Embed Size (px)

Citation preview

www.pwc.de

Going East in Life Science:An Introduction

4th DVFA – Life Science ConferenceFrankfurt, May 17, 2011

Dr. Martin SchlohHead of Pharma &Healthcare Consulting Practicein Germany

PwC

Agenda

1. China will become a superpower in Pharma & Healthcare

2. Overview of the investment trends in China along the Pharmaceutical Value Chain

3. Overview of Chinese Life Science M&A

May 2011Going East in Life Science

Slide 2

PwC

China will become a superpower in Pharma & Healthcare

3

PwC

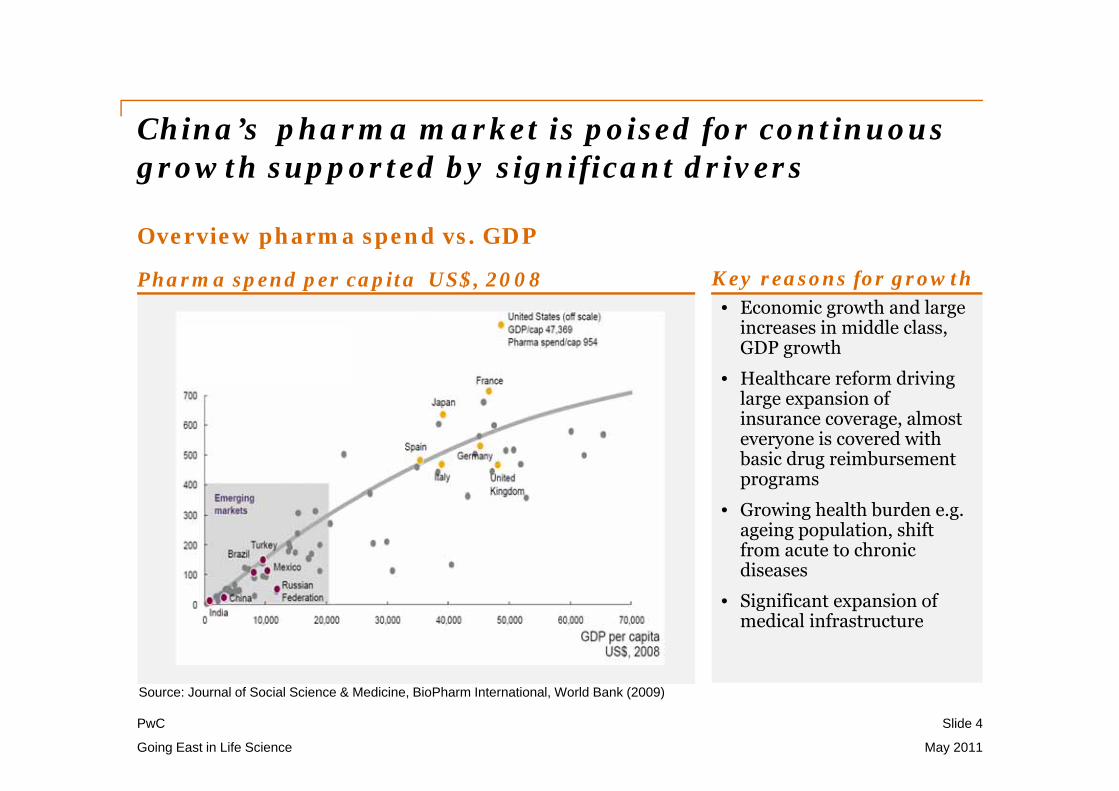

China’s pharma market is poised for continuous growth supported by significant drivers

Slide 4

Going East in Life Science May 2011

Overview pharma spend vs. GDP

Pharma spend per capita US$, 2008

Source: Journal of Social Science & Medicine, BioPharm International, World Bank (2009)

• Economic growth and large increases in middle class, GDP growth

• Healthcare reform driving large expansion of insurance coverage, almost everyone is covered with basic drug reimbursement programs

• Growing health burden e.g. ageing population, shift from acute to chronic diseases

• Significant expansion of medical infrastructure

Key reasons for growth

PwC

13,4

10,1 10,3

7,87,0 7,2

5.4

5,4

4,6 4,4

16,2

11,711,3

9,6 9,3 9,05.4

5,4

4,64,2

2000 2009

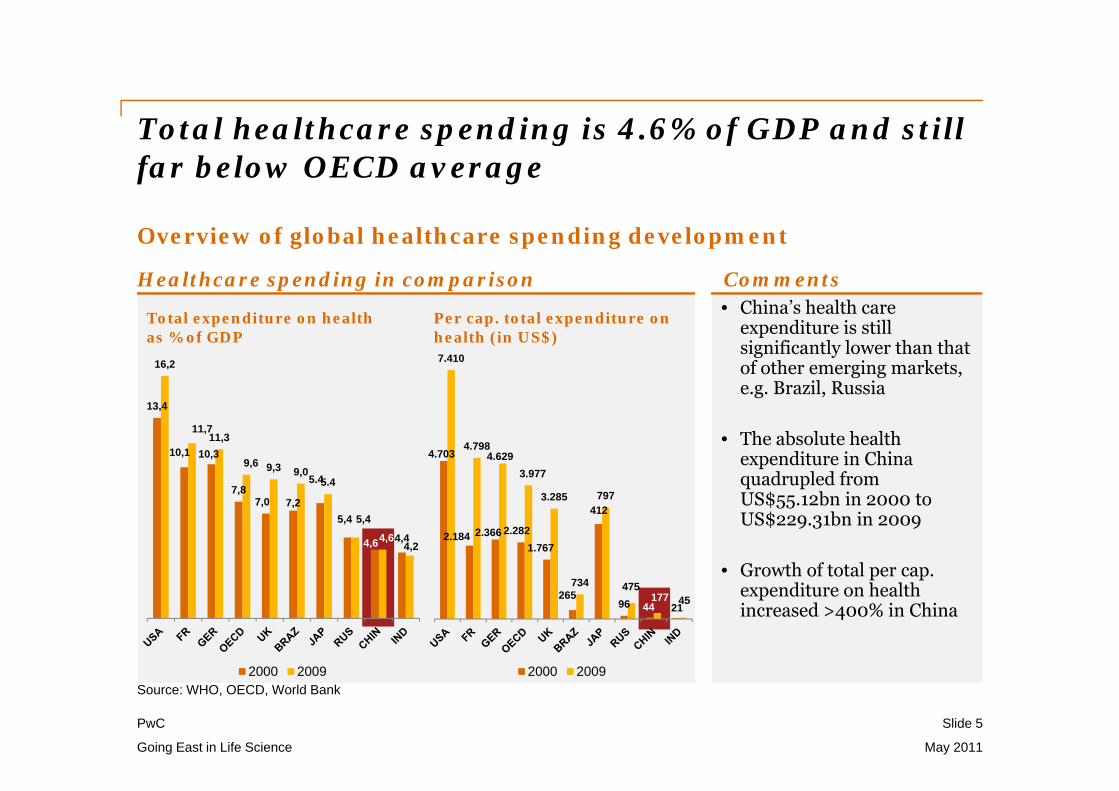

Total healthcare spending is 4.6% of GDP and still far below OECD average

Slide 5

Going East in Life Science May 2011

Overview of global healthcare spending development

Healthcare spending in comparison

Total expenditure on health as % of GDP

Per cap. total expenditure on health (in US$)

4.703

2.184 2.366 2.2821.767

265

412

96 44 21

7.410

4.7984.629

3.977

3.285

734

797

475177 45

2000 2009Source: WHO, OECD, World Bank

• China’s health care expenditure is still significantly lower than that of other emerging markets, e.g. Brazil, Russia

• The absolute health expenditure in China quadrupled from US$55.12bn in 2000 to US$229.31bn in 2009

• Growth of total per cap. expenditure on health increased >400% in China

Comments

PwC

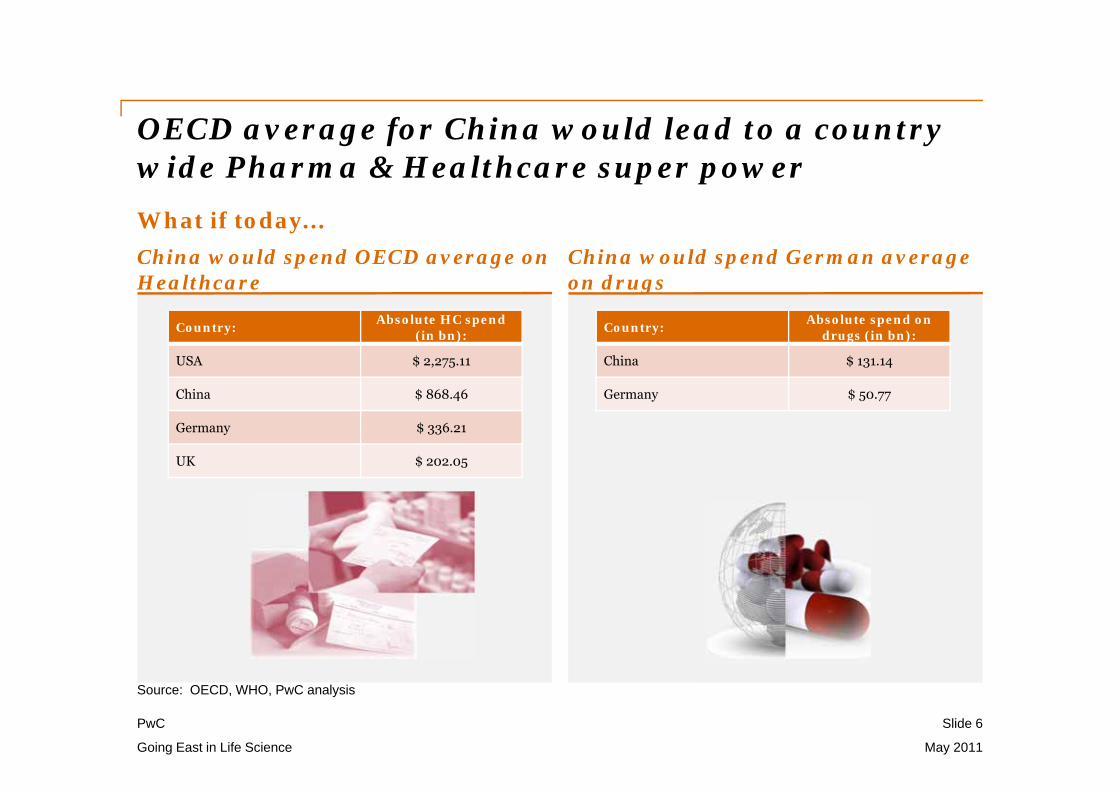

OECD average for China would lead to a country wide Pharma & Healthcare super power

Slide 6

Going East in Life Science May 2011

What if today...China would spend OECD average on Healthcare

Source: OECD, WHO, PwC analysis

China would spend German average on drugs

Country: Absolute HC spend (in bn):

USA $ 2,275.11

China $ 868.46

Germany $ 336.21

UK $ 202.05

Country: Absolute spend on drugs (in bn):

