Embed Size (px)

Citation preview

Goldman Stanley

Goldman Stanley, Inc.

Confidential Draft

Project Aardvark

Presentation to the Board of Directors

January 29, 2010

Goldman Stanley

Table Of Contents

Executive Summary 3

Aardvark Valuation 5

Potential Acquisitions 11

Process Recommendations 16

Appendix 19

Goldman Stanley

Executive Summary

Goldman Stanley

Executive Summary

• As of January 29, 2010, Aardvark’s share price and valuation are at all-time highs, having more than doubled since early 2009

• As Aardvark’s stock price has soared in value, it has also generated over $35B in cash & cash-equivalents

• As Aardvark’s cash balance grows, it is likely to face shareholder pressure to re-invest the cash in its business and to make significant acquisitions

• Given Aardvark’s strong currency and cash balance, it could easily make several “tuck-in” acquisitions – or larger-scale acquisitions to acquire customers

• Such a strategy would allow Aardvark to capture more of the smartphone, laptop, and desktop markets, and significantly improve its software offerings

• Given Aardvark’s cash position, such acquisitions could be made with 100% cash – or in the case of a larger deal, stock could also be used

Goldman Stanley

Aardvark Valuation

Goldman Stanley

Valuation Summary

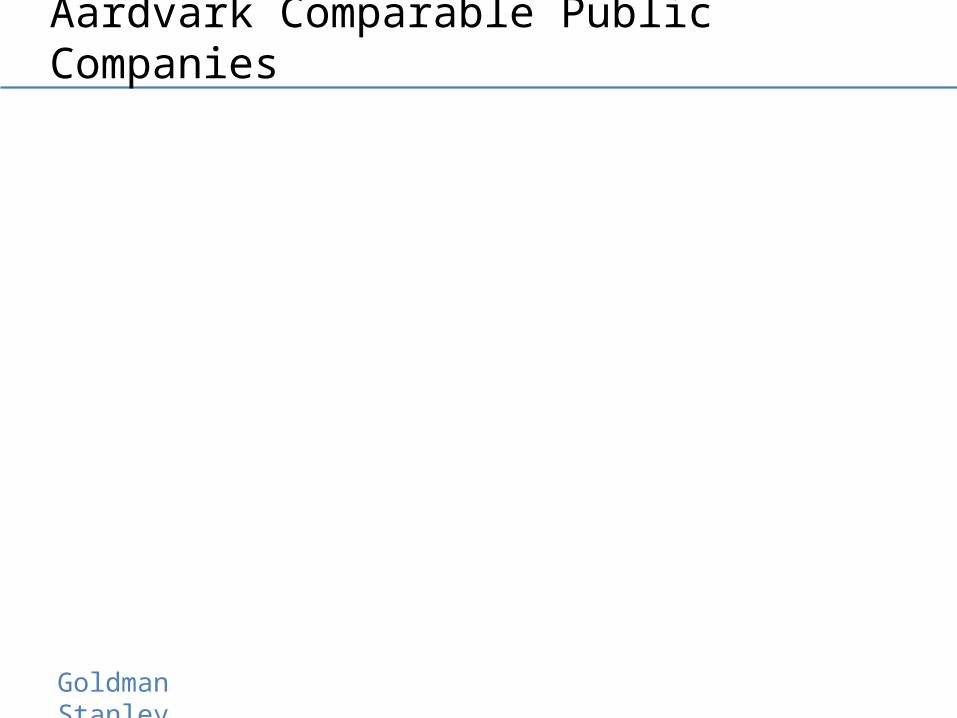

• Aardvark’s current share price of $192.61 far exceeds the value implied by comparable public companies

• Recent comparable transactions show higher implied valuation ranges due to flurry of consolidation and hardware M&A activity over 2009

• Discounted Cash Flow Analysis under base-case assumptions shows implied valuation on-par with Aardvark’s current share price, implying that share price is justified

• All valuation analysis is based on “base-case” financial projections in line with Wall Street analyst expectations

• Given Aardvark’s cash balance and high valuation multiples vs. similar public companies, few competitors are well-positioned to make substantial acquisitions

