Embed Size (px)

Citation preview

1

Goldman Sachs Global Energy Conference

January 2017

2

Forward-Looking Statements

Statements contained in this press release that are not historical facts are forward-looking statements within the meaning

of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Forward-looking

statements include words or phrases such as “anticipate,” “believe,” “estimate,” “expect,” “intend,” “plan,” “project,”

“could,” “may,” “might,” “should,” “will” and similar words and specifically include statements involving expected financial

performance, effective tax rate, expected expense savings, day rates and backlog, estimated rig availability; rig

commitments and contracts; contract duration, status, terms and other contract commitments; estimated capital

expenditures; letters of intent or letters of award; scheduled delivery dates for rigs; the timing of delivery, mobilization,

contract commencement, relocation or other movement of rigs; our intent to sell or scrap rigs; and general market,

business and industry conditions, trends and outlook. Such statements are subject to numerous risks, uncertainties and

assumptions that may cause actual results to vary materially from those indicated, including commodity price

fluctuations, customer demand, new rig supply, downtime and other risks associated with offshore rig operations,

relocations, severe weather or hurricanes; changes in worldwide rig supply and demand, competition and technology;

future levels of offshore drilling activity; governmental action, civil unrest and political and economic uncertainties;

terrorism, piracy and military action; risks inherent to shipyard rig construction, repair, maintenance or enhancement;

possible cancellation, suspension or termination of drilling contracts as a result of mechanical difficulties, performance,

customer finances, the decline or the perceived risk of a further decline in oil and/or natural gas prices, or other reasons,

including terminations for convenience (without cause); the cancellation of letters of intent or letters of award or any

failure to execute definitive contracts following announcements of letters of intent or letters of award; the outcome of

litigation, legal proceedings, investigations or other claims or contract disputes; governmental regulatory, legislative and

permitting requirements affecting drilling operations; our ability to attract and retain skilled personnel on commercially

reasonable terms; environmental or other liabilities, risks or losses; debt restrictions that may limit our liquidity and

flexibility; our ability to realize the expected benefits from our redomestication and actual contract commencement dates;

tax matters including our effective tax rate; cybersecurity risks and threats; and the occurrence or threat of epidemic or

pandemic diseases or any governmental response to such occurrence or threat. In addition to the numerous factors

described above, you should also carefully read and consider “Item 1A. Risk Factors” in Part I and “Item 7.

Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Part II of our most recent

annual report on Form 10-K, as updated in our subsequent quarterly reports on Form 10-Q, which are available on the

SEC’s website at www.sec.gov or on the Investor Relations section of our website at www.enscoplc.com. Each forward-

looking statement speaks only as of the date of the particular statement, and we undertake no obligation to publicly

update or revise any forward-looking statements, except as required by law.

3

Executive Summary

• Positive medium-/long-term outlook for offshore market

• Ensco is well positioned to capitalize on future recovery

• Strong record of proactive capital, fleet and expense management

• Record operational utilization and safety performance

• #1 customer satisfaction – six consecutive years (EnergyPoint Research Inc.)