China $ 131.14

Germany $ 50.77

PwC

Chinese pharmaceutical market will become the third largest market by 2013

Slide 7

Going East in Life Science May 2011

Overview of global ranking of pharma markets

Source: IMS Health

2003 Rank

1 USA

2 Japan

3 Germany

4 France

5 Italy

6 UK

7 Spain

8 Canada

9 China

10 Brazil

2008 Rank

1 USA

2 Japan

3 France

4 Germany

5 China

6 Italy

7 UK

8 Spain

9 Canada

10 Brazil

2013 Rank

1 USA

2 Japan

3 China

4 Germany

5 France

6 Italy

7 Spain

8 Brazil

9 Canada

10 UK

PwC

€ in billion

3,4

5,8

18,0

5,7

11,2

10,1

12,0

14,5

17,8

51.9

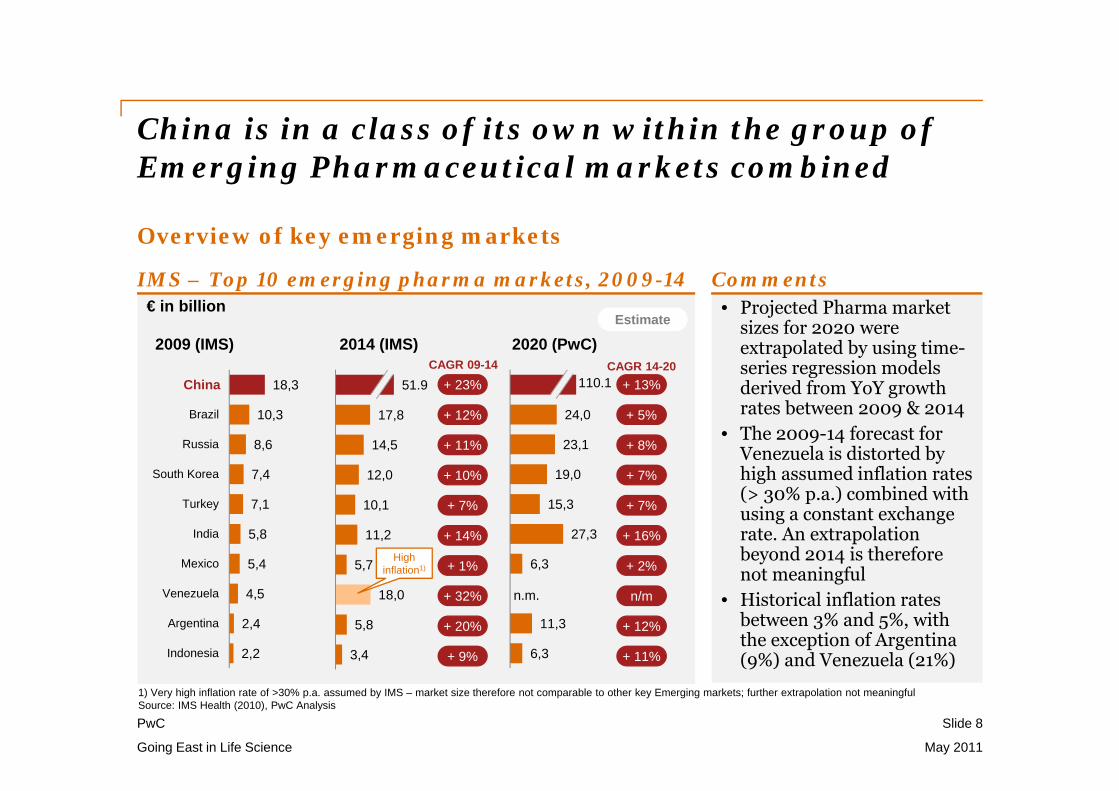

China is in a class of its own within the group of Emerging Pharmaceutical markets combined

Slide 8

Going East in Life Science May 2011

Overview of key emerging markets

IMS – Top 10 emerging pharma markets, 2009-14• Projected Pharma market

sizes for 2020 were extrapolated by using time-series regression models derived from YoY growth rates between 2009 & 2014

• The 2009-14 forecast for Venezuela is distorted by high assumed inflation rates (> 30% p.a.) combined with using a constant exchange rate. An extrapolation beyond 2014 is therefore not meaningful

• Historical inflation rates between 3% and 5%, with the exception of Argentina (9%) and Venezuela (21%)

Comments

1) Very high inflation rate of >30% p.a. assumed by IMS – market size therefore not comparable to other key Emerging markets; further extrapolation not meaningfulSource: IMS Health (2010), PwC Analysis

2,2

2,4

4,5

5,4

5,8

7,1

7,4

8,6

10,3

18,3

Indonesia

Argentina

Venezuela

Mexico

India

Turkey

South Korea

Russia

Brazil

China

6,3

11,3

6,3

27,3

15,3

19,0

23,1

24,0

110.1

+ 5%

+ 8%

+ 7%

+ 7%

+ 16%

+ 2%

n/m

+ 11%

+ 12%

+ 23%

+ 12%

+ 11%

+ 10%

+ 7%

+ 14%

+ 1%

+ 32%

+ 9%

+ 20%

High inflation1)

China

n.m.

110.1 + 13%

2009 (IMS) 2014 (IMS) 2020 (PwC)CAGR 14-20CAGR 09-14

Estimate

PwC

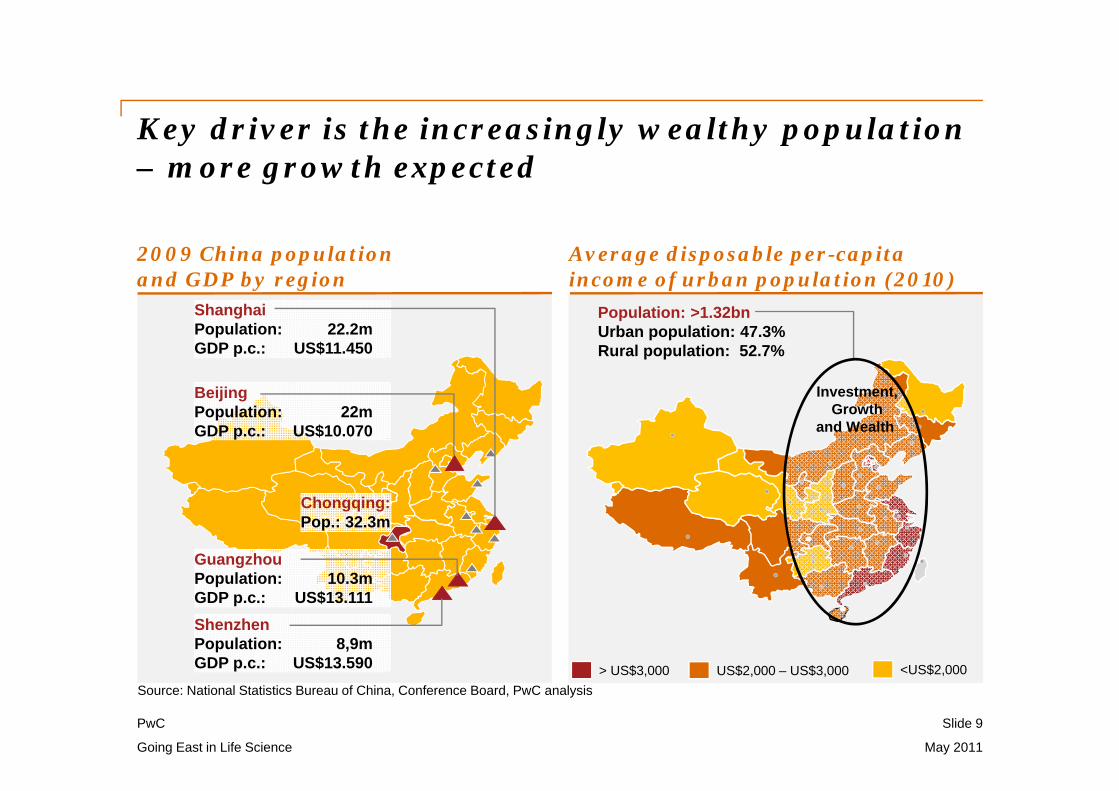

Key driver is the increasingly wealthy population – more growth expected

Slide 9

Going East in Life Science May 2011

2009 China populationand GDP by region

ShanghaiPopulation: 22.2mGDP p.c.: US$11.450

Chongqing:Pop.: 32.3m

Population: >1.32bnUrban population: 47.3%Rural population: 52.7%

> US$3,000 US$2,000 – US$3,000 <US$2,000Source: National Statistics Bureau of China, Conference Board, PwC analysis

GuangzhouPopulation: 10.3mGDP p.c.: US$13.111ShenzhenPopulation: 8,9mGDP p.c.: US$13.590

Investment,Growth

and Wealth

Average disposable per-capita income of urban population (2010)

BeijingPopulation: 22mGDP p.c.: US$10.070

PwC

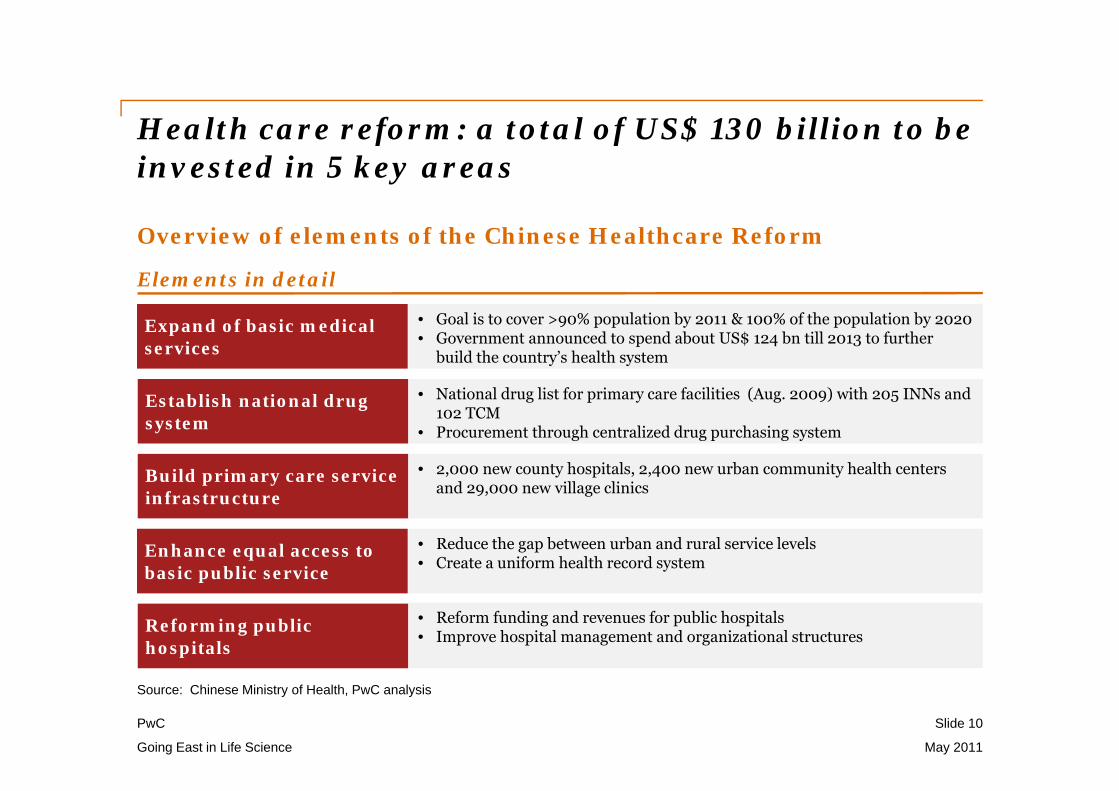

Health care reform: a total of US$ 130 billion to be invested in 5 key areas

Slide 10

Going East in Life Science May 2011

Overview of elements of the Chinese Healthcare Reform

Elements in detail

Expand of basic medical services

Establish national drug system

Build primary care service infrastructure

Enhance equal access to basic public service

Reforming public hospitals

• Goal is to cover >90% population by 2011 & 100% of the population by 2020• Government announced to spend about US$ 124 bn till 2013 to further

build the country’s health system

• National drug list for primary care facilities (Aug. 2009) with 205 INNs and 102 TCM

