Embed Size (px)

DESCRIPTION

Case study

Citation preview

ACY 5903A Financial Management Group 3

1 INTRODUCTION

Grand Metropolitan Plc

Grand Metropolitan Plc (GrandMet) is the world’s largest wine and spirits seller. With a

total sales of GBP8.75 billion (in 1991), the company ranked among Britain’s 10 largest

companies.

Company Background

GrandMet was founded in the late 1940s as the Washington Group, a chain of hotels

established by Sir Maxwell Joseph. In 1957, with the acquisition of the Mount Royal Hotel,

the company changed its name to Mount Royal Ltd. In 1962, the company renamed again to

Grand Metropolitan Hotels.

As the name told us, the company was concentrated on hotel businesses at its early time.

However, by a series of acquisitions of different companies, GrandMet started to diversify into

non-hotel businesses since 1966.

Learnt from GrandMet’s historical information, acquisition and divestiture seemed to be the

company’s major activities during 1960s to 1980s. Especially in 1980s, the company was

highly involved in buying and selling with huge capital gains (e.g. GrandMet bought

Intercontinental Hotels for $500 million and sold for $2 billion later).

Development of Core Businesses

Some companies, e.g. Watney (the owner of International Distillers & Vintners), Pillsbury (the

owner of Burger King & Haagen-Dazs), etc. acquired by GrandMet have been eventually

developed as the group’s core businesses.

In 1991-92, GrandMet had even divested all of its hotels, breweries, gaming establishments,

soft-drink bottling plants, fitness products, and all food brands that were judged not to have

international branding potential. As a result, the company sold off close to GBP800 million in

Case: Grand Metropolitan Plc P. 1 of 10

ACY 5903A Financial Management Group 3

businesses in order to focus on core activities: food, drinks, and retailing.

Strategic Core Competence

With the strategy of focusing on the company’s core competence - management of

international brands in food, drinks, and retailing, GrandMet founded itself successfully beat

the market forecasts in 1991 with a 4.8% increase in pretax profits (GBP963 million) despite

during world recession time.

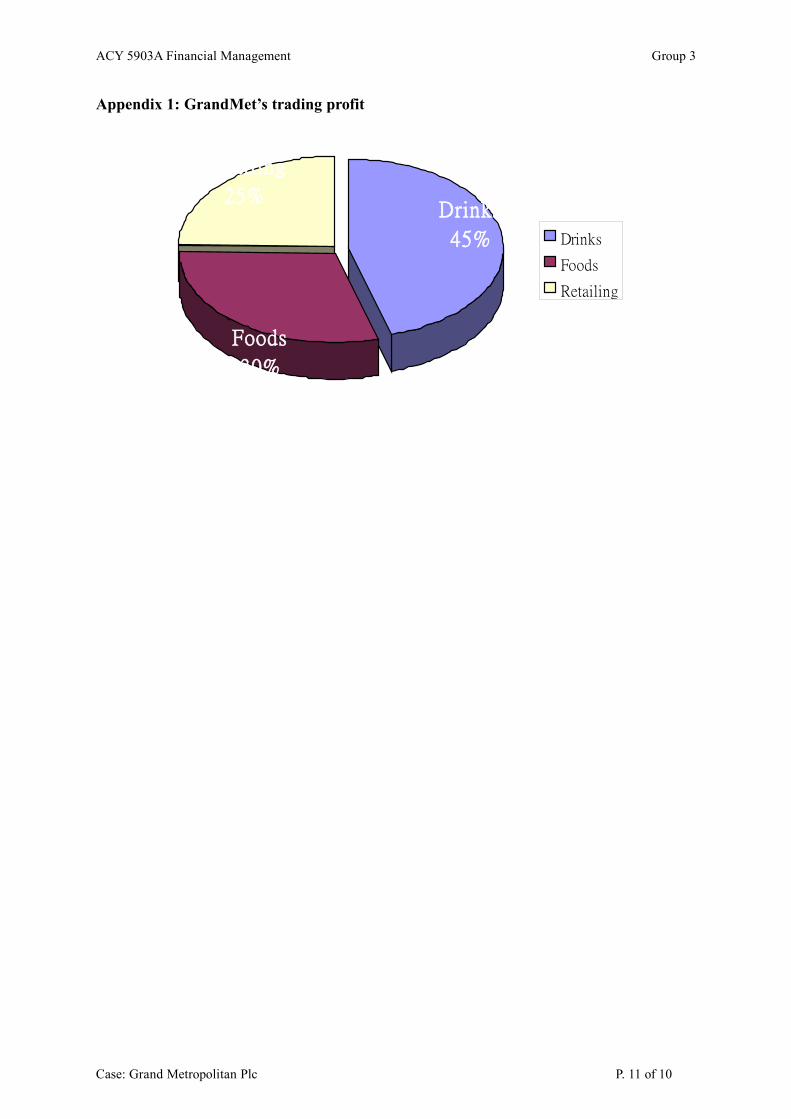

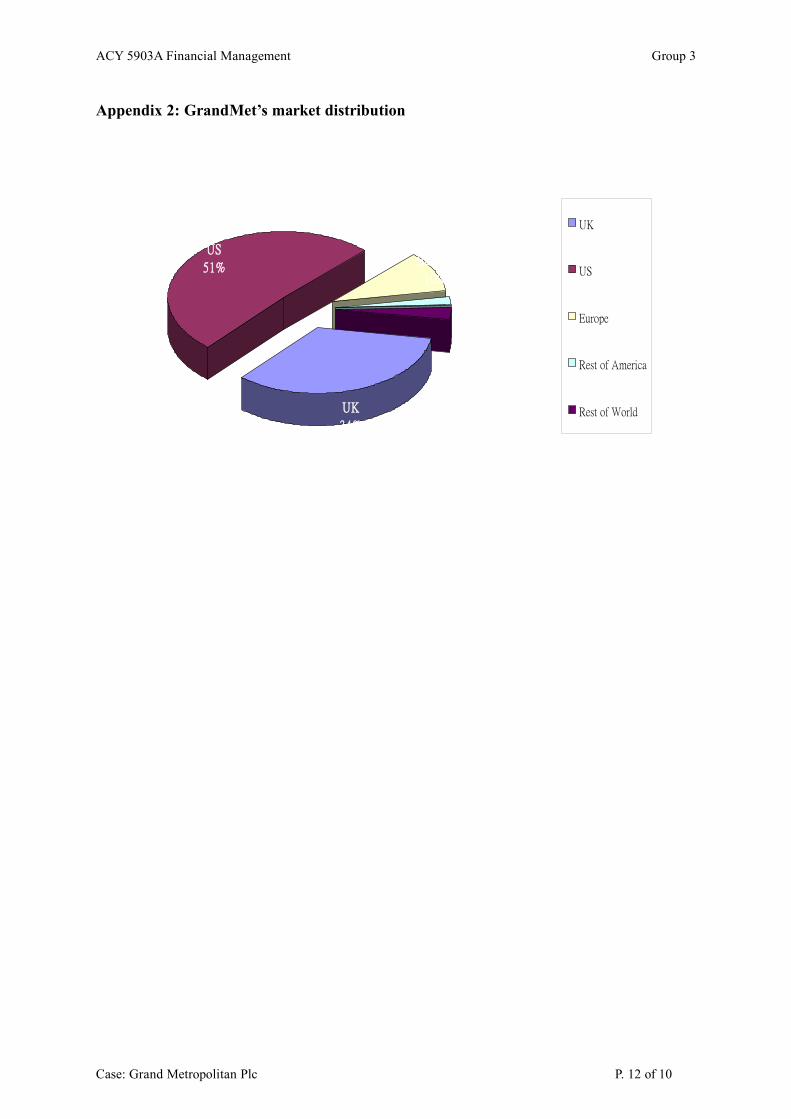

Three Strategic Business Units (SBU)

Currently, GrandMet acted as a pure holding company for a group of SBUs that were widely

diversified both geographically and in terms of products. The three major operating divisions

are foods, drinks, and retailing. Please refer to Appendix 1 for their distribution of the

group’s trading profit. The major markets of the group are US, UK, and Europe. Please refer

to Appendix 2 for the percentage of turnover contributed by the group’s different market

regions.