• Among highest net income/revenue margins

• High-quality rig fleet that leverages standardization

• Global presence and large/diverse customer base

4

Agenda

• Market Conditions

• Decisive actions to persevere through the downturn

– capital & expense management

– fleet restructuring

– investments in engineering and innovation to improve operational &

safety performance

• Outlook for offshore drilling

– efficiency & cost improvements

– attrition of older rigs & deferral/cancellation of newbuild deliveries

– catalyst markets

5

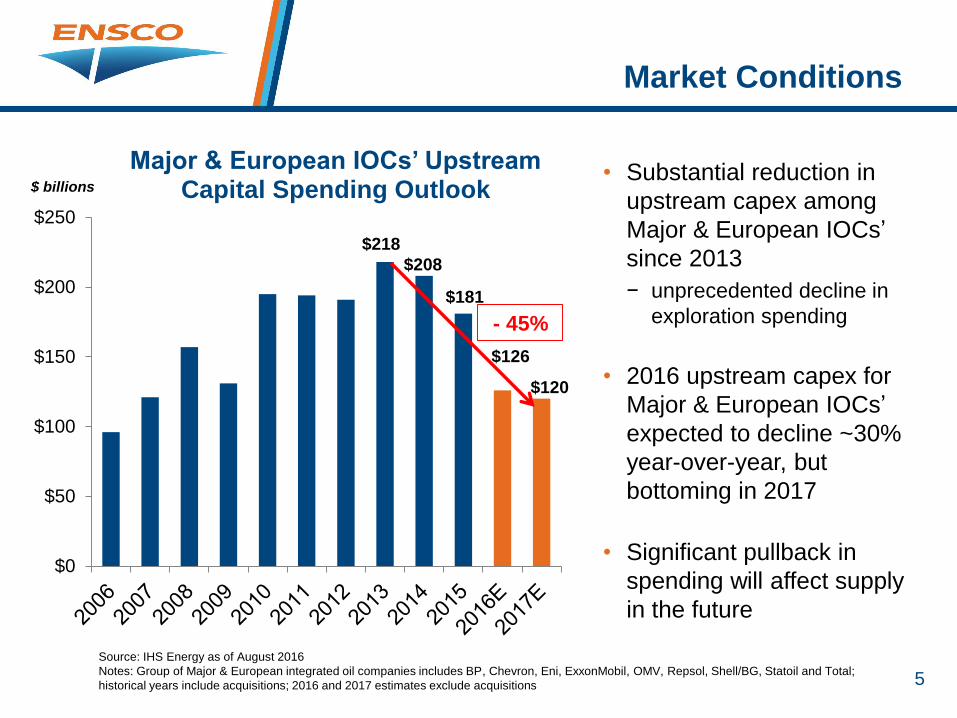

$218

$208

$181

$126

$120

$0

$50

$100

$150

$200

$250

$ billions

Major & European IOCs’ Upstream Capital Spending Outlook

Market Conditions

Source: IHS Energy as of August 2016

Notes: Group of Major & European integrated oil companies includes BP, Chevron, Eni, ExxonMobil, OMV, Repsol, Shell/BG, Statoil and Total;

historical years include acquisitions; 2016 and 2017 estimates exclude acquisitions

• Substantial reduction in

upstream capex among

Major & European IOCs’

since 2013

− unprecedented decline in

exploration spending

• 2016 upstream capex for

Major & European IOCs’

expected to decline ~30%

year-over-year, but

bottoming in 2017

• Significant pullback in

spending will affect supply

in the future

- 45%

6

• Capital management

• Expense management

• Fleet restructuring

• Investments to improve

operational & safety

performance

– engineering & innovation

– process improvements

Decisive

Actions To

Persevere

Through The

Downturn

7

• Accessed the debt markets initially to bolster liquidity and refinance ‘near-term’ debt maturities: $1.25 billion raised in 2014 and $1.1 billion raised in 2015

• Raised equity in April 2016 to further enhance liquidity position

• Increased revolver to $2.25 billion and extended to September 2019; then extended maturity of $1.13 billion of revolver commitments by one year to September 2020

• Reduced capital expenditures and dividend to preserve cash

• Delayed delivery of newbuilds to postpone final milestone payments

• Recently refinanced ‘medium-term’ debt maturities to further improve financial flexibility

• Significantly reduced leverage

Proactive Capital Management

8

Benefits of Capital Management

Actions Through 3Q16

Note: Net debt is a non-GAAP financial measure defined as long-term debt less cash and short-term investments. Non-GAAP financial measures should

be considered as a supplement to, and not as a substitute for, or superior to, financial measures prepared in accordance with GAAP. 4Q15 net debt-to-

capital is calculated as follows: long-term debt of $5.9 billion, less $1.3 billion of cash and short-term investments, divided by the sum of long-term debt

of $5.9 billion plus shareholders’ equity of $6.5 billion, minus $1.3 billion of cash and short-term investments. 3Q16 net debt-to-capital is calculated as

follows: long-term debt of $4.7 billion, less $1.8 billion of cash and short-term investments, divided by the sum of long-term debt of $4.7 billion plus

shareholders’ equity of $8.0 billion, minus $1.8 billion of cash and short-term investments.

