Embed Size (px)

Citation preview

GOOD GOVERNANCE, PARLIAMENTARY OVERSIGHT + FINANCIAL ACCOUNTABILITY

Budget Management and Financial Accountability

Rick Stapenhurst, World Bank Institute

OVERVIEW OF PRESENTATION

Good Governance + Legislatures

Core Functions + Types of Legislatures,

The Budget Cycle + The Legislature (Ex-Ante)

The Budget Cycle + The Legislature (Ex-Post)

Conclusions

20

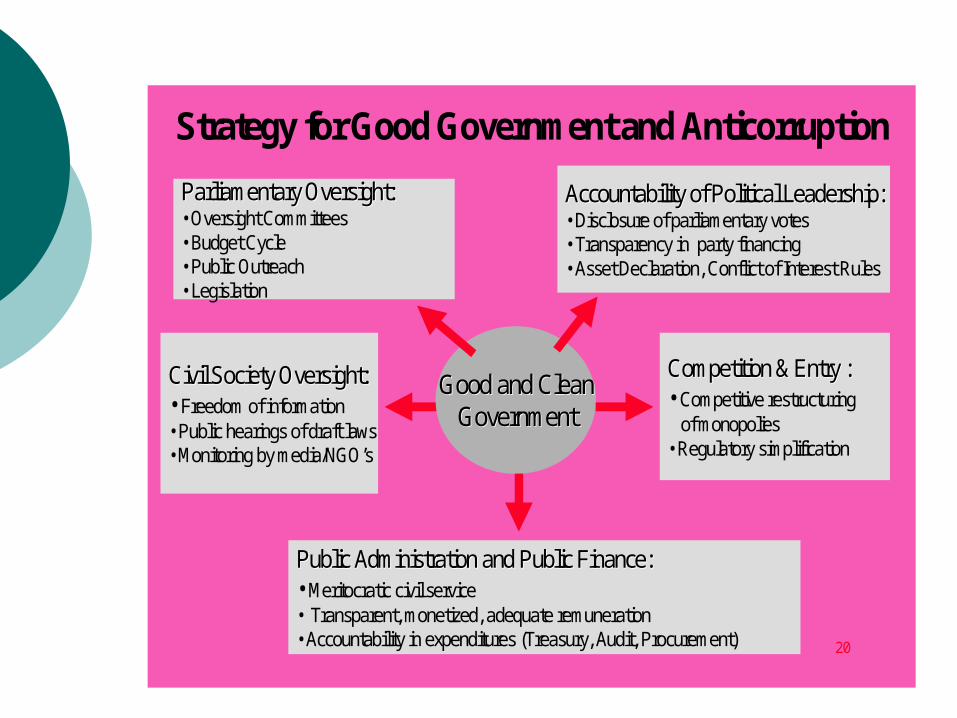

Civil Society Oversight:Civil Society Oversight:• Freedom of information• Public hearings of draft laws • Monitoring by media/NGO’s

Good and CleanGood and CleanGovernmentGovernment

Competition & Entry :Competition & Entry :• Competitive restructuring

of monopolies• Regulatory simplification

Public Administration and Public Finance: Public Administration and Public Finance: • Meritocratic civil service • Transparent, monetized, adequate remuneration • Accountability in expenditures (Treasury, Audit, Procurement)

Strategy for Good Government and Anticorruption

Accountability of Political Leadership:Accountability of Political Leadership:• Disclosure of parliamentary votes • Transparency in party financing• Asset Declaration, Conflict of Interest Rules

Parliamentary Oversight:Parliamentary Oversight:• Oversight Committees• Budget Cycle• Public Outreach• Legislation