• Procurement through centralized drug purchasing system

• 2,000 new county hospitals, 2,400 new urban community health centers and 29,000 new village clinics

• Reduce the gap between urban and rural service levels• Create a uniform health record system

• Reform funding and revenues for public hospitals • Improve hospital management and organizational structures

Source: Chinese Ministry of Health, PwC analysis

PwC

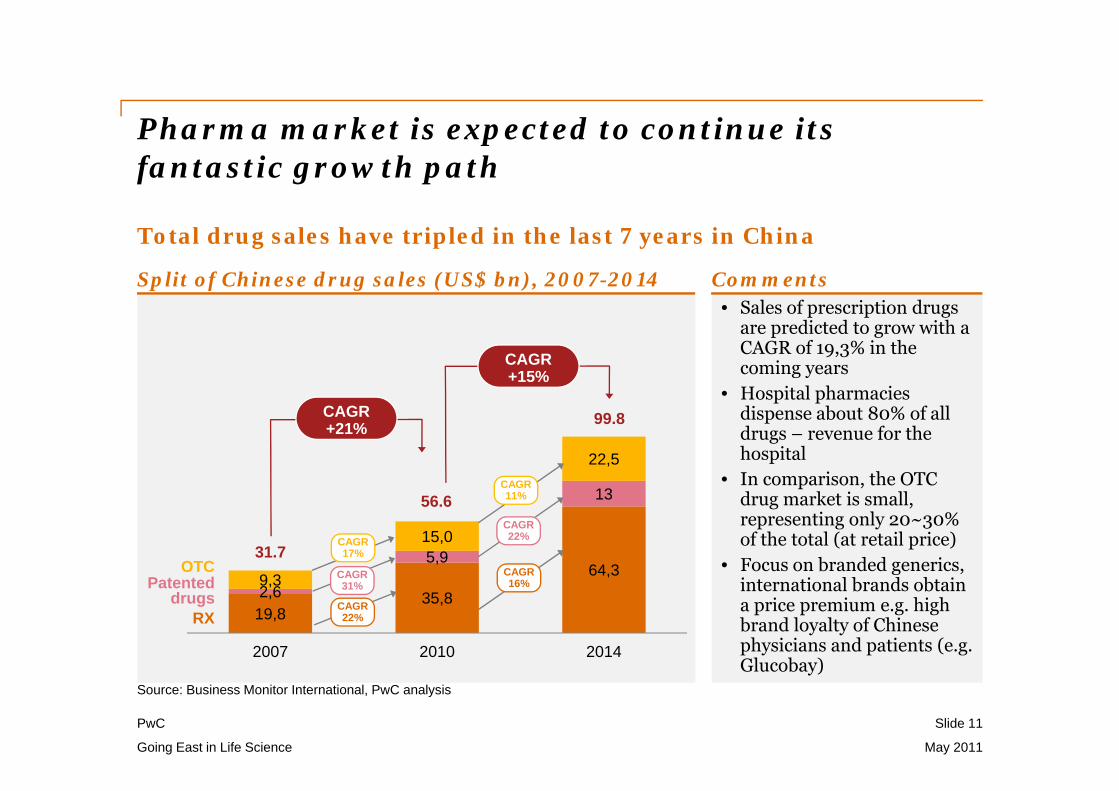

19,835,8

64,32,6

5,9

13

9,3

15,0

22,5

2007 2010 2014

Pharma market is expected to continue its fantastic growth path

Slide 11

Going East in Life Science May 2011

Total drug sales have tripled in the last 7 years in China

Source: Business Monitor International, PwC analysis

• Sales of prescription drugs are predicted to grow with a CAGR of 19,3% in the coming years

• Hospital pharmacies dispense about 80% of all drugs – revenue for the hospital

• In comparison, the OTC drug market is small, representing only 20~30% of the total (at retail price)

• Focus on branded generics, international brands obtain a price premium e.g. high brand loyalty of Chinese physicians and patients (e.g. Glucobay)

CommentsSplit of Chinese drug sales (US$ bn), 2007-2014

CAGR 31%

31.7

56.6

99.8

RX

OTCPatented

drugs

CAGR+21%

CAGR+15%

CAGR 22%

CAGR 17%

CAGR 22%

CAGR 16%

CAGR 11%

PwC

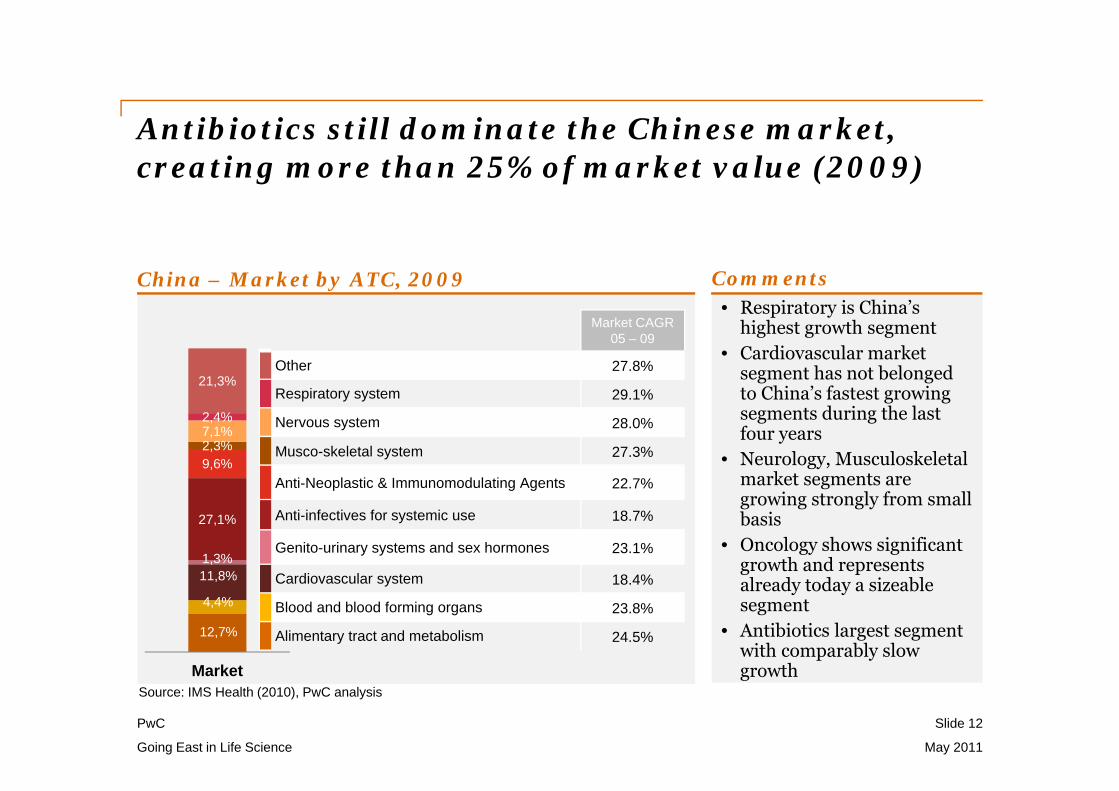

12,7%

4,4%

11,8%1,3%

27,1%

9,6%2,3%7,1%2,4%

21,3%

Market

Antibiotics still dominate the Chinese market, creating more than 25% of market value (2009)

Slide 12

Going East in Life Science May 2011

China – Market by ATC, 2009

Source: IMS Health (2010), PwC analysis

• Respiratory is China’s highest growth segment

• Cardiovascular market segment has not belonged to China’s fastest growing segments during the last four years

• Neurology, Musculoskeletal market segments are growing strongly from small basis

• Oncology shows significant growth and represents already today a sizeable segment

• Antibiotics largest segment with comparably slow growth

Comments

Market CAGR05 – 09

Other 27.8%

Respiratory system 29.1%

Nervous system 28.0%

Musco-skeletal system 27.3%

Anti-Neoplastic & Immunomodulating Agents 22.7%

Anti-infectives for systemic use 18.7%

Genito-urinary systems and sex hormones 23.1%

Cardiovascular system 18.4%

Blood and blood forming organs 23.8%

Alimentary tract and metabolism 24.5%

PwC

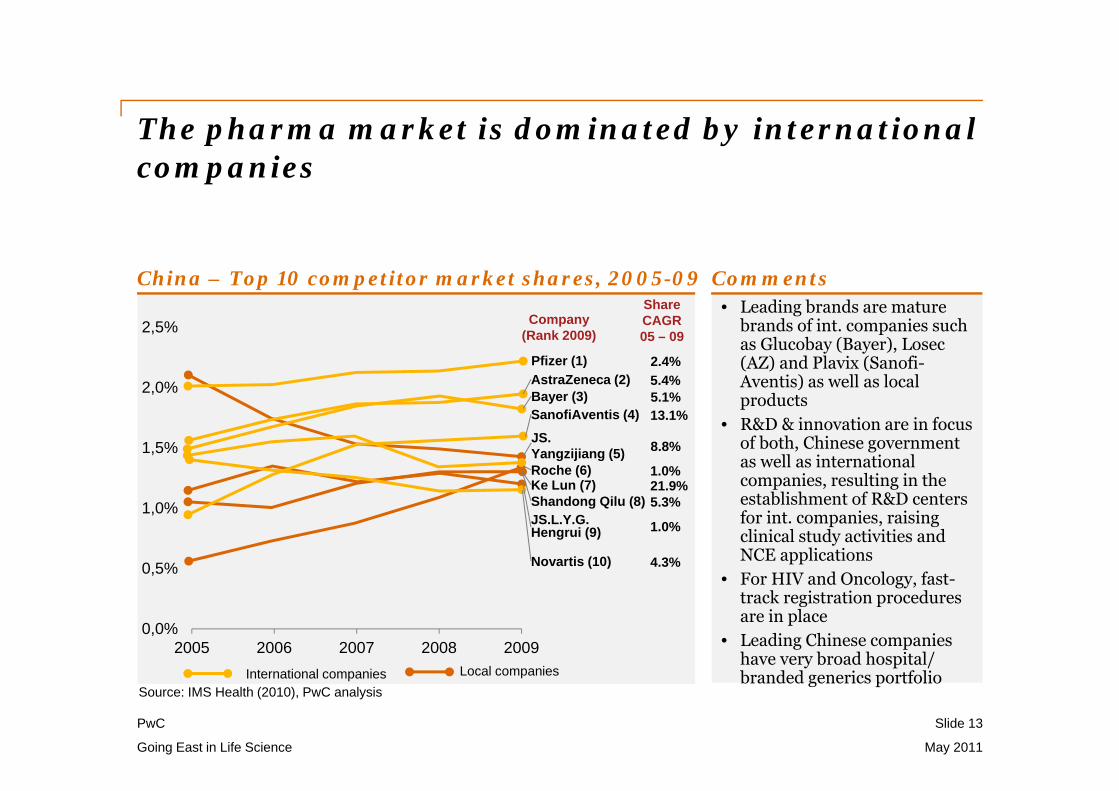

The pharma market is dominated by international companies

Slide 13

Going East in Life Science May 2011

China – Top 10 competitor market shares, 2005-09

Source: IMS Health (2010), PwC analysis

• Leading brands are mature brands of int. companies such as Glucobay (Bayer), Losec(AZ) and Plavix (Sanofi-Aventis) as well as local products

• R&D & innovation are in focus of both, Chinese government as well as international companies, resulting in the establishment of R&D centers for int. companies, raising clinical study activities and NCE applications