GrandMet Stock Exchange

GrandMet’s shares were listed on the London stock exchange and New York stock exchange

(NYSE). However, NYSE was not trading actual shares, instead, the trading was in the form

of “rights” to shares held in trust, called American Depositary Receipts (ADRs). The majority

of shareholders for the group were still in UK.

Financial Strategy

In December 1991, the CEO of the group set the objectives: build brands, cut costs, develop

products, all within the framework of total quality. From the financial point of view, there

were three financial strategies include 1) capitalize brand value, 2) increase interest coverage,

Case: Grand Metropolitan Plc P. 2 of 10

ACY 5903A Financial Management Group 3

and 3) dispose of products that do not provide an adequate return to support the group’s

operational principles.

Therefore, the group’s financial objectives would be reducing financial leverage (e.g. the

group had successfully fallen its ratio of debt / capital by 9% so that the interest-coverage ratio

had risen from 4.8 times to 6.6 times in 1991); and only investing in projects meeting growth

criteria, which also means that the group would continue to exit businesses if its future

potential earnings do not meet the growth (a 20.5% per year compound growth rate in pretax

profits has been generated during 1987-91 fiscal years).

2 PROBLEMS FACED BY THE GROUP

The group was faced two problems, they were 1) the PE ratio of GrandMet shares in New

York is 10% below the average ratio of the Standard & Poor’s company; 2) there was a

circulation of rumor that GrandMet may be a takeover target.

To address the problems, the group had to evaluate its performance. Had the entire group as

well as all their SBUs performed badly? Were the group’s financial objectives consistent with

the creation of value? Were all segments of the group’s business portfolio performing equally

well? Might one or two of them be targeted for aggressive restructuring?

3 FOUR ANALYZING APPROACHES

In order to find out the underlying cause(s) of the problems and provide recommendations, we

will go through the following analysis:

1) Financial Analysis: with the given financial statements, we will evaluate the group’s

financial performance in view of its position in profitability, liquidity, efficiency and

leverage.

2) Valuation Analysis (DDM): to explain why the group has a low PE ratio, we calculate

Case: Grand Metropolitan Plc P. 3 of 10

ACY 5903A Financial Management Group 3

the intrinsic value of the group’s share according to the Dividend Discount Model (DDM)

model and then compare it with the market value.

3) Corporate and Segment Analysis (WACC): to evaluate the performance of the group, we

calculate the weighted-average cost of capital for the group as a whole, and also

according to the group’s segments.

4) Geographic Market Analysis: besides analyzing the SBU’s performance at approach

above, we have also done a brief analysis based on the information provided for the

geographic markets.

4 FINDINGS AND RECOMMENDATIONS

1) Financial Analysis

From the financial analysis, we have the following findings:

a. Profitability

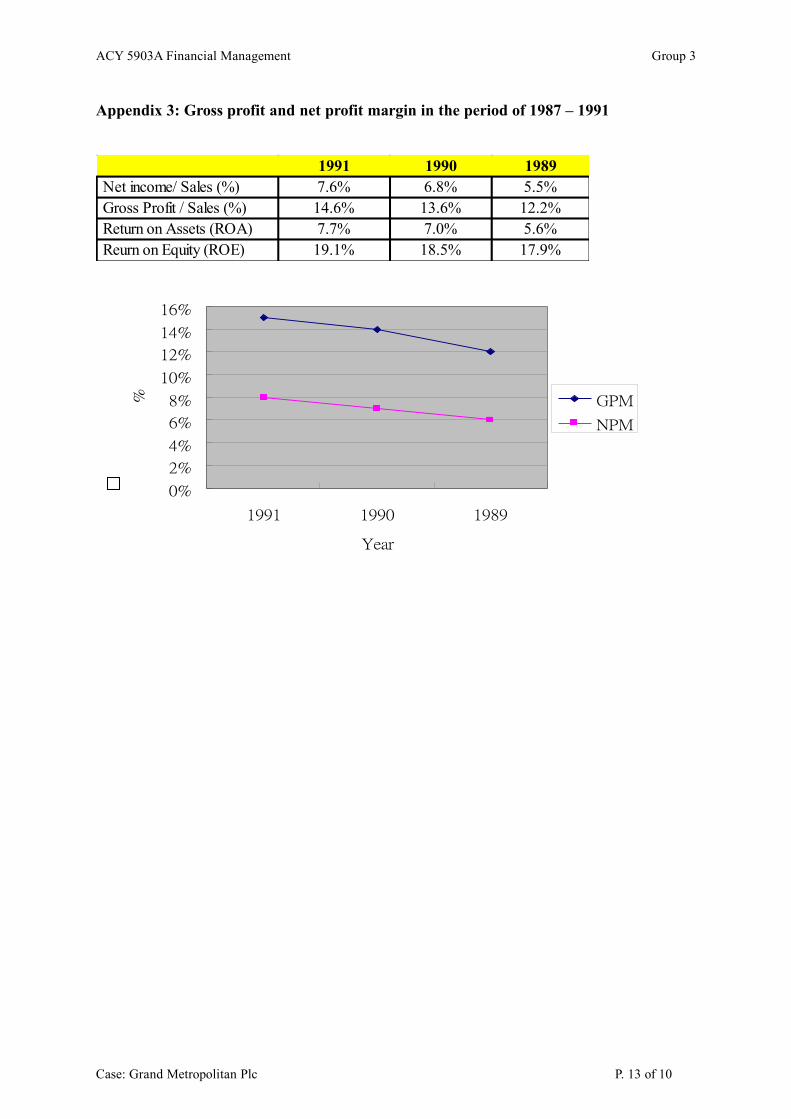

The turnover was slightly decreased by 7% from 9,394m/FY90 to 8,748m/FY91, however, the

gross profit margin (GPM) and net profit margin (NPM) were significantly improved from

13.6%/FY90 to 14.6%/FY91 and 6.8%/FY90 to 7.6%/FY91 respectively (Appendix 3). It

was mainly attributed to the lower cost of purchase and lower debt policy, which GrandMet

could enjoy lower interest expenses. Increasing NPM was also a result of sharp increase in the

profit margin from the drink’s segment (form 15.8%/FY90 to 18.7%).

