Embed Size (px)

Citation preview

GOLD NOWUnlocking The Potential OfDomestic Supply Of Gold

Neha MalikResearch Analyst, NCDEX

NCDEX Investor (Client) Protection Fund Trust

Issued in Public Interest

Executive Summary....................................................................... 1 to 1

Introduction................................................................................... 2 to 3

Patterns of Gold Demand in India.................................................. 4 to 6

Gold Loans (An Overview)............................................................. 7 to 7

Stemming Gold Imports................................................................. 8 to 9

NCDEX ‘Gold Now’ Forwards.................................................... 10 to 13

Other Ways to Achieve Self-Sufficiency in Gold........................ 14 to 14

Pricing of Gold in India.............................................................. 15 to 16

Conclusion................................................................................. 17 to 18

Index

NCDEX Investor (Client) Protection Fund Trust

Issued in Public Interest

Gold occupies an important place in the Indian economy. Its possession has

always been considered as a sign of prosperity. Acquisition of gold is governed by

both consumption and investment requirements with the latter gaining importance

in the recent past. Since domestic production of gold is close to negligible, almost

entire demand is met by imports which has exerted pressure on India’s current

account balance. Enabling India to become self-sufficient in gold by generating

domestic supply channels is therefore extremely crucial.

As per available estimates, approximately 22,000 tonnes of gold is currently lying

with the Indian households. If tapped effectively, this could create an opportunity

for facilitating domestic supply of gold while reducing reliance on imports. Various

measures have already been adopted to bring this gold into circulation but they

have met with limited success.

By launching India Good Delivery based gold forwards, NCDEX plans to

encourage domestic supply of gold and stem the growing reliance on imports. In

the process, NCDEX also plans to standardise domestic refineries through

accreditation as per international quality parameters. The forwards gold platform

may also be ideal for jewellers for efficiently managing their inventories. More

importantly, pricing of gold under such contracts will be left to the market forces to

promote transparency.

Effective monetisation of gold and creation of its domestic supply however calls

for an appropriate policy response in both regulatory and monetary spheres.

Change in the government perception therefore, becomes a pre-requisite for

achieving this goal.

Executive Summary

1

1

Introduction

Gold occupies an important place in the Indian economy. Possession of

gold has always been considered as a sign of prosperity. Over the years, it has

also become a preferred investment class providing an effective hedge against

inflation. A consistent rise in the investment demand for gold bears testimony to

this fact. Gold has also always been easily accepted as a collateral to meet liquidity

requirements of the borrower. This practice has been further facilitated by intro-

duction of the gold loan scheme under the formal banking network.

Both India and China accounted for 54 percent of consumer gold demand in

20141. Since domestic production of gold in India is close to negligible, almost

entire demand is met by way of imports. For instance, of the total supply of gold

in India, imports constituted close to 90 percent during 2011-2014. 2A high level of

gold imports has been a drag on India’s current account. Current account deficit

equalled 4.7 percent of GDP in 2012-133 due to which the RBI was forced to

impose restrictions on imports of gold4.

As per available estimates, approximately 22,000 tonnes of gold is currently

resting with the Indian households5. If tapped effectively, this could create an

opportunity for facilitating domestic supply of gold while reducing reliance on

imports. Various measures (such as the gold deposit scheme) have already been

adopted to bring this gold into circulation. However, they have not been

successful given the lack of a requisite infrastructure and standardisation norms

essential for developing a domestic market for gold.

Since domestically refined gold does not enjoy the same recognition and

acceptance in India as the London Bullion Market Association (LBMA) certified

gold, there is a need to scale up the standards of the former in order to create

self-sufficiency in this product.

1) Gold Demand Trends, World Gold Council, Full Year 2014. 2) Please refer to Table 1 in the

Appendix for details. 3) Economic Survey 2013-14, Ministry of Finance. 4) “Import of Gold by

Nominated Banks/Agencies”, RBI/2012-13/499, Circular No.103, May 13, 2013. 5) “Why

India Needs a Gold Policy”, FICCI, Dec. 2014

2

2

1By allowing India ‘Good Delivery Gold’ to be delivered under ‘Gold Now’ forwards,

NCDEX aims to encourage domestic supply of gold and facilitate development of

domestic gold refineries, while helping the gems and jewellery sector move up the

value chain. More importantly, pricing of gold under such contracts will be left to

the market forces to promote transparency.