Goldman Stanley

Aardvark Valuation Summary

Goldman Stanley

Aardvark Comparable Public Companies

Goldman Stanley

Aardvark Precedent Transactions

Goldman Stanley

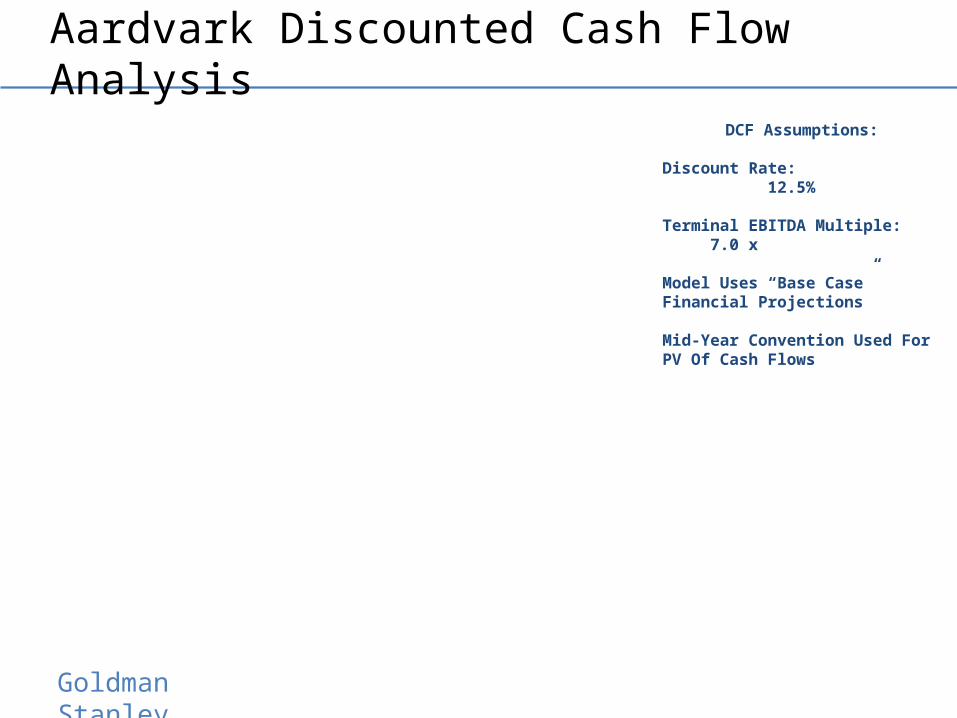

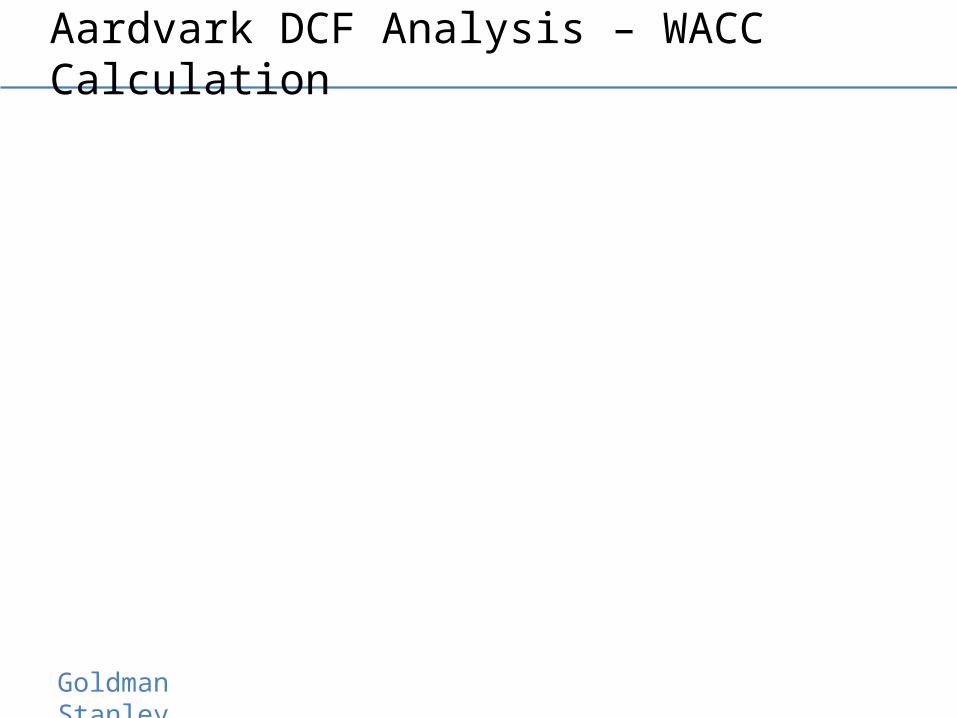

Aardvark Discounted Cash Flow Analysis

DCF Assumptions:

Discount Rate: 12.5%

Terminal EBITDA Multiple: 7.0 x

Model Uses “Base Case” Financial Projections

Mid-Year Convention Used For PV Of Cash Flows

Goldman Stanley

Potential Acquisitions

Goldman Stanley

Potential Acquisitions

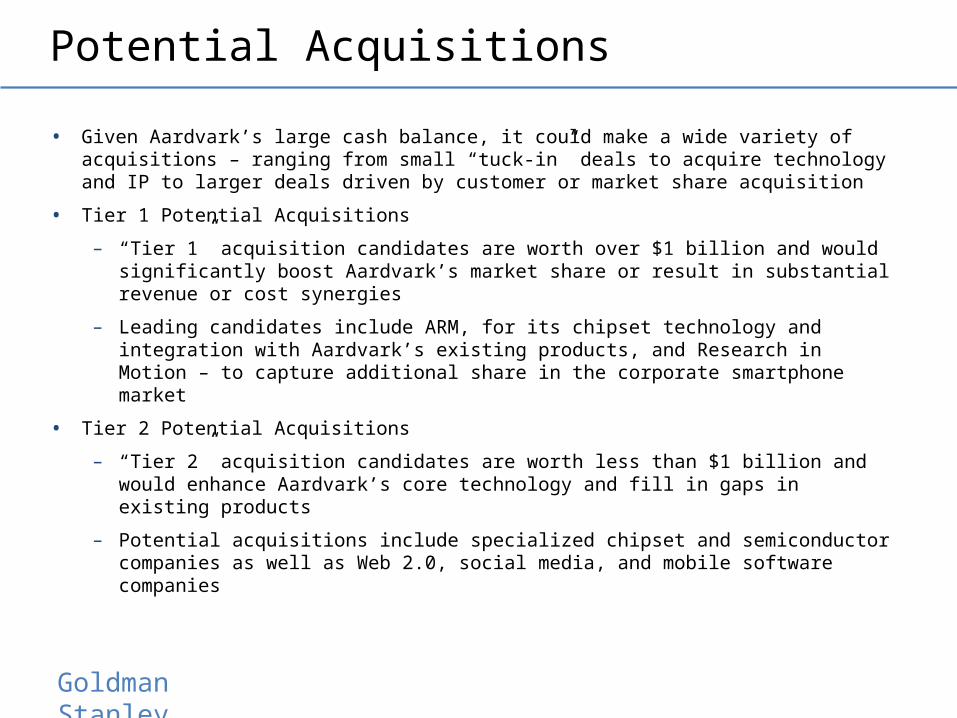

• Given Aardvark’s large cash balance, it could make a wide variety of acquisitions – ranging from small “tuck-in” deals to acquire technology and IP to larger deals driven by customer or market share acquisition

• Tier 1 Potential Acquisitions

– “Tier 1” acquisition candidates are worth over $1 billion and would significantly boost Aardvark’s market share or result in substantial revenue or cost synergies

– Leading candidates include ARM, for its chipset technology and integration with Aardvark’s existing products, and Research in Motion – to capture additional share in the corporate smartphone market

• Tier 2 Potential Acquisitions

– “Tier 2” acquisition candidates are worth less than $1 billion and would enhance Aardvark’s core technology and fill in gaps in existing products

– Potential acquisitions include specialized chipset and semiconductor companies as well as Web 2.0, social media, and mobile software companies

