Embed Size (px)

Citation preview

Golden Dragon Hong Kong

Operations Finance

Customer Migration Capital Investment

High ARPU

Company Orientation

Urgent Issues Analysis Strategies Implementation Financial Projections

Objectives

EBITDA 10.0% CAGR

ARPU HK$112 159

Urgent Issues Analysis Strategies Implementation Financial Projections

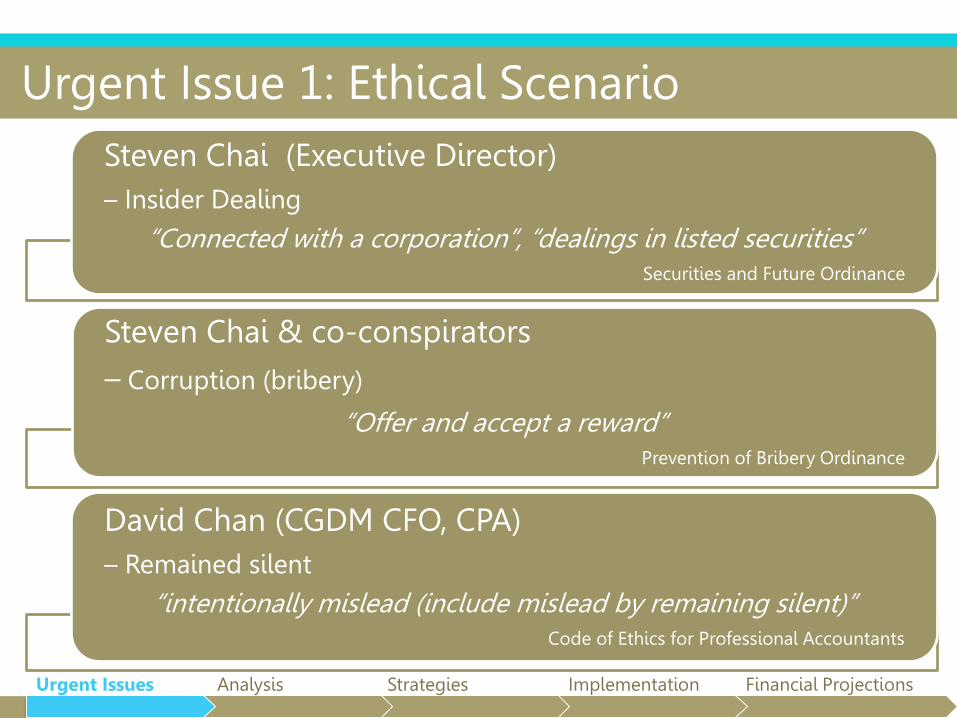

Urgent Issue 1: Ethical Scenario

Steven Chai (Executive Director)

– Insider Dealing

“Connected with a corporation”, “dealings in listed securities” Securities and Future Ordinance

Steven Chai & co-conspirators

– Corruption (bribery)

“Offer and accept a reward” Prevention of Bribery Ordinance

David Chan (CGDM CFO, CPA)

– Remained silent

“intentionally mislead (include mislead by remaining silent)” Code of Ethics for Professional Accountants

Urgent Issues Analysis Strategies Implementation Financial Projections

Urgent Issue 1: Ethical Scenario

Approach David Chan (CGDM CFO, direct superior)

Inform Michael Yip (CEO)

Speak to Board Members

Urgent Issues Analysis Strategies Implementation Financial Projections

Urgent Issue 2: Deficit in 30 Days

Financing Need:

• Deficit of HK$397mn in 30 days

Considerations:

• Bank deposits insufficient

• Involve interests

Solution:

• Immediate loan of HK$500mn

Projected Cash Position (GDHK) (HK$mn)

Cash (1 Jan) 118

Revenue 2400

Operating Cost -1500

Dividend -480

Tax -280

Capex -410

Lower Acct Payable -190

Advertising -40

Fine -15

Balance (30 June) -397

Urgent Issues Analysis Strategies Implementation Financial Projections

Position of GDHK: Laggard of the Competition

112

184

244 249

0

50

100

150

200

250

300

GDHK Competitors

GDHK lags the average ARPU by 43% HK$

Average: HK$197

Operations:

• Failure in low ARPU customer migration

Finance:

• Failure in utilizing debt to improve cash position

* Competitors: Data from the annual reports of HK Telecom (left), Hutchison (middle) and SmarTone (right)

Urgent Issues Analysis Strategies Implementation Financial Projections

Operations: Low Postpaid Subscribers Reduce ARPU

3.1%

13.8%

17.0%

6.3%

0%

5%

10%

15%

20%

Low receivables • Fewer postpaid • More prepaid

10x lower ARPU

Receivables as a % of revenue

Failed to migrate low-tier customers to high ARPU plans

(% of subscribers)

Competitors

3G Postpaid 65% 49% 71%

2G Postpaid 1.4% 14% -

Prepaid 34% 37% 29%

* Competitors: Data from the annual reports of HK Telecom (left), Hutchison (middle) and SmarTone (right)

