Embed Size (px)

Citation preview

0

GMR Hyderabad International Airport Ltd.

(GHIAL)

Tariff Filing Presentation to AERA

December 19, 2012

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 1 of 136

1

GMR Hyderabad International Airport Ltd. (GHIAL)

GHIAL is a PPP Enterprise for building & operating Rajiv Gandhi International Airport, Hyderabad, with the following equity participation

63% 11% 13% 13%

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 2 of 136

2

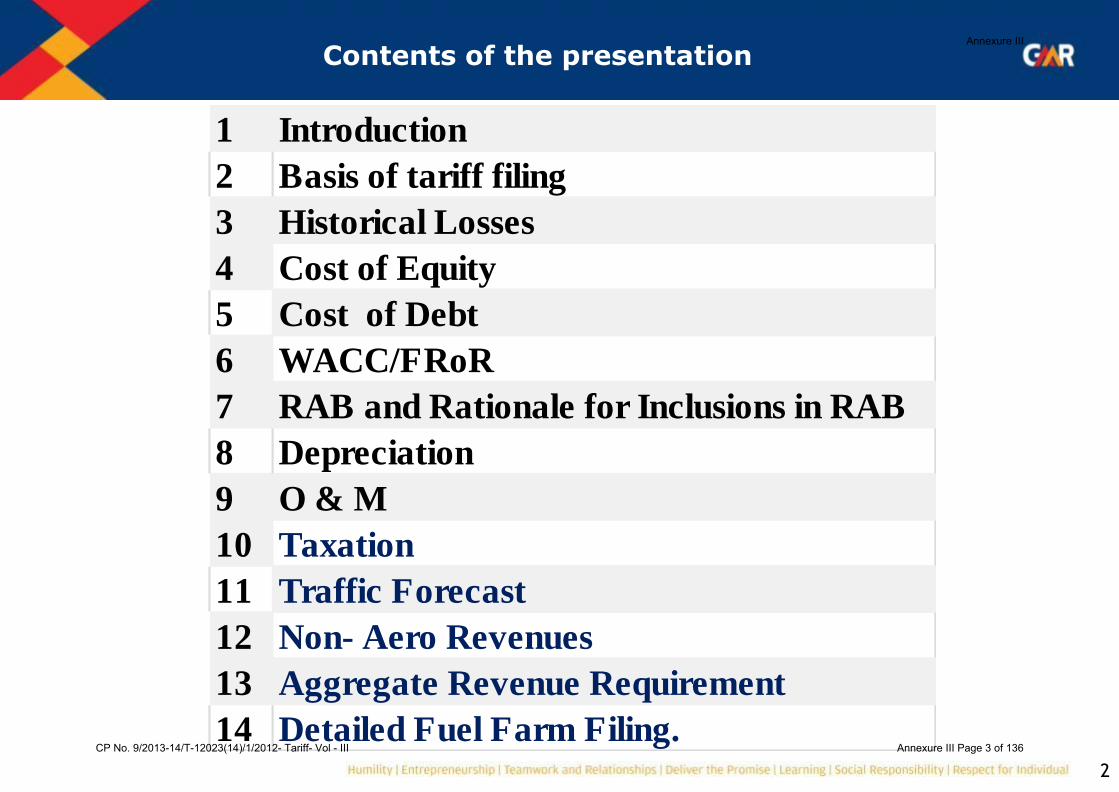

Contents of the presentation

1 Introduction

2 Basis of tariff filing

3 Historical Losses

4 Cost of Equity

5 Cost of Debt

6 WACC/FRoR

7 RAB and Rationale for Inclusions in RAB

8 Depreciation

9 O & M

10 Taxation

11 Traffic Forecast

12 Non- Aero Revenues

13 Aggregate Revenue Requirement

14 Detailed Fuel Farm Filing.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 3 of 136

3

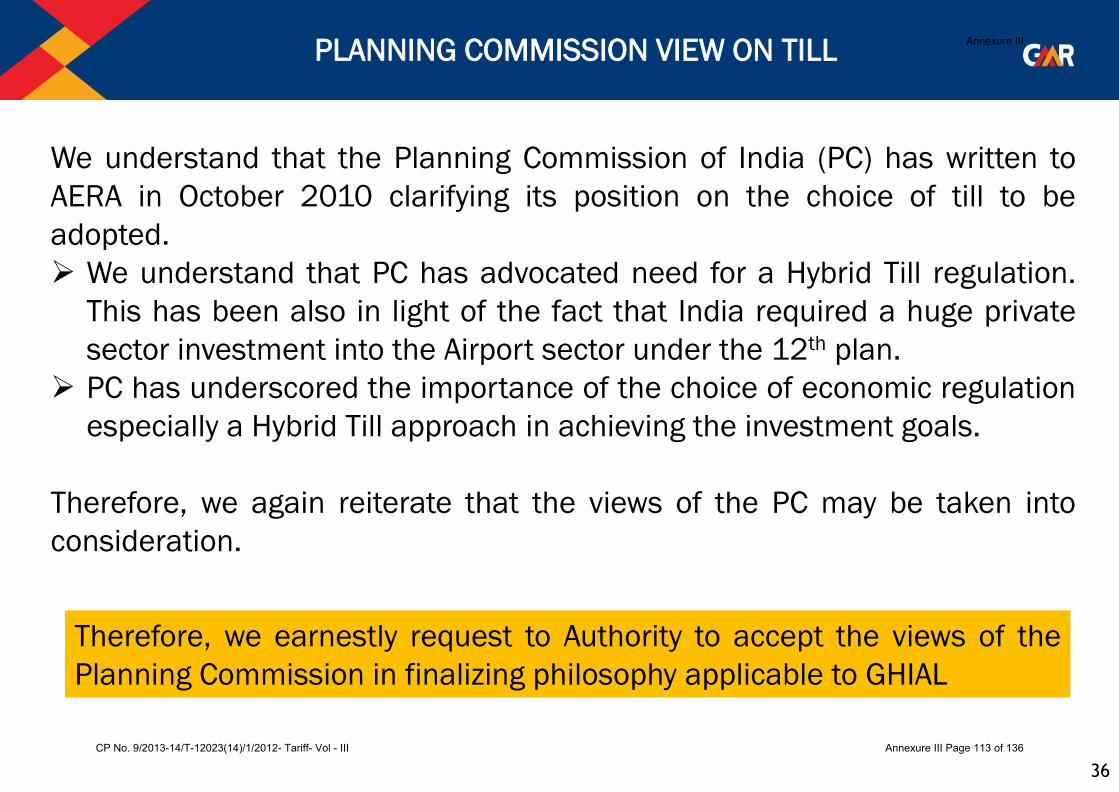

Introduction

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 4 of 136

4

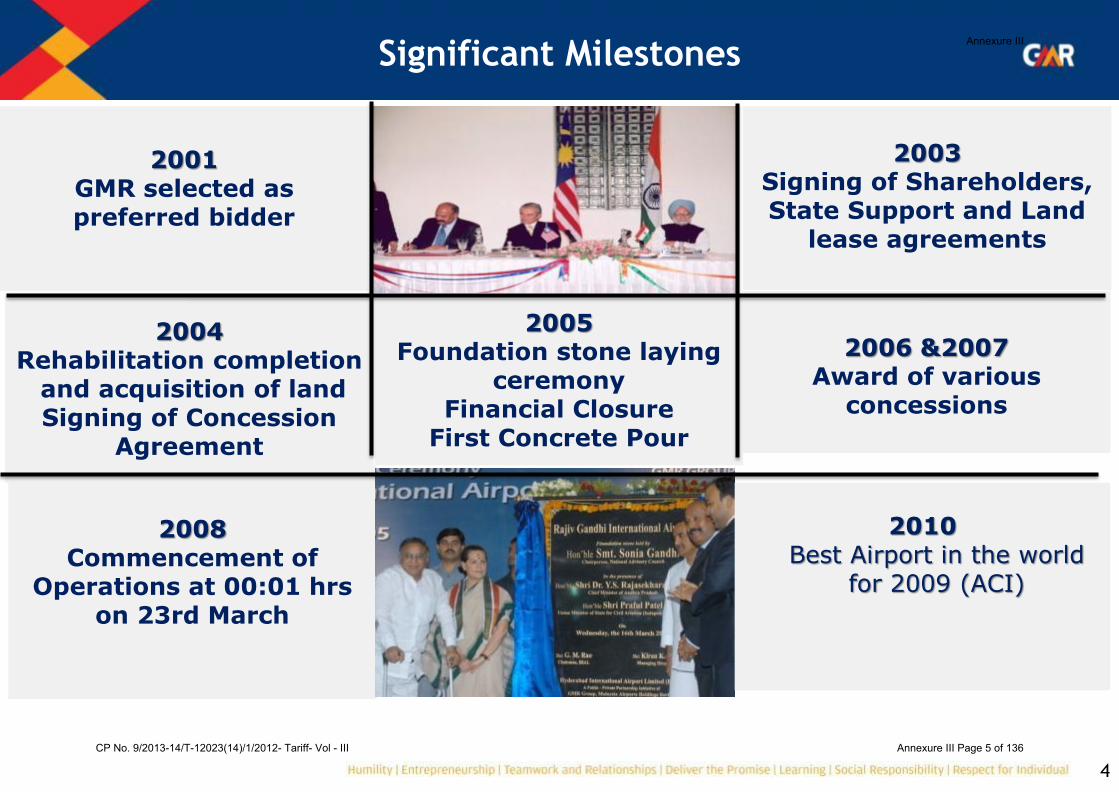

• Jhjhjh 2001

GMR selected as preferred bidder

2003 Signing of Shareholders, State Support and Land

lease agreements

2004

Rehabilitation completion and acquisition of land Signing of Concession

Agreement

2005 Foundation stone laying

ceremony Financial Closure

First Concrete Pour

2006 &2007

Award of various concessions

2008 Commencement of

Operations at 00:01 hrs on 23rd March

2010 Best Airport in the world

for 2009 (ACI)

Significant Milestones Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 5 of 136

5

Benefits to Passengers and Airlines 1/4

Better Infrastructure

• Terminal Building - 117,000 sq.m

• Integrated Terminal building for quick transfer of

connecting passengers and ample seating.

• 4 Inclined Baggage carousels & 46 Immigration

counters

• 42 aircraft parking stands,12 boarding bridges

• 30 Escalators and 32 Elevators

• Several international and domestic F&B and Retail

outlets

• Free Wi-Fi, Free Buggy Service, Barrier-free access

for elderly and physically challenged.

• Adjacent car park for >3500 cars

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 6 of 136

6

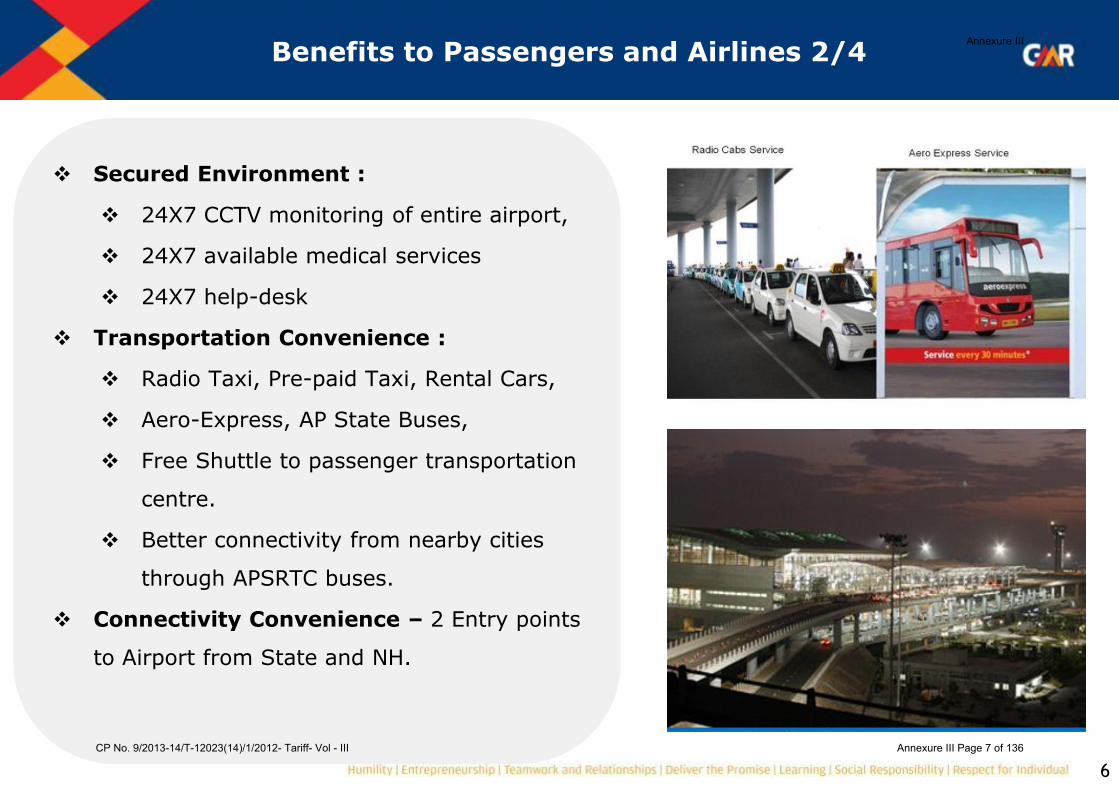

Secured Environment :

24X7 CCTV monitoring of entire airport,

24X7 available medical services

24X7 help-desk

Transportation Convenience :

Radio Taxi, Pre-paid Taxi, Rental Cars,

Aero-Express, AP State Buses,

Free Shuttle to passenger transportation

centre.

Better connectivity from nearby cities

through APSRTC buses.

Connectivity Convenience – 2 Entry points

to Airport from State and NH.

Benefits to Passengers and Airlines 2/4 Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 7 of 136

7

Benefits to Passengers and Airlines 3/4

Multiple Lounges including special Arrival

Lounge with nap & shower facility positioned for

Transit passengers.

Economic Stay for passengers: Passenger

Transportation Centre provide value options for short

stay.

Multiple Food and Beverage options in the

Arrival, Departure Areas and the Airport Village.

Better Services: Porter Services, Cloak Room,

APTDC counter for Tirupati packages, numerous

FIDS, ATMs, clean and green ambience

Caring and Smiling Terminal operations staff

including Security, Customs, Immigration and other

agencies.

Proactive listening to Travelers' feedback

through Kiosk, Website, Help-Desk, Twitter and

implementing suggestions

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 8 of 136

8

Hyderabad is best choice to target South and

Central catchment area of India

Better Infrastructure with 146 Check-in counters

including 16 with Self-service facilities

Various Initiatives launched to promote RGIA as

a transfer gateway.

Fly via Hyderabad campaign in 19 catchment

cities to promote RGIA as a transfer gateway.

Seamless transit & transfer facilities with

Dedicated Airport Facilitation Cell. First-of-its-kind

concept in India for transfer passengers. Transfer

Desk manned by Airport staff, Baggage transfers,

airport and airline information assistance etc.

Working closely with the AP tourism to promote

Hyderabad and other cities in AP as a destination.

Benefits to Passengers and Airlines 4/4 Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 9 of 136

9

Socio-Economic Benefits: Findings of a study by NCAER

National Council of applied Economic research (NCAER) has conducted a study on the economic impact of GHIAL airport. This study provides an assessment of the economic impact of Hyderabad‟s Rajiv Gandhi International Airport (RGIA) on the regional and national economies in terms of output, value added (income) and employment. The study has been finalized and shall be released shortly. Some of the findings of the study are as under:

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 10 of 136

10

Socio-Economic Benefits: Findings of a study by NCAER

RGIA‟s operations contributed Rs 75.9 billion to the national GDP in 2009-10. Its contribution relative to Andhra Pradesh‟s GSDP was 1.55 per cent. This total impact comprises of:

Rs 11.1 billion contributed directly through value added (air transport and airport services).

Rs 19.9 billion contributed indirectly through supply chain (multiplier impact).

Rs 44.9 billion in induced impact through tourism and investment.

RGIA airport‟s construction contributed Rs 11.9 billion to the national GDP in a single year of the construction phase. It is important to note here that this was a one-time impact which included one-third of the total project cost plus inflation adjustments. The total impact of the construction phase will, therefore, be three times this estimate but spread over three years. This total impact of the construction phase in a year comprises of:

Rs 4.65 billion contributed directly through value added.

Rs 7.25 billion contributed indirectly through supply chain (multiplier impact).

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 11 of 136

11

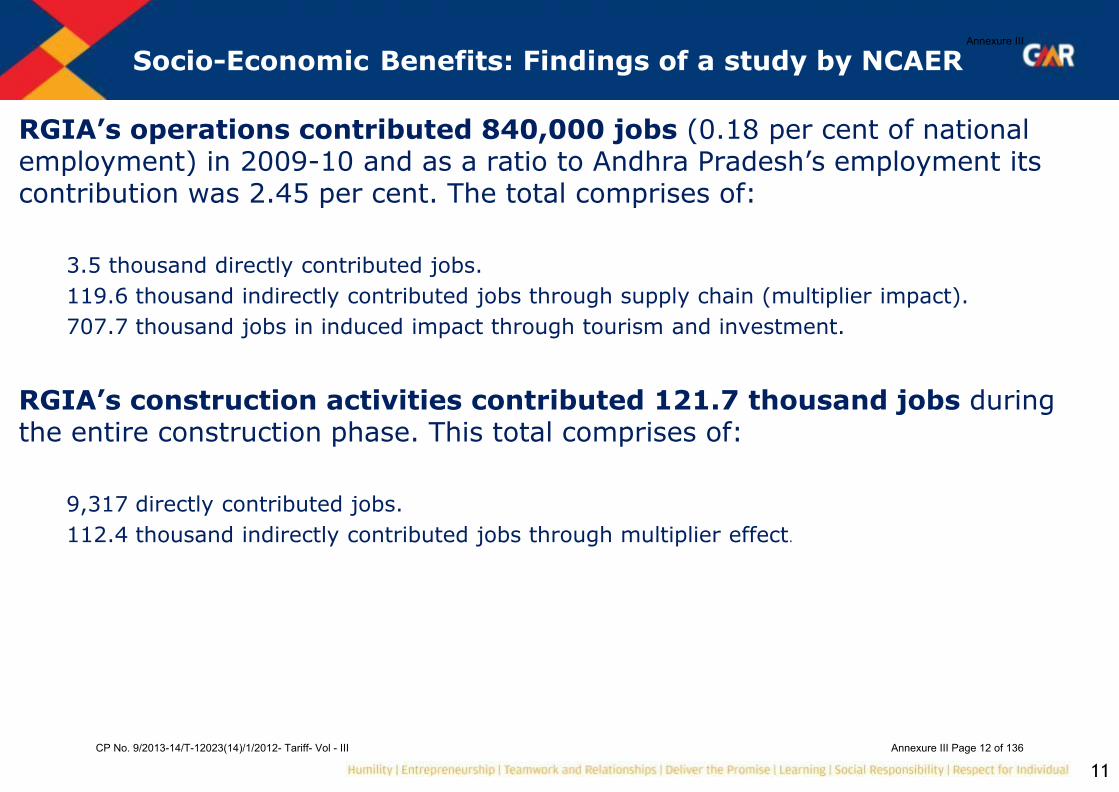

RGIA‟s operations contributed 840,000 jobs (0.18 per cent of national employment) in 2009-10 and as a ratio to Andhra Pradesh‟s employment its contribution was 2.45 per cent. The total comprises of:

3.5 thousand directly contributed jobs.

119.6 thousand indirectly contributed jobs through supply chain (multiplier impact).

707.7 thousand jobs in induced impact through tourism and investment.

RGIA‟s construction activities contributed 121.7 thousand jobs during the entire construction phase. This total comprises of:

9,317 directly contributed jobs.

112.4 thousand indirectly contributed jobs through multiplier effect.

Socio-Economic Benefits: Findings of a study by NCAER Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 12 of 136

12

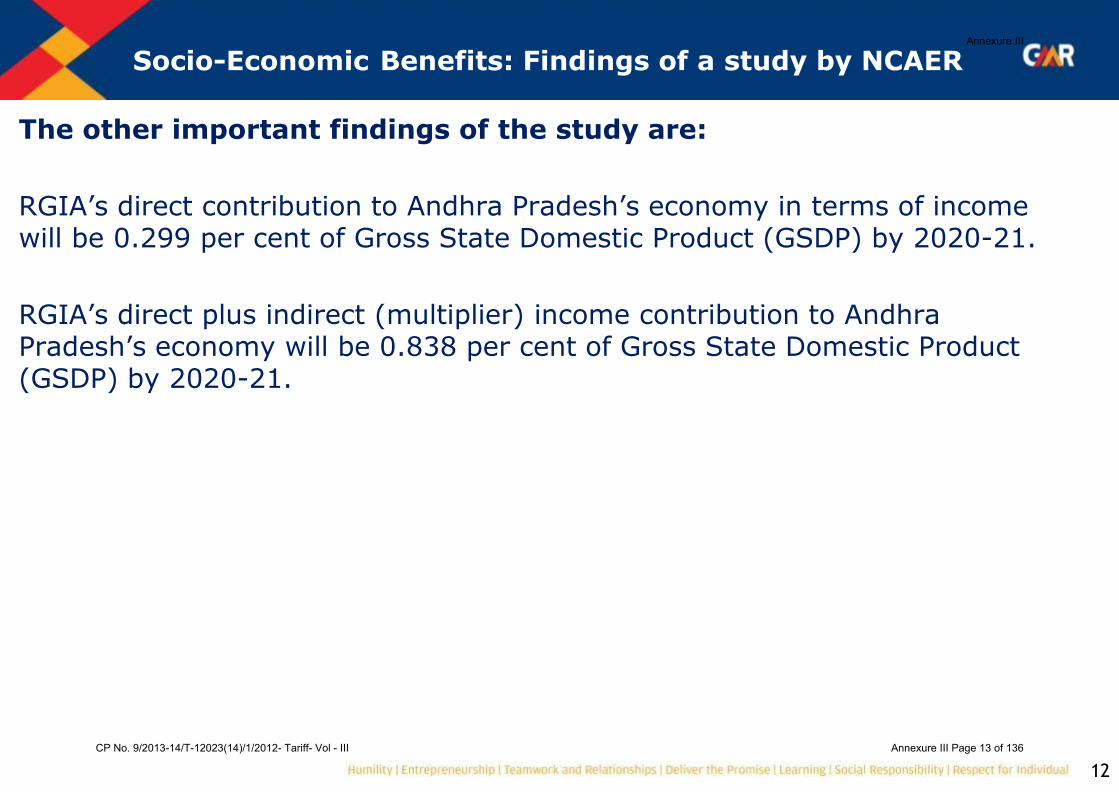

The other important findings of the study are:

RGIA‟s direct contribution to Andhra Pradesh‟s economy in terms of income will be 0.299 per cent of Gross State Domestic Product (GSDP) by 2020-21.

RGIA‟s direct plus indirect (multiplier) income contribution to Andhra Pradesh‟s economy will be 0.838 per cent of Gross State Domestic Product (GSDP) by 2020-21.

Socio-Economic Benefits: Findings of a study by NCAER Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 13 of 136

13

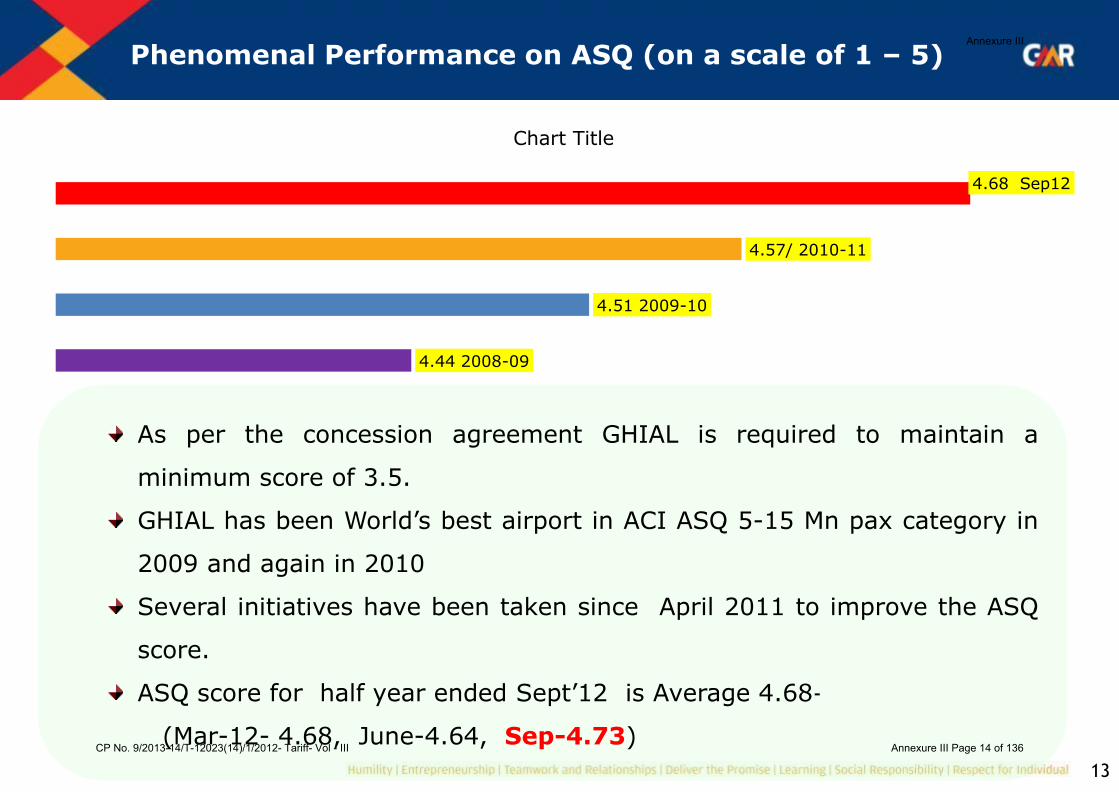

Phenomenal Performance on ASQ (on a scale of 1 – 5)

As per the concession agreement GHIAL is required to maintain a

minimum score of 3.5.

