Embed Size (px)

Citation preview

©2016 Lincoln National Corporation

December 7, 2016 Chris Giovanni 484-583-1793 [email protected]

GOLDMAN SACHS U.S. FINANCIAL SERVICES CONFERENCE 2016

Dennis R. Glass | President and Chief Executive Officer

New York, NY

LINCOLN STORY

2

3

Highly Integrated

U.S. RETAIL-CENTRIC; TARGETING SELECT HIGH-GROWTH AREAS

Four Core Businesses

High Growth Segments

Centralized Distribution

Retail Focused Products

Risk Management

Strong Capital Position

• Annuity

• Group Protection (GP)

• Life

• Retirement Plan Services (RPS)

• Mass affluent Annuity

• Employee-paid Group Protection

• High end Life

• Gen X / millennial markets

• Small employers and government

• Broad shelf space

• Wholesale

• Retail

• Worksite

• Comprehensive

• Innovative

• Diversified

• Multi-solution

• Rigorous planning

• Active monitoring

• Centralized

• Integral to product design

• Free cash flow generation

• Steady growth in dividends and buybacks

• Appropriate leverage

Clear and consistent focus on retail products in the United States

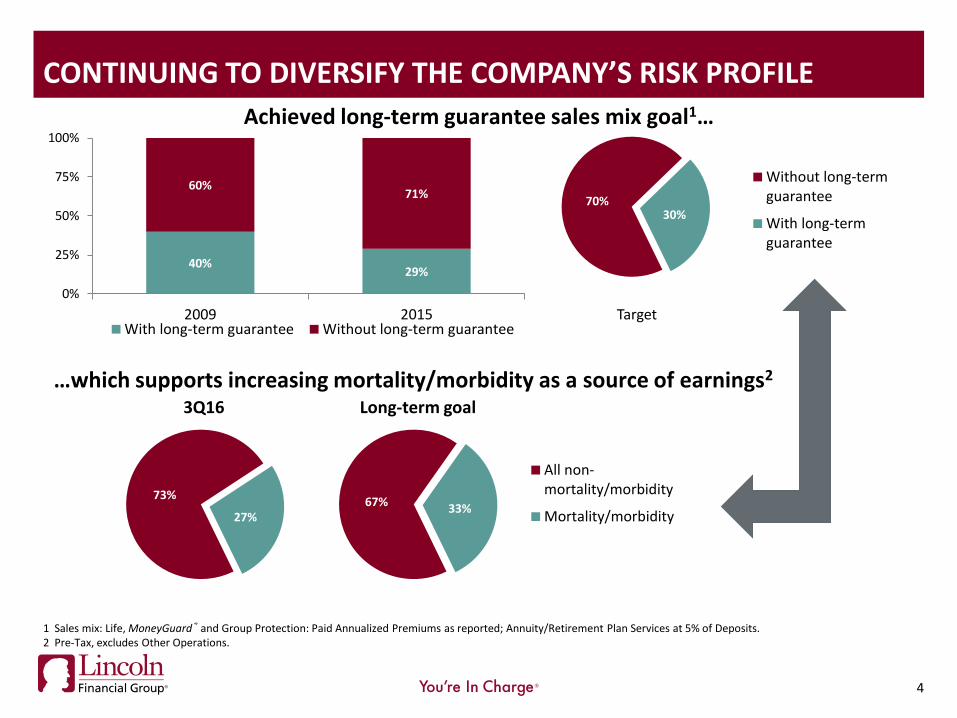

40% 29%

60% 71%

0%

25%

50%

75%

100%

2009 2015With long-term guarantee Without long-term guarantee

67% 33%

All non-mortality/morbidity

Mortality/morbidity

CONTINUING TO DIVERSIFY THE COMPANY’S RISK PROFILE

Achieved long-term guarantee sales mix goal1…

…which supports increasing mortality/morbidity as a source of earnings2

70% 30%

Without long-termguarantee

With long-termguarantee

1 Sales mix: Life, MoneyGuard® and Group Protection: Paid Annualized Premiums as reported; Annuity/Retirement Plan Services at 5% of Deposits. 2 Pre-Tax, excludes Other Operations.

4

Target

73%

27%

3Q16 Long-term goal

5

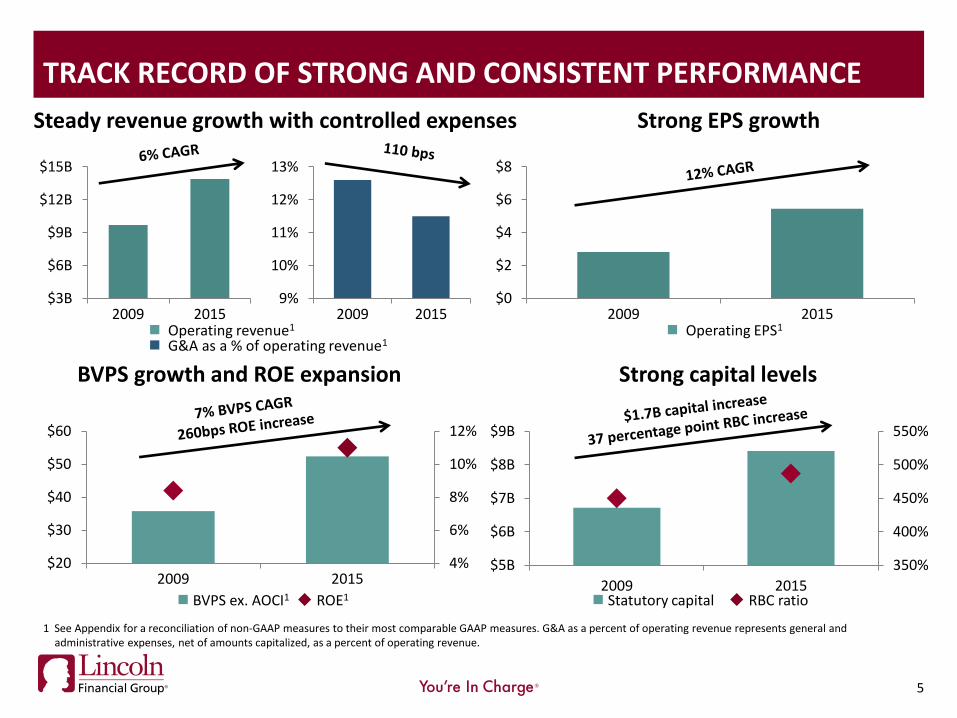

TRACK RECORD OF STRONG AND CONSISTENT PERFORMANCE

350%

400%

450%

500%

550%

$5B

$6B

$7B

$8B

$9B

2009 2015

4%

6%

8%

10%

12%

$20

$30

$40

$50

$60

2009 2015

Strong capital levels BVPS growth and ROE expansion

BVPS ex. AOCI1 ROE1 Statutory capital RBC ratio

$0

$2

$4

$6

$8

2009 2015 Operating EPS1

Strong EPS growth Steady revenue growth with controlled expenses

$3B

$6B

$9B

$12B

$15B

2009 2015 Operating revenue1

G&A as a % of operating revenue1

9%

10%

11%

12%

13%

2009 2015

1 See Appendix for a reconciliation of non-GAAP measures to their most comparable GAAP measures. G&A as a percent of operating revenue represents general and administrative expenses, net of amounts capitalized, as a percent of operating revenue.

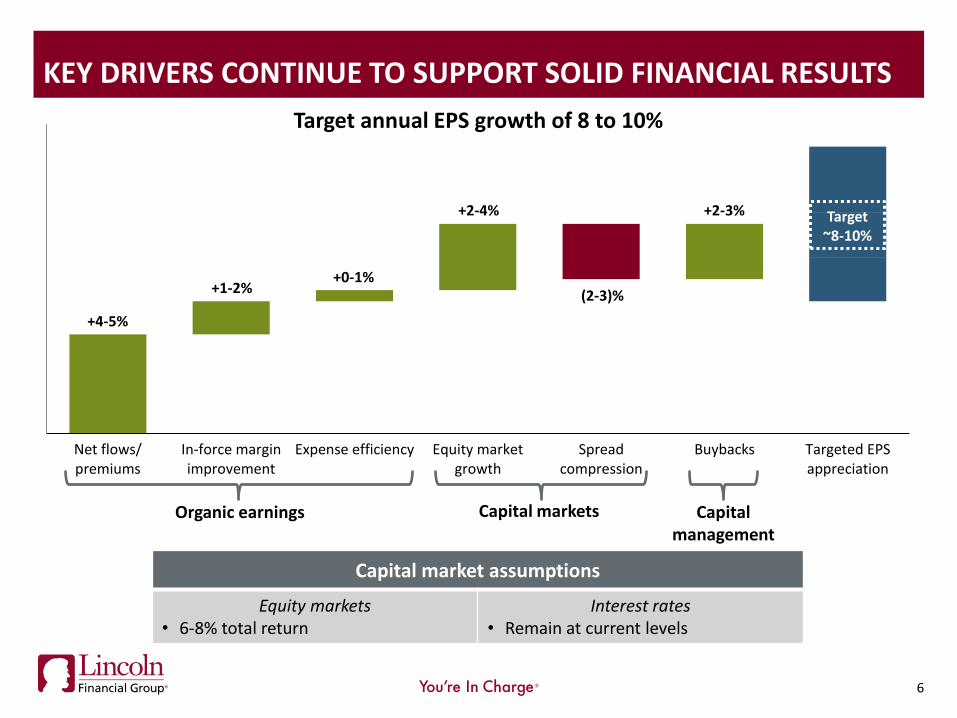

KEY DRIVERS CONTINUE TO SUPPORT SOLID FINANCIAL RESULTS

6

Organic earnings Capital management

Capital markets

Net flows/premiums

In-force marginimprovement

Expense efficiency Equity marketgrowth

Spreadcompression

Buybacks Targeted EPSappreciation

+2-4%

+1-2%

+4-5%

(2-3)%

+2-3%

+0-1%

Target ~8-10%

Capital market assumptions

Equity markets • 6-8% total return

Interest rates • Remain at current levels

Target annual EPS growth of 8 to 10%

7

7

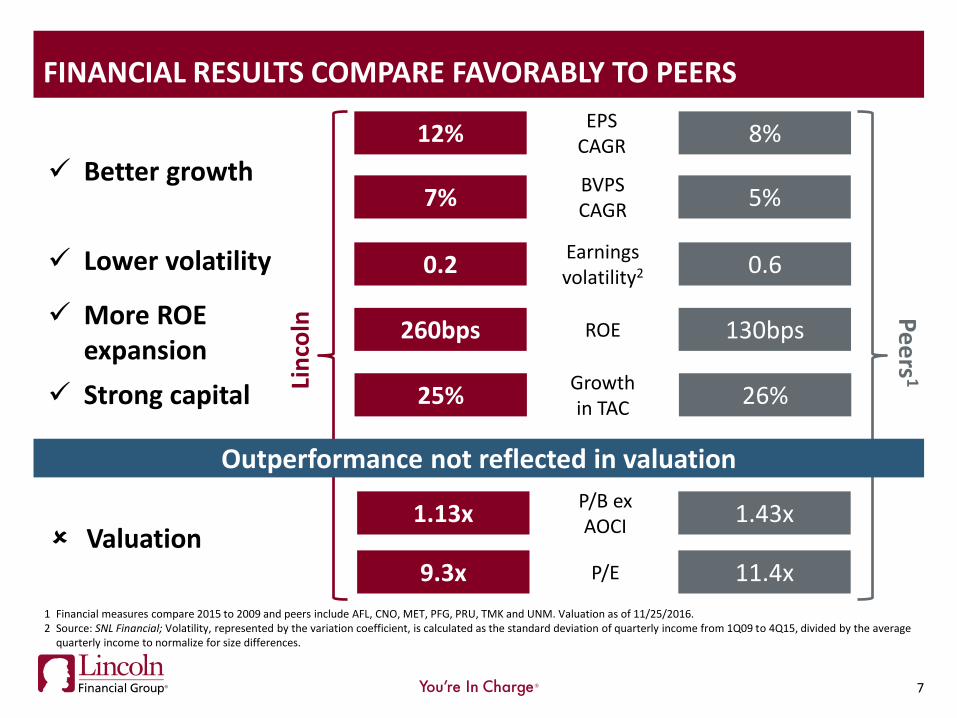

FINANCIAL RESULTS COMPARE FAVORABLY TO PEERS

1 Financial measures compare 2015 to 2009 and peers include AFL, CNO, MET, PFG, PRU, TMK and UNM. Valuation as of 11/25/2016. 2 Source: SNL Financial; Volatility, represented by the variation coefficient, is calculated as the standard deviation of quarterly income from 1Q09 to 4Q15, divided by the average

quarterly income to normalize for size differences.