• For HIV and Oncology, fast-track registration procedures are in place

• Leading Chinese companies have very broad hospital/ branded generics portfolio

Comments

0,0%

0,5%

1,0%

1,5%

2,0%

2,5%

2005 2006 2007 2008 2009

Pfizer (1)

Bayer (3)AstraZeneca (2)

SanofiAventis (4)JS. Yangzijiang (5)Roche (6)

Shandong Qilu (8)Ke Lun (7)

JS.L.Y.G. Hengrui (9)

Novartis (10)

Company(Rank 2009)

ShareCAGR05 – 09

2.4%

5.1%5.4%

13.1%

8.8%

1.0%

5.3%21.9%

1.0%

4.3%

Local companiesInternational companies

PwC

Overview of the investment trends in China along the Pharmaceutical Value Chain

14

PwC

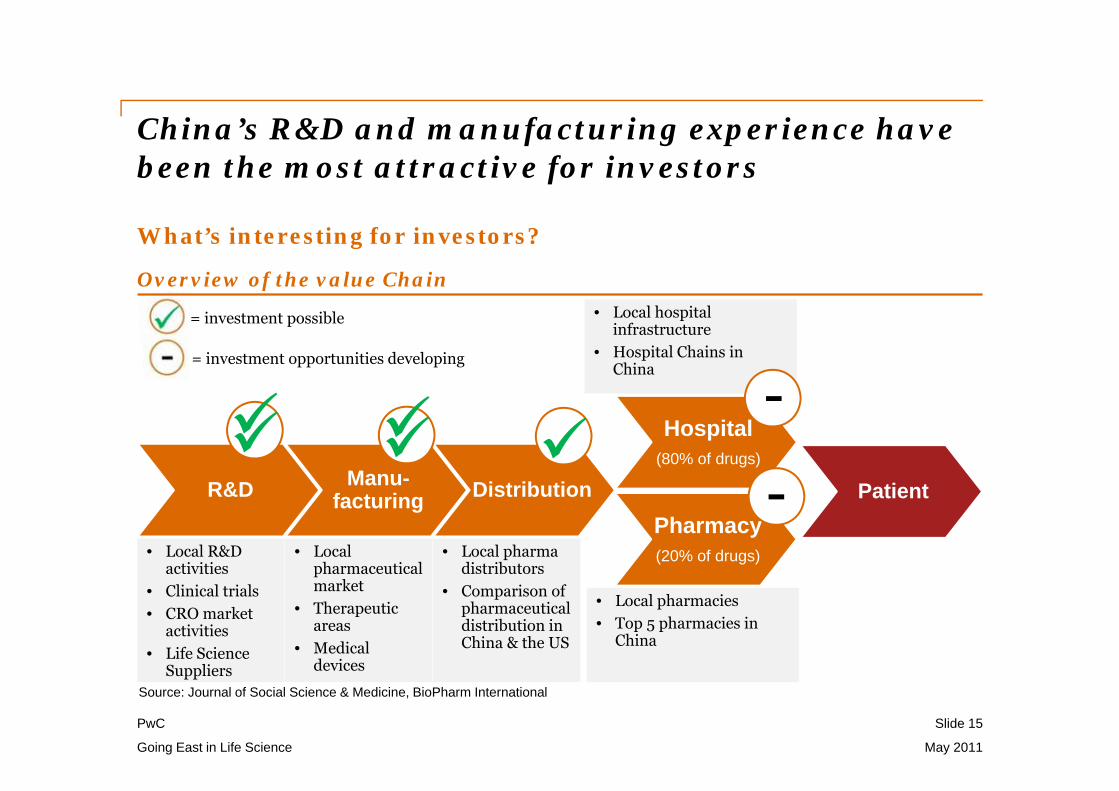

China’s R&D and manufacturing experience have been the most attractive for investors

Slide 15

Going East in Life Science May 2011

What’s interesting for investors?

Overview of the value Chain

Source: Journal of Social Science & Medicine, BioPharm International

R&D Manu-facturing Distribution

Hospital(80% of drugs)

PatientPharmacy(20% of drugs)• Local R&D

activities• Clinical trials• CRO market

activities• Life Science

Suppliers

• Local pharmaceutical market

• Therapeutic areas

• Medical devices

• Local pharma distributors

• Comparison of pharmaceutical distribution in China & the US

• Local hospital infrastructure

• Hospital Chains in China

• Local pharmacies• Top 5 pharmacies in

China

--

= investment possible

= investment opportunities developing

PwC

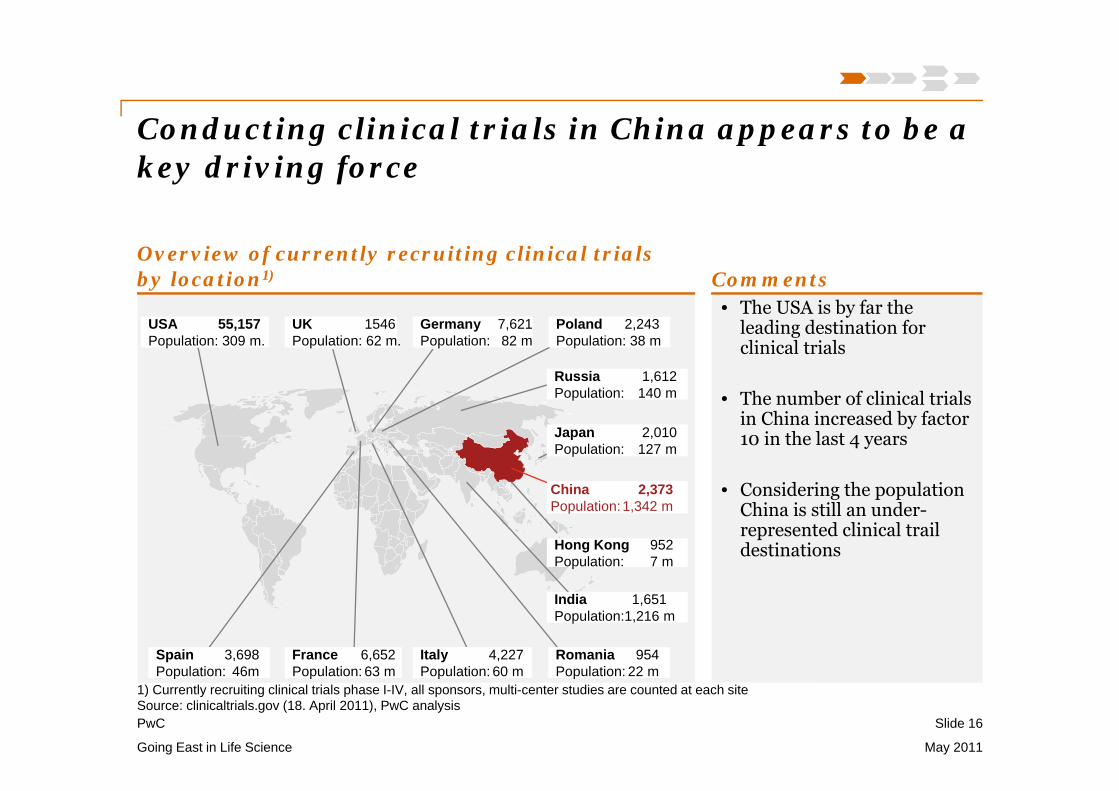

• The USA is by far the leading destination for clinical trials

• The number of clinical trials in China increased by factor 10 in the last 4 years

• Considering the population China is still an under-represented clinical trail destinations

Conducting clinical trials in China appears to be a key driving force

Slide 16

Going East in Life Science May 2011

Overview of currently recruiting clinical trials by location1)

Germany 7,621Population: 82 m

Poland 2,243Population: 38 m

Russia 1,612Population: 140 m

Japan 2,010Population: 127 m

China 2,373Population:1,342 m

Hong Kong 952Population: 7 m

India 1,651Population:1,216 m

Romania 954Population: 22 m

Italy 4,227Population: 60 m

Spain 3,698Population: 46m

France 6,652Population: 63 m

UK 1546Population: 62 m.

USA 55,157Population: 309 m.

Comments

1) Currently recruiting clinical trials phase I-IV, all sponsors, multi-center studies are counted at each siteSource: clinicaltrials.gov (18. April 2011), PwC analysis

PwC

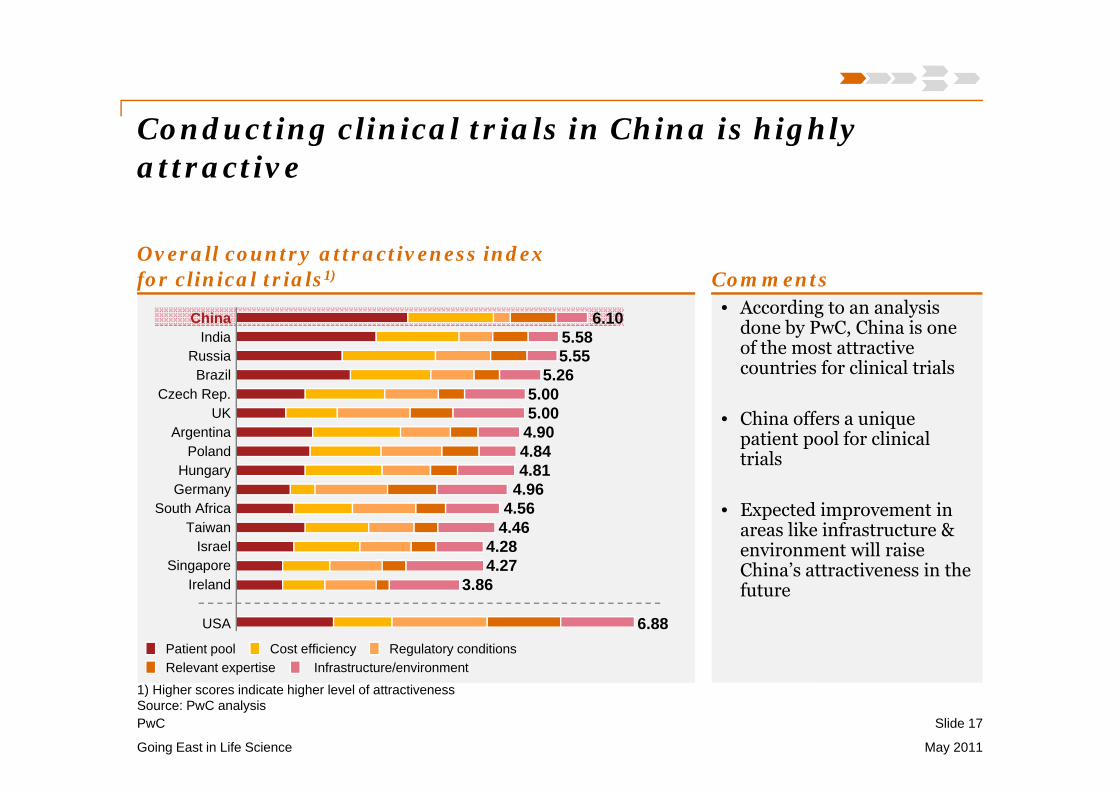

• According to an analysis done by PwC, China is one of the most attractive countries for clinical trials

• China offers a unique patient pool for clinical trials

• Expected improvement in areas like infrastructure & environment will raise China’s attractiveness in the future

Conducting clinical trials in China is highly attractive

Slide 17

Going East in Life Science May 2011

Overall country attractiveness indexfor clinical trials1) Comments

Patient pool Cost efficiency Regulatory conditionsRelevant expertise Infrastructure/environment

