Embed Size (px)

Citation preview

Running Head: FINANCIAL LITERACY 1

A Study to Examine Financial Literacy among Undergraduate Students at Merrimack College

Kristen N. English

Merrimack College

Dr. Susan Marine

FINANCIAL LITERACY 2

Abstract

Recent studies on nationwide comprehensive financial literacy conclude that many U.S.

adults lack a basic understanding of a variety of different personal finance topics (National

foundation for credit counseling, 2013). Data also suggest that the student loan crisis is

worsening, and increasing numbers students are having trouble with repayment. This study uses

interviews from sixteen college students at Merrimack College to explore the following 1)

college students’ personal financial literacy 2) how they think colleges can foster it, and 3) their

perceptions of a college’s responsibility to do so. Results indicated that, consistent with existing

literature, undergraduate students at Merrimack are not very financially literate. They lacked

significant awareness of the financial aid process and substantive knowledge about their own aid

packages, though they perceived an understanding of these topics as essentially important.

Students also lacked a comprehensive understanding of non-aid personal finance topics, like

credit. Students were surprisingly hesitant to say that colleges should be responsible for

providing personal finance education, and were much more likely to insist that students and their

families are personally responsible for this education. They were slightly more likely to agree

that colleges could do more to help students understand financial aid, and had several ideas about

how colleges could do so. Based on these findings, I recommend an investment in a

comprehensive financial literacy program at Merrimack and suggest ways to promote awareness

of the program, by integrating an introduction into the first-year experience course and creating

targeted awareness campaigns.

FINANCIAL LITERACY 3

Table of Contents

Introduction ________________________________________________________ 4

Literature Review ____________________________________________________ 5

Personal Finance _________________________________________________ 6

Credit and Credit Cards ___________________________________________ 8

Fianncial Aid and Student Loans ___________________________________ 10

Financial Literacy Initiatives ______________________________________ 12

Methods __________________________________________________________ 15

Methodological Paradigm ________________________________________ 15

Data Collection – Method and Participants ___________________________ 16

Implementation and Expected Outcomes ____________________________ 16

Findings and Discussion _____________________________________________ 17

Financial Aid and Student Loans ___________________________________ 17

Credit and Credit Cards __________________________________________ 21

Personal Finance and Financial Literacy Initiatives ____________________ 24

Recommendations __________________________________________________ 30

Conclusion ________________________________________________________ 37

References ________________________________________________________ 39

Appendix A _______________________________________________________ 43

Appendix B _______________________________________________________ 44

Appendix C _______________________________________________________ 45

Appendix D _______________________________________________________ 57

FINANCIAL LITERACY 4

In 2013, conversations surrounding the cost of college and student debt are a daily fact of life. In

just the first ten years of the new millennium, the average total cost of attendance (the sum of

tuition, housing, meals and fees) rose 42% for public institutions and 31% for private institutions

nationally after adjustment for inflation (NCES, 2012), and the average bachelor’s degree

graduate now walks across the commencement stage $26,600 in debt (Denhart, 2013). Student

borrower default rates are rising dramatically as a result, with 41% of borrowers now facing the

negative consequences of delinquency or default within their first five years of repayment

(Cunningham & Kienzl, 2011). Under the stress of strained financial resources, recent graduates

are more than 50% more likely to put off life choices associated with financial independence,

such as buying a home, creating a compounding economic issue (College savings foundation,

2012). Colleges are under more pressure than ever to address these problems, and a few are

starting to rise to the challenge by establishing comprehensive financial literacy programs on

their campuses.

The President’s Advisory Council on financial literacy defines financial education as “the

process by which people improve their understanding of financial products, services and

concepts, so they are empowered to make informed choices, avoid pitfalls, know where to go for

help, and take other actions to improve their present and long-term financial well-being” (Kezar

& Yang, 2010, p. 15). In 2008 JumpStart, a D.C.-based non-profit coalition dedicated to

promoting financial literacy, conducted a comprehensive survey of 1,030 full-time college

students nation-wide. Students were asked a variety of financial literacy focused questions and

answered an average of only 62% of questions correctly (Mandel, 2008). Subsequent research at

individual institutions has consistently produced similar findings, yet 69% of college seniors

FINANCIAL LITERACY 5

have undergraduate student loans to repay, 55% have a credit card and 55% say they are “very

concerned” about building a positive credit history (Capital One, 2011).

In this qualitative interview study, I interviewed sixteen current undergraduate college

students of varying class year, gender identity and academic major at Merrimack College, a

small private liberal arts college in New England. The primary purpose was to learn what these

students understand about their own financial aid and credit histories as well as general personal

finance topics, plus how receptive they might be to different kinds of financial literacy education.

My interview questions focused on three major over-arching categories: Financial aid (including

student loans), credit and credit cards, and general personal finance or financial literacy,

including the extent to which students believe that colleges should be responsible for financial

literacy education.

A qualitative approach to this topic allowed me to examine these students’ levels of

awareness, attitudes and behaviors in-depth in an effort to answer my primary research question:

What do current college students understand about their own financial aid and credit histories as

well as general personal finance topics? My secondary research question was: How do students

feel about the idea of an on-campus financial literacy program at their college, and how receptive

are they to different kinds of financial education content and formats?

Literature Review

In order to gain some insight into the best way to approach my research, it was important

to understand the context by reviewing the existing knowledge base and past research studies on

similar topics. A comprehensive review of existing literature on my three primary subtopics,

personal finance and financial literacy, financial aid and credit was essential to ensuring the

efficacy of my study.

FINANCIAL LITERACY 6

Personal Finance

In the past decade especially, the existing financial literacy and financial education

among a variety of populations has been an increasingly popular research topic, and sadly the

findings are consistently bleak. In 2013, the National Foundation for Credit Counseling

conducted its 7th

annual survey of financial literacy among American adults, attempting to

measure American’s attitudes and behaviors related to personal finance. The study, conducted by

telephone for NFCC by Harris Interactive, surveyed a representative sample of 2,037 adults

nation-wide ages 18 and older (2013).

In this study, it was found that one in four consumers indicated spending more in 2013

than the year before, while 77% admitted to having financial worries. Twenty-six percent of

respondents were worried about their ability to pay off their debts and 57% worry over a lack of

savings. Nineteen percent of adults were worried about their credit scores; though less than two-

thirds of all adults checked their credit reports or scores in the 2013. Finally, consistent with

results from the past 3 years, a full 40% of U.S. adults gave themselves a grade of C, D or F

when asked to grade themselves on their knowledge of personal finance (National foundation for

credit counseling, 2013).

An increased focus has also been placed on specifically assessing the financial literacy of

young adults, including K-12 and college-aged students, in an effort to determine whether early

intervention might be a key strategy for increasing the financial literacy of adults. The first truly

comprehensive study of financial literacy among college students was completed by Chen and

Volpe (1998), who collected survey responses from 924 college students at a variety of higher

education institutions in several states across the country. The survey included 52 questions

covering a broad scope of personal finance topics, and was piloted for refinement before full-

FINANCIAL LITERACY 7

scale administration. Chen and Volpe’s (1998) study was specifically designed to assess the

knowledge of a wider sample of students, not just students from one institution as many previous

studies had examined, as well as to explore demographic variables that may impact student’s

financial literacy levels.

Overall, survey participants answered only 53% of questions correctly, leading the

researchers to conclude that in general college students were not very knowledgeable about

personal finance. Non-business majors, women, students under age 30, underclassmen students

(freshmen and sophomores), and students with little to no work experience were more likely to

have lower levels of knowledge than their counterparts (Chen & Volpe, 1998).

Since the Chen and Volpe (1998) study, other national and comprehensive studies among

college students have returned similar conclusions. The JumpStart Coalition for Personal

Financial Literacy was founded in 1995 with a mission to “evaluate the financial literacy of

young adults: develop, disseminate and encourage the use of standards for grades K-12; and

promote the teaching of personal finance” (Mandel, 2008, p.11). JumpStart has been

administering comprehensive surveys on financial literacy to high school students since the late

1990’s and, for the first time in 2008, added current college students to its population of students

surveyed (Mandel, 2008).

The 2008 JumpStart questionnaire surveyed 1,030 full-time college students nation-wide

and consisted of 56 questions, designed to measure a variety of financial behaviors, including

credit card use, debt accumulation, spending and saving habits and tax preparation. The good

news is that according to the survey, college students are much more financially literate than

high school seniors. The mean score among college students was 61.9% compared with just

48.3% for high school seniors. College student scores also increased with each class year,

FINANCIAL LITERACY 8

college seniors scoring 5.5% better than college freshmen. However, 35.7% of college students

failed the exam completely, and the 61.9% average comes in just over the passing score of a 60%

(Mandel, 2008).