GDHK Competitors

Urgent Issues Analysis Strategies Implementation Financial Projections

Operations: Failed to Respond to Smartphone Trend

Market share of smartphone OS

• Android & iPhone OS > 80% share

• Price of smartphone > HK$2500

• 3G & ARPU not accelerated by low-priced handsets

Smartphone trend in Hong Kong

Response of GDHK

Produces low-priced handsets

Unpopular, failed to raise ARPU

Response of Competitors

Partner with popular brands, launch high-tier plans

Welcomed by market, ARPU raised

51%

31%

18% Android

iPhone OS

Others

Urgent Issues Analysis Strategies Implementation Financial Projections

Operations: Slow Mobile Data Products Development

(Products) GDHK Competitors

Mobile Gaming Considering

Mobile TV Considering

Mobile Music App ×

4G LTE Service ×

* Competitors: Data from the annual reports of HK Telecom, Hutchison , SmarTone

• Competitors: LTE and products Capture demand for data

• GDHK: lacks data-driving products Should develop 3G/4G

Growing demand for data products

Urgent Issues Analysis Strategies Implementation Financial Projections

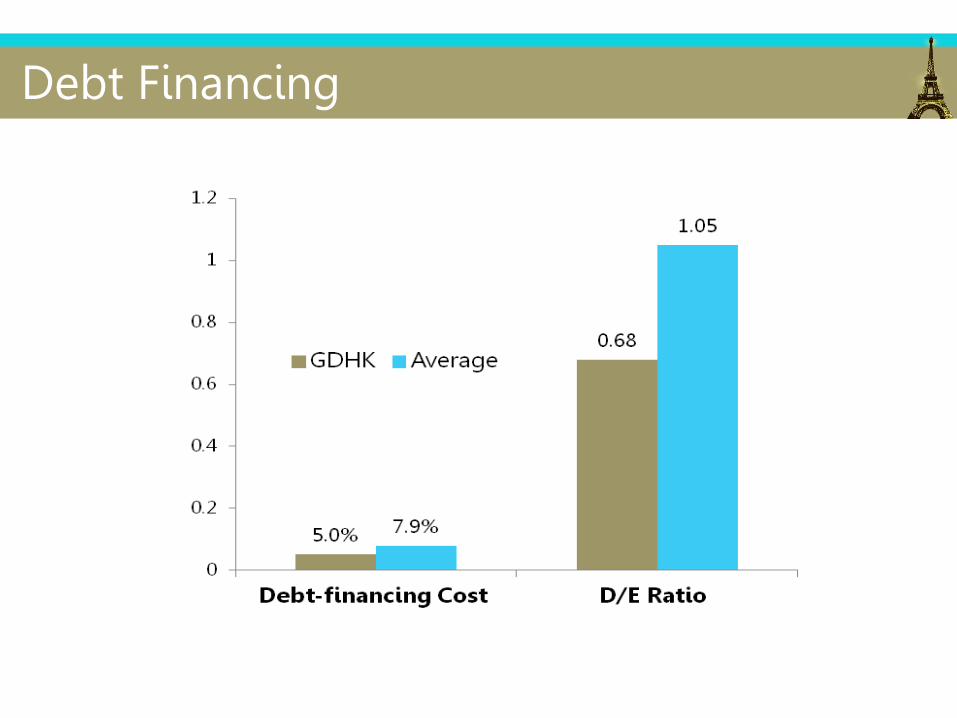

Finance: Illiquid and Debt Financing Capacity Idled

High profit margin, but low liquidity ratios 31.96% 0.35

0.31

0.06 9.11%

0.65

0.57

0.17

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Profit Margin Current Ratio Quick Ratio Cash Ratio

GDHK

Average

Low interest cost & D/E ratio Capacity of debt financing for capital investment

Urgent Issues Analysis Strategies Implementation Financial Projections

Grand Strategy

Operations Finance

Customer Migration Capital Investment

High ARPU

Company Orientation

Urgent Issues Analysis Strategies Implementation Financial Projections

Operations: Migrate Customers to Higher ARPU Plans

1. Partner with Apple & Samsung

∵ - Customers prefer smartphones

- Handsets: NOT core competency

2. Cheaper data plan trials

Entice trials & attract subscribers of other operators

3. Better and new mobile products

Monthly Fee $150 $200 $300 $400

Discounted Fee $90 $120 $180 $250

Voice (mins)

Basic 1000 1000 1500 2000

Intra 200 500 1000 1500

Local Data Usage

200MB

300MB

800MB

Unlimited Thereafter charge $10/30MB

and monthly capped at $250

Services included

• Intra SMS • 10 intra MMS • Voice mail, call forwarding, caller

number display, call waiting and conference call

Urgent Issues Analysis Strategies Implementation Financial Projections

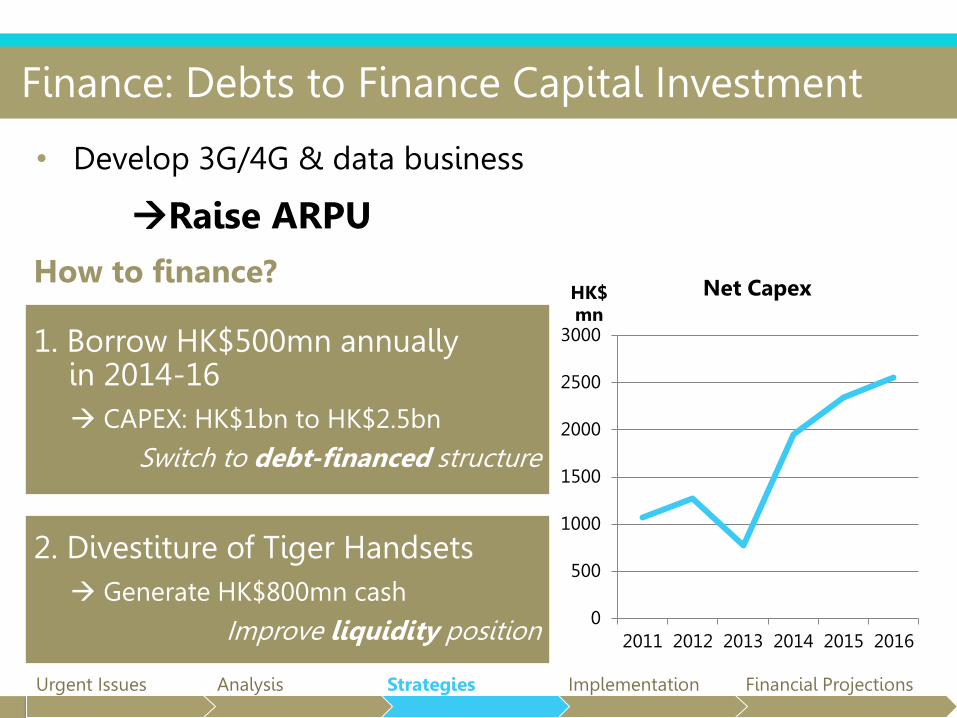

Finance: Debts to Finance Capital Investment

• Develop 3G/4G & data business

Raise ARPU

0

500

1000

1500

2000

2500

3000

2011 2012 2013 2014 2015 2016

HK$ mn

Net Capex

1. Borrow HK$500mn annually in 2014-16

CAPEX: HK$1bn to HK$2.5bn

Switch to debt-financed structure

2. Divestiture of Tiger Handsets

Generate HK$800mn cash

Improve liquidity position

How to finance?

Urgent Issues Analysis Strategies Implementation Financial Projections

Implementation Schedule 2012 2013 2014 2015 2016

Q3 Q4 Q1 Q2 Q3 Q4 H1 H2 H1 H2 H1 H2

Customer Migration

Partnership with popular mobile brands

Negotiate with Apple for its iPhone 5, Samsung's S4

Partner with other popular smartphone brands

Lower cost data plan trials

New mobile data products

Improvement of 3G services

Explore possibility of LTE/4G

Capital Investment

Spin-off Tiger Handsets

Improve cash position by loans

Urgent Issues Analysis Strategies Implementation Financial Projections

Financials: Debt-financing Improves Efficiency

Non-current loans

• HK$420mn 1900mn

D/E Ratio

• 0.68 0.77

Cost of Financing

• Debt: 5%

• Equity: 23%

Financing Efficiency

Investment: CAPEX / Liquidity

Customer Migration & ARPU

Profitability & Revenue

Growth

60% 57%

40% 44%

2011 2016

Debt

Equity

Urgent Issues Analysis Strategies Implementation Financial Projections

Financials: Improved Liquidity and CAPEX

Cash Reserves:

• HK$110mn 709mn

Cash Ratio:

• 0.06 0.36

Financing Efficiency

Investment: CAPEX / Liquidity

Customer Migration & ARPU

Profitability & Revenue

Growth

Capital Expenditure:

• 23% 35% of Sales

CAPEX-to-Income Ratio:

• 0.61 1.23

Cash Flow Projections

CAPEX-to-Income Ratio

Urgent Issues Analysis Strategies Implementation Financial Projections

Financials: Customer Migration & ARPU Uplift

ARPU: HK$112 159 by 2016 Financing Efficiency

Investment: CAPEX / Liquidity

Customer Migration & ARPU

Profitability & Revenue

Growth

112

159

0

20

40

60

80

100

120

140

160

180

2011 2016

Receivable Days: 7.6 20

0.33

0.67

0.72

0.28

Prepaid Postpaid

2011

2016

Urgent Issues Analysis Strategies Implementation Financial Projections

Segment Growth

GDHK Industry

Fee CAGR 2.60% -1.70%

VAS CAGR 22.60% 12.90%

Financials: Revenue Restructuring & Growth

• VAS boosted to take same proportion of revenue as Fee

Financing Efficiency

Investment: CAPEX / Liquidity

Customer Migration & ARPU

Profitability & Revenue

Growth

Growth Benchmarks - Overall

Industry Expectation 4.9%

Revenue CAGR 9.8%

EBITDA CAGR 10.0%

67%

28%

5%

FeeValue-added ServiceOther

47% 48%

5%

Urgent Issues Analysis Strategies Implementation Financial Projections

Summary

EBITDA 10.0% CAGR

ARPU HK$112 159

Customer Migration Capital Investment

Appendices Company Background

• Structure and History

• Mission and Values

• Domestic Market

• Income Statement

• Balance Sheet

• Cash Flow Statement

• CGDM Management

• GDHK Management

Ethical Scenario

• Staff Involved

• Securities and Futures Ordinance

• Prevention of Bribery Ordinance

• Code of Ethics for Professional Accountants

• ICAC Insider Dealing Case

• Amendment to Code of Ethics

Cash Deficit

• Projected Cash Position

Environmental Analysis

• SWOT Analysis

• PEST Analysis

• Porter’s Five Forces Model

• Competitor Technology and Product Comparison

• Market Share of Operating System

• Increase of Net Profit of Operators

Financial Analysis

• Financial Ratios

• ARPU Comparison

• Debt Financing

• Receivables Structure

Customer Migration Strategy

• Partnership with Smartphone Brands

• Lower Cost Data Plan Trials

• Special Package (1)

• Special Package (2): Mix & Match

• Upgrade and develop new mobile products

Capital Investment Strategy

• Valuation of Tiger Handsets

• Pricing of Tiger Handsets

• Increase in CAPEX

Implementation

• Implementation Schedule

Financial Projections

• Pro Forma Income Statement

• Pro Forma Cash Flow Statement

• Pro Forma Balance Sheet

• Sensitivity Analysis

• Projected Ratios

• Revenue and VAS Growth

Structure and History

• China Golden Dragon Mobile Limited (CGDM)

• Listed on HKEx and NYSE

• State-owned

• Largest mobile telecommunications provider in China – 31 provinces

• Golden Dragon Mobile Hong Kong Company Limited (GDHK)

• Established 1996, first Personal Communications Service provider

• Under brand “Dragon Magic Mobiles”

• Services: mobile voice, international direct dialing, roaming, wireless data

• Original Equipment Manufacturer acquirement:

• Tiger Handsets Company Limited, based in Guangdong

• Some manufacturing of DMM falls under GDHK

• Caring Company since 2000, Quality Tourism Service since 2003

Mission and Values

• Mission Statement:

“Dragon Magic – placing the magic of mobile technology at your fingertips.”

• Company Values:

Value Incorporates

Responsibility Safe products, responsible product development and R&D, social and corporate

responsibility, environmental responsibility, fiscal responsibility, responsible staffing

policies adhering to established national and international standards

Innovation Leading the market in new products and innovations, being first with value-added

mobile products, leveraging and improving upon existing mobile technologies,

anticipating customer needs and wants

Value Value for money products, price leading, value for shareholders, value for employees,

value of contribution to local and global communications industry, correct pricing,

cost leadership

Entrepreneurship Seizing opportunities in the market to increase existing market shares, looking for

new strategies to build markets and products, free-thinking and “big picture”

management, consider risk-takers

Quality Product safety, high quality product, low to no manufacturing and parts faults,

providing quality innovative mobile technologies, innovation with the aim to produce

safe, high quality new products and systems, “perfecting” products taken to market

Domestic Market

• Fixed line density: 52%, highest in Asia

• Market penetration rate 2011: 170%

• Restructuring & launch of new products

• Four mobile operators:

32%

27%

23%

18%

Market Share of Providers

Dragon Magic Mobiles

Vodatele

Tele Hong Kong

Lifestyle Phones

Income Statement HKD Million 2011 2010 Operating Revenue

Fees 3,062 2,789 Value-added Services 1,257 1,084 Handset sales 155 153 Other 95 101

Total operating revenue 4,569 4,127

Operating Expenses Leased Lines 30 26 Interconnection 245 230 Depreciation 680 619 Personnel 293 252 Handset manufacture 336 285 Other Operating Expenses 1,226 1,037

Total Operating Expenses 2,810 2,449

Profit from operations 1,759 1,678 Interest Income 11 13 Financing costs (21) (22) Profit before tax 1,749 1,669 Tax (16.5%) (289) (275) Profit after tax 1,460 1,394