ChinaIndia

RussiaBrazil

Czech Rep.UK

ArgentinaPoland

HungaryGermany

South AfricaTaiwan

IsraelSingapore

Ireland

USA

6.105.585.55

5.265.005.00

4.904.844.81

4.964.56

4.464.284.27

3.86

6.88

1) Higher scores indicate higher level of attractivenessSource: PwC analysis

PwC

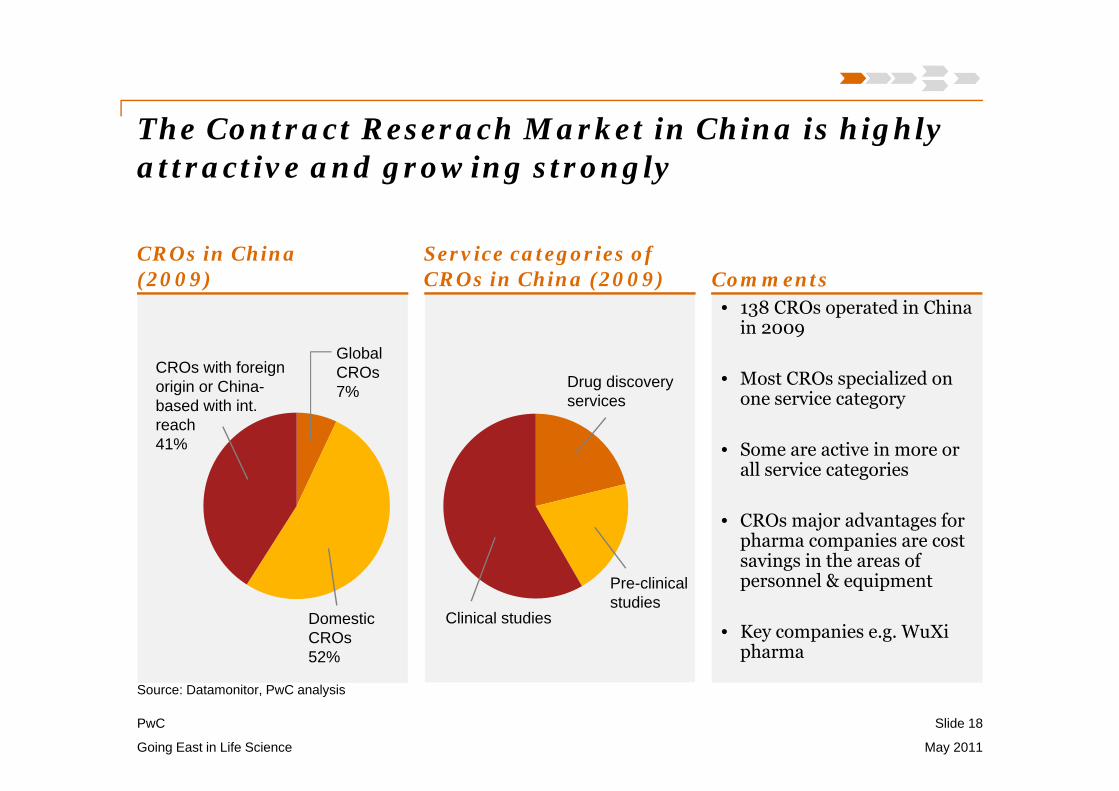

The Contract Reserach Market in China is highly attractive and growing strongly

Slide 18

Going East in Life Science May 2011

CROs in China(2009)

Source: Datamonitor, PwC analysis

• 138 CROs operated in China in 2009

• Most CROs specialized on one service category

• Some are active in more or all service categories

• CROs major advantages for pharma companies are cost savings in the areas of personnel & equipment

• Key companies e.g. WuXipharma

CommentsService categories of CROs in China (2009)

CROs with foreign origin or China-based with int. reach 41%

Drug discovery services

Domestic CROs 52%

Pre-clinical studies

Clinical studies

GlobalCROs7%

PwC

Multinational companies have located R&D activities to China

Slide 19

Going East in Life Science May 2011

R&D activities in China

• 10-year plan to establish research centre• Plans to employ over 1000 researchers at the

Shanghai research centre by 2017

• Spent >US$150m between 2005 and 2009• Consecutively moving research resources from

the USA to China

• Is planning to invest US$ .25b in R&D in China between 2009 and 2014

• Will employ 1000 R&D associates in China by 2014

• Built the first fully functional clinical drug R&D centre by a multinational in China (US$ 100m)

• Is planning to intensive its R&D activities in China continuing from 2011

• Opened a R&D headquarters in China in 2008• Estimates to spend US$100m on R&D in China

between 2008 and 2012

• Built a US$1oomn research centre in China in 2006

• Is in the process of constructing new R&D facilities in China at present

Source: Business Monitor International, China Daily, The Times, Datamonitor

PwC

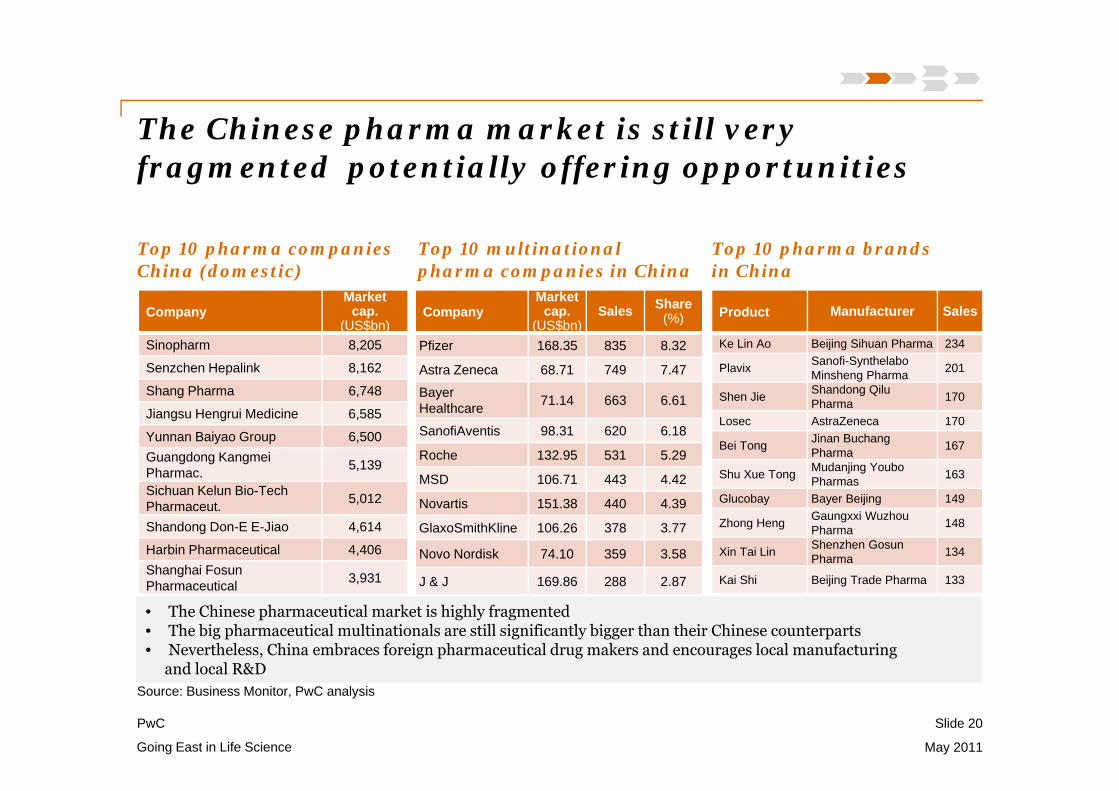

The Chinese pharma market is still very fragmented potentially offering opportunities

May 2011Going East in Life Science

Slide 20

Top 10 pharma companiesChina (domestic)

Top 10 multinational pharma companies in China

Top 10 pharma brandsin China

Source: Business Monitor, PwC analysis

CompanyMarket

cap. (US$bn)

Sales Share(%)

Pfizer 168.35 835 8.32

Astra Zeneca 68.71 749 7.47

Bayer Healthcare 71.14 663 6.61

SanofiAventis 98.31 620 6.18

Roche 132.95 531 5.29

MSD 106.71 443 4.42

Novartis 151.38 440 4.39

GlaxoSmithKline 106.26 378 3.77

Novo Nordisk 74.10 359 3.58

J & J 169.86 288 2.87

Product Manufacturer Sales

Ke Lin Ao Beijing Sihuan Pharma 234

Plavix Sanofi-SynthelaboMinsheng Pharma 201

Shen Jie Shandong QiluPharma 170

Losec AstraZeneca 170

Bei Tong Jinan BuchangPharma 167

Shu Xue Tong Mudanjing YouboPharmas 163

Glucobay Bayer Beijing 149

Zhong Heng Gaungxxi WuzhouPharma 148

Xin Tai Lin Shenzhen GosunPharma 134

Kai Shi Beijing Trade Pharma 133

• The Chinese pharmaceutical market is highly fragmented• The big pharmaceutical multinationals are still significantly bigger than their Chinese counterparts• Nevertheless, China embraces foreign pharmaceutical drug makers and encourages local manufacturing

and local R&D

CompanyMarket

cap. (US$bn)

Sinopharm 8,205

Senzchen Hepalink 8,162

Shang Pharma 6,748

Jiangsu Hengrui Medicine 6,585

Yunnan Baiyao Group 6,500Guangdong KangmeiPharmac. 5,139

Sichuan Kelun Bio-Tech Pharmaceut. 5,012

Shandong Don-E E-Jiao 4,614

Harbin Pharmaceutical 4,406Shanghai FosunPharmaceutical 3,931

PwC

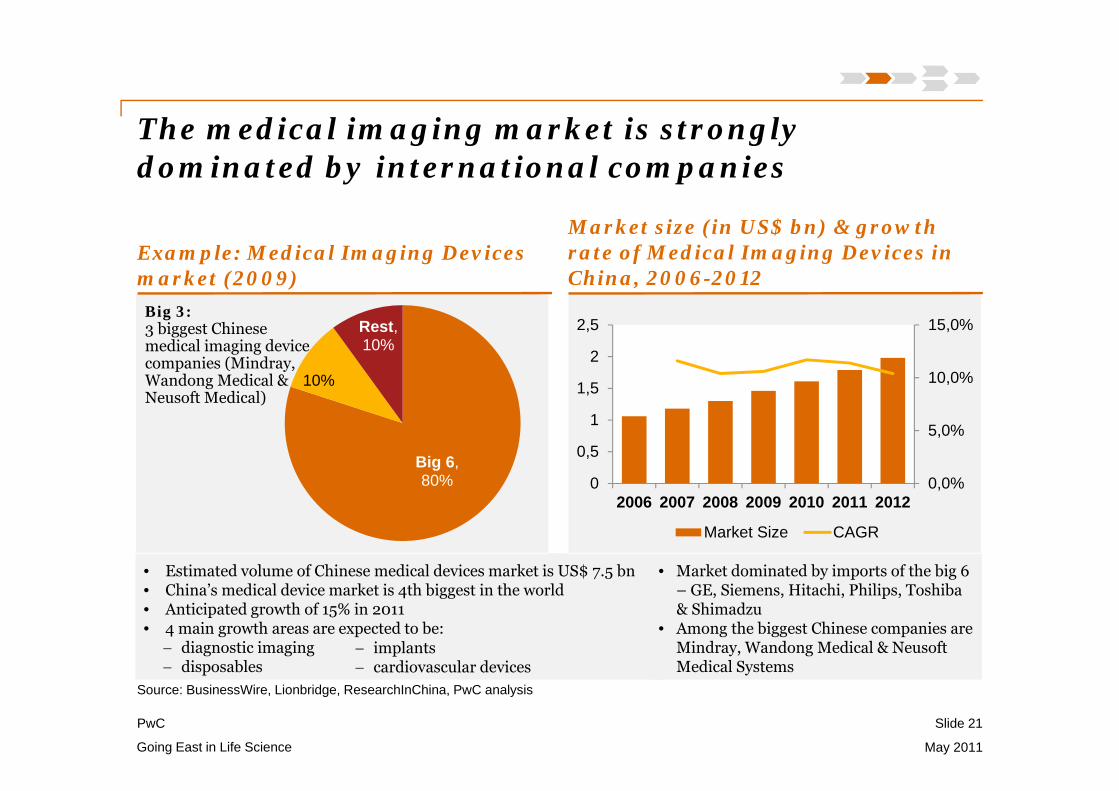

• Estimated volume of Chinese medical devices market is US$ 7.5 bn• China’s medical device market is 4th biggest in the world• Anticipated growth of 15% in 2011• 4 main growth areas are expected to be:

diagnostic imaging disposables

implants cardiovascular devices

• Market dominated by imports of the big 6 – GE, Siemens, Hitachi, Philips, Toshiba & Shimadzu