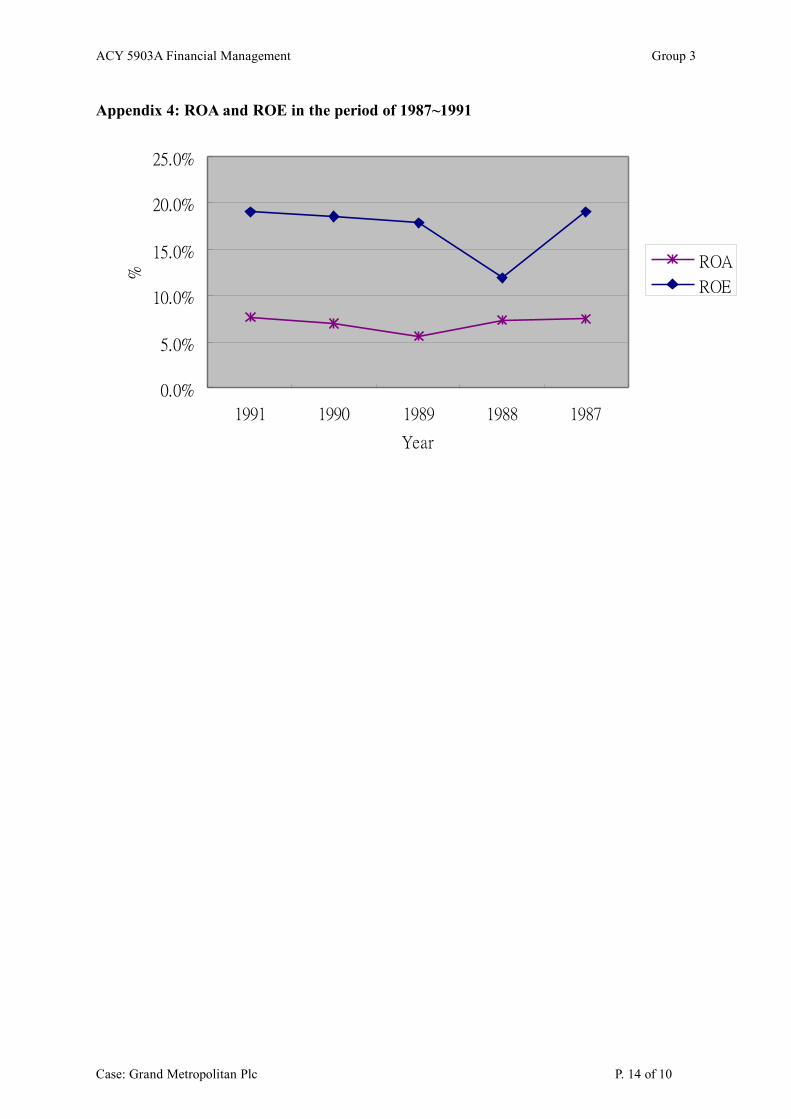

There were a slightly increased in ROA (from 6.8%/FY90 to 7.6%/FY91) and ROE

(7.0%/FY90 to 7.7%/FY91), referring to Appendix 4,which was not only due to the

increased in retained profit but also lower total asset after disposing ~ GBP800m business

segments. (Those were mainly related to the retailing business). Better ROA also was a result

of out-performance in GrandMet’s drinks segment, especially after acquiring two drink-related

companies: Remy Martin-Cointreau and Anglo Espanola de Distribution. The performance of

drinks segment was also outperforming comparing to Food and Retails segments. (In FY91,

Case: Grand Metropolitan Plc P. 4 of 10

ACY 5903A Financial Management Group 3

RONA of Drinks/Food/Retails: 19.2%/9.8%/6.6%).

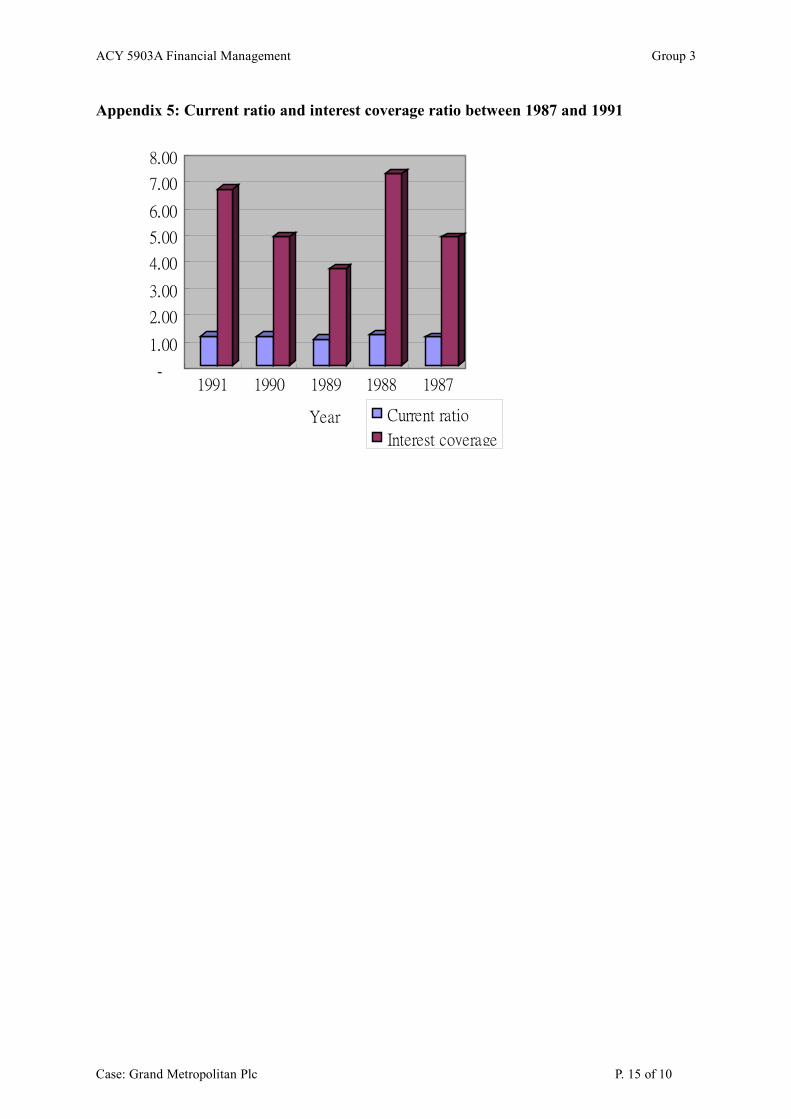

b. Liquidity: Stable

No significant change in the current and quick ratios was shown between FY90 and FY91.

(Appendix 5)

c. Efficiency: deteriorating

A sharp decline in the inventory turnover was found. (fr 38 times/FY90 to 9 times/FY91).