International studies of financial literacy among college students have returned similar

findings. Sharabani (2013) surveyed 574 students at public colleges in Israel in 2010, with

students sampled representing a variety of academic majors and class years, as well as ethnicities

and national origins. Of note is that the average age of students surveyed was 24.6 years old, not

unusual considering that the average age of college-going students in Israel is usually older due

to mandatory military service and a culture that encourages work experience before university.

The survey contained multiple choice questions designed to measure comprehensive financial

literacy by assessing students’ knowledge and awareness on a variety of topics such as savings,

financial planning, compounding interest and investment vehicles.

Overall the average student responded correctly to only 55% of financial literacy specific

survey questions, findings similar to the Chen and Volpe and Jump Start surveys in the U.S. and

likely indicating an overall lack of knowledge and awareness. Male students and Jewish students

(non-Arabs) were generally significantly more likely to be more financially literate. Business and

Economics majors and students with two or more years of work experience were also more

likely to respond correctly more often than students in other academic majors or those with no

work experience.

Credit and Credit Cards

In 2011 Capital One’s Financial Corporation partnered with Braun Research to conduct

403 interviews nationally of graduating college seniors as well as students who had graduated

college between 2008 and 2010. Interviews were conducted by phone using a computer assisted

FINANCIAL LITERACY 9

telephone interviewing system and questions generally focused on saving and spending trends as

well as credit knowledge. Their findings supported the JumpStart findings, further indicating that

student awareness and knowledge did not necessarily correspond with behavior. Fifty-five

percent of the current seniors surveyed had a credit card, whereas 78% of the students who had

graduated 1-3 years before did. Of the students without a credit card only half correctly identified

the definition of “APR”; 74% of card-holders did know this information (Capital One, 2011).

According to a 2006 study students at five different colleges (Norvilitis et al., 2006), the

incidences of credit card possession and credit-card debt among college students may be even

higher than the JumpStart study suggests. Of the 448 students who participated in this study,

74% of them had at least one credit card and 19% had three or more. Four hundred of the 448

students reported credit card debt and of that group the average debt amount was $1,035.

Interestingly, the Capital One survey (2011) results also highlighted student concern over

their financial situations. Despite their lack of knowledge, students are increasingly worried

about their debt. Sixty-nine percent of students surveyed reported that they were graduating with

some student loan debt to be paid back and a full 60% of those are “very worried” or “somewhat

worried” about their ability to pay back those loans. Less than half, 43%, of respondents

indicated that they were putting money in a savings account at least monthly, though males were

more likely than females to save.

Though despite concerns about saving and the likelihood of college students to have at

least one credit card, the data indicate that most American adults, including college-aged

students, know shockingly little about their own credit and are not very likely to regularly check

on their credit report and scores. According to the Consumer Federation of America’s 2013

survey, fewer than half (45%) of respondents from a survey of a national sample of more than

FINANCIAL LITERACY 10

1,000 adults knew their credit score and more than one-third of respondents (37%) reported

never having pulled a credit report even once in their life. Only one-quarter (25%) of respondents

have pulled a credit report within the last year.

Financial Aid and Student Loans

Unfortunately, the data indicate that students have a very good reason to be as worried as

they are. In 2011 the Institute for Higher Education Policy produced a deeply concerning report

on student loan borrowing and delinquency trends. The report analyzes and aggregates data from

the five largest student loan guaranty agencies in an effort to understand the repayment behaviors

of student-loan borrowers. Researchers examined the experiences of more than 8.7 million

borrowers with a sum $27.5 million in loans. The populations of borrowers were those who

entered into repayment between the fall of 2004 and the fall of 2009, though special attention

was paid to a cohort of 1.8 million borrowers whose loans went into repayment in 2005

(Cunningham & Kienzl, 2011).

Thirty-seven percent of borrowers in the 2005 cohort were able to make consistent on-

time payments without postponing any repayment or becoming delinquent. Twenty-three percent

applied for a variety of repayment options allowing them to postpone payments without

becoming delinquent, such as deferment or forbearance. Another 26% of the 2005 cohort of

borrowers became delinquent on their loans at some point, even though postponement or other

repayment alternatives were available to them, and a full 15% not only became delinquent but

also defaulted at some point during the first five years of repayment. Students who left college

without graduating were far more likely to have difficulty repaying their loans than those who

graduated, and students who attended two-year colleges or four-year for-profit institutions were

also less likely to successfully make timely payments than students who attended four-year non-

FINANCIAL LITERACY 11

profit institutions. In total, 41% of borrowers faced the negative consequences of delinquency or

default within their first five years of repayment (Cunningham & Kienzl, 2011).

As a direct result of the difficulty of repaying student loans, research has suggested that

recent college graduates are more likely than ever to delay traditional adult life choices, many of

which, like homeownership, significantly impact local and national economies. In 2012 the

College Savings Foundation surveyed over 600 college graduates between the ages of 20 and 35,

about half of whom had graduated in the past seven years and the other half who graduated more

than seven years before. The results were striking; overall the recent college graduates were 50%

more likely to put off life choices usually associated with financial independence and adulthood.

Thirty-six percent of respondents graduating within the last year said they had to live

with their parents longer than expected, compared with 24% who graduated more than seven

years ago. Forty percent of recent grads indicated they would definitely delay buying a house,

versus 22 percent of graduates seven or more years out. More than double the number of recent

graduates than older graduates said they also planned to delay getting married (College savings

foundation, 2011).

The amalgamation of these concerning statistics has the federal government, as well as

state and local governments, deeply and understandably worried. In 2003, the federal

government established the Financial Literacy and Education Commission (FLEC) under the

Fair and Accurate Credit Transactions Act. The commission is focused on creating a national

strategy for financial education, and beginning in 2012, early financial literacy initiatives,

namely K-12 and post-secondary education initiatives, became a research priority for the

commission.

FINANCIAL LITERACY 12

According to the recently released 2013-2014 update, “preparing youth to have a basic

understanding of financial transactions and to make informed decisions about paying for post-

secondary education are key priorities for FLEC” (p. 2). In support of these priorities, FLEC has

organized three committees, one of which focuses on post-secondary education. A fourth

research and evaluation committee will develop a consistent set of metrics used to evaluate the

effectiveness of financial education programs (Financial literacy and education commission,

2013).

These concerning findings do not end just with an increased focus on financial education

research. The federal government is laying out plans that will place enormous pressure squarely

on the shoulders of colleges, holding them responsible for the financial and educational success

of their students. Just this past August, President Obama outlined an aggressive plan to combat

dramatically rising tuition prices in a national address (Lewin, 2013). The proposed legislation

he identified would rate colleges according to a variety of factors including tuition, graduation

rates and debt and earnings of graduates, endeavoring to combat dramatically increasing tuition

prices and to keep college accessible and affordable for as many students as possible. Under the

plan, the federal financial aid eligibility of colleges would be tied to the rankings, meaning

schools with lower graduation rates or higher average debt numbers could be at significant risk

of losing valuable and often essential federal aid dollars.

Financial Literacy Initiatives

In response to President Obama’s recent remarks as well as the multitude of concerning

statistics regarding student loan borrower default rates and the ways in which loan debt are

affecting the post-graduation behavior of students, many colleges have started to reevaluate the

level of financial education they should be providing students. In an attempt to aid colleges by

FINANCIAL LITERACY 13

providing an easy path to establishing a financial education program, American Student

Assistance (ASA), a fifty-year-old non-profit based in Boston, Massachusetts launched the

SALT program in 2012. ASA’s public purpose mission is to empower students and alumni to

successfully manage and repay their college loan debt. ASA (2013) currently provides services

to more than 1.5 million borrowers and manages a portfolio with approximately $40 billion in

student loans. Ninety-four percent of all loans in ASA’s portfolio are in good standing.

The SALT program partners with colleges to provide comprehensive financial education,

debt management tips and ongoing resources to current students, to help them better understand

their personal financial situation and all available options. Just one year later, SALT is partnering

with more than 200 schools nation-wide.

ASA is hoping its SALT program will make it easier for college presidents and

administrators who recognize the importance of providing financial education for their students

to implement financial literacy programs without having to invest a significant amount of time,

money or valuable and increasingly scarce resources. Many colleges struggle with launching

programs because it can be difficult to determine which office or administrator on campus really

owns the responsibility of making sure students graduate financially literate. To implement truly

effective and comprehensive programs, multiple offices across institutions must work together,

which is challenging to say the least and, at some colleges, may feel nearly impossible.