GHIAL has been World‟s best airport in ACI ASQ 5-15 Mn pax category in

2009 and again in 2010

Several initiatives have been taken since April 2011 to improve the ASQ

score.

ASQ score for half year ended Sept‟12 is Average 4.68-

(Mar-12- 4.68, June-4.64, Sep-4.73)

4.44 2008-09

4.51 2009-10

4.57/ 2010-11

4.68 Sep12

Chart Title

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 14 of 136

14 14

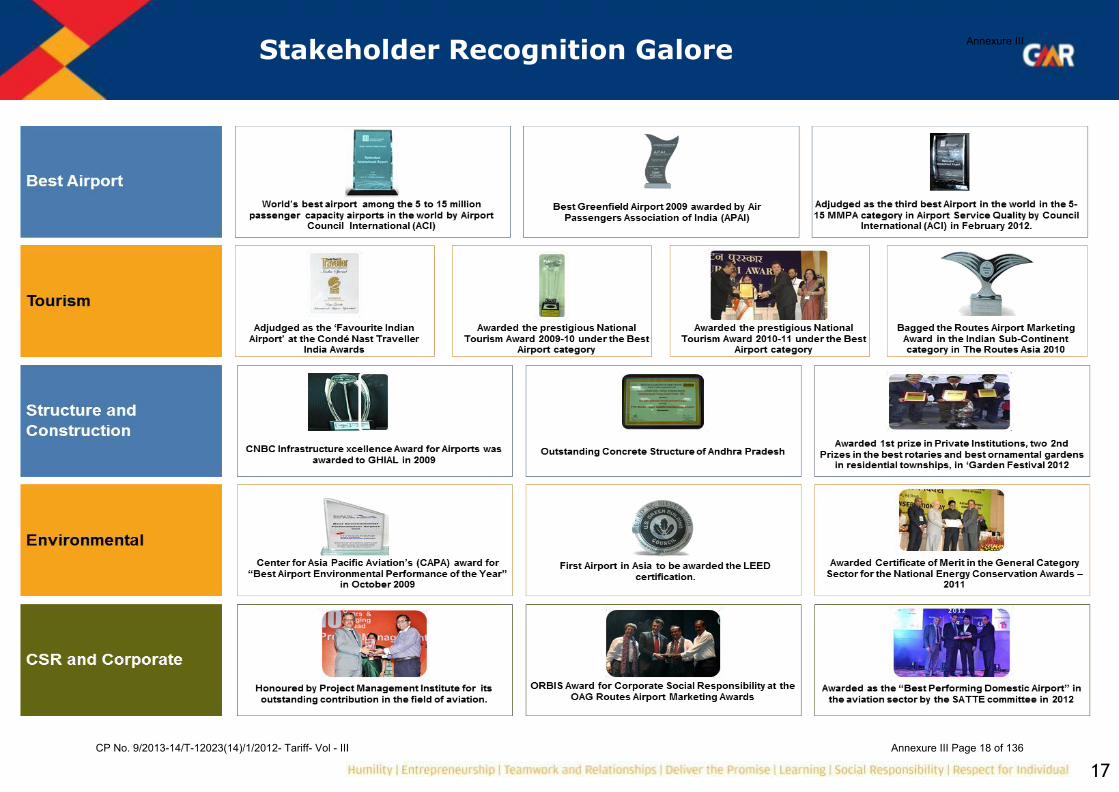

Stakeholder Recognition Galore 1/3

Passenger and Airline Recognition

Best performing Domestic Airport Award in SATTE 2012 Travel awards

during the Annual Tourism Trade Show SATTE-2012, held from 10th -12th February, 2012

at New Delhi.

World‟s Best Airport in ACI ASQ 5-15 mn pax category in 2009 and again in

2010

„Best Greenfield Airport in India‟ by Air Passengers Association of India

„Favourite Indian Airport‟ award by Conde‟ Naste Traveller magazine.

Best Airport India‟ Award at the Skytrax World Airports Awards 2010.

Best Airport Marketing award in Routes 2009 and again in Routes

2010 Asia Pacific Conference

Best Cargo Airport & Best Cargo Terminal of the Year” Award (Air

Cargo Agents Association of India (ACAAI))

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 15 of 136

15 15

Stakeholder Recognition Galore 2/3

Industry Recognition 1/2 Best Airport in India‟ National Tourism Award 2009-10 and

2010-11 by Ministry of Tourism

„Certificate of Merit‟ in National Energy Conservation Awards – 2011 by Ministry of Power Govt. of India on 14th December‟11

Airport Landscape awarded 1st Prize by Dept. of Horticulture, GoAP for the second time in a row.

CAPA Environment Award of the year : Airport, 2009

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 16 of 136

16 16

Stakeholder Recognition Galore 3/3

Industry Recognition 2/2 Leadership in Energy & Environmental Design (LEED) “silver rating” - 1st

airport in Asia & 2nd airport globally to have won this certification.

Outstanding Concrete Structure of AP award 2008 by Indian Concrete Institute (ICI).

World Routes award by ORBIS UK, for CSR projects undertaken around the Airport.

CNBC Infrastructure excellence award for Airports.

ISO 9001-2008 (Quality Management System), ISO 14001-2004 (Environment Management System) and OHSAS 18001 – 2007 (Occupational Health and Safety Management System) certified.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 17 of 136

17

Stakeholder Recognition Galore Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 18 of 136

18

Basis of tariff filing

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 19 of 136

19

Background on earlier filing

• In February 2008, MoCA approved an UDF charge of INR 1,000 per international passenger. In addition to the international UDF, MoCA approved UDF of INR 375 per domestic passenger in August 2008.

• In Oct 2010, AERA provided an adhoc Approval to charge INR 1,700 per international pax and INR 430 per domestic pax (Exclusive of service tax) . The adhoc approval was provided on the basis of single till.

• AERA issued Final Guidelines for tariff determination based on single till in Feb 2011. GHIAL filed an appeal with the AERA appellate tribunal(AERAAT) majorly contesting single till methodology of tariff determination.

• Pending the decision of AERAAT on our appeal, as per the requirement of guidelines GHIAL had made an application with AERA for tariff determination as per Dual Till for 5 year control period on 31st July 2011.

• Subsequently, as per the order of AERA, GHIAL had filed the tariff application under the single till for the 5 year control period (2011-16) on 15th September‟2011. Pending the decision on the appeal, AERAAT had instructed AERA to go-ahead and determine the tariff but suggested not to implement the same until the appeal is disposed off.

• Since substantial period has elapsed from our earlier filing done in September 2011 and as there has been a substantial change in the assumptions and the business environment, revised application was filed on 14th December‟ 2012 .

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 20 of 136

20

Basis of Current filing

Current filing for tariff determination is made under Single Till. Fuel Farm filing has been made separately.

The current application is for the aggregate revenue requirement for

the control period (ARR) which has been calculated as per the Authority‟s guidelines.

The control period considered is 5 years starting from April 1st 2011 up to March 31, 2016 as per the guidelines, considering the past 3 years losses from April 2008 to March 2011.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 21 of 136

21

Basis of Current filing

We have not factored in inflation in our O & M forecast. It is assumed that the Authority will give a year on year WPI based inflation increase over and above approved yield calculated, based on actual WPI data.

Actual audited numbers of FY 2011-12 have been used for calculation of

ARR.

Inclusion of 100% operational subsidiaries of GHIAL- ssubsidiaries of GHIAL namely GMR Hyderabad Aviation SEZ Limited, GMR Hotels and Resorts Limited and Hyderabad Duty Free Retail Limited have been considered in the current tariff proposal. The entire capex, opex and revenues are considered as part of current filing.

We would submit a detailed pricing proposal in due course

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 22 of 136

22

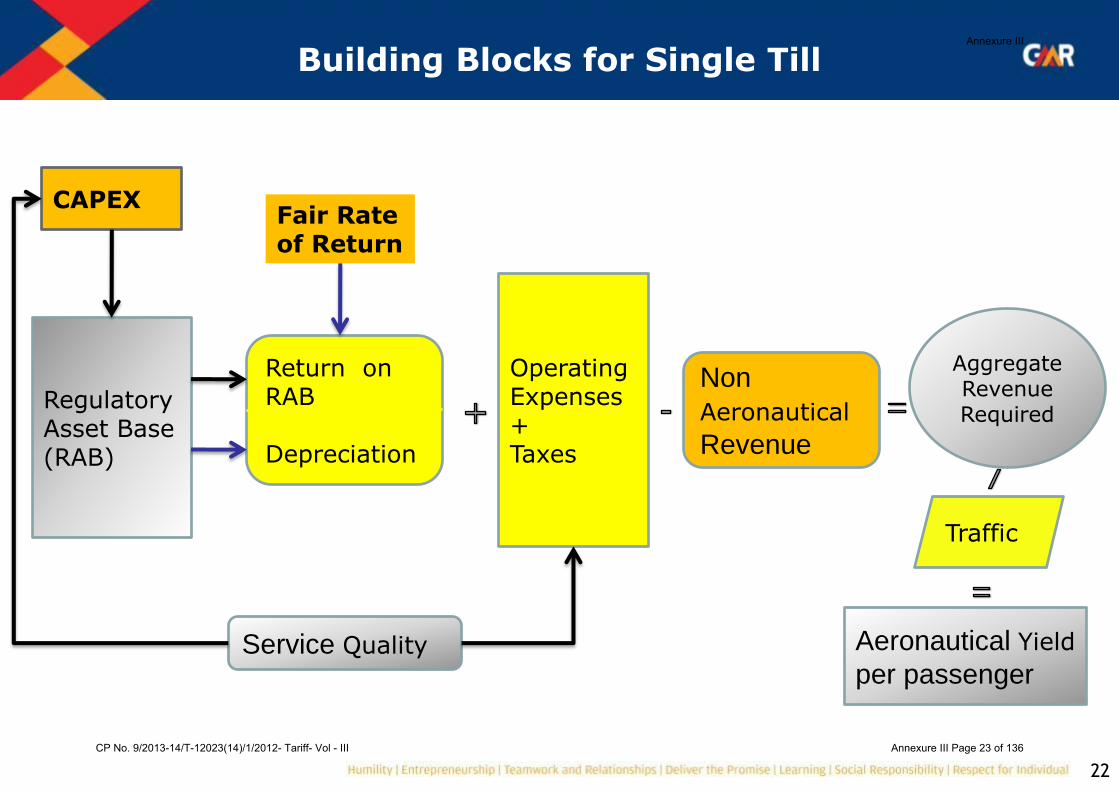

Building Blocks for Single Till

CAPEX

Regulatory Asset Base (RAB)

Return on RAB Depreciation

Operating Expenses+ Taxes

Non

Aeronautical

Revenue

Aggregate Revenue Required

Traffic

Aeronautical Yield

per passenger Service Quality

Fair Rate of Return

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 23 of 136

23

Historical Losses

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 24 of 136

24

Financial performance over past 3 years

GHIAL has been continuously making losses over the first 2 years of

operations. The Company has made marginal profits during the year 2010-11,

due to the fact that the tariff had been revised upward by the Authority Effective

November 1, 2010 on Adhoc basis.

As on March 31, 2011 the accumulated losses of the Company after considering

the DTA is Rs.164 Crores

Equal to 43% of the Equity invested

accumulated losses without considering DTA is Rs.267 Crores which is almost

70% of the Equity invested by the promoters.

Therefore, for survival of organization, for recovering the past losses and to ensure

a fair rate of return to the promoters, it is very important for a substantial increase

in tariff levels from the current levels.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 25 of 136

25

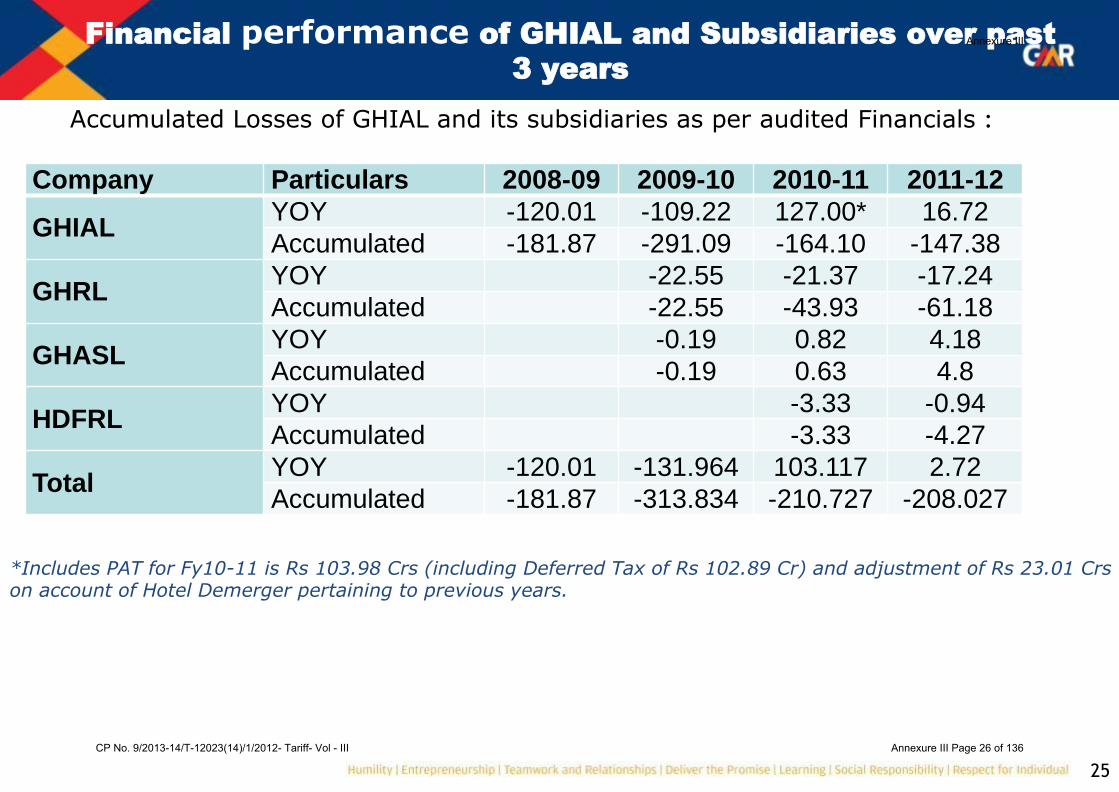

Financial performance of GHIAL and Subsidiaries over past

3 years

Accumulated Losses of GHIAL and its subsidiaries as per audited Financials :

Company Particulars 2008-09 2009-10 2010-11 2011-12

GHIAL YOY -120.01 -109.22 127.00* 16.72 Accumulated -181.87 -291.09 -164.10 -147.38

GHRL YOY -22.55 -21.37 -17.24 Accumulated -22.55 -43.93 -61.18

GHASL YOY -0.19 0.82 4.18 Accumulated -0.19 0.63 4.8

HDFRL YOY -3.33 -0.94 Accumulated -3.33 -4.27

Total YOY -120.01 -131.964 103.117 2.72 Accumulated -181.87 -313.834 -210.727 -208.027

*Includes PAT for Fy10-11 is Rs 103.98 Crs (including Deferred Tax of Rs 102.89 Cr) and adjustment of Rs 23.01 Crs on account of Hotel Demerger pertaining to previous years.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 26 of 136

26

Cost of Equity

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 27 of 136

27

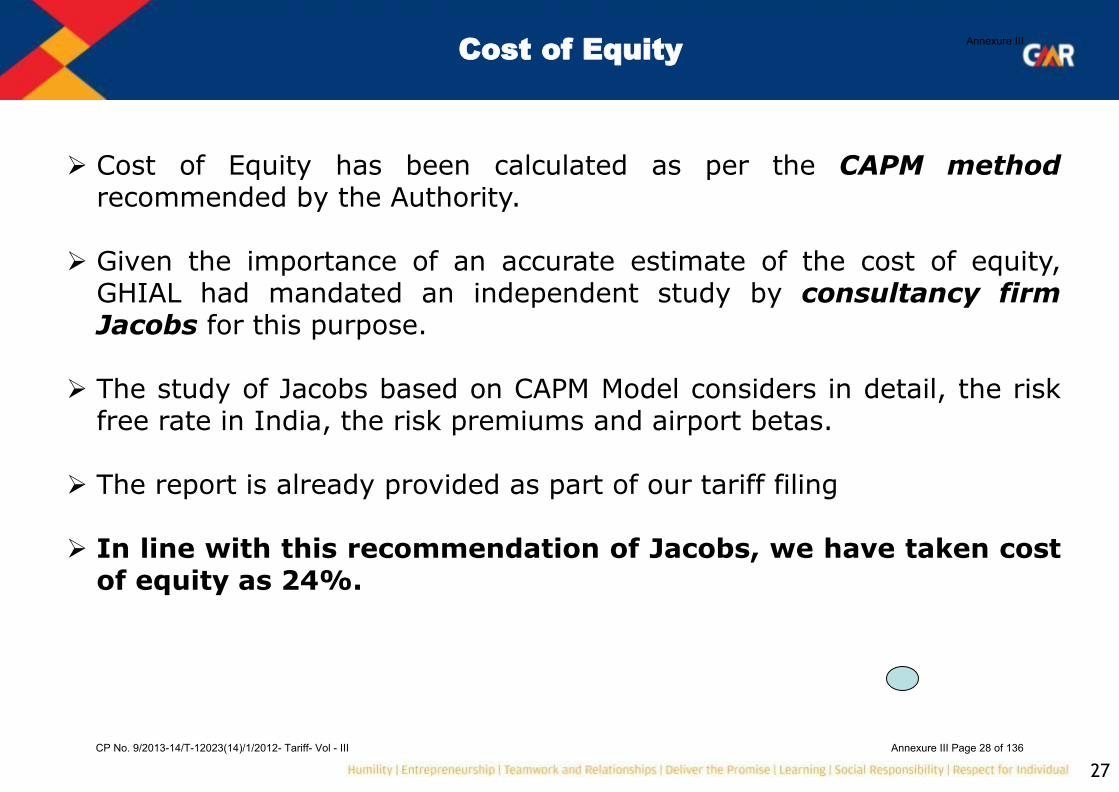

Cost of Equity

Cost of Equity has been calculated as per the CAPM method recommended by the Authority.

Given the importance of an accurate estimate of the cost of equity, GHIAL had mandated an independent study by consultancy firm Jacobs for this purpose.

The study of Jacobs based on CAPM Model considers in detail, the risk free rate in India, the risk premiums and airport betas.

The report is already provided as part of our tariff filing

In line with this recommendation of Jacobs, we have taken cost of equity as 24%.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 28 of 136

28

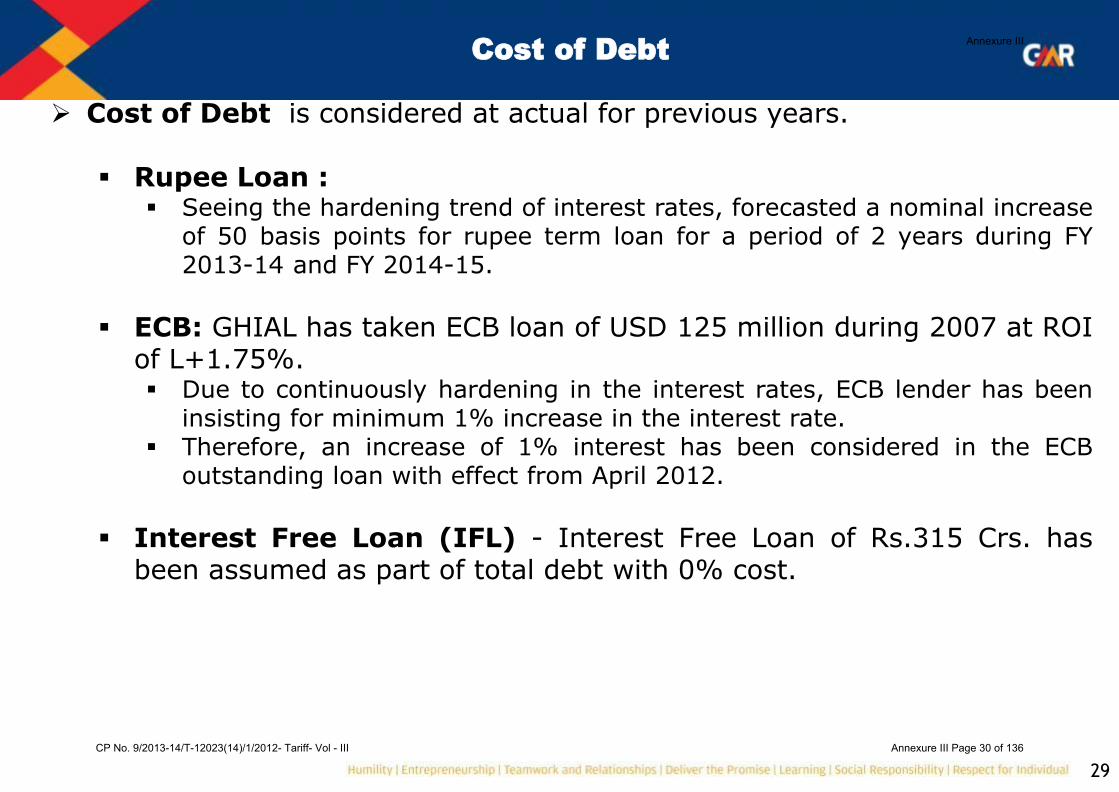

Cost of Debt

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 29 of 136

29

Cost of Debt

Cost of Debt is considered at actual for previous years. Rupee Loan :

Seeing the hardening trend of interest rates, forecasted a nominal increase of 50 basis points for rupee term loan for a period of 2 years during FY 2013-14 and FY 2014-15.

ECB: GHIAL has taken ECB loan of USD 125 million during 2007 at ROI

of L+1.75%. Due to continuously hardening in the interest rates, ECB lender has been

insisting for minimum 1% increase in the interest rate. Therefore, an increase of 1% interest has been considered in the ECB

outstanding loan with effect from April 2012.

Interest Free Loan (IFL) - Interest Free Loan of Rs.315 Crs. has

been assumed as part of total debt with 0% cost.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 30 of 136

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 31 of 136

31

Weighted Average Cost of Capital/Fair Rate of Return

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 32 of 136

32

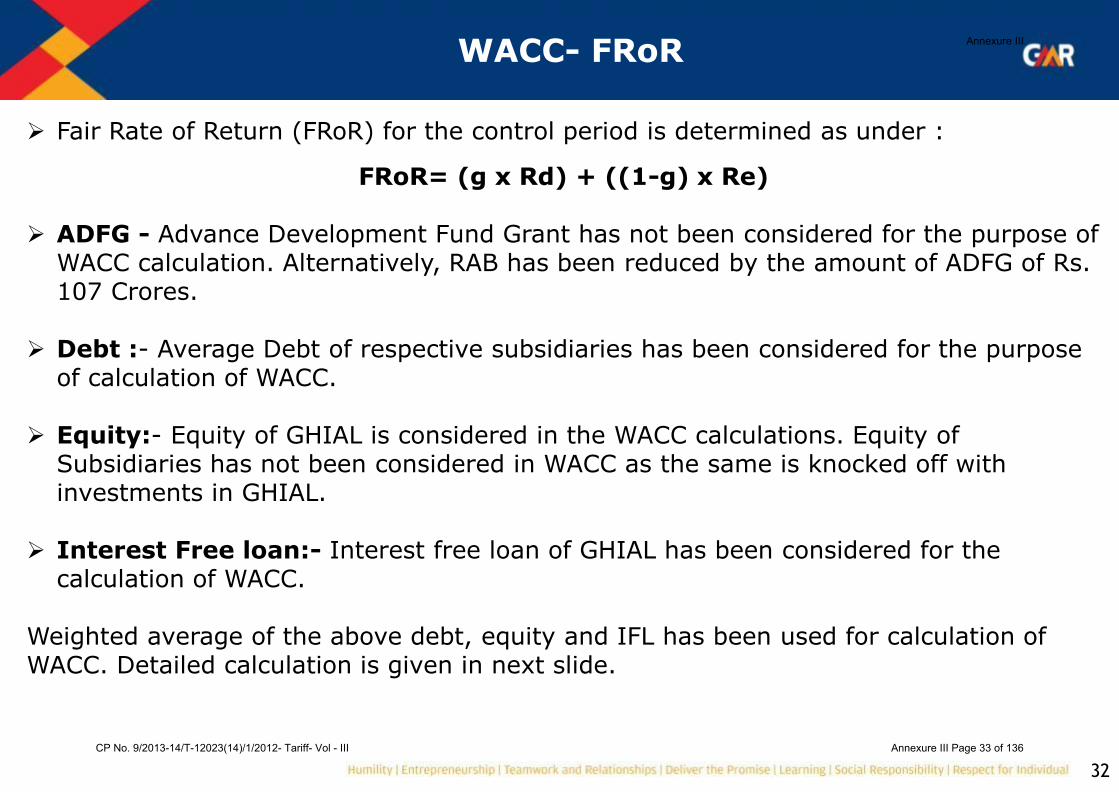

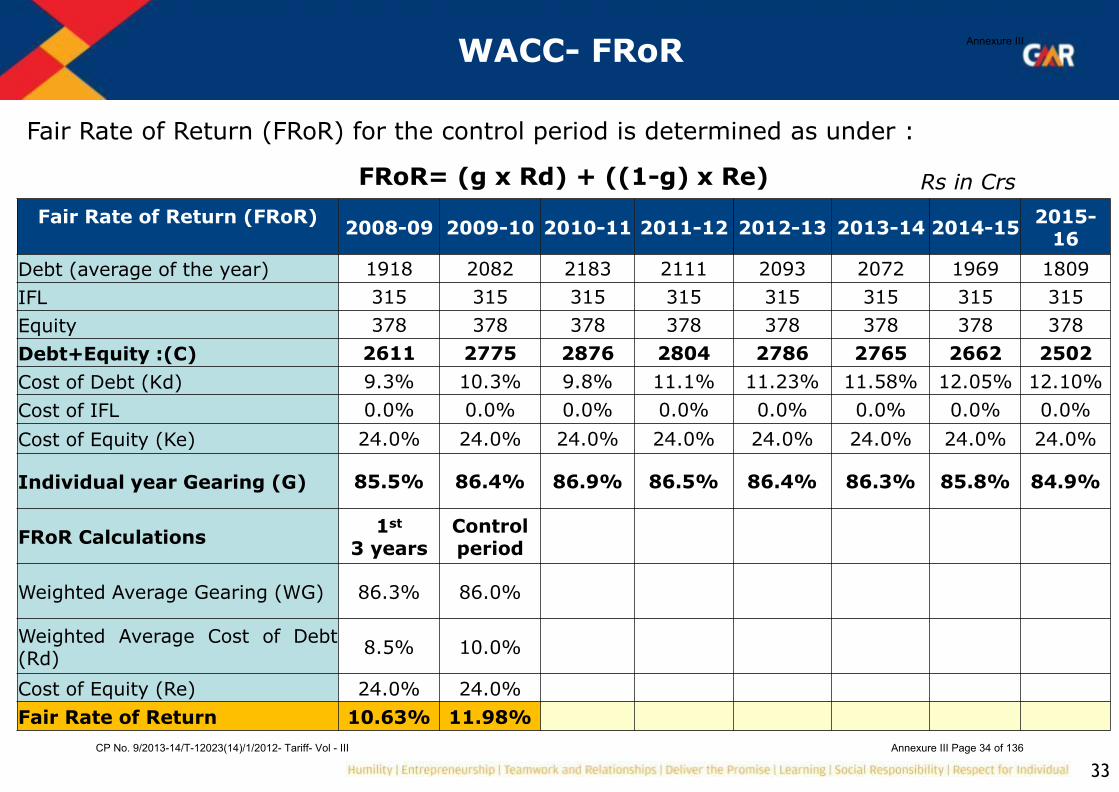

WACC- FRoR

Fair Rate of Return (FRoR) for the control period is determined as under :

FRoR= (g x Rd) + ((1-g) x Re)

ADFG - Advance Development Fund Grant has not been considered for the purpose of WACC calculation. Alternatively, RAB has been reduced by the amount of ADFG of Rs. 107 Crores.