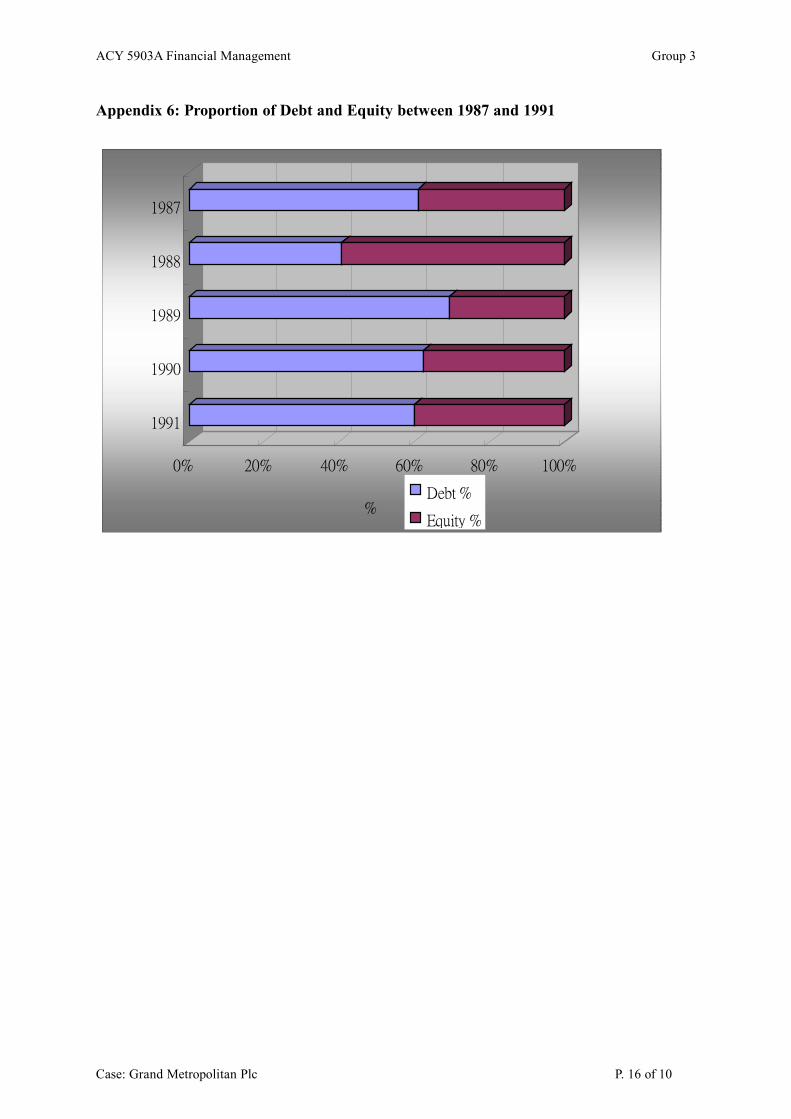

d. Leverage: improving

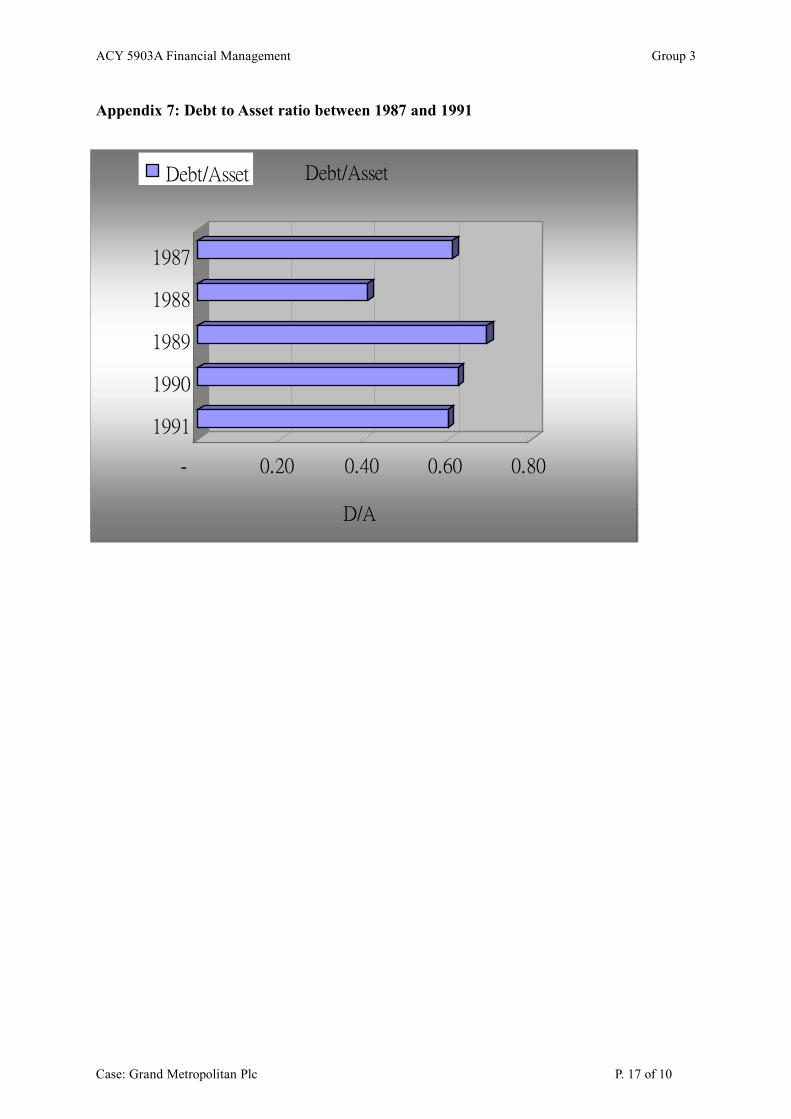

A jump in D/A ratio from 0.41x/ FY88 to 0.69 FY89 was shown after acquisition of Pillsbury

Co (i.e. A Minneapolis-based corporation incorporated in US). (Appendix 6 & 7)

To sum up, We found that the existing asset-allocation in the three segments (Drink, Food and

Retails) and also the debt-policy did not maximize GrandMet’s profitability and return on

asset, provided that:

- Misallocation of assets to the three segments appeared which distorted GrandMet’s

optimal profitability. Since the Drinks segment was out-performed in operating profit

margin and RONA comparing to the Food and Retails segments.

- The increase proportion of ROE was restricted by having high interest coverage ratio

supporting by the principal of Dupont analysis. In which, Dupont System suggests there is

an inverse relationship between ROE and debt leverage.