Champlain College in Vermont has been an early adopter of the idea of holistic financial

education and boasts a nationally-recognized Center for Financial Literacy on campus (though

the school actually prefers the term “financial sophistication” which it views as having a more

positive connotation) (Champlain college website, 2013). While the center is responsible for

research beyond just the financial literacy of current college students, it also offers programming

FINANCIAL LITERACY 14

to current Champlain students in the context of Champlain’s LEAD program, a four-year

comprehensive life skills education program. Students participate all four years in in-person

seminars and online activities designed to help them understand topics like budgeting, credit,

employee benefits, student loan repayment, and even buying a car. Champlain conducted focus

groups, interviews and other on-campus research before the launch of the program after Student

Life administrators expressed concern that students wouldn’t want something like this

(Champlain college website, 2013). On the contrary, students on the whole were extremely

receptive to having a financial education program, suggesting they are aware of what they don’t

know and interested in a structured and even compulsory way of accessing this information.

In the early 2000’s Texas Tech University launched a similarly comprehensive program

called “Red to Black” which serves to “to help students by advocating responsible financial

behaviors through financial coaching and transfer of skills” (Texas Tech website, 2014). Red to

Black in an outreach of Texas Tech’s Personal Financial Planning program and provides students

with access to one-on-one counseling, seminars, workshops, online resources and even walk-in

hours where students can connect with financial planners. All services are free of charge for

students, and the program has even recently begun to provide services for some community

members as well, in response to requests from the community. The Red to Black program has

been extremely well received by all institutional constituents, and Texas Tech hopes their

program can serve as a model for other colleges nationally who are looking to establish similar

programs.

While Champlain and Texas Tech’s programs and programs like them are arguably still

young enough that it can be difficult to track long-term outcomes, institutional leaders across the

country are starting to take note of these best-practices models. The New York Times “Your

FINANCIAL LITERACY 15

Money” columnist Ron Lieber (2011) visited Champlain’s campus and published an article on

the financial sophistication and LEAD programs in 2011. The article was the number one most e-

mailed article the day it was published on thenewyorktimes.com and has been re-printed

repeatedly in other news sources. Additionally, according the Director of the Red to Black

program, at least twenty-six other colleges have reached out since the program’s inception to

learn more about how it functions and how they got started (Supiano, 2008).

Based on my review of the existing literature, it’s clear that college students, and

Americas in general, could certainly benefit from an increased focus on improving financial

literacy. The fact that people report stress and concern regarding their finances suggests they

may be receptive to resources designed to help them do more, and colleges who are beginning to

address these gaps have benefited from overwhelming positive feedback. Based on the findings

from my literature, I designed my study to measure how these findings compare with findings

from Merrimack, and to explore potential action-items for the college.

Methods

Methodological Paradigm

For my capstone project, I researched the financial literacy levels among undergraduate

college students at Merrimack College, a small private college in New England, in an effort to

assess where these students fall on the spectrum of knowledge and awareness. The pragmatic

methodological paradigm likely best describes my worldview in approaching this type of

research (Mackenzie & Knipe, 2006). Given unlimited time and resources, I would have likely

employ mixed methods to best address my research question, supplementing my qualitative

interviews with a quantitative survey that actually measured what students understand about

these topics, in addition to assessing through interviews how they perceive their own knowledge

FINANCIAL LITERACY 16

and awareness. Though I can understand the validity in other paradigms, the pragmatic approach

places primary focus on designing studies based on what I consider the ultimate goal: addressing

the research question and gathering data that may ultimately help inform best practices.

Data Collection – Method and Participants

My qualitative research consisted of a series of 16 interviews with current Merrimack

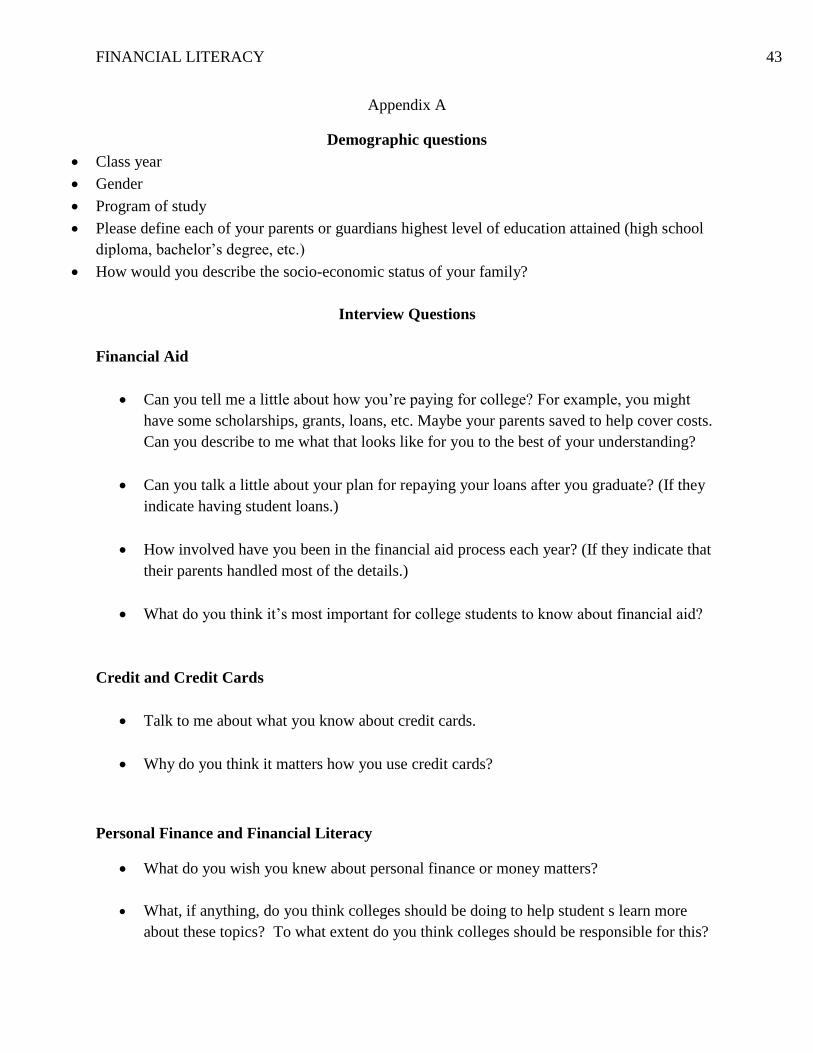

undergraduate students. The interview protocol (see Appendix A) was designed to assess

existing financial literacy levels among these students, in terms of knowledge and awareness of

personal finance topics including financial aid, credit, credit cards, and loan borrowing, among

other topics. The protocol also asked students to talk about their thoughts on financial literacy

programs, and the purposes and mission of colleges. All students who participated in the

interviews did so voluntarily and each interview lasted approximately 20-25 minutes. Interviews

were recorded, and each recording was erased once the interviews were transcribed. I assigned

each interview subject an alias for the purposes of presenting my findings here, so all of the

students’ identities will remain anonymous.

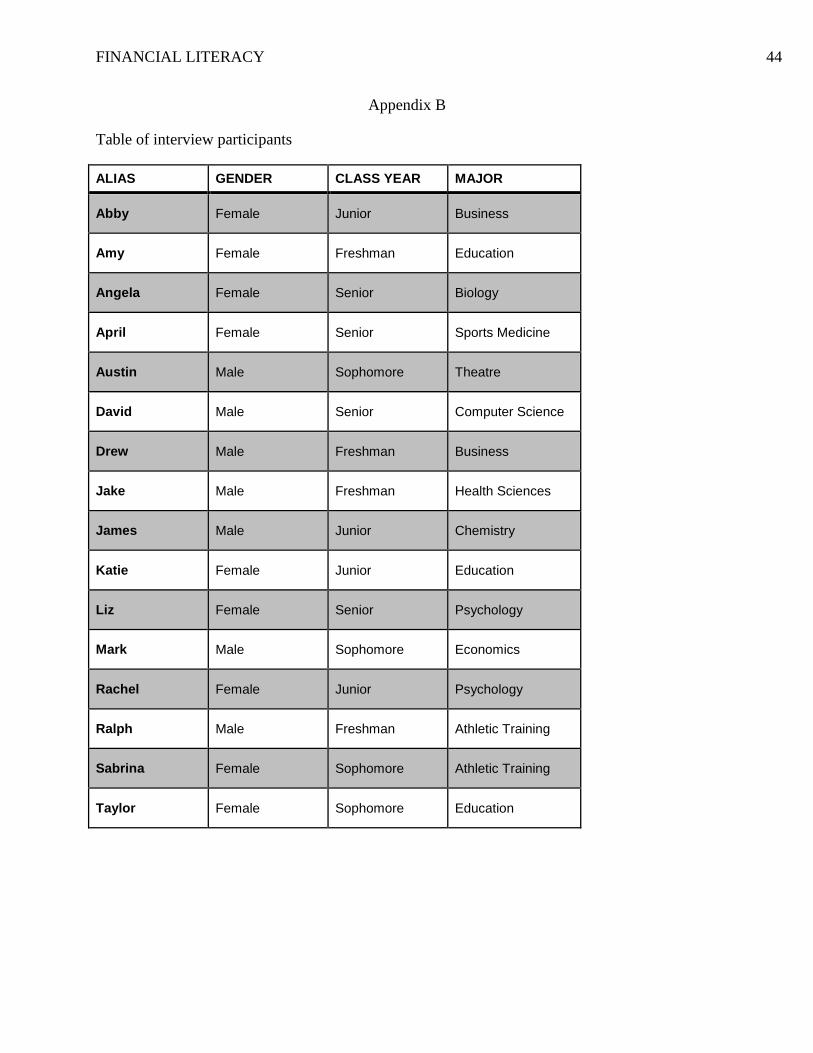

The sample of students interviewed represents the overall demographics of Merrimack’s

total undergraduate student population in terms of major, class year, and gender identity (see