This however, needs to be backed by an appropriate policy and regulatory

support. Greater awareness on the benefits of using dematerialised and paper

gold can also address the growing appetite for the commodity without exerting

pressure on India’s current account. Facilitation of domestically refined physical

gold coupled with efforts to encourage investment in paper gold can help India

become self-sufficient in the product.

3

3

6) Please refer to Table 2 in the Appendix for additional details.

Patterns of Gold Demand in India

Gold demand in India can be bifurcated into three components i.e. consumption,

investment and industrial demand. Industrial demand for gold is highly

insignificant when compared to its other counterparts. For instance, in 2013,

industrial demand for gold equalled 12 tonnes only as compared to consumer

and investment demand which stood at 975 tonnes and 362 tonnes respectively6.

While both consumer and investment demand have been consistently rising over

time (Fig.1), consumer demand has been much higher than its investment

counterpart.

Figure1: Consumer and Investment Demand of Gold in India (In tonnes)

Source: GFMS, Thomson Reuters

0200400600800

10001200

Investment Demand Consumer Demand

As per GFMS (Thomson Reuters) methodology, components of gold supply

include primary mine production, old scrap returned to the market and net

hedging activity while the demand for gold is a function of jewellery fabrication,

gold used in electronics as well as in medical and industrial applications. Retail

investment (comprising of net consumption of gold bars and coins) and central

bank holdings of gold also form a part of the demand. Table 1 uses this

methodology to determine the level of physical demand-supply gap in India. Net

hedging activity (on the supply side), use of gold in dental applications and net

official sector (on the demand side) have been excluded from the calculations

due to non-availability/applicability of data. A significant domestic deficit is

observed for India which explains the increasing dependency on gold imports.

4

7) “Long run price elasticity of gold import demand varies from -0.69 to -1.01, indicating moderately

inelastic to unitary elastic demand”. Source: Kanjilal, K., and Ghosh, S., “Income and price elasticity of

gold import demand in India: Empirical Evidence from threshold and ARDL bounds test cointegration”,

Resources Policy 41 (2014), 135-142. 8) Please refer to Fig. 1 in the Appendix. 9) Kanjilal, K., and

Ghosh, S., “Income and price elasticity of gold import demand in India: Empirical Evidence from

threshold and ARDL bounds test cointegration”, Resources Policy 41 (2014), 135-142

In addition to the above, demand for gold in India is inelastic which implies that an

increase in the price of gold does not necessarily induce a fall in its demand7.

Instead, it is usually associated with a rise (or an inconsequential change) in

consumer demand for gold8. Rising consumer demand for gold and hence,

imports, has been a drag on India’s current account (Fig. 2). Empirical research

has established a long-run relationship (co-integration) between gold import

demand, real gold price and real GDP. Short-run causality from gold import

demand to real price of gold by way of changes in the custom duty has also been

proven.9

Table 1: Domestic Gold Demand and Supply Balance Sheet (In tonnes)

1.6

101.0

102.6

1.7

113.0

114.7

2.3

59.0

61.3

2.8

81.0

83.8

2010 2011 2012 2013

1. Mine Production

2. Gold Supply from Scrap

3. Total Supply (1+2)

607.4

12.1

2.4

9.7

362.1

265.8

96.3

981.6

879

618.2

11.5

2.4

9.1

312.2

205.9

106.3

941.9

827.2

667.0

14

2.5

11.5

368

288

80

1049

987.7

685.0

15.7

2.5

13.2

348.9

266.3

82.6

1049.6

965.8

4. Jewellery

5. Industrial Fabrication (5.1+5.2)

5.1 Of which Electronics

5.2 Of which Other Industrial Uses

6. Retail Investment (6.1+6.2)

6.1 Of which Bars

6.2 Of which Metals and Imitation Coins

7. Total Demand

8. Domestic Deficit (Demand- Supply) (7-3)

Supply

Demand

Source: Author’s calculations based on the data extracted from GFMS, Thomson Reuters

5

10) Rosch, A. and Schmidbauer, H., “Impact of Festivals on Gold Price Expectation and Volatility”, FOM

University of Applied Sciencies, Munich, Germany, 2012.