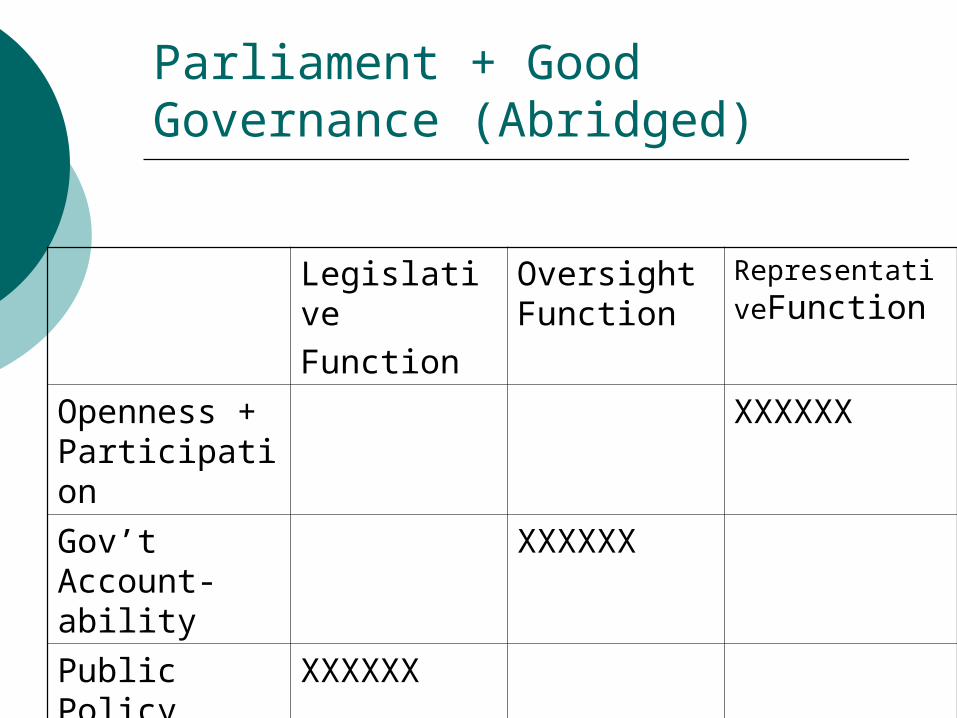

Reminder : Core Functions of Legislatures

The Legislative Function Passing Laws Participation in Public Policy Making

The Oversight Function Holding Governments to Account

• The Representative Function Representing Constituents

Parliament + Good Governance (Abridged)

LegislativeFunction

Oversight Function

RepresentativeFunction

Openness + Participation

XXXXXX

Gov’t Account-ability

XXXXXX

Public Policy Dev’t

XXXXXX

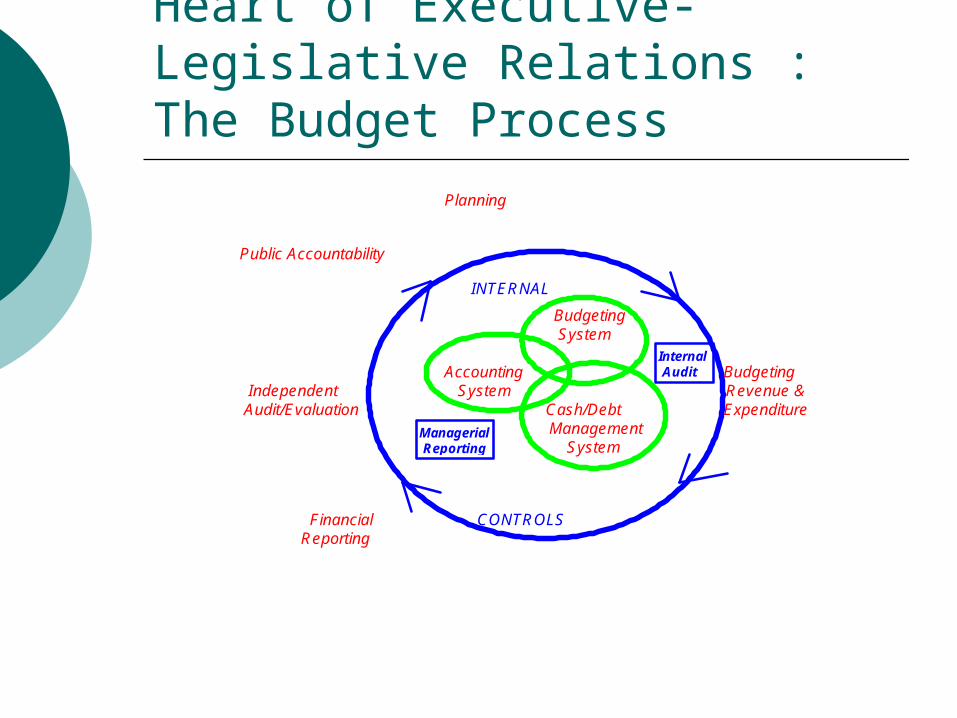

Heart of Executive-Legislative Relations : The Budget Process

Planning

Public Accountability

INTERNAL

Budgeting System

Accounting Budgeting Independent System Revenue & Audit/Evaluation Cash/Debt Expenditure