Appendix B for a table of aliases and demographic characteristics). Because I work in the

Admissions Office on campus, I had access to about 40 current students who work in our office

as student ambassadors. I primarily recruited students from that group who expressed an interest

in participating, as well as asked them to promote the opportunity for participation to their

friends and residents (for those who are Resident Advisors). Every participant signed a consent

form after we discussed the logistics and the goals of my research. Although personal finance

FINANCIAL LITERACY 17

and financial aid may be considered somewhat sensitive topics, my questions were designed as

not to ask students to disclose detailed personal information.

Implementation and Expected Outcomes

I used my findings to inform a one-time financial literacy and financial aid workshop I

conducted on April 24, 2014 in partnership with the O’Brien Center for Student Success’s

Generation Merrimack program. Generation Merrimack is a program targeted at first-generation

Merrimack students and aims to support this population and their unique needs through all four

years of their undergraduate experience. The program includes a mentorship component, and my

workshop will be targeted at the G1 upperclassmen mentors for this academic year.

Beyond my limited involvement with this initiative this year, I have hopes that my

research will provide evidence in support of a recommendation to the college to invest in a long-

term comprehensive financial literacy program for students. I know from conversations with the

Director of Financial Aid that the college has explored such an investment and has met with

different organizations that provide such programs, but has yet to commit to anything. My

primary goal for this project is that my findings may encourage an affirmative decision to partner

with an outside organization which can provide financial literacy services to Merrimack students,

such as SALT, an organization mentioned in my literature review and one that I know the

college has had discussions with.

Findings and Discussion

Financial Aid and Student Loans

When asked to describe how they’re paying for college, most students were able to

describe in general terms how they are financing their college education. Every student

interviewed received some kind of gift aid from the institution, usually in the form of a

scholarship, though a few mentioned institutional grants. Some also mentioned federal or state

FINANCIAL LITERACY 18

grants. Many students indicated that loans were helping to cover part or much of their expenses,

the percentage of the total sample was slightly higher but close to the 60% of all college students

nationally who borrow loans to help cover their tuition expenses (American Student Assistance,

2013). Interestingly, many of those who had loans were unsure of whether they had loans in their

name or if their parents had borrowed on their behalf. A few students had no loans and

unsurprisingly these students seemed to understand little regarding the details of student loan

borrowing. One student interviewed is attending Merrimack on a full athletic scholarship which

covers tuition as well as all living expenses.

Although most could describe how they are paying for school generally, almost all of the

students who had taken on loans seemed to be only vaguely aware of the details of any and all

loans they or their parents had borrowed. A few mentioned specific terms or borrowers, such as

“subsidized,” “unsubsidized,” and “MEFA” (the Massachusetts Educational Financing

Authority), but almost none of the participants could identify the total amount of loans they

thought they had borrowed to date.

When asked to discuss a plan for loan repayment after graduation, many students

interviewed reported having somewhat of an idea of what their plan might be, but their responses

were extremely nebulous. Their plans vaguely involved eventually securing a job and then

making payments towards their loans, but very few students had a concrete idea of how much

they owed, how much their payments might be, or a specific timeline for when they hoped to

have them paid off. A few admitted to not having much of a plan at all. James shared the

following:

I’ve thought about it, don’t really have a plan per se...I have kind of a deal with my

parents where we’ve been paying off the interest on them while I’m in school, to try and

make it a little bit easier when I get out. So I work during the summer and then I kind

FINANCIAL LITERACY 19

of…pay them back some of the school years ones. Just to try to cut it down for when I get

out but. Don’t really know quite the post-school plan yet…

We know from the literature that the amount of loans students borrow is increasing each

year (Denhart, 2013), and that students are more likely than ever to struggle with repayment

(Cunningham &Kienzl, 2011). Students’ lack of awareness regarding how much they’re

borrowing as they borrow, coupled with dramatically rising costs of college tuition (NCES,

2012), could certainly be contributing to an overall increase in the average student debt. Higher

debt loads added to the fact that many students seems to have no more than a vague idea about

their plans for repayment may also help to explain the rise in delinquency and default.

Additionally, the research clearly indicated that despite the fact that there are a variety of

repayment options available, such an income-based repayment, designed to adjust payments to

help improve the borrower’s ability to avoid delinquency, high numbers of students are either

unaware of these options or neglecting to pursue them (Cunningham & Kienzl, 2011).

Some students did mention that they or their parents, or both, were making small

payments on some of their loans while they were in school. A few students also mentioned

intentions of going straight into graduate school after graduation, and their plans were to

continue to defer their loans during graduate school. For these students, the plans for repayment

seemed to be even more unformulated. These students seemed less concerned about making

plans now since they perceived repayment dates to be in the distant future.

In general, when discussing financial aid and especially loans and repayment, several

students alluded to feelings of stress and anxiety. Some referred to their own fears while others

described their perception of “panic” among their peers. For example, below is an exchange

between me and Katie. After she asserted that she felt she had a pretty good understanding of her

financial aid, I asked her if she knew how much she had borrowed to date:

FINANCIAL LITERACY 20

Katie: No. Absolutely not. I feel like I would pass out if I see that! I feel like I would pass

out.

Researcher: So it sounds like you have some stress and anxiety related to loans?

Katie: Oh yeah, I feel like everyone does.

This finding was consistent with the literature, which presented that a full 60% of students

graduating with some student loan debt are “worried” or “very worried” about their ability to pay

it back (Capital One, 2011).

One finding that became clear to me quickly as I started interviewing was that many

students seemed to be involved in the financial aid process only as secondary participants, and

that often a parent or parents had really taken control of managing the process and working out

the details. I added a question about students’ perception of their level of involvement in the

financial aid process because I wanted to explore the relationship between how much they knew

and how much they perceived their parent’s knew, and their motivations to actively participate or

not.

Some of the students reported that they had taken the lead on managing their own

financial aid, though interestingly these students weren’t necessarily any more likely to be able

to explain their financial aid packages in detail. Many students said they were somewhat

involved, but that their parents managed most of the process and some seemed to have little to no

involvement at all. A few students even indicated that their parents seemed to be intentionally

shielding them from the process, primarily to alleviate any potential emotional stress and to

encourage them to focus on their studies. For example, Taylor explained:

I think from the beginning my parents didn’t want me involved in it. I know whenever I do

ask my parents they’re kind of unsure of it too, so they don’t want to try to…they don’t

want to stress me out by like telling me. They just keep saying ‘just get good grades! get

good grades! That’s all we’re asking you to do!’

FINANCIAL LITERACY 21

In addition to what these students knew about their own financial aid, I wanted to

understand what they thought it was most important for students in general to know about

financial aid. Many of the students said the number one thing they think college students should

know is more information regarding student loans, including the loan process, interest, and

specifically how much they will owe when they graduate. Some students cited their own

experiences and lack of knowledge here, while others asserted that they were more

knowledgeable than their friends. Most students who mentioned loans agreed that in general

college students don’t have much awareness, which they perceived can easily lead to over-

borrowing. Angela’s reaction below is a good summary of these responses.

I think it’s important for them to really know what they’re getting into. I feel like

it’s easy to be like ‘oh I’ll just borrow this or take a loan out’, but I don’t

think…like maybe what payments are going to be like, how large they might be

and stuff, because you don’t think…when you’re signing for loans you don’t think

about paying them off. So I feel like putting it into reality, like after you graduate

every month you could be paying this.