Debt :- Average Debt of respective subsidiaries has been considered for the purpose of calculation of WACC.

Equity:- Equity of GHIAL is considered in the WACC calculations. Equity of Subsidiaries has not been considered in WACC as the same is knocked off with investments in GHIAL.

Interest Free loan:- Interest free loan of GHIAL has been considered for the calculation of WACC.

Weighted average of the above debt, equity and IFL has been used for calculation of WACC. Detailed calculation is given in next slide.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 33 of 136

33

WACC- FRoR

Fair Rate of Return (FRoR) for the control period is determined as under :

FRoR= (g x Rd) + ((1-g) x Re)

Fair Rate of Return (FRoR)

2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-

16

Debt (average of the year) 1918 2082 2183 2111 2093 2072 1969 1809

IFL 315 315 315 315 315 315 315 315

Equity 378 378 378 378 378 378 378 378

Debt+Equity :(C) 2611 2775 2876 2804 2786 2765 2662 2502

Cost of Debt (Kd) 9.3% 10.3% 9.8% 11.1% 11.23% 11.58% 12.05% 12.10%

Cost of IFL 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Cost of Equity (Ke) 24.0% 24.0% 24.0% 24.0% 24.0% 24.0% 24.0% 24.0%

Individual year Gearing (G) 85.5% 86.4% 86.9% 86.5% 86.4% 86.3% 85.8% 84.9%

FRoR Calculations 1st

3 years Control period

Weighted Average Gearing (WG) 86.3% 86.0%

Weighted Average Cost of Debt (Rd)

8.5% 10.0%

Cost of Equity (Re) 24.0% 24.0%

Fair Rate of Return 10.63% 11.98%

Rs in Crs

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 34 of 136

34

Regulated Asset Base (RAB)

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 35 of 136

35

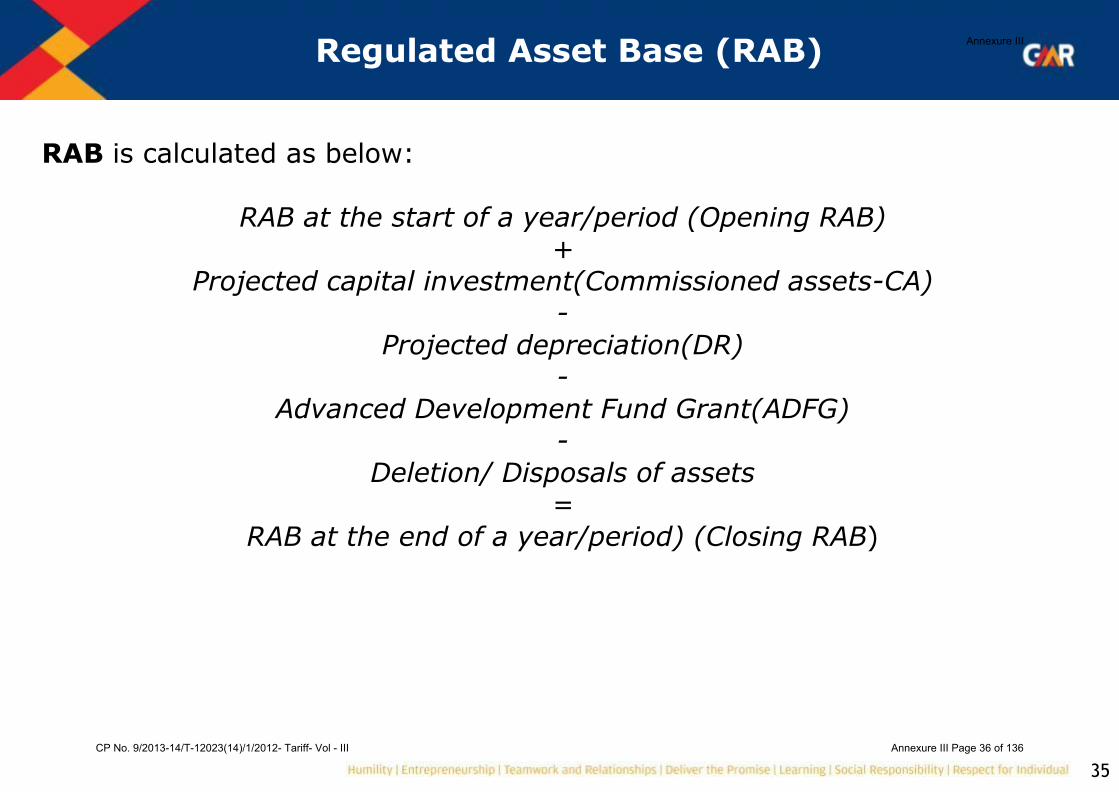

Regulated Asset Base (RAB)

RAB is calculated as below:

RAB at the start of a year/period (Opening RAB) +

Projected capital investment(Commissioned assets-CA) -

Projected depreciation(DR) -

Advanced Development Fund Grant(ADFG) -

Deletion/ Disposals of assets =

RAB at the end of a year/period) (Closing RAB)

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 36 of 136

36

Regulated Asset Base (RAB)

Following approach has been adopted for firming up the RAB during the regulatory control period: • Financial year 2011-12 has been taken as the first year of the control period. • Initial RAB is as per the books of accounts. RAB for the control period has been

firmed up by aggregating the total assets (including assets in subsidiary books) other than fuel farm assets (for which separate filing is being made), at book value on the last day of the previous year (FY 2010-11).

• The Actual Numbers of 2011-12 has been updated in the model. Addition and

deletion to the assets has been taken as per audited financial statements.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 37 of 136

37

Regulated Asset Base (RAB)

• Advance Development fund grant (ADFG) of Rs. 107 Crores has been excluded from assets base. RAB and the corresponding depreciation also have been reduced accordingly.

• Fuel farm assets have been separated from total assets and subsequently

airport RAB as separate filing is required under the Authority‟s guidelines. • Assets of the fully owned subsidiaries have been included in the

calculation. GMR Hotel & Resorts Ltd. (GHRL) GMR Hyderabad Aviation SEZ Ltd. (GHASL) an Hyderabad Duty Free Retail Limited

For the financial year 2012-13 to 2015-16, Capex is projected and added to the respective year.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 38 of 136

38

Background of Hotel

• In line with this global practice, GMR has developed a Airport Hotel as part of the Hyderabad International Airport project. The hotel is operated by a reputed global operator “Accor” under its Novotel brand. It started its operations in the year 2008.

• Airport Hotel is fully owned by GHIAL and is mainly catering to the

passengers and airlines crew. Therefore, we have considered the asset base of the hotel fully as part of GHIAL RAB

• Hotel play a crucial role in facilitating the Airport for emerging as a

regional transit hub for both passenger and cargo and are required near the Airport to meet the requirements of Transit Passengers, Airline Crew and Other Business and MICE.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 39 of 136

39

Hotel : Facts of last 4 years

• Hotel has primarily been used by Airport travelers/transit

passengers, Airline Crew and by Corporates for their Meetings/Incentives and for Conferences and Social Events.

• Individual Airport Travellers contributed about 120,000 room-nights (54% of total occupancy)

• Airline Crew contributed about 48,000 room-nights (22% of the occupancy)

• In addition to the above, the Airport Hotel is also an integral part of the

Airline emergency Evaluation Plan for the passengers and airline staff Hotel has significant synergy with the Airport and has both directly and indirectly benefiting the Airport and Air Travellers.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 40 of 136

40

Background of SEZ

• GMR Hyderabad Aviation SEZ Ltd. (GHASL) is developing a world class aviation and

aerospace SEZ park. And was notified by the Government of India (GOI) on October

20th 2009 in the name of GHIAL. Consequently, on March 3rd 2010, at GHIAL’s

request, the approval granted earlier was transferred by GOI in the name of GHASL.

• GHASL is a 100% subsidiary of GHIAL, and is undertaking all capital investments

required for the development of infrastructure in the Aviation SEZ.

• The development of SEZ has been planned to enhance the business activities and

traffic of RGIA and to create a larger multiplier economic impact in the region

• Currently, there are 2 operating units in SEZ namely MRO Services: Engine Maintenance Training.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 41 of 136

41

SEZ : detailed facts

• The presence of various aerospace units in aerospace cluster creates advantages of synergy in terms of resources such as

• Skilled manpower, • Special purpose machines, • Training etc.

and it makes aerospace units more competitive. This ultimately become a key engine for development and thereby provide the much required impetus and boost to the Airport Business.

• SEZ units would attract incremental ATM‟s into the MRO unit since the MRO would be competitive and would attract many domestic airlines to get their aircraft serviced within India as against the current practice of sending them overseas thereby being a valuable proposition.

• In the long run presence of facilities such as MRO, FTZ, Aviation Training Centers, Aerospace Manufacturing and Assembly Units in GMR Aerospace Park shall contribute significantly in Hyderabad Airport becoming a HUB

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 42 of 136

42

Background of Duty Free

• Hyderabad Duty Free Retail Limited (HDFRL) was set up as a 100% subsidiary of GHIAL in June 2010 with the objective of owning and managing the Duty Free business in the international terminal.

• Prior to 2010 the Duty Free concession was given to Nuance Group. They

were not able to run the business successfully and GHIAL has to enter into a settlement to take over the assets and operations of the store.

• A careful consideration of options and business models was done to understand the profitability of the duty free operations. Hence in order to maximize the sales potential and ensure smooth store operations it was decided that GHIAL would run the duty free business on its own and build the necessary systems, processes and people capability required.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 43 of 136

43

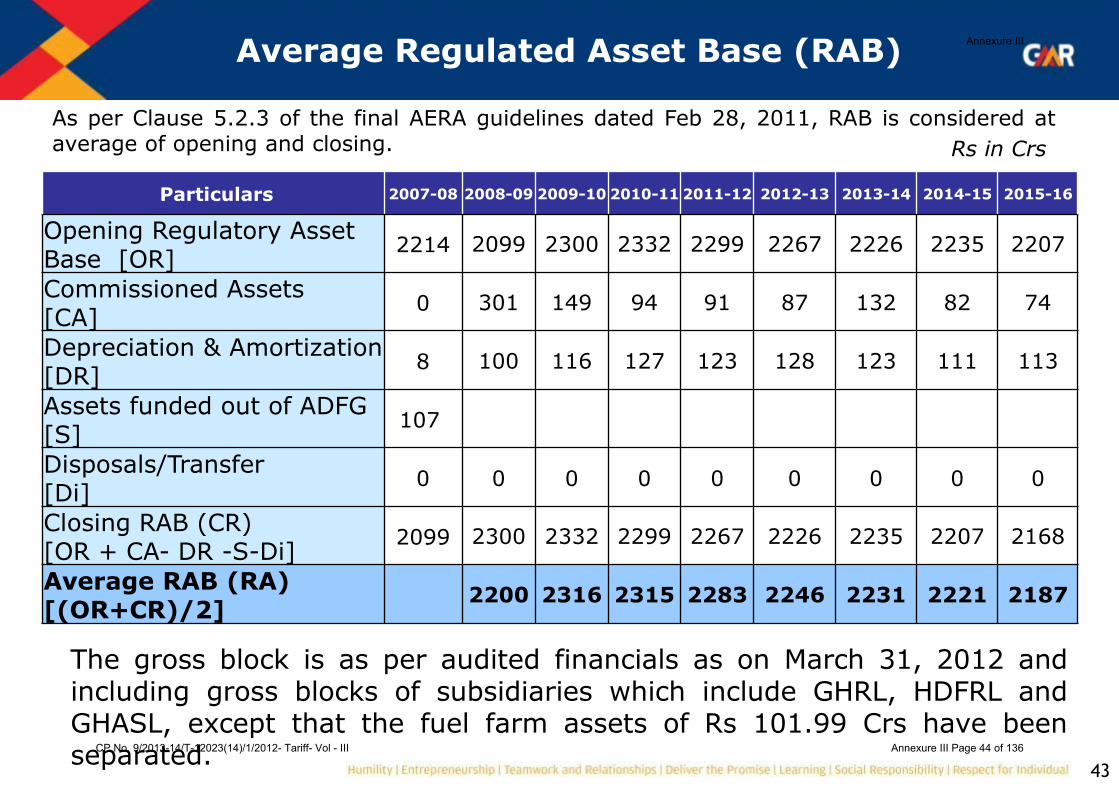

Average Regulated Asset Base (RAB)

Particulars 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16

Opening Regulatory Asset Base [OR]

2214 2099 2300 2332 2299 2267 2226 2235 2207

Commissioned Assets [CA]

0 301 149 94 91 87 132 82 74

Depreciation & Amortization [DR]

8 100 116 127 123 128 123 111 113

Assets funded out of ADFG [S]

107

Disposals/Transfer [Di]

0 0 0 0 0 0 0 0 0

Closing RAB (CR) [OR + CA- DR -S-Di]

2099 2300 2332 2299 2267 2226 2235 2207 2168

Average RAB (RA) [(OR+CR)/2]

2200 2316 2315 2283 2246 2231 2221 2187

The gross block is as per audited financials as on March 31, 2012 and including gross blocks of subsidiaries which include GHRL, HDFRL and GHASL, except that the fuel farm assets of Rs 101.99 Crs have been separated.

As per Clause 5.2.3 of the final AERA guidelines dated Feb 28, 2011, RAB is considered at average of opening and closing. Rs in Crs

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 44 of 136

44

Regulated Asset Base (RAB)

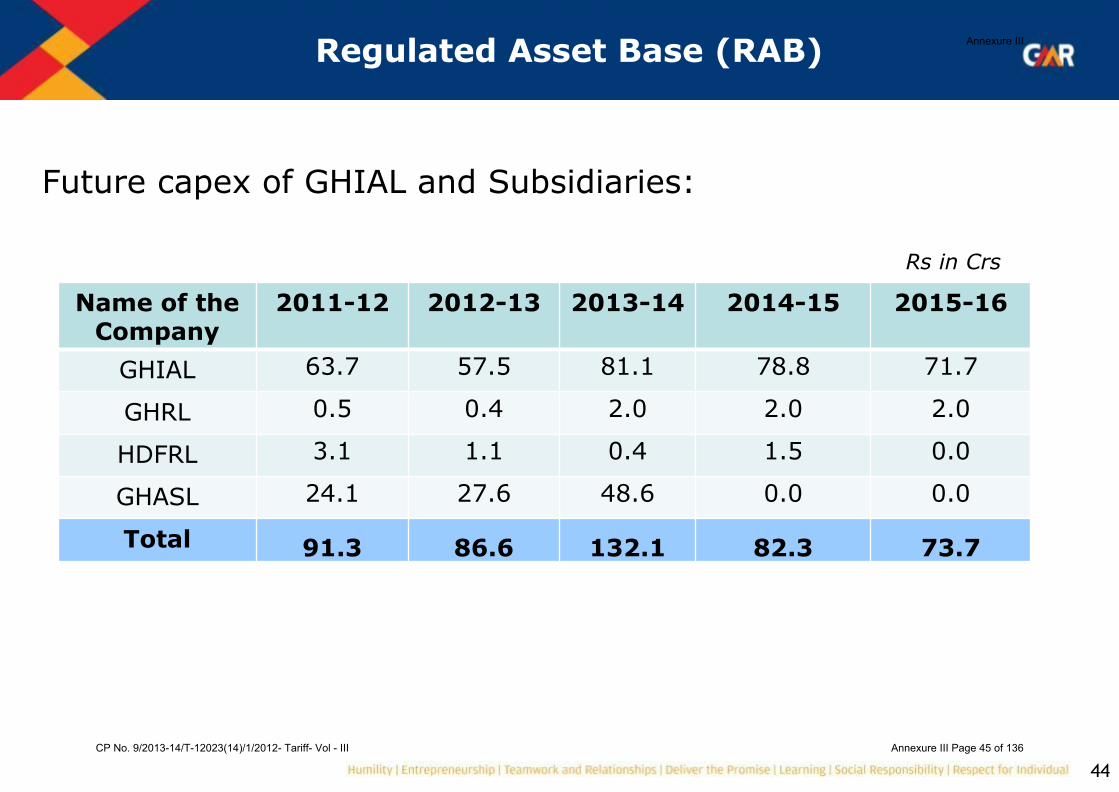

Future capex of GHIAL and Subsidiaries:

Name of the Company

2011-12 2012-13 2013-14 2014-15 2015-16

GHIAL 63.7 57.5 81.1 78.8 71.7

GHRL 0.5 0.4 2.0 2.0 2.0

HDFRL 3.1 1.1 0.4 1.5 0.0

GHASL 24.1 27.6 48.6 0.0 0.0

Total 91.3 86.6 132.1 82.3 73.7

Rs in Crs

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 45 of 136

45

Depreciation

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 46 of 136

46

Depreciation

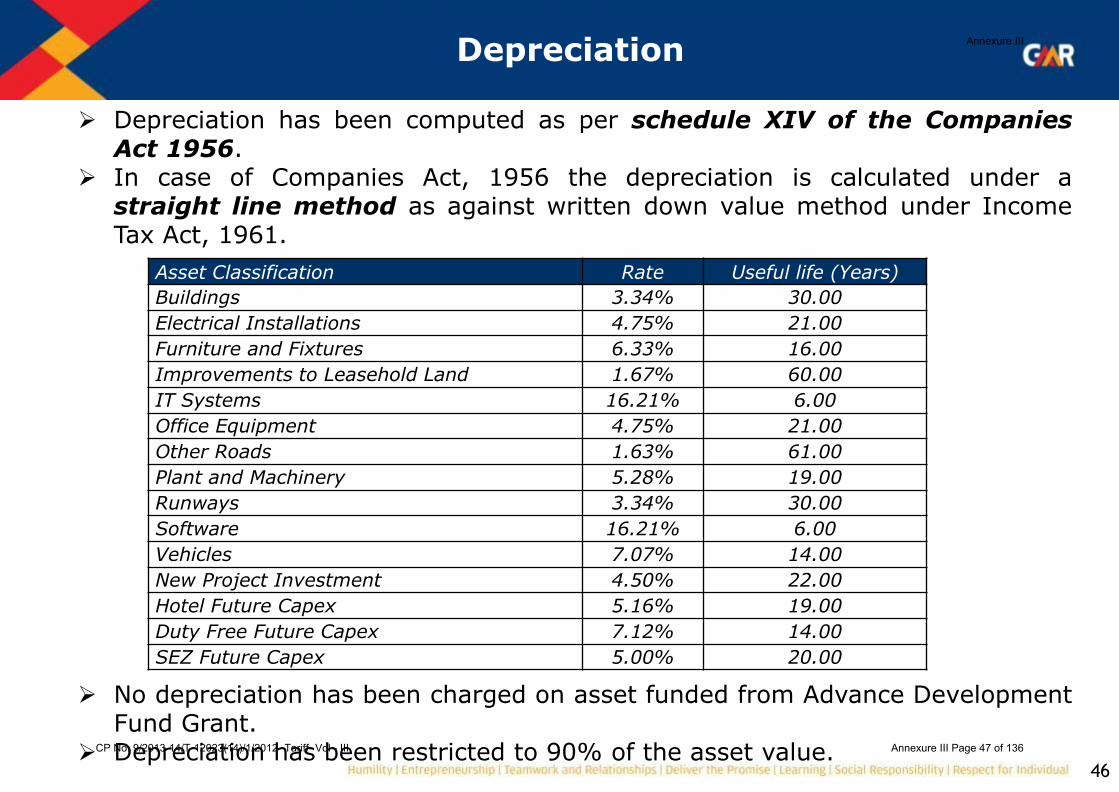

Depreciation has been computed as per schedule XIV of the Companies Act 1956.

In case of Companies Act, 1956 the depreciation is calculated under a straight line method as against written down value method under Income Tax Act, 1961.

No depreciation has been charged on asset funded from Advance Development

Fund Grant. Depreciation has been restricted to 90% of the asset value.

Asset Classification Rate Useful life (Years)

Buildings 3.34% 30.00

Electrical Installations 4.75% 21.00

Furniture and Fixtures 6.33% 16.00

Improvements to Leasehold Land 1.67% 60.00

IT Systems 16.21% 6.00

Office Equipment 4.75% 21.00

Other Roads 1.63% 61.00

Plant and Machinery 5.28% 19.00

Runways 3.34% 30.00

Software 16.21% 6.00

Vehicles 7.07% 14.00

New Project Investment 4.50% 22.00

Hotel Future Capex 5.16% 19.00

Duty Free Future Capex 7.12% 14.00

SEZ Future Capex 5.00% 20.00

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 47 of 136

47

Operations and Maintenance Expenditure

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 48 of 136

48

O&M Projection

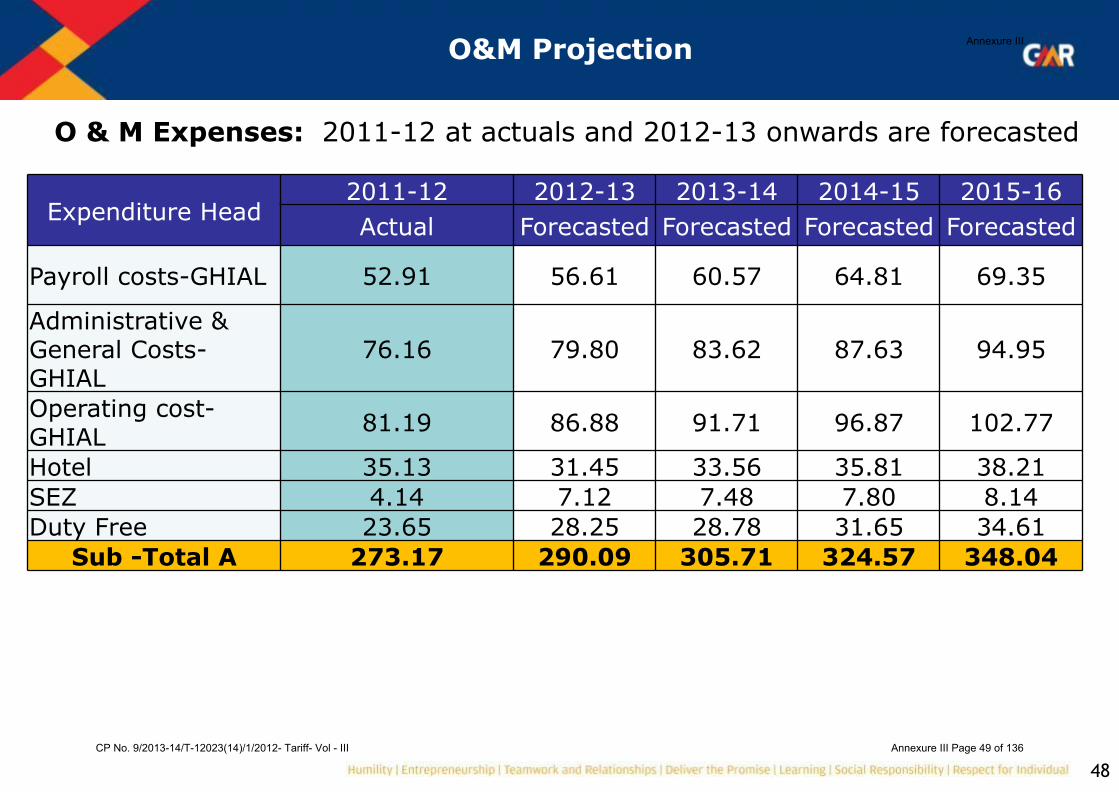

O & M Expenses: 2011-12 at actuals and 2012-13 onwards are forecasted

Expenditure Head 2011-12 2012-13 2013-14 2014-15 2015-16

Actual Forecasted Forecasted Forecasted Forecasted

Payroll costs-GHIAL 52.91 56.61 60.57 64.81 69.35

Administrative & General Costs-GHIAL

76.16 79.80 83.62 87.63 94.95

Operating cost-GHIAL

81.19 86.88 91.71 96.87 102.77

Hotel 35.13 31.45 33.56 35.81 38.21

SEZ 4.14 7.12 7.48 7.80 8.14

Duty Free 23.65 28.25 28.78 31.65 34.61

Sub -Total A 273.17 290.09 305.71 324.57 348.04

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 49 of 136

49

Assumptions for O & M Expenses

The total operating and maintenance expenditure have been classified as under and the same have been escalated over the actuals of FY 2011-12 as given below: Salaries and manpower outsourcing: Real increase in salaries is taken

at 7% p.a. An increase is assumed in manpower by 10% for every 1.5 million increase in traffic.