More ROE expansion

Lower volatility

7%

260bps

0.2

5%

130bps

0.6

Lin

coln

Pe

ers

1

Better growth

12% 8%

Strong capital 25% 26%

BVPS CAGR

ROE

Earnings volatility2

EPS CAGR

Growth in TAC

Outperformance not reflected in valuation

Valuation 1.13x 1.43x

P/B ex AOCI

9.3x 11.4x P/E

6.8% 6.8%

3.4% 3.6%

12.5 12.0

■ Actual ■ Expected

8

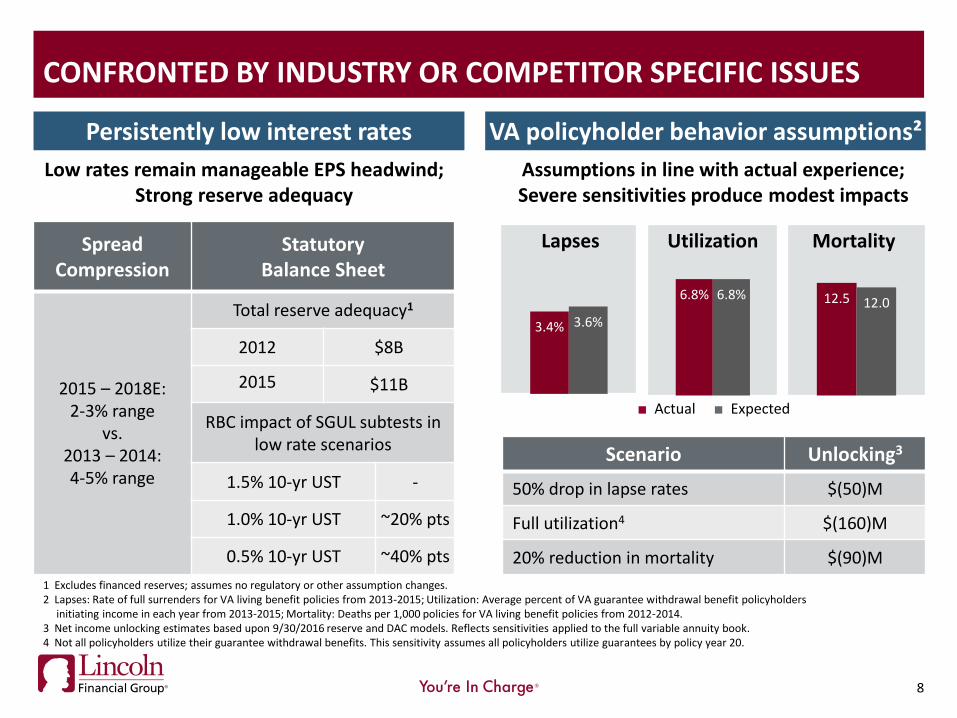

CONFRONTED BY INDUSTRY OR COMPETITOR SPECIFIC ISSUES

1 Excludes financed reserves; assumes no regulatory or other assumption changes. 2 Lapses: Rate of full surrenders for VA living benefit policies from 2013-2015; Utilization: Average percent of VA guarantee withdrawal benefit policyholders initiating income in each year from 2013-2015; Mortality: Deaths per 1,000 policies for VA living benefit policies from 2012-2014. 3 Net income unlocking estimates based upon 9/30/2016 reserve and DAC models. Reflects sensitivities applied to the full variable annuity book. 4 Not all policyholders utilize their guarantee withdrawal benefits. This sensitivity assumes all policyholders utilize guarantees by policy year 20.

Utilization Lapses Mortality

Scenario Unlocking3

50% drop in lapse rates $(50)M

Full utilization4 $(160)M

20% reduction in mortality $(90)M

Assumptions in line with actual experience; Severe sensitivities produce modest impacts

Spread Compression

Statutory Balance Sheet

2015 – 2018E: 2-3% range

vs. 2013 – 2014: 4-5% range

Total reserve adequacy1

2012 $8B

2015 $11B

RBC impact of SGUL subtests in low rate scenarios

1.5% 10-yr UST -

1.0% 10-yr UST ~20% pts

0.5% 10-yr UST ~40% pts

Persistently low interest rates VA policyholder behavior assumptions²

Low rates remain manageable EPS headwind; Strong reserve adequacy

Actions to date

RPS: base spread

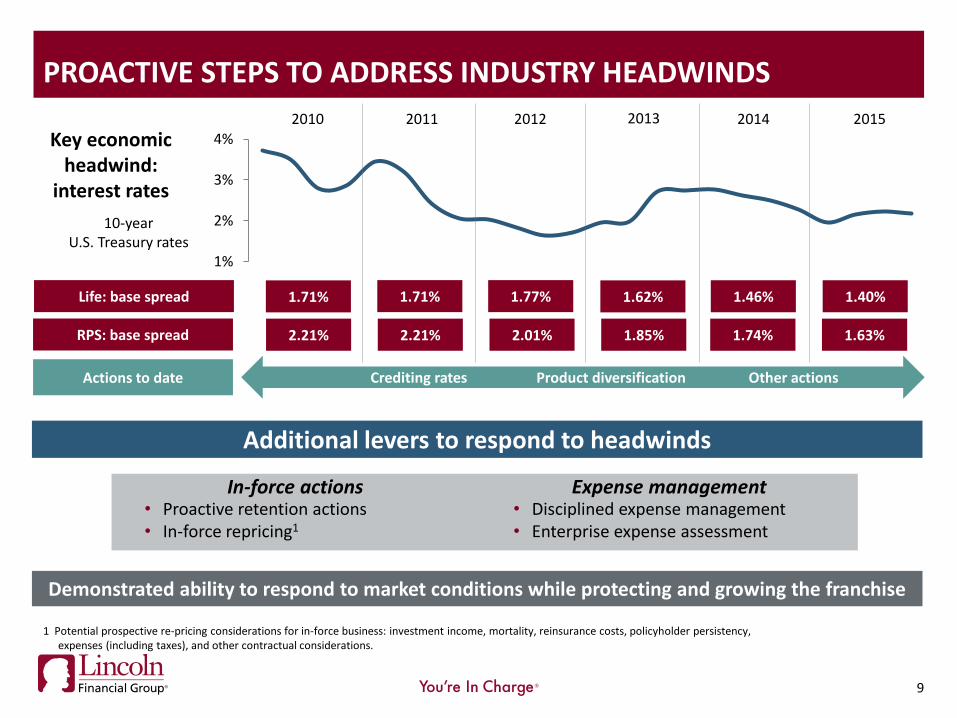

9

1%

2%

3%

4%2010 2011 2012 2013 2014 2015

Key economic headwind:

interest rates

Demonstrated ability to respond to market conditions while protecting and growing the franchise

Crediting rates Other actions

1 Potential prospective re-pricing considerations for in-force business: investment income, mortality, reinsurance costs, policyholder persistency, expenses (including taxes), and other contractual considerations.

• Proactive retention actions • In-force repricing1

Life: base spread 1.71% 1.71% 1.77% 1.62% 1.46% 1.40%

10-year U.S. Treasury rates

• Disciplined expense management • Enterprise expense assessment

In-force actions

PROACTIVE STEPS TO ADDRESS INDUSTRY HEADWINDS

Additional levers to respond to headwinds

Expense management

Product diversification

2.21% 2.21% 2.01% 1.85% 1.74% 1.63%

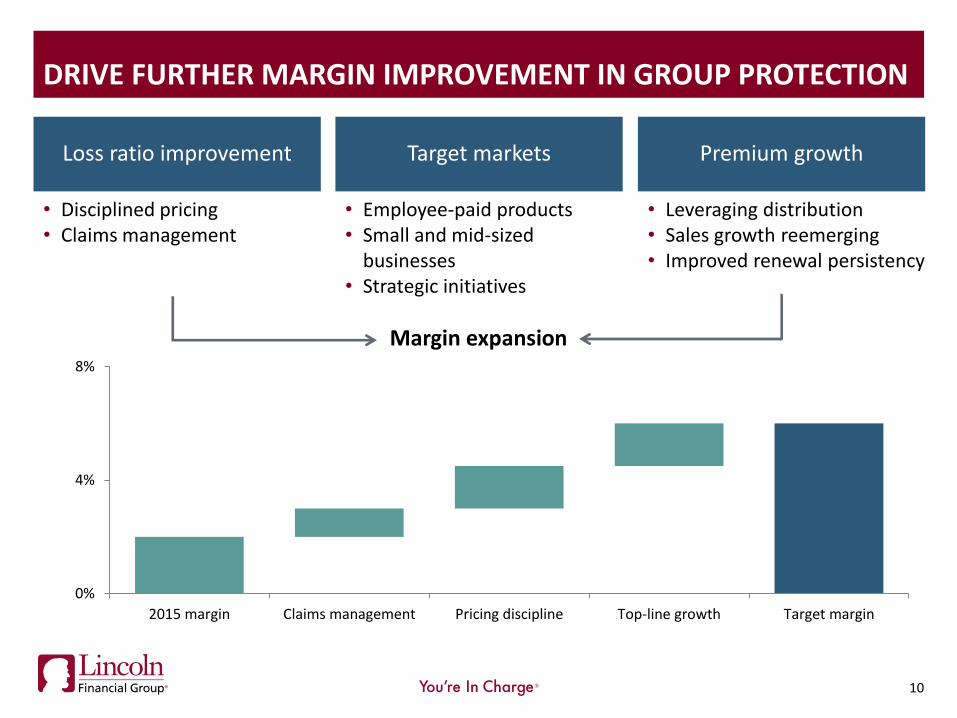

0%

4%

8%

2015 margin Claims management Pricing discipline Top-line growth Target margin

10

Loss ratio improvement Premium growth Target markets

• Disciplined pricing • Claims management

• Employee-paid products • Small and mid-sized

businesses • Strategic initiatives

• Leveraging distribution • Sales growth reemerging • Improved renewal persistency

Margin expansion

DRIVE FURTHER MARGIN IMPROVEMENT IN GROUP PROTECTION

11

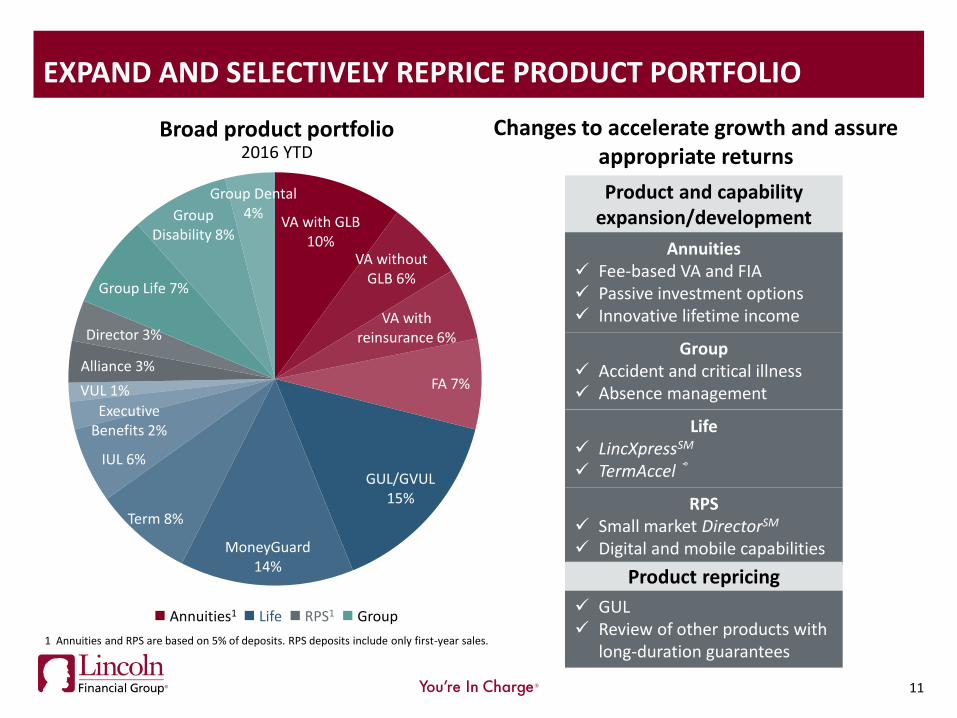

EXPAND AND SELECTIVELY REPRICE PRODUCT PORTFOLIO

Broad product portfolio 2016 YTD

Changes to accelerate growth and assure appropriate returns

Product and capability expansion/development

Annuities Fee-based VA and FIA Passive investment options Innovative lifetime income