• Among the biggest Chinese companies are Mindray, Wandong Medical & NeusoftMedical Systems

Big 6, 80%

10%

Rest, 10%

The medical imaging market is stronglydominated by international companies

May 2011Going East in Life Science

Slide 21

Source: BusinessWire, Lionbridge, ResearchInChina, PwC analysis

0,0%

5,0%

10,0%

15,0%

0

0,5

1

1,5

2

2,5

2006 2007 2008 2009 2010 2011 2012

Market Size CAGR

Big 3:3 biggest Chinese medical imaging device companies (Mindray, Wandong Medical & Neusoft Medical)

Example: Medical Imaging Devices market (2009)

Market size (in US$ bn) & growth rate of Medical Imaging Devices in China, 2006-2012

PwC

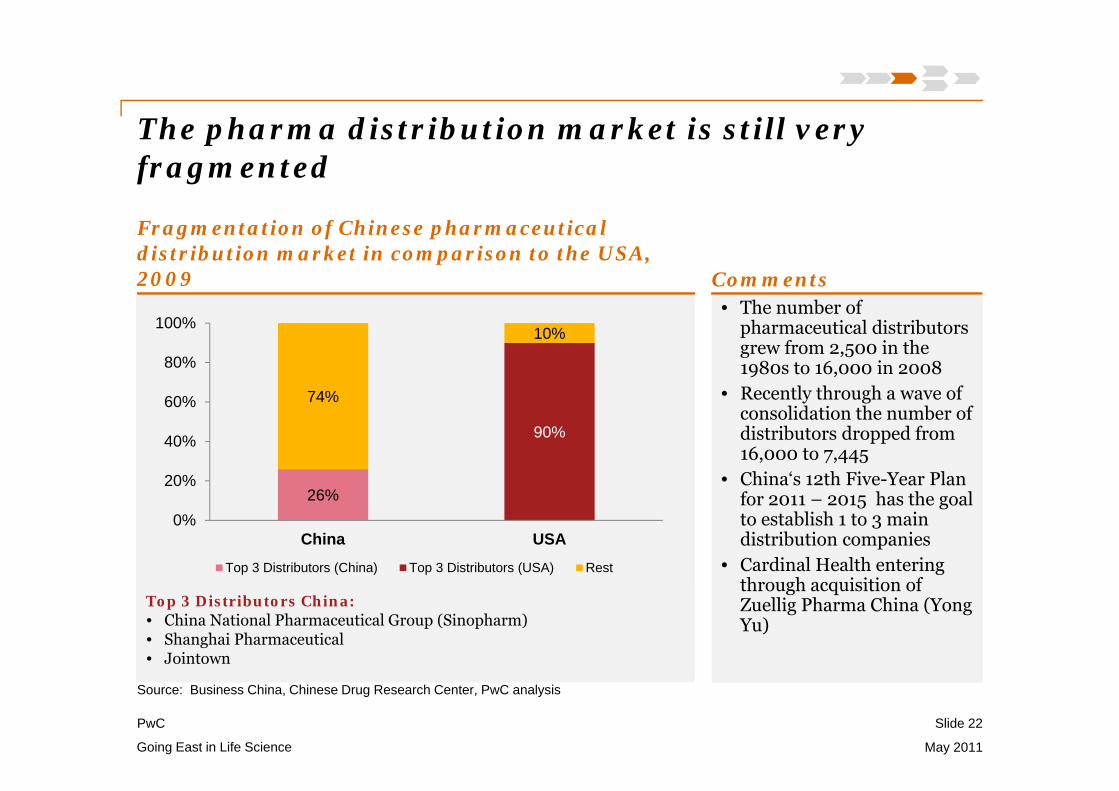

The pharma distribution market is still very fragmented

May 2011Going East in Life Science

Slide 22

Top 3 Distributors China:• China National Pharmaceutical Group (Sinopharm)• Shanghai Pharmaceutical• Jointown

26%

90%

74%

10%

0%

20%

40%

60%

80%

100%

China USATop 3 Distributors (China) Top 3 Distributors (USA) Rest

Source: Business China, Chinese Drug Research Center, PwC analysis

• The number of pharmaceutical distributors grew from 2,500 in the 1980s to 16,000 in 2008

• Recently through a wave of consolidation the number of distributors dropped from 16,000 to 7,445

• China‘s 12th Five-Year Plan for 2011 – 2015 has the goal to establish 1 to 3 main distribution companies

• Cardinal Health entering through acquisition of Zuellig Pharma China (Yong Yu)

Comments

Fragmentation of Chinese pharmaceutical distribution market in comparison to the USA, 2009

PwC

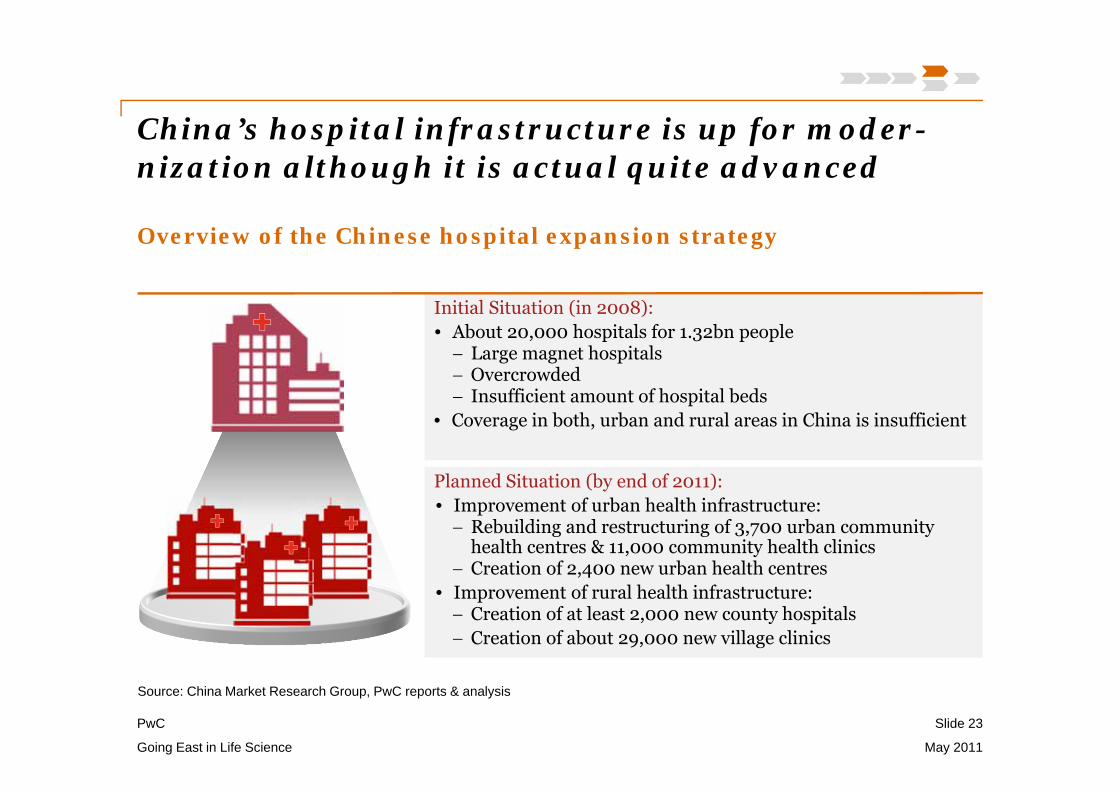

China’s hospital infrastructure is up for moder-nization although it is actual quite advanced

Slide 23

Going East in Life Science May 2011

Overview of the Chinese hospital expansion strategy

Initial Situation (in 2008):• About 20,000 hospitals for 1.32bn people Large magnet hospitals Overcrowded Insufficient amount of hospital beds

• Coverage in both, urban and rural areas in China is insufficient

Planned Situation (by end of 2011):• Improvement of urban health infrastructure: Rebuilding and restructuring of 3,700 urban community

health centres & 11,000 community health clinics Creation of 2,400 new urban health centres

• Improvement of rural health infrastructure: Creation of at least 2,000 new county hospitals Creation of about 29,000 new village clinics

Source: China Market Research Group, PwC reports & analysis

PwC

Overview Hospitals in China

May 2011Going East in Life Science

Slide 24

Source: Chinese Ministry of Health, China Statistics, PwC analysis

• Over 16,000 large public non-profit hospitals- management view:◦ less sophisticated in management systems◦ weak organizational structure◦ simple financial management◦ limited planning & organizational control◦ government subsidies only cover <10% of total expenses

Not yet true corporate bodies with self-controlling& self-stimulating mechanisms

• Supplemented by approx. 4,000 smaller private for-profit hospitals foreign investor able to hold 70% of joint-venture (regulation in 2000)

• Average joint-venture hospital in China <50 beds

PwC

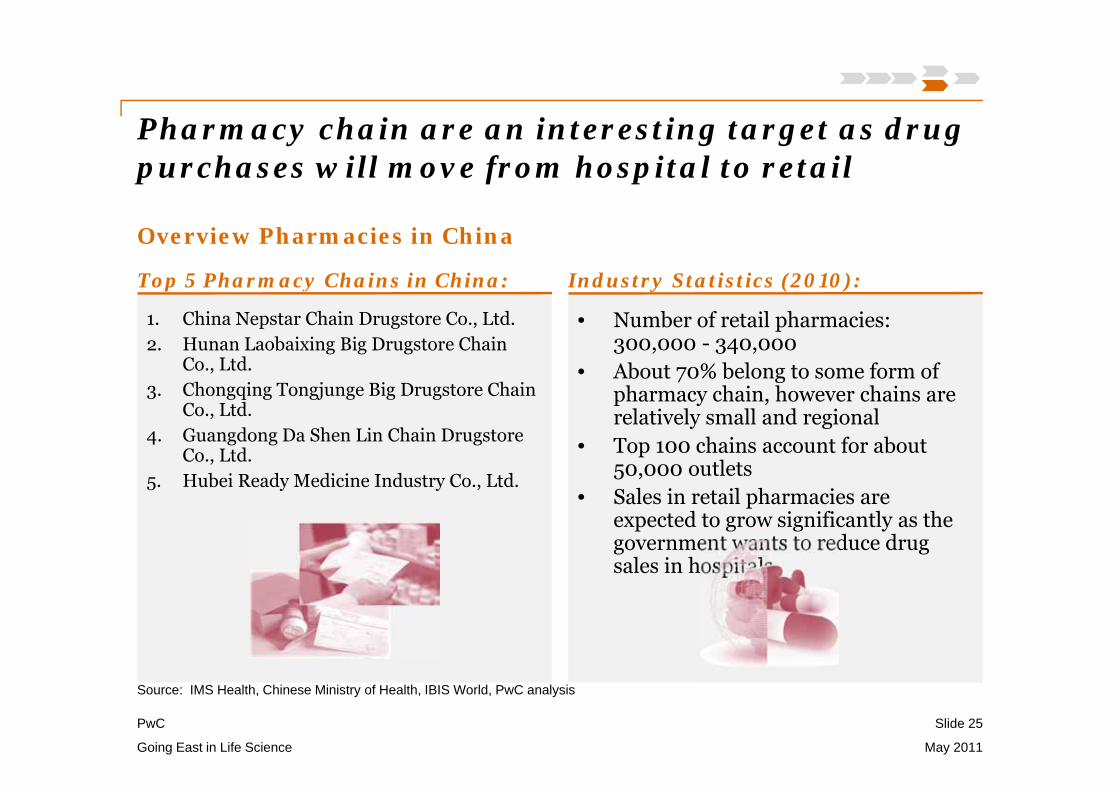

Pharmacy chain are an interesting target as drug purchases will move from hospital to retail

Slide 25

Going East in Life Science May 2011

Overview Pharmacies in China

Top 5 Pharmacy Chains in China:

1. China Nepstar Chain Drugstore Co., Ltd.2. Hunan Laobaixing Big Drugstore Chain

Co., Ltd.3. Chongqing Tongjunge Big Drugstore Chain

Co., Ltd.4. Guangdong Da Shen Lin Chain Drugstore

Co., Ltd.5. Hubei Ready Medicine Industry Co., Ltd.

