Embed Size (px)

Citation preview

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

University of Maryland Extension

Grain Marketing101

Jenny Rhodes

Shannon Dill

John Hall

Extension Educators,

Agriculture & Natural Resources

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Marketing terminology

CBOT futuresBasis Contracts

• Forward Contract• Hedge to Arrive• Basis Contract• Futures Contract

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Marketing terminology

Options• Put• Calls

Futures months• Corn • Soybeans• Wheat

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Marketing terminology

BearBearish MarketBullBullish Market

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Marketing terminologyWeb resources:Chicago Board of Trade

www.cbot.com after to 1/9/09 will be www.cmegroup.comDTN Ag Data–www.agdayta.com

Ag Webwww.agweb.com

Grain Marketing - MCEwww.mdgrainmarketing.umd.edu

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Marketing terminology

Basis • is the difference between a cash

price and a futures price of a particular commodity on a given futures exchange.

• It is calculated as: Basis = cash price - futures price. Basis can be positive or negative.

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Marketing terminology

Contracts• Forward Contract

– is a contract for the cash sale of grain at a specified price for future delivery.

• Hedge to Arrive– Is a contract for the cash sale of grain

which locks in the futures price at the date of contracting, the basis can be locked in later.

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Marketing terminology

Contracts• Basis Contract

– is an agreement between a producer and grain elevator (or feedlot) that specifies the cash price upon future delivery as a fixed amount in relation to the futures price (above or below), thus fixing the basis

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

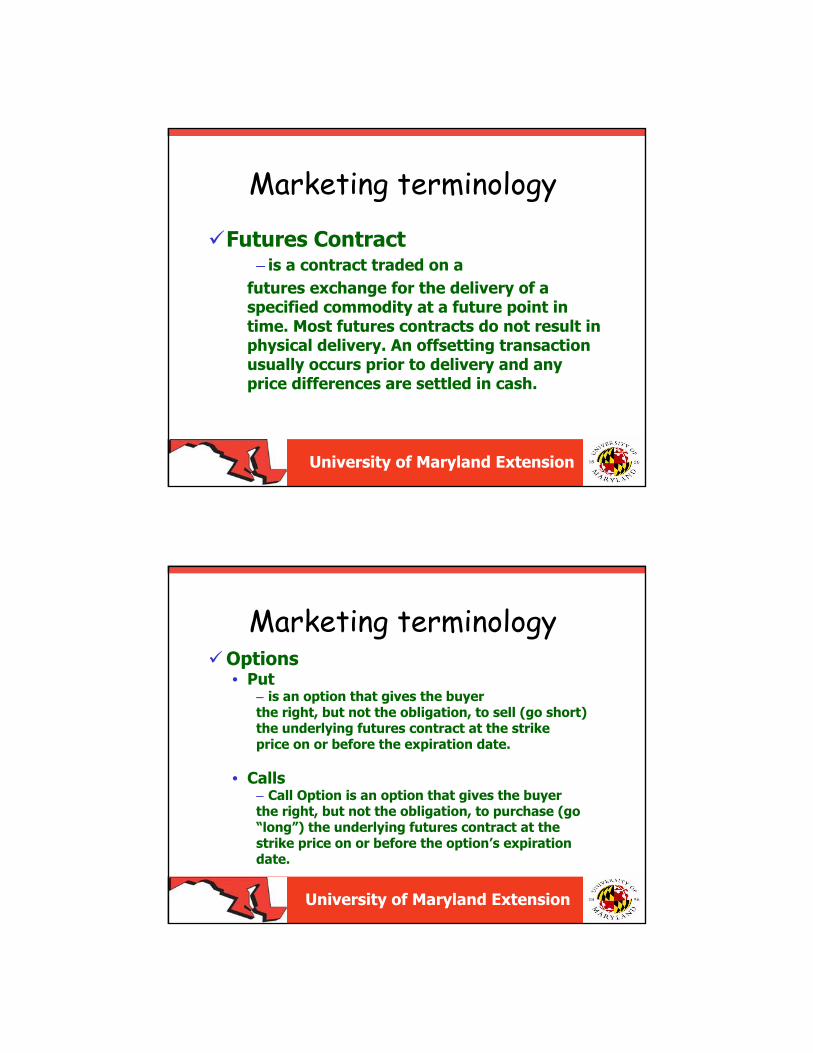

Marketing terminology

Futures Contract– is a contract traded on a

futures exchange for the delivery of a specified commodity at a future point in time. Most futures contracts do not result in physical delivery. An offsetting transaction usually occurs prior to delivery and any price differences are settled in cash.

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Marketing terminologyOptions• Put

– is an option that gives the buyerthe right, but not the obligation, to sell (go short)the underlying futures contract at the strikeprice on or before the expiration date.

• Calls– Call Option is an option that gives the buyerthe right, but not the obligation, to purchase (go“long”) the underlying futures contract at thestrike price on or before the option’s expirationdate.

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Marketing terminologyFutures month• The months at which the futures trade

• Corn – Harvest – Dec – Store - JFM

• Soybeans– Harvest - Nov – Store - JFM

• Wheat– Harvest - July

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Marketing terminologyBear• is a person who expects lower prices.

Bearish Market• is a market in which prices are declining.

Bull• is a person who expects higher prices.

Bullish Market• is a market in which prices are increasing.

