– Additional Compensation 10%

Equipment

Cost $1,000 & Useful Life 2 Years Exclusive use by project

– Computers– General purpose

equipment

Equipment

Itemize and Justify– Competitive Pricing ( 3 bids > $2,500)– Price Reasonableness

Identify Sole Source Suppliers at the Proposal Stage

Supplies

Must be specific to project (check A-21) Avoid general purpose items Itemize and justify Examples

– Chemicals, glassware, non-capital equipment– Animal purchases, enzymes

Travel

Itemize and justify Who, what, when, where, why and how Include business purpose and destination Separate domestic and foreign travel Do not include patient care or consultant

travel

Other

Animal housing Publication and page charges Subject incentive and travel reimbursement Rentals & maintenance contracts Equipment Usage (# hours and rate) Long distance

Subcontracts

Itemized budget Statement of work Commitment to perform (w/signature) Justify need and selection criteria Include direct and F&A in your budget

Consultants

Employee vs. Consultant (substantial fines) Justify contribution to project and budget Include name and affiliation Include all costs including travel & per

diem Include biographical sketches

Flags Animal Research Radioactive/DNA Human Subjects Effort > 100% Employees ??? Subcontract > 50% Unallowable (get it in

writing) Space or Cost Sharing

Facilities and Administrative Costs (a.k.a. Indirect Costs) “…costs incurred for common or joint

objectives and [that] therefore cannot be identified readily and specifically with a sponsored project…” OMB Circular A-21, Sec.E.1

Two Components– Facilities

– Administration

Facilities and Administrative Costs Federal rates set by our cognizant agency

ONR in negotiation with Carnegie Mellon– Applies to subcontracts with federal prime

Modified Total Direct Cost Base Industrial Rate 56 % Federal Rate 45% (DOD Contracts 49%) Federal Rate Off-Campus 28.8%

Facilities

Depreciation and Use Allowance– Interest on Debt (specific buildings)– Equipment & Capital Improvements

Operation & Maintenance Expenses Library Expenses

Administration

GA - General Administration – Executive & Administrative, Central functions

DA - Department Administration– Administrative and Clerical Staff, office

supplies, telephones, travel

Sponsored Project Administration Student Administration & Services

Calculation

Modified Total Direct Cost Base Carnegie Mellon example

– Total Direct Costs Less:– Equipment– 1/2 graduate student costs– Portion of sub-awards in excess of $25,000

On-site vs. Off-site rate Check Sponsor Terms

Summary

Preplanning Know regulations and sponsor requirements Know special requirements

– Animals, Human Subjects, Subcontracts, Cost Sharing

Check Math

Questions???

Getting Started

Sponsor– Federal, Non-federal (what rates and rules apply)– Special Rules or Instructions (caps, F&A)

Project Dates Subcontracts or Multi-departmental Budgets Special Approvals (animals, human subjects)

Personnel

Who will work on this project? What will this person contribute? Where will this person work? What is this person’s status? Employee,

graduate student, consultant??? Type of Appointment How much effort is required? Are there security issues?

Equipment

What do you need? What is the importance of this item to the

research? Does it qualify as capital equipment? Is it general purpose equipment? Is it available elsewhere? Borrow or share Cost analysis Lease vs. Purchase

Travel

How does this trip enhance the goals of the proposed research?

Who will travel? Where? Why?

Supplies and Other Expenses

What do you need? What is the best way to estimate the cost?

– Do the numbers-avoid excessive guessing– Check recharge rates, facility charges, historical

expenses– Match budget detail to accounting system

Controlled Substances? Cost of an Audit

Proposal Routing

Contact Business Manager

SPEX Sponsored Projects Exchange

Generates Proposal Routing and Sign-off Sheet

Carnegie Mellon Proposal Number

Disclosure and Signatures

Investigator(s) Disclosure and Assurances– Must read and check appropriate box

– Conflicts must be resolved –Susan Burkett

All proposals require approval prior to submission– Signatures

• PI

• Department Head

• Dean

• Pre-award Office

• Associate Provost-Institutional Official

Routing Time

Allow Adequate time for review Carnegie Mellon reserves the right to

withdraw any proposal AND You need time to copy and collate before

the express mail pick-up Electronic Submissions

![[2007] WAMW 4 · 2020-06-24 · [2007] wamw 4 2007wamw4.doc () page 1 jurisdiction : mining warden title of court : open court location : perth citation : murrin murrin](https://img.pdfslide.us/doc/110x75/5f0fbc4a7e708231d445a0cf/2007-wamw-4-2020-06-24-2007-wamw-4-2007wamw4doc-page-1-jurisdiction-.jpg)