Management System

Financial CONTROLS Reporting

Managerial Reporting

Internal Audit

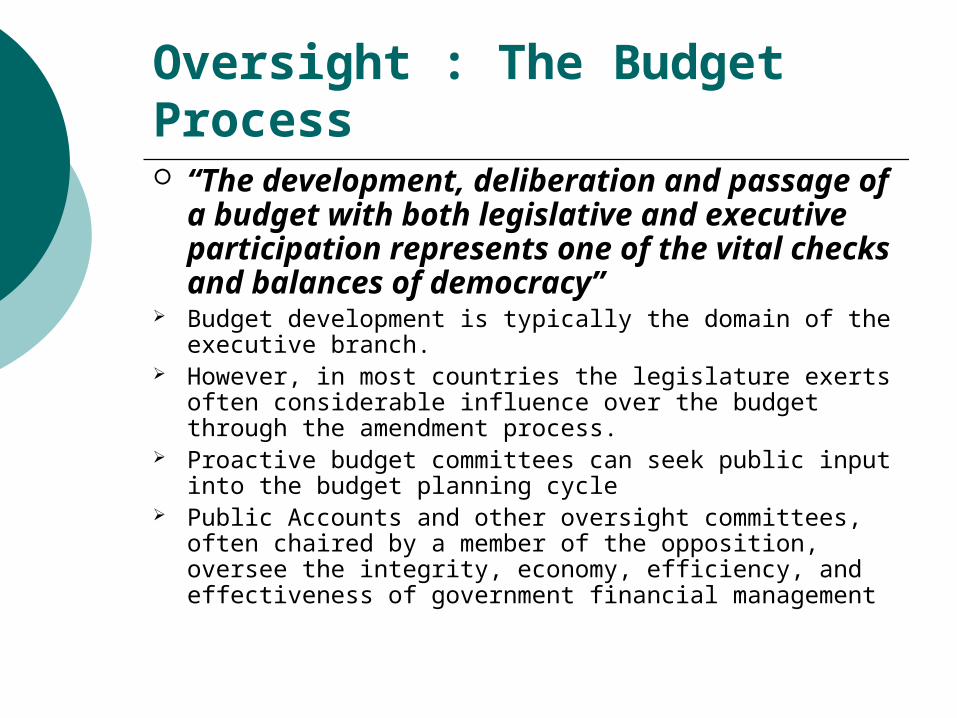

Oversight : The Budget Process “The development, deliberation and

passage of a budget with both legislative and executive participation represents one of the vital checks and balances of democracy”

Budget development is typically the domain of the executive branch.

However, in most countries the legislature exerts often considerable influence over the budget through the amendment process.

Proactive budget committees can seek public input into the budget planning cycle

Public Accounts and other oversight committees, often chaired by a member of the opposition, oversee the integrity, economy, efficiency, and effectiveness of government financial management

Oversight : The Budget Process

“The development, deliberation and passage of a budget with both legislative and executive participation represents one of the vital checks and balances of democracy”

Budget development is typically the domain of the executive branch.

However, in most countries the legislature exerts often considerable influence over the budget through the amendment process.

Proactive budget committees can seek public input into the budget planning cycle

Public Accounts and other oversight committees, often chaired by a member of the opposition, oversee the integrity, economy, efficiency, and effectiveness of government financial management