Group Accident and critical illness Absence management

Life LincXpressSM

TermAccel ®

RPS Small market DirectorSM Digital and mobile capabilities

GUL Review of other products with

long-duration guarantees

Product repricing

1 Annuities and RPS are based on 5% of deposits. RPS deposits include only first-year sales.

Annuities1 Life RPS1 Group

VA with GLB 10%

VA without GLB 6%

VA with reinsurance 6%

FA 7%

GUL/GVUL 15%

MoneyGuard 14%

Term 8%

IUL 6%

Executive Benefits 2%

VUL 1%

Alliance 3%

Director 3%

Group Life 7%

Group Disability 8%

Group Dental 4%

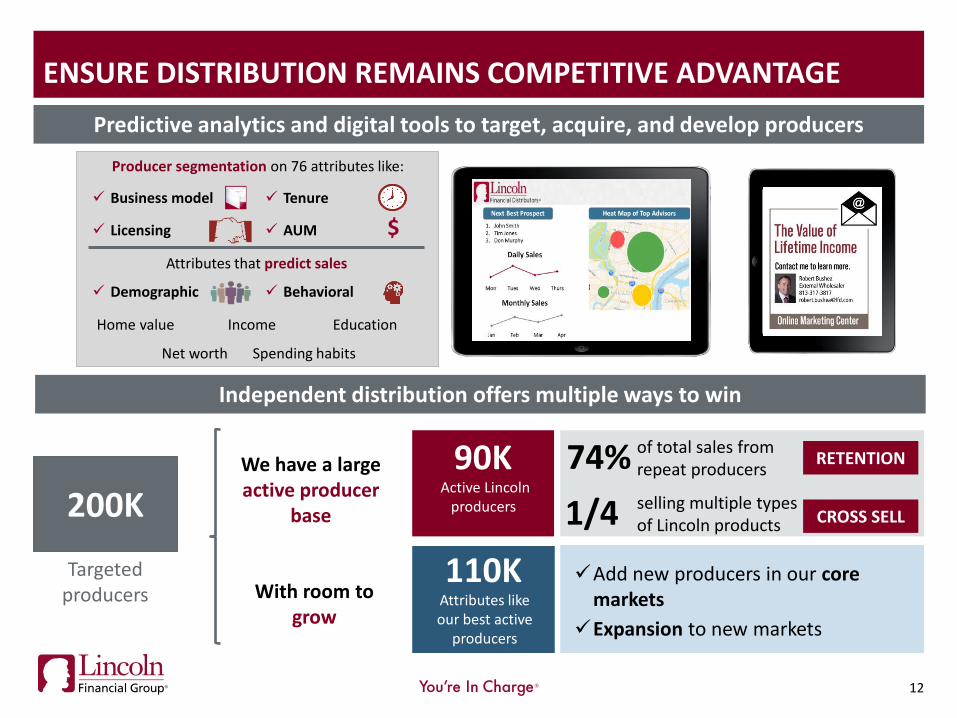

RETENTION We have a large active producer

base

With room to grow

Add new producers in our core markets

Expansion to new markets

of total sales from repeat producers 74%

1/4 selling multiple types of Lincoln products

Predictive analytics and digital tools to target, acquire, and develop producers

CROSS SELL

90K

110K

Active Lincoln producers

Attributes like our best active

producers

Targeted producers

ENSURE DISTRIBUTION REMAINS COMPETITIVE ADVANTAGE

200K

12

$

Producer segmentation on 76 attributes like:

Behavioral Demographic

Tenure

Licensing AUM

Business model

Attributes that predict sales

Home value

Net worth

Income

Spending habits

Education

Independent distribution offers multiple ways to win

13

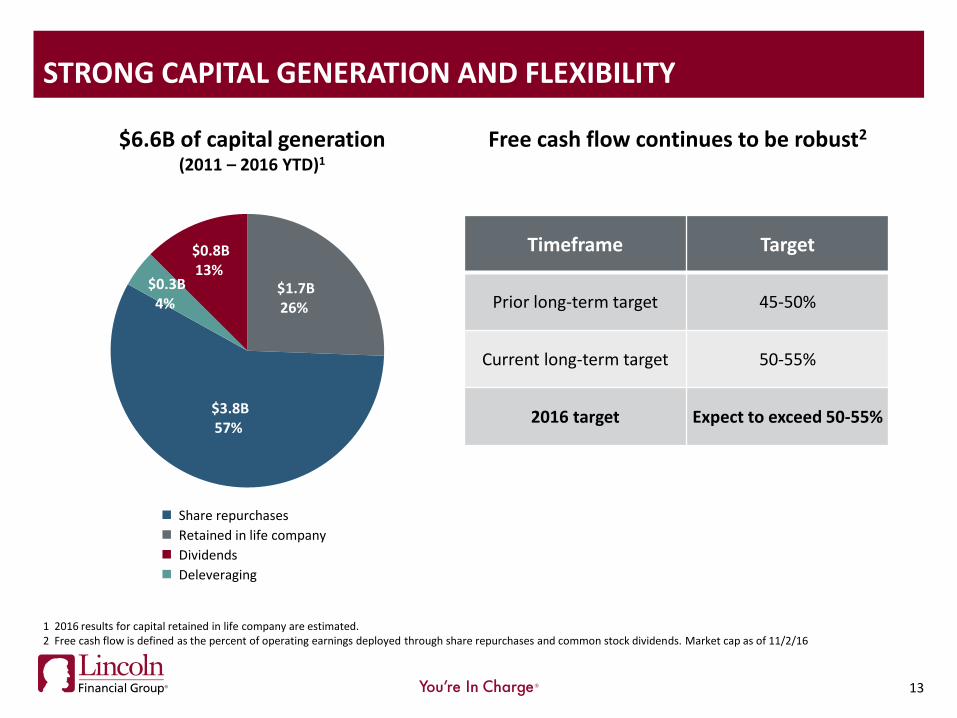

Share repurchases

Retained in life company

Dividends

Deleveraging

STRONG CAPITAL GENERATION AND FLEXIBILITY

$6.6B of capital generation (2011 – 2016 YTD)1

1 2016 results for capital retained in life company are estimated. 2 Free cash flow is defined as the percent of operating earnings deployed through share repurchases and common stock dividends. Market cap as of 11/2/16

$1.7B 26%

$3.8B 57%

$0.8B 13%

$0.3B 4%

Free cash flow continues to be robust2

Timeframe Target

Prior long-term target 45-50%

Current long-term target 50-55%

2016 target Expect to exceed 50-55%

ANNUITIES

14

$0M

$200M

$400M

$600M

$800M

$1,000M

$1,200M

20

09

20

10

20

11

20

12

20

13

20

14

20

15

YTD

15

YTD

16

2015 YTD 2016 YTD

15

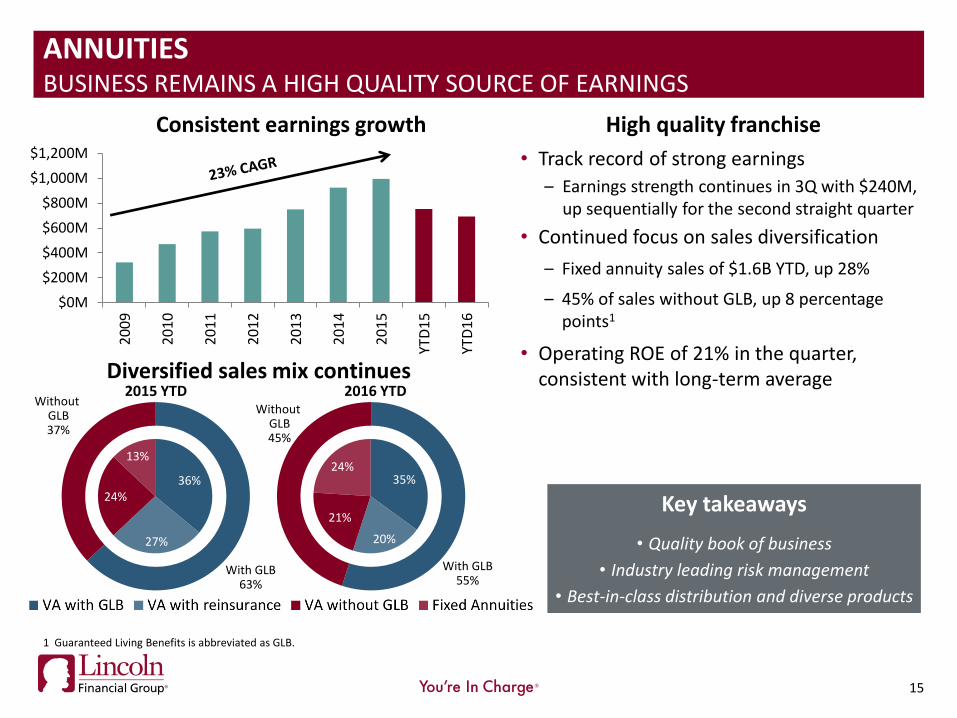

Diversified sales mix continues

1 Guaranteed Living Benefits is abbreviated as GLB.

ANNUITIES BUSINESS REMAINS A HIGH QUALITY SOURCE OF EARNINGS

Consistent earnings growth

With GLB 63%

Without GLB 37%

With GLB 55%

35%

20%

21%

24%

Without GLB 45%

36%

27%

24%

13%

• Track record of strong earnings

– Earnings strength continues in 3Q with $240M, up sequentially for the second straight quarter

• Continued focus on sales diversification

– Fixed annuity sales of $1.6B YTD, up 28%

– 45% of sales without GLB, up 8 percentage points1

• Operating ROE of 21% in the quarter, consistent with long-term average

Key takeaways

• Quality book of business

• Industry leading risk management

• Best-in-class distribution and diverse products

High quality franchise

$(3)B$(2)B$(1)B

$0B$1B$2B$3B

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

Change in hedge target Hedge program performance (net breakage)