Power Cost: Real increase of 7% p.a. has been considered.

Security Cost: Real Increase of 7 % has been taken for future year on manpower cost. Increase in manpower numbers by 10% has been considered for every increase in pax by 1.5 million.

General and Administration charges: Real increase is taken as 5% pa

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 50 of 136

50

Assumptions for O & M Expenses

Repair and Maintenance: Real increase of 7% is considered pa and additional increase of 10% is taken for every increase in pax by 1.5 million

Utilities, other operating expenses and insurance: - Real increase of 7% is considered pa.

Revenue share- A revenue share of 4% as per the terms of the concession agreement.

Hotel, Duty Free and SEZ Opex - The total O&M expenditure for the FY 2011-12 has been taken as per audited numbers. The opex for FY 2012-13 is considered as per six months extrapolation and thereafter the growth rates as discussed above in GHIAL has been considered.

Inflationary increase is not considered as it is understood that the Authority will give an allowance towards inflation (WPI) over and above the target revenue being submitted herewith based on actual WPI numbers during the filing of annual tariff proposal every year.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 51 of 136

51

Taxation

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 52 of 136

52

Assumption for Taxes

The computation of income tax, on total income, has been made on the prevailing Income Tax laws and rules.

Further, the assumptions are as under:

• Tax Computation has also considered MAT provisions.

• 80IA benefits have been considered for normal tax calculations.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 53 of 136

53

Traffic

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 54 of 136

54

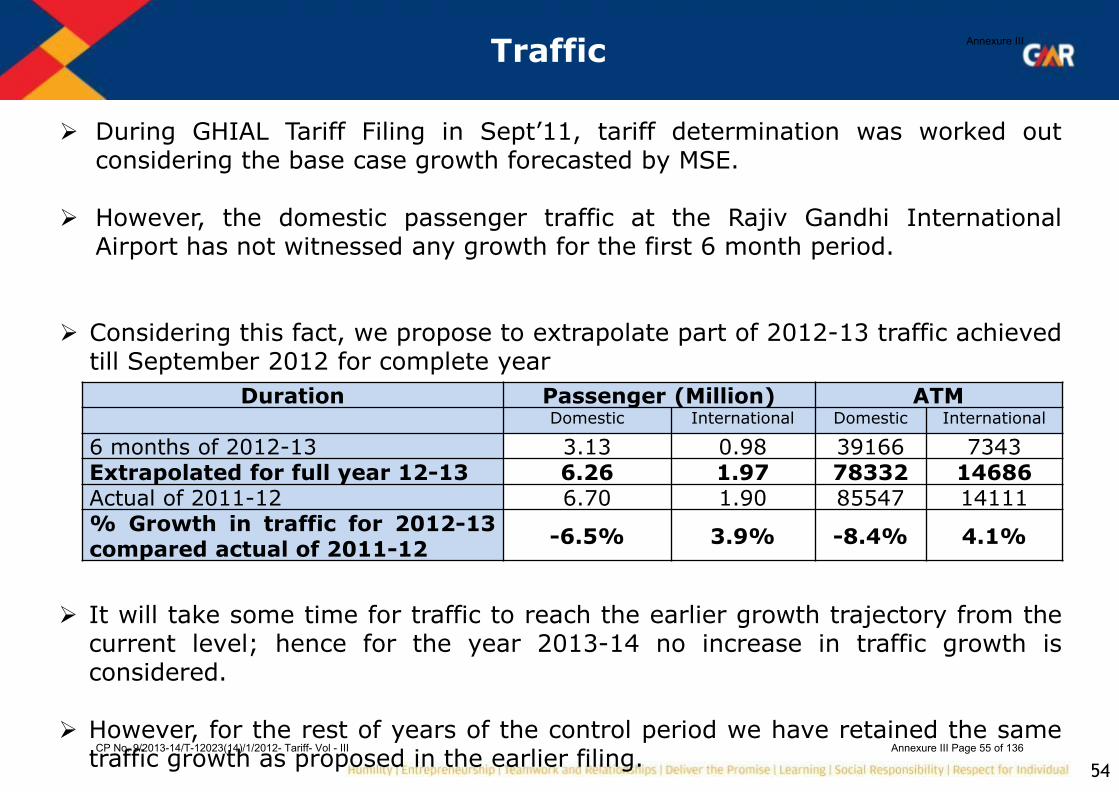

Traffic

During GHIAL Tariff Filing in Sept‟11, tariff determination was worked out

considering the base case growth forecasted by MSE.

However, the domestic passenger traffic at the Rajiv Gandhi International Airport has not witnessed any growth for the first 6 month period.

Considering this fact, we propose to extrapolate part of 2012-13 traffic achieved

till September 2012 for complete year

Duration Passenger (Million) ATM Domestic International Domestic International

6 months of 2012-13 3.13 0.98 39166 7343 Extrapolated for full year 12-13 6.26 1.97 78332 14686 Actual of 2011-12 6.70 1.90 85547 14111 % Growth in traffic for 2012-13 compared actual of 2011-12

-6.5% 3.9% -8.4% 4.1%

It will take some time for traffic to reach the earlier growth trajectory from the current level; hence for the year 2013-14 no increase in traffic growth is considered.

However, for the rest of years of the control period we have retained the same

traffic growth as proposed in the earlier filing.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 55 of 136

55

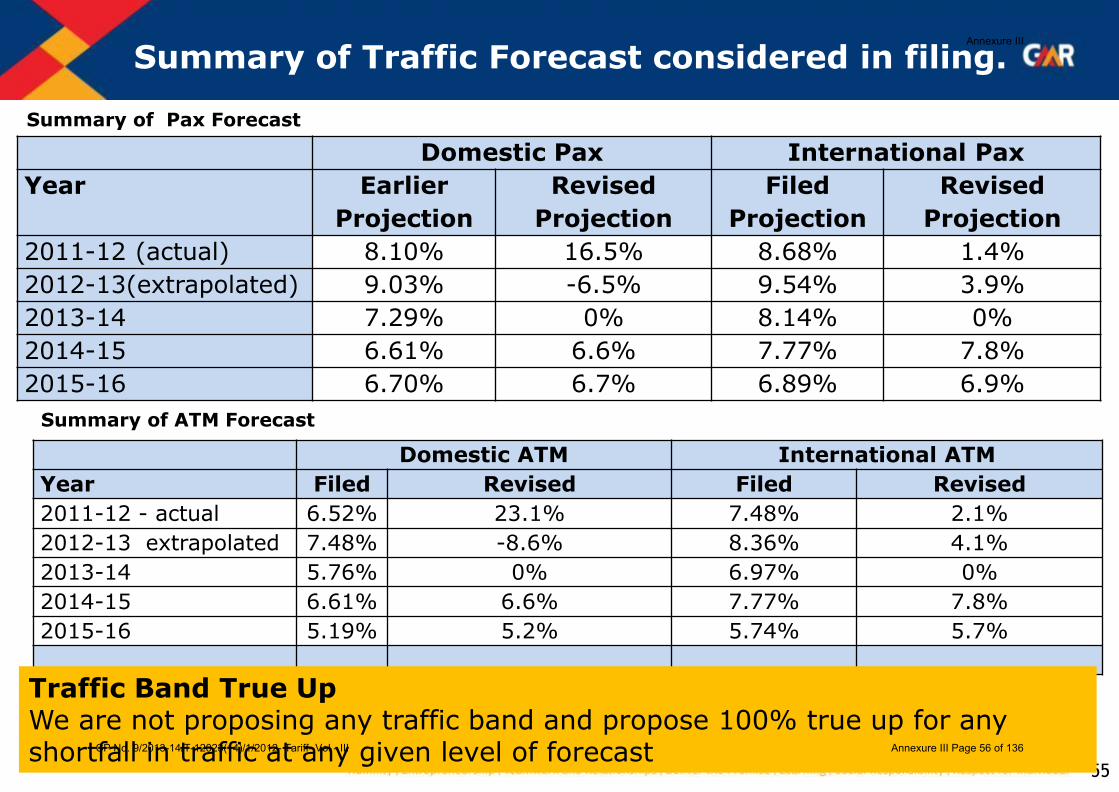

Summary of Traffic Forecast considered in filing.

Domestic Pax International Pax

Year Earlier

Projection

Revised

Projection

Filed

Projection

Revised

Projection

2011-12 (actual) 8.10% 16.5% 8.68% 1.4%

2012-13(extrapolated) 9.03% -6.5% 9.54% 3.9%

2013-14 7.29% 0% 8.14% 0%

2014-15 6.61% 6.6% 7.77% 7.8%

2015-16 6.70% 6.7% 6.89% 6.9%

Domestic ATM International ATM

Year Filed Revised Filed Revised

2011-12 - actual 6.52% 23.1% 7.48% 2.1%

2012-13 extrapolated 7.48% -8.6% 8.36% 4.1%

2013-14 5.76% 0% 6.97% 0%

2014-15 6.61% 6.6% 7.77% 7.8%

2015-16 5.19% 5.2% 5.74% 5.7%

Summary of ATM Forecast

Summary of Pax Forecast

Traffic Band True Up We are not proposing any traffic band and propose 100% true up for any shortfall in traffic at any given level of forecast

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 56 of 136

56

Non Aero Revenues

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 57 of 136

57

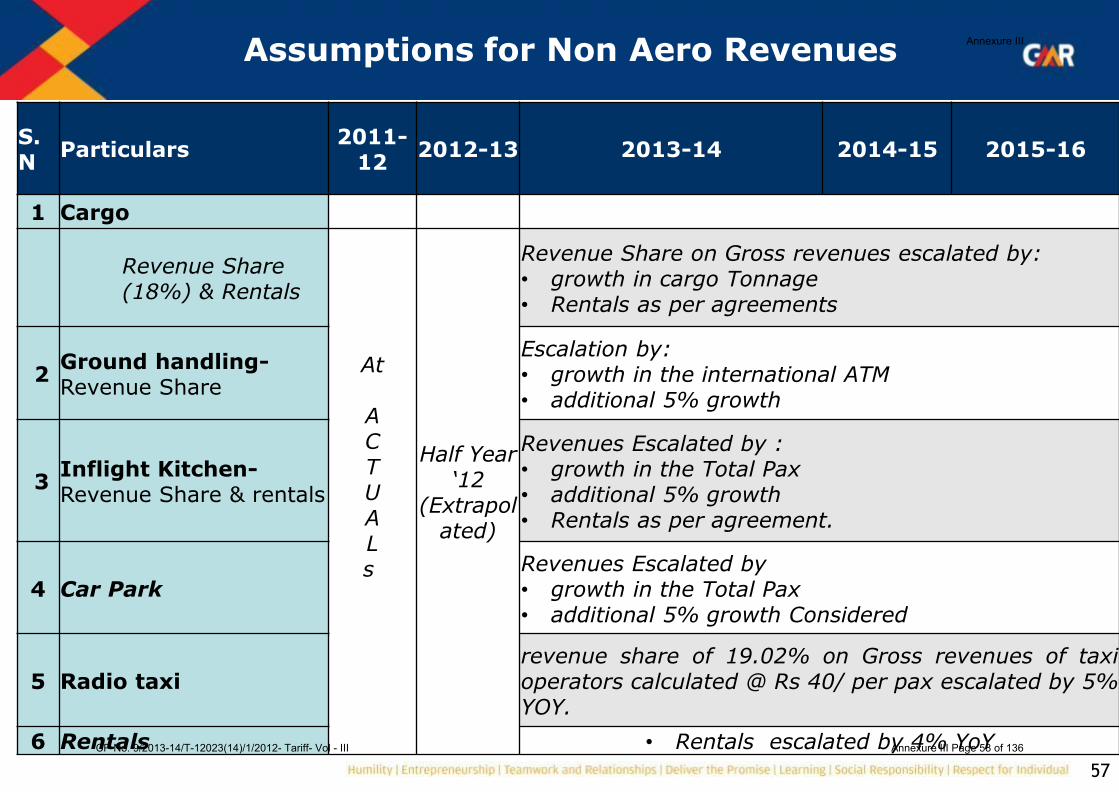

Assumptions for Non Aero Revenues

S.N

Particulars 2011-

12 2012-13 2013-14 2014-15 2015-16

1 Cargo

Revenue Share (18%) & Rentals

At A C T U A L s

Half Year ‘12

(Extrapolated)

Revenue Share on Gross revenues escalated by: • growth in cargo Tonnage • Rentals as per agreements

2 Ground handling- Revenue Share

Escalation by: • growth in the international ATM • additional 5% growth

3 Inflight Kitchen- Revenue Share & rentals

Revenues Escalated by : • growth in the Total Pax • additional 5% growth • Rentals as per agreement.

4 Car Park Revenues Escalated by • growth in the Total Pax • additional 5% growth Considered

5 Radio taxi revenue share of 19.02% on Gross revenues of taxi operators calculated @ Rs 40/ per pax escalated by 5% YOY.

6 Rentals • Rentals escalated by 4% YoY

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 58 of 136

58

Assumptions for Non Aero Revenues

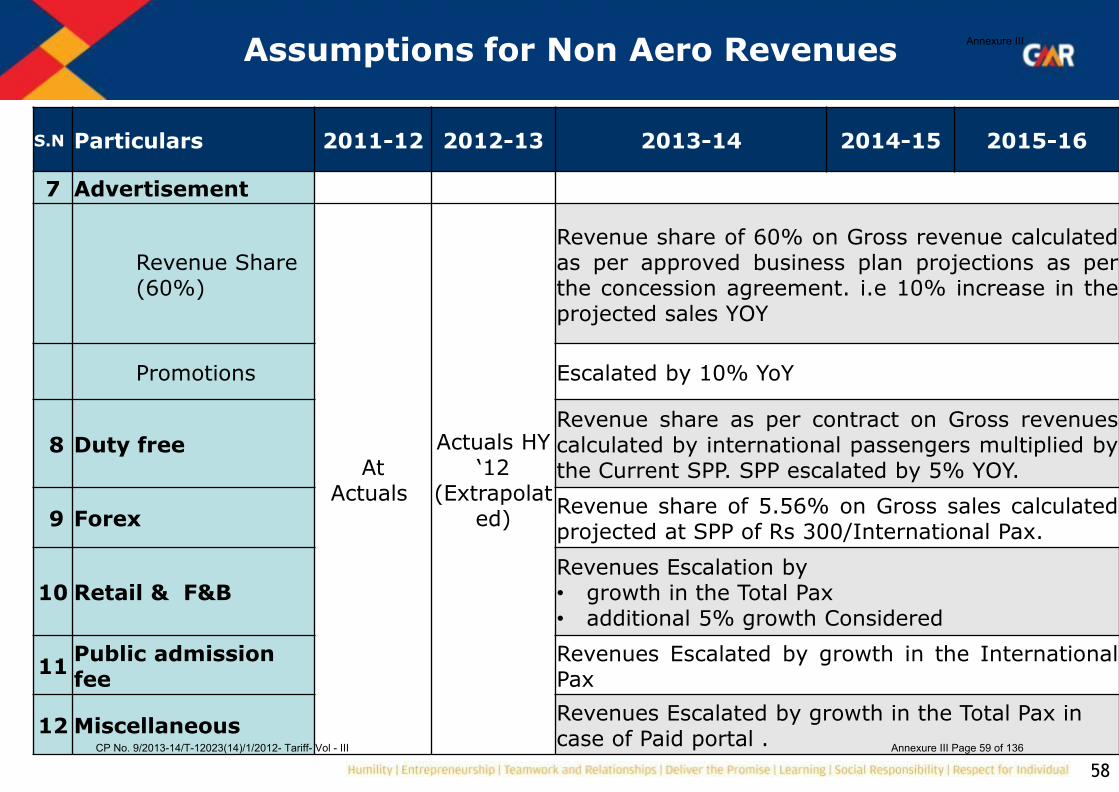

S.N Particulars 2011-12 2012-13 2013-14 2014-15 2015-16

7 Advertisement

Revenue Share (60%)

At Actuals

Actuals HY „12

(Extrapolated)

Revenue share of 60% on Gross revenue calculated as per approved business plan projections as per the concession agreement. i.e 10% increase in the projected sales YOY

Promotions Escalated by 10% YoY

8 Duty free Revenue share as per contract on Gross revenues calculated by international passengers multiplied by the Current SPP. SPP escalated by 5% YOY.

9 Forex Revenue share of 5.56% on Gross sales calculated projected at SPP of Rs 300/International Pax.

10 Retail & F&B Revenues Escalation by • growth in the Total Pax • additional 5% growth Considered

11 Public admission fee

Revenues Escalated by growth in the International Pax

12 Miscellaneous Revenues Escalated by growth in the Total Pax in case of Paid portal .

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 59 of 136

59

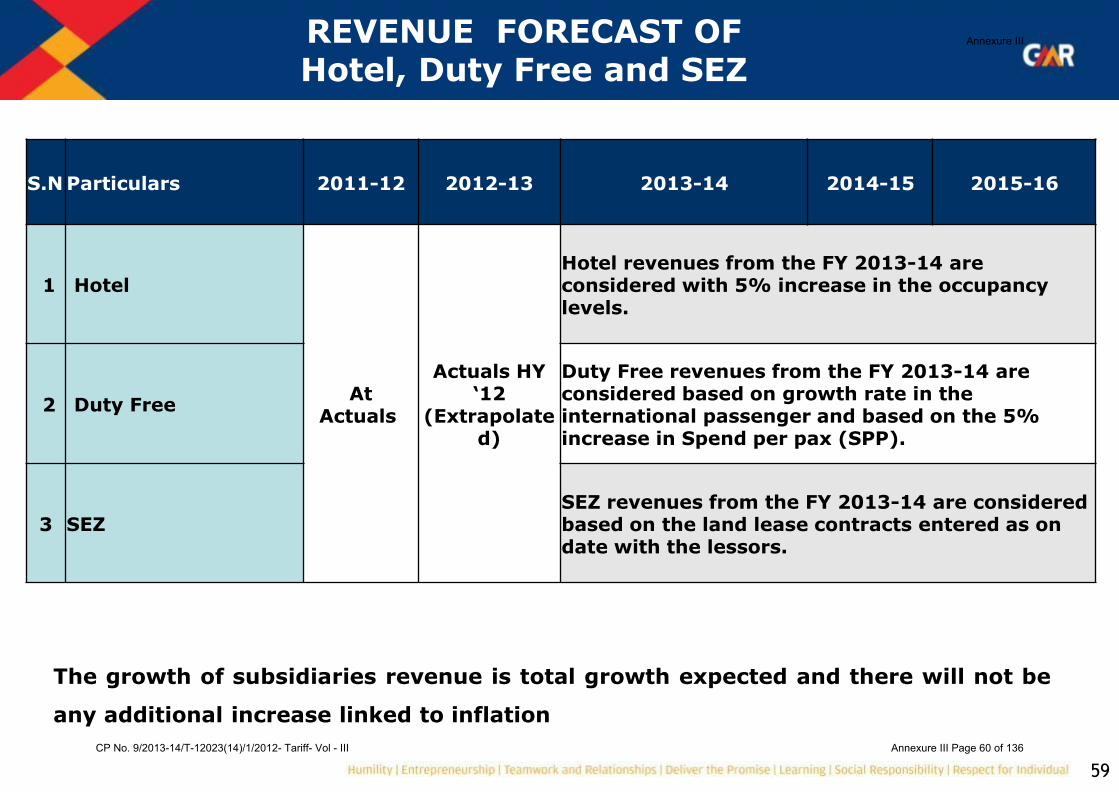

S.N Particulars 2011-12 2012-13 2013-14 2014-15 2015-16

1 Hotel

At Actuals

Actuals HY „12

(Extrapolated)

Hotel revenues from the FY 2013-14 are considered with 5% increase in the occupancy levels.

2 Duty Free

Duty Free revenues from the FY 2013-14 are considered based on growth rate in the international passenger and based on the 5% increase in Spend per pax (SPP).

3 SEZ SEZ revenues from the FY 2013-14 are considered based on the land lease contracts entered as on date with the lessors.

REVENUE FORECAST OF Hotel, Duty Free and SEZ

The growth of subsidiaries revenue is total growth expected and there will not be

any additional increase linked to inflation

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 60 of 136

60

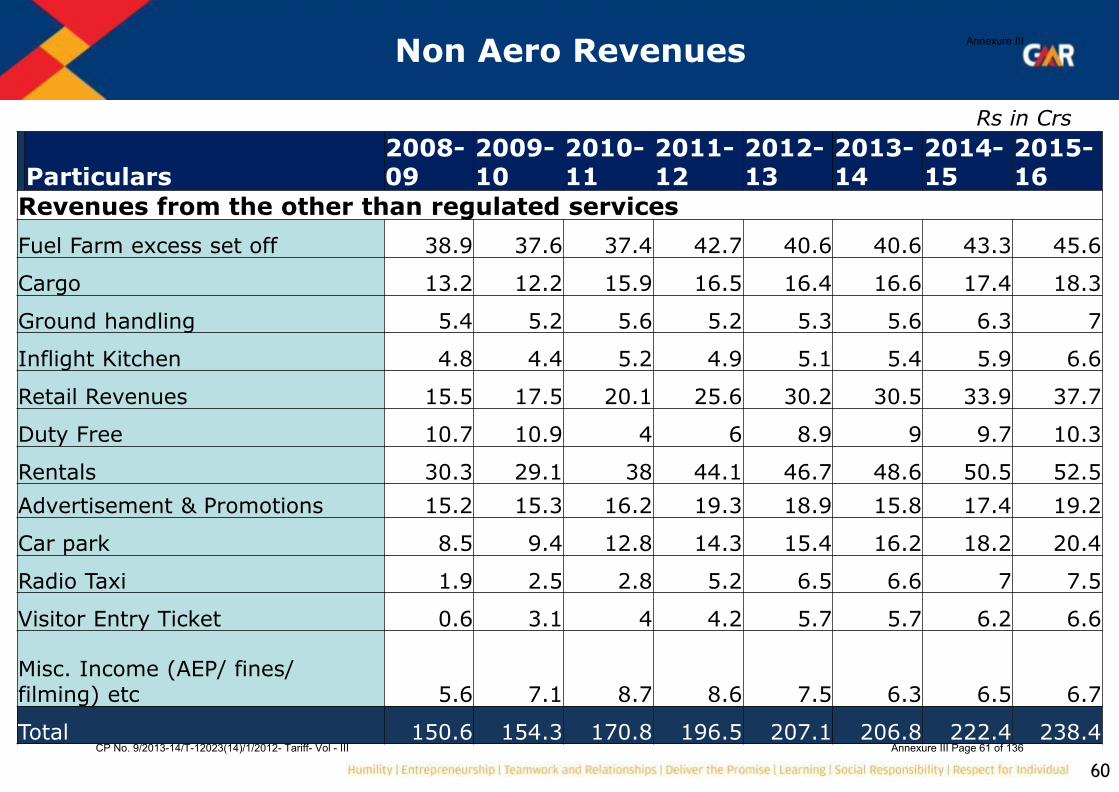

Non Aero Revenues

Particulars 2008-09

2009-10

2010-11

2011-12

2012-13

2013-14

2014-15

2015-16

Revenues from the other than regulated services

Fuel Farm excess set off 38.9 37.6 37.4 42.7 40.6 40.6 43.3 45.6

Cargo 13.2 12.2 15.9 16.5 16.4 16.6 17.4 18.3

Ground handling 5.4 5.2 5.6 5.2 5.3 5.6 6.3 7

Inflight Kitchen 4.8 4.4 5.2 4.9 5.1 5.4 5.9 6.6

Retail Revenues 15.5 17.5 20.1 25.6 30.2 30.5 33.9 37.7

Duty Free 10.7 10.9 4 6 8.9 9 9.7 10.3

Rentals 30.3 29.1 38 44.1 46.7 48.6 50.5 52.5

Advertisement & Promotions 15.2 15.3 16.2 19.3 18.9 15.8 17.4 19.2

Car park 8.5 9.4 12.8 14.3 15.4 16.2 18.2 20.4

Radio Taxi 1.9 2.5 2.8 5.2 6.5 6.6 7 7.5

Visitor Entry Ticket 0.6 3.1 4 4.2 5.7 5.7 6.2 6.6

Misc. Income (AEP/ fines/ filming) etc 5.6 7.1 8.7 8.6 7.5 6.3 6.5 6.7

Total 150.6 154.3 170.8 196.5 207.1 206.8 222.4 238.4

Rs in Crs

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 61 of 136

61

Non Aero Revenues

2008-09

2009-10

2010-11

2011-12

2012-13

2013-14

2014-15

2015-16

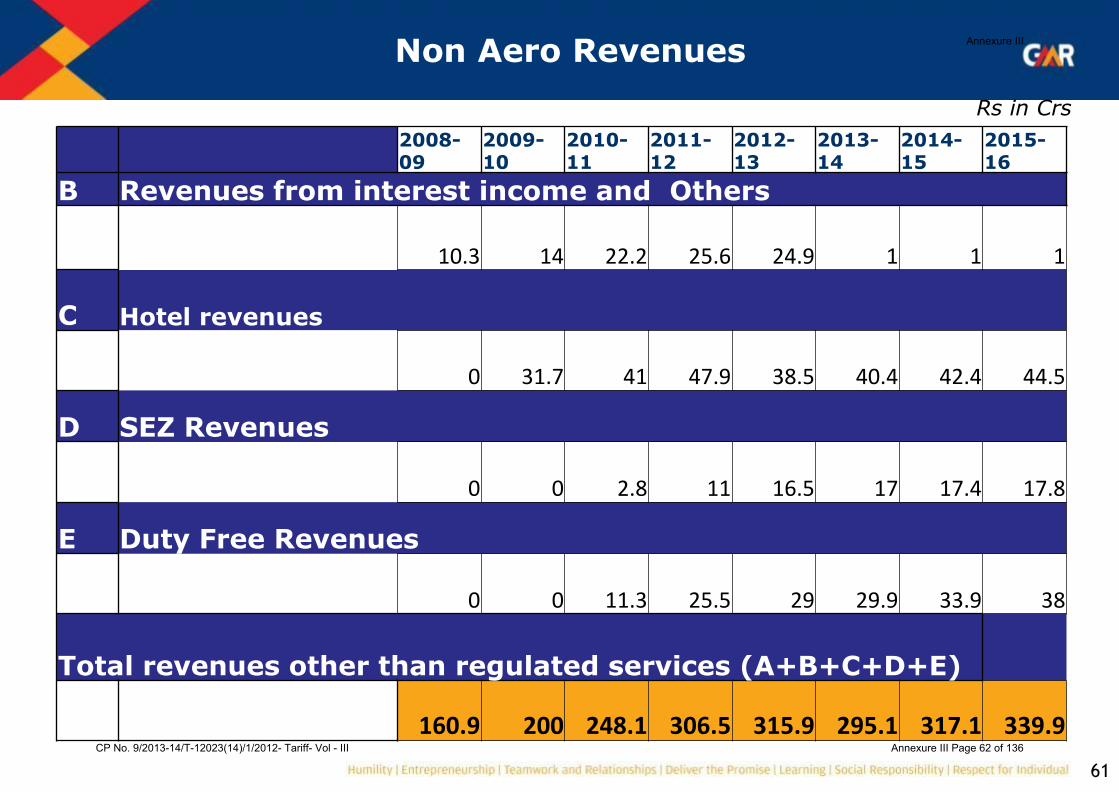

B Revenues from interest income and Others

10.3 14 22.2 25.6 24.9 1 1 1

C Hotel revenues

0 31.7 41 47.9 38.5 40.4 42.4 44.5

D SEZ Revenues

0 0 2.8 11 16.5 17 17.4 17.8

E Duty Free Revenues

0 0 11.3 25.5 29 29.9 33.9 38

Total revenues other than regulated services (A+B+C+D+E)