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Marketing tools

Using Crop InsuranceCrop Budgets

• Need to know cost of production– Overall– By farm– By field

• Need to know break-even price you must receive

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Marketing tools

Traditional market trends• Market highs usually occur January

to May• Market volatility during growing

time

May need upside potential

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Marketing tools

Marketing tools• Fixed price tools

– Forward Contracts– Hedge to Arrives– Futures contracts

• Minimum price tools– PUT option – setting a price floor– CALL option – upside potential

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

BasisCash price = Futures Price –BasisBasis continues to change!Need to recognize good basisNew processing plants are adding a new level of volatility to basis, particularly in the corn belt - this will affect the East Coast too. Keep up with the changes!

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Maryland Lower Eastern ShoreNearby Corn Basis, 1999-2007

Nearby Basis = Cash Price – Nearby Corn FuturesSource: Maryland Grain and Livestock Report, Maryland Department of Agriculture

University of Maryland Extension

25242724262627241914412Avg

4134221516171513322007

815171819161821219-262006

12519152329352721154132005

1471918222528272018-312004

323537333231353431271272003

4051484952545346444541312002

342631313029261872-1412001

212426191403-3-11-13-1022000

22192522263033321999

AugJulJunMayAprMarFebJanDecNovOctSep

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Maryland Lower Eastern ShoreNearby Soybean Basis, 1999-2007

Nearby Basis = Cash Price – Nearby Soybean Futures

Source: Maryland Grain and Livestock Report, Maryland Department of AgricultureUniversity of Maryland Extension

-12-4-8-6-6-235-17-24-18-16Avg-29-31-16-21-17-19-39-11-322007

-614679415-12-22-20-182006

-18-12-11-10-1034-10-26-17-9-122005

-10-11-15-12-11-74-6-20-32-2132004

-9-17-49-13-3-7-9-25-29-28-212003

-233-3-641416151919622002

6283-1-4-4-1-6-18-36-29-332001

-30-22-13-4-5-5-7-27-50-50-26-202000

-8-4-15-12-8-5-3-21999

AugJulJunMayAprMarFebJanDecNovOctSep

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

(0.04)2.682.722006(0.21)2.062.272005(1.11)2.063.172004

(0.10)3.693.792007

0.362.562.202002

(0.24)2.422.65Average

(0.13)2.202.332003

(0.16)2.112.272001(0.63)1.992.622000(0.26)2.052.311999(0.58)2.052.621998(0.20)2.562.761997(0.44)2.903.3319960.483.112.631995

(0.44)2.142.5819940.002.432.431993

(0.41)2.122.5319920.012.542.531991

(0.42)2.292.701990Change1-Oct1-MayYear

CBOT December Corn Futures, 1990-200714 years (78%) the market declined

4 years (22%) the market improved

7 years the market declined more than 40 cents!

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Chicago December Corn Futures, 1990-2007 average

1-Ja

n 1-Fe

b 1-M

ar

1-A

pr

1-M

ay

1-Ju

n

1-Ju

l

1-A

u g

1-Se

p

1-O

ct

1-N

ov

1-D

ec

240

245

250

255

260

265

270

275

approximate dates

cent

s pe

r bu

shel

Don’t forget to sell something!

But remember your minimum price….

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

(0.81)5.456.262006(0.49)5.736.222005(2.10)5.357.452004

2.089.927.842007

0.865.424.562002

(0.21)5.946.16Average

1.346.875.532003

0.18 4.524.342001(0.90)4.905.802000(0.33)4.815.141999(1.02)5.156.171998(0.76)6.216.961997(0.08)7.497.5819960.326.376.061995

(0.90)5.386.2819940.226.185.961993

(0.72)5.336.051992(0.20)5.896.091991(0.51)6.056.551990Change1-Oct1-MayContract

CBOT November Soybean Futures, 1990-2007

12 years (67%) the market declined

6 years (33%) the market improved

8 years the market declined more than 50 cents!

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Chicago November Soybean Futures, 1990-2007 average

1-Ja

n

1-Fe

b

1-M

ar

1-Ap

r

1-M

a y

1-Ju

n

1-Ju

l

1-A

ug 1-Se

p

1-O

ct

1-N

ov

580

585

590

595

600

605

610

615

620

approximate dates

cent

s pe

r bu

shel

Don’t forget to sell something!

But remember your minimum price….

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

0.06 3.72 3.65 20060.01 3.24 3.23 2005

(0.60)3.31 3.90 2004

0.695.705.012007

0.25 3.062.82 2003

(0.12)3.36 3.47 Average

0.42 3.16 2.74 2002(0.31)2.51 2.82 2001(0.05)2.60 2.65 2000(0.22)2.46 2.68 1999(0.28)2.74 3.01 1998(1.03)3.23 4.25 1997(1.13)4.84 5.97 19960.87 4.46 3.59 1995

(0.23)3.12 3.35 1994(0.09)2.92 3.01 1993(0.13)3.46 3.59 1992(0.16)2.67 2.83 1991(0.15)3.27 3.42 1990Change1-Jul1-MayYear

Chicago July Soft RedWinter Wheat, 1990-2007

12 years (67%) the market declined

6 years (33%) the market improved

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Chicago July Wheat Futures, 1990-2005 average

1-Au

g 1-Se

p

1-O

ct

1-N

ov

1-D

ec

1-Ja

n 1-Fe

b

1-M

ar

1-Ap

r 1-M

ay

1-Ju

n

1-Ju

l

310

315

320

325

330

335

340

345

approximate dates

cent

s pe

r bu

shel

But remember your minimum price….

Don’t forget to sell something early!

