Embed Size (px)

Citation preview

Government Mortgage to Buy Scheme – An argument to support

the idea

Emmanuel Sithole, Thomas Field, Jonathan Fearis, Arundeep Gill, Nasima

Ahmed

Learning Objectives

•What is and why the scheme?

•How does it work

•Supporting Facts

•What are the benefits of the scheme?

What is the Mortgage to Buy Scheme?

• It operates in the same manor as a normal mortgage, with the exception that the government provide an option to guarantee a partial purchase on the mortgage.

• This allows lenders to offer more ‘high-loan-to-value’ mortgages.

• The total valuation for the scheme till year 2020 is £9.7 billion which will cover 194,000 new home buyers and is administrated by Homes and Communities Agency.

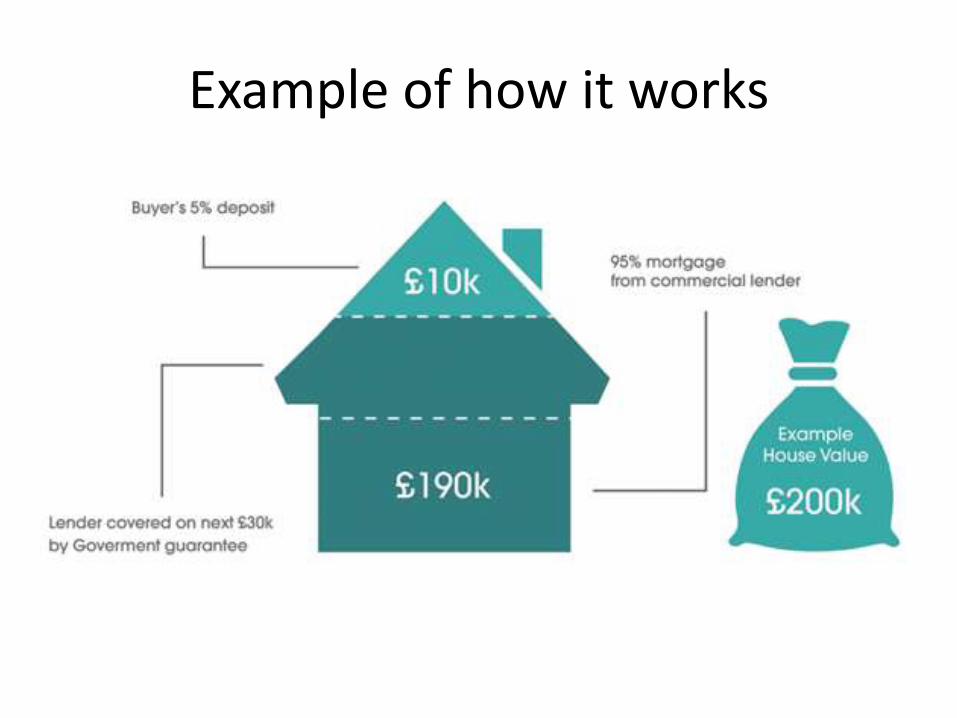

Example of how it works

Supporting Facts

• Small deposit is required under this scheme with manageable level of 5 percent and borrowing at interest free for the first five years.

• Gives the chance of breather to settle down with lower interest rate

• Individuals get competitive loan after completion of five years with increase of 1 percent in sixth year

• The scheme is tax free and the individuals do not require paying income tax.

What type of properties can you buy? • The ’Help to Buy’ scheme allows people to

purchase a home up to £600,000.

• A deposit as little as 5% has to be made for the house.