2.25 2.25

1.3

1.8

4Q15 3Q16

Liquidity

Revolver Cash + Short-term investments

$ billions

4Q15 3Q16

Net Debt-to-Capital Ratio

$3.55

$4.0541%

27%

$1.6 billion

reduction in

net debt

9

Debt Maturity Schedule: 9/30/16

$438

$681 $683$623

$669

2017 2018 2019 2020 2021 2022 2023 2024 2025 2027 2040

$300

2044

$ millions

$1,001

No debt

maturities

until 2019

$150

Note: Reflects principal amount outstanding as of September 30, 2016, as adjusted to give effect to $24.5 million aggregate principal amount of 2044

senior notes that were exchanged for 1.8 million shares on October 3, 2016.

$2.25B Revolver to Sept.

2019 then $1.13B to Sept.

2020

Recent debt raise/tender/exchange

announcements to be completed in 1Q17

10

Capital Expenditure Outlook

$70

$375

$225

4Q16E 2017E 2018E 2019E

Newbuild Capital Expenditures

New rig construction

$ millions

$0

Note: Estimates for 2016, 2017, 2018 and 2019; final capex estimates to be determined upon completion of annual budget process and subject to

change based on rig contracting; new rig construction represents contractual commitments plus anticipated capex associated with rig construction;

2017 and 2018 rig enhancements capex are estimates and not earmarked for any specific projects at this time; capex for minor upgrades and

improvements are based on the currently active fleet.

2050 50

2550

4Q16E 2017E 2018E

Other Capital Expenditures

Rig enhancements Minor upgrades & improvements

$ millions

$20

$75$100

11

2015 Actions

• 15% reduction in offshore unit labor cost

• $60+ million of annual savings from 27% reduction in onshore support

headcount

– consolidated business unit reporting structure from five to three

– centralized certain functions

• $100+ million of additional contract drilling and G&A expense savings

– repair and maintenance rate reductions and lower rig insurance premiums

– other savings through negotiated discounts with vendors

Recent Actions

• Recently instituted a lower base salary structure for new hire offshore crews

• Further streamlining organizational structure: reduced onshore support costs

and compensation expense that is expected to result in more than $50 million of

annualized cost savings per 3Q16 earnings release

Expense Management Actions

12

Strong 3Q16 Results

• Revenues exceeded initial outlook driven by record rig uptime performance

– 99% operational utilization fleet wide

– record safety statistics

• Awarded 30% of rig years contracted industrywide during 3Q16(1)

• Additional expense savings announced

– $50 million annualized savings from onshore support and compensation plans versus 2Q16 levels

• Repurchased additional $189 million of senior notes

• Extended $1.1 billion of $2.25 billion revolver by one year to September 2020

• Solid financial position at quarter end September 30, 2016:

– $3.8 billion contracted backlog

– $4.0 billion of liquidity: $1.8 billion cash and ST investments + $2.25 billion revolver

– 27% net debt-to-capital ratio(2)

(1)Source: IHS Markit RigPoint(2) Net debt is a non-GAAP financial measure. See slide 8.

13

Fleet Management Strategy

• Leverage record uptime/safety performance to negotiate extensions for contracted rigs

• Maintain warm stacked rig availability in each region in order to bid into new opportunities, examples include:

– West Africa: ENSCO DS-7

– U.S. Gulf of Mexico: ENSCO 8503, ENSCO 68 & ENSCO 87

– Asia: ENSCO DS-9, ENSCO 8504 & ENSCO 106

– Middle East: ENSCO 140/1 & ENSCO 110

– North Sea: ENSCO 120, ENSCO 121 & ENSCO 102

• Preservation stack excess high-spec rig capacity to prudently reduce expenses, yet maintain high-spec capacity that may be reactivated within 90 – 120 days

• Retire older, less capable rigs as they roll off contract as part of continuous high-grading/expense management