Number of shares (Mil) 20 20 Earnings per share (HK$) 73 69.7

Balance Sheet

HKD Million 2011 2010 2011 2010

Current Assets Current Liabilities

Inventories 74 56 Accounts Payable 760 695

Accounts Receivables 94 69 Deferred Revenue 356 327

Prepayments and other CA 136 124 Accrued expenses and other payables

683 568

Deposits with Banks 233 199 Current taxation 92 112

Cash & Cash Equivalents 118 110 1891 1702

655 558 Non-current Liabilities

Non-current Assets Interest-bearing borrowings 420 420

Property, Plant, Equipment 4319 3932 Deferred revenue 5 4

Construction in progress 451 340 425 424

Goodwill 238 238 Equity

Deferred tax assets 75 66 Share capital 200 200

5083 4576 Reserves 3222 2808

Total Assets 5738 5134 3422 3008

Total Equity and Liabilities 5738 5134

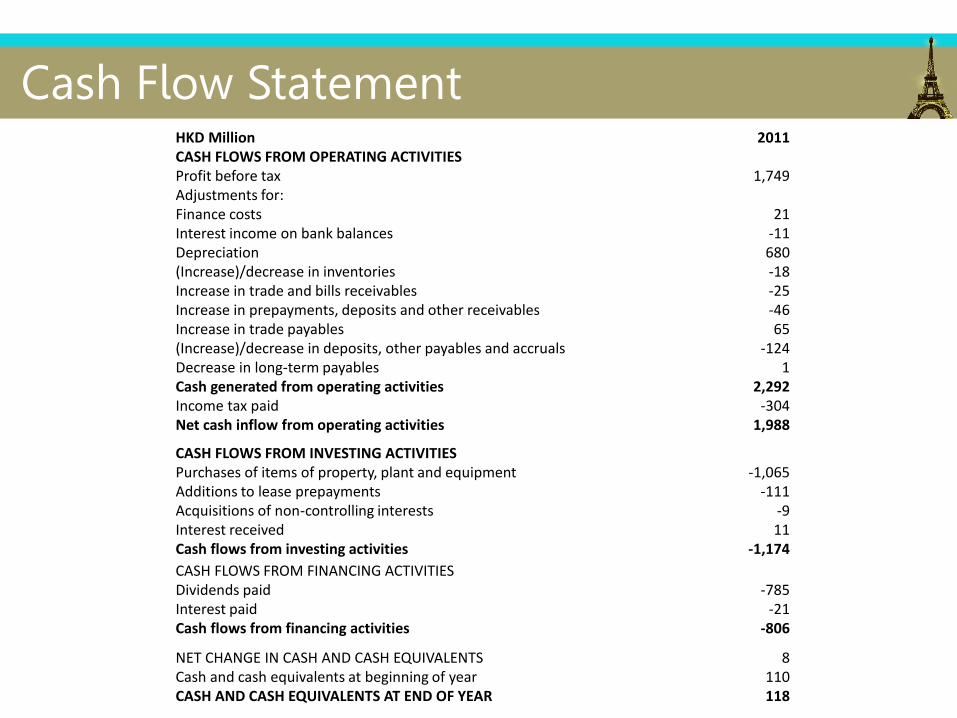

Cash Flow Statement HKD Million 2011 CASH FLOWS FROM OPERATING ACTIVITIES Profit before tax 1,749 Adjustments for: Finance costs 21 Interest income on bank balances -11 Depreciation 680 (Increase)/decrease in inventories -18 Increase in trade and bills receivables -25 Increase in prepayments, deposits and other receivables -46 Increase in trade payables 65 (Increase)/decrease in deposits, other payables and accruals -124 Decrease in long-term payables 1 Cash generated from operating activities 2,292 Income tax paid -304 Net cash inflow from operating activities 1,988

CASH FLOWS FROM INVESTING ACTIVITIES Purchases of items of property, plant and equipment -1,065 Additions to lease prepayments -111 Acquisitions of non-controlling interests -9 Interest received 11 Cash flows from investing activities -1,174

CASH FLOWS FROM FINANCING ACTIVITIES Dividends paid -785 Interest paid -21 Cash flows from financing activities -806

NET CHANGE IN CASH AND CASH EQUIVALENTS 8 Cash and cash equivalents at beginning of year 110 CASH AND CASH EQUIVALENTS AT END OF YEAR 118

CGDM Management

Selection of the Board of Directors

• Michael Yip, 55 – Executive Director, Chairman and CEO

• Michael Yip has been Chairman of the Board since 2002 and has been with the company for 20 years. He is highly respected in the Chinese and global telecommunications industry. He has an economics degree from Oxford and a Master of Business Administration (MBA) from London Business School.

• Moses Wong, 46 – Executive Director and Chief Operations Officer

• Moses Wong has been an executive director since 2002 and is seen as the next Chairman of the Board. He joined the company as a fresh university graduate and is an ambitious and extremely competent director and employee.

• Steven Chai, 39 – Executive Director

• Steven Chai is the youngest member of the Board of which he has been a director since 2008. He is a high-flyer in the telecommunications industry and holds an MBA from the Harvard Business School. He is a member of the audit committee.

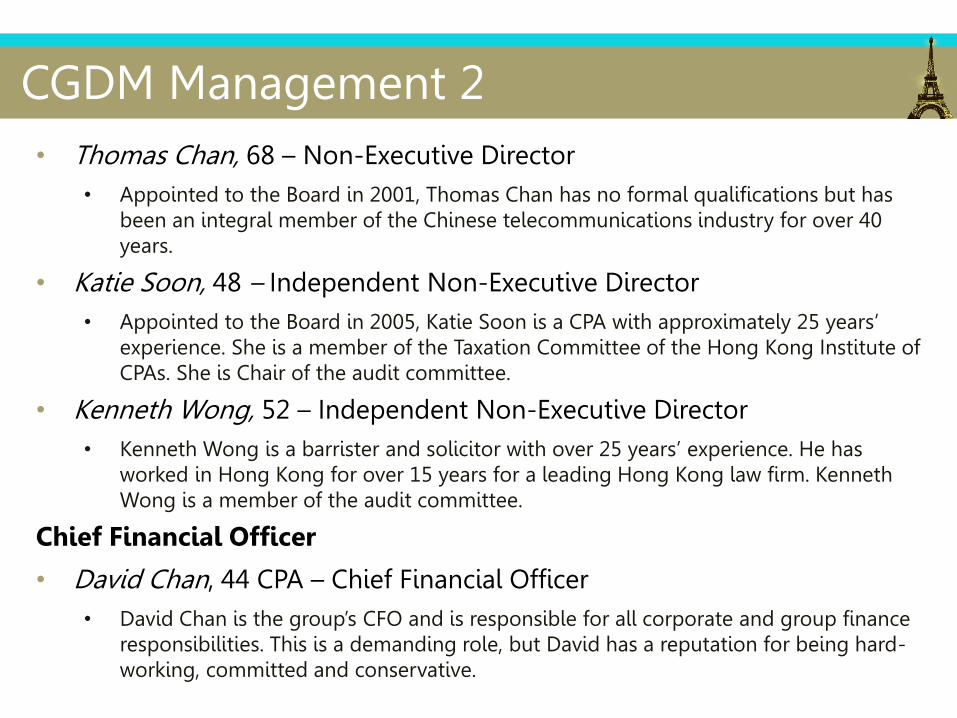

CGDM Management 2

• Thomas Chan, 68 – Non-Executive Director

• Appointed to the Board in 2001, Thomas Chan has no formal qualifications but has been an integral member of the Chinese telecommunications industry for over 40 years.

• Katie Soon, 48 – Independent Non-Executive Director

• Appointed to the Board in 2005, Katie Soon is a CPA with approximately 25 years’ experience. She is a member of the Taxation Committee of the Hong Kong Institute of CPAs. She is Chair of the audit committee.

• Kenneth Wong, 52 – Independent Non-Executive Director

• Kenneth Wong is a barrister and solicitor with over 25 years’ experience. He has worked in Hong Kong for over 15 years for a leading Hong Kong law firm. Kenneth Wong is a member of the audit committee.

Chief Financial Officer

• David Chan, 44 CPA – Chief Financial Officer

• David Chan is the group’s CFO and is responsible for all corporate and group finance responsibilities. This is a demanding role, but David has a reputation for being hard-working, committed and conservative.

GDHK Management

• Matthew Xu, 52 – Chief Executive Officer

• Matthew Xu is the company’s CEO and reports to the China Golden Dragon Mobile board. He has been in telecommunications since 1992 and with the company since 1997. He has no formal qualifications but is an astute and well-connected entrepreneur.

• Penny Wong, 55 – CPA & Chief Financial Officer

• Penny Wong is responsible for all accounting, IT, finance and administration for the GDHK subsidiary and must report to the group CFO. She has been with the company since 2008 and has previously worked in large accounting firms.

• Jenny Wang, 48 – Sales and Marketing Manager

• Jenny Wang is widely regarded as the best sales manager in telecommunications in Hong Kong and is now responsible for the sales and marketing of both voice and value-added business.

• Alison Cheng, 36 – General Manager

• Alison Cheng has worked for GDHK since it began operations in 1996. She is responsible for the overall operations of the Hong Kong head office and all of the retail subsidiaries.

Staff Involved

• Steven Chai, 39 – Executive Director

• Steven Chai is the youngest member of the Board of which he has been a director since 2008. He is a high-flyer in the telecomm industry and holds an MBA from the Harvard Business School. He is a member of the audit committee.