Another crucial observation is seasonality in consumer demand for gold

determined mainly by festivals such as Akshaya Tritiya and Diwali. It has been

found that festivals like Akshaya Tritiya have an impact on the distribution of gold

price changes.10

Fig. 2 India’s Gold Imports and Current Account

Source: Handbook of Statistics for the Indian Economy 2013-14, RBI Note: Imports are measured on the LHS and the Current Account Balance on the RHS

-6000

-5000

-4000

-3000

-2000

-1000

0

0

500

1000

1500

2000

2500

3000

3500

2008-09 2009-10 2010-11 2011-12 2012-13 2013-14

Import of gold (Rs. Cr) Net Current Account Balance (Rs. Bn)

6

11) Gupta, S. et al, “All that glitters is Gold: India Jewellery Review, 2013”, AT Kearney and FICCI,

November 2013. 12) “Committee on Comprehensive Financial Services for Small Businesses and Low

Income Households”, RBI, Dec. 2013. 13) “Surveying the Indian Gold Loan Market”, Cognizant 20-20

insights, January 2012. 14) Report of the Working Group to Study the Issues Related to Gold Imports

and Gold Loans NBFCs in India, RBI, Feb 2013. 15) The RBI working report on gold (2013) was the only

report to publish time series data on the growth of gold loans by banks and NBFCs. No other

publication has attempted to provide such statistics after this report. 16) “Surveying the Indian Gold

Loan Market”, Cognizant 20-20 insights, January 2012. 17) Report of the Working Group to Study the

Issues Related to Gold Imports and Gold Loans NBFCs in India, RBI, Feb 2013

Gold Loans (An Overview)

A significant proportion of demand for gold jewellery i.e. about 60 -65 percent

comes from tier two towns and rural parts of the country11. Since most rural

pockets still do not have access to formal banking facilities12, investment in gold

is usually preferred as it offers a hedge against inflation.

Another benefit of investing in gold is its use as a collateral to satisfy immediate

liquidity requirements. Borrowings against gold as a collateral have been an age

old practice in India, mainly in the informal market, a part of which has

subsequently been captured by formal loan companies.13 Commercial and

Co-operative banks as well as the non-deposit taking, systemically important

NBFCs (NBFC-ND-SI) are some of the prominent players in the formal market for

gold loans14. Over time, total outstanding gold loans (sum total of banks and

NBFCs) have exhibited a rising trend15 (Table 2).

Factors such as higher loan to value ratios coupled with relatively easy disbursals

have contributed towards increasing the demand for gold loans and

consequently for gold jewellery. This has ultimately impacted the level of gold

imports16. It has been estimated that 1 percent change in gold loans leads to

0.3 percent change in volume of gold imports.17

Table 2: Annual Growth Rate of Gold Loans Outstanding (In percent)

52.5

62.6

67.2

78.3

41.4

169.3

126.7

80

54.2

47.7

52.1

77.6

2008-09

2009-10

2010-11

2011-12

Bank Gold Loans NBFC Gold Loans Total Gold Loans

Source: Report of the Working Group to Study the Issues Related to Gold Importsand Gold Loans NBFCs in India, RBI

4

7

18) “Why India Needs a Gold Policy”, FICCI, Dec. 2014.19) The actual imports in 2014 amounted to 769

tonnes as per World Gold Council. 20) Rangarajan, C., “Containing the Demand for Gold”, 6th

International Gold Summit, The Associated Chambers of Commerce and Industry of India, New Delhi,

May 2013. 21) “All Scheduled Commercial Banks authorised to deal in Gold”, RBI, February 14, 2013.

http://www.rbi.org.in/scripts/NotificationUser.aspx?Id=7865&Mode=0. 22) “Why India Needs a Gold