160.9 200 248.1 306.5 315.9 295.1 317.1 339.9

Rs in Crs

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 62 of 136

62

Aggregate Revenue Requirement(ARR)

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 63 of 136

63

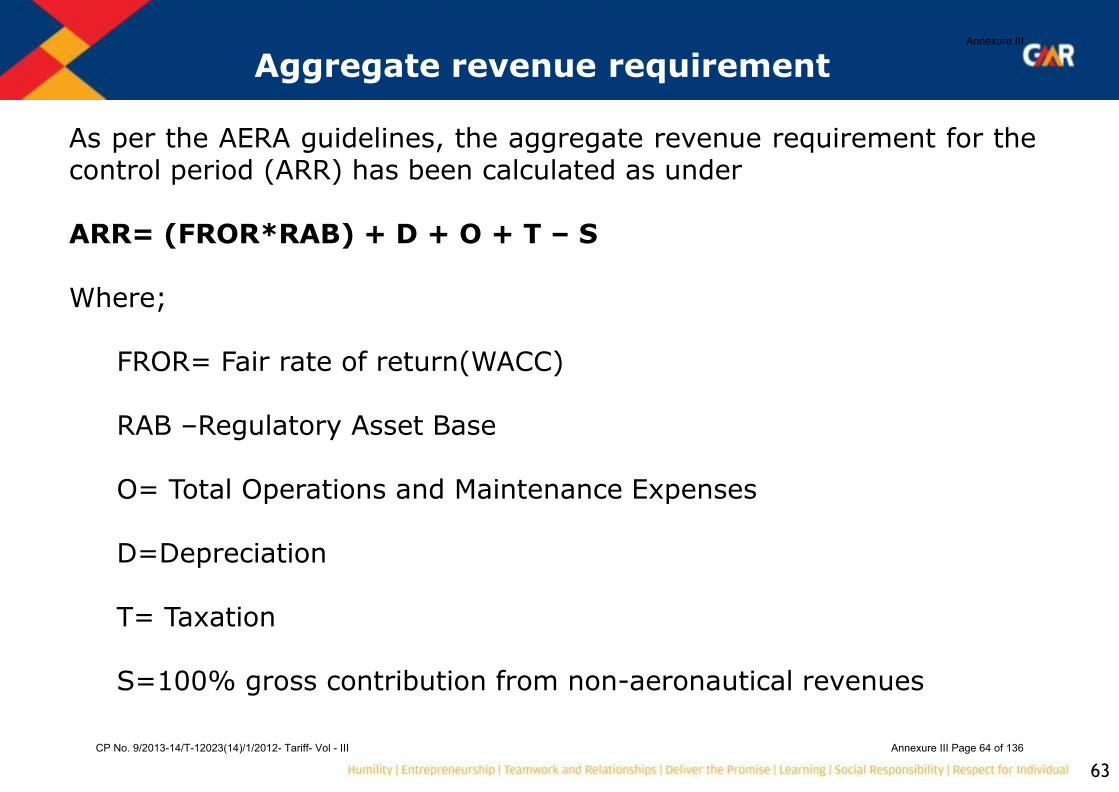

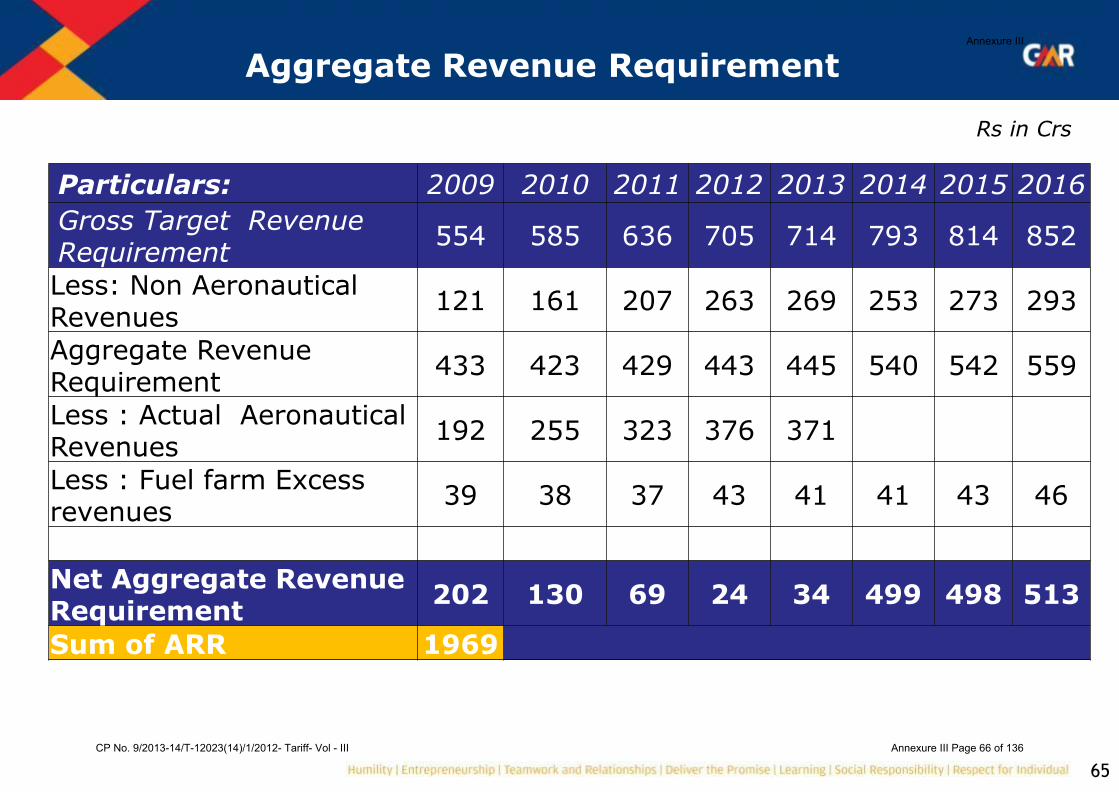

Aggregate revenue requirement

As per the AERA guidelines, the aggregate revenue requirement for the control period (ARR) has been calculated as under ARR= (FROR*RAB) + D + O + T – S

Where;

FROR= Fair rate of return(WACC) RAB –Regulatory Asset Base O= Total Operations and Maintenance Expenses D=Depreciation T= Taxation S=100% gross contribution from non-aeronautical revenues

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 64 of 136

64

Aggregate Revenue Requirement

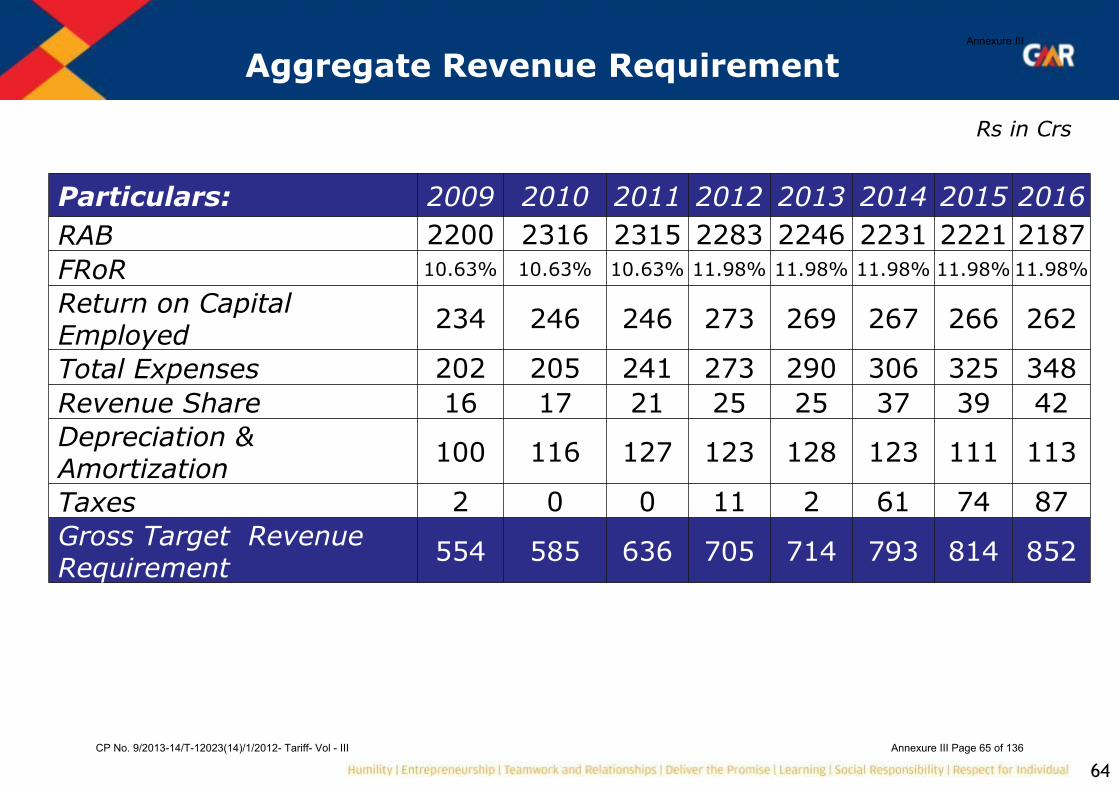

Particulars: 2009 2010 2011 2012 2013 2014 2015 2016

RAB 2200 2316 2315 2283 2246 2231 2221 2187

FRoR 10.63% 10.63% 10.63% 11.98% 11.98% 11.98% 11.98% 11.98%

Return on Capital Employed

234 246 246 273 269 267 266 262

Total Expenses 202 205 241 273 290 306 325 348

Revenue Share 16 17 21 25 25 37 39 42

Depreciation & Amortization

100 116 127 123 128 123 111 113

Taxes 2 0 0 11 2 61 74 87

Gross Target Revenue Requirement

554 585 636 705 714 793 814 852

Rs in Crs

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 65 of 136

65

Aggregate Revenue Requirement

Particulars: 2009 2010 2011 2012 2013 2014 2015 2016

Gross Target Revenue Requirement

554 585 636 705 714 793 814 852

Less: Non Aeronautical Revenues

121 161 207 263 269 253 273 293

Aggregate Revenue Requirement

433 423 429 443 445 540 542 559

Less : Actual Aeronautical Revenues

192 255 323 376 371

Less : Fuel farm Excess revenues

39 38 37 43 41 41 43 46

Net Aggregate Revenue Requirement

202 130 69 24 34 499 498 513

Sum of ARR 1969

Rs in Crs

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 66 of 136

66

Fuel Farm Filing

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 67 of 136

67

Fuel Farm Filing

Based on the requirements of guidelines, the fuel farm tariff proposal has been filed by us separately.

The excess amount collected considering the continuation of existing fuel charges over the eligibility has been considered towards subsidizing aeronautical charges.

In case there is a change in the tariff approved for fuel farm charges, GHIAL tariff filing shall be revised accordingly.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 68 of 136

68

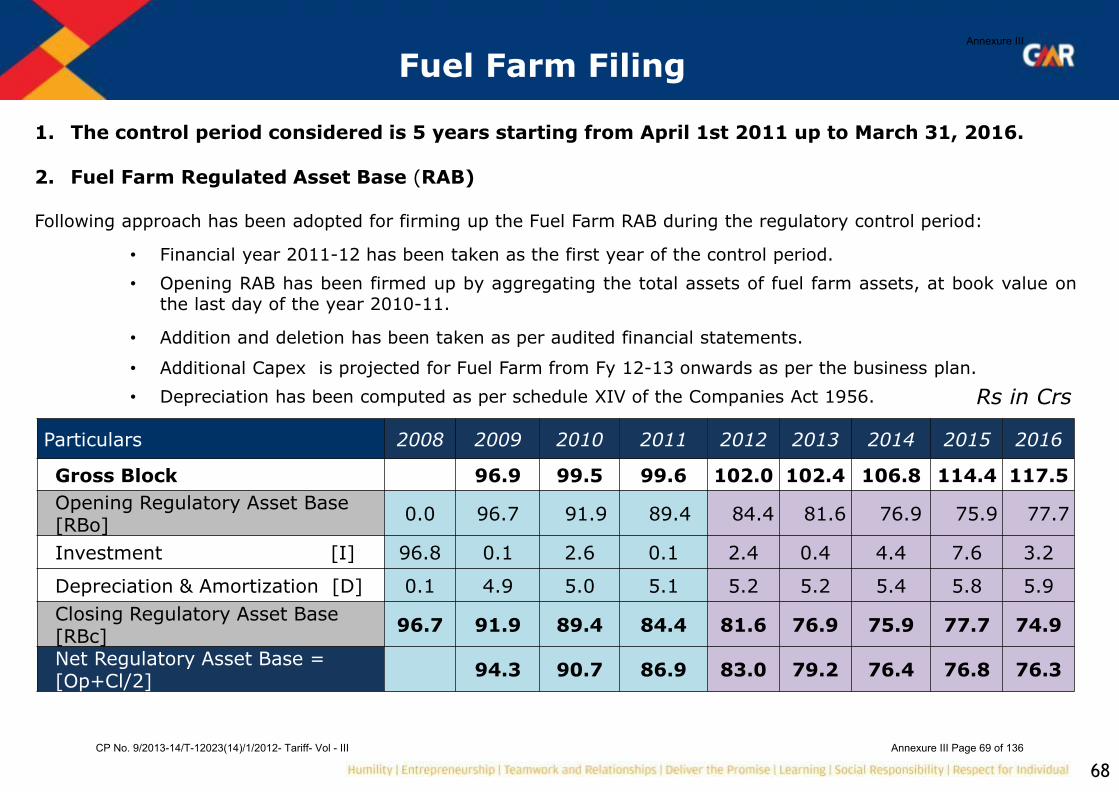

Fuel Farm Filing

1. The control period considered is 5 years starting from April 1st 2011 up to March 31, 2016.

2. Fuel Farm Regulated Asset Base (RAB) Following approach has been adopted for firming up the Fuel Farm RAB during the regulatory control period:

• Financial year 2011-12 has been taken as the first year of the control period.

• Opening RAB has been firmed up by aggregating the total assets of fuel farm assets, at book value on the last day of the year 2010-11.

• Addition and deletion has been taken as per audited financial statements.

• Additional Capex is projected for Fuel Farm from Fy 12-13 onwards as per the business plan.

• Depreciation has been computed as per schedule XIV of the Companies Act 1956.

Particulars 2008 2009 2010 2011 2012 2013 2014 2015 2016

Gross Block 96.9 99.5 99.6 102.0 102.4 106.8 114.4 117.5

Opening Regulatory Asset Base [RBo]

0.0 96.7 91.9 89.4 84.4 81.6 76.9 75.9 77.7

Investment [I] 96.8 0.1 2.6 0.1 2.4 0.4 4.4 7.6 3.2

Depreciation & Amortization [D] 0.1 4.9 5.0 5.1 5.2 5.2 5.4 5.8 5.9

Closing Regulatory Asset Base [RBc]

96.7 91.9 89.4 84.4 81.6 76.9 75.9 77.7 74.9

Net Regulatory Asset Base = [Op+Cl/2]

94.3 90.7 86.9 83.0 79.2 76.4 76.8 76.3

Rs in Crs

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 69 of 136

69

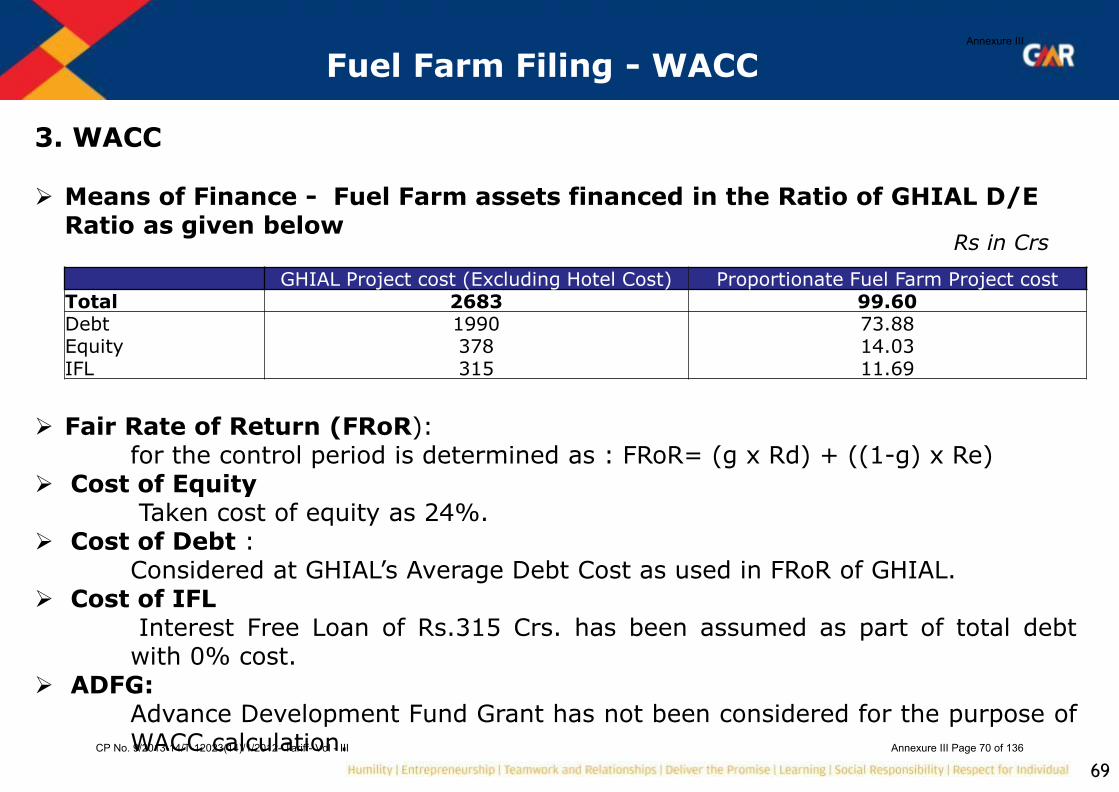

Fuel Farm Filing - WACC

3. WACC Means of Finance - Fuel Farm assets financed in the Ratio of GHIAL D/E

Ratio as given below Fair Rate of Return (FRoR): for the control period is determined as : FRoR= (g x Rd) + ((1-g) x Re) Cost of Equity Taken cost of equity as 24%. Cost of Debt : Considered at GHIAL‟s Average Debt Cost as used in FRoR of GHIAL. Cost of IFL Interest Free Loan of Rs.315 Crs. has been assumed as part of total debt with 0% cost. ADFG: Advance Development Fund Grant has not been considered for the purpose of WACC calculation.

GHIAL Project cost (Excluding Hotel Cost) Proportionate Fuel Farm Project cost Total 2683 99.60 Debt 1990 73.88 Equity 378 14.03 IFL 315 11.69

Rs in Crs

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 70 of 136

70

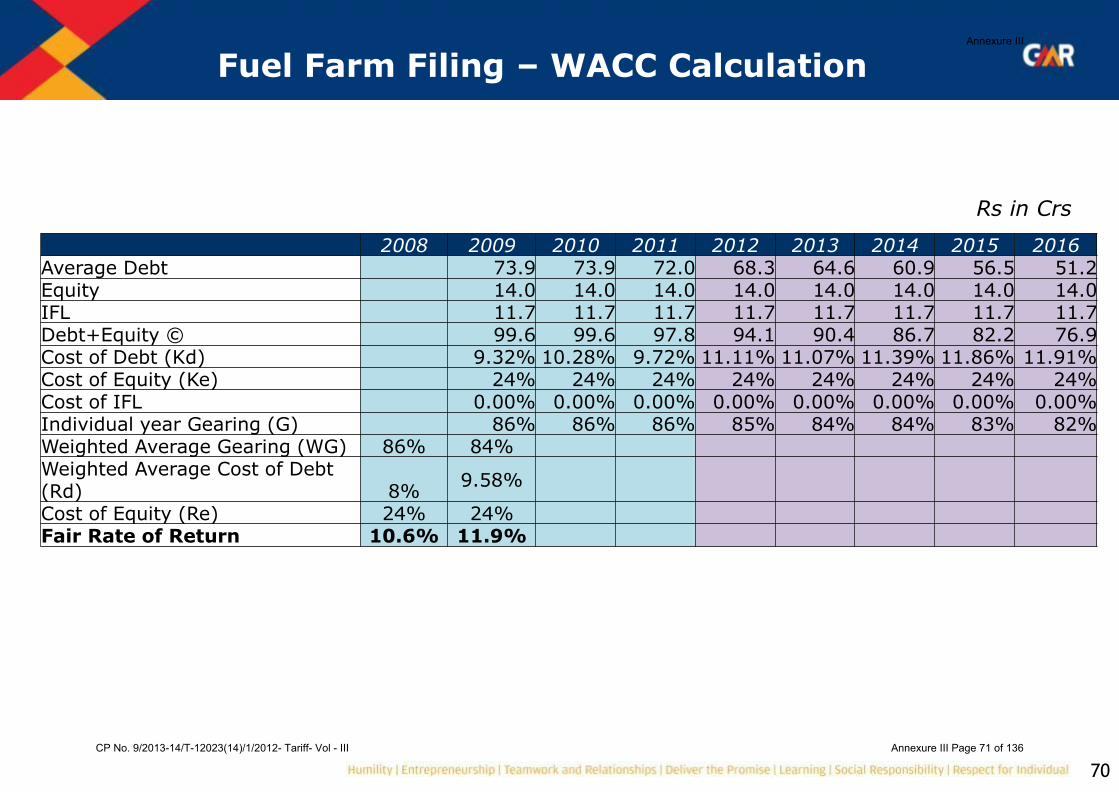

Fuel Farm Filing – WACC Calculation

2008 2009 2010 2011 2012 2013 2014 2015 2016 Average Debt 73.9 73.9 72.0 68.3 64.6 60.9 56.5 51.2 Equity 14.0 14.0 14.0 14.0 14.0 14.0 14.0 14.0 IFL 11.7 11.7 11.7 11.7 11.7 11.7 11.7 11.7 Debt+Equity © 99.6 99.6 97.8 94.1 90.4 86.7 82.2 76.9 Cost of Debt (Kd) 9.32% 10.28% 9.72% 11.11% 11.07% 11.39% 11.86% 11.91% Cost of Equity (Ke) 24% 24% 24% 24% 24% 24% 24% 24% Cost of IFL 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% Individual year Gearing (G) 86% 86% 86% 85% 84% 84% 83% 82% Weighted Average Gearing (WG) 86% 84% Weighted Average Cost of Debt (Rd) 8%

9.58%

Cost of Equity (Re) 24% 24% Fair Rate of Return 10.6% 11.9%

Rs in Crs

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 71 of 136

71

Fuel Farm Filing

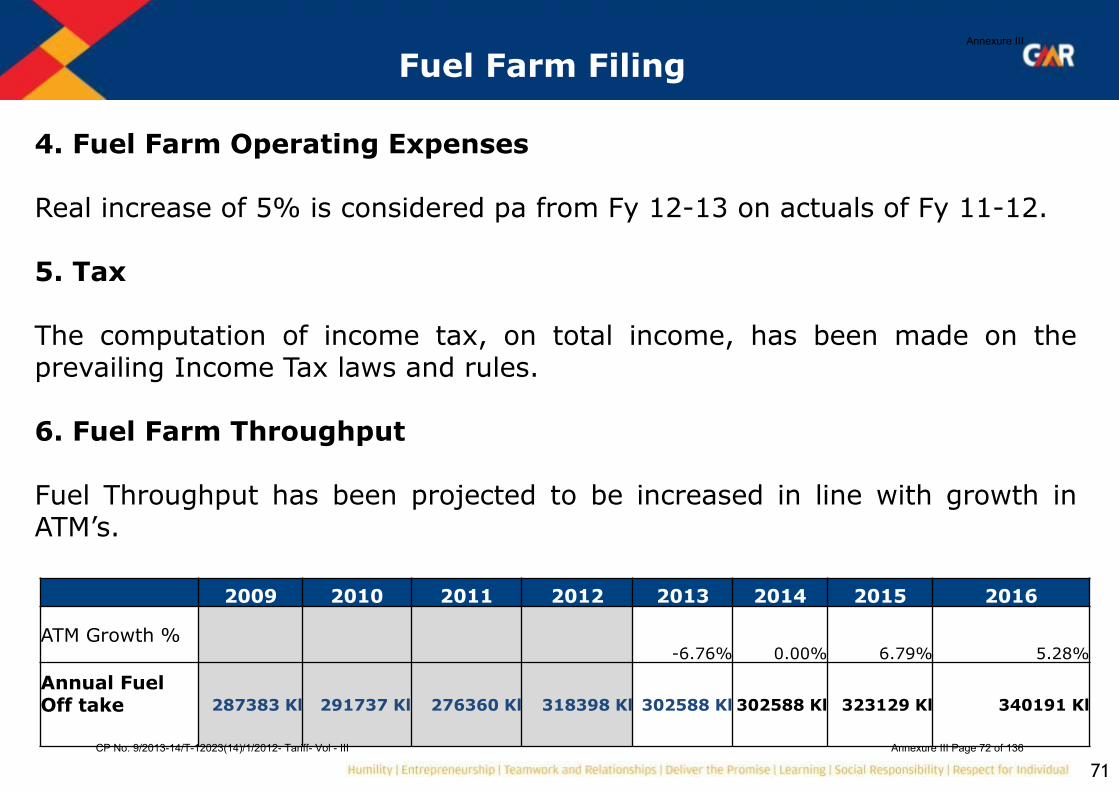

4. Fuel Farm Operating Expenses Real increase of 5% is considered pa from Fy 12-13 on actuals of Fy 11-12. 5. Tax The computation of income tax, on total income, has been made on the prevailing Income Tax laws and rules.