2010 2011 2012 2013 2014 2015 3Q16YTD

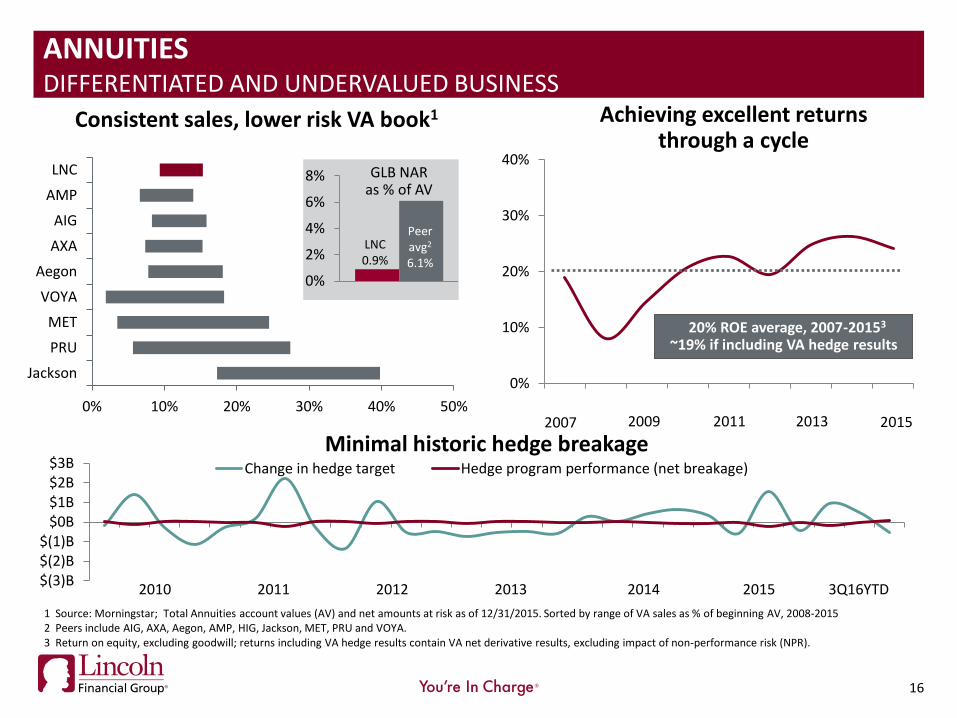

0% 10% 20% 30% 40% 50%

LNC

AMP

AIG

AXA

Aegon

VOYA

MET

PRU

Jackson

16

Consistent sales, lower risk VA book1

0%

2%

4%

6%

8% GLB NAR as % of AV

LNC 0.9%

Peer avg2

6.1%

ANNUITIES DIFFERENTIATED AND UNDERVALUED BUSINESS

Minimal historic hedge breakage

Achieving excellent returns through a cycle

0%

10%

20%

30%

40%

20% ROE average, 2007-20153

~19% if including VA hedge results

2007 2009 2011 2013 2015

1 Source: Morningstar; Total Annuities account values (AV) and net amounts at risk as of 12/31/2015. Sorted by range of VA sales as % of beginning AV, 2008-2015 2 Peers include AIG, AXA, Aegon, AMP, HIG, Jackson, MET, PRU and VOYA. 3 Return on equity, excluding goodwill; returns including VA hedge results contain VA net derivative results, excluding impact of non-performance risk (NPR).

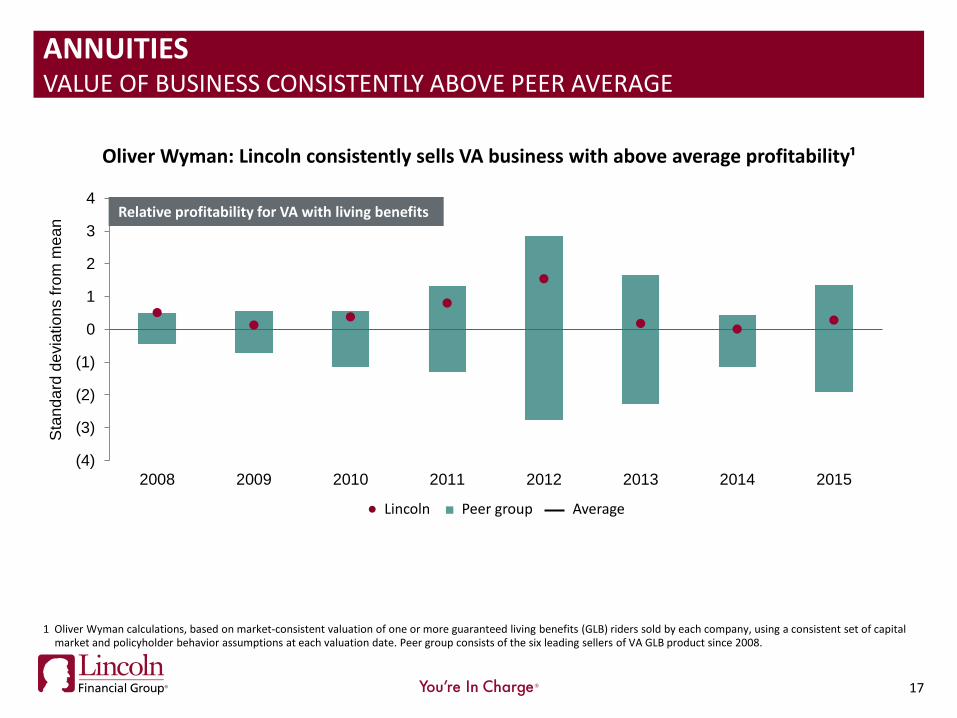

ANNUITIES VALUE OF BUSINESS CONSISTENTLY ABOVE PEER AVERAGE

(4)

(3)

(2)

(1)

0

1

2

3

4

2008 2009 2010 2011 2012 2013 2014 2015

Sta

nd

ard

de

via

tion

s f

rom

me

an

Oliver Wyman: Lincoln consistently sells VA business with above average profitability¹

Relative profitability for VA with living benefits

17

● Lincoln ■ Peer group Average

1 Oliver Wyman calculations, based on market‐consistent valuation of one or more guaranteed living benefits (GLB) riders sold by each company, using a consistent set of capital market and policyholder behavior assumptions at each valuation date. Peer group consists of the six leading sellers of VA GLB product since 2008.

18 18

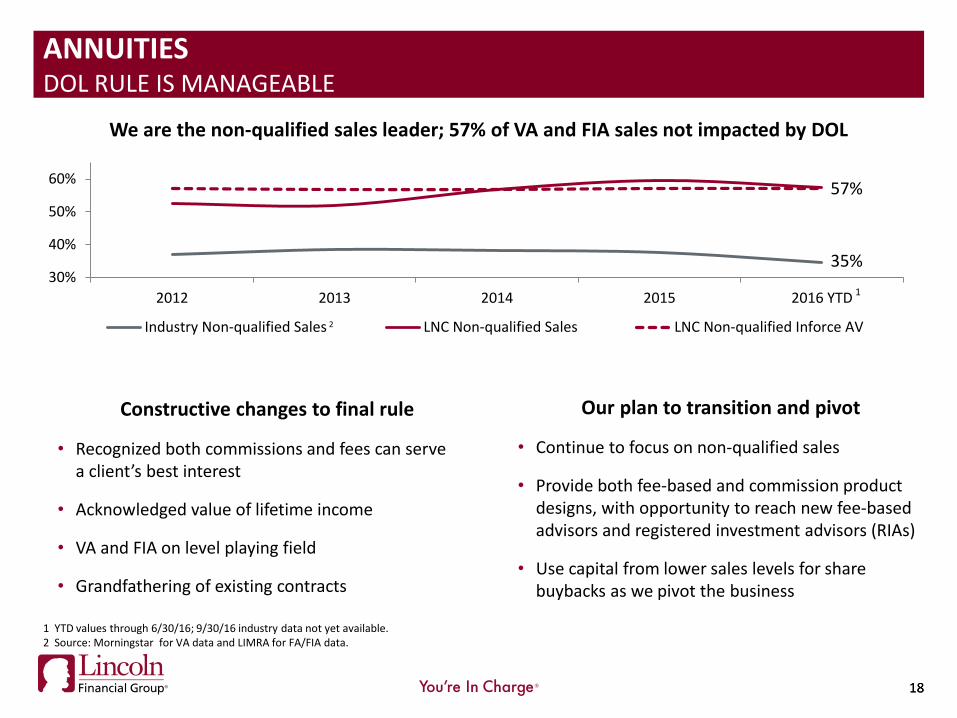

ANNUITIES DOL RULE IS MANAGEABLE

Our plan to transition and pivot

• Continue to focus on non-qualified sales

• Provide both fee-based and commission product designs, with opportunity to reach new fee-based advisors and registered investment advisors (RIAs)

• Use capital from lower sales levels for share buybacks as we pivot the business

We are the non-qualified sales leader; 57% of VA and FIA sales not impacted by DOL

Constructive changes to final rule

• Recognized both commissions and fees can serve a client’s best interest

• Acknowledged value of lifetime income

• VA and FIA on level playing field

• Grandfathering of existing contracts

35%

57%

30%

40%

50%

60%

2012 2013 2014 2015 2016 YTD

Industry Non-qualified Sales LNC Non-qualified Sales LNC Non-qualified Inforce AV

1 YTD values through 6/30/16; 9/30/16 industry data not yet available. 2 Source: Morningstar for VA data and LIMRA for FA/FIA data.

1

2

RETIREMENT PLAN SERVICES

19

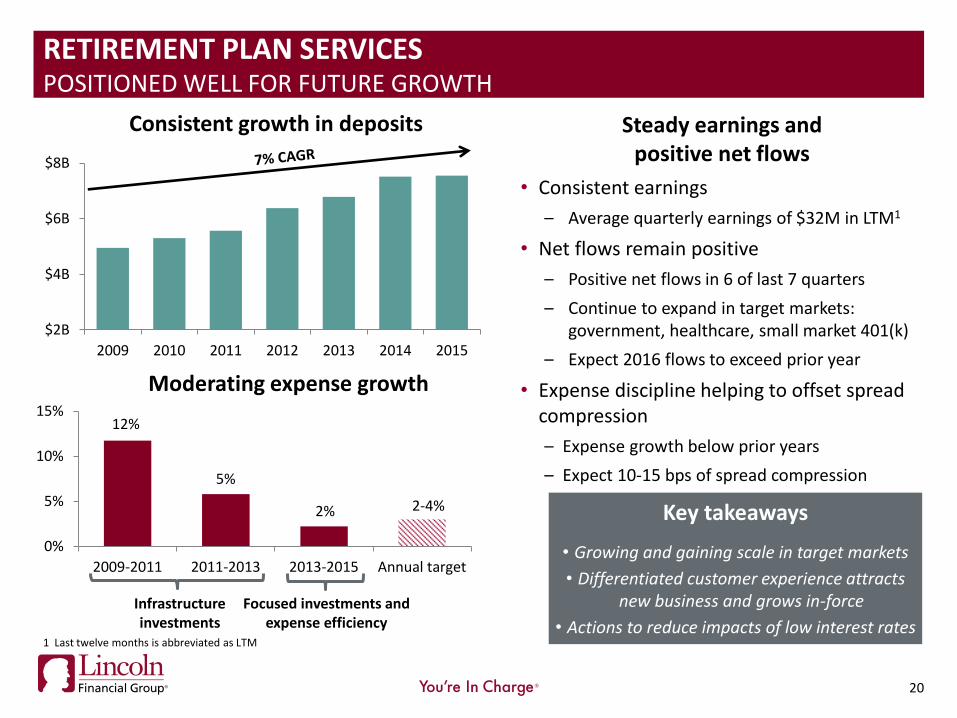

Steady earnings and positive net flows

• Consistent earnings

– Average quarterly earnings of $32M in LTM1

• Net flows remain positive

– Positive net flows in 6 of last 7 quarters

– Continue to expand in target markets: government, healthcare, small market 401(k)