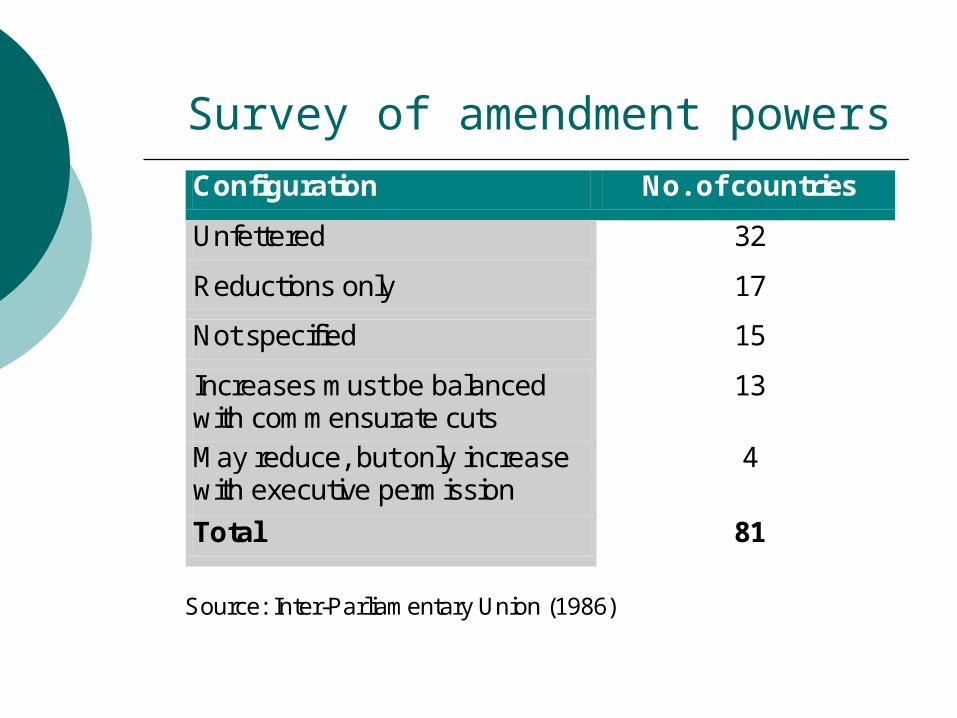

Survey of amendment powers

Configuration No. of countries

Unfettered 32

Reductions only 17

Not specified 15

Increases must be balanced with commensurate cuts

13

May reduce, but only increase with executive permission

4

Total 81

Source: Inter-Parliamentary Union (1986)

Case Study : Parliamentary Oversight (Commonwealth Countries)

54 countries in the Commonwealth

“Old” Commonwealth (UK, Canada, Australia, New Zealand) + the New

The “Large” (India, Pakistan, Bangladesh) + the “Small” (Caribbean, Pacific Islands)