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

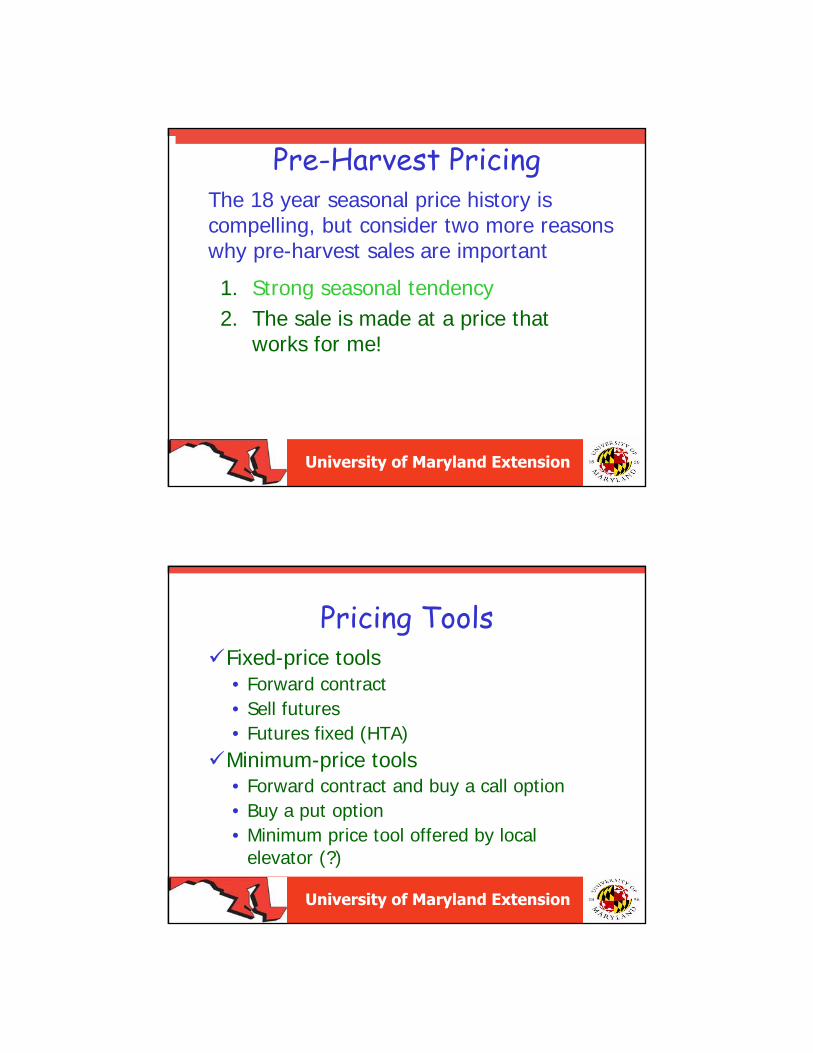

Pre-Harvest PricingThe 18 year seasonal price history is compelling, but consider two more reasons why pre-harvest sales are important

1. Strong seasonal tendency2. The sale is made at a price that

works for me!

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Pricing ToolsFixed-price tools• Forward contract• Sell futures• Futures fixed (HTA)Minimum-price tools• Forward contract and buy a call option• Buy a put option• Minimum price tool offered by local

elevator (?)

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Pricing ToolsFixed-price tools+Final price is known (or nearly known)– No “upside” potential if prices go higherMinimum-price tools (Options)+Upside potential– High cost makes it difficult to use in

early sales (which are likely lower price sales)

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Fixed-Price ToolsForward contract+Exact price is known (basis is fixed)+Contract can be for any bushel amount,

not just 5,000 bushel increments+No brokerage fee, margin accounts or

margin calls– Ends in delivery– Sometimes difficult to get a “fair” basis

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Buyer: Nagel Farm Service, Inc Date: 06/05/08P. O. Box 340 Contract: 005345Preston, MD 21655 Account # RHODEJ

Seller: Jennifer L. Rhodes180 Chestnut Vale Farm LaneCentreville, MD 21617

We confirm PURCHASE from you as follows:---------------------------------------------------------------------------------------------------------------------------

------Commodity Quantity Price Delivery From Price Basis Loc Buyer ---------------------------------------------------------------------------------------------------------------------------#2 Corn 5,000.00 7.20 01/01/09-03/31/09 Delivered 001 Chad---------------------------------------------------------------------------------------------------------------------------

Remarks: #2 CornDelivered to Bridgeville or SeafordJ/F/M 2009

---------------------------------------------------------------------------------------------------------------------------

Fixed-Price Tools- Forward Contract

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Buyer: Nagel Farm Service, Inc Date: 11/18/08P. O. Box 340 Contract: 005472Preston, MD 21655 Account # RHODEJ

Seller: Jennifer L. Rhodes180 Chestnut Vale Farm LaneCentreville, MD 21617

We confirm PURCHASE from you as follows:---------------------------------------------------------------------------------------------------------------------------------Commodity Quantity Basis Option Delivery From Price Basis Loc Buyer ---------------------------------------------------------------------------------------------------------------------------------#2 Corn 5,000.00 .08000- MAR09 03/01/09-03/31/09 Dlvd: Wye Mills 001 Chad---------------------------------------------------------------------------------------------------------------------------------

Remarks: ‘08 Corn Harvest---------------------------------------------------------------------------------------------------------------------------------BASIS CONTRACTS MUST BE PRICED OR ROLLED DURING CBOT TRADING HOURS PRIOR TO FIRST

NOTICE DAY OF THE CORRESPONDING FUTURES CONTRACT***********************************************************************

Fixed-Price Tools- Basis Contract

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Fixed-Price ToolsSell futures (hedging)+ Average price is usually higher compared to

forward contracting+ Not locked into delivery, can be rolled into a

storage hedge to capture market carry after harvest

– Contract in units of 5,000 bushels– Requires margin account and must provide margin

money as market fluctuates (margin calls)– Must buy futures to exit the position– Basis risk