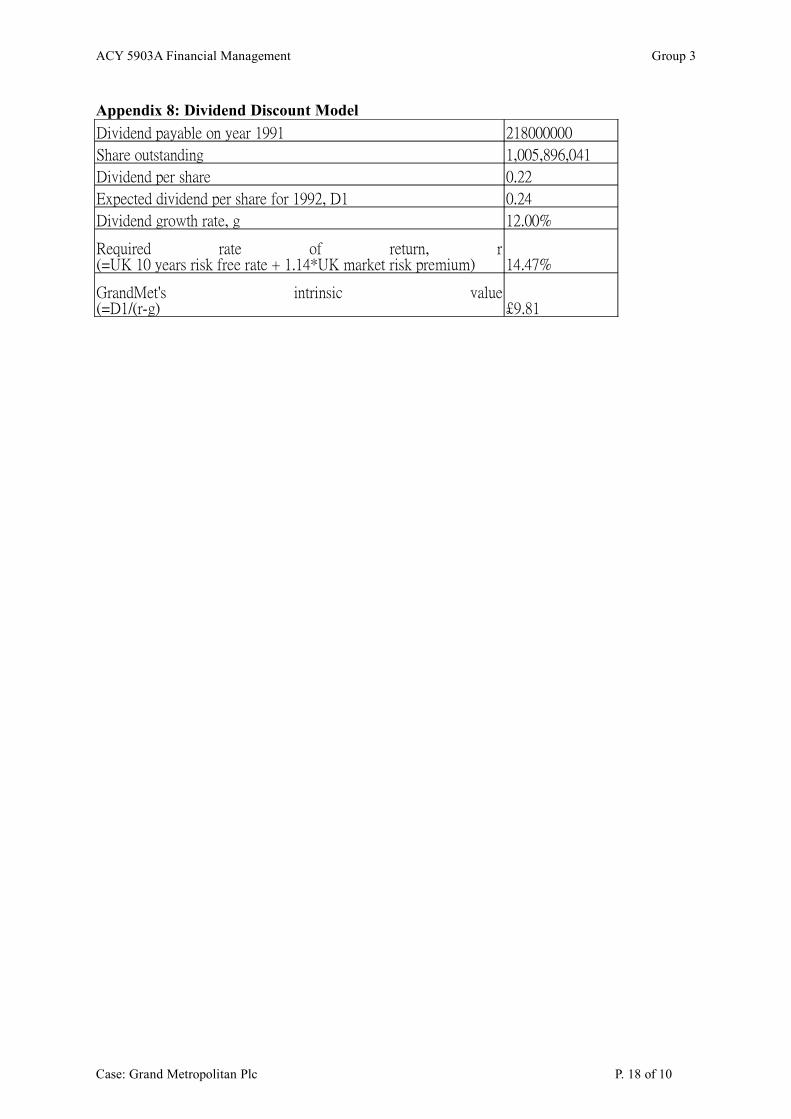

2) DDM Calculation

Appendix 8 shows the calculation of GrandMet’s intrinsic value which is equal to ₤9.81, in

which constant dividend growth and dividend policy are assumed. Compare to the market

value (₤9.48), the stock is obviously undervalued. Historically, the group had involved highly

in acquisition activities in 1980s. It is a common phenomenon for the stock price to fall on the

Case: Grand Metropolitan Plc P. 5 of 10

ACY 5903A Financial Management Group 3

bidder side and this resulted in a low P/E ratio.

3) WACC Calculation

WACC analysis is used as the assessment tool to accept or rejecting company projects/

business segment. In our analysis, company level WACC is calculated to determine the

company overall’s cost of capital. After that, we find that the company level WACC is not

enough to assess the performance of the business segment in Grand Metro but only to the

overall company performance (company overall RONA). After that we also calculate the

segment level WACC (to compare with the individual RONA) so as to find out the

underperformed sectors.

Before the calculation, we have made some assumptions on the model:

a. They are similar in financial & operating leverage among the competitors in the same

industry.

b. There is no segmentation between US & UK market with the assumption of correlation

between return in US & UK market equals to 1.

Beta in ₤ = Beta in $ x 1.4

c. There are no currency risk and interest risk as they are assumed to be perfectly eliminated

by hedging.

Company level WACC

The calculated company level WACC (in accordance to the cost of the financing component –

debt, preferred stock, convertible bond, equity) is 12.99%.

The weighted average debt component is calculated in accordance to the existing debt

financing situation in the company. On the other hand, the weighted average equity component

is computed by the CAPM model Please refer to Appendix 9 for the detailed calculation

The company level WACC is not appropriate to compare different segments’ performance with

the assumption of similar operational risk in each segment component. Hence, segment WACC

Case: Grand Metropolitan Plc P. 6 of 10

ACY 5903A Financial Management Group 3

is formed out.