6. Fuel Farm Throughput Fuel Throughput has been projected to be increased in line with growth in ATM‟s.

2009 2010 2011 2012 2013 2014 2015 2016

ATM Growth % -6.76% 0.00% 6.79% 5.28%

Annual Fuel Off take

287383 Kl 291737 Kl 276360 Kl 318398 Kl 302588 Kl 302588 Kl 323129 Kl 340191 Kl

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 72 of 136

72

Fuel Farm Filing : Aggregate Revnue requirement

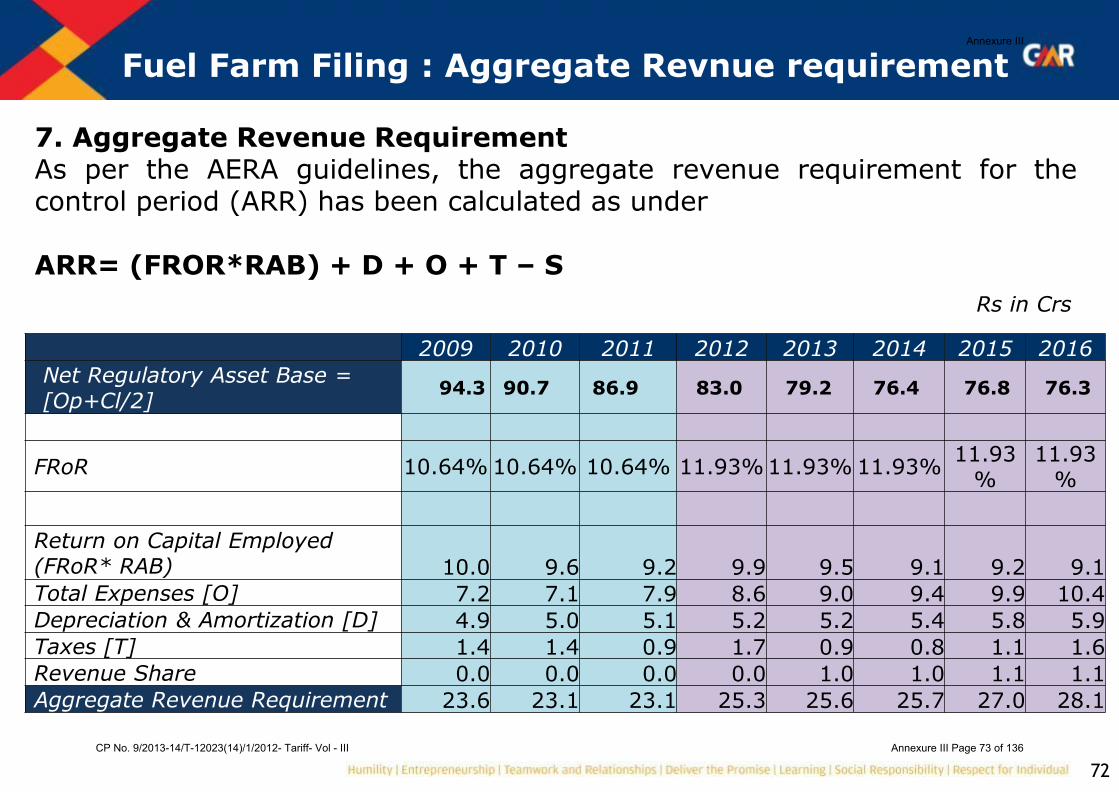

7. Aggregate Revenue Requirement As per the AERA guidelines, the aggregate revenue requirement for the control period (ARR) has been calculated as under ARR= (FROR*RAB) + D + O + T – S

2009 2010 2011 2012 2013 2014 2015 2016

Net Regulatory Asset Base = [Op+Cl/2]

94.3 90.7 86.9 83.0 79.2 76.4 76.8 76.3

FRoR 10.64% 10.64% 10.64% 11.93% 11.93% 11.93% 11.93

% 11.93

%

Return on Capital Employed (FRoR* RAB) 10.0 9.6 9.2 9.9 9.5 9.1 9.2 9.1

Total Expenses [O] 7.2 7.1 7.9 8.6 9.0 9.4 9.9 10.4

Depreciation & Amortization [D] 4.9 5.0 5.1 5.2 5.2 5.4 5.8 5.9

Taxes [T] 1.4 1.4 0.9 1.7 0.9 0.8 1.1 1.6

Revenue Share 0.0 0.0 0.0 0.0 1.0 1.0 1.1 1.1

Aggregate Revenue Requirement 23.6 23.1 23.1 25.3 25.6 25.7 27.0 28.1

Rs in Crs

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 73 of 136

73

Fuel Farm Filing

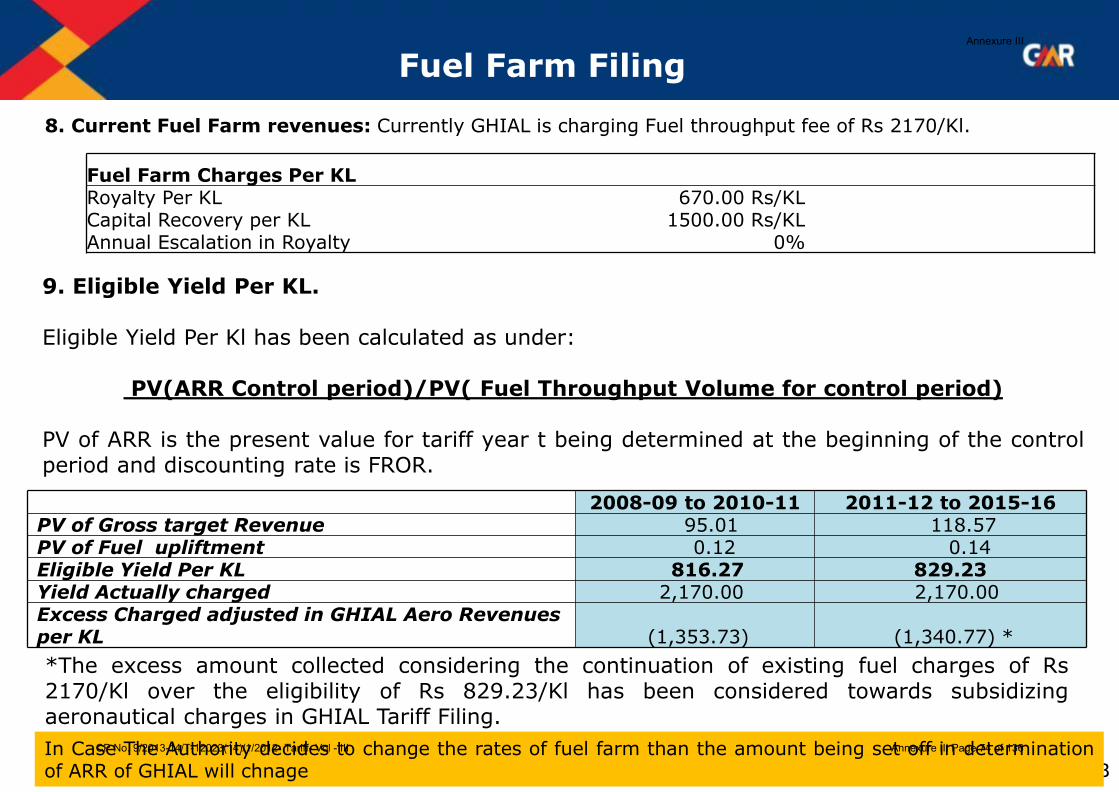

9. Eligible Yield Per KL. Eligible Yield Per Kl has been calculated as under:

PV(ARR Control period)/PV( Fuel Throughput Volume for control period)

PV of ARR is the present value for tariff year t being determined at the beginning of the control period and discounting rate is FROR. 2008-09 to 2010-11 2011-12 to 2015-16 PV of Gross target Revenue 95.01 118.57 PV of Fuel upliftment 0.12 0.14 Eligible Yield Per KL 816.27 829.23 Yield Actually charged 2,170.00 2,170.00 Excess Charged adjusted in GHIAL Aero Revenues per KL (1,353.73) (1,340.77) *

*The excess amount collected considering the continuation of existing fuel charges of Rs 2170/Kl over the eligibility of Rs 829.23/Kl has been considered towards subsidizing aeronautical charges in GHIAL Tariff Filing.

8. Current Fuel Farm revenues: Currently GHIAL is charging Fuel throughput fee of Rs 2170/Kl.

Fuel Farm Charges Per KL Royalty Per KL 670.00 Rs/KL Capital Recovery per KL 1500.00 Rs/KL Annual Escalation in Royalty 0%

In Case The Authority decides to change the rates of fuel farm than the amount being set off in determination of ARR of GHIAL will chnage

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 74 of 136

74

Disclaimer

‘Please note that filing is being made solely in view of the Hon’ble Airports Economic

Regulatory Authority Appellate Tribunal’s order dated May 11, 2011 in Appeal Nos.

8/2011 and 10/2011 and to ensure compliance with the same. The said filing is being

made without prejudice to the claims and contentions raised by GHIAL pursuant to

the said Appeal Nos. 8/2011 and 10/2011 and is further being made without prejudice

to the factum of the impugned Order No. 14/2010-11 and Direction No. 5/2010-11

being erroneous and ultra vires the Airports Economic Regulatory Authority Act, 2008.

The annexed/enclosed filing should not be construed as an admission on the part of

the GHIAL as to the validity or legality of the said Order No. 14/2010-11 or Direction

No. 5/2010-11. We would also draw your attention to the order of the Hon’ble

Appellate Tribunal dated May 11, 2011 wherein the Hon’ble Tribunal has directed

AERA to maintain strict confidentiality of The information/filing made by GHIAL and

accordingly call upon you to strictly comply with the orders of the Hon’ble Appellate

Tribunal as to confidentiality.’

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 75 of 136

75

THANK YOU

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 76 of 136

0

GMR HYDERABAD INTERNATIONAL AIRPORT LIMITED

PRESENTATION TO AERA

1ST APRIL 2013

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 77 of 136

1

OUR SUBMISSION AT THE TIME OF CONSULTATIONS

We had made various representations at the time of consultation process for

finalizing the regulatory philosophy of Major Airports in India. The major

observations in our submissions were as under:

Concession Agreement should be adhered.

Privatization and Single Till does not go hand in hand.

Dual Till should be allowed for Hyderabad;

Review of the consultation mechanism as suggest by the Authority.

Additional service quality parameter should not be mandated.

Cargo, Ground Handling and Fuel should be outside regulation.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 78 of 136

2

OUR SUBMISSION AT THE TIME OF CONSULTATIONS

• Airports having Single till do not necessarily have lower charges. In long run,

prices are determined by the characteristics of the airport, their ownership

structure and the way it is managed rather than the charging methodology.

• World over, in the matured regulatory regimes, airports are moving towards

dual or hybrid till to encourage better infrastructure and maintain efficient

level of service.

• In general airports under Dual/hybrid till have better quality rating than

airports under single till.

• There is a very important correlation between privatization and Dual/Hybrid

till. There is no major airport privatization under single till (except BAA which

was kept under Single till due to extraneous reasons).

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 79 of 136

3

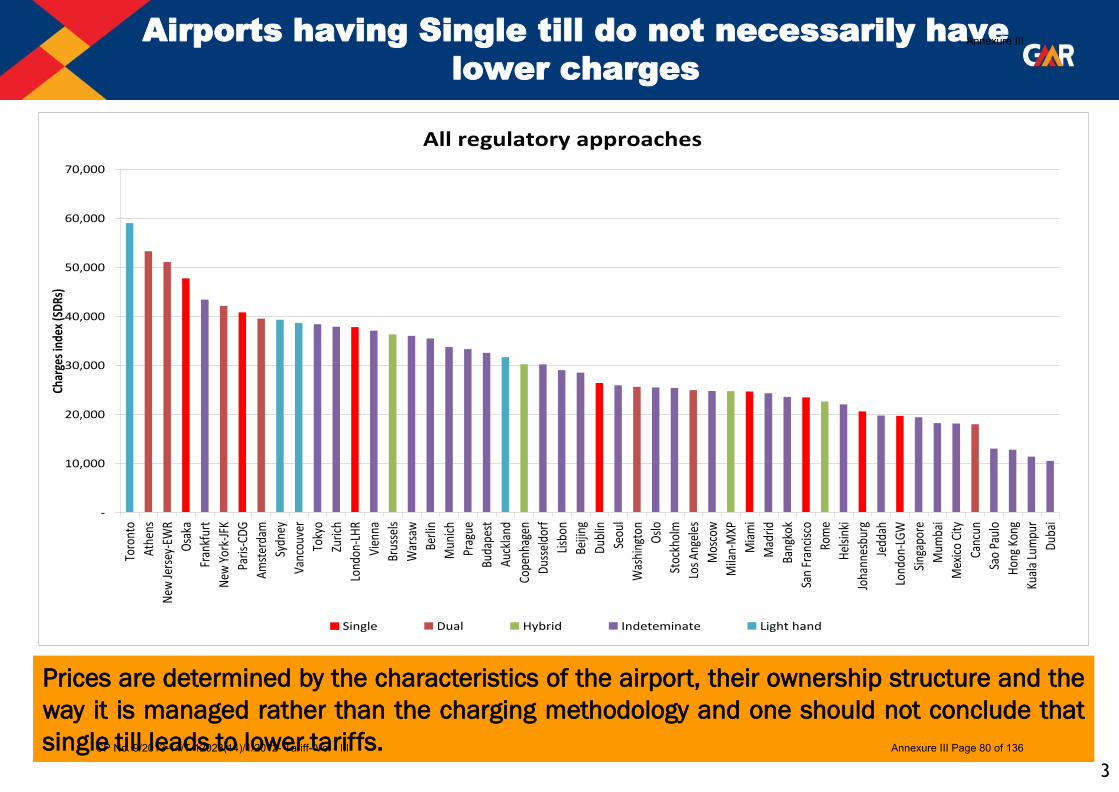

Airports having Single till do not necessarily have

lower charges

All regulatory approaches

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Toro

nto

Athe

ns

New

Jers

ey-E

WR

Osa

ka

Fran

kfur

t

New

Yor

k-JF

K

Paris

-CD

G

Amst

erda

m

Sydn

ey

Vanc

ouve

r

Toky

o

Zuric

h

Lond

on-L

HR

Vien

na

Brus

sels

War

saw

Berli

n

Mun

ich

Prag

ue

Buda

pest

Auck

land

Cope

nhag

en

Dus

seld

orf

Lisb

on

Beiji

ng

Dub

lin

Seou

l

Was

hing

ton

Osl

o

Stoc

khol

m

Los

Ange

les

Mos

cow

Mila

n-M

XP

Mia

mi

Mad

rid

Bang

kok

San

Fran

cisc

o

Rom

e

Hel

sink

i

Joha

nnes

burg

Jedd

ah

Lond

on-L

GW

Sing

apor

e

Mum

bai

Mex

ico

City

Canc

un

Sao

Paul

o

Hon

g Ko

ng

Kual

a Lu

mpu

r

Dub

ai

Char

ges

inde

x (S

DRs

)

Single Dual Hybrid Indeteminate Light hand

Prices are determined by the characteristics of the airport, their ownership structure and the

way it is managed rather than the charging methodology and one should not conclude that

single till leads to lower tariffs.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 80 of 136

4

Airports and their quality standards

Ranked quality

-

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

Seou

l

Sing

apor

e

Hon

g Ko

ng

Bei

jing

Canc

un

Toky

o

Ban

gkok

Kual

a Lu

mpu

r

Van

couv

er

Mex

ico

City

Zuri

ch

Auc

klan

d

Mun

ich

Mum

bai

Cope

nhag

en

Toro

nto

Joha

nnes

burg

Stoc

khol

m

Ath

ens

Dub

ai

Am

ster

dam

Osl

o

Hel

sink

i

Mos

cow

Lond

on-L

HR

Lond

on-L

GW

Sydn

ey

Mad

rid

Vie

nna

Dub

lin

Rom

e

Bud

apes

t

Fran

kfur

t

Pari

s-CD

G

Lisb

on

Mila

n-M

XP

ASQ

sco

re f

or

ove

rall

sati

sfac

tio

n

Single Dual Hybrid Indeterminate Light hand

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 81 of 136

5

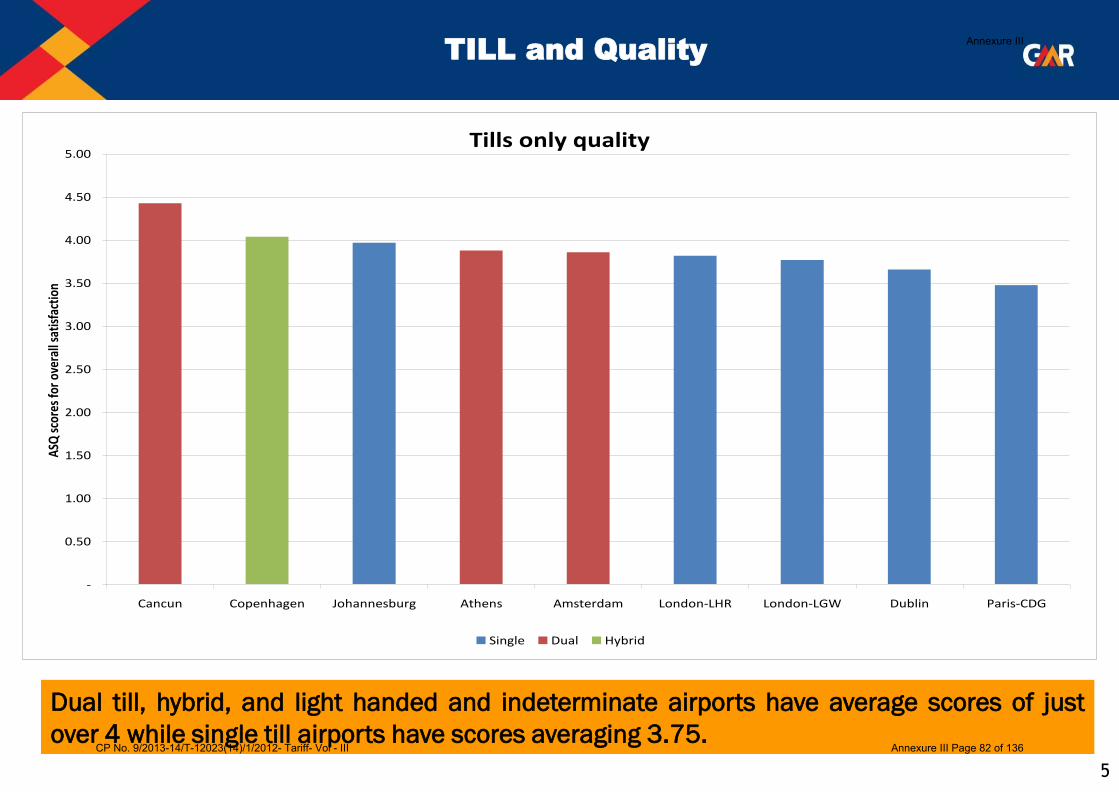

TILL and Quality

Tills only quality

-

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

Cancun Copenhagen Johannesburg Athens Amsterdam London-LHR London-LGW Dublin Paris-CDG

ASQ

sco

res

for o

vera

ll sa

tisfa

ctio

n

Single Dual Hybrid

Dual till, hybrid, and light handed and indeterminate airports have average scores of just

over 4 while single till airports have scores averaging 3.75.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 82 of 136

6

No major airport privatised on a single till basis

Country AirportMajority Private

Ownership

Till at

PrivatisationTill now

Belgium Brussels Yes Dual till gradually Dual till gradually

Denmark Copenhagen Yes No till Hybrid

Hungary Budapest Ferihegy Yes No till No till

Italy Rome Yes No till Hybid

Naples Yes No till Hybid

Venice Yes No till Hybid

Malta Malta International Yes Dual till Dual till

Slovak Republic Bratislava Yes N/a

Australia Melbourne Yes No till/dual till? Unregulated/dual

Perth Yes No till/dual till? Unregulated/dual

Brisbane Yes No till/dual till? Unregulated/dual

Adelaide Yes No till/dual till? Unregulated/dual

Sydney Yes Unregulated/dual Unregulated/dual

New Zealand Auckland Yes Unregulated/dual Unregulated/dual

Wellington Yes Unregulated/dual Unregulated/dual

Mexico Cancun Yes Dual till Dual till

Guadalejara Yes Dual till Dual till

Monterrey Yes Dual till Dual till

Mexico City Yes No till/dual till? No till/dual till?

List of privatised airports and their till (Except UK Airports-BAA)

No privatization under single Till Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 83 of 136

7

TREATMENT OF LAND

• The treatment of land as envisaged in the Authority‟s Order No.

13/2010-11 was not subject to any consultation.

• Our current submission in this regard may kindly be

considered.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 84 of 136

8

Request

Its earnestly requested that our earlier submissions made at

time of consultation and also the submissions made in our

appeal are relooked and reconsidered in the review of

philosophy applicable to GHIAL.

Since, the treatment on land was not laid down in the

Consultation Paper, our views in this regard may kindly be

considered.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 85 of 136

9

AERA’s Position vide its Order No. 13/2010-11 dtd 12th January 2011.

The Authority opined that "Single Till is most appropriate for the economic

regulation of Major Airports in India".

The Authority opined the general framework for economic regulation of

aeronautical services i.e. Single Till regulation is consistent with the ICAO

policies. Therefore, the framework being laid down here would also be

applicable to Bengaluru and Hyderabad airports.

New Land Ring fencing principle and New Service Quality regulations

have been advocated (which were not mandated under the Concession

Agreements).

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 86 of 136

10

AERAAT Order dtd February 15th 2013

GHIAL appealed against the Orders of the Authority which enshrined the

Single Till philosophy in the AERAAT. AERAAT had recently disposed off the

appeal with directions as under;

AERAAT Judgment extract

8. In that view, we would dispose off these appeals with the direction to the AERA to

complete this exercise of determination of tariff and while doing so, the AERA would give

opportunities to all the stakeholders to raise all the plea and contentions and consider

the same. The impugned orders herein would not come in the way of that exercise. We

would, however, request AERA to complete the determination exercise as expeditiously as

possible. We have taken this view as we are of the firm opinion that it would not be proper

to entertain the appeals on different stages of determination of tariff and to give the

finality to the questions of final determination of tariff.