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Fixed-Price ToolsSell futures – What is my expected price?

futures price (when sold) + expected harvest basis – brokerage fees = expected price

$8.20 + (-0.30) - 0.01 $7.89

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

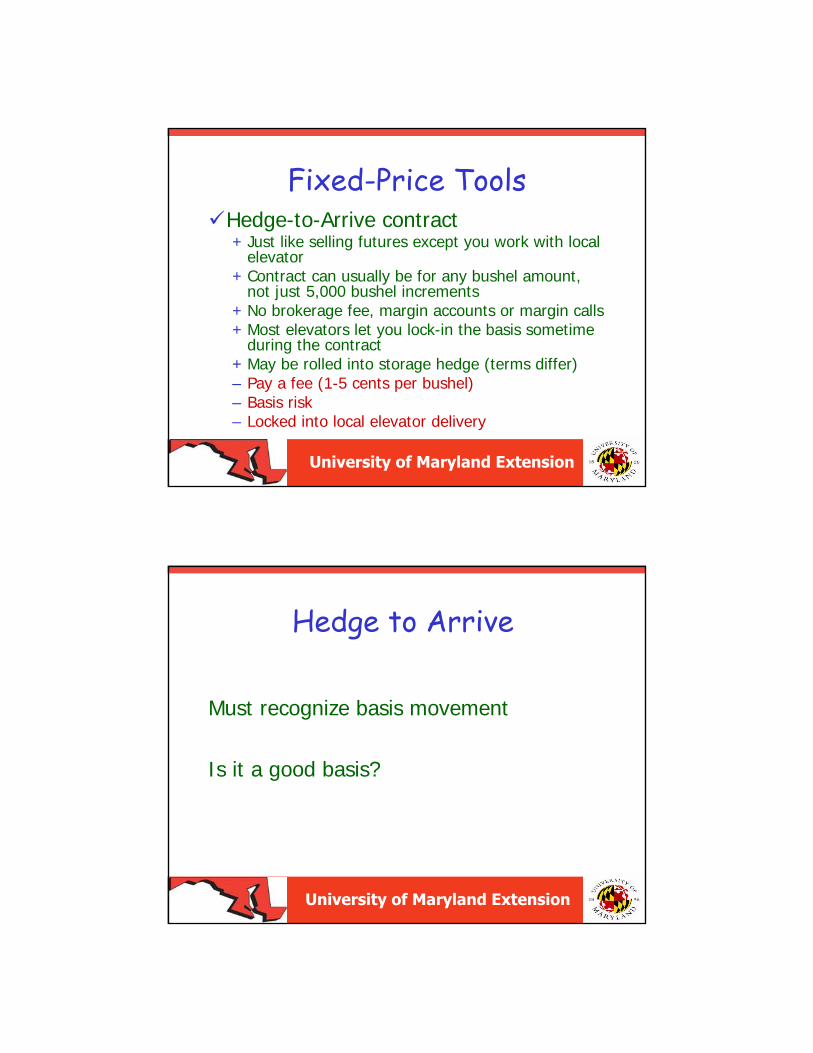

Fixed-Price ToolsHedge-to-Arrive contract+ Just like selling futures except you work with local

elevator+ Contract can usually be for any bushel amount,

not just 5,000 bushel increments+ No brokerage fee, margin accounts or margin calls+ Most elevators let you lock-in the basis sometime

during the contract+ May be rolled into storage hedge (terms differ)– Pay a fee (1-5 cents per bushel)– Basis risk– Locked into local elevator delivery

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Hedge to Arrive

Must recognize basis movement

Is it a good basis?

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Costs of tools

A. Forward ContractBushels * (Futures Price + Basis)

Cost?

No cost – Must guarantee bushels with the elevator

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Fixed-Price ToolsSell forward contract – What is my expected price?

Contract price = expected price$2.51 = $2.51

What happens if prices go up?Go down?