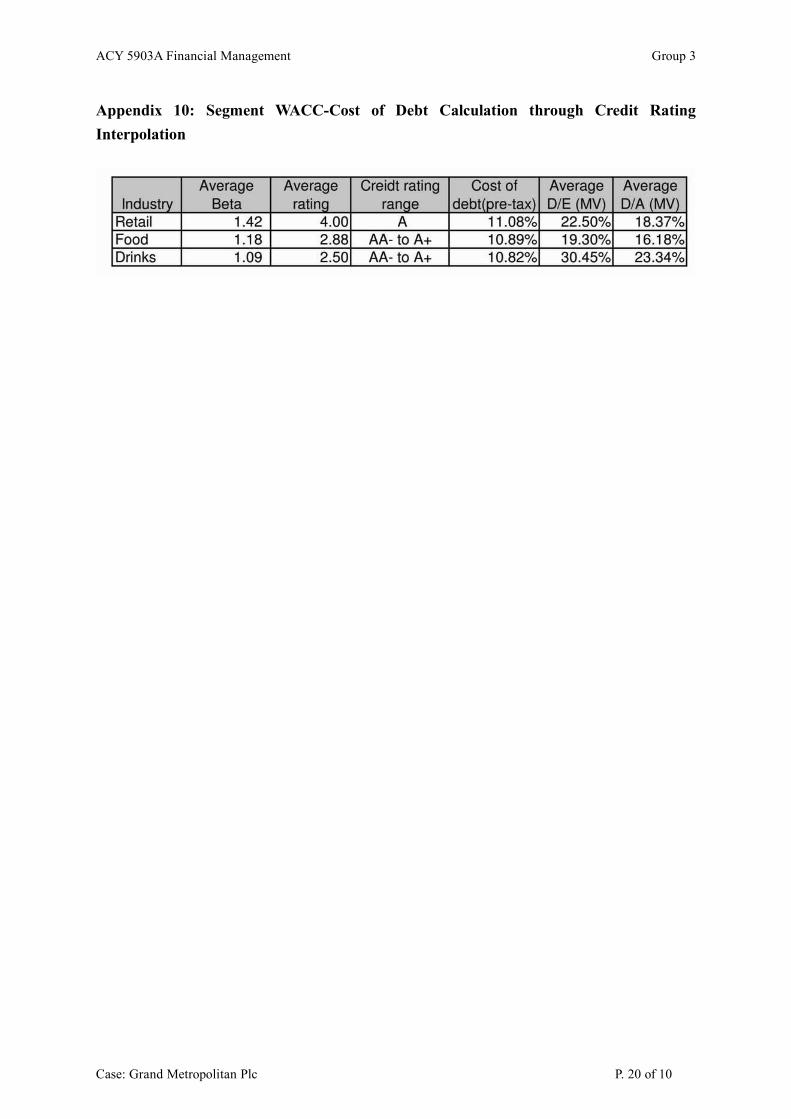

Segment WACC

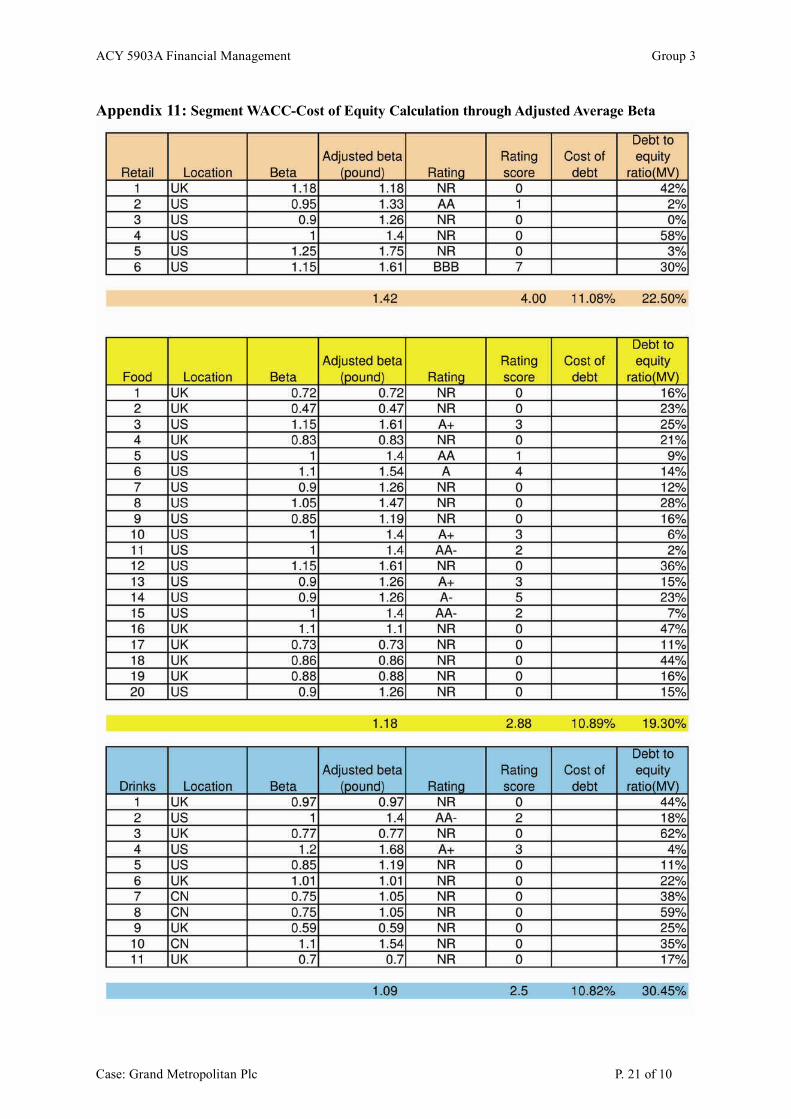

To find out the segment WACC, some industry information (i.e. cost of equity: average beta,

risk free rate, market premium; cost of debt: average credit rating & respective cost of fund;

average D/A ratio in Appendix 10-12) are gathered to formulate the result as follows:

It is formed that only the drinks industry is outperformed and the other 2 industries (Retails &

Food). Further investigation should be taken to improve the situation. Please refer to

Appendix 13 for detailed calculation.

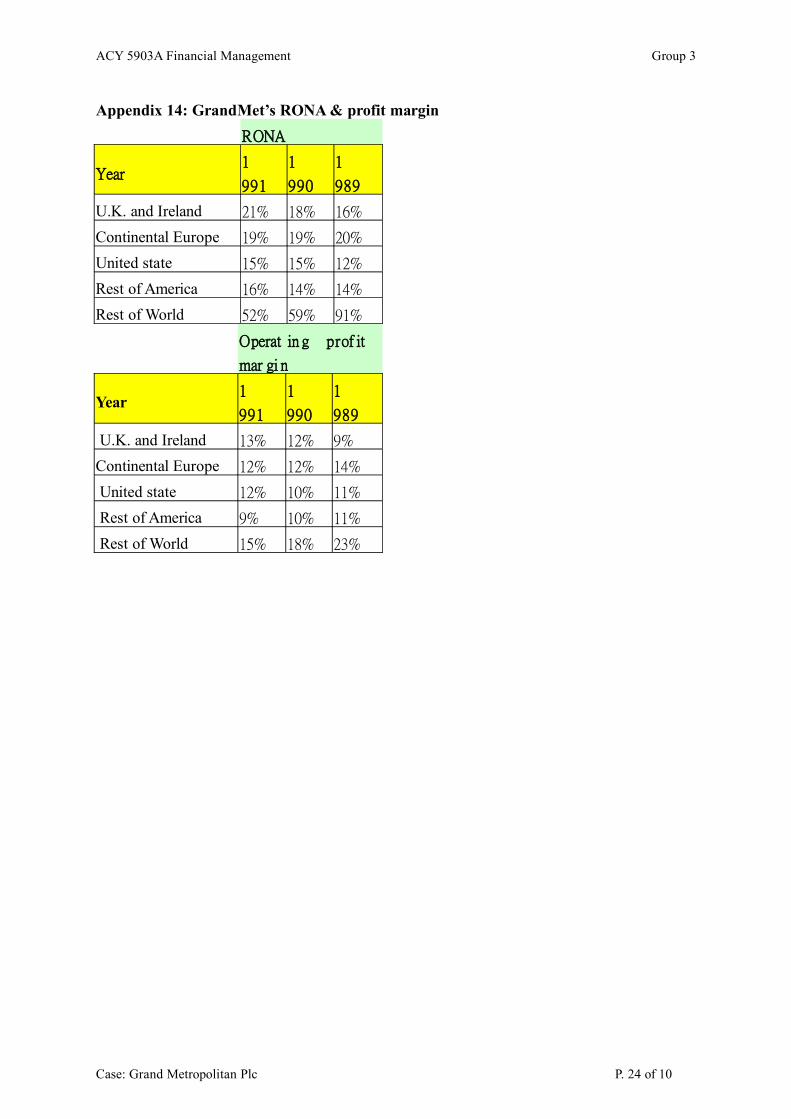

4) Geographic Market Analysis

By cost and benefit analysis, we can find out the outperformed region to be the core

developing business.

To assess the benefit, we have to select RONA & profit margin as our assessment tools

(Appendix 14):

It is found that UK should be the best efficient of asset utilization in terms of RONA among

UK, US & Europe markets. Meanwhile the profit margins among these 3 regions are similar,

while both UK and Europe show a higher RONA from 1989 to 1991 comparing with US.

The expectation of borrowing cost will be the benchmark to determine whether the region is

profitable or not. The larger the positive difference between RONA & cost of borrowing, the