– Expect 2016 flows to exceed prior year

• Expense discipline helping to offset spread compression

– Expense growth below prior years

– Expect 10-15 bps of spread compression

20

RETIREMENT PLAN SERVICES POSITIONED WELL FOR FUTURE GROWTH

Key takeaways

• Growing and gaining scale in target markets

• Differentiated customer experience attracts new business and grows in-force

• Actions to reduce impacts of low interest rates

Moderating expense growth

12%

5%

2%

0%

5%

10%

15%

2009-2011 2011-2013 2013-2015 Annual target

2-4%

Focused investments and expense efficiency

$2B

$4B

$6B

$8B

2009 2010 2011 2012 2013 2014 2015

Consistent growth in deposits

1 Last twelve months is abbreviated as LTM

Infrastructure investments

21

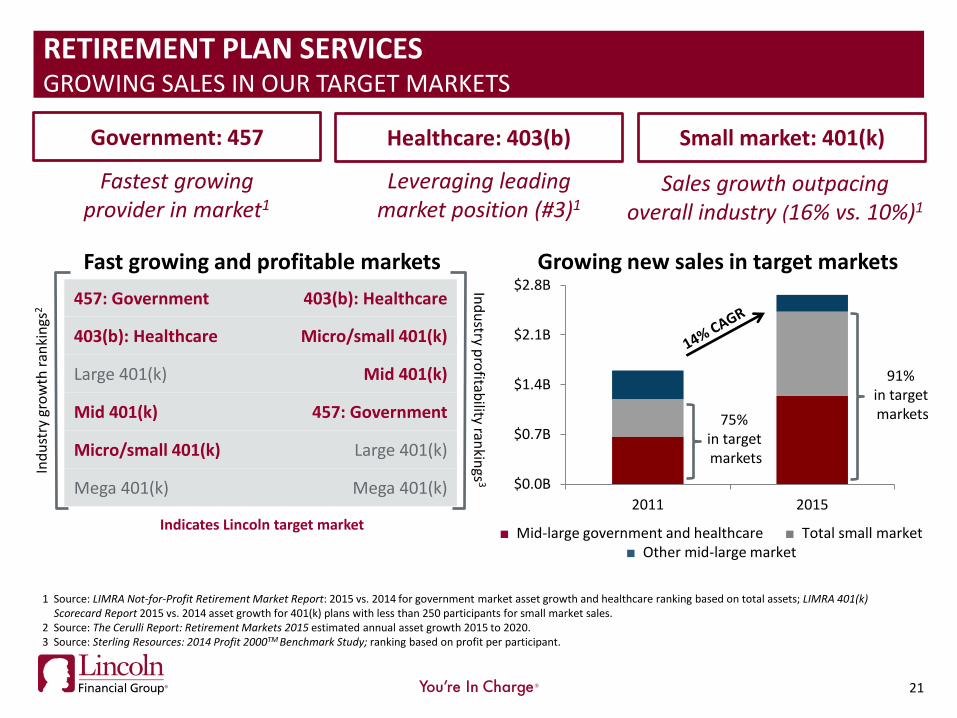

Government: 457

Healthcare: 403(b) Small market: 401(k)

Fastest growing provider in market1

Leveraging leading market position (#3)1

Sales growth outpacing overall industry (16% vs. 10%)1

21

1 Source: LIMRA Not-for-Profit Retirement Market Report: 2015 vs. 2014 for government market asset growth and healthcare ranking based on total assets; LIMRA 401(k) Scorecard Report 2015 vs. 2014 asset growth for 401(k) plans with less than 250 participants for small market sales.

2 Source: The Cerulli Report: Retirement Markets 2015 estimated annual asset growth 2015 to 2020. 3 Source: Sterling Resources: 2014 Profit 2000TM Benchmark Study; ranking based on profit per participant.

$0.0B

$0.7B

$1.4B

$2.1B

$2.8B

2011 2015

Growing new sales in target markets

■ Mid-large government and healthcare ■ Total small market ■ Other mid-large market

91% in target markets 75%

in target markets

Ind

ust

ry g

row

th r

anki

ngs

2

Ind

ustry p

rofitab

ility rankin

gs3

Fast growing and profitable markets

457: Government 403(b): Healthcare

403(b): Healthcare Micro/small 401(k)

Large 401(k) Mid 401(k)

Mid 401(k) 457: Government

Micro/small 401(k) Large 401(k)

Mega 401(k) Mega 401(k)

Indicates Lincoln target market

RETIREMENT PLAN SERVICES GROWING SALES IN OUR TARGET MARKETS

22

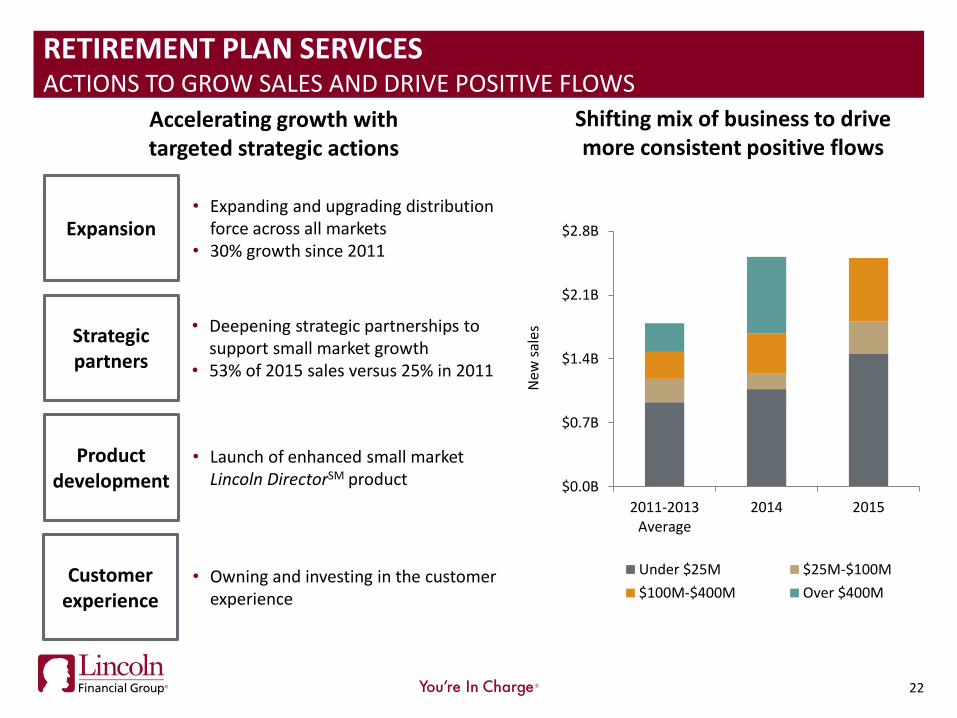

Shifting mix of business to drive more consistent positive flows

Accelerating growth with targeted strategic actions

Expansion

Strategic partners

Product development

Customer experience

• Expanding and upgrading distribution force across all markets

• 30% growth since 2011

• Deepening strategic partnerships to support small market growth

• 53% of 2015 sales versus 25% in 2011

• Launch of enhanced small market Lincoln DirectorSM product

• Owning and investing in the customer experience

$0.0B

$0.7B

$1.4B

$2.1B

$2.8B

2011-2013Average

2014 2015

New

sal

es

Under $25M $25M-$100M

$100M-$400M Over $400M

RETIREMENT PLAN SERVICES ACTIONS TO GROW SALES AND DRIVE POSITIVE FLOWS

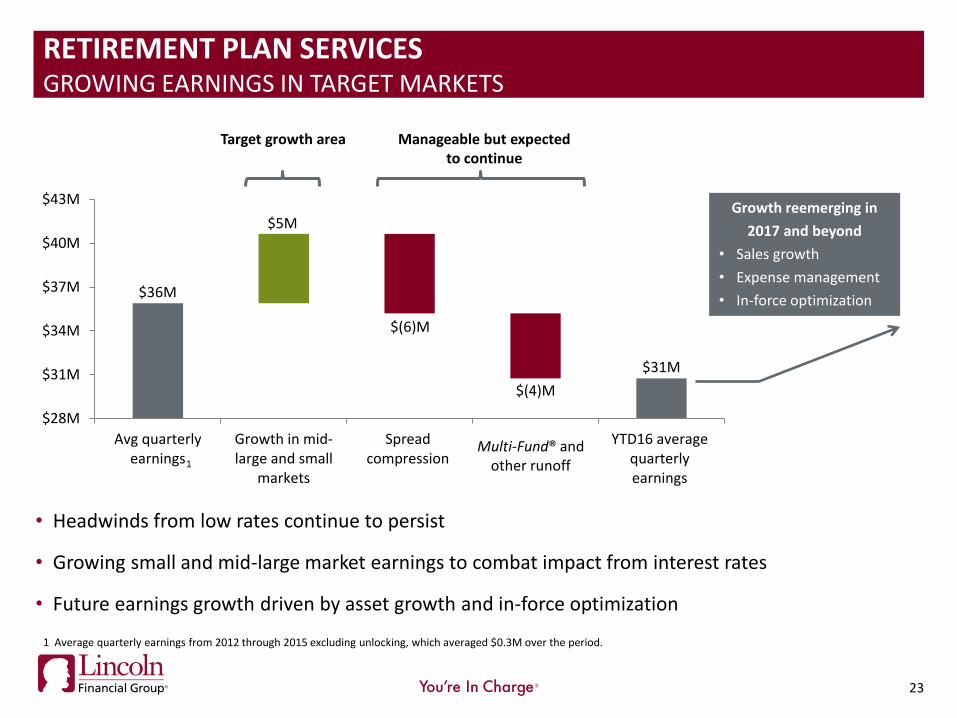

$36M

$31M

$5M

$(6)M

$(4)M

$28M

$31M

$34M

$37M

$40M

$43M

Avg quarterlyearnings

Growth in mid-large and small

markets

Spreadcompression

Multi-Fund® andOther Run-off

YTD16 averagequarterlyearnings

23

RETIREMENT PLAN SERVICES GROWING EARNINGS IN TARGET MARKETS

• Headwinds from low rates continue to persist

• Growing small and mid-large market earnings to combat impact from interest rates