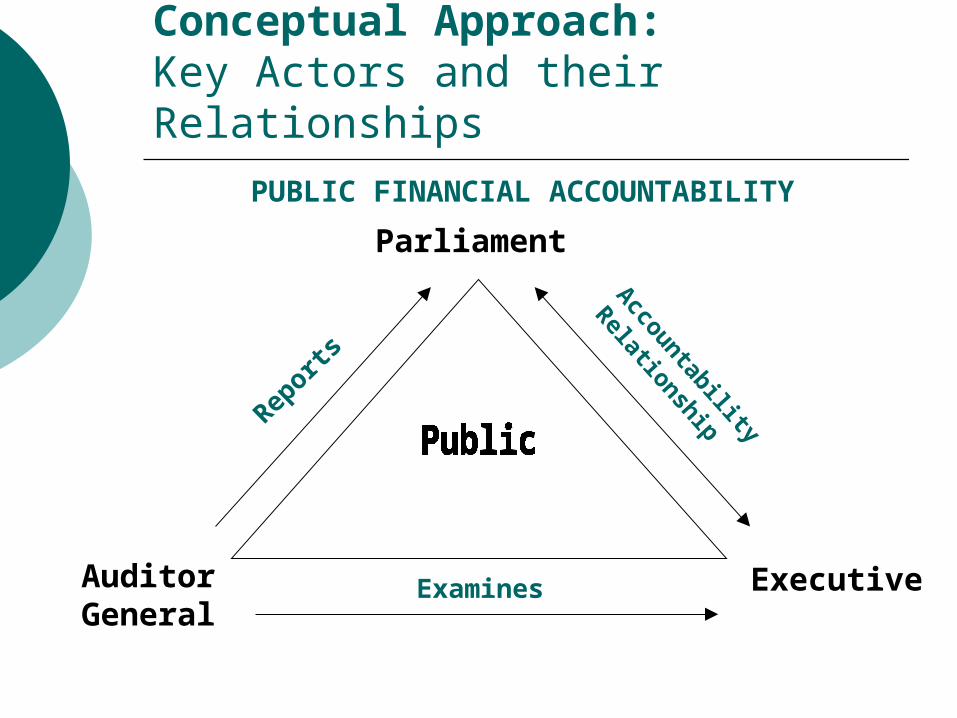

Conceptual Approach: Key Actors and their Relationships

Auditor General

Parliament

Executive

Reports

Examines

Accountability

Relationship

PUBLIC FINANCIAL ACCOUNTABILITY

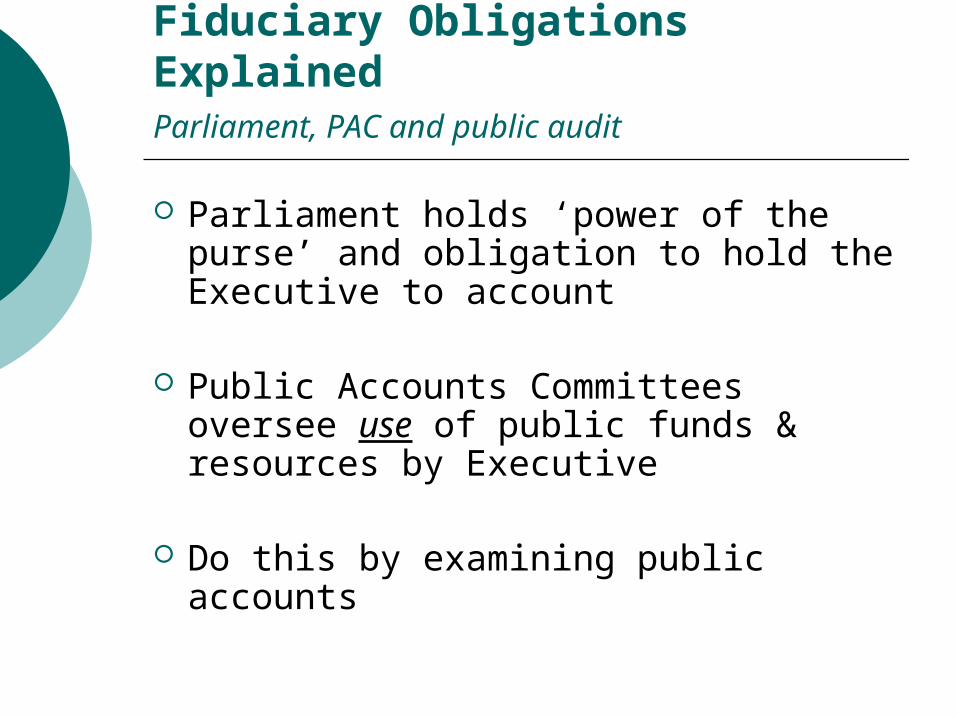

Conceptual Approach…cont. : Fiduciary Obligations ExplainedParliament, PAC and public audit

Parliament holds ‘power of the purse’ and obligation to hold the Executive to account

Public Accounts Committees oversee use of public funds & resources by Executive

Do this by examining public accounts

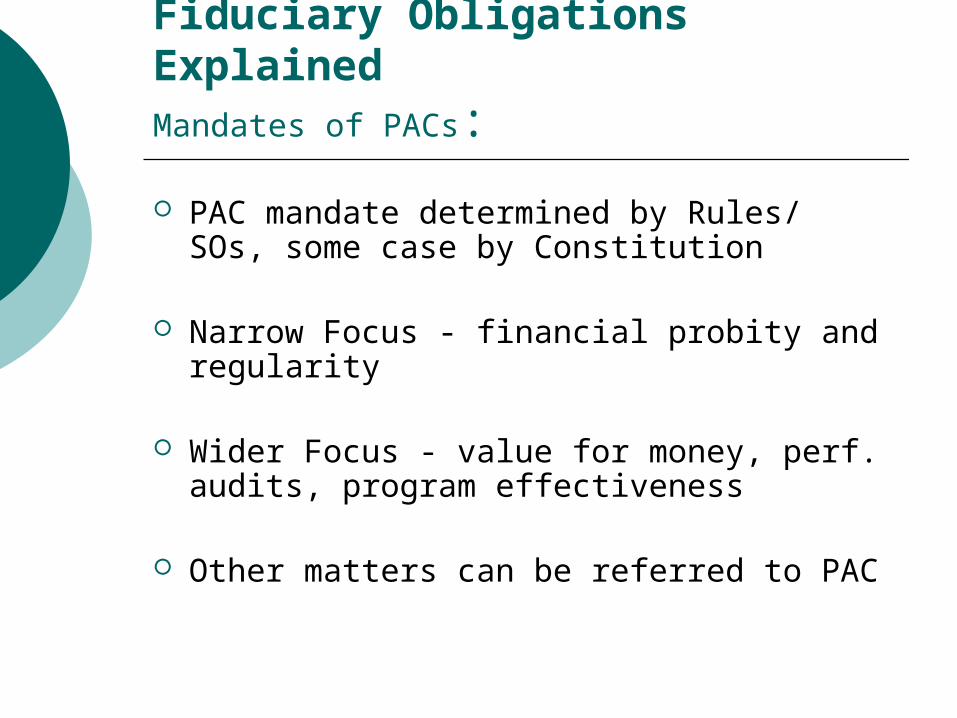

Conceptual Approach…cont. : Fiduciary Obligations ExplainedMandates of PACs:

PAC mandate determined by Rules/ SOs, some case by Constitution

Narrow Focus - financial probity and regularity

Wider Focus - value for money, perf. audits, program effectiveness

Other matters can be referred to PAC

Conceptual Approach…cont. : Fiduciary Obligations ExplainedPAC and the Auditor General

PAC work often determined by the AG reports

PAC must decide follow-up issues An effective PAC = depts. taking

AG concerns more seriously Cooperation with AG on follow-up

= greater accountability Ensures Depts. are taking

corrective action

Purpose of PACs

How can parliament ensure that the budget as approved was properly implemented?

Audit report only effective if findings are used to improve public financial management

First PAC established in 1861 as an institutional mechanism to close the “circle of financial control” (Gladstone)

Traditional focus on regularity and propriety Increasingly also on “value for money”

First principles:policy neutrality & non-partisanship

PAC not to question underlying policy Main interaction with departmental

officials In practice, often difficult to separate

administrative and political responsibility Inter-party co-operation and preference

for unanimity in decisions Opposition chairperson in 67% of PACs

Current Situation in the Commonwealth (Recent Empirical Work):

Recent CPA study on PACs – The Overseers

- similar issues, developments and challenges across Commonwealth

Key issues : Status of PAC, Relations with the AG, Membership, Training/ Capacity-Building, Resources, Working Practices, Reporting and Follow-up

Current Situation in the Commonwealth: Common Features:

Average size = 11 MPs

Size reflects party in legislature.

2/3 of Chairs from an opposition party; and 1/3 from the governing party

Prime focus on Public Accounts & reports of AG.

PAC reports generally available to the public.

Generally, PAC hearings are open to the public and media.

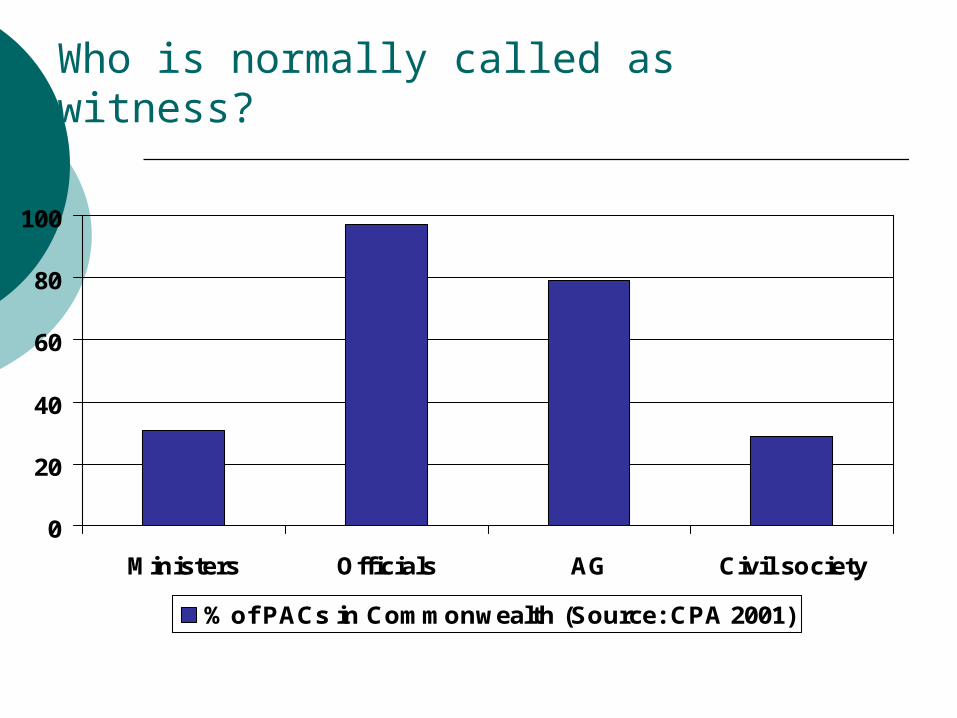

Who is normally called as witness?