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

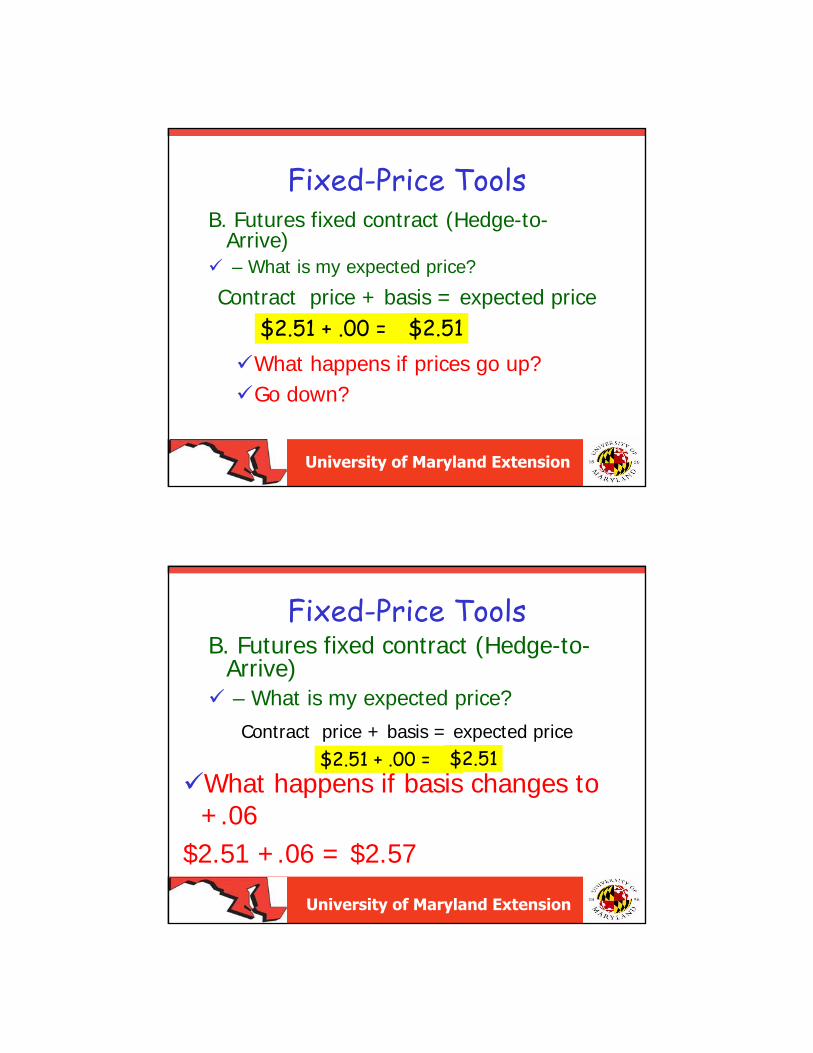

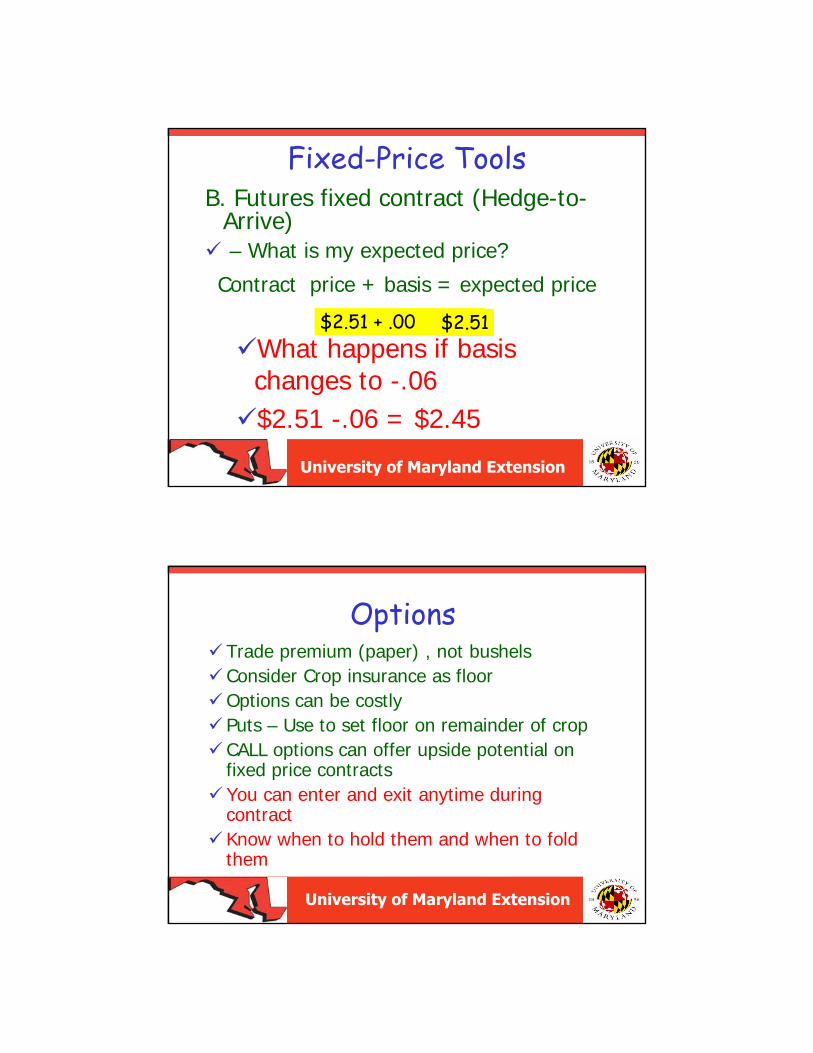

Fixed-Price ToolsB. Futures fixed contract (Hedge-to-

Arrive)– What is my expected price?

Contract price + basis = expected price$2.51 + .00 = $2.51What happens if prices go up?Go down?

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Fixed-Price ToolsB. Futures fixed contract (Hedge-to-

Arrive)– What is my expected price?Contract price + basis = expected price

$2.51 + .00 = $2.51What happens if basis changes to +.06

$2.51 +.06 = $2.57

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Fixed-Price ToolsB. Futures fixed contract (Hedge-to-

Arrive)– What is my expected price?