• Future earnings growth driven by asset growth and in-force optimization

Multi-Fund® and other runoff

1 Average quarterly earnings from 2012 through 2015 excluding unlocking, which averaged $0.3M over the period.

Target growth area Manageable but expected to continue

Growth reemerging in

2017 and beyond

• Sales growth

• Expense management

• In-force optimization

1

LIFE INSURANCE

24

2016 YTD

Tilt to products without long-term guarantees 2015 YTD

25

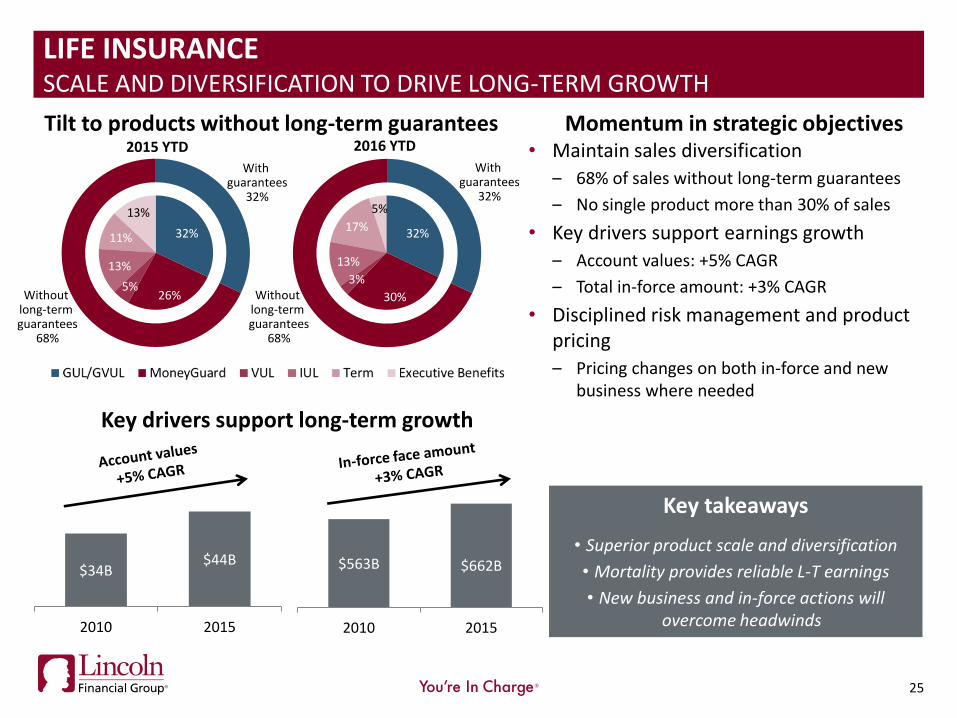

LIFE INSURANCE SCALE AND DIVERSIFICATION TO DRIVE LONG-TERM GROWTH

Momentum in strategic objectives • Maintain sales diversification

– 68% of sales without long-term guarantees

– No single product more than 30% of sales

• Key drivers support earnings growth

– Account values: +5% CAGR

– Total in-force amount: +3% CAGR

• Disciplined risk management and product pricing

– Pricing changes on both in-force and new business where needed

With guarantees

32%

32%

30%

3%

13%

17%

5%

Without long-term guarantees

68%

With guarantees

32%

Without long-term guarantees

68%

Key takeaways

• Superior product scale and diversification

• Mortality provides reliable L-T earnings

• New business and in-force actions will overcome headwinds

$34B $44B

2010 2015

$563B

$662B

2010 2015

Key drivers support long-term growth

32%

26% 5%

13%

11%

13%

10

9

8

7

6

5

4

Lincoln

2

1

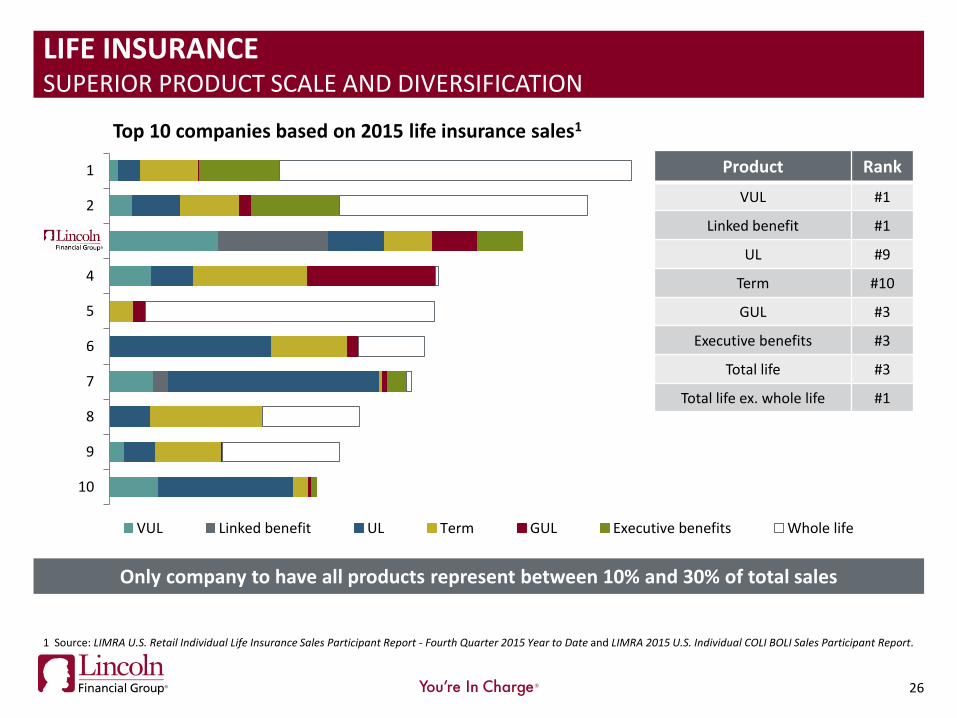

Top 10 companies based on 2015 life insurance sales1

VUL Linked benefit UL Term GUL Executive benefits Whole life

Only company to have all products represent between 10% and 30% of total sales

26

Product Rank

VUL #1

Linked benefit #1

UL #9

Term #10

GUL #3

Executive benefits #3

Total life #3

Total life ex. whole life #1

1 Source: LIMRA U.S. Retail Individual Life Insurance Sales Participant Report - Fourth Quarter 2015 Year to Date and LIMRA 2015 U.S. Individual COLI BOLI Sales Participant Report.

LIFE INSURANCE SUPERIOR PRODUCT SCALE AND DIVERSIFICATION

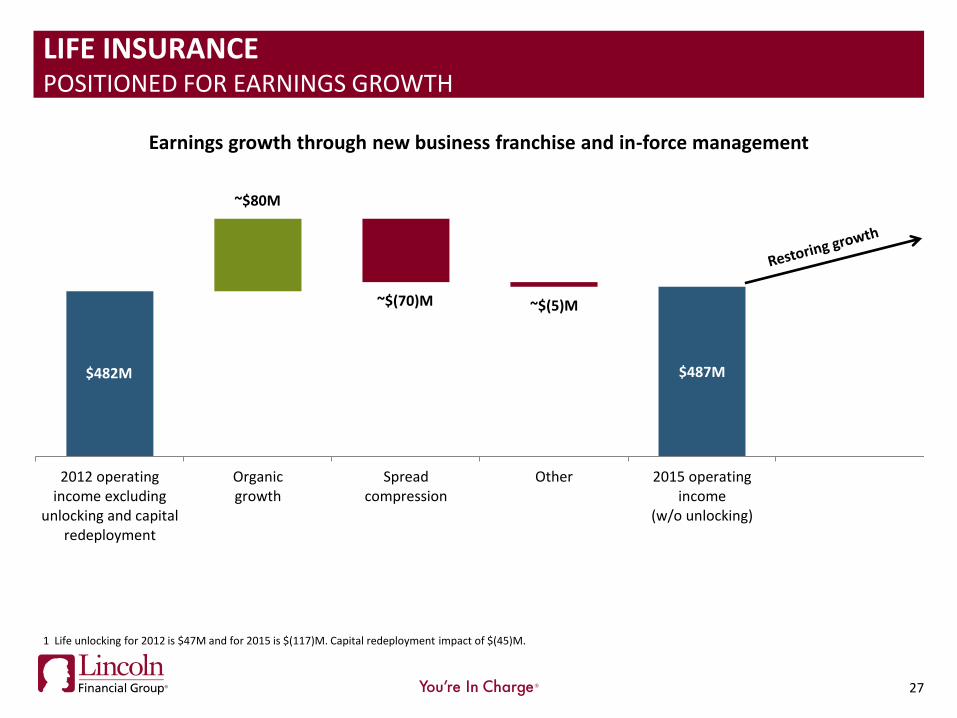

$487M

2012 operatingincome excluding

unlocking and capitalredeployment

Organicgrowth

Spreadcompression

Other 2015 operatingincome

(w/o unlocking)

27

LIFE INSURANCE POSITIONED FOR EARNINGS GROWTH

~$80M

~$(70)M ~$(5)M

Earnings growth through new business franchise and in-force management

1 Life unlocking for 2012 is $47M and for 2015 is $(117)M. Capital redeployment impact of $(45)M.

$482M

GROUP PROTECTION

28

55%

60%

65%

70%

75%

80%

85%

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

Non-medical LR TTM Non-medical LR

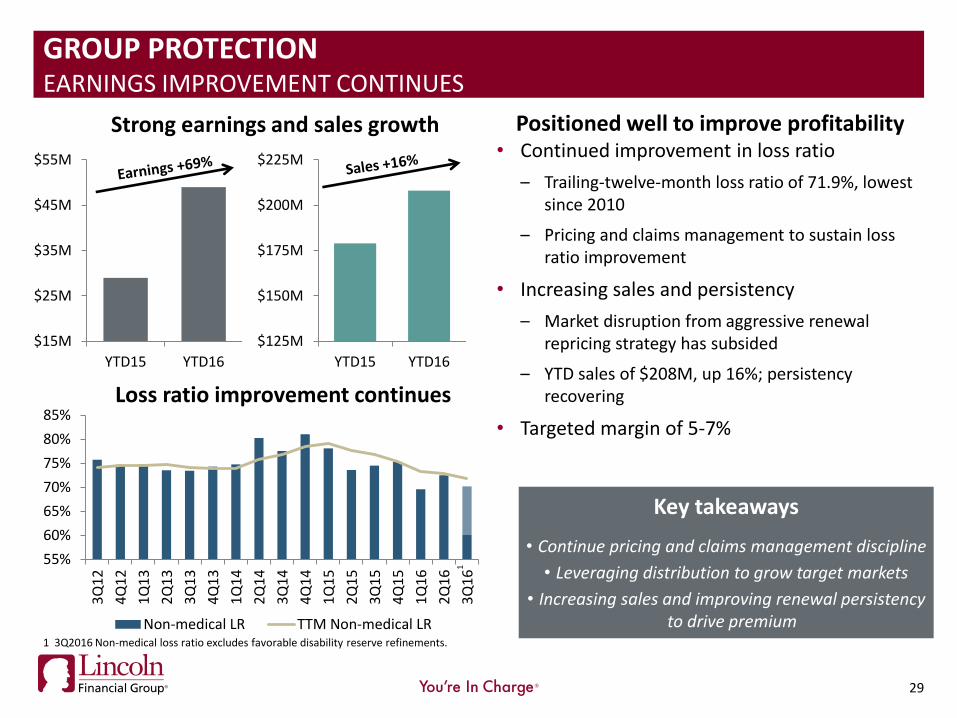

Positioned well to improve profitability • Continued improvement in loss ratio

– Trailing-twelve-month loss ratio of 71.9%, lowest since 2010

– Pricing and claims management to sustain loss ratio improvement

• Increasing sales and persistency

– Market disruption from aggressive renewal repricing strategy has subsided

– YTD sales of $208M, up 16%; persistency recovering

• Targeted margin of 5-7%

29

GROUP PROTECTION EARNINGS IMPROVEMENT CONTINUES

Strong earnings and sales growth

Loss ratio improvement continues

$15M

$25M

$35M

$45M

$55M

YTD15 YTD16

Key takeaways

• Continue pricing and claims management discipline

• Leveraging distribution to grow target markets

• Increasing sales and improving renewal persistency to drive premium

$125M

$150M

$175M

$200M

$225M

YTD15 YTD16

1 3Q2016 Non-medical loss ratio excludes favorable disability reserve refinements.