Policy”, FICCI and World Gold Council, Nov.2014

Stemming Gold Imports:Key Areas of Concern

Approximately 22,000 tonnes of gold is estimated to be lying with the Indian

Households18. Even if a small percentage of the estimated stock is brought into

circulation, it may lead to a considerable reduction in gold imports and help India

gain self-sufficiency in the product. Considering the hypothetical case presented

in Table 3, the imports in 2014 would have amounted to approximately 300 tonnes

instead of the actual 769 tonnes if 2 percent of the estimated stock was mobilised

and recycled.19

Several solutions such as the Gold Deposit Scheme (GDS), Gold

Exchange-Traded Funds (ETFs) as well as the possibility of setting up a bullion

corporation have been suggested and even implemented20. While the Gold

Deposit Scheme has met with limited success, Gold ETFs have actually

exacerbated the problem of growing dependency on gold imports. The RBI

introduced the Gold Deposit Scheme (GDS) in 1999 with the objective of bringing

privately held gold into circulation21. Some of the main attributes of the scheme

include interest rate on deposited gold, partial withdrawal of deposited gold,

maturity period ranging from six months to seven years, pre-payment of the

deposit, etc.22

1Table 3: Possible Impact of Release of ‘Under the Pillow’ Gold on Imports

22,000

400 (approximately)

400 (approximately)

Total amount of gold estimated to beresting with the Indian households

Mobilisation and recycling of 2% of theestimated amount annually

Expected annual fall in imports

Amount (in tonnes)

Source: Author’s calculations based on the available estimates of gold lying with the Indian households

5

8

23) Refer to footnote 22 . 24) Rangarajan, C., “Containing the Demand for Gold”, 6th International Gold

Summit, The Associated Chambers of Commerce and Industry of India, New Delhi, May 2013

Products such as GDS and Gold ETFs are therefore not complete solutions in

themselves and need to be supplemented with an overall system overhaul

involving upgradation of domestic infrastructure for recycling gold coupled with

appropriate regulatory measures.

Although all Scheduled Commercial Banks (SCBs) are authorised by the RBI to

accept gold deposits, currently only a few select banks i.e. State Bank of India,

Indian Overseas Bank and Corporation Bank offer GDS. Partial success of the

scheme has been primarily attributed to an unreasonably high minimum amount

of deposit (500 grams), lack of assaying facilities and absence of

standardisation norms.23

Gold ETFs in India are required to maintain 100 percent gold reserves against

investments. Moreover, the gold held in reserves needs to be LBMA certified.

Demand for ETF units therefore, cannot be delinked from demand for gold which

suggests a direct relationship between ETFs and gold imports (Fig.3). Hence,

ETFs cannot be considered as an effective instrument to stem gold imports since

they only defer demand instead of lowering it.24

Fig.3 Assets under Management in Gold ETFs and Imports of Gold (Monthwise)

Source: Association of Mutual Fund and Thomson Reuters

0

50

100

150

200

250

300

350

0

2000

4000

6000

8000

10000

12000

14000

Dec-11 Mar-12 Sep-12 Dec-12 Mar-13 Sep-13 Dec-13 Mar-14

AUM (Rs.cr) LHS Imports (Rs. Bn) RHS

9

25) “All that glitters is Gold: India Jewellery Review”, AT Kearney, FICCI, 2013. 26) Jose, J.,“Gold

Refining Industry in India”, Association of Gold Refineries and Mints. 27) Refer to footnote 26

28) http://www.lbma.org.uk/_blog/lbma_media_centre/post/mmtcpamp/

NCDEX ‘Gold Now’ Forwards: Enabling India to become self - sufficient in gold

Gold bullion imported into India (from global refineries) is certified by London

Bullion Market Association (LBMA). Gold used in the Indian financial system i.e.

gold reserves under ETFs and gold bought back by banks is also required to be

LBMA approved25. Operations of the Indian gold refineries are based on gold

dore bars imported mainly from Africa and Latin America as well as scrap gold

supplied in the domestic market26.

Domestic gold refineries are currently operating at 25 percent of their installed

capacity27. Fall in the domestic scrap supply in the recent past (Fig.4) has also

adversely impacted the business of the refineries. Fig. 4 also shows domestic

scrap supply has a direct positive relationship with the price of gold. More

importantly, since domestic gold refineries (apart from MMTC-PAMP) do not enjoy

the same status as LBMA accredited refineries, it severely retards their growth.