Some students indicated that in addition to details regarding student loans, it was most

important for college students to understand the details of every piece of their financial aid

package, including the different types of aid, where money for each type comes from, how they

qualified for each type and how much is gift aid versus how much must be paid back. A few

students also mentioned other things they thought were important for students to know. Other

responses included how to get more money, and that money shouldn’t restrict your decision to

attend college because college is an investment in your future.

Credit and Credit Cards

When asked to talk about what they knew about credit cards, many students could

describe generally what a credit card is and how it works, though some students’ knowledge was

much more comprehensive than others. Most students articulated that credit cards allow you to

FINANCIAL LITERACY 22

“buy now and pay later”. A few students had very limited knowledge and often seemed to

confuse credit cards and debit cards in their responses. Only a few students indicated that they

had a personal credit card, which is much lower than the 55 percent of graduating seniors who

reported having a credit card in the Capital One survey from the literature (Capital One, 2011).

However, a separate study of college students and credit cards usage (Nellie Mae, 2005) found

that the Northeast region of the United States had the lowest percentage of college students who

possessed a credit card, compared with the Midwest, the South, the West, and national averages.

I would also posit that students at small, private schools with higher tuition costs may be less

likely to have credit cards, strictly due to the likelihood that their families have somewhat higher

socioeconomic statuses considering their ability to access a higher cost institution.

Some students seemed to have an overall negative perception of credit cards, primarily

citing the temptation to overspend. This finding wasn’t completing surprising to me considering

the recent economic recession and the fact that these students would have been old enough

during the recession to understand its potential implications for their family. One study that

examined how business students’ attitudes towards credit cards changed as a result of the recent

recession found that students are more judicious with their credit card spending now than they

were prior to 2008, largely because of their awareness that it’s easy to overspend (Kohut, et al.,

2011). One student interviewed described the “hook” by which credit card companies convince

to you sign up, by offering a much lower introductory interest rate and then hiking the rate after a

few months. Others were concerned, like those in the Kohut study (2011) about their own ability

to control their spending. For example, Mark elaborates:

It just seems to me that credit cards are more so a hurt to personal finance, especially

among young people, than they are a help. Because I feel like a lot of time people,

especially…myself included, I mean if I had a credit card I’d be spending so much

money! I’d never be able to pay it back, I mean within a reasonable amount of time. I’d

FINANCIAL LITERACY 23

be getting hit with fees and penalties and all this stuff. So I just think for young people it’s

not a great thing to have…because we can’t control ourselves (laughter).

With the credit card conversation as with financial aid, parental influence seemed to be a

common theme among many responses. Several students who indicated that they did not have a

credit card mentioned that it was based on the advice or a directive from their parents. Others

indicated they probably should get a credit card during or soon after college, despite the potential

temptation to overspend, because they needed one to help build credit. This idea also seemed to

frequently stem from parental advice. A few students mentioned direct mail solicitations, and

receiving "pre-approved” credit cards offers in the mail sometimes or frequently.

When asked to explain why it matters how we use credit cards, almost every student said

that it was very important to pay off the money you charge on a credit card, and many again

mentioned the ease with which you can get into significant debt and the importance of not

“spending money you don’t have”. While in general they all seemed to understand that it was a

“bad thing” if you didn’t pay your credit card bill or if you racked up excessive debt, some were

able to clearly articulate why while others were not. Eventually several of them used the term

“credit” as they attempted to explain why the way you use credit cards matters. When students

mentioned credit, I asked them to elaborate on their perception of the relationship between credit

cards and credit, and what credit measures. Of those who proactively mentioned the relationship

between credit cards and personal credit, only a few were able to comprehensively articulate the

connection. If students did not bring it up on their own by the end of the credit card questions on

my protocol, I asked them to talk about what they knew about credit or credit scores.

Interestingly, among those who were able to clearly and comprehensively explain credit,

students’ confidence in their own responses varied. Some students were very certain of their own

knowledge, while others seemed to doubt that what they knew was correct. Those who had a

FINANCIAL LITERACY 24

vague understanding at best were mostly aware of their own lack of awareness. They all seemed

to understand that it was important to have good credit, but they were only somewhat sure why.

For example, Rachel discusses her own perceptions:

As far as credit scores, I don’t…I mean obviously I know you want to have a good one,

you don’t want to have a bad score on anything. I want to say it’s out of 800, but I could

be totally off on that. Honestly my perception of a credit score is looking at the 3 men on

the commercial that have the signs… I know that I’ve had family members in that

situation where unfortunately bad credit scores have kind of come back to bite them in

the bum… But yeah, once again, I’m just not too knowledgeable.

Another student also mentioned recalling commercials that discussed credit and credit

scores, and a few others recalled specific experiences of family members or news stories

highlighting the potential consequences of bad credit. The students’ lack of knowledge regarding

credit and especially their own personal credit histories was again consistent with the literature,

where we learned that fewer than half adults in one survey knew their credit score and more than

one-third of them reported never having pulled a credit report even once in their life (ACFA,

2013).

Personal Finance and Financial Literacy Initiatives

Before delving into a discussion about potential financial literacy initiatives at colleges, I

asked students to tell me what they most wished they knew more about in terms of personal

finance. About half of the students harkened back to financial aid, and said they wished they

understood more about the types of aid, where each type comes from, and especially how the

student loan process works. Several students also mentioned they wish they knew exactly how

much they will owe in student loans when they graduate, and what their monthly payments may

look like. Other responses varied and covered both financial aid and personal finance topics. A

few students mentioned they wished they knew more about taxes, including where they money

goes and how to file. One student mentioned investments. Others generally referred to what one

FINANCIAL LITERACY 25

student called “Personal Finance 101,” elaborating to mean they wish they knew more about

pretty much everything, including credit cards, credit and money management. For example,

David, whose existing knowledge was actually much more significant than many of his peers,

was interested in knowing a lot more:

I mean everything. Everything, right, you can never know too much. Everything from

taxes to 401Ks to how to invest money to should you be building up this credit, should

you be using debit, should you be doing this, should you be doing that.

For the final section of my protocol, I was especially interested in understanding what

these students though colleges could be doing to help them learn more about these topics,

including both financial aid and other non-financial-aid-specific personal finance topics.

Students had a wide variety of ideas about this. Only two students interviewed felt that it wasn’t

very important for them to know much about these topics at this point, especially since their

parents can still help. Some students mentioned initiatives they knew were already in place at

Merrimack, including Financial Aid workshops during Accepted Students Days for prospective

incoming first year students and additional workshops during fall orientation for new first-year

students. Some students mentioned that we could offer workshops regularly, targeted at current

students or possibly current seniors, though they were divided on whether or not they thought

students would be interested in attending.

A few students thought Merrimack could be doing a better job of helping students

understand their financial aid packages, by offering one-on-one meetings with a financial aid

counselor after aid letters are mailed, or by including additional information with the letters that

explained the different types of aid. These responses were highly interesting to me, since