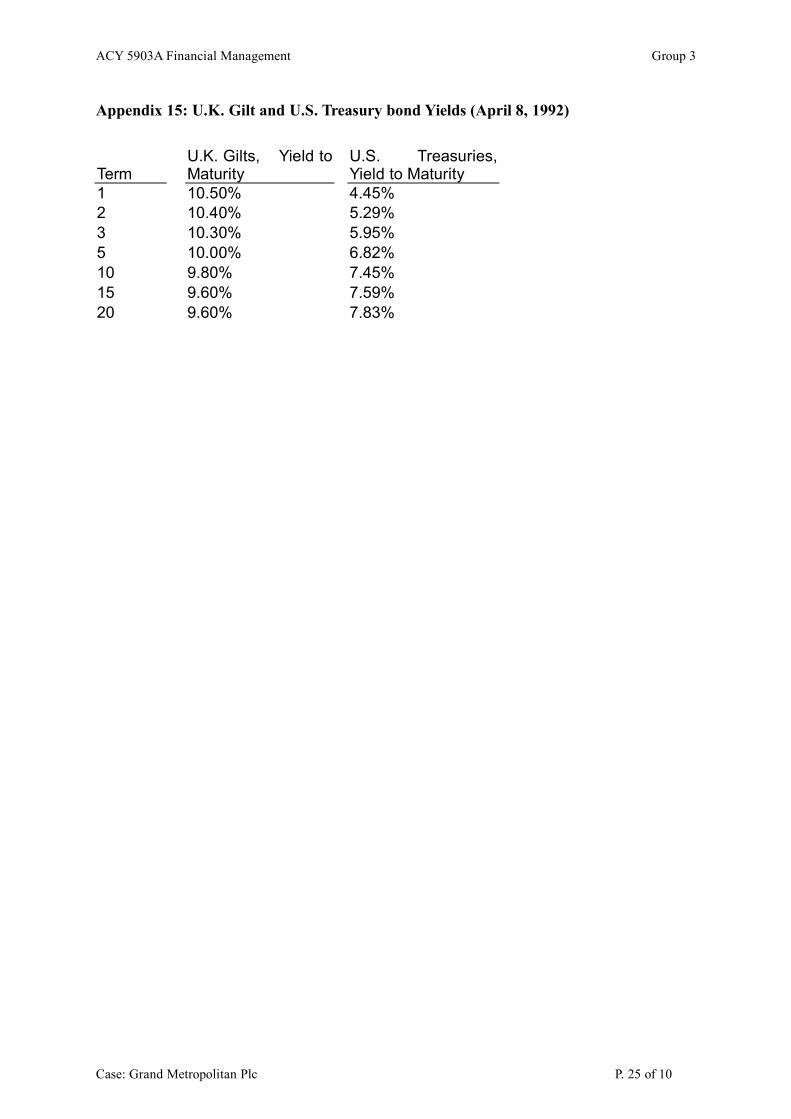

more profitable the region is. According to the yield curve trend of UK and US, we find out

that UK yield curve has a downward sloping while the US is the opposite. This shows a lower

borrowing cost in terms of debts is in UK in coming 10 years, in contrast with a high RONA in

UK. This large positive difference between RONA & cost of borrowing in UK and a relatively

high RONA in Europe are signals for us to focus and develop business in UK and Europe.

5 CONCLUSION

Case: Grand Metropolitan Plc P. 7 of 10

ACY 5903A Financial Management Group 3

GrandMet is facing a query about the company’s value (low PE ration). Besides rumors

surface that it becomes a takeover target. So, what is going wrong?

According to our analysis, we should be able to conclude as follows. In the financial analysis,

as GrandMet is a conglomerate and it is difficult to look for a similar corporate which has

similar business composition as that of GrandMet. As a result, we can only compare the

figures with the company’s own historical values.

In the valuation analysis, we use DDM to calculate the intrinsic value of GrandMet. Although

we find out the stock is undervalued, DDM is a theory which requires a lot of assumption such

as constant dividend growth. It may not be realistic to stick on this finding as well.

WACC would be a right approach to analysis the problem but a single hurdle rate does not fit

as well. With the use of segment WACC analysis, we find out that the Drinks segment

outperformed the Retails and Food segments.

6 RECOMMENDATIONS

As Drinks segment is the only segment having good performance, should GrandMet sell off

and cut the other segments? Here , we have to consider that GrandMet is a huge conglomerate

and there is a very good synergistic effect and diversification. Also, the company could enjoy

the benefit from the economic of scope and scale. By simply withdrawing from the food and

retailing industries would be risky to GrandMet as the competitor will take up the market

share. Besides, synergistic effect will be sacrificed. As a result, it is not wise to sell off or cut

the under-performed segments immediately.

We recommend GrandMet to develop a long term strategic planning divided into 2 phases to

tackle the problems.

Phase I) Restructuring & reengineering of food and retail segments

Case: Grand Metropolitan Plc P. 8 of 10

ACY 5903A Financial Management Group 3

Existing management structure should be reviewed and business processes need to be

reengineered. This is what the company should focus on immediately with constant

evaluation. If they are still underperformed, we move on to Phase II.

Phase II) Selling out underperformed business sectors in Food and Retails segments

Underperformed segments in Food and Retails markets should be sold out gradually. Focus

will be back to the Drinks segment. Further merger and acquisition should take place on

potential outperformed market players.

In the long run, the most important is, the company should keep working on better corporate

governance and increase its transparency to the public. Only have the outsiders realized that

the company is moving on the right track, the company’s “adding value” goal can be achieved

and this will be reflected in the stock price eventually.

Geographically, there are good operating margins in UK, the highest RONA (efficiency on

asset) in UK and satisfactory RONA in Europe. We would suggest further development in the

UK and European markets. From the downward sloping of the UK yield curve which

represents a lower interest rate and lower cost in coming years, this is also a beneficial

opportunity to move the business to Europe compared with the upward yield curve in US. As

both trends in cost and return are comparatively better in UK, UK and Europe will be our

target market in the coming ten years.

6 POSTSCRIPT

On 1996, GrandMet acquired William Hill Organization Limited. European food business was

revamped by selling out Erasco Group and refocusing on brands like Pillsbury, Green Giant

and Haagen-Dazs again. Its headquarters also moved from Britain to Paris in the same year.

In the Food and Retails segment, there was a dramatic change. First of all, senior management

Case: Grand Metropolitan Plc P. 9 of 10

ACY 5903A Financial Management Group 3

of Burger King was re-assigned on 1997. Afterwards, GrandMet further merged with

Guinness to form the Diageo. Further restructuring then took place and Burger King and

Pillsbury were sold out. The company sold out most food businesses and refocused on

premium Drinks market in 2002. All these movements were in line with our conclusion in the

previous section.

Therefore, we do believe our 2 phases’ recommendations could constructively tackle the

problems of GrandMet.

Case: Grand Metropolitan Plc P. 10 of 10

ACY 5903A Financial Management Group 3

Appendix 1: GrandMet’s trading profit

Case: Grand Metropolitan Plc P. 11 of 10

Retailing

25%Drinks

45%

Foods

30%

Drinks

Foods

Retailing

ACY 5903A Financial Management Group 3

Appendix 2: GrandMet’s market distribution

Case: Grand Metropolitan Plc P. 12 of 10

Rest of America

2%

Europe

10%

Rest of World

3%

UK

34%

US

51%

UK

US

Europe

Rest of America

Rest of World

ACY 5903A Financial Management Group 3

Appendix 3: Gross profit and net profit margin in the period of 1987 – 1991

Case: Grand Metropolitan Plc P. 13 of 10

0%

2%

4%

6%

8%

10%

12%

14%

16%

1991 1990 1989

Year

% GPM

NPM

1991 1990 1989 Net income/ Sales (%) 7.6% 6.8% 5.5% Gross Profit / Sales (%) 14.6% 13.6% 12.2% Return on Assets (ROA) 7.7% 7.0% 5.6% Reurn on Equity (ROE) 19.1% 18.5% 17.9%