MMTC-PAMP was the first Indian refinery to get the LBMA certification in 201428. It

is, however, an extremely difficult and cumbersome procedure to receive LBMA

accreditation. In order to create self-sufficiency in gold, it is imperative to devise

ways and methods to upgrade the status of domestic gold refineries.

6

4Figure : Scrap Gold Supply and Price of Gold in India

Source: GFMS, Thomson Reuters and Handbook of Statistics on the Indian Economy

0

5000

10000

15000

20000

25000

30000

35000

0

20

40

60

80

100

120

2010 2011 2012 2013

Scrap Gold (in tonnes) LHS Price (10 gms) RHS

10

29) “Banks in the Southern states rejected a reasonable amount of gold deposit under the GDS scheme

owing to lack of proper assaying facilities”, “Why India needs a Gold Policy”, FICCI, Dec. 2014.

30) Rangarajan, C., “Containing the Demand for Gold”, 6th International Gold Summit, The Associated

Chambers of Commerce and Industry of India, New Delhi, May 2013. 31) “Why India needs a Gold

Policy”, FICCI, Dec. 2014.

NCDEX ‘Gold Now’ forwards is an initiative towards encouraging domestic supply

of gold by providing an impetus to the Indian gold refinery industry. The

underlying scheme entails NCDEX accreditation to domestic gold refineries

based on international quality parameters and standards where a stipulated

minimum level of production and tangible net worth, as well as audit of financial

statements comprise some of the basic qualifying criterion. A stringent procedure

for sample assaying is also a part of the process. Standardisation accorded to the

domestic refiners will add credibility to the quality of domestic gold and also

widen its acceptance in the Indian financial system29. NCDEX ‘Gold Now’

forwards, by encouraging only ‘India Good Delivery Gold’ to be delivered on the

exchange can thus help in creation of a professional domestic refinery industry

similar to that achieved in the warehousing industry a few years ago.

At present, gold is bought and sold through both formal and informal channels30.

As pointed earlier, an estimated stock of 22,000 tonnes is lying with the Indian

households. A small percentage of this stock if mobilised effectively could help

create a domestic supply channel for gold. In order to encourage supply of

privately held gold into the system, it is important to facilitate transparent price

formation mechanism, upgrade domestic refinery infrastructure and introduce

innovative financial schemes while modifying existing products (such as the Gold

Deposit Scheme). A survey by FICCI (2014) shows that consumers are willing to

part with their gold if provided with the right kind of incentives in the form of

properly structured savings and investment products. It also shows that

attachment to ancestral gold is not as rigid as it is perceived to be31.