14

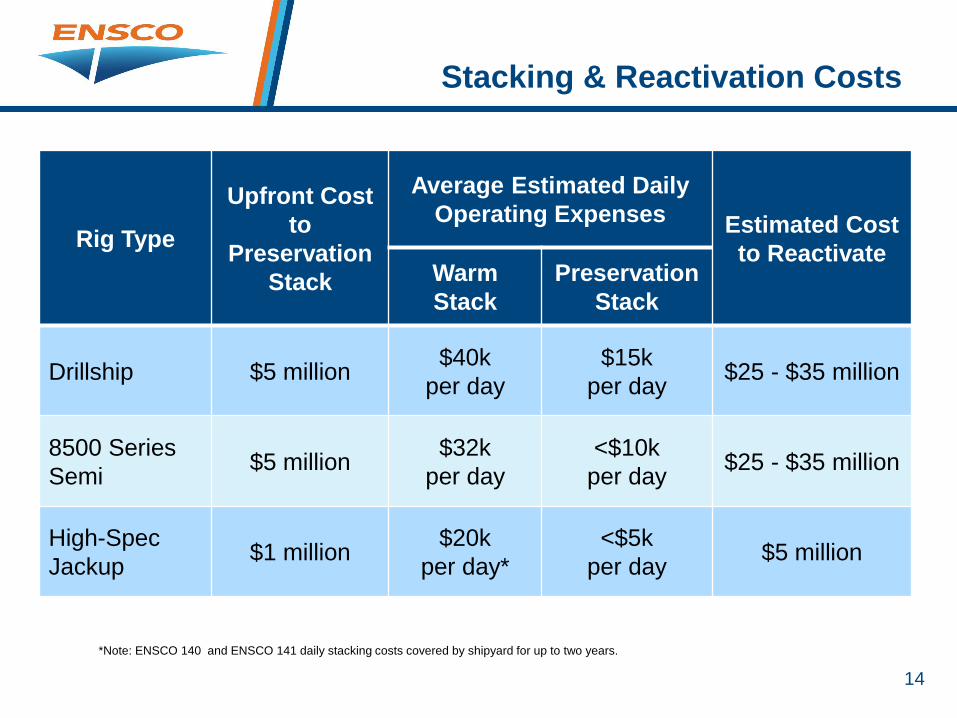

Stacking & Reactivation Costs

Rig Type

Upfront Cost

to

Preservation

Stack

Average Estimated Daily

Operating Expenses Estimated Cost

to ReactivateWarm

Stack

Preservation

Stack

Drillship $5 million$40k

per day

$15k

per day$25 - $35 million

8500 Series

Semi$5 million

$32k

per day

<$10k

per day$25 - $35 million

High-Spec

Jackup$1 million

$20k

per day*

<$5k

per day$5 million

*Note: ENSCO 140 and ENSCO 141 daily stacking costs covered by shipyard for up to two years.

15

(1) Includes ENSCO DS-10 newbuild currently scheduled for delivery in 1Q17

(2) Includes ENSCO 7500 that is expected to be retired from Ensco’s go-forward fleet

Note: adjusted for 2011 acquisition of Pride International; ultra-deepwater defined as 7500 ft. or greater

17

Fleet Restructuring: Floaters

Newbuilds(1)

Current

Fleet

Year-End

2009

Retirements

& Sales(2)

+13 -10 20

17 years Lower average fleet age

Greater drilling capabilities

10 years

4 ultra-deepwater

capable floaters

7 floaters with

15k psi BOPs

15 ultra-deepwater

capable floaters

18 floaters with

15k psi BOPsEnhanced well control

16

51

Fleet Restructuring: Jackups

Current

Fleet

Year-End

2009

+7 -26 32

6 newbuild jackups delivered

since 2013

Jackup sales since 2009 have

generated ~$600 million in

proceeds

Newbuilds(1)

Retirements

& Sales(2)

(1) Includes ENSCO 140 and ENSCO 141 newbuilds that were delivered in August and November 2016, respectively, and ENSCO 123 with

scheduled delivery of 1Q18.