Contract price + basis = expected price

$2.51 + .00 = $2.51What happens if basis changes to -.06$2.51 -.06 = $2.45

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

OptionsTrade premium (paper) , not bushelsConsider Crop insurance as floorOptions can be costlyPuts – Use to set floor on remainder of cropCALL options can offer upside potential on fixed price contractsYou can enter and exit anytime during contractKnow when to hold them and when to fold them

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

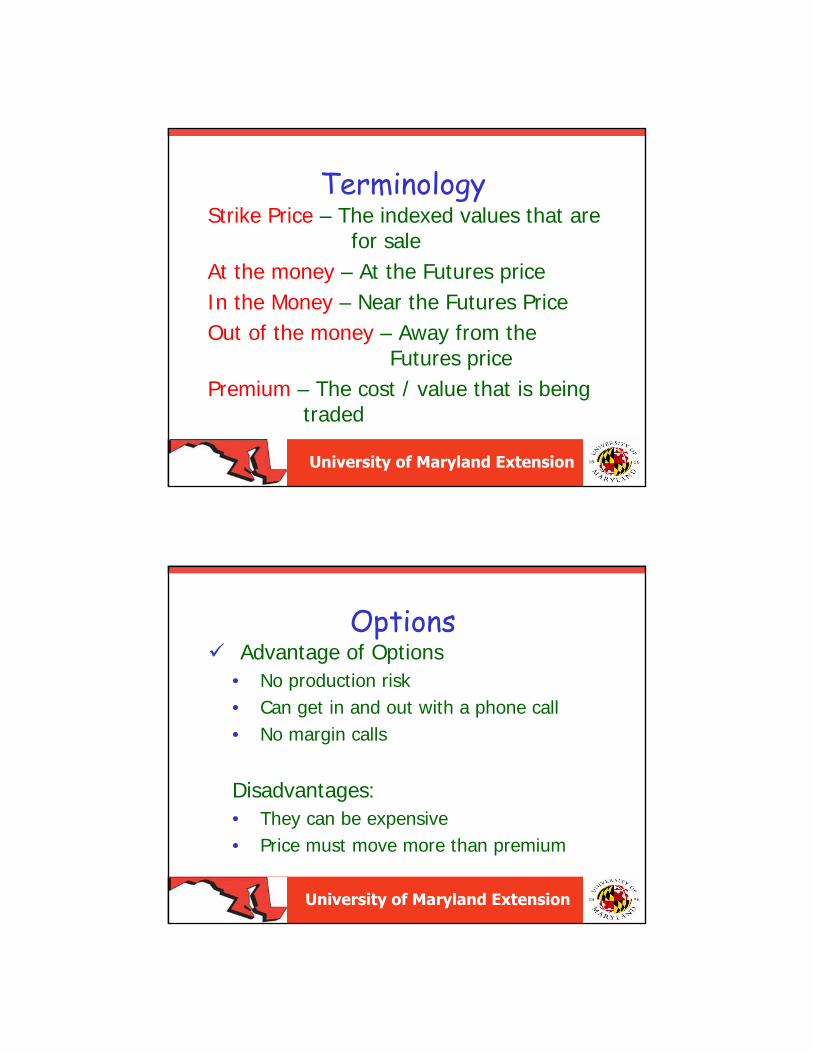

TerminologyStrike Price – The indexed values that are

for sale At the money – At the Futures priceIn the Money – Near the Futures PriceOut of the money – Away from the

Futures pricePremium – The cost / value that is being

traded

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

OptionsAdvantage of Options

• No production risk• Can get in and out with a phone call• No margin calls

Disadvantages:• They can be expensive• Price must move more than premium

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Costs of toolsCALL optionsThe right to buy

Futures Prices are $2.50Buy a option with a $2.50 strike price

If prices go to $2.70 and you have the right to buy at $2.50, is that value?

If prices go to $2.30 and you have the right to buy at $2.50, is that value?

Use for upward price potential

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

CALL- Prices go upFutures Strike Option Price Price Premium Value2.53 2.50 0.13 $650.00

2.73 2.50 0.27 $1350.00

Cash in 0.27 –(.02) =.25 -.13= +$0.12 per bushel

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

CALL- Prices go downFutures Strike Option Price Price Premium Value2.53 2.50 0.13 $650.00

2.30 2.50 0.03 $150 (-$500)Cash in 0.03 –(.02) =.01 -.13= - $0.12 PER BUSHEL

If they expire worthlessCommission $.02 + + .13 = -$0.15 per bushel

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

When to use Call Options

To cover Forward contracts when there is an need for upward price movement

During volatile times in the summer

To extend the marketing year• Sell harvest – Buy a March Call

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Calls…..Strike Fwd Contract & Buy Price Premium Call, Min Local Price 2.70 0.18 2.452.80 0.14 2.492.90 0.12 2.513.00 0.09 2.543.10 0.08 2.553.20 0.06 2.57

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Costs of tools PUT optionsThe right to sell

Futures Prices are $2.50Buy a option with a $2.50 strike price

If prices go to $2.30 and you have the right to sell at $2.50, is that value?

If prices go to $2.70 and you have the right to sell at $2.50, is that value?

Use to set price floor

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

PUT FormulaStrike Price

- Premium

-Commission and Interest

Minimum Effective Selling Price

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

When to use PUT’sTo cover the bushels we cannot forward contractPut options do not have production riskIn our game, we have 19,000 bushels that are unprotected.Consider a PUT when prices are high