• There are three types of the ’Help to Buy’ scheme, which are;

• Help to Buy: Equity loan

• Help to Buy: Mortgage guarantee

• Help to Buy: ISA

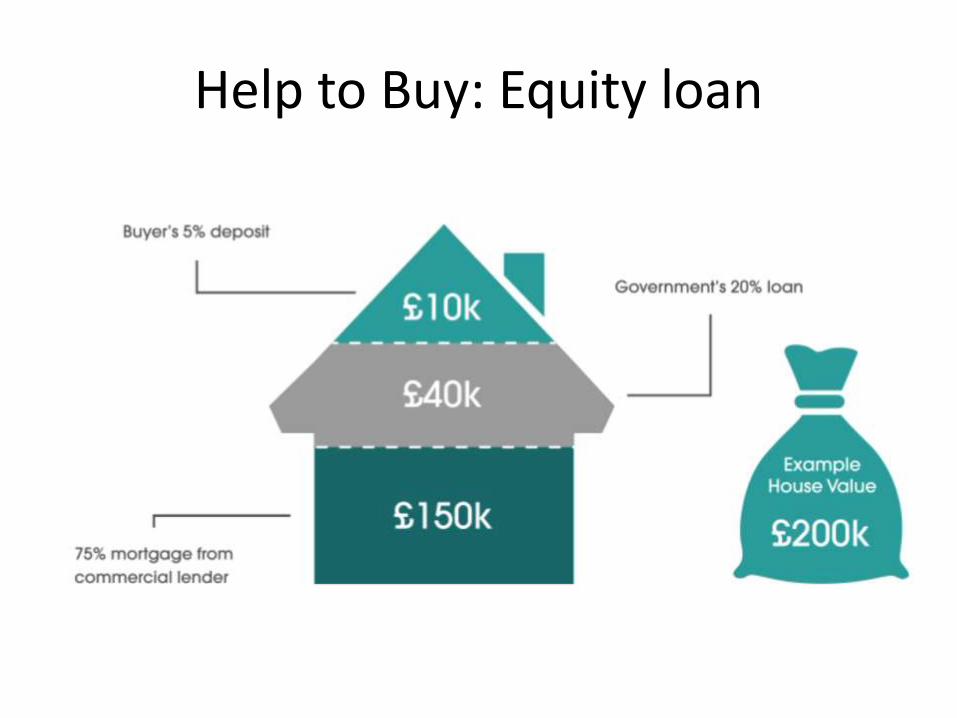

Help to Buy: Equity loan

Help to Buy: Equity loan

• Usually for a new build home

• The buyers receive 20% of the value of the new home from the Government

• This requires the buyer to have 5% for the deposit.

• They will also need a 75% mortgage

• The Government has specifically helped buyers in London boroughs.

Help to Buy: Mortgage Guarantee

• The buyers require 5% of the house value for the deposit.

• A 95% mortgage loan repayment is the buyer’s responsibility.

• The lenders are offered to buy a guarantee on mortgage loans.

• Buyers are offered ‘high-loan-to-value’ mortgages because of the Government support.