ACY 5903A Financial Management Group 3

Appendix 4: ROA and ROE in the period of 1987~1991

Case: Grand Metropolitan Plc P. 14 of 10

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

1991 1990 1989 1988 1987

Year

%

ROA

ROE

ACY 5903A Financial Management Group 3

Appendix 5: Current ratio and interest coverage ratio between 1987 and 1991

Case: Grand Metropolitan Plc P. 15 of 10

-

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

1991 1990 1989 1988 1987

Year Current ratio

Interest coverage

ACY 5903A Financial Management Group 3

Appendix 6: Proportion of Debt and Equity between 1987 and 1991

Case: Grand Metropolitan Plc P. 16 of 10

0% 20% 40% 60% 80% 100%

%

1991

1990

1989

1988

1987

Debt %

Equity %

ACY 5903A Financial Management Group 3

Appendix 7: Debt to Asset ratio between 1987 and 1991

Case: Grand Metropolitan Plc P. 17 of 10

- 0.20 0.40 0.60 0.80

D/A

1991

1990

1989

1988

1987

Debt/AssetDebt/Asset

ACY 5903A Financial Management Group 3

Appendix 8: Dividend Discount Model

Dividend payable on year 1991 218000000

Share outstanding 1,005,896,041

Dividend per share 0.22

Expected dividend per share for 1992, D1 0.24

Dividend growth rate, g 12.00%

Required rate of return, r(=UK 10 years risk free rate + 1.14*UK market risk premium) 14.47%

GrandMet's intrinsic value(=D1/(r-g) £9.81

Case: Grand Metropolitan Plc P. 18 of 10

ACY 5903A Financial Management Group 3

Appendix 9: Calculation of group level WACC

Case: Grand Metropolitan Plc P. 19 of 10

ACY 5903A Financial Management Group 3

Appendix 10: Segment WACC-Cost of Debt Calculation through Credit Rating

Interpolation

Case: Grand Metropolitan Plc P. 20 of 10

ACY 5903A Financial Management Group 3

Appendix 11: Segment WACC-Cost of Equity Calculation through Adjusted Average Beta

Case: Grand Metropolitan Plc P. 21 of 10

ACY 5903A Financial Management Group 3

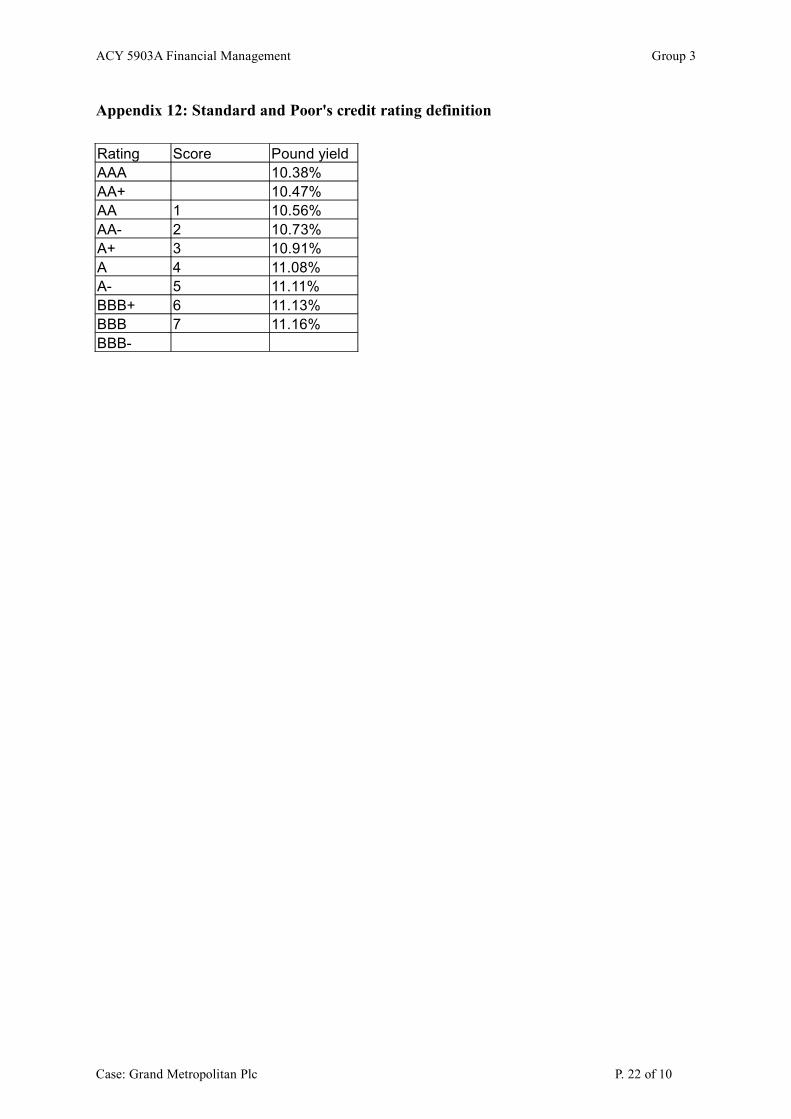

Appendix 12: Standard and Poor's credit rating definition

Rating Score Pound yieldAAA 10.38%AA+ 10.47%AA 1 10.56%AA- 2 10.73%A+ 3 10.91%A 4 11.08%A- 5 11.11%BBB+ 6 11.13%BBB 7 11.16%BBB-

Case: Grand Metropolitan Plc P. 22 of 10

ACY 5903A Financial Management Group 3

Appendix 13: Calculation of segment WACC

Case: Grand Metropolitan Plc P. 23 of 10

ACY 5903A Financial Management Group 3

Appendix 14: GrandMet’s RONA & profit margin

RONA

Year1

991

1

990

1

989

U.K. and Ireland 21% 18% 16%

Continental Europe 19% 19% 20%

United state 15% 15% 12%

Rest of America 16% 14% 14%

Rest of World 52% 59% 91%

Operat in g prof it

mar gi n

Year1

991

1

990

1

989

U.K. and Ireland 13% 12% 9%

Continental Europe 12% 12% 14%

United state 12% 10% 11%

Rest of America 9% 10% 11%

Rest of World 15% 18% 23%

Case: Grand Metropolitan Plc P. 24 of 10

ACY 5903A Financial Management Group 3

Appendix 15: U.K. Gilt and U.S. Treasury bond Yields (April 8, 1992)

Term U.K. Gilts, Yield to Maturity

U.S. Treasuries, Yield to Maturity

1 10.50% 4.45%2 10.40% 5.29%3 10.30% 5.95%5 10.00% 6.82%10 9.80% 7.45%15 9.60% 7.59%20 9.60% 7.83%

Case: Grand Metropolitan Plc P. 25 of 10

ACY 5903A Financial Management Group 3

Reference

The writing is based on the following materials:1. The Investopedia - http://www.investopedia.com/articles/fundamental/04/041404.asp2. Keown, Martin, Petty, & Scott, Jr., Financial Management: Principles and Applications

(Pearson Education International, 10th ed, 2005)3. Philippe Demigne, Jean-Christophe Donck, Bertrand George and Michael Lev with

Professor Robert F. Bruner, Case of Grand Metropolitan PLC (Darden Business Publishing, University of Virginia)

Case: Grand Metropolitan Plc P. 26 of 10