(2) Includes ENSCO 56, ENSCO 81, ENSCO 82, ENSCO 86, ENSCO 90 & ENSCO 99 that are expected to be retired from Ensco’s go-forward fleet

Note: adjusted for 2011 acquisition of Pride International

17

Investment in Engineering:

8500 Series Mooring Upgrade

Source: IHS Markit RigPoint as of December 2016; Ultra deepwater defined as 7500 ft. or greater

Dynamically Positioned

288

Rig CountGlobal Floater

Fleet

Ultra-deepwater capable

15K+ psi & 6+ ram BOP

8 mooring

winches

194

162

130

9

• Low-cost mooring

upgrade increases the

versatility of our 8500

Series rigs, placing

them among a select

group of floaters with

superior technological

capabilities and the

ability to operate in a

dynamically

positioned and/or

moored capacityENSCO 8503

ENSCO 8505

18

• Improving the drilling process

– advanced hybrid DP/Moored 8500 Series semis

– ENSCO 120/140 Series cantilever advantage

• Asset uptime and efficiency

– Ensco Asset Management System

• Re-engineering the support structure

– business unit consolidation

– centralization of staff functions

Investments in Innovation

19

Improved Operational Utilization

98.5%

99.0%99.1%

99.3%

2013 2014 2015 YTDSep16

Jackups

92.0% 92.9%

94.0%

99.1%

2013 2014 2015 YTDSep16

Floaters

20

Excellent Safety Performance

Total Recordable

Incident Rate

• Record 2016 TRIR

• Leading-edge safety

management systems

• Enhancing process

safety to drive further

improvements

0.0

0.2

0.4

0.6

0.8

1.0

1.2

2008 2009 2010 2011 2012 2013 2014 2015 2016

Ensco Industry

Note: IADC industry statistics are as of 3Q16.

21

Net Income Margin

Ensco Peer Average

24%

18%

Source: FactSet; sum of trailing eight quarters of net income divided by sum of trailing eight quarters of revenue. FactSet's data is based on

aggregation of information collected from industry equity research analysts and may not be based on GAAP reported financial data. Financials as

of 3Q16. Peer average includes Transocean, Noble Corp., Diamond Offshore, Seadrill, and Rowan Co.

Consistent

outperformance

versus major

peer average

22

High Levels of Customer Satisfaction

Rated #1• Total Satisfaction

• Safety & Environment

• Performance & Reliability

• Job Quality

• Special Applications

• Ultra-Deepwater Wells

• Deepwater Wells

• Harsh Environment Wells

• Horizontal & Directional Wells

• Shelf Wells

• North Sea

• Middle East

• Asia & Pacific Rim

23

Outlook for

Offshore Drilling

24

Offshore Exploration & Production

• Offshore production is ~33% of global supply

• Offshore reserves are a critical part of major E&P portfolios and

are vital to the economies of several countries

• Excessive costs/inefficiencies crept into sector during the $100+

oil environment

• Industry is proactively responding to commodity price pressures

and breakeven commodity prices for offshore programs are

declining

• Unprecedented decline in E&P spending will lead to supply side

challenges – the longer the duration of the pullback, the greater

the chance of significant upward movements in commodity prices

25

Catalyst

Markets

Offshore

Rig Supply

Path to Recovery

Breakeven Economics

Commodity

• Improvement /

stabilization in oil

prices

• Re-engineering /

standardization /

innovation

• Cost deflation

and efficiency

gains

• Brazil opens pre-

salt to more

players

• Mexico offshore

lease sales and

entrance of

international

operators

• Retirement of

older, less

capable assets

• Deferral and

cancellation of

newbuild

deliveries

26

• Cost estimates reduced to less than $10 billion from previous

estimate of $22 billion

• Project re-engineering through standardization and scope

optimization, coupled with industry deflation, resulted in significantly

less capital required to develop approximately 90% of resources

Industrywide Re-Engineering,

Efficiency Gains & Cost Deflation

BP Mad Dog:

Phase 2

Shell

Appomattox

Statoil

• 20% reduction in project costs from supply chain savings, design

improvements, etc.