• Number of retail pharmacies: 300,000 - 340,000

• About 70% belong to some form of pharmacy chain, however chains are relatively small and regional

• Top 100 chains account for about 50,000 outlets

• Sales in retail pharmacies are expected to grow significantly as the government wants to reduce drug sales in hospitals

Source: IMS Health, Chinese Ministry of Health, IBIS World, PwC analysis

Industry Statistics (2010):

PwC

Overview of Chinese Life Science M&A

26

PwC

78

77

101

92

118

153

191151

228

214

85

101

124

129

137

181128

197

268

310

Financial Services

Healthcare

Consumer Staples

Consumer Products andServices

Energy and Power

High Technology

Conglomerate

Real Estate

Industrials

Materials

1H '10 1H'09

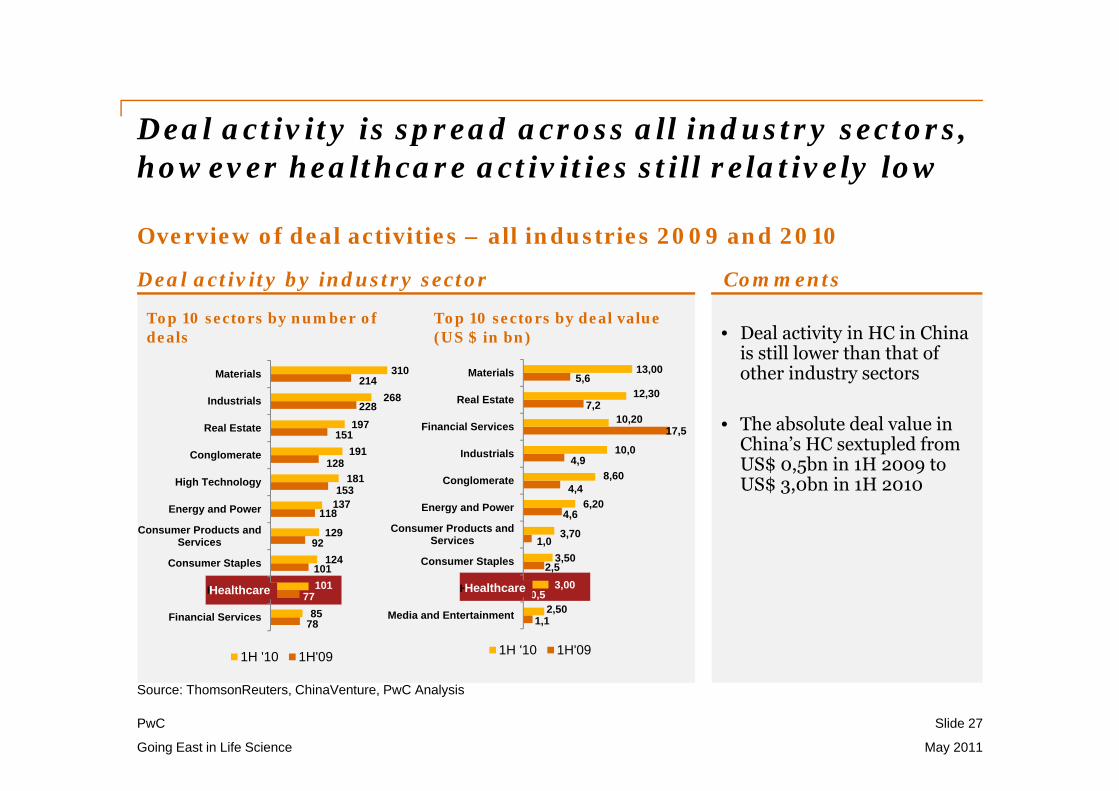

Deal activity is spread across all industry sectors, however healthcare activities still relatively low

Slide 27

Going East in Life Science May 2011

Overview of deal activities – all industries 2009 and 2010

Deal activity by industry sector

Top 10 sectors by number of deals

Top 10 sectors by deal value (US $ in bn)

Source: ThomsonReuters, ChinaVenture, PwC Analysis

• Deal activity in HC in China is still lower than that of other industry sectors

• The absolute deal value in China’s HC sextupled from US$ 0,5bn in 1H 2009 to US$ 3,0bn in 1H 2010

Comments

1,1

0,5

2,5

1,0

4,6

4,4

4,9

17,5

7,2

5,6

2,50

3,00

3,50

3,70

6,20

8,60

10,0

10,20

12,30

13,00

Media and Entertainment

Healthcare

Consumer Staples

Consumer Products andServices

Energy and Power

Conglomerate

Industrials

Financial Services

Real Estate

Materials

1H '10 1H'09

Healthcare Healthcare

PwC

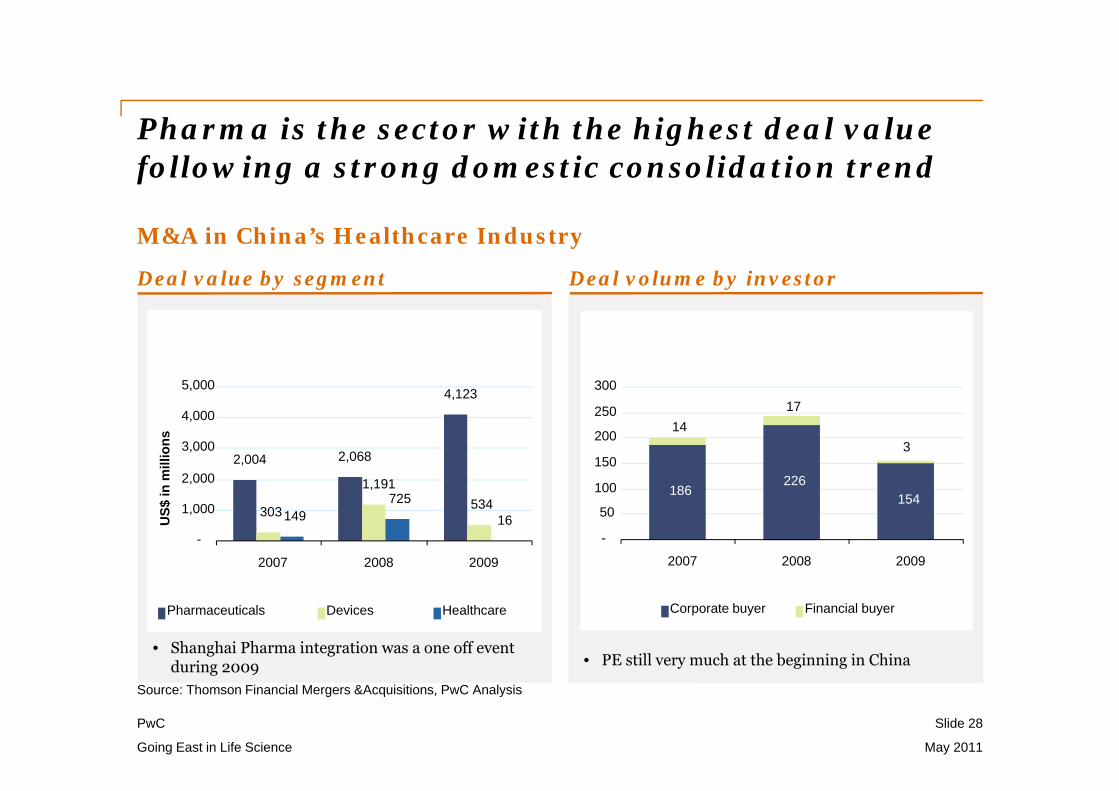

Pharma is the sector with the highest deal value following a strong domestic consolidation trend

Slide 28

Going East in Life Science May 2011

Deal value by segment Deal volume by investor

• PE still very much at the beginning in China • Shanghai Pharma integration was a one off event