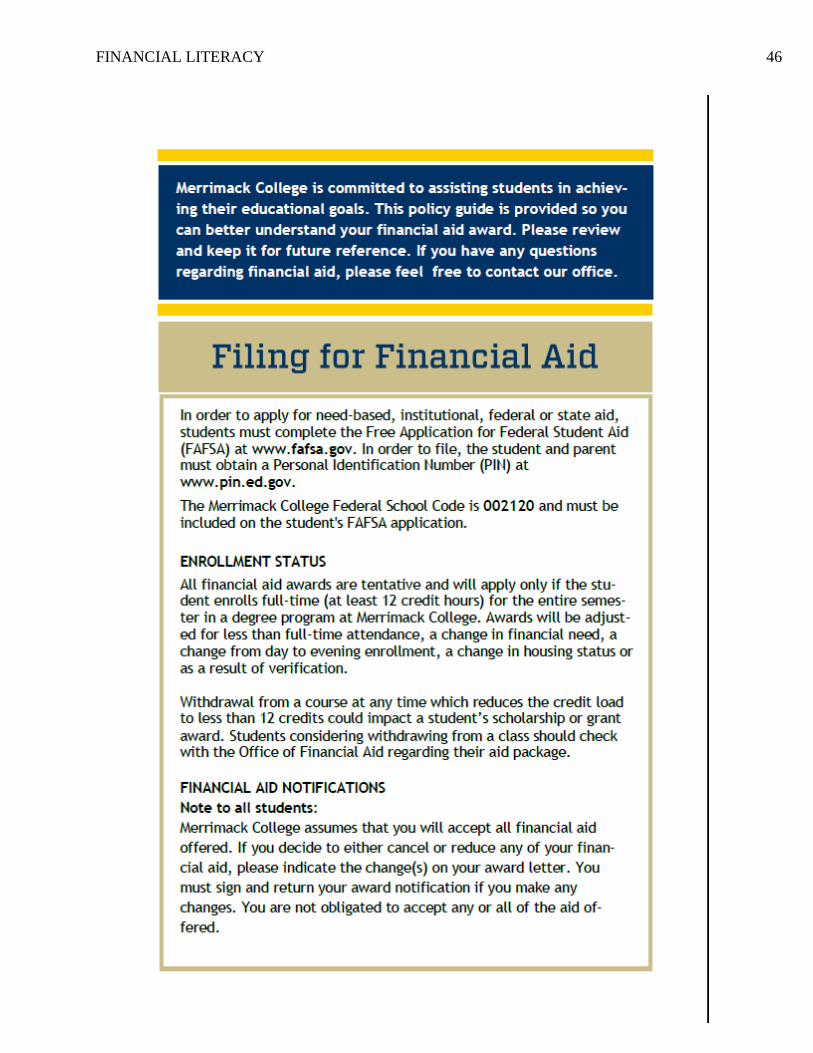

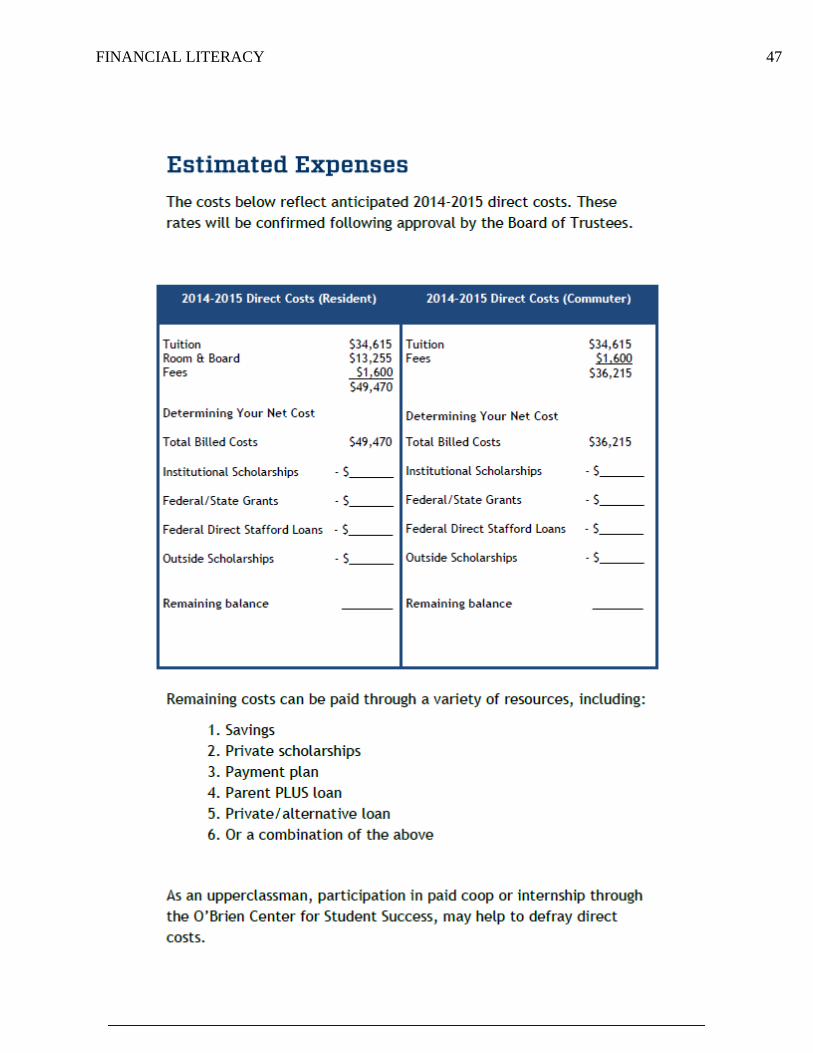

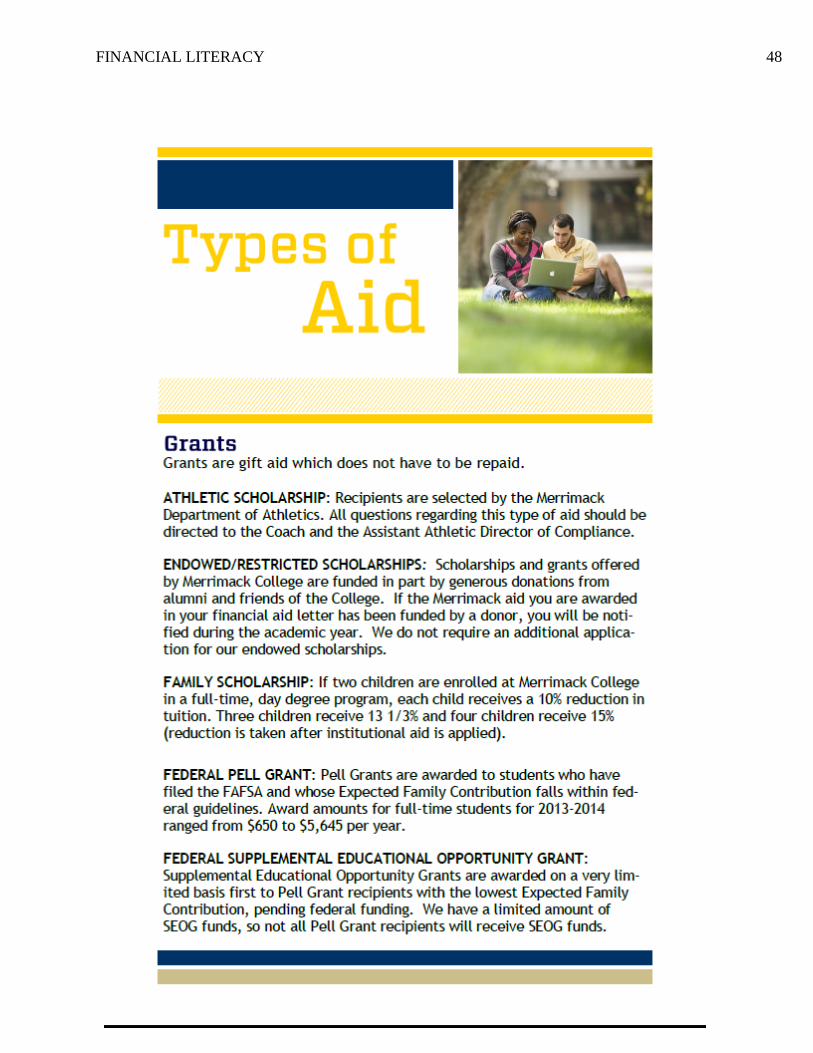

Merrimack already does both of these things. All financial aid award letters for prospective first

year students are mailed home with a financial aid brochure (see Appendix C) which describes

FINANCIAL LITERACY 26

each type of aid students may see on their award letter and also includes additional information

such as direct and indirect costs, payment options, alternative financing options, and next steps

for student loans. Returning students access their aid packages online, but again details regarding

each type of aid they may see are easy accessible directly from the page where they view their

awards.

The fact that students are asking for information already provided clearly indicates there

is a gap between what’s being communicated and what information is being received and

processed. Interestingly, past research supports that this finding is not anomalous. Perna (2006)

articulated a disconnect between the prolific availability of information regarding college costs

and financial aid and the lack of awareness and understanding among students and parents, and

especially among low-income students and parents. At Merrimack this seems to ring true on a

micro level for the students interviewed. Due to the limitations of this study, parents were not

included in interviews, but assessing parents’ understanding of their students’ aid and financial

aid in general would be an interesting future research topic.

In addition to mentioning one-on-one meetings vaguely, some students said they wished

the college had some kind of office on campus where students could go to learn more about their

financial aid or personal finance topics; a few mentioned the College’s Career Development

Office for comparison—an office they perceived as having a specific mission and purpose and

which serves both current students and alumni. These responses were also very interesting to me

since it seemed that some students were largely unaware of the services provided by the Office

of Financial Aid which, though arguably more limited than the Career Development Office, do

include one-on-one counseling. Without mentioning the Office of Financial aid, I asked this

small group of interviewees if they thought there was anywhere on campus now where they

FINANCIAL LITERACY 27

might go if they had questions about financial aid or personal finance issues. Most of them

eventually mentioned the Office of Financial Aid, but often hesitantly. They seemed collectively

unsure of what services this office could or would provide, and expressed perceptions of an

atmosphere that is less than welcoming, primarily due to past observations of office staff

members as extremely busy. For example, Taylor described her experiences visiting the

Financial Aid Office:

Well the only office I can think of is the financial aid office but…from like the vibe that

I’ve gotten when I’ve been in there it’s like…everyone’s so busy, you know, everyone’s

like rushing around and doors are opening, doors are closing, there’s lines, and people

calling in. That, to me, isn’t somewhere where I would go and sit down and say hey can

you help explain this to me, or oh could you talk to me about this...maybe they do have

that sort of, that type of resource there. But I don’t know.