• “Standardization is the new innovation”

Total Block

32

• Capital expenditure estimate reduced by $4 billion to $16 billion

• Optimized project design and contracting strategy

Recent Customer Commentary on Deepwater ProjectsOffshore Outlook

• Customers attention

has turned to project

re-engineering,

efficiency gains and

better expense

management

• Cost deflation across

supply chain:

operators, service

companies

• Break-even

economics are

improving

significantly for

offshore projects

27

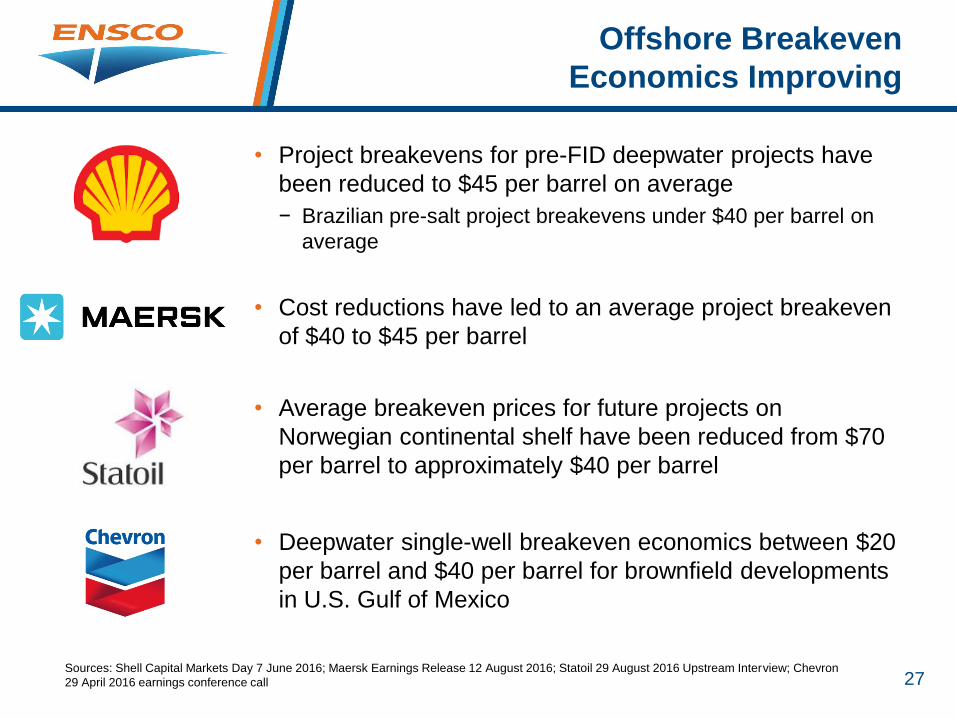

• Cost reductions have led to an average project breakeven

of $40 to $45 per barrel

• Average breakeven prices for future projects on

Norwegian continental shelf have been reduced from $70

per barrel to approximately $40 per barrel

• Project breakevens for pre-FID deepwater projects have

been reduced to $45 per barrel on average

− Brazilian pre-salt project breakevens under $40 per barrel on

average

Offshore Breakeven

Economics Improving

Sources: Shell Capital Markets Day 7 June 2016; Maersk Earnings Release 12 August 2016; Statoil 29 August 2016 Upstream Interview; Chevron