Goldman Stanley

Potential Acquisition Candidates

Tier 1 Acquisition Candidates

Tier 2 Acquisition Candidates

Goldman Stanley

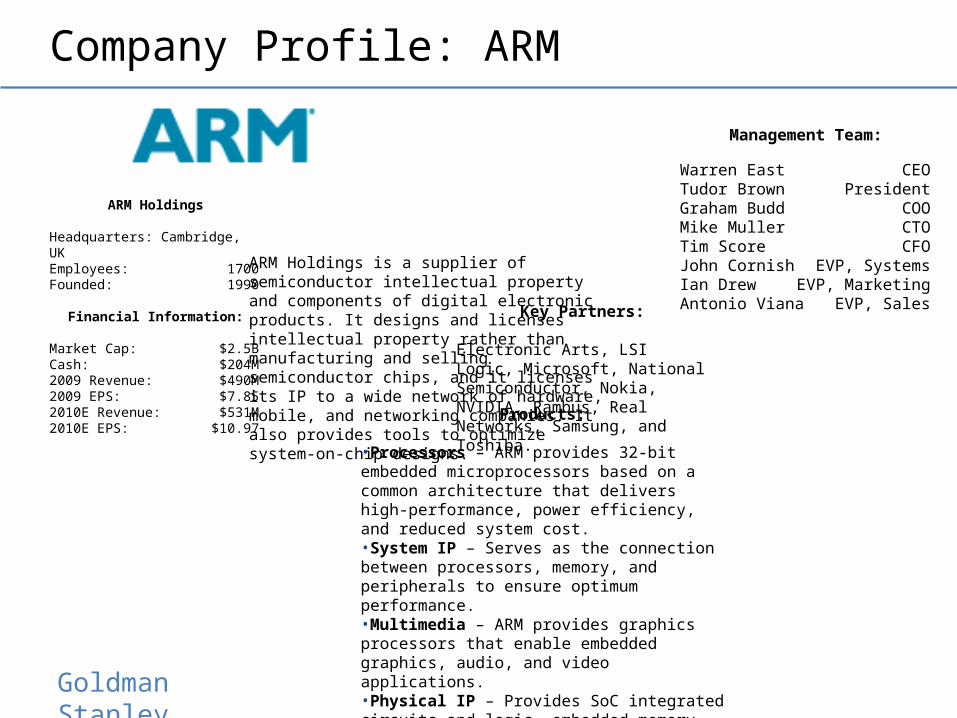

Company Profile: ARM

ARM Holdings is a supplier of semiconductor intellectual property and components of digital electronic products. It designs and licenses intellectual property rather than manufacturing and selling semiconductor chips, and it licenses its IP to a wide network of hardware, mobile, and networking companies. It also provides tools to optimize system-on-chip designs.

Products:

•Processors – ARM provides 32-bit embedded microprocessors based on a common architecture that delivers high-performance, power efficiency, and reduced system cost.•System IP – Serves as the connection between processors, memory, and peripherals to ensure optimum performance.•Multimedia – ARM provides graphics processors that enable embedded graphics, audio, and video applications. •Physical IP – Provides SoC integrated circuits and logic, embedded memory, and interface IP.•Tools – ARM subsidiaries provide compilers, debuggers, simulators, and other optimization tools for a wide variety of chip and processor families.

Key Partners:

Electronic Arts, LSI Logic, Microsoft, National Semiconductor, Nokia, NVIDIA, Rambus, Real Networks, Samsung, and Toshiba.

Headquarters: Cambridge, UKEmployees: 1700Founded: 1990

Market Cap: $2.5BCash: $204M2009 Revenue: $490M2009 EPS: $7.852010E Revenue: $531M2010E EPS: $10.97

Warren East CEOTudor Brown PresidentGraham Budd COOMike Muller CTOTim Score CFOJohn Cornish EVP, SystemsIan Drew EVP, MarketingAntonio Viana EVP, Sales

ARM Holdings

Financial Information:

Management Team:

Goldman Stanley

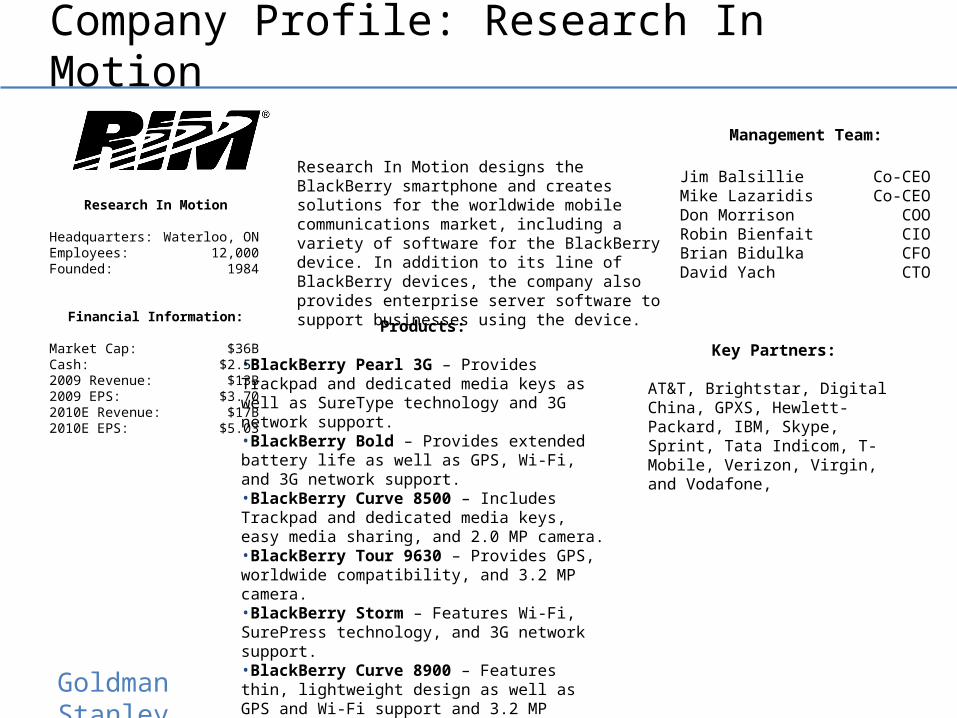

Company Profile: Research In Motion

Research In Motion designs the BlackBerry smartphone and creates solutions for the worldwide mobile communications market, including a variety of software for the BlackBerry device. In addition to its line of BlackBerry devices, the company also provides enterprise server software to support businesses using the device.

Products:

•BlackBerry Pearl 3G – Provides Trackpad and dedicated media keys as well as SureType technology and 3G network support.•BlackBerry Bold – Provides extended battery life as well as GPS, Wi-Fi, and 3G network support.•BlackBerry Curve 8500 – Includes Trackpad and dedicated media keys, easy media sharing, and 2.0 MP camera.•BlackBerry Tour 9630 – Provides GPS, worldwide compatibility, and 3.2 MP camera.•BlackBerry Storm – Features Wi-Fi, SurePress technology, and 3G network support.•BlackBerry Curve 8900 – Features thin, lightweight design as well as GPS and Wi-Fi support and 3.2 MP camera.

Key Partners:

AT&T, Brightstar, Digital China, GPXS, Hewlett-Packard, IBM, Skype, Sprint, Tata Indicom, T-Mobile, Verizon, Virgin, and Vodafone,

Headquarters: Waterloo, ONEmployees: 12,000Founded: 1984

Market Cap: $36BCash: $2.5B2009 Revenue: $13B2009 EPS: $3.702010E Revenue: $17B2010E EPS: $5.03

Jim Balsillie Co-CEOMike Lazaridis Co-CEODon Morrison COORobin Bienfait CIOBrian Bidulka CFODavid Yach CTO

Research In Motion

Financial Information:

Management Team:

Goldman Stanley

Process Recommendations

Goldman Stanley

Key Recommendations

• We recommend engaging in targeted discussions with the Tier 1 acquisition candidates and assessing their receptiveness to M&A discussions

• At the same time, Goldman Stanley will reach out to Tier 2 candidates and introduce Aardvark as a potential acquirer

• M&A process with Tier 1 candidates will take significantly longer due to the scale of the companies, so we recommend conducting both processes simultaneously

• Depending on responses from Tier 1 and Tier 2 candidates, Goldman Stanley and Aardvark may do additional research to determine other potential acquisitions and then approach them

Goldman Stanley

Process Recommendation

BroadMarketing

Goldman Stanley

Appendix

Goldman Stanley

Aardvark Projected Income Statement

Goldman Stanley

Aardvark Comparable Public Companies

Goldman Stanley

Aardvark DCF Analysis – WACC Calculation