during 2009 Source: Thomson Financial Mergers &Acquisitions, PwC Analysis

2,004 2,068

4,123

303

1,191534

149725

16-

1,000

2,000

3,000

4,000

5,000

2007 2008 2009

US$

in m

illio

ns

Pharmaceuticals Devices Healthcare

186226

154

1417

3

-

50

100

150

200

250

300

2007 2008 2009

Corporate buyer Financial buyer

M&A in China’s Healthcare Industry

PwC

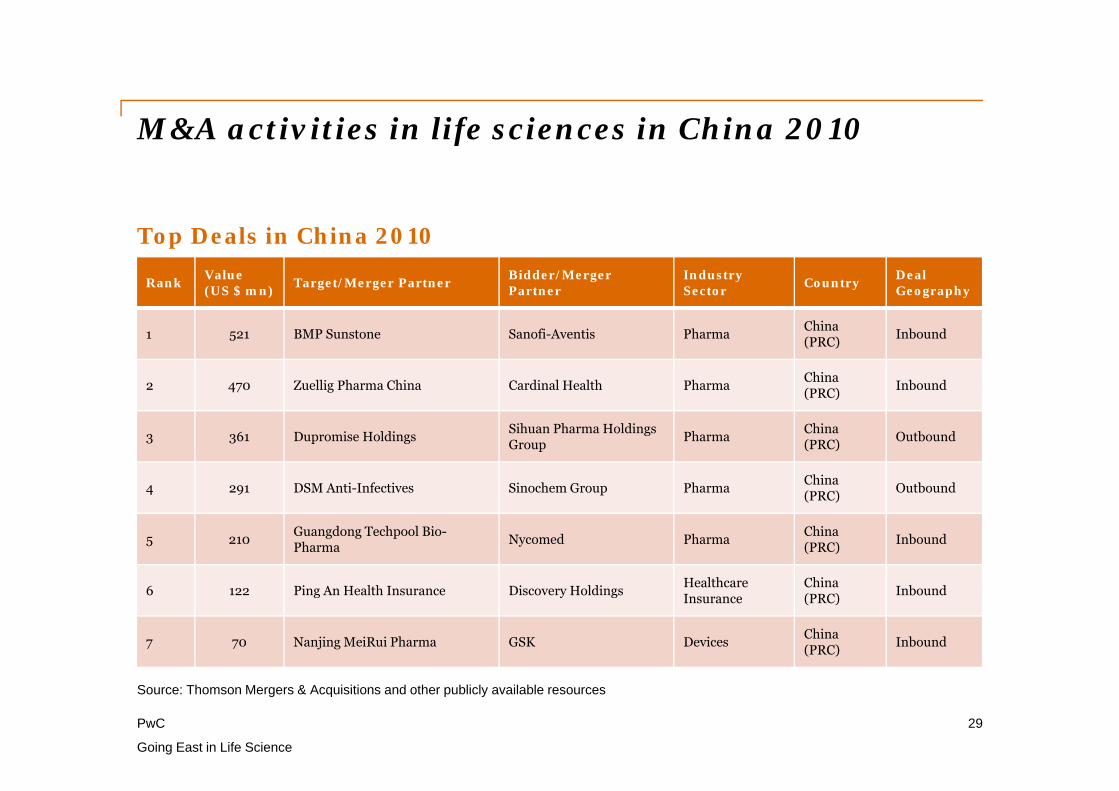

M&A activities in life sciences in China 2010

29

Going East in Life Science

Rank Value (US $ mn) Target/Merger Partner Bidder/Merger

PartnerIndustrySector Country Deal

Geography

1 521 BMP Sunstone Sanofi-Aventis Pharma China (PRC) Inbound

2 470 Zuellig Pharma China Cardinal Health Pharma China (PRC) Inbound

3 361 Dupromise Holdings Sihuan Pharma Holdings Group Pharma China

(PRC) Outbound

4 291 DSM Anti-Infectives Sinochem Group Pharma China (PRC) Outbound

5 210 Guangdong Techpool Bio-Pharma Nycomed Pharma China

(PRC) Inbound

6 122 Ping An Health Insurance Discovery Holdings HealthcareInsurance

China (PRC) Inbound

7 70 Nanjing MeiRui Pharma GSK Devices China (PRC) Inbound

Source: Thomson Mergers & Acquisitions and other publicly available resources

Top Deals in China 2010

PwC

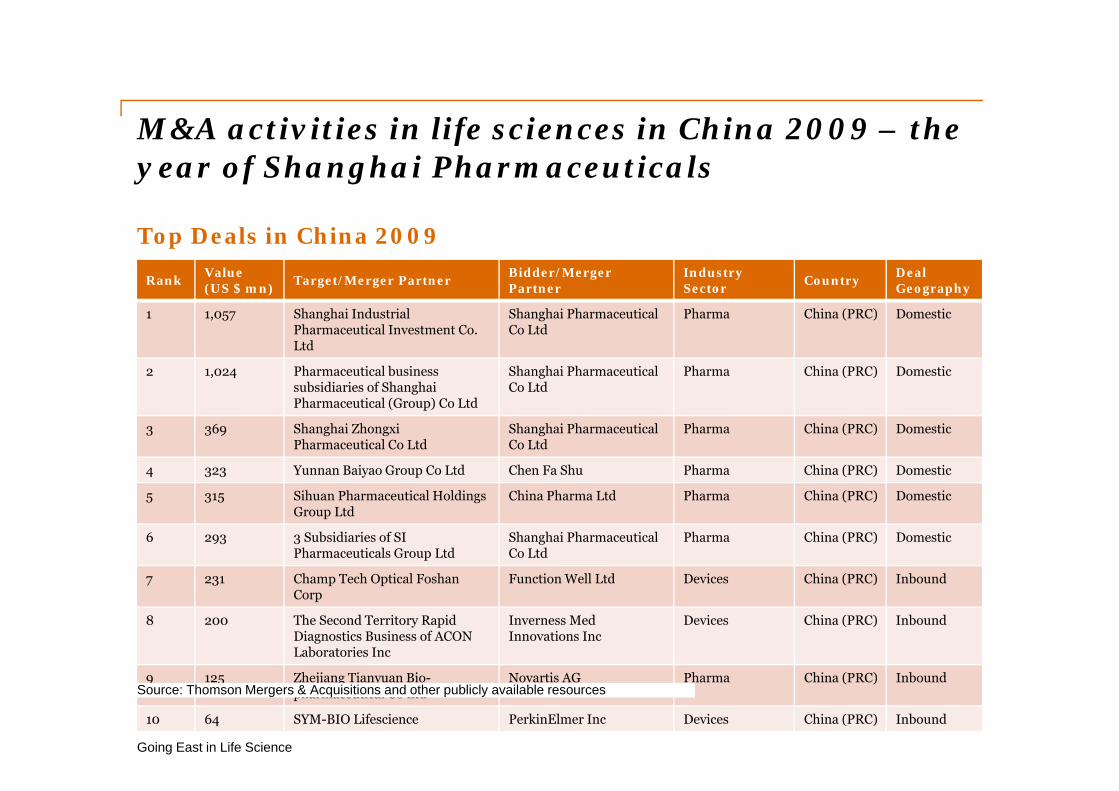

M&A activities in life sciences in China 2009 – the year of Shanghai Pharmaceuticals

30

Going East in Life Science

Rank Value (US $ mn) Target/Merger Partner Bidder/Merger

PartnerIndustrySector Country Deal

Geography

1 1,057 Shanghai Industrial Pharmaceutical Investment Co. Ltd

Shanghai Pharmaceutical Co Ltd

Pharma China (PRC) Domestic

2 1,024 Pharmaceutical business subsidiaries of Shanghai Pharmaceutical (Group) Co Ltd

Shanghai Pharmaceutical Co Ltd

Pharma China (PRC) Domestic

3 369 Shanghai ZhongxiPharmaceutical Co Ltd

Shanghai Pharmaceutical Co Ltd

Pharma China (PRC) Domestic

4 323 Yunnan Baiyao Group Co Ltd Chen Fa Shu Pharma China (PRC) Domestic

5 315 Sihuan Pharmaceutical Holdings Group Ltd

China Pharma Ltd Pharma China (PRC) Domestic

6 293 3 Subsidiaries of SI Pharmaceuticals Group Ltd

Shanghai Pharmaceutical Co Ltd

Pharma China (PRC) Domestic

7 231 Champ Tech Optical FoshanCorp

Function Well Ltd Devices China (PRC) Inbound

8 200 The Second Territory Rapid Diagnostics Business of ACON Laboratories Inc

Inverness Med Innovations Inc

Devices China (PRC) Inbound

9 125 Zhejiang Tianyuan Bio-pharmaceutical Co Ltd

Novartis AG Pharma China (PRC) Inbound

10 64 SYM-BIO Lifescience PerkinElmer Inc Devices China (PRC) Inbound

Source: Thomson Mergers & Acquisitions and other publicly available resources

Top Deals in China 2009

PwC

M&A activities in life sciences in China 2008

31

Going East in Life Science

Rank Value (US $ mn) Target/Merger Partner Bidder/Merger

PartnerIndustrySector Country Deal

Geography

1 345 Molecular Diagnostics-Assets China Medical Technologies Inc

Devices Hong Kong Domestic

2 336 China Cord Blood Services Corporation

Pantheon China Acquisition Corp

Services China (PRC) Inbound

3 209 Datascope Corp-Patient Monitor Mindray Medical International

Devices China (PRC) Outbound

4 204 Yunnan Baiyao Group Co Ltd Ping An Insurance (Group) Co

Pharma China (PRC) Domestic

5 195 Asiapharm Group Ltd. MBK Partners Pharma China (PRC) Inbound

6 185 Topsun Science & Tech Qidong Bayer Healthcare AG Pharma China (PRC) Inbound

7 163 APPTec Laboratory Services Wuxi Phama Tech Services China (PRC) Outbound

8 128 United Premier Medical Group Cavalier Group Services Hong Kong Domestic

9 113 Core Healthcare Investment Ltd Laboratory Holdings Co Ltd

Services Hong Kong Domestic

10 106 Topshine Investment Ltd GM Hospital Management Co Ltd

Services Hong Kong Domestic

Source: Thomson Mergers & Acquisitions and other publicly available resources

Top Deals in China 2008

PwC

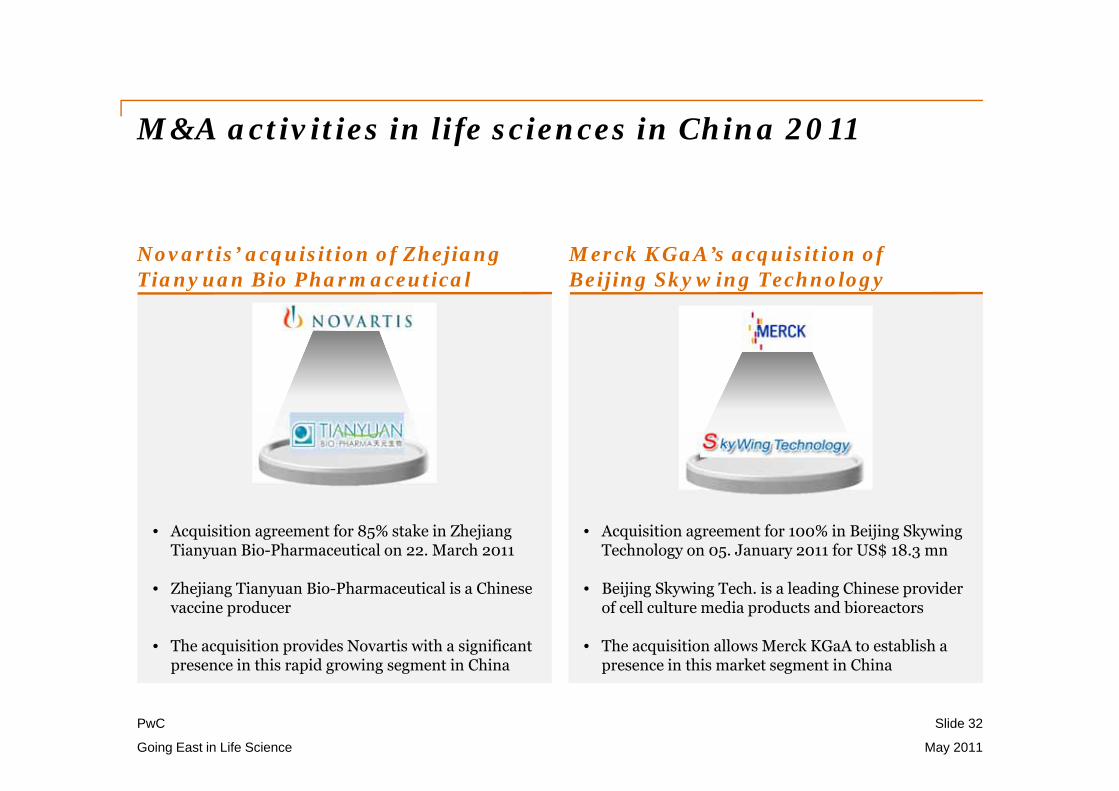

M&A activities in life sciences in China 2011

Slide 32

Going East in Life Science May 2011

Novartis’ acquisition of Zhejiang Tianyuan Bio Pharmaceutical

Merck KGaA’s acquisition of Beijing Skywing Technology

• Acquisition agreement for 100% in Beijing SkywingTechnology on 05. January 2011 for US$ 18.3 mn

• Beijing Skywing Tech. is a leading Chinese provider of cell culture media products and bioreactors

• The acquisition allows Merck KGaA to establish a presence in this market segment in China

• Acquisition agreement for 85% stake in Zhejiang Tianyuan Bio-Pharmaceutical on 22. March 2011

• Zhejiang Tianyuan Bio-Pharmaceutical is a Chinese vaccine producer

• The acquisition provides Novartis with a significant presence in this rapid growing segment in China

Questions?