29 April 2016 earnings conference call

• Deepwater single-well breakeven economics between $20

per barrel and $40 per barrel for brownfield developments

in U.S. Gulf of Mexico

28

Strategic Combinations & Alliances

Among Offshore Service Companies

Strategic combinations and alliances drive greater efficiencies and lower the

breakeven commodity prices for offshore projects

Innovation, efficiencies

and cost reductions in

deepwater projects

Enhance project delivery,

improve recovery and

optimize cost/efficiency of

subsea developments

Overhaul subsea field

operations to drive

efficiencies

Integrated FPSO solutions

to reduce costs of offshore

developments

Optimize the cost and

efficiency of subsea well

intervention systems

Develop production

solutions to boost output,

increase recovery rates

and reduce costs for

subsea fields

29

Attrition of Older Rigs

50 more floaters could be retired by year-end 2017 if attrition

continues at similar rates observed throughout the downturn

Retired to Date

69 floaters retired

since 3Q14

Currently Idle

~35 floaters >30 years of

age idle without follow-

on work could be retired

Expiring Contracts~15 floaters >30 years of

age have contracts expiring

before YE17 without follow-

on work could be retired

Source: IHS-ODS Petrodata as of December 2016

Note: (1) ‘Retired’ includes scrapped rigs, announced scrapping and rigs converted to non-drilling units; (2) Competitive jackups are independent leg cantilever rigs; (3) Historical

attrition ratio of 88% for floaters older than 35 years of age and 67% for floaters between 30 and 35 years of age applied annually to rigs that are currently idle or rolling off contract

for each age category.

Up to ~150 additional jackups could be retired as expiring contracts

and survey costs lead to the removal of older rigs from drilling supply

Retired to Date

27 competitive

jackups retired

since 3Q14

Currently Idle97 competitive

jackups >30 years of age idle without follow-

on work could be retired

Expiring Contracts49 jackups >30 years of

age have contracts expiring

before YE17 without follow-

on work could be retired

FLO

AT

ER

SJA

CK

UP

S

30

Newbuild Order Book

Source: IHS-ODS Petrodata as of December 2016; marketed competitive floaters and jackups (independent leg cantilever rigs). Jackups numbers

above do not include recently announced intention by Middle East Joint Venture to order up to 20 rigs to be delivered over ten years beginning as

early as 2021.

Floaters

2

Uncontracted,

On Order

3

Contracted

45%27

Uncontracted,

Under

Construction

5%

3%

47%

News reports

suggest SETE

Brasil program

could be reduced to

8 newbuilds in total

Jackups

8 – 28

SETE Brasil

4

Contracted,

Established

Drillers

34

Uncontracted,

Established

Drillers

? – 62

Uncontracted,

Speculators

4%

34%

62%

Zero rigs built in

China by

speculators have

been contracted

31

Jackup Delivery Deferrals

05

1015202530

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

2Q

19

3Q

19

4Q

19

1Q

20

2Q

20

3Q

20

4Q

20

May 2014 Delivery Schedule

Delivered Under Costruction

05

1015202530

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

2Q

18

3Q

18

4Q

18

1Q

19

2Q

19

3Q

19

4Q

19

1Q

20

2Q

20

3Q

20

4Q

20

December 2016 Delivery Schedule

Delivered Under Costruction

Source: IHS-ODS Petrodata as of December 2016

Note: December 2016 delivery schedule includes 20 new orders and excludes 11 orders cancelled since May 2014. Numbers above do not include recently

announced intention by Middle East Joint Venture to order up to 20 rigs to be delivered over ten years beginning as early as 2021.

105 Scheduled Deliveries49 Actual Deliveries

130 Scheduled Deliveries 15 Scheduled Deliveries

32

Future Catalyst Markets: Brazil

• Following Senate approval earlier this

year, the Brazilian House recently passed

a bill that would eliminate requirement for

Petrobras to manage all pre-salt

operations and hold a minimum 30%

stake in pre-salt projects

• More recently, Statoil has acquired

Petrobras’ 66% operating interest in BM-

S-8 offshore Brazil including the Carcará

discovery for $2.5 billion

• Diversification of customer base offshore

Brazil is ongoing with outstanding tenders

from Premier, Total and Chevron

“We believe in the strong

fundamentals of Brazil

and the fundamentals of

its geology. We will be

looking at a substantial

part of our production

from Brazil.”

– Ben van Beurden,

Shell CEO

February 2016

33

Future Catalyst Markets: Mexico

• During 4Q15, an auction was completed

for shallow-water blocks offshore Mexico,

awarding licenses to several exploration

and production companies

• Deepwater acreage auctioned in 4Q16

with eight of ten blocks awarded to large

companies including several majors,

integrated, and national oil companies

“Regardless of what

happens in the

international context,

Mexico will move forward

with the energy reform

implementation.”