• Michael Yip, 55 – Executive Director, Chairman and CEO

• Michael Yip has been Chairman of the Board since 2002 and has been with the company for 20 years. He is highly respected in the Chinese and global telecommunications industry. He has an economics degree from Oxford and a Master of Business Administration (MBA) from London Business School.

• David Chan, 44 CPA – Chief Financial Officer

• The group’s CFO, and is responsible for all corporate and group finance responsibilities. This is a demanding role, but David has a reputation for being hard-working, committed and conservative.

Staff Involved 2

• Penny Wong, 55 – CPA & Chief Financial Officer

• Penny Wong is responsible for all accounting, IT, finance and administration for the GDHK subsidiary and must report to the group CFO. She has been with the company since 2008 and has previously worked in large accounting firms.

• Holly Lee, 28 – Fund Manager at ABC Funds Management

• Holly Lee is the number one Fund Manager for ABC Funds Management based in Hong Kong. She has a Master in Economics from Oxford and is viewed as a rising star in the Hong Kong funds management industry. She is extremely talented and ambitious, and has a reputation for taking large risks to facilitate large returns.

Securities and Futures Ordinance

• Cap 571

Section 247

Section 249

Securities and Futures Ordinance 2

• Cap 571

Section 249

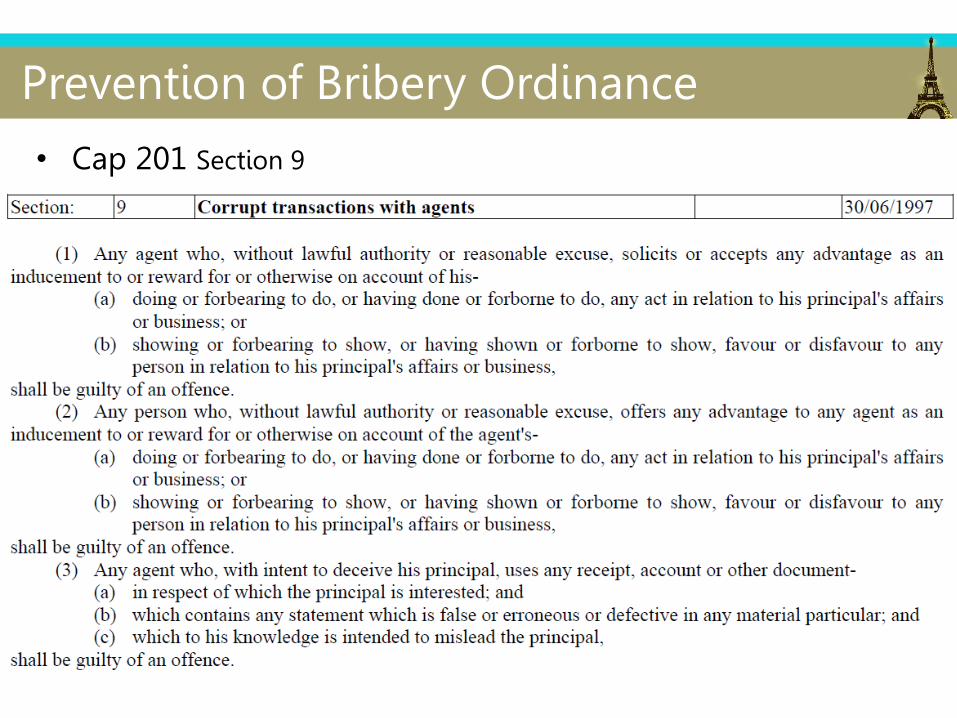

Prevention of Bribery Ordinance

• Cap 201 Section 9

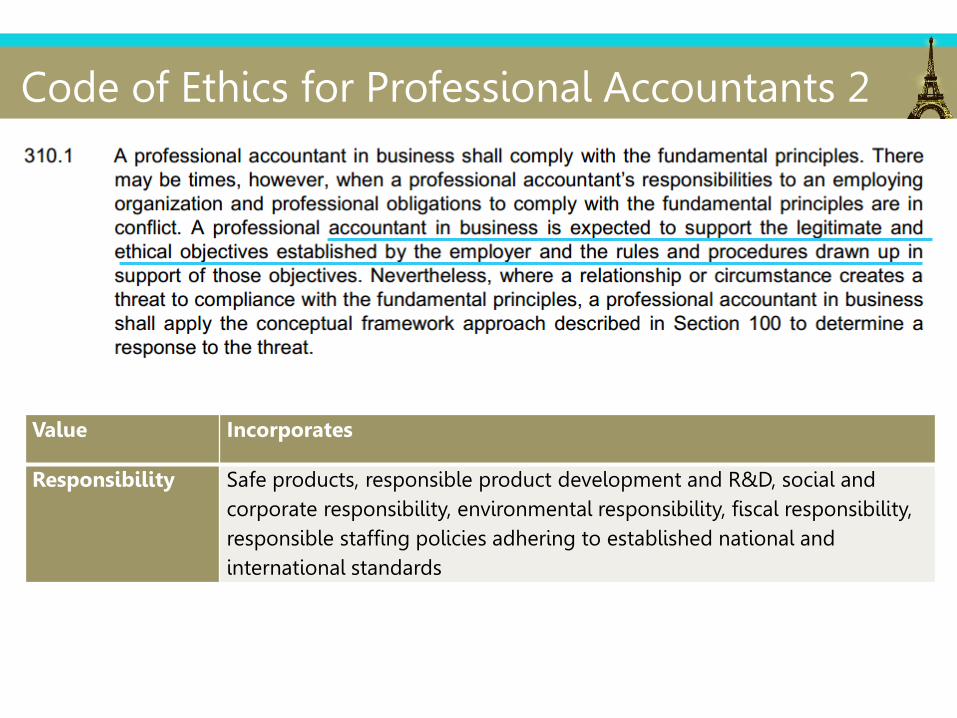

Code of Ethics for Professional Accountants (Jan 2011)

• Related parts: (Section 310 Potential Conflicts)

• Penalty (Preface)

Value Incorporates

Responsibility Safe products, responsible product development and R&D, social and

corporate responsibility, environmental responsibility, fiscal responsibility,

responsible staffing policies adhering to established national and

international standards

Code of Ethics for Professional Accountants 2

ICAC Insider Dealing Case

The trial judge, in sentencing, reckoned that the "insider dealings" case presented investigators with immense difficulties. To preserve market integrity, the judge ruled that penalties of sufficient deterrence had to be meted out.

ICAC Post, Jun 2007

Amendment to Code of Ethics • Proposed amendment to the code of ethics IESBA exposure draft on

Responding to a Suspected Illegal Act

• Background

The International Ethics Standards Board for Accountants (IESBA) issued an Exposure Draft on Responding to a Suspected Illegal Act on 22 Aug 2012. (Local Invitation to Comment with comments requested by 31 Oct 2012)

• New requirements to accountants in public practice and in business

• Address responsibilities in disclosing suspected illegal acts committed by clients or employers to an appropriate authority.

• Effects

• Far-reaching implications on accountants' courses of action in discharging their professional responsibilities

• Change the existing interaction between professional accountants and their clients as well as between employers and employees being accountants in organizations.