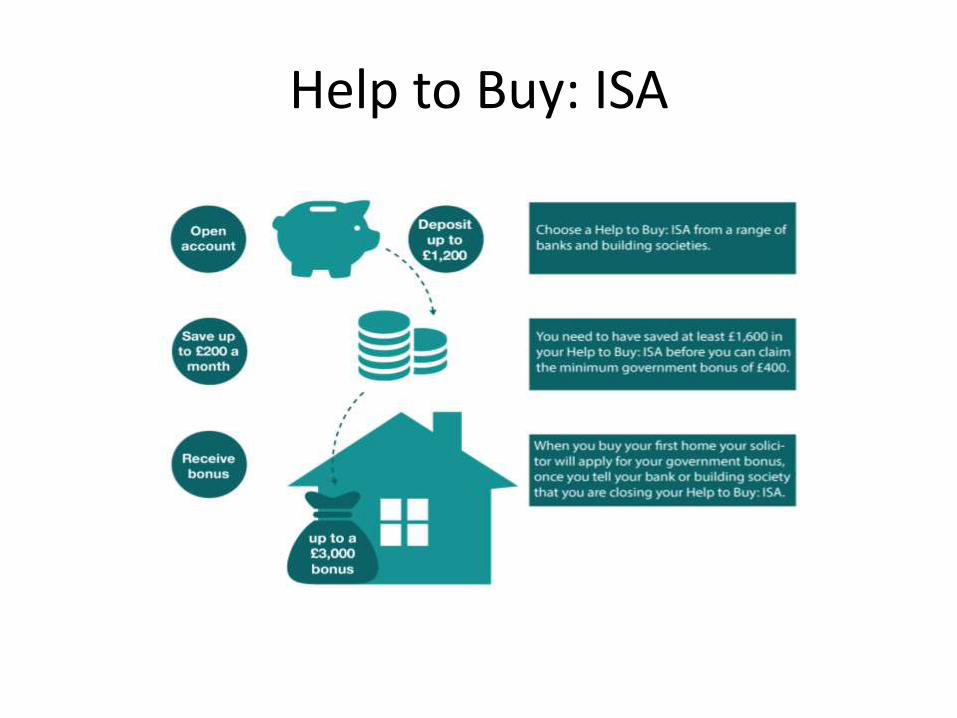

Help to Buy: ISA

Help to Buy: ISA

• The Government is offering 25% more savings if the buyers save into a Help to Buy: Individual Savings Account.

• A numerous amount of banks and building societies offer the scheme.

• The minimum Government bonus is £400

• The maximum Government bonus is £3,000

• A solicitor of conveyancer is to apply to the Government for the loan on the buyers behalf.

What are the benefits of the scheme?

• Improving access to mortgage finance and affordable to individuals specially with reference to first time buyers which helps in stimulating housing demand in the market

• Creation of demand domestically for housing sector with the provision of Government offering lenders the option of purchasing guarantee on mortgage loans with borrower deposit between 5-20 percent

• The scheme can be utilized for mortgage on new build, existing houses, initial buyers, movers and remortgaging individuals with mandatory setup criteria guarantying lenders for compensating from portion of net losses

Conclusion

• The initiative has helped in increasing the role of local demand authorities through new housing supply initiative

• At end of the year 2015, 55000 properties has been bought under this scheme

• Evaluation that in the first 22 months since the introduction of this scheme it has helped 42000 households for home ownership with the target at end of fiscal year 2016 at 74000.

• The scheme is mainly demand led with fewer restrictions as compared with previous scheme of first Buy with entrance to first buyers and related categories and no income limit with nil equity contribution of developers.

• We evaluate the argument in support of the Government through first discussing the arguments in support and against the Government initiative, presentation of facts and statistics in favour of this initiative and more importantly bringing out main details from the “Evaluation of the Help to Buy Equity Loan Scheme” survey in 2016.

References

• GOV.UK. 2015. 2010 to 2015 government policy: homebuying. [ONLINE] Available at: https://www.gov.uk/government/publications/2010-to-2015-government-policy-homebuying/2010-to-2015-government-policy-homebuying. [Accessed 04 March 16]. – What is a mortgage to buy scheme

• Help to Buy. 2015. How does it work?. [ONLINE] Available at: https://www.helptobuy.gov.uk/equity-loan/equity-loans/. [Accessed 06 March 16]. – Equity loans

• Help to Buy. 2015. How does it work?. [ONLINE] Available at: https://www.helptobuy.gov.uk/mortgage-guarantee/how-does-it-work/. [Accessed 06 March 16]. – Mortgage Guarantee

• Help to Buy. 2015. How does it work?. [ONLINE] Available at: https://www.helptobuy.gov.uk/help-to-buy-isa/how-does-it-work/. [Accessed 06 March 16]. – ISA

• Simon Gompertz. 2015. Help to Buy 'propping up housing market'. [ONLINE] Available at :http://www.bbc.co.uk/news/business-35051348. [Accessed 07 March 16]. – Benefits of Help to Buy

• Stephen Finlay, Ipsos MORI, in partnership with Peter Williams, Christine Whitehead and the London School of Economics. 2016. Evaluation of the Help to Buy Equity Loan Scheme. [Online] Available at: https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/499701/Evaluation_of_Help_to_Buy_Equity_Loan_FINAL.pdf. [Accessed 09 March 16]. – Conclusion