When discussing their ideas about types of financial literacy programming, students were

divided on how interested they thought their peers might be in college-provided financial

education initiatives. Some thought their peers would definitely access these opportunities if they

existed; others worried that students might be apathetic, or unwilling to attend due to busy

schedules or a perception of a lack of immediate importance. A few students mentioned that

finding ways to make programming fun or engaging might encourage better participation. For

example, Sabrina shared the following:

Yeah meetings or like maybe something educational but like in a fun way, which sounds

so bad but… Like here for example, when I came to Accepted Student’s Day when I was a

senior in high school there was a Financial Aid session and yeah I sat through it but was

I really excited like ‘let’s go to Financial Aid!’? No I wasn’t. But looking back now I

think it’s so important to be educated on it. So I mean…I guess the only way to do it is to

make it fun.

According to my research of financial literacy initiatives at other colleges, students at Champlain

College expressed significant interest in financial education services when surveyed by the

college, suggesting that some students are not totally apathetic. I would hypothesize that students

FINANCIAL LITERACY 28

might express more interest in financial education if they could be made aware of the substantial

benefits, and if the financial literacy programming formats were easily accessible and user-

friendly.

After talking with students about what types of things colleges could be doing to help

them learn more about personal finance topics, I asked them to what extent they felt that colleges

should be held responsible for this type of education. Interestingly, most students were very

hesitant to say that educating students about personal finance is part of a college’s job. Many

seemed uncomfortable with this idea, and insisted that understanding personal finance is first and

foremost a personal responsibility, and something that should start at the family level. However,

many did agree that providing financial education services could mutually benefit both students

and colleges, so it’s certainly something colleges should be considering, even if it’s not

technically something for which they’re responsible. Drew explains:

Colleges technically aren’t responsible. But…it just makes the college look better…the

people themselves are responsible for knowing that kind of stuff, but I feel like colleges

should care about the people they put through their system…a college is for preparing

you for life…and personal finance is a part of that, but technically they aren’t

responsible. But…personally I think they should feel like they should be…Colleges

should care about their students and the students should care about the college.

Drew highlights one motivator colleges might consider that also came up in the Supiano (2008)

article from the literature. At a time when colleges are under increased public scrutiny and

receiving significant criticism for dramatically rising costs, offering financial education could go

a long way towards generating much needed good will. Though some students were wary about

whether personal finance education is part of a college’s job, many students were somewhat

more comfortable with the idea that helping educate students about their financial aid should be a

college’s responsibility, since financial aid is directly related to their participation in higher

education. Katie elaborated:

FINANCIAL LITERACY 29

I do think so because you’re making the check to the college. Like, at the end of the day

you’re giving the money to Merrimack…We’re paying, so we should get these

opportunities like that to show where everything goes and how to do it all and

everything… I think if it’s related to Merrimack, hold the workshops, but if it’s something

other than that then that’s something you could do like your own individual research on.

A few students disagreed with the majority and felt strongly that colleges should be held

responsible for helping their students learn about financial aid as well as other personal finance

topics. These students believed that the overall purpose of college is to prepare students for the

“real world”, and that financial literacy is a part of that. They also believed that this was

especially true for colleges like Merrimack that tout a liberal arts education, the goal of which is

to produce “well-rounded” students. David explained his reasoning as follows:

David: Obviously [colleges] are required more or less to teach you whatever you want to

major in, to prepare you for that field, but all these electives or requirements that you

have to take, that don’t have anything to do with the field…what is the purpose of these

requirements? I think a college’s answer would be to prepare you for the real world. So

with that, how has that prepared you for the real world?...that’s how I would assess how

well a college is doing.

Researcher: Do you think the college’s responsibility extends beyond financial aid to

other personal finance topics?

David: Without a doubt. Because as soon as you start getting those paychecks from your

first job, you need to know what to do with them—how to pay taxes on them, where to put

the money, how to not blow all the money, how to save it, how to prepare for a mortgage,

how to prepare for car loans. Everything.

Of the dissenters one other, like David, was a senior, and the third, Mark, while only a

sophomore, has a brother who is a senior with whom he’s very close. I was surprised by the fact

that most of the group hesitated to hold colleges responsible for financial education, but I would

posit that if you interviewed these students again five years after college, they may feel

differently. Perhaps many of them don’t realize how much they don’t know at this point, but

once their loans go into repayment or they begin to face day-to-day decision making related to

FINANCIAL LITERACY 30

personal finance, they will more fully understand all they need to know and may wish their

college had done more.

Mark, the sophomore student with a brother who is a senior, was not the only student to

bring up the influence of older siblings. Interestingly, a fair number of students mentioned older

siblings in responses to a variety of questions, spanning all research topics. This finding was

supported by a closer look into literature surrounding family dynamics. While childrens’

behaviors, specifically economic behaviors, are most strongly influenced by their parents, they

are also impacted by siblings (Cotte & Wood, 2004).

In summary, my findings revealed that, consistent with previous studies among college

students, students at Merrimack are not very financially literate. They lack an overall

understanding of the financial aid process and often even their own aid packages, and while they

have a surface-level familiarity with some personal finance topics, they are lacking in

comprehensive knowledge of most topics and complex concepts like credit. They do value

financial literacy; they think it’s important for college students to have knowledge and

understanding of these topics, and they are often mindful of their own lack of awareness. While

some students were hesitant to place the full burden of responsibility on colleges to help them

learn more about financial topics, they did all agree that it would be mutually beneficial for both

the colleges and students if institutions were to provide access to opportunities to learn more

about personal finance and financial aid topics.

Recommendations

Based on the findings of my research and their integration with the literature, I have made the

following recommendations:

1.) Merrimack College should commit to an investment in a financial literacy program, such as the

SALT program mentioned in the literature, which would allow all current students and alumni

FINANCIAL LITERACY 31

access to on-going and comprehensive resources designed to help them better understand and

navigate financial aid and personal finance.

Due to my position as an employee in the Office of Admissions at Merrimack, I am

aware that Merrimack College administration has explored the idea of investing in the SALT

program, and is strongly considering an investment for the 2014-2015 academic and fiscal year,

though no contract has officially been signed as of this paper’s submission. The cost of this

program according to the most recent quote is only about $6,000 per year, a more than

reasonable investment considering the return we should expect. Financial literacy levels among

the population of students I interviewed were generally low, and many students expressed an

interest in financial education. I also strongly believe these services would be perceived as

extremely valuable by alumni, as well as by parents of prospective, current and former students.

Run by American Student Assistance, the SALT program mentioned in the literature is a

web-based non-profit service that exists to provide students access to a network of resources

designed to help educate them about financial aid and personal finance. When colleges partner

with SALT the colleges pay an annual fee to allow their students to register with SALT online

for free, where they can access content like articles, videos, infographics, self-paced courses on a

variety of topics and additional resources for questions about debt management, repayment

options, and even accessing internships. Students with SALT accounts also have access to free

live one-on-one counseling, and the program includes tools to help students set up and monitor a

repayment plan for their loans—an especially valuable resources for alumni, who also have

access to SALT when their institution establishes a partnership (saltmoney.org, 2014).

Investing in a partnership with an organization like SALT would allow Merrimack to

offer all the benefits of a comprehensive program without having to dedicate extremely

significant additional time and resources (including human resources) internally. Considering the

FINANCIAL LITERACY 32

size of Merrimack’s student population and the existing Financial Aid staff, this option likely

makes the most sense in terms of return on investment. Alternatively, if the college was

interested in a capacity-building approach they could consider the launch of an in-house

program, led by a new administrative staff member or possibly a graduate fellowship student

dedicated exclusively to directorship of the program, similar to the Red to Black program at

Texas Tech University. Even if the college does not add an additional professional staff member

to oversee the program on campus, it is important that ownership of the operations of the

program be clear. If, as is likely at Merrimack, the program will be housed in the Office of

Financial Aid, a staff member, or perhaps a graduate fellow, should be designated as responsible

for ensuring the programs viability and success.