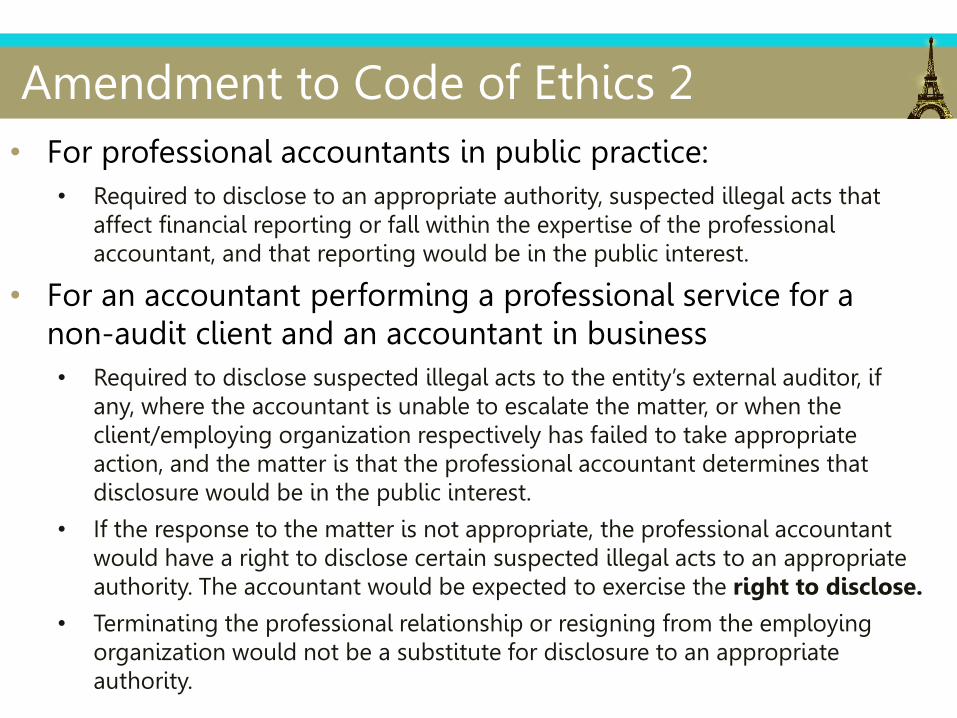

Amendment to Code of Ethics 2

• For professional accountants in public practice:

• Required to disclose to an appropriate authority, suspected illegal acts that affect financial reporting or fall within the expertise of the professional accountant, and that reporting would be in the public interest.

• For an accountant performing a professional service for a non-audit client and an accountant in business

• Required to disclose suspected illegal acts to the entity’s external auditor, if any, where the accountant is unable to escalate the matter, or when the client/employing organization respectively has failed to take appropriate action, and the matter is that the professional accountant determines that disclosure would be in the public interest.

• If the response to the matter is not appropriate, the professional accountant would have a right to disclose certain suspected illegal acts to an appropriate authority. The accountant would be expected to exercise the right to disclose.

• Terminating the professional relationship or resigning from the employing organization would not be a substitute for disclosure to an appropriate authority.

Projected Cash position

Projected Cash Position (GDHK) (HK$mn)

Cash (1 Jan) 118

Revenue 2400

Operating Cost -1500

Dividend -480

Tax -280

Capex -410

Lower Acct Payable -190

Advertising -40

Fine -15

Balance (30 June) -397

SWOT Analysis

Strength:

1. Largest subscriber base

2.Highly profitable

3. Low cost leadership

4. Low costs in debt-financing

Weakness:

1. Low ARPU

2. Weak cash flow and low liquidty

3. Failure in migrating minutes to bytes

4. Failure in recognizing the importance of high end smartphones

5. Lack of service variety and R&D

6. Low proportion of postpaid customers

Opportunity:

1. Growing 3G market and greater demand for mobile data services

2. Growing 4G market

3. Mobile data growth

Threat:

1. Competitors are investing intensively in 3G network upgrade and 4G development

2. Competitors are partnering with high end smartphones brands

3. Relationship with the authority being ceased

4. Voice growth stagnates

PEST Analysis

Political: Relationship with the government

being ceased

Economic: The industry performed strongly

despite global economic downturn

Social: Increasing demand for

smartphones and mobile data usage

Technological: Mobile

operators are innovating mobile data products and network quality

Porter’s Five Forces Model

High-ARPU

Competitors: 1. Right customer focus

2. Branded handset subsidy

3. Services can meet demand

Customers: Growing demand on smartphones and mobile data

services

Entrants:

High entry barriers as new entrants have to obtain licence from

government to operate

Substitutes: It is difficult to

substitute the operators

Suppliers: Spectrum is invited by OFCA for the bid of the

15-year licence Supply cost is relatively

stable

Competitor Technology and Product Comparison

(Products) GDHK Competitors

Mobile Gaming Considering

Mobile TV Considering

Mobile Music App ×

4G LTE Service ×

Competitors Product

SmarTone • Cloud Storage Manager • X-Power

Hong Kong Telecom • NPC Mobile Payment

Hutchison • 3tv • 3Books

Market Share of Operating Systems

Increase in Net Profits of Operators

1460

1271 1261

765

1394

972 900

255

0

200

400

600

800

1000

1200

1400

1600

GDHK

Operators booked increase in net profit

2011

2010

(HK$ mn)

Other Competitors*

* Other Competitors: Data from the annual reports of HK Telecom (2nd), Hutchison (3rd) and SmarTone (4th)

Financial Ratios

GDHK Other Competitors Liquidity

Current Ratio 0.35 1.19 0.27 0.80

Quick Ratio 0.31 1.04 0.23 0.70

Cash Ratio 0.06 0.32 0.02 0.27

Solvency

Debt Ratio 0.40 0.52 0.48 0.60

D/E 0.68 1.10 0.93 1.49

LT Debt Ratio 0.11 0.47 0.10 0.31

Times Interest Earned 84.29 2.07 11.6 10.2

Asset Management

Receivables Turnover 56.06 8.54 8.17 20.0

Total Asset Turnover 0.80 0.30 0.67 0.92

Fixed Asset Turnover 0.90 0.35 0.75 1.38

Profitability (%)

Profit Margin 31.96 6.41 9.41 11.5

ROA 25.45 1.95 6.28 10.6

ROE 42.68 4.11 12.1 26.3

ARPU Comparison

* Other Competitors: Data from the annual reports of HK Telecom (left), Hutchison (middle) and SmarTone (right)

112

184

244 249

0

50

100

150

200

250

300

GDHK Competitors

Average: HK$197

HK$

Debt Financing

Receivables Structure

Receivable as a % of Revenue

GDHK 3.1%

Other Competitors*

13.8%

17.0%

6.3%

* Other Competitors: Data from the annual reports of HK Telecom (left/top), Hutchison (middle) and SmarTone (right/bottom)

GDHK Other Competitors*

Partnership with Smartphone Brands

• Partner with Apple, Samsung, HTC, Sony etc.