– Enrique Peña Nieto,

President of Mexico

February 2016

34

Recap

• Proactive steps to:

– improve capital structure

– reduce expenses

– restructure fleet

– invest in engineering and innovation that improves operational and safety

performance

• Positive steps taken by the offshore sector to reduce breakeven

economics are building the foundation for future market recovery

• Rig attrition improving rig supply dynamics

• Our actions and investments position Ensco to capitalize as we

navigate through the market cycle

35

36

Source: IHS Petrodata as of December 2016; competitive floaters and jackups (independent leg cantilever rigs); ‘contracted’ includes rigs currently under contract

or with a future contract; Newbuilds do not include recently announced intention by Middle East Joint Venture to order up to 20 jackups to be delivered over ten

years beginning as early as 2021; Potential retirements calculated using historical attrition ratio of 88% for floaters older than 35 years of age and 67% for floaters

between 30 and 35 years of age applied annually to rigs that are currently idle or rolling off contract for each age category.(1) News reports suggest SETE Brasil program could be reduced to 8 newbuilds in total

Appendix:

Global Rig Fleet

Newbuilds

Floaters Jackups

Contracted 140 237

Idle/Other 65 140

Cold Stacked 66 46

Total 271 423

Established Drillers 32 38

Uncertain (SETE Brasil(1) or Speculator) 28 62

Total 60 100

Potential Incremental

Retirements by Year-End

2017

Up to 50 Up to 150

DeliveredFleet

Attrition

-? -?

-? -?

37

Appendix:

Liquidity and Leverage

*Pro forma for new debt issues: $850 million of 3% exchangeable senior notes issued in December 2016 and approximately $332 million of 8% senior notes to be issued

in January 2017, both due 2024. A portion of the 3% exchangeable senior notes is treated as shareholders’ equity and the remainder as debt.

Note: Net debt is a non-GAAP financial measure defined as long-term debt less cash and short-term investments. Non-GAAP financial measures should be considered as

a supplement to, and not as a substitute for, or superior to, financial measures prepared in accordance with GAAP. 4Q15 net debt-to-capital is calculated as follows: long-

term debt of $5.9 billion, less $1.3 billion of cash and short-term investments, divided by the sum of long-term debt of $5.9 billion plus shareholders’ equity of $6.5 billion,

minus $1.3 billion of cash and short-term investments. 3Q16 net debt-to-capital is calculated as follows: long-term debt of $4.7 billion, less $1.8 billion of cash and short-

term investments, divided by the sum of long-term debt of $4.7 billion plus shareholders’ equity of $8.0 billion, minus $1.8 billion of cash and short-term investments.

2.25 2.25 2.25

1.3

1.82.3

4Q15 3Q16 3Q16Pro forma*

Liquidity

Revolver Cash + Short-term investments

$ billions

41%

27%

25%

4Q15 3Q16 3Q16Pro forma*

Net Debt-to-Capital Ratio

$3.55

$4.05

$4.54

38

Appendix:

Debt Maturity Schedule Proforma 9/30/16

$292

$551

$309

$623

$669$332

$850

2017 2018 2019 2020 2021 2022 2023 2024 2025 2027 2040

$300

2044

$ millions

$1,001No debt

maturities

until 2019

$150

Note: Reflects principal amount outstanding as of September 30, 2016, as adjusted to give effect to $24.5 million aggregate principal amount of 2044

senior notes that were exchanged for 1.8 million shares on October 3, 2016 and recent offerings: $850 million of 3% exchangeable senior notes and

$332 million of 8% senior notes, both due 2024.

$2.25B Revolver to Sept.

2019 then $1.13B to Sept.

2020

Recent

tender/exchange

announced for

2019-2021

maturities; $650M

tendered

$1,805 $1.182B of debt raised in Dec ‘16/

Jan ’17; $494M excess cash to be

used for additional debt

repurchases and/or general

corporate purposes