In view of above judgment its 'earnestly requested that the philosophy of

economic regulation applicable to GHIAL is reconsidered by the Authority

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 87 of 136

11

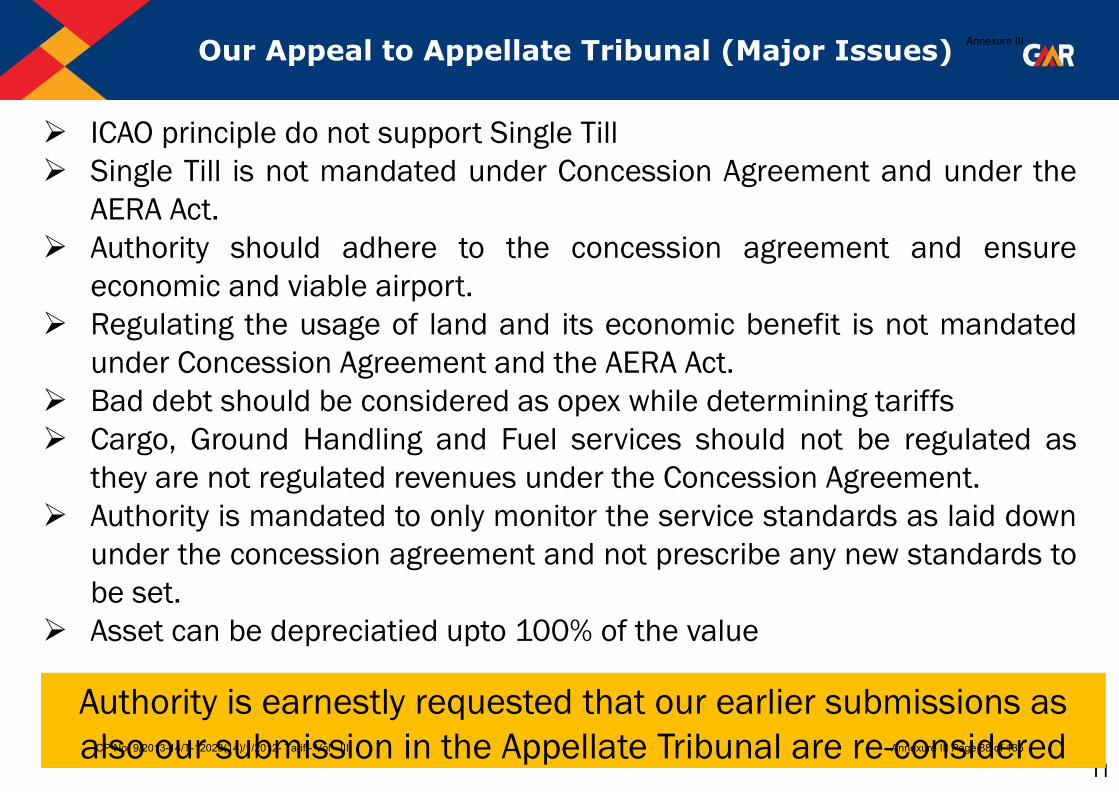

Our Appeal to Appellate Tribunal (Major Issues)

ICAO principle do not support Single Till

Single Till is not mandated under Concession Agreement and under the

AERA Act.

Authority should adhere to the concession agreement and ensure

economic and viable airport.

Regulating the usage of land and its economic benefit is not mandated

under Concession Agreement and the AERA Act.

Bad debt should be considered as opex while determining tariffs

Cargo, Ground Handling and Fuel services should not be regulated as

they are not regulated revenues under the Concession Agreement.

Authority is mandated to only monitor the service standards as laid down

under the concession agreement and not prescribe any new standards to

be set.

Asset can be depreciatied upto 100% of the value

Authority is earnestly requested that our earlier submissions as

also our submission in the Appellate Tribunal are re-considered

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 88 of 136

12

Our Submission

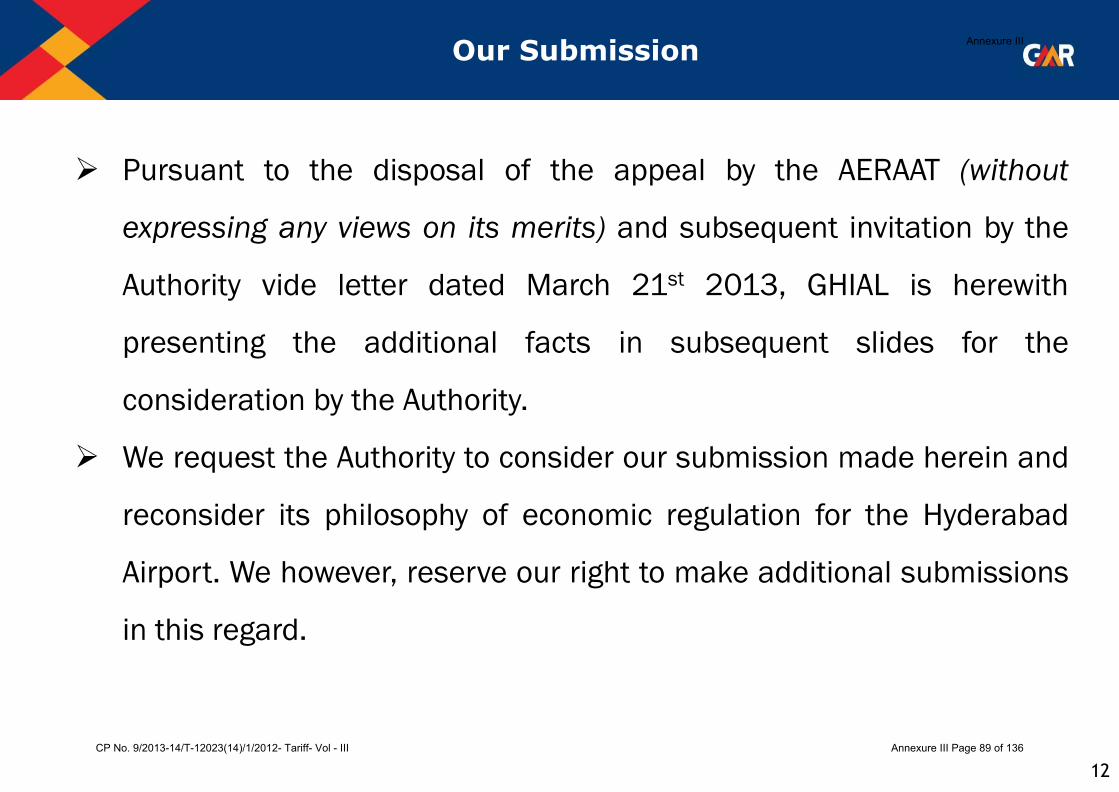

Pursuant to the disposal of the appeal by the AERAAT (without

expressing any views on its merits) and subsequent invitation by the

Authority vide letter dated March 21st 2013, GHIAL is herewith

presenting the additional facts in subsequent slides for the

consideration by the Authority.

We request the Authority to consider our submission made herein and

reconsider its philosophy of economic regulation for the Hyderabad

Airport. We however, reserve our right to make additional submissions

in this regard.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 89 of 136

13

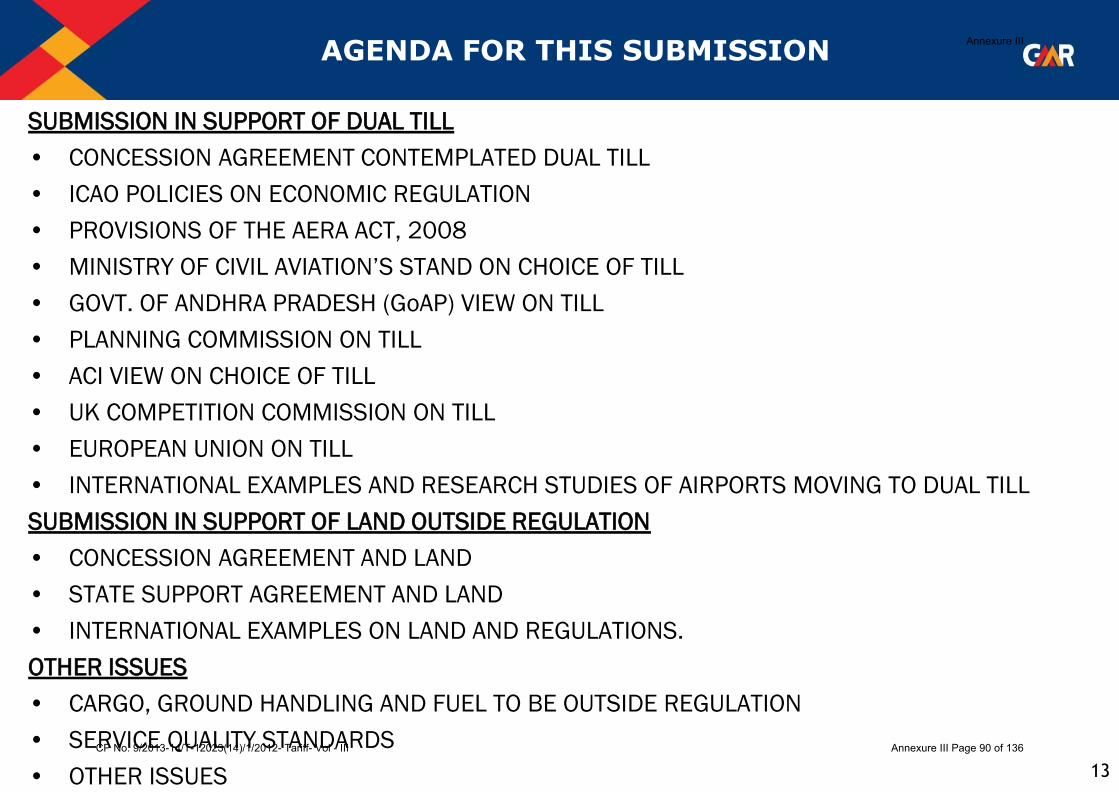

AGENDA FOR THIS SUBMISSION

SUBMISSION IN SUPPORT OF DUAL TILL

• CONCESSION AGREEMENT CONTEMPLATED DUAL TILL

• ICAO POLICIES ON ECONOMIC REGULATION

• PROVISIONS OF THE AERA ACT, 2008

• MINISTRY OF CIVIL AVIATION‟S STAND ON CHOICE OF TILL

• GOVT. OF ANDHRA PRADESH (GoAP) VIEW ON TILL

• PLANNING COMMISSION ON TILL

• ACI VIEW ON CHOICE OF TILL

• UK COMPETITION COMMISSION ON TILL

• EUROPEAN UNION ON TILL

• INTERNATIONAL EXAMPLES AND RESEARCH STUDIES OF AIRPORTS MOVING TO DUAL TILL

SUBMISSION IN SUPPORT OF LAND OUTSIDE REGULATION

• CONCESSION AGREEMENT AND LAND

• STATE SUPPORT AGREEMENT AND LAND

• INTERNATIONAL EXAMPLES ON LAND AND REGULATIONS.

OTHER ISSUES

• CARGO, GROUND HANDLING AND FUEL TO BE OUTSIDE REGULATION

• SERVICE QUALITY STANDARDS

• OTHER ISSUES

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 90 of 136

14

SUBMISSION IN SUPPORT OF DUAL TILL

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 91 of 136

15

Regulated Charges are to be in accordance with ICAO policies

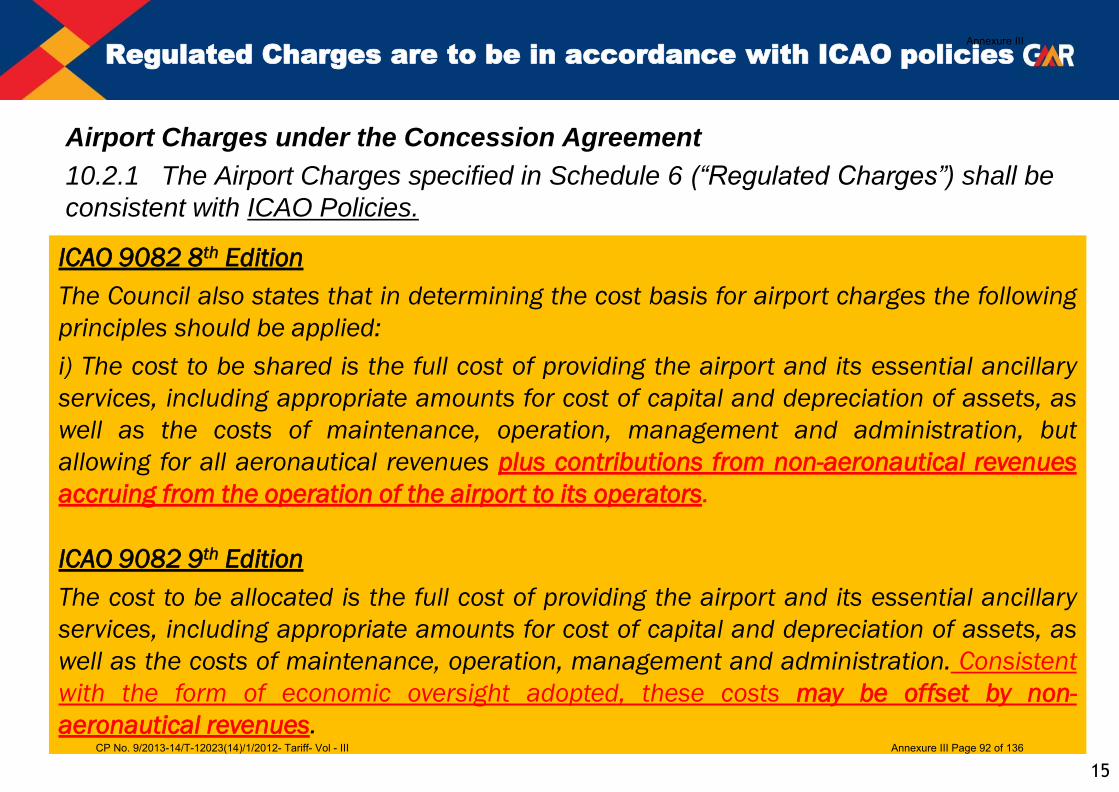

Airport Charges under the Concession Agreement

10.2.1 The Airport Charges specified in Schedule 6 (“Regulated Charges”) shall be

consistent with ICAO Policies.

ICAO 9082 8th Edition

The Council also states that in determining the cost basis for airport charges the following

principles should be applied:

i) The cost to be shared is the full cost of providing the airport and its essential ancillary

services, including appropriate amounts for cost of capital and depreciation of assets, as

well as the costs of maintenance, operation, management and administration, but

allowing for all aeronautical revenues plus contributions from non-aeronautical revenues

accruing from the operation of the airport to its operators.

ICAO 9082 9th Edition

The cost to be allocated is the full cost of providing the airport and its essential ancillary

services, including appropriate amounts for cost of capital and depreciation of assets, as

well as the costs of maintenance, operation, management and administration. Consistent

with the form of economic oversight adopted, these costs may be offset by non-

aeronautical revenues.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 92 of 136

16

ICAO current position on till

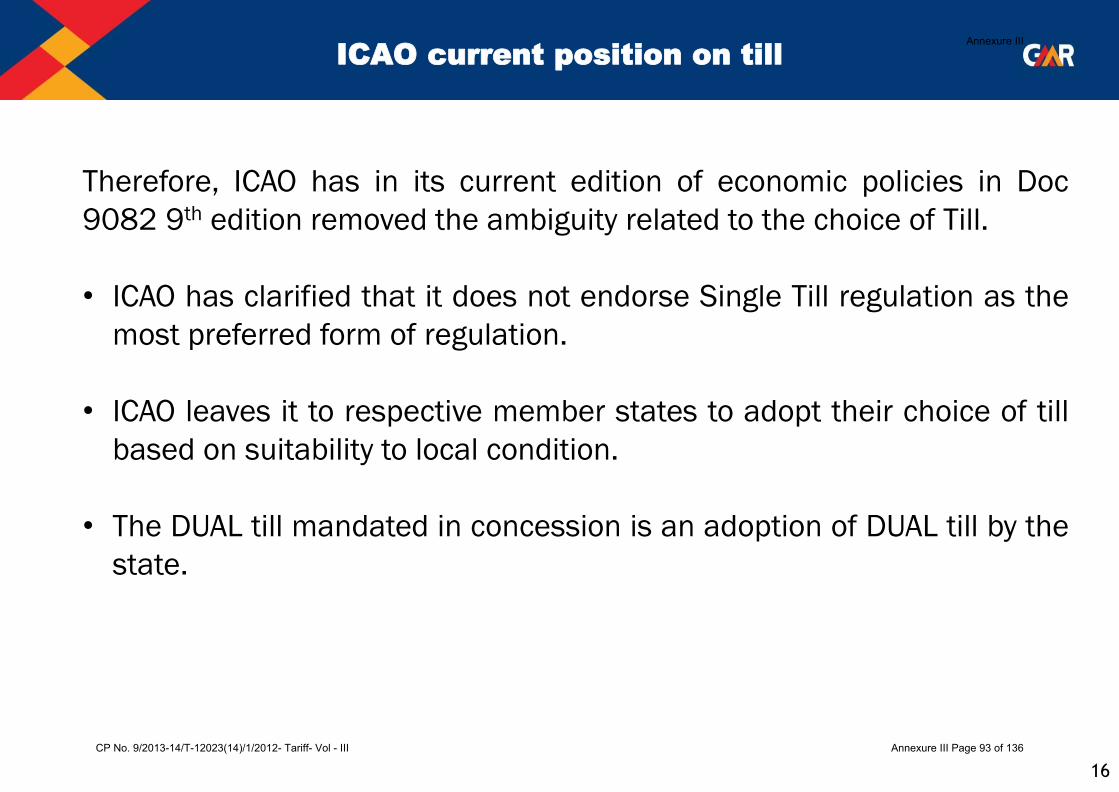

Therefore, ICAO has in its current edition of economic policies in Doc

9082 9th edition removed the ambiguity related to the choice of Till.

• ICAO has clarified that it does not endorse Single Till regulation as the

most preferred form of regulation.

• ICAO leaves it to respective member states to adopt their choice of till

based on suitability to local condition.

• The DUAL till mandated in concession is an adoption of DUAL till by the

state.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 93 of 136

17

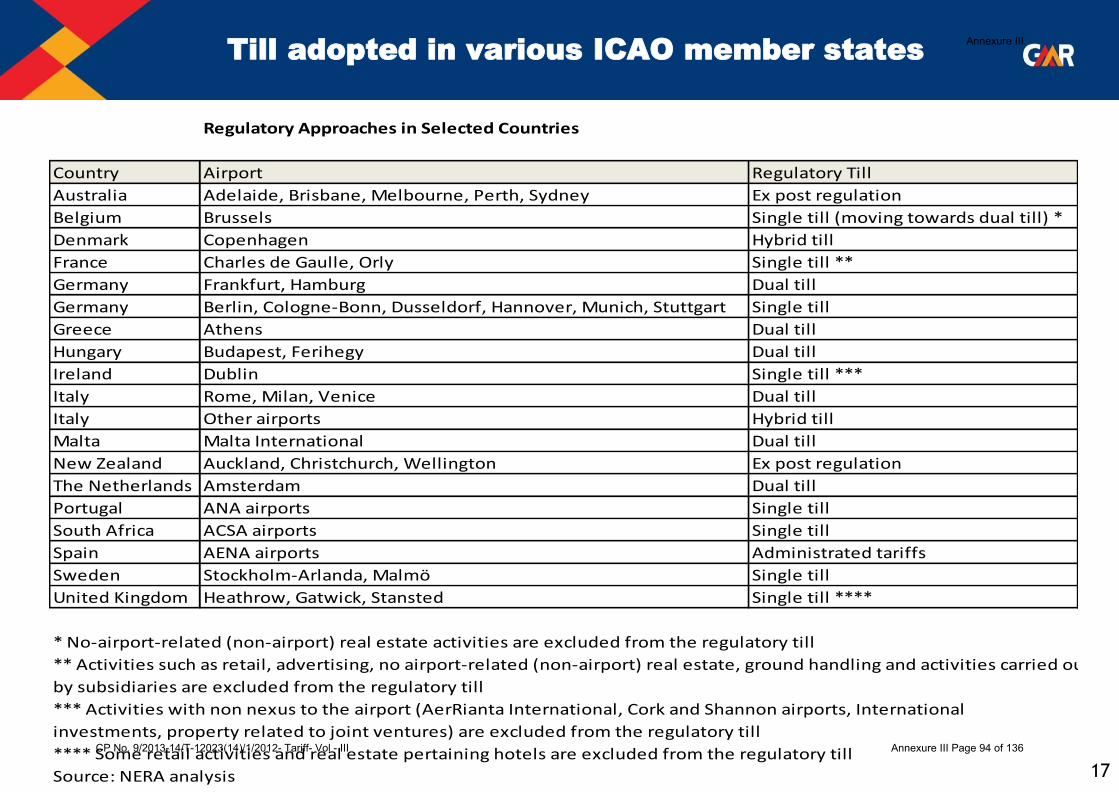

Till adopted in various ICAO member states

Regulatory Approaches in Selected Countries

Country Airport Regulatory Till

Australia Adelaide, Brisbane, Melbourne, Perth, Sydney Ex post regulation

Belgium Brussels Single till (moving towards dual till) *

Denmark Copenhagen Hybrid till

France Charles de Gaulle, Orly Single till **

Germany Frankfurt, Hamburg Dual till

Germany Berlin, Cologne-Bonn, Dusseldorf, Hannover, Munich, Stuttgart Single till

Greece Athens Dual till

Hungary Budapest, Ferihegy Dual till

Ireland Dublin Single till ***

Italy Rome, Milan, Venice Dual till

Italy Other airports Hybrid till

Malta Malta International Dual till

New Zealand Auckland, Christchurch, Wellington Ex post regulation

The Netherlands Amsterdam Dual till

Portugal ANA airports Single till

South Africa ACSA airports Single till

Spain AENA airports Administrated tariffs

Sweden Stockholm-Arlanda, Malmö Single till

United Kingdom Heathrow, Gatwick, Stansted Single till ****

* No-airport-related (non-airport) real estate activities are excluded from the regulatory till

** Activities such as retail, advertising, no airport-related (non-airport) real estate, ground handling and activities carried out

by subsidiaries are excluded from the regulatory till

*** Activities with non nexus to the airport (AerRianta International, Cork and Shannon airports, International

investments, property related to joint ventures) are excluded from the regulatory till

**** Some retail activities and real estate pertaining hotels are excluded from the regulatory till

Source: NERA analysis

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 94 of 136

18

An overview of regulatory approaches implemented in selected

countries gives evidence that the regulatory approaches that enforce

ICAO principles may comprise Light handed (ex post regulation) as well

as Heavy handed (ex ante regulation).

In this latter case, the scope of the regulatory till may include

contributions of all or some non-aeronautical activities performed by

airport (single till approach), or may include only a percentage of

contributions of non- aeronautical activities (hybrid till and dual till

approach).

As such it is evident that majority of contracting states of ICAO

have followed dual till with only a handful of airports following

single till.

It is requested that AERA may review its conclusion that ICAO

recommends single till.

ICAO Position on till-Conclusion Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 95 of 136

19

Regulation of Regulated Charges

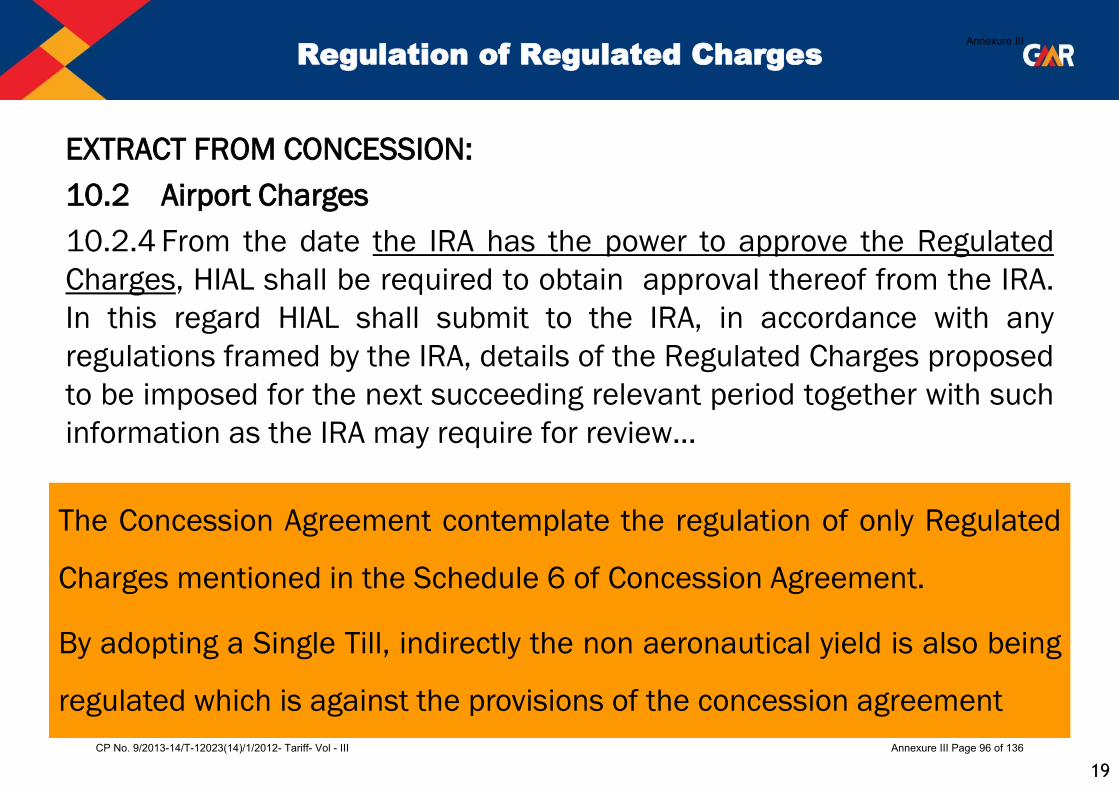

EXTRACT FROM CONCESSION:

10.2 Airport Charges

10.2.4 From the date the IRA has the power to approve the Regulated

Charges, HIAL shall be required to obtain approval thereof from the IRA.

In this regard HIAL shall submit to the IRA, in accordance with any

regulations framed by the IRA, details of the Regulated Charges proposed

to be imposed for the next succeeding relevant period together with such

information as the IRA may require for review…

The Concession Agreement contemplate the regulation of only Regulated

Charges mentioned in the Schedule 6 of Concession Agreement.