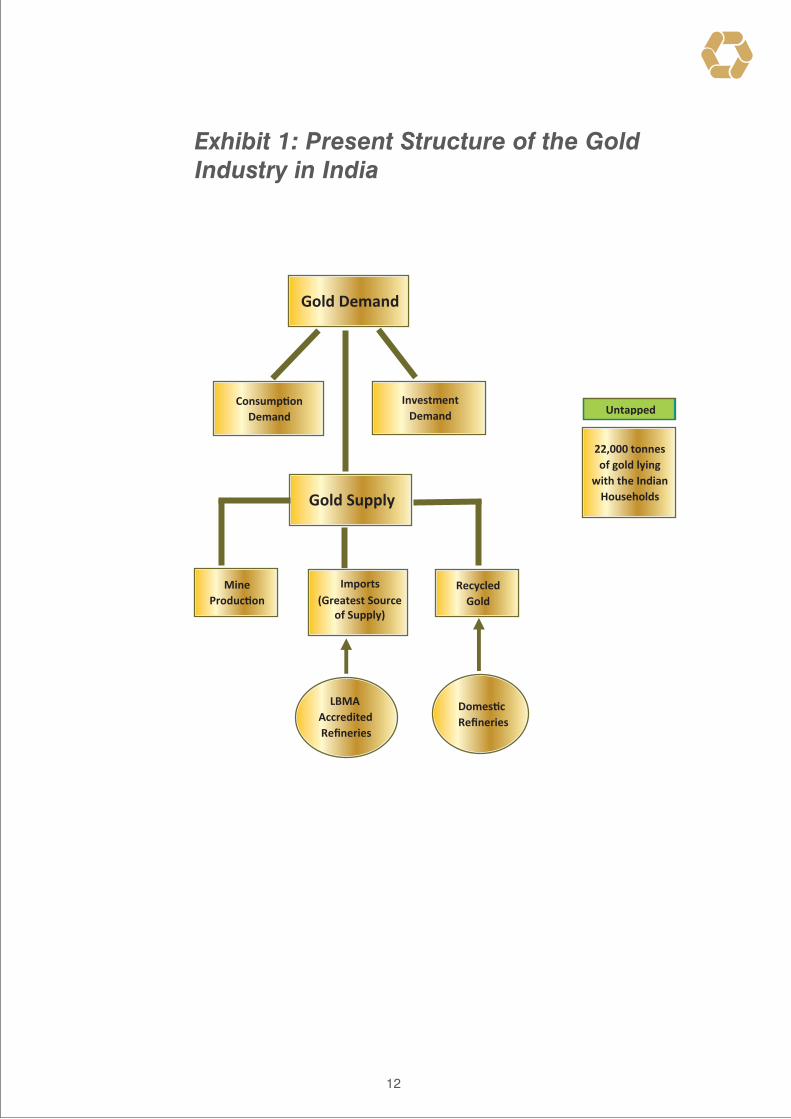

Exhibits 1 and 2 present the current and the proposed structure of gold industry

in India.

11

Exhibit 1: Present Structure of the Gold Industry in India

12

Gold Demand

Consumption Demand

Investment Demand

Gold Supply

Mine Production

Recycled Gold

LBMA Accredited Refineries

22,000 tonnes of gold lying

with the Indian Households

Untapped

Domestic Refineries

Imports(Greatest Source

of Supply)

Exhibit 2: Proposed Structure of the Gold Industry in India

Gold Demand

Consumption Demand

Investment Demand

Gold Supply

Mine Production

Imports Recycled Gold

LBMA Accredited Refineries

22,000 tonnes of gold lying with

the Indian Households

NCDEX Accredited Refineries

Market for buying and selling gold

Gold Deposit Scheme

13

Other Ways to Achieve Self-Sufficiency in Gold

Initiatives taken to upgrade the infrastructure of the domestic gold industry

need to be accompanied with commensurate policy response. Since gold is

increasingly being preferred as an investment class, innovative solutions to tap

this component of demand need to be developed. Some of these are

explained below -

Gold Certificates

Investment demand for gold could be captured without actually creating the need

to physically hold the gold by way of issuance of gold certificates. Gold certificates

are essentially a way to invest in gold without actually physically owning it. Since

the investment in gold is restricted to owning the paper, such certificates represent

a great substitute to the purchase of bars and coins. The issuer i.e. the bank

entitles the investor to redeem the amount of gold (in cash) specified on the

certificate according to the value of gold on the day of redemption.

If investment demand for gold in the form of bars and coins could be substituted

with gold certificates, there will be an additional advantage of earning interest on

the investment apart from the relief of physically storing gold. Gold certificates can

be of two kinds i.e. allocated and unallocated. In case of an allocated gold

certificate, the bank holds the amount of gold specified on the certificate while

unallocated gold certificates are usually not backed by any physical gold.

India Branded Gold Coins

The Government could also promote India branded gold coins which could be

minted by recycling gold. Commencement of work on developing the Indian gold

coin as announced in the Budget (2015-16) is a step in this direction. Gold

currently estimated to be lying with the Indian households could be brought into

the system to be recycled by recognised domestic refineries. Additional

measures could also be undertaken to develop an effective channel for buying

and selling gold.

7

14

Table 4: Daily Gold Rates (`per 10 gms) in different cities

(9th Feb-16th Feb 2015)

Source: Thomson Reuters

Pricing of Gold in India

Although a high positive correlation is observed between domestic and

international gold prices32, there is no clear criteria for pricing of gold in India.

Domestic price of gold is a function of the international price of gold, India/US

exchange rate, customs duty and local premium.33 The divergence in domestic

and international price of gold is mainly explained by customs and premium

component. While determining the price of gold applicable to each state, an

additional component of Value Added Tax (usually in the range of 1-2 percent)

also gets added.