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

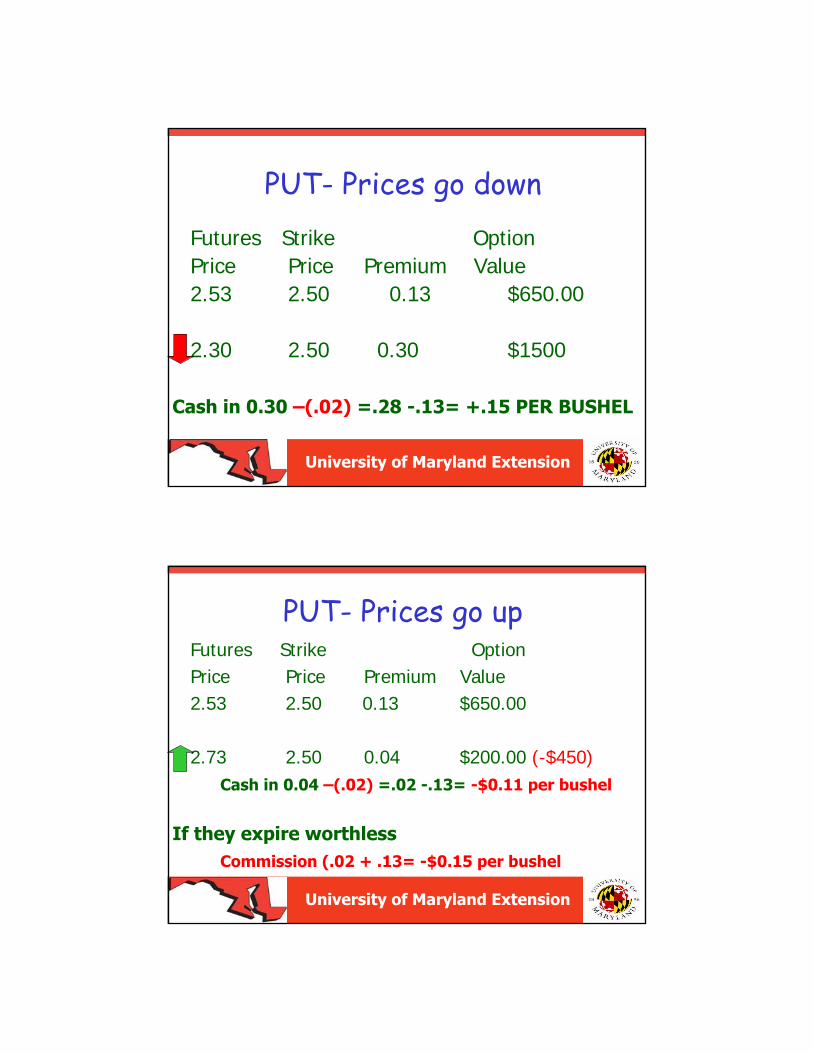

PUT- Prices go downFutures Strike Option Price Price Premium Value2.53 2.50 0.13 $650.00

2.30 2.50 0.30 $1500

Cash in 0.30 –(.02) =.28 -.13= +.15 PER BUSHEL

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

PUT- Prices go upFutures Strike Option Price Price Premium Value2.53 2.50 0.13 $650.00

2.73 2.50 0.04 $200.00 (-$450)Cash in 0.04 –(.02) =.02 -.13= -$0.11 per bushel

If they expire worthlessCommission (.02 + .13= -$0.15 per bushel

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Puts…Strike Buy Put, MinPrice Premium Local Price 2.30 0.02 2.212.40 0.05 2.282.50 0.08 2.352.60 0.13 2.402.70 0.18 2.45

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Minimum-Price ToolsForward contract AND buy a call option• Soybean example: Forward contract price

is $7.80, Nov futures trading at $8.20, a call at $8.20 strike price has a 65 cent premium

• What is the minimum price?

forward contract price – call premium – brokerage fee = minimum price

$7.80 - 0.65 - 0.01 = $7.14

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Quiz Time!To use options profitably, which of the following three aspects of price movement must you forecast correctly?

A. Price directionB. The magnitude of the price moveC. The timing of the price move D. All of the above

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Quiz Time!To use options profitably, which of the following three aspects of price movement must you forecast correctly?

A. Price directionB. The magnitude of the price moveC. The timing of the price move D. All of the above√

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Minimum-Price ToolsBuy a put option• Corn example: Dec futures trading at

$3.90, a put at $3.90 strike price has 40 cent premium

• What is the minimum price?put strike price + expected basis - put premium - brokerage fee = minimum price

$3.90 + (-0.00) - 0.40 - 0.01 = $3.49

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Minimum-Price ToolsSo what is the difference between buying a put option VS. forward contracting and buying a call option?

• They both set a minimum price

• Do you want to fix the basis?

• You have to calculate which method offers the best minimum price at any given time

• See your tax advisor about call option losses

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

University of Maryland Extension

Marketing is Important!The average farm earns 20-30 cents per bushel (including gov’t payments). Just 10 cents more per bushel could increase

net income by 33-50%!

Great marketing is not finding the high price. It’s finding an extra 10-20 cents per

bushel with a solid plan that avoids mistakes.

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

University of Maryland Extension

What is a Marketing Plan?A marketing plan is a proactive strategyto price your grain that considers your financial goals, cash flow needs, price objectives, storage capacity, crop insurance coverage, anticipated production, and appetite for riskProactive, not reactive, not overactive

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

University of Maryland Extension

Why do I need a Marketing Plan?

Fear and greed are powerful emotions -they will affect your decisions. A solid plan is the only effective weapon against these emotions

“Plan your trades, trade your plan”

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Decision Dates

Decision dates are needed to make it a real plan for action

Crop insurance and/or options allow us to forward price with confidence

What’s so special about the March to May period in pre-harvest pricing?

How do they work? If I reach a decision date before my pricing target is met, I will price the grain (if prices are above my minimum pricing threshold).

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Objective: Buy crop insurance to protect my production risk and have 75% of my anticipated corn crop (based on APH yield) priced by early June.

Price 10,000 bushels at $3.00 cash price ($3.00 Dec. futures) using forward contract/futures hedge/futures fixed contract.Price 10,000 bushels at $3.15c/3.15f, or by Mar 7, using a fixed-price contract.Price 10,000 bushels at $3.30c/3.30f, or by Apr 4, using a fixed-price contract.Price 15,000 bushels at $3.45c/3.45f, or by Apr 15, consider options/trend system.Price 10,000 bushels at $3.60c/3.60f, or by May 5, consider options/trend system.Price 10,000 bushels at $3.75c/3.75f, or by June 3, consider options/trend system.