0

20

40

60

80

100

Ministers Officials AG Civil society

% of PACs in Commonwealth (Source: CPA 2001)

Current Situation in the Commonwealth: Success Factors*

A broad scope Power to

select issues w/o gov’t direction

Power to report, suggest improvements, and follow-up

Strong support from AG, MPs and research staff that creates a unity of purpose about PAC work.

* Based on recent World Bank survey

Current Situation in the Commonwealth: Common Challenges:

Highly partisan climate Government dislike of legislative

oversight Lack of media or public involvement Lack of a strong ethical baseamong

parliamentarians

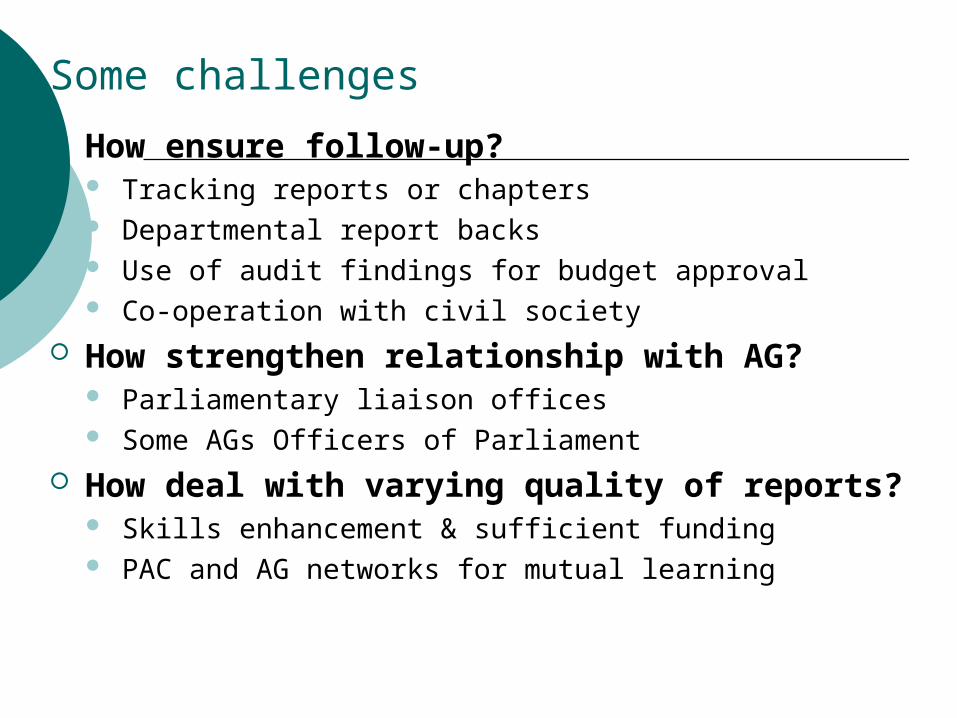

Some challenges

How ensure follow-up? Tracking reports or chapters Departmental report backs Use of audit findings for budget approval Co-operation with civil society

How strengthen relationship with AG? Parliamentary liaison offices Some AGs Officers of Parliament

How deal with varying quality of reports? Skills enhancement & sufficient funding PAC and AG networks for mutual learning