An Example

We consider the landed domestic gold price for 12th of Feb 2015 (`27120/10

gms) derived from the international price on the same day (Table 3 in the

appendix). We also consider the local gold prices for three cities i.e. Ahmedabad,

Mumbai and Chennai on the same day. It can be seen that the local price of gold

as on 12th Feb. 2015 in all three cities in question deviates from the derived

landed price (Table 4). The data also suggests variation in gold pricing across the

cities on 12th Feb. 2015 and all other days of the week considered in the example.

Since the VAT component (1-2 percent) is almost uniform across all states, it is

mainly the local premium which can be held responsible for the state-wise

divergence in gold pricing.

Date Ahmedabad Mumbai Chennai

2/11/2015

2/12/2015

2/13/2015

2/16/2015

2/9/2015 27,400 27,200 27,650

27,600

27,480

27,500

27,550

27,200

26,700

26,800

27,000

27,375

27,200

27,225

27,325

8

32) Report of the Working Group to Study the Issues Related to Gold Imports and Gold Loans NBFCs

in India, RBI, Feb 2013. 33) Domestic price of gold is arrived at by multiplying the international price of

gold with the RBI reference rate and adjusting the same for custom duties and tariff values as well as

value added tax (for local pricing of gold). A local premium component is then added to this.

15

Apart from this, significant changes in daily gold rate for a particular state can also

be observed. Fig. 5 provides movement in daily gold rates for Ahmedabad for the

week of 9th Feb. 2015. There is a lack of clarity on the assessment of the premium

component embedded in the local price of gold. Not only does it vary across

states but is also subject to volatility within a particular area/state.

NCDEX ‘Gold Now’ forwards aim to promote transparency in domestic gold

pricing by subjecting it to the market forces. In addition, under the scheme of

NCDEX Gold Futures, the premium component will be polled by an independent

and unbiased entity which will further add to the transparency.

Source: Reuters Database

27,100

27,150

27,200

27,250

27,300

27,350

27,400

27,450

09-02-2015 11-02-2015 12-02-2015 13-02-2015 16-02-2015

16

Figure 5: One week’s gold rate movement in Ahmedabad (per 10 gms) (in Rs.)

Conclusion

Gold occupies a special place in the Indian economy. Apart from being acquired

for consumption purposes, it is also increasingly being preferred as an investment

class. Since domestic production of gold is close to negligible, almost entire

demand is met by imports which has exerted pressure on India’s current account

balance. Enabling India to become self-sufficient in gold by generating domestic

supply channels is therefore extremely crucial.

Approximately 22,000 tonnes of gold has been estimated to be lying with the

Indian households, in addition to the stock with the temple trustees. Efforts need

to be directed towards developing ways to mobilise and recycle the estimated

stockpile so as to create a domestic market for gold. Upgradation and

refurbishment of the domestic gold refinery and recycling infrastructure becomes

imperative in this context.

By launching ‘India Good Delivery based gold forwards, NCDEX plans to

encourage domestic supply of gold and stem the growing reliance on imports. In

the process, NCDEX also plans to standardise the domestic refineries through

accreditation as per international quality parameters. The forwards gold platform

will also be ideal for jewellers to help them efficiently manage their inventories.

The gems and jewellery sector in India is dominated by MSMEs34. Since the sector

is one of the major contributors to India’s exports, its growth is important for

India’s external sector. Creation of domestic supply of gold will also help such

MSMEs move up the value chain and receive a better pricing for their inputs

through transparent price discovery.

Effective monetisation of gold and creation of its domestic supply however calls

for appropriate policy response in both regulatory and monetary spheres. Banks

could also devise ways to spread greater awareness on the benefits of depositing

gold so as to mop up the ‘under the pillow’ stock currently lying with the Indian

households and temple trustees and put it to effective use.