By adopting a Single Till, indirectly the non aeronautical yield is also being

regulated which is against the provisions of the concession agreement

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 96 of 136

20

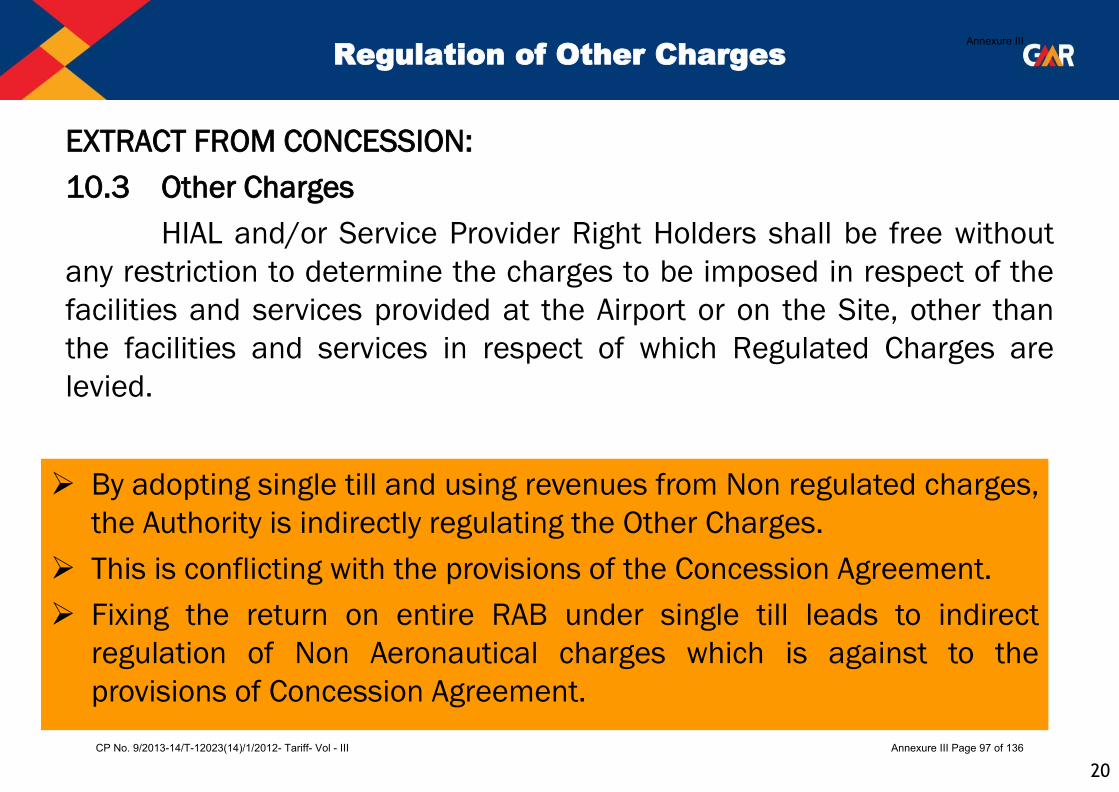

Regulation of Other Charges

EXTRACT FROM CONCESSION:

10.3 Other Charges

HIAL and/or Service Provider Right Holders shall be free without

any restriction to determine the charges to be imposed in respect of the

facilities and services provided at the Airport or on the Site, other than

the facilities and services in respect of which Regulated Charges are

levied.

By adopting single till and using revenues from Non regulated charges,

the Authority is indirectly regulating the Other Charges.

This is conflicting with the provisions of the Concession Agreement.

Fixing the return on entire RAB under single till leads to indirect

regulation of Non Aeronautical charges which is against to the

provisions of Concession Agreement.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 97 of 136

21

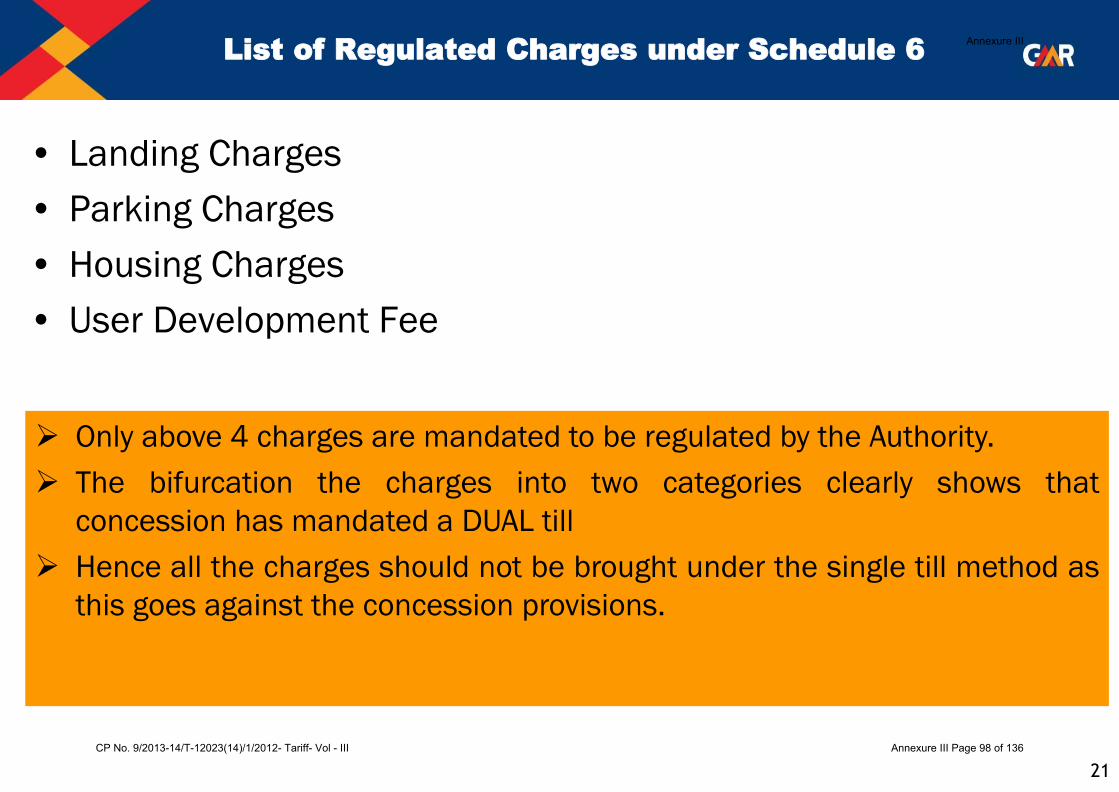

List of Regulated Charges under Schedule 6

• Landing Charges

• Parking Charges

• Housing Charges

• User Development Fee

Only above 4 charges are mandated to be regulated by the Authority.

The bifurcation the charges into two categories clearly shows that

concession has mandated a DUAL till

Hence all the charges should not be brought under the single till method as

this goes against the concession provisions.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 98 of 136

22

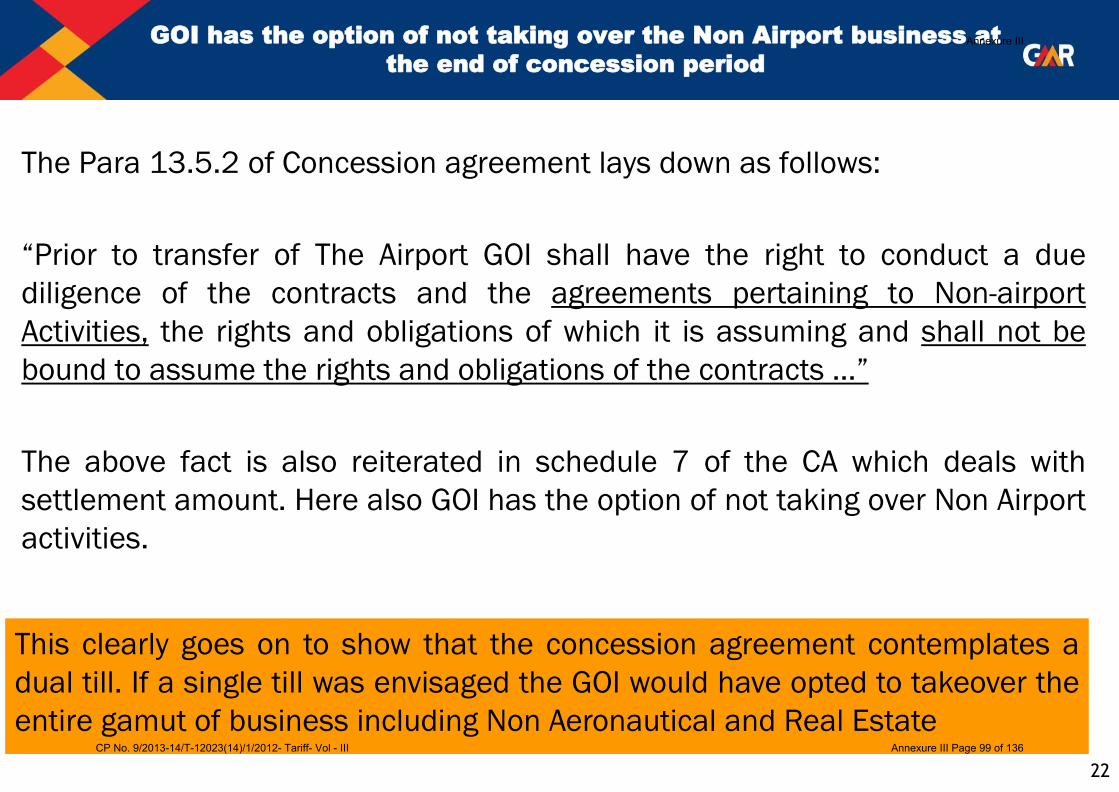

GOI has the option of not taking over the Non Airport business at

the end of concession period

The Para 13.5.2 of Concession agreement lays down as follows:

“Prior to transfer of The Airport GOI shall have the right to conduct a due

diligence of the contracts and the agreements pertaining to Non-airport

Activities, the rights and obligations of which it is assuming and shall not be

bound to assume the rights and obligations of the contracts ...”

The above fact is also reiterated in schedule 7 of the CA which deals with

settlement amount. Here also GOI has the option of not taking over Non Airport

activities.

This clearly goes on to show that the concession agreement contemplates a

dual till. If a single till was envisaged the GOI would have opted to takeover the

entire gamut of business including Non Aeronautical and Real Estate

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 99 of 136

23

CONCESSION ENVISAGES GHIAL TO OPERATE AS A

COMMERCIAL UNDERTAKING

Clause 8.9 of Concession Agreement states that

“HIAL shall...manage and operate the Airport in a competitive, efficient and

economic manner as a commercial undertaking”

AERA‟s Single Till approach may not be in sync with the above clause as

• Under Single Till, the “Total Return‟ , considering Aeronautical and Non

Aeronautical revenues together, is capped.

• Single Till scenario leaves no incentive for the operator to maximize its non-

aeronautical revenue since any increase in the non-aeronautical income will

be offset by an equivalent reduction in the aeronautical tariffs

• Providing aeronautical services at artificially lower tariffs provides a

distorted economic picture. Charges to passengers should be reflective of

actual cost

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 100 of 136

24

Request

The concession agreement clearly lays down regulation of

Regulated Charges as given in schedule 6.

Adopting of Single Till goes against the provisions of

concession agreement (as indirectly we are restricting the

return on Non Aero and Real Estate activities) which are

against the prudent commercial principles.

As such it is earnestly requested that Dual till may kindly be

approved for GHIAL

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 101 of 136

25

PROVISIONS OF THE AERA ACT, 2008

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 102 of 136

26

AERA Act was enacted in 2008, pursuant to which the Airports

Economic Regulatory Authority was established. The preamble of

the AERA Act, is as follows:

“An Act to provide for the establishment of an Airports Economic

Regulatory Authority to regulate tariff and other charges for the

aeronautical services rendered at airports and to monitor performance

standards of airports and also to establish Appellate Tribunal to

adjudicate disputes and dispose of appeals and for matter connected

therewith or incidental thereto.”

PROVISIONS OF THE AERA ACT, 2008

As such it is contemplated that Aeronautical Charges will be

regulated and the performance standards will be monitored

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 103 of 136

27

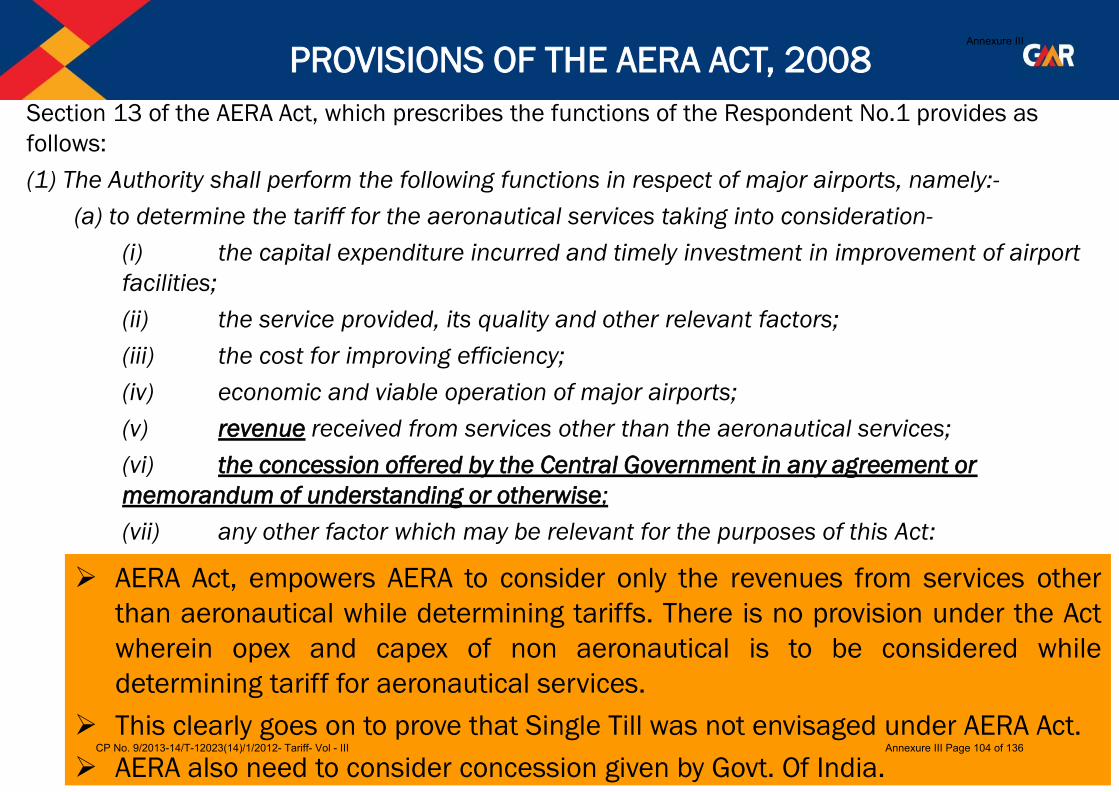

Section 13 of the AERA Act, which prescribes the functions of the Respondent No.1 provides as

follows:

(1) The Authority shall perform the following functions in respect of major airports, namely:-

(a) to determine the tariff for the aeronautical services taking into consideration-

(i) the capital expenditure incurred and timely investment in improvement of airport

facilities;

(ii) the service provided, its quality and other relevant factors;

(iii) the cost for improving efficiency;

(iv) economic and viable operation of major airports;

(v) revenue received from services other than the aeronautical services;

(vi) the concession offered by the Central Government in any agreement or

memorandum of understanding or otherwise;

(vii) any other factor which may be relevant for the purposes of this Act:

AERA Act, empowers AERA to consider only the revenues from services other

than aeronautical while determining tariffs. There is no provision under the Act

wherein opex and capex of non aeronautical is to be considered while

determining tariff for aeronautical services.

This clearly goes on to prove that Single Till was not envisaged under AERA Act.

AERA also need to consider concession given by Govt. Of India.

PROVISIONS OF THE AERA ACT, 2008 Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 104 of 136

28

STAND ON CHOICE OF TILL OF MINISTRY OF CIVIL AVIATION

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 105 of 136

29

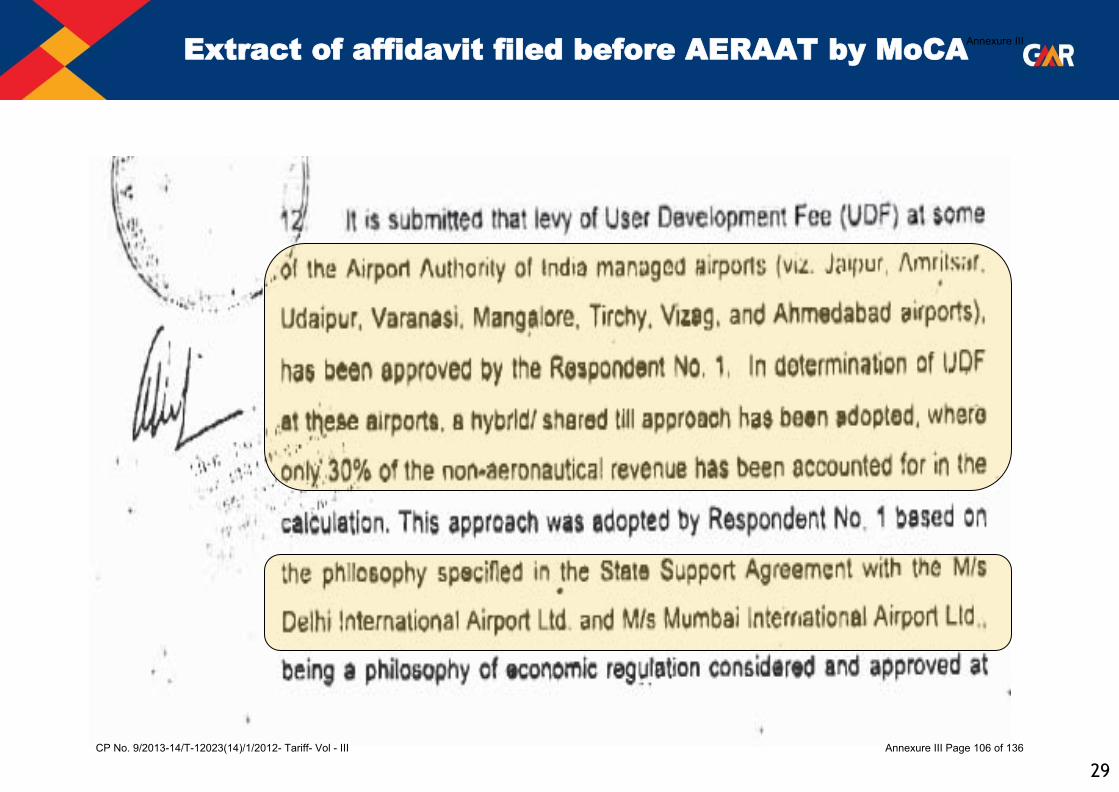

Extract of affidavit filed before AERAAT by MoCA Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 106 of 136

30

MoCA Affidavit before AERAAT

MoCA in its affidavit has categorically laid down a hybrid/shared till (30% of

Non Aero revenues considered for cross subsidy) based regime for levying User

Development Fee at;

• Jaipur

• Amritsar

• Udaipur

• Varanasi

• Mangalore

• Trichy and

• Ahmedabad

Further, hybrid/shared till philosophy has been adopted in the case of Delhi

and Mumbai.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 107 of 136

31

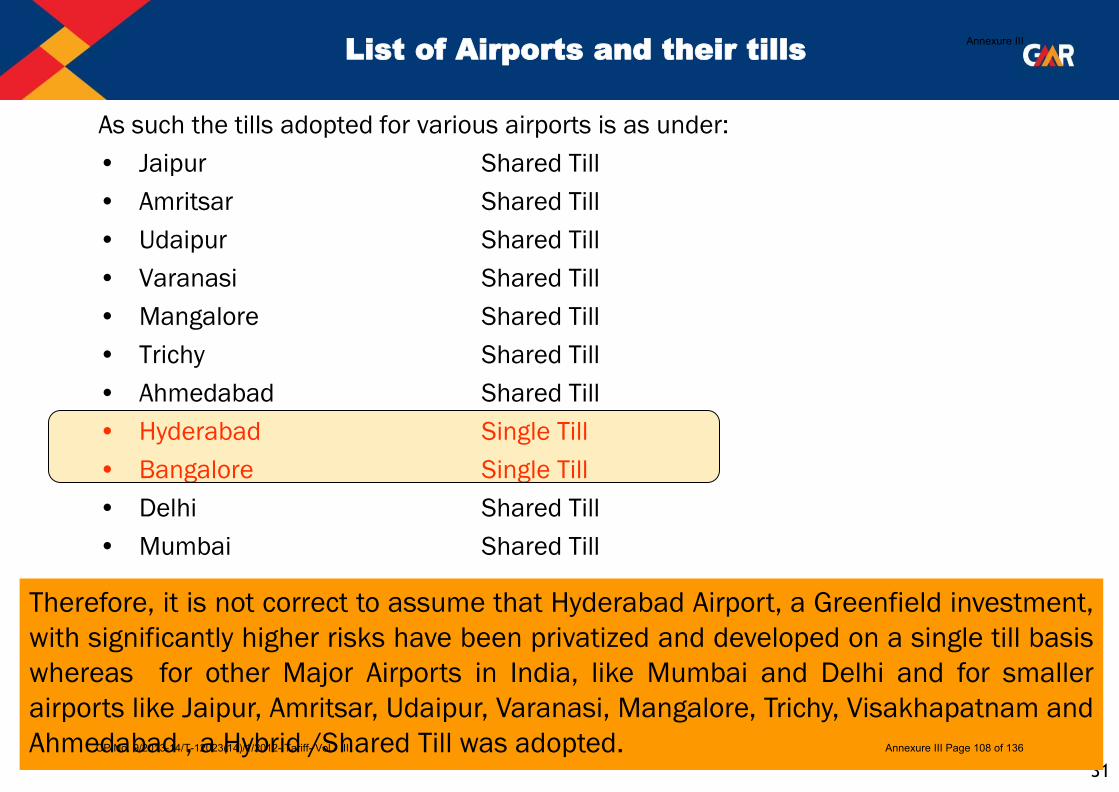

List of Airports and their tills

As such the tills adopted for various airports is as under:

• Jaipur Shared Till

• Amritsar Shared Till

• Udaipur Shared Till

• Varanasi Shared Till

• Mangalore Shared Till

• Trichy Shared Till

• Ahmedabad Shared Till

• Hyderabad Single Till

• Bangalore Single Till

• Delhi Shared Till

• Mumbai Shared Till

Therefore, it is not correct to assume that Hyderabad Airport, a Greenfield investment,

with significantly higher risks have been privatized and developed on a single till basis

whereas for other Major Airports in India, like Mumbai and Delhi and for smaller

airports like Jaipur, Amritsar, Udaipur, Varanasi, Mangalore, Trichy, Visakhapatnam and

Ahmedabad , a Hybrid /Shared Till was adopted.

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 108 of 136

32

GOVT. OF ANDHRA PRADESH VIEW ON TILL

Annexure III

CP No. 9/2013-14/T-12023(14)/1/2012- Tariff- Vol - III Annexure III Page 109 of 136

33

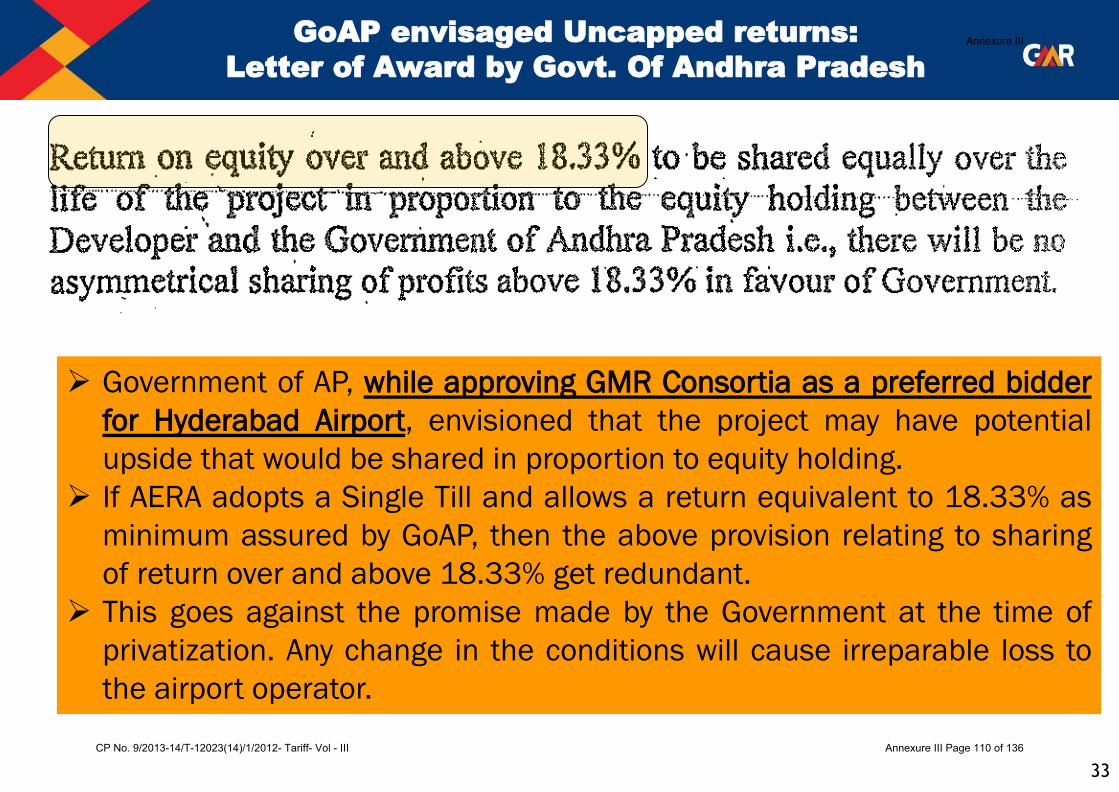

GoAP envisaged Uncapped returns:

Letter of Award by Govt. Of Andhra Pradesh

Government of AP, while approving GMR Consortia as a preferred bidder

for Hyderabad Airport, envisioned that the project may have potential