A program like the SALT program at Merrimack must be regularly monitored and

evaluated to ensure that it serves its purposes and that students are accessing the resources

available to them. I would recommend an assessment at the end of the first academic year of the

program primarily designed to measure students’ levels of awareness of the program and the

resources it provides. This might make a great future capstone project for a Higher Education

graduate student. Long-term, Merrimack should also seek to measure the impact of this program

by evaluating patterns among data points like the number of students accessing SALT resources,

average loan debt of those students upon graduation, and delinquency and default rates. It would

also be interesting eventually to measure alumni giving patterns to determine if any correlation

can be made between those who donate, especially as young alumni, and those who accessed

significant SALT resources. Convincing young alumni to give is challenging, I suspect largely

because so many young alumni are focused on loan repayment, which they may identify as

already creating revenue for their alma maters. It would be interesting in the future to determine

FINANCIAL LITERACY 33

if young alumni who had consistent access to SALT resources may be more likely to give, given

that they may feel slightly more confident in the management of their personal finances.

2.) Merrimack should integrate an introduction to its Financial Literacy program into the First Year

Experience course all first-year students will take beginning in the 2014-2015 academic year.

The mission of the First Year Experience (FYE) course is to help new Merrimack

students transition to college life successfully, and to “encourage self-exploration, active

engagement and understanding of the world” (Merrimack website, 2014). FYE classes meet once

a week for most of the fall semester during students’ first year, and beginning with the 2014-

2015 academic year participation will be compulsory for all first-year students. These classes

would be a great forum for introducing new Merrimack students to the college’s financial

literacy program. We already know from a breadth of research that first-year seminars positively

impact retention for all students (Schnell, 2003). We also know that students’ financial issues can

often negatively impact retention (Wohlgemuth et. al., 2007). Financial issues can sometimes be

combatted when students know how or where to access additional resources, and who they can

talk to about their aid. I believe that integrating an introduction to Merrimack’s financial literacy

program into FYE could help students access this knowledge.

Based on feedback from the 2013-2014 pilot of the FYE program, the office of the

Associate Dean of Campus Life and Dean of First Year Students has produced a sample draft of

the syllabus for next year’s FYE (see Appendix D). This syllabus outlines three major categories

of learning goals, the second of which is to “create a positive Merrimack College campus

experience.” One learning outcome under this goal is that as a result of FYE students will be able

to “identify appropriate campus resources and opportunities that contribute to their educational

experience, goals, and campus engagement.” An introduction to a comprehensive financial

FINANCIAL LITERACY 34

literacy program is directly in line with this objective. It could easily be integrated into the

existing class meeting during week 2 that has already been identified as a time to go over the

variety of campus resources available to students.

3.) Merrimack should design and implement parallel internal and external campaigns designed to

promote awareness of the SALT (or other) Financial Literacy program to current students,

parents, faculty, administrators, community members and alumni.

Having a financial literacy program in place is not sufficient; Merrimack should promote

the regular use of the program by students and other users to ensure the program’s impact. I

suggest establishing two parallel promotional campaigns designed primarily to establish

ubiquitous awareness of the program. The first campaign should be an internal campaign

targeted at current students, faculty and staff; the second campaign should target external

constituents, including primarily alumni, parents, and prospective students, and secondarily other

community members. The major goal of these campaigns, to establish (or increase, for future

iterations) awareness of Merrimack’s Financial Literacy Program among the target population,

should be operationalized so that progress may be measured. For example, Merrimack may set

goals that 75% of all current students can recognize the program by name by the end of the first

academic year, and 50% of students can list at least two services offered through the program by

the same deadline. Progress toward both of these goals could be measured easily through a

survey. Campaign tactics will vary by target population, but some financial and human resources

should be allocated.

Who would be responsible for creating and implementing these campaigns could be up

for discussion on campus. It’s difficult for me to make a recommendation without a

comprehensive understanding of the resources available in different offices, especially human

and financial resources, but the campus-wide Marketing or P.R. team likely makes the most

FINANCIAL LITERACY 35

sense. Alternatively, this would be a great campaign for student input, especially considering that

current undergraduate students are the primary target audience. A group of upperclassmen

Marketing or Communication majors, or a group of undergraduate or graduate students may be

able to do much of the legwork on a project like this, either in the context of a class or an

internship or fellowship.

4.) Merrimack should find ways to promote the services and resources available through the

Financial Aid Office on campus, and to establish an atmosphere that students perceive as more

welcoming so they are more likely to access services and resources.

In my opinion, one of the most interesting findings from my research was learning how

students perceived the Financial Aid office on campus; they were hesitant to seek guidance from

Financial Aid staff for a variety of reasons, largely stemming from a lack of awareness of what

services are provided by the office. I recommend addressing these perceptions, and suggest a few

ways that Merrimack may do so. One thing we could consider is moving toward a Student

Financial Services model structurally, which integrates two or more offices on campus

completely, most commonly Financial Aid and the Bursar’s Office. According to a 2007

NACUBO survey (the National Association of College and University Business Officers), many

colleges across the country have already started to shift towards integrated models, and more

than half of respondents in their survey said they were mostly or highly satisfied with the results

(NACUBO, 2007). It’s considered industry best practice to put student service first in financial

dealings especially (Kurz, Scannell & Vedeer, 2007), by minimizing the number of times a

phone call or in-person inquiry must be transferred and by cross-training staff to be prepared to

answer a variety of questions. Though Kurz et. al. (2007) proposes a Student Financial Services

model versus an Enrollment Management structural model (which Merrimack has already

adopted) in my opinion these two models need not necessarily be mutually exclusive.

FINANCIAL LITERACY 36

Fortunately, our Financial Aid, Bursar and Registrar’s Offices are already physically close in

location. Revisiting a Student Financial Services or “One Stop Shop” model (which Merrimack

originally explored in 2010-2011), could benefit students significantly.

Massachusetts College of Pharmacy and Health Sciences University (MCPHS) has

adopted a Student Financial Services model, designed to give students and families one point of

contact for all aid and billing questions during their full three-to-six year tenure at the school

(mcpsh.edu, 2014). Though not officially integrated into Student Financial Services, the

Admissions Office at MCPHS is also heavily integrated into this model, and admission

counselors serve as primarily points of contact for all prospective students for all questions

including those related to financial aid, which I believe can work very well at a small school

where it’s likely that prospective students have formed a relationship with their counselor by the

time they get to their first aid season. MCPHS also employs an Associate Director for

Affordability and Financial Aid housed in the Admissions Office, which is very unique

structurally. The goal of this position is to ensure that those on the admissions team are

adequately prepared to work with families on financial aid until the point of matriculation for

their students. Although all Merrimack students technically have an assigned financial aid

counselor, it’s clear that most students don’t know that. Integrating Financial Aid and Student

Accounts and then actively promoting to students who their contact is may strongly positively

influence students’ likelihood to reach out with questions, since they would know who

specifically to call.

Prior to, or in the absence of, a restructure, Merrimack could also help promote the

services offered through the Financial Aid Office by integrating this promotion into the larger

awareness campaigns recommended previously. Especially for the internal campaign targeted at

FINANCIAL LITERACY 37

students, marketing and communication pieces could refer students back to the Financial Aid

Office and attempt to slightly re-brand the office as more open and welcoming. Perhaps the

office could consider implementing a regular schedule of “walk-in hours”, as the career

development office on campus does, or establish a system that makes it easy for students to

schedule one-on-one appointments, perhaps even through an online calendar that would

automate scheduling.

Conclusion

We know from the literature that American adults in general are not very financially

literate, and that this is especially true for college students. The literature supports the findings

from my study, which make clear that at least some students at Merrimack are largely

uninformed about personal finance and especially financial aid. Those who have borrowed are

unsure of how much, and very few have a concrete plan for repayment or any awareness of

repayment options. Fortunately, they seem receptive to the idea that colleges may be able to help

them learn more about these topics, and though they were somewhat wary about this education

being presented in the form of required classes or workshops, I believe they will likely be

extremely receptive to a largely web-based format like the SALT program.

There were some limitations to my study, which are important to recognize. All of the 16

students interviewed were white, and while Merrimack’s racial and ethnic diversity is limited, it

would be important in a larger-scale study to make sure the voices of students of color are

included. I would also be interested to explore the experiences and opinions of international

undergraduate students at Merrimack, as well as graduate students at Merrimack, as they relate to

financial literacy and their thoughts on financial literacy programs. Both of these populations are

FINANCIAL LITERACY 38

growing rapidly and these student groups will soon represent significant percentages of the

overall Merrimack student population.

In terms of recommendations for future research, I think interviewing alumni could be

extremely valuable, as I would guess that alumni, especially those currently in repayment on

their loans, might be much more likely to agree that Merrimack should be providing students

more and better financial education. Interviewing parents of prospective and current students as