9

34) “All that glitters is Gold: India Jewellery Review”, AT Kearney, FICCI, 2013

17

860 825

117

10

987

87.13

101

7

934

88.33

769

77

9

855

89.94

969

59

12

1039

93.26

2011 2012 2013 2014

Net imports, available for domesticconsumption

Domestic supply from recycled gold (a)

Domestic supply from other sources (b)

Total supply

Imports as a percentage of total supply

References

i. “Committee on Comprehensive Financial Services for Small Businesses and Low Income Households”, RBI, Dec. 2013

ii. Gold Demand Trends, World Gold Council, Full Year 2014

iii. Gupta, S. et al, “All that glitters is Gold: India Jewellery Review, 2013”, AT Kearney and FICCI, November 2013.

iv. Jose, J. “Gold Refining Industry in India”, Association of Gold Refineries and Mints

v. “Why India Needs a Gold Policy”, FICCI, Dec. 2014

vi. Kanjilal, K., and Ghosh, S., “Income and price elasticity of gold import demand in India: Empirical Evidence from threshold and ARDL bounds test cointegration”, Resources Policy 41 (2014), 135-142

vii. Rosch, A. and Schmidbauer,H., “Impact of Festivals on Gold Price Expectation and Volatility”, FOM University of Applied Sciencies, Munich, Germany, 2012.

viii. Report of the Working Group to Study the Issues Related to Gold Imports and Gold Loans NBFCs in India, RBI, Feb 2013

ix. “Surveying the Indian Gold Loan Market”, Cognizant 20-20 insights, January 2012

x. Rangarajan, C., “Containing the Demand for Gold”, 6th International Gold Summit, The Associated Chambers of Commerce and Industry of India, New Delhi, May 2013

Appendix

Table 1: Supply of Gold in India (in tonnes)

Source: World Gold Council, Gold Demand Trends Report and GFMSNote: a) Domestic supply from local mine production, recovery from imported copperconcentrates and disinvestment. b) This supply can be consumed across the three sectors -jewellery, investment and technology. Consequently, the total supply figure in the table willnot add to jewellery plus investment demand for India.

18

Table 3: Domestic gold price (24 carat) derivation from the international price

as on 12th Feb. 2015

Table 2: Components of Gold Demand in India (in tonnes)

16

14

12

12

349

368

312

362

1,007

986

864

975

Dec-2010

Dec-2011

Dec-2012

Dec-2013

STEP 1 LBMA AM price of gold as on 12th Feb 2015

(in USD/Troy oz)

CONVERSION TO RS./KG (31.9899927)

RBI REFERENCE RATE on 12th Feb 2015

PRICE OF 1 KG OF GOLD (In Rs.)

CUSTOMS TARIFF VALUE for 12th Feb 2015

CUSTOMS DUTY

DOMESTIC SPOT PRICE ROUNDED OFF

(RS./10 GRAMS)

PRICE OF 1 KG OF GOLD INCLUDING

CUSTOMS DUTY

CURRENCY RATE BY CBEC FOR

IMPORTS/EXPORTS on 12th Feb 2015

STEP 2

STEP 3

STEP 4

Consumer Demand Investment Demand Industrial Demand

Source: GFMS, Thomson Reuters

Source: Author’s calculations

31.9899927

$412/10 GRAMS

62.45

10.30%

39195.73856

62.43

2446989.958

1225.25

2572940

265012.82

2712002.778

27120

Figure 1 : Demand Inelasticity of Gold in India

Source: GFMS, Thomson Reuters and Handbook of Statistics on the Indian Economy 2013 - 14

05000100001500020000250003000035000

0

200

400

600

800

1000

1200

Pric

e of

gol

d (R

s pe

r 10

gm

)

Gol

d D

eman

d (in

Ton

nes)

Consumer Demand Price of gold

19

20

Disclaimer: Trading in commodities contracts is subject to inherent market risks and the traders/investors should understand and consult their financial advisers before trading/investing. The contents in this publication are for guidance only and should not be treated as recommendatory or definitive. Neither NCDEX nor the NCDEX IPF Trust or their affiliates, associates, representatives, directors, employees or agents shall be responsible in any manner to any person or entity for any decisions or actions taken on the basis of this publication. No part of this publication may be redistributed or reproduced without written permission from NCDEX.

National Commodity & Derivatives Exchange Limited,

Akruti Corporate Park,1st Floor, Near G.E.Garden, L.B.S. Marg,

Kanjurmarg (West), Mumbai - 400 078

Tel.: (+91-22) 66406609-13 | Fax: (+91-22) 66406899

E-mail: [email protected]

CIN: U51909MH2003PLC140116

NCDEX Investor (Client) Protection Fund Trust

Issued in Public Interest