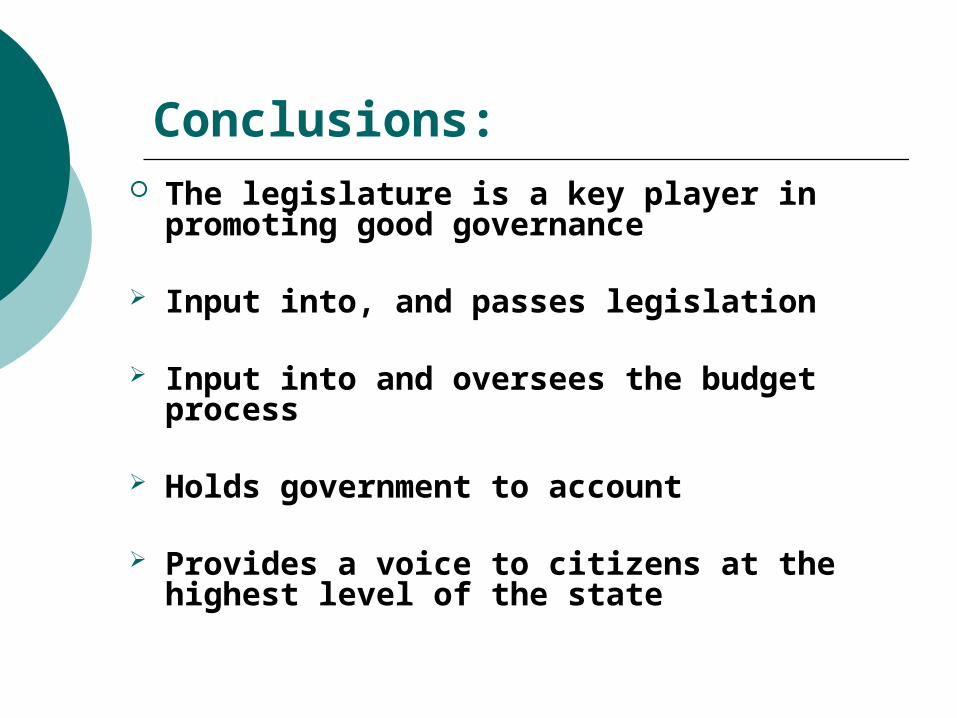

Conclusions: The legislature is a key player in

promoting good governance

Input into, and passes legislation

Input into and oversees the budget process

Holds government to account

Provides a voice to citizens at the highest level of the state

Concluding remarks

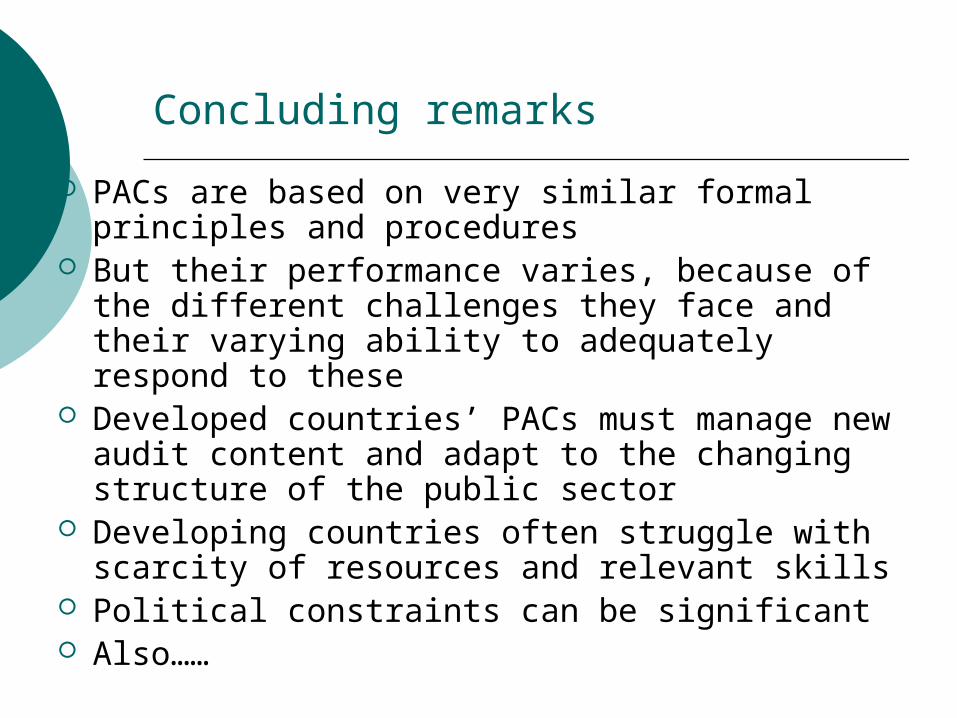

PACs are based on very similar formal principles and procedures

But their performance varies, because of the different challenges they face and their varying ability to adequately respond to these

Developed countries’ PACs must manage new audit content and adapt to the changing structure of the public sector

Developing countries often struggle with scarcity of resources and relevant skills

Political constraints can be significant Also……

![NATIONAL ACCOUNTABILITY ORDINANCE - Financial … ACCOUNTABILITY... · commencement of the National Accountability Bureau (Amendment) Ordinance, 2001;] 9[(j) ... financial institution,](https://img.pdfslide.us/doc/110x75/5b3d06607f8b9a28308bb0c8/national-accountability-ordinance-financial-accountability-commencement.jpg)