Plan starts on November 1, 2007. Earlier sales will be made at a 30 cent premium to price targets noted above and will be limited to 30,000 bushels.Ignore decision dates and make no sale if prices are lower than $3.00 local cash price/$3.00 December futures.Exit all options positions by mid-September 2008.

Tillman FarmPre-Harvest Corn Marketing Plan

(1) Pricing targets

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Objective: Buy crop insurance to protect my production risk and have 75% of my anticipated corn crop (based on APH yield) priced by early June.

Price 10,000 bushels at $3.00 cash price ($3.00 Dec. futures) using forward contract/futures hedge/futures fixed contract.Price 10,000 bushels at $3.15c/3.15f, or by Mar 7, using a fixed-price contract.Price 10,000 bushels at $3.30c/3.30f, or by Apr 4, using a fixed-price contract.Price 15,000 bushels at $3.45c/3.45f, or by Apr 15, consider options/trend system.Price 10,000 bushels at $3.60c/3.60f, or by May 5, consider options/trend system.Price 10,000 bushels at $3.75c/3.75f, or by June 3, consider options/trend system.

Plan starts on November 1, 2007. Earlier sales will be made at a 30 cent premium to price targets noted above and will be limited to 30,000 bushels.Ignore decision dates and make no sale if prices are lower than $3.00 local cash price/$3.00 December futures.Exit all options positions by mid-September 2008.

Tillman FarmPre-Harvest Corn Marketing Plan

(2) Decision dates

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Objective: Buy crop insurance to protect my production risk and have 75% of my anticipated corn crop (based on APH yield) priced by early June.

Price 10,000 bushels at $3.00 cash price ($3.00 Dec. futures) using forward contract/futures hedge/futures fixed contract.Price 10,000 bushels at $3.15c/3.15f, or by Mar 7, using a fixed-price contract.Price 10,000 bushels at $3.30c/3.30f, or by Apr 4, using a fixed-price contract.Price 15,000 bushels at $3.45c/3.45f, or by Apr 15, consider options/trend system.Price 10,000 bushels at $3.60c/3.60f, or by May 5, consider options/trend system.Price 10,000 bushels at $3.75c/3.75f, or by June 3, consider options/trend system.

Plan starts on November 1, 2007. Earlier sales will be made at a 30 cent premium to price targets noted above and will be limited to 30,000 bushels.Ignore decision dates and make no sale if prices are lower than $3.00 local cash price/$3.00 December futures.Exit all options positions by mid-September 2008.

Tillman FarmPre-Harvest Corn Marketing Plan

Why March-April-May?

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Objective: Buy crop insurance to protect my production risk and have 75% of my anticipated corn crop (based on APH yield) priced by early June.

Price 10,000 bushels at $3.00 cash price ($3.00 Dec. futures) using forward contract/futures hedge/futures fixed contract.Price 10,000 bushels at $3.15c/3.15f, or by Mar 7, using a fixed-price contract.Price 10,000 bushels at $3.30c/3.30f, or by Apr 4, using a fixed-price contract.Price 15,000 bushels at $3.45c/3.45f, or by Apr 15, consider options/trend system.Price 10,000 bushels at $3.60c/3.60f, or by May 5, consider options/trend system.Price 10,000 bushels at $3.75c/3.75f, or by June 3, consider options/trend system.

Plan starts on November 1, 2007. Earlier sales will be made at a 30 cent premium to price targets noted above and will be limited to 30,000 bushels.Ignore decision dates and make no sale if prices are lower than $3.00 local cash price/$3.00 December futures.Exit all options positions by mid-September 2008.

Tillman FarmPre-Harvest Corn Marketing Plan

(3) Pricing tools

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Objective: Buy crop insurance to protect my production risk and have 75% of my anticipated corn crop (based on APH yield) priced by early June.

Price 10,000 bushels at $3.00 cash price ($3.00 Dec. futures) using forward contract/futures hedge/futures fixed contract.Price 10,000 bushels at $3.15c/3.15f, or by Mar 7, using a fixed-price contract.Price 10,000 bushels at $3.30c/3.30f, or by Apr 4, using a fixed-price contract.Price 15,000 bushels at $3.45c/3.45f, or by Apr 15, consider options/trend system.Price 10,000 bushels at $3.60c/3.60f, or by May 5, consider options/trend system.Price 10,000 bushels at $3.75c/3.75f, or by June 3, consider options/trend system.

Plan starts on November 1, 2007. Earlier sales will be made at a 30 cent premium to price targets noted above and will be limited to 30,000 bushels.Ignore decision dates and make no sale if prices are lower than $3.00 local cash price/$3.00 December futures.Exit all options positions by mid-September 2008.

Tillman FarmPre-Harvest Corn Marketing Plan

(1) Pricing targets

(2) Decision dates

(3) Pricing tools

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

References

Chicago Board of TradeWinning the Game, University of

MinnesotaDTN

University of Maryland Extension

Copyright © 2007 Center for Farm Financial Management, University of Minnesota. All rights reserved.

Thank youQuestions

Contact information:[email protected] [email protected] [email protected] 410-778-1661

University of Maryland Extension

![Writing Wills it] Maryland - University of Maryland Extension](https://img.pdfslide.us/doc/110x75/6203998bda24ad121e4b4911/writing-wills-it-maryland-university-of-maryland-extension.jpg)