• Leverage on:

• Huge subscriber base;

• Long-established operating model;

• Connection with CGDM

• Reasons:

• Increase no. of customers buy smartphones via GDHK use more costly plans raise ARPU;

• Producing handsets is out of GDHK core competency

• Partners and their new handsets

• Apple launches iPhone on 5 Sept 2012 (main contributor to 27-fold increase in data usage from 2008-2011)

• Samsung Galaxy launches S4 in Feb 2013

Producer Model/Series

Apple iPhone 5

Samsung S4

Sony Xperia

HTC HTC One

RIM BlackBerry 10

Nokia Nokia Lumia

Partnership with Smartphone Brands 2

Lower Cost Data Plan Trials

Monthly Fee $150 $200 $300 $400

Discounted Fee $90 $120 $180 $250

Voice (mins)

Basic 1000 1000 1500 2000

Intra 200 500 1000 1500

Local Data Usage

200MB 300MB 800MB

Unlimited Thereafter charge $10/30MB and monthly capped at $250

Services included

• Intra SMS • 10 intra MMS • Voice mail, call forwarding, caller number

display, call waiting and conference call

Special Package (1)

Handset

Monthly Fee $150

Monthly Fee $250

Monthly Fee $300

Samsung S3 (16GB) $3,200 $1,800 $0

Samsung S3 (32GB) $3,500 $2,100 $0

iPhone 5 (16GB) $3,600 $1,100 $450

iPhone 5 (32GB) $4,500 $2,000 $1,300

iPhone 5 (64GB) $5,300 $2,800 $1,700

Special Package (2): Mix & Match

Monthly Fee $100

Basic min 2000 1000

Intra min 1000 600

Intra SMS Unlimited Unlimited

Data Usage - 100MB

Self selected Value-added services

Free to pick one item: • 30MB local data • Mobile Reading • Mobile Gambling • Mobile “Weibo” • Mobile Music • Call Guard

$10 for each item: • Mobile Reading • Mobile Gambling • Mobile “Weibo” • Mobile Music • Call Guard

Services included Voice mail, call forwarding, caller number display, call waiting and conference call

Upgrade and develop new mobile products

• Upgrade existing mobile products:

• Mobile Gaming: partner with local mobile gaming companies e.g. LazyBug Studio expand on current game variety

• Mobile Gambling: partner with the Hong Kong Jockey Club to provide mobile services

• Mobile Reading: provided by almost all competitors and very popular among smartphone users provide unlimited access to e-books, comics and magazines

Upgrade and develop new mobile products 2

• Upgrade existing mobile products:

• 3G Dual number service plan: work with CGDM to provide the service in Hong Kong and Mainland China enjoy voice, message and data services

• Call Guard: operate on a cloud-based platform to avoid disturbance and report nuisance callers

• Other value-added services: International data roaming, Mobile Music (free access to KKBOX) and Mobile “Weibo” (partner with Xinlang Wang)

Valuation of Tiger Handsets

Valuation of Tiger Handset (HK$mn)

Current Situation Scenario IF all handsets are purchased instead of gifted

Sales 155 Sales 420

Cost of Sales 124 Cost of Sales 336

Profit 31 Profit 84

Assumptions:

Profit roughly equals Free Cash Flow

WACC = 10% Profitability remains same (20%)

Perpetuity Growth = 0% Operating Years = 20

NPV of Tiger Handset: 799.14

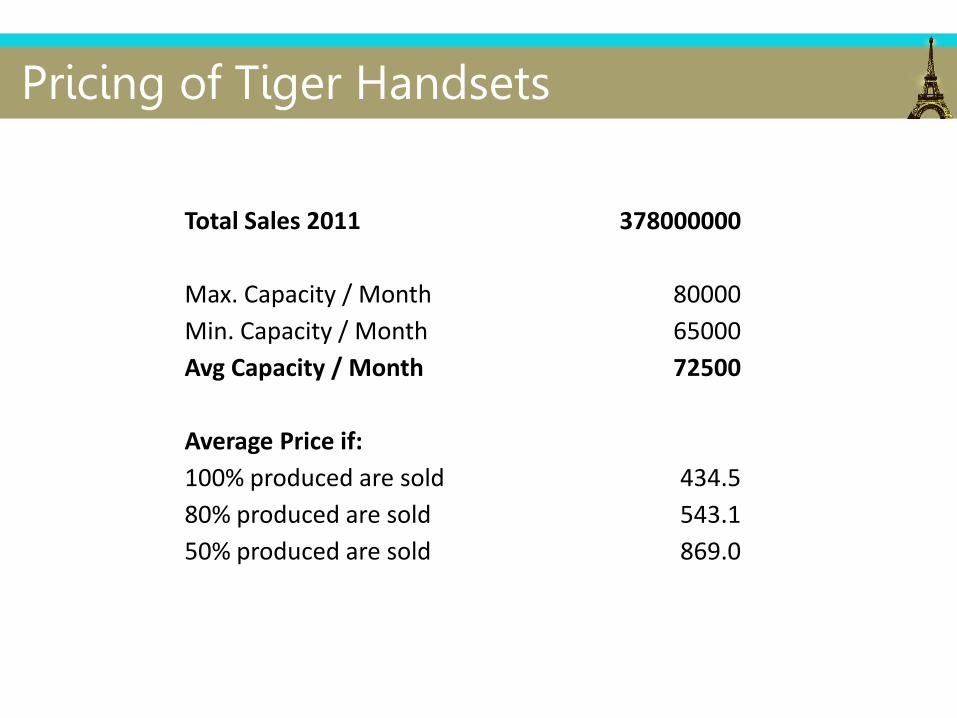

Pricing of Tiger Handsets

Total Sales 2011 378000000

Max. Capacity / Month 80000

Min. Capacity / Month 65000

Avg Capacity / Month 72500

Average Price if:

100% produced are sold 434.5

80% produced are sold 543.1

50% produced are sold 869.0

Increase in CAPEX CAPEX

2010 2011 2012 2013 2014 2015 2016

Net PPE projections

BoP 3,932 4,319 4,473 4,194 4,913 5,772

Net Capex 1,065 1,273 778 1,952 2,344 2,556

Depreciation -678 -1,118 -1,058 -1,233 -1,485 -1,781

EoP 3,932 4,319 4,473 4,194 4,913 5,772 6,547

Capex projections

Gross Capex 0 -1,065

Less disposals 0 0

Net Capex 0 -1,065 -1,273 -778 -1,952 -2,344 -2,556

% of sales 0.0% 23.3% 25.0% 28.0% 32.0% 35.0% 35.0%

Depreciation projections

Existing assets -864 -648 -432 -216

Capex in 2011 -255 -255 -255 -255 -255

Capex in 2012 -156 -156 -156 -156

Capex in 2013 -390 -390 -390

Capex in 2014 -469 -469

Capex in 2015 -511

Total depreciation -619 -680 -1,118 -1,058 -1,233 -1,485 -1,781

Implementation Schedule

2012 2013 2014 2015 2016

Q3 Q4 Q1 Q2 Q3 Q4 H1 H2 H1 H2 H1 H2

Customer Migration

Partnership with popular mobile brands

Negotiate with Apple for its iPhone 5, Samsung's S4

Partner with other popular smartphone brands

Lower cost data plan trials

New mobile data products

Improvement of 3G services

Explore possibility of LTE/4G

Capital Investment

Spin-off Tiger Handsets

Improve cash position by loans

Pro Forma Income Statement

HKD Million 2012 2013 2014 2015 2016

REVENUE 5,091 5,637 6,101 6,696 7,303

Cost of inventories sold -374 -415 -449 -492 -537

Staff costs -322 -355 -390 -429 -472

Depreciation and amortisation -1,118 -1,058 -1,233 -1,485 -1,781

Rental expenses -35 -40 -46 -52 -60

Fuel and utility expenses -257 -270 -284 -298 -313

Other operating expenses -1,374 -1,522 -1,647 -1,808 -1,972

Finance costs -46 -21 -46 -71 -96

PROFIT BEFORE TAX 1,563 1,957 2,007 2,060 2,073

Income tax expense -258 -323 -332 -340 -342

PROFIT FOR THE YEAR 1,305 1,634 1,676 1,720 1,730

Pro Forma Cash Flow Statement HKD Million 2012 2013 2014 2015 2016

CASH FLOWS FROM OPERATING ACTIVITIES

Profit before tax 1,563 1,957 2,007 2,060 2,073

Adjustments for:

Finance costs 46 21 46 71 96

Depreciation 1,118 1,058 1,233 1,485 1,781

(Increase)/decrease in inventories -8 -9 -7 -10 -10

Increase in trade and bills receivables -45 -46 -65 -80 -70

Increase in trade payables -190 61 52 67 68

Cash generated from operating activities 2,484 3,043 3,265 3,594 3,938

Income tax paid -258 -323 -332 -340 -342

Net cash inflow from operating activities 2,226 2,719 2,933 3,254 3,595

CASH FLOWS FROM INVESTING ACTIVITIES -1,273 -778 -1,952 -2,344 -2,556

CASH FLOWS FROM FINANCING ACTIVITIES

New bank loans 500 0 500 500 500

Repayment of bank loans 0 -500 0 0 0

Dividends paid -1044.4 -1307.31 -1340.88 -1376.27 -1384.49

Interest paid -46 -21 -46 -71 -96

Cash flows from financing activities -590 -1,828 -887 -947 -980

NET CHANGE IN CASH AND CASH EQUIVALENTS 363 113 94 -37 59

Cash and cash equivalents at beginning of year 118 481 594 688 651

CASH AND CASH EQUIVALENTS AT END OF YEAR 481 594 688 651 709

Pro Forma Balance Sheet HKD Million 2010 2011 2012 2013 2014 2015 2016

NON-CURRENT ASSETS

Property, plant and equipment 3,932 4,319 4,473 4,194 4,913 5,772 6,547

Construction in progress 340 451 452 452 452 452 452

Intangible assets 238 238 238 238 238 238 238

Deferred tax assets 66 75 75 75 75 75 75

4,576 5,083 5,238 4,959 5,678 6,537 7,312

CURRENT ASSETS

Inventories 56 74 81 90 97 107 117

Trade receivables 69 94 139 185 251 330 400

Prepayments, deposits and other receivables 323 369 369 369 369 369 369

Cash and cash equivalents 110 118 481 594 688 651 709

558 655 1,071 1,238 1,405 1,457 1,595

TOTAL ASSETS 5,134 5,738 6,309 6,197 7,083 7,994 8,907

CURRENT LIABILITIES

Bank loans 0 0 500 0 0 0 0

Trade payables 695 760 570 631 683 750 818

Deposits, other payables and accruals 568 683 683 683 683 683 683

Deferred Revenue 327 356 356 356 356 356 356

Tax payable 112 92 92 92 92 92 92

1,702 1,891 2,201 1,762 1,814 1,881 1,949

NON-CURRENT LIABILITIES

Bank loans 420 420 420 420 920 1,420 1,920

Long-term payables 4 5 5 5 5 5 5

424 425 425 425 925 1,425 1,925

TOTAL LIABILITIES 2,126 2,316 2,626 2,187 2,739 3,306 3,874

EQUITY

Issued capital 200 200 200 200 200 200 200

Reserves 2,808 3,222 3,483 3,809 4,144 4,487 4,833

TOTAL EQUITY 3,008 3,422 3,683 4,009 4,344 4,687 5,033

Sensitivity Analysis

Scenario 2012 Fee Drop by 10% No VAS Growth 2013 Fee Drop by 10% No VAS Growth

HKD Million # % # % # % # % # % # %

REVENUE 5,091 100% 4769 94% 4740 93% 5,637 100% 5303 94% 5238 93%

Cost of inventories sold 374 7% 374 7% 374 7% 415 7% 415 7% 415 7%

Staff costs 322 6% 322 6% 322 6% 355 6% 355 6% 355 6%

Depreciation and amortisation 1,118 22% 1118 22% 1118 22% 1,058 19% 1058 19% 1058 19%

Rental expenses 35 1% 35 1% 35 1% 40 1% 40 1% 40 1%

Fuel and utility expenses 257 5% 257 5% 257 5% 270 5% 270 5% 270 5%

Other operating expenses 1,374 27% 1374 27% 1374 27% 1,522 27% 1522 27% 1522 27%

Finance costs 46 1% 46 1% 46 1% 21 0% 21 0% 21 0%

PROFIT BEFORE TAX 1,563 31% 1242 24% 1213 24% 1,957 35% 1623 29% 1558 28%

Income tax expense 258 5% 205 4% 200 4% 323 6% 268 5% 258 5%

PROFIT FOR THE YEAR 1,305 26% 1037 20% 1013 20% 1,634 29% 1355 24% 1301 23%

Projected Ratios Liquidity 2016 2011 2010

Current Ratio 0.82 0.35 0.33

Quick Ratio 0.76 0.31 0.29

Cash Ratio 0.36 0.06 0.06

NWC to TA -0.04 -0.22 -0.22

Interval Measure 113.37 85.08 83.16

Solvency

Total Debt Ratio 0.43 0.40 0.41

Debt Equity Ratio 0.77 0.68 0.71

Equity Multiplier 1.77 1.68 1.71

Long term Debt Ratio 0.28 0.11 0.12

Times interest earned ratio 22.58 84.29 76.86

Cash Coverage ratio 41.14 116.67 105

Asset Management

Receivable Days 20.00 7.59 6.10

Total Asset Turnover 0.82 0.80 0.8

Fixed Asset Turnover 1.00 0.90 0.9

Profitability (%)

Profit Margin 23.69 31.96 33.77

ROA 19.42 25.45 27.14

ROE 34.38 42.68 46.33

ROS 29.69 38.50 40.66

Revenue and VAS Growth

FEE 2010 2011 2012 2013 2014 2015 2016

% growth 9.8% 5.0% 4.0% 2.0% 1.0% 1.0%

Total Fee 2,789 3,062 3,215 3,344 3,411 3,445 3,479

Value-add

Value-added services 1,084 1,257 1,608 2,006 2,387 2,928 3,479

% of total fee 38.9% 41.1% 50.0% 60.0% 70.0% 85.0% 100.0%

Other revenue

Handset 153 155 173 192 208 229 250

Others 101 95 95 95 95 95 95

Total other revenue 254 250 268 287 303 324 345

Total Revenue

Fee 2,789 3,062 3,215 3,344 3,411 3,445 3,479

Value-added Service 1,084 1,257 1,608 2,006 2,387 2,928 3,479

Other 254 250 268 287 303 324 345

Total 4,127 4,569 5,091 5,637 6,101 6,696 7,303