1

30

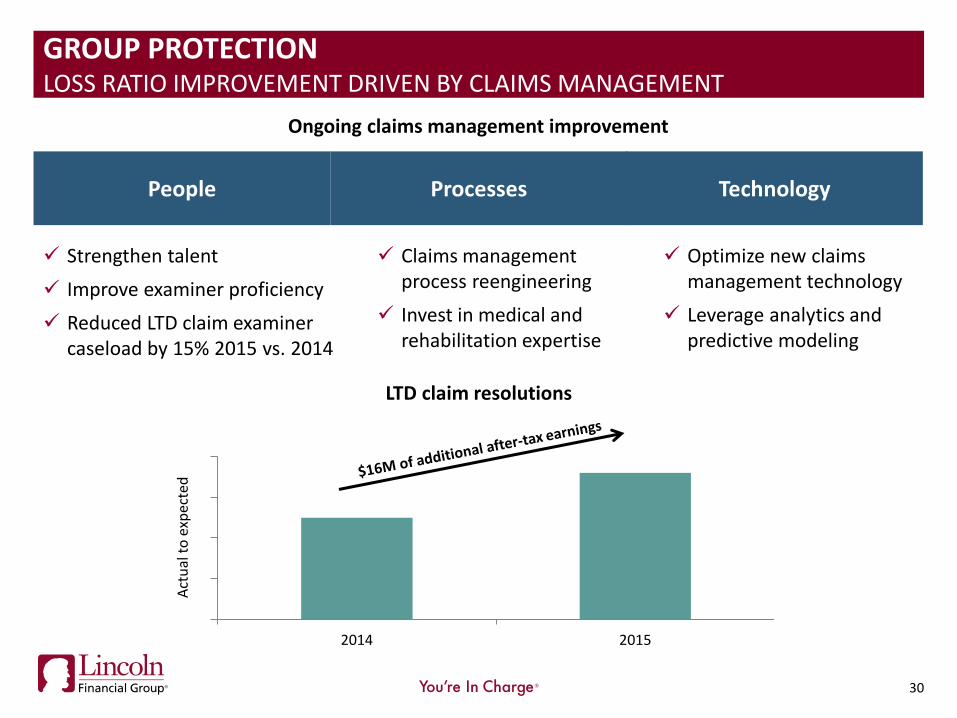

GROUP PROTECTION LOSS RATIO IMPROVEMENT DRIVEN BY CLAIMS MANAGEMENT

Optimize new claims management technology

Leverage analytics and predictive modeling

Strengthen talent

Improve examiner proficiency

Reduced LTD claim examiner caseload by 15% 2015 vs. 2014

Claims management process reengineering

Invest in medical and rehabilitation expertise

Technology People Processes

Ongoing claims management improvement

120%

130%

140%

150%

160%

2014 2015

Act

ual

to

exp

ecte

d

LTD claim resolutions

31

Consumer marketing

Data and analytics

Education and advice

Customer buying experience

Service delivery

Onboarding process and data exchange

Selling and renewal processes

Value added services – absence management

+29

+1

0

10

20

30

LNC Peers2

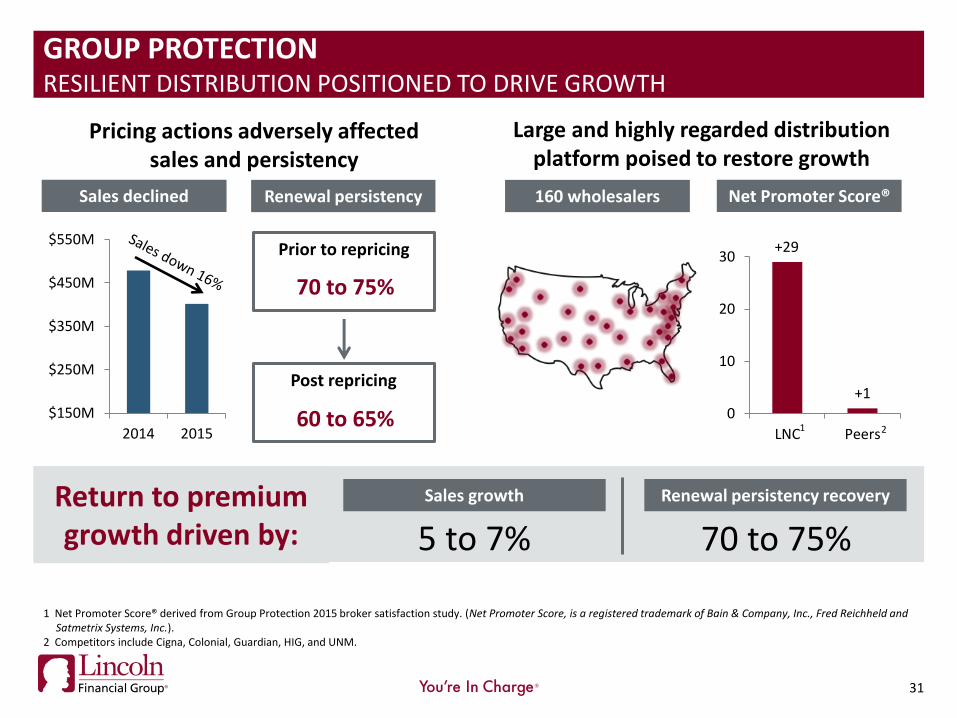

Pricing actions adversely affected sales and persistency

Large and highly regarded distribution platform poised to restore growth

1

5 to 7%

Sales growth Renewal persistency recovery

70 to 75%

Return to premium growth driven by:

$150M

$250M

$350M

$450M

$550M

2014 2015

Sales declined Renewal persistency

Prior to repricing

70 to 75%

Post repricing

60 to 65%

160 wholesalers Net Promoter Score®

1 Net Promoter Score® derived from Group Protection 2015 broker satisfaction study. (Net Promoter Score, is a registered trademark of Bain & Company, Inc., Fred Reichheld and Satmetrix Systems, Inc.).

2 Competitors include Cigna, Colonial, Guardian, HIG, and UNM.

GROUP PROTECTION RESILIENT DISTRIBUTION POSITIONED TO DRIVE GROWTH

APPENDIX

32

33

33

FORWARD LOOKING STATEMENTS – CAUTIONARY LANGUAGE Certain statements made in this presentation and in other written or oral statements made by Lincoln or on Lincoln's behalf are "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995 (PSLRA). A forward-looking statement is a statement that is not a historical fact and, without limitation, includes any statement that may predict, forecast, indicate or imply future results, performance or achievements, and may contain words like: "believe," "anticipate," "expect," "estimate," "project," "will," "shall" and other words or phrases with similar meaning in connection with a discussion of future operating or financial performance. In particular, these include statements relating to future actions, trends in Lincoln's businesses, prospective services or products, future performance or financial results, and the outcome of contingencies, such as legal proceedings. Lincoln claims the protection afforded by the safe harbor for forward-looking statements provided by the PSLRA.

Forward-looking statements involve risks and uncertainties that may cause actual results to differ materially from the results contained in the forward-looking statements. Risks and uncertainties that may cause actual results to vary materially, some of which are described within the forward-looking statements include, among others:

• Deterioration in general economic and business conditions that may affect account values, investment results, guaranteed benefit liabilities, premium levels, claims experience and the level of pension benefit costs, funding and investment results;

• Adverse global capital and credit market conditions could affect our ability to raise capital, if necessary, and may cause us to realize impairments on investments and certain intangible assets, including goodwill and the valuation allowance against deferred tax assets, which may reduce future earnings and/or affect our financial condition and ability to raise additional capital or refinance existing debt as it matures;

• Because of our holding company structure, the inability of our subsidiaries to pay dividends to the holding company in sufficient amounts could harm the holding company’s ability to meet its obligations;

• Legislative, regulatory or tax changes, both domestic and foreign, that affect: the cost of, or demand for, our subsidiaries' products; the required amount of reserves and/or surplus; our ability to conduct business and our captive reinsurance arrangements as well as restrictions on revenue sharing and 12b-1 payments; and the potential for U.S. federal tax reform and the effect of the Department of Labor’s regulation defining fiduciary;

• Actions taken by reinsurers to raise rates on in-force business;

• Declines in or sustained low interest rates causing a reduction in investment income, the interest margins of our businesses, estimated gross profits and demand for our products;

• Rapidly increasing interest rates causing contract holders to surrender life insurance and annuity policies, thereby causing realized investment losses, and reduced hedge performance related to variable annuities;

34

34

FORWARD LOOKING STATEMENTS – CAUTIONARY LANGUAGE (CONT.)

• Uncertainty about the effect of rules and regulations to be promulgated under the Dodd-Frank Wall Street Reform and Consumer Protection Act on us and the economy, and financial services sector in particular;

• The initiation of legal or regulatory proceedings against us, and the outcome of any legal or regulatory proceedings, such as: adverse actions related to present or past business practices common in businesses in which we compete; adverse decisions in significant actions including, but not limited to, actions brought by federal and state authorities and class action cases; new decisions that result in changes in law; and unexpected trial court rulings;

• A decline in the equity markets causing a reduction in the sales of our subsidiaries' products; a reduction of asset-based fees that our subsidiaries charge on various investment and insurance products; an acceleration of the net amortization of deferred acquisition costs, or "DAC;" value of business acquired, or "VOBA;" deferred sales inducements, or "DSI;" and deferred front end sales loads, or "DFEL;" and an increase in liabilities related to guaranteed benefit features of our subsidiaries' variable annuity products;

• Ineffectiveness of our risk management policies and procedures, including various hedging strategies used to offset the effect of changes in the value of liabilities due to changes in the level and volatility of the equity markets and interest rates;

• A deviation in actual experience regarding future persistency, mortality, morbidity, interest rates or equity market returns from the assumptions used in pricing our subsidiaries' products, in establishing related insurance reserves and in the net amortization of DAC, VOBA, DSI and DFEL, which may reduce future earnings;

• Changes in accounting principles generally accepted in the United States, or "GAAP," including convergence with International Financial Reporting Standards (IFRS), that may result in unanticipated changes to our net income;

• Lowering of one or more of our debt ratings issued by nationally recognized statistical rating organizations and the adverse effect such action may have on our ability to raise capital and on our liquidity and financial condition;

• Lowering of one or more of the insurer financial strength ratings of our insurance subsidiaries and the adverse effect such action may have on the premium writings, policy retention, profitability of our insurance subsidiaries and liquidity;

• Significant credit, accounting, fraud, corporate governance or other issues that may adversely affect the value of certain investments in our portfolios as well as counterparties to which we are exposed to credit risk requiring that we realize losses on investments;

• Inability to protect our intellectual property rights or claims of infringement of the intellectual property rights of others;

• Interruption in telecommunication, information technology or other operational systems, or failure to safeguard the confidentiality or privacy of sensitive data on such systems from cyberattacks or other breaches of our data security systems;

35

• The effect of acquisitions and divestitures, restructurings, product withdrawals and other unusual items;

• The adequacy and collectability of reinsurance that we have purchased;

• Acts of terrorism, a pandemic, war or other man-made and natural catastrophes that may adversely affect our businesses and the cost and availability of reinsurance;

• Competitive conditions, including pricing pressures, new product offerings and the emergence of new competitors, that may affect the level of premiums and fees that our subsidiaries can charge for their products;

• The unknown effect on our subsidiaries' businesses resulting from changes in the demographics of their client base, as aging baby-boomers move from the asset-accumulation stage to the asset-distribution stage of life; and

• Loss of key management, financial planners or wholesalers.

The risks included here are not exhaustive. Our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and other documents filed with the SEC include additional factors which could impact our business and financial performance. Moreover, we operate in a rapidly changing and competitive environment. New risk factors emerge from time to time, and it is not possible for management to predict all such risk factors.

Further, it is not possible to assess the impact of all risk factors on our businesses or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. Given these risks and uncertainties, investors should not place undue reliance on forward-looking statements as a prediction of actual results. In addition, Lincoln disclaims any obligation to update any forward-looking statements to reflect events or circumstances that occur after the date of this presentation.

The reporting of RBC measures is not intended for the purpose of ranking any insurance company or for use in connection with any marketing, advertising or promotional activities.

FORWARD LOOKING STATEMENTS – CAUTIONARY LANGUAGE (CONT.)

36

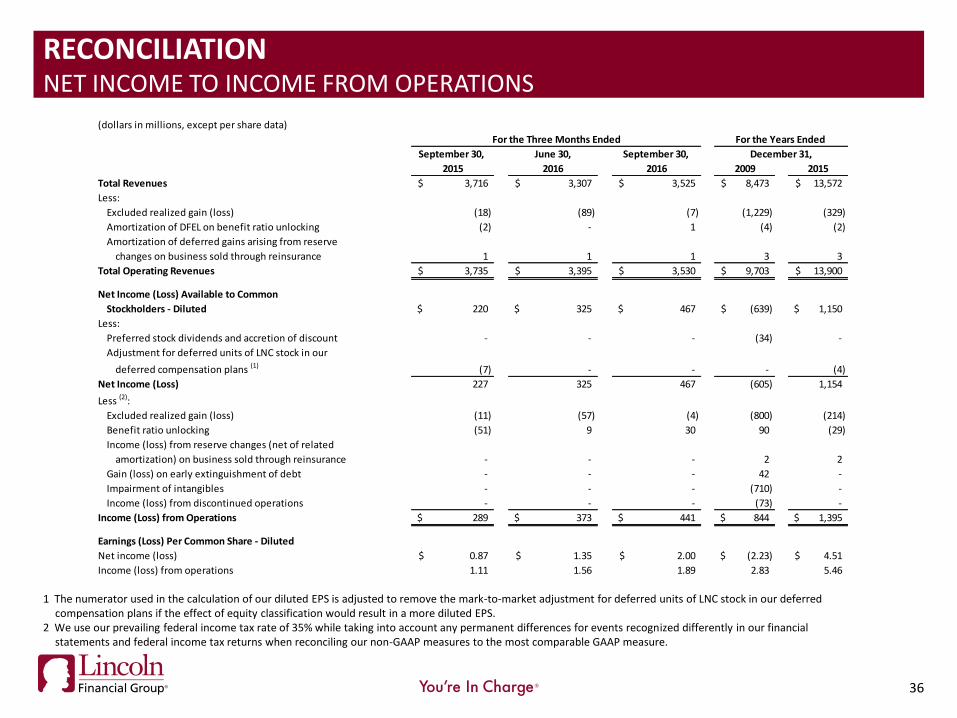

RECONCILIATION NET INCOME TO INCOME FROM OPERATIONS

1 The numerator used in the calculation of our diluted EPS is adjusted to remove the mark-to-market adjustment for deferred units of LNC stock in our deferred compensation plans if the effect of equity classification would result in a more diluted EPS.

2 We use our prevailing federal income tax rate of 35% while taking into account any permanent differences for events recognized differently in our financial statements and federal income tax returns when reconciling our non-GAAP measures to the most comparable GAAP measure.

(dollars in millions, except per share data)

September 30, June 30, September 30,

2015 2016 2016 2009 2015

Total Revenues 3,716$ 3,307$ 3,525$ 8,473$ 13,572$

Less:

Excluded realized gain (loss) (18) (89) (7) (1,229) (329)

Amortization of DFEL on benefit ratio unlocking (2) - 1 (4) (2)

Amortization of deferred gains arising from reserve

changes on business sold through reinsurance 1 1 1 3 3

Total Operating Revenues 3,735$ 3,395$ 3,530$ 9,703$ 13,900$

Net Income (Loss) Available to Common

Stockholders - Diluted 220$ 325$ 467$ (639)$ 1,150$

Less:

Preferred stock dividends and accretion of discount - - - (34) -

Adjustment for deferred units of LNC stock in our

deferred compensation plans (1) (7) - - - (4)

Net Income (Loss) 227 325 467 (605) 1,154

Less (2):

Excluded realized gain (loss) (11) (57) (4) (800) (214)

Benefit ratio unlocking (51) 9 30 90 (29)

Income (loss) from reserve changes (net of related

amortization) on business sold through reinsurance - - - 2 2

Gain (loss) on early extinguishment of debt - - - 42 -

Impairment of intangibles - - - (710) -

Income (loss) from discontinued operations - - - (73) -

Income (Loss) from Operations 289$ 373$ 441$ 844$ 1,395$

Earnings (Loss) Per Common Share - Diluted

Net income (loss) 0.87$ 1.35$ 2.00$ (2.23)$ 4.51$

Income (loss) from operations 1.11 1.56 1.89 2.83 5.46

For the Three Months Ended

December 31,

For the Years Ended

37

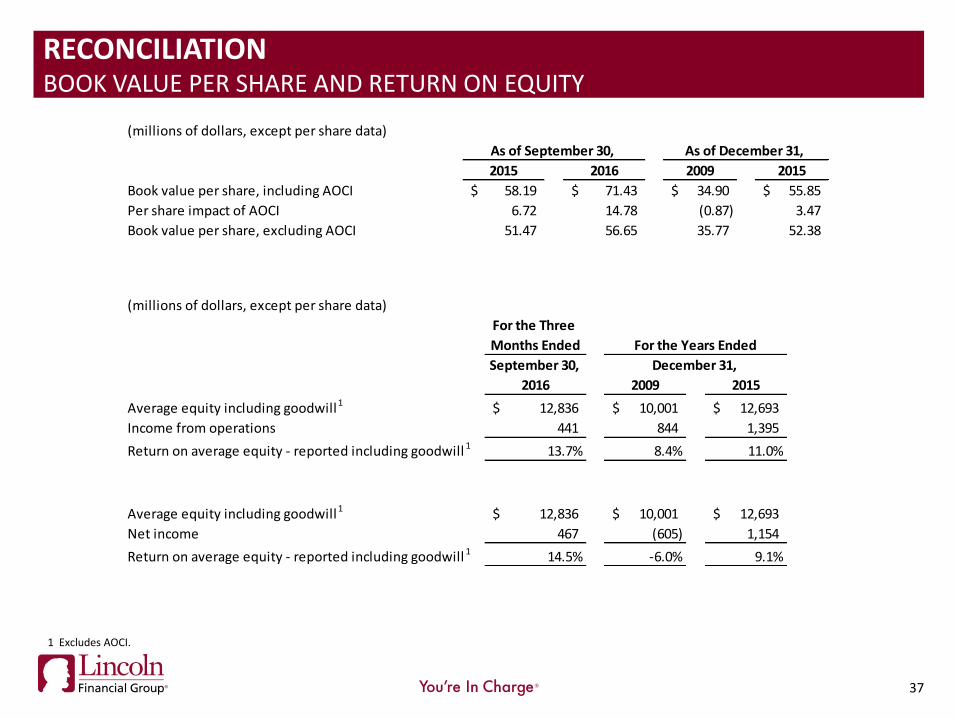

RECONCILIATION BOOK VALUE PER SHARE AND RETURN ON EQUITY

1 Excludes AOCI.

(millions of dollars, except per share data)

2015 2016 2009 2015

Book value per share, including AOCI 58.19$ 71.43$ 34.90$ 55.85$

Per share impact of AOCI 6.72 14.78 (0.87) 3.47

Book value per share, excluding AOCI 51.47 56.65 35.77 52.38

As of December 31, As of September 30,

(millions of dollars, except per share data)

For the Three

Months Ended

September 30,

2016 2009 2015

Average equity including goodwill1 12,836$ 10,001$ 12,693$

Income from operations 441 844 1,395

Return on average equity - reported including goodwill 1 13.7% 8.4% 11.0%

Average equity including goodwill1 12,836$ 10,001$ 12,693$

Net income 467 (605) 1,154

Return on average equity - reported including goodwill 1 14.5% -6.0% 9.1%

December 31,

For the Years Ended

38

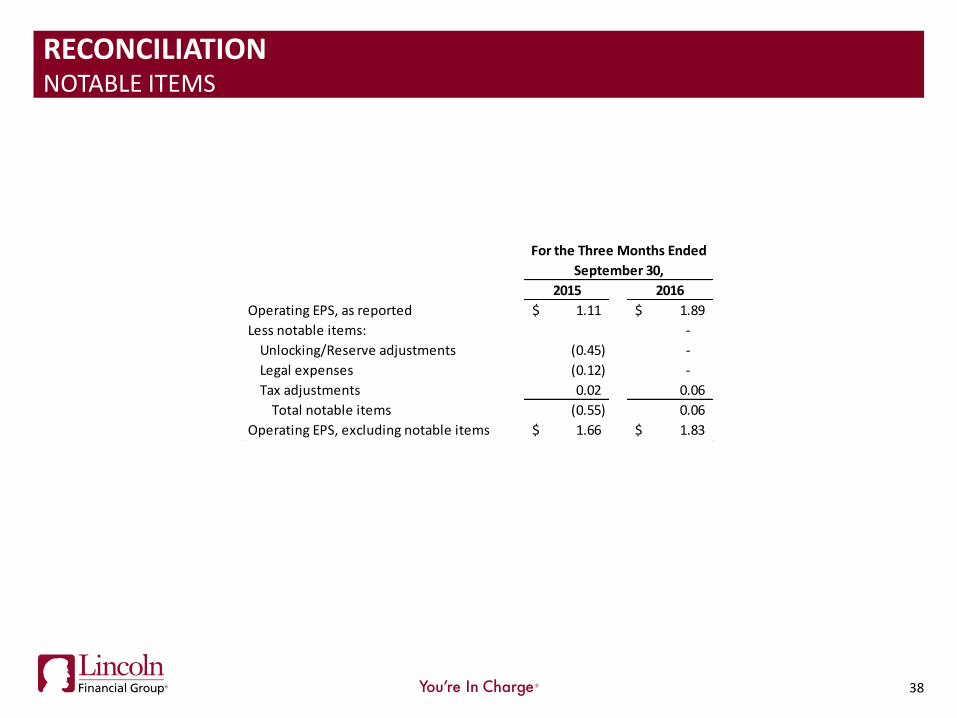

RECONCILIATION NOTABLE ITEMS

September 30,

2015 2016

Operating EPS, as reported 1.11$ 1.89$

Less notable items: -

Unlocking/Reserve adjustments (0.45) -

Legal expenses (0.12) -

Tax adjustments 0.02 0.06

Total notable items (0.55) 0.06

Operating EPS, excluding notable items 1.66$ 1.83$

For the Three Months Ended

39

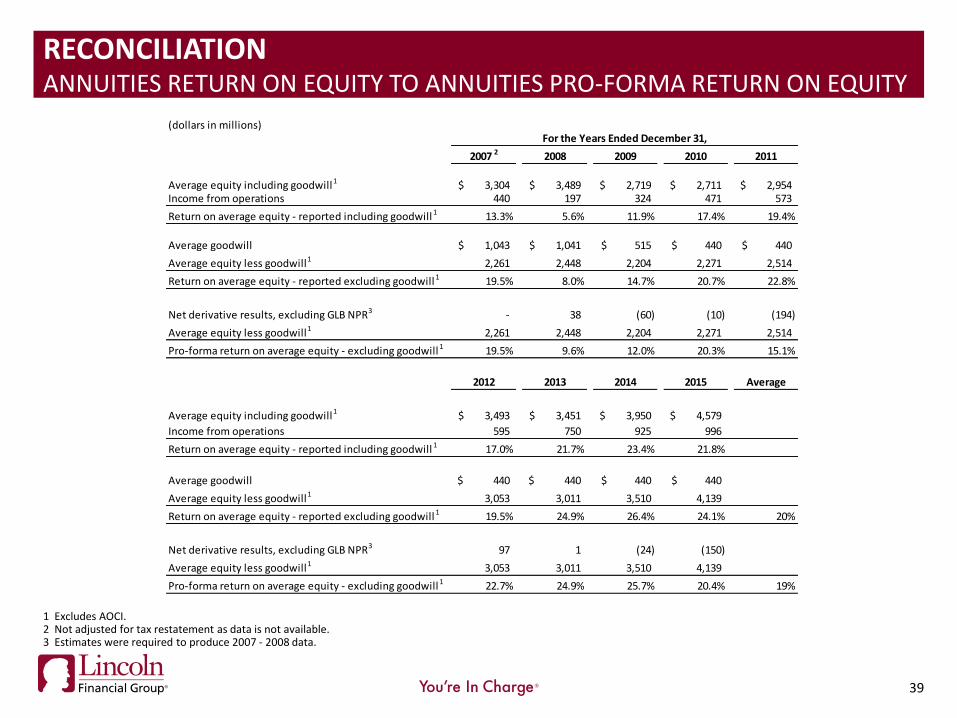

RECONCILIATION ANNUITIES RETURN ON EQUITY TO ANNUITIES PRO-FORMA RETURN ON EQUITY

1 Excludes AOCI. 2 Not adjusted for tax restatement as data is not available. 3 Estimates were required to produce 2007 - 2008 data.

(dollars in millions)

2007 2 2008 2009 2010 2011

Average equity including goodwill1 3,304$ 3,489$ 2,719$ 2,711$ 2,954$ Income from operations 440 197 324 471 573

Return on average equity - reported including goodwill1 13.3% 5.6% 11.9% 17.4% 19.4%

Average goodwill 1,043$ 1,041$ 515$ 440$ 440$

Average equity less goodwill1 2,261 2,448 2,204 2,271 2,514

Return on average equity - reported excluding goodwill1 19.5% 8.0% 14.7% 20.7% 22.8%

Net derivative results, excluding GLB NPR3 - 38 (60) (10) (194)

Average equity less goodwill1 2,261 2,448 2,204 2,271 2,514

Pro-forma return on average equity - excluding goodwill1 19.5% 9.6% 12.0% 20.3% 15.1%

2012 2013 2014 2015 Average

Average equity including goodwill1 3,493$ 3,451$ 3,950$ 4,579$

Income from operations 595 750 925 996

Return on average equity - reported including goodwill1 17.0% 21.7% 23.4% 21.8%

Average goodwill 440$ 440$ 440$ 440$

Average equity less goodwill1 3,053 3,011 3,510 4,139

Return on average equity - reported excluding goodwill1 19.5% 24.9% 26.4% 24.1% 20%

Net derivative results, excluding GLB NPR3 97 1 (24) (150)

Average equity less goodwill1 3,053 3,011 3,510 4,139

Pro-forma return on average equity - excluding goodwill1 22.7% 24.9% 25.7% 20.4% 19%

For the Years Ended December 31,